Abstract

Background (see MECIR checklist, items 1 and 3)

The problem, condition or issue

Financial inclusion is presently one of the most widely recognised areas of activity in international development. Financial inclusion initiatives have built upon donors’ experience with microfinance, but have displaced and superseded microfinance interventions in recent years with a more encompassing agenda of financial services for poverty alleviation and development (Mader 2016). With financial inclusion, policymakers and donors hope that access to financial services (including credit, savings, insurance and money transfers) provided by a variety of financial service providers (FSPs), of which microfinance institutions are a subset, will allow poor and low-income households in low- and middle income countries to enhance their welfare, grasp opportunities, mitigate shocks, and consequently escape poverty, as well as advance macroeconomic development which is also expected to benefit poor/low-income households. More recently, some donors have suggested behavioural changes (such as household spending decisions) to also be desired outcomes of access to financial services. Unlike most previous systematic reviews, which focused on microfinance interventions (or sub-sets thereof), we explicitly adopt a broader scope to review any available systematic review or meta-analysis evidence on financial inclusion as a whole field.

Systematic reviews, meta-analyses and research syntheses (in short: meta-studies) have sought to clarify the impacts from financial inclusion on poor people in low- and middle-income countries, based on an array of different underlying studies which include quantitative and qualitative work based on long-term and short-term data. The bulk of these meta-studies have been focused on microfinance, and many specifically on microcredit. The very different quality and approaches of these meta-studies, and of the studies underlying them, however, pose a major challenge for policymakers, programme managers and practitioners in assessing the benefits and drawbacks of finance-based approaches to poverty alleviation. Increasingly there is confusion about the impacts, and a risk of “cherry picking” among different findings. Further, many meta-studies are not taking into account what is missing from their primary studies, which would affect understanding of the evidence, for example by not analysing or reporting gendered impacts. More recently, primary studies 1 have also sought to understand the impacts of financial inclusion initiatives more broadly (Cull, Ehrbeck and Holle 2014; Demirgüc-Kunt and Klapper 2013), but the systematic review evidence has not yet progressed as far as for microfinance.

Our primary aim is to gain better clarity about the impacts from financial inclusion on the poor by systematically reviewing the existing systematic reviews and meta-analyses (in the broader field of meta-studies). This generation of greater clarity through greater evidence systematisation is urgent given the strong focus on expanding access to financial services in the Sustainable Development Goals (SDGs), in particular SDG 1 on eradicating poverty

2

and SDG 5 on achieving gender equality and women's empowerment

3

, and in light of the risks that some forms of financial inclusion may pose to vulnerable populations (Guérin et al. 2014). We have three sub-objectives: to better inform the decisions of development donors, policymakers and programme managers by establishing what is known and not known about the impacts, using a meta review methodology; to facilitate better research by assessing the strengths and weaknesses of existing systematic reviews and meta-analyses, and suggesting pathways toward improved and common standards and methods, and particularly more explicit attention to gendered equity determinants and a better use of qualitative studies; to understand the political economy of knowledge, which may explain which questions are asked and why, what analysis used and why, and how results are interpreted.

The intervention

The field of financial inclusion in low- and middle-income countries is diverse and complex, encompassing microfinance as the best-known intervention in this space, but increasingly extending beyond it. Microfinance refers to the provision of financial services including loans, savings accounts, insurance (e.g. health, crop, life, credit life or default insurance), and money transfer services, specifically to poor and low-income people in low- and middle income countries around the world who are not usually served by the regular banking sector, by dedicated providers who collectively identify as micro-finance institutions (MFIs); these providers may range in size and type from small, local non-profit NGOs to large commercial microfinance companies. Financial inclusion encompasses this set of services, while acknowledging a wider possible range of service providers, including community finance organisations, government programmes, commercial banks, fintech enterprises, and mobile network operators. It also highlights the connection of financial access with other services, for instance digital technologies, access to government welfare provision, mhealth services, or agricultural innovations. In short: microfinance is focused on specific financial services provided by a particular set of providers; financial inclusion more broadly aims to address poor and low-income people's ability to access and use financial services for broader ends, and is agnostic about who provides them.

The most commonly-provided services within financial inclusion still are microcredit loans, made to about 211 million families worldwide (Microcredit Summit Campaign 2015), with durations of around 12 months, which are repaid in weekly (and sometimes bi-weekly or monthly) instalments, and are often guaranteed by group membership, small collateral, or personal guarantors. Savings and insurance services are usually offered only in conjunction with loans, but also sometimes independently. Money transfers and mobile payments services (i.e. financial technologies, or fintech, that have the potential to disrupt established business models of the inclusive financial space by delivering financial services via digital platforms) are a relatively new area of activity, which is still under development in many countries, but has achieved scale in parts of East Africa and South Asia; reviews of mhealth interventions will also be included to understand the role of mobile technologies in potentially shaping the provision of inclusive financial services. The space of financial inclusion is changing rapidly, and the purpose of this systematic review of reviews 4 is to assess evidence for the broader range of inclusive financial services increasingly being offered, including but going beyond (micro)credit.

How the intervention might work

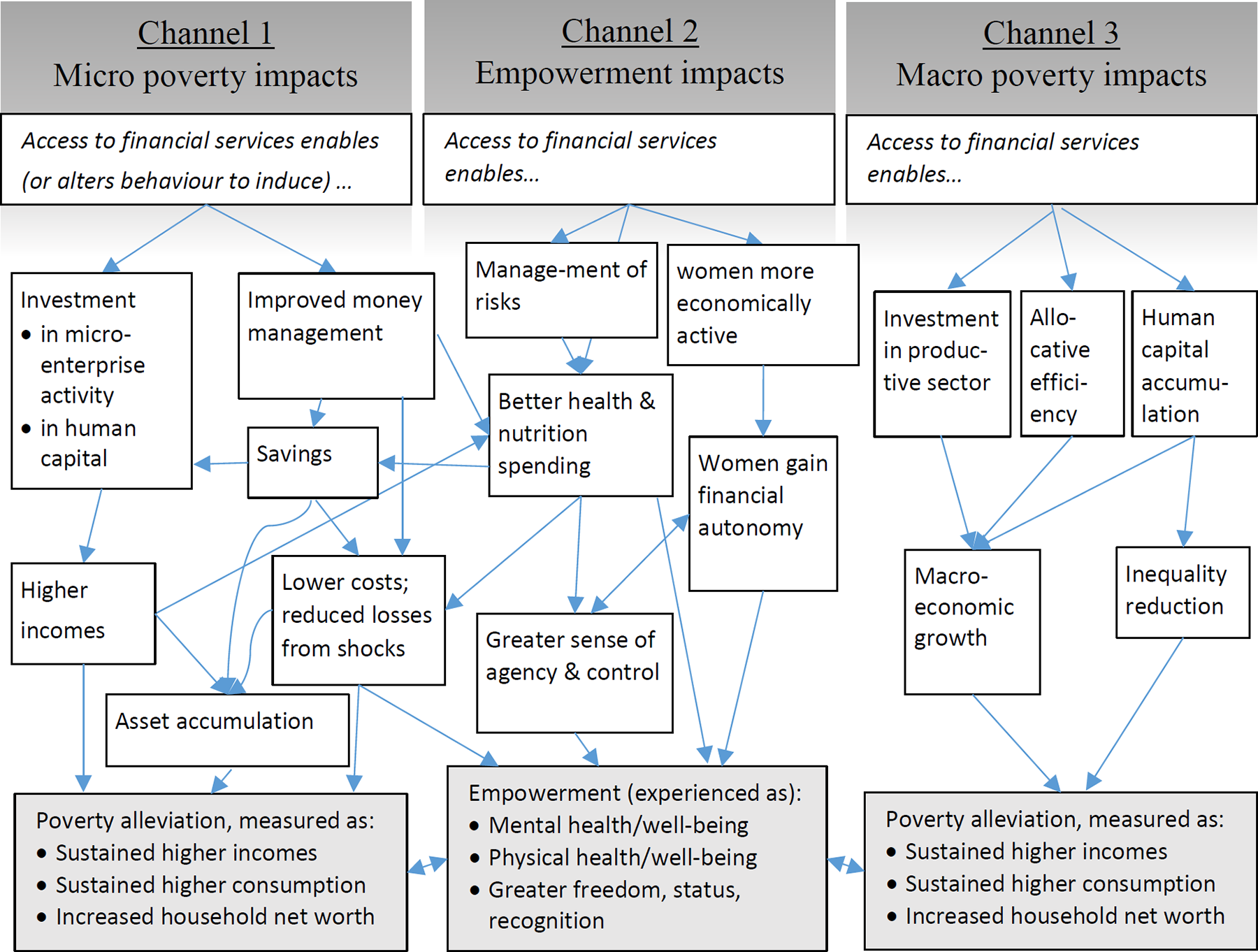

The policy rationale behind financial inclusion activities is that the usage of financial services is expected to improve the lives of poor and low-income people in low- or middle-income countries (i.e. generate a positive impact) through one or more of three possible channels: (1) personal/household financial improvements, in the form of increased incomes, lower costs, building assets, sustainably consuming more goods and services, or managing the impacts of shocks better; (2) empowerment gains, primarily an increase in well-being and health, and enhanced women's freedom, status, and recognition; (3) and macroeconomic development, when broader financial access drives inclusive growth or generates reductions in inequality. These channels and their most important impact pathways are shown schematically in the figure below.

Pathways to financial inclusion impacts

Channel 1 refers to the (presumed) ability of individuals to translate financial services usage into financial improvements for themselves or their families. These improvements may result, to simplify, through two pathways: firstly, investments by the “economically active poor” (Ledgerwood 1999: 1) in revenue-generating assets, primarily microenterprise (Grosh and Somolekae 1996), but also in human capital; secondly, through improved money-management capability (ability to move money over space and time, from where/when it is earned to where/when it is needed) to enable smoothing consumption, saving, hedging against risk, and access to liquidity (Collins et al. 2007). Included in these channel is the potential of particular modes of financial service provision leading to changed attitudes and behaviours, wherein people reprioritise expenditures in ways that are more conducive poverty-alleviation (e.g. less spending on “temptation goods”, more on asset accumulation), suggestions of which have grown more prominent in recent years (Banerjee et al. 2015; World Bank 2015).

Channel 2 refers to the (presumed) translation of financial services into the (subjectively-experienced and/or objectively observable) empowerment of individuals who use them. The literature generally articulates two forms of empowerment: improved subjective well-being and physical health regardless of gender, and empowerment for women. Physical outcomes may result from financial options which allow control of risk (e.g. insurance) or better spending on health (Dercon et al. 2012). Mental health/well-being outcomes may result from improved life satisfaction, sense of self-worth, feeling of being included and having more choices thanks to gaining access to financial services (Angelucci et al. 2014). Women's empowerment may result from access to financial services increasing women's status, freedom, and recognition (both within and outside the household), for instance when women are enabled to be more active in the public sphere, or increase their intra-household economic decision-making power, or gain greater autonomy (Kabeer 2005; Suri and Jack 2016).

Channel 3 refers to the potential for inclusive financial sectors to be conducive to macroeconomic development in low- or middle-income countries, from which poor and low-income people in turn benefit (Cull, Demirgüç-Kunt, and Morduch 2013; World Bank 2014). The economic literature sees inclusive financial sector development as driving economic growth by mobilising savings and investments in the productive sector, and reducing information, contracting and transaction costs across the economy, leading to efficiency gains (Banerjee and Newman 1993; Galor and Zeira 1993; King and Levine 1993); poverty alleviation will result if poor people benefit from subsequent economic growth. Inclusive financial sector development is also seen as potentially reducing economic inequality, either indirectly (through growth leading to lower inequality) or through enabling lower-income individuals to invest in their own human capital (Jalilian and Kirkpatrick 2005; Beck et al. 2007).

Notably, these channels of potential (that is: widely-discussed, but not yet clearly demonstrated) impact of financial services usage on poverty (as well as their respective pathways) are interdependent, as indicated by some of the cross-connections in the figure. But most existing reviews have focussed on individual channels or only certain pathways within them. A higher level of review systematisation will enable us to better understand the interconnections and contingencies between the different impact channels and pathways.

In each impact channel, furthermore, the possibility of adverse impacts (on average, or for parts of the population) must be considered, as there is no reason to assume the impacts will be positive. Among the adverse impacts that have been discussed at length in the literature so far are worsened impoverishment (Mosley 2001), financial and emotional stress (Ashta et al. 2015), debt traps and permanent indebtedness (Schicks 2010; Guérin et al. 2014), gender-based violence and women's disempowerment (Rahman 1999), undermined economic development and social greater inequality (Bateman 2010; Sandberg 2012).

Why it is important to do the review

While a large number of methodologically robust studies have systematically synthesised evidence on microfinance, the same cannot yet be said for financial inclusion more broadly. Some donor agencies, especially the World Bank, have carried out primary studies on financial inclusion of various types including microfinance facility to justify why financial inclusion policy matters, how it matters, and what it means to policymaking (cf. Cull, Ehrbeck and Holle 2014; Demirgüc-Kunt and Klapper 2013; Demirgüc-Kunt, Klapper and Singer 2017; World Bank 2014). But the existing research syntheses on financial inclusion (beyond microfinance) have been unsystematic in their approach.

Polanin et al (2017) provide 4 reasons for why systematic reviews of reviews are important: They can contribute to the knowledge base going beyond what systematic reviews and meta-analyses report examining trends over time and thus be particularly useful to policymakers, practitioners and researchers. Where many systematic reviews on a given topic exist reporting discordant views, systematic reviews of reviews can be particularly useful to make sense of these diverging conclusions by comparing and contrasting the results of multiple systematic reviews. They have the potential to conduct network meta-analysis (Ioannidis, 2009) to allow comparisons of multiple treatment and control groups. They can point out when systematic reviews need updating again.

Finally, it is worth noting that systematic reviews of reviews also have a role to play in translating knowledge into policy impact.

In the context of financial inclusion, without robust evidence that financial services generate significant and meaningful – ideally: transformative – impacts in poor people's lives, financial inclusion efforts would lack a clear justification in developmental or social policy terms. This can be said without pre-judging the evidence. However, the existing systematic reviews and meta-analyses which we are presently aware of (and which have focused on microfinance rather than financial inclusion broadly-defined) have generated few strong or unambiguous results, suggesting that the improvements in poor people's lives that accrue from financial inclusion are relatively small or manifest mainly as intermediary impacts – changes in behaviours and spending patterns, rather than changes in incomes or well-being –, at least in the shorter term. Presently, too little is known across different meta-studies with different approaches, and we expect a systematic review of reviews will generate a clearer picture.

Existing systematic reviews and meta-analyses have reviewed primary studies of many different types of financial services. As indicated in the table below, a substantial number of systematic reviews, meta-analyses and research syntheses on financial inclusion and closely-connected topics exist. However, the focus of the bulk of studies (in keeping with the activity focus of the financial inclusion sector) has been on credit and credit-type (e.g. leasing) services, particularly those provided by MFIs. The evidence base on other services is smaller but growing rapidly, particularly in the area of mobile service provision and fintech for development.

The existing systematic reviews and meta-analyses have followed diverse approaches. Some of the systematic reviews are fairly broad, aiming to cover the whole microfinance spectrum (e.g. Duvendack et al. 2011). Others cover specific interventions, such as microcredit (e.g. Vaessen et al. 2014), formal banking services (Pande et al. 2012), microenterprise (e.g. Grimm and Paffhausen 2015), microsavings and microleasing (Stewart et al. 2012), and microinsurance (Cole et al. 2012). Some systematic reviews focus on particular populations, such as Sub-Saharan African recipients (e.g. Stewart et al. 2010), particular methods of providing financial services, such as self-help groups (e.g. Brody et al. 2016) or particular outcomes, such as health (e.g. Leatherman et al. 2012) or empowerment (Vaessen et al. 2014; Brody et al. 2016). The systematic reviews also differ by focus, many covering effectiveness evidence, but others incorporating participant views (e.g. Brody et al. 2016) and barriers or enablers of uptake and effectiveness (e.g. Panda et al. 2016) including innovations in information and communications technology (e.g. Gurman et al. 2012, Jennings and Gagliardi 2013, Sondaal et al. 2015, Lee et al. 2016).

The systematic reviews and meta-analyses use a range of methodologies to synthesise the evidence, including theory-based approaches, narrative syntheses and statistical meta-analyses. Many of them have not been conducted to standards that would support a ‘high confidence’ rating 5 ; not all meta-studies that have impacted policy discussions have used a systematic methodology (Odell 2010; Bauchet et al. 2011; Beck 2015). In addition, the majority of systematic reviews and meta-analyses are available in technical reports where there is no transparent decision rule for determining implications of the findings, including critical appraisal and strength of evidence tools like GRADE assessment (Guyatt et al. 2013) and user-friendly presentation of results (e.g. translating standardised effect sizes into metrics commonly used by decision makers). In addition, there is no overall synthesis of the implications for policy, programming, practice and research for the sector from this body of synthesised evidence.

Below is a chronological overview of many known systematic reviews, meta-analyses and research syntheses of financial inclusion interventions:

This array of meta-studies, often focused on different geographies and dealing with different interventions, presents policymakers and practitioners with a potentially perplexing mosaic of findings, non-findings, and knowledge gaps. Our systematic review of reviews will bring a systematic overview about what is known about what aspects of financial inclusion (what, where, how?) and which gaps and white spaces remain. To visualise these gaps and white spaces, we will adopt a mapping approach which is a loose adaptation of the more formal evidence gap map approach developed by Snilstveit et al (2013) and Gough et al (2013). Our map will be guided by a range of parameters, e.g. intervention type, outcome measures, geographical focus, etc. which in turn will inform our synthesis approach which, among other things, will also focus on the following unresolved questions (discussed in more depth in the section outlining our approach to data synthesis): What can explain which questions are asked in some systematic reviews and meta-studies about the impact of financial inclusion, and which ones not? What can explain different interpretations of results from existing studies?

A clear mapping of knowledge gaps will allow policy-related research funders to better direct research funds towards addressing the gaps, and the systematic reviewing of known impacts will allow policymakers to focus their efforts on those interventions that are known to work best, on where they work best, or otherwise to eschew or improve them. Our stakeholder engagement strategy will include a policy brief, a collection of blogs, and dissemination events, as well as working with our advisory board to disseminate the findings.

Objectives (see MECIR checklist, item 2)

The objective of this systematic review of reviews is to systematically collect and appraise the existing systematic reviews and meta-analyses of financial inclusion impacts, analyse the strength of the methods used, synthesise the findings from those systematic reviews and meta-analyses, and report implications for policy, programming, practice and further research.

Systematic reviews of reviews are undertaken in other sectors for which evidence is widely available, especially health (Becker and Oxman 2008) and recently education (Polanin et al. 2017), but they are non-existent in international development, and thus this study will address a notable gap. 6 It provides the opportunity to develop and pilot an evidence synthesis approach in a sector where there is a large body of evidence of variable quality, but a systematic appraisal and synthesis of the body of systematic reviews and meta-analyses is lacking. Polanin et al (2017) provide useful guidance on how best to conduct such systematic reviews of reviews; they point towards methodological challenges of such reviews and suggest ways forward to improving them.

This study will critically review existing approaches to systematic reviews of reviews with a view to further developing systematic review of review methods and it will aim to answer the following questions to gain better clarity about financial inclusion impacts: Impacts: What is known from existing systematic reviews and meta-analyses about the poverty impacts (social, economic, and behavioural) of different types of inclusive financial services (e.g. credit, savings, insurance, money transfers), regardless of provider, on poor and low-income people in low- and middle income countries?

7

This includes the poverty impacts from macroeconomic development to the extent that it results from financial inclusion.

8

What is known from existing systematic reviews and meta-analyses about the gendered differential impacts of different types of financial inclusion activity (e.g. credit, savings, insurance, money transfers) – in other words, what does the evidence tell us about how gendered social and structural determinants of inequality affect intervention effects, as well as whether or not financial services empower women, and in what ways, in low- and middle income countries? What is known from existing systematic reviews and meta-analyses about reasons for financial services uptake, or other participant views about the financial services on offer? Methodology: Including using a gender and equity lens, what methods and standards have the systematic reviews and meta-analyses used to draw conclusions from the studies they reviewed? What difference does the choice of methods and standards make to the results? How could the methods and standards be improved in order to draw more robust and reliable conclusions via systematic reviews and meta-analyses?

Methodology

Criteria for including and excluding studies (see MECIR checklist, items 5-14)

Types of reviews (see MECIR checklist, item 9)

We will include studies which self-identify as systematic reviews and or meta-analyses of the impacts of financial inclusion (including, but not limited to, microfinance). These in turn will have focused on synthesising quantitative, qualitative and or mixed methods evidence. According to the Campbell Collaboration, “A systematic review summarizes the best available evidence on a specific question using transparent procedures to locate, evaluate, and integrate the findings of relevant research” (The Campbell Collaboration 2014, p.6).

In the Cochrane Handbook (Higgins and Green 2011), the following definition of systematic reviews is outlined which we will adopt: “A systematic review attempts to collate all empirical evidence that fits pre-specified eligibility criteria in order to answer a specific research question. It uses explicit, systematic methods that are selected with a view to minimizing bias, thus providing more reliable findings from which conclusions can be drawn and decisions made” (Section 1.2 in Higgins and Green 2011).

Higgins and Green (2011) specify the key elements a systematic review should contain: A set of clearly stated objectives and pre-defined eligibility criteria A methodology that is clearly defined allowing reproducibility A search strategy that allows the identification of studies meeting the pre-defined eligibility criteria A critical appraisal of included studies A systematic synthesis, in many cases systematic reviews adopt a meta-analytical approach which is a statistical method to synthesise the results of primary studies included in a systematic review

To identify meta-analyses, we adopt the definition of the Cochrane Handbook (Higgins and Green, 2011): “Meta-analysis [is] the statistical combination of results from two or more separate studies” to produce an overall statistic with the aim to provide a precise estimate of the effects of an intervention (Section 9.1.2 in Higgins and Green 2011).

It should be noted that not every systematic review automatically contains a meta-analysis, e.g. if primary studies are too heterogeneous in terms of study designs, conceptual framings and or outcomes, then a meta-analysis may not be appropriate. Furthermore, occasionally meta-analyses are published separately without drawing on the broader systematic review they may have been originated from.

We exclude any evidence that did not meet the definitions we outlined above.

Types of participants (see MECIR checklist, item 5)

The scope of the systematic reviews and meta-analyses we will include may be diverse (different questions are often addressed; a range of linked interventions are examined such as credit, savings, insurance, leasing, money transfers etc.) but there is considerable overlap in terms of their population of interest. Almost all systematic reviews and meta-analyses focus on the impacts of financial inclusion on poor households based in low- or middle-income countries (using the World Bank definition 9 ). In other words, our population is the population of participants in inclusive finance activities that are conducted in low- and middle-income countries. Where systematic reviews and meta-analyses include evidence from high-income countries, we will only consider the findings that are presented for low- and middle-income countries; we will also consider systematic reviews and meta-analyses covering particular regions within low- and middle income countries, e.g. Sub-Saharan Africa or fragile and conflict-affected areas.

At the primary study level, our population of interest would be participants taking part in inclusive finance activities in low- and middle-income countries.

Types of interventions (see MECIR checklist, item 7)

In this systematic review of reviews, we will include all systematic reviews and meta-analyses that address at least one or more types of intervention for financial inclusion, as described above. In the majority, we expect the interventions will be one or more sub-categories of microfinance: microcredit, micro-savings, micro-insurance, micro-leasing, and/or money transfers. However, our search strategy explicitly targets the broader range of inclusive finance activities, such as mobile monies, index insurance, or savings promotion. For our purposes, to warrant inclusion of the systematic review or meta-analysis, the reviewed intervention must have at least one financial service as an essential element of the intervention – for instance, not all systematic reviews of mhealth interventions would qualify for inclusion, but systematic reviews of mhealth interventions that require participants to purchase an insurance service would. The key is that the intervention is fundamentally a financial service directed at poor and low-income people.

At the primary study level, our intervention of interest would be interventions that address at least one or more types of financial inclusion interventions.

Types of outcome measures (see MECIR checklist, items 8 and 14)

Existing systematic reviews and meta-analyses of financial inclusion typically examine a wide range of poverty indicators (including income, assets, expenditure, personal networks, gender/empowerment, well-being, health, etc.). In this systematic review of reviews, we will include all systematic reviews and meta-analyses that address at least one or more of these domains. We will group the indicators in three categories of impacts: social, economic, or behavioural. We will not distinguish between primary or secondary outcomes but consider all outcome measures.

Our systematic review of reviews will also assess the evidence for outcomes further back along the causal chain; most importantly rates of uptake, and then investment in productive activity, human capital accumulation, improved money management, savings accumulation, risk/shock management, health and nutrition spending, and women's economic activity. These might be enablers of improvements on poverty indicators (over a longer term) even if, importantly, should not in themselves be taken as evidence of impact in terms of poverty alleviation.

At the primary study level, our outcomes of interest would be outcomes that address at least one or more of the poverty domains described above.

Timeframe

The first systematic reviews engaging with financial inclusion issues (Stewart et al 2010, Duvendack et al 2011) indicated that no systematic reviews existed prior to their reviews. The primary studies these two systematic reviews included date back to the late 1990s reporting on data that was collected in the early 1990s – this coincides with rigorous impact evaluations of financial inclusion becoming more mainstream, hence our searches will be limited to 2010 onwards.

Language

No restriction was placed on language of papers.

We do not expect to make any changes to the eligibility criteria set out in this section but should we need to make any adjustments we will justify and documents these carefully and any changes will be in line with the objectives of this systematic review of reviews (relates to MECIR checklist, item 13).

Evidence will be included irrespective of its publication status (relates to MECIR checklist, item 12).

Search strategy (see MECIR checklist, items 19, 24, 32, 33, 35, 36 and 37)

We will adopt a multi-pronged search strategy which was informed by Kugley et al (2016) and that explores bibliographic databases to identify published literature, institutional websites for published and unpublished literature, and back-referencing from recent systematic reviews (see Table 1 above) to ensure additional sources are identified.

Overview of systematic reviews, meta-analyses and research syntheses of financial inclusion interventions

We will search the following bibliographic databases: Business Source Premier (Ebsco) Academic Search Complete (Ebsco) Econlit – Via Ebsco Discovery Service Repec – Via Ebsco Discovery Service World Bank e-Library – Via Ebsco Discovery Service Scopus (Elsevier) Web of Science

The following institutional websites will be searched:

Financial inclusion-specific institutions and web portals:

CGAP: www.cgap.org

Microbanking Bulletin: www.themix.org

Microfinance Gateway: www.microfinancegateway.org

Microfinance Network: www.mfnetwork.org

Grameen Foundation BRAC Research and Evaluation Division Alliance for Financial Inclusion Accion Center for Financial Inclusion

Multilateral and bilateral and non-governmental donor organizations:

World Bank (WB e-library was searched within Ebsco's Discovery Service but will also be searched and screened online via the World Bank's website) African Development Bank Asian Development Bank Inter-American Development Bank DFID – R4D website USAID

Research institutions and research networks:

Center for Global Development J-PAL 3ie databases on systematic reviews ELDIS SSRN ResearchGate

After completing the screening process, we will also run citation searches on included systematic reviews and meta-analyses in Google Scholar, Scopus and Web of Science to identify more recent systematic reviews or meta-analyses not retrieved in database searches.

We piloted our key search terms (see Appendix 1 for full search strategies) and ran preliminary searches in Econlit (Ebsco) (510 hits), Scopus (1035 hits), Repec (Ebsco) (238 hits), Academic Search Complete (Ebsco) (366 hits), and Web of Science (2014 hits). Search strategies were constructed using both textwords (title/abstracts) and where available index terms. Each strategy consisted of 3 parts – Intervention (financial inclusion, microfinance and other relevant terms), Study design (adapted from 3ie's search filter for its systematic review database), and LMICs (adapted from the Cochrane EPOC Group's LMICs filter based on World Bank definition of LMICs). We adjusted our search strategy for each database and web source. No restriction was placed on language of papers but all searches were limited to 2010 onwards (rationale provided above) and only English language papers were identified. We will adopt a snowballing, also called reference harvesting, approach to ensure we have not missed any key systematic reviews or meta-analyses. We will also consult our advisory board to get their views on the sample of included studies. We will update our searches for all relevant databases within 12 months before publication of our study and screen all new systematic reviews and meta-analyses using the eligibility criteria outlined above.

Selection of studies (see MECIR checklist, items 39 and 41)

One review author (MD) will screen all titles and abstracts of the systematic reviews and meta-analyses identified by the search. The second review author (PM) will independently review each systematic review and meta-analysis for inclusion to confirm the inclusion decision of the first review author (MD). Full texts will be obtained and screened when a decision cannot not be made based on title and abstract screening. Disagreements will be resolved by discussion or by involving a third party (e.g. a member of the advisory board) if a consensus cannot be reached.

A PRISMA flow diagram will be used to summarise the study selection process and a table with the characteristics of excluded studies will be included in the appendix.

Description of methods used in systematic reviews (see MECIR checklist, item 44)

The systematic reviews and meta-analyses we will include will have included primary studies that employed quantitative, qualitative and mixed methods approaches. Hence, many of the systematic reviews and meta-analyses in our study sample will have adopted a narrative synthesis approach to deal with the methodological diversity found in the included primary studies (e.g. Stewart et al 2010 and 2012, Duvendack et al 2011). In some cases, however, meta-analysis is feasible and the preferred synthesis approach (e.g. Yang and Stanley 2013, Awaworyi 2014, Lee et al 2016). In very few cases, a combination of qualitative and quantitative synthesis approaches can be found (e.g. Vaessen et al 2014).

Criteria for determination of independent reviews (see MECIR checklist, items 40 and 42)

Some of the systematic reviews and meta-analyses in our study sample will have been published in multiple places, e.g. they may have been published as a Campbell systematic review but also as a peer-reviewed journal article (e.g. Vaessen et al 2014). Or they may have been published on DFID's R4D website as well as a peer-reviewed journal article (e.g. Stewart et al 2012). Where this is the case, we will treat them as duplicate reviews with data extracted from the most comprehensive review. Should we identify multiple versions of the same systematic review or meta-analysis, we will only include the latest updated version. An issue that remains after removing duplicate systematic reviews and meta-analyses is that of overlap. In our sample of included systematic reviews, we may find reviews that included some of the same primary studies. One way to address overlap is to present a matrix (see Polanin et al 2017) that includes all primary studies captured in the systematic reviews with a high and medium conference rating, this would allow us to understand the extent of overlap, i.e. which primary studies were included in which one of the high quality systematic reviews in our study sample.

Where systematic reviews or meta-analyses do not report data in useable formats, we will still attempt to include them as long as they meet our eligibility criteria.

Details of study coding categories (see MECIR checklist, items 43, 46, 47, 50 and 51)

Data will be extracted by a research assistant (RA) using an Excel spreadsheet and independently checked by the two review authors (MD, PM). In case of disagreements, they will be resolved by discussion. The original authors of included systematic reviews and meta-analyses will be contacted where data are missing.

We will extract data on the following areas (for details see Table 2 below which was informed by Sniltsveit et al 2014): Context Type of intervention Type of review, design and methods used Outcome measures Quality assessment Study results and findings

Data extraction form (template)

We will aim to extract the most detailed data (also numerical data if available) to allow similar analyses of included studies.

We will primarily be extracting information at the systematic review level. However, for systematic reviews classified as high and medium confidence we will also extract information at the primary study level on, e.g. especially individual programme design, quality, etc. We may also explore whether effect size estimates can be extracted from t-statistics if feasible and necessary.

Assessment of quality (see MECIR checklist, items 20, 52, 53, 54 and 61)

Assessment of methodological quality of included reviews (see MECIR checklist, items 52, 53 and 54)

The quality of the included systematic reviews and meta-analyses will be assessed using the 3ie critical appraisal checklist 10 , which is a variation of the checklist developed by the Specialist Unit for Review Evidence (SURE) in 2013. The objective of the original SURE 11 checklist was to allow a critical appraisal of systematic reviews to ensure that minimum levels of methodological rigour are met across included reviews. We will explore extensions to the 3ie checklist in collaboration with 3ie and may add a critical appraisal component that relates to the explicit use of theory in systematic reviews and to what extent an analysis of the causal chain has been undertaken.

Furthermore, to corroborate the findings of the 3ie critical appraisal checklist, we will also be employing the ‘A MeaSurement Tool to Assess systematic (AMSTAR 2) developed by Shea et al (2017) which is often used in the context of Cochrane overview studies. AMSTAR 2 is building on the original AMSTAR tool developed by Shea et al (2007), it has 16 criteria 12 and each will be given a rating: ‘yes’, ‘partial yes’ or ‘no’ allowing the user to make a broad assessment of the quality of the included reviews.

The 3ie critical appraisal checklist and AMSTAR 2 tool will be applied independently by both review authors (MD, PM), disagreements will be resolved by discussion or by involving a third party (e.g. a member of the advisory board) if a consensus cannot be reached.

Assessment of the quality of the evidence in reviews (see MECIR checklist, items 61, 76 and 77)

We will extract GRADE ratings from each included systematic review to assess the quality of the evidence. It is highly likely that many of the included systematic reviews will have adopted quality assessment approaches other than GRADE, where this is the case we will report the tool that was used and record its overall quality score. We will re-evaluate the quality score (i.e. potentially downgrade or upgrade it) retrospectively using the main GRADE criteria related to risk of bias, inconsistency, imprecision, indirectness and publication bias (Guyatt et al 2008 13 ). This re-evaluation will only be done for systematic reviews that have a medium or high confidence rating. The quality assessment will be conducted independently by both review authors (MD, PM), disagreements will be resolved by discussion or where necessary by involving a third party (i.e. a member of the advisory board).

Data synthesis and presentation (see MECIR checklist, items 21, 78 and 79)

The included systematic reviews will have adopted a wide range of synthesis approaches ranging from narrative syntheses to meta-analyses. Having reviewed the various synthesis methods set out by Barnett-Page and Thomas (2009), we will adopt a narrative synthesis approach as this accommodates both quantitative and qualitative information and is thus best suited for our purpose.

Quantitative information

Some of the systematic reviews in our sample will have taken a meta-analytical approach; where this is the case, we will explore the possibility of reporting the pooled effects sizes for all outcomes and/or explore whether there is value in compiling and synthesising the magnitudes of the effect sizes from their included primary studies. Where systematic reviews drawing on meta-analytical techniques do not report this information, we will downgrade the review 14 . Where feasible, we will attempt to back-translate effect size data (e.g., such as standardised mean differences) into a (from a policy perspective) more understandable magnitude of units (e.g. mean differences in standard units and or percentage changes).

Qualitative information

We expect that the majority of the included systematic reviews will have adopted qualitative synthesis approaches. To synthesise the qualitative evidence, we will use a thematic synthesis approach, which is particularly useful to understand systematic reviews (including effectiveness reviews) which address questions in relation to appropriateness and acceptability of interventions as well as to understanding barriers and enablers of an intervention. Thematic synthesis first organises content into ‘descriptive’ themes, which are then explored to generate ‘analytical’ themes for further analysis (Barnett-Page and Thomas 2009).

In addition, we will present our findings according to the statistical information available in each systematic review, which may often be a textual commentary. This commentary will be enhanced by drawing on summary tables and figures using frequencies and percentages to describe and summarize the evidence we collected from the included reviews (see Smith et al 2011 for suggestions for summary tables). Where possible, we will also attempt to report findings in metrics of effect sizes and 95% confidence intervals, which may require the use of standard formulae to translate between effect sizes (e.g. see Sanchez-Meca et al 2003 for guidance) – we should note that this is an exploratory exercise.

Baker et al (2014) argue that the emphasis of systematic reviews of reviews should be on the presentation of the results and conclusions of the included reviews in accordance with their overall objectives. With this in mind, we may organise our synthesis by data extraction areas (as outlined above): Context Type of intervention Type of review, design and methods used Outcome measures Quality assessment Study results and findings

Following Jadad et al (1997), the synthesis will also be guided by the following two questions introduced above as part of the rationale for doing the review: What can explain which questions are asked in some systematic reviews and meta-studies about the impact of financial inclusion, and which ones not? What can explain different interpretations of results from existing studies?

The findings from our synthesis will inform the conclusions of this study; we will not stray beyond the studies included in this review when discussing the implications for research and practice.

Treatment of qualitative research

A large number of the included systematic reviews will have adopted a qualitative synthesis approach; where this is the case, we will use appropriate data synthesis and presentation formats, as outlined in the previous section, to allow a comparison across systematic reviews.

Sub-group analysis (relates to MECIR checklist, item 22)

We will report sub-group analyses adapting the PROGRESS-Plus checklist 15 which was originally developed for Cochrane reviews focusing on health equity. Sub-group analyses enhance our understanding of impact heterogeneity, i.e. impacts of certain elements of financial inclusion interventions may differ by gender, ethnic background, poverty level, etc. Reporting sub-group analyses may allow us to comprehend which interventions (or elements thereof) may or may not be effective in relation to certain sub-groups in the population.

Footnotes

Review authors

|

Name: Maren Duvendack |

|

|

Title: Dr. |

|

|

Affiliation: |

University of East Anglia |

|

Address: |

School of International Development Norwich Research Park |

|

City, State, Province or County: |

Norwich |

|

Postal Code: |

NR2 3HT |

|

Country: |

United Kingdom |

|

Phone: |

07788777818 |

|

Email: |

|

|

|

|

|

Name: Philip Mader |

|

|

Title: Dr. |

|

|

Affiliation: |

Institute of Development Studies |

|

Address: |

Library Road, University of Sussex |

|

City, State, Province or County: |

Brighton, East Sussex |

|

Postal Code: |

BN19RE |

|

Country: |

United Kingdom |

|

Phone: |

07711 761418 |

|

Email: |

|

Duplicate the co-author table as necessary to include all co-authors.

Roles and responsibilities

Content: Maren Duvendack, Philip Mader Systematic review methods: Maren Duvendack, John Eyers (search strategy) Statistical analysis: Maren Duvendack, Philip Mader Information retrieval: John Eyers, Ada Sonnenfeld

Sources of support

The International Initiative for Impact Evaluation (3ie) is funding this work.

Declarations of interest

Maren Duvendack was lead author on one systematic review (Duvendack et al. 2011) and contributing author on one (![]() ).

).

Philip Mader conducted an overview of (only most recent) financial inclusion impact evidence in early 2017 for a consultancy (unpublished).

Preliminary timeframe

30 July 2018

Plans for updating the review

Ideally, this review should be updated every five years to include new systematic reviews on financial inclusion. However, regular updates are subject to availability of funding.

AUTHOR DECLARATION

1

We use the term primary studies to denote individual studies that make up a systematic review, meta-analysis or research synthesis.

4

We use the term systematic review of reviews to denote our population of studies consisting of systematic reviews and meta-analyses.

5

6

Evans and Popova (2015) produced a review that claimed to find divergent findings in six “systematic reviews” of education programmes. However, the authors did not screen or critically appraise included reviews according to standard definitions. Hence, further analysis indicated only one of the included studies was undertaken using systematic review methods, the other five being literature reviews and meta-analyses which did not use comprehensive approaches to select, appraise and/or synthesise the evidence (Snilstveit, Vojtkova and Phillips, 2015).

7

Our review will disaggregate the impacts of different services provided by different provider-types, and examine heterogeneous impacts on different user groups, as much as the data permits.

8

We are not presently aware of any systematic reviews or meta-analyses that address this type of impact, but hope to find and include such evidence to the extent that it matches our inclusion criteria.

14

We explored the possibility of conducting a network meta-analysis (Ioannidis, 2009) to synthesise the reviews that performed meta-analysis but our sample of meta-analyses will be too small to allow a meaningful network meta-analysis.