Abstract

Prior research has found evidence of large racial and gender disparities in wealth, with blacks possessing less wealth than whites and women having less wealth than men. An intersectionality approach suggests that the overlapping impacts of racial and gender domination are likely to combine in a multiplicative fashion that places black women in a uniquely precarious economic position. However, little is known about the wealth holdings of black women and even less is known about whether their wealth increases, decreases or remains stable as they approach retirement age, a stage of life when savings are especially important. This study utilizes seven waves of panel data from the Health and Retirement Study (HRS) and growth curve models to estimate the wealth trajectories of black women between the ages of 51 and 73. Results reveal that black women have especially low levels of net worth and net financial assets during middle and late life, suggesting high risk of economic insecurity in later life. Consistent with political economy and intersectionality perspectives, their persistently low wealth trajectories are likely the result of state policies, discrimination, residential segregation and health disparities. Ameliorative policy prescriptions are discussed.

Introduction

Despite our prosperity as a nation, empirical evidence shows an unparalleled degree of wealth inequality in the United States (Wolff 1995). Wealth is an especially important indicator of economic well-being, because, unlike income or educational attainment, this measure of economic status captures the consequences of the accumulation of assets across and within generations. Wealth can be used to pay for college, put a down payment on a home, or start a business—keys to upward socioeconomic mobility. Moreover, it cushions the economic impact of unexpected costs associated with job loss, medical expenses and divorce. Wealth also has consequences for future generations because it can be passed on in the form of inter vivos transfers and inheritances.

Existing research shows that there are large race and gender disparities in wealth, with blacks possessing less wealth than whites (Oliver and Shapiro 1995) and women having less wealth than men (Chang 2010a). Nevertheless, studies on wealth have tended to treat race and gender as separate dimensions, ignoring the ways that race and gender may intersect to shape the accrual of economic resources. An intersectional approach to understanding how race and gender produce wealth trajectories would consider the unique position of individuals who must navigate both race and gender statuses simultaneously.

The central aim of this study is to investigate how much wealth black women possess in middle and late life. An intersectional lens may be especially important for understanding outcomes for black women, who occupy two lower statuses (i.e., “black” and “woman”) in American society (see e.g., Shields 2008). In terms of wealth accumulation, black women encounter barriers to opportunities due to both racism and sexism, which may even emanate “from members of their own social groups—they may experience sexism from within the black community and racism from other women…” (Settles 2006, p. 590). Furthermore, taking into account the aging process, the number and proportion of black older adults is projected to increase over the next two decades (He et al. 2005). Although it is well-documented that black women have longer life expectancies than their male counterparts (Kochanek et al. 2005), less is known about how the numerous race and gender barriers to building wealth faced by black women affect them in this stage of the life course. That is, little is known about black women's wealth trajectories in later life. An intersectionality perspective would suggest that racial and gender disadvantages are likely to exacerbate each other and compound over time, and consequently that black women are likely to experience substantial economic insecurity, accumulating little wealth over the life course.

Wealth holdings are especially important among older black women given their economic insecurity over the life course (Brown and Warner 2008; Christie-Mizell et al. 2007), limited employment opportunities, and the increasing likelihood of health limitations as they age (Warner and Brown 2011). The life cycle hypothesis (LCH)— the dominant economic paradigm for understanding savings and consumption behavior—posits that rational actors should accumulate wealth until they retire, whereupon they begin decumulating wealth, such that average wealth levels will increase until around retirement age, after which they decline (Modigliani and Brumberg 1954; Modigliani 1986). Implicit in LCH is the untenable assumption that individuals are able to achieve economic success without the constraints of artificial barriers such as institutional racism and sexism. However, well-documented discrimination on the basis of both race and gender faced by black women (Darity and Mason 1998) makes the LCH unlikely to be adequate for explaining their wealth trajectories. Therefore, this study utilizes an intersectionality approach and panel data from the Health and Retirement Study to investigate black women's wealth trajectories (net worth and net financial assets) between ages 51 and 73. Black women are hypothesized to have extremely modest wealth holdings throughout middle and late life. Below are brief reviews of the literature on racial and gender inequality in wealth and explanations for the wealth gaps, followed by a discussion of how race and gender disadvantages are hypothesized to shape black women's wealth trajectories. Next, the data and methods utilized are discussed, followed by a description of analysis results. Finally, the conclusion section contextualizes the findings and discusses future directions for research as well as policy prescriptions.

Race and wealth

A number of studies have found that racial inequality in wealth is enormous and even greater than the inequality found among groups in terms of income (Blau and Graham 1990; Conley 1999; Menchik and Jianakoplos 1997; Oliver and Shapiro 1995; Shapiro 2004). The most common and comprehensive measure of wealth in the literature is net worth, which is calculated as the value of all assets less any debts. Kochhar 2004 found that the median net worth of white households is approximately $89,000, compared to only $6,000 among blacks. Moreover, blacks experience high rates of asset poverty, with nearly a third having zero or negative net worths (Kochhar 2004; Shapiro 2004). For middle class households, home ownership is the primary vehicle for wealth accumulation and upward economic mobility, and home equity represents a major portion of net worth (Keister 2000). However, less than half of black families are homeowners and among those that are, home equity values are low, especially relative to their white counterparts (Kochhar et al. 2009; Oliver and Shapiro 1995).

Black households are also in a perilous position with respect to net financial assets, which exclude real estate and vehicle equity, and thus, consist of liquid assets that can be readily converted into cash for immediate household consumption. Compared to whites, blacks are much less likely to have any cash savings or own stocks or bonds (Kochhar 2004). As a result, the black-white gap in net financial assets is even greater than the race gap in net worth (Oliver and Shapiro 1995; Shapiro 2004). Collectively, these findings suggest that blacks have meager levels of wealth relative to their white counterparts, and that a substantial proportion of minorities do not have the financial wherewithal to meet unexpected financial setbacks such as being laid off from a job, a visit to the hospital or divorce. Several potential explanations for the negligible wealth accumulation among black households have emerged in the research literature.

Behavioral economic explanations focus on black households’ savings and investment behavior. First, some have argued that minorities experience reduced wealth growth compared to whites because they commit less of their income to savings and investments (Altonji and Doraszelski 2005). Indeed, blacks are much more likely to be “unbanked” (i.e., lacking an account at a depository institution such as bank, credit union or thrift) and “underbanked” (i.e., relying on non-bank money orders and check cashing services, payday loans, rent-to-own agreements or pawn shops) than whites (FDIC 2009). Similarly, a study by Ariel/Hewitt found that blacks had lower participation and contribution rates to 401(k) plans, however, findings from this study should be interpreted with caution due to what appear to be inconsistencies in the results and a lack of clarity in the methods used (Hamilton and Darity 2010). Moreover, the Ariel/Hewitt study has several limitations that may lead to biased estimates, including controlling for individual income rather than household income among married respondents. Importantly, empirical analyses utilizing appropriate methods cast doubt on explanations of wealth disparities that focus on savings behavior, for instance, studies by Conley (1999) and Gittleman and Wolff (2004) showed that, after controlling for household income, blacks have savings rates that are equivalent to or slightly higher than whites.

A second behavioral economic explanation—differential returns on investments—concerns blacks receiving lower rates of return on investments than whites. One cause of the differential return is thought to be racial differences in the composition of wealth portfolios. Compared to white households, a disproportionate amount of the wealth of black households is invested in functional assets (e.g., homes or vehicles) rather than financial assets (e.g., stocks and bonds) which yield better long-term rates of return (Oliver and Shapiro 1995; Terrell 1971). However, research shows that blacks and whites with comparable levels of income have similar rates of return on investments (Gittleman and Wolff 2004); for these reasons and others, Hamilton and Darity (2010) cogently argue that the aforementioned behavioral economic explanations do not account for the black-white wealth gap.

Clearly, wealth accumulation is facilitated by socioeconomic resources such as higher levels of educational attainment, white-collar jobs, and greater earnings (Keister 2000; Land and Russell 1996). A socioeconomic explanation posits that blacks have meager wealth accumulation because they lack adequate education, training, job skills and wages to invest and save. Blacks are known to be disadvantaged vis-à-vis whites on a wide range of socioeconomic and related characteristics including social origins, education, occupations, wages and marriage rates (Darity and Mason 1998; Mason 2010; Tomaskovic-Devey et al. 2005; Brown and Warner 2008). Therefore, one expectation might be that blacks would have more wealth than they currently do, or achieve wealth parity with whites, if they had the same socioeconomic resources as whites. Empirical studies, however, do not support this position. While racial differences in social origins and socioeconomic characteristics play a role in creating wealth disparities (Altonji and Doraszelski 2005; Land and Russell 1996), more than 70% of the race gap in wealth levels persists after controlling for a range of demographic, marital and socioeconomic factors (Oliver and Shapiro 1995; Shapiro 2004). Inherent in the differential socioeconomic hypothesis is a Friedmanian assumption that in a free-market capitalist society, impersonal market forces protect minorities from economic discrimination (Friedman 1962). Substantial evidence to the contrary (see below; Darity and Mason 1998; Mason 2010; Pager and Shephard 2008), and the persistence of racial wealth disparities despite accounting for an array of factors, indicate that a differential socioeconomic resource hypothesis, which does not account for discrimination or differences in inheritances and inter vivos transfers, is inadequate for explaining why black households have small amounts of wealth.

Given historic patterns of racial domination in economic domains and the fact that wealth is accumulated and transferred from one generation to the next, it is necessary to consider the importance of the role of historical discrimination in leading to the intergenerational transmission of asset poverty. Oliver and Shapiro (1995) argue that wealth is the best indicator of the ‘sedimentation of racial inequality’, the notion that the cumulative impact of historical inequalities have anchored minorities to the bottom of societies’ economic hierarchy, because it “captures the historical legacy of low wages, personal and organizational discrimination, and institutional racism” (p. 5). Because wealth is often passed on from one generation to another in the form of inheritance or inter vivos transfers, it is cumulative in nature; thus, the wealth holdings of contemporary cohorts are shaped by historical forms of racial domination such as slavery, Jim Crow laws, and discrimination.

Structural discrimination has shaped the life chances of blacks through processes of differential treatment. For a substantial part of U.S. history, not only did laws prohibit blacks from owning property, but they themselves were considered property. Whereas free labor during slavery resulted in unjust enrichment for wealthy white households, black families experienced intergenerational economic immobility. New forms of oppression emerged during the Jim Crow era that crippled upward social mobility among black families. For example, New Deal policies implemented in the 1930s, aimed at helping families recover economically from the Great Depression and credited with growing the middle class, provided old age insurance, aid to dependent families, unemployment insurance, and a minimum wage, however, many blacks were precluded from benefiting from these policies because disproportionately black occupations (e.g., agricultural and service jobs) did not qualify for benefits (Oliver and Shapiro 1995). Blacks also faced discrimination when applying for GI benefits such as loans for college tuition, purchasing a home, starting a business, and buying farmland—keys to upward mobility and the accumulation of wealth. Katznelson (2005) refers to this era as a time when affirmative action was white, underscoring the fact that whites benefited disproportionately from wealth enhancing policies while blacks did not.

Historical discrimination in housing and lending markets (e.g., redlining, steering, blockbusting, housing covenants, federal housing policies) has limited black home ownership and circumscribed the neighborhoods where blacks may live, resulting in severe residential segregation (Massey and Denton 1993). The racial composition of a neighborhood has significant implications for housing values and appreciation rates; homes in communities with a high proportion of blacks are worth less and appreciate at a much lower rate than those in predominantly white neighborhoods (Flippen 2004). Moreover, the concentration of black households in inner cities in tandem with the relocation of many businesses and well-paying jobs to primarily white suburbs resulted in diminished job opportunities and concentrated spatial disadvantage for blacks (Carrington and Troske 1998; Wilson 1987).

In addition to historical discrimination, present-day discrimination also hinders wealth accumulation in the black community. Although a majority of whites believe that whites and blacks have similar economic opportunities (Pager 2007) and 44% of Americans believe that discrimination against whites is just as big of a problem as discrimination against blacks and other minorities (Jones and Cox 2010), there is strong evidence that blacks continue to face substantial economic discrimination in employment, housing, and consumer and credit markets (Darity and Mason 1998; Pager and Shepherd 2008; Tomaskovic-Devey et al. 2005). Widespread employment discrimination, specifically discriminatory practices in hiring and wages, is confirmed in numerous studies using an array of methods including statistical regression, newspaper advertisements, audit studies and court cases (Darity and Mason 1998; Mason 2010). Compared to whites, blacks are less likely to be hired, have to search longer for jobs, have less work experience and tenure, and earn lower wages, controlling for all relevant human capital characteristics (Pager and Shepherd 2008; Tomaskovic-Devey et al. 2005). Such labor market discrimination leads to diminished lifetime earnings and, thus, reduces wealth accumulation.

Housing discrimination among blacks also continues to be a pervasive issue in the U.S. (Pager and Shepherd 2008). Audit studies of discrimination in housing markets reveal that blacks are discriminated against (e.g., steered to minority or less wealthy neighborhoods, offered less information, shown fewer properties, and given less assistance with financing) 16% of the time when looking for housing (Turner et al. 2003). Though declining recently, significant residential segregation along racial lines persists in the U.S. (Glaeser and Vigdor 2001)—segregation levels in many U.S. cities are nearly as high as they were in South African cities when segregation was legally enforced under the system of apartheid (Massey and Denton 1993)—and contributes to racial wealth disparities.

Present-day discrimination in consumer and credit markets means that blacks pay more than whites for the same goods and services; thus blacks are able to commit less of their income to savings and investments. For example, careful audit studies show that blacks pay between $446 and $1132 more than whites for a car despite having comparable credit histories, incomes, and negotiation strategies (Ayres 1995; Ayres and Seigelman 1995). Neighborhood characteristics also place blacks at a disadvantage in consumer markets. For example, Fellowes (2006) found evidence of a “ghetto tax”, whereby prices for an array of goods and service (car prices, car insurance, home insurance, check cashing, furniture, appliances, groceries) are higher in poor neighborhoods than they are in more affluent neighborhoods.

The cost of credit is also higher for blacks than it is for whites. With the recent collapse of the housing bubble, the high prevalence of predatory lending in mortgage markets has received considerable attention. Blacks are more likely than whites to receive sub-prime mortgages (i.e., high interest rates, pre-payment penalties and balloon payments, all of which increase the likelihood of foreclosure), even after controlling for factors such as the amount of the loan, and the borrower's income and credit rating (Avery et al. 2006; Philips 2010). Importantly, the negative economic consequences of discrimination in the arenas of employment, housing, and consumer and credit markets are likely to accumulate over time, severely limiting blacks’ capacity to build wealth.

Racial differences in social networks are also likely to influence wealth inequalities, because the family and friends of blacks are likely to be economically disadvantaged relative to those of whites, and in economically depressed communities there may be especially strong norms of social responsibility whereby prosperous individuals are expected to help those in need (Chiteji and Hamilton 2002). Thus, the wealth accumulation of high-earners in minority communities may be diminished because discretionary income is transferred to family and friends in need instead of being saved or invested. Indeed, accounting for racial differences in the economic situations of parents and siblings reduces the black-white wealth gap by more than a quarter (Chiteji and Hamilton 2002).

Another explanation that has received little attention is that health disparities likely contribute to the wealth gap between blacks and whites. Health problems are known to inhibit a family's ability to accumulate wealth by limiting their capacity to earn income and by increasing medical expenses (Smith 1999). Thus, given that blacks consistently have worse health than whites (Warner and Brown 2011; Williams and Collins 1995), their poor health is likely to hinder wealth accumulation and exacerbate wealth inequality (Smith 1995). Although considerable research has investigated the race gap in wealth, little is known about gender differences in wealth accumulation patterns. Below, I discuss several social pathways that may lead to gender inequality in wealth.

Gender and wealth

It is well-documented that women are economically disadvantaged relative to men, yet prior research on women's economic security and mobility has focused almost exclusively on income, with little attention to wealth. Consequently, relatively little is known about women's wealth holdings. As noted above, wealth is distinct from income, and a particularly important component of economic well-being. One reason for the scant attention to the gendered nature of wealth is the fact that wealth is considered to be a characteristic of households while gender is an individual-level characteristic. Because marriages have historically been between men and women, the gender-wealth relationship is principally relevant for nonmarried households (Chang 2010b). Yet, nonmarried households represent a major proportion of households in the overall population, and especially in the black community (Cherlin 1992). Therefore, gender disparities in wealth are likely to affect a significant proportion of women generally, with heightened disadvantage present for black women, in particular.

Chang (2010b), which is one of the only studies to investigate the relationship between gender and wealth, found that women have less wealth than men. Specifically, the study's findings revealed that widowed, divorced, and never married women have 60%, 45%, and 6%, respectively, of the wealth of their male counterparts. The finding that the gender gap is greatest among the never married, and smallest among widows, is consistent with research showing that marriage is a wealth enhancing institution—especially for women (Waite and Gallagher 2000)— and the fact that the entirety of marital wealth is retained by surviving spouses in the case of widowhood, rather than being split in two as is the case in the event of divorce. Due to the dearth of scholarship on women's wealth, the gendered nature of wealth has been undertheorized, with the exception of Chang's (2010a, b) insightful explanations for the gender gap discussed below.

Because present-day wealth holdings are shaped not only by contemporary opportunities and circumstances but also by those experienced earlier in life, the legacy of gender discrimination is likely to shape women's present-day amounts of wealth (Chang 2010a). For example, women faced especially high levels of discrimination in credit markets because it was lawful to deny applications on the basis of sex and marital status prior to the Equal Credit Opportunity Act, passed in 1974. In addition, Goldin (1990) notes that it was legal to deny jobs to women, pay them less than men, and fire them for getting married or pregnant until the passage of the 1963 Equal Pay Act and Title VII of the 1964 Civil Rights Act. Thus, for current cohorts of older women, building wealth for was particularly difficult, owing to the cumulative effects of rampant discrimination in lending and labor markets.

Present day pay inequality also plays a role in generating wealth gaps between men and women. Given the importance of income for saving and investing, the persistent wage gap between men and women contributes to the gender inequality in wealth. In 2007, women were paid only 78% of what men earn (Bishaw and Semega 2008). Moreover, women's long-standing higher rates of poverty (Mason 2010), referred to as the feminization of poverty (Pearce 1978), is a major obstacle for women's wealth accumulation. While wage inequality certainly contributes to the wealth gap, Chang's (2010a) finding that the gender wealth gap persists after controlling for income, sociodemographic characteristics and inheritances, suggests that other factors also underlie the wealth gap.

One reason that the income-wealth relationship among women is not as strong as it is for men is because they are less likely than men to benefit from the “wealth escalator”, a term dubbed by Chang (2010a) to describe how an array of fringe benefits (e.g., employer pensions, health insurance, stock options), tax codes (e.g., capital gains taxes, tax credits), and government benefits (e.g., Social Security, unemployment insurance, welfare) accelerate the conversion rate of income to wealth for advantaged groups. For example, employer-sponsored retirement plans augment one's ability to accumulate wealth faster than just relying on income, especially given the tax benefits and compounding of interest over time. However, women are more likely than men to work part-time (Blossfeld and Hakim 1997; Fuchs 1989) and are more likely to have clerical, service, or sales jobs (Weeden 2004) —the types of jobs that are less likely to include fringe benefits. Despite appearing to be gender-neutral, fringe benefits have a disparate impact on women's economic security. Chang (2010a) notes that gender differences in debt also contribute to wealth disparities; although men and women have comparable rates of overall debt, and the fact that women are less inclined to use credit to purchase luxury items, they have higher annual percentage rates on their credit cards, and are more likely to have credit card debt due to their greater reliance on credit to cover living expenses when income is inadequate. Women's reduced access to the wealth escalator in tandem with their greater credit card debt further accentuates the gender wealth gap.

Mothers often take breaks from full-time employment, and a substantial proportion exit the labor force for an extended period of time to parent. Due to their disproportionate caregiving roles, women continue to be more likely than men to work part-time (Blossfeld and Hakim 1997; Fuchs 1989), accrue less work tenure and experience less job continuity over the life course (Christie-Mizell 2006). The intermittent work histories of many mothers reduce their lifetime earnings and limit access to the wealth escalator (Chang 2010a, b). The responsibilities and challenges of single motherhood, which is particularly common in communities of color (Martin et al. 2003), make building wealth an especially difficult task. In addition to lower wages and reduced access to the wealth escalator, single parents shoulder the costs of raising a child alone. Because single mothers are more likely than single fathers to have custody of children, they pay disproportionate financial costs in raising children. Moreover, of all single mothers awarded child support, nearly two-thirds of them did not receive the full amount of support owed (U.S. Census Bureau 2003). Thus, it is not surprising that Chang (2010b) found that the gender gap in wealth among single adults is greatest among those with children under the age of 18.

Women's poorer health relative to men may also limit their ability to build wealth. Despite living longer than men, women are more likely to be disabled (Warner and Brown 2011), to suffer from chronic health problems, and to have multiple comorbidities (Laditka and Laditka 2002; Newman and Brach 2001). Women's greater number of years spent in poor health is likely to limit their ability to earn income and lead to higher health-related expenses, thus exacerbating the gender wealth gap. While this section has discussed the gendered nature of wealth, less is known about how gender inequality in wealth interacts with racial wealth inequality. We now turn to this topic, discussing hypotheses about black women's wealth accumulation.

Black women's wealth accumulation

How do race and gender inequality combine to shape black women's wealth trajectories? As noted above, studies have shown that blacks possess less wealth than whites (Oliver and Shapiro 1995) and that women have less wealth than men (Chang 2006). However, prior research on wealth has tended to treat race and gender as independent dimensions of social stratification, examining race differences while statistically controlling for gender or vice versa. Because fewer studies have investigated the joint and simultaneous consequences of race and gender, it is unclear how race and gender intersect to shape the wealth accumulation of black women. A key goal of this paper is to employ an intersectionality approach to elucidate wealth trajectories for black women.

The intersectionality perspective, an integral aspect of Black Feminist Thought (Collins 2000) and Critical Race Theory (Delgado and Stefancic 2001), emphasizes the fact that dimensions of stratification (e.g., race, class and gender) are interconnected and simultaneously create social locations that structure life chances (Andersen and Collins 1995; Crenshaw 1989; McCall 2005). In terms of the current focus, black women are simultaneously disadvantaged as a result of being both black and female and face both the racialized and gendered obstacles to wealth accumulation discussed above (Davis 1981; King 1988). Specifically, black women's capacity to build wealth is likely to be constrained by racial differences in socioeconomic resources, the legacy of historical discrimination, present-day racial discrimination, social networks, and racial health disparities in addition to gender inequality in wages and labor market characteristics, the costs of single parenthood, and gender disparities in discrimination and health.

Andersen and Collins (1995) note that, “seeing race, class and gender only in additive terms misses the social structural connections between them and the particular ways that different configurations of race, class, and gender affect group experiences” (p. xii). Consistent with an intersectionality approach, the overlapping impacts of racial and gender domination are likely to combine in a multiplicative fashion that places black women in a uniquely precarious economic position (Brewer 1993; Landry 2006). Indeed Mason (2010) found that black women have the highest rates of poverty of all other race-gender groups, suggesting that the feminization of poverty is racialized and compounded for black women. Similarly, Chang's (2010b) study showed that the gender gap in wealth is greatest among blacks and that nonmarried black women have the least wealth of all groups—only $100 of net worth (excluding vehicle equity).

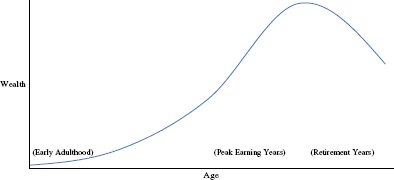

While a few prior studies have found that black women have low levels of wealth at any single point in time, it remains unclear how black women's trajectories (i.e. intra-individual rates of stability and change) unfold as they approach retirement age. According to the life cycle hypothesis (LCH), the standard economic model for understanding savings and consumption behavior, rational actors will accumulate wealth by saving and investing throughout their working years in anticipation of retirement, when they will begin dissaving, tapping into their nest egg for retirement income (Modigliani and Brumberg 1954; Modigliani 1986). Thus, steep increases in wealth are expected during high earning years, peaking around retirement age (approximately 65) and subsequently declining (see Fig. 1). Although the LCH is the dominant economic explanation for wealth accumulation as individuals/households age, few studies have utilized appropriate methods to test the hypothesis (i.e., panel data spanning multiple life stages and longitudinal analysis that account for attrition). Instead, studies have used cross-sectional data (Land and Russell 1996) or examined differences in wealth across two time points (Gittleman and Wolff 2004) to approximate life course patterns, both of which are subject to biases.

Life cycle model of wealth accumulation

The use of an intersectional approach in this study attempts to raise questions about whether the LCH is an appropriate model for representing black women's patterns of wealth accumulation. The LCH's central tenet that individuals are able to earn income, save and invest without artificial barriers or constraints is inconsistent with the experiences of black women in light of well-documented institutional racism and sexism in the economic sphere (Darity and Mason 1998; Mason 2010; Pager and Shepherd 2008). The LCH would predict steady increases in wealth resulting in substantial wealth accumulation prior to decumulation in later life. However, consistent with intersectionality, this research hypothesizes that black women experience chronic asset poverty in middle and late life, having modest amounts of wealth and relatively flat wealth trajectories.

Data and methods

Data from waves 1 through 7 of the Health and Retirement Study (HRS) is used to investigate black women's wealth trajectories between ages 51 and 73. The target population for Wave 1 of the HRS includes adults in the contiguous United States, aged 51–61 in 1992 (1931–41 birth cohort), who reside in households; blacks were oversampled to allow independent analysis of racial groups. Respondents were re-interviewed in 1994, 1996, 1998, 2000, 2002, and 2004. Married respondents are not included in the analytic sample due to the focus on the gendered nature of wealth, which is only relevant for nonmarried households (Chang 2010a). Therefore, the sample consists of nonmarried black women (baseline N=786). Because of changing marital statuses across waves, respondents exit and enter the analytic sample based on their marital status at each wave. They are included in the sample for each wave that they meet the selection criteria. This results in 3,072 repeated observations of widowed (1,387), divorced (1,313) and never married (372) black women.

Wealth measures.

Household net worth is the sum of home equity (primary residence value—mortgage), real assets (other real estate, vehicles, and business equity), and financial assets (checking, savings and money market accounts, IRA/Keogh, 401(k), stocks, trusts, mutual funds, investment trusts, and bonds) minus debts. Pension wealth is not included because of serious data quality issues. The measure of net financial assets is the sum of financial assets (checking, savings and money market accounts, IRA/Keoghs, stocks, trusts, mutual funds, investment trusts, and bonds) less debt. Because repeated wealth measures are taken from different years, wealth is converted to 2004 dollars using the Consumer Price Index (CPI). Additionally, because wealth variables are measured at the household-level, wealth equivalencies across households are created by dividing wealth by the square-root of household size (Azpitarte 2010; Brady 2009); the wealth measures are also logarithmically transformed to normalize for the left skewness.

Covariates.

Age (range=51–73; mean=61) is used to estimate how wealth trajectories change as a function of age. A measure of the number of measurement occasions (range=1–7; mean=4.1) is also included in the models to control for the fact that asset poor households are likely to attrit at higher rates than wealthy households.

Analytic strategy.

To investigate wealth trajectories between the ages of 51–73, random coefficient growth curves were modeled within a mixed model framework (i.e., hierarchical linear model), which is an integrated approach for studying the structure and predictors of individual growth. These models are well-suited for panel data where individuals are repeatedly interviewed, and for the assessment of individual change with age (Raudenbush and Bryk 2002). A hierarchical strategy is used, where repeated observations (Level 1) are nested within respondents (Level 2). The growth curve models generate individual trajectories that are based on estimates of person-specific intercepts (initial value) and slopes (rate of change) that describe intra-individual patterns of change in wealth as a function of age. Comparisons of nested likelihood ratio tests (LRTs) of various shapes of wealth trajectories (e.g., linear, quadratic or cubic models), suggested that a linear growth curve with random intercepts and random linear age slopes provided the best fit to the data.

Given that this study draws on wealth data from 7 different years between 1992 and 2004 and the occurrence of fluctuations in the business cycle, the wealth of the respondents may be somewhat higher (or lower) during particular years. Supplemental analyses with dummy indicators of survey years suggested that the findings of this study are robust to period effects; for the sake of parsimony, controls for survey year are excluded from the models. Since the dependent variables are logged, the coefficients for continuous covariates indicate the relative change in wealth for a one unit increase in the covariate. The percentage change in wealth is revealed by multiplying the relative change coefficient by one-hundred (Hardy 1993: 57).

Results

Table 1 presents the median values of net worth and net financial assets for black women who are widowed, divorced, and never married at age 51. Net worth levels for all groups of single black women are very low: on average, black women who are widowed, divorced, or never married have only $14,045, $7,026, and $6,750, respectively. Moreover, their low levels of net worth would be substantially lower if vehicle equity were excluded (Chang 2010b). To put the amount of their wealth in perspective, Chang (2010b) found that similarly aged nonmarried white men, white women, and black men had approximately $123,000, $111,000, and $61,000, respectively (in 2007 dollars). The fact that widowed women have more wealth than divorced and never married women is likely due to the facts that widows accrue the economic benefits of marriage and receive all marital property upon the death of their spouse, rather than splitting assets in two as is the case in the event of divorce (Waite and Gallagher 2000). The median value of net financial assets (which exclude tangible assets such as homes and vehicles) for widowed, divorced, and never married black women is zero, indicating that at least half of nonmarried black women have zero or negative net liquid assets.

Median net worth and net financial assets at baseline by marital status

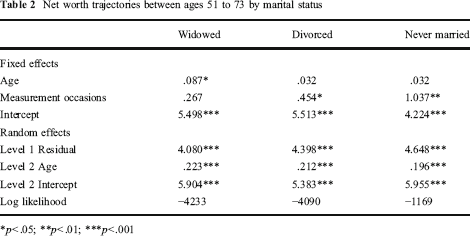

Table 2 presents estimates from the random coefficient growth curve models on the impact of age on growth in net worth by marital status. The age coefficients are not statistically significant for divorced or never married women, indicating that they experience no growth in net worth leading up to retirement, which contradicts predictions of the LCH. Widowed women, however, have $14,045 in net worth at age 51 and that their net worth grows at a rate of 8.7% (.087 * 100) per year resulting in a total of $40,927 at age 73, which is still relatively small from a LCH perspective—nonmarried men (of all races) in their 60 s have median wealth values of $168,500 (Chang 2010a). Figure 2 shows the magnitude and shape of black women's model-implied net worth trajectories based on the initial wealth levels and age coefficient estimates in Table 2.

Net worth by marital status

Net worth trajectories between ages 51 to 73 by marital status

p<.05;

p<.01;

p<.001

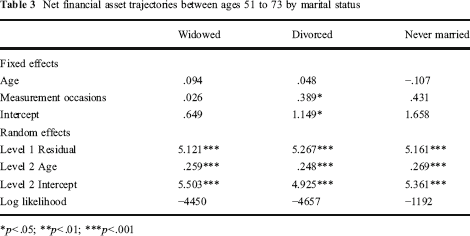

Growth curve models of net financial asset trajectories are presented in Table 3 and illustrated in Fig. 3. They reveal that the picture of black women's net financial assets is even bleaker than that of net worth: average widowed, divorced and never married black women have virtually no net financial assets at age 51, and do not accumulate any as they age. Overall, results show that most black women experience chronic asset poverty characterized by persistently low and flat trajectories of net worth and net financial assets.

Net financial assets by marital status

Net financial asset trajectories between ages 51 to 73 by marital status

p<.05;

**p<.01;

p<.001

Discussion

Stratification of opportunity structures by race and gender result in the accumulation of economic disadvantages for black women. This study is among the first to investigate nonmarried black women's wealth trajectories leading up to retirement age. Findings reveal that, despite strong labor force attachment and job stability across the life course (Brown and Warner 2008), the average black woman has very little wealth in middle and late life. In sharp contrast to the LCH—which predicts that individuals build a nest egg by saving and investing over the course of their careers in anticipation of using the substantial accumulated wealth for living expenses during retirement and to pass on to future generations—most black women have low levels of wealth in their early fifties and experience little to no wealth growth through their mid-seventies. Most alarming is the finding that at least half of black women have zero or negative liquid assets throughout middle and late life, suggesting that they lack the savings to cover minor, unanticipated expenses such as the costs of moving, home or car repair or a medical bill.

While the LCH may be suitable for predicting the savings, investment, and consumption patterns of white, middle class, married families in the mid-twentieth century, it is inadequate for explaining the experiences of black women. The LCH's implicit assumption that impersonal market forces in a capitalist society protect minorities from artificial barriers (e.g., institutional racism and sexism) to building wealth is contradicted by many high-quality empirical studies (See Darity and Mason 1998; Pager and Shepherd 2008). Far from the meritocratic assumptions of neoclassical economic theories, black women's capacity to build wealth is constrained by the intersection and accumulation of both racial and gender disadvantages. Such detriments include racial differences in socioeconomic resources, the legacy of historical racial discrimination, present-day racial discrimination, the lack of resource-rich social networks, gender inequality in wages and the labor market, gendered access to the wealth escalator, the costs of single motherhood, and race-gender disparities in health (Chang 2010a, b; Oliver and Shapiro 1995). Moreover, these disadvantages are likely to have reciprocal and compounding negative consequences that mount over the life course and across generations.

The lack of wealth accumulation among black women has serious implications for their economic security in later life. For instance, many black women must delay or forego retirement due to a lack of savings; a disproportionate number of older black women are too poor to retire, yet too ill to work, placing them in a particularly precarious position (Brown and Warner 2008). Issues of late-life economic security are increasingly important as the baby boom cohort approaches retirement age. The metaphor of a “three-legged stool” is often used to characterize the three major sources of retirement income—Social Security, employer-provided pensions, and personal savings—in order to convey the idea that all three approaches are needed to provide income security in retirement. Recently, pensions have become a less reliable income source, as many employers have shifted to providing pensions that are less costly to employers, yet more costly and less generous to employees. Also, the increasing old-age dependency ratio has sparked a great deal of concern and speculation about the future solvency of the Social Security system, leading some to propose cuts in benefits. In this context, personal savings and investments are likely to become increasingly important sources of economic security in later-life.

Black women's miniscule wealth holdings are likely to have negative consequences for the distribution of wealth among future generations. Parental wealth affects children's prospects for intra-generational upward wealth mobility by increasing access to educational and occupational opportunities, as well as access to credit (Holtz-Eakin et al. 1994). A major source of the wealth gap stems from the fact that minorities are less likely than whites to possess transformative assets such as homes and inheritances, which are keys to economic mobility (Shapiro 2004). Just as the present-day paucity of transformative assets in the black community is a direct consequence of inter-generational asset poverty (Smith 1995; Wilhelm 2001), the racial wealth gap among future generations is likely to be maintained or exacerbated, unless appropriate policy measures are taken.

There are a number of policies that would increase wealth among black women and reduce wealth inequality. Eliminating racial and gender differences in human capital and labor market characteristics is necessary for black women's economic security, however, it is not sufficient, owing to widespread discrimination. As noted above, pervasive racial and gender discrimination in the economic arena carries significant cumulative cost (Darity and Mason 1998; Pager and Shepherd 2008). Importantly, aggressive enforcement of anti-discrimination laws would mitigate these costs and facilitate asset accumulation among black women.

Consistent with the human rights principle of redistributive justice, some have proposed policies of economic reparations for black Americans to ameliorate hundreds of years of injustice ranging from slavery, to the Jim Crow system, to present-day discrimination (Darity 2008). Although an overwhelming proportion of the American public (92%) favors a more equitable distribution of wealth than current levels when asked about their abstract preferences without regard to race (Norton and Ariely 2011), there is weak public support for economic reparations for blacks (Dawson and Popoff 2004). However, historical precedents exist: the U.S. awarded $1.25 billion to Japanese Americans who were in internment camps during WWII and, in 2010; $1.25 billion was awarded to black farmers who experienced discrimination when applying for loans from the U.S. Department of Agriculture. Broad-based reparations for black Americans would likely ameliorate asset poverty in the black community and help close the black-white wealth gap (Oliver and Shapiro 1995). Darity (2008) notes that economic reparations would serve a number of important functions including the acknowledgement of past injustices, redress for the injustices, and closure of the grievances held by blacks.

Hamilton and Darity (2010) propose ‘baby bonds’ as a means for increasing the wealth holdings of all asset poor Americans. They propose that U.S. citizens born to parents with wealth holdings below the national median wealth level would receive a trust fund with an average value of $20,000, with higher values going to those from families with the least assets. These funds would not be accessible until the individuals’ 18th birthday. Despite being ‘race-neutral’, a disproportionate number of blacks would benefit from such a policy because the vast majority of black households have less than the national median level of wealth.

In addition to explicit asset-building policies, reforms aimed at strengthening the social insurance safety net for older adults generally, and older black women in particular are needed. For example, establishing a minimum benefit for Social Security benefits would reduce poverty rates among financially vulnerable populations. A caregiver credit for Social Security should also be implemented to compensate individuals for unpaid family labor such as raising children and providing care for the elderly, which has traditionally been done by women (Chang 2010b).

The collapse of the U.S. housing bubble and recession of the late 2000s has likely had a disproportionately negative impact on black women's wealth because this group is particularly vulnerable to macroeconomic fluctuations (Conrad and Brown 2011; Mason 2009). In fact, the recent recession resulted in dramatic declines in household wealth and there is some evidence that it may have increased the wealth gap between blacks and whites. For example, whereas the white-to-black wealth ratio was 11 in 2004, it increased to 19 by 2009 (Kochhar et al. 2011). Moreover, between 2003 and 2009, the black-white gap in homeownership rates for women increased (Conrad and Brown 2011). Thus, future research examining the influence of the recent recession on wealth inequality is urgently needed.

This study, like all studies, has limitations that warrant discussion. For example, while the HRS has high quality wealth data (Smith 1995), it lacks information on discrimination experiences. Consistent with critical race theory's tenet that individuals are able to effectively communicate and explain their experiences with racism (Brown 2003), future studies should directly examine the impact of discrimination experiences on wealth accumulation. In addition, because the HRS samples households, homeless individuals are excluded, which likely upward biases estimates of black women's wealth. Therefore, it is important that future research on wealth inequality should include homeless persons.

Overall, the present study demonstrates the utility of an intersectionality approach for understanding how racial and gender inequality combine and accumulate over time, placing black women in an economically vulnerable position. As black women approach retirement age, they are on the precipice of financial peril. Their financial fragility in later life is directly linked to barriers to wealth accumulation and transmission faced by previous generations, as well as their own exposure to institutional racism and sexism throughout their lives. Therefore, future research should examine how intergenerational transmission of asset poverty and social and economic factors across the life course contribute to late-life financial fragility among black women.

Footnotes

Acknowledgements

Research support was provided to the author by the Robert Wood Johnson Foundation Center for Health Policy at Meharry Medical College (RWJF Grant 64300 and sub-award 100927DLH216–02). I thank William A. Darity, Jr., Darrick Hamilton, and C. André Christie-Mizell for helpful comments and suggestions on prior drafts.