Abstract

The development of China’s steel industry has been phenomenal, and in 2018, China’s crude steel production reached 928.3 million tonnes and accounted for 51.3% share of global crude steel production. In the past 70 years, along with the country's growth and development, China steel industry has experienced a period of unstable development, rapid growth, reduction and optimization. The purposes of this article are to provide some historical background of the steel industry development in China. In this article, we will summarize the unstable development of China’s steel industry from 1949 to 1978. We will, then, describe stable development over the reform and opening-up period from 1978 to 1999 and rapid development in the boom period from 2000 to 2014. Finally, we will discuss how the steel industry copes with the new challenges in China’s move towards supply-side reform since 2015 and the future directions of the development of China’s steel industry.

Introduction

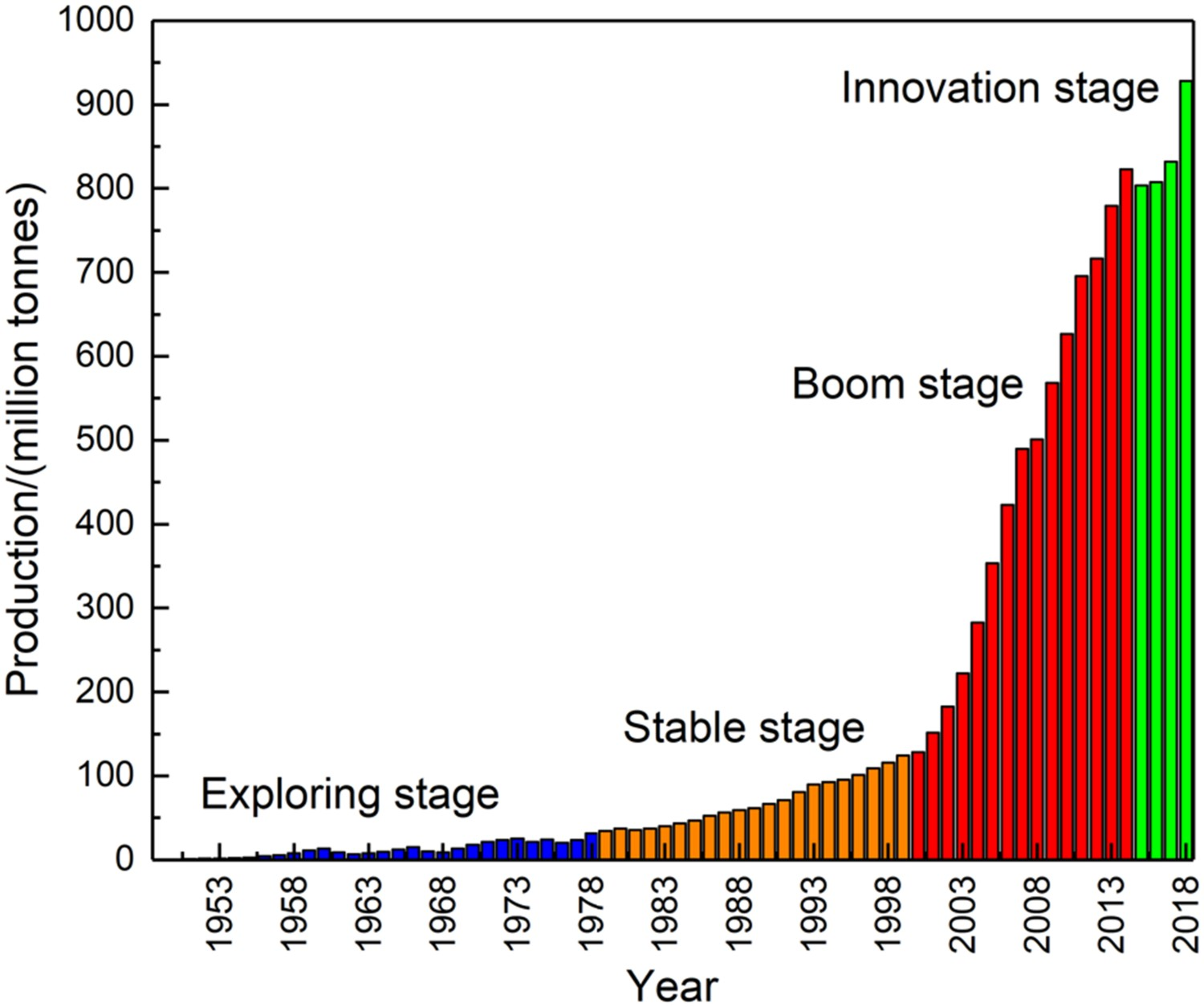

The development of China’s steel industry has been phenomenal, and in 2018, China’s crude steel production reached 928.3 million tonnes and accounted for 51.3% share of global crude steel production. In the past 70 years, along with the country's growth and development, China steel industry has experienced a period of exploring, growth and optimization, which is generally divided into four stages as shown in Figure 1. The first stage is from the founding of the People's Republic of China in 1949 to the end of the Cultural Revolution in 1978 and is an exploring stage with unstable development. The second, from the beginning of reform and opening-up to the end of the twentieth century, is an early stage of stable development. The third, from the beginning of the twenty-first century to 2014, is an accelerated stage with rapid development. The fourth is from 2015 and has been a stage of innovation and optimization of steel industry. This paper consists of four sections accordingly.

The purposes of this article are to provide some historical background of the steel industry development in China, including its rapid expansion over the reform period, and how the steel industry copes with the new challenges in China’s move towards supply-side reform in recent years, and the future directions of the development of China steel industry.

Exploring stage with unstable development

China steel industry is in its exploring stage from 1949 to 1978 with a very unstable development trend. In 1949, China steel output was only 158,000 tonnes, ranking 26th in the world. After 1949, the development and modernization of China steel industry was carried out with the restoration, transformation and expansion of steel equipment before 1949. From 1949 to 1952 (3-Year Recovery), 34 blast furnaces and 26 flat furnaces were restored. In 1952, China produced 1.929 million tonnes of iron and 1.349 million tonnes steel. In 1953, electric arc furnace production resumed in steel companies in Daye, Chongqing and Taiyuan [3]. During the period of the first Five-Year Plan (1953–1957), the iron and steel production was resumed after the repair and transformation of the steel production equipment left before 1949. During the Great-Leap-Forward period (1958–1961), 5 years of adjustment (1961–1965) and the Cultural Revolution (1966–1976), the output of crude steel in China has risen and fallen three times, with successful experience and lessons of failure.

From 1949 to 1978, China's cumulative steel output is about 300 million tonnes. Three large-scale steel bases in Anshan, Wuhan and Baotou were built, as well as local backbone steel companies in Taiyuan, Panzhihua, etc. At the eve of reform and opening-up stage (1978), China had 982 ironmaking blast furnaces with a total volume of 87,204 cubic meters; 98 steelmaking furnaces with a total capacity of 17,188 tonnes; 276 steelmaking converters with the total capacity of 3034 tonnes; 1678 electric steelmaking furnaces with a total capacity of 4156 tonnes. At this stage, China has also established several education and research institutes that had focused on metallurgy, such as University of Science and Technology Beijing, Northeastern University, and Central Iron & Steel Research Institute. They developed and applied technologies such as oxygen top-blown converter, continuous casting, refining furnace and continuous rolling, initially formed a relatively complete steel R &D system in China.

An early stage of stable development

Since the reform and opening-up (from 1978 to 2000), China's economy developed rapidly and steel demand continued to grow. China’s planned economy gradually transited to the market system. After the transition, steel productivity gradually increased. This period was the startup stage of China steel industry with a stable development situation for more than 20 years. At this stage, China's crude steel output increased from 31.78 million tonnes in 1978 to 128.5 million tonnes in 2000, an increase of 4.04 times, and an annual growth rate of 6.56%. In 1996, China's crude steel output reached 101 million tonnes, and China became the world's largest steel producer then. It shall be pointed out that during this period Baosteel was established, the most modern and competitive steel company in China. Baosteel is the first modern steel manufacturing in China [4].

Technology transformation of existing steel companies

At the beginning of reform and opening-up, China steel industry was far behind the world's advanced level, e.g. production efficiency is low, and there is no real modern steel companies. At that time, the output of open-hearth steel still accounts for about one-third steel production, and continuous casting billet accounts for less than 10%. The ironmaking and steelmaking processes were not optimized for their full production in a considerable number of steel companies. During this period, most of the State investment in the steel industry was used for the construction of Baosteel.

In the middle and late 1980s, steel industry focused on building new capacities and adapting new technologies. For example, WISCO built 3200 cubic meters of blast furnace, Tangshan Steel built two 1200 cubic meters blast furnaces; Shougang constructed a 210-ton converter steelmaking plant, and TISCO built a 50-ton converter steelmaking plant. More than 70 continuous casting machines were built in the same period and the national total continuous casting capacity reached more than 30 million tonnes. The production capacity of medium and large plates has also been greatly improved through the construction of Ansteel 4300-mm-thick plate rolling mill, Baosteel 4200 mm/3500 mm rolling mill and NISCO, Handan Steel 2800 mm medium plate rolling mill.

Modernization of China steel industry through the establishment of Baosteel

In early 1977, Chinese government planned to build an ironmaking company in Shanghai. This was the original vision of Baosteel Project. To realize the modernization of China steel industry and to promote the further development of the national economy, in 1998 Chinese government decided to build a large-scale modern steel company. On the 23rd December of 1978, the second day of proclamation of Reform and Opening-up, Baosteel Project started. Baosteel Project was the largest engineering project in China after 1949. At that time, there was no experience in building large-scale modern steel companies in China. In the beginning, all the production lines were completely imported from Japan, so the investment was huge. In 1995, Phase I of Baosteel project was completed and in operation, while Phase II already started in 1992. The total investment of Baosteel Phase I and Phase II projects cost more than 30.12 billion Chinese Yuan, and a total of 670,000 tonnes of equipment were purchased, including 466,000 tonnes of imported equipment and 204,000 tonnes of domestically produced equipment. The domestic equipment accounted for 12% in Phase I, 57% in Phase II and finally increased to 80% in Phase III in 1993.

Market-oriented operation in China steel industry

In the 1990s, the Handan Steel pioneered a market-oriented operation mode which helped them succeeded in turnaround from deficit to profit-making company. The market-oriented operation mode greatly incentivized the company to adopt modern management strategy, and the results have been remarkable. From 1991, 1992–1993, the operation cost was reduced by 6.4%, 4.8% and 6.1% respectively over the previous year, and the accumulated profit for the third consecutive year exceeded 700 million yuan. Even in the difficult period of the Asian financial crisis, Handan Steel still maintained a profit of more than 500 million yuan. In 1996, Chinese government commanded all steel manufacturers in China to adopt the market-oriented operation model.

High-speed development at the boom stage

The third stage of China steel industry is from the beginning of the twenty-first century to 2014. On the 11 December 2001, China became a member of the World Trade Organization (WTO), and the admission of China to the TWO was preceded by a lengthy process of negotiations and required significant changes to the Chinese economy. It must be noted that China's accession to the WTO brought the golden decade to development of the steel industry. Despite the impact of the international financial crisis, China's crude steel output was maintained a rapid growth trend, from 128.5 million tonnes in 2000 to 822.7 million tonnes in 2014; more importantly, the quality of the products improved significantly. This is the boom stage of China steel industry, achieving a high-speed development.

Since the beginning of the twenty-first century, important technological progresses of China steel industry included independent design, independent construction, independent operation and independent management of a new generation of steel companies in coastal areas, like Caofeidian and Zhanjiang steel companies. These new coastal steel manufacturers aim for high-efficiency and low-cost clean steel manufacturing, efficient energy conversion and recycling, processing and recycling of large-scale social wastes [5].

Expansion to meet market need for rapid economic development

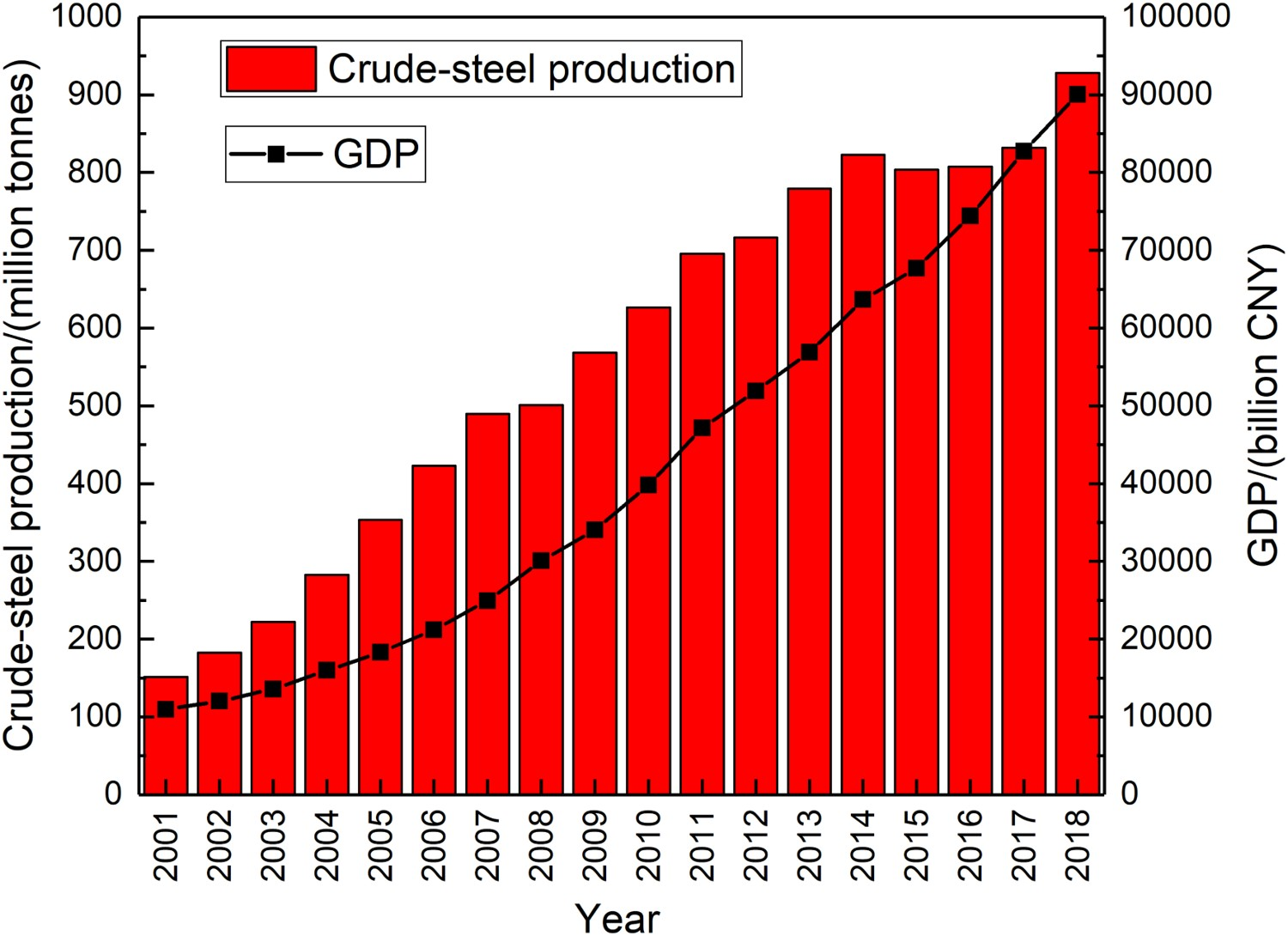

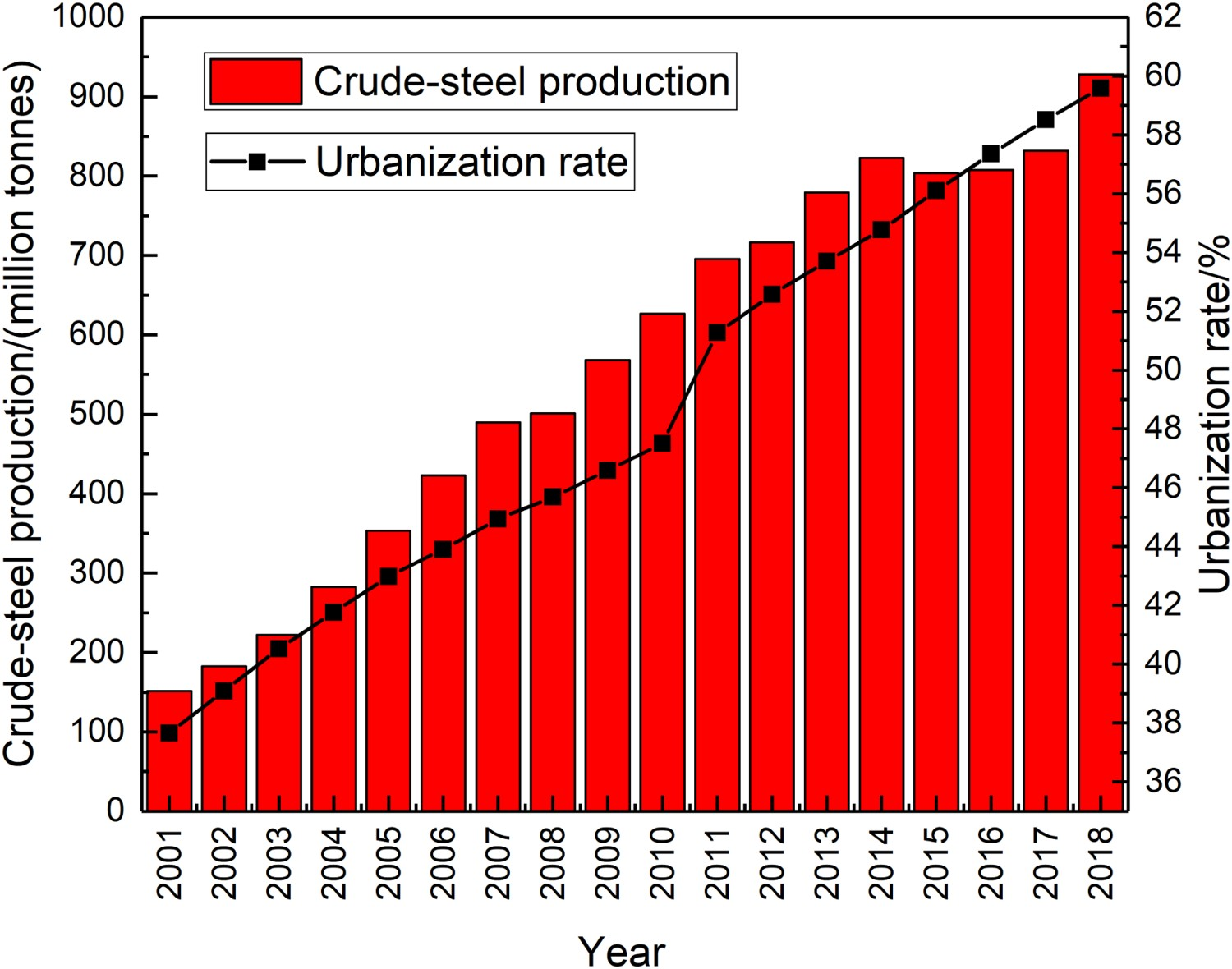

As shown in Figure 2 and Figure 3, during the 10th Five-Year Plan period (2002–2007), China's GDP grew at an average annual rate of 9.8%, and the urbanization rate increased by 1.36% per year. The crude steel output increased 2.75 times, with an average annual growth rate of 22%. During the 11th Five-Year Plan period (2008–2013), the average annual growth rate of China's GDP is 11.4%, and the urbanization rate is increased to 1.39% per year. The crude steel production increased 1.81 times, with an average annual growth rate of 12.6%, to meet the demand for the rapid GDP growth. . The growth of national economy and crude steel production (2001–2018) [6]. . The urbanization rate and crude steel production (2001–2018).

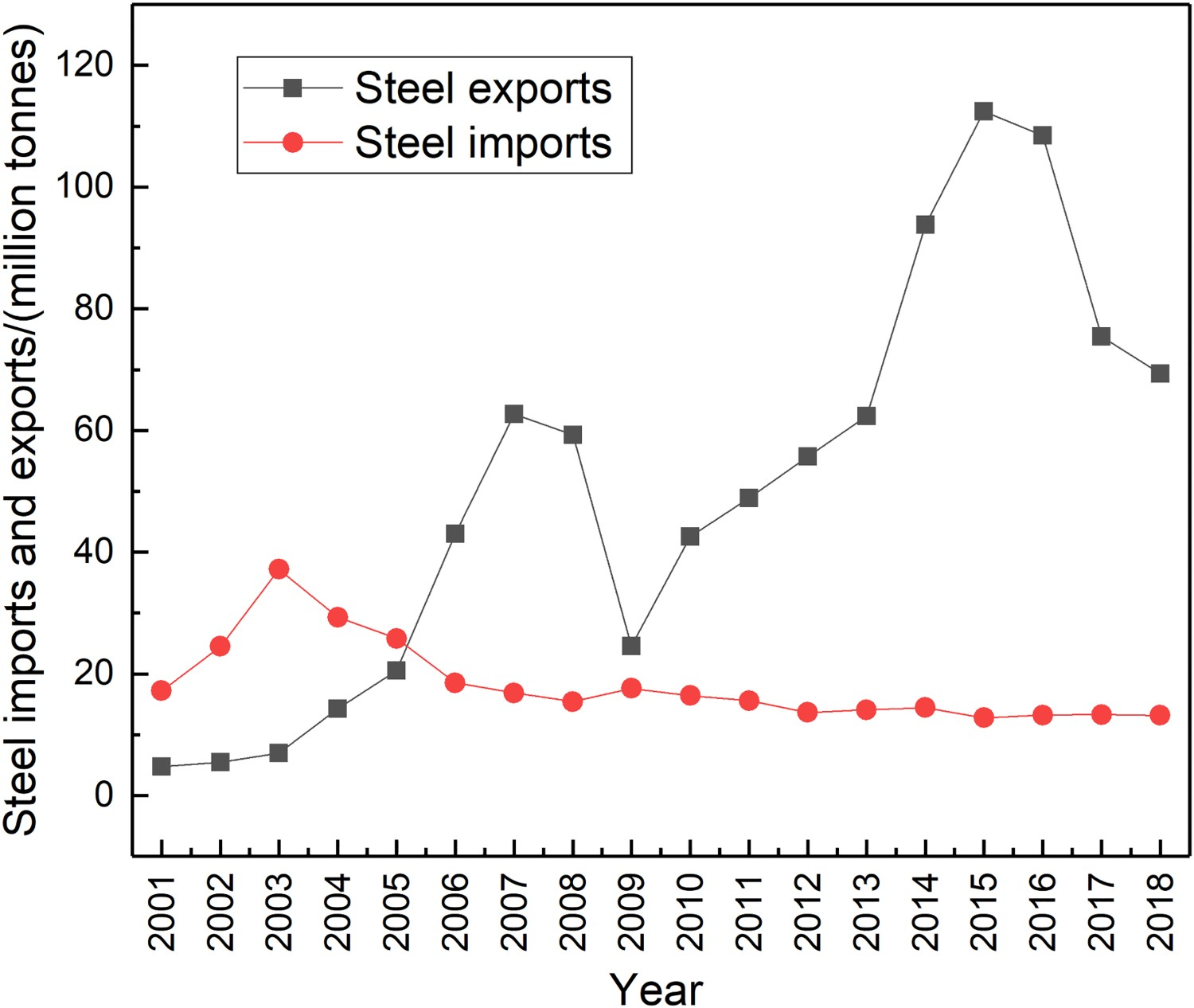

The end of China's steel shortage era

China had always faced the problem of long-term net import of steel products by 2005. In 2006, China exported 43.01 million tonnes of steel and imported 18.51 million tonnes of steel. As shown in Figure 4, the net export of steel in China reached 24.5 million tonnes in the whole year, which ended the history of net import of steel for 57 consecutive years after 1949. . Comparison of China's steel imports and exports from 2001 to 2018 [7].

Modernization of China steel industry

With the commissioning of a large number of new ironmaking, steelmaking and rolling facilities, and the replacement of old equipment, the technical level of China steel industry has been further improved in this period.

State key projects such as Shougang Jingtang and Ansteel Bayuquan were completed and in production, which means China has the ability to independently integrate and construct modern coastal steel bases. Meanwhile, China reduced 170 million tonnes capacity of old ironmaking production lines and 69 million tonnes capacity of steelmaking production lines during the 11th Five-Year Plan period (2008–2013). During the 12th Five-Year Plan period, China further reduced 91 million tonnes capacity of old ironmaking production lines and 94.8 million tonnes capacity of old steelmaking production.

At the end of 2014, the blast furnaces with over 1000 cubic metres capacity accounted for about 65% of the total ironmaking production, and the converters of over 100 tonnes capacity (electric furnaces) accounted for more than 56% of the total steelmaking production. The steel industry built 89 production lines of hot-rolled wide-band steel rolling mills, 84 production lines of medium-thick plate mills and 58 production lines of cold-rolling mills. Automation and the level of informatization in the metallurgical industry increased significantly, and new industrial model represented by E-commerce has taken place in some steel companies.

Innovative development

Since 2015, China's economic growth has transformed from high speed (annual GDP growth rate over 10%) to medium-high speed (annual GDP growth rate around 6–8%). In 2015, China's crude steel production was 804 million tonnes, fell 2.3% year-on-year. It was the first time for steel production to decline since 1982. In the same year, China's actual steel consumption was 664 million tonnes, fell 5.4% year-on-year, the first time to decline since 1996. China Steel industry faced new challenges.

The challenges for China steel industry

The growth of the China steel industry has benefitted from the rapid economic development and strong domestic demand, in 2014, China's steel production reached 800 million metric tonnes. However, China steel industry is facing two challenges: overcapacity and production fragmentation. First, for long-term sustainable development, domestic steel manufacturer will have to put a cap on their production. Second, China's steel industry is fragmented to some extent. The lack of consolidation in China Steel industry results in duplicated development and cut-throat competition among China steel manufacturers. Most of small-medium size steel companies suffer from weak competitiveness. China steel industry is big, but not strong. Mergers and acquisitions, and innovative development are the key strategy for the development of China's steel industry.

Internationally, the uneven pace of global economic recovery continues to raise concerns and the global steel demand has entered a period of plateau. Overcapacity in steel industry has become a global problem. China steel industry has strong competitiveness and will need to play an important role in international capacity cooperation and innovative development.

Supply-side reform of China steel industry

The development of China steel industry from 1980 to 2010 relied on the demand side. There were three stimulating forces of the growth: investment, consumption and export, and these three forces determined the rapid growth in China steel production over the period. From the 2015, China steel industry has gone into supply-side reform which is a long-term issue and requires in-depth institutional planning and long-term adjustment. The first step of the supply-side reform in China steel industry was to eliminate the supply surplus. Eliminating the steel supply surplus and releasing the excessive resources trapped inside steel industry improve the efficiency of resource use and promote economic growth, which, currently, is the essence of supply-side structural reform in China steel industry. In 2016, China steel industry made new breakthroughs in the supply system reform by dissolving the excess capacity of 150 million tonnes, turning losses into profit. The profit of China steel industry increased significantly in 2017, reached the best level in history in 2018 [8].

Innovate development of China steel industry

After the supply-side reform, China steel industry shall take innovation as the main driving force to develop the steel industry. While appropriately expanding market demand, China steel industry is focusing on the following strategies to lead the innovation in the steel industry. Green development: This is an important prerequisite for the survival of the steel industry in China and the World and a guarantee for achieving the sustainable target. The steel industry is implementing the ‘green mine, green procurement, green logistics, green manufacturing, green products and green industry’ concept, and establishing effective and sustainable green factories and green industrial system. Intelligent development: China steel industry is actively engaged in applying automation, big data and AI in developing smart ironmaking and steelmaking factories. Some leading manufacturers in China have built key equipment intelligent detection systems and are carrying out remote operation and maintenance services such as fault prediction. Steel factories will have more robots in steel production lines with harsh environments, high risks and high operational consistency. Consolidated development: China steel industry is re-organizing itself with an aim to establish a consolidated mechanism to reduce disorderly competition. Brand and Quality: China steel industry will pay more attention to brand building and the quality improvement is a guarantee for achieving sustainable development of steel manufacturers. Standardization: China steel industry is promoting the standardization for the sector in the fields of steel logistics, green transformation, integration, power demand management, etc. Differentiation: This is the only way to adjust, transform and upgrade the steel industry, and it is also the inevitable choice for steel companies to survive and develop. This includes strategic differentiation, product differentiation, production line differentiation and service differentiation. Service: Steel companies shift from simple value-added manufacturing to service manufacturing. More importantly, through the combination of manufacturing and service, optimized business models for steel companies can be available in the near future. Diversification: China steel industry shall focus on the development of products with superior products, advanced technologies and market competitiveness. In conjunction with the reform of state-owned enterprises in China, steel companies have been encouraged to explore various forms of asset/share release to incentivize the steel industry. Internationalization: China Steel industry is accelerating its internationalization through the Belt and Road Initiative.

Disclosure statement

No potential conflict of interest was reported by the authors.