Abstract

This paper offers a comparative analysis of various aspects of transition of the iron and steel industry in countries of Central-East Europe as well as in Russia and Ukraine during a quarter of century after the collapse of Soviet Union. Different socio-economic patterns of transition resulted in significant divergence in the outcomes achieved so far in the countries covered in this study. Restructuring of iron and steel industry, successful modernisation of machinery manufacturing sector and robust domestic demand for steel in the countries of Central-East Europe delivered more sustainable and technologically flexible socio-economic model where value-added finishing dominates over energy-intensive and polluting manufacturing of semi-product, whereas Russia and Ukraine are more specialised in semi-product and reliant on the global demand for steel. After 2014 in Russia and Ukraine, transition of iron and steel industry is driven by different vectors: Russia tends to recombine self-sufficient market within the Euro-Asian Economic Union, and Ukraine explores opportunities of Deep and Comprehensive Free Trade Area with the EU. Understanding of experience gained is important to better withstand new challenges related to modernisation of installed capacities, deployment of new technologies, and optimisation of resource and energy usage in the context of transition towards a low-carbon and sustainable economy.

Introduction

Twenty five years ago, Soviet Union ceased to exist and new independent states started challenging journey towards market economy and liberal society, as – few years earlier – did former Soviet satellites in Central-East Europe. Different driving vectors and socio-economic patterns have led to substantial divergence in further transition and the results achieved so far. The comprehensive study of metals’ sector transition in the region concerned performed by Hanzl and Havlik (2004) does not cover Ukraine and mostly deals with first decade of transition, whereas more holistic comparative analysis of sector's evolution in East European countries through the entire post-Soviet period of history, is largely missing in the literature. This paper aims to analyse the experience of transition and the results gained during a quarter of century in the countries concerned. Such analysis is important to better withstand new challenges and to explore opportunities of sustainable development.

Methodology

Scope of study and sources

In this paper, we cover the countries producing at least part of steel via primary route: for the Central-East European Countries (CEEC), former members of Council of Mutual Economic Assistance (CMEA) are included — Bulgaria, Czechia, Hungary, Poland, Romania and Slovakia; for the former Soviet Union (fSU) — Russia and Ukraine. Major statistic source used is World Steel Association's (WSA 2016) archive. To simplify reading of the graphs, legends for each figure are sorted towards the values of last year's indicator.

Post-Soviet issues and iron and steel industry

In this study, the transition of iron and steel industry is analysed through a prism of inherited ‘post-Soviet’ features:

This sector was a driver of economic development and industrialisation, contributing to communist policy of ‘overtaking the west’ and providing basis for self-sufficiency of CMEA block, with defence industry and huge infrastructural projects playing a prominent role in steel consumption (Troschke and Wittmann 2014). This industry was instrumental for integrating East European satellites to the USSR's orbit under aegis of the CMEA through exchange of cheap raw materials and semi-products from fSU versus finished products from CEEC.

1

Many steelworks were ‘city-forming’ being responsible not only for production, but also for providing services to the population. Planned economy established industrial facilities in ‘rational locations’ based on military, political, bureaucratic and economic criteria aiming to maximise regional specialisation — in contrast to ‘chaotic’ patterns of the capitalist economies (World Bank 2010). International trade of the counties concerned was chiefly the trade between the USSR and CMEA. Therefore, Ukraine's rail system is oriented predominantly east–west, reflecting the desire of Soviet planners to tightly integrate the economies of its western neighbours. The N–S orientation was weaker, owing to less emphasised trade via the Black Sea (Levine and Bond 1998). Under planned economy, manufacture in iron and steel sector was largely tailored for a particular industrial ‘co-operator’ (often thousands miles away in another country). Inflexible production model has not incentivised modernisation and made the process of separation and transition to market economy harder.

Results and Discussion

Crude steel production statistics

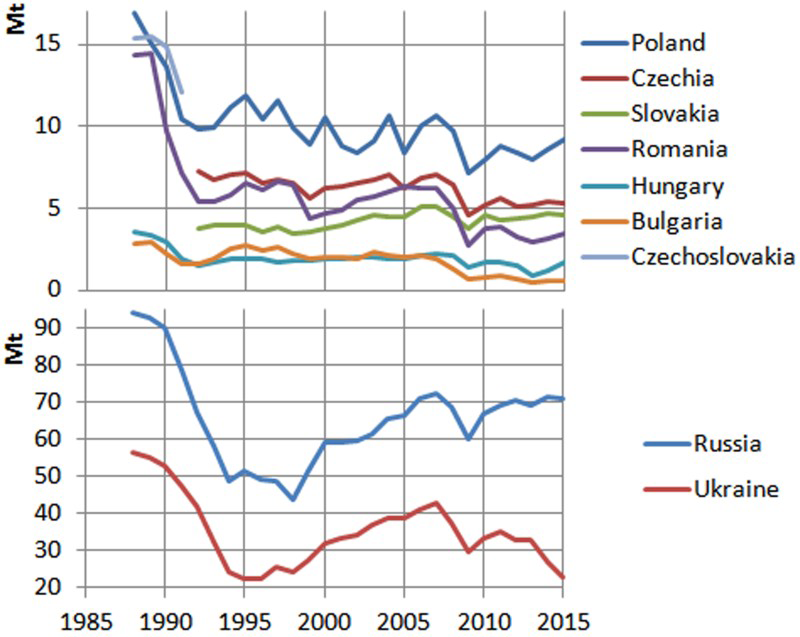

After the collapse of communism in 1990, former cooperative links broke. Further decline of infrastructural projects and defence industry drastically reduced domestic consumption, leaving the sector with huge overcapacity. Evolution of steel production in CEEC and fSU from 1988 when production was already stagnant but still large to 2015 is shown in Fig. 1. For fSU, most dramatic drop is observed during 1990–1994. CEEC hit the bottom faster, with recovery started 2–3 years earlier.

Evolution of crude steel production from 1988 to 2015. Source – Author's elaboration on WSA 2016

Steel production after 1995 depicts different transition in CEEC and fSU. In fSU, steel companies opportunistically tried to remain large, closing only most obsolete facilities. In 2007, before crisis, steel production in Ukraine was up almost twofold and in Russia – by 40%, compared to 1995; however, in most of CEEC production levels of 1995 have never been exceeded (WSA 2016). In Czechia, Poland and Romania, production fluctuates with the trend to reduction. In Hungary, production remains nearly stable since 1991. Only in Slovakia, growth is observed with slight drops in 2008 and 2011. In Bulgaria, production was nearly stable up to 2007, then — after shutting down Kremikovtzy — country ceases to produce pig iron and steel output drops.

The difference in the production yield rates has explanation in the processes of socio-economic transition and related industrial policies driven by different vectors in CEEC and fSU.

Transition

Russia and Ukraine – transition to current state

In 1990s, problems of steel sector in Russia and Ukraine lay in the delayed restructuring and privatisation of former big state-owned enterprises with thousands of employees (Durand 2003). Governments led by the former communist leaders were reluctant to apply ‘shock therapy’: farms, kindergartens, residential areas, resorts, hospitals, etc., were part of enterprises, and radical restructuring would trigger social problems. Privatisation, by the voucher method, provided no resources for investment. Selling the ‘all peoples ‘heritage’ to foreign capitalists was confronted, though, anyway, uncertainties and opaque privatisation rules discouraged international investors. Former economic instruments disappeared, and steel trade was captured by ‘middlemen’, some of whom accumulated considerable amounts and became big shareholders (Durand 2003).

Gradually, ownership was consolidated in handful individuals who — in the context of uncertainty of ownership and legislative vacuum — were focused on short-term goals and not on strategic investment. Instead, a massive capital flight to offshore countries — 10 times higher than total investments in Russia in 1996 — took place (Durand 2003). Domestically up to 80% of steel was bartered, which also impeded accumulation of capital (Hanzl and Havlik 2004).

Ownership was generally settled within first decade of independence (though, change of ownership is continuing), but predatory practices for capturing of property and profit have led to impoverishment of the sector's industrial potential — the contrary of what was expected at the onset of transition (Durand 2003).

No science-based strategy for restructuring and development of steel industry existed during that period and lacks even today. Several strategic documents delivered (e.g. – Strategy (2009) in Russia) are rather declarative and offer no instruments for reaching the targets. In Ukraine, ‘sectorial experiment’ conducted from August 1999 to January 2003 provided steel producers with state assistance, allowing companies to accumulate finances for improving technologies and environmental safety under special taxation regime (Talkin 2016). Own development strategies of steel companies are rather focused on corporate targets, not necessarily coherent with national socio-economic goals, hence holistic vision for the industry's future is lacking.

Developed to use own natural resources, infrastructure of steel industries in fSU is very different from those in CEEC: production of raw materials (ore beneficiation, cokemaking, ferroalloy) outweighs the finishing mills. Therefore in fSU, large vertically integrated holdings dominate, covering production chain from mining to manufacturing of finished product (e.g. Metinvest in Ukraine, Evraz, Severstal, Mechel in Russia). Being less vulnerable to volatile raw materials’ prices, these companies better survived crises. More profitable, they capture gradually larger share in the sector.

No international company entered Russia's steel industry. In Ukraine, thanks to the pressure of public society on governments, exceptions were possible: the largest steelworks Kryvorizhstal (ca. 8 Mt per annum), renationalised in the aftermath of Orange Revolution, was sold in 2005 at an open auction, being the first transparent privatisation procedure in this sector, bringing ArcelorMittal as the first international owner. Russian capital also penetrated to Ukraine: DMZ Petrovskogo (ca. 1 Mt per annum) is owned by EVRAZ; Alchevsk Iron & Steel Works and Dniprovsky Iron & Steel (ca. 4.5 and 3.5 Mt per annum, respectively) are owned by ISD, which originates from Ukraine but has Russian major shareholder.

Steel companies in fSU were able to take advantage of globally growing demand for steel. Spectacular production growth after 1998 enabled – despite continuing capital flight – accumulation of the amounts needed for modernisation (details in the section ‘Modernisation’). 2 However, financial crisis dropped production by 17% in Russia and 30% in Ukraine in 2009 compared to 2007. Although production was regained nearly to a pre-crisis level in Russia and to 80% of that level in Ukraine, profit margins narrowed (Vlasyuk 2011) and enterprises are trying to finish continuing projects, rarely initiating new ones.

Russia and Ukraine – current trends

Before 2008 Russian steel holdings, seeking for access to high-tech markets and know-how, actively purchased foreign assets, often with the help of significant loans. Now expansion becomes less prominent. In 2012, Mechel initiated selling its foreign assets to cover the debts exceeded in 2013 US$9bn (INFOMINE 2014). Same does Evraz whose net debt exceeds US$6bn (Evraz 2015).

In 2013, opportunities for international trade shrank owing to the situation on the global market, while domestic demand for steel in Russia stagnated in the aftermath of falling oil prices. After aggression to Ukraine in 2014, sanctions imposed by the USA, the EU, Japan, Canada, and Australia – notably in financial sphere – are limiting possibilities for steel companies to refinance the debts and to credit new projects (INFOMINE 2014). Capacity utilisation during December 2014–January 2015 dropped to a record low level of 72.5% (Revinskaya 2015). Russian government revised the development strategy for metallurgical branch of 2009 which indicators have not been achieved, and in May 2014 approved new development strategy for 2014–2020 and towards 2030 (Strategy 2014).

To cope with problems, Russia, in particular, relies on Euro-Asian Economic Union (EAEU), bringing back together Armenia, Belarus, Kazakhstan and Kyrgyzstan. A recent report by the Eurasian Economic Commission (EEC 2014) on the current state of iron and steel sector largely reproduces Soviet-style rhetoric, prioritising ‘development of industrial cooperation’. Transnational ‘rationalisation’ mechanisms are sought after to reduce overcapacity and to cut the share of steel import from ‘third’ countries (now — 40%) to the EAEU. Governmental support becomes prominent: all major steel companies are included to the list of ‘systemic organisations entitled for the state aid’. Thus, the EAEU aims to recombine fSU practices for creating a self-sufficient market, less vulnerable to global crises.

In 2014, despite Russia's political and economic pressure, Ukraine escaped involvement to the EAEU, making this project less ambitious. Further participation in the EU-Ukraine Deep and Comprehensive Free Trade Area (DCFTA), provisionally applied from 1 January 2016 ahead of ratification of the Association Agreement, might be challenging for iron and steel industry in terms of compliance with the EU regulations and norms, although, judging from the CEEC experience, may bring opportunity for modernisation. Under DCFTA, about 95% of tariff lines would be set at zero, and for the rest, tariffs would be reduced. This will be particularly important for Ukraine's iron and steel sector and likely to increase its exports to the EU (DCFTA 2016).

Political crisis followed in 2014 by war in Ukraine brought 20% of production capacity in industrialised Eastern territories out of governmental control. Three out of nine integrated steelworks and five out of 12 cokemakers are located there. Some enterprises were stopped, and production in 2015 was down by nearly 30% compared to 2013. All iron ore mining and processing industry is on the territory controlled by government, but many coal mines, notably producing coking grades, and nearly a half of total coke production capacity are on the occupied territory. The domestic coking coal supply in 2015 was down by 61% year on year (Metallurgprom 2016, 1), and the share of imported (mostly from the USA) coal in coking mix during January–May 2016 was as high as 67% (Metallurgprom 2016, 2).

With obsolete facilities, lack of profit and continuing military conflict, future of Ukraine as a player on global steel market is uncertain. Its huge potential for reducing the energy consumption and, respectively, to cut the CO2 emissions might be attractive under carbon trade schemes and might help modernise the industry, although other factors shall be put in place to attract investors.

CEEC

In the CEEC, restructuring of steel industry was driven by pressure related to accession to the EU. This concerned capacity reductions, questioning the viability of companies, and solving of social, technological and environmental problems in order to comply with the EU rules of state aid and the EU legislation regarding the environmental issues, occupational health and safety requirements (Hanzl and Havlik 2004; Trappmann 2015).

In the late 1980s, the EU steel industry has just recovered from crisis, and control of European Coal and Steel Community (ECSC) over production, prices and capacities was lifted in 1988 (Tomlinson 2014). High production levels and lower prices in CEEC would put the EU15 steel industry again under risk. Therefore, the accession was made conditional on privatisation and downsizing of steel industry. In 1993, the EU set additional protocols to the Europe Agreement with Poland and Czechia, obliging them to comply with the European Steel Aid Code: reduction of the production capacities was made conditional for any state aid (Trappmann 2015). In Romania, privatisation was also conditioned on restructuring: capacity of largest steelwork Galati was cut from 10 260 to 6000 kt per annum during 1993–2003, whereas total country's steelmaking capacity shrank from 17 505 to 9400 kt per annum during the same period (OECD 2015). Restructuring strategy for Romania was validated by the European Commission in the context of the Accession Treaty and successfully performed (COM 2010).

In contrast to fSU, the CEEC governments in their privatisation policies placed emphasis on financially sound foreign partners, capable of providing funding and introducing new technologies (Deutsche Bank Research 2004). Participation of large EU groups in the privatisation of CEEC steel industries has failed, but ArcelorMittal acquired companies in Romania — Galati and Hunedoara in 2001 and 2003, respectively, in Poland — Katowice Steelworks in 2005 and in Czechia — Ostrava in 2007. In Slovakia, the largest steelworks in Kosice were acquired by US Steel as early as in 2000.

Companies from fSU also acquired some CEEC steelworks, thus creating a window to the EU market: Ukrainian ISD owns Polish Huta Częstochowa since 2003, and Hungarian DUNAFERR since 2004. Russian Mechel and Severstal owned the assets in Romania and Czechia, but, as mentioned above, recently largely withdrew steel businesses from CEEC.

Despite the controversial role of the EU in guiding the restructuring of steel sector in CEEC, finally it has led to the modernisation of steel mills (details in the section ‘Modernisation’), which would otherwise not compete on the European and global market (Trappmann 2015).

Export versus domestic consumption

Steel

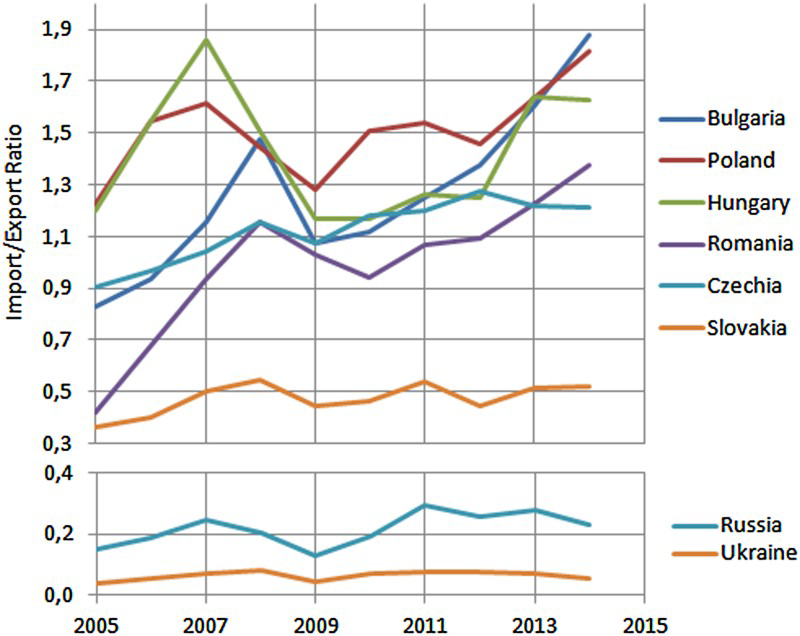

Patterns of international trade in fSU and CEEC after separation are rather different. Trying to keep the industry large, Russia and Ukraine exploited opportunities of international trade, becoming world-leading steel exporters with export far exceeding import (Fig. 2). Instead, all CEEC (Slovakia is the only exception, but anyway it exports more steel products than produces crude steel) became net steel importers which demonstrates transition to economically viable, technologically flexible and more environmentally clean model where value-added finishing dominates over energy-intensive and polluting manufacturing of semi-product, and domestic steel consumption is robust.

Import/export ratio (Source – Author's elaboration on WSA 2016)

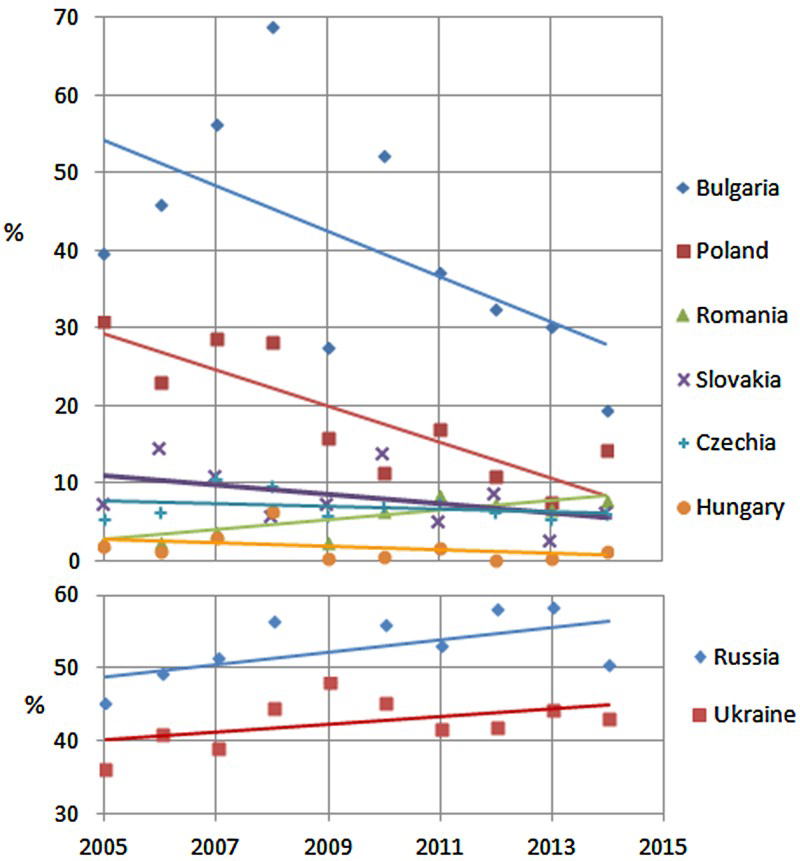

Structure of export is rather different for the two groups (Fig. 3). Share of ingots and semi-product in Russian export is above 50% and in Ukrainian – ca. 45%, whereas for Czechia, Hungary, Romania and Slovakia it is just 1.4–8.0%. Moreover, for fSU the share of semi-product in export tends to increase, while for the CEEC, it either shrinks (for Bulgaria, Poland and Slovakia) or remains nearly stable at very low level (for Czechia and Hungary). It slightly grew only for Romania but remains low (below 10%) also for this country. In fSU export is exclusively based on local production of crude steel and covers mostly semi-products, whereas export from CEEC is largely based on processing of the imported semi-products and selling value-added items.

Share of ingots and semi-products in export (Source – Author's elaboration on WSA 2016)

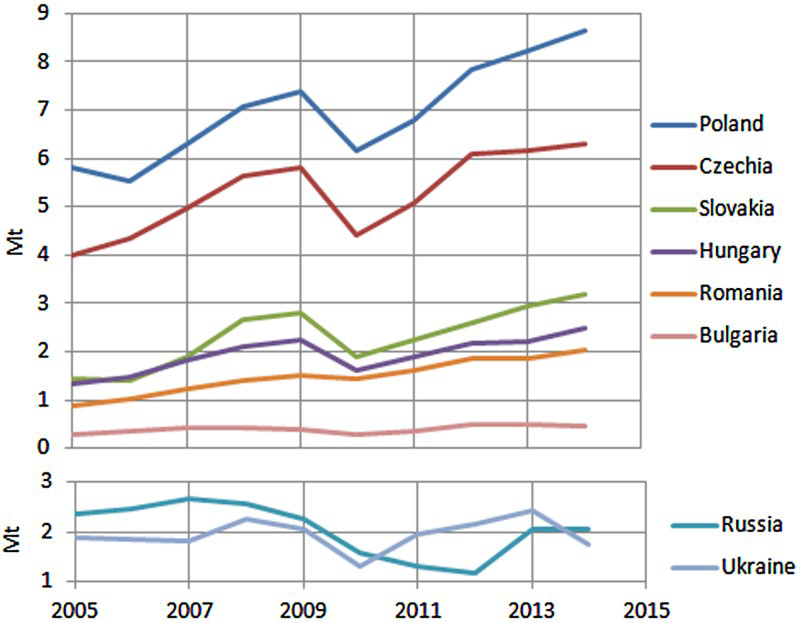

Besides different approaches for restructuring steel industry, another important feature has been noted by Hanzl and Havlik (2004) — in CEEC transition in machinery manufacturing was more successful than in steel industry, whereas in fSU transition in machinery manufacturing was worse. In Ukraine, share of iron and steel sector in industrial gross value added rose from 11% in 1990 to 27.4% in 2000, whereas share of machinery manufacturing sector shrank from 30.5 to 13.4% during the same period (Efimenko et al. 2010). In CEEC, profound change in machinery manufacturing was fostered by foreign direct investments. As shown in Fig. 4, indirect steel export (i.e. export of steel-containing goods) even in absolute figures for the most of CEEC exceeds that for fSU (only for Bulgaria, it is rather small). Poland even became 8th world's biggest indirect steel exporter in 2015. With respect to size of the economies concerned, success of CEEC is obvious. Increasing specific weight in the economy of steel-intensive industries (automotive, home appliances’, electronics, etc.), these countries created more sustainable economic structure: machinery manufacturing is more flexible than steelmaking and better adjusts to crises and to consumer's needs.

Indirect export (Source – Author's elaboration on WSA 2016)

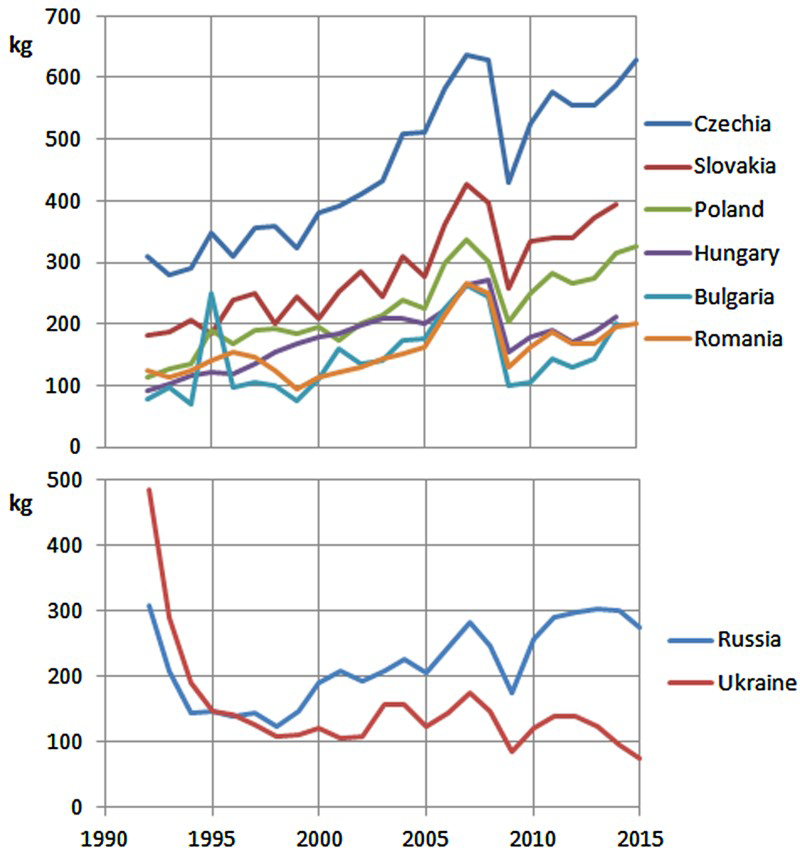

In all CEEC, apparent steel use per capita grows almost steadily, exceeding in 2007 level of 1993 within the range of 210–340%, whereas in Russia it shrank by 10% and in Ukraine – by 60% (Fig. 5). Stagnation of steel consumption in Russia and its continuing decline in Ukraine increase the vulnerability of sector to situation on the global market.

Apparent steel consumption per capita (Source – Author's elaboration on WSA 2016)

In Ukraine, accumulated demand for replacing depreciated steel-made facilities is estimated at 330 Mt (Amosha, Bolshakov and Minayev 2013) – the value close to ten years’ steel output with full utilisation of current capacity. If the conflict in the Eastern Ukraine, where the industrial and civil infrastructures are severely damaged, will be resolved, this figure will increase. Russia's delayed steel demand is estimated at 170 Mt (Ivanova 2013).

Iron ore

CEEC have no significant resources of iron ore — Ukraine was and remains among the major suppliers. Russia and Ukraine have abundant reserves of iron ore: probable reserve exceeds 40 Gt in Russia and 9 Gt in Ukraine; however, share of rich ore (54–62% Fe) is relatively small – 15 and 10%, respectively (Popov 2000; Kolosov 2011). Relatively high content of silica in Ukrainian concentrate (7–8%) makes competition on international markets harder.

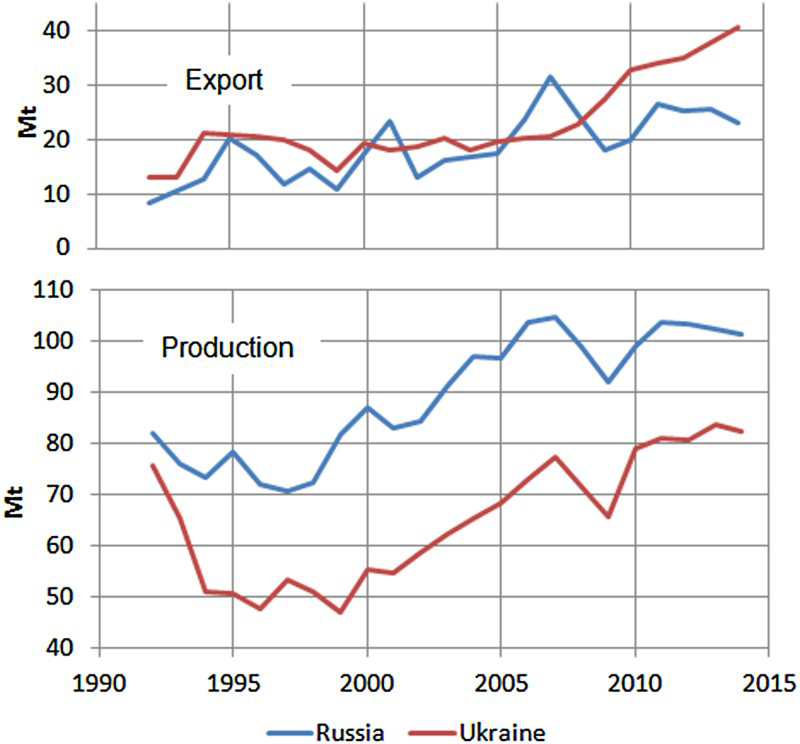

After the collapse of the USSR, production of iron ore (Fig. 6) dropped in both countries, then stabilised and gradually grew, currently exceeding the level of 1992 – in contrast to steel production (Fig. 1) which has never regained pre-independence volume. In Ukraine (the world's 4th biggest iron ore exporter), export grew by 213% and in Russia by 180% in 2014 compared to 1992 with main consumers in the EU (mostly CEEC), China and Japan.

Production and export of iron ore (Source – Author's elaboration on WSA 2016)

Modernisation

Energy efficiency and environmental requirements are major drivers for modernisation in the iron and steel industry. Cheap energy and poor environmental regulations weaken the pressure on restructuring (Hanzl and Havlik 2004). Patterns related to these two factors are rather different for the countries concerned in this study.

In CEEC, especially in the earlier period of transition, emphasis was put to eliminate obsolete facilities and technologies in the process of reducing production capacity. The EU environmental requirements are getting increasingly important. Application of cap-and-trade EU Emission Trade System provides incentive for technological change, although further enforcement of environmental pressure, concerning reduction of CO2 emissions, is widely seen as an impediment to competitiveness on global market (Skuza, Prusak and Kolmasiak 2013). Polish steel association recently submitted to European Commission a list of demands that would protect the international competitiveness of the steel sector as the new ETS Directive would be made effective (Polish Steel Industry 2016).

Relatively poor environmental regulation is a particular feature in fSU. End-of-pipe regulatory approach persists till now with numerous nearly unchanged over decades pollution limits and insufficient tariffs of fines (Troschke and Wittmann 2014): since January 2015, in Ukraine a tax on CO2 emissions of just 0.33 UAH (ca. US$0.013) per tonne (Taxation code of Ukraine 2015) has been set which does not incentivise modernisation. Hence, environmental aspect for modernisation is weaker in fSU, although in Ukraine, during above-mentioned sectorial experiment, investment to environmental protection was conditional for taxation benefits.

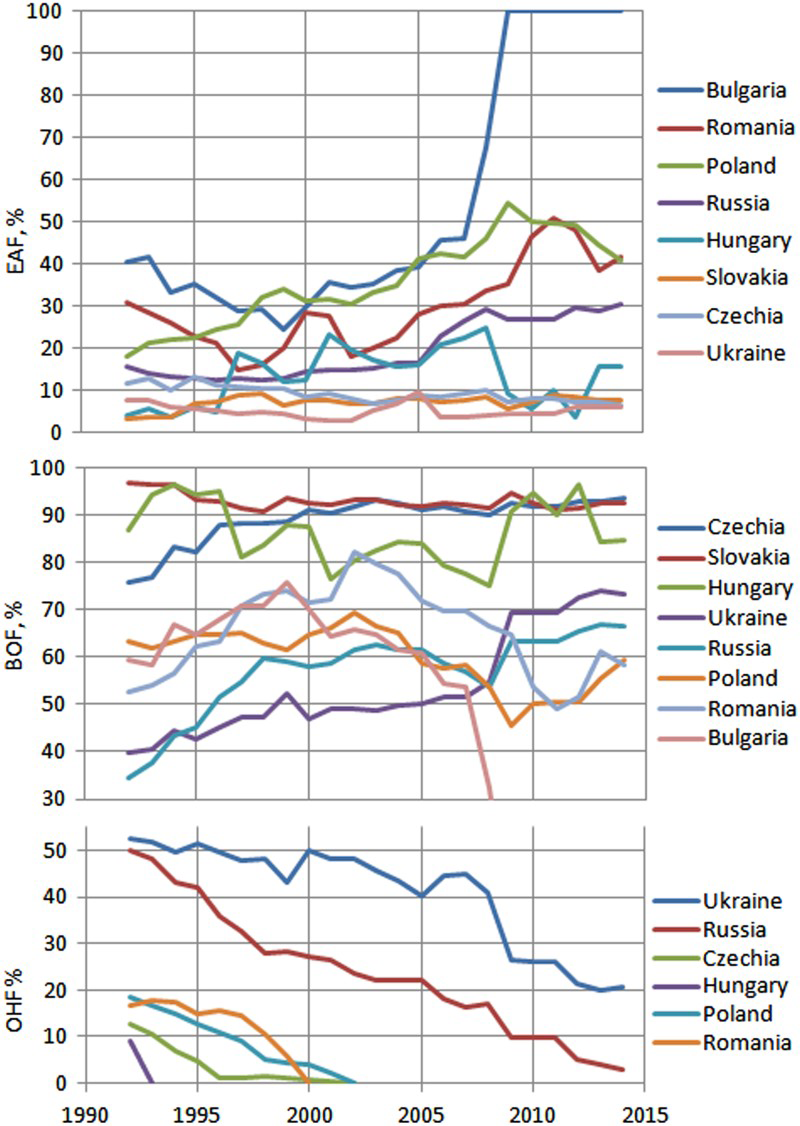

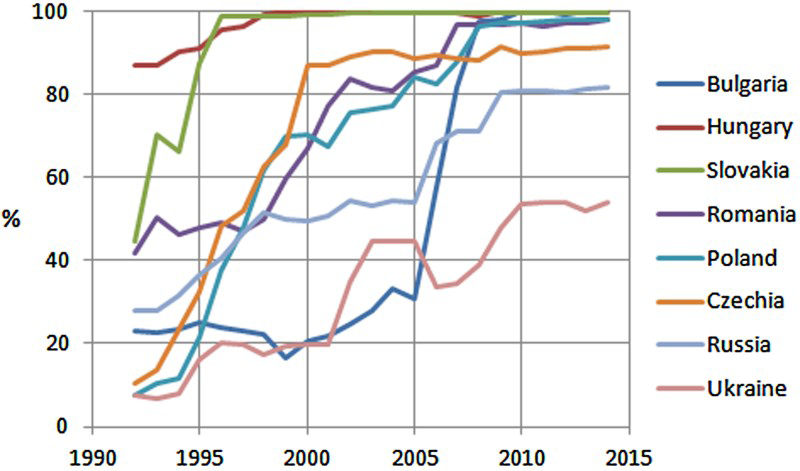

Russia has abundant and cheap energy: the domestic price of natural gas during 2008–2012 was from US$84 to US$115 per 1000 m3, whereas in the EU it was from US$348 to US$560 per 1000 m3. Although cheap energy does not promote modernisation, it generates profit for investment: during 2005–2012, Russia's steelmakers invested nearly US$8bn per year average (ca. US$80–90 per tonne of crude steel). In Russia, share of steel production in open-hearth furnaces (OHF) reduced from 22% to nearly zero (Fig. 7), air pollution cut by 12% and energy consumption approaches the best available technology level (Ivanova 2013). Share of continuous casting increased from 54% in 2005 to 82% in 2014 (Fig. 8). Nevertheless, the pace of modernisation is at least twice lower than it was during the planned economy (Novikov and Novikova 2011).

Production of steel by method (Source – Author's elaboration on WSA 2016) Share of the continuous casting in crude steel production (Source – Author's elaboration on WSA 2016)

Ukraine, in the same period, invested much less to modernisation: maximum investments peaked in 2007 at the level of US$47 per tonne of crude steel with the average level of about US$25 per tonne of crude steel (Shatokha 2016). Obviously, this level of investment was far from sufficient, hence the energy intensity of Ukraine's iron and steel industry remains among the world's largest: the potential to reduce energy consumption via the BAT deployment for Ukraine exceeds 7 GJ per tonne of steel, whereas for Russia it is just 4 GJ (IEA 2014). Even though some success in eliminating obsolete technologies has been reached, shares of OHF (20.5% in 2014) and ingot casting (45.9% in 2014) remain too high. In 2015, specific investments comprised just 372 UAH (ca. US$15) (Metallurgprom 2016, 1).

CEEC completely eliminated OHFs as a part of capacity reduction processes (Fig. 7). They increased the share of continuous casting much faster and to higher levels, compared to Russia and Ukraine (Fig. 8). Bulgaria, where restructuring period was extended owing to insolvency of Kremikovtzi (Trappmann 2015), is the only exception.

Steel production infrastructure in terms of EAF (electric arc furnace) to BOF (basic oxygen furnace) ratio in Ukraine, Czechia, Slovakia and Hungary after 2000 remains stable with low share of EAF, whereas in Russia, Poland and Romania nearly twofold growth of the EAFs share is observed. Bulgaria is a special case with steel produced only via the EAF since 2009.

Conclusions

Different socio-economic patterns driving the transition of iron and steel industries in CEEC and fSU resulted in significant divergence in the pathways and the results achieved so far. In CEEC, downsizing and modernisation towards compliance with the EU standards in energy efficiency, environmental, health and labour safety have been conditional for accession, whereas fSU iron and steel industries through most of the period of transition opportunistically tried to stay as large as possible, focusing rather on short-term goals irrespectively of national strategic priorities. Initial period of privatisation and economic liberty in fSU resulted in impoverishment of the iron and steel industry followed by delayed modernisation and unsolved social problems. From 1998 to 2007, Russia and Ukraine exploited advantages of renaissance caused by the growing global demand for steel. Iron and steel companies, largely consolidated to vertically integrated holdings, developed own corporate strategies resulting in substantial modernisation, more successfully performed in Russia. In CEEC, restructuring processes resulted in the formation of more compact but rather competitive iron and steel sector. Inherited from the past, specialisation of CEEC in finished items and of fSU in semi-product became even deeper: the share of value-added product grows in CEEC and declines in fSU. Restructuring of iron and steel industry, successful modernisation of machinery manufacturing industry and robust domestic steel demand in CEEC resulted in the delivery of more sustainable and technologically flexible socio-economic model where value-added finishing dominates over energy-intensive and polluting manufacturing of semi-product. Political crisis of 2014 and Russia's aggression in Ukraine have led to the divergence of driving vectors for further transition: Russia tries to develop self-sufficient market, recombining Soviet-style economic relationships within the EAEU, whereas Ukraine explores challenges and opportunities of participating in the DCFTA.

Footnotes

Acknowledgements

1

Latest large collaborative project was construction of iron ore beneficiation plant by Soviet Union, East Germany, Czechoslovakia, Romania and Hungary near Kryvyi Rih (Ukraine) to produce iron ore concentrate from oxidised quartzites for the countries involved. Romania alone invested nearly US$526m out of US$1.6bn totally spent. Started in 1984, the construction has never been finished.