Abstract

Illegal logging has become a global issue because of its adverse effects on biodiversity and climate change. In order to reduce illegal logging, many countries around the world have introduced regulations for the international trade of forest products. This paper examines the effects of these efforts on international trade of forest products. The analysis is conducted using the Heckscher–Ohlin–Vanek model, where the number of regulations against illegal logging is used to describe the level of efforts, and is included as an explanatory variable for national net export of forest products. The results show that efforts against illegal logging have had significant and positive impacts on the net export of forest products.

Introduction

Illegal logging can take place in various forms, including using corrupt means to gain access to forests, extraction without permission or from a protected area, harvesting of protected tree species, or the extraction of timber in excess of agreed limits (REM 2009; Bisschop 2012). Illegal harvesting has existed for a long time. It has, in some cases significantly influenced forest ecosystems and the forest carbon storage. Illegal logging is perceived to pose significant obstacles to the achievement of sustainable management of forests. It leads to the destruction of forest resources, loss of biodiversity and other forest ecosystem services, and undermines economic growth and equitable development (Kinnaird et al. 2003; Bala et al. 2007; Kishor and Lescuyer 2012). In addition, and equally importantly, illegal logging gives rise to or supports other undesirable outcomes, such as corruption network, generating significant volumes of ‘black’ money and crime (Smith et al. 2003; Tacconi 2007; Tanczos 2011). Moreover, illegal harvesting can drastically reduce national financial revenues and produce inefficiency in logging operations, loss of productivity and unemployment (Gutierrez-Velez and MacDicken 2008).

Although illegal logging mainly occurs in some developing countries, it has become a global issue because of the increasing worldwide concerns about biodiversity and climate change (Visseren-Hamakers and Glasbergen 2007). Many countries around the world have made serious efforts in an attempt to reduce illegal logging, and the effects of such efforts have been examined by many researchers. Prestemon (2015) found that the 2008 Lacey Act Amendment led to significant decrease in the import of tropical lumber and hardwood plywood from suspected illegal timber source countries. Bosello et al. (2013) used an Intertemporal Computable Equilibrium System model to estimate the effects of an EU legislation proposal aimed to ban illegal timber from the EU market. Their results show that an EU ban targeting only log imports is not effective in reducing illegal logging – for, while the legislation can eliminate illegal logs from international markets, it will increase production of processed wood products in illegal logging countries as their exports become relatively more competitive. Atyi et al. (2013) concluded that the Forest Law Enforcement, Governance and Trade Voluntary Partnership Agreement (FLEGT/VPA) between Cameroon with the European Union will have positive impacts for industrial forest concessions who export harvested timber products to international markets. However, the implementation of FLEGT/VPA brings substantial financial costs for forest managers and the national government, and may have adverse impacts on the livelihoods of small-scale loggers. Moiseyev et al. (2010) estimated the impact of four different policy options to curb EU imports of illegally harvested wood. They found that the FLEGT/VPA can lead to significant reduction in timber harvest and production of wood industry in the VPA countries, whereas the harvest and production in non-VPA countries will increase. Lawson and MacFaul (2010) assessed the impacts of the actions against illegal logging and related trade, taking in 12 producer, processing and consumer countries in the 2000s. They estimated that illegal logging had fallen by 50–75% during one decade, and imports of illegally sourced wood to the consumer and processing countries studied decreased by 30% from their peak in 2004. According to Li et al. (2008), the overall impact of eliminating illegal logging on the world forest sector is small. Without illegal logging, the production of industrial roundwood would decrease in developing countries, but the reduced illegal timber will to a large extent be substituted by legal wood.

The aim of this paper is to examine the impact of international efforts to reduce illegal logging on global trade of forest products. The remainder of the paper is organised as follows. Second section provides an overview of governance policies. Third section provides an introduction of wood products in trade. The next section presents the method and data used in this study. Fifth section presents the model estimation result and discussion. Sixth section provides summaries and conclusions.

Governance policy

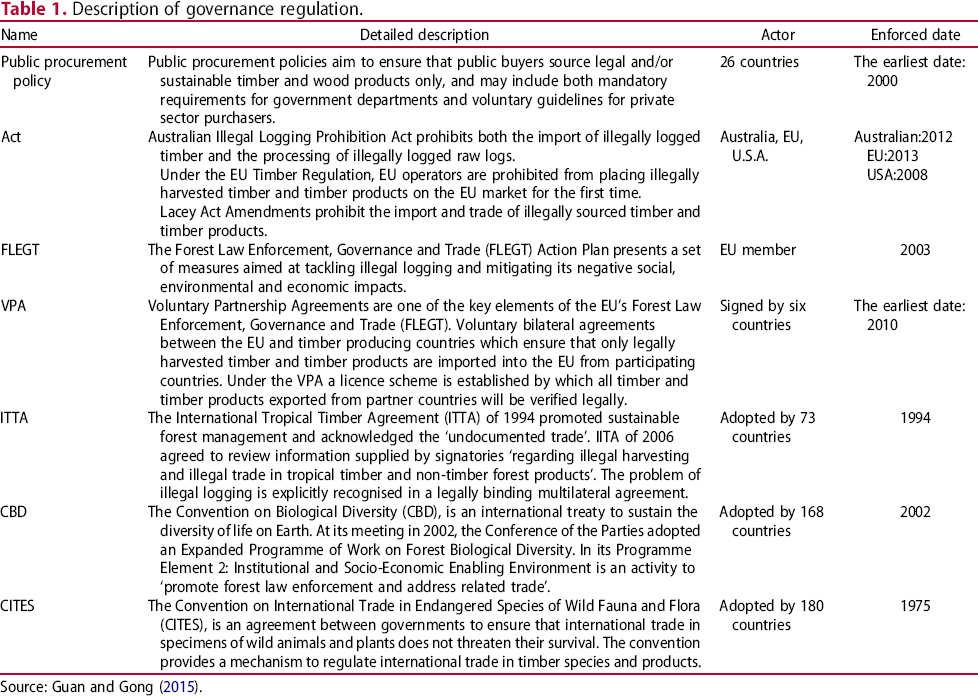

Description of governance regulation.

Source: Guan and Gong (2015).

Many from the private-sectors have also taken similar steps to exclude illegal or unsustainable timber from their own supply chains. Many supply-chain controls, both public and private, make use of the main voluntary certification systems, those of the Forest Stewardship Council (FSC) and Programme for the Endorsement of Forest Certification (PEFC), as relatively straightforward ways of identifying sustainable or legal products (Brack and Bailey 2013). Both FSC and PEFC are complex schemes with a wide range of criteria, demonstrating that products have been produced in accordance with the principles of sustainable forest management (which include compliance with national laws), and are traceable throughout their entire supply chain (Guan and Gong 2015). As noted, the application of these in developing countries are particularly difficult, and as a result a number of simpler legality verification schemes have been developed to help in meeting demand for legal (though not sustainable) products from both public and private sectors (Brack 2014; Overdevest and Zeitlin 2014).

Wood forest products trade

Status of the net export in wood in different continents in 2016.

Source: International Trade Centre Trade Statistics.

Top 5 import and export countries of wood products in Asia in 2016.

Source: International Trade Centre Trade Statistics.

Top 5 import and export countries of wood products in Europe in 2016.

Source: International Trade Centre Trade Statistics.

Top 5 import and export countries of wood products in Africa in 2016.

Source: International Trade Centre Trade Statistics.

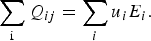

Top 5 import and export countries of wood products in America in 2016.

Source: International Trade Centre Trade Statistics.

Top 5 import and export countries of wood products in Oceania in 2016.

Source: International Trade Centre Trade Statistics.

Table 3 shows that China and India are the main importing countries of roundwood, China and Japan are the main importing countries of sawnwood, and China is the main exporting country of fibreboard, plywood and veneer sheet. A number of illegal logging countries in Southeast Asia such as Thailand and Indonesia are not the main exporting countries of roundwood, in contrast, these countries export wood-processing products. For example, Indonesia exports fibreboard, plywood and veneer sheet. This indicates that wood production countries have developed their own wood industry.

Table 4 provides the exports and imports of wood products in Europe. The Russian Federation exports roundwood, sawnwood and plywood, and its roundwood exports have taken more market share compared with other countries. These countries which rank top 5 in Table 4 are all EU countries except for Ukraine and the Russian Federation, which indicates that some EU countries have developed forest industry and owned relative forest endowment. For example, Germany and France export roundwood, while Sweden, Finland and Austria export sawnwood. Some EU countries also have developed a large domestic forest industry, making it possible to export some processed products.

Table 5 shows that Equatorial Guinea, Republic of Congo and Cameroon are still the main exporting countries of roundwood, however the high risk of illegal logging is high in these countries. Ghana, Gabon and South Africa have developed their forest industry; they have exported some wood products. In spite of a good development in the forest industry in some countries, there is still a gap in wood-processing fields between Africa and Europe.

Table 6 shows that the U.S.A. and Canada are the main importing and exporting countries of roundwood. Also, these two countries export and import processed wood products. The possible reason for this is that there is a relatively large domestic forest industry and a limited range of tree species in these two countries, making it necessary to import certain species and processed wood products in order to facilitate a desired range of production when exporting. Brazil and Suriname are seen as illegal logging countries, but the two countries have reduced roundwood export, developed wood-processing industry, and began to export processing products.

In Table 7, it is obvious that New Zealand is the largest country in the import and export of plywood, fibreboard, sawnwood and roundwood in Oceania, and also is the biggest exporting country of veneer sheet. Austria is the biggest country in the import of veneer sheet. Papua New Guinea and Solomon Islands are regarded as illegal logging countries; the two countries are still the main exporting countries of roundwood, however, a good sign is that these countries are also developing their own forest industry, and have begun to export processed products gradually, though the traded volume is low.

Method and data

Method

In general, the magnitude and direction in trade flows of forest product are determined by geography, size of economies, character of forest endowments and government policies. Classical trade theory prescribes that trade occurs because there are differences among trading partners in their relative costs of production. The link between net trade, prices and resource endowments is provided by the Heckscher–Ohlin model (Heckscher 1919; Ohlin 1933), which has had mixed success in empirical analyses. The Heckscher–Ohlin model predicts that the net exports of a country for a given good are a positive function of its resource endowments and a negative function of its income. There are a number of assumptions underlying the Heckscher–Ohlin model (Prestemon and Buongiorno 1997): (i) there exists factors that are immobile between countries; (ii) markets are competitive, with no barriers to trade; (iii) the same technology is universally available; and (iv) consumption is homothetic with respect to income, which means that consumption is positively correlated to income.

Following Learner (1984), Bonnefoi and Buongiorno (1990), and Prestemon and Buongiorno (1997) all suggest that the primary factor determining net trade is the size of a country's forest endowment relative to the size of its economy. This approach is formalised by the Heckscher–Ohlin–Vanek (HOV) model (Vanek 1963). In country i, assuming a balanced trade (i.e. where factor demand equals factor supply), the output of commodity j (Qij) is a function of forest endowments (Ei),

A country's consumption of commodity j (Cij) can be defined as:

Using Equation (2), we can rewrite Equation (4) as:

Equation (5) is known as the HOV equation. Assuming factor-price equalisation and identical homothetic preferences across countries, a country's consumption share can be written as:

Some scholars have applied the HOV model in studying the trade of forest products. Lundmark (2010) used an extended HOV model to test the comparative advantage between EU member states. His results suggest that forest endowments are an important determinant for explaining differences in net trade of the included forest commodities; yet, domestic demand measured by income level is not. Liu and Tian (2007) tested the applicability of HOV model to analyse the international trade of forest products using the data of 54 countries in 1995, 1998, 2001 and 2004. They concluded that the international trade flows of total forest products, logs, other wood, sawnwood, wood-based panel, wood pulp and recycled paper are in line with the trade theory of comparative advantage. They took the number of environmental agreements signed by a country as environmental variables to test their effects on the trade flow of forest products. Although their result shows that the environmental variables did not have any significant effect, the conclusion does not rule out the impact of a government's environmental policy on forest products trade flow. Uusivuori and Tervo (2002), using 18 OECD countries for the period 1977–98, analysed how forest endowment and economic activity affected the net trade of industrial roundwood and forest products. They found limited support for the Heckscher–Ohlin model and concluded that while historical differences in forest industries and resources still exist, the role of forest resources is becoming less important in shaping the development of forest industries. However, they fail to include the increasingly more important energy sector where forest resources are used as fuel. Bonnefoi and Buongiorno (1990) empirically tested the model and concluded that for all examined commodities (roundwood, sawnwood, panels, pulp and paper) forest endowment has a positive effect on net trade. Furthermore, they found that domestic demand, measured by income, has a negative effect on net trade. Both results are coherent with theoretical predictions.

The impacts of international efforts to reduce illegal logging on wood products in trade are required to be examined in the paper; the most common way is to check trade flow within the traditional comparative advantage theory based on HOV model. In order to do this, we extend the traditional HOV model by introducing an environmental variable related to the efforts of combating illegal logging and study how it affects trade flow. We extend Liu and Tian's (2007) analysis in a number of ways: (1) The selection of wood products follows the FAO definition strictly, and these products are directly affected by illegal logging; (2) the samples are expanded to 89 countries including the main forest trade and abundant forest endowment countries, and their trade amount represents about 95% of world imports and exports; (3) the international efforts to reduce illegal logging have increased since 1998, but the real impact against illegal logging began with the EU FLEGT action in 2003. Therefore the aggregated effect of 2003 to 2015 is analysed; (4) the number of regulations aimed at combating illegal logging is to describe the level of efforts, and is included as an explanatory variable. If one country adopts less governance policy, the country is considered to show less effort against illegal logging. If one country adopts more governance policy, the country is considered to show more efforts against illegal logging. According to the Table 1, the regulations number of countries is on a scale of zero to seven, where number corresponds respectively to levels of combating illegal logging: none, lowest, lower, low, moderate, high, higher and highest; (5) per capita income is also included as an explanatory variable. Per capita income influences the market demand for forest products. It also reflects people's environmental attention due to the strong correlation between per capita income and environmental attention (Dasgupta et al. 2001).

Based on all these, in the model, we examine the impact of efforts against the illegal logging on wood product. The dependent variable is the net export value of roundwood, sawnwood, veneer sheet, plywood and fireboard, whereas the independent variables include country's capital stock, three types of labor force according to education level, forestland area, per capita income, the first-order lag of dependent variable, and the number of regulations adopted to combat illegal logging. The model is expressed as follows:

In the above model, the estimated coefficient β6 indicates whether the measures against illegal logging has had an impact on the growth of the net trade in wood product and the extent to which this impact has arisen. If the value of β6 is greater than 0, it indicates that the measures does promote the growth of the net trade in wood products.

Data

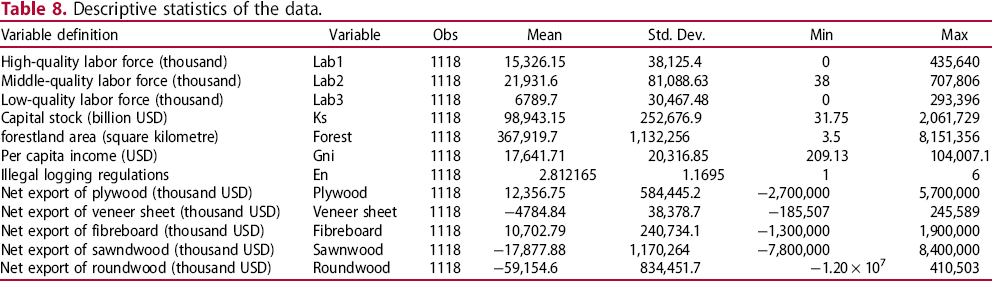

Descriptive statistics of the data.

Results and discussion

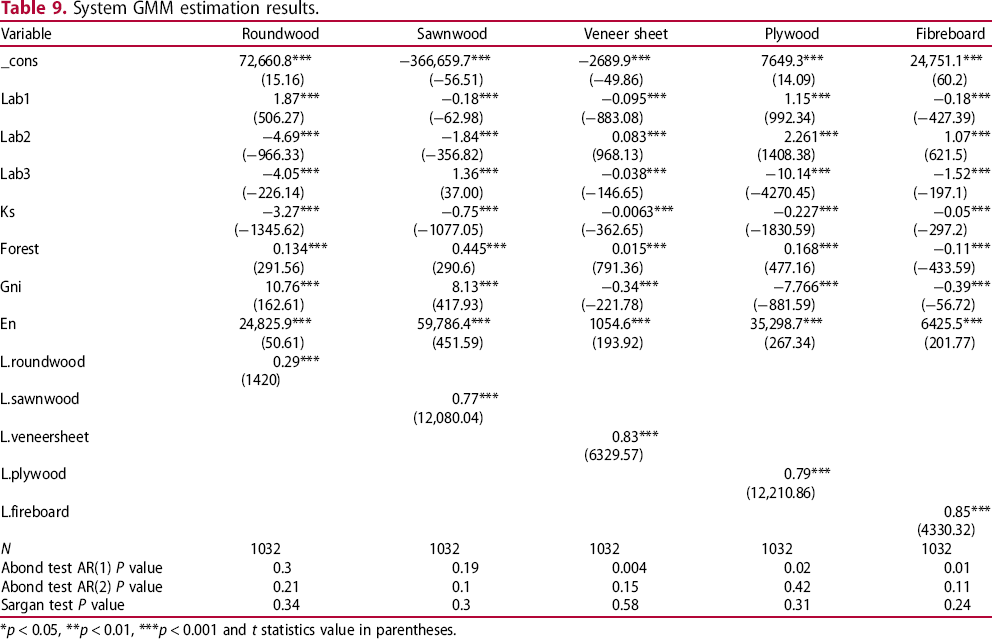

System GMM estimation results.

*p < 0.05, **p < 0.01, ***p < 0.001 and t statistics value in parentheses.

According to the theory, the endowment variable should have a positive linear effect on the net trade, and the per capita income reflecting the positive relationship between net trade and factor endowments should also have a positive effect, but the real regression result is inconsistent with what was expected. The different factor endowments have different effects on the net export of forest products. The capital stock affects the net export of roundwood, sawnwood, veneer sheet, plywood and fireboard significantly, and its effects are negative. It means that a larger capital stock is disadvantageous to the net export of wood forest products. The forestland area also has significant effects on the net export of all these products, and its effects are positive for all wood products except fibreboard. High-quality labour affects sawnwood and veneer sheet significantly and negatively, and affects roundwood, plywood and fireboard significantly and positively. Medium quality labour affects roundwood and sawnwood significantly and positively, while they affect veneer sheet, plywood and fireboard significantly and negatively. This result is inconsistent with the theory of international trade. It may be due to the development of other and more important factors, such as restructuring of the forest industries, technological development and movement towards more value-added products, which act as major drivers for a country's comparative advantage in the different types of trade in wood products (Uusivuori and Tervo 2002). The per capita income affects roundwood and sawnwood significantly and positively, while it affects veneer sheet, plywood and fireboard significantly and negatively. The negative effect of the per capita income on the net export of veneer sheet, plywood and fireboard is inconsistent with the theory that the demand would automatically increase when income increases. The result seems that the per capita income has structural effects on the forest sector such that richer countries have better developed wood-processing industry. This would explain the observed effects of the per capita income on the net export of different types of forest products. The first-order lag effects of all kinds of forest product are both positive and significant.

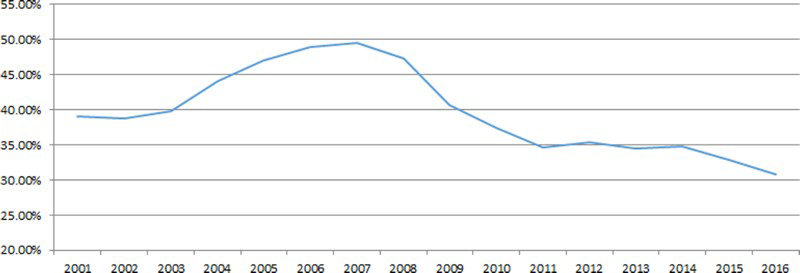

The environmental variable has significantly positive effects on the net export of all type of wood products. This suggests that the international efforts against illegal logging have brought positive effects on net trade, and all efforts are not an impediment to the net trade of wood products, but rather a contributing factor. Some illegal cutting sources have been cut off; high-risk wood of illegal logging has maintained a downward trend, while legal wood has increased in the world market. The countries with a corruption perceptive index below 50 indicate that the illegal-logging risk ratio in these countries is higher (Forest Trends 2013). In reality high-risk wood maintains a downward trend in the global market, its export ratio has decreased from 39% in 2001 to 30% in 2016 (Figure 1). The positive effects on sawnwood, veneer sheet, plywood and fireboard are likely that the efforts against illegal logging resulted in the increase of the legal-processed products, and their exports are enlarged. Canada and the U.S.A. are the main producing countries of sawnwood, their exports volume has taken 31% of world market share, and these two countries are also governing illegal logging strictly. Some big wood-processing countries such as China and India have imported great amount of roundwood, their import share has taken 45% of the global market in 2016, and they use the imported wood to produce the wood-processing product, export and obtain a great market share, such as their plywood, fibreboard and veneer sheet having obtained 35%, 13% and 11% of world market share, respectively, in 2016.

Export ratio of high-risk wood from 2000 to 2016. Source: International Trade Centre Trade Statistics.

Conclusions

In this paper, the data of 89 countries from 2003 to 2015 are used to examine the impact of efforts against illegal logging on wood products in trade based on the HOV model. The estimated model has shown that the efforts against illegal logging have contributed towards the increase in net trade of wood products. Our study has confirmed the conclusion that all the measures taken over the last decade have had positive effects, with a significant reduction (about 25%) in illegal logging between 2000 and 2008, and a similar fall (30%) in imports of illegal timber by major countries from 2004 to 2008 (Lawson 2010).

Although illegal logging has declined, it remains a major problem and while progress has been made, additional gains are likely to become increasingly hard to achieve. Advances in tackling illegal logging have slowed down in recent years (Chatham House 2015). In seeking to bring illegal logging to a complete end, it is important that producer countries take more actions to reduce illegal logging, and some consumption countries like Japan and China must also follow the footsteps of the U.S. and EU and prohibit the import and sale of illegally sourced wood (Leipold and Winkel 2016). Also, the importing countries need to expand cooperation with source countries along the lines of the policy or regulation against illegal logging.

Footnotes

Disclosure statement

No potential conflict of interest was reported by the authors.