Abstract

Introduction

Growth in the biobased industry is being driven by evolving global megatrends that include mitigating the impact of fossil fuel price and supply volatility, meeting consumer expectations for safer and greener products, and responding to more stringent regulations governing product standards and processes. These market drivers coexist with equally mercurial opportunities. Manufacturers recognize the competitive advantage of leading the way when it comes to improving their corporate social responsibility amid consumer demand for sustainability. Incorporating biobased materials into their product lines offers a first-mover advantage in emerging markets and a proactive response to changing global regulatory requirements in existing markets. In addition, the abundance of natural gas liquids (NGLs) from North American shale deposits is affecting the petrochemical feedstock landscape, creating opportunities to produce key carbon intermediates from alternative technologies that would otherwise be too expensive. Finally, biotransformation is now emerging as a dominant biobased technology as new advances in microbial engineering and processing help overcome key technical challenges, such as improving yields and producing novel entities. Early stage white biotechnologies, namely enzymatic conversion and fermentation, are now market-ready and fueling a global fermentation chemicals market predicted to grow to $60 billion USD by 2019. 1

The global bioproducts market is expected to reach $700 billion USD by 2018 (CAGR 5.5%), led by 14.9% CAGR growth in the $250 billion USD non-energy markets of chemicals, pharmaceuticals, and materials. 2 For example, the $3 billion USD global biobased chemicals market alone is projected to grow to $13 billion USD (13.3% CAGR) according to the most conservative estimates. 3 However, there is seldom a “green premium” for biobased products that are more expensive than their fossil fuel-based counterparts. Companies needing (for regulatory reasons) or wanting (for market perception reasons) to adopt biobased materials must ensure competitiveness with companies using traditional products. Addressing this challenge involves either overcoming the technical hurdles associated with decreasing the cost of producing biobased products or finding niche applications for biobased products that can better absorb the higher costs. These niche products tend to support segmented markets, such as personal care and natural health products, have greater perceived value built on brand awareness and consumer intimacy, and rely on biobased materials as key differentiating factors for commanding these higher prices.

The Biobased Landscape: A Canadian Perspective

Canada has all the ingredients required to sustain a viable biobased sector and capitalize on global opportunities, including abundant and diverse biomass resources, a strong and growing core of biobased industries, and scientific expertise and infrastructure to support innovative bioproducts research. The most recent Statistics Canada survey of the bioproducts industry estimated that there were 208 firms employing 3,000 workers and generating $1.3 billion in annual revenues. 4 Bioenergy and biofuels companies concentrated in Ontario and the Prairie Provinces are responsible for 70% of these revenues, but the sector is still in the early stages of growth. By 2020, bioproducts and renewable biomass resources combined are projected to account for $100 billion of Canada's gross domestic product, with an additional $1 billion in annual cost savings for industry associated with the use of bioproducts internally. Currently, many firms are small, privately owned, less than 5 years old, and engaged in pre-commercial R&D that is focused on developing technologies for converting biomass into higher-value consumer and industrial products, most notably organic chemicals, polymers and materials, biopesticides, and biocatalysts.

In particular, Canada's $300 million (USD228 million) biobased chemical sector is nascent relative to the petrochemical industry. The vast majority of biobased chemical companies, which are also concentrated in the Ontario-Quebec corridor, are engaged in production that is roughly divided between low-volume industrial intermediate platforms and specialty chemicals for personal care, cosmetics, health care, and household products. As with the larger Canadian bio-products industry, biobased chemical firms are mainly small, pre-market, start-up technology developers. Companies are focused on technologies for primary conversion and upgrading of biomass into biobased chemicals, often producing a single entity or ingredients for producing other bioproducts. Approximately 40% of companies are new entities and many are self-capitalized during the pre-commercial development process, or are subsidiaries of larger companies with an established presence in other sectors. These firms include new entrants dedicated to producing biobased chemicals, producers of other bioproducts, such as bioethanol, that view biobased chemicals as value-added pipelines, and large traditional chemical producers with subsidiaries focused on biobased chemicals.

Regardless of size or market niche, Canadian biobased chemical firms are responding to global market drivers and opportunities with common strategies. Companies are eschewing high-volume commodity chemicals, for which competition from petroleum is greatest, and instead focusing on industrial intermediates of moderate scale and fine and specialty chemicals for differentiated products. This focus makes embracing research and development (R&D) and diversity in both product chemistries and applications a necessity. Within the sector, Canadian companies are also particularly willing to engage in partnerships and collaborations along the value chain to access key R&D capabilities and risk-share new development. In particular, companies in legacy markets, such as pulp mills, are seeking to partner with biobased companies that have market-ready technologies. Adopting these strategies comes with an equally common set of challenges that are not unique to Canada. Biobased chemical companies require access to technical services to support commercialization (performance, specifications, compliance), custom R&D to identify and develop new applications and markets for their core technologies, and access to infrastructure for scale-up and demonstration. There is also an industry-wide need for both a coordinated effort to build core biobased technologies with cross-industry applications and a better mechanism for facilitating partnerships and collaborations across the value chain.

The National Research Council (NRC): Canada's Innovation Engine

Being competitive on a global scale requires that Canada's biobased industries achieve productivity through innovation, namely the conversion of ideas into commercially successful technologies and products. The National Research Council is Canada's research and technology organization (RTO) and engine for industrial innovation. 5 With more than 3,000 employees located at research sites across Canada and an annual budget of nearly $1 billion (USD760 million), the NRC mission is to build economic competitiveness and improve national industrial productivity by delivering technology development programs and specialized facilities and services. In doing so, it helps bridge the gap between discovery R&D and commercialization by providing the expertise, equipment, and infrastructure that Canadian industry needs to innovate and compete.

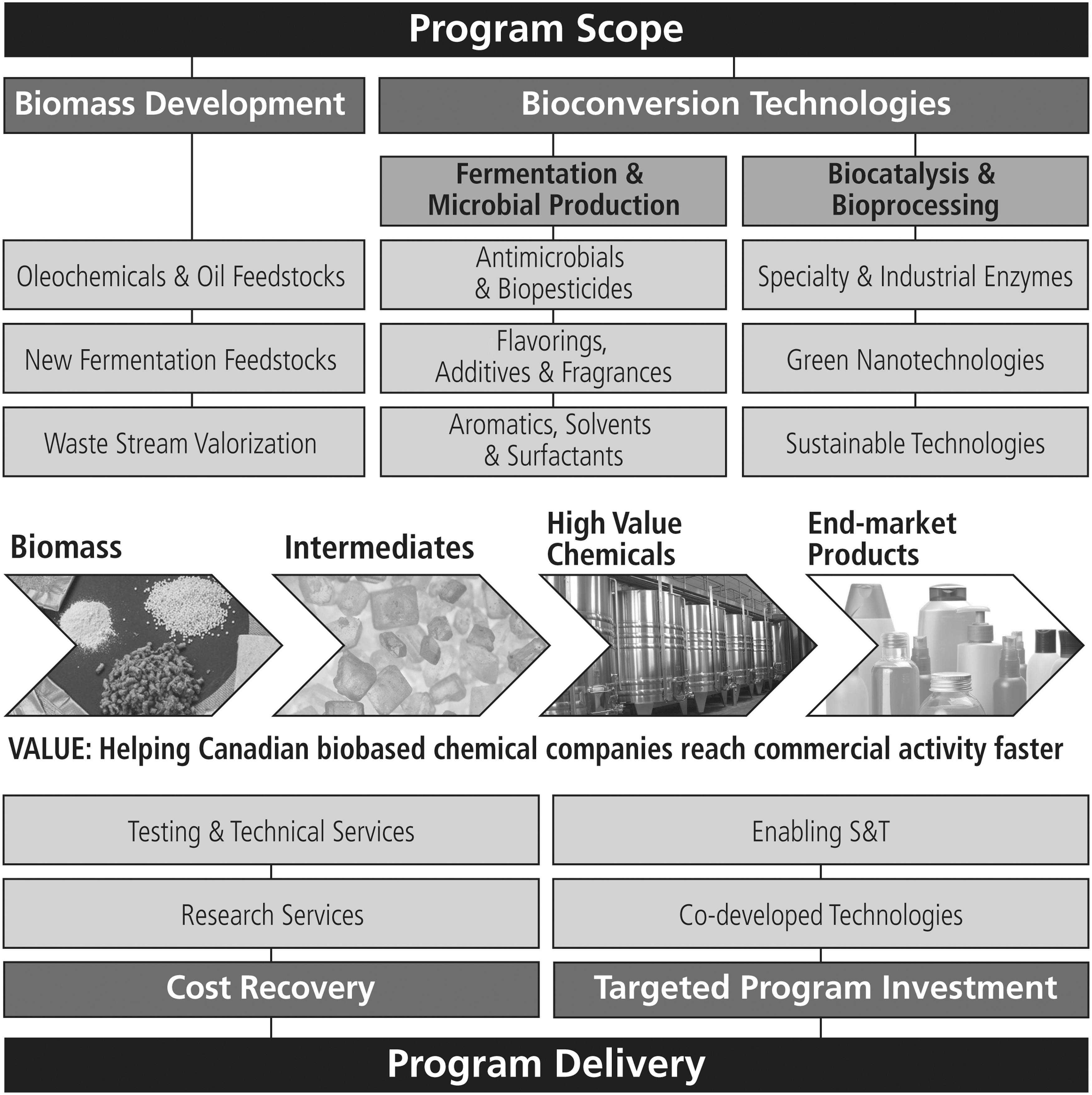

Through a strategic focus on aquatic and crop resource development, NRC is supporting efforts to generate greater value from Canadian biomass and waste streams in such varied areas as algal technologies, natural products chemistry, ingredient characterization (safety and efficacy), biomass development, bioprocessing, fermentation, and enzyme technologies. NRC works directly with small to large companies in Canada's growing biobased industry to facilitate the development and commercialization of new products and technologies with applications in bioenergy, food and nutritional ingredients, and biobased specialty chemicals and materials. Research and technology development efforts span the entire value chain from resource to product. NRC clients, partners, and stakeholders benefit by leveraging activities in these programs for licensing opportunities, new product development, and market expansion. At the recent Biotechnology Industry Organization's (BIO) World Congress on Industrial Biotechnology (Montreal, July 2015), the NRC highlighted several of its initiatives in the bioproducts R&D sector. Table 1 summarizes the market focus, target industry, and strategic objectives for these programs. The present article focuses on one of these initiatives, the Bio-based Specialty Chemicals (BSC) program (Fig. 1), as illustrative of how industry partners and stakeholders can engage NRC to advance their strategic innovation and commercialization goals in the biobased sector.

The structure and components of the National Research Council of Canada's Bio-based Specialty Chemicals program.

Overview of NRC Bioproduct R&D Programs

NRC's BSC Program

The BSC program targets the specialty segment of the biobased chemicals industry that is projected to lead growth over the next 5 years. 6 Fine and specialty chemicals, both platform and niche, account for more than 90% of non-energy revenues in the Canadian biobased chemicals sector. Major product segments include industrial chemicals (31%), health and cosmetics (23%), household agents (13%), and agricultural chemicals (9%). 4 Specialty chemicals are “differentiating agents” in consumer-driven manufacturing sectors. They are used for specific functions on the basis of performance or effect and support targeted marketing to increase the appeal of products in specific end market applications. Greater industry uptake of biobased chemicals has been limited primarily by their higher prices and the perception that they are less qualified fungible replacements that cannot be produced in sufficient quantities to meet demand. These challenges are particularly evident for commodity chemicals that are manufactured according to rigid standards and differentiated in the market solely on the basis of price. In contrast, specialty chemicals can accommodate higher costs than commodity chemicals because they command higher per unit prices, have smaller batch production volumes that reduce biomass burdens, and are associated with higher value, differentiated end-products that have sustainable profit margins.

Intermediates, such as glycerin and lactic acid, comprise the bulk of a global biobased chemicals industry in which market trends have traditionally centered on C2 and C3 feedstocks for bioplastics and biomaterials, such as polyethylene and monoethylene glycol. This demand is expected to continue through the next decade, but new chemicals like biobased succinic acid and butanediol are beginning to diversify the market and capture a larger share of its value. Within the specialty chemicals segment, however, market trends are driven largely by “lifestyle of health and safety” (LOHAS) consumers for whom market pull is described as being strongest “close to the skin.” Solvents, surfactants, and adhesives are dominant trends in industrial applications, with coatings and paints, cosmetics, food additives, and cleaning agents leading innovation in the consumer product sector. Thus, specialty chemicals are essential inputs into a variety of industrial and consumer products and establish the market line of sight for the BSC program.

For the Canadian sector to be successful and viable over the long-term, small and medium enterprises (SMEs) competing in the biobased specialty chemicals arena need to attract the interest of larger firms and multinational enterprises (MNEs) that sit closer to the production of end-market goods. To do so, companies must demonstrate that their technologies and products meet the immediate and strategic goals of these key industry partners along the value chain. The majority of near-commercial firms in the Canadian biobased chemicals industry have identified gaps between customer engagement, product demonstration, and sales. The BSC program will partner with these firms to bridge R&D gaps, commercialize technologies faster, and successfully engage larger manufacturers en route to solvency, growth, and the ability to further invest in new innovations and applications. Achieving this goal requires the program to provide partners with the research expertise, technical services, and infrastructure needed to help address the challenges firms face in reaching commercial viability, including improving cost-competitiveness, capitalizing on early market opportunities and diversifying market applications, and increasing acceptance of biobased chemicals into existing products and production methods. This mandate places the BSC program strategically within activities of NRC bioenergy (stationary power) and biomaterials (construction, automotive) programs, as well as initiatives focused upstream (algal carbon conversion) and downstream (natural health products) of its position in the larger, integrated bioproduct value chain.

The BSC program has three high level objectives that reflect the need to achieve sustainable impact in the biobased specialty chemicals sector by both responding to the specific needs of individual companies with core technologies and facilitating the development of the expertise and infrastructure required to strategically address common, industry-wide challenges: • Creating a competitive advantage for Canadian biobased chemical companies by allowing them to enter the global market ahead of competitors • Diversifying the bioproduct industry in Canada and supporting the creation of higher value markets for Canadian biomass producers • Positioning Canadian firms to remain in markets with ever more stringent regulatory and safety requirements, while ensuring a made-in-Canada response to domestic regulatory changes

A focus on improving the processes used to produce biobased specialty chemicals, specifically by adding incremental value to the core technologies of partners and stakeholders, connects these objectives and makes advances in the technology readiness levels (TRL) and commercialization readiness levels (CRL) of partnered technologies the key performance indicators of program success. The BSC program concentrates on solutions at the primary processing (biomass refinement, intermediates extraction), conversion and upgrading (production of specialty chemicals from intermediates), and product application (integrating chemicals into consumer products) stages. However, the program will also engage in the strategic development of Canadian biomass with partners that include primary producers, and work with manufacturers to overcome technical hurdles in bioproduct integration and identifying new applications for biobased chemicals.

Scope and Strategic Focus

The BSC program emphasizes the “bio” aspects of biomass transformation by concentrating on the application of white biotechnologies (enzymatic conversion, microbial production, biocatalysis) to produce high-value, application driven chemicals from biomass resources. This focus aims to capitalize on Canadian R&D strengths, valorize Canada's biomass diversity, and position the industry to grow and be competitive over the longer term. The BSC program's consultations with industry and other stakeholders to gain an understanding of the market drivers shaping the biobased specialty chemicals sector in Canada led to the identification of specific R&D gaps. These were highly varied, reflecting the makeup and diversity of the sector itself; however, common trends included the need to optimize existing bioconversion processes, develop novel technologies to produce next generation high-value chemicals, support new opportunities for existing biobased chemicals, and reduce production costs at all stages of product development.

The BSC program comprises three technology pillars (Table 2), each with core strategic areas of opportunity:

Overview of the NRC Bio-based Specialty Chemicals Program

Biomass development

Any initiative with the goal of promoting the development and adoption of biobased products must include activities that address feedstock supply and security. Identifying end users and applications for their materials was identified by biomass producers as the key barrier to entering the higher-value biobased specialty chemicals sector. End-users of the biomass faced the challenge of identifying the most suitable biomass sources and then integrating the new feedstocks in a cost-effective manner. The R&D objectives of this pillar are to increase the utility of biomass sources for specialty chemical production, identify new or alternate biobased sources of specialty chemical feedstocks, and add value to existing feedstocks with new applications in biobased specialty chemicals. Core strategic opportunities include valorizing waste streams as specialty chemical feedstocks, identifying Canadian alternatives for high-value oleochemical feedstocks currently obtained from volatile external sources, and developing purpose-grown or non-food alternatives for fermentation feedstocks traditionally derived from food crops.

Fermentation and microbial synthesis

Fermentation and microbial production systems have quickly emerged as the area of greatest interest for potential stakeholders of the BSC program, particularly for assistance in overcoming technical challenges such as strain optimization, process scale-up, and end-market integration. The R&D objectives of this pillar are to address the gaps that impede the scale-up and commercialization of microbial technologies, to develop and optimize new microbial systems to produce biobased specialty chemicals for which alternatives are limited, and to provide technical solutions to integrate microbial systems into production pipelines. Strategic opportunities include antimicrobials and biopesticides, biobased solvents and surfactants, and high-value ingredients such as flavorings and fragrances.

Biocatalysis and bioprocessing

The third pillar encompasses competencies that are numbered among NRC's traditional R&D strengths, namely addressing barriers to the development and application of enzyme technologies, developing and optimizing new enzymes with industrial and commercial applications, and improving traditional conversion technologies through biobased or greener alternatives. Strategic activities focus on addressing technical hurdles to commercial-scale enzyme production and adoption and process improvements to introduce alternatives for less sustainable conversion technologies, such as green nanotechnologies.

Working with NRC through the BSC Program

The bioproducts industry is characterized by a “demonstrate first” approach to investment and development. Collaborations within the sector are numerous, and larger firms are seeking opportunities and advances among SMEs and academia. However, these companies require strong evidence of potential commercial viability before they will commit more aggressively to investing in and adopting specific biobased technologies. This ability to reach and clearly demonstrate market readiness represents the key challenge for many biobased technology developers. Therefore, the BSC program initially emphasizes helping Canadian biobased chemical companies de-risk the development of existing technologies with the greatest potential to interest the (often larger) companies further down the value chain that produce consumer and industrial products. This phase targets SMEs with on-the-cusp technologies that are near market ready and poised to achieve commercial viability and generate positive net cash flows. The second phase of the program aims to help grow and diversify the biobased chemicals sector by working with companies to increase market penetration for their technologies and develop next generation processes and new applications. This phase entails greater MNE involvement as technologies become better proven and able to attract the involvement of downstream users.

Broadly speaking, infrastructure and technical expertise across NRC's two dozen research facilities can be accessed through four business lines: • Strategic R&D: to accelerate commercial development timelines in areas of national priority by engaging in collaborative research projects with partners • Technical and Advisory Services: to assist clients in solving immediate technical problems by delivering specialized fee-for-service support • The Industrial Research Assistance Program (IRAP): to help SMEs grow and succeed by delivering advisory services and financial support • Scientific Infrastructure: to enable the effective use of Canada's most specialized, large-scale scientific infrastructure

The BSC program operates by engaging partners and championing project development opportunities using these standard NRC business lines to ensure consistent client engagement, effective use of resources, and strategic risk management. Project development occurs on a continuous basis as opportunities arise during the course of the program, with no fixed submission or review dates. In its simplest form, the BSC business model is divided into cost recovery projects with limited program investment (Service) and projects that entail some degree of investment for which a return is expected (Strategic). Projects to improve or develop new capacity within NRC serve to bridge these two categories.

Service projects provide opportunities for companies to access expertise and facilities that lie outside their core capabilities by engaging NRC in a RTO capacity under a cost-recovery model. Activities are diverse, ranging from standardized testing and technical services to custom research projects that address research needs specific to a client's technology. Service projects serve an integral role within NRC's larger client engagement strategy that exceeds simple revenue generation. They afford a mechanism by which NRC and potential clients can interact and evaluate their respective capabilities with reduced risk, laying the groundwork for subsequent projects. Service projects also provide insight into client needs and R&D trends within the sector, guiding new NRC capacity development.

Strategically engaging R&D partners along the value chain is essential to meet the long-term program goal of strengthening and growing the biobased specialty chemicals industry in Canada. Strategic projects are developed around three general classes of activities, and are subject to techno-economic modeling to enable a better evaluation of their impact on the industry, technological viability, and potential return on investment. Projects involving co-developed technologies are typically conducted in collaboration with a single partner to address a specific technology barrier. Collaborative projects target near-market technologies to de-risk the final stages of development, accelerate commercialization, and help establish client relationships with moderate risk investment. NRC programs focus on de-risking technology development, not subsidizing it, with the expectation that a return will be realized as the technologies become viable. Enabling science and technology encompasses projects intended to advance the sector by addressing key R&D or sector-wide technology barriers. Revenue generation is not the focus, but projects are expected to be developed in collaboration with multiple stakeholders to distribute the cost and risk. Finally, capacity development activities are non-revenue generating projects intended to modernize and enhance NRC's expertise and capabilities for biobased technology development. The NRC sponsors and leads these projects, but they are client-facing with strong industry pull and have the potential to improve future service offerings.

Conclusions

Canada's NRC has a mandate to help industry address strategic priorities through targeted research and technology development, as exemplified by the breadth of initiatives aimed at increasing the competitiveness of the Canadian bioproducts sector. The BSC program provides an opportunity for NRC to spearhead efforts to grow Canada's emerging biobased chemicals sector by capitalizing on the strategic opportunity represented by specialty chemicals with applications in high-value consumer and industrial markets. The long-term success of the Canadian biobased chemicals industry cannot be achieved solely by focusing on niche, yet lucrative products and ignoring the larger commodity market. However, a concentration on specialty chemicals provides an initial platform to strengthen and diversify the biobased chemicals sector and lays a firm foundation for subsequent R&D programs to expand into additional markets. The primary goal of the BSC program is to accelerate the commercial readiness of Canadian firms and enable them to compete in the biobased chemicals market by reducing costs, diversifying market applications, and increasing the acceptance of biobased chemicals into existing products and production lines. The program objectives will be achieved with a focus on improvements to the technologies used to produce biobased specialty chemicals, especially white biotechnologies. Ultimately, the success of the BSC program is directly linked to the success of the Canadian biobased chemicals industry as evidenced by increase revenue, increased market share, and sustainable growth.