Abstract

The prevailing response of the Indian banking sector to implementing sustainable environmental practices is to delay compliance with internationally prevailing disclosures and protocols. The objective of this study is to analyze the sustainability reporting practices of the Indian banking sector. Sustainability reports or business responsibility reports of top 10 Indian banks are analyzed and compared on four reporting principles: stakeholder inclusiveness, credibility, materiality, and sustainability. Only four out of the 10 banks have adopted the international sustainability reporting framework, engaged their stakeholders, provided external audit assurance, and identified material issues in their sustainability reports. This study is valuable for the banks and policy makers as it provides a comprehensive picture of sustainability practices of the Indian banking sector vis-à-vis international practices and guidelines with a focus on sustainability reporting.

Introduction

Sustainable development has been well defined by the (Brundtland, 1987) as development that meets the requirements of today without impeding the ability of upcoming generations to meet their own requirements. The practices through which we can minimize the negative impact of business on the environment, society, and economy are referred to as sustainable practices. These practices incorporate principles of sustainability in all business decisions, which include delivering environment-friendly products or services and adhering to environmental principles in business operations. (Elkington, 1997) coined the term Triple Bottom Line emphasizing that businesses should focus not just on the economic value they add, but also on the fundamental and social value they add and destroy. Many research studies suggest that superior performance on environmental, social, and governance issues gets translated into better profits in the long run (Olmo et al., 2021; Ullmann, 1985; Zappi, 2007).

Initiatives have been taken at the international level for broader adoption of sustainable practices across all kinds of business organizations. For example, the United Nations Principles for Responsible Investments (UN PRI) is a nongovernmental and nonprofit organization for sustainable finance worldwide. United Nations Environment Programme Finance Initiative (UNEP-FI) aims to inspire better implementation of sustainability principles at all levels of operations in financial institutions. Similarly, the Equator Principles (EP) developed by the Equator Principles Association is a risk-management structure that is adopted and implemented by financial institutions for defining, evaluating, and handling environmental and social risk in projects; its primary aim is to offer a minimum standard for scrutiny and monitoring to support responsible decision making around risk evaluation.

Because finance is the lubricant for the wheels of the economy, adoption of sustainability practices by firms in the financial sector can affect overall sustainability and social responsibility Scholtens (2006). Financial institutions have an informational advantage since they can evaluate the societal, environmental, and governance performance of their borrowers. The banking sector across the globe is increasingly adopting sustainability practices and innovative sustainable products and services (Kumar, 2020).

When banks are working actively toward implementing sustainable practices, it is important that they communicate and disseminate the information effectively to all stakeholders (Laskar & Maji, 2016). Business responsibility reports, sustainability reports, and corporate social responsibility reports have emerged as vital tools that help banking organizations engage all stakeholders and demonstrate the commitment of the organization to adopting sustainability practices (Kumar & Prakash, 2019b). Moreover, sustainability reporting provides an avenue for stakeholders to benchmark the firms' performance in sustainable development vis-à-vis international practices (Laskar & Maji, 2016). Requiring sustainability reporting is the key to catalyzing government sustainability efforts (Bonifácio Neto & Branco, 2019).

The response to implementing sustainable practices in the Indian banking sector has been extremely delayed and slow, specifically in terms of internationally prevailing disclosures and protocols related to environmental issues (Kumar & Prakash, 2019a, 2019b, 2020). There are more than 300 banking institutions and hundreds of other financial institutions in India. However, out of 3,191 signatories of UN PRI, as of July 2020 only four financial institutions are from India. Similarly, out of 329 members of UNEP-FI only one Indian bank is a member and only one single financial institution from India has adopted the EP.

Kumar and Prakash, (2019b) in their study on Indian banks found that the banks are actively engaged in considering social dimensions of sustainability as they essentially disclose information about their community development programs, financial literacy initiatives, and financial inclusion developments. However, the environmental consideration practices are limited to the statement of the policy toward environment protection. Most of the public sector banks have established environmental policy, but only a few have disclosed their actual environmental practices. Although banks issue disclosures in the form of the Business Responsibility Report (BRR), they are mandatory and thus mere compliance of regulatory requirements (Kumar & Prakash, 2019b).

This study focuses on the adoption of sustainability practices and reporting in the Indian banking sector. It includes a review of existing literature on sustainable finance, Indian banking, and policy initiatives taken by the Indian government related to the promotion of sustainability practices. A discussion of international initiatives vis-à-vis the position of Indian banks is also included, along with a description of the methodology used in the research. Data analysis and findings as well as the implications and limitations of the study are also discussed.

Literature Review

Sustainable banking started way back with the management of environmental risks of financing projects since these risks can raise credit risks. The financial sector explored business prospects that would result from integrating environmental and social issues into mutual funds, institutional products, pension plans, and project finance (Ramnarain & Pillay, 2016; Weber, 2012). Recognizing the need for sustainable practices in financial institutions spurred the development of global institutions such as the UNEP-FI in 1992, the Global Reporting Initiative (GRI) in 2002, the EP in 2003, the Principles for Responsible Investment in 2006, the Global Impact Investing Network in 2007, and the Global Alliance for Banking on Values in 2008. These organizations have since updated and strengthened their guidelines from time to time (Weber, 2012). GRI-G4 guidelines launched in 2013 are widely accepted standard guidelines for sustainability reporting.

In the Indian banking sector, banks have made some effort to integrate sustainability into their business models. However, these efforts are mainly concentrated on Corporate Social Responsibility (CSR) activities such as education, balanced growth (different strata of society), health, environmental marketing, and customer satisfaction (Mahabir, 2007; Sharma & Mani, 2013; Wise & Ali, 2009). Many researchers recognize that the financial sector can play a significant role in controlling environmental damage. The lenders need to examine the effects of their lending and investment decisions on the environment in long run (Bihari & Pradhan, 2011; Ventura & Vieira, 2007). Indian banks are required to be fully aware of the environmental and social guidelines agreed to among banks worldwide. Indian banks are far behind their foreign counterparts in green banking. They must recognize their environmental and social responsibilities to enter the global markets and they must strive to grab the opportunities available in the green banking segment (Khawaspatil & More, 2013; Kumar & Prakash, 2020).

Though financial institutions ought to play an active role in the field of sustainable finance by financing those projects that support sustainable development and denying the same to projects that hinder the same, they have been completely lacking in active engagement in sustainable finance in primary markets. The lack of widespread implementation of sustainable finance demonstrates a significant void in the application of ethical leadership (Richardson, 2009). While the financial institutions have incorporated the idea of sustainability into business, they have actually done little to act on the concept. For example, an institution that sells green bonds might, in another division of their company, offer financing for coal mines or Arctic drilling projects. This paradox is attributable to a major gap in the way sustainability has been introduced into primary and secondary markets, a situation that calls for a serious consideration of uniform operationalization of sustainability (Urban & Wójcik, 2019).

Currently, sustainable finance initiatives are largely focused on secondary markets. Instead of issuing new debt and equity instruments, institutions are wrapping old instruments into new packaging by some taxonomical exercise of labeling them as green instruments. Although this repackaging has remained successful in meeting investors' preferences, the true sustainability transition requires seamlessly incorporating sustainable development goals into the practices of issuing new finance (Scholtens, 2006).

Assessment can capture the operationalization of sustainability by including other parameters. Principles, namely, stakeholder inclusiveness, credibility, materiality, sustainability context, and other attributes can be weighted or evaluated based on asset size categories (Kumar et al., 2018; United Nations Educational Programme and Federation of Indian Chambers of Commerce and Industry [UNEP & FICCI] 2016).

Policy Initiatives in India

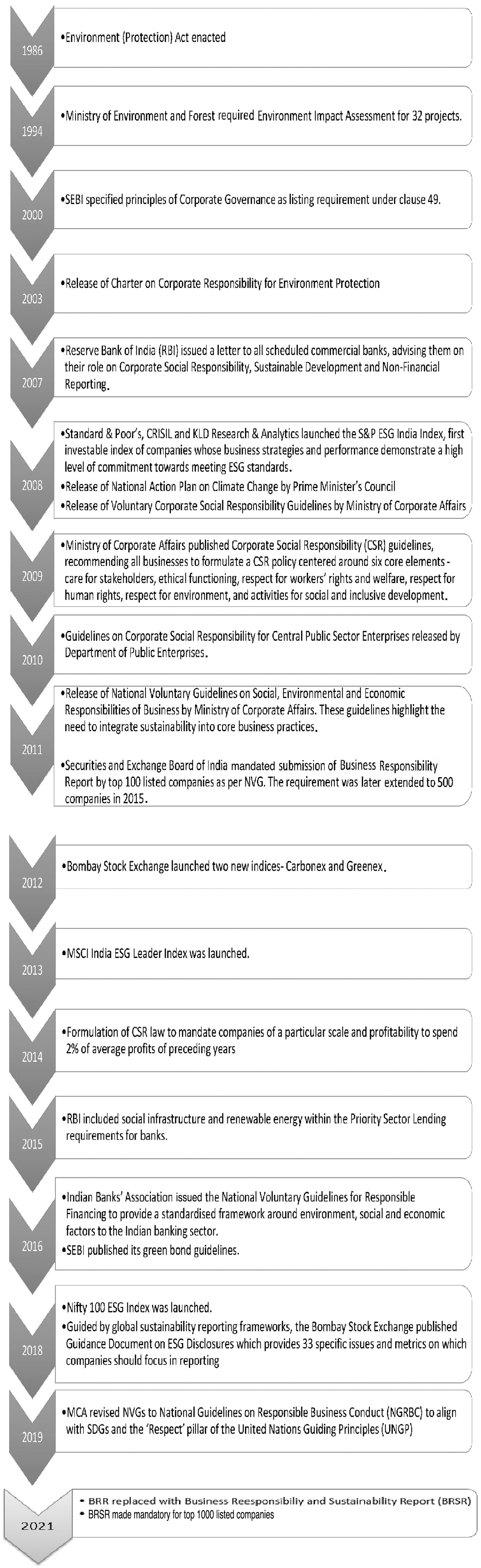

The Government of India has taken many initiatives to encourage businesses to integrate sustainability practices into their core business operations. Policy initiatives started in 1978 when the government first introduced an Environment Impact Assessment (EIA) on river valley projects; these assessments were later expanded to include other developmental projects. Since then, there have been many additional policy changes some of which are still ongoing. The most important of these initiatives was the introduction of Section 135 in the Companies Act of 2013, which requires companies to develop CSR policies, establishing a committee on their board to carry out the mandate. The companies also must spend 2 percent of their profits on CSR activities. Under CSR activities, companies can work on poverty eradication, malnutrition, education, gender equality, female empowerment, and sustainability.

In addition, the Securities and Exchange Board of India (SEBI) in 2017 mandated that the top 500 listed companies produce a Business Responsibility Report (BRR) as a part of their annual report (Goel, 2021; WBCSD, 2018) However, some banks go beyond the mandatory requirement and also publish stand-alone sustainability reports (SR) based on international guidelines like GRI-G4. In May 2021, SEBI replaced the BRR with the Business Responsibility and Sustainability Report (BRSR), which is intended to provide quantitative and standardized disclosure on environmental, social, and governance (ESG) parameters. This report is now mandatory for the top 1,000 listed companies on the Indian stock exchanges.

Against this backdrop, this study analyzes the position of Indian banks vis-à-vis international initiatives and compares the sustainability practices of the top 10 banks in India. The policy initiatives are shown chronologically in Figure 1.

Sustainability policy initiatives in India

Position of Indian Banks vis-à-vis International Initiatives

United Nations Principles for Responsible Investment (UN PRI)

The UN PRI consists of a coalition of assets owners, investment managers, and service providers who issue guidelines for incorporating environmental, social, and governance (ESG) issues into investment practices. The coalition advocates two approaches to investing responsibly: considering ESG issues while building a portfolio and improving the investee's ESG performance. The signatories of these principles must demonstrate their commitment to responsible investment by publicly publishing an annual Transparency Report, a mandatory requirement. Members of the coalition who don't release their climate-related financial disclosures can lose their accreditation for UN PRI.

In the court of public opinion, membership in the UN PRI bestows prestige and ensures compliance to ESG principles, which is why a large number of asset owners and investment managers across the globe are joining the association and meeting the requirements (Brown Brothers Harriman, 2019; Middleton, 2009). However, in India, the response to ESG principles is almost nil not only among asset owners and investment managers but also among government bodies and the public—there are only four signatories, and they joined very recently (one 2016, one in 2017, one in 2018, and one in 2020). In contrast, there are 48 signatories from China, 62 from Brazil, and 101 from countries in Africa and the Middle East. The numbers are larger for other developed economies such as the United States, Japan, and others (UN PRI, 2020).

A study conducted to identify the keys barriers to ESG integration revealed that the demand for ESG products and practices in the Asia Pacific region has been very slow over the years. The finance professionals in India assign more importance to governance issues than to environmental and social issues. The main barriers are lack of understanding of ESG issues, lack of company culture that supports these issues, and lack of client demand. In India, large institutional investors have not paid much attention to ESG investing. This attention has made a difference in other markets (UN PRI, 2019) where companies' ESG parameters are available in their performance reports. Indian companies need to come up with more qualitative ESG reporting and disclosures on the financial value of additions attributed to ESG factors. Such disclosures can assist investors in making informed decisions (Sinha, 2021). ESG investing and interest in ESG products has substantially increased since the Covid-19 pandemic, which prompted realization of the long-term implications of climate change and the social consequences of pandemics (Kumar, 2021).

Equator Principles

The Equator Principles (EP) is a framework for determining, assessing, and managing environmental and social risk in projects. Primarily intended to provide minimum standards of responsible risk in decision making, financial institutions have adopted it as such. The EPs apply globally to all industry sectors, especially to project finance, project finance advisory services, project-related corporate loans, and bridge loans. Currently, 105 Equator Principles Financial Institutions (EPFIs) in 38 countries have officially adopted the EPs, covering the majority of international project finance debt within developed and emerging markets (The Equator Principles Association, 2009). Financial institutions adopt the EPs to ensure that the projects they finance are developed in a socially responsible manner and reflect sound environmental management practices. Adoption and adherence to the EPs benefit their borrowers through engagement with local communities. Adopters are also able to assess, document, monitor and mitigate the credit risk associated with financing projects (The Equator Principles Association, 2009). The adopters are required to comply with the minimum reporting standards to implement EPs.

In 2019, the 2013 EPs were updated in an attempt to make them more future proof by considering the outcomes of the 2015 Paris Climate Agreement. However, critics argue that the new principles are simply tweaks to the text, with no meaningful improvement, and thus completely fail to address the call to take bold action on climate change and human rights. The updated principles are hardly distinguishable from the older version (BankTrack, 2019). As critics point out, under the new EP developed countries can continue to enjoy a lower level of scrutiny and the EPFIs continue to finance environmentally hazardous projects such as Dakota Access Pipeline in the United States and dozens of other fossil fuel projects in other developed countries. Moreover, the EPs do not take into consideration many popular ways of project financing, for example general corporate loans and project-related bonds, which have been used by the EPFIs to finance disastrous projects like the Line 3 tar sands pipeline that runs from Canada to the US Midwest. The project is running with grave climate implications and impacts on Indigenous people along the route. EPs are failing to maintain their commitment to upholding the rights of Indigenous peoples, including their right to grant or withhold consent for projects situated on Indigenous land (Women's Earth and Climate Action Network, 2019).

Indian banks are among the largest banks worldwide that arrange project funds. However, out of the current 105 members of EP, only one Indian bank—IDFC First Bank—is a signatory, joining July 2020. IDFC First Bank's institutional history of infrastructure and project financing provides it leverage in the integration of social and environmental concerns into their business model.

However, other institutions have not established an Environmental and Social Risk Management framework that can be mainstreamed into their credit risk appraisal and monitoring. This may be because they perceive the cost of developing human resources and systems for integrating nonfinancial risk assessment into their business to be too high. Moreover, financial institutions have low expectations for social and environmental risk management so risk to their reputations is quite low; an institution would face less reputational risk by not signing the EPs than failing to meet the requirements. Thus ESG integration of the level required by the EPs is widely seen more as a threat than an opportunity (Preece, 2018).

United Nations Environment Programme Finance Initiative (UNEP-FI)

The United Nations Environment Programme Finance Initiative (UNEP-FI) is a partnership between the United Nations Environment Programme and the global financial sector to mobilize private sector finance for sustainable development. The organization works with banks, insurers, and investors to help create a financial sector that serves people and the Earth with a positive impact. The aim is to catalyze the integration of sustainability into financial institutional practices through three sets of industry-based principles: Principles for Responsible Banking, established in 2019; Principles for Sustainable Insurance, established in 2012; and Principles for Responsible Investment, established in 2006. This principles' framework establishes the norms for sustainable finance and provides the basis for standard-setting and helping to ensure that private finance fulfills its potential role in achieving the 2030 Agenda for Sustainable Development and Paris Agreement on Climate Change agreed by governments around the world in 2015.

UNEP-FI has more than 300 member signatories and more than 100 supporting institutions worldwide. Of these 400 institutions there is only one Indian bank namely, Yes Bank representing member institutions from India. The UNEP India Report (UNEP & FICCI, 2016) identifies three main challenges for sustainable development financing in the Indian financial sector. First, financing for sustainable development requires low-cost, long-term finance, and India does not have substantial access to multilateral finance or grant funding to support sustainable financing. India can spend only about one-fourth of the amount that it needs to spend on basic infrastructure. Concessional lending from the World Bank has also been reduced because India has graduated from low-income country status to a lower-middle-income country. Second, there is limited participation of the private sector in infrastructural financing, which is linked to perceived political risks and lack of sufficient economic reforms. Despite these challenges the positive aspect as per the report is that India has begun to adopt instituting an overarching political framework where the industry is led by government. Such a framework could become a global model for sustainable development (UNEP & FICCI, 2016).

Research Methodology

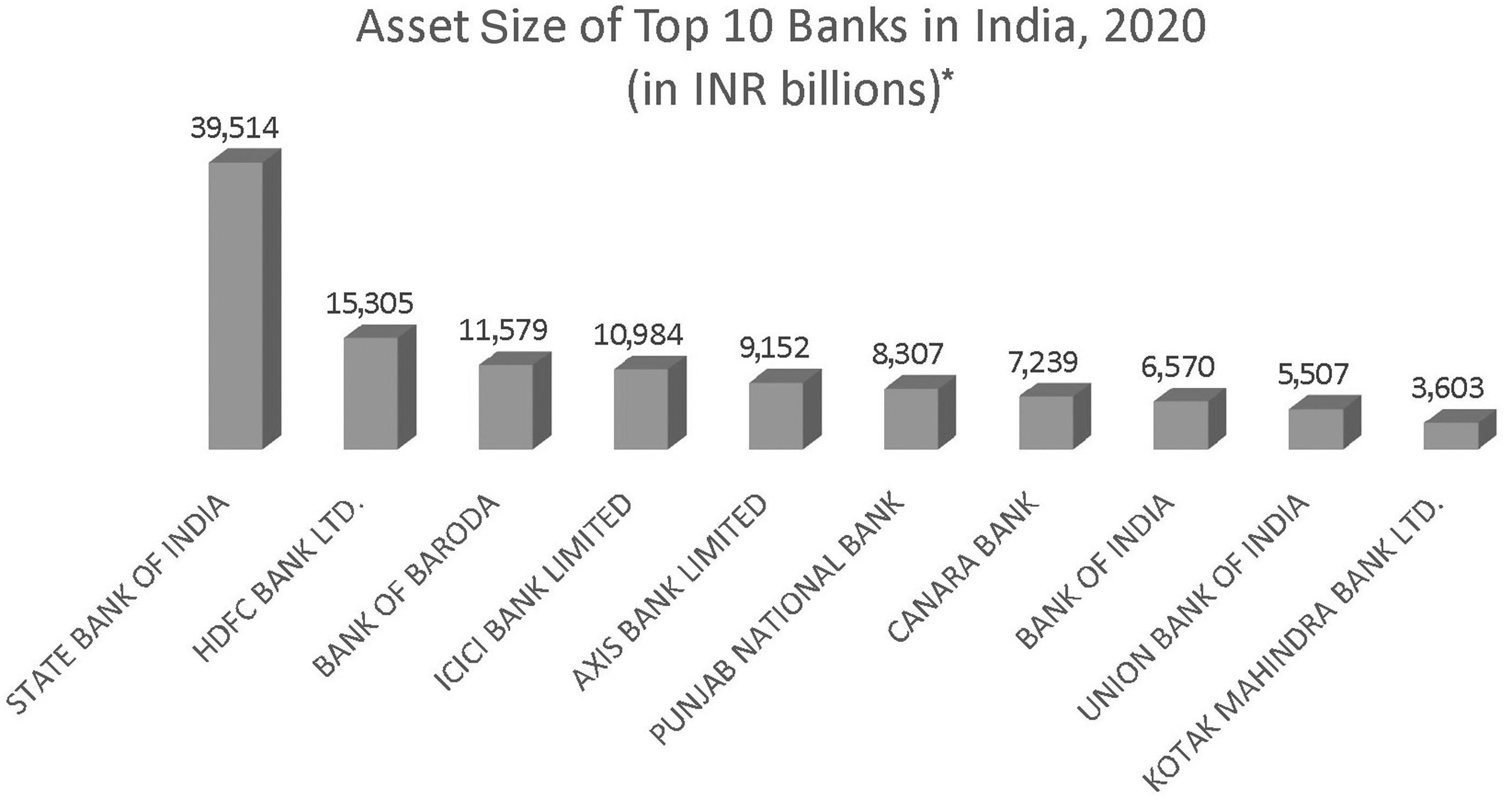

This study compares the performance of the top 10 Indian banks on sustainability reporting. Figure 2 shows the top 10 banks based on their asset size and reflects the data provided on the banks' websites. Since large firms tend to have significantly higher SR quantity and quality scores (Aggarwal & Singh, 2019), large banks were selected for comparison. Out of the 10 banks selected for the study six banks namely, State Bank of India (SBI), Bank of Baroda (BOB), Punjab National Bank (PNB), Canara Bank (CANB), Bank of India (BOI) and Union Bank of India (UBI) are public sector banks while the remaining four banks namely, HDFC Bank, ICICI Bank, Axis Bank, and Kotak Mahindra Bank (KMB) are private sector banks. For the purpose of comparison of sustainability reporting, SR or BRR of the top 10 selected banks have been collected for the financial year 2019-20.

Top 10 Indian banks based on asset size

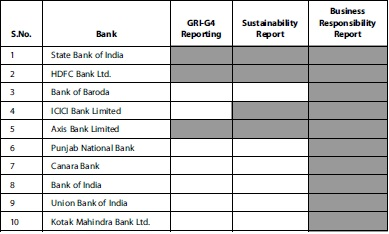

It should be noted that not all 10 banks publish SRs. The sustainability reporting status of the 10 banks is shown in Table 1. A shaded cell indicates compliance with the reporting standard; a nonshaded cell indicates noncompliance. Although all banks comply with the disclosure requirement mandated by the BRR, only four banks (SBI, HDFC Bank, Axis Bank, and ICICI Bank) go beyond the mandatory requirements and voluntarily publish comprehensive stand-alone sustainability reports. Of these four banks, only three have adopted GRI-G4 SR guidelines (SBI, HDFC Bank, and Axis Bank). Interestingly, Table 1 indicates that bigger in asset size doesn't necessarily translate into better SR responses. The third-largest bank, i.e., BOB, neither publishes a separate SR nor adopted the GRI-G4 guidelines.

Sustainability Reporting Status of Top 10 Banks in India

Gray cells indicate compliance with the reporting standard and white cells indicate noncompliance.

A content analysis of the SRs and BRRs of these banks was carried out for further evaluation. Content analysis is a technique used to objectively and systematically analyze textual material on some predetermined criteria in order to draw inferences in a quantifiable manner (Kumar & Prakash, 2020). Four reporting principles were used for content analysis: stakeholder inclusiveness, credibility, materiality, and sustainability context. These parameters have been identified from a GRI-based sustainability reporting matrix and other related studies (GIZ, 2012; Ranjan et al., 2018). The GRI-G4 reporting guidelines define 10 reporting principles at the core of reporting of which four (stakeholder inclusiveness, materiality, sustainability context, and completeness) are related to the content of the report and six (balance, comparability, accuracy, timeliness, clarity, and reliability) are defined as the principles that determine the quality of reporting. Out of the 10 reporting principles, three content principles and one quality principle have been used in this study (see Table 2). SRs and BRRs have been thoroughly analyzed on these indicators and the findings tabulated.

Parameters of Sustainability Reporting

Source: GIZ, 2012; Ranjan et al., 2018.

Data Analysis and Findings

Stakeholder Inclusiveness

Stakeholder identification and stakeholder engagement

These parameters are important aspects of sustainability reporting. The sustainability report should not only identify the key stakeholders of the business but also explain how the report responds to the expectations and interests of stakeholders. Stakeholders include a wide variety of entities and individuals who have some interest in the organization, from investors, employees, and suppliers to customers and communities. Stakeholders' expectations and interests therefore vary as each is associated with the organization for different purposes. Stakeholder engagement is the process of identifying the stakeholders and understanding their reasonable expectations. GRI-G4 reporting requires organizations to document the stakeholder engagement process and consider their expectations.

Stakeholder inclusiveness is studied by international research agencies (GIZ, 2012) using the following parameters: detailing stakeholder engagement process in the report, prioritization, frequency of engagement, mode of engagement, reasons for engagement, review of previous engagement, and identification of the person responsible for follow-up action. Out of the 10 banks in this study, four (Axis Bank, HDFC Bank, SBI, and KMB) included in their SRs the stakeholder engagement process, prioritization, topics of discussion, mode of engagement, and frequency of engagement. To have a greater level of disclosure, HDFC Bank and SBI have also reported their focus areas of engagement and their responses to the expectations and needs of customers. Surprisingly, the KMB, which is currently not complying with GRI guidelines, has been not only disclosing the stakeholder inclusiveness parameters but also including the name of the team or department responsible for the engagement process.

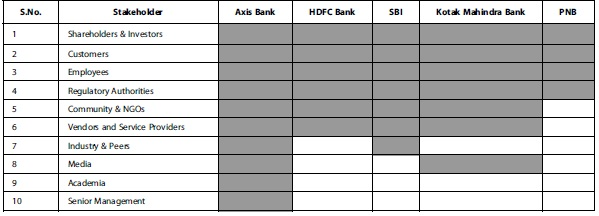

Table 3 presents the types of stakeholders identified by each bank. A shaded cell indicates that the stakeholder is identified; a non-shaded cell indicates that the stakeholder is not identified. Axis bank identified the most different types of stakeholders while Punjab National Bank identified the fewest. The banks not listed in Table 3 state that they have identified their stakeholders but they don't specifically mention them in their reports.

Stakeholders Identified by Each Bank

Gray cells indicate stakeholders identified by the bank and white cells indicate stakeholders not identified by the bank.

Emotional appeal

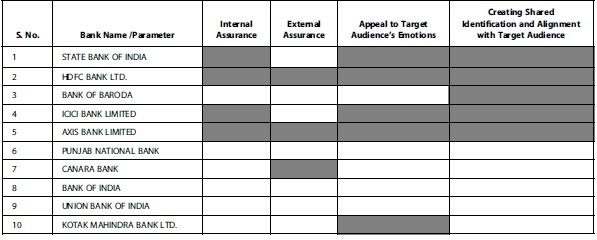

This parameter refers to the method of persuasion which is designed to create an emotional response by manipulating the emotions of the audience. Use of relevant images and metaphors provides an emotional appeal to stakeholders and is a means of stakeholder engagement. Out of the 10 banks in this study, five use pictures and images in their SR while the other five banks which prepare their BRR in the prescribed format of SEBI don't use images or metaphors, as the prescribed format is in the form of questions, which can be answered in terms of numbers/percentages or yes/no responses.

HDFC Bank, ICICI Bank, KMB, and SBI have used real images of their customers, products, buildings, and development projects, among other images, to enhance the emotional appeal of their reports. HDFC Bank, ICICI Bank, and SBI have used an attractive graphical representation of the facts and figures related to their performance. Axis Bank, ICICI Bank, and KMB provide success stories with pictures of the beneficiaries of their development efforts. For example, the ICICI Bank shares the success story of Bindu Yogi who went from being an unskilled laborer to a skilled tailor after joining the ICICI Foundation Rural Livelihood program. ICICI Bank has enhanced stakeholder engagement of its report by providing case studies about its funding of development projects, such as setting up an Oxygen Generation Plant at Siachen, for which ICICI bank provided a large amount of grant money to an NGO.

Creating shared identification and alignment through linguistics

Use of inclusive pronouns such as “we,” “your,” and “us” indicate the linguistic strategy of the bank to create an alignment with the target audience. Five out of 10 banks use inclusive pronouns in their SR or BRR for reporting their performance on sustainability parameters while the other banks have prepared their reports in passive voice.

Credibility

Both internal and external assurance are related to the authenticity and credibility of the report.

Internal assurance

This parameter indicates assurance that top management of the company, for example the managing director, CEO, and others, has confirmed the sustainability practices. Reports that include a message from the management personnel about their sustainability practices are assumed to meet this criterion. Out of the 10 banks in this study, only four banks (SBI, HDFC Bank, ICICI Bank, and Axis Bank) provided a message from management as part of their SR. The banks that don't publish separate SRs don't provide any such internal assurance.

External assurance

An audit of SR by a third party, though voluntary, is a key GRI-G4 recommendation. If the SR includes a certificate of independent audit, this criterion is considered to have been met by the bank. Of the 10 banks in this study, only three have provided certificates of external assurance—Axis Bank, HDFC Bank, and Canara Bank. Though Canara Bank doesn't publish a separate SR, it has included the audit certificate in its BRR. It is startling that the biggest bank, SBI, is not carrying out an external audit while Canara Bank, which ranks seventh, is conducting an external audit for its business responsibility report.

Table 4 shows the performance of the 10 banks on credibility and stakeholder inclusiveness parameters of sustainability reporting. Shaded cells indicate that the parameter is met; a non-shaded cell indicates that the parameter is not met by the bank.

Position of Top 10 Banks on Four Parameters of Sustainability Reporting

Gray cells indicate compliance with the reporting parameter and white cells indicate noncompliance.

Materiality

Under the materiality principle of GRI-G4 reporting, organizations are required to identify material sustainability issues based on two aspects: 1.) the issue should be an outward impact of the organization on the economy, environment, and society, where outward impact means the impact of the organization on economy, environment, and society and not vice versa; and 2.) the issue should be significant enough for stakeholders to impact their decisions about the organization. Thus, material issues are the issues which rank high on atleast one of the two dimensions of materiality. As a result of this analysis, companies can create their long-term sustainability strategy and targets. The principle ensures that in determining material topics, the organization considers the full picture of its outward impacts rather than only immediate impacts from a business perspective, such as penalties, higher costs, or a damaged reputation.

SR and BRR of the 10 banks analyzed in this study show that the three GRI compliant banks (Axis Bank, HDFC Bank, and SBI) have carried out materiality assessment through a two-dimensional materiality matrix as defined under GRI-G4. Two banks (ICICI Bank and KMB) have attempted to identify material issues, but their method of identification is not clear.

Material issues identified by the three GRI compliant banks have been divided into economic, environmental, and social issues (see Table 5). The materiality matrix of the banks shows more economic issues (at least six identified by each bank) than either of the other issues, suggesting that economic issues are the most important. The economic issues identified are related to compliance with regulations, data security, customer privacy, customer satisfaction, risk control, product innovation, etc. Surprisingly, SBI, the largest bank, doesn't identify any environmental issues except digital innovation and paperless banking. Axis bank stands alone in identifying the integration of environmental risk in its investment and lending decisions as a material issue. Only HDFC bank identifies e-waste management, energy management, emissions, and climate change as issues that have a material impact on the environment. These issues actually reflect environmental issues that a commercial bank may have. Other banks should also identify these issues in their materiality matrix.

Material Issues Identified by GRI Compliant Banks

The banks have given reasonable importance to social issues: Axis bank has identified a maximum of five issues while the other banks have all identified financial inclusion, financial literacy, community development, and the like, which could be considered economic issues.

Sustainability Context

This parameter is used to assess the banks' performance in the wider context of sustainability. The objective of sustainability reporting is to report current and future impacts of the organization on the deterioration or improvement of environmental, social, and economic conditions at a local, regional, or global level. This concept is clearer in the context of the environment in terms of the usage of scarce resources and pollution levels. Therefore, the organization should report social and economic impacts in terms of their socioeconomic goals for sustainable development.

Out of the 10 banks in this study, only four (Axis Bank, HDFC Bank, ICICI Bank, and SBI) map their activities to the Sustainable Development Goals of the United Nations Development Programme (UNDP). KMB maps its activities to the nine principles of National Voluntary Guidelines of reporting. The rest of the banks included in this study have prepared their reports based on the BRR. It is notable that these four banks recognize their responsibility to carry out an environmental and societal risk assessment of their financing projects and state that this risk assessment is carried out before lending. These banks finance many such projects, which have a positive effect on the environment, for example renewable energy-related projects. However, only HDFC Bank explicitly states that they do not lend to projects that produce a negative environmental impact. For example, the HDFC banks boldly state in their report: “We do not lend to businesses that produce ozone-depleting substances (CFC-11, CFC-12, CFC-113, Carbon Tetrachloride, Methyl Chloroform, Halons-1211, 1301, and 2402).”(HDFC Bank, 2019, p. 23).

Summary Policy Implications and Limitations

It is worth mentioning here that this study is based on the data for 2019-2020 for only the top 10 banks of India, thus the results should not be generalized for all the banks. A longitudinal study with a larger sample of banking organizations is needed for more generalized results. The findings of this study are purely based on self-reported disclosures made by the banks; they may or may not convey their real performance. Moreover, the comparison of sustainability reporting is limited to assessment of mainly the content principles rather than the quality principles due to limitation of availability of data to assess the quality principles.

Conclusion

The financial sector can have a great impact on its clients since investing companies are the major source of capital for businesses. They can not only adopt the sustainability practices in their operations, but they can also ensure the adoption by clients because of their ability to evaluate their economic, societal, environmental, and governance performance. The clients may in turn influence their suppliers and other entities controlled by them. Thus, higher participation by the banking sector could transform the landscape of sustainability practices.

This article provides a unique comparison of sustainability reporting of the top 10 Indian banks on the basis of GRI-G4 reporting principles. This study has several implications for bankers and policy makers as it provides a broad picture of sustainability practices of the Indian banking sector vis-à-vis international practices and guidelines with a greater focus on sustainability reporting. The banks low on GRI-G4 reporting principles need to expand their CSR communication strategies to not only focus on meeting the regulatory requirements but to address the needs of all their stakeholders.

Footnotes

Author Disclosure Statement

No competing financial interests exist.