Abstract

Due to the lower production costs, maturity of commercial off-the-shelf technologies, and flexibility to adapt to technological change cycles, Smallsats are rapidly gaining in importance, in particular in the New Space Economy. Several new applications such as mega-constellations and clusters of Smallsats contribute to this trend. The average mass of Smallsats has been increasing over recent years as technology demonstration satellites move toward commercial technology deployment using larger platforms and more power supply, and it is forecast that this trend will continue to increase. This leads to an increased interest in dedicated Micro-launchers, avoiding the disadvantages of shared piggyback launching, in particular in terms of launch delays. Several of these launchers are under development, and this article is intended to qualify the market for such Micro-launchers allowing to launch up to 500 kg in low Earth orbit. At the same time, the launch site location needs to be taken into account to allow for the required high launch cadences demanded by NewSpace business models as well as optimal orbit insertion and maximal launch window flexibility with minimal interference on air and maritime traffic. The example of a launch site in the southern hemisphere, in particular in Southern Australia, is presented, describing its features to comply with these requirements.

Smallsats and Their Evolution

Technically speaking, the first satellites launched fall into the category of what was defined later as Smallsats and preceded therefore by far in time the New Space evolution (whereby we have to note here that there is no generally accepted definition of New Space (Economy). Various definitions are still under discussion. 1 Indeed, the first satellites launched in the period 1957–1958, at the occasion of the start of the International Geophysical Year, Sputnik I, Explorer I, and Vanguard 1 would fall under the present definition of Smallsats, with masses of 83.6, 13.9, and 1.47 kg, respectively. 2

During the 1960s, a large number of Smallsats were launched by mainly government organizations to obtain more data on the space environment and to flight-test new technologies as demonstrators. After this period, Smallsats were overtaken in importance by larger satellites, mainly those placed into geosynchronous Earth orbit (GEO) 35,786 km above the equator, and the number of dedicated Smallsat launches decreased considerably. The move to GEO was in part forced upon the industry because of the market demand these new satellites were being used to fulfill, namely telecommunications services. For the first time ever, disparate locations around the globe could be connected by relaying signals via a satellite, seemingly stationary in the sky. But the design of a GEO satellite to achieve this seemingly impossible task is based around the analog radio components that receive and retransmit the signals from the Earth. The largest components are the waveguides that connect the antennas to the receivers and transmitters. These metal tubes must be tuned to match the physical wavelength of the telecommunication signals themselves, and the satellite must have a waveguide for each frequency the satellite supports. Couple the large number of waveguides with their corresponding analog transmitters and receivers, as well as the space-rated support electronics also being large and very costly artifacts to build and get into orbit, a standard GEO satellite can weigh up to 6,500 kg. It is important that the satellite has an operational life span of 10–15 years to get a perceived good return on investment for the operator in view of the high initial capital expenditure (CAPEX). This is only achievable by placing the large satellite in a location that provided a fixed financial return with constant coverage on the globe, something a GEO location allows.

This market pull toward big GEO satellites is the reason why many of the world's existing launch sites are located as close to the equator as possible, and on the eastern seaboard of continents. The requirements are set to maximize the component of the Earth's rotational velocity that is in the same plane as the intended orbit at launch, following a launch trajectory out to the East.

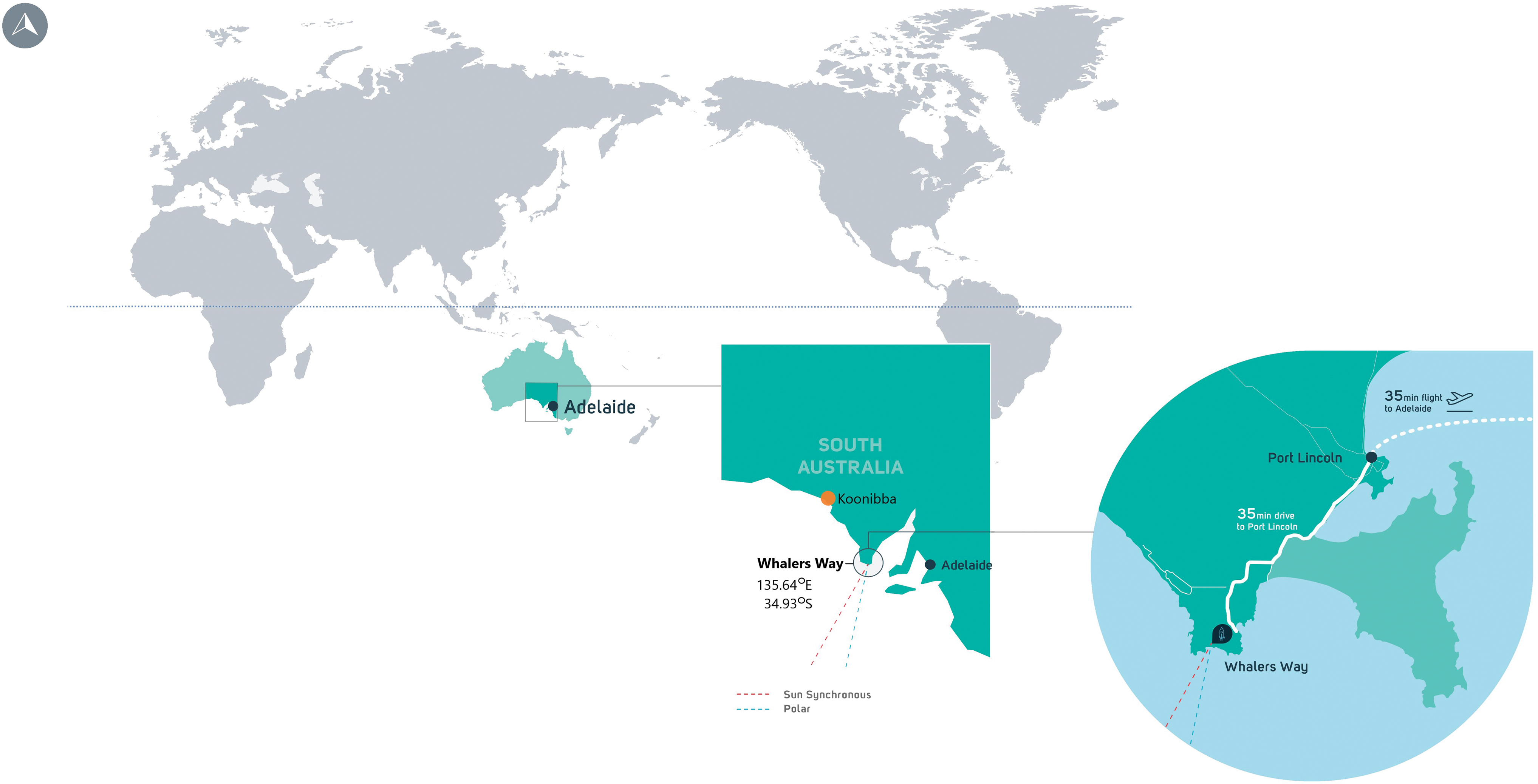

Other locations concentrated afterward, with the increasing importance of Smallsats, on locations with a direct insertion to polar orbits, such as the location of the Southern Launch (SL) site, as per Figure 1, which will be further explained later in this article.

Location of Southern Launch polar orbit launch site (credit: SL). SL, Southern Launch. Color images are available online.

Indeed, the situation changed from 1987 onward, with a Smallsat “revival” initiated by DARPA and NASA, among others with the so-called LIGHTSAT program of DARPA. Under this program among others, two 66 kg communication satellites (MACSATs) and seven 22 kg MICROSATS (with digital communication payloads) were produced and successfully launched. 3

Interesting contributions were made during that period by the University of Surrey with Prof. Sir Martin Sweeting as main proponent, who built the UoSAT-1 (also known as UoSat-OSCAR 9) amateur radio satellite in his Centre for Satellite Engineering Research (CSER) at Surrey. This 52 kg Smallsat is often considered as a milestone in the Smallsat evolution (in particular by the novelty to use amateur radio bands and the use of in-orbit reprogrammable computers) and was launched as a secondary payload by NASA in 1981. Originally designed for 2 years of operation, it stayed operational for 6 more years, and as such demonstrated at the same time the high commercial potential of Smallsats.

The research at the CSER focused initially on remote sensing applications, which led to the creation of a commercial subsidiary called Surrey Satellite Technology Ltd (SSTL) in 1985.

†

The visionary character of SSTL can be underlined by the fact that SpaceX took a stake in the company in 2004 with Elon Musk stating on that occasion

4

:

SSTL is a high-quality company that is probably the world leader in small satellites. We look at this as more a case of similar corporate cultures getting together.

SSTL, which was taken over by Airbus in 2008 but remained an independent unit in the consortium, thus played a paramount role in the awareness of the commercial potential of Smallsats and will go into the space history as an important Smallsat pioneer, in particular demonstrating the commercial potential.

With an increasing level of miniaturization, smaller satellites such as CubeSats started to gain popularity over the past 2 decades, with a growing number of nanosatellite and picosatellite developments and launches, also covering educational purposes and prepared at universities with the help of (postgraduate) students with very limited budgets.

This made it necessary to implement definitions in function of the mass of the satellites, as shown in Table 1.

Definition of Smallsats as per Federal Aviation Administration a

Reference 5

We have to note here that many organizations use other definitions, for example, defining Smallsats up to the range of 500 kg instead of 600 kg as per Table 1. This needs to be taken into consideration, in particular when comparing historical statistical data and future forecasts.

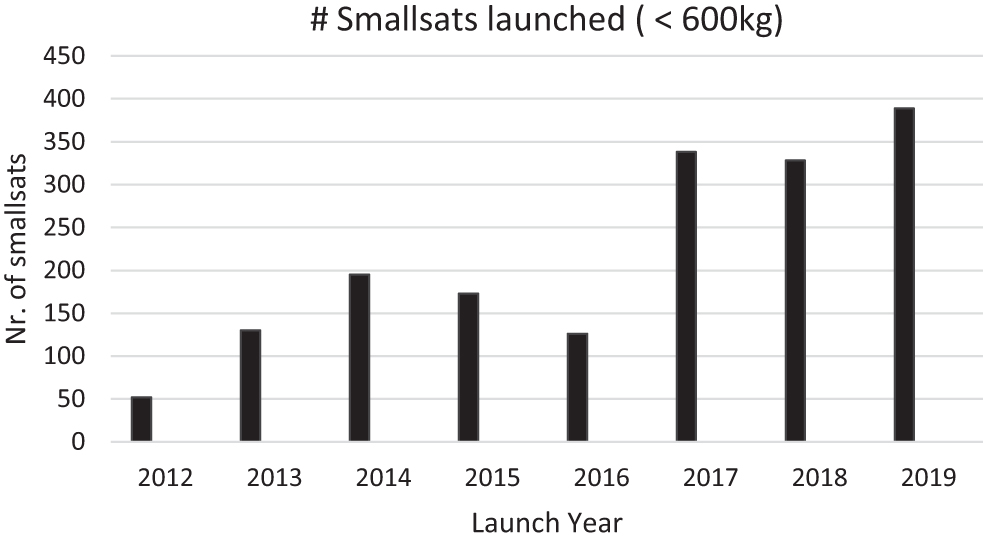

If we adhere to the 600 kg definition, we can, based on a recent report, 6 show the evolution of the number of satellites launched during the last years as per Figure 2.

Number of Smallsats launched (<600 kg), based on Bryce. 6

With a rapid number of increasing applications, in-depth evaluations have been made on future trends in the Smallsat ecosystem. Analysts consider fleets of Smallsats in low Earth orbit (LEO), operating in orbits between 160 km and 1,000 km above the Earth, are as a most probable future trend. 7 In particular, if Internet-from-space constellations will become operational, we will see an important growth in the number of Smallsats to be launched, just think of such constellations such as OneWeb (648 satellites), Kuiper (Amazon, 3,236 satellites), and the Starlink constellation of SpaceX with even more than 12,000 satellites planned.

Issues Linked to Smallsat Deployments

Whereas the advantages of the Smallsat development have been highlighted, we should not ignore a number of challenges associated with this development. Indeed, the right attention must be given to control a number of challenges associated with Smallsat operations such as, just to mention a few:

Lack of high-capacity power systems, which will require space qualification of the present terrestrial battery developments to prolong (if needed) the satellite lifetimes or to allow more payloads on 1 platform. Limited propulsion capacity for orbital corrections and end-of-lifetime interventions, which will require more efficient application of small (electrical) thrusters or other deorbiting devices. Generation of space debris, which will require attention to reliable Smallsat deorbiting techniques and non-defragmentation design of the Smallsats themselves, to be supported by global regulatory policies. Access to high-inclination orbits that have historically not been a focus for existing launch vehicle operators. Access to launch sites that allow for high launch cadences while still providing optimal insertion trajectories into higher inclination orbits. Potential issues with frequency allocations, in particular when the mega-constellations will require extensive bandwidth and risk to interfere even with GEO satellite services. Also, new policies (ITU) and interference avoidance techniques will be required. Increasing need for dedicated Smallsat launchers, to reduce the limitations associated with secondary/shared payloads (as will be developed further in this article). Competition with alternatives (e.g., unmanned aerial vehicles) cannot be ignored. Here in particular the main cost driver of Smallsats, the launch cost, will play a paramount role.

The Need for Dedicated Smallsat Micro-Launchers

The Bryce report “Smallsat by the numbers 2020” 6 points out the average growth in Smallsat mass over the last years from, for example, 40 kg in 2014 to 109 kg in 2019. This is mainly due to a shift of satellites from the nano- and lower class of Smallsats (<10 kg) toward the 11–600 kg class as per the definitions in Table 1. As an illustration of this trend, the 11–600 kg class of satellites accounted for only 11% of all Smallsats launched in 2017, growing to 27% of the launches in 2018 and then 53% in 2019. 6

This trend can be explained by the fact that a decade ago there were many experimental low mass Smallsats, produced at, for example, low cost by universities. Most of these satellites only covered a limited number of applications, sometimes even only one dedicated application or instrument as the payload. At present, now that a number of technologies are proven on the basis of these technological evaluations, most Smallsats require larger platforms (and power supply) to cover multiple applications, leading to a gradual increase in average mass as described above.

Independent assessments such as the one by Euroconsult 8 predict that the average mass of the Smallsats will be around 139 kg in the period 2019–2028 (compared with 109 kg at present), with a gradually growing tendency over the next few years.

Initially, Smallsats were launched as secondary payloads in the so-called piggyback mode. Up to the 1990s, this opportunity was offered by launch providers at nominal cost, sometimes even for free. This changed in the following years, in particular when launch providers became aware of the commercial value of Smallsats (although some university-built Smallsats such as CubeSats and Cansats were sometimes still launched free of charge for public relations reasons). Afterward, commercial launches were offered, for example, by Arianespace using the Ariane Structure for Auxiliary Payloads adaptor. In view of the limited income and sometimes extra efforts needed by the launch operator, this option had only a limited response and was not really fully marketed. With the fall of the Soviet Union and the need for hard currency, in particular the Cosmos small launcher and the Dnepr launcher were used frequently initially to launch larger payloads and in the period 2000–2015 to launch Smallsats, despite often challenging negotiations and schedule uncertainties. 9

In particular, for commercial Smallsat operators, such dual launches have considerable drawbacks:

The schedule is driven by the primary payload and its launch window. In general, the orbital trajectory is determined by the primary payload. Delays in the primary payload delivery delay the whole launch, hence also the launch of the secondary payload. The primary payload operator will dictate strong contamination avoidance and interference avoidance measures to the secondary payload.

Several Smallsat operators therefore had satellites blocked for months at the launch site. A survey of Bryce, 10 covering the period 2015–2019, shows us that over the past 5 years such delays were on average in the order of 5 months, with even extremes of more than 24 months launch delays. In particular, for young companies, this delayed time-to-orbit meant they ran the risk of not capturing an early market share. Evidently for young companies and start-ups, this also has severe financial consequences leading to cash flow problems and, on its turn, delayed investment rounds or increasingly worried investors due to sometimes slower time-to-market effects. Evidently, the reliability of the launcher is still a prevailing factor in this market.

Initially, a number of air-based launch systems have also been proposed to overcome this problem. Such systems, such as Pegasus, have not fully proven to bring a good cost-effective solution for the problem, although some projects are still pursuing this possibility, with probably LauncherOne as the best known example. 11 In this case, however, we cannot ignore that coupled to the cost of the launch aircraft is the cost and engineering complexity of certifying “the drop,” the mechanism and method of safely releasing the orbit capable rocket from the underside of the carrier aircraft before it successfully ignites and propels the payload into orbit.

Realizing this market need, the major space agencies have studied or started the development of Micro-launchers, such as VEGA lite (Light version of VEGA) (ESA), Epsilon (JAXA), KuaiZhou (China), and SSLV (ISRO). DARPA is following an open-market approach and initiated the DARPA Launch Challenge, with the objective to select from a list of candidates the one demonstrating the best responsive launch capability. 12

Also, private companies were soon aware of the market potential. SpaceX developed Falcon-1 for this market and in 2009 successfully launched a Malaysian satellite in orbit, but afterward concentrated on more lucrative markets. Recently, SpaceX has announced that they are considering a “dedicated rideshare,” launching a collection of Smallsats on its Falcon 9. 13 This is evidently applauded by Smallsat operators such as PLANET and SPIRE, which presently have considerable backlogs in launches.

A key driver for the cost-effective development of these Micro-launchers was the advent of affordable intricate rocket engine components, affordable three-dimensional (3D) metal printing machines and access to space capable commercial off-the-shelf (COTS) electronics to start-ups. An example of this advanced approach is Relativity Space ‡ who are vertically integrating robotics, software, and patented 3D printing technologies to digitize manufacturing and enable faster, more frequent, and lower cost access to space.

We can give here an analogy with transitions in the aeronautical sector. The aviation industry has seen over the past decade that four-engine wide-body aircraft (e.g., Airbus A380) are being replaced with newer cost-effective two-engine narrow-body aircraft (e.g., Boeing 787) over long haul flights, so the above advances in design and manufacture are making these Micro-launchers cost-effective compared with larger launchers. In the aircraft industry, operating a smaller two-engine aircraft more frequently across the routes previously only flown by the larger aircraft due to range and efficiency limitations provides passengers with more opportunities to choose their departure and arrival times. These smaller aircraft have also allowed the airlines to expand their destination offerings by flying the smaller aircraft to destinations not accessible by larger aircraft. This same ongoing revolution in air travel is underpinning the Micro-launcher transitions in the space launch industry.

At present, it is estimated over 100 so-called Micro-launchers are under study or under development. A website, the NewSpace Index, is kept up to date in a dynamic way, listing the different launchers officially announced in publications. 14

A number of the projects are labeled as canceled, retired, or dormant. We can safely assume that the probability of these projects coming to realization is low, if not negligible. More complex is the situation for those projects that are labeled as concepts, in this case the indication on funding levels can be used as an important indicator.

If we consider the potential market for these Micro-launchers, and the need for a sustainable market to justify a serial production, it is evident that only a limited number of them will be able to present a credible business case for investors in the next decade.

A selection of promising or operational projects is summarized in Table 2, whereby again as mentioned before, there is no guarantee that these projects will obtain a fair market share. As a basis to judge the feasibility of these projects, an assessment has been taken into consideration. 15 Note that, to avoid that any sense of preference is expressed, the projects are put in alphabetic order.

List of Private Company Announced or Operational Micro-launchers (Selection)

?, not announced.

An example of a launcher under development is shown in Figure 3.

Artist impression of a Micro-launcher under development (courtesy: HyImpulse).

Note again that this list is not exhaustive and highly speculative; only the near future will prove which of these projects will be successful. As far as performance and prices are concerned, public communications from the different suppliers has been used or is indicated as presently unknown.

To define the different categories of launch vehicles, a similar table, as the one for Smallsats, is proposed in Table 3.

Proposed Definition of Launch Vehicles a

Reference 16

LEO, low Earth orbit, between 160 to 1000 km from Earth.

Note that, as mentioned earlier, the use of the payload capacity mass in LEO of 500 kg compared with 600 kg for Smallsats in Table 1 makes the correlation between Smallsats and Micro-launchers more complex.

Whereas aforementioned larger constellations could use dedicated rideshares due to similarity in orbits, there is still a considerable need for specific Earth Observation and communication-oriented Smallsats to be launched individually, as these require precise orbit injection and an accurate calendar that is not influenced by third parties.

It is generally assumed that Smallsats with a mass over 50 kg could benefit from a dedicated single launch, as the economy of a shared launch is outweighed by the flexibility of a dedicated launch in terms of schedule and accurate orbital injection in accordance with an optimal launch window.

This of course leads to 2 interrelated questions. First of all, it has to be established if the market for single Smallsat launches (hence for the number of Micro-launchers) is large enough to guarantee a production of sufficient launchers to depreciate the development cost of the launcher and the launch campaign offering an acceptable price per launch? For new launchers and launch sites, it is important to distinguish between the cost and the pricing strategy. One difficult factor to estimate in this context is the learning curve factor, 17 which was estimated by the RAND Corporation to be in the 80%–90% range.

This has an immediate effect on the second question, namely can the launcher manufacturers and launch operators assume a target market, which is sufficiently large to be able to offer an attractive launch price from the beginning onward, to be at least competitive with secondary payload launch prices? The importance of this question is linked to the different business models. If we refer to the projects mentioned in Table 2, many are carried out by start-ups that require equity funding. The business models will therefore have to convince the equity financers (in this case mostly Venture Capitalists) that the future market will be large enough to sustain a high launch frequency (say in the order of a minimum of 40 launches per year per operator). Only such frequency can lead to a solid business case convincing risk-averse capital providers. It has to be mentioned here that such high frequency will also allow better planning for the Smallsat operators to reduce waiting times compared with the present ridesharing possibilities as the delays will no doubt be considerably reduced.

A recent development in Europe is related to a public-private partnership approach for Micro-launchers. Both ESA and DLR have launched a competition to select a promising Micro-launcher project. DLR recently selected a short list of 3 projects (HyImpulse, RFA, and Isar). All 3 received a grant to further develop their projects, with the aim to select the most promising project in early 2021. In total, an amount of US$25 million is earmarked as supporting grants. 18

Therefore, the next chapter will be dedicated to estimate the future Smallsat market of satellites with a mass larger than 50 kg, as this mass is considered a threshold for a single launch.

Future Smallsat Launcher Market Assessment

The Smallsat market is very dynamic, and therefore, a number of organizations, specialized in forecasting, are issuing regularly updated reports. A first market survey was based on the number of launches till 2015, so before the more rapid growth of Smallsats potentially compatible with a single launch. Even based on the relatively modest growth till 2017, PWC came to the conclusion that this was still a promising market. 19

A number of recent forecasts were consulted as per references.8,20–22 It is evident from this comparison that the results vary considerably, in particular for the years 2025+. These differences are based on the assumptions made in the respective reports, such as:

The probability that the presently planned mega-constellations will be financed and will be implemented. The final number of Smallsats assumed per constellation (these figures change regularly based on new system design results). The assumption of future constellations, presently only under concept stage. The probability of new applications, as the ones mentioned before, which are not planned yet. The expected lifetime of future Smallsats and the replacement sequence evolving from this. As mentioned earlier, the Smallsat definitions used (in terms of 500 or 600 kg mass), which complicate the comparison between the different reports.

As an example of the rapidly changing environment, we can quote the uncertain future of the OneWeb constellation, which was counted for 648 Smallsats in the aforementioned reports (with presently 74 already placed in orbit). 23 Note that in line with the definitions used in the reports, all figures expressed hereafter refer to satellite masses <500 kg.

Globally, all the reports predict a compound annual growth rate in the order of 14% for a 10-year period, which shows that the market is very promising.

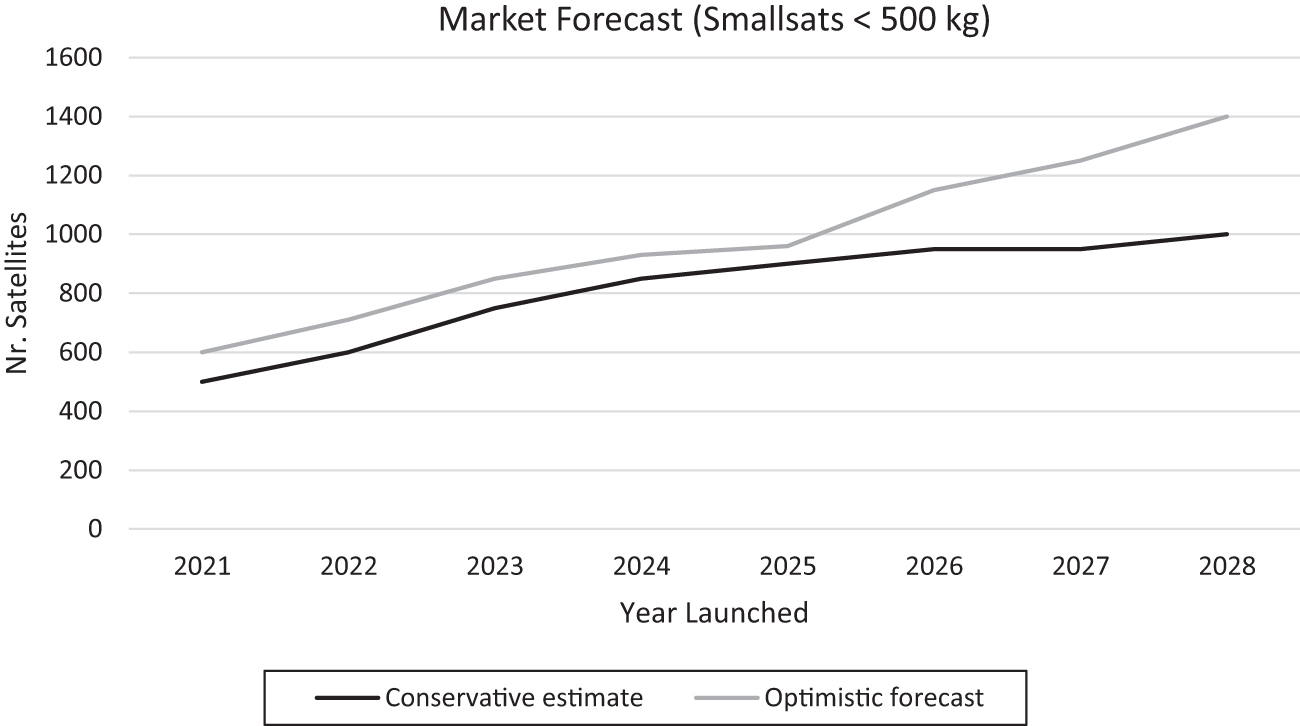

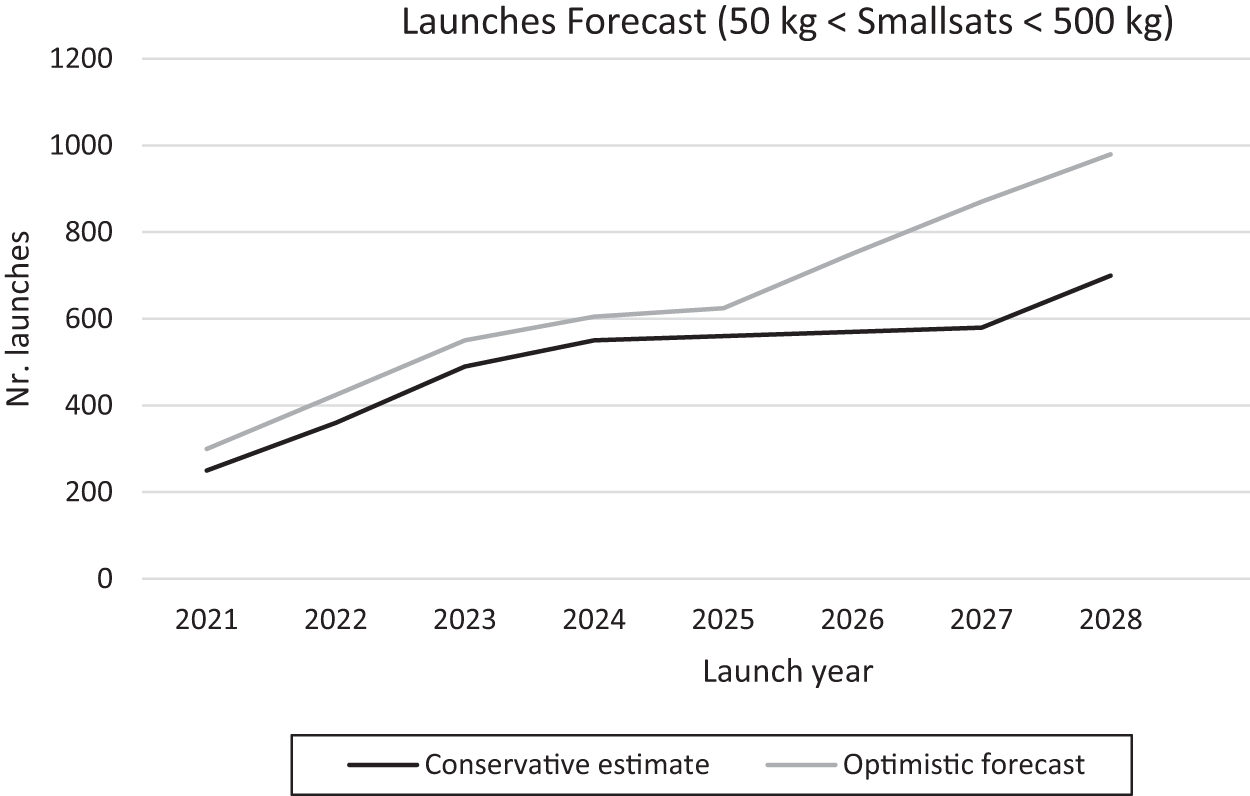

Taking into account the various characteristics of previous forecasts, a conservative (pessimistic) and an optimistic forecast has been deduced in this article as per Figure 4, as a basis for realistic financial revenue data and analysis.

Forecast of number of future Smallsats of <500 kg.

From previously mentioned analyst assumptions, 22 we can deduce that the trend is changing and that the number of satellites to be launched with a mass <10 kg will remain stable, but that there will be a considerable growth in particular in the class of 50–500 kg satellites. Furthermore, based on these forecasts, the class of these satellites can be estimated at 50% of the total Smallsats in 2020 and is expected to grow to some 70% in terms of the number of satellites in this 50–500 kg mass class by 2028.

As shown in Figure 4, the forecasts differ considerably from 2025 onward. The main reason, as mentioned before, is that some analysts take into account new (presently unknown or uncertain) constellations, whereas other more conservative analyses are based on present plans and renewals only. If we further assume that satellites >50 kg will be subjected to dedicated launches, § we can deduce (by interpolating the 50%–70% ratio) that the number of dedicated launches with Micro-launchers will evolve as per Figure 5.

Forecast of number of dedicated launches with Micro-launchers.

Whereas this Figure 5 represents the global market, for each launcher and/or launch operator, the target market will have to be defined in function of a number of parameters such as the payload capacity of the launcher, the orbital constraints linked to the launch site, the attainable market in function of geopolitical and export control constraints, and the number of competitors expected in that specific market segment.

A very paramount factor related to the future use of orbits can be found in Euroconsult. 8 The Euroconsult experts came to the conclusion that soon >50% of the Smallsat launches will use Sun-synchronous orbit (SSO), strongly reducing the number of future Smallsat launches in an equatorial orbit, and as such will become an important market driver. An example of a solution offered, in particular for these polar orbit and SSO, is given in the case study presented in the next chapter.

Note that both in Figure 4 as well as in Figure 5, the data point for 2020 has been suppressed due to present COVID-19 uncertainties, which also heavily influence logistics and travel of specialist to launch sites. The impact of the COVID-19 impact is a factor that cannot be ignored and requires some attention. A recent report on this topic 24 reevaluated the situation and, although some delays are signaled, confirms that a rate of ∼1,000 Smallsats by 2029 is still very realistic, with a market volume of estimated at US$51 billion (from which US$33 billion is for the Smallsats and US$18 billion for the launch activities). An interesting observation in the report is an expected increase in governmental and military Smallsat projects. A potential illustration of this is the participation of the U.K. Government for US$500 million in the OneWeb project. 25 Another report, made by the International Space University, confirms the feeling that the delay will be quickly compensated. 26

Case Study: SL

SL was created in 2017, ** based on an analysis and subsequent market validation that there was a shortage of commercial launch sites that support high-inclination orbits. The founder and early employees herald from previous space companies and Australian Defence research, ensuring that launch operations are conducted using world-class standards and processes. Based on the depth of experience SLs staff have in designing and launching rockets, the company works alongside customers with the goal of minimizing the time it takes to get a customer's rocket onto the launch pad and into space. Hence, every aspect of, process for, or procedure at SLs sites are developed to ensure that a NewSpace operator can minimize the effort required to maximize the payload to orbit and profitability of their company.

Finding an optimal location for a new orbital launch facility is not a simple task as a modern, safety first, site requires an unhindered downrange distance of ∼3,000 km. Coupled to that requirement is the fact that as the payload masses of NewSpace launch vehicles are low, these new rockets must follow a direct ascent profile to orbit to realize their full market potential. Any dogleg maneuvers to fly around populated areas, infrastructure or delicate marine environments, force the rocket to burn more fuel and reduce the payload mass the rocket can carry. Furthermore, locations closer to the equator pose significant efficiency challenges to launching into high-inclination orbits as the rockets must burn additional fuel to fly into the Earth's spin direction to cancel out the Earth's rotational velocity imparted on the rocket at launch as this rotational velocity is perpendicular to the desired orbit plane. This final point is a clear fact why equatorial launch locations are less economical to operate out of for NewSpace rockets aiming for high-inclination orbits.

An important economic side effect to be noted here is the prospect of activities and employment opportunities for the (indigenous) local population, besides the fact that this can be considered as a revival of Australian launch experience, which was well known in the 1950s and 1960s at the Woomera range, which is in the same area. It is therefore evident that the project attracts lot of attention in the local press. 27

As described prior, a key market component for NewSpace rockets is the reconstitution of satellite constellations. Under these missions, the launch vehicle must be able to be launched with surgical precision and do so frequently. Maritime and air traffic density through the range as well as weather conditions have a major effect on operations and launch window availabilities. Potential launch locations with heavy air or maritime traffic in the area could face future opposition from airlines and shipping companies as frequent rocket launch operations could create large-scale disruptions and drive up costs for air and maritime operators.

An excellent location that realizes a maximum of these boundary conditions can be found near the regional city of Port Lincoln in Southern Australia close to the headquarters of the Australian Space Agency in Adelaide. Known as the Whalers Way Orbital Launch Complex, this site is very well suited for unobstructed and optimal launches to inclinations between 60° and 110°, as shown in Figure 1.

The site encompasses >6 km of southward ocean frontage and is connected via an existing network of roads across the site. Being just a 35-min drive from Port Lincoln and with excellent year-round weather, the site has unique access and launch window flexibility.

The initial launch site infrastructure has been designed based on 3 key elements:

A multiuser launch pad from where the rocket is launched. The Vehicle Assembly building. A Range Operations Center.

Over time, the infrastructure at the site will be expanded upon to include multiple launch pads to support a variety of launch customer requirements and rocket sizes.

Stage Preparation and Payload Processing functions are to be provided from the nearby regional city of Port Lincoln. As most of the time before a launch is spent undertaking engineering checks and inspections of the hardware, the launch vehicle operator can reduce costs through the following means:

The workforce can be conveniently located close to their primary work location reducing commute times. Replacement parts for defective components can be expedited to Port Lincoln using existing, high-capacity logistics infrastructure reducing “replacement part” delays. Port Lincoln has a vibrant existing tourism industry infrastructure ensuring the standard of accommodation for all employees is high, while the cost of living is relatively low. The regional city is directly serviced by numerous commercial airlines multiple times a day simplifying staff and dignitary movements between the launch site and the rest of the world. The existing deep water port at Port Lincoln, and future bulk commodities port at Cape Hardy 50 km north of Port Lincoln, support containerized goods landing near the site simplifying the transport of goods to location.

It would therefore be conceivable for high-frequency launch vehicle operators to station permanent employees within the area and integrate their staff into the fabric of the local community. This would further reduce international commute costs and increase overall staff satisfaction levels. It is only when the flight vehicle and payloads are ready that the components are then moved on to Whalers Way for final stage assembly, fueling, and launch.

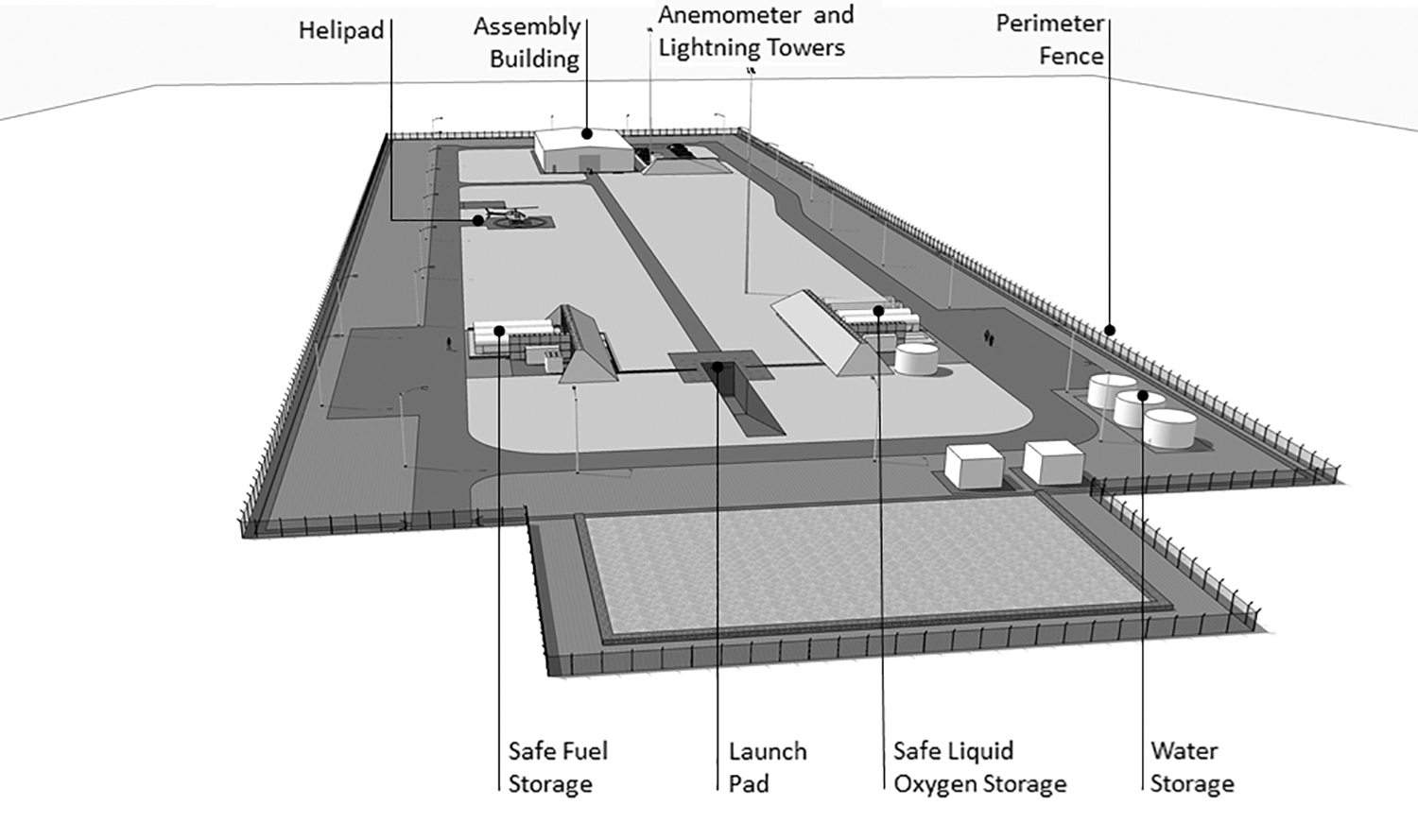

The overall architectural design of the first launch site is shown in Figure 6 showing a Vehicle Assembly Building located a safe distance away from the Launch Pad. This image shows a mid-sized vehicle assembly building and separate fuel and oxidizer storage facilities.

Architectural sketch of SL facility (under construction) (credit: SL).

The flight prepared stages and payload assembly arrive by vehicle to the Vehicle Assembly Building where the final preflight checks are undertaken. Once the stages are mated horizontally, the assembled vehicle is moved out to the launch pad. A rocket specific launch pedestal is bolted to the launch pad and used to support the rocket pre-launch. The launch pedestal also provides the interface between the provided power, communications, propellant, and water deluge systems. Larger vehicles are supported using the excavated flame trench and augmented water deluge system designed to reduce acoustic loads on the vehicle during launch. Once all final checks are completed, the Launch and Range Control located within the site boundary provide the authorization to launch. The higher level Mission Control function is either operated by the customer from their chosen site or from SLs facility located in Adelaide.

After a launch event has been concluded, secure storage is located at the rear of the site to further reduce the time required to demobilize the site, increasing profitability for the launch vehicle operator.

Over time, up to 6 of these launch facilities can be located on the site to satisfy the different launcher prerequisites. Different sites will be configured to match the requirements associated to a particular launcher, or class of launchers with specific needs such as supply of propellant types, or a different launch pad infrastructure. Ultimately, the construction of multiple pads allows for multiple companies to be simultaneously preparing for launch at any one time.

The advantage of this concept and the location, in comparison with a number of other launch projects under development, can be summarized as per a number of distinct features, listed hereafter:

Optimal launch windows can be guaranteed by minimal air and maritime traffic restrictions, excellent year-round weather conditions and easy site access. Very low local population density ensures the safety and security of the launch site and the operations onsite. Direct injection to orbit, thanks to the possibility to have direct ascent trajectories to orbit, without the need to overfly populated areas, infrastructure assets or delicate marine environments (as previously mentioned avoiding fuel-consuming “dogleg” maneuvers). Access to orbits in a first pass, increasing the probability to reach the desired orbit, at the same time enabling early satellite system checking soon after launch. Highly accessible launch site, close to the regional city of Port Lincoln with existing heavy industry, excellent wharf facilities, a commercial airport with multiple flights per day and vibrant tourism industry. Geographically secure, in a country with excellent border controls and a launch site with open ocean access. Availability of an overland rocket Test range, the complementary Koonibba Test Range is part of the SL offering. Located near the regional transportation hub of Ceduna along the Far West Coast of South Australia, the range is purpose built to support suborbital rocket and satellite subsystem testing. With >10,000 km2 range area, the site allows downrange flights of up to 145 km.

Note that this Koonibba range also allows for an interesting experimental military program, which is under development, namely rapidly launching payloads to allow observations of a relatively short distance but beyond the line-of-sight for observations. 28 It will also be very useful for incremental early trajectory test launches of the different Micro-launchers presently under development.

The feasibility of this project has been critically evaluated in an independent study,

29

which came to the following conclusion:

The role that NewSpace will play in pursuing this access is significant; the market survey indicates that the Smallsat market is increasing in size across the space business sector and will continue to do so. A case study of Australia had identified considerations for nations looking to encourage NewSpace launch companies, from infrastructure requirements to potential changes. From the case study, the team has concluded that Australia has potential to develop launch capability and would be well suited as a launch state within the framework.

An overview impression of the operational Whalers Way global site is presented in Figure 7, whereby it has to be mentioned here that SL has no exclusivity constraints and is flexible to accommodate different launchers from different countries, thanks to the export control neutral position of Australia. The potential location of different launch pads on the site is indicated in this figure.

Overview of 4 potential launch pad locations at Whalers Way (credit: SL).

Conclusions

Historically launch vehicles have been built to service large satellites in GEO orbits, and as such, launch sites have been built close to the equator to optimize operations and trajectories getting into low-inclination orbits. NewSpace Smallsats fly constellations to gain global coverage and increasingly use COTS technologies to reduce costs. Launching constellations requires access to high-inclination orbits such as polar or Sun-synchronous ones, an emerging market demand underpinned by recent NewSpace trends, as predicted in the recent report of a leading Smallsat expert. 9 As Smallsats transition away from tech demonstration into commercial utilization, the number of Smallsats being developed with a mass between 50 and 500 kg is rapidly increasing. Traditionally, Smallsats were launched as secondary payloads, but this launch option is less and less compatible with NewSpace companies favoring fast and timely launch turnarounds. To have a flexible and independent launch window, and to have a more accurate orbit injection, NewSpace Smallsat operators are increasingly in favor of dedicated launches, which make them independent from the (schedule) constraints often imposed by the primary payload.

With the objective to evaluate the market potential for such dedicated Micro-launchers, this article has tried to assess the growth in the Smallsat market over the next decade. Assuming that Smallsats with a mass of >50 kg have an increasing tendency to be launched with a dedicated launcher, a deduction has been made on the potential for those Micro-launchers and the number of launch opportunities. Based on a number of assumptions, the number of dedicated launches is estimated to grow to some 600 yearly over the next 5 years, with a growth potential between 700 and 1,000 launches per year within a decade.

It is of high importance to note at this point in time that the COVID-19 pandemic surely has caused a temporarily shift in the launch activities, but most analysts are convinced that this delay will be compensated in the near future to reach the aforementioned predicted launch sequence up to 1,000 launches yearly. Although such figure looks high at present, it is certainly compatible with the planned constellations of Internet-from-space providers, requiring networks of several hundreds, even thousands of Smallsats. It is also worthwhile mentioning that many organizations such as DARPA, ESA, and DLR are presently actively supporting technologies and young start-ups to develop Micro-launchers, which will certainly lead to reduced launch costs for dedicated launches.

In addition to an affordable launch cost, the location of a launch site plays a paramount role. In particular, for high-inclination orbits (estimated by analysts to be applicable for >50% of Smallsats in the coming years), an unobstructed direct orbit injection provides the highest efficiency. Linked to a minimal interference with air and maritime traffic, an example of launch opportunities in Southern Australia is described. It is also important to mention that the limited interferences will help considerably in respecting launch dates and reduce launch delays, which is at present an important issue for Smallsat operators.

Footnotes

Acknowledgments

Southern Launch acknowledges and thanks the Australian Space Agency and the South Australian State Government for their leadership in the Australian space environment and ongoing support to the emerging Australian industry. Southern Launch also thanks Regional Development Australia Whyalla and Eyre Peninsula and the communities of Lower Eyre and Far West Coasts of South Australia for their ongoing support and encouragement for the development of the facilities.

Author Disclosure Statement

No competing financial interests exist.

Funding Information

No external funding was received. This study was privately funded by Southern Launch.