Abstract

Given the significant volume of capital that will be required to develop the space resource industry, it is important to understand the fundamentals and drivers of funding in this growing industry. This article distills a series of 30 interviews with individuals representing different aspects of the space resource funding ecosystem—including entrepreneurs, corporate employees, brokers, academics, government and agency personnel, investors, and advisors—to examine and report on the current state of space resource sector funding, including identifying key partners and examining current regulation and legislation. The results of this research are intended to be used as a lens through which to understand the current state of funding within the space resource sector and to help observers interpret certain actions on the parts of individuals and companies operating in the industry.

INTRODUCTION

Outer space, with its many unique features, serves as an ideal incubator for the development of diversified commercial activities such as space launching, space tourism, remote sensing, telecommunications, small satellites and, importantly, space mining and the development of space resources, 1 whether it be on asteroids or the surface of the Moon.

Furthermore, resources from the Moon, Mars, and certain asteroids have been proposed for use in human space exploration to produce propellants, water for life support, structural materials, and radiation and heat shielding.2(p1–6) These asteroids in particular present the possibility of a vast source of minerals, free from environmental or land use restrictions. A dream of science fiction for decades, recent developments in the areas of robotics, autonomy, artificial intelligence, and, most notably, reduced launch vehicle costs, now place space resource development within technological and cost-effective reach.

This research examines the current state of funding of space resource industries, including a summary of the current international and national space resource legislation that is in place.

The scale of this opportunity is enormous. The Space Project Team of the Organization for Economic Co-operation and Development International Futures Program (IFP) determined that future demand for commercial space applications is likely to be substantial. They presented three likely scenarios, with different geopolitical, socioeconomic, and energy and environment characteristics. Using the three IFP scenarios for Space 2030 and the presented cost of access to space, this research determines the potential impact, for the U.S. economy, of the change in final demand of the space value chain. The IFP estimates encompassed an 18%–40% growth for the industry from 2004 to 2030. 3

This estimate is a conservative one, as Morgan Stanley estimates that the industry will be worth more than USD 1 trillion by 20404,5; and, in 2021, the Space Foundation found that by 2020, the global space economy had risen to USD 447 billion, an increase of 4.4% from $428 billion in 2019, and of 55% from a decade ago. Commercial space activity grew 6.6% to nearly $357 billion in 2020, representing close to 80% of the total space economy. 6

Historically, funding for space projects has come at the expense of the public purse, whether in the United States, Russia, China, or any other country involved in space activities. However, the funding model for space projects is changing, with increased participation by the private sector.

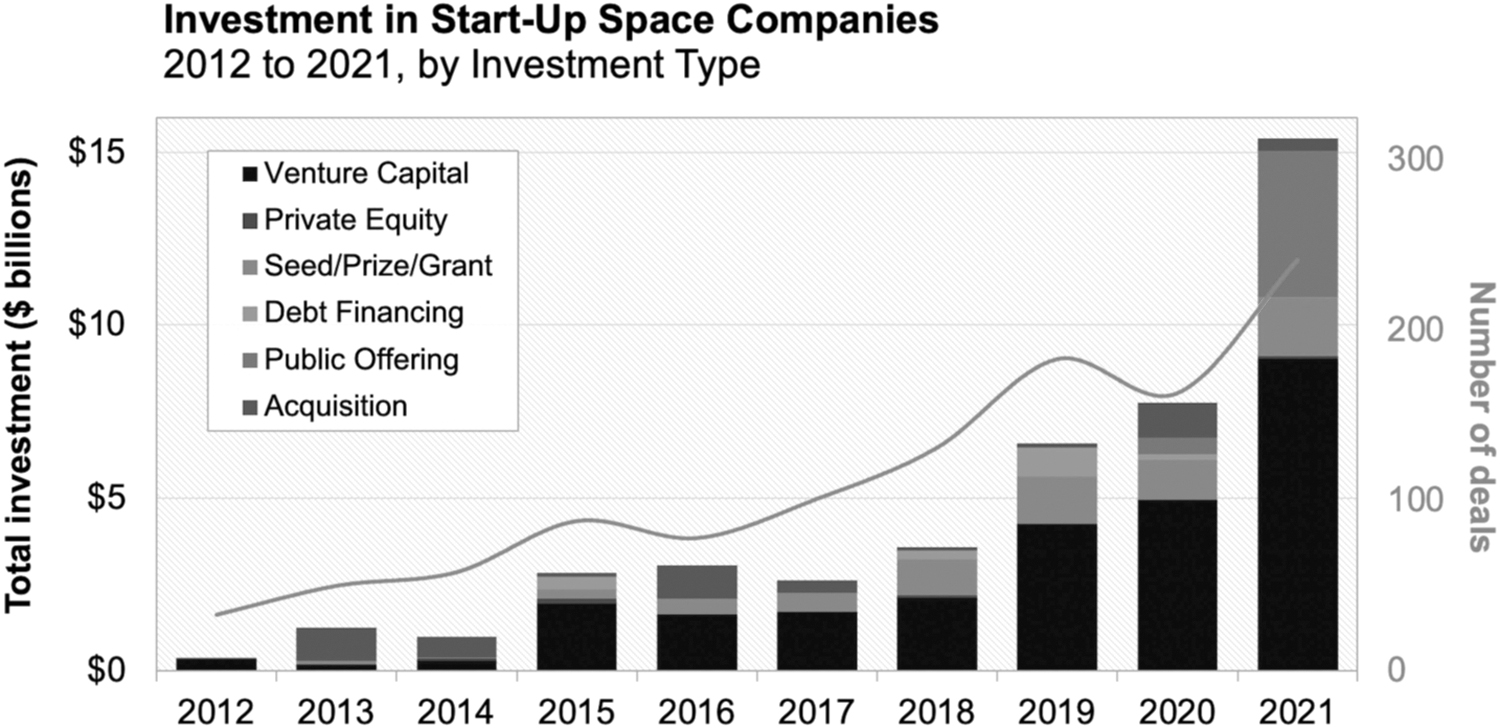

As illustrated in the Figure 1, investment in start-up space companies has increased significantly since 2012, through a variety of investment types.

Investment in start-up space companies (BryceTech 32 ).

Following a literature review, the author concluded that there is a dearth of research regarding the sources and effects of, and a general lack of understanding regarding, the funding ecosystem that is currently developing to support the exploitation of space resources. Relevant research includes studies by Atkins, 7 DePagter, 8 Foster, 9 George, 4 and Masson-Zwaan and Richards 10 ; however, these articles tend to focus more on the international and legal ramifications of space resource activities rather than how the industry is funded. Information on funding of space resources is more often found outside of academic research journals and is reported, rather, by commercial parties such as the Space Capital investment fund and consulting contractors such as Bryce Tech, Euroconsult, and others.

This lack of relevant academic research is understandable due to the relative newness of the industry. However, given the significant amounts of capital that will be required to develop the space resource industry, it is important that researchers begin to examine drivers of funding for space resources.

This research focuses on examining and reporting on the state of the space resource industry, in general, and how it is funded, in particular. It includes a review of the funding partners involved and the effectiveness of the regulation and legislation currently in place. Questions such as “What are the biggest opportunities in the space resource sector,” “what are the biggest challenges in terms of funding in the space resource sector,” and “who should regulate funding in the space resource sector?” do not lend themselves easily to experimental or statistical analysis, particularly when the number of studies on the subject is still small. To this end, it was decided to approach expert respondents in the space resource industry to aggregate an understanding of the state of funding within the sector.

Although a significant sampling of experts was selected for this research, it is by no means exhaustive. This article is intended to highlight key themes, pinpoint differences, and identify shortfalls that may exist within the current funding structure of the space resource sector. Following from this research are various further opportunities to build on these findings, such as conducting additional interviews within a specific subcategory of expertise, or using the findings to augment a study of empirical data.

METHODOLOGY

The findings discussed in this article are derived from an interview-based study of space resource industry funding. As such, it is informed by the knowledge and expertise of individuals identified due to their involvement within some aspects of the industry. In developing the methodology for this research, the author leaned heavily on the framework published by Dejonckheere. 11

An interview structure was chosen for this research, as interviews are an accessible, affordable, and effective method to understand the socially situated world of the research participants. 12 All interviews were semistructured, typically consisting of a dialogue between the researcher and participant, guided by a flexible interview protocol and supplemented by follow-up questions, probes, and comments. 11 Interviews were conducted using standardized questions. A semistructured interview style was chosen, as qualitative semistructured interviews use verbal communication, mostly in face-to-face interactions, to collect data on participants' attitudes, beliefs, and experiences. 12

Out of the total 30 interviews, 27 were conducted via Zoom, allowing the author also to observe respondents' facial expressions and body language. Interviews were recorded and transcribed for reference while compiling data. Each interview was scheduled for 1 h, during which the interview sought to keep the discussion to the allotted time; however, respondents who wished to elaborate further were allowed extra time to complete the discussion and convey their responses appropriately. No follow-up questions or sessions were used with any of the respondents. Each respondent was asked to reconfirm their willingness to be acknowledged in this article and, if interested, to review a draft. No revisions were requested following this review.

The remaining three interviews were submitted as written responses, as no convenient time slot could be found to connect via videoconference. Each respondent was provided in advance with a list of standardized questions, so that the interview could be carried out most efficiently; however, the interviewer was permitted some leeway to expand further on relevant topics and viewpoints. In addition, respondents were asked to provide their qualitative views and opinions, consistent with the approach of a semistructured interview.

Interviews were conducted over a period of ∼1 month, during February 2023, such that all respondents shared a comparable frame of reference with regard to time when commenting on the state of funding for space resources.

It was originally planned to interview more than 50 relevant individuals and requests for interviews were sent to more than 90 potential participants. This target number was set to ensure that the number of people interviewed in each category and professional role was sufficient, such that reserves would be in place should any individual decline to participate or be prevented from taking part. 13

As expected, in several instances, potential respondents declined due to time constraints or work restrictions and in one instance because the author was based in Hong Kong, for which the individual's employer declined to approve the individual to participate.

After successfully carrying out thirty interviews, the author concluded that the data set had reached theoretical saturation—or, as Glaser and Strauss 14 put it, “the point in grounded theory analysis where collecting and analyzing additional data does not teach you more about your topic.”

DATA COLLECTION

The sampling strategy used in this research was selected to identify relevant individuals within the author's personal network, as well as key companies from which relevant individuals within those companies might be identified and contacted. In addition, following the formal interview, each respondent was asked “if there was anyone else I should speak further to on this topic?” This created a snowball effect, a popular sampling method through which researchers begin with a small number of initial contacts (seeds) who fit the research criteria and are invited to become research participants. 15 This snowball sampling strategy helped maximize the pool of interview candidates for this study, both in quantity and in quality.

In total, 30 people were interviewed, representing different aspects of the space resource funding ecosystem. These included entrepreneurs, corporate employees, brokers, academics, government and agency personnel, investors, and advisors. Within these categories, interview subjects held a wide range of positions, including CEO, department head, consultancy partner, law firm partner, head of business development, and professor.

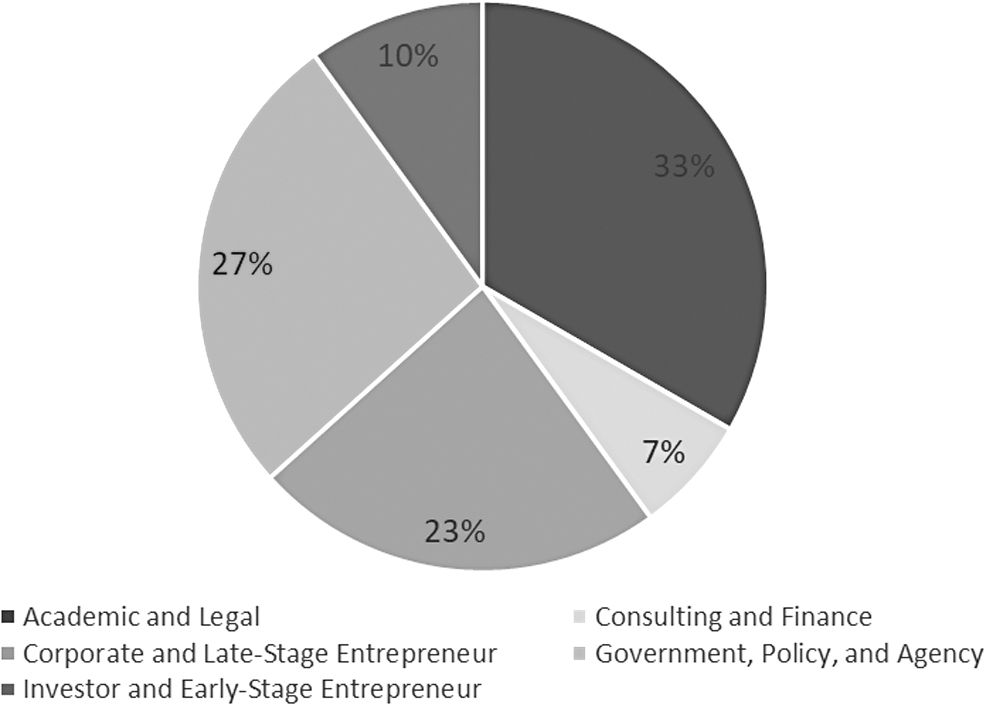

This sampling strategy was designed to capture a range of different organizational contexts, and to pinpoint similarities and differences between the study respondents' answers. Respondents were thus categorized into the following five broad categories: Academic and Legal; Consulting and Finance; Corporate and Late-Stage Entrepreneur; Investor and Early-Stage Entrepreneur; and Government, Policy, and Agency, with the common thread being active participation in the space resource industry as illustrated in Figure 2. The wide range of respondents helped to ameliorate the problems of information gaps and personal biases, as expert testimony is inherently personal and not necessarily representative or replicable. 16

Professional breakdown of respondents.

The Academic and Legal category comprised professors and lawyers; in certain cases, respondents occupied both roles. The Consulting and Finance category comprised respondents actively involved in providing advisory services to space resource industry companies and agencies. The Corporate and Late-Stage Entrepreneurs classification comprised respondents who worked in companies with recurring cash flow and/or funding beyond “Series A”; while Investor and Early-Stage Entrepreneur respondents were either active investors in the space resource industry, typically investing in early-stage companies, or entrepreneurs active in the industry but at an early stage of company development. Placing respondents into one of these two categories entailed a degree of subjectivity. The Government, Policy, and Agency category comprised politicians and civil servants directly involved in formulating the space resource policy, individuals employed by a country's sovereign space agency, and/or individuals involved in the development of a government's space resource policy, either nationally or internationally.

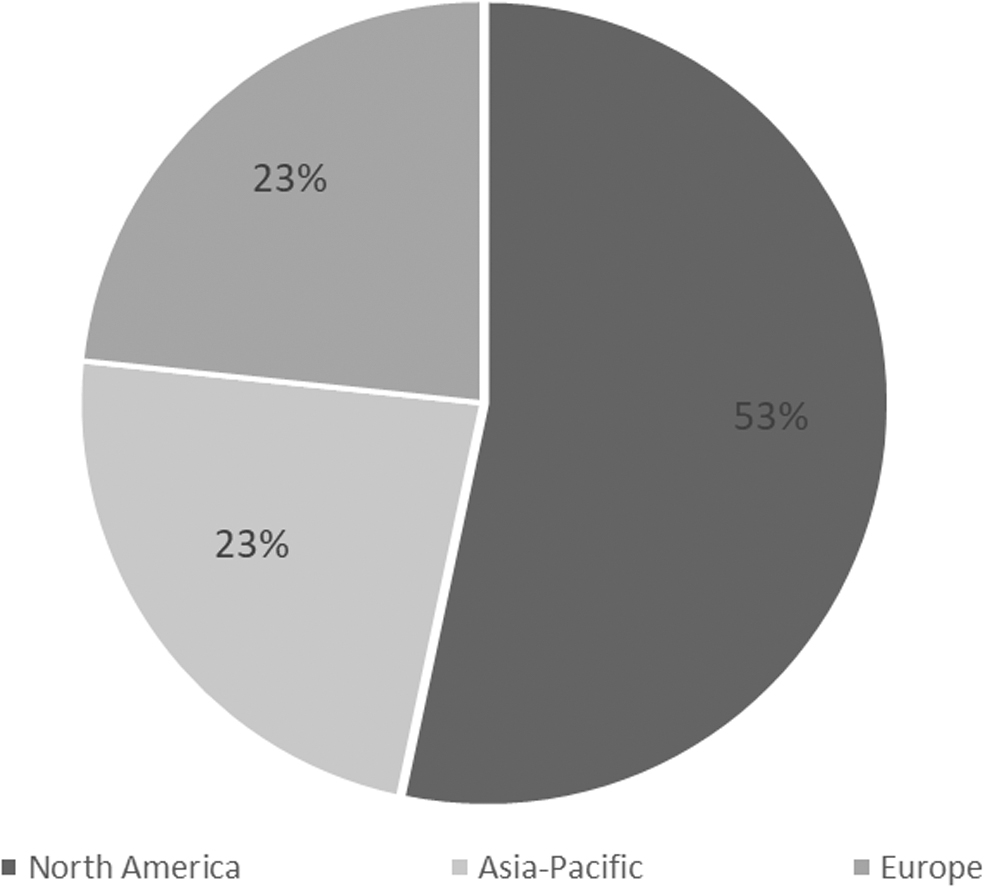

Geographic profiles of respondents were dispersed globally (Figure 3), with ∼50% of respondents based in North America, 25% in Europe, and 25% in the Indo-Pacific region (including Australia). This breakdown is also reflective of the dispersion of space resource funding (more about this below).

Geographic breakdown of respondents.

It is important to note that certain prospective respondents associated with multinational banks declined to participate in this study due to restrictive compliance regulations and concerns around proprietary strategy. In addition, certain other prospective respondents declined to participate citing security concerns related to the author's physical location in Hong Kong.

All the respondents agreed to speak in the understanding that although they are associated with organizations that are relevant to the development of space resources, the opinions they expressed are their own and do not reflect the positions of the organizations that they work for.

All respondents consented to the listing of their names in the publication. A list of research participants' roles and organization type can be found in Table 1 below. This research was deemed to be exempted from Human Subjects Research Approval by the Institutional Review Board (IRB) of the Colorado School of Mines.

List of Research Participants

DEFINING SPACE RESOURCES

Under U.S. law, space resources are defined as “any tangible or intangible benefit which can be realized only from (A) aeronautical and space activities; or (B) advancements in any field related to space” 17 ; and by the Hague Working Group as “extractable and/or recoverable abiotic resource[s] in situ in outer space.”18(para2.1) However, as interviews progressed, it became apparent that respondents in the space resource industry are not just heterogeneous in terms of background but also in how they approach the industry. The third question posed to respondents, following those regarding name and occupation, was: “How do you define space resources?” The basis of the respondent's answer to this question set the direction for the rest of the interview. However, in the responses to this question, there was but little repetition. As one respondent observed, “the scope can be quite large!”

The broadest similarity observed in the respondents' answers was in the use of key terms: for example, value, use/usability, consumable, extracted/extraction, minerals/materials/metals, and capture.

More than half of the respondents conflated space resources with In-Situ Resource Utilization (ISRU). When asked to elaborate and, if necessary, expand their definition, most respondents expressed the belief that space resources are focused on usable minerals and materials of value that are extracted from celestial bodies. There was limited consensus among respondents as to whether the definition of space resources includes resources returned to Earth for terrestrial consumption or resources consumed exclusively in space or both.

The second-most common definition of space resources was sufficiently expansive to include power beaming, data, and gravitational resources such as Low Earth Orbit (LEO), Geosynchronous Earth Orbit, and space debris. Significantly, one respondent specifically excluded space debris from a broader definition because, in his view, space debris should be regulated differently than space resource development and exploitation.

Of significant note were the definitions posited by respondents associated with large terrestrial mining interests. Such companies are making significant investments in space resources, but for purposes of definition, these respondents characterized space resources as a research and development opportunity, through which space and research on space resources might be adapted and exploited to advance terrestrial mining.

In addition, certain respondents preferred to direct me to published definitions such as the U.S. Commercial Space Launch Competitiveness Act, of 2015, in which a space resource is defined as “an abiotic resource in situ in outer space” 19 ; or to the Hague Building Blocks, in which it is defined as “an extractable and/or recoverable abiotic resource in situ in outer Space” that includes mineral and volatile materials, including water, but excludes (a) satellite orbits; (b) the radio spectrum; and (c) energy from the Sun, except when collected from unique and scarce locations. 18

Respondents' definitions also reflected professional biases: economists looked at the economics of space resources, mining professionals considered the mining potential, and lawyers focused on the legal aspects and ramifications of defining space resources. Although, among this broad selection of industry respondents, there was little coherence as to a single definition of space resources, this result is likely reflective of the nascence of the industry and the opportunity it entails—a sentiment that was universally shared by respondents.

A similar ambiguity in the definition of space resources is reflected in a series of articles and editorials in the journal New Space that seeks to define new space and commercial space, of which space resources are a subset. An author's note in one editorial states succinctly: “The definition of space market ‘segments,’ ‘sectors,’ or ‘domains' is somewhat arbitrary, and could include Earth observation, satellite communications, space science, security, satellite navigation, human spaceflight, space manufacturing, and debris removal.” 20

As noted earlier, survey respondents' definitions of space resources influenced their responses to the subsequent questions. In addition to recognizing the significant fact that there is little consensus on how to define space resources, for the purposes of this article, we define a space resource broadly, as a material or commodity located in space that is exploitable and has a value to humankind.

CURRENT STATE OF THE SPACE RESOURCE INDUSTRY

Initially, respondents were asked for their impressions of the space resource industry via these three questions:

i. What do you think are the greatest opportunities in the development of the space resource sector?

ii. What do you think are the biggest challenges in the development of the space resource sector?

iii. Which countries do you think are doing a good job promoting the development of the space resource sector?

Unlike the previous question on definition, here the responses exhibited significant similarity or conformity, across all the respondents' associated industries.

Greatest Opportunities in the Space Resource Industry

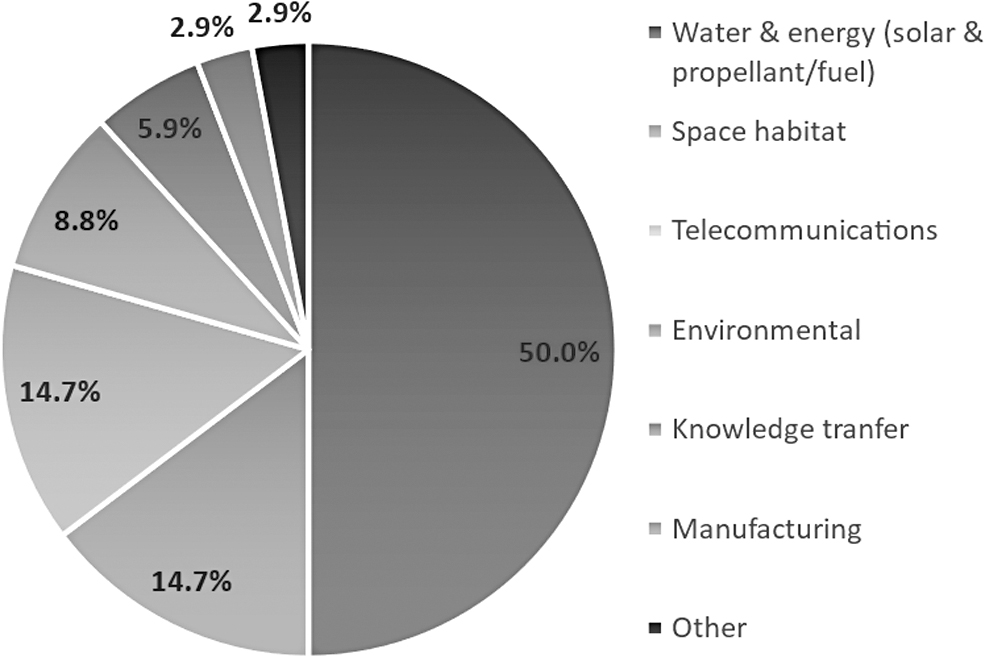

As seen in Figure 4, respondents leaned heavily toward the view that water extraction and energy production represent the greatest near-term opportunity in space resources. This includes energy collection for beaming power back to Earth (as highlighted by three respondents) as well as creating energy, propellant, and fuel primarily from the extraction and hydrolysis of water.

Opportunities in the space resource industry.

After water and energy, the next-most popular space resource opportunity was split between human habitation in space (primarily on the Moon but also in Cislunar space) and telecommunications.

Environmental opportunities included the following: “using space resources and ISRU to lessen the impact of launches on Earth”; mining and disposing of space debris; and “lessening environmental degradation on Earth through mining in space.” These answers, similar to the others, tended to reflect the respondents' various biases and roles.

In the author's view, the category of knowledge transfer was perhaps the least expected and the most interesting. This category was raised by respondents associated with large terrestrial mining corporations, as representing not only a near-term opportunity but also one that is, in fact, currently being exploited.

These mining companies are looking to their activities in space to provide greater knowledge and efficiency for their terrestrial mining operations. It is this capture of value through knowledge transfer that helps maintain these companies' interest in developing space resources.

The final categories were manufacturing, which many respondents saw as a longer term opportunity (compared with water and energy, for example); and other, the choice of respondents who saw the greatest opportunity in space resources as a means for inspiring interest among young people in science, technology, engineering, and mathematics education.

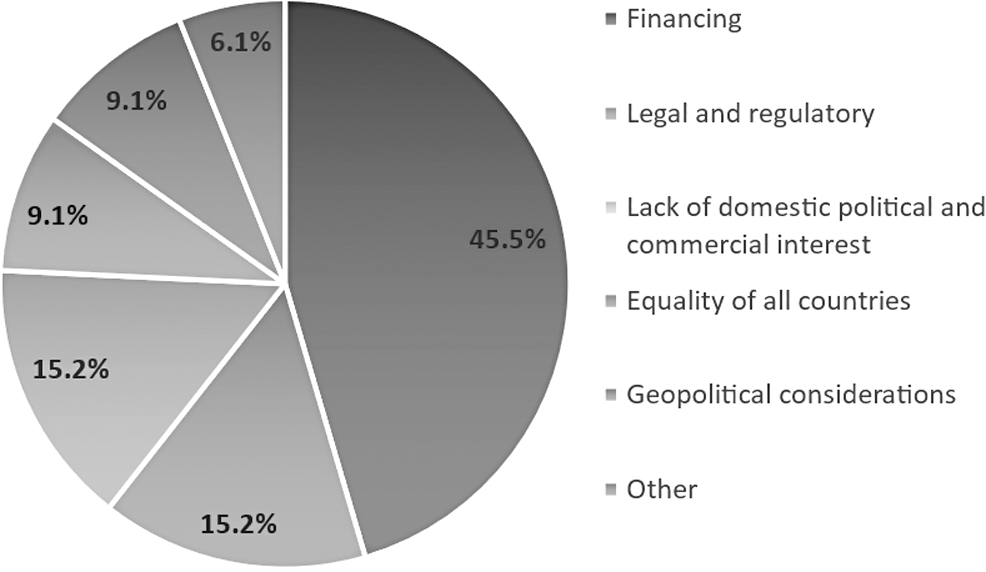

Greatest Challenges in the Space Resource Industry

When asked to describe the greatest challenges facing the space resource sector, participants responded with a dominant theme: financing. Primarily, respondents expressed the feeling that the sector faces a dearth of capital investment, but they also noted misalignment in the funding cycle (i.e., investors expect return before the sector can realistically deliver economic results), the inability of investors to understand and price risk, the lack of an established commercial market, and a perceived lack of commerciality.

After finance, respondents identified legal and regulatory challenges, including the perceived lack or inadequacy of both, and expressed concern that the space resource industry cannot be enjoyed and exploited by all countries—not just the “rich” countries—evenly and equitably.

The current geopolitical environment was also raised as a concern, as were two unique responses under the other category: the viability of development in LEO due to space debris and the viability of returning resources to the Earth.

It is worth noting that no respondent mentioned technology as one of the space resource industry's greatest challenges. Figure 5 visually represents the breakdown of the respondent's views on challenges in the space resources industry.

Challenges in the space resource industry.

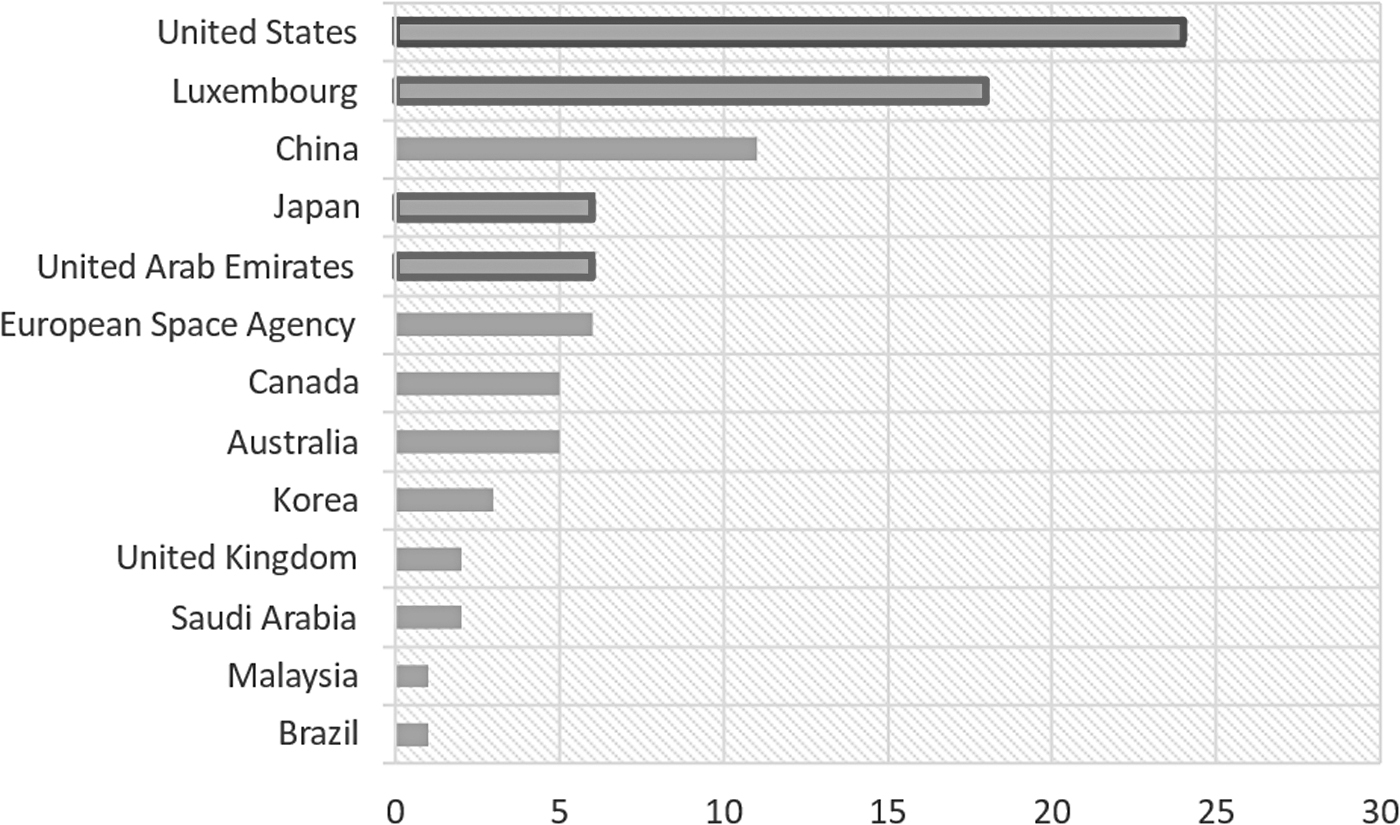

Countries Actively Supporting the Space Resource Sector

The Figure 6 records the number of mentions by respondents when asked which countries were the most supportive of the space resource industry. Each respondent was allowed to name, however, many countries they believed were supportive; in most cases, respondents would mention two or three. The United States, Luxembourg, the United Arab Emirates, and Japan are marked with red dashes, as these countries have enacted legislation and/or legal frameworks related to space resources in some form or another.

Respondents' attitudes regarding countries supporting the space resource industry.

It is evident that, in the opinion of the respondents, the United States is clearly the country that is the most supportive of space resources. When asked to elaborate, many respondents replied that this is because of the sheer size of the U.S. economy, and also because of its Commercial Space Launch Competitiveness Act, of 2015.

Following the United States was Luxembourg. In 2016, Luxembourg enacted a draft law to create a legal framework for space resource companies to operate in that country. Shortly thereafter, in July 2017, Luxembourg became the first European nation to provide a legal framework for the utilization of space resources. Many respondents also believed that Luxembourg was the best promoter, among the world's nations, of space resources as an investable industry.

Rather than name individual European countries, respondents often identified the European Space Agency as a supportive entity. Also, quite interestingly, Canada and Australia were also mentioned often. These mentions were always made in the context of strong crossover and support on the part of the both countries' significant terrestrial mining industries. Responses are shown in Figure 6.

Another key observation was the location bias inherent in these answers. Respondents would invariably mention the country or region in which they resided as being one of the countries most supportive of the space resource industry; but it also became apparent that many Western-based respondents would not mention China, or would mention it only as an afterthought. When pressed on this, respondents suggested that they had limited exposure to China's activities in the space resource sector, outside of what appeared in the media, and, as such, did not think of China as a particularly active supporter of space resources.

FUNDING OF THE SPACE RESOURCE INDUSTRY

Following these general questions on the state of the space resource industry, respondents were asked to share their opinions and insights on the state of funding for the space resource industry. Specifically, they were asked the following:

i. What is your current position on whether or not the sector is adequately funded and the state of the ecosystem at present?

ii. Where do you think the majority of funding for the space resource sector is currently coming from (private sector, public sector, etc.)?

iii. Where do you think the primary funding for the development of space resources should come from in the future?

iv. Where are the biggest opportunities for funding the space resource sector?

v. Where are the biggest challenges for funding the space resource sector?

vi. Which country or geography do you think is the most supportive financially of the space resource sector? Does that change if separating private versus public support?

Respondents were also asked their views on success stories in regard to space resource sector funding, but it was found that respondents were unable or unwilling to answer this question or that there was no learning or theme that could be extracted from the respondents' answers, and it was decided that those responses were not relevant to the findings of this article.

As the interviews progressed, it became apparent that respondents were quite comfortable discussing the space resource sector in general; however, when questioned more granularly on funding, respondents' answers were (perhaps intentionally) vague, or else they chose not to answer due to a lack of familiarity with the topic. The quality and insight value were significantly lower for these more specific responses than for the respondents' observations about the industry in general. This supports the thesis that although funding is an integral part of any commercial industry, in the nascent space resource industry, it is not yet well understood.

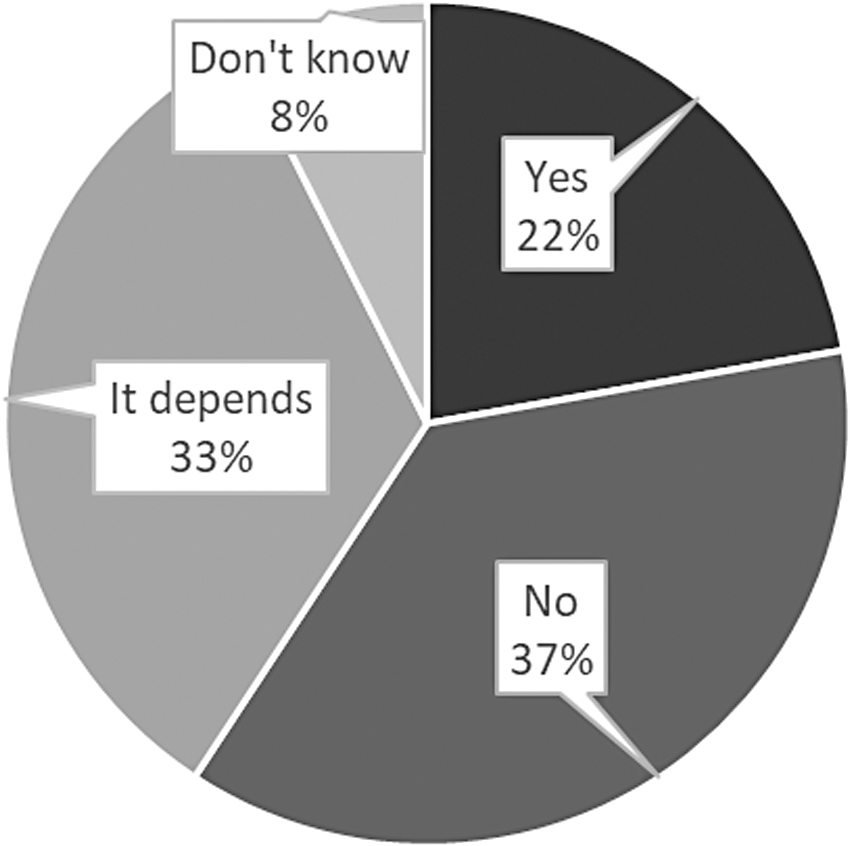

Funding Level and State of the Ecosystem

Asking respondents' opinions on whether the space resource sector is adequately funded did not elicit simple yes or no responses. The answers generally fell into four categories—an emphatic “no,” a soft “yes,” or “it depends,” or “don't know.” A respondent declining to answer was also noted. These responses are shown in Figure 7.

Respondents' opinions on whether the space resource sector is adequately funded.

The true value of these responses was to be found not so much in the initial answer as in the nuance and insight that accompanied that answer. Asked why they arrived at their conclusion, respondents' answers were entirely distinct; as such, when taken as a whole, the responses amount to an impressive mosaic of knowledge regarding space resource industry funding and underline the nascent and disorganized state of the industry. Table 2 details the various elements of this insight.

Summary of Responses Regarding Funding Level and State of Space Resource Ecosystem

Funding Sources for the Space Resource Sector

Respondents were then asked their opinion on where the majority of space resource sector funding is currently coming from (e.g., public sources, private sources, other) and where it should come from in the future.

Regarding current funding, respondents replied overwhelmingly that most funding comes from public sources, with NASA and the Chinese government cited most often as the biggest space resource sector funders. Some outlier respondents, who believe that most funding for space resources currently comes from the private sector, admitted that their opinions were based on trade shows and media exposure, and not grounded in research.

An interesting consideration raised by one respondent was how space resource funding from military sources today compares with military sponsorship of resource exploration during the Age of Discovery. Although such research is outside the scope of this article, it is perhaps worth mentioning that this would be a relevant and related subject for further research.

When asked about future funding sources, respondents were almost evenly split, with half believing that the space resource sector will in the future be mostly privately funded and the other half believing that it will be supported through a mix of public and private funds, including the model, widely used, of public–private partnerships, and accompanied by heavy government regulation and/or incentives to stimulate private investment. A small minority (two) believed that in the future, most of the funding for space resources will continue to come from the public purse.

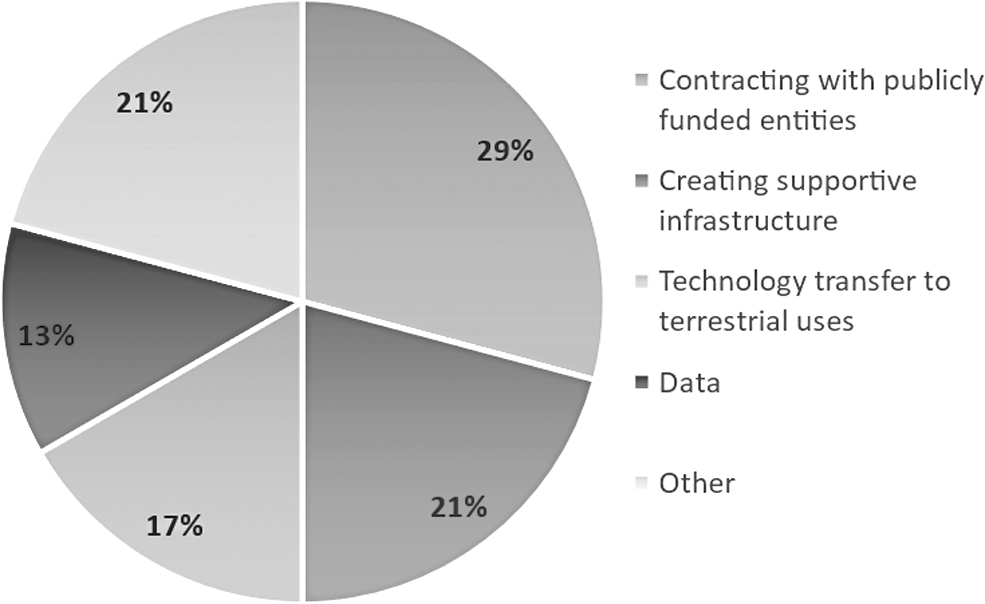

Opportunities and Challenges in Funding the Space Resource Sector

Unlike the respondents' unified focus regarding the greatest opportunity in space resources (water and propellant), when asked about the greatest opportunities in funding for the space resource sector, the answers were more varied.

Approximately 30% of respondents believed that developing programs and services to contract with publicly funded entities and government programs was the greatest opportunity. This was primarily the view of Western respondents, who often cited NASA as the public entity that represents the greatest opportunity for funding.

The second-most common response was creating an infrastructure to support the space resource industry. More than once, respondents who cited this as the top opportunity made an analogy to the California Gold Rush of the mid-1800s and the role of hardware suppliers and general stores in supporting the speculating miners. These respondents often referred to the sale of “picks and shovels” to the space resource industry as the top opportunity. When respondents were asked for more detail, one theme that emerged was the development and commercialization of geological data on asteroids and planets, which can be sold to companies planning on engaging in resource extraction.

The third-most common response was technology transfer for terrestrial resources. It is worth noting that this answer was given by respondents associated with large terrestrial corporations such as mining companies, as well as by politicians and policymakers.

Similarly, respondents also saw data and data transfer as an opportunity in space resource sector funding. Further answers included lowering environmental impact through a reduced number of space launches and the ability to scale operations. These responses are shown graphically in Figure 8 below.

Opportunities in funding the space resource industry.

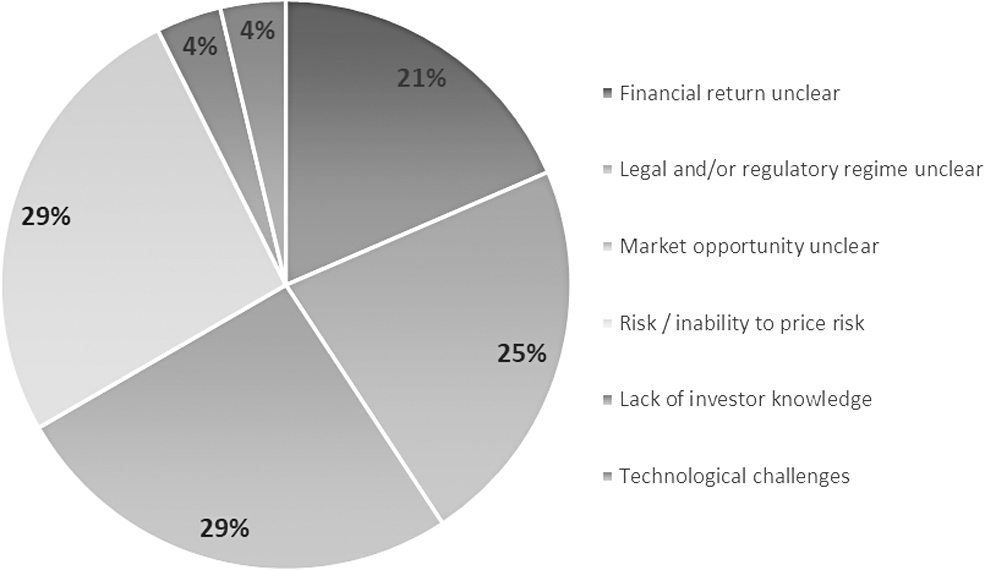

When asked about funding challenges facing the space resource industry, responses generally fell into the following four categories: the financial return is uncertain, the legal and/or regulatory regime is unclear, the market opportunity is uncertain, and the risk and/or the understanding of risk are too high. It could be argued that all these challenges are interrelated, reflective of a nascent market, and may well be addressed as the sector matures and its players gain experience. Indeed, when questioned on this point, the general feeling among the respondents was that such challenges will be ameliorated over time, as the industry grows (Figure 9).

Challenges in funding the space resource industry.

Following the above questions regarding the opportunities and challenges for space resource industry funding, respondents were asked to identify a success story in the space resource industry. However, as stated earlier, due to the inability to distill learnings or themes, the responses to this question were deemed insufficiently relevant to include in this report.

Supportive Geographies

Next, respondents were asked to share their views on which countries or regions were the most supportive of the space resource sector financially. The respondents were given clear instructions that their answers were to focus on the financial aspect of the industry—in contrast to Question 5 (discussed above), concerning countries successfully promoting the development of the sector.

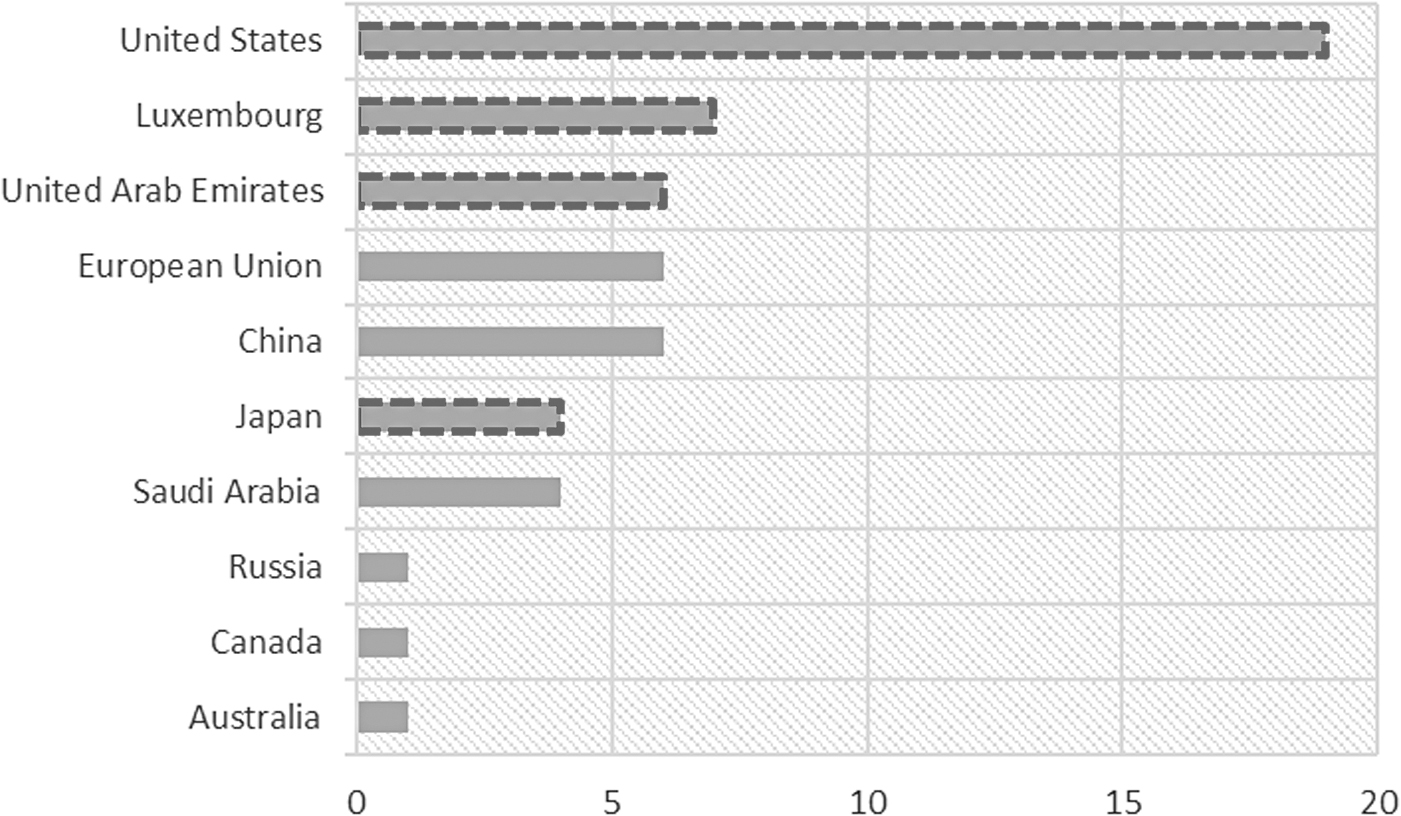

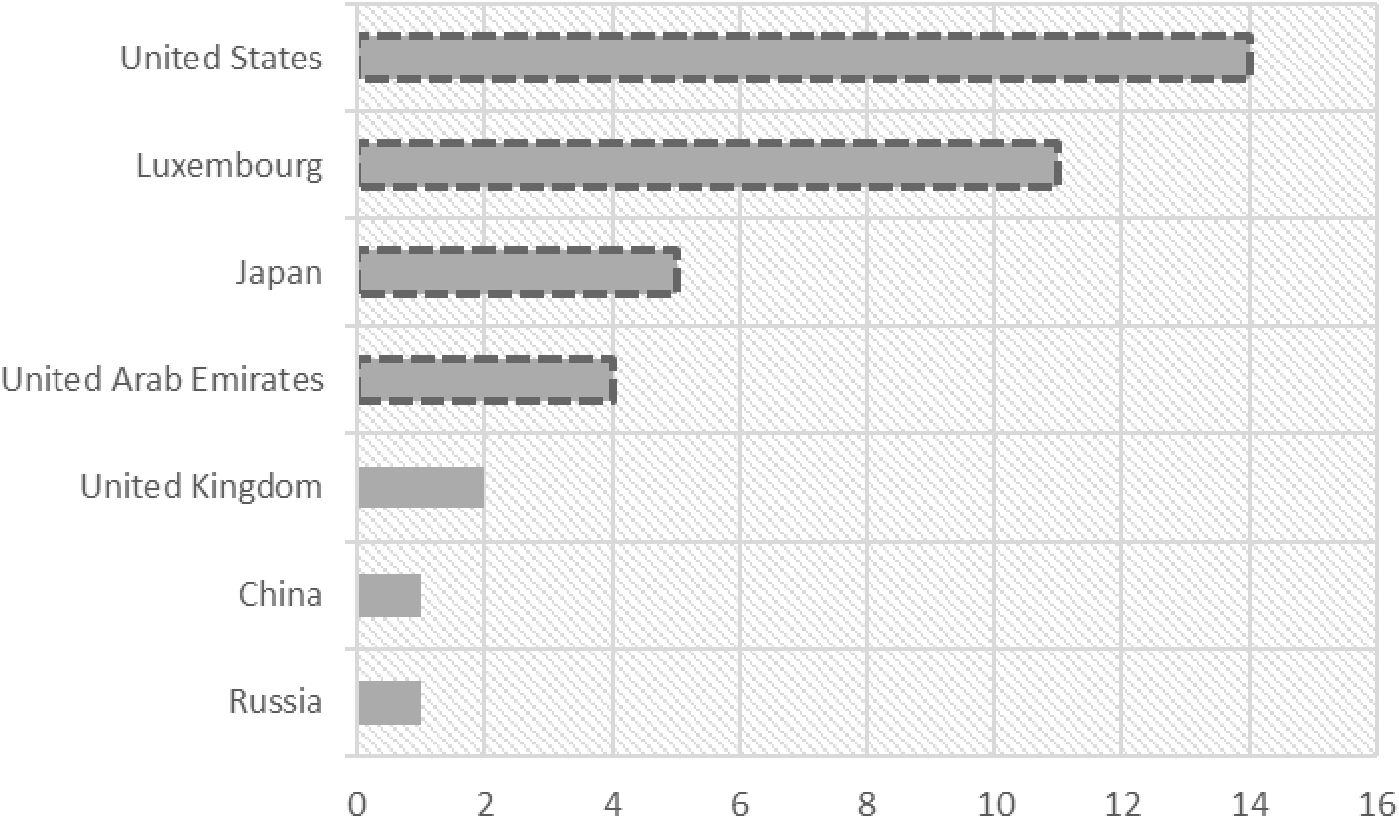

As illustrated in Figure 10, respondents believed that the primary country supporting the space resource sector financially is the United States. Two answers, from respondents who replied “the Middle East” rather than naming individual countries, were added to the tallies for both the United Arab Emirates and Saudi Arabia (rather than creating a new category).

Respondents' attitudes regarding countries financially supportive of the space resource industry.

A key insight gleaned from this discussion was that although the respondents almost invariably believed that the United States is the sector's primary financial supporter, they also felt that this is a function of the size of the U.S. economy. Table 3 illustrates the size of the economy of select countries as represented by the gross domestic product in 2022. These countries have been selected as they have passed or are expected to pass national space resource legislation.

2022 Gross Domestic Products (in Millions of USD) of Selected Economies

From International Monetary Fund 2023. 31

GDP, Gross Domestic Product.

Although no respondent provided numerical evidence, many did suggest that the European Union or individual countries such as Luxembourg were in fact more financially supportive of the sector than the United States inasmuch as their respective commitments represented a greater proportion of their economies.

In addition, when pressed on this point, respondents suggested that in the United States, financial support derived primarily from public sources of capital, while other countries and regions had a larger proportion of private funding.

As given in Figure 6, the United States, Luxembourg, the United Arab Emirates, and Japan are all identified with a dashed red border, as these countries have enacted legislation and/or legal frameworks related to space resources in some form or other.

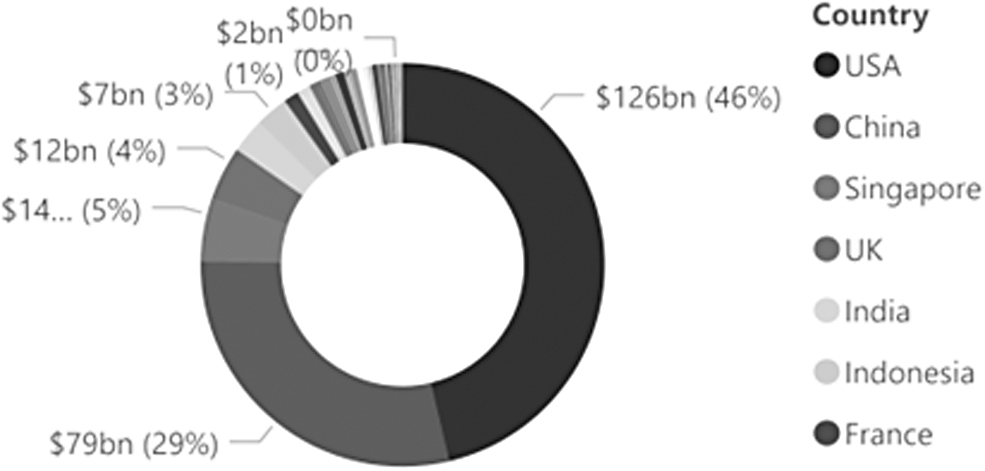

Respondents' views of the United States as the dominant funder of the space resource sector are reinforced by data compiled by Space Capital, a seed-stage venture capital firm that invests in the space economy and produces quarterly reports of investment data. As illustrated in Figure 11, between January 1, 2014, and March 31, 2023, the United States was the dominant investor with regard to all aspects of the space economy.

Ten-year equity investment in space by country. Source: www.spacecapital.com.

KEY FUNDING PARTNERS AND SUPPORTERS

In the next section of the research, respondents were asked to share their views on partnerships and support for the space resource sector. Specifically, they were asked:

xiii. Do you think that there is sufficient communication and understanding between providers of capital in the space resource sector and users of capital?

xiv. How well are national governments doing in regard to support for the space resource sector around the world?

xv. How effective is the private sector in supporting the space resource sector?

This section is important for understanding the quality of financial support for the space resource sector and where that support is coming from. In response to the first question, in general, the participants believed that currently there is not sufficient communication and understanding between the providers of capital and users of capital in the space resource sector. With the exception of two respondents, who said that communication and understanding are adequate and/or improving, it was apparent that the respondents in these interviews were frustrated by a lack of communication and understanding.

Several respondents noted that they believe there is significant information available on the space resource sector—in the form of conferences such as Investing in Space or FT Live, academic journals such as Space Policy, New Space, or Acta Astronautica, and popular media articles such as “The Space Industry Is Taking Off. Space Law Is Still a Mystery,” in the New York Times, 21 or “Space Companies Struggle to Meet Lofty Goals,” in the Wall Street Journal. 22 However, respondents also reported a lack of education on the part of investors and providers of capital, or simply a lack of interest in educating themselves.

A further theme in the responses to this question was a perceived lack of professionals who properly understand the opportunities and risks inherent in space resources and who can communicate appropriately with the investment community. This shortfall of interlocution extends to a lack of understanding of risk and the inability, on the part of the space resource community, to provide the financial community with the necessary risk education and due diligence materials.

When asked how well national governments are performing in regard to supporting the space resource sector, the dominant theme from respondents was that such performance is mixed and that only a few governments are truly engaged in the industry at this point. Not surprisingly, the United States, China, and Luxembourg, and to a lesser extent Japan and the United Arab Emirates, were cited as being the most supportive countries and possessing the political will to continue to support the sector. Few other governments were mentioned as being engaged in a meaningful way. One respondent posited that governments are having a hard time defining and distinguishing between commercial space activities over against government space activities, and that, because of this difficulty, governments are having a difficult time nurturing a private, commercial space resource sector.

One response to highlight was that the governments that are currently committed to space resources are doing quite well in supporting the industry, with strong interest and open communications; but, because of the way in which public funding is deployed (grants, competitions, etc.), governments are excluding partnerships and collaborations with companies beyond their domestic borders, thereby stunting the global advancement of the industry and creating less efficient domestic market ecosystems.

When asked about support for space resources on the part of the private sector, as with the responses to the question about government support, the dominant theme here was that performance is mixed. Many respondents pointed to strong support from the venture capital market, but added that support from the larger, more traditional sources of private funding, including debt capital providers, was limited. In addition, most respondents were optimistic that support from the private sector is growing, a phenomenon being stimulated by the success of launch companies such as SpaceX and manufacturers of CubeSats.

The respondents also clearly believed that for private sector players to become stronger partners and meaningful funders of the space resource industry, a significant amount of education about the sector, its commensurate risks, and the return time line will be required. One respondent also observed that a country's level of private sector support is directly commensurate with the degree of support provided by the public sector in the same country.

REGULATIONS AND LEGISLATION IN FUNDING SPACE RESOURCES

As humankind's activities in space are no longer limited to exploration and research, and now include commercial activities, including through the exploitation and development of space resources, in 2017, the United Nations Committee on the Peaceful Uses of Outer Space encouraged members to start national space legislation. 1

The basic international space treaties—the Outer Space Treaty (1967), the Rescue Agreement (1967), the Liability Convention (1972), the Registration Convention (1974), and the Moon Agreement (1979)—were executed at relatively early stages in the development of space exploration and exploitation, and, as such, may require updating to address the needs of the growing space resource industry.

International Space Treaty Summary

The Outer Space Treaty was considered by the UN Legal Subcommittee in 1966 and agreement was reached in the General Assembly the same year (Resolution 2222 [XXI]). The Treaty was largely based on the Declaration of Legal Principles Governing the Activities of States in the Exploration and Use of Outer Space, which had been adopted by the General Assembly in Resolution 1962 (XVIII) in 1963, but added a few new provisions. The Treaty was opened for signature by the three depository governments (the Soviet Union, the United Kingdom, and the United States) in January 1967, and entered into force in October 1967. The Outer Space Treaty provides the basic framework for international space law. 23 It has been ratified by more than 100 countries and remains the most important and foundational source of space law. 24

The Rescue Agreement was considered and negotiated by the UN Legal Subcommittee between 1962 and 1967. Consensus was reached in the General Assembly in 1967, in the form of Resolution 2345 (XXII), and the Agreement entered into force in December 1968. Elaborating on elements of articles 5 and 8 of the Outer Space Treaty, the Rescue Agreement provides that “States shall take all possible steps to rescue and assist astronauts in distress and promptly return them to the launching State, and that States shall, upon request, provide assistance to launching States in recovering space objects that return to Earth outside the territory of the Launching State.” 25

The Liability Convention was considered and negotiated by the UN Legal Subcommittee between 1963 and 1972. Agreement was reached in the General Assembly in 1971—Resolution 2777 (XXVI)—and the Convention entered into force in September 1972. Elaborating on Article 7 of the Outer Space Treaty, the Liability Convention provides that “a launching State shall be absolutely liable to pay compensation for damage caused by its space objects on the surface of the Earth or to aircraft, and liable for damage due to its faults in space. The Convention also provides for procedures for the settlement of claims for damages.” 26

The Registration Convention was considered and negotiated by the UN Legal Subcommittee from 1962 onward, until its adoption by the General Assembly in 1974 as Resolution 3235 (XXIX). It was opened for signature on January 14, 1975, and entered into force on September 15, 1976. Responding to a desire expressed by states party to the Outer Space Treaty, the Rescue Agreement, and the Liability Convention for a mechanism that would provide states with “a means to assist in the identification of space objects,” the Registration Convention expanded the scope of the United Nations Register of Objects Launched into Outer Space, which had been established by Resolution 1721B (XVI) in December 1961, addressing issues relating to state parties' responsibilities concerning their space objects. 27

The Moon Agreement was considered and elaborated by the UN Legal Subcommittee between 1972 and 1979, and was adopted by the General Assembly in 1979 as Resolution 34/68. It was not until June 1984, however, that a fifth signatory country, Austria, ratified the Agreement, allowing it to enter into force in July the same year. The Agreement reaffirms and elaborates on many of the provisions of the Outer Space Treaty as applied to the Moon and other celestial bodies, providing that those bodies should be used exclusively for peaceful purposes, that their environments should not be disrupted, and that the United Nations should be informed of the location and purpose of any station established on those bodies.

In addition, the Agreement provides that the Moon and its natural resources are the common heritage of mankind and that an international regime should be established to govern the exploitation of such resources when exploitation is about to become feasible. 28

National Space Resource Legislation

Today, individual states are beginning to regulate an industry that did not exist when the basic space treaties were originally signed. In addition, some believe that nontraditional space activities (such as ISRU) lack clear and dedicated international rules to govern them. 29

To address this, countries are beginning to develop their own frameworks and legislation, under which space resource companies can operate. Commercial space activities, such as other commercial activities, are governed by their respective states' national laws. 30 These include contract, property, tort, creditors' rights, bankruptcy, insolvency and reorganization, and other laws.

Currently, the following four countries have actively developed frameworks for the development of space resources: the United States, Luxembourg, the United Arab Emirates, and Japan. Certain other countries, such as Saudi Arabia, are actively working on developing their own frameworks.

With this background, the following questions were asked of respondents, focusing on regulation and legislation in funding the space resource sector:

xvi. Who should regulate funding in the space resource sector and why?

xvii. If there was one piece of regulation you would enact or change to help develop a stronger funding ecosystem for space resources, what would that be?

xviii. Describe which country has the strongest legislation to support space resources. Are there any shortcomings or obviously missing regulation?

Respondents cited a lack of in-depth knowledge or insight when answering questions in this category, particularly when asked about specific pieces of regulation and legislation.

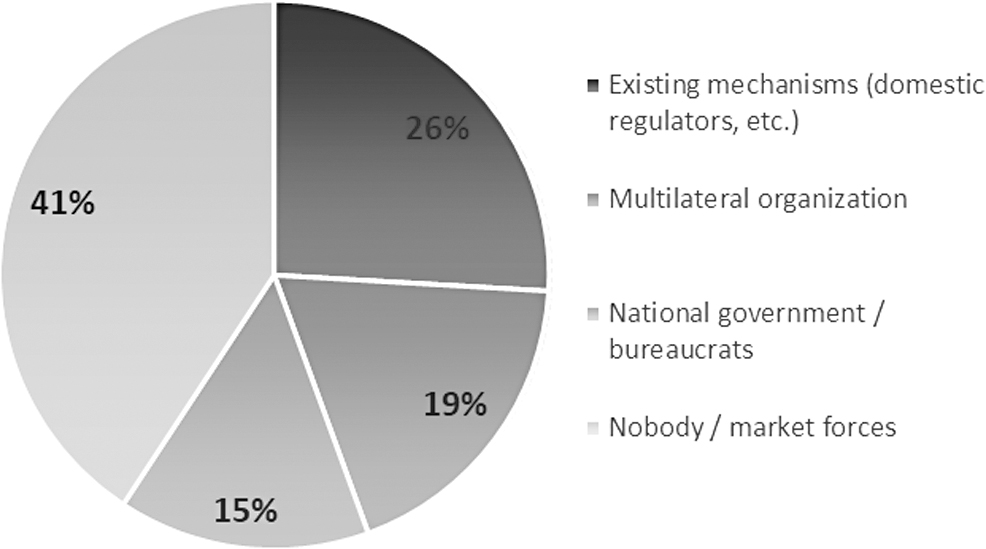

On the matter of who should regulate funding of the space resource sector, answers fell into the following four categories: let existing mechanisms such as securities regulators (i.e., the Securities and Exchange Commission, in the United States, the Ontario Securities Commission in the Canadian province of Ontario) oversee this type of funding; create a multilateral organization to provide regulatory oversight; leave regulation to national governments and their bureaucrats; or (the most common response) no one should regulate the sector, that is, let funding be subject to market forces. Nonetheless, several respondents who gave the latter answer added the caveat that some kind of oversight would be necessary to prevent the emergence of monopolies and ensure companies are not acting illegally.

Interestingly, when comparing respondents' views on appropriate regulation with the same respondents' background, a correlation became apparent. Respondents who were entrepreneurs typically advocated for no regulation, multinational lawyers called for creating a multilateral organization, and so on (Figure 12).

Who should regulate funding in the space resource industry?

As noted earlier, respondents were hesitant to comment on the final three questions. However, when asked to name a single piece of regulation that they would enact, or amend, to help develop a stronger funding ecosystem for space resources, participants who were sufficiently comfortable to respond invariably pointed toward ensuring clarity regarding property rights and providing assurance that such rights will be applied and respected internationally. The sole deviations from this position came from two respondents, who proposed tax credits or tax breaks for space resource activities. One of these two respondents also suggested that policy should be adapted to provide for limitation and removal of space debris.

Countries with Strong Legislation to Support the Space Resource Sector

When asked to describe which country has the strongest legislation to support space resources, respondents identified the four countries that have enacted such legislation. In addition, the United Kingdom, due to the strength of its aviation regulation, as well as China and Russia, was mentioned. As with government support for the industry, regulatory and legislative support varies from country to country. This is shown in Figure 13 below.

Respondents' attitudes regarding countries with strong space resource legislation.

Interestingly, no respondent was willing to describe any given country's specific shortcomings or obviously missing regulation, but many felt that no single country's regulatory measures were currently sufficient to support and develop a space resource sector. One respondent mentioned that political science, as a discipline, lacks the patience necessary to project the potential future impact of the development of a space resource industry due to a limited ability to demonstrate impact in the near term. In this respondent's opinion, this inability is a key factor underpinning the insufficiency of current legislative and regulatory efforts regarding the space resource sector.

DISCUSSIONS AND FINDINGS

Additional themes, which respondents shared outright, or which emerged over the course of the interviews, were also revealing as to the state of space resource industry funding.

KEY FINDINGS

Biases

Table 4 summarizes the key findings from this research. Certain biases became apparent when examining the respondents' answers collectively. Interviewees were selected to include a wide range of industries—law, entrepreneurship, corporations, finance—and, as such, each respondent spoke to whatever they were knowledgeable and comfortable speaking about. The differences in the answers returned by respondents operating in different subindustries call attention to the need for increased communication and education between industry actors. Conversely, the fact that all the respondents are active in the space resource industry may bias them toward the view that this industry is of greater importance than what society or governments currently accord it.

Summary of Key Findings

Another bias that emerged pertained to geography. In their answers, respondents based in North America tended to focus on Western countries and companies, whereas respondents based in Europe and, especially, the Indo-Pacific region tended to mention China more often. When asked directly about this discrepancy, following the formal questions, one respondent pointed to the fact that actors in these two groups (North America versus Europe and the Indo-Pacific) exhibit little overlap in the conferences they attend or the research they undertake; and that a lack of exposure to one another affects the importance they accord to the contributions to the sector from their respective spheres.

It is also important to acknowledge the author's bias. The information presented in this article is the distillation of 30 h of conversation. Using transcripts, the author collated and interpreted the information to present a coherent, collective view of thirty individuals from disparate professions as to how they view the state of space resource funding. As such, the author needed to make certain assumptions and generalizations, such as inferring context while categorizing responses, to present these data as succinctly and accurately as possible.

Other Thematics

Several respondents made references to space resource companies that were very active and successful in raising money, but less successful in executing their business plans. Among these respondents, there was a general feeling that these companies have harmed the industry's funding prospects and even tainted governments' views on providing support for the industry. Some respondents identified a need to educate government personnel, as well as both the investing and the noninvesting public, to win broader acceptance for the industry.

Respondents also drew analogies to the California Gold Rush of the late 19th century. The space resource sector, these respondents observed, is similarly a nascent industry—a “wild west”—but they also noted that there is room in the industry for a wide variety of players, from active leaders to providers of infrastructure, such as markets or “pick and shovel” providers.

The issue of debris arose quite often as a topic of conversation, not as a space resource but as a potential impediment to the industry's development. There was a consensus among these respondents that space debris is a genuine problem, which will need to be tackled and does not currently receive sufficient attention from the industry.

When asked about other relevant themes and issues that had not yet been discussed, responses ranged from the value of public–private partnerships to the need to educate the investing community about space resources, to potential inequalities between wealthy countries and poor countries. Each interview suggested avenues for further research; however, for the purposes of this article, we remain focused on the state of the space resource industry, the state of funding for the industry, partnerships in the ecosystem, and regulation and legislation. Advancing this research, the author believes, promises significant potential for the industry.

CONCLUSION

The pool of respondents for this research comprised individuals from significantly varied backgrounds (law, business, education, etc.) and the resulting discussions and responses reflected these differences. As such, the author may have imbedded unconscious biases into the responses, simply through processing and distilling the responses, and seeking to identify commonalities and unique differences among the respondents. However, because all of the respondents are active participants in the space resource sector, significant thematic similarities emerged, which contributed greater certainty and confidence in presenting the responses. As the interview process progressed, it was interesting to be able to identify certain unique differences and to try to discern the reasons for them. Perhaps future research may explore these differences further, yielding new insights and understanding, and thereby helping to develop the industry.

In addition, the interview findings suggest that due to the industry-wide lack of a universally accepted definition of space resources, it is difficult for the supporting financial infrastructure to gain a foothold in the wider business community and become recognized as a legitimate funding branch. Interview evidence suggests that apart from (Research and Development) funding aimed at the development of terrestrial mining technologies, funding for space resources will continue to be either an afterthought in the wider market, a derivative of technology and start-up funding, or simply be linked to and constrained by the public purse.

It was also found (although it is perhaps also intuitively obvious) that more developed countries, particularly those that have enacted laws supporting space resource exploitation, such as the United States, China, Japan, and Luxembourg, tend to be the most active in funding space resources and supporting space resource development in general. Following these countries are other countries that have well-established markets for funding terrestrial resource development, such as Canada and the Scandinavian countries.

A significant difference was also observed with regard to the understanding of funding sources between individuals focused solely on the space resource industry and individuals involved with larger companies where space resources represent but one aspect of their operations among many. Further research could and should be focused on a better understanding of the latter type of company, and how they make capital allocation decisions.

Footnotes

AUTHOR DISCLOSURE STATEMENT

The author declares that he has no competing interests.

FUNDING INFORMATION

This researcher received no specific grants from funding agencies in the public, commercial, or not-for-profit sectors.