Abstract

Sirmon and Hitt (2003) do an excellent job of describing the pivotal role that resources unique to a family firm can play in a company's survival and success. Grounded in the resource–based view (RBV) of the firm, their article maps how these firm–unique resources affect the efficacy of resource management through which a family firm may leverage its resources to achieve a competitive advantage. Aside from showing how the RBV can improve our understanding of a family firm, the article articulates and defines the various managerial roles and challenges in evaluating, adding, shedding, bundling, and leveraging resources. We believe that this approach makes the RBV more accessible to managers, overcoming a common criticism of the theory (Priem & Butler, 2001).

This commentary has two purposes. First, it seeks to extend the contributions of the authors by considering how family influences on strategy formulation will affect a firm's competitive strategy to leverage resources. The goal is to highlight additional important research issues that arise from applying the RBV to the study of family businesses. Second, it expands the applicable boundaries of the RBV set forth by the authors to include family firms for whom wealth creation may not be the sole or primary goal.

Extending the RBV of Family Influence

At the most basic level, what differentiates a family business from other profit–seeking organizations is the family's important influence on the decision making and operations of the firm. Litz (1995) defines family business by their intentions, whereas Chua, Chrisman, and Sharma (1999) define a family business based on the vision and behavior of a dominant coalition of family members. Habbershon and Williams (1999) and Habbershon, Williams, and MacMillan (2001) refine our understanding of family firms by introducing the concept of familiness—the unique, inseparable, and synergistic bundle of resources and capabilities resulting from idiosyncratic family influences—to explain their wealth–creating potential. Following this logic, Sirmon and Hitt are successful in developing several important propositions on the relationships between family business behaviors, resource management, and company performance.

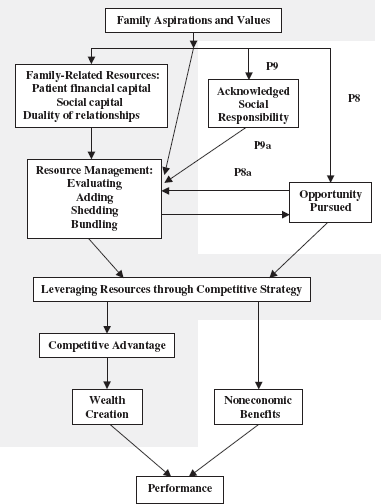

In their article, Sirmon and Hitt also show how family aspirations and values indirectly influence a family firm's effectiveness and efficiency in resource management through the creation of unique resources: patient financial capital, social capital, and human capital resulting from duality in relationships. They also provide some useful insights on how a family's aspirations and values may directly influence resource management, for example, because of emotional ties or escalating commitments within the family. These variables are shown in Figure 1 within the shaded area.

Family influence on resource management, strategy, and performance (shaded area is from Sirmon and Hitt, 2003)

Resource management is an important part of the process of managing an organization strategically to gain a competitive advantage. However, while resources are the essential building blocks, whether an organization gains a competitive advantage and thereby achieves above–normal returns will be a function of the strategy used to leverage those resources to pursue environmental opportunities (cf. Barney, 1996; Hofer & Schendel, 1978; Ward, 1987). In their discussions of family influences on resource management, Sirmon and Hitt assume implicitly that the opportunity pursued is given. Following Andrews’ (1980) conception of the factors that influence strategy formulation, we suggest that a family's aspirations and values will have a profound effect on strategic choices, both in terms of resources, as described by Sirmon and Hitt, and in terms of opportunities pursued. By making this additional relationship endogenous in Figure 1, we can determine how family aspirations and values affect opportunities pursued and, through this, further affect the family firm's resources, competitiveness, and performance.

Social responsibility is another channel by which family aspirations and values may affect the firm's resource management. Andrews (1980) asserts that, in the attempt to match opportunities with organizational resources, the strategy a company follows will be affected by senior managers’ acknowledged noneconomic responsibilities to society. These noneconomic responsibilities relate to the family itself and society at large. For example, family firms may focus on creating jobs for family members or offering their members opportunities for growth and development, even if these objectives lower the firm's overall profitability. Noneconomic responsibilities to society include improving the quality of life in a given community, fighting poverty, and promoting key social causes (e.g., literacy), among others.

In summary, we believe that the authors’ RBV of family influence on resource management can be enhanced by explicitly considering all of the factors that influence the formulation of strategy (Andrews, 1980). This highlights two other sets of paths— opportunity pursued and social responsibility—by which family aspirations and values may shape resource management and competitive strategy. These paths are shown in Figure 1 within the unshaded section and are discussed next.

Influence of Family Aspirations and Values

In a small and medium–size family firm, there is typically a single owner–manager (Gersick, Davis, Hampton, & Lansberg, 1997). Here, there is no doubt that the aspirations and values of the family owner–manager will strongly influence the governance and management of the business. In a larger business, especially one where there are outside shareholders, the family will typically hold sway over the governance and management of a business through majority ownership. Even when the family does not own the majority voting rights in the firm, however, it may still significantly influence the firm by controlling the dominant coalition. Although the family's influence may be one step removed in the professionally managed firm, agency theory suggests that, despite monitoring costs and inefficient risk sharing, a dominant shareholder and monetary incentives may be sufficient to make congruent the interests of the owners and managers. 1 Thus, it is possible for the family's aspirations and values to be reflected in the opportunities pursued, resource management, and acknowledged social responsibilities.

Family Influence on Opportunity Pursued

As noted earlier, the aspirations and values of the family will affect the opportunities pursued by the business. This could take the form of a commitment to maintain company headquarters or plants in a given community, religious beliefs prohibiting engagement in certain business activities, a family member's political career creating conflict with the pursuance of a particular line of business, or risk aversion (Fiegenbaum & Thomas, 1988). Family aspirations and values can significantly determine the nature of the opportunities to be pursued and the extent to which resources of different types are dedicated to pursuing them. Thus,

As Porter (1980) shows, opportunities pursued will affect a business's potential profitability because some industries are inherently more profitable than others. More important, the nature of the industry will influence the types of resources that are necessary to compete effectively. Therefore, decisions on which opportunities to pursue affect the potential value of the resources controlled by a family business, as well as the resources that must be acquired or shed to create economic value. As shown in Figure 1, this interaction is bidirectional. Assessment, addition, shedding, and bundling of resources influence which opportunities are pursued, while the opportunity pursued determines which resources have to be added, shed, and bundled.

Family Influence on Acknowledged Social Responsibility

A family's aspirations and values will also influence the manner in which the family firm assesses its noneconomic responsibilities to society. For example, Post (1993) reported a case of how a family's values demanded that the business be environmentally responsible. Family values, therefore, determine which noneconomic goals the firm should pursue. Thus,

As P9 makes clear, social responsibilities are only one component of the noneconomic goals family firms might pursue. As noted, noneconomic goals might also include maintaining family harmony and employment of family members. Still, the social responsibilities acknowledged will affect the criteria by which a family firm evaluates a given resource, especially when the employment of that resource creates a trade–off between wealth creation and social responsibility. Social responsibilities differ in their importance, but often challenge managers to establish a priority system to allocate necessary resources. Family values and aspirations, as well as the perceived importance of various social responsibilities, are likely to affect how the firm adds, sheds, and bundles resources and capabilities. Therefore,

One useful extension of the work of Sirmon and Hitt (2003) is to propose that the family firm's acknowledged social responsibilities will influence the scope and type of the opportunity pursued. Social responsibilities acknowledged by the firm are likely to frame managers’ perceptions of the nature of opportunities and the speed by which they are pursued. For example, family firms that value being environmentally sensitive may seek opportunities to invest in new technologies that make this goal a reality. These firms are likely to allocate resources to acquire (or even develop) these technologies ahead of their rivals that do not have the same orientation.

Expanding the Scope of the Model

In developing their RBV of family influence, Sirmon and Hitt emphasize family firms whose primary goal is wealth creation. This focus does not detract from the authors’ important contributions, but the resulting model does exclude family firms that do not pursue wealth maximization as their dominant objective. Many family firms fall in this category, which compels us to consider these firms.

Family businesses are less likely than nonfamily firms to pursue wealth maximization as their dominant objective (Sharma, Chrisman, & Chua, 1997). This does not mean that family firms are unconcerned with making money. Rather, family firms are likely to have important noneconomic goals or constraints, such as maintaining family harmony or job creation for family members. Sirmon and Hitt acknowledge this numerous times in their article, explaining how concerns about family members and generational outlook can augment or impede the development of a sustainable competitive advantage. Omission of noneconomic objectives or constraints leads us away from a full understanding of the family form of organization. Thus, rather than excluding those firms that place great emphasis on noneconomic considerations from an RBV of family firms, we propose that they should be embraced in theory development. As shown in Figure 1, this involves consideration of noneconomic benefits in evaluating the family firm's performance.

There are three good reasons for considering noneconomic goals. First, the theory will better reflect reality since many family businesses are likely to include noneconomic considerations as a major component in their set of goals and constraints. Second, explicit acknowledgment in theory development that some, if not all, family firms have greater noneconomic proclivities than other businesses will not alter the relationships between the resources accumulated and controlled by a company and its economic performance. Third, however, and as Sirmon and Hitt show, incorporating all types of family businesses in theory will certainly alter the way we view how their resources and capabil–ities are evaluated, acquired, shed, built, and leveraged. As noted, the noneconomic goals of family businesses will have an influence on their rent–seeking behaviors through the aspirations and values of key decision makers. Thus, the pursuit of noneconomic goals may alter economic performance if resource accumulation, development, and deployment are compromised. However, that is exactly what a theory of family businesses should help explain. A theory that considers these factors will be richer and more likely to contribute to effective practice since family business managers will be able to gain a greater appreciation of the trade–offs required to pursue different types of goals.

As our discussion makes clear, resource acquisition, evaluation, and shedding are important for goal attainment in both family and nonfamily firms. However, the mix of resources and the approaches used to acquire, evaluate, and shed resources are likely to vary considerably between family firms and nonfamily firms. Ownership structures and corresponding managerial goals influence these decisions. Perhaps, future researchers can explore the potential differences that might exist between family and nonfamily firms as well as across family firms that pursue different goals. This information can enrich future theory building and testing.

Conclusion

In this commentary, we have attempted to extend the work of Sirmon and Hitt (2003) by arguing for an explicit consideration of a family's noneconomic goals and by briefly discussing how a family's influence on the formulation of a firm's strategy may affect its resource management practices. We do not know if the above observations will hold empirically. But logic would suggest a need for a greater recognition of the limits of pure RBV arguments within family business firms. This recognition does not diminish the value of the RBV; it only highlights the boundaries of the theory and the conditions under which its predictions are valid. Given the infancy of most of the empirical research on family business, we believe this can only improve future scholarship.

Footnotes

1.

See Gomez–Mejia, Nunez–Nickel, and Gutierrez (2001) and ![]() for detailed treatments of agency in family firms.

for detailed treatments of agency in family firms.