Abstract

Greater managerial ownership in family firms need not mitigate agency problems, especially when each family controls a group of publicly traded and private firms, as is the case in most countries. Such structures give rise to their own set of agency problems, as managers act for the controlling family, but not for shareholders in general. For example, to avoid what we call “creative self–destruction,” a family might quash innovation in one firm to protect its obsolete investment in another. At present, we do not know whether these agency problems are more or less serious impediments to general prosperity than those afflicting widely held firms.

Executive Summary

Much discussion of corporate governance problems highlights managers’ failure to act for shareholders in widely held firms. This discussion typically assumes that greater insider ownership leads to better corporate governance. This is because managers who own larger equity blocks in their firms are less likely to take actions that reduce the value of their shares. This logic, taken a step further, suggests that agency problems might be minimized in narrowly held firms, such as those controlled by families.

This framework is certainly relevant in economies, such as the United States and United Kingdom, where most large firms are widely held. However, in other countries, most large firms are parts of family business groups. In a family business group, a family firm holds control blocks in several publicly traded firms, each of which holds control blocks in yet more publicly traded firms, and so on.

We show that such structures give rise to their own set of agency problems. In widely held firms, the concern is that professional managers may fail in their fiduciary duty to act for public shareholders. In family business group firms, the concern is that managers may act for the controlling family, but not for shareholders in general. These agency issues are the use of pyramidal groups to separate ownership from control, the entrenchment of controlling families, and non–arm's–length transactions (a.k.a. “tunneling”) between related companies that are detrimental to public investors. At present, we simply do not know if these agency problems are more serious impediments to general prosperity than those afflicting widely held firms.

To illustrate how such agency problems might be socially destructive, we consider investment in innovation, which current economic theory holds responsible for the larger part of economic growth. Schumpeterian “creative destruction” creates new wealth for entrepreneurs, while destroying the value of old capital. Established wealthy families who own the latter might be reluctant to back much innovation. Recent empirical findings on R&D spending are consistent with this hypothesis, but it clearly requires much more proof. Moreover, although this would certainly slow economic growth, it might also be desirable from some perspectives. For example, it might ease social problems associated with redundant workers and obsolescent industries.

The contribution of this article is to underscore that concentrated corporate control need not eradicate agency problems, especially in the large family business groups common outside the United States and United Kingdom. Without taking a final position on its social welfare consequences, we argue that much more research is needed on family control. This need is especially urgent at present because postcommunist and emerging economies are presently choosing between the Anglo–U.S. and the family business group models of corporate ownership. Research into the problems of widely held firms is abundant, while research on family business groups is only beginning—perhaps because the latter are absent in the United States and United Kingdom, where most corporate governance research is done. This asymmetric focus could color critical policy decision in some countries.

Agency Problems in Large Family Business Groups

[B]eing the managers of other people's money than of their own, it cannot well be expected that [the managers of widely held corporations] should watch over [public investors’ wealth] with the same anxious vigilance with which partners in a private copartnery frequently watch over their own. Like the stewards of a rich man, they … consider attention to small matters as not for their master's honour and very easily give themselves a dispensation from having it. Negligence and profusion therefore must prevail more or less in the management of such a company.

Adam Smith, The Wealth of Nations, volume 2, 1776.

1. Introduction

Family firms have always been important to free–market economies. The names Rothschild, Medici, Ford, Thomson, Krupp, and Mitsubishi are inseparable from the sagas of economic development of today's industrial democracies. Indeed, Smith's words in the introductory quote reflect the view that “joint stock” (widely held) companies are a disreputable distraction from the real engines of growth in a free–enterprise economy: family firms.

Smith's view informs much current thinking regarding corporate governance. Thus, Jensen and Meckling (1976), Shleifer and Vishny (1997), and others argue that concentrated corporate ownership leads to better corporate governance. We argue that this view is incomplete with regard to the large family–controlled business groups that dominate many economies.

La Porta, Lopez–de–Salines, and Shleifer (1999) find that the role of leading families in corporate governance varies greatly across developed (and emerging) free–market economies. Most large U.S. and U.K. businesses are controlled not by families, but by professional managers acting, however imperfectly, as fiduciaries for multitudes of public investors. In contrast, La Porta, Lopez–de–Salinas, and Shleifer (1999) document that most large firms in most other countries are organized into business groups controlled by a few wealthy old families. Thus, firms controlled by the Noboa family provide the incomes of about three million of Ecuador's eleven million people. The family's banana operations alone, which account for 40 percent of Ecuador's banana exports, generate about 5 percent of the country's GDP. 1 Likewise, Agnblad et al. (2001) report that the Wallenberg family controls 43 percent of the Swedish economy, measured by the 1998 market value of firms traded on the Stockholm Stock Exchange. Barca and Becht (2001) describe similar situations throughout the European continent. Claessens, Djankov, and Lang (2000) describe similarly concentrated corporate control in the hands of a few leading families in Asia. A few countries, including Canada and Australia, are in between, having some large widely held firms, but also containing business groups controlled by wealthy old families. Of course, these countries contain numerous smaller firms too, and these may play critical roles. However, the economic importance of these groups to their countries far outweighs the importance of the largest widely held firms to the United States or United Kingdom.

While governance problems in widely held firms clearly can be serious, we argue that family control can give rise to other, potentially worse, corporate governance problems. Our emphasis differs from previous work, notably that of Schultz et al. (2001), who convincingly point out that agency problems can occur between family members. We argue that, in addition to these problems, another set of agency issues arise when family controlled firms organized into business groups obtain outside equity financing. These agency issues are the use of pyramidal groups to separate ownership from control, the entrenchment of controlling families, and non–arm's–length transactions (a.k.a. “tunneling”) between related companies that are detrimental to public investors. At present, we simply do not know if these agency problems are more serious impediments to general prosperity than those afflicting widely held firms.

To illustrate how these agency problems might be worse, we consider investment in innovation. The New Endogenous Growth Theory holds that the larger part of economic growth occurs as Schumpeterian “creative destruction” creates new wealth for entrepreneurs while destroying the value of old capital. 2 Established wealthy families who own the latter might consequently, and understandably, be reluctant to back much innovation. Recent empirical findings on R&D spending are consistent with this hypothesis, but it clearly requires much more proof. Moreover, although this would certainly slow economic growth, it might also be desirable from some perspectives. For example, it might ease social problems associated with redundant workers and obsolescent industries.

Without taking a final position on the social welfare consequences of vesting corporate control in old families, we argue that much more research is needed on family control. The contribution of this article is to underscore that that concentrated corporate control need not eradicate agency problems, especially in the large family business groups common outside the United States and United Kingdom.

The article proceeds as follows: Section 2 describes some basic corporate governance concerns in a widely held economy like the United States. Section 3 argues that different, but related concerns are important in economies in which family–controlled business groups are important players. Section 4 argues that the problems raised in section 3 are likely to be most important in older family firms. Section 5 presents an example, related to investment in innovation, where the problems raised in section 3 might be, potentially at least, more harmful than those raised in section 2. Section 6 concludes.

2. Corporate Governance—A Tale of Two Systems

Adam Smith's remark recalls the widespread fraud in an initial public offering (IPO) boom of widely held firms early in the eighteenth century. This episode in British financial history neatly encapsulates both the limitations and advantages of the family firm.

Large trading firms, such as the British East India Company and the Hudson's Bay Company, had been organized during the previous century as public joint stock companies because no single family had the capital or gambler's disposition necessary to build the fleets of ships and the networks of trading posts and forts these ventures required.

This need to pool capital and share risks captures the key limitation of the family firm. Even the wealthiest family's capital is limited, as is its willingness to take on great risks. Indeed, Chandra and McConaughy (1999) present evidence that U.S. family firms continue to pass up potentially profitable investments for these reasons. The solution British merchants devised was the widely held firm, where numerous investors pool capital to undertake a venture beyond the means of any individual investor. Since each investor's holdings are diversified across many widely held firms, and because individuals investors’ liability is limited, the widely held corporation can undertake ventures with risks greater than any family firm could accept.

The initial backers of these trading companies became immensely wealthy. Those left behind sought opportunities to catch up. An IPO boom of increasingly shady new joint stock companies met this demand. 3 These included the infamous South Seas Company, as well as ventures “to build salt works in the Holy Land,”“to build a wheel of perpetual motion,” and even “to undertake an investment of great advantage and no–one to know what it is.” When these companies collapsed, numerous prominent Britons were ruined.

These events capture the key limitation of the widely held firm. The managers are supposed to serve as agents of the firm's principals, its shareholders. When mangers serve their own interests instead, the widely held firms have an agency problem.

This episode in British economic history neatly highlights two key economic problems that underlie much of modern corporate finance. Agency problems make investors unwilling to entrust their wealth to others, and thus limit the scope of activity of widely held firms. Wealth constraints and risk aversion prevent wealthy families from undertaking certain ventures, and thus likewise limit the scope of activity of family firms.

2.1 The Managerial Model of Corporate Governance

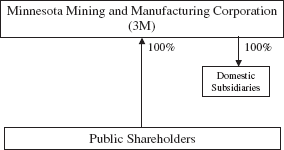

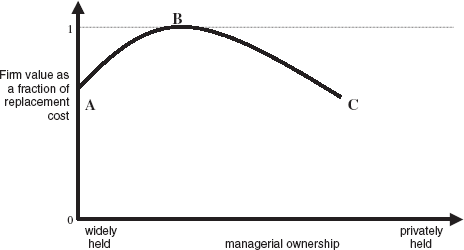

Over the subsequent centuries, the United States and United Kingdom developed corporate governance laws to limit the agency problems that afflict widely held firms. 4 Thus, Figure 1 illustrates the ownership structure of a typical large U.S. or U.K. firm. Professional managers run the firm, which is financed by a multitude of diverse shareholders. Berle and Means (1932), echoing Smith, argue that the managers of such firms still pursue their own interests and neglect shareholders. For brevity, we refer to this sort of agency problem as an other people's money problem. Jensen and Meckling (1976) argue that, all else equal, firm value should rise with increased insider ownership because managers are more attentive to shareholder value when they themselves are shareholders. The region between points A and B in Figure 2 illustrates this hypothesis.

A Typical Large U.S. Corporation

A Stylized Representation of Firm Value and Managerial Ownership in the United States

However, numerous studies, beginning with Morck, Shleifer, and Vishny (1988), find that firm value only rises with insider ownership where initial insider ownership is very small. Where insider ownership is already substantial, further insider equity ownership is associated with reduced shareholder value, as in the region from B to C in Figure 2. A possible explanation is managerial entrenchment: beyond a certain point, increased managerial ownership reduces the efficacy of the corporate governance mechanisms, surveyed by Shleifer and Vishny (1997), which constrain inept or faithless managers. Beyond point B, these detrimental effects of increased managerial ownership come to dominate its beneficial effects.

A vast literature on the corporate governance of widely held firms supports the general validity of Jensen and Meckling's (1976) model. 5 A lesser, but still large literature confirms the importance of managerial entrenchment. Although there is debate about the precise location of the “turning point” in Figure 2, the general importance managerial entrenchment is accepted. 6 Discussions of agency problems in the United States generally follow from these arguments.

2.2 The Family Model of Corporate Governance

An alternative solution to the problem of pooling capital and sharing risks, used in most other countries, is the family business group.

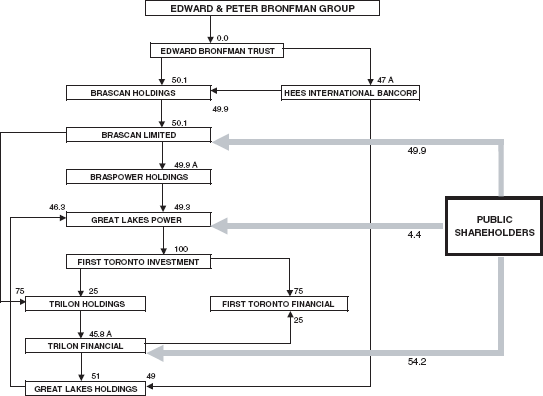

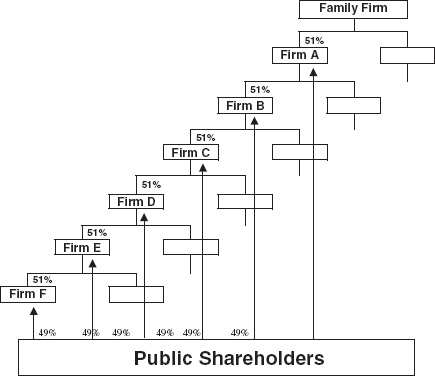

Figure 3 illustrates part of a typical family business group, that of the Toronto branch of the Bronfman family. This group contains several hundred firms and is too large to be illustrated in a single diagram. Figure 3 does, however, illustrate the characteristic structure of a family business group. A family firm controls other firms, each of which controls yet other firms, which in turn control yet more firms. Public shareholders are brought in to provide capital wherever necessary within this structure, but are never allowed a majority of the votes in any firm in the group. The essence of a family business group is captured in the pyramidal stylized representations of La Porta, Lopez–de–Salinas, and Shleifer (1999), Morck, Stangeland, and Yeung (2000), and others, shown in Figure 4.

A Typical Large Corporation in Other Countries: Part of the Bronfman Family Business Group in Canada

A Stylized Representation of a Family Business Group as a Pyramid

The family pools its capital with that of public investors, who also share the risks. Yet the family controls each firm in the group, and so can discipline self–serving managers. 7

Bebchuk, Kraakman, and Triantis (2000), Morck, Stangeland, and Yeung (2000), and others argue that family business groups can have serious corporate governance problems. They argue that the key difference between widely held firms and family business groups is that three agency problems in the former involve managers not acting for shareholders, while agency problems in the latter involve managers acting solely for one shareholder, the family, and neglecting other shareholders. 8

First, the family is entrenched in all the firms in the group, for it controls at least 51 percent of the votes in the shareholder meetings of every firm in the business group. Thus, entrenched management problems can occur.

Second, other people's money problems can also be severe in firms low in the business group's pyramidal structure. In Figure 3, the family only owns the family firm outright. It controls firm A with a 51 percent stake, and firm A controls firm B with a 51 percent stake, giving the family an actual stake of 25.5 percent in the profits of firm B. Firm B controls firm C with a 51 percent stake, giving the family a 12.75 percent stake in its profits. That is, the family pays only 12.75 percent of the cost of any losses by firm C. At each lower level in the pyramid, the family's real stake in the profits of the firm falls by half, so that when we get to firm F, the family bears less than 1 percent of any losses. 9 All else equal, other people's money problems should be as evident in firm F as in a widely held firm whose managers owned less than a 1 percent stake. Thus, firms in the lower pyramid levels can experience both other people's money problems and entrenchment problems concurrently.

Thus, unlike direct managerial ownership, intercorporate equity blocks in family groups do not mitigate other people's money problems. Nor do intercorporate equity stakes resemble the direct holdings of outside institutional investors, which Shleifer and Vishny (1986) argue also mitigate other people's money problems.

Finally, an additional way for insiders to misappropriate public shareholders’ wealth, called self–dealing or tunneling, presents itself in business group firms. Firms controlled by the same family often obtain goods, services, or financing from each other in the normal course of business. But by doing this at artificially high prices, the group can transfer profits from the buyer to the seller firm. Similarly, artificially low prices transfer profits from the seller to the buyer firm. Since the controlling family is entitled to less than 1 percent of the profits of firm F in Figure 3, but receives 51 percent of the profits of firm A, the family may be tempted to transfer profits from firm F to the family firm at the apex of the pyramid. In general, the controlling family gains by transferring as much wealth as possible from firms low in the pyramidal structure to firms at or near its apex. 10

Johnson et al. (2000) present several detailed case studies of business groups in which tunneling is alleged to have occurred. Gomez–Mejia, Nunez–Nickel, and Guiterrez (2001), Faccio and Lang (2001) and Claessens, Djankov, and Lang (2000) present econometric evidence consistent with the occurrence of such problems in family business groups in Western Europe and Asia, respectively. Bertrand, Mehta, and Mullainathan (2000) present preliminary cross–country evidence supporting the ubiquity of tunneling. Shleifer and Summers (1988) suggest that families might redistribute rents from employees to themselves.

In summary, all the firms in family business groups are vulnerable to managerial entrenchment problems. Firms many times removed from the controlling family by a chain of intercorporate ownership are also subject to other people's money problems. Both problems can be exacerbated by self–dealing transactions, through which the family transfers wealth from firms it controls, but in which its economic interest is slight, to firms it owns outright (or at least to firms in which its economic interest is greater).

3. Old Families and Corporate Governance

The vulnerability of family business groups to these corporate governance problems highlights the importance of the ethics and competence of the families to which corporate governance is entrusted in most countries in the world. If the family members in control of a business group are ethical and competent, the group can be a valuable asset to its economy. Otherwise, family business groups can become economic liabilities.

Most psychologists agree that intelligence is, at most, only partly an inherited genetic trait. 11 Inasmuch as business ability is a dimension of intelligence, empirical studies of family firms support this consensus. As noted above, empirical studies consistently find firms run by heirs underperforming not only similar firms run by founders, but also similar firms run by professional managers. 12 In addition, Pérez–González (2001) finds that announcements of scions replacing founders trigger stock price declines, while announcements of control passing to an outsider trigger increases in family firms’ stock prices.

These simple observations have profound implications for economies that depend heavily on family business groups. When corporate control passed from a highly able entrepreneur to the next generation, the heir is likely to be less able, and the heir's heir even less able. This means, that family business groups, that are national assets when run by a highly able patriarch, can become national liabilities when the scion takes over, and are even more likely to become liabilities when the next generation assumes corporate control.

In a widely held firm, shareholders can oust inept heirs, but in a family business group this is not possible because the family holds voting control over every firm in the group. La Porta, Lopez–de–Salinas, and Shleifer (1999) show that family business groups dominate many economies. Consequently, heirs may well inflict poor corporate governance on such a large fraction of an economy's productive assets to render themselves economic problems of macroeconomic importance.

Morck, Stangeland, and Yeung (2000) undertake a first pass at exploring this issue. After excluding the Unites States and United Kingdom, where family business groups are unimportant, they find that countries—in which billionaire heir wealth is large relative to GDP—grow statistically significantly more slowly than other countries with similar initial per capita GDP levels, education levels, capital accumulation rates, and self–made billionaire wealth. They argue that, in economies dominated by family business groups, inherited control can retard economic growth.

4. Creative Self–Destruction

An exhaustive study of this issue is beyond the scope of this article. Inherited wealth might, all else equal, be associated with low economic growth simply because each generation is a bit less able than its predecessor, and that extensive corporate control by heirs adversely affects corporate decision making on such a scale as to affect economic growth. Or, heirs might be less hardworking and ethical than the self–made, a hypothesis Holtz–Eakin, Joulfaian, and Rosen (1993) call the Carnegie Conjecture, after the U.S. billionaire Andrew Carnegie who advanced such views. However, numerous other explanations are also possible.

In this section, we propose an explanation based on the unwillingness of family business groups to invest in innovation, as opposed to political lobbying. We advance this explanation, not as an unequivocal conclusion, but as an example of the sorts of problems researchers should consider when studying family business groups. Our objective is to convince the reader that these problems are potentially important enough to merit serious consideration.

4.1 Creative Destruction

Schumpeter (1912, 1942), Romer (1986), and many others argue that investment in innovation is a key determinant of economic growth. Entrepreneurs devise innovations, and these innovations, when developed, raise the productivity of the whole stocks of the economy's existing capital and labor, causing economic growth. However, despite its overall positive effect on the economy, the innovation renders obsolete certain economic processes and the capital invested in them. This destruction of the value of some businesses caused by the creativity of others motivates Schumpeter (1912) to describe economic growth as “creative destruction.”

The new endogenous growth theory, advanced by Romer (1986) holds that innovations have positive externalities or spillovers. That is, innovation is a positive sum game. This is because an innovation, once devised, can be reapplied elsewhere. For example, compact disks, originally devised to record music, were reinvented as digital data storage devices. Likewise, electric lights were designed to illuminate darkened rooms, but also led to motion pictures, neon sign advertising, and heat lamps.

Romer (1986) argues that such positive externalities have increasing returns to scale. That is, they are more valuable if the economy's stocks of other assets are larger. This mutual increase in value due to spillovers from innovations allows a self–sustaining positive feedback loop that fuels long–term economic growth, as described by Murphy, Shleifer, and Vishny (1989).

4.2 Creative Self–Destruction

Creative destruction destroys the value of old capital, creating new wealth through innovation. The wealth of old, moneyed families is directly tied up in the economy's existing stock of capital. Consequently, it is the direct economic interests of old, moneyed families to subvert creative destruction by new innovative firms that compete with their established firms.

One way in which old, moneyed families might do this is to starve innovative upstarts of capital. Rajan and Zingales (2001) present an exhaustive historical study of financial institutions and argue that, having used these institutions to become wealthy, the elite in many countries then used their political influence to subvert these same institutions to lock in their positions. Olson (1963, 1982, 2000) explores these issues in detail, and we revisit them below.

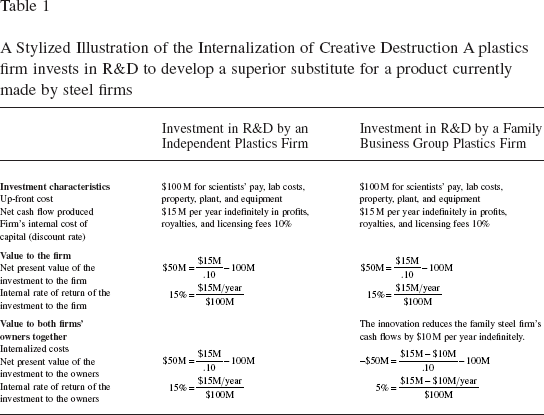

Another possibility is that old, moneyed families block creative destruction among their own firms. To see why this might occur, consider a family plastics firm that develops a superior substitute for a product produced by the family steel firm. The family might suppress the innovation to protect the cash flows of the steel firm. Table 1 compares the return to an independent plastics firm that develops this innovation to that of a family whose group firm does the same. The innovation costs the same to develop ($100M), and has the same benefit to the firm that develops it ($15M per year indefinitely) in both cases. If the family fully owns both firms, the family must bear the cost of its steel firm's losses ($10M per year indefinitely), the return to the family business group is only 5 percent, as opposed to 15 percent for the independent firm. At a 10 percent discount rate, the project has a +001$50M net present value for the independent plastics firm, but a −$50M net present value for the family group. Consequently, the innovation sees the light of day in an economy of independent firms, but not in the family business group economy.

A Stylized Illustration of the Internalization of Creative Destruction A plastics firm invests in R&D to develop a superior substitute for a product currently made by steel firms

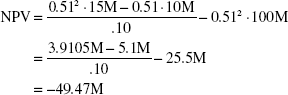

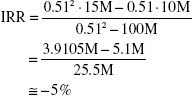

Some complications to this picture deserve mention. First, if a different family controlled the steel firm, the innovation might go ahead—unless the other family had an innovation that threatened the first family and could bargain to suppress the first innovation. Second, the situation in Table 1 can be exacerbated if the firms are controlled by the family, but held via pyramids of the sort illustrated in Figures 2 and 3. If the steel firm is closer than the plastics firm to the apex of a pyramidal family business group, the situation is exacerbated. The family then gets only a small part of the $15M per year benefit that accrues to the plastics firm, but pays a larger part of the costs inflicted on the steel firm. For example, if the steel firm is in level two of the pyramid shown in Figure 3, the family bears 51 percent of any hit it takes. If the plastics firm is in level three of the pyramid, the family gains only 25.5 percent (51 percent of 51 percent) of its added cash flow. The net present value of the innovation to the family is then

and the innovation's internal rate of return is

Allowing the innovation to proceed is clearly very harmful to the family's financial interests. In essence, creative destruction becomes creative self–destruction.

A restructuring that moved the steel firm lower in the pyramid is not a solution, because public shareholders, seeing the innovation waiting in the wings, would only buy shares in the steel firm at rock bottom prices.

The bottom line is that the family business group internalizes the destruction resulting from creative destruction. That is, the family gains from the plastics firm's innovation, but pays the full cost that innovation visits upon the steel firm. In contrast, if an independent firm produces the new product, the destruction is wrought upon others. This internalization of creative destruction induces a controlling family to “manage” innovation cautiously.

Consistent with these arguments, Morck, Stangeland, and Yeung (2000) find that Canadian firms controlled by heirs are statistically significantly less active in research and development than benchmark firms of the same age and size in the same industries. To see whether these results carry across to other countries, Morck, Stangeland, and Yeung (2000) then regress each country's private sector R&D spending on per capita GDP and on inherited and self–made billionaire wealth to GDP ratios. They find a highly statistically significantly negative relationship between private sector R&D and inherited wealth as a fraction of GDP.

4.3 Economic Institutions

That economywide private sector R&D spending is depressed in countries with substantial heir billionaire wealth is perhaps surprising. If old, established firms fail to innovate because of a fear of creative self–destruction, independent new firms should innovate all the more.

Of course, new innovative firms might not arise if they cannot raise capital, or are handicapped with onerous regulatory burdens. Morck (2000) argue that this is exactly what happens. They provide empirical evidence that old family firms in Canada enjoy preferential access to capital, and also that foreign investment in local firms is more severely restricted in countries with higher ratios of inherited billionaire wealth to GDP. Rajan and Zingales (2001) show that large companies in all developed countries were heavily dependent on stock markets for financing in their early years. They further show that, in some countries stock markets shrank dramatically after a pre–World War I zenith, and argue that this financial atrophy prevented innovative new firms from arising and left old family business groups entrenched in control. Thus, if the economic institutions that allocate capital across firms are tilted to favor old family group firms over their competitors, an economywide dearth of innovation might ensue.

Both Morck, Stangeland, and Yeung (2000) and Rajan and Zingales (2001) suggest that this is in fact the case in many countries. Veblen (1899, 1920), Krueger (1974), Olson (1963, 1982, 2000), and others emphasize the power of vested interests to influence government. Morck, Stangeland, and Yeung (2000) propose that old families manipulate their countries’ political systems to entrench themselves in this way. Morck (1995) proposes that old families excel at political lobbying because of the dependence of successful lobbying on connections, discretionary wealth, and an ability to act with discretion. Rajan and Zingales (2001) argue that the financial atrophy they document results from political lobbying by old, moneyed interests intent on erecting a barrier to entry to stymie competition.

Thus, while “managing” innovation may be optimal for the family, it can have the side effect of impeding overall economic growth. Some might argue that such “managed” creative destruction is socially superior to unhindered creative destruction, but it is important to keep in mind that the family is pursuing its own interests, not the general good. Conceivably, higher social welfare might incidentally result from these actions. But, there is at present no empirical evidence that social objectives, such as income equality or low unemployment, are better realized when overall economic growth is slower. Clearly, further study of the economic institutions in economies that depend heavily on family business groups is needed.

5. Conclusions

In most countries, most large firms are parts of family business groups. We have argued above that such structures could conceivably give rise to agency problems at least as serious as those known to afflict widely held firms. In widely held firms, the concern is that professional managers may fail in their fiduciary duty to act for public shareholders. In family business group firms, the concern is that managers may act for the controlling family, but not for shareholders in general. We explore various possible agency problems of this sort in family business groups, and consider where they might be most important. We then go through an example showing how family business groups can blunt the incentive to innovate by internalizing the costs of creative destruction.

At present, we simply do not know which set of agency problems are worse, and we clearly need more research in this area. This need is especially urgent at present because postcommunist and emerging economies are presently choosing between the Anglo–U.S. and the family business group models of corporate ownership. Research into the problems of widely held firms is abundant, while research on family business groups is only beginning—perhaps because the latter are absent in the United States and United Kingdom, where most corporate governance research is done. This asymmetric focus could color critical policy decisions in some countries.

Footnotes

1.

De Cordoba, J. (1995). Heirs battle over empire in Ecuador. Wall Street Journal. December 20.

2.

See e.g., Aghion & Howitt (1997); ![]() .

.

3.

See MacKay (1841) for an overview of these events.

4.

See Shleifer and Vishny (1997) and La Porta et al. (1997, ![]() ) for details.

) for details.

6.

Shleifer and Vishny (1989) model managerial entrenchment. Johnson et al. (1985) show that firm's share prices typically rise on the news that very old CEOs have died in office, indicating that shareholders have come to view that these managers are liabilities rather than assets. Such managers would presumably have been removed were they not entrenched. Morck, Shleifer, and Vishny (1988) find that, while U.S. firms run by founders have elevated share prices, the share prices of U.S. firms run by heirs are depressed. Morck, Stangeland, and Yeung (2000) find that large Canadian firms controlled by heirs perform more poorly than benchmark firms the same size and age in the same industry, while firms run by founders outperform those benchmarks. ![]() find similar evidence for U.S. family firms. These situations should not persist unless the heirs are entrenched.

find similar evidence for U.S. family firms. These situations should not persist unless the heirs are entrenched.

8.

9.

The family's fractional entitlement to the firm's profits is .517 = .897%.

10.

Note that tunneling can occur when the managers of widely held firms control private firms with which the public firm does business, as was apparently the case in the Enron scandal of 2002 in the United States.

11.

12.

See footnote 4.