Abstract

This research note tests whether extraordinary high growth (e.g., sales growth rates of 500 percent to 31,000 percent over five years) is correlated to firm profitability. Using longitudinal data from three separate cohorts of Inc. 500 firms (from 1992 to 1996; 1993 to 1997; and 1994 to 1998), firm growth was operationalized in terms of sales and number of employees. Controlling for industry sector and ranking on the Inc. 500 lists, analyses found that extraordinary high growth—in terms of sales and number of employees—was not related to firm profitability. Firm age, however, was significantly, and inversely, related to profitability; younger firms experience slightly higher profitability rates. Implications for management and future study of extraordinary high–growth firms are discussed.

Introduction

Many scholars have suggested that firm growth creates employment, wealth, and broad economic development. For example, “firms that grow at rates in excess of 20 percent”—or what Birch (1987) dubs “gazelles”—contribute prominently to job creation in the U.S. economy (Fischer, Reuber, Hababou, Johnson, & Lee, 1997). Surprisingly, and despite its economic upside potential, growth research has focused predominantly on “normal” to “high” growth rates (5 percent to 20 percent) (cf. Ardishvili et al., 1998; Davidsson & Wiklund, 2000; Delmar, 1997) while overlooking formidably high growth or “hyper–growth” such as 500 percent to 30,000 percent. To this end, this article explores whether extraordinary high–growth firms can achieve profitability while growing, or whether such firms are likely to be unprofitable as they attempt to overcome the hurdles of change while achieving significant size.

The literature review suggests that value of growth for the success of firms is viewed in two conflicting ways. Briefly, the first perspective holds that firm growth is a precursor to the achievement of a sustainable competitive advantage and profitability. Larger firms have higher rates of survival compared to smaller firms (Aldrich & Auster, 1986) and firm size is often associated with favorable economies of scale (Porter, 1985). On the other hand, the second perspective sees the process of rapid firm growth as leading toward a series of sizeable hurdles that diminish a firm's ability to generate profits (Gartner, 1997). This, in turn, may create internal friction capable of hindering normal operating procedures or even lead to complete failure (Hambrick & Crozier, 1985). Following the method and results sections, we conclude this study with a detailed discussion, where we outline the implications and make concrete recommendations for further research on firm growth.

Literature Review

As suggested above, there are two dominant yet divergent views regarding firm growth. The view that rapid growth could lead to high profitability is based on evidence suggesting that new firms become more profitable when they enter markets quickly and on a large scale (MacMillan & Day, 1987). High–growth firms that have achieved substantial market share may be able to generate economies of scale or first mover advantages that will eventually result in profitability (Lee, Smith, Grimm, & Schomburg, 2000). For example, early access to distribution channels, securing favorable contracts with suppliers, buyers, and rivals, as well as spreading supervisory costs across larger numbers of employees may lead to more favorable prices. As larger firms have higher survival rates (Aldrich & Auster, 1986) and firm size economies of scale are related (Porter, 1985; 2001), firm growth is seen as an important indicator of firms’ health and market potential. In addition to greater operational scope, some extraordinary high–growth firms, such as Amazon.com, have created value and brand name recognition through high stock prices for shares sold through public stock offerings even though they have, often for prolonged periods of time, generated substantial losses (Spector, 2000). Capitalizing sales gains into high stock valuations, without regard to profits, may be short lived and inappropriate for valuing firms (Porter, 2001), yet it is expected that—over time—profitability will reduce its lag time behind sales growth. Finally, growth–oriented firms may be more likely to attract extraordinary management talent (Penrose, 1959) as well as financial support from investors, allies, and competitors. Growth, therefore, is assumed to be beneficial and something that entrepreneurial firms should attempt to achieve (Sexton & Smilor, 1997).

In sharp contrast to the above rationales, high growth might also create numerous problems and challenges (Churchill & Lewis, 1983; Greiner, 1972; Kazanjian, 1988; Shuman & Seeger, 1986). To be more explicit, Hambrick and Crozier (1985) identified four fundamental challenges—instant size, a sense of infallibility, internal turmoil and frenzy, and extraordinary resource needs—that high–growth firms must solve. Findings also show that different organizational life cycles call for different managerial priorities (Smith, Mitchell, & Summer, 1985). For example, entering a high–growth stage may necessitate shifts in firm structure, reward system, and methods of decision making. A fast–growing company may need to quickly hire many new employees, additional space, equipment, supervisors, and mechanisms to train, educate, monitor, control, and coordinate its new taskforce. While some high growth might successfully overcome the myriad problems that growth engenders, many “stumble” (Hambrick & Crozier, 1985). For example, rapid growth in the number of employees hinders knowledge transfer; it might alter a company's internal structure and dilute or erode its original culture and entrepreneurial spirit. Finally, expeditious expansion in marketing, sales, and consumer service may expose companies to additional perils (Barr, 1998). In a review of research on the strategy of high–growth firms, Hoy, McDougall, and D'Souza (1992) concluded that the pursuit of high growth may be minimally or even negatively correlated with firm profitability. In sum, addressing new needs, meshing fast changes into current operations, and coping with increased managerial complexity, may lead to a momentous upsurge in costs (Covin & Slevin, 1997).

Although the scope of research on new venture growth has increased in recent years, (cf. Ardishvili et al., 1998; Davidsson & Wiklund, 2000; Delmar, 1997), empirical evidence on the specific link between growth and profitability remains mixed. Using a longitudinal database of 45,525 firms, Sexton, Pricer, & Nenide (2000), found that firm profitability was correlated with sustainable growth. Firms that could finance growth through internally generated funding were more profitable than firms with uncontrolled or unbridled growth. On the other hand, Shuman and Seeger (1986) found no statistical relationship between firm growth and financial performance in their studies of small high–growth firms. In a similar vein, Chandler and Jansen (1992) discovered that sales growth and profitability were not correlated. Others report that although product innovation has been associated with improved market share, rapid market expansion was negatively related to financial and marketing performance (Manu, 1993). Likewise, profit increase was not related to the growth and expansion of the law firms (Weisbord, 1994).

While arguments can be marshaled for both perspectives, conceptual and anecdotal evidence lean more heavily toward a view that extreme expansion—500 percent to 30,000 percent growth over short periods of time—is exceedingly strenuous and thus to be negatively correlated to firm profits. Hence we suggest the following hypothesis:

Extraordinary high–growth rates—as measured by sales and employment—are negatively correlated to profitability.

Method

Sample

There are many challenges to identifying, selecting, and measuring the characteristics of extraordinary high–growth entrepreneurial firms (Brush & Vanderwerf, 1992; Camp et al., 1999; Chandler & Hanks, 1993; Delmar, 1997; Mata, 1994; Weinzimmer, Nystrom, & Freeman, 1998, to name a few). A key difficulty, of course, is the lack of longitudinal databases from which to draw a representative sample of the fastest–growing entrepreneurial firms in the country. While there is easy access to accounting information on any publicly traded companies, financial data on young, privately held, firms remain largely undisclosed. To be fair, large–scale datasets—such as ones compiled by Dun and Bradstreet, the Small Business Administration, or Kauffman Longitudinal Financial Statements database of over 45,000 firms—are quite useful for studying diverse management questions, but they are not designed to specifically spotlight the fastest growing companies in the nation. Indeed, firms in the Kauffman Longitudinal Financial Statements database are growing at a rate substantially lower than the Inc. 500 firms (e.g., from 22.1 percent in retail to 84.2 percent in construction) (Sexton, Pricer, & Nenide, 2000). The Inc. 500 firms with their 559 percent to 31,000 percent hyper–growth rate, therefore, are firms with extraordinary growth no other dataset is currently providing.

Unlike most research on firm growth, our study focuses uniquely on the link between profitability and very intense growth (i.e., hyper–growth as measured by hundreds to thousands of percent). As such, the Inc. 500 firms with their 559 percent to 31,000 percent hyper–growth rate were the focus of our study. Also, the Inc. dataset is checked and verified by certified public accountants, and unlike small–scale, regional, cross sectional or survey–based studies, the sample is both large enough to be meaningful and it provides a five–year longitudinal perspective on companies from around the country. As suggested by Davidsson and Wiklund (2000), because growth is an ongoing process, research on firm growth should be based on longitudinal data.

To be more precise, at the end of every year, Inc. Magazine publishes a list of the 500 fastest growing privately held companies in the United States, where firms are ranked by sales growth over a five–year period. For example, at the end of 1996, Optiva had the highest five–year sales growth rate of 31,507 percent, while Telogy Networks, had the lowest growth rate of 559 percent. Because the yearly ranking yields national publicity, many thriving companies apply to be listed on the Inc. 500. The selected firms must be privately held, report at least $200,000 in sales, and show a sales increase. In sum, the Inc. 500 is a longitudinal dataset of privately held, high–growth companies from around the nation. The data used in this study traced the growth of three cohorts of firms. These include firms on the 1997 Inc. 500 list (from 1992 to 1996); the 1998 Inc. 500 list (from 1993 to 1997); and the 1999 Inc. 500 list (from 1994 to 1998). We also used an aggregated dataset based on all three cohorts combined (1997, 1998, and 1999).

Procedures

Inc. 500 publications provide rich longitudinal data that include: (a) company name and “rank”—1 to 500—on the list; (b) date the company was founded and a short business description; (c) total number of employees for year one and year five; (d) five–year sales growth; (e) absolute dollar sales in year one and year five; and finally, (f) profit in percent range for year one and year five (e.g., A = 16 percent or more; B = 11–15 percent; C = 6–10 percent; D = 1–5 percent; E = 0 percent; and F = loss). Adhering to this presentation, two of our control variables included company age and rank, where rank reflects a firm's relative growth. Analyses of U.S. firm–growth patterns indicate that industry may have an important effect on firm–growth rates and profitability (cf. Camp et al., 1999; Lumpkin & Dess, 1995; Sexton, Pricer, & Nenide, 2000). To this end, a content analysis, conducted independently by each author, sorted the business description given in Inc. publications into four binary business–sector categories including service, manufacturing, distribution, and retail. Thus, other control variables were three dummy codes to capture industry sectors.

Following suggestions made elsewhere, we operationalized growth as absolute and relative measures of sales and number of employees (Delmar, 1997; Weinzimmer, Nystrom, & Freeman, 1998). For example, subtracting sales figures at year one form sales figures at year five captured absolute growth in sales. Similarly, subtracting the number of employees at year one from the number of employees at year five captured absolute growth in employment. We obtained the relative growth measures of sales and employment by dividing the absolute growth measures described above by, respectively, sales and number of employees at year one. We focused our growth measures on sales because of the consensus that sales “are the best growth measure” and it “has high generality,” and on the number of employees, because of the broad economic implications of job creation (Davisson & Wiklund, 2000, p. 37).

Since firm profits were codified as letters rather than numbers, we operationalized profits for year one and year five by recoding the ordinal scale used by Inc. Magazine as follows: A = 20 percent; B = 15 percent; C = 10 percent; D = 5 percent; E = 0 percent; and F = −10 percent. Two reasons motivated us to rely on uneven increments for loss. First, while Inc. Magazine is somewhat explicit about positive profits or breakeven, its ambiguity regarding losses hints that large negative earnings were likely. Second, and more important, our phone interviews with Inc. Magazine's representatives confirmed that it was not uncommon to attain a 10 percent loss. Taken together, we operationalized “F” as minus 10 percent. 1 All in all, the growth measures (i.e., absolute and relative sales, number of employees, and profits) offer important commonality with empirical work on firm growth done in the past and, thereby, further future theoretical and construct development (Davidsson, 1991; Davidsson & Delmar, 1997; Delmar, 1997; Weinzimmer, Nystrom, & Freeman, 1998).

Analysis

While we performed stepwise hierarchical regressions on both absolute and relative growth and profitability, since findings from both types of growth measure were highly similar, the correlation and regression tables showcase only the models on absolute growth and profitability. The four separate stepwise hierarchical regressions included one for each of the three five–year cohorts (1992–1996, 1993–1997 and 1994–1998), and then for the dataset that encompassed all three cohorts. We reasoned that attaining similar results on all four analyses would confer stronger convergent validity. Of the 1,500 firms identified in the combined dataset, 267 firms were listed on two or more lists. To avoid repeated measures, we only retained data for the first year a firm appeared on the list. In each analysis, the control variables—firm age, rank, and three industry dummy codes—were entered as a block in Step 1. Next, in Step 2, we entered the variables that capture absolute growth in employment and in sales. This allowed us to examine whether growth in employment and in sales—over and above the control variables—were significantly related to growth in profits. The test of the hypothesis is provided from the findings that indicate the sign and level of statistical significance of the regression coefficients of the growth variables (sales and employment). These analyses also show the amount of unique variance in profit growth that is accounted for by growth in sales and employment.

Results

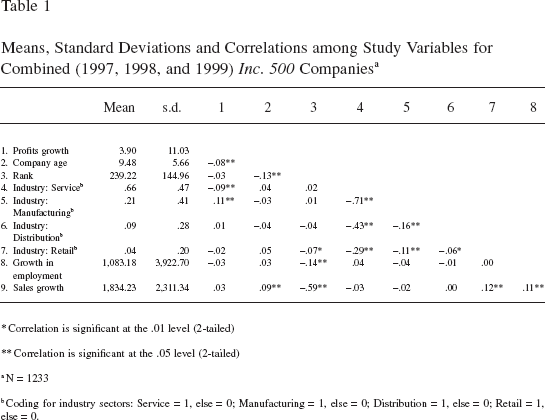

Table 1 provides means, standard deviations, and correlations for the combined dataset (1992–1998) of the Inc. 500 firms.

Means, Standard Deviations and Correlations among Study Variables for Combined (1997, 1998, and 1999) Inc. 500 Companies a

Correlation is significant at the .01 level (2–tailed)

Correlation is significant at the .05 level (2–tailed)

N = 1233

Coding for industry sectors: Service = 1, else = 0; Manufacturing = 1, else = 0; Distribution = 1, else = 0; Retail = 1, else = 0.

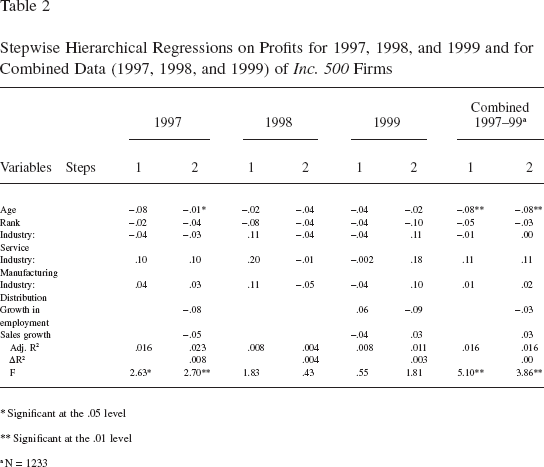

While the correlation matrix presented in Table 2 provides limited insights about associations among variables, it is interesting to note that only firm age and service and manufacturing (industry sectors) were significantly related to profit growth. Nonetheless, the low correlations are admittedly weak despite the large sample size (N = 1,233). Following assessment of the correlation matrix, separate stepwise hierarchical regressions—for each Inc. 500 cohort, as well as for a combined dataset of all firms from 1992 to 1998—tested whether absolute or relative growth in either sales or in employment predict profit growth. As explained earlier, the first step in each regression equation controlled for company age, rank, and industry sectors, and followed with Step 2, which included growth in employment and sales. Regression equations for each individual cohort and for the combined cohort generated nearly identical findings: Neither absolute nor relative growth (in either sales or employment) were associated with profit growth. Thus, our hypothesis regarding the negative relationship between profitability and growth in sales and employees was not supported. Interestingly, company age was the only significant predictor of profit growth. That is, younger firms were more likely to have an increase in profitability, over time, than older firms. The models, despite the large sample size, explained less than 2 percent of the variance in profitability. In the interest of conciseness and since all equations yielded very similar results, Table 2 presents only the equations for absolute growth.

Stepwise Hierarchical Regressions on Profits for 1997, 1998, and 1999 and for Combined Data (1997, 1998, and 1999) of Inc. 500 Firms

Significant at the .05 level

Significant at the .01 level

N = 1233

Discussion

Extraordinary–growth firms garner national visibility and esteem from the business community for their formidable high growth, yet they are largely excluded from academic research. We attempted to correct this oversight. First, we classified Inc. 500 firms as hyper–growth—rather than high–growth—companies. Second, by asking whether extraordinary high growth corresponds to formidable profits, we provided an empirical view about growth–profitability relationships among this sample of extraordinary high–growth firms. We found that growth rate (in sales or employees) of Inc. 500 firms is unrelated to profitability. This finding was surprising as we, like others before us, reasoned that extraordinary growth poses significant hazards to the longevity and viability of emerging companies. For example, over a five–year period the high–ranked Inc. 500 firms are growing hundreds of times their original size, whereas the lower–ranked Inc. 500 firms were “merely” growing at five to six times their original size. One might assume, therefore, that companies that are growing at rates that are 50 times higher than other firms might have lower rates of profitability. This was not the case.

Why was there no relationship between growth in sales and employment and profits? While our analyses and the data do not allow causal inferences, one plausible explanation is a larger lag effect. Lag effects have been identified in many performance studies including strategic management and top management team (Murray, 1989), executive pay (Balkin, Markman, & Gomez–Mejia, 2000), operation management (Boyer, 1999; Riezebos & Gaalman, 1998), and marketing (Ganesh & Kumar, 1996). For example, there is a 20–year lag effect between the appearance of research in the academic community and its impact on productivity in the industry (Adams, 1990). Given the nonsignificant relationship between extraordinary growth and profitability reported in this research, there may be a lag effect longer than the five–year data provided for these firms.

It is equally plausible that hyper–growth draws tremendous (external) capital, which more than offsets growth–related difficulties. Extraordinary growth creates an attractive image that bestows greater credibility and draws powerful strategic allies and partners (Kale, Singh, & Perlmutter, 2000). This, in turn, may facilitate economies of scale, access to inexpensive distribution channels (to circumvent barriers to entry), knowledge fusion, and technology transfer. Extraordinary growth may also attract exceptional talent that in turn increases efficiencies and productivity. While it is possible that extraordinary growth garners offsetting benefits, this proposition is beyond the scope of our study and is thus awaiting empirical testing.

The stepwise hierarchical regression analyses reported in Table 2 show that firm age was significantly related to profitability; younger companies tended to be more profitable than older companies. This is not a surprising finding, because as companies grow, so is the difficulty of maintaining the same rate of growth (Christensen, 1997). Similarly, age is a function of time, and as companies mature and grow they expand hierarchically and thus experience increased complexity (Baker & Cullen, 1993). This may necessitate costly organization–wide changes in administrative policy, control mechanisms, and infrastructure, all of which may account for some of the inverse relationship between profits and age.

Measuring growth based on initial size echoes caveats made by other scholars who suggest that different firm sizes and different measures provide very different growth options (cf. Davidsson & Wiklund, 2000). Delmar (1997) noted that the decision to rank firms’ growth based on relative sales—rather than absolute—creates a bias in favor of small firms. As exemplified below, percentage sales growth will tend to celebrate the smaller firms who can have a larger percentage of sales increase on the same absolute sales growth as their larger counterparts (Christensen, 1997). Thus, measures of relative growth favors firms that start with smaller sales figures or fewer employees (Davidsson & Wiklund, 2000). To this end and as explained earlier, we used two measures, but neither relative growth in sales nor in employment was correlated to change in profitability.

Nonetheless, and as suggested above, once all but the dummy measures were log–transformed, our hypothesis was actually supported. To be more precise, under log–transformed analyses, sales and employees were statistically and negatively related to profits. Hence, how growth is analyzed may have an abstruse impact on insights into organizational growth. To this end, we undertook a variety of additional tests (e.g., discriminant analysis, split sample, and so forth) on the data and we found consistent results with what we reported earlier. Most interestingly, even a test that compared the top and bottom 20 percent of the Inc. companies (i.e., companies ranked 1 through 100 with companies ranked 401 through 500; raw data) showed no significant differences in profitability. Thus, the convergent finding that—for our samples of Inc. 500 firms—growth in sales and number of employees is unrelated to profitability, holding all else equal, appears to be a fairly robust result. To recap, using different measures and analyses yet obtaining similar results suggests that (nontransformed) growth in sales and employment—for our samples of extraordinary high–growth firms—is unrelated to profits.

This research note has several insights for research, theory, and practice. One clear conclusion from this study is that extraordinary high growth, as demonstrated by the companies studied here, is probably not related to profitability. Extraordinary growth rates were distinct from profitability, even after we controlled for firm age, industry, and ranking, despite the large sample size, and even when we compared the lower–ranking firms with the highest–ranking firms. Lack of demarcation among extraordinary high–growth firms may suggest that while growth in sales and employment garnered these companies’ prominent place on the Inc. list, these constructs foretell very little about a company's profitability and success. One plausible implication of this is that hyper–growth firms might not be fully amendable to traditional financial measures or that we should apply more diverse performance measures. For example, traditional metrics such as growth in sales or profits, return on capital employed (ROCE), or cash flow, are inappropriate for young pharmaceutical and biotech firms that are illustrious for losing money during their early years. We hope that future studies will pursue new economic and noneconomic yardsticks (e.g., respectively, economic value added—(EVA)—and brand name recognition) to gauge the performance of super high–growth firms.

One factor that does seem to reflect a similarity for most firms in the database is age. The median age of firms at the beginning of their five–year extraordinary growth was two years. Given the finding that firm age was a better (though clearly not perfect) predictor of profitability, it appears that Inc. 500 firms, as a sample, reflect a group of predominantly young firms that undergo an extraordinary spurt of growth. Given that the median sales for Inc. 500 firms at the beginning of their five–year extraordinary growth was above $600,000, one plausible conclusion is that Inc. 500 firms are able to handle change. For example, Inc. 500 firms grew substantially larger than most firms that are less than two years old (Aldrich & Auster, 1986).

While our research note provides the foregoing implications and conclusions, one should carefully assess some of the inherent limitations associated with growth studies and possible avenues for future research. For example, our data came predominantly from a single source—Inc. 500 publications. While the fact that the business press endorsed these firms after public accountants certified firms’ financial statements gave us confidence in the data, the problem of single–method bias in growth studies remains an issue (Davidsson, 1991; Davidsson & Delmar, 1997; Delmar, 1997; Weinzimmer, Nystrom, & Freeman, 1998). We therefore hope that future studies on growth and profitability may address this challenge more thoroughly. Similarly, we hope that Inc. Magazine will expand its data collection efforts to explore a wider variety of factors and firm characteristics that might be correlated to extraordinary growth, and that this information be made available for empirical analysis. Finally, we conclude with a caveat. While failure to find any significant relationship between profitability and extraordinary growth in sales and employment might imply that a strategy of high growth would entail few consequences to a firm's profits, managers who pursue high growth must be reminded that Inc. 500 companies are the exception, rather than the rule.

Footnotes

*

A version of this paper was presented at Babson College/Kauffman Foundation Entrepreneurship Research Conference, Columbia, South Carolina, May 13–15, 1999. The authors would like to thank two anonymous reviewers for their insights and suggestions during the revision process.

1.

Sensitivity analyses (with loss as low as 5 percent or high as 15 percent) yielded the same findings as we report in our results section. We thank an anonymous reviewer for this suggestion.