Abstract

This study sheds light on the evolution of the specialized marketing capability, pricing. We develop an operationalization for and empirically validate the pricing–capability dimensions from the perspective of the resource–based view. Using a sample of 420 technology–based ventures, we examine the relationship between pricing capabilities and firm performance, with a particular focus on how age and uncertainty impact these relationships to determine how entrepreneurial firms can profit. We deconstruct pricing capability into four dimensions—price discrimination, dynamic orientation, performance goal orientation, and value delivery—to show, for example, that young companies should focus on their price discrimination capability to improve performance.

Introduction

Because of changes in the current economy, companies’ ability to achieve competitive advantage no longer depends on their manufacturing assets but on intangible assets like marketing experience (Ramaswami, Srivastava, & Bhargava, 2009). Studies have shown the performance–enhancing effects of marketing capabilities (e.g., Krasnikov & Jayachandran, 2008; Morgan, Slotegraaf, & Vorhies, 2009; Morgan, Vorhies, & Mason, 2009; Vorhies & Morgan, 2005) and that marketing capabilities have more impact on performance than R&D or operational capabilities do (Krasnikov & Jayachandran). Pricing is considered a specialized marketing capability (Vorhies, Morgan, & Autry, 2009) and centrally important in the specialized marketing capabilities framework. As Rao argues, “price is the only marketing mix variable that generates revenues; all others involve expenditures (or possibly investments) of funds” (Rao, 1984, p. S39). In the same vein, Piercy, Cravens, and Lane (2010) show the strategic importance of pricing in harsh economic conditions. Other researchers emphasize the effect that pricing has on firms’ profits (Lancioni, 2005; Marn & Rosiello, 1992). Reuber and Fischer (2005) confirm that, especially for entrepreneurial companies, pricing should be considered in the marketing mix. Entrepreneurial firms usually struggle with pricing because they operate in new, unknown environments without referential prices, which leads to the danger of under– or overpricing. If they start at a low price level, firms endanger their margins, and if the price level is too high, they risk potential customers’ being unwilling to purchase their products or services (Simmonds, 1999).

The broad focus of studies that analyze the relationship between specialized marketing capabilities and firm performance reveals no explicit insights regarding the particular performance effect of pricing capabilities in the context of either established or entrepreneurial firms (e.g., Morgan, Vorhies et al., 2009). Those studies that do capture the performance–enhancing effect of pricing use operationalizations at a high level of abstraction (e.g., Vorhies & Morgan, 2005) and call for more fine–grained measures (Vorhies et al., 2009). Dutta, Zbaracki, and Bergen (2003) show that pricing consists of complex routines and processes, so a detailed analysis and operationalization of the pricing capability dimension is necessary.

Dutta et al. (2003) argue that firms use the price–setting process, a capability that combines routines, skills, types of expertise, coordination mechanisms, and other difficult–to–imitate resources, to gain and sustain a competitive advantage (Dierickx & Cool, 1989; Peteraf, 1993; Wernerfelt, 1984). Based on the routines and processes that Dutta et al. identify as relevant, we pursue an exploratory approach and develop four dimensions that reflect firms’ pricing capability: price discrimination, performance goal orientation, dynamic orientation, and value delivery. Accordingly, our first research questions are:

Out of which underlying routines are the dimensions of pricing capability assembled? How do the dimensions of pricing capability impact firm performance?

According to Welsh and White (1981), entrepreneurial firms have certain characteristics—primarily youth and environmental uncertainty—that differentiate them from their more established counterparts. These characteristics suggest that “classic” marketing principles, most of which have been derived in the context of large, established firms, may not be applicable to entrepreneurial firms (Berthon, Ewing, & Napoli, 2008; Hills, Hultman, & Miles, 2008).

Because of their youth, entrepreneurial firms typically lack historical data (Romanelli, 1989), which makes it more difficult for them to execute pricing routines like collecting customers’ purchase histories or tracking the results of past pricing actions (Dutta et al., 2003). In addition, environmental uncertainty prevents entrepreneurial companies from predicting market movements easily, such as movements in production techniques (Gruber, 2003). Accordingly, it is challenging to perform required pricing routines like the definition of functionally equivalent products and the assessment of potential product alternatives for customers (Dutta et al.) because alternative products might emerge from completely unexpected competitors from other industries. Accordingly, whether entrepreneurial companies can profit from the same pricing capabilities that established companies do is subject to debate. Therefore, our third research question is:

How does the importance of the pricing capability dimensions change for entrepreneurial companies?

Our study makes three main contributions. With the first, which relates to the broader marketing capability literature, we identify and operationalize the specific marketing capability of pricing in order to clarify its detailed effects (Vorhies et al., 2009). With the second, which contributes to entrepreneurial marketing literature, we argue theoretically and show empirically that entrepreneurial firms should develop specific pricing capabilities but not necessarily the same capabilities as those of established firms. Thus, this study is among the first in the entrepreneurial marketing literature to build on large–scale empirical data to confirm differences in marketing phenomena between entrepreneurial firms and established firms, as this literature stream has been dominated by conceptual and case–study research (Brettel, Engelen, Müller, & Schilke, 2011). Third, our study shows that the resource and capability–based view is appropriate theory with which to explain the performance of entrepreneurial firms (Autio, George, & Alexy, 2011). This insight contributes to the broader entrepreneurship literature, which has been criticized for its lack of theories (Amit, Glosten, & Muller, 1993). In so doing, our findings refute claims that the resource–based view (RBV) is not suitable in the entrepreneurial firm context since these typically young firms cannot build firm–level capabilities (Sapienza, Autio, George, & Zahra, 2006; Sine, Mitsuhashi, & Kirsch, 2006).

Theory and Hypotheses

Pricing Capability as a Specialized Operational Marketing Capability

Whereas most research on pricing concentrates on external determinants, such as the competitive situations that determine a firm's pricing tactics (e.g., Noble & Gruca, 1999; Tellis, 1986), this paper follows Dutta et al. (2003) in considering pricing a specialized operational marketing capability that is grounded in the RBV. In their case study of a large manufacturing firm, Dutta et al. go beyond the external determinants of pricing to focus on the internal processes and routines that enable a company to set its prices successfully. Their study identifies two challenges related to pricing: the external challenge of setting new prices in response to competitors’ pricing strategies and the internal challenge of implementing the adjusted prices in the firm's internal pricing system. According to Dutta et al., pricing is a capability that is “based on the combination of routines, coordination mechanisms, systems, skills, and other complementary resources that are difficult to imitate” (p. 619); it takes a firm approximately 5 years to develop a pricing system, and the pricing capability cannot be learned through a training program but must evolve over time and from experience. Moreover, Dutta et al. show that a strong pricing capability enables firms to generate higher rents through such means as improving the match between prices charged and customer value.

According to the RBV, achieving a competitive advantage (Barney, 1991) requires heterogeneous resources that are valuable, scarce, difficult to imitate, and non–substitutable (Dierickx & Cool, 1989). Dutta et al. (2003) show that these conditions apply to pricing by describing pricing's two main activities as price setting within the firm and in regard to customers. Among Dutta et al.'s findings is that the pricing process is inimitable and imperfectly mobile (nontransferable) because a firm cannot simply buy the pricing systems and skills required for effective pricing but must design, develop, and enhance a proprietary pricing system to ensure it is suitable for both the firm's requirements and those of its customers. In addition, as an extension of the RBV, the capabilities perspective argues that value creation by firms is driven not only by resources but also by capabilities (Grant, 1996), which are the multifaceted collections of skills and expertise that are embedded in a company's processes (Helfat & Peteraf, 2003). Marketing capabilities in particular evolve from knowledge about customer needs (Day, 1994), so these capabilities are difficult to codify (Simonin, 1999). In line with that reasoning, Morgan, Slotegraaf et al. (2009) and Krasnikov and Jayachandran (2008) show that marketing capabilities cannot be adapted by rival firms easily and that they are difficult to imitate, which makes them an important and sustainable resource for achieving competitive advantage.

Based on Dutta et al.'s (2003) exploratory analysis and on insights from the marketing capabilities research stream (Krasnikov & Jayachandran, 2008; Morgan, Slotegraaf et al., 2009; Morgan, Vorhies et al., 2009; Vorhies & Morgan, 2005), we develop a pricing capability construct that is comprised of four dimensions: price discrimination, the dynamic orientation of pricing, performance goal orientation, and value delivery. Based on these dimensions, we define pricing capability as the ability to integrate resources in order to determine the most promising price for maximizing profit. Therefore, companies need price–setting routines in which the pricing team members combine their varied skills, experiences, and functional backgrounds to determine the optimal price for customers, taking into account competitors’ prices and the product value the firm has created. Therefore, in what follows we define and exemplarily connect each pricing capability dimension with its underlying routines. Each dimension evolves out of a combination of external routines in which the company interacts with a third party (e.g., customers) and firm–specific internal routines (e.g., information transfers) (Day, 1994; Dutta et al.).

We define the price discrimination dimension as a firm's ability to adapt prices to various target groups (Tellis, 1986). The essential internal activity in this dimension is the price–setting strategy (Dutta et al., 2003), which includes routines for collecting customer data from former purchasers and the ability to communicate pricing decisions to customers in such a way that they accept the price change. The external routines and skills for this action include the ability to incorporate customers’ responses into future price changes and sufficient knowledge to anticipate customers’ reactions (Dutta et al.).

The dynamic pricing orientation refers to a firm's ability to set prices strategically and to include long–term market developments in its decision. An essential internal activity for this dimension is the identification and assessment of competitors’ prices and the identification of competitors’ underlying routines and product changes (Dutta et al., 2003). One routine for dealing with the external stimuli of customer response is the preparation of negotiation materials (Dutta et al.).

The third dimension, performance goal orientation, reflects the continuous improvement of processes (e.g., method application) in order to enhance the firm's performance. Necessary internal activities are identifying competitors’ prices and translating pricing strategy into actual prices. The corresponding external skills include nested routines for tracking competitors’ prices and nested conflict–resolution routines. An important routine for this dimension that enables the firm to negotiate with its customers is the assessment of customers based on past performance and available alternatives (Dutta et al., 2003).

Finally, the value delivery dimension refers to the ability to keep customers with the product and to ensure their satisfaction with its price (Athanassopoulos, 2000; Hallowell, 1996). The required internal activity is the identification of competitors’ prices through internal routines like defining functionally equivalent products. Important external routines for convincing customers that a price change is fair are information exchanges with the customers’ pricing systems and/or preparation of price change presentations that educate the company's own pricing team on how to educate customers.

Marketing in Entrepreneurial Firms

The major tenet of the entrepreneurial marketing literature is that marketing concepts from established firms cannot be adopted easily by entrepreneurial companies but must first be adapted to their specific requirements (Berthon et al., 2008; Hills et al., 2008). To date, the entrepreneurial marketing literature has been dominated by conceptual and case–study work, which has provided first insights into the marketing of entrepreneurial firms but is not generalizable or based on empirics (Brettel et al., 2011).

In order to derive the specifics of pricing in entrepreneurial firms theoretically, we argue that entrepreneurial firms differ from established firms in two major ways: entrepreneurial firms are younger (Stinchcombe, 1965), and they typically face more environmental uncertainty (Bjerke & Hultman, 2002). These two factors have been consistently stated as major characteristics of entrepreneurial firms in the entrepreneurship—and, more specifically, in the entrepreneurial—marketing literature (Gruber, 2004).

Stinchcombe (1965) argues that new firms face certain challenges because of their youth. Typically, these companies lack a broad knowledge base (Stinchcombe) because of their lack of historical data (Romanelli, 1989), which results in restricted capabilities to anticipate (for example) market changes. Moreover, especially in the beginning, these firms struggle because they are focused on establishing roles, structures, and processes that are feasible for all employees (Stinchcombe). This orientation phase requires much of employees’ and managers’ capacity. Furthermore, in the beginning the young firm has no established relationships with external parties like customers and suppliers (Stinchcombe), and their lack of reputation in the market (Gruber, 2004) makes it difficult to build such relationships. Such companies often stay small until they have acquired the necessary reputation (Freeman, Carroll, & Hannan, 1983), and smallness is connected with scarce financial and human resources (Aldrich & Auster, 1986; Carson, Cromie, McGowan, & Hill, 1995). However, young age also brings certain advantages. Khavul, Pérez–Nordtvedt, and Wood (2010) state that young firms are less formalized and more flexible than established firms. Similarly, researchers like Kazanjian and Drazin (1990) argue that young firms usually have flat hierarchies and low levels of bureaucracy, both of which enable them to adapt quickly to changes, saving them money and time (O'Dwyer & Ryan, 2000).

As the second primary characteristic of entrepreneurial firms (Bjerke & Hultman, 2002), environmental uncertainty describes the high level of turbulence in the companies’ surroundings, which limits the predictability of (for example) the potential marketing acceptance, customer reactions, and production techniques, (Gruber, 2003). In general, the behavior of all external market participants is unknown and difficult to forecast in an entrepreneurial context. This effect is augmented by the fact that entrepreneurial firms often create new industrial sectors, which tend to evolve quickly and to underlie radical changes (Robertson & Gatignon, 1986; Shepherd & Shanley, 1998).

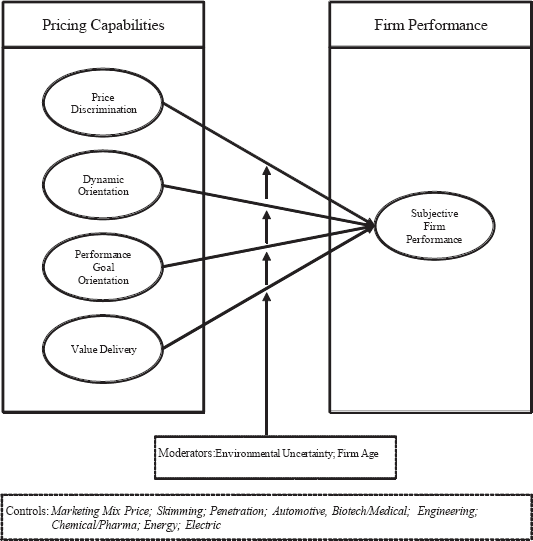

In the following, we link the four pricing capabilities theoretically to firm performance based on the RBV and argue, based on the particularities of entrepreneurial firms, whether these performance relationships are stronger for young or old and for uncertain or certain environments. Figure 1 depicts the research model.

Research Model Pricing Capabilities

Derivation of Hypotheses

Price Discrimination Capability

Based on the RBV and Dutta et al.'s (2003) insights regarding pricing capabilities, we derive hypotheses that link the four pricing dimensions to firm performance. The price discrimination capability requires a firm to consider the heterogeneity of its customers in setting prices (Tellis, 1986) based on their distinguishing characteristics. The price offered may depend on the distribution channel a customer uses, on the amount of product a customer purchases, or on a customer's level of loyalty (Khan & Jain, 2005). Composing the right portfolio of offers necessitates a substantial knowledge base related to customers’ and competitors’ behaviors (Chintagunta, Dubé, & Singh, 2003; Montgomery, 1997).

Certain routines are necessary for the price discrimination dimension: the firm must identify its relevant competitors and their corresponding product offerings by applying a routine for tracking prices, collect information on its customers’ purchasing behavior, and anticipate its customers’ reactions to the price change in order to communicate the change effectively (Dutta et al., 2003). The efficient use of the price discrimination capability should enable the company to gain and sustain competitive advantage (Dutta et al.) because it enables the firm to negotiate better prices with their heterogeneous target groups than their competitors do. As Marn and Rosiello (1992) show, a 1% increase in prices affects a firm's profit more strongly than a 1% increase or decrease in other profit drivers, such as cost or units sold. Moreover, Dutta et al. argue that superior capability in the identification of price–insensitive customers results in the ability to charge higher prices, which leads to higher profitability on the company level. Slater and Narver (2000) argue that such capabilities allow firms to identify underserved targets, thereby growing revenues by expanding market share (Morgan, Anderson, & Mittal, 2005). Therefore, we state:

Next, we seek to determine whether a company's price discrimination capability retains its performance–enhancing effect in an entrepreneurial context. Therefore, the next two hypotheses focus on the two main characteristics of entrepreneurial companies: youth and environmental uncertainty.

Because young companies frequently rely on a comparatively small customer base that often consists primarily of former business relationships, they have ample knowledge about these first customers (Carson, 1985; Tyebjee, Bruno, & McIntyre, 1983). Moreover, the first relationships between a young company and its customers tend to be close. In most cases, start–ups gather information about the needs of their first customers by first developing a customized product using a trial–and–error process (Zahra, Sapienza, & Davidsson, 2006) that enables them to determine the degree to which its customers value certain product features. However, the situation is different when it comes to information on potential customers because the young firm's limited knowledge base (Romanelli, 1989) restricts its ability to forecast potential customers’ behavior. Even so, the firm's youth could be an advantage for the new venture since youth facilitates flexibility and direct communication internally, leading to faster decisions (Gruber, 2004), a product that is shaped according to customers’ wishes, and a possible first–mover advantage. Hence, we suggest:

Dutta et al. (2003) argue that uncertainty regarding customers’ reactions makes the pricing process more demanding. A highly relevant resource for the price discrimination capability is knowledge about how customers differ (Tellis, 1986). To compose the right portfolio of prices and acquire comprehensive knowledge about customer behavior, the company must be aware of its competitors’ behavior and strategic actions (Chintagunta et al., 2003; Dutta et al.). Examples of relevant skills include those related to understanding customers’ price sensitivity, developing and executing a negotiation strategy, and acquiring knowledge about competitors’ offerings (Dutta et al.). It is difficult to collect this data in an uncertain environment because new competitors may enter the market, suppliers may become competitors, and new products from other industries may appear on the market as substitution products (Tushman & Anderson, 1986). These uncertainties render it more difficult to forecast customers’ and competitors’ behavior and to predict and analyze the consequences of strategic actions (Robertson & Gatignon, 1986; Shepherd & Shanley, 1998). In contrast, managers in more stable markets can draw on their existing knowledge, established heuristics, and rules of thumb (Burns & Stalker, 1966) to determine their pricing tactics. Therefore, we state:

Dynamic Orientation Capability

The required routines for the dynamic pricing dimension focus on the firm's activities related to identifying competitors’ prices and anticipating customers’ reactions (Dutta et al., 2003). The internal pricing routines include routines to assess competitors’ prices and planned product changes. The company also has to handle its customers’ reactions, so it must provide its pricing team negotiating materials in order to negotiate successfully with customers. The combination of these routines should lead to a competitive advantage in the market (Dutta et al.) by allowing the company to adapt its prices to relevant market movements. A superior dynamic orientation capability fosters the company's growth by enabling it to set a price that its customers are willing to pay and that prevents them from buying competitors’ products. This capability also allows firms to ask the optimal price without reducing its number of customers or their purchase amounts (Dutta et al.). Accordingly, we hypothesize that:

Next, we seek to determine whether a company's dynamic orientation capability retains its performance–enhancing effect in an entrepreneurial context, so the next two hypotheses focus on age and environmental uncertainty.

The underlying routines for the dynamic pricing capability include routines for tracking competitors’ price settings and routines regarding the customers, such as learning and talking about customers’ responses to price. The unique combination of those intangible routines leads to a competitive advantage in the market (Dutta et al., 2003).

Because of the youth that characterizes entrepreneurial firms, these routines are comparatively easy to implement. Research shows that young ventures tend to be more flexible and less formalized than established companies (Gruber, 2003), enabling them to use their resources and routines in line with the RBV through continuous enrichment and development of resources (Montgomery & Wernerfelt, 1988; Peteraf, 1993). Close, informal relationships among the members of young firms, such firms’ typically flat hierarchies and the distribution of knowledge and decision making into cross–functional teams enhance the firms’ convertibility (Schoonhoven, Eisenhardt, & Lyman, 1990; Stinchcombe, 1965) and result in cost and time savings (Bjerke & Hultman, 2002). Furthermore, a young firm can adjust its intangible resources to environmental changes easily (Schoonhoven et al.; Stinchcombe), giving it a competitive advantage through the first–mover effect, while more established companies must cope with organizational obsolescence and a mismatch between organizational competencies and environmental demands (Barron, West, & Hannan, 1994). Therefore, we conclude:

Since the underlying pricing routines for the dynamic pricing capability are tracking the competitors’ price settings and translating the knowledge about customer responses into price changes, this capability depends heavily on real–time information and widespread communication within the firm, so managers must develop intuition about their markets. In an uncertain and unpredictable environment, the dynamic pricing capability allows a firm to recognize changes early on and to turn them into opportunities (Eisenhardt & Martin, 2000). Acting under high uncertainty is a classic situation for entrepreneurial firms because of the unpredictability of the economic environment in general and since those companies have caused change themselves (Miller & Friesen, 1982; van Gelderen, Frese, & Thurik, 2000). Therefore, we argue that the dynamic pricing capability, which relies on simple routines that create new knowledge (Eisenhardt & Martin), fosters firm performance especially well in companies that face a high level of external uncertainty. Hence, we state:

Performance Goal Orientation Capability

The performance goal orientation dimension is characterized by the continuous enhancement of employees’ abilities to accomplish tasks, so some researchers have proposed that internal and external pricing factors, such as negotiating positions and needs and desires, can change over time (Katz–Navon & Goldschmidt, 2009).

Important activities for this capability are the identification of competitors’ prices and the translation of the firm's pricing strategy into actual prices. Therefore, the company has to focus on the continuous improvement of routines to track competitors and solve conflicts with customers. Organizations must also develop their skills in negotiating price changes, so they must enhance their customer–assessment skills (Dutta et al., 2003). As Brandenburger and Stuart (1996) show, firms’ abilities to leverage customer value differ since their negotiating skills differ. Based on a firm's unique combination of routines, the performance goal orientation capability enables it to gain a competitive advantage in the market by anticipating changes and taking the corresponding actions (Dierickx & Cool, 1989). As a result, it can set a price that is superior to those of its competitors. Therefore, we conclude:

To determine whether a company's goal orientation capability retains its performance–enhancing effect in an entrepreneurial context, the next two hypotheses focus on firms’ youth and environmental uncertainty as two main characteristics of entrepreneurial firms.

Performance goal orientation is characterized by a permanent improvement in the firm's ability to improve how it performs its tasks, but insights from the field of absorptive capacity show that a firm first must be able to acquire the relevant external knowledge and process the new information successfully (Cohen & Levinthal, 1990). Because of their youth, young companies have only sparse marketing experience and knowledge (Gruber, 2004), while their more established counterparts have accumulated necessary experiences and routines over time (Hannan & Freeman, 1984; Stinchcombe, 1965). Older firms have an advantage in combining new information efficiently with their existing knowledge base, while young companies seldom know which operational routines they need to implement for this kind of teamwork or have developed environmental scanning routines. Therefore, we state:

Because the capability of performance goal orientation requires information on what customers value, firms have to collect data on their customers in order to determine what discounts to grant based on past performance (Dutta et al., 2003). Such routines are particularly necessary in highly uncertain environments, where they help to secure the high customer–retention rate that is essential for high–value customers. However, these routines may have less impact on firm performance in stable environments than in dynamic ones because the future moves of customers and competitors in stable environments are more predictable, and it is easier to keep customers satisfied with standardized prices. Therefore, we argue:

Value Delivery Capability

The value delivery dimension focuses on the company's ability to keep its customers satisfied with an offer, so it is a result of how the customers perceive the product or service quality relative to its price (Athanassopoulos, 2000; Hallowell, 1996). According to Slater and Narver (2000), this capability can provide new insights concerning which of the firm's offerings customers value most. The value delivery capability is characterized by routines like constantly monitoring functionally equivalent products, but the company must also be able to convince the customer of a price change's fairness, so routines like information exchange with the customers’ pricing system (Dutta et al., 2003) are also helpful. Gathering this knowledge is a team effort, as the firm must determine which competitors’ products can be compared to the company's own offer, decide how to convince the customer that the price change is fair, and decide on a strategy to avoid negative customer reactions based on insights about competitors’ equivalent product offerings. Depending on the firm's product portfolio, this process can be complex because of the need to obtain data not only on how pricing affects their direct customers but also on how it affects their distribution partners’ customers (Dutta et al.). If firms implement these routines successfully, they can use their value delivery capability as a basis for a competitive advantage (Peteraf, 1993) because it enables them to operate with an advanced price perception in the customers’ minds. Moreover, based on the acquired knowledge about what customers appreciate about the firm's offerings, the firm may be able to lower its average costs by improving how it matches product features with customer requirements. Hence, we state:

The next two hypotheses examine whether a company's value delivery capability retains its performance–enhancing effect in an entrepreneurial context, by focusing on firm age and environmental uncertainty.

Because of their lack of reputation (Gruber, 2004), young firms often sell their products to their personal networks (Tyebjee et al., 1983) or to early adopters (Hills & LaForge, 1992), a customer group that differs from the customers in the general market. For example, early adopters tend to be less price sensitive than the general market (Moore, 2002), assigning more value to innovation, personalized solutions, and highly qualified sales and support service than to low price (Slater & Mohr, 2006). Personal contact with a customer, which young entrepreneurial firms typically have, also makes it easier to assess the product's value to that customer and to set an adequate price. Moreover, because of the flat organizational hierarchies and flexibility of young organizations (Gruber), the actions required to ascribe prices to the product features customers value are likely to be performed quickly and inexpensively. However, as a company ages, a significant change in the customer base occurs. Whereas young companies sell products to price–insensitive customers who focus on superior service and innovation or to customers with which they have close personal contacts, more established firms must serve the mass market to be profitable (Moore), and customers in the mass market are typically risk–averse, price–sensitive slow adopters (Slater & Mohr). Therefore, the entire pricing concept and all pricing processes must be realigned as the company ages, a process that can take years to establish (Dutta et al., 2003); once the first pricing concept has become obsolete, the company must undergo a trial–and–error learning process to develop a reconfigured pricing concept for the mass market. This process is at once expensive and time consuming because of the established firms’ organizational rigidity that makes it more difficult to develop and implement new routines (Barron et al., 1994). Therefore, we postulate:

In highly uncertain markets, the typical environment of entrepreneurial firms, the value delivery capability is particularly important to gain and sustain a competitive advantage. This capability requires skills like technical expertise with competitors’ products and planned product changes (Dutta et al., 2003). Using this capability, the company can offer its consumers the best purchase option available in the market. Therefore, according to our reasoning in hypothesis 4b based on Moore's (2002) customer types, the firm must have a broad knowledge about its customers, including insights regarding its customers’ customers (Dutta et al.). Moreover, regarding product innovations, several scholars argue that uncertainty motivates firms to search for opportunities and adapt to changes quickly (Baldridge & Burnham, 1975; Miller & Friesen, 1984; Utterback, 1971). Therefore, the value delivery capability is particularly useful for companies in highly uncertain markets because it allows the company to respond to changing market needs and situations in advance. Hence, we state:

Method

Sample

To test our hypotheses, we gathered data by means of an online questionnaire. The companies included in the survey were drawn randomly from the membership data of the German Chamber of Industry and Commerce with the objective of covering a broad range of companies in terms of size and age. We focused the study on technology–based companies by selecting specific industry affiliations. Members of top management were selected as relevant key informants for the survey because they have the most comprehensive overview of their organizations (Kumar, Stern, & Anderson, 1993) and so are the most knowledgeable about their companies’ pricing policies and procedures. In the spring of 2008, we contacted via personalized e–mail one managing director from each of 3,378 technology–based companies and invited him or her to participate in our survey. After sending two reminder e–mails to nonrespondents, we received 420 responses, corresponding to a response rate of 12.4%. According to Klassen and Jacobs (2001), the response rate for online surveys should exceed 9%, so our response rate meets this requirement.

We chose multiple hierarchical regression analysis with interaction terms (Baron & Kenny, 1986; Cohen & Cohen, 1983) for the data analysis (Fornell & Bookstein, 1982). To validate our hypotheses, we conducted multiple regression analyses with the respective interaction terms and reduced the likelihood of multicollinearity by standardizing the mean–centered values of all independent variables to form interaction terms (cf. Aiken & West, 1991).

As Armstrong and Overton (1977) recommend, we tested the sample for nonresponse bias by comparing early and late respondents and found no significant differences between the two groups, so nonresponse bias is not a concern. Since measurement of the dependent variable in our survey followed the measurement of the independent variables, and since the dependent and independent variable data were gathered from a single informant, following Podsakoff and Organ (1986), we conducted a Harman's single factor test. We found 11 factors with an eigenvalue larger than 1.0, with no one factor accounting for the majority of the variance among the measures. Therefore, a common method bias does not present a difficulty in our data.

Measures

Following Churchill (1979), we developed the survey instrument based on established constructs whenever possible. All measures used a 7–point Likert–type response scale, and we specified all measures as reflective constructs (Jarvis, Mackenzie, Podsakoff, Mick, & Bearden, 2003). To establish reliable, valid measures that reflect pricing capabilities (Churchill; DeVellis, 2003), we developed multi–item scales for all facets of a company's pricing capability. After performing a literature review of associated research streams to generate initial constructs, we conducted several rounds of interviews with researchers and practitioners to identify the most relevant items for pricing capabilities. In line with Churchill, we then analyzed two large independent empirical samples to develop a reliable, valid scale for pricing capability and chose 11 items to reflect a company's pricing capability: three items for price discrimination, three items for dynamic orientation, four items for performance goal orientation, and one item for value delivery. Appendices 1 and 2 describe the scale development and display the pricing capability scale.

Since firm performance is complex and challenging to assess (Dess & Robinson, 1984), we measured it as a multidimensional construct reflecting a firm's profitability, customers, and market. Therefore, we measured firm performance with five subjective items (Pelham, 1999) that asked the respondents to indicate how satisfied they were with their firms’ performance relative to its competitors’ performance (Covin & Slevin, 1989; Pelham). Gathering the perception of performance, rather than performance data, is especially advantageous in the context of small, privately held companies like the new ventures that make up part of our sample, since these companies often consider this kind of information to be classified (Fiorito & LaForge, 1986), and there is little, if any, public data available. In addition, the interpretation of subjective, relative performance data is easier and more precise when performed across a range of contexts, such as across industries (Covin & Slevin).

We measured the moderating variable of age based on the year of company's foundation, provided by the respondents. A threshold of 10 years was applied to categorize a company as a young or an established venture. We also divided the sample into companies that act in highly dynamic environments and companies that act in more stable environments, as measured by three items: “In our industry sector, actions of competitors are unpredictable,” “Demand and customer tastes are fairly difficult to forecast,” and “Our products/services have short life cycles; the rate of obsolescence is very high.”

As control variables for our research model, we included the relevance of pricing as a marketing–mix instrument; several pricing strategies, including skimming and penetration; and industry affiliation. These items are shown in Appendix 2.

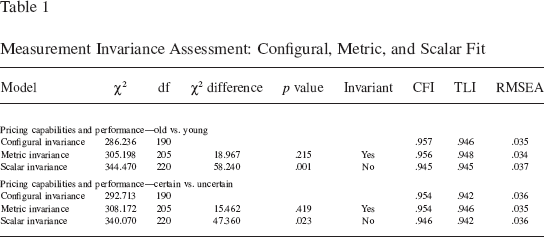

To determine whether the groups in our sample can be compared, we tested for measurement invariance following Steenkamp and Baumgartner's (1998) procedure, which shows whether measures are comparable across contexts and recommends fitting a sequential set of increasingly constrained multi–group structural equations. We used covariance–based structural equation modeling (AMOS 21.0, IBM, Chicago, IL, USA) to conduct this procedure. In the first step, we tested for configural invariance (representing the same pattern of factor loadings) by allowing the scale indicators to load freely on the construct in all four groups. Then we used the configural model as a baseline model, with which a restricted model was compared to test for metric invariance (equal loadings) and scalar invariance (equal intercepts). As depicted in Table 1, the results show that our models achieve configural and full metric invariance.

Measurement Invariance Assessment: Configural, Metric, and Scalar Fit

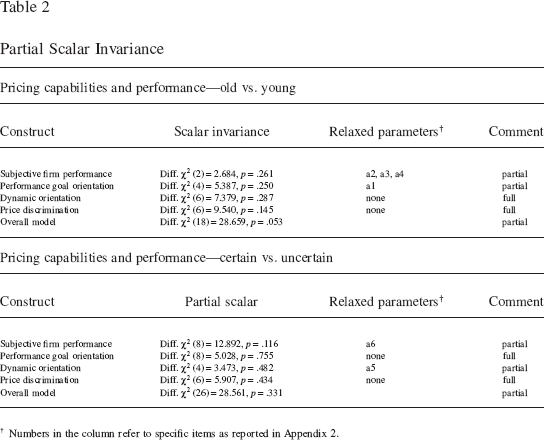

However, because of significant increases in χ2, the results did not support full scalar invariance, so we had to relax some parameters in order to achieve partial metric invariance. The results are depicted in Table 2. Overall, the test indicates equivalence of our measurement scales and that our constructs are comparable within the groups of old vs. young companies and stable vs. dynamic environments.

Partial Scalar Invariance

Numbers in the column refer to specific items as reported in Appendix 2.

Findings

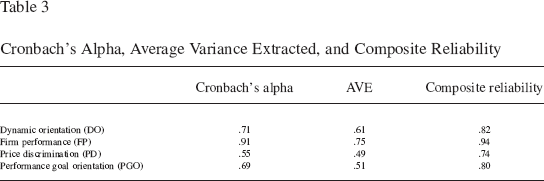

We conducted a confirmatory factor analysis using the software package AMOS 21.0 to assess measurement reliability and validity. To ensure reliability, we eliminated items with factor loadings less than .4 (Hulland, 1999). We calculated Cronbach's alpha (threshold = .6), composite reliability (threshold = .6), and average variance extracted (AVE) (threshold = .5) and achieved satisfactory reliability for most constructs (DeVellis, 2003). Moreover, our results indicate a sufficient model fit (χ2/df = 2.92; goodness–of–fit index (GFI) = .92; adjusted goodness–of fit–index (AGFI) = .90; comparative fit index (CFI) = .91; Tucker–Lewis Index (TLI) = .90; root mean square error of approximation (RMSEA) = .068; standardized root mean square residual (SRMR) = .0826). Table 3 shows the results of these calculations.

Cronbach's Alpha, Average Variance Extracted, and Composite Reliability

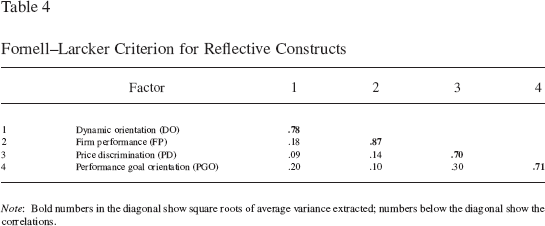

Next, we analyzed discriminant validity. According to Fornell and Larcker (1981), sufficient discriminant validity is present when a construct shares more variance with its measures than it does with other constructs in the models. Table 4 shows that most reflective constructs correspond to this condition. We also tested for item discriminant validity and achieved satisfactory levels since all items shared more variance with their own constructs than with any other construct. Overall, satisfactory discriminant validity is present at both the item level and the construct level.

Fornell–Larcker Criterion for Reflective Constructs

Note: Bold numbers in the diagonal show square roots of average variance extracted; numbers below the diagonal show the correlations.

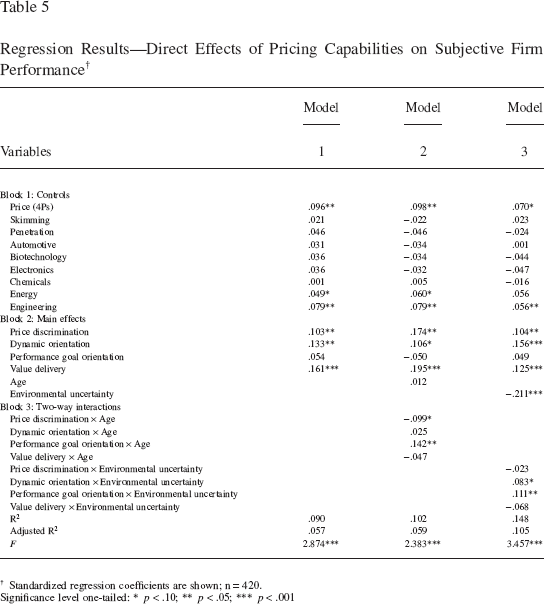

We used multiple regression models with interaction terms to validate our hypotheses. In line with Chan, Yim, and Lam (2010), interaction terms consisted of the research model's independent variables and the two moderators, age and external uncertainty. After entering the control variables (model 1; Table 5), we integrated the independent variables (model 2; Table 5), and finally the interaction terms (model 3; Table 5).

Regression Results—Direct Effects of Pricing Capabilities on Subjective Firm Performance †

Significance level one–tailed

Standardized regression coefficients are shown; n = 420.

p < .10

p < .05

p < .001

Hypotheses 1a, 2a, and 4a, which postulate the performance–enhancing impact of price discrimination, dynamic orientation, and value delivery, were confirmed. We rejected hypothesis 3a, which postulates the positive impact of performance goal orientation on firm performance because of an insignificant path coefficient.

Hypotheses 1b–4b stated a positive moderating influence of age on the relationship between the four pricing capabilities and young companies’ firm performance. We confirmed hypotheses 1b (β = −.099; p = .085) and 3b (β = .142; p = .034), validating the stronger impact of price discrimination on performance for young companies and performance goal orientation for established companies, and rejected hypothesis 2b and 4b because of insignificant path coefficients.

The moderating impact of uncertainty was hypothesized in hypothesis 1c, hypothesis 2c, hypothesis 3c, and hypothesis 4c. We rejected hypothesis 1c and hypothesis 4c because of insignificant path coefficients but confirmed hypothesis 2c (β = .086; p = .047) and hypothesis 3c (β = .111; p = .014), corroborating the importance of dynamic orientation and performance goal orientation in uncertain environments.

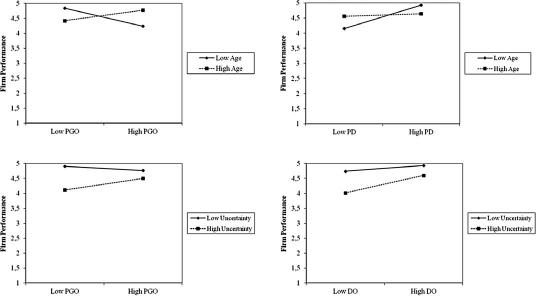

Table 5 shows the corresponding path coefficients and significances, and Figure 2 illustrates the two–way interaction effects.

Significant Two–Way Interactions

Discussion

Implications for Theory

To the best of our knowledge, this is the first study to develop a conceptualization and operationalization of the specialized marketing capability of pricing, and the study's examination of the direct impact of the pricing capability dimensions on firm performance contributes to the marketing management literature. Most importantly, the study's focus on the dimensions of pricing capability shows that entrepreneurial firms, which are typically characterized by young age and pronounced environmental uncertainty, profit from pricing capabilities that differ from those of more established firms, so the study contributes to the entrepreneurial marketing literature and the broader entrepreneurship literature.

Until now, most research on pricing has centered on the role of external determinants like competition in deriving a pricing tactic (e.g., Noble & Gruca, 1999; Tellis, 1986), but it has been particularly sparse in dealing with the pricing strategies of entrepreneurial companies. Researchers have shown that young companies need a pricing strategy (Gruber, 2005; Terpstra & Olson, 1993) and that their approach to pricing differs from that of established firms (Hills et al., 2008), but insights into how entrepreneurial and non–entrepreneurial companies should develop their pricing capabilities are lacking. Based on insights from Dutta et al.'s (2003) case study, our study is the first to develop and validate empirically an operationalization by which to measure firms’ internal pricing capabilities. Our first research question is answered by the development and validation of the four dimensions of the dynamic pricing capability—price discrimination, dynamic orientation, performance goal orientation, and value delivery—and by theoretical explanations of how firms develop these capabilities on the basis of internal and external routines, processes, expertise, and skills (Dutta et al.). As for the second research question, our results confirm that pricing capabilities in general have a performance–enhancing effect.

With regard to our third research question, the importance of these four dimensions changes in an entrepreneurial context, where we show that only price discrimination is more important for young firms than for established ones. The ability to develop internal routines and processes that reflect the needs of customer is an essential success factor for young firms, which are characterized by rapid growth, making the ability to adapt organizational structures necessary (e.g., Greiner, 1972; Tyebjee et al., 1983). Rapid development necessitates continuous adjustment of the underlying internal routines and processes required for the price discrimination dimension. When a new venture develops internal routines and processes, it must ensure that they facilitate its ability to understand customer needs and the value of the benefit it delivers to customers, detects patterns in customers’ needs and their willingness to pay, and approaches new customer groups with different characteristics with different offers.

We find that dynamic orientation has a significant impact on firm performance in firms that act in dynamic environments, which supports our supposition that dynamic orientation enables firms to develop simple routines and processes that are easy and quickly adaptable to their environment. Performance goal orientation is also important for companies that act in dynamic environments, confirming the theory that this capability is based on simple routines that enable companies to remain flexible and to generate new knowledge so they can anticipate changes in the market and turn them into opportunities.

This study contributes to entrepreneurial marketing research by analyzing the relationship between pricing capability and performance based on a large sample of new technology–oriented ventures. Whereas the extant literature on entrepreneurial marketing focuses mainly on conceptual contributions (Hills et al., 2008), our study empirically validates the relationship between pricing and firm performance in entrepreneurial settings—represented by young firm age and high levels of environmental uncertainty—using a large–scale empirical study. The pricing capability should be one of the first steps in a step–by–step marketing approach because firms can leverage new resources and develop required capabilities based on their early sales (Morris, Schindehutte, & LaForge, 2002). Beyond that, firms with efficient pricing capabilities are more likely to avoid under– and overpricing, which are often pitfalls when new firms introduce products to the market (Simmonds, 1999).

This work also resumes the discussion about the importance of capabilities in entrepreneurial firms. There is little extant research on capabilities in the entrepreneurial literature (Autio et al., 2011; Zahra et al., 2006), perhaps because entrepreneurship scholars reason that the lack of capabilities may be an entrepreneurial advantage, especially in turbulent environments where strong capabilities can evolve into inertia (Sapienza et al., 2006; Sine et al., 2006). However, Autio et al. argue that both new and established organizations “draw on existing routines developed in prior environments and initiate task–focused actions to execute specific tasks” (2011, p. 12). This study empirically validates Autio et al.'s view that the development of capabilities is as important for young companies in gaining and maintaining a competitive advantage as it is for established companies, but our results reveal that entrepreneurial firms and established firms do not profit from the same capabilities. Therefore, a nuanced investigation of required capabilities in an entrepreneurial setting is necessary. Accordingly, we show that the RBV can be a valuable theoretical lens through which to explain entrepreneurial firms’ performance and call for future research to shed more light on the capability development in an entrepreneurial context in general and the evolution of entrepreneurial marketing capabilities like selling and marketing communication in particular.

Our study is subject to some limitations that suggest useful opportunities for further analyses. One such opportunity is a replication of this study in other national or cultural settings in order to validate the scale development and provide insights into the impact of culture on the path–dependent and context–based development of dynamic pricing capabilities. Future research could also examine ventures in other industries and compare findings to our study of technology–based ventures. Other studies could focus on the internal and external routines, processes, skills, and expertise that cross–functional teams use to determine prices, which would help to clarify how those teams handle the codified and tacit knowledge that underlie these capabilities.

Managerial Implications

Our study provides insights into the evolution of pricing capabilities in technology–based ventures by explaining the internal routines and processes that such ventures must have in order to develop a successful and unique pricing capability. We suggest that managers not concentrate solely on external determinants when they set their prices but rely also on the internal capabilities that enable them to create a competitive advantage based on their pricing. We recommend that managers focus their pricing tactics on the dimensions of price discrimination, dynamic orientation, and value delivery, which enable managers to track developments in the market and adapt their products and prices accordingly and in a timely way.

However, managers should also consider that different contextual situations suggest advantages for different combinations of the components of pricing capability. In particular, managers of entrepreneurial firms should take care in choosing the capabilities in which they invest. Based on the results of our study, we recommend that these managers pursue a step–by–step development of pricing capabilities, starting with the price discrimination capability. For this particular pricing capability, the ability to develop broad knowledge about customers’ requirements and competitors’ actions is an essential skill if a young firm is to compete successfully in the market. Managers in highly dynamic environments should concentrate on dynamic orientation and performance goal orientation by developing routines like production cost estimations (experience curve effects) and creating customer–oriented condition budgets.