Abstract

We use the articles and commentaries in this special issue to reinvigorate the theme of family business governance and extend its scope beyond the single business, single–family approach that has traditionally dominated the family business literature. Through a discussion of the implications of the articles and commentaries included in this special issue we begin to chart a new and expanded research program for governance that addresses the challenges of the large and complex multifamily and/or multibusiness family enterprise. We hope to encourage research in a direction that will add significantly to our understanding of business families’ contributions to the global economy.

Introduction

This article introduces the 12th special issue in the ongoing series “Theories of Family Enterprise” published in Entrepreneurship Theory and Practice. These articles and commentaries represent a portion of those presented at the 2014 Theories of Family Enterprise Conference in Edmonton, Alberta, sponsored by the University of Alberta and Mississippi State University. Started over a decade ago, every year we have invited leading scholars from a range of mainstream disciplines to come together with leading scholars in family business management in order to explore and extend the application of prominent interdisciplinary perspectives to the context of family business. The papers presented in this special issue are selected from this collaborative conference and were accepted for publication after a double–blind review process (the reviewers are listed in the Appendix).

After every conference, we reflect upon an overarching theme that captures the essence of the topics covered. This year the contributions contained within this special issue are reinvigorating and creatively updating the theme of governance. This return to governance as the common theme, which, along with goals and resources is one of the key distinguishing features of the family form of organization (Chrisman, Sharma, Steier, & Chua, 2013), is both overdue and refreshing. Collectively, we feel, the papers in this special issue offer a foundation from which new and interesting extensions on this old theme can be developed. Indeed, while we have explored iterations of the topic in previous special issues in this series (Eddleston, Chrisman, Steier, & Chua, 2010; Steier, Chrisman, & Chua, 2004), this special issue takes a slightly different tack, focusing on the challenges involved in the governance of firms with family involvement and the challenges involved in the governance of families that own and/or manage firms. We think such a focus is appropriate given the increasing recognition that families today often own more than one business or firm and that the nature of the involvement of family members can vary greatly over time and from family to family (Michael–Tsabari, Labaki, & Zachary, 2014).

The governance challenges covered in this special issue are diverse, and include: (1) the agency problems emanating from conflicts among family blockholders and the double agency problems that result when families employ intermediate agents to manage family wealth; (2) rules for executive team formation and setting decision–making boundaries in complex, multifamily businesses; (3) generation of the tacit knowledge, reputation, relationships, and slack resources needed to compete in industries with high uncertainty in quality, value, and demand; (4) how to nurture potential family successors to build both competence and commitment; (5) the work–family conflict that occurs among founders of family and nonfamily firms; and (6) utilization of family human capital to meaningfully manage the creation, preservation, and distribution of wealth through long–term involvement in enterprise. Whereas all of these challenges can affect families that own a single business, the challenges tend to escalate as family assets become more diverse and the structure needed to monitor the assets more complex. Before turning to a discussion of the articles and commentaries in this special issue we first discuss governance and how it differs between family businesses and business families.

Governance of Family Businesses

Governance is widely recognized as a key determinant in the success and failure of all organizing activity. Family involvement introduces a unique dimension to governance, which we define broadly as the mechanisms used to ensure that the actions of organizational stakeholders are consistent with the goals of the dominant coalition (cf. Aguilera & Jackson, 2003; Chua, Chrisman, & Sharma, 1999; Sirmon & Hitt, 2003). Although governance has long been recognized as an important topic in family business research (Gersick, 2015; Morck & Steier, 2005), its various dimensions remain understudied (Berrone, Cruz, & Gómez Mejía, 2012). Furthermore, leading governance models in family business have tended to assume a single–family, single–business structure and have not provided useful explanations for how different organizations, such as multifamily and/or multibusiness firms, align their governance systems with their goals. Thus, the common theoretical assumptions about organizing activity offer little guidance for understanding how multibusiness families deal with various sources of heterogeneity. For family–influenced firms, factors such as the following complicate the challenge of designing effective governance systems.

Variation in Institutional and Industry Contexts

A history of corporate governance throughout the world (Morck & Steier, 2005) reveals that, although family firms are overwhelmingly present in all but a handful of developed countries, they are incredibly different. Their different evolutionary paths can be attributed to broader institutional contexts. These different evolutionary paths can also be explained via notions of adaptability and alignment with macro environments.

Heterogeneity of Family Firms

A perennial challenge in family business research is the lack of a clear definition of family firms (Litz, 1995). A reason for the difficulty may be that family firms vary in terms of family involvement in ownership and management and other essential features influencing governance such as transgenerational intentions (Chua et al., 1999).

Dispersion in Goals

The aspirations of family–influenced or controlled firms greatly complicate the governance challenge. For example, recent research (Gómez–Mejía, Haynes, Nuñez–Nickel, Jacobson, & Moyano–Fuentes, 2007) introduces the concept of socioemotional wealth (SEW) and clearly illustrates that many family firms measure performance in different ways—in other words, something other than financial return drives decision making. By illustrating that family owners are guided by different motives, the SEW approach introduces topics related to family firm governance that have yet to be fully explored (Berrone et al., 2012).

Multiple Stakeholders

Multiple stakeholders, their differing organizational identities (Cannella, Jones, & Withers, 2015) and their desire for control and influence further affect a firm's governance. Business interests are not always aligned among members of a single family. How, when, and why assets should be passed on to kin who often have divergent interests introduces additional intergenerational challenges. Varied ownership patterns may also introduce conflicts among controlling family owners and between family owners and nonfamily owners, who hold minority stakes in the firm (Morck & Yeung, 2003). Governance challenges can become even more complex when owners or managers come from more than one family that may, or may not, be related.

Although traditional corporate models of governance recognize stakeholder diversity, they do not adequately account for the various permutations of stakeholders and interests that manifest in family–influenced firms. Additionally, a good deal of the family business literature focuses on developing structures for solving problems at the family level and the business level in a parallel fashion (Carlock & Ward, 2001). At times, the focus is on how these systems interact, but most of the emphasis is at the level of the unitary firm. The papers in this special issue expand our horizons by considering situations involving multiple families and/or firms.

Existing studies of governance in family firms largely derive their theoretical perspectives from agency theory (Goel, Jussila, & Ikäheimonen, 2014). Early theorizing from this perspective viewed the corporation as a “nexus of contracts” between owner principals and their agent managers (Fama & Jensen, 1983a, 1983b) and considered the various mechanisms that align their economic interests. This idealized model (Steier, 2009) of separation of ownership and control emphasizes the firm rather than the family and thereby potentially misses some of the complexities associated with enterprising family behavior when the identities of stakeholders are diverse rather than monolithic. Thus, an unmet theoretical challenge (Aguilera & Jackson, 2003, p. 449) is to “conceptualize corporate governance in terms of its embeddedness in different social contexts.” The papers in this special issue address this theoretical challenge by presenting families and their economic and social activities in a variety of contexts, including that of multifamily and multibusiness firms.

From Family Business to Business Family

Much of the family business literature has implicitly assumed that the involved family has a single business and has focused on the goals and objectives, strategies, structure, culture, and performance pertaining to that family business. But as the business and the family both prosper, they often accumulate other assets, some within the firm and some outside. For example, the single–family, single–business firm may acquire the building in which it operates or construct its own building. Initially, there may be space in the building that is not being utilized, which could lead the family firm into the property rental business. Excess cash may be invested in the stock market leading to a financial securities portfolio. Alternately, excess cash may be invested in other business ventures. As the original business expands and becomes more complex, the complexity of the family enterprise as a whole will develop in a different manner than that of the original business (see e.g., Michael–Tsabari et al., 2014).

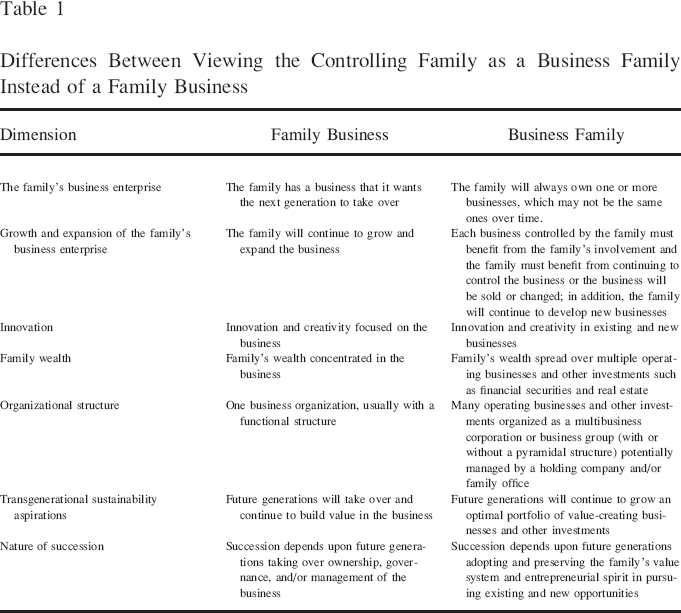

We began noticing, in the early 2000s, that families whose enterprises had evolved to this stage began calling themselves business families instead of family businesses, and some family business centers started calling themselves centers for business families. As summarized in Table 1, we believe that looking at the family enterprise as a business family instead of a family business involves important shifts in the conceptualization of governance.

Differences Between Viewing the Controlling Family as a Business Family Instead of a Family Business

As Table 1 shows, the first shift is in the family's attachment to their original business. While family businesses remain in the same business, the business family is more ready to exit from (enter into) a business that no longer benefits (will benefit) from the family's involvement or no longer benefits (will create value for) the family in unique ways that other businesses or passive financial market investments cannot. The business family grows not just through innovation in the original business but also through venturing into other related and unrelated markets (Habbershon & Pistrui, 2002). The enterprise may be organized into a group structure with a holding company at the top and operating subsidiaries or business units at the bottom. In countries where the tax treatment is favorable, the structure would typically be in the form of a pyramid (Morck & Yeung, 2003). Since the family's wealth is not concentrated in a single business, they benefit from the risk–reducing effects of holding a diverse portfolio of businesses. The family's hope for the family enterprise in the hands of future generations is no longer limited to building value in the original business but value creation through a constantly adapting portfolio of businesses and other investments. With respect to succession, a topic that continues to occupy a large portion of the family business literature, the business family's focus would emphasize the preservation of the family's value system, entrepreneurial spirit, and capacity for innovation, not necessarily the preservation of a particular business.

A business family perspective shifts governance toward addressing the challenges of encouraging and managing the entrepreneurial activities of family members, whereas a family business perspective needs to simply address the challenges of managing the growth and profitability of a single business. From the governance structure point of view, a business development department that constantly searches for new ventures and evaluates existing ones may become a necessity.

Since the different businesses may operate in varying institutional and industrial environments, the relevance of context is intensified. How diverse goals are achieved through multiple businesses requires a very different governance structure compared to what would be necessary in a single business setting. Additionally, the heterogeneity of enterprises in a business family would have additional complexity in the form of the goals, strategy, and structure the family sets for each business. There would no longer be one set of inside and outside stakeholders for the family enterprise. For example, some of the businesses may have minority nonfamily shareholders while others may not.

While, as we mentioned previously, business families appear to have switched their perspectives for decades, family business scholars have not yet formally or fully brought these changes in perspective into the academic literature. We hope that this introduction and the articles included in this special issue will help stimulate such development.

Article and Commentary Summaries

In the following sections we discuss the articles and commentaries in this special issue with regard to the governance challenges of family businesses and business families.

Blockholder and Double Agency Costs

Zellweger and Kammerlander (2015) elaborate upon the work of Carney, Gedajlovic, and Strike (2014) by focusing on the governance challenges associated with multiple family firm owners who do not necessarily have common goals. The heterogeneity of goals of multiple family owners introduces unique agency problems, which Zellweger and Kammerlander refer to as blockholder conflicts. They distinguish blockholder conflicts from the majority–minority agency conflicts typically discussed in the literature (e.g., La Porta, Lopez–de–Silanes, & Shleifer, 1999; Morck & Yeung, 2003). Blockholder conflicts involve disputes over the disparate goals of controlling owners, whereas majority–minority conflicts involve controlling and noncontrolling owners. Zellweger and Kammerlander argue that blockholder conflicts are particularly costly because owners on both sides of the struggle have more power to act to achieve goals that are not in the best interests of the firm. According to the authors this can lead to a “race to the bottom” where family members attempt to sequester resources before other family members are able to do so.

As Zellweger and Kammerlander (2015) note, a common response to this problem is to interpose an intermediate agent between recalcitrant family members and family assets in a previously “uncoordinated family” governance structure. These alternative governance structures include “embedded family offices,” “single family offices,” and “family trusts,” each of which progressively distances family owners from the control of family assets. Unfortunately, the responses can create as many problems as they solve owing to the double agency costs that can occur if the intermediate agents chose to act in their own interests instead of the interests of family owners. Apparently, the threat is very real, as the governance structure instituted, often by founders who mistrust the ability of their heirs to manage family assets, do not always provide adequate checks on the power of intermediate agents. In fact, in the extreme case of family trusts, the intermediate agent or trustee can obtain ultimate authority over family assets without being answerable to the actual owners, who are relegated to the role of passive beneficiaries.

Commentary: Advancing the Model

The commentary by Chandler (2015) attempts to identify and define variables that need to be measured to study the blockholder and double agency problems discussed by Zellweger and Kammerlander (2015). The types of variables Chandler covers include family heterogeneity, size and diversity of the asset base, sources of agency costs, and outcome variables. His enumeration of these variables make the nature of the relationships involved clearer and emphasizes why the governance challenges facing family firms might be different from the problems facing business families, at least in degree if not also kind. For example, family heterogeneity is affected by the number of family members involved, investment preferences, generational effects, and sources of power, all of which are apt to be more varied in business families than family businesses. Likewise, the family's asset base can vary according to its value, the number and relatedness of the business units under family control, and the other assets that the family owns.

Multifamily Firms

Pieper, Smith, Kudlats, and Astrachan (2015) study five companies that are owned and managed by the members of more than one unrelated family. Such firms are less common and more complex than firms owned by a single family but given the number of business partnerships that exist, it is somewhat surprising that multifamily firms have not received more attention in the literature. Given the lack of prior work, Pieper et al. attempt to build theory by addressing research questions pertaining to how and why multifamily firms persist. They discover that the persistence of the multifamily firm over time is largely a consequence of the development of simple rules concerning executive team formation based on competence fit, and the structure of decision–making boundaries within the firm with regard to voting, ownership, and management. Long–lasting multifamily firms are also characterized by mutual monitoring based on open communications and transparent decisions. Interestingly, Pieper et al. also find governance rules and processes are typically imprinted by founders at an early stage of development. By contrast, the one firm in their sample that had difficulties maintaining the multifamily form used complex rules, relied too much on outsiders, and was characterized by the involvement of family members with overlapping skills and responsibilities. Apparently, such a governance structure bred conflict and confusion between the two families.

Commentary: Multifamily Firms as a Transitional State

As Brigham and Payne (2015) indicate, it is obvious that multifounder firms frequently emerge from partnerships and alliances and often evolve into multifamily firms. However, Brigham and Payne refer to multifamily firms as a transitional state influenced by initial founding conditions and recurrent factors such as risk and uncertainty, resources, and intentions. Regardless of whether this form of organization endures or is transcended by other organizational forms, it is abundantly clear from the commentary of Brigham and Payne that the endurance and evolution of multifamily firms depends on goals and resources as well as the governance structures studied by Pieper et al. (2015).

Industry Attributes and Family Firm Performance

Le Breton–Miller and Miller's (2015) discuss the role of industry in explaining the performance of family firms. Similar to the earlier work of Carney (2005), their paper provides a reminder that the value of a firm's resources is conditional on how well they match the key success factors in the environment (Hofer & Schendel, 1978). According to the authors, family firms do well in industries with high uncertainty in quality, value, and demand because their long–term orientation makes them better suited to produce and transfer tacit knowledge, build relationships and reputation based on trust, and generate slack resources.

Based on their analysis, one set of industries that seems conducive to the family form of organization is the arts or, more appropriately, the business side of art. These include “creative industries” such as art galleries, antiques markets, auction houses, fashion design, film and television production, publishers, opera houses, and so forth. Le Breton–Miller and Miller (2015) argue that art industries possess the characteristics that breed family business success in that tacit knowledge is required to recognize, create, and price high quality art; a reputation for competence and honest dealing is needed to be able to attract customers and assuage fears of opportunistic behaviors or downright fraud; strong networks of relationships with potential customers and suppliers are essential and largely developed through direct contact and referrals; and slack resources are necessary to enable the firm to act when buying opportunities of often singular and unique products become available and to finance production and inventory until the products can be sold, a process which can sometimes take several years. Since family firms tend to be oriented toward the long term they tend to have greater ability to pass on tacit knowledge. Furthermore, the identification of family members with the family firm provides a credible signal of their veracity and helps forge enduring relationships. Finally, because identification creates both economic and noneconomic value for family members through their association with the firm, they are often more willing to reinvest and build the reserves necessary to take advantage of the opportunities and weather the threats associated with the business of art (cf., Sirmon & Hitt, 2003).

Commentary: Configurations and Equifinality

In their commentary Suddaby and Young (2015) remind us that there is usually no single best way to compete in a given industry. Consequently, they present a configuration perspective of competition in arts industries and suggest that the resources that family firms seem to possess in abundance have substitutes that can work equally well in certain situations. For example, bureaucracies can compete with clans by, for example, substitution of brands for reputation, institutionalization of collaborative creativity for tacit knowledge, and development of extensive yet shallower networks for close relationships. Thus, instead of focusing on which form of organization fits an industry best, Suddaby and Young suggest we should focus on how different organizations with different value clusters can adapt while preserving their unique institutional character.

Preparing Successors

The ability of family owners and managers to pursue idiosyncratic strategies and noneconomic goals that yield SEW is widely known (Carney, 2005; Gómez–Mejía et al., 2007). What is sometimes overlooked is that family owners and managers must have the willingness to do so and that ability and willingness are not perfectly correlated (De Massis, Kotlar, Chua, & Chrisman, 2014). Unfortunately, in grooming successors to take over the family business, incumbent leaders often forget that building competence and experience is only half the battle. In response, McMullen and Warnick (2015) use self–determination theory to explain how successors can be nurtured as well as groomed so that they will be willing as well as able to take over the family firm and build on the legacy with which they have been charged. The authors explain that potential successors (as well as any individual) have a need for competence, autonomy, and relatedness. They suggest that attention to these needs by parent–incumbents can increase the affective commitment and autonomous motivation of potential successors, which should increase the probability that members of the next generation will accept a leadership role and career in the family firm. Self–determination theory suggests that successors with affective commitment will be more effective in the sense that they will invest more resources in the firm, benefit from higher efforts on the part of employees, and be more willing to pursue the family's noneconomic goals. Consequently, McMullen and Warnick argue that the governance challenge facing family firms in preparing for leadership transitions is to provide a family and firm environment where potential successors’ need for self–fulfillment and self–determination are apt to be obtained.

Work and Family Conflict

Founders of both family and nonfamily businesses must deal to a greater or lesser extent with conflicts in their work and/or family domains, either of which can spillover from one domain to the other. Carr and Hmieleski (2015) theorize that the level of conflict and the attribution of the directionality of the conflict (work–to–family or family–to–work) differ for founders of family and nonfamily firms because of varying role pressures and role salience in the two domains. In family firms, conflicts that lead to work tensions—psychological strains from coping—are expected to originate in the family domain whereas in nonfamily firms work is more often the source of conflict. Using a sample of 223 firm founders obtained from the Dun & Bradstreet Market Identifiers database, Carr and Hmieleski find support for their hypotheses.

Family Human Capital Utilization

In the final article of this special issue Gersick (2015) discusses what he foresees as the role of family firm advisors in the coming years. Whereas succession, governance, and intergenerational dynamics have been the dominant topics of interest to family owners and managers over the past three decades, Gersick suggests that family human capital utilization is apt to emerge as the dominant topic in the next decade. Related to this, he identifies four areas of consultation that could be expected to become much more important to family owners and managers in the years to come. These include: (1) dreamwork, which deals with conversations about legacy, ownership continuity, and goals; (2) capacity building, which deals with developing the human capital necessary to govern the family firm; (3) careers and meaningful work, which deals with instilling value into the work and communicating the value of the work; and (4) utilization of wealth, which deals with the growth, preservation, and dispersal of the family fortune. Overall, Gersick's paper indicates that as the integration of wealth and character and the shift from successor to beneficiary become more important, the burning questions family stakeholders will seek to address will shift from “how can we” to “why should we” carry on, grow, and become involved in the family enterprise.

Discussion of Articles and Commentaries

Besides providing important contributions on their independent topics, the articles and commentaries in this special issue also offer unique insights for future work on the governance challenges facing family businesses and business families. The remainder of this introductory article attempts to draw out and integrate these insights.

Governance Challenges for Complex Families and Firms

Zellweger and Kammerlander's (2015) work identifies two sources of agency costs in family firms that have not received much attention in the literature to date. As they suggest, how to manage the governance challenges inherent in blockholder conflicts is difficult in a family business setting. However, these challenges can become even more difficult and costly to resolve in a business family where the structure, goals, and prospects of the family are more diverse and the sources of the family's wealth are more complex. On the other hand, business families also have more options to address the challenges since the assets under their control may be easier to divide or divest. Clearly, more attention is needed on how blockholder conflicts emerge and evolve, as well as the family and environmental characteristics that influence the effectiveness of the solutions chosen. Likewise, double agency problems are just beginning to be recognized as an issue in the literature (Child & Rodrigues, 2003; Chrisman, Chua, Steier, Wright, & McKee, 2012) and the methods by which they can be controlled in a family business and business family setting are not well understood and therefore need attention.

With regard to agency costs, Chandler (2015) suggests that power differentials are key. If his supposition that issues such as access to information, replacement costs, and learning impact the differentials that exist among and between family and nonfamily stakeholders are correct, then the power differentials should be larger or at least different in business families than family firms. Overall, his work suggests that in business families more degrees of freedom for diversity exist.

Governance Challenges for Firms with Multifamily Involvement

Pieper et al.'s (2015) study adds to both theory and practice by illustrating the value of simple governance structures. Of course, simplicity is only effective if the rules are clearly communicated and enforced consistently over time; that appears to be where mutual monitoring comes into the equation. Of at least equal importance are the many implications their study provides for further research on family businesses and business families. For example, multifamily firms bear some similarities to cousin consortiums, as well as family firms with substantial in–law involvement. Even when such firms have dominant coalitions of decision–makers (Chua et al., 1999), the complexity of family involvement suggests that there will be competing coalitions with disparate interests and abilities that must be reconciled. We suggest that this reconciliation is likely to lead to business families who control portfolios of businesses and other assets since the pursuit of different opportunities might be an effective way to achieve the participation of individuals with wide–ranging interests. Thus, studies that investigate how simple governance structures interact with different goals, resource configurations, and environmental factors and conditions to influence paths of growth and development seem worthwhile. The same is of course true for studies of business families, which often emerge from the entrepreneurial actions of family members and can evolve into other, more complex forms.

Governance Challenges for Family Businesses and Business Families in Different Contexts

Le Breton–Miller and Miller's (2015) arguments provide a theoretical description of families in arts industries that roughly corresponds to a family–in–business mindset where a family perceives its identity and abilities to be associated with a particular type of business (Habberson & Pistrui, 2002; Michael–Tsabari et al., 2014). This is in contrast to the family–as–investor mindset where families consider themselves as guardians of wealth and are committed to generating new wealth through the exploitation of market opportunities. In other words, families–in–business tend to focus on internal competencies and families–as–investors tend to focus on external portfolios of opportunities. However, it also seems clear from Le Breton–Miller and Miller's work that a natural progression of successful families–in–business would be to entrepreneurially invest in related businesses, thus achieving the family–as–investor status while maintaining the family–in–business linkages that were at the root of their success. Consequently, we argue that business families are more likely to have characteristics that give equal, or perhaps sequential attention to competencies and opportunities, a mindset that might be characterized as one of a family–with–strategy. We further argue that families in arts–related businesses might be an excellent setting to study the distinctions and relationships between family businesses and business families.

On the other hand, we agree with Suddaby and Young (2015) about the importance of understanding the institutional characters of family businesses and business families, especially since they are likely to vary substantially, perhaps even more substantially than the institutional characters of nonfamily businesses. Nevertheless, there is still some value to be gained by considering the general and specific competencies of family firms in relation to one another and in relation to nonfamily firms for two reasons. First, these competencies at least partially determine and are determined by their institutional characters (Selznick, 1957). Second, the value of these competencies is often influenced by industry context (Naldi, Cennamo, Corbetta, & Gómez–Mejía, 2013). Thus, we concur with Le Breton–Miller and Miller (2015) that further work on the compatibility of family firms with different industry environments is needed. For example, the involvement of family in firms may be more or less advantageous depending on the difficulty of monitoring, technological complexity, the specificity of human capital, the extent of information asymmetry, and the threat of adverse selection (Chrisman, Memili, & Misra, 2014; Pollak, 1985; Verbeke & Kano, 2012).

Governance Challenges in Leadership Transitions

With respect to the commitment of future generations, one aspect that McMullen and Warnick (2015) did not consider is the difference between ownership succession and management succession. This separation is even more important for business families because of the size of their resource endowments. The family business literature's treatment of future–generation commitment has focused on management succession. It is not obvious what minimum level of future–generation commitment is required with respect to ownership succession in order to achieve the family's economic and noneconomic goals.

Considering the distinction between family businesses and business families it seems ironic that the need for self–determination on the part of successors is probably more important in the former but more organically embedded in the governance structure of the latter. We think this is partly because the governance of a business family is by its very nature more democratic since the family is committed to seizing whatever opportunities their resources might allow, rather than exploiting a specific opportunity with a particular bundle of resources. In other words, we conjecture that business families are more likely to subscribe to effectuation logic than family businesses. Effectuation suggests that given means are used to search for acceptable ends, rather than acceptable means are sought for the achievement of a given end (Sarasvathy, 2001). Since such an approach allows family members in the next generation more freedom to chart their own course, we believe it is more conducive to the development of their willingness and ability.

Governance Challenges in Controlling Work–Family Conflict

Since the conflicts and tensions discussed by Carr and Hmieleski (2015) can affect work performance and relationships within the family and the business, a challenge of any governance system is to attempt to eradicate sources of conflict and provide remedies when conflicts do occur. The problem, as with any control mechanism or system, is to calibrate the costs and benefits. Obviously, in a family business the challenges are greater than in a nonfamily business because of the permeability of the family–and–business boundaries. However, it is not entirely clear whether the problem is more or less soluble in a business family where the goals are to maximize family utility through enterprise as opposed to maximizing family utility through an enterprise. The reason is that the asset bases of business families are likely to be more complex, meaning there are more potential sources of problems as well as solutions. For example, in business families there will often be more discrete assets to allocate and manage, which can exponentially increase work– or family–based conflicts. On the other hand, more assets also could provide family members with more opportunities to create, acquire, and/or manage their own independent enterprises. Thus, there is still a lot we need to learn about conflicts in a business family as opposed to family business setting as well as the governance systems used to manage those conflicts.

Future Governance Challenges for Family Businesses, Business Families, and Advisors

Assuming that Gersick's (2015) predictions are even close to being correct, the governance challenges of family businesses are going to get more complex because “why” issues are more value–laden than “how” issues, which tend to be more technical in nature. In this regard, we refer back to the article by McMullen and Warnick (2015) who use self–determination theory to explain why some potential successors might be more willing than others. Overall, the movement from “how” questions to “why” questions can, if properly handled, be a very welcome development for family firms and for the economies in which they compete. The reason is similar to the agency theory axiom that greater ability is associated with greater effort (Chua, Chrisman, & Bergiel, 2009); greater willingness can lead to greater effort to improve ability, and greater satisfaction with the consequences of ability and effort, which suggests a virtuous cycle of positive and self–reinforcing relationships. Given the discussions and distinctions made above between family business and business families, the evolution of the former toward the latter is also very positive because the potential for self–development and self–determination seems greater in business families than in family businesses. However, as is the case for much of the discussion we have provided in this article, research is needed to investigate whether and when the movement of a family business to a business family leads to greater value creation and if so, how and why.

Understanding Patterns of Organization and Governance Evolution

A distinguishing feature of enterprise throughout the world is the endurance of familial capitalism as an organizational form. Many familial enterprises demonstrate a remarkable ability to survive in the long term through an unwavering adherence to rigid strategies, structures, and governance practices; however, others survive through change and adaptation. Although prevailing research adopts a somewhat static view of organizational governance, many forms of governance are evolutionary or transitional (Brigham & Payne, 2015). The heterogeneity of family firm governance as well as the why and how various governance structures evolve remains understudied. Thus the longevity of family–based enterprises suggests temporal aspects to their evolution and governance that warrant further consideration. In other words, the examples and illustrations in this special issue broadly suggest there is merit in conducting further research that focuses on evolutionary patterns of governance in family–based enterprise.

Conclusions

The Theories of Family Enterprise Conference has two primary objectives. The first is to expand the community of family business researchers. So, over the years, we have invited many scholars noted for their management specialities who have not examined the consequences of family involvement to participate in the conference. A second objective is to help stimulate research, particularly in directions that have not received as much attention as they should. In this special issue based on the papers presented at the Conference, we highlight the governance challenges of complex multifamily and multi–business family enterprises. We believe that most highly successful family firms eventually develop into such enterprises. While the sheer number of small and medium–sized family enterprises does play an important role, these business families may prove to be the stiffest competitors for nonfamily firms in the global economy. It therefore behooves family business scholars to begin directing their attention toward those organizations.