Abstract

Upper echelon theory highlights the importance of top management teams in large and established firms; however, effects are not always clear outside of this context. Due to the unique nature of new ventures, the composition of entrepreneurial teams and its effects on performance is worthy of investigation. Accordingly, we meta–analyze the effect of three characteristics of entrepreneurial team composition (i.e., aggregated, heterogeneity, team size) on new venture performance. Our meta–analysis, which includes 55 empirical samples and 8,892 observations, finds significant and unique effects of entrepreneurial team characteristics on new ventures. Based on our findings, we derive avenues for future research.

Introduction

Developed three decades ago, upper echelons theory (UET) stated that organizational performance is partially predicted by the background characteristics of the members of the top management team (Hambrick & Mason, 1984). Upper echelon research in large and established firms has supported this theory by demonstrating that the composition and characteristics of the top management team have a strong effect on organizational outcomes (Hambrick, 2007). Likewise, entrepreneurship research has leveraged UET to focus on the entrepreneurial teams that are responsible for founding, developing, and leading new ventures (Beckman, 2006; Ensley, Hmieleski, & Pearce, 2006; Gartner, Shaver, Gatewood, & Katz, 1994; West, 2007). New ventures, broadly defined as early stage firms with respect to their development and growth (Klotz, Hmieleski, Bradley, & Busenitz, 2014), are rarely the product of a solo entrepreneur working in isolation (Steffens, Terjeses, & Davidsson, 2012). Instead, most new ventures are created by a team of entrepreneurs (Kamm, Shuman, Seeger, & Nurick, 1990), defined as a “group of individuals that is chiefly responsible for the strategic decision making and ongoing operations of a new venture” (Klotz et al., p. 227). Under the specific circumstances and contingencies of new ventures and their distinctive and unique nature, like the top managers of established organizations, entrepreneurial teams and their characteristics might also partially predict organizational outcomes.

Extant research examines the effects of different entrepreneurial team characteristics, such as aggregated entrepreneurial team characteristics (Beckman & Burton, 2008; Kor, 2003; Vissa & Chacar, 2009; Zhao, Song, & Storm, 2013), the heterogeneity of entrepreneurial team characteristics (Ensley & Hmieleski, 2005; Hmieleski & Ensley, 2007; Souitaris & Maestro, 2010), and entrepreneurial team size (Bruton & Rubanik, 2002; Chaganti, Watts, Chaganti, & Zimmerman–Treichel, 2008) on new venture performance. Conflicting results in the literature create uncertainty as to whether and to what extent these characteristics relate to new venture performance. For example, research on the individual entrepreneur suggests that human capital has a positive association with new venture performance (Unger, Rauch, Frese, & Rosenbusch, 2011), while some research finds that greater levels of professional experience and education hinder the entrepreneurial opportunity search process (Marvel, 2013). When applying these findings to the entrepreneurial team level, this implies that the team's aggregated level of individual human capital may or may not have a positive impact on new venture performance. With regard to heterogeneity, UET research demonstrates that team heterogeneity has a positive impact on performance because of the diversity of skills and perspectives on the team (Finkelstein & Hambrick, 1996; Hambrick & Mason, 1984); however, it is also found to be detrimental due to the conflict and need for reconciliation brought about by this diversity (O'Reilly, Caldwell, & Barnett, 1989). Additionally, research on the relationship between entrepreneurial team size and new venture performance is equivocal, with some suggesting larger teams facilitate increased performance due to their ability to handle complex situations (Hmieleski & Ensley), while others suggest smaller teams facilitate increased performance due to their strengthened behavioral integration ability (Simsek, Veiga, Lubatkin, & Dino, 2005).

Given that entrepreneurial teams are perhaps more influential than the individual entrepreneur on new venture performance, but that research reveals conflicting results, we meta–analyze the extant entrepreneurial team studies. Our meta–analysis, which includes 52 studies comprised of 55 samples of 8,892 observations, synthesizes findings on the relationship between entrepreneurial team composition characteristics and new venture performance. We investigate aggregated entrepreneurial team characteristics, heterogeneity of entrepreneurial team characteristics, and entrepreneurial team size. We chose these composition characteristics because they have been used to analyze relationships between team design features and team performance (Cohen & Bailey, 1997; Stewart, 2006) and because variables used in entrepreneurial team research are typically assigned to these categories. We chose meta–analysis as our method because it is suitable for aggregating results on relationships of interest (Hunter & Schmidt, 2004), and in particular, to synthesize results across studies while accounting for the presence of sampling and measurement errors. Meta–analysis not only allows researchers to determine whether positive or negative relationships exist, but also to calculate the magnitude (i.e., size) of relationships to estimate a population parameter (Hunter & Schmidt).

We aim to make multiple contributions with this study. First, by arguing that the entrepreneurial context is appropriate to test UET predictions, we contribute to upper echelon research by highlighting the importance of contextual considerations. Our findings support the view that the composition characteristics of entrepreneurial teams are consequential for new venture performance. Second, by asserting that teams can be distinguished by aggregated characteristics, heterogeneity of characteristics, and size, we were able to categorize the relationships in prior studies. This categorization allowed us to conduct the first meta–analysis examining the new venture performance implications of different entrepreneurial team composition characteristics. This is important because these three distinct characteristics tap into different team features and might reveal different performance effects. Third, owing that research on entrepreneurial teams has produced mixed results, we contribute to this literature by synthesizing extant empirical inquiry to show whether and to what extent entrepreneurial team composition characteristics influence new venture performance. Our meta–analysis permits a more precise understanding of entrepreneurial teams and builds a foundation for future research.

Theoretical Framework and Hypotheses Development

Upper echelon theory has been a prominent theoretical framework in the strategic management literature for analyzing the effect of the characteristics of top management teams on organizational outcomes. Applying an information processing perspective, Hambrick and Mason (1984) developed a strategic choice model under bounded rationality that describes the executive's construed reality. Based on this model, the experiences, values, and personalities of executives have a strong effect on the interpretations of the situations and options they face and, in turn, on the strategic decisions they make and the behavior they demonstrate. Hence, organizations are a reflection of their top management teams (Hambrick & Mason). Although early studies focused on the individual effect of the top executive (e.g., CEO), recent research focuses on the team as a level of analysis because management and leadership of an organization are a shared activity (Hambrick, 2007). The characteristics of top management team members and the composition of the top management team help explain organizational outcomes. Narrative reviews of this literature (e.g., Carpenter, Geletkanycz, & Sanders, 2004) and a meta–analysis (Certo, Lester, Dalton, & Dalton, 2006), however, conclude that the effect of top management team characteristics and composition on organizational outcomes is context specific.

Applying UET to the entrepreneurial context, we argue that the effect of entrepreneurial team characteristics will be strongly and uniquely reflected in new venture performance. Entrepreneurial teams of new ventures differ from top management teams of large and established firms. The literature proposes that the impact of executives may not remain constant over time, but should be stronger when the firm is small and/or young (Hatton & Raymond, 1994; Miller & Dröge, 1986). Entrepreneurial ventures are described as independent firms that have been in business 10 years or less (Forbes, 2005); therefore, given their young age, we expect the characteristics of the entrepreneurial team to have a strong impact on the venture. Furthermore, we argue that the uniqueness of entrepreneurial ventures stems from heightened executive job demands and an increased need to exercise managerial discretion (Hambrick, 1993, 1994; Hambrick & Finkelstein, 1987; Hambrick, Finkelstein, & Mooney, 2005). According to UET, the greater these factors, the stronger the reflection of the top management team's characteristics on organizational outcomes. Accordingly, we suggest that entrepreneurial team composition is highly likely to be reflected in new venture performance.

Job Demands, Aggregated Team Characteristics, and New Venture Performance

Entrepreneurial ventures present a unique context to examine UET because of differences in executive job demands between new and established ventures. Executive job demands is defined as “the degree to which a given executive experiences his or her job as difficult and challenging,” and this perspective recognizes that jobs differ widely in level of difficulty (Hambrick et al., 2005, p. 474). New ventures are described as operating under complex, dynamic, and uncertain conditions (Chandler, Honig, & Wiklund, 2005), thereby placing heightened job demands on the entrepreneurial team. Upper echelon theory suggests that the greater the job demands of the top management team, the stronger the reflection of their characteristics on organizational outcomes. Furthermore, we suggest that greater levels of human capital (i.e., functional experience, education, skills) enable entrepreneurial teams to better cope with the job demands of new ventures.

Research analyzing team composition characteristics has been based on the typology of Kozlowski and Klein (2000), which suggests that one method of aggregation of team characteristics is simple combination. Applied to entrepreneurial teams, this approach suggests that team member attributes would be aggregated to a summarized or averaged higher–level construct in a linear fashion (Harrison & Klein, 2007). The assumption underlying the simple combination of individual team member characteristics is that desirable dispositions and abilities of individuals provide the team with a resource, and that more of each resource is beneficial for team performance (Stewart, 2006).

Human capital attributes have been identified as critical resources for entrepreneurial success (Unger et al., 2011). A recent meta–analysis analyzed the effect of individual–level human capital on entrepreneurial success (e.g., Unger et al.), and we extend this human capital perspective by applying UET at the team level. The human capital embedded in entrepreneurial teams is a unique, valuable, and difficult to imitate resource that can provide the basis for new ventures’ competitive advantages (Barney, 1991) and enables new ventures to discover and exploit opportunities, plan strategies, and acquire additional resources (Unger et al.). Our assumption is that more embedded team–level human capital in terms of education, experience, knowledge, and skills is likely to positively affect new venture performance.

When analyzing the human capital of entrepreneurial teams, individual team member characteristics emerge to form team–level constructs that, in turn, relate to collective performance (Kozlowski & Klein, 2000). Research that examines entrepreneurial team composition characteristics that are aggregated in an additive way assesses whether the inclusion of individuals with desirable abilities and dispositions affects new venture performance. Results show significant effects in terms of team background and experience (Beckman & Burton, 2008; Hsu, 2007; Vissa & Chacar, 2009), team skill and capability level (e.g., Sullivan & Marvel, 2011; Zhao et al., 2013), and team personality traits (Ensley & Hmieleski, 2005; Ensley & Pearce, 2001; Ensley, Pearson, & Amason, 2002; Souitaris & Maestro, 2010). Executives’ knowledge and skills are derived from prior professional experiences (Hambrick & Fukutomi, 1991; Kor, 2003), which help explain and predict managerial intentions, strategic choices, and biases (Boeker, 1997; Finkelstein & Hambrick, 1996). Prior industry experience provides entrepreneurial teams with knowledge of markets, suppliers, and industry conditions, and it has been found to have a significant relationship with new venture success (Delmar & Shane, 2003). Executives’ past and current professional experiences also produce social capital (Florin, Lubatkin, & Schulze, 2003), which is valuable because it helps the firm access critical resources and initiate new business relationships (Burt, 1992, 1997). Research shows that entrepreneurial teams must engage in networking to be successful (de Carolis, Litzky, & Eddleston, 2009) and to survive over time (Huggins, 2000). Furthermore, experiences and functional expertise of the entrepreneurial team members are related to entrepreneurial tasks, which include environmental scanning, selecting opportunities, and formulating strategies for exploitation of opportunities, as well as organization, management, and leadership (Chandler & Jansen, 1992; Shane & Venkataraman, 2000). Individual task–related human capital is strongly related to new venture performance (Unger et al., 2011) and has a direct negative effect on business failure (Rauch & Rijsijk, 2013).

Applying UET and human capital theory to the entrepreneurial context, we argue that the aggregation of entrepreneurial team composition characteristics has a positive effect on new venture performance because higher levels of human capital enable teams to cope with the job demands of new ventures. Stated formally:

Managerial Discretion, Team Heterogeneity Characteristics, and New Venture Performance

Managerial discretion describes the latitude of action that is available to decision makers in a given situation (Hambrick & Finkelstein, 1987). When managerial discretion is high, UET predictions are more salient and organizational outcomes are more reflective of managerial team characteristics (Finkelstein & Hambrick, 1990; Li & Tang, 2010). We argue that entrepreneurial ventures offer more latitude when compared to large, established organizations; therefore, new venture performance is likely to be more reflective of entrepreneurial team characteristics. Discretion is likely to be pronounced in new ventures (Hambrick & Abrahamson, 1995; Klotz et al., 2014) because new ventures are, by nature, less mature and have less clear standards involving resources, competencies, and capabilities (Sarasvathy, 2001; Starr & MacMillan, 1990). Due to their small size and young age, new ventures are more flexible, innovative, and unconstrained by an ingrained culture. We argue that heterogeneous team characteristics allow entrepreneurial teams more latitude of action because constraints to strategic choice are reduced through this heterogeneity (Wangrow, Schepker, & Barker, 2015).

Heterogeneity, rather than simple aggregation, of team characteristics has been considered in research that analyzes the effects of team composition on organization outcomes (Kozlowski & Klein, 2000). In this method, heterogeneity indices aggregate the higher–level team construct as the variance of team members’ individual characteristics (Harrison & Klein, 2007). Research using heterogeneity indices focuses on the mix rather than on the sum of desirable dispositions and abilities of individuals (Kozlowski & Klein). The literature is divided as to whether heterogeneity of team characteristics is detrimental or beneficial to organizational outcomes. The social categorization perspective and the similarity–attraction perspective suggest a negative effect, while the information processing perspective assumes a positive effect of heterogeneity on team outcomes.

The social categorization perspective assumes that differences between team members may engender the classification of others as either similar or dissimilar; these categorizations may disrupt team processes leading to conflict and, in turn, weaken team performance (van Knippenberg & Schippers, 2007). The result of such categorization processes may be that teams function more smoothly when they are homogeneous rather than heterogeneous, and that team members are more satisfied with and attracted to homogeneous teams. This perspective is supported by studies that find higher group cohesion (e.g., O'Reilly et al., 1989), lower turnover (e.g., Wagner, Pfeffer, & O'Reilly, 1984), and higher performance (e.g., Murnighan & Conlon, 1991) in more homogeneous teams. In line with the social categorization perspective, the similarity–attraction perspective (Williams & O'Reilly, 1998) focuses on interpersonal similarity, primarily in attitudes and values, as determinants of interpersonal attraction (Berscheid & Reis, 1998; Byrne, 1971), and suggests that people prefer to work with similar others (Jackson, 1992). Both perspectives suggest that entrepreneurial team member heterogeneity is likely to increase team conflicts and, in turn, decrease new venture performance.

While we recognize and acknowledge the social categorization and similarity–attraction perspectives, we argue that the information processing perspective of UET is more aligned with the new venture context. The information processing perspective emphasizes a positive effect of the heterogeneity of team characteristics (Finkelstein & Hambrick, 1996; Hambrick & Mason, 1984). It assumes that heterogeneous teams possess a broader range of task–relevant knowledge, skills, and abilities because their members have different opinions and perspectives. This gives heterogeneous teams a more diverse pool of resources that may be helpful in dealing with nonroutine problems and reaching higher quality, more creative, and innovative outcomes (van Knippenberg & Schippers, 2007). Entrepreneurial teams are often confronted with nonroutine problems that require strong information processing and decision making, where more heterogeneity should be more beneficial (van Knippenberg, De Dreu, & Homan, 2004). Research indicates that the diversity of characteristics, such as functional background and education, is beneficial for team performance (Jackson & Joshi, 2011), including a meta–analytic review revealing that functional diversity has the strongest positive effect on team performance (Joshi & Roh, 2009).

Different types of teams (e.g., management, production, project) have been analyzed in extant research. Entrepreneurial teams can be most likely compared to project teams, which engage in nonrepetitive tasks and usually require application of knowledge and expertise (Cohen & Bailey, 1997), indicating a need for heterogeneity. In his meta–analysis, Stewart (2006) found a positive relationship for heterogeneity in project teams, suggesting that heterogeneity is more desirable for teams (e.g., entrepreneurial teams) engaged in creative and nonroutine tasks. New venture entrepreneurial teams often operate in uncertain and dynamic environments, in which heterogeneity is most beneficial (Stewart).

In sum, UET arguments are salient to entrepreneurial teams because in this context there is a heightened need for exercising managerial discretion. Heterogeneous team characteristics grant entrepreneurial teams the ability for strategic decision making under reduced constraints, which allows for organizational outcomes to be reflective of the team (Finkelstein & Hambrick, 1990). Furthermore, heterogeneous team characteristics have been empirically shown to increase performance. Taking these arguments together, we hypothesize:

Team Size and New Venture Performance

Haleblian and Finkelstein (1993) identified top management team size as an important determinant of firm performance in large and established firms. From an information processing perspective, larger top management teams are better able to absorb and process information. Larger teams can provide the firm with more access to information and execute more tasks simultaneously (Eisenhardt & Schoonhoven, 1990; Haleblian & Finkelstein, 1993). It is assumed that more team members increase the availability of resources to the team, which, in turn, increases the level of human capital that is available to the organization. Supporting this positive effect, human capital and social capital perspectives use team size as a proxy for the gross amount of human capital and knowledge information resources available to a new venture (Leary & DeVaughn, 2009; Wezel, Cattani, & Pennings, 2006). Larger entrepreneurial teams may be beneficial because they provide greater access to resources; greater ability to process, gather, and absorb information; a larger bandwidth of specialization and diversity; and greater ability to execute more tasks in parallel (Eisenhardt & Schoonhoven; Haleblian & Finkelstein; Sanders & Carpenter, 1998).

As new ventures are often associated with increased complexity, we assume that larger entrepreneurial teams are better able to understand and cope with complexity resulting from strategic choices. For example, information processing needs for new ventures may increase because new products need to be developed and introduced to the market or new customers need to be gained, which increases information processing requirements for entrepreneurial teams. To address these requirements, increased entrepreneurial team size may be beneficial for new ventures. Kozlowski and Bell (2003) indicate that the benefits of a larger team depend on the team type and its environment and suggest that larger teams provide more resources, such as time, energy, money, and expertise, which are particularly beneficial for completing difficult tasks in complex and uncertain environments. Stewart (2006) supports this view by showing that larger team size is more helpful for project teams. As entrepreneurial teams, which can be compared to project teams, are confronted by complex tasks and uncertain environments, larger entrepreneurial team size is likely to improve new venture performance. Stated formally:

Industry Influences

Industry conditions might affect the relationship between entrepreneurial team composition characteristics and new venture performance. All industries experience a varying amount of uncertainty (Bygrave, 1988), that is, the degree to which the outcome of an event cannot be predicted (Knight, 1921). For example, an emerging high–tech industry (e.g., aerospace) faces much more uncertainty than a mature low–tech industry (e.g., clothing). Uncertainty derives from environmental factors that can result in a lack of information needed to assess means–ends relationships, make decisions, and assign probabilities to their outcomes (Carpenter & Fredrickson). Upper echelon theory suggests that top management teams operate under highly uncertain conditions, characterized by ambiguity, complexity, and information overload, and that the more uncertain the decision making situation, the more likely top management team characteristics will be reflected in organizational outcomes (Carpenter & Fredrickson; Hambrick & Mason, 1984).

High–tech industries are those “in which rapid technological change and high inputs of scientific research and development expenditure are producing new, innovative and technologically advanced products” (Keeble, 1990, p. 361). Assuming that new ventures operating in high–tech industries are confronted by higher uncertainty than new ventures in low–tech industries, entrepreneurial team composition characteristics are likely to be more strongly reflected in new venture performance in high–tech industries. Uncertainty creates higher job demands for the entrepreneurial team, which result from task challenges that arise from the environment (e.g., scarcity, complexity, dynamism) (Hambrick et al., 2005). We argued that aggregated entrepreneurial team human capital enables top management teams to better cope with these higher job demands. As such, we hypothesize a stronger effect of aggregated entrepreneurial team characteristics on performance for new ventures operating in high–tech industries.

Effects of the heterogeneity of entrepreneurial team characteristics on new venture performance may be especially important in high–tech industries, which are more dynamic, use sophisticated and complex technologies, and typically require extensive knowledge and research in uncertain environments (Khandwalla, 1976; Utterback, 1996). Additionally, these environments would require a higher need for managerial discretion, for which heterogeneity of entrepreneurial team characteristics are deemed more salient. Diversity of knowledge and information can reduce the uncertainty associated with innovation and dynamic environments (Jansen, Van den Bosch, & Volberda, 2006; Kirzner, 1997; McMullen & Shepherd, 2006). Empirical research supports this argument by demonstrating that heterogeneous top management teams achieve better performance under high environmental uncertainty, whereas less heterogeneous teams are more successful in stable contexts (Eisenhardt & Schoonhoven, 1990; Hambrick, Cho, & Chen, 1996; Iaquinto & Fredrickson, 1997; Lant, Milliken, & Batra, 1992). By contrast, new ventures in low–tech industries find it more beneficial when team members maintain less heterogeneity. Individuals can more easily share and absorb knowledge when they have similar backgrounds and experiences (Reagans & McEvily, 2003), suggesting that heterogeneity increases the effort and resources necessary to effectively coordinate and communicate. Because new ventures in low–tech industries obtain fewer performance benefits from innovation, the novelty value of access to diverse knowledge is reduced. Thus, in low–tech industries, the costs of member heterogeneity are more likely to outweigh the benefits. Compared with high–tech industries, new ventures in low–tech industries face less risky and complicated decisions. In the decision–making process, efficiency is more important than innovativeness. Taken together, we hypothesize:

Methodology

Study Identification and Sample

To identify empirical studies investigating relationships among entrepreneurial team composition characteristics and new venture performance, we followed a four–step procedure. First, we read through the literature to identify terms, resulting in combinations of the following team– and performance–related keywords: entrepreneurial team, new venture team, venture team, venture top management team, new venture performance, venture performance. Second, we performed keyword searches in the databases of ABI/Inform, Business Source Complete (BSC), EBSCOhost, Social Science Citation Index (SSCI), JSTOR, PsycInfo, and CNKI, 1 that allowed us to identify 238 relevant studies. Third, we manually searched journals in entrepreneurship (Entrepreneurship Theory & Practice, Journal of Business Venturing) and management (Academy of Management Journal, Journal of Management, Organization Science, Strategic Management Journal) for other studies that might not have been captured in our keyword search. To reduce the potential for publication bias, we also searched for unpublished studies in the databases of Social Science Research Network, conference proceedings of the Academy of Management (1984–2012), conference proceedings of the Southern Management Association (1984–2012), and ProQuest Dissertations and Theses; this step resulted in the identification of 17 additional studies. Fourth, we reviewed the reference section of the studies we found and identified three additional relevant studies. These steps allowed us to identify a comprehensive list of 258 studies.

To be included in our meta–analysis, studies had to meet four criteria. First, we considered only studies examining entrepreneurial team composition characteristics at the team level and new venture performance at the firm level. Those focused on solo entrepreneurs (i.e., at the individual unit of analysis) were excluded. Studies focused on obtaining venture capital funding (e.g., Hsu, 2007; Patzelt, 2010) were also excluded from our analysis. Second, studies had to examine relationships in the context of new ventures, not established firms. Extant research fails to provide a strictly uniform standard for defining the age of entrepreneurial firms. For example, Forbes (2005) defines new venture as independent firms in business 10 years or less, while Zhang and Li (2010) identify 8 years as an appropriate measure. We utilized the aforementioned 10 years as cutoff. Third, studies needed to contain a measure of entrepreneurial team composition characteristics, a measure of new venture performance, and to report the bivariate relationship (i.e., correlation) between the two measures and the sample size. If information was missing, we contacted the respective authors. Fourth, studies had to draw from independent samples. If studies leveraged the same sample, we computed the mean effect sizes across studies to develop one effect to include in our meta–analysis (Hunter & Schmidt, 2004). Applying these criteria, our final search resulted in 52 usable studies (of which three are unpublished) with 55 independent samples involving a total of 8,892 observations.

Measures

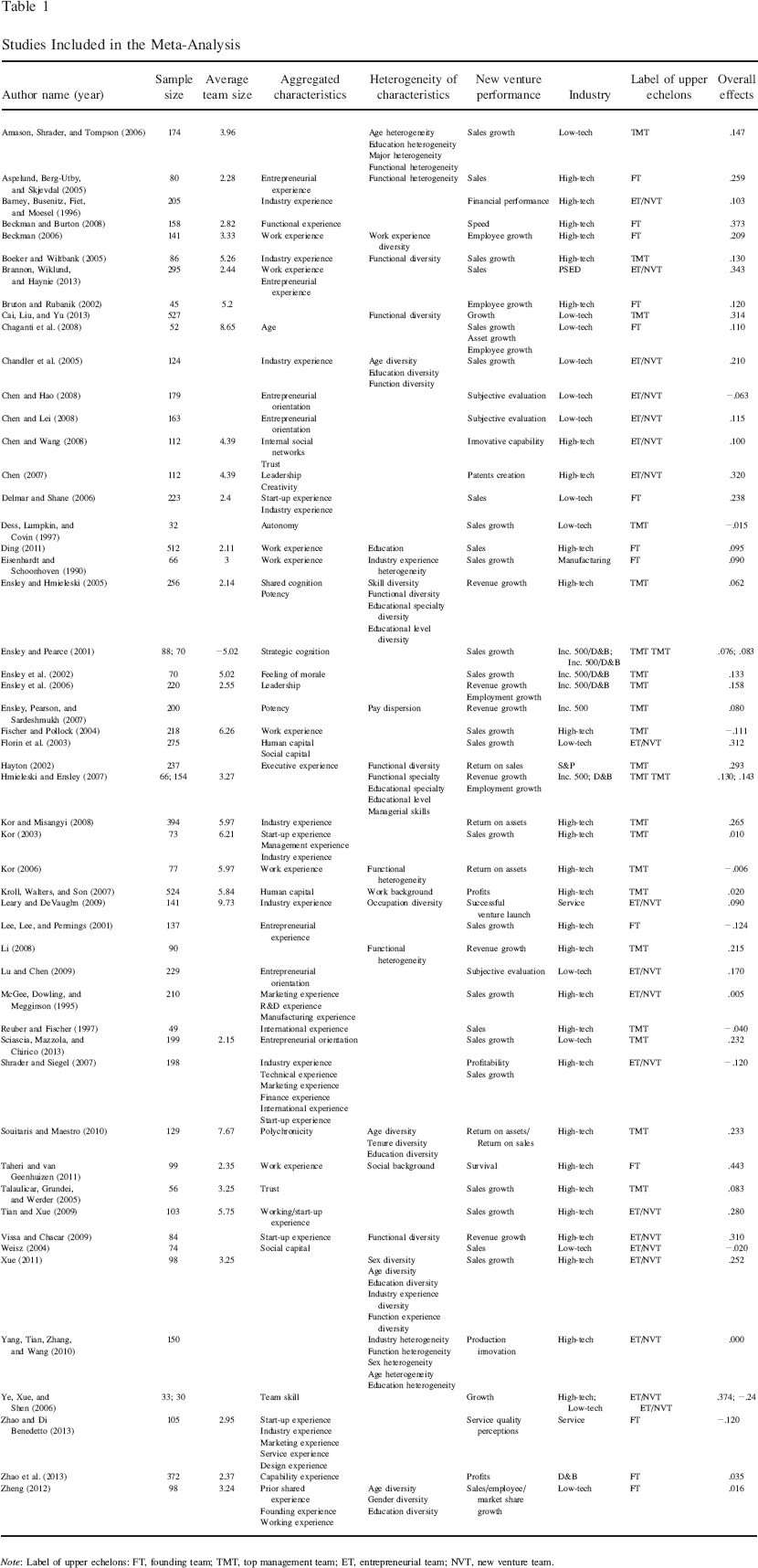

Table 1 displays the characteristics of the studies included in our meta–analysis and how each study's variables were assigned to the entrepreneurial team composition characteristics. A standard coding approach was developed by three of the co–authors. All 52 studies were coded independently by two of the co–authors. There was agreement on 95% of initial coding; disagreements were resolved through discussion.

Studies Included in the Meta–Analysis

Note: Label of upper echelons: FT, founding team; TMT, top management team; ET, entrepreneurial team; NVT, new venture team.

Dependent Variable

The primary studies in our meta–analysis relied on varying measures of new venture performance. Although Combs, Crook, and Shook (2005) consider financial performance via three dimensions (i.e., profitability, growth, and stock market), the studies we found only captured profitability and growth measures. Most ventures studied in entrepreneurship research are analyzed before initial public offering, therefore stock market performance measures were unavailable (Unger et al., 2011). Measures of profitability include accounting–based indicators such as return on assets, return on investment, return on sales, and self–reported assessments. Growth measures include objective or perceived growth in sales, employment, and market share. To test our hypotheses, we recorded the overall effect sizes between all measures of new venture performance and the relevant independent variables.

Independent Variables

Aggregated entrepreneurial team characteristics reflect desirable abilities and dispositions of individuals, which are additive such that the sum or mean of individual characteristics represents the team–level construct. Accordingly, we coded aggregated measures such as collective industry experience, start–up experience, and work experience. These measures used the mean of individual–level characteristics as the aggregated measure. Heterogeneity of entrepreneurial team characteristics is not additive and instead reflects the mix of individual characteristics across the team members. The studies in our analysis used the Herfindal–Hirschman or Blau index as measures of heterogeneity across the dimensions of gender, age, and functional experience. Meta–analysis allows us to combine the different measures and types of heterogeneity into a global heterogeneity measure (cf. Hunter & Schmidt, 2004). Entrepreneurial team size reflects the number of entrepreneurs on the team.

Moderator

We grouped studies into high–tech and low–tech industries. Sample high–tech industries include computer hardware and software, Internet, telecommunications, medical, surgical and dental instruments (SIC = 384; 3841–3845), biotechnology, and semiconductors. Low–tech included other industries.

Analysis

Meta–analysis statistically aggregates findings from extant literature to reveal whether a relationship exists, whether the relationship is positive or negative, and the magnitude (i.e., effect size) of the relationship (Hunter & Schmidt, 2004). Effect size estimates were calculated as the mean of the sample size weighted correlations (

After sampling error, measurement error has the largest impact on findings. Because some studies do not report reliability coefficients for entrepreneurial team composition or new venture performance, it is impossible to correct each study individually for measurement error. After we computed our sample size weighted correlation (i.e.,

To test our hypotheses, we constructed confidence intervals around each

The main effects of entrepreneurial team composition characteristics on new venture performance stated in hypotheses 1, 2, and 3 were tested by whether the confidence interval for

Results

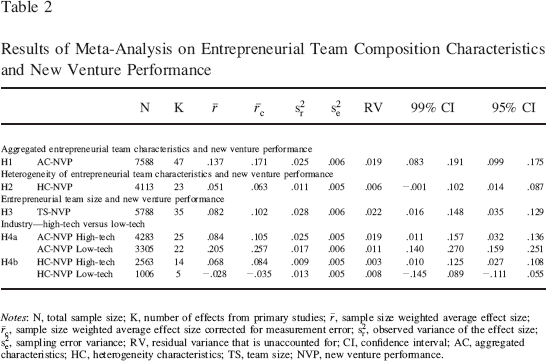

The results are presented in Table 2. Because some studies did not contain the requisite variables, the sample size differs for each test.

Results of Meta–Analysis on Entrepreneurial Team Composition Characteristics and New Venture Performance

Notes: N, total sample size; K, number of effects from primary studies;

Hypothesis 1 predicted that aggregated entrepreneurial team characteristics would be positively related to new venture performance, and we found support for this hypothesis:

Robustness Checks and Further Analysis

We conducted several tests to check the robustness of our results. First, because there is a lack of consensus regarding the length of time an entrepreneurial firm should be classified as a new venture, we reanalyzed our results based on different cutoff criteria in the literature. Our initial analysis adheres to Forbes (2005), who defines entrepreneurial ventures as those that have been in business 10 years or less. Seven years (Boeker & Karichalil, 2002) and 5 years (Bloodgood, Sapienza, & Almeida, 1996) are other established cutoff values; therefore we examined our predictions using only those studies in which the average age of the new venture was 7 years or less and 5 years or less. The new venture performance predictions were supported in those firms in business for 7 years or less using aggregated characteristics (

Second, we reanalyzed our main effect hypotheses using subgroups of new venture performance; namely, growth and profitability. To elaborate, the main effects were initially analyzed by examining the overall effect size between all measures of new venture performance and the independent variables. For the purposes of this robustness check, we compared the effects of studies using growth measures to those using profitability measures. Research suggests there might be a trade–off between achieving growth and profitability (Zahra, 1996) and that growth often supersedes profitability in the new venture context (e.g., Zhao, Seibert, & Lumpkin, 2010). However, our results indicate no statistically significant differences in effect sizes for growth versus profitability measures of new venture performance with regard to (1) aggregated entrepreneurial team characteristics (i.e., the confidence intervals overlap with

Third, we conducted a test to determine if the operationalization of the entrepreneurial team impacted our findings. Entrepreneurship studies use different terms and conceptualizations to refer to upper echelons in new ventures. A commonality in UET research is that top managers are those involved in strategic decisions, but extant entrepreneurial research reveals three distinct categories of upper echelons (Maschke & Knyphausen–Aufseß, 2012). The first is a new venture top management team, which is comprised of those who hold a 10% stake or are a founder (e.g., Ensley et al., 2002). The second is an entrepreneurial/new venture team, in which one or more team members worked for an earlier venture capital backed firm (e.g., Busenitz, Fiet, & Moesel, 2005). The third is a founding team, which refers to a team comprised of the venture's founders (e.g., Chaganti et al., 2008). Because these three conceptualizations might lead to performance differences (e.g., Finkelstein & Hambrick, 1996), we reanalyzed our main effects to determine if new venture performance implications change as different upper echelon operationalizations are applied. The confidence intervals reveal that the magnitude of the effects is statistically similar across each of the categories; thus, it appears the results of our meta–analysis are robust regardless of how the entrepreneurial team is operationalized. We should mention, however, that the effects are strongest for the teams categorized as entrepreneurial/new venture teams.

Fourth, following the approach of Palich, Cardinal, and Miller (2000), we further analyzed the effects of team size on new venture performance. We created subgroups of studies based on small (average team size of 3 or less), moderate (average team size between 3 and 6), and large (average team size of 6 or more) teams. We computed confidence intervals and critical ratios to estimate nonlinear effects (Hunter & Schmidt, 2004); we found that small and large teams (

Discussion

Upper echelon research highlights the importance of top management team characteristics in large and established firms (Hambrick, 1995, 2005); however, the effects may be context dependent (Carpenter et al., 2004). Applying UET to the new venture context, we argue that the effects of entrepreneurial team composition characteristics on new venture performance may be more pronounced and reveal unique findings compared to established firms. We found that all entrepreneurial team composition characteristics are positively related to new venture performance but differ in strength of effect. Aggregated entrepreneurial team characteristics have the strongest effect, followed by entrepreneurial team size and heterogeneity of entrepreneurial team characteristics. The magnitude of the effect between aggregated entrepreneurial team characteristics and new venture performance was estimated to be

The relationship between the heterogeneity of entrepreneurial team characteristics and new venture performance is

The effect of entrepreneurial team size on new venture performance is

Our findings reveal differences in the relationships between entrepreneurial team characteristics and new venture performance across industries. The effects of aggregated entrepreneurial team characteristics and new venture performance are significantly positive in both high–tech (

Additionally, in low–tech industries, our results demonstrate that aggregated team characteristics are significantly more beneficial to new venture performance than heterogeneous entrepreneurial team characteristics (i.e., the confidence intervals do not overlap with

Limitations and Future Research

Our meta–analysis is not without limitations; however, our study's limitations lend themselves to future research opportunities. We argued that new ventures are different from established ventures and are an ideal context to which to apply UET theory. Our arguments and findings suggest that entrepreneurial team aggregated characteristics help overcome high executive job demands, heterogeneity of characteristics helps teams exercise managerial discretion, and the appropriate entrepreneurial team size facilitates behavioral integration and information processing benefits. However, we were unable to capture these constructs directly because a meta–analysis is limited to the measures captured in extant studies. Accordingly, future research that directly captures these constructs in new ventures and compares their effects with those of top management teams of large and established firms would appear fruitful. For example, although the information processing perspective serves as the theoretical rationale for many arguments regarding the benefits of team heterogeneity (e.g., Amason et al., 2006; Certo et al., 2006; Leary & DeVaughn, 2009), information processing ability is not a construct that is empirically measured in these studies. Investigating these constructs directly will help shed light on the strategic decision–making process that ultimately leads to organizational outcomes that are reflective of upper echelon characteristics.

Although Hambrick and Mason (1984) is often cited for arguing that organizations, and hence, performance outcomes, are a reflection of their top management teams, Hambrick and Mason also assert that certain managerial backgrounds are expected to result from prior organizational actions. Although they call for research designs that disentangle managerial background effects on performance from performance effects on managerial backgrounds (p. 197), a limitation of our study is that we cannot make strong inferences about causality because we are overly reliant on studies that were cross–sectional in design. Thus, although our meta–analysis reveals that entrepreneurial team characteristics and performance are related, future research should take care to better capture causality via longitudinal designs so that a future meta–analysis can more precisely assess the strength and direction of UET relationships.

Research on top management teams in large and established firms has started to analyze the nonlinearity of the effects of team composition characteristics and firm performance (Certo et al., 2006). For example, heterogeneity may reach optimality for organizational outcomes and may have a dysfunctional, diminishing, or negative effect when the team members are too similar or too diverse. We were unable to investigate the potential curvilinear effect of heterogeneity on new venture performance in our meta–analysis. To test curvilinear effects, we would need to categorize and compare the level of team heterogeneity in each study analyzed. Heterogeneity is most often captured through the use of the Blau index (e.g., Blau, 1977); however, this measure does not allow for comparisons across index scores if there are differences in the number of diversity categories measured or different team sizes. As such, we could only test the strength of the relationship between heterogeneity and performance, rather than being able to categorize and compare heterogeneity levels between teams across studies. Therefore, we encourage future research to investigate the potential curvilinear effects of team composition and characteristics on new venture outcomes.

We were limited in our ability to test additional moderators that may influence entrepreneurial team–performance relationships because of the low number of studies examining such moderators. Power within the entrepreneurial team may be a potential moderator and offers another avenue for future research. Examining power may reveal whether characteristics of some team members are more important than those of other team members and if characteristics of the more powerful members become more strongly reflected in new venture performance. Considering ownership levels of team members may be one way to measure power differences (Kraiczy, Hack, & Kellermanns, 2015). Another potential moderator for future research is personality. Examinations of similar or varying personalities on the team may reveal what goals or strategies are important and therefore would be reflected in organizational outcomes (Pitcher & Smith, 2001).

Effects that may mediate the relationship between entrepreneurial team composition characteristics and new venture performance need to be explored. We were unable to examine mediators in the relationship because there are not enough primary studies investigating them to meta–analyze these relationships. Although research on entrepreneurial teams has started to focus on team processes (e.g., membership changes, team conflict) and emergent states (e.g., collective cognition, cohesion, team confidence) as mediators between entrepreneurial team inputs and outputs (Klotz et al., 2014), mediators need further analysis to better explain the effects of entrepreneurial team composition on new venture performance.

Our findings indicate that future research should compare different measures of new venture performance and control for the venture's life cycle stage, which may change the goal orientation of the entrepreneurial team. Entrepreneurial teams of larger and more established new ventures in later life cycle stages may focus more strongly on profitability than on growth. In this context, type of new venture and industry effects may also be interesting for future research. While growth may be of high importance for high–tech new ventures and in high–tech industries, it is unlikely to be of high importance in all industries and for all new ventures, as some entrepreneurial teams may prefer to control growth or maximize profitability (Klotz et al., 2014). Future research may also investigate if growth intentions of entrepreneurial team members affect growth measures more strongly than profitability measures.

Because several of our analyses are based on a relatively small number of studies, some of our findings related to these constructs are tentative and some of our aggregates are not as fine–grained as desired. Furthermore, we were unable to capture additional contingencies such as new venture size. Meta–analysis can be valuable for assessing broader constructs, as it provides significant insight in understanding the underlying relationships (see for example Campbell–Hunt, 2000). Although our initial results are important and informative, a meta–analysis based on additional studies is needed.

Another shortcoming is that many of the studies in our meta–analysis suffer from “survival bias” because nearly 95% of start–ups fail within 5 years. This suggests that our results might be aggressive estimates of the relationships we investigated. We followed Rosenthal (1979) and ran tests to determine the number of published studies that would be needed to negate our results (i.e., have an effect of zero). We found that, on average, almost 40 studies with null results would be required. Although Rosenthal's test assesses publication bias, we believe these results help strengthen our findings. A key implication is that since our meta–analysis is based on previous studies that often use survival or successful ventures as their samples, future studies should account for this in primary research. Adopting a survival indicator and other performance indicators in models of entrepreneurial team composition–new venture performance would help a future meta–analysis to examine such effects.

Conclusion

This is the first meta–analysis to examine the relationship between entrepreneurial team composition characteristics and new venture performance. The entrepreneurial team literature is growing and inconsistent results were being found. Through our meta–analysis, we demonstrate that upper echelon theory in general, and in particular, executive job demands, managerial discretion, and behavioral integration and information processing ability, can be extended into the context of entrepreneurial ventures to help reconcile these inconsistencies. We demonstrate that entrepreneurial team composition characteristics are strongly and uniquely reflected in the success of new ventures, which provides a solid foundation on which future research can build.

Footnotes

1.

CNKI is a Chinese database for academic papers.