Abstract

This case describes Michel Kripalani's entrepreneurial journey culminating in his third start–up, Oceanhouse Media. Oceanhouse Media, ranked 114 in the 2013 Inc. 5,000 list of the fastest growing companies, offers desktop and digital applications, for iOS, Android, and other platforms with digital book applications for children comprising half of annual revenues. It explores: (1) Kripalani's evolution as an entrepreneur, (2) the operating strategy of Oceanhouse Media, (3) the economics and structure of the digital applications market and the children's segment within that market, and (4) key decisions—structural, organizational, and financial—as Kripalani maps out Oceanhouse Media's future growth path and exit strategy.

Introduction

As 2013 drew to an end, Michel Kripalani took stock of his journey with Oceanhouse Media, the digital applications company he had founded in 2009. Several of Oceanhouse Media's venture–capital funded competitors had either been acquired at discounted valuations or were restructured within the last 12 months. He wondered if this was an opportune time to consider an appropriate exit strategy for his five–year–old venture. While he had not considered a sale of Oceanhouse Media, he was now open to the possibility of a sale if the “right” offer materialized. However, Kripalani's assessment of a “right” offer would be determined by Oceanhouse Media's estimated worth at year–end 2013. While the company had been profitable, cash flow positive, and self–funded, Kripalani realized that Oceanhouse Media was at a critical juncture necessitating key decisions with respect to the financial, organizational, and execution challenges resulting from continued rapid growth. 1 Kripalani saw 2013 as a year of consolidation in the digital apps market; the market was becoming increasingly saturated, highly concentrated, with increasing competitive pressures that were driving app prices toward zero.

Oceanhouse Media's 2013 revenue growth had slowed considerably relative to the torrid growth rate of 2009–2012; while company revenue grew at a compound annual growth rate exceeding 200% from 2009–2012, it grew only 5% in 2013. As he focused on Oceanhouse Media's growth path post–2013, Kripalani articulated his perspective on external financing: “We are bootstrapped, have not taken capital, do not intend to.” He also noted that while venture capitalists earlier “had been knocking on our doors,” he had been reluctant to take on VC money because of what he perceived to be the high cost of VC investment in the firm. While Oceanhouse Media had not utilized nonequity funding sources to date, Kripalani was open to the possibility of using such funding sources to support anticipated future growth.

Based in Encinitas, California, Oceanhouse Media, Inc., was Kripalani's third start–up. The company was currently structured as an S–Corporation with Kripalani and his wife, Karen, as sole shareholders. It was a publisher of more than 380 mobile and desktop apps for iOS (iPhone, iPad, iPod touch), Android, NOOK tablets, Kindle Fire, HP TouchPad, and Windows 8 devices. The company's mantra was “Creativity with Purpose,” and it developed and offered a diverse portfolio of apps in the Books, Games, Music, Photography, Health & Fitness, Reference, and Finance categories. 2 Oceanhouse Media was ranked #114 in the 2013 Inc. 5,000 list of the fastest growing companies. It was also ranked #9 in Inc.'s Top 100 Software Companies category. Mobile or digital apps were software programs that ran on smartphones, tablets, and other mobile devices. The rapid development of distribution platforms, such as the Apple App Store, Google Play, Windows Phone Store, and Blackberry App World facilitated the availability of apps to consumers. These distribution platforms were generally operated by the owners of mobile operating systems.

Evolution of Michel Kripalani as Entrepreneur

After graduating in 1989 with a degree in visual arts media from University of California, San Diego (UCSD), Kripalani started his first company, Moov Design, and for the first year and a half, he and a partner created CD–ROMs and trade show graphics for their clients; they developed and programmed the world's first interactive CD–ROM magazine, VERBUM Magazine. According to Kripalani, this experience “really got my foot in the door, and I was learning a lot of this new language before people were even talking about it … I found I was good at it. It just clicked, and as a visual person I was able to put together interactive projects fairly easily” (Potts, 1998, p. B1).

Founding of Presto Studios

Kripalani's experience at Moov Design led him and a partner and some college friends to the founding of Presto Studios in February 1991; Presto created high–end video games for the next 11 years. Renting two houses, living in one and working in the other, the team borrowed $70,000 from friends and family (repaid at a 10% interest rate) and created The Journeyman Project, which was the world's first photo–realistic adventure video game. The company needed to sell 10,000 copies to be profitable. Within a year, they had a prototype that was previewed at a computer convention in San Francisco. Kripalani recalled that the overwhelming response to the prototype convinced him and his team to quit their jobs so as to focus full time on the business of video games. They introduced the game in January 1993 beating a competing game Myst (published by Broderbund Software) to the market by 10 months. Presto Studios ended up selling 150,000 copies of the game.

The original Myst game was created by the brothers Rand and Robyn Miller who ran a software company called Cyan. Riven ®: The Sequel to Myst was introduced by them in 1998. Both Myst and Riven ® had collectively sold more than 9 million units since 1993. Both of the Myst games were marketed by their publisher Broderbund Software. Meanwhile, in January 1995, Kripalani and Presto Studios introduced the sequel to The Journeyman Project, The Journeyman Project: Buried in Time which shipped more than 120,000 copies. A follow–on version, The Journeyman Project 3: Legacy in Time was shipped out in February 1998.

The right to market the third game in the Myst series, Myst III: Exile was acquired by another publisher, Mattel Interactive (a division of Mattel, Inc.). Mattel selected Presto Studios to develop Myst III; Presto received a strong endorsement from Rand Miller, CEO of Cyan, “We couldn't think of a more logical choice to design and develop the next installment in the Myst series. We're confident that the next Myst adventure will live up to the expectations of our fans” (Business Wire, 2000). Myst III was introduced in 2001 after taking Presto Studios 2 years to develop at a cost of $3 million. Myst III sold a million units in the first 12 months following its introduction.

Closure of Presto Studios

Despite the success of Presto Studios, Kripalani announced the closure of Presto Studios on August 31, 2002. The news shocked Presto's fans and many of its 21 employees. The company was riding a wave of success after producing the top–selling Myst III: Exile and the upcoming Whacked game for Microsoft's XBOX system. According to Kripalani, Presto had earned about $2.5 million a year, had no debt, and was rich in talent; however, achieving consistent profitability had proved to be a challenge. What happened?

According to Kripalani,

The video game industry is changing. Presto used to fund the production of its own games, but now game titles cost millions of dollars to make. Companies that can afford to produce them often hesitate to spend money on new, untested ideas. As in the movie industry, the sequels and established characters like the Warcraft IIIs and the Mario Brothers get the investments. The innovative, never–been–done ideas that Presto specializes in are sometimes viewed as risky. Game companies were not willing to pay Presto's fees for game development. Competitors could do the job at lower cost. Developing games was turning into a hard–edged business. We were at the point where we had so many expenses and such a high payroll that we started to lose passion in the games. (Peterson, 2002, p. 1)

Presto also lost out on the development rights to the next game in the Myst series, and a number of its other game ideas sputtered in talks with Microsoft and other companies. In addition to severance packages, Presto employees also were assured that they would receive royalties from future game sales. After the closure, Kripalani took a six–month break from work and traveled the world.

Period after Presto Studios

From about 2004 through early 2009 Kripalani worked as Director of Business Development at Discreet (based in Montreal, Canada), a division of Autodesk, a publicly traded firm listed on NASDAQ. Based in San Rafael, California, Autodesk was a design, digital media creation, and distribution company. Discreet developed software solutions that included film and television visual effects, color grading, editing, animation, game development, web interactivity, and design visualization. He was laid off from Autodesk during the recession of 2008–2009. With the introduction of the iPhone in 2007 and Apple's announcement in 2008 that app developers could sell their own apps on the Apple App Store, Kripalani was now eager to get into his own software development business. With his experience at Discreet and at Presto Studios, Kripalani was positioned well for his next start–up, Oceanhouse Media, which he founded in early 2009.

Oceanhouse Media

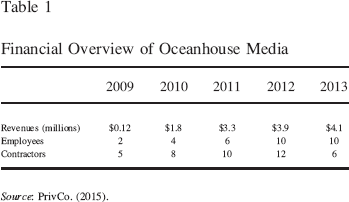

Oceanhouse Media was a publisher of digital books and digital apps for iOS and Android devices. Its products resulted from licensing agreements with renowned organizations or publishers such as Dr. Seuss Enterprises (DSE), Hay House Publishers, Zondervan (a division of HarperCollins), Houghton Mifflin Harcourt Publishing Company, HarperCollins, Mercer Mayer, Soundprints, Andersen Press, Kidwick Books, Child Matters Media, Character Arts, and Chronicle Books. In many cases, the company worked directly with authors and brought their favorite books to the mobile market. These apps were created by the Oceanhouse Media team that included both in–house staff and contractors who comprised about 40% of the employees in 2013. The team included software developers, graphic artists, music composers, professional voice actors, and sound designers. Many of these individuals had worked with Kripalani in his two previous start–ups over 20 years ago. Oceanhouse Media and its competitors were part of the nascent digital apps industry dating to 2007 when the Apple iPhone was introduced in the market. Consequently, Oceanhouse Media and its competitors all started as privately held companies with sparse historical financial information. Oceanhouse Media's balance sheet, however, was known to be debt–free, and with the exception of computer equipment and peripherals the business had few tangible assets (Table 1).

Financial Overview of Oceanhouse Media

Source: PrivCo. (2015).

Oceanhouse Media App Offerings

Oceanhouse Media's first app, Bowls, offered a relaxing way to play authentic Tibetan singing bowls on the iPhone and iPod touch. This app remained a best–seller four years after its initial release. The company released on average one to two new apps each week and had more than 300 apps on the Apple App Store. A number of its apps frequently appeared on Top 100 lists on the App Store. In late 2010, it created more than 100 apps for the Android platform. Oceanhouse Media was approved by Google Inc. as one of its Top Developers, a distinction granted to only 150 apps developers worldwide; there were estimated to be over 400,000 apps developers for iOS, Android, and Windows 8 mobile operating systems. In April 2011, the company launched apps on Barnes and Noble's NOOK Color™, and for the Windows 8 Operating system in Fall 2012.

Seventeen of the company's apps reached the number one spot within their category on the App Store. For example, The Lorax—Dr. Seuss reached the number one spot on the overall iPad Top 100 paid chart in March 2012. Information provided by Oceanhouse Media indicated that (as of March 2013) it had more apps in the Top 300 book apps (for the iPad) compared to other competing publishers such as Disney, HiT, Tab Tale, Sesame Street, Zukka!, Loud Crow, Nickelodeon, Scroll Motion, and Random House.

Oceanhouse Media Children's App Offerings

The company's children's apps that carried the omBook™ (Oceanhouse Media digital book) trademark, focused on promoting reading and literacy. The company's Dr. Seuss apps received critical acclaim (Children's Technology Review) and numerous awards (such as Parents’ Choice Awards). Twelve of the company's children's omBooks reached the number one spot on the App Store in the Top Paid Books category. Oceanhouse Media's children's digital book apps format that comprised its combination of “Read To Me, Read It Myself and Auto Play” features, as well as word highlighting and picture/word association techniques (first introduced in Fall 2009), were adopted by many children's digital book app publishers.

Children's digital applications—books and games—contributed about half of Oceanhouse Media's total revenues. A mainstay of Oceanhouse Media's children's apps was the collection of Dr. Seuss books offered as interactive digital book apps. These apps resulted from licensing agreements that were executed by Oceanhouse Media with DSE; the latter owned the digital rights to the Dr. Seuss books and managed the books, the movies, the apps, and the television shows based on them. In a recent development, the New York Times reported that Random House Children's Books (a division of Random House, Inc.), publisher of the Dr. Seuss books, would release the first titles of the Dr. Seuss collection in eBook format starting September 2013. Susan Brandt, President of DSE, said, “the e–books will be faithful reproductions of the print books in terms of text, illustrations and layout …. Enhanced versions with bells and whistles might come later” (Bosman, 2013). Oceanhouse Media had to navigate a profitable growth path in this increasingly crowded but very rapidly growing digital applications market.

Kripalani attributed Oceanhouse Media's success in the overly crowded app market to key features of its app creation, development, and marketing process. It developed its own technology platform that comprised unique app engines that enabled easy updates of its app portfolio, and agile product development by avoiding lengthy development cycles. It provided strong customer support to its mobile audience through effective use of social media that facilitated promotion of new apps to new and current customers, and enabled rapid response to customer feedback. It controlled app production costs by omitting superfluous animation and games in children's book apps, which facilitated the sale of low–priced apps. Finally, it established strong relationships with key publishing houses and authors that enabled the creation of apps for immensely popular brands that were promoted cost–effectively and reached a large customer base quickly.

Oceanhouse Media Business Model

In an interview in 2011, Kripalani indicated how Oceanhouse Media identified potential app opportunities:

Our business model is focused on securing licensing agreements primarily for well–known series and popular authors. We typically will not sign one–off or small scale deals. For some series that do not have the name recognition of say Dr. Seuss or The Berenstain Bears, we look for books that feature both illustrations and content that would effectively translate into a digital format. Not all children's books can be enhanced by them being turned into apps. We look for the ones that would shine. When looking for our next licensor, we try to find content that is in line with our company's mantra of creating apps that uplift, educate, and inspire. We have an in–house review policy and regularly research potential licensors. (Des Roches Roca, 2011)

The company's cost structure reflected its hiring strategy which minimized the use of full–time employees relative to contract employees. Employee compensation also included a share of the revenues (over the life time) of each individual app created by an employee.

Kripalani, an alumnus of the UCSD, served on the Advisory Board of the UCSD Geisel Library (named in honor of Ted Geisel, a.k.a. Dr. Seuss). He secured an introduction to DSE through the head librarian. In an interview, Kripalani said, “I went into my presentation with DSE holding a sample of what I knew a Dr. Seuss book app should look like on an iPhone. It was a full working prototype. They were intrigued and allowed us to develop a number of Grinch–themed apps, including our first omBook, How The Grinch Stole Christmas! We later secured the rights to bring all 44 classic Dr. Seuss books to the app market” (Des Roches Roca, 2011). While these rights were not exclusive, Kripalani indicated that his personal cultivation of the relationship with Dr. Seuss Enterprises was a key ingredient to the success of Oceanhouse Media.

The company's primary revenue was generated from sales of digital book apps typically sold for prices ranging from $0.99 to $3.99. For apps sold at a positive price, generally 20–30% of the sale price accrued to the distribution platform provider (i.e., Apple App Store, Google Play, Windows Phone Store), and the remainder to the app developer. However, the company also created mobile games, most of which were related to the book titles. Many of the books that were converted into apps sold over 25,000 copies with popular names selling into the hundreds of thousands. For the company's apps that were targeted at children, its revenues were generated through app sales as opposed to display advertising. Kripalani had concluded that success in the digital applications market required publishing a large number of games and electronic books under license from big names such as Dr. Seuss. While each one of the apps sold in small numbers, the large volume of apps was enough to generate a diverse portfolio of products that sustained the business.

Oceanhouse Media's business model could exemplify the “long tail effect” which referred to the observation that firms using digital distribution technologies could garner significant revenues from selling a large number of different products, where each product generated a small amount of revenue (Ostenwalder & Pigneur, 2010, pp. 66–75). Since digital distribution could significantly lower app variable production costs (excluding development, design costs), selling a large number of different apps, with each app generating a small amount of revenue, could still result in positive profits and cash flow.

The Mobile Apps Market

Apps Market Overview

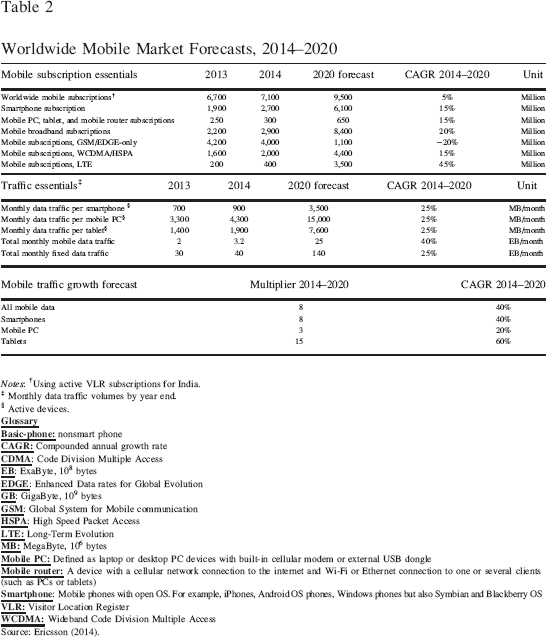

Apps are end–user software programs designed for mobile device operating systems that enhance mobile device capabilities. Apps were first introduced in 2007 with the Apple iPhone. Since then, growth of the apps market has rapidly accelerated as other smartphone platforms as well as tablet computers have embraced apps. Revenue from mobile apps comprised both paid downloads and revenue from advertising and sale of virtual goods. According to Portio Research, globally, app revenues were approximately $12 billion in 2012, a figure forecasted to grow to over $60 billion in 2017 (Whitfield, 2013). The growth of the apps market was fueled by: (1) the availability of mobile devices with powerful processors, (2) wireless networks that delivered consistently high bandwidths with better user experiences, and (3) increasing interest and creativity of apps developers. The growth forecasts were robust and pointed to significant growth for the digital applications market since digital apps were created primarily for use on mobile devices (Table 2).

Worldwide Mobile Market Forecasts, 2014–2020

Notes: †Using active VLR subscriptions for India.

Monthly data traffic volumes by year end.

Active devices.

Source: Ericsson (2014).

Salient Features of the Apps Market

The rapid growth in apps development was facilitated by mobile platforms such as the Apple iOS and Google Android systems; these systems along with their distribution counterparts—the Apple App Store and Google Play—lowered both the development and distribution costs of mobile apps (Bresnahan, Davis, & Yin, 2014). The mobile apps industry/market was young and had its origins in the 2007 introduction of the iPhone. At this early stage of its evolution uncertainty surrounded key issues for this market: What kinds of apps would be used by consumers? Would apps be purchased by consumers or would the apps be supported by advertising? Which existing industries would be disrupted by the apps? How would new apps be discovered by prospective users?

Consumers access apps primarily through distribution platforms such as the Apple App Store, and Google Play; each of these had over 800,000 apps available for consumers in its stores. Additionally, the Windows Phone Store offered 145,000 apps; BlackBerry World offered about 120,000 apps. While Google Play accounted for 51% of all app downloads from these four platforms, the Apple App Store accounted for 74% of all revenues from these four stores (Canalys, 2013). The app store mode of distribution presented challenges to app developers in that app store conditions could be restrictive; the stores took a significant share of revenue from each app sold in the store. For example, the Apple App Store received 30% of the app price and the over–crowded app stores made it difficult for new apps to be discovered by users.

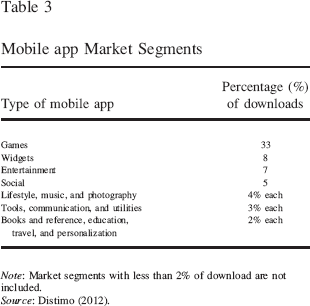

Mobile App Market Segments

The mobile apps market had evolved with diverse segments that comprised e–books (with limited interactivity), digital books (integrating the story with substantial interactivity), games, other consumer applications including health, finance, and self–help (to name just a few). Games were the most downloaded of all apps (Table 3).

Mobile app Market Segments

Note: Market segments with less than 2% of download are not included.

Source: Distimo (2012).

Challenge of Discoverability: Matching Digital Apps to Customers

The mobile apps market needed mechanisms that matched apps and their developers to mass–market buyers. New apps were introduced at a very high rate and the problem of categorizing apps remained unresolved and resulted in broad apps categories (market segments) such as games, education, travel, health and fitness, music, and so forth. This increased the challenge of search for relevant apps for customers. Games companies were spending 60–70% of their gross profit on marketing. At a recent Apple's developer conference with an attendance of around 5,000 participants, a common concern expressed by developers was a “dearth of ways to promote their app in the app store, which they viewed as vital to their survival” (Vascallero, 2012, p. B1).

The solutions offered by the online stores such as Apple App Store and Google Play took the form of “top lists” of apps, which were problematic at matching app demand by prospective customers. A prospective user could search for apps by keyword or look at “top lists” such as “top free apps,” or “top paid apps,” or “top–grossing apps,” that is, highest revenue. An important implication of the “top lists” structure was that, “an app can be popular because it is highly visible on the top lists, but it is on top because it is very popular” (Bresnahan et al., 2014, p. 7). Since rankings were closely associated with an app's popularity, developers were likely to be incentivized to manipulate the rankings by purchasing apps downloads to improve their rankings, thus making downloads problematic as a gauge of app demand.

Another implication of the “top lists” feature in promoting an app was that it engendered a strong winners–take–all flavor. This was reflected in a highly skewed distribution of app demand: 50% of all app revenues were shared between just 25 developers (Canalys, 2012). Ten percent of the revenue in Google Play and Apple App Store accrued to just four and seven apps, respectively. The huge installed base of apps and the continued development of new apps increased substantially the marketing costs of app developers, and especially developers without a pre–existing connection to their customers.

Children's Digital Apps Market Segment

While a narrow segmentation of the apps market was problematic, broad market segments of the apps market comprised games, education, travel, health and fitness, social networking, utilities, and retailing. The children's digital apps market segment was typically subsumed under education and generally comprised e–books, enhanced e–books (which merged film, gaming, and interactivity in an app), and “learning” games. While estimating the size of the children's segment was problematic, annual survey data from the Association of American Publishers and the Book Industry Study Group indicated that e–book sales in 2012 in the children and young–adult categories increased 170% to $469.2 million from 2011.

The survey found that while print formats were flat or declining, e–books and downloadable audio books grew substantially (attributed in part to the widespread use of mobile devices). E–books accounted for nearly 23% of publisher net revenues in 2012, up from 17% in 2011, just 1% in 2008, and 0.05% in 2002. Children's e–books were up 120% in 2012 to $233 million, due in part to the success of titles like The Hunger Games. According to Bowker, a company that tracked the book industry, about 7.4% of children's books sold in the first quarter of 2011 were digital (excluding young adult titles) compared with 13.5% across all book segments over the same period. Kelly Gallagher, vice president of publishing services at Bowker, predicted that the share of digital units in children's book publishing could double in 2012 to as much as 15% (boosted in part by the growth of tablet use). A mix of established publishers and start–ups produced, marketed, and sold children's book apps. While children's publishing powerhouses like Scholastic Inc. and Sesame Workshop had active digitization and app–development efforts, a slew of start–ups entered the market with children's book apps, too.

App Use by Children

The Joan Ganz Cooney Center at Sesame Workshop completed a study of 200 top–selling children's paid apps in the Education category of the Apple Apps Store (Shuler, 2012). The study found that while over 80% of the apps targeted children ranging in age from toddler to high school, 58% of the apps targeted toddler/preschool children. Since 2009, the percentage of apps for children in every age category increased; this age group also experienced the greatest growth, 23% from 2009 to 2011. In 2009, nearly half of the top–selling apps targeted preschool or elementary school children. That figure increased to 72 % in 2011. In 2009, almost 90% of paid apps that targeted children were at the lowest price point of $0.99; however, that percentage declined to 36% in 2011. In 2011 apps priced at $1.99 comprised 38%, and apps priced at $2.99 comprised 14% of top–selling apps. App creation was only half the battle even for children's apps. App discovery was critical, and the most effective method of getting found (especially for children's apps)—being charted or featured/blogged—was typically out of the developer's control. Hence, an outstanding app had to be discovered and downloaded by a prospective user to benefit the app developer.

Economics of the Apps Market

Business models for apps continued to evolve; earlier models focused primarily on paid download or subscription fees that bundled other forms of content like ringtones and pictures with applications. However, over the last few years, advertising–based models had become more prevalent and successful with developers. Thus from an app developer's perspective, its revenues were obtained from selling apps for a price (paid apps), for a subscription fee or by allowing users to download the app for free (so–called “freemium” apps), but with the expectation that the developer would capture revenues through the sale of ads in the app or through in–app purchases of some kind (for example, sale of virtual goods) by app users.

The profit relationship for an apps developer could be expressed as: Expected Economic Profit = Expected Revenues − Expected Costs, where costs comprised licensing, development, and marketing costs; overhead expenses; taxes; and debt and equity costs.

App Revenue Generation

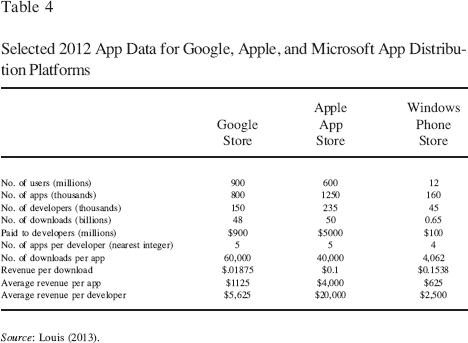

A survey of more than 10,000 app developers reported that app businesses were not sustainable at current revenue levels (VisionMobile, 2014). Fifty percent of iOS developers and 64% of Android developers were below the “app poverty line” characterized as $500 per app per month. Twenty–four percent of developers interested in making money earned nothing at all. A further 23% made less than $100 per app per month. While the overall app market was still growing, the revenues were highly concentrated. At the top end of the revenue scale there were just 1.6% of developers with apps that generated more than $500,000 per month; collectively they earned multiples of revenues of the remaining 98.4% of developers. Games dominated app store revenues, yet most games developers struggled; 57% of games generated less than $500 per month. The difficulty in generating sufficient revenue from the average app was caused by the change in the composition of free versus paid apps in recent years. The percentage of apps (on the Apple App Store) between 2010 and 2012 that were free varied between 80% and 84% but by 2013 90% of apps in use were free. Revenues were generated from a combination of (1) paid apps downloads, or subscription fees, and (2) ad sales or in–app purchases. Table 4 contains estimates of the revenue components of the profit relationship for 2012 across the major app stores—Apple App Store, Google Store, and Windows Phone Store.

Selected 2012 App Data for Google, Apple, and Microsoft App Distribution Platforms

Source: Louis (2013).

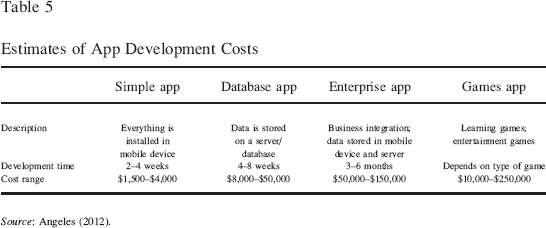

App Development Cost

High quality mobile apps were based on strong conceptual foundations, top–notch talent in both the design and engineering phases, and effective planning of the app creation and development process. App development comprised the following activities: designing and programming, testing and debugging, additional functionality (including social media integration, in–app purchasing, and infrastructure and database management). After an app was built, tested, and ready to be released, the app developer hosted (or obtained services to host) the app, and maintained the infrastructure, and back–end support systems that facilitated the sale of the app. These activities were in addition to the actual marketing of the app (Table 5).

Estimates of App Development Costs

Source: Angeles (2012).

Oceanhouse Media Competitors

In conversations with Michel Kripalani, he had identified five privately held VC– backed firms with products in the children's mobile apps market segment that were viewed as strong competitors to Oceanhouse Media's children's apps. Their business models had evolved with revenues generated from both free and paid apps. These firms were all founded post–2008; and, as very early stage start–ups did not have a history of revenues or earnings. However, all of these firms had received VC investments and were expected to have significant future growth prospects.

Callaway Digital Arts

Callaway Digital Arts (CDA), founded by industry veteran Nicholas Callaway, was a privately held, mobile application development company. In November 2010 venture capital (VC) firm Kleiner, Perkins, Caufield, and Byers (KPCB), and two angel investors, Ram Shriram and Mark Pincus, collectively invested $6 million in an A round. Ram Shriram, based in Silicon Valley, California, had invested in Google, Zazzle, StumbleUpon, and Pinkberry. Mark Pincus, based in San Francisco, California, had invested in Facebook, Grockit, and Buddy Media. CDA was reported to have received a five–year $12 million grant from the Department of Education to create a series of game–based mobile applications to build reading and math skills for children ages two through eight. The company catered to children and families. CDA formed partnerships with children's content creators that featured notable characters in children's apps. The company used Sesame Street characters and Miss Spider in their apps, including The Great Cookie Thief and Miss Spider's Tea Party. CDA had offices in New York City and San Francisco. In May 2012, the company relocated all of its operations to San Francisco, and Nicholas Callaway stepped down from his role of chief creative officer at CDA (Reid, 2012).

CDA Business Model

Callaway Digital Arts sold all of its apps on the Apple App Store to generate revenues. The company offered 14 different apps priced from $1.99 to $4.99. Most of CDA's costs were incurred when it created and developed apps. CDA's goal was to be profitable by 2013. In 2011, it reported revenues of $6.4 million with 40 employees at the firm.

Duck Duck Moose, LLC

Duck Duck Moose, LLC, headquartered in San Francisco, was a privately held company that offered apps in: Educational Games, Educational Media and Online Curricula, and Mobile Applications segments. In September 2012, it received $7 million in an A round investment from Sequoia Capital, Lightspeed Venture Partners, and participation from Stanford University. The additional funding would be used to grow its product line with more Android apps and to develop a custom analytics and parent–reporting feature that monitored and reported to parents about their child's progress (Perez, 2012).

The company was founded in 2008 by Caroline Hu Flexer, who worked formerly as a design consultant at IDEO; her husband Michael Flexer, who had extensive start–up experience; and designer Nicci Gabriel. The company grew its brand through word–of–mouth alone; it had created 17 apps and received 15 Parents’ Choice awards, 15 Children's Technology Review Editor's Choice Awards, and received a KAPi award for the “Best Children's App” at the 2010 International Consumer Electronics Show.

In July 2013, the company appointed Alan Shusterman as Chief Executive Officer and a member of the Board of Directors. He was an early investor and Vice President of Client Services at Edusoft, a web–based assessment management platform used by school districts to manage students’ performance. In 2 years, he helped grow Edusoft revenues 20–fold, which led to its purchase by Houghton Mifflin Corp.

Duck Duck Moose Business Model

The company worked closely with educators and children as it tested its apps, the focus of which ranged from creative play to learning numbers and letters. Almost all the apps (iOS and Android) sold for $1.99 apiece, with just a few iPhone versions at $0.99, and none offered in–app purchases (which according to the company diminished the learning experience for younger children who tended to tap all over the screen).

Ruckus Media Group

Ruckus Media Group, headquartered in Wilton, Connecticut, was a privately held, venture capital–backed social media company that created interactive applications for mobile devices. The apps were designed to entertain and educate children and were recognized with over 30 parenting and app awards for its digital storybooks. Ruckus was founded in 2010 by Rick Richter, formerly the President of Children's Publishing at Simon & Schuster, and founder of Candlewick Press. The company's Board of Directors included leaders with substantial media, business, and financial experience. 3

In March 2011, it received $3.5 million in an A round investment from Alsop Louie Partners, and an unspecified investor. In a press release dated May 23, 2013, the company reported that it had received a grant from the U.S. National Science Foundation (NSF) to build Read Together While Apart ™ (RTWA) Technology, a collaboration infrastructure that ran on networked mobile and nonmobile devices and enabled a parent and child to read Ruckus’ eBooks together and to play interactive games in the eBook even when the parent and the child were not in the same location.

In 2012 the company introduced the Ruckus Reader App, which provided a single–stop destination for digital content and included classic books, popular characters and brands for kids’ ages 2 through 10 years; this app was available for Apple devices including the iPod Touch, iPad, and iPhone. Ruckus offered three types of content: iReaders that were interactive digital books (with voice–over narration) and featured integrated activities and video clips; ReadAlongs that were eBooks with voice–over narration that brought the traditional picture book experience to a mobile device, and Videos were downloadable episodes from some of today's most popular brands that were commercial–free and airplay–enabled, allowing users to view them via Apple TV as well as all IOS devices.

In November 2013, KiwiTech, a Washington, DC–based mobile technology company, acquired a 75% interest in the company for an undisclosed amount. Ruckus founder, Rick Richter, would leave the company following the completion of the deal. The VC firm Alsop Louie Partners retained a minority stake in the company. The change in ownership resulted in the closing of Ruckus' office in Wilton, CT. Jason Root, previously Ruckus’ chief content officer, became the CEO of Ruckus Media Group and reported to Rakesh Gupta, KiwiTech CEO (Publishers Weekly, 2013).

Ruckus Media Business Model

The company's apps were priced from $0.99 to $3.99 in the Apple App Store. The company always offered one free title which was regularly switched out to offer other titles of free content. The company was expected to enhance its product offerings across all major mobile devices by expanding distribution from Apple's iTunes to Google's Android Market, Research In Motion's Blackberry App World, Amazon's App Store and the Barnes and Noble Nook.

TabTale

TabTale was a privately held company headquartered in Tikva, Israel. Founded in 2010, TabTale offered a growing catalogue of classic children's stories, creative mobile games, and innovative learning experiences—many ranked as the top apps for children on the iPhone, iPad, and Droid phones. The company had released more than 250 games, interactive books, and educational apps.

The company raised $12 million in Series B funding in October 2013 from Qualcomm, Inc., Magma Venture Partners, Vintage Investment Partners, and some existing investors for a total of $13.5 million since it was founded. These funds were used to seek expansion opportunities around the globe. TabTale acquired Israel–based Kids Games Club, maker of apps like “Paint Sparkles,” in a deal valued between $3 million–$4 million (Lunden, 2013). In May 2014, TabTale acquired Coco Play Limited, a Hong Kong– and China–based developer of educational apps and games for kids. Coco Play's portfolio of 3D children's games included some of the top free apps for kids in several East Asian countries, such as Coco Princess, the number one free kids’ app in China. Coco Play's two million users would join the 25 million users of TabTale apps. Over 350 million downloads of TabTale products had occurred over the last 3 years, among them some of the most popular kids’ educational apps in the Apple App Store and Google Play. The company had over 180 employees in its offices in Israel, the United States, Macedonia, Ukraine, and Bulgaria. These employees would be joined by several dozen Coco Play employees.

TabTale Business Model

All of TabTale's apps were built on top of a shared back–end allowing it to develop many apps without wasting time coding and recoding core assets. This platform strategy enabled a rapid flow of new apps and updated back catalogue to build rapport with its customers. Nearly all of TabTale's downloads were based on a freemium model, with the app or game available for free but extra features provided for a fee. In Outdoor Baby, one of its popular games, for example, users could play for free and buy virtual goods, such as tents and flashlights, for real money. TabTale derived much of the approximately $20 million of its annual revenue from such fees, according to industry sources.

Zuuka

Zuuka, founded in 2009, was a privately held publisher of mobile children's content. It provided content owners a distribution channel for delivery on a global scale. The company used iStoryTime as its flagship label, but also published Zuuka Comics and iTalk Smurfs. iStoryTime was an interactive storytelling experience in the form of ebooks for mobile devices and featured a series of illustrated and narrated books. It was designed for toddlers aged 2 years and up and featured original as well as known stories and characters. The application included animation, sound effects, narration, and activities that entertained its audience. iStorytime also had narration options and onscreen text that helped children develop early reading skills. With over 120 titles to choose from, Zuuka had developed titles for several major digital mobile licensing partners including Harper Collins, Nickelodeon, Random House, Cartoon Network, Sony Pictures Entertainment, and more.

In 2011 Zuuka reported revenues of $480,000 and had six employees at the firm. Zuuka had offices in Santa Barbara, California, Frankfurt, Germany and Los Angeles, California. In August 2011, Frankfurt, Germany–based investment bank, CFP Beratungs, GMBH invested about $2 million in an A round. In March 2014, Zuuka was acquired by Cupcake Digital, a New York–based developer of a large portfolio of brand–name children's mobile applications (Perez, 2014). Cupcake Digital offered a number of mobile apps and games, that featured characters from Kung Fu Panda, Jim Henson's Fraggle Rock, Strawberry Shortcake, VeggieTales, Yo Gabba Gabba!, Animal Planet, Wow Wow Wubbzy, and The Smurfs, for example. Combined, the acquisition would enable Cupcake Digital to offer a library of over 250 titles and a reach of over 8.5 million downloads.

Zuuka Business Model

Zuuka held a number of licenses to notable characters and stories from children's content owners and created multimedia stories. iStorytime apps were priced from free to around $4.99 per app. The company's costs comprised licensing costs, operating costs of managing the iStorytime platform, and maintaining relationships with partners. Zuuka's iStoryTime app was expected to expand its e–book library significantly in the future with access to Cupcake Digital's licensing portfolio and relationships.

Financing Considerations for Oceanhouse Media

Oceanhouse Media was structured as an S–Corporation with Kripalani and his wife, Karen, as sole shareholders; to date the company was self–funded. While several of its competitors had received VC funding, and Kripalani was approached in the past by VCs interested in investing in the company, he was concerned about the impact VC investments would have on founders’ ownership interests, the company's future growth path, and its exit options. Mobile/digital start–ups had received significant VC investments in recent years. According to Rutburg & Co., an investment banking firm in San Francisco, VCs spent $6.3 billion, or 42% of their budgets, on mobile investments in 2011 compared to $4.5 billion or 32% of their investment budgets in 2010. In 2011, mobile marketing and advertising start–ups secured $592 million versus $128 million in 2010; mobile commerce and payments start–ups secured $558 million in 2011 versus $276 million in 2010; and mobile health start–ups secured $356 million versus $209 million in 2010.

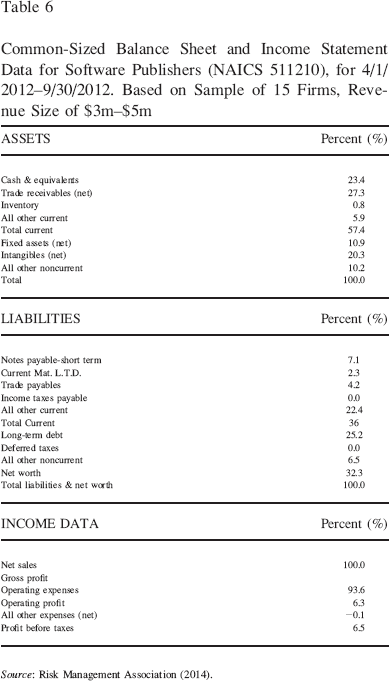

Several high–profile mobile games start–ups had recently secured significant amounts of VC investments, compared with digital book app start–ups that had secured relatively modest amounts of VC funding (per amounts indicated in the previous section). Kabam, a maker of mobile games like “Kingdoms of Camelot” and “Dragons of Atlantis” received a total of $240 million (since its founding 8 years ago) from VCs including the $120 million round in September 2014 from Alibaba that valued Kabam at $1 billion; Kabam's 2013 revenue was $360 million (Chapman, 2014). Other mobile game start–ups that had recently gone public included Zynga (operating online social games) with 2013 revenues of $873 million and a market capitalization in September 2014 of $2.8 billion; King Digital Entertainment, LLC, creator of the popular Candy Crush Saga mobile game with 2013 revenue of $1.88 billion and a market capitalization in September 2014 of $4.2 billion (Table 6).

Common–Sized Balance Sheet and Income Statement Data for Software Publishers (NAICS 511210), for 4/1/2012–9/30/2012. Based on Sample of 15 Firms, Revenue Size of $3m–$5m

Source: Risk Management Association (2014).

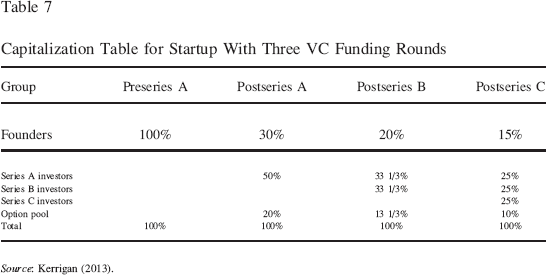

Kripalani was intrigued by the possibility of the debt financing alternative to support his company's growth though he was unsure of how the business would be viewed from a traditional lender's perspective. The issues of VC financing for, and possible sale of, Oceanhouse Media were both related to its estimated valuation at year–end 2013 (Table 7).

Capitalization Table for Startup With Three VC Funding Rounds

Source: Kerrigan (2013).

Conclusions

As he looked back on Oceanhouse Media's five–year journey at year–end 2013, Michel Kripalani noted that Oceanhouse Media had been profitable, cash flow positive, and self–funded in a growing but increasingly competitive digital applications market wherein mere survival for the typical app developer had been a continuing challenge. Random House Children's Books (a division of Random House, Inc.), and publisher of the Dr. Seuss books had announced that it would release the first titles of the Dr. Seuss collection in eBook format starting September 2013. While the eBooks would be faithful reproductions of the print books, enhanced digital versions with interactivity would surely follow in the near future given Random House's access to resources. Access to resources could enable Random House's rapid development of such digital applications by, for example, contracting with programmers, illustrators, designers, engineers, and voice actors outside the United States. As he contemplated on Oceanhouse Media's future growth path at year–end 2013, Kripalani believed that the time was ripe for a comprehensive assessment of Oceanhouse Media's valuation, and relatedly its financial, organizational, and structural choices given its product mix at year–end 2013.

Kripalani was also keenly aware that several of Oceanhouse Media's competitors had been acquired or restructured within the last 12 months. The economic environment for start–ups had improved considerably by year–end 2013; the NASDAQ Composite Index stood at 4156 at year–end 2013 compared to its value of 1632 on January 2, 2009 (the year Oceanhouse Media was founded); while only 41 IPOs were completed in 2009, the number of completed IPOs in 2013 had accelerated to 157. Thus, faced with increasing competition, especially in the children's digital applications market segment (comprising about half of Oceanhouse Media revenues) and a robust start–up market, Kripalani thought that a careful review of Oceanhouse Media's exit strategy was also warranted at year–end 2013.

Footnotes

1.

In an interview in 2013 Kripalani had forecasted an annual 20 revenue growth rate for Oceanhouse Media going forward. Casewriter interview, June 6, 2013.

3.

Per the company website amongst the board members were Jack Romanos, former CEO, Simon & Schuster Publishing; Kay Koplovitz, founder of USA Networks and the Sci–Fi Channel and Chairman of the Board for Liz Claiborne; Neal Zuckerman, management consultant in digital media and mobile industries, formerly of Time Warner and McKinsey; and Dan Weiss, Publisher at Large, St. Martin's Publishing, creator of the bestselling book and television series “The Vampire Diaries” and “Sweet Valley High.”