Abstract

Loss aversion occurs because people expect losses to have greater hedonic impact than gains of equal magnitude. In two studies, people predicted that losses in a gambling task would have greater hedonic impact than would gains of equal magnitude, but when people actually gambled, losses did not have as much of an emotional impact as they predicted. People overestimated the hedonic impact of losses because they underestimated their tendency to rationalize losses and overestimated their tendency to dwell on losses. The asymmetrical impact of losses and gains was thus more a property of affective forecasts than a property of affective experience.

People often prefer to avoid losses rather than gamble for even greater gains. For example, most people are unwilling to accept a 50-50 bet unless the amount they could win is roughly twice the amount they might lose (Kahneman, 2003; Rabin & Thaler, 2001). This reluctance—called loss aversion—influences decision making in a wide variety of domains, including investing, negotiation, politics, and health (Camerer, 2000; Kahneman & Tversky, 1979; McDermott, 2004).

People's choices are often based on their predictions about how different outcomes will make them feel (Loewenstein, O'Donoghue, & Rabin, 2003; Mellers, Schwartz, & Ritov, 1999; Wilson & Gilbert, 2003), and loss aversion is no exception. People seem to believe that the hedonic impact of a loss will be greater than the hedonic impact of an equal-sized gain. If they are correct that the asymmetry of predicted reactions to losses and gains is matched by an equal asymmetry in actual reactions to losses and gains, then people would be wise to avoid losses (Tversky & Kahneman, 1991). For example, if losing $100 is severely distressing, whereas gaining $200 is only slightly pleasant, then it would be rational for gamblers to decline a 50-50 bet with these payoffs. However, if losses do not have a greater hedonic impact than gains, then declining this bet would maximize neither affective nor monetary benefits.

Research suggests that although negative outcomes (such as losses) can be quite painful, people typically overestimate the intensity and duration of their reactions to them. This impact bias has been replicated in both field and laboratory studies of a variety of hedonically relevant outcomes. When people are asked to predict how they will feel if they lose a job or a romantic partner, if their candidate loses an important election or their team loses an important game, or if they flub an interview or flunk an exam, they consistently overestimate the intensity and duration of their negative feelings (Gilbert, Driver-Linn, & Wilson, 2002; Kahneman & Snell, 1992; Loewenstein et al., 2003; Mellers & McGraw, 2001; Wilson & Gilbert, 2003). Research has documented numerous coping processes—including dissonance reduction, self-affirmation, motivated reasoning, and positive illusions—that allow people to recover quickly from negative events (e.g., Festinger, 1957; Kunda, 1990; Steele, 1988; Taylor, 1991; Tesser, 2000). The impact bias occurs in part because these defensive processes operate automatically and unconsciously. Consequently, people fail to anticipate how much they will transform a negative event psychologically (Gilbert, Pinel, Wilson, Blumberg, & Wheatley, 1998).

Thus, losses may loom large in prospect but not feel so large in reality because people find ways to minimize or rationalize them (Ariely, Huber, & Wertenbroch, 2005; Novemsky & Kahneman, 2005; Strahilevitz & Loewenstein, 1998). If this is true, then loss aversion is both a wealth-maximizing error and an affect-maximizing error. To our knowledge, there have been no attempts to test this hypothesis by assessing people's predicted and experienced affective reactions to monetary gains and losses.

STUDY 1

Method

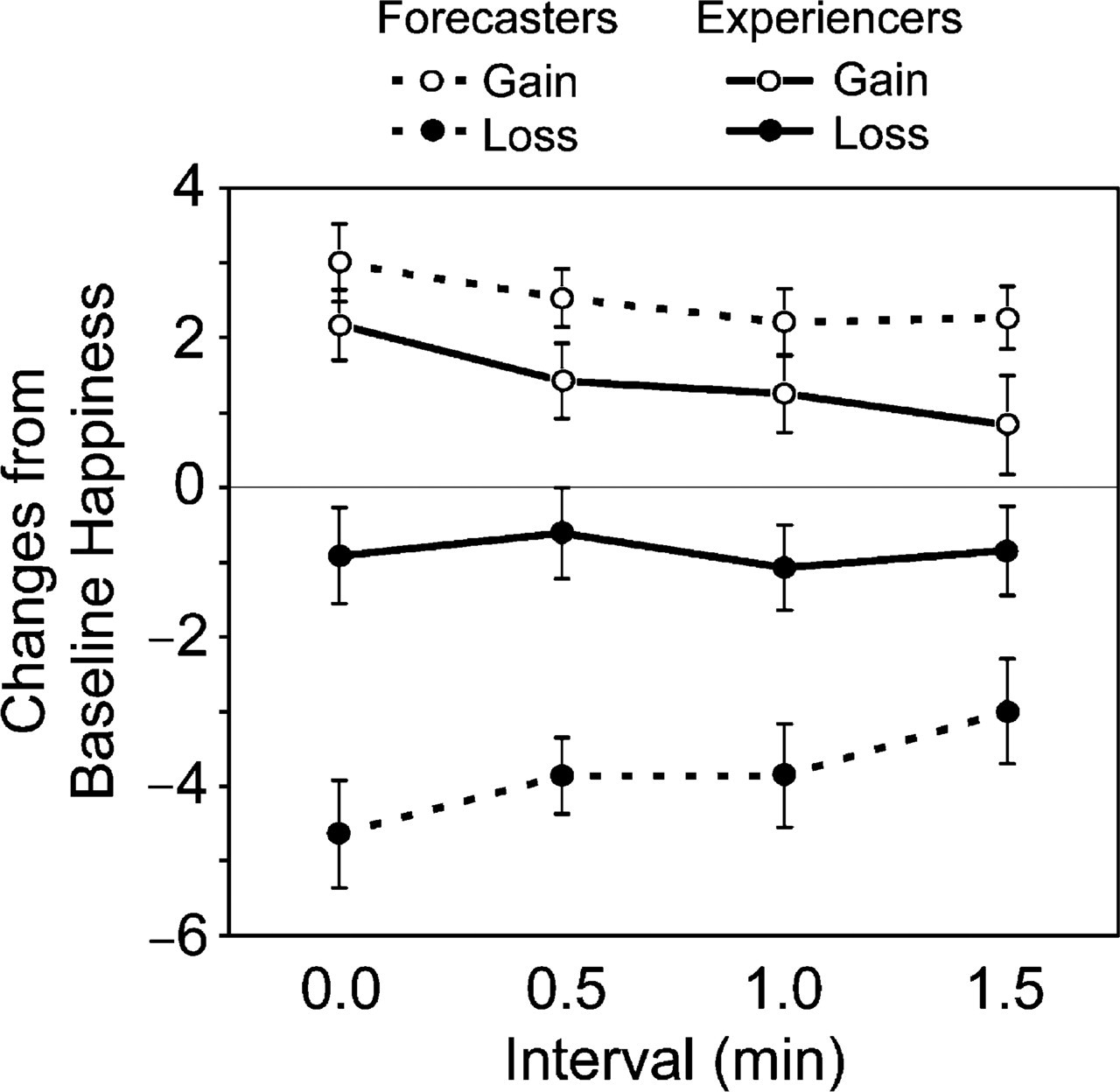

Fifty-four participants (33 females, 21 males) played 44 trials of a gambling game in which a computer randomly ranked playing-card suits (hearts, spades, diamonds, clubs) from first to last and participants guessed what the top-ranked suit would be. They won 50¢ if the suit they guessed was top ranked, won 25¢ if it was ranked second, lost 25¢ if it was ranked third, and lost 50¢ if it was ranked fourth. These amounts were doubled after the 25th trial. Before playing the game, participants reported how happy they felt “right now,” using unmarked lines anchored with not very happy and very happy.

Some participants, randomly assigned to the role of experiencers, were given $5 at the outset and saw their earnings increase or decrease after each trial. In the gain condition (randomly assigned), they ended with a profit of $4, whereas in the loss condition, they ended with a deficit of $4. After the game, experiencers rated how happy they were at 30-s intervals for 2 min. Other participants, randomly assigned to the role of forecasters, watched the computer play either the win or the loss version of the game and then predicted how they would feel had they played.

Results and Discussion

We subtracted participants' baseline ratings of how happy they felt before the game from their forecasted or their experienced happiness. As hypothesized, forecasters were loss averse, predicting that the magnitude of their negative affect following a loss would be greater than the magnitude of their predicted positive affect following a gain (see Fig. 1). Loss forecasters predicted a significantly greater change from baseline than did gain forecasters at the first three time points, ts(27) > 2.29, p reps > .94, ds > 0.88, though not at the last, t(27) = 1.41, p rep = .83, d = 0.54. 1 As hypothesized, though, the loss forecasters significantly overestimated how unhappy they would feel at all time points, ts(25) > 2.32, p reps > .94, ds > 0.93. Gain forecasters marginally overestimated how happy they would be at all time points, ts(25) < 1.90, p reps > .90, ds > 0.76. Finally, gain experiencers were no happier than loss experiencers, ts(23) < 1, n.s. 2

Predicted and experienced happiness after winning or losing $4 in Study 1. Participants made ratings on an unmarked line labeled at the endpoints not very happy and very happy. For purposes of scoring, the line was transformed into 12 units. Participants' baseline happiness, rated at the beginning of the study on the same scale, was subtracted from their later ratings.

STUDY 2

Study 2 tested whether the results of Study 1 would be replicated with a favorable gamble (50% chance of winning $5, 50% chance of losing $3) and whether people would fail to anticipate how much they would rationalize a negative outcome. In a within-participants design, participants forecasted how they would feel if they won or lost the gamble and then reported how they actually felt upon winning or losing. To confirm that people would be loss averse with this gamble, we gave pretest participants (16 females, 5 males) $5 and told them they could either keep the money or participate in a 50-50 gamble in which they could win an additional $5 or lose $0, $1, $2, $3, $4, or $5. Participants indicated whether they would accept each of these gambles. The mean amount that participants were willing to risk was $1.86, which was significantly less than $3, t(20) = 3.59, p rep = .99, d = 1.61. Most participants (16 of 21, 76%) were unwilling to risk losing $3 (different from chance, p rep = .96).

Method

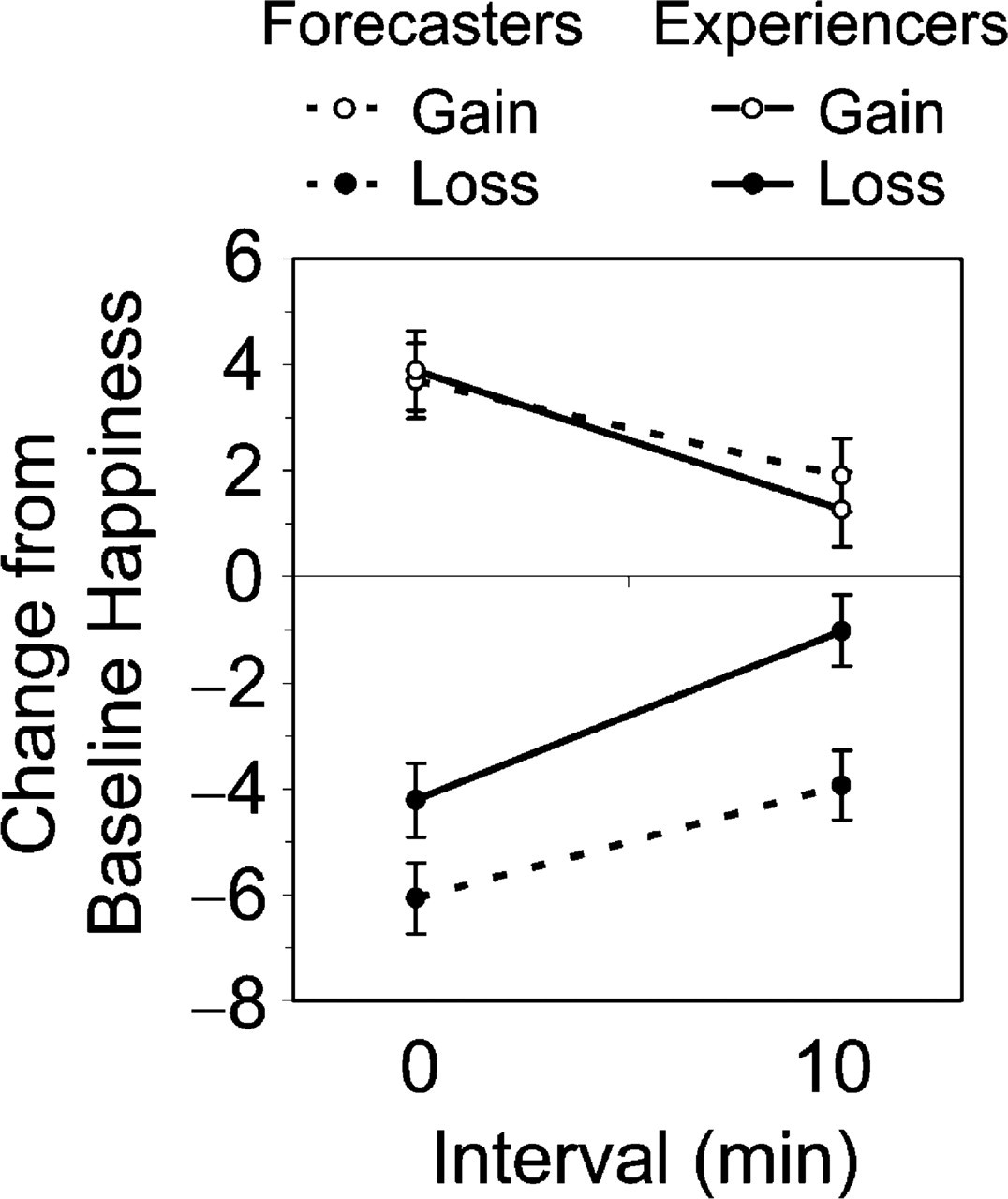

Fifty-one students (35 females, 16 males) received $5 and then answered filler items and rated their baseline affect (how happy, pleased, disappointed, and sad they felt “right now”). These and all subsequent ratings were made on 21-point dotted scales anchored with not at all and extremely. Participants then learned that they would win an additional $5 if a coin landed on heads (or tails) and lose $3 if it landed on tails (or heads). Next, they predicted how they would feel immediately after the coin toss if they lost and if they won, and also how they would feel 10 min later (after reading a description of a filler task). The last 27 participants also predicted what they would be thinking about 10 min after winning or losing the coin toss. At this point, the experimenter flipped a coin and gave participants an additional $5 if they won and took back $3 if they lost. Participants then rated their affect, completed the 10-min filler task, and rated their affect again. The 27 participants who had predicted their thoughts then reported their actual thoughts. 3

Results and Discussion

Participants' ratings of how sad and disappointed they were or would be were reverse-scored and averaged with their ratings of how happy and pleased they were or would be, to create an affect index (the alphas for predictors and experiencers at the different time points ranged from .82 to .93). We subtracted participants' baseline affect from their forecasted and experienced affect. As shown in Figure 2, participants expected the loss of $3 to have greater hedonic impact than the gain of $5 both immediately and 10 min after the gamble, ts(49) > 2.13, p reps > .93, ds > 0.61; that is, their predictions for a loss were significantly more distant from the neutral baseline than were their predictions for a win. As in Study 1, these forecasts were wrong. We analyzed people's predicted and experienced affect with a 2 (gain vs. loss) × 2 (forecast vs. experience) × 2 (Time 1 vs. Time 2) analysis of variance, with the last two variables treated as repeated measures. There was a significant three-way interaction, F(1, 49) = 4.42, p rep = .93, d = 0.60. Participants who lost felt happier than they predicted both immediately and 10 min after the gamble, F(1, 49) = 17.04, p rep > .99, d = 1.18, but participants who won felt as happy as they had predicted at both times, F(1, 49) < 1.

Predicted and experienced happiness after winning $5 or losing $3 in Study 2. Participants made ratings on a 21-point dotted scale, labeled at the endpoints not at all happy and extremely happy. Their baseline happiness, rated at the beginning of the study on the same scale, was subtracted from their later ratings.

Two coders independently assigned participants' predicted and actual thoughts to categories. Their ratings for each category (1 = participant listed a thought that fit the category, 0 = participant did not list a thought that fit the category) were averaged. As hypothesized, participants who lost failed to anticipate how they would think about losing $3. They were most likely to predict that they would feel disappointed (M = .63, SD = .43; coder agreement = 67%), and relatively few mentioned that they would focus on the fact that they had made a profit of $2, given that they had initially received $5 (M = .42, SD = .47; coder agreement = 88%). Once these participants lost, however, they most commonly reported thinking about the $2 profit (M = .75, SD = .40), significantly more than they had predicted, t(11) = 2.35, p rep = .93. Relatively rarely did participants report feeling disappointed (M = .29, SD = .33), significantly less than they had predicted, t(11) = 2.97, p rep = .97, d = 1.79. In short, most participants predicted that when they lost they would think about the disappointment of losing $3, but in fact, when they did lose, most thought about the satisfaction of keeping $2. Participants who won $5 made relatively accurate predictions about their thoughts. Their most frequently predicted and actual thought was that they would be (or were) happy that they won (Ms = .93, SDs = .07).

GENERAL DISCUSSION

Participants exhibited loss aversion in their affective forecasts: They predicted that losing would have a greater emotional impact than winning, even when the amount they stood to lose ($3) was less than the amount they stood to win ($5). However, there was no evidence that losing actually had a greater emotional impact than winning. Instead, participants erroneously predicted they would be disappointed if they lost, and failed to realize that they would reframe the loss positively (e.g., “at least I have $2”).

It might be argued that we did not test loss aversion because people gambled with money the experimenter gave them. Dozens of studies on the endowment effect, however, have shown that once people are given something, they consider it their own and are reluctant to part with it (e.g., Kahneman, Knetsch, & Thaler, 1990). And indeed, participants in both studies predicted that a loss would have a larger hedonic impact than a gain (even though in Study 2, the gain exceeded the loss). By endowing people with $5, we did provide them with an easy way to rationalize a loss (“I still made $2”). Our main point is that participants did not anticipate the degree to which they would take advantage of this convenience.

We acknowledge that losses may sometimes have a greater hedonic impact than gains. Negative events appear to be processed in different regions of the brain than positive events and trigger more intense neural activity (Baumeister, Bratslavsky, Finkenauer, & Vohs, 2001; Cacioppo & Berntson, 1994; Gehring & Willoughby, 2002). Nevertheless, research suggests that even when people have stronger affective reactions to losses than to gains, they are likely to overestimate the hedonic impact of the losses. Studies have found that people overestimate the hedonic impact of important negative events, including losing one's job and getting unwanted results from a pregnancy test (Mellers & McGraw, 2001; Wilson & Gilbert, 2003). Thus, even if losing $7,500 does have a larger hedonic impact than winning $10,000, it probably does not have as great an impact as people expect. Loss aversion would still be stronger in prospect than in actual experience.

It might seem that people would learn from experience that losses have less emotional impact than they anticipated. However, studies have revealed a number of obstacles to such learning. As noted, many psychological defenses occur outside of conscious awareness, making them difficult to observe and anticipate. Further, to predict correctly, people must recognize when they have experienced a similar event in the past, make the effort to recall how they reacted to that event, and recall accurately what that reaction was. We have found that people often fail to meet one or more of these conditions (Wilson, Meyers, & Gilbert, 2001, 2003). People might, however, learn that losses have less emotional impact than they predicted if they have the opportunity to experience repeated losses in the same domain over a short period of time (List, 2003; Novemsky & Kahneman, 2005).

To summarize, people believe that losses will have more impact than gains because they fail to anticipate how easily they will cope with losses. This may lead people to make decisions that maximize neither their wealth nor their happiness.

Footnotes

Acknowledgements

The present research was supported by Research Grant RO1-MH56075 from the National Institute of Mental Health. George Loewenstein and Richard Thaler provided valuable comments on a previous draft of this article. We also wish to thank undergraduate research assistants Robert Chan, Jason Chin, Amanda Greslick, Lisa Guttentag, Ginly Lau, and Mika Richardson for their assistance with data collection.

1We report the significance of results using p rep, an estimate of the probability of replicating an effect (Killeen, 2005).

2It is possible that our affect measure is not a ratio scale (e.g., a score of +3 might not represent the same psychological distance from the 0 midpoint as a score of −3). Nor can we be certain that forecasters used the scale in the same way as experiencers. It is implausible to assume, however, that forecasters and experiencers used the scale in the same way for gains but in different ways for losses (see ![]() ). This issue was addressed in Study 2 by using a within-participants design. It is unlikely that people used the scale one way when making predictions and another way when reporting their experiences.

). This issue was addressed in Study 2 by using a within-participants design. It is unlikely that people used the scale one way when making predictions and another way when reporting their experiences.

3We also told the final 27 participants that they could decline to gamble, to see if having a choice altered the results. We employed techniques typically used in research on cognitive dissonance (e.g., Festinger & Carlsmith, 1959), telling participants that the choice was theirs, but explaining that it would be helpful for them to agree. No participant declined to accept the gamble, but at the end of the study most reported that they had had a choice. The forecasting and experience data from participants who were given a choice were very similar to the data from those who were not.