Abstract

One well established phenomenon today is the return of inequalities during the late 20th century and the rise of a new elite – called the working rich by Atkinson and Piketty (2007). Wealthy chief executive officers (CEOs), who more or less directly set their own pay at higher levels each years (Bebchuck et al., 2002), are not solely responsible for this trend. As Savage and Williams argue in the introduction to this volume, financial intermediaries play an important part, especially in financial centres. What is more, inequalities grow not only between finance and the rest of the economy but also within financial firms (Godechot and Fleury, 2005). In one of France's leading banks, Societé Générale, the differential ratio between the shares of the best paid 10 percent and the worst paid 10 percent increased from four times in 1997 to eight times in 2006. Higher up the ladder, the trends are even more marked. The average compensation (fixed wage and bonus) of the ten best paid persons in Societé Générale moved from 760,000 Euros in 1994 up to 6 millions Euros in 2000. 1 The top ten best paid includes many who are neither CEO nor chief financial officers nor, strictly speaking, ‘traders’ or ‘sales’ managers, although they are often designated by these terms. They are generally ‘Head of’ some activity or department, as in Head of Dealing Rooms, Head of (big) desks, or Head of Departments such as ‘Equities’, ‘Equity Derivatives’, ‘Credit Derivatives’.

Such a shift is not well explained by the common neoclassical hypothesis of biased technological progress, which raises the demand for, and hence the price of, rare and productive skills. (Murphy and Zábojník, 2004). Other explanations need to be explored. In our previous work (Godechot, 2006; Godechot, 2007), we have shown how elite financial workers gain power through the appropriation of productive assets within the firm. First, this implicit property provides the legitimacy for claiming the fruits of ‘their’ assets. Second, employees benefit fully from any moves they make (or could potentially make) through this dynamic labour market since they carry with them intangible assets, like know-how or customer lists, that are difficult to protect, (Godechot, 2006).

In this chapter we would like to detail the importance of social capital for workers in finance, especially for the Heads of Dealing Rooms. Several studies have already shown the importance of social capital in this sector as well as its impact on compensation (Burt, 1997; Burt, 2006; Gargiulo et al., 2006). Lacking precise analysis of how labour markets function, however, previous research has concentrated solely on certain dimensions of social capital, like how information circulates in an organization or the mechanisms of selective matching leading to pay disparities between men and women (Roth, 2006). In order to understand the effects of social capital more broadly, it is important not to rely solely on formal and managerial relations, as described in HR 360 evaluations and such like. One must also analyse carefully what heads of dealing rooms really do. To make some progress in this direction, we undertook three years of mixed methods fieldwork on compensation in the financial industry between 2000 and 2002 mainly in Paris but secondarily in London. During this field-work, a hundred interviews were conducted with diverse actors in the financial industry. In one bank, I was able to make direct observations as a trainee in the internal HR service that had to manage the bonus pool process. In a second bank, with the help of a trade union, I distributed a questionnaire to employees in order to measure their subjective feelings about bonus and obtained 80 answers. In a third bank, after HR insiders gave me access to wage data, I could study the compensation structure. Financial and social annual reports (les bilans sociaux) were collected as well as corporate press releases.

One important issue concerns how social capital relates to workforce flows in the labour market. Some senior employees are able to use the leverage of their accumulated social capital and take their teams with them whenever they change employers, seemingly mobilizing diversified contacts and relatively tightly-knit groups towards this end. Multiple employee moves from one company to another may be hard to measure statistically but they do appear frequent in this world. We counted around a dozen in our survey of the Paris financial sector. We observed that collective moves were particularly beneficial to the person organizing this operation, usually the Head. In 1999, for example, the Head of an Equity Derivatives group and his deputy resigned together, giving their employer, a large bank, just 48 hours to match a rival offer they had received. During the ensuing negotiations, they used the threat of leaving the bank with their entire team. Hence, they could use their social capital to move the scheme along. Their new contracts earned the Head and his deputy €10 million and €7 million respectively in 2000 (Godechot, 2006).

Analysing the relational structure underlying team moves can help us to trace the making of a financial elite. But it also enables us to develop our understanding of social capital. In recent years, many studies on social capital (Granovetter, 1995; Burt 2005; Godechot and Mariot, 2004) have tried to link two contradictory aspects of relational activities: profits generated by the diversification and the non-redundancy of relationships (Burt, 1992); and profits relating to network closure and group cohesion (Coleman, 1988). Diversified relationships make it easier to build entities that are larger but more fragile in nature. Cohesive relationships create team spirit but also generate a lateral control system that makes it harder for a leader to emerge. To study these questions, we need to analyse what Heads of Dealing Rooms do to produce a system of relationships that is profitable both in the workplace and also in the labour market. Towards this end, we suggest that these people are internal entrepreneurs, similar to the proto-industrial ‘bosses’ described by Marglin (1974). Like them, Heads of Dealing Rooms try to create a central lynchpin role for themselves by subdividing and recombining work. In addition, they must be able to get the whole group to move en masse – raising questions as to the stability of a firm's boundaries when, as is the case in finance, social capital-based internal entrepreneurship has started to emerge.

The head of dealing room as an internal entrepreneur

Heads of Dealing Rooms seem to be in a privileged position in financial dealing rooms. Statistical analysis of pay in the finance sector has revealed the rising compensation of these Heads (Godechot and Fleury, 2005). In terms of legitimising the appropriation of profits, a Head of Trading or Head of Sales running a financial products team, and to an even greater extent a Head of Dealing Room, occupies a position akin to a first-tier contractor and original promoter of the activity (Godechot, 2007). Changes in financial organization have also tended to increase the Heads' power to capture profit by concentrating it in their hands. It is more than a suggestive metaphor to call the Heads entrepreneurs. In this extreme example, we may very well discover certain basic characteristics of entrepreneurship, traits that are more visible when the entrepreneurship is in its embryonic phase, that is, when other entrepreneur functions have not yet started to mask the prime function of capturing profit.

Reading Bernard Mottez's (1960, 1966) history of the different forms of wage-earning, one is struck by the formal similarity between the position of a Head of Dealing Room, who is technically an employee, and the ‘hagglers’ or subcontractor who used to practice ‘bargaining’ in the early 19th century. The Head of Dealing Room monopolizes most of the power to recruit. He negotiates the bonus system for the whole of the room and presides over its distribution. Usually the Head is in the practical position of being able to determine, via a budget, how much a subordinate is supposed to be paid. The company provides capital, equipment and a back office. The Head of Dealing Room provides a team of professionals.

Stephen Marglin (1974), an astute observer of the early Industrial Revolution, has analysed the embryonic forms of capitalist firms under ‘the putting-out system’ and characterized, in a famous article entitled ‘What do bosses do?’ the essence of entrepreneurial activity. Reversing the technological determinism found in some of Marx's texts, he has tried to show how technology is a consequence of social order and not a cause thereof. In his opinion, the division of labour was not adopted because of its greater efficiency but because it dispossessed workers of any control over their work and turned entrepreneurs into coordinators who by becoming indispensable to production acquire a situation of power in which they could earn greater profits and pursue a capital accumulation logic. The entrepreneurs' strategy is therefore to ‘divide and conquer’ (Marglin, 1974: 35).

By transforming complex work into simple work, entrepreneurs shift the rent generated at the level of the individual self-employed craftsperson into the hands of the entrepreneur-coordinator. The division of labour is a strategic option, not as much because it makes it possible to produce things in a more technical fashion but because it modifies the locus where rent is captured. The entrepreneur who dispossesses the workers of their work can pay them less and can force them into competition with less skilled workers. Marglin alludes to imperfect competition, which probably plays a major role in this mechanism. A product market is protected by entry barriers, seemingly unlike an unqualified labour market. This means that entrepreneurs are capturing the rents that self-employed craftsperson used to possess. At the same time, entry barriers protect entrepreneurs from the transfer of this rent to consumers via some kind of price mechanism. Under these conditions, the resulting division of labour is politically optimal for the entrepreneurs alone: it is neither a technical optimum nor a social one.

This comparison of recent changes in the finance sector with the beginnings of the Industrial Revolution may appear odd and forced. It brackets employees in very different circumstances, the miserable conditions of manual industrial workers contrasting with the opulence of financial traders and executives who are empowered to conduct negotiations. But there are suggestive similarities between the processes at work, despite the differences in context. In our case, it is not so much the capitalist entrepreneur per se who pursues the ‘divide and conquer’ strategy but an employee, the Head of Dealing Room. The Head is tantamount to a workforce subcontractor who appropriates some of the subordinates' rent by subdividing, re-combining and managing the assigned workload to ensure his own indispensability. Pay in the finance sector may have globally increased in recent years, due to a sharp rise in volume, but this has been accompanied by greater hierarchical disparities. This chapter explains how basic financial traders or salespeople have been appropriating a relatively smaller share of increased profits, with Team Managers appropriating a relatively larger share.

Subdivide and recombine

The political division of labour is an emerging effect, because the multiple effects that the division of labour produces often become visible only over time. In a new activity in finance, people always start out with the idea of subdividing work so as to increase efficiency, then occupy the terrain and mine the ore for as long they can before the competition attacks. A division is initially organized, sometimes euphorically, and everyone is keen to take part. It is only at a much later stage that people notice that the division of labour has been a process for managing interpersonal competition and that it conveys pre-determined forms of value sharing. The history of the division of financial labour is a recurring one of product discoveries by development teams, company launches as with hedge funds, and back office re-organizations; and all of these have emerging effects.

For instance, the Head of a Sales team at Mars Bank became very successful in a short period of time by promoting a range of derivative products tailor-made for customer needs. The team he put together to build on this success, however, was not comprised of peers or apprentices to whom he might communicate the whole of the business. The exceptions were team members located abroad, colleagues of equal seniority and peers he could not really control whom he described as ‘free options’. But, more generally, any newcomers brought in were specialists in fields like tax, law, financial engineering or marketing, so that individuals had a particular set of competencies and undertook a series of tasks that the Head of Sales alone was in a position to re-combine:

I've got guys now who are doing pure structuring [ie designing financial products] so my commercial staff can concentrate on sales and nothing else. (…) What I've done is separate the work into two so that some guys' job is to have ideas and produce brochures, whereas others are supposed to become best friends with CFOs who are potential customers.

The division of labour here possesses a Smithian dimension of efficiency as well as a Marglinian political dimension that is not necessarily intentional but whose force is augmented precisely because the former dimension masks the latter. By positioning himself in the middle of a division of labour that he orchestrates, the Head of Sales can keep the lion's share of a rent whilst enjoying the legitimization of its distribution (as he said, ‘If you ask me, I've made a positive contribution’.

The political division of labour is not always an unintentional effect of a Smithian division of labour. If we retrace the division of labour in the derivative products area from the mid-1980s until the mid-1990s, we note that the division of labour has also been viewed as a political instrument for preventing autonomous financial actors from capturing an activity. The main organizer of the Saturn Bank's Options Department designed its development in opposition to the ‘trader’ model prevalent at the time in other banks, which he criticized for poor change management and for inability to devise a lasting activity. He also explained that he always wanted to avoid the kind of financial handicraft that relies on the juxtaposition of autonomous crafts persons:

There was an inherent weakness in the old way of doing things: these were individual performances, not group ones. (…) What was really bad was how this personalized the work. At times we had a star system, with just one person dominating the whole marketplace. But it's impossible for a single individual, lacking the support of a group or a particular methodology, to last.

Individual performance cannot be relied upon long term because it is safe neither from adverse economic conditions nor from the possibility that the person in question will leave one day. This former Head of Options said about his experience at Saturn Bank that his aim had been to create a ‘collective rent’.

This ex-engineer educated at one of France's top schools, after working a few years for banking information system was given the opportunity in 1985 to construct an options trading operation. He immediately realized then that this new product ‘offered both leverage and safety’ and sensed an opportunity to ‘build an empire’. With a process background acquired during the reorganization of the bank's information system, he came into this new product area firmly committed to creating an entity that would be both technically and socially integrated:

Our policy was to develop our own software and buy nothing … we wanted significant integration between our processes, back office, accounting, front office, etc. We also wanted to be responsible for sorting out any problems, if possible by applying a standard of maximum excellence.

To counter any departures that might have undermined his new structure, he tried to promote, via an advanced division of labour, what Durkheim called ‘organic solidarity’ (Durkheim, 1998 [1893]), that is a solidarity rooted in differentiation, which is more robust than mechanical solidarity when social norms weaken.

In the end, it was this outsider to finance who began to promote an industrial conception of finance (Clark, Thrift, 2005) that could not really come from more traditional activities like stock-broking, portfolio management in Equities or the ‘cambists’ in Foreign Exchange. His approach was based on starting from scratch with the models he wanted to use; creating his own software; training his own employees who were recruited directly upon graduation from the best schools; and, above all, being sceptical about past techniques or actors, bearers of an individual rent that could not be merged with the collective rent he was trying to create. Describing Saturn Bank's Options Department, Uranus Bank's Executive Officer would later say:

They began to develop software to allow them to manage Foreign Exchange options or any other kind of option. As a result, they took two years longer than we did to launch their options business. But when they finally got going in 1985–1986 they were quite successful.

The goal for the Saturn Head of Options at the time was to create an ‘engineering bank’ that unlike ‘commercial banks’ or ‘marketing banks’ would try to ‘to have perfect control over the whole of the risk management and manufacturing process’. Commercial activity was only embarked upon when information technology, modelling, trading and arbitrage processes were all ready. One symbol of such integration was that Saturn Bank was the first to set up rolling Foreign Exchange option books, trade for 24 hours a day and pass from Paris to New York and on to Tokyo.

This modus operandi should be compared with the way that competitors like Uranus Bank constructed their own options trading groups. Uranus opted to acquire blocks of activity that already had a large market presence by buying in teams, software, etc. It took less time for them to become productive – but they were easier to spin off and formed a less durable collective activity. The strengths of Saturn Bank's advanced integration and division of labour should not be exaggerated, however. Despite in-house software and processes, the different elements comprising the entity managed by Saturn's Head of Dealing Room were easy to detach and there was always the threat that a not insignificant proportion of the business could go missing at any point in time. Our exmanager spoke bitterly about American ‘arbitrage’ banks (as opposed to the ‘innovative’ bank he was running) systematically hiring away entire teams with the help of English head-hunters. By taking his employees, they were eating into his collective rent.

Nevertheless, and despite its imperfect efficiency, this is the kind of work organization process that all of the banks surveyed would ultimately end up adopting, and it helped to shift the level at which rents were being capturing. A Head of Dealing Room (and to a lesser degree, a Desk Manager) is there to subdivide, recombine and orchestrate, personally crystallizing a lion's share of a trading division's total value creation. The specialists working below the Heads are often more competent in their own area of specialization but possess little awareness of what is being done on other desks, and even less knowledge of the back or middle offices. In reality, thanks to this divide and conquer strategy, the Head of a Dealing Room is theoretically in a position to break a room's secret value, at least partially, down into simple elements. The manufacturing of these elements can be delegated, but the Head is the only person in a position to recombine them. This is why some, like Saturn Bank's Head of Equity Derivatives group, under whose orders this particular product area had been developed, considered himself:

lucky to have never had to specialize … It would have been completely counterproductive for me to get tied to one area, to settle into it, to say, ‘I need to read up on new models’, etc. Others could do that. My job was to fit the pieces of the puzzle together so that things ran harmoniously and we could grow as quickly as possible.

Top-down coordination is, de facto, inevitable even when it is disputed. A Head of Dealing Room ends up monopolising the rents that the traders used to split amongst themselves. The Head of Options at Saturn Bank was sufficiently powerful to suggest to Senior Management that a partnership should be set up, a specialist options subsidiary autonomous from the parent company, jointly owned by Saturn Bank and its dealing room managers on a partnership basis.

Engineering a collective move

Hence organizing work and managing subordinates is not only a technical process undertaken in order to enhance material productivity. It is also a way of managing social capital and building an indispensable position inside the group. This process of centralization is, to a certain extent, similar to the whole structural aspect of social capital described by Burt (1992). But if we were to view it only in this way, we would focus solely on the exercise of power within the group and ignore the power of the group itself when it copes with other groups. An understanding of social capital requires us to link both dimensions.

Bourdieu (1980, 2) is generally cited for his emphasis on group closure because he stresses the durability and permanent nature of relationships and the strong interconnectivity of agents. These are all factors that are likely to engender a strong group when it interacts with other groups. When, on the other hand, Bourdieu affirms that ‘it is the same principle that produces a group instituted to enhance the concentration of capital and infra-group competition for the appropriation of social capital’ (1980, 3), he is distancing himself from the idea of a jointly-owned form of capital and adopting a more balanced strategic perspective that is closer to Burt. Studying kinship inside Kabyle clans, Bourdieu (1977) showed that the homogeneity and the size of the group was, for its leader, both a positive strength (for harvests or local wars against other clans) and a threat, because it generated costly consumption, risks of schism within the clan and a resulting division of the clan's property. The leader of the clan tries to maintain an equilibrium favourable to his power by constraining its members to appropriate types of marriage (inside or outside the clan). In parallel, Burt's most recent studies (2005) seem to attribute a greater role to group cohesion. He still sees diversification as the main vector of ‘value added’ (Burt, 2006) but now specifies that the group's cohesion enables trust to develop, reputations to stabilize and the group to line up behind an ‘entrepreneur’.

In finance, Heads of Dealing Rooms are powerful not only because they can organize their primacy within the group but also because they build strong groups that can act in their favour. The most striking manifestation of their power is that they can threaten to take all of their subordinates with them if ever they jump ship. The opportunity to redeploy collective assets in the finance business increases the power that the Head acquires through a divide and conquer strategy. He can therefore re-allocate groups of people ruling a range of tangible or intangible assets (market share, products, software, customers, etc.). The advantage inherent in a Head of Dealing Room position is organizational, structural and statutory.

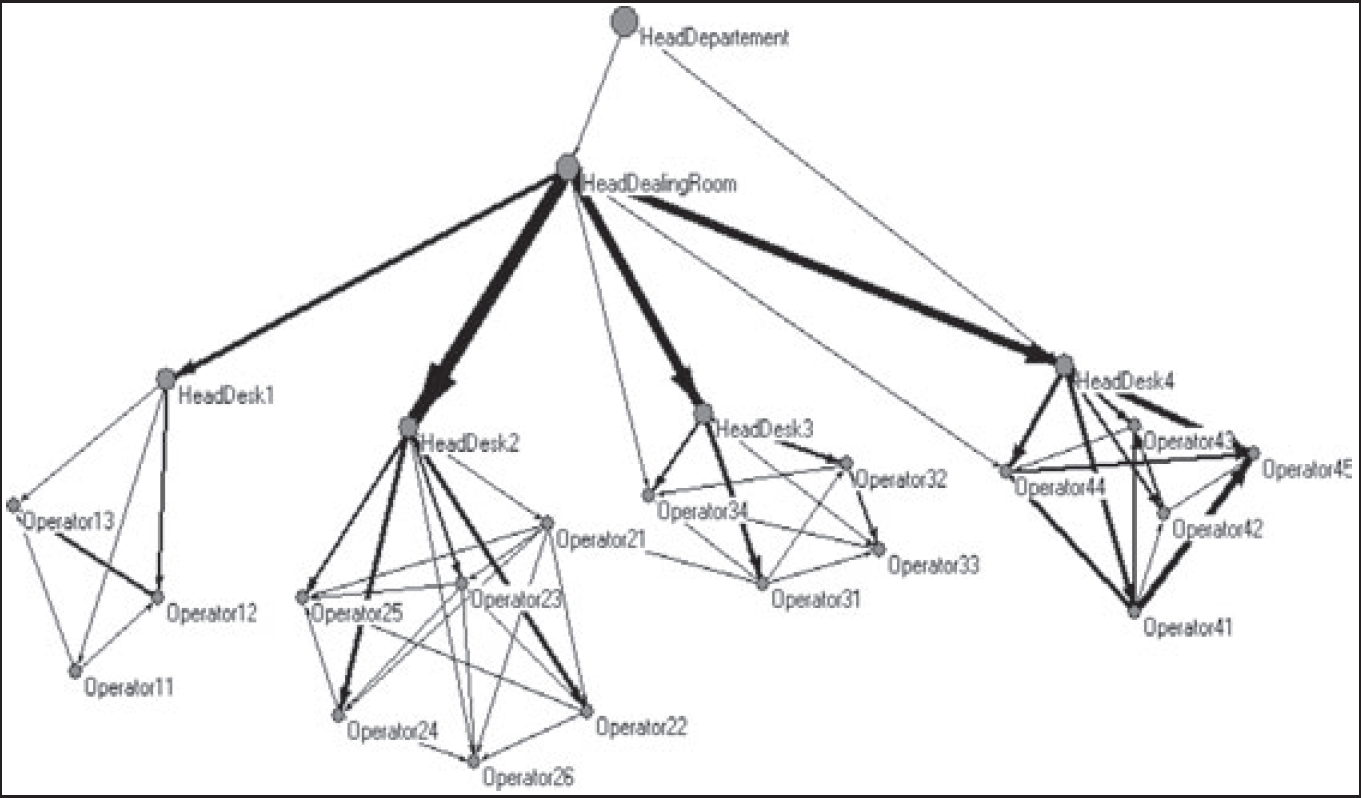

The following analytical schema of networks can illustrate and specify our point about the power to engineer a collective move (see Graph 1). A Head of Dealing Room is best placed to get the whole of the floor to move. It would be much harder for a subordinate financial trader to offer a team for sale because coordination costs would be much higher; and it would be even harder to sell the Head or the whole of the dealing room because this would require a reversal in existing subordination and asset allocation relationships.

Collaborative Relationships within a Dealing Room.

The Head of a Market Department is generally not well placed to organize a transfer of activities, for several reasons relating both to the history of markets and to the organization of work. Department Heads like Jean-François Lepetit (2002) are often individuals who supervize a market's development without doing any real trading themselves. They often suffer from a lack of legitimacy and above all from a lack of control over actual assets in the form of customers, market share, etc. For these individuals, it is more a case of approving subordinates' sharing of assets than of granting their own assets. In addition, Heads of Department often supervize the activity from afar. They work in an office, isolated and protected by ranks of secretary desks and their interactions with the Heads of Dealing Rooms remain sporadic. On the contrary the Head of Dealing Room works directly in the dealing room, interacting on a daily basis with all subordinates, engaging in both business and informal discussions. The Head of Dealing Room will make connections that are both strong and diversified. The work organization will ensure that the centrality lying at the heart of the organizational chart is an effective one. Due to this relational centrality, the Head of Dealing Room is better placed to engineer a collective move. He becomes an indispensable intermediary between contacts separated by ‘structural holes’ (Burt, 1992), among whom he can develop competition in his favour.

But the Head of Dealing Room must take care to preserve also some redundant contacts so as to circumvent, if need be, any second-in-command who may be insufficiently loyal or cooperative. As Gargiulo et al. (2006) demonstrate so clearly, to maximize your profits in the finance industry it can be useful to act as the necessary go-between for your dependents (low density ties) whilst entertaining redundant relationships (high density ties) with the persons upon whom you depend. For instance, the Head of Dealing Room on one of the floors we observed (Godechot, 2001) cultivated all sorts of relationships beyond his direct subordinates. Moreover, an overly porous network could weaken the group dynamic and compromise the chances of a collective move. Closely-knit, united teams are more likely to move en masse, since the group as a whole will put pressure on individual members. Employees will be all the more inclined to leave if they think that the bulk of the team is going, with little more than a skeleton activity being left behind.

The originality of this way of managing social capital is that it incorporates the connections' strength as well as their selectivity, density and porosity. Strong connections are more effective than weak ones when the aim is to engineer a team move. To free up the time to cultivate these crucial connections, a Head has to decide which players are the most important, whilst delegating secondary players' relational networks. It can be more economical to get Desk Heads to organize their own teams' departure than to try to strike up a relationship with every single subordinate and then with their subordinates etc. To become a lynchpin, the Head of Dealing Room must also take care to maintain a modicum of relational porosity. If Desk Heads are in a position to move a whole market group without needing the Head of Dealing Room, the latter becomes surplus to requirements. But at the same time, it is also dangerous for the Head of Dealing Room to depend excessively on the Desk Heads' ability to get their own teams to jump ship.

Rising trading volumes have changed the balance of power in dealing rooms. Where a financial activity is still run by a small team of four or five traders, everyone interacts with everyone and the Team Manager has no significant structural advantage over anyone else. The manager has a kind of statutory privilege, and it is hard to imagine a manager accepting a subordinate position at the team's new company. At the same time, where a manager's style has displeased a team, the latter may well decide to jump ship without him. Larger activities encompassing several teams and reporting levels are marked by a more differentiated power structure. What can happen here is that a subordinate trader may well decide to jump ship along with a few colleagues, possibly accompanied by some outsiders, the manager of the group's largest desk and possibly another desk as well (if the individual in question relates well to the other desk managers). The only person capable of moving the whole trading floor, however, is the Head of Dealing Room, who becomes the key element in engineering collective moves due to the fact that he is the person who coordinates and subdivides the work.

During our investigations (based on nearly 100 interviews covering this and other topics), we heard many stories of collective moves, including:

In 1990, after Drexel Burnham Lambert went bankrupt, its ex-Head of Futures negotiated with Indosuez the recruitment of a 60-person team (Lepetit, 2002: 115); A market-making team resigned en masse from Neptune Bank because members refused new risk control measures; An equity derivatives team resigned en masse from a London investment bank, starting up a rival firm in Dublin where contractual non-compete clauses did not hold; In 1999, a Head of Equity Derivatives and his deputy threatened to leave with the entire floor if the bank employing them did not accede to their pay demands (Godechot, 2006).

These stories are often swapped nonchalantly and can be old and second-hand. Better to understand the mechanisms by means of which a Head of Dealing Room will mobilize a group, it is also useful to undertake a detailed analysis of some failures.

Limitations on the power to mobilize

It is risky for the bank to organize the replacement of a quitting Head of Dealing Room. Either the Head's successor finds it hard to get along with the teams under his direction and cannot stop people from leaving, or he gets along well with everyone and de facto replicates the ex-Head's structural position including any associated bargaining power. These difficulties about replacing a quitting Head of Dealing Room are especially acute where the successor is apt to show similar secessionist tendencies in the future. But the organization of a succession often provides the bank with an opportunity to gain time and to lock-in company assets.

Some of these issues can be illustrated by considering the story of a failed proposal for internal reorganization in Saturn Bank and the confrontational resignation of Saturn Bank's Head of Options. In 1990 and 1991, facing mass defections by traders head-hunted by English or American banks, this manager's reaction was to try and invent a new institutional form, a partnership that would be 75 percent owned by Saturn Bank and 25 percent by 20 or so partner employees. The purpose of this new system was to a stabilise staffing and develop long-term incentives for those who hoped to become a partner. The project's eventual failure was due, according to the Head of Options, to several factors. The Head of Fixed Income and Head of Equities were impatient rivals who wanted to break up his empire. The young Co-Chief Executive Officer, a newly appointed former government inspector, showed little understanding because he was primarily concerned with maintaining the unity of the bank he hoped to chair one day. Finally, the Head of Options did not have the time to promote his project internally. Trusting in his own power and empire, he tried to bulldoze his way through opposition partly by threatening resignation: ‘To me this was paramount so I threatened to resign if I didn't get what I wanted’. His miscalculation may have been to think that his department's success was attributable to him personally, when his real power lay in his ability to engineer collective moves.

To combat the impending resignation and staunch the haemorrhaging, the bank organized what its HR managers described as ‘a real putsch’. HR allegedly made a surreptitious promise to promote all of the Head of Options' direct subordinates so to prevent them from resigning along with their boss and leaving behind a ‘burnt-out shell’. When the Head of Options finally did threaten to resign in 1992, he had not yet developed a credible project in another bank and could offer his team no other host structure if it followed him. It took him a year to put together an alternative project, finally concretizing his partnership idea in the subsidiary of a German bank and taking around a dozen colleagues from Saturn Bank to this new venture. But most of the financial power in the old Options Department, a total of around 300 or 400 employees, stayed put at Saturn.

The ex-Head of Options' rivals were the Heads of Equities, Fixed Income and Foreign Exchange who split up the Options Department so that each ran the options teams associated with their own cash product. Some of the Head of Options' subordinates were promoted to Desk (and even Dealing Room) Manager role and offered a chance to run a relatively autonomous derivative products section within the confines of departments defined by the underlying asset classes. More specifically, three direct subordinates of the ex-Head of Options were put in charge of the Equity Derivative Products group that would by the late 1990s become Saturn Bank's most profitable financial activity as the three subordinates rose hierarchically and revolutionized the pay scale. The ex-Head of Options would still talk about the trio with affection but others called them ‘traitors’. Certainly, the ex-Head of Options had taken too much time to engineer a collective departure. By the time he made his move it was too late because the bank had already promoted the key figures he was counting on, realizing that they would be less inclined to leave if they felt attached to the old structure. The ex-Head of Options had lost his ability to take Saturn Bank's assets with him to the new structure.

It is not true that the ability to engineer a collective move automatically increases proportionately with the size of the team involved or the volumes traded. Higher volumes imply the mobilization of a bigger area but also diminish the intensity of mobilization. Going further up the hierarchical scale and dealing with larger volumes connects activities that are more distant and heterogeneous with less intense connections. Governance is done at a distance here and less time is spent with each individual. Leaders can easily fall prey to the counter-manoeuvring of direct subordinates who may hope that the boss will go to make room for their own rise. In the late 1990s, the most strategic structural position for engineering collective moves seems to have been the Head of Dealing Room. After 2000, 15 or so years on from their arrival in the finance industry, these Heads of Dealing started wondering how they might secure their ascent by attaining a status that would finally legitimize their astounding economic success. The lack of any clear response to this meant a whole array of career trajectories took shape within an organization where up to 2001 in the astute judgement of an R&D team manager ‘no one questioned the hierarchy established [here] in the 1990s’. After the Head of Options left in 1992, his second-in-command inherited the Equity Derivatives Department, with the original number three becoming Head of Trading and the original number four Head of Sales. Two or three years later, the original second-in-command was promoted to run a financial products subsidiary in Asia, with the original number three replacing him as Head of Equity Derivatives and the original number four becoming his deputy.

The career trajectory of the original third-in-command is particularly interesting. By late 1999, he had been promoted to co-manage, working alongside an American, the whole of the Equity and Investment Department (stock brokerage, equity derivatives, financial analysis and IPOs) and got onto the firm's Executive Committee. The doors to the bank's highest echelons, traditionally closed to market professionals, seemed finally to have opened. Yet this was a risky ascent since it meant that the man being promoted was losing control over the Equity Derivatives group where his former deputy was now responsible. In other words, promotion put a distance between the manager and the entities that had first helped him to gain power. Two years later, the rise of the Equity Derivatives group was consecrated in a new reorganization. It became a distinct and autonomous department at exactly the same level as the equity department that the original third-in-command headed. Hence, this man definitively lost control over the Equity Derivatives group he had originally used as a springboard. He did take over some of the M&A activities that had heretofore escaped his clutches but lost out on control of the more powerful department. His remaining activities, like stock brokerage or M&A, were generally smaller earners at Saturn Bank and were substantial loss makers during the 2001/2002 recession.

Financial traders describing this case talked about how the original third-in-command had been duped, since his former assistant ‘did him in’ a claim which some traders softened with the reminder that ‘it's the least thing to do in this business’. One year later, this former Head of Equity Derivative Dealing Room, had been isolated to the point where he left the bank and indeed the finance business. Unable to control his assets and teams, he had lost much of his power and legitimacy. He had been incapable, during the course of his risky rise, of converting market capital into a different kind of organizational capital.

In the early 2000s, banks were also looking for new contractual limitations on collective moves. But such retention policies have perverse effects and loopholes. The first solution was to try to grant financial operators a deferred bonus or ‘golden handcuffs’ because the bonus in cash or stocks will be paid only if the employee is still working for the bank. Traders and heads may have good salaries but may be reluctant to move because, if they move to another employer, they will lose accumulated bonuses from previous years. In 2002, a trader from Syrius Bank was trying to build a hedge fund with former colleagues from his bank but did not want simply to resign and abandon his deferred compensation: with the help of his father, an important lawyer, he was successfully fighting to have his bank fire him and therefore pay him his two million Euros of deferred bonus, instead of resigning and abandoning part of his past compensations. In another bank, I was told, some traders were trying to get fired in order to claim deferred bonus. The second solution was to tie employees with non-compete clauses. But the enforceability of such clauses is generally difficult in the courts of law of most countries. Their validity is generally limited in terms of time and space; and it is always possible for a team to escape non-compete clauses by moving from Paris to London, or from London to Dublin. If contractual limitations are not very effective at present, they may become more efficient in the future. But banks will also have to cope with traders and Heads' inventiveness as they try to circumvent them.

This section has demonstrated three kinds of constraints restricting Heads' ability to engineer collective moves in financial dealing rooms during the 1990s: circumstantial constraints as when the Head of Options jumped ship; structural as when the original third-in-command was run out a decade later; and contractual limitations through deferred bonus and non-compete clauses. This analysis of constraints also delineates the forces at work here. A Head of Dealing Room has to manage social capital in a way that is both practical and strategic, an art that cannot be reduced to a mere set of principles. Not only must Heads manage their social capital in a way that will enable them to engineer collective moves but also, in their relationships with their own bosses, they must transform it into a symbolic capital. They must get their own managers, top bank executives in the traditional sense of the term, to believe that they are basically the delegates of a closely-knit team of traders who are all ready to set sail if their conditions aren't met; and that belief in cohesion is often more important than the real cohesion of the team in question. The Head of Dealing Room appropriates the power of the group when speaking with the senior executive in the name of the trading group. At the same time and to maintain primacy, the Head of Dealing Room must add to the number of divisions, distribute privileges, get people to show patience, reward them and avoid being replaced by some alternative coordinator.

Social capital, the frontiers of the firm and the dynamic of capitalism

We have drawn a highly political portrait of financial activities, which will help us to understand both the concentration of corporate assets in an individual at one point and the advent of internal entrepreneurs, formally categorized as employees but similar to Marglin's (1974) entrepreneur-capitalist. The character of these actors is both capitalist and anti-capitalist. Like traditional entrepreneurs, they accumulate a capital that they will be basically lending to another company or investing in a new business like a hedge fund. But, of course, such capital-intensive accumulation is detrimental to the company employing them and its formal owners (Folkman et al., 2006). It transgresses the traditional boundaries of the firm and the idea of capital as shareholders' exclusive property (Rajan and Zingales, 2001). Through their social capital, internal entrepreneurs get control over a substantial part of the firms' productive assets. Since they can move such assets to another firm, they become their practical owner. Hence, the concept of the boundaries of the firm, already shaken by human capital's greater impact (Zingales, 2000), is going to be further undermined by the rising power of social capital which lies even further outside of shareholders' control.

If this expropriation mechanism locally undermines the boundaries of the firm and shareholders' power, is it a threat for capitalism? Not exactly because internal entrepreneurs, with sufficient power and self-confidence, can turn into classical entrepreneurs and true capitalists. With the assets accumulated through working for employers in finance, they can launch a hedge fund. On the ruins of their previous employers' firm, they give birth to new capitalist structures. For instance, John Meriwether had been Head Bond Trader at Salomon Brothers before he founded the giant hedge fund Long Term Capital Management, whose 1998 bankruptcy was a front page item. Meriwether launched this fund in 1994 with a team of ex-Salomon colleagues (MacKenzie, 2003). More recently, John D. Arnold was cited by the newspapers as the most highly paid trader who was said to have earned two billion dollars in 2006. But he is no longer an ordinary ‘trader’ but now a full entrepreneur. 2 Originally, Arnold was one of Enron's biggest traders. After the company's bankruptcy, he founded Centarius hedge fund using his 2001 bonus of eight million dollars bonus and hiring former colleagues who accounted for half of his 17 traders in 2006. While many shareholders and workers lost money in Enron's collapse, part of its elite was able to reinvest Enron's intangible assets (team workforce, clients, knowledge of trading techniques) in new firms for their own interests. Hedge funds are therefore not just a new class of financial actor or asset class but also a kind of appendix to the traditional banking industry. They are the locus where elite financial workers, raised by traditional banks, gain their autonomy and become new capitalist players.

In a sense, we can see this dynamic as a creative destruction process (Schumpeter, 1943). As Marx says in the Communist Manifesto, ‘the bourgeoisie cannot exist without constantly revolutionizing the instruments of production, and thereby the relations of production, and with them the whole relations of society’ (Marx, 2000) Sudden access to wealth is difficult to explain without requiring some form of unequal exchange, some loopholes in the exchange of equivalents against equivalents. The transgression of the boundaries of the firm thanks to social capital provides the basis for one of these unequal exchanges.

Footnotes

1

Salaries are given in constant euros 2005.

2

See for instance Barrionuevo, A., ‘Energy Trading, Post-Enron‘, The New York Times, January 15, 2006.