Abstract

This case focuses on the decisions confronting Sally Bennett, the new Director of Market Risk Management (MRM), a unique department created within the Marketing Division of a large, diversified energy conglomerate. MRM played a crucial role in supporting the trading and marketing operations in a complex, competitive environment. Bennett was facing important challenges as the demand for MRM's service exploded. She wondered if a more formalized approach to risk assessment might be better and if so, who should design the new system. The proper organizational arrangement for MRM was also unclear. Overlaid upon these issues were larger questions of when and how the department should transition from an entrepreneurially oriented to professionally managed department.

Bennett realized that there were a number of issues that needed prompt attention. She expected that some of these would come up at the meeting she was scheduled to attend that afternoon with David Coal, Vice President (VP) of Information Systems and Asa Birch, President of the Marketing Division. A major issue that was sure to be controversial was a proposal by the information systems group to design a better risk management system. There were several questions that needed to be addressed here. First, would a more formalized approach to risk assessment really suit the needs of the corporation, given the recent and predicted future volatility of its markets and the ever–changing requirements of its users? Second, assuming the answer to that question was yes, who should be responsible for designing a new system? MRM had proved that with its bootstrap approach to design, it could meet deadlines; but was it time for it to step aside and let the more established IS group take the concept to the next level? Third, where should MRM be housed in the corporate hierarchy? Throughout its existence, the department had operated as a quasi–independent entity reporting directly to the President of the Marketing Division and the Exposure Committee. Was it time to fold the department into the information systems group?

Although Bennett had a feeling that the decisions on these matters would be determined as much by politics as by economic considerations, she was not overly territorial. She felt her position and new promotion were secure whatever was decided. If anything, the possibility of merging MRM with information systems might improve her career opportunities. MRM was an important and visible operation and since Coal was likely to be promoted someday, she might be in line to take his place as Vice President of information systems for the Marketing Division. Furthermore, she hoped that the protection coming from being part of a larger entity might give her more job security. However, she knew that her future career progress mostly rested on making good decisions and on ensuring that MRM continued to provide timely and accurate decision–making support for the corporation.

Industry Background

The U.S. energy industry was composed of the following segments: coal, electricity, natural gas, nuclear, and petroleum. In total, the industry supplied 73 quadrillion British thermal units (BTU) of energy in 1998, of which four quadrillion (mostly in the form of coal) were exported to other countries. At the same time, U.S. energy consumption was 95 quadrillion BTUs, necessitating imports of additional 26 quadrillion BTUs. In total, Americans consumed over $500 billion of energy in 1998.

The market for energy consisted of three major usage categories: residential, commercial, and transportation. Each market segment had grown over time; more importantly, the proportion of the consumption of the various sources of energy had changed. For example, early in the twentieth century, residential heating was a major market for coal producers. However, with the construction of gas pipelines and electric power grids, residential coal use declined dramatically. Likewise, natural gas replaced coal as the dominant energy source for industrial users in 1958. On the other hand, the transportation industry had been almost totally reliant upon petroleum since 1949. In 1998, the United States had record net imports of 9.5 million barrels of petroleum per day.

In 1998, residential consumption of electricity and natural gas was approximately 8.5 quadrillion BTUs each, while petroleum was less than 3 quadrillion BTUs and coal usage was negligible. In contrast, the commercial sector used more petroleum and natural gas energy (approximately 9 quadrillion BTUs each) than electricity (approximately 3 quadrillion). Two thirds of the energy consumed by the commercial sector was used for manufacturing.

In terms of total U.S. energy usage, petroleum supplied 42% of national energy needs, followed by coal (25%) and natural gas (20%). The remaining 12% was generated by nuclear, hydroelectric, solar, and other technologies. Insofar as the energy sources used to create electricity in 1998, 52% of all domestic electricity was generated by coal–fired power plants, followed by nuclear (19%), and gas and petroleum (18%). Hydroelectric and other sources of power generated 11% of production.

The energy industry itself has gone through tremendous changes in the last quarter of the twentieth century. The first energy commodity market was oil, which was deregulated in the 1970s. The emergence of the Organization of the Petroleum Exporting Countries cartel as a major international force resulted in extreme volatility in oil prices. The need to control exposure to such risk led to the sale of oil futures and derivatives. The New York Mercantile Exchange began selling heating oil contracts in 1978. Other energy future markets followed: gasoline futures, crude oil, natural gas, and electricity in 1981, 1983, 1990, and 1996, respectively. This formerly regulated industry began the painful process of adapting to a deregulated environment. The shift toward an open market created many fundamental changes in the way the industry operated. Furthermore, the use of technology and financial instruments had changed the dynamics of marketing all forms of energy commodities.

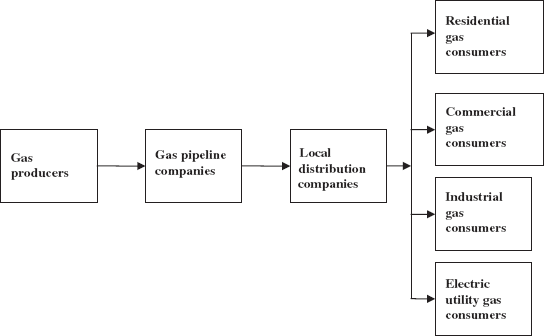

Before deregulation, the critical success factors in the industry were to secure adequate energy supplies for customers, make sure that the production of these supplies increased at a rate consistent with demand, and to ensure that adequate supplies reached the customer. None of these success factors depended upon basic marketing functions such as price management, customer service, or advertising. This was directly attributable to the regulation of various segments of an industry dominated by local monopolies. Production capacity and internal efficiency ruled the day. As an example, Figure 1 depicts the traditional pattern of marketing and distribution for natural gas before deregulation.

Traditional Gas Marketing

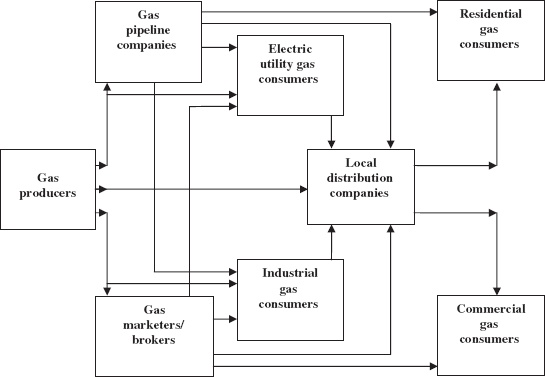

After deregulation, new opportunities and risks emerged. Deregulation eliminated natural monopolies, allowing companies to compete in new markets. Direct negotiations between industrial buyers and sellers, and direct sales to core market customers was now possible. Prices also became more volatile. This created new risks for both buyers and sellers, as well as the possibility of profits through arbitrage, energy brokering, and the buying and selling of purchase options in energy and financial markets. 2 The result was that functional boundaries between energy marketing and energy production became fuzzy, and specialized marketing companies emerged. A key to success for the marketer was now to identify and exploit energy commodity arbitrage opportunities. These arbitrage opportunities could be found in financial markets, location advantages, transmission capabilities, and service delivery to customers.

Arbitrage is the exploitation of temporary differences in price in different markets. Energy brokering is when a company acts as an intermediary between buyers and sellers of energy, charging one or both commissions for the service.

In the natural gas market, transmission companies still delivered producers’ gas to local distribution companies, which in turn continued to distribute it to consumers. However, the contractual path of gas sales had changed dramatically, as shown in Figure 2.

Gas Marketing after Deregulation

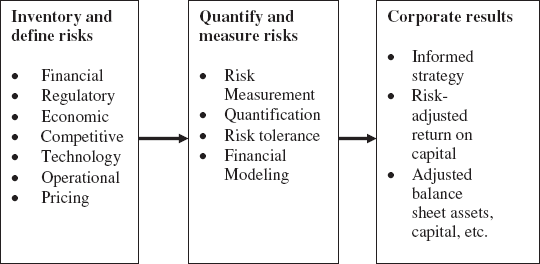

By 1998, the domestic energy market had become much more complex and dynamic. Energy needs could shift unpredictably, and some consumers even became suppliers of energy to other consumers. Because of this complexity, energy companies faced significant risk exposures as they produced, bought, and sold energy. As shown in Figure 3, a large number of risk sources had to be identified, quantified, and controlled for in strategic and operational decisions. Competitive pressures, regional and global economic shifts, changes in the cost of capital, changes in governmental policy, and other factors could potentially have a major and sometimes unpredictable effect on demand, supply, prices, and costs. Thus, the management of these risks became increasingly important for energy companies.

Managing Risk in Diversified Energy Markets

Company Background

The Marketing Division was a subsidiary of NAPECOR, a major national energy company with assets of $14.5 billion and over $12 billion in revenue in 1997. With a history spanning over 40 years, NAPECOR was a leading producer, transporter and marketer of electricity and natural gas to major markets in the United States. NAPECOR business operations were conducted within five major units:

Marketing Division—included the marketing and trading of hydrocarbon energy products and electric power.

Transmission Division—comprised natural gas and oil pipeline operations.

Processing Division—encompassed the gathering, extracting and processing of hydrocarbons into other energy forms or products, including specialty chemicals.

Generation Division—involved in generation of electrical power through the use of gas turbine and wind–powered cogeneration plants.

International Division—involved in energy–related opportunities in three principal regions of the world: Latin America, Europe, and the Middle East.

The Marketing Division was the marketing arm of NAPECOR. It had been created by a merger between NAPECOR's Texacan Marketing (the original marketing division) and Piper Energy near the end of 1994. At that time, Piper was a relatively young, entrepreneurial company trading the entire range of energy commodities. The entrepreneurial culture that Piper brought to NAPECOR was a large reason for the merger. The energy marketing industry was changing, and new skills, abilities, and attitudes were required to survive and prosper within this new environment.

After the merger, NAPECOR was suddenly faced with an array of business issues as it continued the strategic expansion from its traditional production and distribution businesses into the complementary, but dynamic and highly competitive energy trading and marketing field. Gas and petroleum production volumes had increased substantially since the early 1990s and electrical energy production was growing in excess of historic rates. Sales had more than doubled since the merger with Piper, while net income had increased from about $25 million to $75 million over the same period.

The Marketing Division's trading and marketing activities involve the buying and selling of natural gas, crude oil, refined petroleum products, natural gas liquids, electric power, and related financial derivative products primarily under short–term contracts with suppliers, customers, marketers, and financial institutions in North America. On a daily basis, the trading room hummed with the sounds of telephones, fax machines, and conversations. Several dozen traders monitored energy prices on computer terminals. Other traders were constantly on the telephone, selling gasoline to car manufacturers in Detroit, buying electricity from producers on the eastern seaboard, checking wholesale gasoline prices in Texas, or negotiating energy contracts. It was a very lively, dynamic, challenging, and competitive environment.

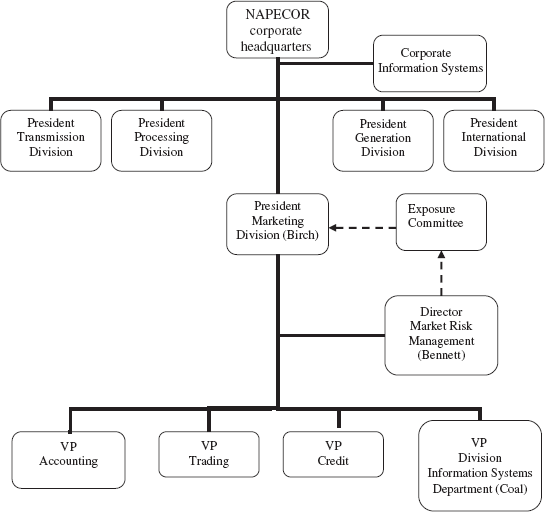

The MRM department was a new venture initiated in the Marketing Division to measure and manage the risk associated with energy marketing and trading. Figure 4 depicts the organizational structure of NAPECOR and the Marketing Division as well as MRM's relationship to other parts of the division.

NAPECOR's Organization Structure

Creation of the MRM Department

While deregulation provided an opportunity for the marketing function to become independent, a number of key trading events occurred in the national financial marketplace. In the cases of Orange County and Barings Bank, senior management failed to fully understand trading risks and suffered tremendous losses. Such well–publicized trading disasters signaled the need for adequate internal controls and for senior management to fully understand trading risks. These factors added fuel to the fire regarding the need for risk management at NAPECOR.

Risk associated with marketing energy generally went up as both the volumes and dollars traded grew, due to the increase in the number of production activities and market transactions associated with generating those larger dollar amounts. In late 1995, NAPECOR's senior management decided to create an independent MRM department to attempt to quantify and report market risk. 3 Management hoped MRM would play a key role in corporate operations, acting as a link between trading and senior management.

Market risk is defined as the loss due to a change in market conditions, including interest rates, foreign currency exchange rates, and energy commodity prices. It results from the types and grades of products marketed, the locations in which they are marketed, and from the different time horizons of closing transactions. There are hundreds of risk impacts to be analyzed each time commodity prices and exchange rates fluctuate in the marketplace.

Management wanted to segregate reporting and trading positions as well as to get an independent view of exposures and mark–to–markets. 4 To accomplish this, a market–risk policy was needed to achieve the careful balance between flexibility and control, with a view toward profitability. An important aspect of this policy was the management and monitoring of the business by the MRM department and by the Exposure Committee. The Exposure Committee, composed of top management who were thoroughly familiar with the business and its risks, met weekly to review positions, strategies, limits, compliance, exceptions, and related market–risk assessments.

Mark–to–market is the comparison of the present market value of a commodity position with its recorded value in corporate financial records. Since market value will vary from book value, this becomes a measure of profit or loss in trading operations.

However, traders had mixed feelings about creating a new department to manage risks. On one hand, they felt the proposed department would be useful in helping to better understand some deals and would help in doing some of the tasks, like data entry. But, on the other hand, the proposal would also be an expense and some traders felt that they were in full control of their positions without any assistance.

Stage 1: Creating the MRM Venture

In 1995, NAPECOR created the position of Director, MRM, with the mandate to immediately develop and implement an MRM system. The position was filled by Chuck Manners, a Certified Public Accountant who had been with a public accounting firm in Chicago before joining NAPECOR as an auditor. Manners understood the challenges the company was facing in moving from a regulated to a free–market environment. He decided to test his skills in mapping out a direction in the new and growing area of energy marketing and risk management.

Manners developed plans, hired a few key people, completed his research, and committed to meet very ambitious deadlines and targets. In October 1995, he promised the NAPECOR Board that by April 1996, MRM would be able to completely and accurately determine open positions, to calculate mark–to–market profits arising from all trading and marketing activities, and to consolidate and report the information to senior management on a timely basis. This was a very bold commitment that Manners knew would either make or break his career with the company.

People

Manners was the champion with the vision to create the new department. He understood, however, that to meet the startup objective, there was a need for a wide range of skill sets. In addition to first class computer programming skills, MRM had to be on par with the traders and marketers in the front line with regard to energy markets and trading. In addition, team synergy was required to ensure that the venture would meet the time deadline and still keep abreast of the continually changing and developing energy markets. Starting with a small cadre of professionals, and supported by highly trained technical staff, the team Manners put together began to develop the process and systems necessary for success. The team was dedicated and driven to meet that April deadline. Manners remarked, “We worked fourteen or sixteen hours a day, seven days a week. It was nuts. The hours were crazy and brutal. But it was fun.”

If Manners was the business champion, then Andy Rawlings was the technical champion. He was one of the few information systems people who could handle Manners and they soon developed a close friendship. Rawlings became the project leader for developing and writing all the trading books. 5 Other key team members included Ronald Josephson, who had been part of Piper Energy before the merger. While his skills were on the business side, Josephson was adept at information systems. He had experience in writing trading books. Julie Harrison, also from Piper Energy, had a background in accounting and had an excellent relationship with the traders. She came on board to build and manage the support team.

A trading book is a term used to represent taking a position in the marketplace. It involves capturing the deals, exposure, and mark–to–market profit, and then managing this position.

Information Systems

It was critical for MRM to obtain a thorough understanding of NAPECOR's market price risks and to communicate this information to senior management. This was not an easy task, given the diverse energy portfolio of physical and financial products traded and marketed in several interrelated unit measurements such as barrels, cubic feet, cubic meters, BTUs, gigajoules, gallons, liters, and megawatt hours. There was a need for a common measure to quantify, correlate, and integrate market price risk into the measurement of performance.

It was clear that information and information systems were the keys to effectively monitor and to proactively manage market risks. Early in their research, the MRM team learned that having effective and efficient information systems was not about investing a large amount of money. Many of NAPECOR's competitors had spent tens of millions of dollars developing elaborate trading systems, often with very little success.

MRM's approach concentrated on making the system effective before it was made efficient. The initial focus was to ensure that the information systems was capable of properly accommodating all physical and financial transactions and of accurately calculating open positions and mark to market profits, no more, no less. During the initial 6 months, the MRM team worked to achieve a common formula for exposure in its crude, natural gas, natural gas liquids, and electric books. Rawlings had the key insight that led to the creation of a unified model that allowed all books to be analyzed simultaneously. With this breakthrough, the MRM team was able to meet the April 1996 deadline.

With the focus on effectiveness, some things were sacrificed. Manners noted, “That was a sufficiently challenging focus without trying to make the systems state–of–the–art at the same time.” There were two aspects to the problem of a risk management system. First, there was the development and implementation of business rules to identify opportunities and to measure risk. Second, there was the need to create an aggregation or bookkeeping function as a form of record keeping and storage. The initial system used a dual rather than single entry system; that is, data had to be entered separately into both the rules and the bookkeeping section. While this put additional demands on human input, it allowed the venture to proceed quickly. Josephson commented that it was “a method of necessity; we had to get something up and running. When you have six months, you just hurry.”

The aggregation was performed by a huge Excel spreadsheet. The business rules section was developed through numerous prototypes using various software products. No detailed systems plan outlined all of the specifications, objectives, needs, and wish lists. Instead, they started with a generic system and modified it for unique groups. Rawlings, who played a big role in building the system, said “When we discovered that an original idea didn't work, we were able to quickly and inexpensively modify it to keep the venture on track.” This approach allowed flexibility, which was a key factor in selling MRM to the rest of NAPECOR. As Rawlings said, “For certain groups we made very few changes to the original prototype systems, in others, where it was necessary, we made improvements or rewrote the systems using more powerful software. As a result, no one trading group had to compromise to accommodate the needs of another group.”

Politics

While the system was being developed and pushed, another game was also being played out. David Coal was the Vice President of information systems. His strengths were his vision and attention to detail in implementation. Coal was credited with moving NAPECOR to client–server technology in 1986 ahead of the market. This key strategic shift earned Coal his current position. Recognizing the importance of people in the implementation of his strategies, he personally hired his staff, and often referred to them as “family.” Clarissa Sullivan, an entry–level analyst who worked for Coal, commented on his attention to the hiring process: “His interviews went for forty–five minutes and he asked tough questions. Not many VPs would spend the time to hire at my level.”

Coal also recognized the opportunity that MRM provided, but he wanted to design and implement a sophisticated trading and risk management system that would be compatible with the rest of the information systems in the division and in the corporation. He also believed that the system should be standardized. While a standardized system would be less flexible, thereby not as conducive to meeting the individualized needs of every user group, it would allow for easier expansion and higher efficiency. The trouble was that such a system would take longer than 6 months to implement. The result of this “game” was that Manners gained control of the project. However, many individuals within the company, particularly senior managers in the IS group, still did not feel that MRM would succeed. As Josephson noted, “It wasn't easy, but we opened up the eyes of corporate.”

Success

In spite of some skepticism, the project progressed quickly and the MRM team expanded to meet the increased workload. New people were brought on as needed. Quentin Martinsburg, son of Corporate Vice President Sam Martinsburg, went to work on the gas books, and Steve Howell, whose father was on the Board of Directors, went to help with the power books. By mid–March 1996, 2 weeks ahead of schedule, MRM was ready for business. Chuck Manners commented on this success. “It took us less than six months to achieve our initial objectives and we did so very economically. Our focus now is to streamline these systems to process information more efficiently and reduce the manual effort. We recognize that our market risk management system will continually evolve and our work in this important area will never be complete.”

Stage 2: Focus on Operating Systems

The success of meeting the first deadline did not result in a slowdown for MRM. Its role evolved to include independently, verifying open positions, monitoring these against authorized limits, explaining the profit or loss, quantifying the returns, supplying an index of risk, and providing general education to senior management and to NAPECOR's Audit Committee. The department had managed to capture the information, but serving a more diverse group of internal clients was putting a strain on the manual system used to report this information. A shift to make the system better proved fundamental.

A tremendous amount of work had been performed to improve the efficiency of MRM. Systems had been rewritten, databases had been expanded and improved, and reports had been generated. Throughout, the focus had been to implement a solution on a very tight and demanding deadline. The day–to–day activities were sped up and at times took on a frenzied quality. Howell remembered preparing for an Exposure Committee meeting: “We were in early Wednesday morning, before seven o'clock, and were still working on the systems after a late dinner at nine o'clock that evening. By Thursday morning, more changes had to be made and we had not even reviewed the reports before two o'clock in the afternoon. Finally, we raced, literally ran to the photocopier at five minutes to three o'clock so we could make the three o'clock meeting. Needless to say, we went home as soon as the meeting was over.” When asked, Howell indicated that such episodes were not uncommon during these months. By 1997, risk management was recognized as essential and fundamental to having a successful marketing and trading operation, and NAPECOR's was seen to be one of the best in their industry.

People

To keep pace with the rapid growth, MRM grew from a department of five people to over 30 people. These individuals were brought in to deal with the tremendous amount of work that had to be done. Some areas were simply overwhelmed by their tasks. Training was very informal. Turnover was higher than normal; people who did stay tended to specialize in their roles and found it hard to learn other aspects of MRM, let alone the company.

The initial make up of the MRM department began to shift as well. Rawlings left the company to start a private risk management consulting firm for energy companies too small to afford a dedicated department. Josephson moved to trading. Perhaps the most important change was the appointment of Chuck Manners to Vice President, Risk Management, at corporate headquarters to head up the development of a corporate–wide risk management system. Josephson, among the last of the original team members to move, summed up his feelings about MRM's future: “Now it just needs streamlining. There's not much need to break ground as quickly as before. It's time for me to move on.”

Information Systems

Management in the Marketing Division realized that it was very difficult to have a single corporate risk book due to the uniqueness of each business line. Natural gas was difficult to transport except by a pipeline, so location was critical. For crude oil, though, the grade or quality was more important than location. However, it soon became apparent that applying a weighting scheme for the components of risk might make an integrated system possible. This was the beginning of a consolidated view. If MRM could get all the deals and exposures in one database, and implement a risk calculator from this information, the process could be improved significantly.

The IS Department also had numerous operational issues to resolve. Capturing data on exposures for MRM had to be done separately for each of the 20 different trading activities, thereby creating a huge data–processing requirement. Brian Norton, the Marketing Division's Manager of information systems, complained “We knew when MRM developed those books that sooner or later the information systems department would have to pay.” He and his people were certainly feeling frustrated over the workload and pressures to get results.

Politics

The shift in focus toward a consolidated view marked a significant turning point. Moving toward a consolidated approach meant that information systems would have to play a more critical role in the future of MRM. The significance of this relationship came from the fact that information systems had a more diverse set of internal customers who increasingly required information on a realtime basis. Accounting, credit, and even trading were seeing the potential value of this information; it was not always possible or desirable for MRM to filter all of the information those customers needed through the Exposures Committee. Furthermore, information systems was responsible for many other systems in the Division. Consequently, the need for efficiency was much greater, precluding a “flexible design” approach such as that of MRM.

But personnel in information systems and MRM were still having trouble seeing the situation from a common perspective. Reflecting on this development Josephson stated, “Working with information systems will certainly be different and I'm not sure MRM will be able to be as entrepreneurial in seizing new opportunities as we were in the past. On the plus side, more people will be getting information on risks than ever before. But if they don't get all the information and if MRM loses its ability to adapt, I'm not sure it's worth it.”

Current Issues

Sally Bennett was well aware of the history of MRM, both its successes and the controversies that surrounded its development. It just seemed that she was doing a lot of reacting and she was not used to working that way. She needed to list the various issues that demanded her attention:

Various trading groups were seeking to increase their limits. They first consulted with MRM to determine if the proposal made sense and if the company could accept the risk. If it looked okay, then the trading group and MRM made a joint presentation to the Exposure Committee.

The Credit Department was seeking to create a system, with MRM's help, to implement a new measurement called Credit Value at Risk.

The International Division planned to begin trading within a few months and MRM was still helping them work out the details of how to effectively perform the control, reporting, and consolidating functions.

Senior management was demanding more frequent reporting of exposures, mark–to–markets, and value at risk. This required a move from weekly to daily reporting.

The information systems group had just asked for an 18–month window to design a new object–oriented data capture system for both trading and risk management. During this development period, only routine support and maintenance would be performed on the existing system. No modifications or enhancements would be made; all available programming resources would be diverted to developing the new system.

Chuck Manners was beginning a corporate–wide initiative that would require significant input from MRM to get up and running.

The issues were critical to the business, and all of them were placing great demands on MRM's personnel. Perhaps the most pressing issue was the information systems proposal. The decision would have ramifications for NAPECOR's entire marketing operation, not to mention the future of risk management practices in other parts of the corporation.

Conclusion

As she finished her coffee, Bennett mulled the possibilities. She could not help but wonder why she was appointed to her current position. What role did Birch want her to play within MRM? Was it time to institutionalize MRM? And if so, how? If a transition was required, what steps should be taken and how should the information systems group fit in? She was troubled by how much politics and power seemed to be influencing the direction the company was heading. However, since what was best for the company was not exactly clear, should she just go with the flow?