Abstract

Agency theory has focused on buyouts as a governance and control device to increase profitability, organizational efficiency, and limited attention to growth. A strategic entrepreneurship view of buyouts incorporates upside incentives for value creation associated with growth as well as efficiency gains. In this paper, we develop the complementarity between agency theory and strategic entrepreneurship perspectives to examine the performance implications for different types of buyouts. Further, we study how the involvement of private equity (PE) firms is related to the performance of the post–buyout firm. These issues are examined for a sample of 238 PE–backed buyouts in the UK between 1993 and 2003. Implications for theory and practice are suggested.

Introduction

Private equity (PE)–backed buyouts have been perceived historically as an efficiency tool to streamline organizational processes, reduce workforces and decrease unit costs (Harris, Siegel, & Wright, 2005; Wright, Hoskisson, & Busenitz, 2000). PE–backed buyouts involve investments in which investors and a management team pool their own money (usually together with debt finance) to buy shares in that company from its current owners to create a new independent entity. Agency theory has been the predominant theoretical lens used to study buyouts, with emphasis on controlling and incentivizing managers’ behavior to improve performance (Fox & Marcus, 1992; Jensen, 1993). This contrasts sharply with mature, public firms where weak corporate governance and managerial incentives can lead to the destruction of firm value.

Besides being efficiency enhancing, buyouts may also be a vehicle for strategic innovation and renewal that fosters upside entrepreneurial growth opportunities (Wright, Hoskisson, Busenitz, & Dial, 2001). While an agency perspective allows for consideration of growth, the agency controls involved in PE transactions, such as high leverage and financial monitoring, may stifle strategic flexibility and risk taking associated with growth (Jensen & Meckling, 1976).

A strategic entrepreneurship perspective, grounded in the resource–based view of the firm, provides recognition of the resources required to exploit growth opportunities in order to create and sustain competitive advantage (Ireland, Hitt, & Sirmon, 2003). The complementarity between agency and resource–based perspectives of the firm are well–recognized (Castanias & Helfat, 1991; Mahoney & Pandian, 1992; Makadok, 2003); in particular, strong governance and strong resources in the form of human capital competences may be especially important in generating performance (Makadok). Exploring the complementarity between agency and strategic entrepreneurship perspectives with respect to buyouts provides richer insights than would be gained from using only one perspective. These perspectives have not hitherto been combined in the context of PE–backed buyouts.

Previous studies have typically used an agency perspective because they largely focused on “going private” buyouts of entire firms that were publicly traded (Jensen, 1989). Buyouts of publicly traded companies, however, account for only a minority of buyouts in the United States and are relatively rare in other countries (Wright et al., 2007). Indeed, other types of buyouts, including divisional buyouts, family buyouts, and secondary buyouts have largely been neglected in previous research. This heterogeneity of buyout types offers considerable opportunity for change and entrepreneurial pursuits that extend traditional agency theory explanations for buyouts. These different types of buyouts have emerged because they are an efficient and effective means of needed organizational change (Wright, Hoskisson, et al., 2000).

Synthesizing agency and strategic entrepreneurship perspectives, the first research question we examine is: How do different types of PE–backed buyout transactions impact post–buyout performance? More specifically, we study the performance implications of divisional buyouts versus buyouts from other private sources. Previous empirical literature has not focused specifically on divisional buyouts, yet we argue they are of particular interest in the context of synthesizing agency and strategic entrepreneurship perspectives. First, numerically, they represent substantially larger shares of the buyout part of the PE market than public–to–private transactions (Centre for Management Buy–Out Research [CMBOR], 2007). Second, divisional buyouts often involve firms where agency problems were previously significant and where entrepreneurial opportunities have been stifled by parental control structures that require conformity and hard objective data as a basis for decision making (Wright, Hoskisson, & Busenitz, 2001; Wright, Hoskisson, Busenitz, & Dial, 2001).

Entrepreneurial firms in general and divisional buyouts in particular may not possess all the required resources and capabilities to exploit growth opportunities, but may seek to acquire them from external partners. These resources and capabilities may be provided by PE firms. Traditional agency perspectives suggest that the principal role for PE firms in buyouts is monitoring. It is long recognized in the venture capital and PE literature, however, that the human capital of financial investors also brings an advisory resource to investees (Dimov & Shepherd, 2005; Gorman & Sahlman, 1989; Wright, 2007). The commonality of these roles across PE firms suggests that monitoring and advisory roles per se may not be a source of competitive advantage (Barney, 2002). However, some PE firms may be better at developing specialist skills that potentially make an important contribution to strategic entrepreneurship in buyouts. The second research question we address in this study, therefore, is how do differences in PE firm experience and intensity of post–buyout involvement impact the performance of firms undergoing a buyout?

Finally, the extent to which PE firms can add value will depend on the type of deals they pursue. The impact of PE firm experience and intensity of post–buyout involvement on firm performance, therefore, will be contingent on the type of buyout transaction. For example, divisional buyouts offer more opportunities for change and entrepreneurial pursuits (Wright, Hoskisson, & Busenitz, 2001). The third research question we address is: Does PE firm experience and intensity of post–buyout involvement impact differently on the performance of divisional buyouts than for other buyout types?

The empirical contexts generally used to analyze buyouts have focused on “going private” buyouts. Since, as already noted, public–to–private transactions actually account for only a minority of buyouts in the United States and the UK and are relatively rare in continental Europe (Harris et al., 2005), the empirical context used in this study considers private buyout transactions. A unique hand–collected data set is used that covers 238 PE–backed buyout transactions in the UK over the period 1993 to 2003.

The value added by the paper includes the following. First, we contribute to extending work on strategic entrepreneurship by considering a context where it has previously not been applied. PE–backed buyouts represent a context for strategic entrepreneurship that is distinct from existing corporations. Specifically, PE–backed buyouts introduce important issues of governance and incentives hitherto neglected in the strategic entrepreneurship concept. Some firms, such as PE firms, may be better than others at developing and utilizing corporate governance mechanisms, and hence can create a resource that generates competitive advantage (Barney, Wright, & Ketchen, 2001). Buyouts also introduce incentives for management that were previously absent. This is important, as a strategic competitive advantage may not be created where the corporate governance system does not incentivize and monitor management to undertake the appropriate actions to recognize opportunities and to gather and utilize resources. Second, we add to the literature that has highlighted the complementarity between agency theory and the resource–based view by considering a particularly important context where changes in ownership reduce agency problems and involve the introduction of new resources, as well as the release and redirection of existing human capital resources (Castanias & Helfat, 1991; Makadok, 2003). Third, we contribute to the debate on the sources of gains in PE–backed buyouts by demonstrating, theoretically and empirically, that performance improvements may derive from value–creating activities related to both growth and efficiency improvements and not just value capture. Finally, we add to a growing body of studies that recognize the heterogeneity of PE firms by focusing specifically on the different resource contributions they can provide.

The rest of this paper is organized as follows. First, we outline the nature of the PE and buyout process, identifying different buyout types. Second, we develop our complementary theoretical perspectives of agency and strategic entrepreneurship and then derive hypotheses. Third, we outline the research setting of our study, the data, and the method used in the analyses. Fourth, we present the results from the empirical analyses. Finally, we discuss our findings, conclude, and outline potential avenues for future research.

PE and Buyouts

Leveraged buyouts (LBOs) emerged as new organizational forms in the United States during the 1980s (Kaufman & Englender, 1993). The phenomenon traversed the Atlantic, with the first UK LBO of a listed corporation occurring in 1985 (Wright, Robbie, Chiplin, & Albrighton, 2000). Today, buyouts are widespread in Continental European countries and Asia (Cumming, Siegel, & Wright, 2007; Wright, 2007).

Buyouts are the principal focus of PE investments, in which investors and a management team pool their own money (usually together with debt finance) to buy shares in that company from its current owners, to create a new independent entity. In contrast with early stage venture capital investments, which may also involve the purchase of a controlling interest, buyouts are equity purchases of companies that are already self–sustaining but have room for growth and management improvement. PE firms become active investors through taking board seats and specifying contractual restrictions on the behavior of management that include detailed reporting requirements. Lenders also typically specify and closely monitor detailed loan covenants (Citron, Robbie, & Wright, 1997).

The form of the buyout may vary. A management buyout (MBO) usually involves a PE acquisition, in which the existing management takes a substantial proportion of the equity, which may be a majority stake in smaller transactions. A management buy–in (MBI) (Wright & Robbie, 1998) is simply an MBO in which the leading members of the management team are outsiders. Although superficially similar to MBOs, MBIs carry greater risks, as incoming management do not have the benefits of the insiders’ knowledge of the operation of the business. PE firms have sought to address this problem by putting together hybrid buy–in/management buyouts (so–called BIMBOs) to obtain the benefits of the entrepreneurial expertise of the outside managers and the intimate internal knowledge of the incumbent management. Investor–led buyouts (IBOs) involve the acquisition of a firm in a transaction led by a PE firm rather than by insider or outsider management teams. The PE firm will typically either retain existing management to run the company or bring in new management to do so, or employ some combination of internal and external management. Incumbent management may or may not receive a direct equity stake or may receive stock options. IBOs have close similarities with traditional LBOs. The differences can be summarized in terms of the metamorphosis of LBO associations into PE firms as the industry has developed.

Pre–buyout agency issues have consequences for the vendor source. As noted in the introduction, LBOs have traditionally been associated with the taking private of listed corporations with diffuse ownership and agency cost problems. But buyouts may emanate from other vendor sources, notably divisions of larger corporations and other private vendors such as family owners and PE owners.

Divisional buyouts are one of the most common forms of PE–backed buyouts, accounting for 41% of these deals from all vendor sources, including publicly listed deals, in our hand–collected dataset between 1993 and 2003 in the UK, the period covered by this study. A divisional buyout is defined as the sale of a division, subsidiary, or other operating unit of a parent firm to members of the management of either the parent or the subunit being divested (Hite & Vetsuypens, 1989). Divisional buyouts generally involve significant agency cost problems prior to buyout. Agency problems may be present in divisions of large, complex corporations where the multidivisional structure lacks the appropriate control and incentive mechanisms (Fama & Jensen, 1983; Hill, 1985; Thompson & Wright, 1987). Management buyouts of divisions alter the ownership structure of corporate assets in a way that can lead to a more efficient and profitable allocation of resources. Increasing the amount of equity held by the unit's managers, buyouts alter management incentives. By having claims more closely tied to the performance of the unit under their control, managers can be expected to improve their performance (Hite & Vetsuypens). This is because shirking becomes more costly to the individual with a share in the net cash flow (Alchian & Demsetz, 1972). Furthermore, the incentives for mutual monitoring by members of the management team improve as they become residual claimants.

In contrast to divisional buyouts, buyouts of family firms and secondary buyouts involve low or no agency costs. These deals account for 45% of all buyouts in the period covered by our study. 1 Buyouts of private or closely held family firms involve a private owner who, while seeking to obtain a good price, may also want his or her company to remain independent but has not identified a family management successor (European Venture Capital Association [EVCA], 2005; Howorth, Westhead, & Wright, 2004). Over the past two decades, this form of buyout has become a widely accepted form of transferring ownership in privately held firms facing succession problems (CMBOR, 2007). In family firms facing succession issues, a buyout may often be perceived as the only way for the firm to stay independent. In private and family firms, there is typically no separation of ownership and control prior to the buyout (Howorth et al.), and hence there is less scope for improvements from improved control mechanisms (Chrisman, Chua, & Litz, 2004). Limited agency issues may arise where ownership is dispersed among family members (Howorth et al.; Schulze, Lubatkin, Dino, & Buchholtz, 2001). Some limited growth opportunities may be available where the private owners have become risk–averse in an effort to preserve the wealth they have created.

Of this total, 38% are family buyouts and 7% are secondary buyouts. Four percent of all deals in this period involved public–to–private buyouts. The balance of 10% of deals involved public sector privatizations and buyouts of failed firms.

In a secondary buyout, an initial buyout deal is refinanced with a new ownership structure including, typically, a new set of PE financiers while the original financiers and possibly some of the management exit. Secondary buyouts represent the acquisition of an initial buyout where agency cost–control mechanisms are already in place: significant managerial ownership and leverage, as well as active involvement by PE firms. Much of the impetus for PE providers to buy portfolio companies from other financial investors has come from difficulties in finding other sources of exit as corporate restructuring programs passed their peak and as the explosion in funding availability placed pressures on PE firms to invest the funds they had raised (Wright, Renneboog, Simons, & Scholes, 2006).

Theory and Hypotheses

Agency and Strategic Entrepreneurship Perspectives on Management Buyouts

Researchers have generally adopted an agency–based approach to buyouts (Renneboog, Simons, & Wright, 2007). Jensen (1989) argues that high leverage, increased equity ownership by managers, and monitoring by specialist fund providers create an organizational form whose incentive structure leads to profit maximization. Using an agency perspective, several empirical studies focusing on public–to–private transactions have found an improvement in the operating performance of the buyout firm reflecting these improved governance mechanisms (Holthausen & Larcker, 1996; Kaplan, 1989; Muscarella & Vetsuypens, 1990).

Agency theory's focus on profit maximization confounds the sources of improvements in performance as performance is a multidimensional construct (Delmar, Davidsson, & Gartner, 2003; Hitt, 1988). Profitability, as a measure of performance, may increase following buyout as a result of value creation and/or value capture (Coff, 1999). Value capture may arise from transfers from other stakeholders. In the PE context, this capture has particularly been portrayed by critics as involving a transfer from employees to investors in the form of job destruction. Value creation can be distinguished in terms of improved efficiency and increased effectiveness (Peteraf & Barney, 2003). Efficiency relates to an input–output ratio; consequently, improved efficiency occurs either when output increases for a given input, or less input is required for a given output. To the extent that cost–cutting strategies to achieve efficiencies have a disproportionately adverse impact on employees, there may also be value capture. Effectiveness concerns an absolute level of input acquisitions or outcome attainment such as growth (Goodman & Pennings, 1977; Ostroff & Schmitt, 1993).

A limitation of agency theory is that it under–emphasizes the upside potential of buyouts. The traditional agency approach to buyouts largely focuses on their reduction of costs associated with over–diversification and over–investment in mature or declining industries with few growth opportunities (Jensen, 1989). Agency controls contribute to cutting back on value–destroying activities and investments. The outcome of these effects is likely an improvement in efficiency (Harris et al., 2005). The agency approach provides incentives for managers to seek out profitable opportunities. However, the controls arising from high leverage and financial monitoring likely limit managerial discretion and stifle flexibility and risk–taking (Jensen & Meckling, 1976). Yet, highly leveraged transactions may be inappropriate when the debt levels restrict the ability to exploit further growth opportunities (Wright, Hoskisson, et al., 2000).

A strategic entrepreneurship perspective, grounded in the resource–based view of the firm, provides complementary insights to the agency perspective (Makadok, 2003). This perspective recognizes that access to resources and capabilities may be important in generating performance, especially value creation through growth (Ireland et al., 2003). Growth is an important indicator of entrepreneurial activity (Delmar et al., 2003). Generating enhanced performance, therefore, may not simply be a function of designing appropriate contracts to control agency problems, which may be problematic where performance is multidimensional and the environment uncertain (Holmstrom & Milgrom, 1991), but may relate to the capabilities of managers to deliver that performance (Hendry, 2002). There may thus be important synergies between strong governance and strong competence (Makadok). In a buyout context, these resources and capabilities relate, first, to the idiosyncratic skills and tacit knowledge of management to identify opportunities for value creation (Castanias & Helfat, 2001; Coff, 1999). This knowledge may be present in existing management or may need to be acquired. Prior to buyout, however, managers may be unable or unwilling to utilize their knowledge and skills. Second, idiosyncratic skills and knowledge relate to the specialist expertise of PE firms in selecting deals and in monitoring and advising management. PE firms may provide complementary resources and capabilities that may be missing from the management team (Zahra & Filatotchev, 2004). The commonality of these roles across PE firms suggests that selection, monitoring, and advisory roles per se may not be a source of competitive advantage (Barney, 2002). However, some PE firms may be much more skilled in how they implement otherwise common selection, monitoring, and advisory devices through learning, thus creating distinctive organizational capabilities (Barney et al., 2001; De Clercq & Dimov, 2007). Problems in learning are well recognized (Bukszar & Connolly, 1988; Darr, Argote, & Epple, 1995; Lieberman, 1989). Differences in PE firms’ capacity to learn from their experience and upgrade organizational capabilities allow some of them to sustain their competitive advantage. The capacity to adapt, extend, and reconfigure capabilities is an important dynamic capability that allows firms to compete more effectively in highly competitive market environments (Teece, Pisano, & Shuen, 1997).

Several studies have explicitly drawn attention to entrepreneurial activity in buyouts. For example, Bull (1989) provides evidence of the entrepreneurial impact of management buyouts and Malone (1989) and Wright, Thompson, and Robbie (1992) also cite evidence of new product innovation. Other research indicates that substantial increases in new product development, technological alliances, and research and development (R&D) staff occur after a buyout (Zahra, 1995).

Building on these ideas, we argue that buyouts should be seen as more than tools to facilitate gains from cost efficiencies and value capture from job destruction, but also as a means to stimulate strategic change that enables growth opportunities to be realized (Wright, Hoskisson, et al., 2000). Our analysis seeks to be indicative of whether buyout investors capture value from employees. Within the context of our study, this would be indicated by a combination of higher profitability and slower employment growth. Improvements in profitability can be created by improvements in productivity; however, both can improve at employees’ expense because of job losses. Profitability may increase if a given amount of sales revenue can be achieved with fewer employees as employment costs would decline. Productivity would also increase since a given output is achieved with a lower employment input. By analyzing sales revenue and employment growth separately we are able to get a better indication of how potential productivity improvements are achieved.

Agency and Strategic Entrepreneurship Perspectives in Divisional Buyouts

Large organizations typically develop elaborate policies, procedures, and organizational structures to clearly define decision–making responsibilities and reduce decision uncertainty. Where the diversified corporation's existing governance or remuneration structure truncates divisional managerial incentives and rewards, the opportunity for a buyout may exist (Wright, Thompson, Chiplin, & Robbie, 1991). From an agency perspective, the introduction of incentive and monitoring mechanisms in a buyout may lead to increased profitability, particularly from efforts to reduce costs and improve efficiency.

Divisional buyouts may also be initiated where managers recognize growth opportunities that are constrained by organizational structures (Wright, Hoskisson, et al., 2000). These divisional buyout opportunities often represent under–investment situations by the parent firm, especially where the division may be peripheral to a parent's strategy. In complex organizations, internal capital markets may not always function in a competitive manner, so that divisions with profitable investment opportunities may be disadvantaged if their division is not regarded as strategically central to the parent organization (Hoskisson & Turk, 1990). With a planned internal capital market, the scope for divisional–level initiators is very limited (Hoskisson & Hitt, 1988).

In this context, managerial effort and motivation may be lacking or misdirected (Castanias & Helfat, 1991, 2001). On one hand, managers with tacit knowledge or idiosyncratic skills in their particular domain may recognize new opportunities for growth but may be prevented by a bureaucratic corporate control structure from implementing the entrepreneurial growth opportunities they identify (Busenitz & Barney, 1997; Green, 1992). To convince corporate management to support these ideas may be problematic where corporate decision systems require hard supporting data for new investment proposals. By their nature, however, such opportunities may rely on subjective information and tacit knowledge of managers. On the other hand, managers in divisions may also be in a weaker bargaining position prior to buyout to capture returns from their tacit knowledge and idiosyncratic skills; governance and remuneration schemes may not adequately incentivize the performance of managers in individual divisions (Makadok, 2003). To obtain a share of the gains that reflect the contribution of their tacit knowledge or idiosyncratic skills, they may seek to undertake a management buyout that would give them a significant equity stake (Castanias & Helfat; Coff, 1999).

Severing ties with the corporate infrastructure can increase buyout managers’ flexibility to more freely initiate and pursue various value–creating activities (Wright, Hoskisson, & Busenitz, 2001). Evidence from divisional managers regarding the reason for buyouts provides further support for this entrepreneurial perspective (Wright et al., 1991). Green (1992) reports that buyout ownership allowed managers to perform tasks more effectively through greater independence.

These problems are likely lower in other private buyouts and hence there is less scope for improvements in performance arising from efficiency improvements and growth (Chrisman et al., 2004). In family firms, owner–managers with substantial equity stakes have incentives to seek out profitable opportunities, and as peak–tier coordinators, have the flexibility to implement new opportunities they identify (Howorth et al., 2004); both of these aspects are absent in divisional cases. The prospects for gains arising from resolving any agency problems may be limited to those cases where ownership was dispersed before the buyout (Howorth et al.; Schulze et al., 2001), which appear to represent a small proportion of family firm buyouts (EVCA, 2003, 2005). Limited growth opportunities may be available after the buyout where the private owners had become risk averse in an effort to preserve the wealth they have created, assuming that the second–tier management taking over are able to identify and implement such opportunities (Wright, Hoskisson, Busenitz, & Dial, 2001).

Secondary buyouts provide a means to continue the buyout organizational form, albeit with a different set of investors. In contrast to managers in divisions of larger corporations, the initial buyout involves equity stakes by management, control by PE firms, and pressure from leverage. The effort to reduce costs in buyouts is usually focused on the first 2–3 years after the buyout (Seth & Easterwood, 1993; Wiersema & Liebeskind, 1995). Beyond this period, it may be difficult to obtain further cost reductions and efficiency improvements. The introduction of an amended incentive and governance structure on second buyout, such as increased managerial equity stakes and loosened controls by PE firms, may facilitate improved performance through pursuit of growth opportunities. However, given that the first buyout will have given scope and incentives for growth, the scope for growth improvements is likely less than for divisional buyouts.

To summarize, divisional buyouts often act as a stronger mechanism to “unlock” profitability, efficiency, and growth strategies previously constrained by inefficient organizational structures than in other types of private buyout. Therefore, we hypothesize:

PE Firms and Post–Buyout Performance

As we have argued, buyouts need to structure their resource portfolio by acquiring resources as needed and creating the capabilities to identify and exploit growth opportunities. Buyouts may not possess all the resources and capabilities that they require to exploit growth opportunities but may seek to acquire them from external partners through their networks (Ireland et al., 2003; Lee, Lee, & Pennings, 2001). Social capital theory suggests that firms should pursue strategies focusing on the development of networks with external resource holders as a valuable resource to enhance performance (Adler & Kwon, 2002). In the context of management buyouts, PE investors’ networks may help them source better deals and put them in a position to provide resources and capabilities the management of the buyout firm is currently missing. Especially in buyouts with value–creating opportunities, PE firms can play a significant role in adding value to the post buyout firm as these buyouts demand different skills than the traditional monitoring skills (Bruining & Wright, 2002; Wright, Hoskisson, et al., 2000).

Early studies tended to treat PE firms as a homogeneous group of investors, yet the resource and capability differences among this group of investors is increasingly recognized. PE firms differ considerably along several dimensions, such as the identity of general and limited partners, reputation, previous experience, specialization, network configuration, and investment styles (Bottazzi, Da Rin, & Hellmann, 2008; Elango, Fried, Hisrich, & Polonchek, 1995; Hochberg, Ljungqvist, & Lu, 2005; Kaplan & Schoar, 2005; Munari, Cressy, & Malipiero, 2007). These differences likely have implications for the selection of deals and for the performance of the post–buyout firm.

More experienced PE investors may be able to select better deals and are likely better both at monitoring the underlying investment and adding value by realizing growth opportunities (Baum & Silverman, 2004). More experienced PE investors may be able to reduce pre–investment agency problems (adverse selection) that arise due to informational asymmetries about potential investees. They may thus be better able to identify investees that are better performing and/or that have the better performance prospects, including cases where they believe that their expertise will enable them to add the most value. They may also have developed competencies in writing effective contracts to minimize agency costs (Kaplan & Strömberg, 2004). Similarly, more experienced PE firms may also reduce agency problems that arise post–investment (moral hazard) by being better able to monitor their investees. As such, experienced PE investors will positively impact the value captured and the value created in a buyout transaction. PE firms with greater breadth and depth of prior experience will be less susceptible to being misled. Prior investment experience, therefore, may help overcome agency risk (De Clercq & Sapienza, 2005). Further, lower levels of informational asymmetries and more effective contracts likely increase the bargaining power of the PE firm toward the different resource holders (Coff, 1999). For example, there is some evidence that buyouts constitute a mechanism to renegotiate contracts with different stakeholders of the firm such as employees in order to transfer wealth to the investors (Ippolito & James, 1992). Overall, it is expected that more experienced investors will be better at monitoring the buyout firms, and therefore, increase the value capture by realizing higher levels of profitability.

The PE firm's expertise and competencies with regard to strategy, operational and financial management, human resources, marketing policy, and mergers and acquisitions, also help create value for the buyout firm (Lee et al., 2001; Wright, Hoskisson, Busenitz, & Dial, 2001). For example, inside management does not always possess the tacit knowledge and idiosyncratic skills required to seize new opportunities (Hendry, 2002). In situations where significant innovation is needed, it may be necessary to bring in outside managers who do possess these skills, as in a management buy–in or an investor–led buyout (Wright, Hoskisson, & Busenitz, 2001). In these cases, PE firms play an important role in assessing the skills of the incumbent managers and their potential replacements. Further, PE–backed buyouts can make use of the PE firm's extensive network and relationships: customers, suppliers, other investors, access to more sophisticated resources in banking, legal and other areas, etc. (Bradford & Smith, 1997). Though management buyouts generally require less investor involvement than earlier stage investments (Sapienza, Amason, & Manigart, 1994), buyouts with opportunities for value creation require greater involvement by the PE provider, who may play an important role in developing entrepreneurial competencies. For such companies, the PE investor contributes to top management decision making by keeping strategy on track; establishing new ventures/acquisitions; broadening market focus; and reviewing R&D, budgets, and marketing plans (Bruining & Wright, 2002).

The more experience PE firms have, the larger the potential to create value. PE firms derive knowledge from prior investments and manifest their absorptive capacity in their evaluation, selection, and management of investment opportunities (De Clercq & Dimov, 2007). As PE firms gain investment experience, they develop a broad range of knowledge about markets. General business experience provides many of the skills needed for exploiting an opportunity, including selling, negotiating, planning, decision making, problem solving, organizing, and communicating. Further, the more investments PE firms undertake, the larger the information network PE firms can rely on. These contacts offer privileged access to expert advice that might help realize growth opportunities (Hochberg et al., 2005; Sorenson & Stuart, 2001). This is important as one major task of PE firms is recruiting highly qualified management for their portfolio companies. Additionally, more experienced investors will have access to more flexible debt arrangements (Cotter & Peck, 2001) that allow the buyout firm to take on more risky projects in order to realize growth opportunities. For example, buyout specialists are more likely to have access to long–term debt arrangements, reducing interest and principal repayments in the short term, allowing the PE investor flexibility to pursue growth opportunities.

Overall, this discussion suggests that more experience will help to reduce agency–related conflicts through improved monitoring and increase the value–adding potential. Hence:

PE firms differ considerably with respect to the number of PE executives available to manage underlying portfolio companies (Cumming & Johan, 2007; Elango et al., 1995). The intensity of monitoring and value adding, therefore, varies among PE firms. Entrepreneurial firms may require greater PE involvement if they are to identify and exploit opportunities. Kanniainen and Keuschnigg (2003) point to an important trade–off between the number of firms in the portfolio of a PE firm and the extent of managerial advice offered to these portfolio companies. By increasing the size of the portfolio with a fixed number of executives and associated limited time and specialist knowledge to add value, the amount of advice available per investee firm likely falls. This likely reduces the prospects of the portfolio companies and thereby undermines the PE firm's returns from the portfolio of firms. Manigart et al. (2002) show that PE firms with more intense monitoring seek higher returns for this costly effort. Cumming and Johan show empirically that venture capital firms with large portfolios per number of fund managers become less involved in the development of their ventures. In particular, their results indicate that venture capital firms with one extra entrepreneurial firm per manager in their portfolio provided on average 2–3 hours per month of less support and 20% less advice. Increasing the portfolio reduces both the monitoring and value adding by the venture capital firm. Therefore, it is expected that the performance of the buyout firm will be lower for PE firms with more portfolio companies per investment manager. Hence:

PE Firms and Type of Transaction

As discussed earlier, different types of buyouts offer different opportunities for efficiency changes and growth activities (Wright, Hoskisson, Busenitz, & Dial, 2001). The extent to which PE firms can add value by efficiency improvements and pursuing entrepreneurial opportunities, therefore, will depend on the type of deals in which they invest. As such, unique resources brought to the deal by experienced PE firms will be more valuable for certain deals as compared with others. In the following paragraphs, we focus on the distinct role PE firms can play in divisional buyouts as compared with other private buyout transactions.

Previous PE investment experience and intensity of follow–up is likely more important for deal selection and realizing efficiency improvements and firm growth in divisional buyouts. At deal selection, information availability is difficult for private firms but may be especially problematic for divisional buyouts. Separable data may be limited for divisions of larger groups; for example, these entities may be cost centers without their own profit and loss accounts; this is less problematic for family firms and secondary buyouts that are stand–alone firms. More experienced PE firms may be better able to analyze the underlying performance prospects of divisions.

As argued previously, parental control problems and constraints on initiatives mean that divisional buyouts often create the potential for efficiency improvements and the exploitation of entrepreneurial opportunities (Wright, Hoskisson, et al., 2000), and these problems are likely greater than in a family of secondary buyouts. More experienced investors and investors with a lower number of portfolio companies per PE manager likely will be better at monitoring investees in order to reduce agency–related problems and to bring efficiency up. Further, identifying and exploiting entrepreneurial opportunities involves high levels of uncertainty. When facing new opportunities, PE firms use their knowledge to understand and evaluate them. In this process, absorptive capacity—the ability to recognize the value of new, external information, assimilate it, and apply it to commercial ends—provides a key learning capability grounded in the firm's prior knowledge (Cohen & Levinthal, 1990). Continuing action and experience in a particular industry creates deeper knowledge of that domain, which in turn enhances domain–specific learning, and consequently, the firm's domain capabilities as a source of competitive advantage. Divisional buyouts that have been constrained by parental control systems may have potential absorptive capacity embodied in incumbent management teams but they lack the experience to identify and exploit opportunities effectively. In a buyout without PE involvement, they may engage in costly, wasteful, and time–consuming learning. Involvement by an experienced PE firm may provide the capabilities that avoid such problems (Zahra & George, 2002; Zahra, Sapienza, & Davidsson, 2006).

To summarize, previous investment experience and intensity of involvement will be especially valuable in divisional buyouts as it enhances a PE firm's monitoring skills and its absorptive capacity, which enhance its ability to monitor investees and to successfully identify and exploit entrepreneurial opportunities. Hence:

Similarly, in respect to the number of portfolio companies per PE manager we have:

Methodology and Research Design

Data Collection

The empirical setting used in this study is the UK market for PE–backed buyout transactions over the period 1993–2003. The UK PE market is the largest and most dynamic in Europe, accounting for some 52% of the whole European PE market in 2004, and is second in size only to the United States on the world stage (Wright et al., 2007). We combine three different data sources to analyze our hypotheses. First, data on individual deal characteristics are drawn from a unique, hand–collected data set maintained by the CMBOR. This database covers the entire population of buyouts in the UK. The population of PE–backed firms during the period 1993 to 2003 of private buyouts of divisions, family firms, and secondary buyouts, the focus of this study, was 2,428. Second, these data are then combined with characteristics of PE firms collected through directories issued by the British Venture Capital Association and the European Venture Capital Association (EVCA). Third, for each buyout firm we collected accounting information from FAME, a commercial database containing information on public and private companies in the UK. Accessing these databases prior to 1993 was problematic. We ended our coverage in 2003 to enable us to measure 3 years of post–buyout profitability and growth (see following discussion). After combining these different data sources, we obtained a sample of 238 PE–backed buyout transactions on which full information is available. In total, 45 different PE firms were involved in these transactions. The sample is representative of the full population of private buyouts in terms of deal vendor source and size. The percentage of divisional buyouts closely approximates the average in the population of private buyouts (47% versus 45%). The median size of the buyouts included in the sample is also very close to the median buyout in the population (£6.7 million versus £6.9 million). The percentage of management buy–ins is lower than the population average (13% versus 21%); management buy–ins are generally riskier and more likely to fail, making it more difficult to track them.

Variables

Dependent Variables

As mentioned earlier, agency theory's focus on profit maximization confounds the sources of improvements in performance, as performance is a multidimensional construct (e.g. Delmar et al., 2003; Hitt, 1988). Therefore, several performance measures are used as dependent variables in this study. Profitability, as a measure of performance, may increase following a buyout as a result of value creation and/or value capture (Coff, 1999). Value creation can be distinguished in terms of improved efficiency (typically measured by productivity) and increased effectiveness. Efficiency relates to an input–output ratio or comparison, that is, by getting more out of the resources the firm uses. Effectiveness concerns an absolute level of input acquisitions or outcome attainment such as growth (Goodman & Pennings, 1977; Ostroff & Schmitt, 1993).

To measure profitability, we use “return on capital employed” (ROCE). 2 ROCE takes into consideration the net capital resources available to generate operating profits, after allowing for current liabilities as part of working capital. ROCE is calculated by dividing operating profits by total assets from which current liabilities were subtracted. We use the absolute change in the value of ROCE from the year of the buyout until 3 years after the buyout as dependent variable. In order to control for macroeconomic and industry factors outside buyout firms’ control, we adjust the change in ROCE by subtracting the change in the four–digit SIC industry average.

As a robustness test, we also used return on assets as a measure of profitability. The results were substantially similar and are therefore not reported here but are available from the authors.

Though financial profitability is important, some behavioral aspects motivated from agency and entrepreneurial perspectives are not captured by such measures. We, therefore, use some measures that capture the efficiency and growth of the buyout firm. In order to measure efficiency, we use the sales per employee ratio. 3 Change in sales per employee is measured as the percentage change in sales per employee from the year of the buyout until 3 years after the buyout. This measure is industry–adjusted in order to control for industry–wide factors that account for efficiency changes.

We also used percentage change in value added per employee as a measure of efficiency but none of the results were significant and are therefore not reported here.

Sales and employment growth are widely used indicators in empirical analyses of entrepreneurial growth (Delmar et al., 2003). In addition, they capture different aspects of how firms grow. Sales growth will capture entrepreneurial growth activity that leads to additional revenue being created. For this to occur, a contemporaneous increase in employment might also be observed. However, if given labor resources are better utilized to create additional sales revenues (see earlier discussion), sales growth may not lead to employment growth. We include employment growth to capture growth in labor resources and as an indicator of growth in the size of the firm (Delmar et al.). We use average sales revenue growth and the average growth in number of employees in the 3 years following the buyout (Munari et al., 2007). Both growth measures are industry–adjusted by calculating them relative to the four–digit SIC average.

Independent Variables

Several independent variables are used in the analyses. First, in order to capture the source of the buyout transaction, we include different dummy variables. A distinction is made between divisional (divisional) and other buyouts (other buyout); as discussed earlier, the other category includes secondary buyouts and private/family buyouts. Second, PE experience is measured by counting the cumulative number of buyout investments for each investor. This measure includes investments from the early 1980s onwards, as recorded in the CMBOR dataset (De Clercq & Dimov, 2007). The logarithm of this measure is used as this variable is highly skewed (PE experience). The intensity of value adding and monitoring is measured by dividing the total number of portfolio companies managed by a specific PE firm by the number of investment executives employed by the PE firm (Cumming & Johan, 2007) (investments/executive).

Control Variables

In the regression analyses, we include several control variables related to the PE firm and the buyout company. First, we include a dummy variable that indicates whether the deal is syndicated or not (syndication). Previous literature has shown that firms syndicate their deals in order to gain access to resources from other PE firms. This might have a positive impact on the performance of syndicated transactions (Manigart et al., 2006). We control for the extent of specialization of the PE firm by calculating a specialization index, derived from similar measures in the literature on international trade specialization and international technology specialization (specialization) (Munari et al., 2007). This index is computed as the share of buyout investments (in number of companies) of a PE firm in a given industry divided by the PE firm's share (in number of companies) in the total PE–backed buyout industry. The industry classification comprises 35 different industries. The index is equal to zero if the PE firm holds no portfolio of companies in a given industry, is equal to 1 when the PE firm's share in the sector is equal to its share in all fields, and grows rapidly when a positive specialization is found, the upper limit depending on the total distribution being used. We take the logarithm of the specialization measure as it is highly skewed. We also include a dummy variable indicating whether the PE firm was an independent investor, because independent firms have higher return requirements compared with captives and other type of investors, and therefore, might seek to increase the performance of their portfolio companies more compared with other investors (Manigart et al., 2002) (independent).

The extent of managerial ownership has been shown to impact firm performance following buyouts. As suggested by Kaplan and Stein (1993), we include the absolute amount invested by the management of the buyout firm (management investment). Further, in order to control for the disciplining effect created by high levels of senior debt, we include the gearing of the buyout firm, which equals the total amount of senior debt divided by the total amount of equity used to structure the buyout transaction (gearing). To take into account scale effects on post–buyout performance, we include buyout firms’ size. Size is measured by sales revenue in the year of the buyout (sales_0). To control for the effect of previous profitability levels, we include ROCE in the year of the buyout (ROCE_0). There might be a concern that PE firms with more experience are better at selecting the best deals than those with less experience. Ideally, forward–looking information may be helpful in distinguishing the best deals, but as this is only available in business plans, it was not accessible to us. In order to distinguish between value adding and selection, therefore, we use a common approach to examine if there are lead effects in the buyout firm (Amess, 2003; Lichtenberg & Siegel, 1990). By examining performance and growth prior to a PE–backed buyout, it is possible to determine whether PE firms are selecting the best deals. As we examine private firms, information disclosure restrictions for divisional cases in particular mean that our data are limited, in that wecan only determine performance and growth at the time of the buyout. Nevertheless, we interact the PE experience variable with our profitability variable in order to determine if PE–backed buyouts had a higher level of profitability at the time of the buyout. To calculate this interaction term, both PE experience and profitability were centered in order to reduce problems of multicollinearity. In order to test whether performance improvements are driven by a strategy of acquisitions, we include a variable that captures the number of acquisitions a buyout firm was involved in (# acquisitions). Given the heterogeneity of buyout types as outlined earlier, dummy variables are included to capture these; a distinction is made between management buyouts (MBO dummy), management buy–ins (MBI dummy), a combination of a buy–in and a buyout (BIMBO dummy), 4 and investor–led buyouts (IBO dummy). Management buyouts are the omitted reference category. Lastly, we introduce year dummies to control for unobserved factors that affect the dependent variables over time that are common to all firms.

A BIMBO is a combination of management buyout and buy–in, where the management team that buys the business includes both existing management and new managers.

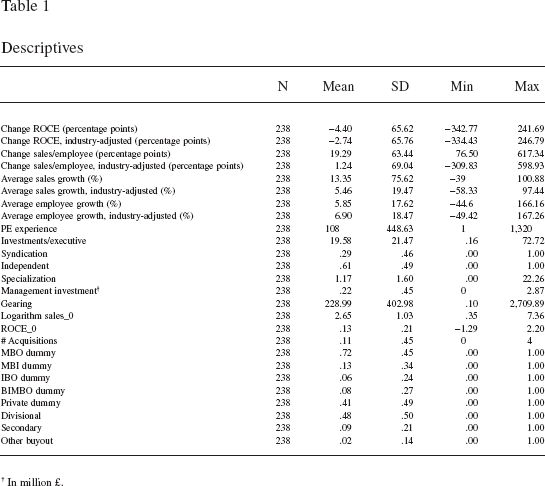

Descriptive Data

The summary statistics for the buyout transactions and the PE firms involved in those transactions are shown in Table 1. The average industry–adjusted change in ROCE in the 3 years following the buyouts amounts to −2.74%. The median change is positive and equals 2%. When looking at the percentage change in sales per employee, buyout firms perform, on average, 10.24% better than the industry average. Average yearly sales growth in the 3 years following the buyout transaction equals 13.35%, which is considerably higher than the industry average. The average yearly growth in number of employees is 5.58%, which is higher than the industry average.

Descriptives

In million £.

The cumulative number of previous investments by PE firms in our sample is, on average, 108. As the standard deviation (SD) indicates, there are huge differences between the PE firms in the sample. One investor, namely 3i, was involved in 1,320 investments in the year prior to its investments. The average number of investments per investment executive equals 19.58 (median = 12). This number is considerably higher compared with figures reported for early stage venture capital firms (Cumming & Johan, 2007).

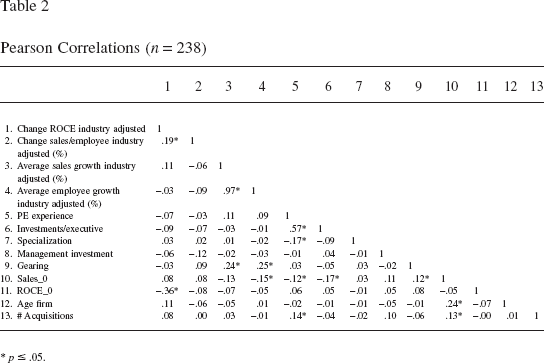

The correlation matrix for the variables used in the analyses is in Table 2. The correlations between all the independent variables used in the regression analyses are below .57, suggesting that there are no multicollinearity problems. Furthermore, variance inflation scores do not indicate problems of multicollinearity. 5

These are not included in the paper but are available on request from the authors.

Pearson Correlations (n = 238)

p ≤ .05.

Results

To test hypotheses 1 to 4, we run OLS regressions with robust standard errors in order to deal with problems of heteroskedasticity. In separate analyses not reported here, we also estimate “treatment effects models” in order to correct and test for possible bias arising from the self–selection of PE–backed buyout transactions. However, the results aresimilar. 6 Our dependent variables are change in ROCE, sales/employee, sales growth, and employee growth. The regression results are reported in Tables 3 and 4.

In the two–step Heckman model, we first predict the probability that a buyout firm will be PE–backed using the size and profitability of the buyout firms as predictors. These are available on request from the authors.

OLS Regression Efficiency and Growth of the Buyout Firm (n = 238) ‡

p < .10,

p < .05,

p < .01,

p < .001.

All the dependent variables are industry–adjusted.

OLS Regression PE Heterogeneity and Source of Transaction (n = 238) ‡

p < .10,

p < .05,

p < .01,

p < .001.

All the dependent variables are industry–adjusted.

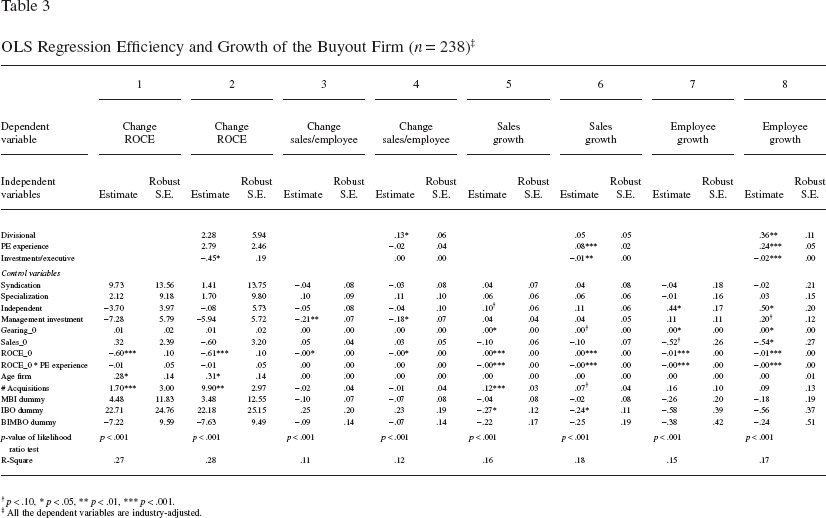

In models 1 and 2, we employ ROCE as the dependent variable. Likelihood ratio tests indicate the independent variables in all models are jointly significant, and R–squares indicate that the models are a reasonable fit of the data. Model 1 shows that ROCE in the year of the buyout has a negative impact on the change in ROCE following the buyout, whereas the age of the buyout firm and the number of acquisitions the buyout firm was involved in have a significant positive impact. In model 2, the variables of interest are added. Only the intensity of follow–up, as measured by the investment per executive, is significant and has the expected sign, lending support to hypothesis 3a. The size of the coefficient indicates that adding one investment per executive decreases the change in ROCE by .45 percentage points over the 3 years post–buyout, implying .15% per year on average. None of the other variables is significant however. Hypotheses 1a and 2a are not supported.

In models 3 and 4, we use sales per employee as the dependent variable. Both profitability and the absolute amount invested by management have a significant negative impact on the performance change in sales per employee following the buyout. In line with hypothesis 1b, our results indicate that efficiency increases, as measured by change in the sales per employee, are higher in divisional buyouts as compared with other types of buyouts. The percentage change in sales per employee is, on average, 13% higher in a divisional buyout as compared with other types of private buyouts over the 3 years post–buyout, implying that average annual growth is 4.3% higher. Our PE–related variables are, however, not significant. Overall, there is some support for hypothesis 1b; however, hypotheses 2b and 3b are not supported.

In models 5 and 6, we use sales growth as the dependent variable. Divisional buyouts experience no significant higher sales growth as compared with private/family buyouts. Therefore, hypothesis 1c is not supported using this measure. The coefficient of the experience of the investor is highly significant and has the expected sign. The more experience an investor has, the higher sales growth following the buyout, consistent with hypothesis 2c. A 1% increase in the experience of the investor will lead to a .08% increase in sales growth in the 3 years following the buyout, implying that average annual growth is .026% higher. Further, a lower intensity of follow–up (measured by the number of investments managed per executive) is associated with lower sales growth following the buyout. This is in line with hypothesis 3c.

Models 7 and 8 in Table 3 use employment growth in the 3 years following the buyout as a growth measure. Model 7 shows that buyout firms backed by independent PE firms have higher levels of employment growth. In model 8, we introduce the variables of interest. Divisional buyouts show significantly higher levels of growth in line with hypothesis 1c. The growth in number of employees following a buyout is, on average, 36% higher in divisional buyouts as compared with other types of private buyouts over the 3 years post–buyout, implying that average annual growth is 12% higher. The results indicate that highly experienced PE investors experience significantly higher levels of growth at their portfolio of companies. This is in line with hypothesis 2c. A 1% increase in the experience of the investor will lead to a .24% increase in employee growth in the 3 years following the buyout, implying an average annual increase in employment growth of .08%. Furthermore, lower intensity of follow–up is associated with lower employment growth following the buyout, which supports hypothesis 3c.

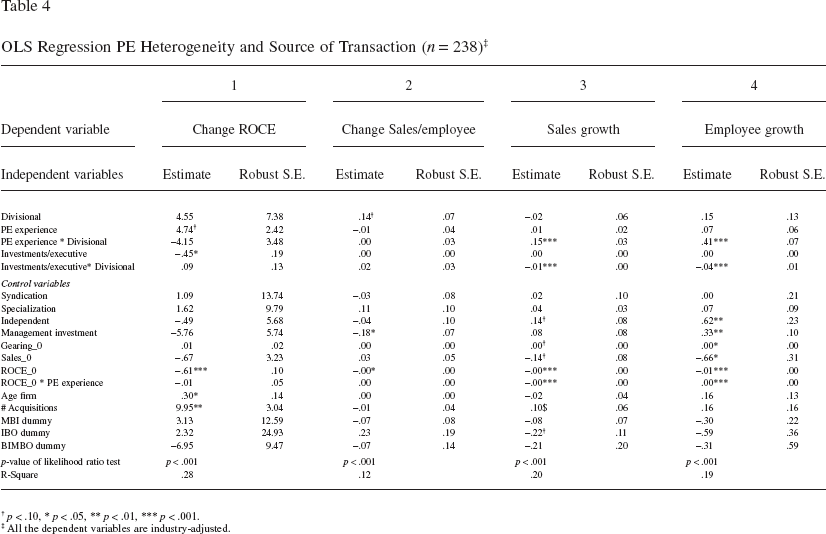

In the analyses presented in Table 4, we introduce an interaction term between the experience of the investor and the type of the buyout. Further, we also include an interaction term between the number of investments per executive and the type of buyout. All the continuous variables used in these interaction terms were centered in order to reduce problems of multicollinearity. Models 1 and 2 show no significant interaction effect. As such, hypotheses 4a, 4b, 5a, and 5b with respect to profitability and efficiency are not supported. Models 3 and 4 with sales growth and employee growth as dependent variables provide strong support for hypotheses 4c and 5c. Investor experience and intensity of follow–up is especially important for realizing firm growth in divisional buyouts.

Discussion and Conclusion

In this study, we have synthesized agency and strategic entrepreneurship perspectives to provide complementary insights into three research questions concerning PE–backed buyouts: (1) how do different types of PE–backed buyout transactions impact post–buyout performance; specifically, how does the performance of divisional buyouts differ from other private buyouts; (2) how do differences in PE firm experience and intensity of post–buyout involvement impact on the performance of firms undergoing a buyout; and (3) does PE firm experience impact differently on the performance of divisional buyouts than for other private buyout types? These research questions were addressed using a unique hand–collected dataset of 238 PE–backed buyouts in the UK between 1993 and 2003.

To summarize our findings in relation to the first research question, divisional buyouts are not associated with significant changes in profitability as compared with other types of buyouts. However, divisional buyouts are associated with increases in efficiency, measured by sales per employee, and growth, as measured by employee growth. The effects are economically significant. For example, the results indicated that the growth in number of employees following a buyout is, on average, 36% higher in divisional buyouts as compared with other types of private buyouts. With respect to our second research question, our analysis indicated that PE firm experience is not related to higher levels of profitability or efficiency. However, higher levels of PE firm experience are associated with higher levels of growth at the buyout firm. These effects are economically significant. Further, the intensity of follow–up was positively associated with changes in profitability and growth following the buyout. Lastly, with respect to our third research question, we found strong support that PE firm experience and intensity of follow–up is mainly important in achieving growth in divisional buyouts as compared with other types of buyouts. Among our control variables, we find that undertaking acquisition activity is significantly associated with profitability but not with growth.

Overall, we find stronger support for the effects of divisional buyouts and PE firm experience on value creation, especially growth, and to a lesser extent, efficiency. Our results are not consistent with value capture occurring in divisional buyouts compared to non–divisional buyouts. Indeed, results in Table 3 indicate that entrepreneurial growth occurs without significant additional value being created via profitability. This might be because post–buyout managers in divisional buyouts are making entrepreneurial investments in growth that do not feed through to contemporaneous profitability. We do find, however, evidence that productivity is higher for divisional buyouts in Table 3. This raises the question as to whether such growth creates value in the longer term that may be realized by investors when they exit their investment through a strategic sale or IPO.

This study contributes to the literature on buyouts and PE investing specifically, and the strategic entrepreneurship literature in general in several ways. Previous literature on buyouts, which has primarily involved public–to–private transactions, has tended to analyze profitability and efficiency changes rather than growth (Kaplan, 1989). Our analysis of divisional buyouts shows that value creation through post–buyout growth is particularly important. Whereas previous literature has acknowledged differences among PE firms (Elango et al., 1995; Kaplan & Schoar, 2005; Munari et al., 2007), few studies have actually looked at the impact of these differences on the performance of portfolio companies. Our results indicate that general investment experience has a positive impact on the performance of the buyout firm, especially in terms of growth. In line with Cumming and Johan (2007), our results show that the extent of value adding delivered by PE firms decreases when investment executives have to manage larger portfolios. This clearly has a negative impact on the growth of the post–buyout firm. These results emphasize the resources and capabilities that buyout specialists bring in terms of monitoring and advice provision to their portfolio companies.

While previous studies have mainly focused on the role of PE firms in early–stage transactions (Hellmann & Puri, 2002), the results of this study show that PE firms can play a major role in fostering growth in buyout stage firms. These findings add to the buyout and PE literature, since they provide more fine–grained insights than hitherto about how some PE firms are more skilled at implementing otherwise common monitoring and advisory devices (Barney et al., 2001). In general, our findings help to extend the strategic entrepreneurship perspective to the buyout and PE context. The findings also complement the traditionally dominant agency theory perspective, helping to enhance understanding of those buyouts that have growth prospects. Specifically, our findings in respect to divisional buyouts provide empirical evidence suggesting synergies between enhanced governance and greater access to resources and capabilities (Makadok, 2003). The greater strength of our findings in respect to growth, rather than profitability or efficiency, indicates that in these cases, incorporating a resource–based strategic entrepreneurship perspective is particularly important. A further implication of our findings is that, not only do divisional buyouts differ from other buyout types primarily with respect to post–buyout growth, but also that PE investors seem to be more valuable with respect to growth than they are with respect to profitability and efficiency gains. This finding seems to be especially important given the criticisms that PE firms obtain their gains primarily through profitability and efficiency gains achieved through cost reductions.

The study has some limitations that suggest avenues for further research. First, we have undertaken limited analysis of the extent to which buyout firms use internal or external (acquisition) strategies to realize firm growth and to fill gaps in resources and capabilities, but found that acquisition activity, while associated with higher profitability, does not appear to be strongly associated with greater growth. Previous research has indicated that different types of investors have different preferences with respect to the type of growth strategies of firms (Hoskisson, Hitt, Johnson, & Grossman, 2002), and this is an area for further research. For example, further research might consider trying to obtain data on the extent of internal versus external growth strategies used by buyout firms or the innovativeness of buyouts’ growth strategies. Second, we have used a restricted set of measures of efficiency and entrepreneurial activity. Further research might usefully examine further measures. For example, the percentage of sales exported might be used as a measure of entrepreneurial activity, since exporting is viewed as a risky activity (Sanders & Carpenter, 1998). Third, while we have examined some dimensions of the differences among PE firms, other dimensions may yield useful insights regarding entrepreneurial activity. For example, PE firms with international experience may be better able to assist investees with growth efforts, especially internationalization. Fourth, while we have recognized that the relationship between better performance and experienced PE firms may be related to both better deal selection and better monitoring and advice, it is problematic to separate out the relative importance of each of these aspects. Baum and Silverman (2004), for example, find for early–stage biotechnology ventures that venture capital investors create value by picking the right ventures and adding value after the investment has been made. Further, Ljungqvist and Richardson (2003) show that reputable buyout investors are especially good at timing their investments. It would be interesting if future research in the buyout area could investigate the relative importance of selecting versus value adding in more detail. Finally, although we conducted representativeness tests, the possibility of a sample selection bias may still arise due to the omission of a large number of deals from our final sample, although our sample clearly covers a wide range of post–buyout performances. This potential problem may be mitigated as PE firms likely will have conducted due diligence to reduce information asymmetries in selecting the deals on the basis of private information in business plans, etc., and similarly, will likely monitor investee firms based on board representation and access to monthly management accounts; both these types of information are not available publicly.

Our analysis has implications for managers and PE firms involved in buyouts. In particular, differences in the contributions that PE firms can make suggests that managers and their advisors need to take considerable care in selecting financial backers for their prospective buyout, because they have differing capacity to fill the gaps in buyout firms’ resources and capabilities. Further, our findings emphasize the need for PE firms to recruit executives with the expertise to seek and exploit growth opportunities rather than solely monitoring skills (Lockett, Murray, & Wright, 2002). The performance differences observed between divisional buyouts and other private buyouts suggest that PE firms may need to consider deal–targeting more carefully. Finally, our findings also speak to the current policy controversy over the sources of gains in buyouts (e.g., Treasury Select Committee, 2007); for an important sector of the PE market, the view that gains are due principally to cost–cutting and efficiency gains is misplaced. Attempts to restrict PE–backed buyouts may mean that growth opportunities with wider economic and social benefits are foregone.