Abstract

Using panel data models, this study investigates whether firm's age is a determinant of Portuguese SMEs’ financing decisions. The results suggest that age is relevant for: the impact of financial deficit on variations of short– and long–term debt; the level of adjustment of short– and long–term debt toward the respective optimal levels; and the relationships between usual determinants and short– and long–term debt. The results for young and old SMEs suggest that Trade–Off Theory and Pecking Order Theory should not be considered to be mutually exclusive, since both theories are necessary to understand the SMEs’ capital structure decisions throughout their life–cycle.

1. Introduction

One of the most controversial questions regarding firms’ capital structure decisions is whether debt adjustments targeting debt ratio are a consequence of financing needs (Myers, 1984; Myers and Majluf, 1984—Pecking Order Theory) or do they arise from firms’ wishes to reach an optimal level of debt (Ang, 1976; Jalilvand and Harris, 1984; Lev & Peckelman, 1975; Taggart, 1977—Trade–Off Theory). In the context of SMEs, only López–Gracia and Sogorb–Mira (2008) study this subject, concluding that the problems of information asymmetry associated with the relationships between Spanish SMEs and creditors contribute to debt adjustments, and that these adjustments are motivated more by the lack of internal finance than an aim to reach a target debt ratio.

A firm's age is an important factor in the study of SMEs’ financing decisions, especially regarding variations and/or adjustments of debt. Information asymmetry takes on greater importance for young SMEs, since they have not yet acquired sufficient level of reputation (Diamond, 1989), credibility, and tangible business assets (Berger & Udell, 1998) to obtain credit on favorable terms. This situation implies that young SMEs must finance their activities with retained earnings rather than borrowing. However, the youngest SMEs may not have had time even to generate internal finance, and as a result need to incur considerable amount of debt at the beginning of their life–cycle (Petersen & Rajan, 1994).

SMEs at the start of their life–cycle, struggling to survive with low or no retained earnings, may become excessively dependent on short–term debt, where repayment of the debt and interests are easily monitored by creditors (Myers, 1977). Heavy resort to short–term debt due to financing needs associated with young SMEs’ investment opportunities can lead to the need for frequent debt adjustments toward a target debt level. These frequent adjustments amount to frequent renegotiations of the terms of short–term debt (Ortiz–Molina & Penas, 2008).

In the later stages of an SME's life–cycle, the effects of reputation (Diamond, 1989), credibility, and tangible business assets (Berger & Udell, 1998) can considerably diminish the problems of information asymmetry faced by SMEs, making it possible for these firms to replace short–term debt with long–term debt, when internal finance is lacking.

The influence of age on SMEs’ sources of finance can be particularly crucial in countries with an undeveloped stock market, where firms depend on retained profits and bank credit for finance. Portugal is one such country, as it has a bank–based financial system and a rather undeveloped stock market, compared with the United States or other European countries such as the United Kingdom. Although SMEs account for around 99.8% of all firms in Portugal, they do not meet the minimum requirements for access to the stock market. In addition, Portuguese firms face obstacles in accessing alternative external sources of equity, namely risk capital or business angels. As a result, when internal finance is insufficient, Portuguese SMEs can become excessively dependent on debt to finance their investment opportunities. Considering that internal finance and debt are the main sources of finance available to Portuguese SMEs, the Portuguese context is appropriate to study.

Given the state–of–the–art on the subject of SMEs’ capital structure decisions over their life–cycle, and the pertinence of the study applied to Portugal, this article seeks to identify the influence of the age of Portuguese SMEs on the impact of financial deficit on variations in short– and long–term debt, as well as on adjustments of short– and long–term debt toward the respective target debt ratios.

To do this, we consider two sub–samples of Portuguese SMEs for the period 1999–2006: (1) 495 young SMEs; and (2) 1,350 old SMEs. As estimation method, we use OLS regressions to determine the variations of short– and long–term debt as a function of firms’ financial deficit, and dynamic panel estimators to determine the adjustments of short– and long–term debt toward respective target debt ratios. In addition, seeking to address possible bias arising from the survival issue, we resort to the two–step estimation method proposed by Heckman (1979).

Our findings allow us to contribute to the literature, showing that age is relevant for: (1) the impacts of financial deficit on variations of short– and long–term debt; and (2) adjustments of short– and long–term debt toward the respective optimal levels. Furthermore, since we consider that optimal short– and long–term debt depend on the determinants usually considered in the literature, the results obtained in this study allow us to make the additional contribution that age is a fundamental characteristic of the relationships established between the determinants usually considered in the literature and short– and long–term debt.

The remainder of the paper is structured as follows: section 2 presents the theoretical framework and research hypotheses; section 3 presents the methodology, namely the database, variables used, and estimation methods used; section 4 presents the results obtained; section 5 discusses the results; and finally, section 6 presents the conclusion and implications of the study.

2. Theoretical Framework and Research Hypotheses

SMEs have more limited access to external finance than do large firms (La Rocca, La Rocca, & Cariola, 2009). The smaller size of SMEs implies a high operational risk associated with their activities, and consequently greater probability of bankruptcy. In addition, many SMEs have considerable difficulty in providing collateral security on debt. Therefore, problems of information asymmetry are particularly relevant in the context of the relationships between the owners/managers of SMEs and creditors. In addition, the majority of SMEs do not fulfil the requirements to be listed on the stock market, and so creditors have greater difficulty in obtaining accurate information about these firms (Cabral & Mata, 2003).

According to various studies (Davidson & Dutia, 1991; Degryse, de Goeij, & Kappert, 2010; Hall, Hutchinson, & Michaelas, 2000; Osteryoung, Best, & Nast, 1992; Walker & Petty, 1978) SMEs, in general, have higher levels of short–term debt than large firms. In this context (García–Teruel & Martínez–Solano, 2007; La Rocca et al., 2009; Peterson & Shulman, 1987) conclude that small firms’ main source of funds is internal, and when this is insufficient they must turn to short–term debt.

Greater SME age can contribute to a reduction of problems of information asymmetry implicit in the relationships with creditors. As these firms consolidate their business, with a past characterized by good performance giving them credibility, they are more able to obtain credit on favorable terms (Diamond, 1989). For Ang (1991), age is a fundamental driver for SMEs being able to replace short–term with long–term debt.

According to Pecking Order Theory, firms increase their capacity to retain profits over their life–cycle, reducing dependence on borrowing to finance investment opportunities. Consequently, we can expect that young SMEs depend on debt, once retained profits are exhausted, to meet their financing needs. The conclusions of Myers (1977) are particularly relevant. According to this author it is easier for creditors to monitor firms regarding repayment of short–term debt, compared with long–term debt. In addition, with short–term debt firms must pay off the principal and interest quickly, which forces them to be more disciplined in managing their resources. Young SMEs are subject to considerable financial stress in servicing their short–term debt (Fagiolo & Luzzi, 2006).

At the beginning of their life–cycle, firms have high rates of growth due to the need to reach a scale of efficiency that allows them to survive in the markets where they operate (Jovanovic, 1982). The need to finance the growth opportunities of young SMEs at the start of their life–cycle, the difficulties in generating internal finance, and the considerable problems they face in accessing external financing sources can contribute decisively to becoming excessively dependent on short–term debt (Petersen & Rajan, 1994). According to Pecking Order Theory, the financial deficits registered by young SMEs can lead to considerable variations of short–term debt due to their heavy dependence on it.

In addition, the SMEs’ high dependence on short–term debt and consequent need to often renegotiate its terms (Ortiz–Molina & Penas, 2008) can lead to considerable adjustments in levels of short–term debt. Those adjustments may not be a consequence of SMEs following the financing patterns predicted by Trade–Off Theory. In fact, young SMEs may make adjustments toward target short–term debt ratio due to their heavy dependence on this type of finance.

Given the limited reputation of young SMEs (Diamond, 1989), their limited credibility, and their low amount of tangible business assets (Berger & Udell, 1998), we can expect the problems of information asymmetry with creditors to considerably hinder access to long–term debt. Consequently, adjustments of long–term debt toward respective target ratio, as well as the impacts of financial deficit on variations of long–term debt may be of a reduced magnitude. When resorting to long–term debt, it is possible that neither the Pecking Order Theory nor the Trade–Off Theory are followed by young SMEs in their financing decisions.

At more advanced stages in the life–cycle of SMEs, we can expect that variations of short–term debt will not depend on financing needs. The effect of reputation (Diamond, 1989), credibility, and tangible assets (Berger & Udell, 1998) in old SMEs may afford these firms access to long–term financing sources. Therefore, old SMEs may have a greater possibility to choose between short– and long–term debt, turning to long–term debt more often than to short–term debt.

As a consequence of their greater age, old SMEs have a higher level of internal finance (Petersen & Rajan, 1994), and they are likely less exposed to financial stress in managing their resources (Auken & Carter, 1990). This is particularly important in allowing old SMEs greater freedom of choice between internal finance, short–term debt, and long–term debt. Consequently, old SMEs are able to set optimal levels of short– and long–term debt. On one hand, the lesser need to resort to short–term debt, and consequently lesser need to renegotiate its terms may imply that old SMEs have lower magnitude of adjustment of short–term debt toward target short–term debt ratio. On the other hand, old SMEs’ greater ability to obtain long–term debt can contribute to a greater magnitude of the adjustments of long–term debt toward target long–term debt ratio. Consequently, old SMEs may follow a financing behavior closer to that predicted by Trade–Off Theory than younger SMEs.

Based on the above, we formulate the following research hypotheses:

3. Methodology

3.1. Research Sample

This study uses the SABI (Sistema de Balanços Ibéricos—Analysis System of Iberian Balance Sheets) database supplied by Bureau van Dijk, for the period between 1999 and 2006. We select SMEs based on the recommendation of the European Union L124/36 (2003/361/CE). According to this recommendation, a firm is considered to be an SME when it meets two of the following criteria: (1) fewer than 250 employees; (2) annual balance sheet total not exceeding 43 million Euros; and (3) annual turnover not exceeding 50 million Euros. Initially we select SMEs that meet these three criteria.

Since one of this paper's main goals is to estimate SMEs’ adjustment of the actual level of short–term and long–term debt toward the respective target ratios, use of dynamic panel estimators is fundamental. According to Arellano and Bond (1991) firms must be present in the database for at least four consecutive years to be considered in the econometric analysis, and in the second–order autocorrelation tests that are essential to validate the robustness of results. This being so, we eliminate from the analysis all firms that are not in the database for at least four consecutive years.

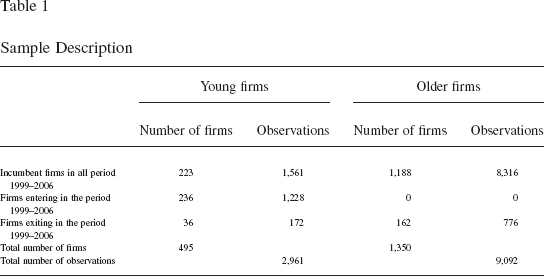

In order to solve the problem of possible sample bias and simultaneously have more representative samples of the Portuguese SME situation, we consider three types of firms: (1) SMEs belonging to the market for the entire period of analysis; (2) SMEs entering the market during the period of analysis; and (3) SMEs leaving the market during the period of analysis. Based on the above, and given that our objective is to study the influence of age on the financing decisions of Portuguese SMEs, we consider two sub–samples of Portuguese SMEs: (1) 495 young SMEs, of which 236 entered and 36 left the market during the period of analysis; and (2) 1,350 old SMEs, of which 162 left the market during the period of analysis. We consider as young SMEs those of up to 10 years of age at the end of the period of analysis, i.e., in 2006; considering as old those SMEs over 10 years of age at the end of the period of analysis. 1

Table 1 presents the structure of the sample used in this study.

Sample Description

Seeking to test the robustness of the empirical evidence, we use an alternative criterion of 10 years of age to separate young and old SMEs. The criterion consists of considering as young SMEs those entering the market in the period 1999–2006, considering the remainder as old SMEs. 2 The results obtained are presented in Appendix A, and show that the results do not depend on the 10–year cut–off.

3.2. Variables

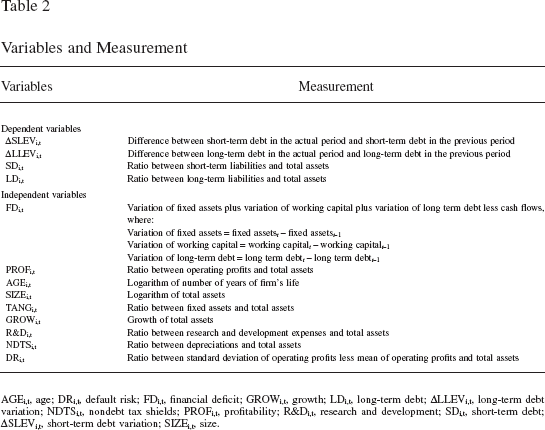

Table 2 presents the dependent and independent variables used in this study

Variables and Measurement

AGEi,t, age; DRi,t, default risk; FDi,t, financial deficit; GROWi,t, growth; LDi,t, long–term debt; ΔLLEVi,t, long–term debt variation; NDTSi,t, nondebt tax shields; PROFi,t, profitability; R&Di,t, research and development; SDi,t, short–term debt; ΔSLEVi,t, short–term debt variation; SIZEi,t, size.

Seeking to estimate the magnitude of the impacts of financial deficit on debt variations, we use as dependent variables: the variation of short–term debt (ΔSLEVi, t ), and the variation of long–term debt (ΔLLEVi, t ). In addition, in order to estimate the adjustment of actual debt toward target debt ratio, we use as dependent variables: the ratio of short–term debt (SDi, t ), and the ratio of long–term debt (LDi, t ).

To estimate the magnitude of the impacts of financial deficit on short– and long–term debt variations, we use as explanatory variable, financial deficit (FDi, t ).

As determinants of debt, this study considers the following variables: profitability (PROFi, t ), age (AGEi, t ), size (SIZEi, t ), asset structure (TANGi, t ), growth (GROWi, t ), research and development (R&Di, t ), nondebt tax shields (NDTSi, t ), and default risk (DRi, t ). These variables and their corresponding measures are in agreement with various empirical studies on SMEs’ capital structure, for example Michaelas, Chittenden, and Poutziouris (1999), Sogorb–Mira (2005), and López–Gracia and Sogorb–Mira (2008).

3.3. Estimation Method

Studying SMEs’ capital structure decisions, without correcting for possible sample bias as a result of not considering the situation of firms that left the market during the period of analysis, could lead to bias in the results, due to omission of the case of firms with survival difficulties, something which could be different from the case of firms with good survival possibilities.

The best way to solve this problem is by using the two–step estimation method proposed by Heckman (1979). In the first stage, considering all firms, both surviving and nonsurviving, we estimate probit regressions where the dependent variable has the value of 1 if the firm is in the market, and the value of 0 if it has left the market. In the second stage, to estimate the impacts of financial deficit on variations of short– and long–term debt, as well as adjustments of short– and long–term debt toward the respective optimal levels of debt, we calculate the inverse Mill's ratio, 3 and use it as an additional explanatory variable in the regressions, considering only surviving firms. In this way, we control efficiently for the possible consequences of bias in the resulting data. 4

The probit regressions to be estimated, corresponding to the first step, can be presented as follows:

where XK, i , t is the vector of the K independent variables used in the study; dt are annual dummy variables measuring the impact of alterations in the economic climate on the surviving likelihood; and zi, t is the error.

In the second step, after determining the inverse Mill's ratio for each of the observations, we consider it as an additional explanatory variable of variations of short– and long–term debt, as well as of the ratios of short– and long–term debt.

According to Pecking Order Theory, changes of firm capital structure are not due to searching for target debt ratio, but rather to the need for financing investment opportunities, when internal finance is exhausted. In this study, so that the survival issue does not have implications for the results obtained, we extend the model proposed by Shyam–Sunder and Myers (1999) including in addition to financial deficit, the inverse Mill's ratio as independent variable: 5

where ΔDi, t is the difference between debt in the current period and debt in the previous period, FDi, t is financial deficit, λi, t is the inverse Mill's ratio, and εi, t is the error, which is assumed to have normal distribution. According to Pecking Order Theory, we can expect that firms’ debt adjustments are a consequence of their financial deficit only, with the expectation that B ≈ 1 (Shyam–Sunder & Myers, 1999).

In order to estimate equation 2, we turn to OLS regressions for two fundamental reasons: (1) the nonexistence of the lagged dependent variable in the relationship forecast by equation 2 makes the use of dynamic estimators impossible; and (2) since the dependent variable is in first differences, nonobservable individual effects (vi) become irrelevant, and it is no use estimating the relationship forecast in equation 2 with panel models considering random or fixed nonobservable individual effects.

Given that heteroskedasticity is normally a relevant phenomenon in empirical studies that use cross–section data, standard deviations of the parameters are estimated according to the White estimator. This estimator allows us to obtain standard deviations of estimated parameters consistent with the possible existence of heteroskedasticity.

To estimate regressions regarding the adjustments of short– and long–term debt toward the respective target debt ratios, we use dynamic panel estimators. Advantages of dynamic estimators are the elimination of firms’ nonobservable individual effects, greater control of endogeneity, and greater control of collinearity between explanatory variables. Use of dynamic panel estimators also has the advantage of allowing determination of the level of adjustment of current debt toward a target debt ratio, according to the dynamic approach of capital structure decisions.

According to Trade–Off Theory, firms adjust their level of actual debt toward target debt ratio (Ang, 1976; Jalilvand & Harris, 1984; Lev & Peckelman, 1975; Taggart, 1977). The process of adjustment can be described as follows: 6

in which: Di, t is the debt ratio of firm i in the period t, Di,t−1 is the debt ratio of firm i in the period t–1, Di,t* is the target debt ratio of firm i in the period t, and α is the speed of adjustment of actual debt ratio toward target debt ratio, in which 0 ≤ α ≤ 1.

If α = 1, then Di,t = Di,t*, the current level of debt being equal to the optimal level of debt. In these circumstances, firms manage to find the optimal debt ratio, transaction costs being nil. On the contrary, if α = 0, then Di, t = Di, t −1, transaction costs being very high in these circumstances. The higher the parameter α, the lower transaction costs will be, and moderately low levels of α mean the existence of high transaction costs.

As mentioned by De Miguel and Pindado (2001), Ozkan (2001), Fama and French (2002), and Gaud, Jani, Hoesli, and Bender (2005), the level of optimal debt ratio depends on the specific characteristics of firms, which is to say, on the determinants considered to be relevant in explaining debt. Therefore, the optimal level of debt is given by:

where: Y is the vector of the determinants of debt used in this study, vi are nonobservable individual effects, and ei, t is the error, which is assumed to have normal distribution.

Substituting (4) in (3), and solving to the order of Di, t , this gives:

where: β0 = αγ0, δ = (1 − α), βK = αγK, θt = αdt, ηi = αvi, εi, t = αei, t .

To estimate equation 5 on the basis of traditional panel methods, considering fixed or random individual effects, we obtain biased and inconsistent estimates of the parameters, since besides there being correlation between ηi and Di, t −1 there is also correlation between εi, t and Di, t −1, which is to say, firm's nonobservable individual effects and the error are correlated with the lagged debt. In addition, using dynamic estimators rather than traditional panel methods has the following extra advantages: (1) greater control of endogeny; (2) greater control of possible collinearity between explanatory variables; and (3) greater effectiveness in controlling effects caused by the absence of relevant explanatory variables for the results.

Blundell and Bond (1998) conclude that when the dependent variable is persistent, 7 and the number of periods is not very high, the GMM 8 (1991) estimator generates results not robust. Therefore, considering that debt is normally characterized by high persistence, i.e., by a high correlation between debt in the current and previous periods, in this study we opt to use the GMM system (1998) estimator in order to correctly estimate the adjustments of short– and long–term debt in young and old SME towards the respective optimal levels.

However, the GMM system (1998) estimator can only be considered valid on two conditions: (1) if the restrictions created, a consequence of using the instruments, are valid; and (2) there is no second–order autocorrelation.

The Hansen test assesses the validity of the restrictions of the GMM system (1998) estimator. The null hypothesis indicates that the restrictions imposed by using the instruments are valid, while the alternative hypothesis shows that the restrictions are not valid. By rejecting the null hypothesis, the conclusion is that the results are not robust.

We test for the existence of first– and second–order autocorrelation. The null hypothesis refers to the existence of autocorrelation, while the alternative hypothesis regards the inexistence of autocorrelation. By rejecting the null hypothesis of nonexistence of second–order autocorrelation, the conclusion is that the results are not robust.

By not rejecting the null hypothesis, that the restrictions imposed by using the instruments are valid, and not rejecting the null hypothesis that no autocorrelation exists, the conclusion is that the results are robust.

We use the Chow test in order to test whether the impacts of financial deficit on variations of short– and long–term debt, and adjustments of short– and long–term debt toward the respective target ratios, are different for young and old SMEs.

4. Results

4.1. Descriptive Statistics

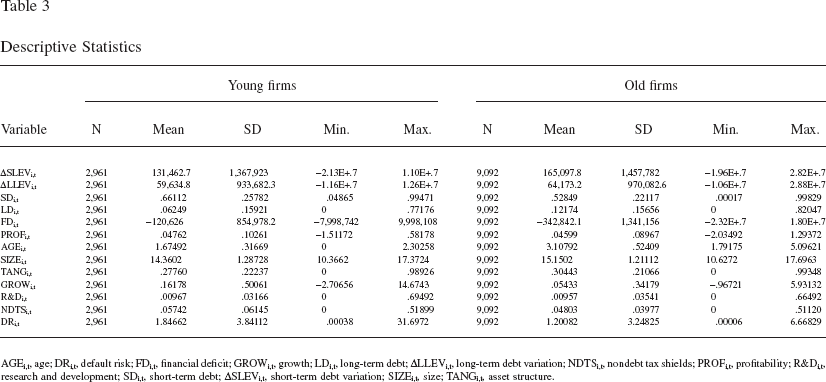

Table 3 presents the results of the descriptive statistics referring to the dependent and independent variables used in this study, for young and old SMEs.

Descriptive Statistics

AGEi,t, age; DRi,t, default risk; FDi,t, financial deficit; GROWi,t, growth; LDi,t, long–term debt; ΔLLEVi,t, long–term debt variation; NDTSi,t, nondebt tax shields; PROFi,t, profitability; R&Di,t, research and development; SDi,t, short–term debt; ΔSLEVi,t, short–term debt variation; SIZEi,t, size; TANGi,t, asset structure.

Average level of short–term debt is higher for young SMEs (.65023) than for old SMEs (.52849). On the contrary, average level of long–term debt is higher for old SMEs (.12174) than for young SMEs (.06249). The results of the descriptive statistics indicate greater dependency of young SMEs on short–term debt, while older SMEs have on average higher long–term debt. 9

4.2. Survival Analysis

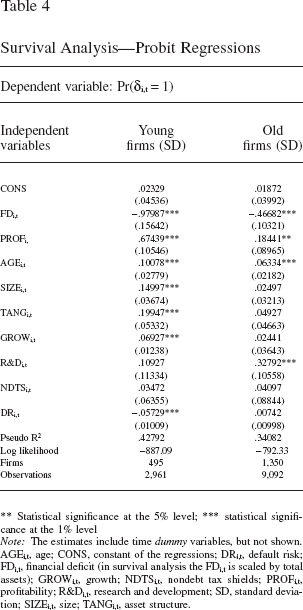

Table 4 presents the empirical evidence regarding the survival analysis.

Survival Analysis—Probit Regressions

Statistical significance at the 5% level;

statistical significance at the 1% level

Note: The estimates include time dummy variables, but not shown.

AGEi,t, age; CONS, constant of the regressions; DRi,t, default risk; FDi,t, financial deficit (in survival analysis the FDi,t is scaled by total assets); GROWi,t, growth; NDTSi,t, nondebt tax shields; PROFi,t, profitability; R&Di,t, research and development; SD, standard deviation; SIZEi,t, size; TANGi,t, asset structure.

We can state that in the case of young SMEs: (1) profitability, size, asset tangibility, growth, and age contribute positively to the probability of survival; and (2) risk and financial deficit contribute negatively to the probability of survival. As for old SMEs: (1) profitability, R&D, and age contribute positively to the probability of survival; and (2) financial deficit contributes negatively to the probability of survival.

4.3. Impacts of Financial Deficit on Variations of Debt

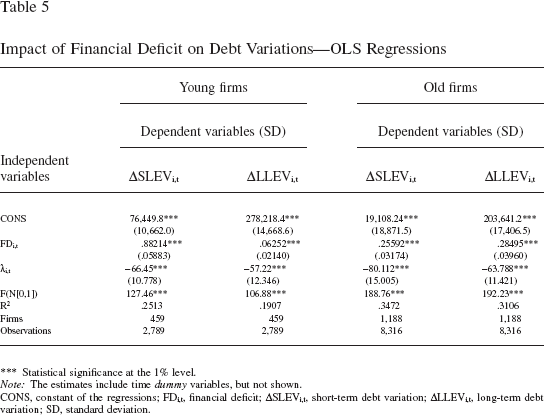

Table 5 presents the results referring to the impacts of financial deficit on short– and long–term debt variations. 10

Impact of Financial Deficit on Debt Variations—OLS Regressions

Statistical significance at the 1% level.

Note: The estimates include time dummy variables, but not shown.

CONS, constant of the regressions; FDi,t, financial deficit; ΔSLEVi,t, short–term debt variation; ΔLLEVi,t, long–term debt variation; SD, standard deviation.

The results obtained allow us to conclude that, for young and old SMEs, financing needs, translated as financial deficit, are important for variations found in their levels of short– and long–term debt.

We also find that the relationship between the inverse Mill's ratio and variations of short– and long–term debt are statistically significant. If the estimated parameters are negative, then the lack of inverse Mill's ratio in the regressions would imply an over evaluation of the parameters that measure the relationship between the financial deficit and the variations of the short–term debt and long–term debt of young and old SMEs. Using the inverse Mill's ratio is appropriate to solve the problem of biases of the results as a consequence of SMEs’ survival.

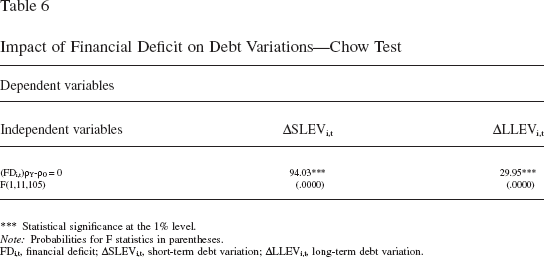

Next, Table 6 presents the results of the Chow test of differences between young and old SMEs for the impacts of financial deficit on short– and long–term debt.

Impact of Financial Deficit on Debt Variations—Chow Test

Statistical significance at the 1% level.

Note: Probabilities for F statistics in parentheses.

FDi,t, financial deficit; ΔSLEVi,t, short–term debt variation; ΔLLEVi,t, long–term debt variation.

Whatever the type of debt considered, short or long term, the results of the Chow test indicate rejection of the null hypothesis of equality of estimated parameters, and so we can conclude that financial deficit has different impacts on variations of short– and long–term debt, according to SMEs being young or old.

4.4. Adjustment of Current Debt toward Target Debt Ratio and Debt Determinants

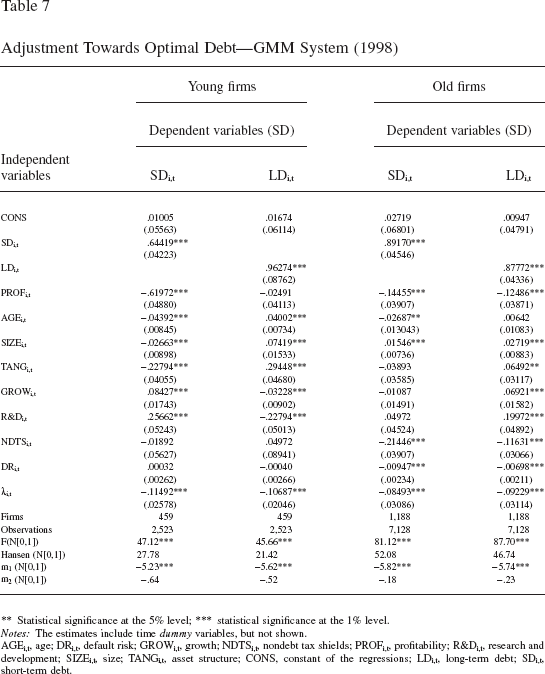

Next we present the results referring to adjustments of short– and long–term debt of young and old SMEs toward the respective target debt ratios. In addition, we present the results regarding the relationships established between the determinants considered previously and short– and long–term debt. The results are presented in Table 7. 11

Adjustment Towards Optimal Debt—GMM System (1998)

Statistical significance at the 5% level;

statistical significance at the 1% level.

Notes: The estimates include time dummy variables, but not shown.

AGEi,t, age; DRi,t, default risk; GROWi,t, growth; NDTSi,t, nondebt tax shields; PROFi,t, profitability; R&Di,t, research and development; SIZEi,t, size; TANGi,t, asset structure; CONS, constant of the regressions; LDi,t, long–term debt; SDi,t, short–term debt.

We can state that, whatever the type of debt considered, short– or long–term debt, young and old SMEs adjust their debt toward target debt ratio.

Regarding the relationships between determinants and short– and long–term debt, we find that there are different relationships according to whether young or old SMEs are the unit of analysis.

In addition to what has already been said, it is worth highlighting that the relationships between the inverse Mill's ratio and short– and long–term debt ratios are statistically significant, whether taking young or old SMEs as the unit of analysis.

The estimated parameters are negative, thus the exclusion of the inverse Mill's ratio in the regressions would imply an over evaluation of adjustments of short–term debt and long–term debt toward the respective optimal levels, as well as of the coefficients that measure the relationships between determinants and short–term debt and long–term debt. We can therefore conclude that use of the inverse Mill's ratio is proven to be efficient in correcting possible bias in the results as a consequence of SME survival.

Whether considering young or old SMEs, results of the Hansen test indicate that we cannot reject the null hypothesis of validity of the instruments used. Besides, for both young SMEs and old SMEs, we cannot reject the null hypothesis of absence of second–order autocorrelation. Given the validity of the instruments used and absence of second–order autocorrelation, we can conclude that the results of the GMM system (1998) dynamic estimator are robust, whether considering young or old SMEs.

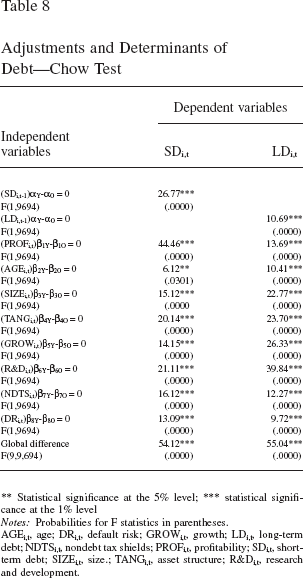

In Table 8, we present the results of the Chow test of possible differences in the estimated parameters for young and old SMEs, regarding the adjustments of short– and long–term debt toward respective target levels, and also for the relationships between determinants and short– and long–term debt.

Adjustments and Determinants of Debt—Chow Test

Statistical significance at the 5% level;

statistical significance at the 1% level

Notes: Probabilities for F statistics in parentheses.

AGEi,t, age; DRi,t, default risk; GROWi,t, growth; LDi,t, long–term debt; NDTSi,t, nondebt tax shields; PROFi,t, profitability; SDi,t, short–term debt; SIZEi,t, size.; TANGi,t, asset structure; R&Di,t, research and development.

On the basis of the results obtained for all estimated parameters, we reject the null hypothesis regarding the equality of parameters for young and old SMEs. The results of the global Chow tests, whatever the type of debt considered, confirm those differences.

5. Discussion of the Results

According to the results of this study, the variations of short– and long–term debt in young and old SMEs are influenced by financing needs, i.e., by the financial deficit existing at a given time. The magnitude of the impact of financial deficit on the variation of short–term debt is greater for young SMEs (BYSD = 0.88214) than for old SMEs (BOSD = 0.25592). However, the impact of financial deficit on the variation of long–term debt is greater for old SMEs (BOLD = 0.28495) than for young SMEs (BYLD = 0.06252). The results of the Chow test indicate that the magnitudes of the estimated parameters are different in the case of young and old SMEs. We therefore accept hypotheses 1 and 2 as valid, since young SMEs have a greater magnitude of the impact of financial deficit on variations of short–term debt than older SMEs, the opposite being found regarding the impact of financial deficit on the variation of long–term debt. 12

Additionally, financial deficit has a considerable impact on the variation of short–term debt in young SMEs, but it has a limited impact on variation of long–term debt (BYSD = 0.88214 > BYLD = 0.06252), suggesting that these firms face difficulties in obtaining long–term debt.

Turning to old SMEs, when internal funds are insufficient, we can conclude that there is a balance between resorting to short– and long–term debt. We even find that old SMEs turn more to long–term debt than short–term debt in order to meet financing needs (BOLD = 0.28495 > BOCP = 0.25592). These results show that young SMEs have greater dependence on short–term debt, and old SMEs have greater possibility to obtain long–term debt. These results now estimated confirm the results of the descriptive statistics according to which young SMEs have higher average short–term debt than old SMEs, whereas old SMEs have higher average long–term debt than young SMEs.

Pecking Order Theory predicts that due to costs of asymmetric information, firms prefer internal finance to external funds and debt to equity (Chittenden, Hall, & Hutchinson, 1996; Holmes & Kent, 1991; Michaelas et al., 1999; Myers, 1984). Frank and Goyal (2003) argue that according to the forecasts of Pecking Order Theory, a firm first issues debt with the lowest information costs after internal finance is exhausted. This suggests that short–term debt should be exhausted before the firm resorts to long–term debt. In this context, the financing behavior of young Portuguese SMEs seems to follow the Pecking Order Theory, because when internal finance is exhausted, these firms are dependent on short–term debt, probably as a consequence of the difficulty in accessing long–term financing sources, which corroborates the results of other studies (García–Teruel & Martínez–Solano, 2007; La Rocca et al., 2009; Peterson & Shulman, 1987).

Greater reputation (Diamond, 1989), credibility, and more tangible assets (Berger & Udell, 1998), as a consequence of increased age, appear to contribute to lessening the problems of information asymmetry for older SMEs. Consequently, older SMEs have access to more diversified external financing sources, namely long–term debt sources, corroborating the conclusions of Ang (1991) regarding age as a determinant for SMEs’ possibility to increase long–term debt, allowing firms to avoid an excessive dependence on short–term debt.

We find that young and old SMEs adjust the level of their short– and long–term debt toward the respective target debt ratios. Adjustment of short–term debt toward the respective target ratio is greater for young SMEs (αYSD = 0.35581) than that found for old SMEs (αOSD = 0.10830). As for adjustment of long–term debt toward the respective optimal level, we find that it is greater for old SMEs (αOLD = 0.12228) than for young SMEs (αYLD = 0.03726). 13 Also in these circumstances, the results of the Chow test indicate that adjustments are of a different magnitude in young and old SMEs. The results obtained in this study allow us to corroborate the hypotheses 3 and 4, since young SMEs have a greater magnitude of adjustment of short–term debt toward the respective optimal level than older SMEs, the opposite being found regarding adjustments of long–term debt toward the respective target levels for young and old SMEs. 14

In addition to what has been stated, we find that for young SMEs the adjustment of short–term debt toward target ratio is considerably greater than the adjustment of long–term debt (αYSD = 0.35581 > αYLD = 0.03726). The magnitude of the adjustment of short–term debt toward short–term optimal debt ratio suggests that the costs of debt adjustments toward the target short–term debt ratio are lower than the costs of financial imbalance for young SMEs. This result is likely due to the high dependence of young SMEs on short–term debt to finance investment opportunities that leads to the need for regular adjustments toward the target short–term debt ratio due to the need to frequently renegotiate the terms of the short–term debt. This being so, the considerable debt adjustments toward target short–term debt ratio of young SMEs may not be the consequence of following the dictates of the Trade–Off Theory, which implies reaching an optimal level of short–term debt. These adjustments seem to be a consequence of the difficulty in gaining long term external financing sources, translating into a strong dependence on short–term debt in response to the impending financial needs associated with young SMEs’ investment opportunities, when internal funds are insufficient for the purpose. However, young Portuguese SMEs’ dependence on short–term debt can cause excessive financial stress (due to the very short time for paying off the debt and charges) possibly preventing young SMEs from making efficient use of good investment opportunities (Fagiolo & Luzzi, 2006).

The adjustment of long–term debt toward the optimal level is quite limited in young SMEs. The costs of adjustment toward target long–term debt ratio borne by young SMEs appear to be higher than the costs of financial imbalance. It is worth noting that these firms present a low level of long–term debt, reinforcing the previous conclusion regarding the impossibility of young SMEs to access long–term financing sources due to the problems of information asymmetry with creditors.

Different results are obtained regarding the adjustments of short– and long–term debt toward the respective target ratios for old SMEs. In these firms, the adjustment of long–term debt is greater than the adjustment of short–term debt (αOLD = 0.12228 > αOSD = 0.10830). This result is particularly relevant because it suggests that old SMEs, first, do not need to frequently renegotiate the terms of short–term debt, and second, are able to adjust to a greater extent long–term debt toward target ratio, suggesting that the costs of adjustment toward the optimal level of long–term debt are lower than the costs deviating from financial balance. In this context, old SMEs’ patterns of financing may be in agreement with Trade–Off Theory, since these firms seem to orient their financing decisions toward target ratios of short– and long–term debt.

Sources of finance for Portuguese SMEs are scarce, since in addition to the limited development of the Portuguese stock market, the majority of Portuguese SMEs do not meet the minimum requirements to be listed. In addition, Portuguese SMEs face obstacles in accessing alternative equity sources such as risk capital or business angels.

The Portuguese SMEs’ lack of access to equity sources may explain SMEs’ high dependence on debt in the absence of internal finance, which is in accordance with other studies (Fagiolo & Luzzi, 2006; Robb, 2002; Robb & Robinson, 2009). Additionally, the results of the current study regarding young SMEs’ dependency on short–term debt corroborates the conclusion of Robb about younger firms depending more on credit from financial institutions than older firms. Portuguese young SMEs face problems in obtaining long–term debt, a consequence of the obstacles in accessing external capital sources, but at later stages of the Portuguese SMEs’ life–cycle, when age allow firms to mitigate the problems of asymmetric information (Berger & Udell, 1998; Diamond, 1989), do these firms have greater access to long–term debt, and they do obtain better terms in securing long–term debt.

The relationships between the determinants previously considered in this study and short– and long–term debt in the context of young and old SMEs, 15 confirm, first, that the young SMEs’ difficulty in accessing external financing sources makes them dependent on short–term debt, and second, that old SMEs enjoy greater possibilities in obtaining long–term debt, suggesting the possibility to access more diversified sources of finance. In addition, the results of the Chow test indicate, for all the determinants considered, rejection of the null hypothesis of equality of the estimated parameters measuring the relationships between determinants and short– and long–term debt for young and old SMEs. This empirical evidence confirms that age has considerable influence on the SMEs’ financing decisions.

Greater profitability of old SMEs means reduced use of short– and long–term debt. However, it should be noted that: young SMEs with greater profitability reduce the level of short–term debt 16 in a greater proportion than old SMEs; and, young SMEs with greater profitability do not reduce their level of long–term debt, unlike old SMEs. These results suggest that the most profitable young SMEs do not replace long–term debt with internal finance, as a probable consequence of the need for long–term debt to finance good investment opportunities, 17 which is expected considering the previous results that suggest obstacles in accessing long–term financing sources.

Greater age, greater size, and higher levels of tangible assets are determinant factors for young SMEs to increase the use of long–term debt, and to diminish their level of short–term debt. At the beginning of SMEs’ life–cycle, age is normally associated with size, since SMEs are growing. At later stages of the life–cycle, in general SMEs’ rates of growth diminish, and greater size is not necessarily associated with greater age. This is what seems to happen in the case of Portuguese SMEs, 18 given that young SMEs increase the use of long–term debt, becoming less dependent on short–term debt. Simultaneous increase of age and size therefore seem to be fundamental for diminishing problems of information asymmetry.

For old SMEs, the determinants age, size, and tangible assets seem to have less relative importance in reducing the problems of information asymmetry, 19 since: (1) greater age contributes to reduced use of short–term debt, it does not contribute to increased long–term debt; and (2) greater size and higher levels of tangible assets, although contributing to greater use of long–term debt, do not mean reduced use of short–term debt.

Regarding the determinants of growth and growth opportunities, 20 we find that young SMEs with higher levels of growth and growth opportunities resort more to short–term debt, with reduced levels of long–term debt, reinforcing the results already obtained regarding the obstacles faced by young SMEs in obtaining long–term debt.

Old SMEs with higher levels of growth and growth opportunities have higher levels of long–term debt, reducing dependence on short–term debt to finance their growth and growth opportunities. 21 This result suggest that the effects of reputation (Diamond, 1989), credibility, and level of tangible assets (Berger & Udell, 1998), associated with greater age, are particularly important in diminishing the problems of information asymmetry, allowing old SMEs to obtain credit on better terms.

It is important to mention that size and growth are relevant determinants for the survival of young SMEs, 22 but not for old SMEs. This result is particularly important as it shows how important it can be to quickly reach a minimum scale of efficiency, for young SMEs to survive. However, when internal finance is insufficient, the credit restrictions that young SMEs face can imply the impossibility to finance good investment opportunities, which contributes to jeopardizing their survival.

Finally, the relationships identified between the determinants of nondebt tax shields and risk, and the short– and long–term debt of young and old SMEs allow us to draw important conclusions about the influence of age on the financing decisions of SMEs: (1) nondebt tax shields and risk are not determinants of the short– and long–term debt of young SMEs; and (2) on the contrary, old SMEs with greater nondebt tax shields and greater risk turn less to short– and long–term debt. These results reinforce the previous conclusion regarding the old SMEs following the Trade–Off Theory, i.e., these firms establish a trade–off between debt tax–shields and bankruptcy costs associated of debt, which is not verified for young SMEs. 23

6. Conclusions and Implications

Considering two sub–samples of Portuguese SMEs: (1) 495 young SMEs; and (2) 1,350 old SMEs, and using various panel data models, this paper investigates whether age is an important determinant of SMEs’ financing decisions.

The results obtained in this study allow us to conclude that age is a determinant of SMEs’ financing decisions, given that: (1) the impact of financial deficit on the variation of short–term debt and the adjustment of short–term debt toward target ratio are of greater magnitude for young SMEs than for old SMEs; (2) the impact of financial deficit on the variation of long–term debt and the adjustment of long–term debt toward target ratio are of greater magnitude for old SMEs than for young SMEs; and (3) there are considerable differences in the relationships between determinants and short– and long–term debt for young and old SMEs.

The empirical evidence obtained in this study allows us to make two specific contributions to the literature on capital structure in SMEs. First, the considerable adjustment of short–term debt toward target ratio of young SMEs seems to be a consequence of the need to turn to short–term debt arising from problems of information asymmetry, and consequently the difficulty in accessing long–term financing sources. So, those frequent adjustments do not seem to come from the young SMEs’ aim to reach an optimal level of short–term debt. The results suggest that, due to the difficulty in accessing long–term financing sources, young SMEs are more likely to follow Pecking Order Theory than what is predicted by Trade–Off Theory.

Second, the effects of reputation, credibility, and level of tangible business assets resulting from greater age are fundamental in lessening the problems of information asymmetry, allowing the access to long–term debt and consequently less dependence on short–term debt. This can be fundamental for small firms to be able to include in their strategies the goal of reaching optimal levels of short– and long–term debt. Thus, for old SMEs, financial behavior appears to be closer to that predicted by Trade–Off Theory than to what is predicted by Pecking Order Theory.

The results obtained for young SMEs and for old SMEs show that Trade–Off Theory and Pecking Order Theory should not be considered to be mutually exclusive, bearing in mind that both theories are necessary to understand the capital structure decisions of SMEs throughout their life–cycle. A firm's age can be particularly important for diminishing the problems of information asymmetry: at the beginning of the SME life–cycle, Pecking Order Theory seems to be particularly important in explaining capital structure decisions; at more advanced stages of the SME life–cycle, Trade–Off Theory becomes more important in explaining SMEs’ capital structure decisions.

Portugal has a bank–based financial system with an undeveloped stock market, where the majority of SMEs do not achieve quotation. This situation, added to the obstacles to firms in accessing alternative equity sources (namely risk capital and business angels), considerably limits Portuguese SMEs’ diversification of finance sources. Therefore, on the basis of the results of this study, which suggest that debt is almost the only external capital source available to SMEs, we suggest to policy makers the following measure to support young SMEs: considering that growth and investment in innovation are fundamental for young SMEs to be able to reach a minimum scale of efficiency, which is fundamental for firms’ survival, and also that young SMEs are restrained in accessing long–term financing sources, which implies firms’ dependence on short–term debt, it would be advisable to give effective long–term financial support to young SMEs, in order to promote their growth and innovative activities.

For future research, we suggest to study SMEs’ capital structure decisions, incorporating research variables to measure the level of difficulty in obtaining external capital. The purpose will be to determine how the level of difficulty in accessing external financing sources influences SMEs’ financing decisions to follow the Pecking Order Theory or the dynamic Trade–Off Theory.

Footnotes

1.

The 10–year cut–off is used in various studies of SMEs, such as Hyytinen and Pajarinen (2004), Oliveira and Fortunato (2006), Ferrando, Köhler–Ulbrich, and Pál (2007) and La Rocca et al. (2009).

2.

According to the alternative criterion we consider as young SMEs those of up to 7 years of age, considering as old SMEs those over 7 years of age. Robb and Robinson (2009) consider young SMEs up to a maximum of 5 years of age. In this study, use of dynamic estimators, with the consequent need for SMEs to be in the sample for a minimum of four consecutive years so as to validate the second–order autocorrelation tests, recommends use of an alternative criterion with a higher maximum age to be classified as young SMEs. However, our alternative criterion is similar to the one used by Robb and Robinson (2009) since, by considering as young SMEs those entering the market in the period 1999–2006, their maximum age is 7. The alternative criterion used in this study is also quite similar to that used by Steffens, Davidsson, and Fitzsimmons (2009), these authors classifying as young SMEs those up to 8 years of age, classifying as old SMEs those over 8 years old.

3.

The inverse Mill's ratio is the ratio between cumulative density function and the density function. The designation of inverse Mill's ratio is due to the fact that Mill's ratio considers the inverse of hazard ratio (also known as force of mortality). For a detailed description of calculation of the inverse Mill's ratio, see Heckman (1979).

4.

Given that the inverse Mill's ratio is calculated on the basis of the survival probability, we may estimate the regressions regarding the impacts of financial deficit on the variations of short–term and long–term debt, as well as the regressions regarding the adjustments of short–term and long term–debt toward respective, optimal levels, considering only the surviving firms, since the possible effects of the probability of firms’ bankruptcy on the estimated results are measured by the inverse Mill's ratio.

5.

ΔDi, t represents variations in debt in general, which in the specific case of this study represents variations in short– and long–term debt.

6.

D represents debt in general, which in the specific case of this study represents short–term debt and long–term debt.

7.

A variable is persistent when there is a high correlation between its values in the current and previous periods.

8.

Generalized Method of Moments.

9.

We use the t–test to obtain the differences of average values of short–term debt and long–term debt for young and old SMEs. Regarding the t–test for the difference between young and old SMEs for the average value of short–term debt, we have obtained t = 2.742, with a probability of .006. The difference between young and old SMEs for the average value of long–term debt was tested with the t–test, which has the value t = 3.936, with a probability of .000. Thus, we have identified significant statistical differences between young and old SMEs for the average values of short–term debt and long–term debt. Young SMEs, are on average more dependent on short–term debt than old SMEs, since these last firms have more access to long–term debt.

10.

In Appendix A, Table A1, we present the results obtained using an alternative criterion for separating young and old SMEs, already presented in the methodology section. The results, concerning the magnitude, signal, and statistical significance of the estimated parameters, are similar to those obtained in ![]() , which confirms the robustness of the empirical evidence obtained in this study. In Appendix B, Table B1, we present the results referring to the impact of financial deficit on variation of the total debt of young and old SMEs.

, which confirms the robustness of the empirical evidence obtained in this study. In Appendix B, Table B1, we present the results referring to the impact of financial deficit on variation of the total debt of young and old SMEs.

11.

In Appendix A, Table A2, we present the results obtained, with the GMM system (1998) estimator, using an alternative criterion for separating young and old SMEs, the criterion already presented in Section 3. Concerning the magnitude, sign, and statistical significance of the estimated parameters, the results confirm those presented in ![]() , which confirms the robustness of the empirical evidence obtained in this study. In Appendix B, Table B2, we present the results referring to adjustments of the total debt of young and old SMEs toward the respective target ratios, and also the relationships between the total debt of young and old SMEs and the determinants previously considered in this study.

, which confirms the robustness of the empirical evidence obtained in this study. In Appendix B, Table B2, we present the results referring to adjustments of the total debt of young and old SMEs toward the respective target ratios, and also the relationships between the total debt of young and old SMEs and the determinants previously considered in this study.

12.

The results presented in Appendix B, Table B1, indicate that the impact of financial deficit on variation of the total debt of young SMEs is BYTD = 0.94467, and BOTD = 0.54087 in the case of old SMEs. The greater magnitude of the impact of financial deficit on variation of the total debt of young SMEs, compared to that found in the case of old SMEs, is clearly due to the considerable magnitude of the impact of financial deficit on variation of short–term debt in young SMEs.

13.

The adjustments of short–term debt and long–term debt of young and old SMEs are calculated on the basis of the estimated parameters that measure the relationship between the short–term debt and the long–term debt in current and previous periods, and those adjustments are calculated using ![]() . For example, in Table 7, we verify that the parameter estimated for the relationship between debt of the current period and the debt of the previous period is .64419, i.e, δ = 0.64419. As presented below equation 5, δ = (1 − α), thus the adjustment of short–term debt toward optimal debt level is αYSD = 0.35581 for young SMEs. An identical process is followed to obtain the estimation of the adjustment of long–term debt toward respective optimal levels for young SMEs as well as for the adjustments of short–term debt and long–term debt toward the respective optimal levels for old SMEs.

. For example, in Table 7, we verify that the parameter estimated for the relationship between debt of the current period and the debt of the previous period is .64419, i.e, δ = 0.64419. As presented below equation 5, δ = (1 − α), thus the adjustment of short–term debt toward optimal debt level is αYSD = 0.35581 for young SMEs. An identical process is followed to obtain the estimation of the adjustment of long–term debt toward respective optimal levels for young SMEs as well as for the adjustments of short–term debt and long–term debt toward the respective optimal levels for old SMEs.

14.

The results presented in Appendix B, Table B2, indicate that the adjustment of total debt towards target ratio is αYTD = 0.39307 in young SMEs and αOTD = 0.23058 in old SMEs. The greater magnitude of adjustment of the total debt toward target ratio of young SMEs, compared to adjustment of the total debt of old SMEs is a consequence of the cons

15.

16.

17.

Michaelas et al. (1999), for British SMEs in general, and Sogorb–Mira (2005), for Spanish SMEs in general, find negative relationships between profitability and short– and long–term debt. We find that long–term debt can have greater relative importance for young Portuguese SMEs than for SMEs in general in the United Kingdom and Spain.

18.

We calculate the correlation coefficients between age and size in the case of young and old Portuguese SMEs. For young Portuguese SMEs the correlation coefficient between age and size is positive and statistically significant (.2789). In the case of old Portuguese SMEs the correlation coefficient between age and size is negative and not statistically significant (−.0104).

19.

Michaelas et al. (1999), for British SMEs in general, find that: (1) greater age means diminished short– and long–term debt; (2) greater size contributes to increased access to long–term debt and to diminished access to short–term debt; and (3) higher levels of tangible assets contribute to increased access to short– and long–term debt. In turn, Sogorb–Mira (2005), for Spanish SMEs in general, finds that: (1) greater size contributes to increased long–term debt, but does not contribute to either diminished or increased short–term debt; and (2) higher levels of tangible assets mean increased access to long–term debt and diminished access to short–term debt. We can state that the determinants of age, size, and level of tangible assets have greater relative importance for young Portuguese SMEs replacing access to short–term debt with access to long–term debt than is the case for old Portuguese SMEs or for SMEs in general in the United Kingdom and Spain. This may be a consequence of the considerable problems of information asymmetry and moral hazard young Portuguese SMEs face in their relationships with creditors.

20.

In this study we measure SMEs’ growth opportunities by intensity of R&D expenditure.

21.

Michaelas et al. (1999), for British SMEs in general, find that greater growth and greater growth opportunities contribute to increased use of short– and long–term debt. Sogorb–Mira (2005) for Spanish SMEs in general, concludes that greater growth opportunities contribute to increased use of long–term debt and diminished use of short–term debt. Compared to what occurs in the case of old Portuguese SMEs and for SMEs in general in the United Kingdom and Spain, problems of information asymmetry and moral hazard in the relationships between SME owners/managers and creditors seem to be more relevant in the case of young Portuguese SMEs. This happens because, when internal funds are not sufficient, they cannot finance their growth and growth opportunities resorting to long–term debt.

23.

For British SMEs in general, Michaelas et al. (1999) find that greater nondebt tax shields mean less long–term debt, having no effect on short–term debt. Regarding the effect of risk, the authors find a positive influence on short– and long–term debt, although of little significance in the case of long–term debt. In turn, Sogorb–Mira (2005), for Spanish SMEs in general, finds that greater nondebt tax shields mean diminished short– and long–term debt. The fact that nondebt tax shields and risk do not contribute to diminished levels of short– and long–term debt in young Portuguese SMEs shows that this type of SME considers less the possibility of reaching an optimal level of short– and long–term debt that corresponds to maximizing tax benefits and minimizing bankruptcy costs, compared to what happens in the case of old Portuguese SMEs and in British and Spanish SMEs in general.