Abstract

This study examines the relationships among angel investor–entrepreneur relationship conflicts, task conflicts, and goal conflicts on the one hand and their intentions to exit on the other. I evaluate the hypotheses with survey data from 65 angel investors and 72 entrepreneurs belonging to 54 ventures located in either California or Belgium. Regression analyses indicate that entrepreneurial intentions to exit are higher for entrepreneurs who face more task and goal conflicts. Angel investors’ intentions to exit are only increased when faced with more goal conflicts. Together, these results indicate the importance of taking into account investor–entrepreneur relations when studying their respective exit processes.

Introduction

For decades, scholars have argued that exit represents one of the key events in the relationship between external investors and entrepreneurs (Black & Gilson, 1998; Mason, 2006). In line with the broader literature on the investor–investee dyad (Lockett, Ucbasaran, & Butler, 2006), exit studies have generally investigated the topic from either the investor's (e.g., Mason & Harrison, 2002; Parhankangas & Landström, 2006; Van Osnabrugge, 2000) or the entrepreneur's standpoint (e.g., DeTienne & Cardon, 2010; Wennberg, Wiklund, DeTienne, & Cardon, 2010). With regard to investor exit, scholars have advanced our understanding of investor preferences in terms of how (e.g., IPO, acquisition, trade sale) and when to exit, determinants of these exit preferences, and the role of contracts in the exit decision (Cumming & MacIntosh, 2003; Freear, Sohl, & Wetzel, 2002; Hellmann, 2006; Mason & Harrison). Similarly, entrepreneurial exit research has provided some insight into the influence of venture performance and entrepreneurs'/founders’ characteristics on the decision of why and how to exit ventures (Boeker & Karichalil, 2002; DeTienne & Cardon; Ucbasaran, Lockett, Wright, & Westhead, 2003; Wennberg et al.).

What both streams of literature have in common is that they have generally depicted entrepreneurs and investors as independent actors. As a result, the context in which these parties are embedded has been neglected. However, previous research has indicated that investigating the nature and social aspects of exchange relationships, including investor–entrepreneur relationships (De Clercq & Sapienza, 2006; Lockett et al., 2006), is crucial to gain a better understanding of their effectiveness (Granovetter, 1985). The relationship between investors and entrepreneurs may be especially important for one specific class of equity investors, namely angel investors, given their concern for agency risk, and resulting emphasis on post–investment involvement (Fiet, 1995; Van Osnabrugge, 2000). Some have even argued that this relationship is the primary means through which angel investors add value (Freear, Sohl, & Wetzel, 1995; Politis, 2008).

I focus on one specific aspect of the angel investor–entrepreneur partnership: their relationship, task, and goal conflicts. A growing body of research has recognized that the angel investor–entrepreneur relationship is not always rosy (Brettel, 2003; Mason & Harrison, 1996). To our knowledge, no empirical work has examined angel investor–entrepreneur conflicts and very little work has addressed conflicts between venture capitalists and entrepreneurs (see Higashide & Birley, 2002; Parhankangas & Landström, 2006; and Yitshaki, 2008, for some of this work). Given that conflict is a clear stressor (Bayazit & Mannix, 2003), conflict theory should provide a useful lens to examine individual investor or entrepreneurial exit.

Task and relationship conflicts are commonly used in studies on intragroup conflict (De Dreu & Weingart, 2003; Jehn & Bendersky, 2003), and as such, have also found their way to the entrepreneurship literature (e.g., Ensley, Pearson, & Amason, 2002; Forbes, Korsgaard, & Sapienza, 2010; Higashide & Birley, 2002). I additionally study the impact of goal conflicts because these reflect actual (goal) incompatibilities, unlike task and relationship conflicts, which pertain to perceived incompatibilities. Early conflict scholars noted that perceived and actual incompatibilities do not necessarily coincide and that both play an important role in the conflict process (Cosier & Rose, 1977; Deutsch, 1973; Thomas, 1976).

Building on recent advances in the exit literature (e.g., Brigham, De Castro, & Shepherd, 2007; DeTienne & Cardon, 2010), I examine the effect of these three types of conflict on entrepreneurs’ and angel investors’ exit intentions. These intentions have been shown to be reliable predictors of actual exit (Brigham et al.), which I corroborate by presenting empirical evidence based on a follow–up study conducted one year after the initial round of data collection. As such, my research provides insight into the drivers of entrepreneurial and angel investor exit.

I contribute to the entrepreneurship literature in two ways. First, this study extends the theoretical understanding of entrepreneurial and investor exit by incorporating the relationships in which they are embedded. By examining the effects of conflicts, it also provides insight into the processes that lead to entrepreneurial (and investor) exit, as called for by Ucbasaran, Lockett et al. (2003). Second, this study is the first to examine drivers of angel investor exit, an issue that is uniquely important, since the ventures in which they tend to invest are very early stage and thus sensitive to the consequences of investor exit. In doing so, I provide a more nuanced understanding of the angel investment process as a whole.

I proceed as follows. First, I discuss the literature on angel investor and entrepreneurial exit and develop hypotheses that relate conflict and intentions to exit. Next, I describe the method used, followed by a presentation of the findings. I then conclude with a discussion of the implications of these findings and their consequences for potential future research.

Angel Investor and Entrepreneurial Exit: A Summary

Entrepreneurial and investor exit is defined as “the process whereby founders [/entrepreneurs] of [or investors in] privately–held firms . . . remove themselves from the primary ownership and decision–making structures of the firm” (DeTienne, 2010, p. 204). 1 Given that these two types of exit have been addressed by separate streams of literature, I provide a summary of both.

Angel Investor Exit

For angel investors, exit is part of their investment process and return maximization is an important objective to consider in the exit decision (Mason, 2006; Wiltbank & Boeker, 2007). Exit, being a liquidity event, implies relinquishing financial ownership of the firm (Mason). Although exit represents a crucial event in angel investors’ partnership with entrepreneurs, extant research on angel investor exit is scarce (Mason; Mason & Harrison, 2002). What we do know is limited to descriptive facts and figures regarding how, when, and with what returns these investors exit.

Excluding failures, angel investors generally liquidate their investments through trade sales or by selling their shares to existing shareholders; initial public offerings (IPOs) are rare (Mason & Harrison, 2002; Mayer, 2002). Angel investor exit is often unplanned and many angels do not have a clear exit route preference (Brettel, 2003; De Clercq, Fried, Lehtonen, & Sapienza, 2006). On average, angel investors prefer to exit their portfolio companies between 4 to 7 years after their initial investment, with about half of their investments resulting in breaking even or losses and one quarter resulting in high returns (Freear et al., 2002; Mason & Harrison).

Previous research has assumed that angel investors are less concerned with exiting than venture capitalists (e.g., Mayer, 2002; Van Osnabrugge, 2000); therefore, little attention has been paid to angel investor exit in general and its antecedents in particular. Recent developments in the angel market such as increased syndication and professionalization have made this previous assumption less applicable, however (Harrison & Mason, 2000; Sudek, 2004).

An additional reason for angel investor exit warranting more scholarly attention is that it has profound implications for portfolio companies, industry, and the economy as a whole. On a company level, investor exit will likely impact the entrepreneur who stands to regain or lose control over the venture (Duxbury, Haines, & Riding, 1996). Further, it may alter the range of resources available to entrepreneurs and their ventures (Mason & Harrison, 2002). Angel investments represent injections of human, social, and financial resources into ventures (Mason, 2006). Hence, investors’ departure is likely to drain those same resources. Conversely, angel investor departure can coincide with venture capitalist entry (Harrison & Mason, 2000), resulting in a replenishment of resources. On a higher level, investor exits through acquisitions or IPOs can affect competition and other dynamics of the industry in which the portfolio company operates (e.g., Akhigbe, Johnston, & Madura, 2006). Finally, exits can free up time and financial resources for the angel investor to reinvest in other entrepreneurial ventures (Van Osnabrugge, 1998), thereby continuing to contribute to the economy.

Entrepreneurial Exit

For entrepreneurs, exit requires relinquishing psychological ownership of the firm in addition to financial ownership (DeTienne, 2010). Although the field is much younger, research on entrepreneurial exit is similar to the investor exit literature in terms of the variety of perspectives, the levels of analysis, and the multidimensionality of the phenomenon itself. Whereas early research generally equated entrepreneurial exit with firm exit, DeTienne argues that entrepreneurial exit warrants a separate research approach because each individual entrepreneur is characterized by his or her own, unique intentions (Bird, 1988). Hence, although the exit of an individual entrepreneur or founder may coincide with the exit of the firm as a whole, for example, in the case of one–man companies, it is important to disentangle firm from entrepreneurial exit.

Entrepreneurs, much like investors, leave their ventures through a wide variety of mechanisms. They can leave voluntarily or involuntarily; they can disband the venture or sell it to third parties, employees, or family members; or their ventures can fail (Bates, 2005; Birley & Westhead, 1993; Petty, 1997). Regarding the likelihood and intentions of entrepreneurs to exit their ventures (in terms of when and how), scholars have revealed the impact of the rate of technological change (Crifo & Sami, 2008), income tax rates (Gurley–Calvez & Bruce, 2008), company performance, and capital flows into the company (Bates; Gimeno, Folta, Cooper, & Woo, 1997; Headd, 2003; Wennberg et al., 2010), the entrepreneurial team's heterogeneity (Ucbasaran, Lockett, et al., 2003) and the entrepreneur's human capital (Bates; DeTienne & Cardon, 2010; Gimeno et al.; Headd; Wennberg et al.).

Although for some entrepreneurs, exit marks the end of their entrepreneurial careers (Dyer, 1994), for others, who are called habitual or serial entrepreneurs, it is merely the beginning of a new adventure (Ucbasaran, Wright, & Westhead, 2003). Thus, exit has implications not only for the entrepreneur but also for the company, industry, and economy. On the company level, entrepreneurial exit may lead to an increase in available resources and skills but also a decrease in employee morale and performance. Industry effects pertain to the exit mechanism rather than the position of the exiting individual. As such, I expect these effects to be similar to those of investor exits. Finally, entrepreneurial exit may affect the overarching economy through entrepreneurial recycling (for a more comprehensive discussion of these effects, see DeTienne, 2010).

Angel Investor and Entrepreneurial Exit: The Importance of Relationships

In summary, entrepreneurial and angel investor exits are important and deserving of our research attention. Despite this fact, the exit literature has largely overlooked the relationship between investors or entrepreneurs and their respective key stakeholders. Especially in relation to angel investors who tend to be personally involved with the ventures in which they invest and who bring their own unique motivations, intentions, experience, and personality to the table (Freear et al., 2002; Mason, 2006), it seems critical that scholars take their interpersonal dynamics with entrepreneurs into account. Similarly, to gain insight into entrepreneurs’ intentions to exit, it is necessary to examine conflict with key stakeholders such as angel investors.

Hypotheses Development

In an average angel–backed company, angel investors and entrepreneurs are dependent on each other in that they make a deal to trade the angel investor's human, social, and financial capital for the opportunity or potential to make financial gains (Mason, 2006; Yitshaki, 2008). This partnership hence requires exchanges among investors and entrepreneurs that facilitate a deeper understanding of each other's goals, needs, values, and viewpoints and that endorse a cooperative working relationship (Cable & Shane, 1997; Harrison, Dibben, & Mason, 1997; Politis, 2008). As with similar types of exchange relationships (e.g., Amason & Schweiger, 1997; De Clercq, Thongpapanl, & Dimov, 2009), conflict is unavoidable in such settings (Mason & Harrison, 1996). Conflict is generally defined as “perceived incompatibilities or discrepant views among the parties involved” (Jehn & Bendersky, 2003, p. 189), with a distinction traditionally made between relationship and task conflicts (De Dreu & Weingart, 2003; Jehn, 1995). In the setting of angel–financed ventures, relationship conflicts pertain to perceived interpersonal incompatibilities or personality clashes between angel investors and entrepreneurs. Task conflicts, on the other hand, refer to perceived disagreements between angel investors and entrepreneurs about what should be done. Although task and relationship conflicts often occur together, empirical evidence suggests that both represent distinct dimensions of intragroup conflict (De Dreu & Weingart; Jehn & Bendersky).

In the organizational behavior literature, it is widely accepted that relationship conflicts among team members are important predictors of their individual intentions to leave their teams and their subsequent turnover behavior (Jehn & Bendersky, 2003). Studies that focus on relationship conflicts have consistently shown them to be detrimental to morale (Bayazit & Mannix, 2003; Jehn, 1995; Jehn, Northcraft, & Neale, 1999; Medina, Munduate, Dorado, Martínez, & Guerra, 2005). The personal nature of relationship conflicts causes feelings of anger, stress, anxiety, avoidance, suspicion, cynicism, and animosity among the parties involved (Amason, 1996; Jehn; Pelled, 1996). A substantial literature has further shown that individuals do not generally enjoy the experience of personal attacks, criticisms, and negative feelings such as anger and frustration. As such, relationship conflicts will lead to a general feeling of dissatisfaction and thus increase individuals’ intentions to leave the team or company (Bayazit & Mannix; Jehn; Medina et al.). A similar effect is expected for relationship conflicts between angel investors and entrepreneurs.

Upon investment, angel investors and entrepreneurs enter their partnership with certain expectations and assumptions. One of these is a good fit between investors and entrepreneurs, given that it is one of the most important investment criteria for angel investors, more so than for venture capitalists (Mason, 2006; Mason & Stark, 2004). Even in the latter setting though, fit has also been shown to matter such that investors prefer entrepreneurs who are like them, in terms of both surface–level attributes such as professional background (Franke, Gruber, Harhoff, & Henkel, 2006) and deeper attributes such as cognitive reasoning processes (Murnieks, Haynie, Wiltbank, & Harting, 2007). Further, entrepreneurs expect their angel investors to deliver several services once the investment has been made, such as serving as a sounding board (Mason; Sudek, 2004). For this reason, they are often advised to think twice about whom to bring on board (Duxbury et al., 1996; Mason & Harrison, 1996). Angel investors’ more active involvement in the venture post–investment combined with their desire to help fellow entrepreneurs generally results in a relationship of a more personal nature than is the case for the average venture capital partnership (Landström, 1998; Sudek). This makes investor–entrepreneur fit an even more crucial requirement for a successful, cooperative relationship between angel investors and entrepreneurs.

Hence, when post–investment investors and entrepreneurs become aware of their (unanticipated) differences in personalities, political norms, values, and taste, disappointment will result. Interpersonal dislikes and associated feelings of resentment and animosity will not only make entrepreneurs and angel investors disillusioned about their perfect marriage, it will also undermine their cooperation by hindering their capability to gather and process information from each other—crucial for the success of their exchange relationship—and by focusing on the emotional problems rather than on the tasks at hand (Amason, 1996; Bayazit & Mannix, 2003; Jehn, 1995). Because typical responses to interpersonal problems include “psychological and physical withdrawal” (Jehn, p. 258), these conflicts should increase investors’ and entrepreneurs’ intentions to exit their ventures. I expect this effect to hold for both angel investors and entrepreneurs given the importance of interpersonal fit between investors and entrepreneurs to enable active and valuable post–investment interaction between them. Thus:

Previous empirical studies on the relationship between task conflict and intentions to exit have suggested that task conflict should have no effect in settings where tasks embody a certain degree of complexity, such as strategic decision making, because conflict would be inherent to the task and thus be expected (Bayazit & Mannix, 2003; Jehn, 1995; Jehn et al., 1999). Because angel investors and entrepreneurs are key strategic decision agents, one could expect the same effect for their task conflicts. Although I follow this line of reasoning for the lack of effect of task conflicts on angel investors’ intentions to exit, I expect a positive effect on entrepreneurs’ intentions to exit.

Entrepreneurs have a strong sense of psychological ownership over and emotional attachment to their ventures (Pierce, Kostova, & Dirks, 2001), even after receiving external equity funding (Arthurs & Busenitz, 2003). They have generally invested substantial amounts of sweat equity into their ventures, have nurtured and developed them from idea inception, and have a firm idea of where to take their ventures next (Arthurs & Busenitz; Forbes et al., 2010). Consequently, they generally prefer investors who they suspect will help them guide their venture towards those ultimate goals (Boot, Gopalan, & Thakor, 2006). They tend to welcome and are receptive to investor advice on how to achieve their vision, although the degree of receptivity varies among entrepreneurs (Barney, Busenitz, Fiet, & Moesel, 1996). However, confrontation with many task conflicts may make entrepreneurs think that investors are working against rather than with them. In this case, rather than viewing an investor's input as well–intentioned advice, entrepreneurs may be more likely to perceive conflicts as threatening (Avey, Avolio, Crossley, & Luthans, 2009). In addition, entrepreneurs may interpret these disagreements as investors questioning their ability, judgment, and contributions to the venture. When they feel pressured by external constituents, such as investors, entrepreneurs are likely to become less committed to their ventures (Dobrev & Barnett, 2005). Taken together, this should make entrepreneurs more susceptible to feelings of fear and distrust and make them less satisfied with their investor relationship, thus leading to detachment and withdrawal.

In contrast, angel investors may frame these disagreements differently. Given that they “suffer” less from emotional bonds to the venture, they will likely see these discussions as part of normal business (Mason & Harrison, 1996; Politis, 2008). Angel investors see it as their job to probe entrepreneurs to help them find and formalize a vision, and they may not be aware of the effects this probing has on the entrepreneur's self–confidence and commitment. To this end, some angel investors have even developed formal planning tools such as questionnaires (see, for instance, Berkus, 2006). Debate is thus innate to the task or job of being an advisor and investor, thereby canceling out task conflict's negative effects (Bayazit & Mannix, 2003). Taken together, I hypothesize:

Thus far, I have focused on conflicts as perceived incompatibilities (Jehn & Bendersky, 2003). A common assumption made when investigating the effect of such perceived incompatibilities is that team members have common goals (Jehn, 1995). However, this assumption does not necessarily hold for angel investors and entrepreneurs. Even though they are united by an overarching goal of value creation, angel investors and entrepreneurs can have different subordinate goals (Fiet, 1995; Mason, 2006; Politis, 2008). For example, angel investors who want to maximize financial gains (Mason; Sudek, 2004) are likely to be more focused on short–term growth and development than their entrepreneurs (De Clercq & Manigart, 2007).

Goal incompatibilities, which are also labeled goal conflicts (Bourgeois, 1985; Cosier & Rose, 1977; Eisenhardt & Bourgeois, 1988), are related to task conflicts. Goal conflicts were taken as a starting point in Jehn's definition of team task conflict (Jehn, 1997, p. 532). Although they are related, these conflict types differ in two important respects. First, whereas goal conflicts pertain to actual goal incompatibilities, task conflicts include, but are not limited to, perceived goal incompatibilities (Jehn). As key strategic decision agents, task conflicts between angel investors and entrepreneurs refer to strategic decision making, which is a broader concept than setting objectives (Eisenhardt & Bourgeois). Second and more importantly, conflict scholars acknowledge that perceptions can be misguiding in that perceived incompatibilities will not necessarily reflect actual incompatibilities, nor will actual incompatibilities necessarily be perceived as such (Deutsch, 1973; Fisher, 1998; Thomas, 1976). Likewise, entrepreneurship scholars recognize that perceived goal incompatibilities do not necessarily correspond with actual goal incompatibilities (Arthurs & Busenitz, 2003). Due to these differences and the key role goal incompatibilities play in investor–entrepreneur settings, I included goal conflicts in this study. 2

Previous research indicated that goal conflicts increase the likelihood of using competitive tactics and make problem solving more difficult (Deutsch, 1973; Eisenhardt & Bourgeois, 1988; Fisher, 1998; Tjosvold, 1998). When angel investors and entrepreneurs truly and substantially differ in terms of the objectives they want to achieve, the probability of finding a compromise and forging a cooperative relationship will significantly decrease (Apfelbaum, 1974; Cable & Shane, 1997). This could lead investors and entrepreneurs to feel that no mutual gain will result from continuing their partnership, thereby making it less desirable and useful for them to remain with their companies (Christensen, Wuebker, & Wüstenhagen, 2009).

I expect this positive effect of goal conflicts on intentions to exit to hold for both angel investors and entrepreneurs. Even though mixed goals are inherent to their partnership, a certain degree of goal alignment is a condition sine qua non for both parties to enter into and achieve successful cooperation (Brettel, 2003; Politis, 2008). Angel investors, who are particularly concerned with agency risk (Fiet, 1995), will not invest unless they are convinced a minimum threshold of goal alignment is present. In other words, whereas some discussion is to be expected concerning actions to be taken, resources to be committed (Mintzberg, Raisinghani, & Theoret, 1976, p. 246), and other crucial strategic discussions, investors do not expect their underlying goals to be very different from the entrepreneurs'. Similarly, entrepreneurs, who are not very experienced with the process of securing financing, often do not have a clear view of investors’ requirements, characteristics, and objectives (Van Auken, 2001). It is therefore likely that they will also expect a certain degree of goal alignment to be present, at least initially. Because highly incongruent goals are undesirable and unexpected for both angel investors and entrepreneurs, the hypotheses are as follows:

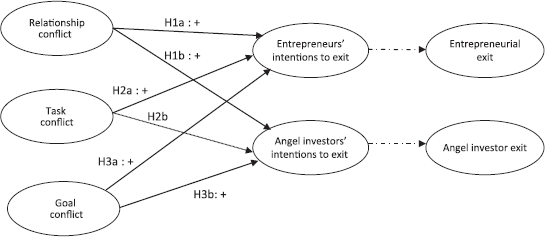

Figure 1 provides a graphical summary of the hypothesized effects of relationship, task, and goal conflicts between angel investors and entrepreneurs on both parties’ intentions to exit.

Conceptual Model

Methods

Sample and Data Collection

Data for this study were gathered in two locations, Continental Europe (Belgium) and the United States (California). For the Belgian sample, 20 different data sources were used, including a random directory of start–ups, deal lists of angel networks, GEM data, 3 directories of high–technology companies, media articles, incubators, and snowballing. In this manner, a list of 305 Belgian potential angel–backed companies was constructed. These companies were contacted by telephone during the summer of 2007 to identify whether they fulfilled the conditions of the research. These conditions were (1) at least one angel investor was a member of the Board of Directors or actively involved in strategic decision making in their portfolio company, and (2) the company received angel financing between January 2003 and August 2006. The latter condition was imposed to avoid the exit period because the effects of conflicts can change as teams approach the end of their relationship (Jehn & Mannix, 2001). In addition, focusing on young angel investments should avoid recall and survival bias (Farrell, Howorth, & Wright, 2008; Paul, Whittam, & Wyper, 2007). This resulted in 64 (potentially) eligible companies. 4 For the Californian sample, the data sources included Zephyr, VentureXpert, Growthink, and the members’ or participants’ lists from the Angel Capital Association, C21 BioVentures, and the California Clean Tech Open competition. This resulted in a list of 1,265 Californian potential angel–backed companies, which were contacted through emails containing a link to a YouTube video in which the research project and the aforementioned conditions were explained. Companies were asked to inform me of whether they fulfilled the research conditions, which resulted in 588 (potentially) eligible companies.

Responses were sought from all entrepreneurial team members and angel investors who had a seat on the Board of Directors or were actively involved in the company. The entrepreneurial team was defined as those individuals who, at the time of the study, had an equity stake and were actively involved or played a key role in strategic decision making (Forbes, Borchert, Zellmer–Bruhn, & Sapienza, 2006; Ucbasaran, Lockett, et al., 2003). The definition of angel investors was external individual investors who invest some of their own wealth in unlisted companies in exchange for shares and who have no family or friend connection to the entrepreneurs (Mason, 2006). When parties agreed to participate, questionnaires were emailed either directly to the concerned team members or, in some cases, through the CEO when angel investors preferred to remain anonymous. This method of distributing surveys is consistent with previous team research (e.g., Simons, Pelled, & Smith, 1999; Srivastava, Bartol, & Locke, 2006). When necessary, follow–up phone calls were performed. Using a team member response rate criterion of 50% (e.g., Ensley et al., 2002; Mooney, Holahan, & Amason, 2007) and the condition that at least one response was needed from the angel investor side and one from the entrepreneur side, a final sample was obtained of 28 Belgian teams (representing 35 angel investors and 40 entrepreneurs) and 26 Californian teams (representing 30 angel investors and 32 entrepreneurs).

Analyses revealed no significant differences between Belgian respondents and non–respondents in terms of company age in 2007, age at time of investment, and industry distribution. The Californian respondents and non–respondents did not significantly differ in terms of company age at time of investment and industry distribution, but the ventures of non–respondents were older at the time of the research project. The latter is not surprising because this research was targeted towards younger angel investments. Given that angel investors tend to invest in the earlier stages of development (Mason, 2006), older, more mature companies would probably not have fulfilled the second condition of this study and were therefore more likely to not respond to the survey request (547 of the 562 nonrespondents could not be contacted). Finally, there were no substantial differences between early and late respondents in both samples regarding the primary variables of interest. Taken together, this indicates that non–response bias should be limited (Armstrong & Overton, 1977).

Given that the number of respondents was rather small in each location, it was deemed desirable to combine them into one larger sample. To do so, I ran a multigroup confirmatory factor analysis to check for measurement invariance (Steenkamp & Baumgartner, 1998). The goodness–of–fit indices suggested by Hu and Bentler (1998) were all above the minimum values (CFI = .96, TLI = .95, SRMR = .06). As such, this provided support for combining the Belgian and Californian samples into one larger sample consisting of 54 teams and 137 individuals, of which 72 were entrepreneurs and 65 were angel investors.

Variables

Dependent Variable.

Intention to exit was measured using two items based on O'Reilly, Chatman, and Caldwell (1991) and Brigham et al. (2007). The questions were “How long do you intend to remain with Venture X?” and “If you have your own way, will you be working for this organization three years from now?” Both questions were slightly adapted for the angel investors (for the first item “remain invested in” was added and “working for this organization” in the second item was changed to “still be a shareholder”). As in Brigham et al., the two items were measured on a 7–point scale ranging from less than 1 year to more than 5 years for the first item and from definitely yes to definitely no for the second item. The first item was reverse scored such that higher scores indicated a higher intent to exit. The two items were averaged to create the final score. The mean value was 2.31 (SD 1.36) for entrepreneurs and slightly higher, i.e., 3.02 (SD 1.57) for angel investors. Both indicate a positive skew (for further details see section on robustness checks). The Cronbach's alpha value was satisfactory (.74). To validate this measure, angel investors were also asked to explicitly formulate the number of years in which they wanted to exit. The correlation coefficient with the intention to exit measure was negative and statistically significant (−.61, p < .001), indicating construct validity. 5

Independent Variables.

Task conflict and relationship conflict were measured using three items for each based on Pearson, Ensley, and Amason's (2002) revised version of Jehn's intragroup conflict scale (Jehn, 1995). For task conflict, respondents were asked to rate how many disagreements over different ideas, differences about the content of decisions, and differences of opinion there had been between the angel investors and entrepreneurs on a scale from 1 (= none) to 5 (= a great deal). For relationship conflict, they were asked how much tension, personal friction, and anger there had been between the angel investors and the entrepreneurs. The mean value for task conflict was 2.24 (SD.72) and 1.80 (SD.89) for relationship conflict. Both Cronbach's alpha values indicated excellent reliability (.92 and .93, respectively). To check whether aggregation was appropriate, the intra–class correlation coefficient (ICC) and within–group agreement index were calculated (James, Demaree, & Wolf, 1984; Klein & Kozlowski, 2000). Both ICCs are significant (p < .001) and the median Rwg(J) values for both constructs exceed the .7 threshold (.94 for both task and relationship conflict). This indicates that, per company, there is adequate consensus between angel investors and entrepreneurs regarding their conflicts and significant variation between companies. Together this justifies aggregation. 6

Goal conflict was measured as the degree of goal incongruence based on Sapienza and Gupta (1994). First, respondents were asked to allocate 200 points across 11 objectives (six financial and five nonfinancial criteria) according to importance to the achievement of the short–term financial goals of Venture X. Second, they were asked how much emphasis should be given to financial and non–financial goals (percentage). For each criterion, a weighted score was then calculated. Illustration: new product development (NPD) is a nonfinancial criterion. Assume the respondent allocated 20 out of 100 nonfinancial points to this criterion and, in general, thinks that non–financial goals should be given 80% emphasis; then, the weighted score for NPD would equal 20 × .80. The average of the weighted scores per criterion was then calculated separately for the two subgroups (i.e., angel investors and the entrepreneurs). Only then were the absolute differences of the average weighted scores of the angel investors and entrepreneurs within the same company taken and summed across criteria. The mean value was 76.57 (SD 26.29). As a point of comparison, the average degree of goal incongruence between venture capitalists and CEOs in the study by Sapienza and Gupta was somewhat higher, that is, 93.92 (SD 31.61).

Control Variables.

In addition to relationship–specific factors such as conflicts, several other aspects pertaining to angel investors, entrepreneurs, or their ventures can influence exit in terms of its type, success, and timing and hence potentially affect angel investors’ and entrepreneurs’ intentions to exit. Therefore, several controls were added for the entrepreneur and angel investor models.

For the entrepreneurs’ intention to exit model, I added controls for industry, company age, team size, entrepreneur's age, and his/her entrepreneurial and consulting experience. Industries might vary in terms of competitive and technological environment, average performance, and exit opportunities (Bates, 2005; Gimeno et al., 1997). Two industry dummy variables were added as controls; one dummy variable was added for software (50%) and another was added for high–tech manufacturing (17% of the sample), which together represented the two most common industries in our sample. Based on other entrepreneurial exit studies (DeTienne & Cardon, 2010; Wennberg et al., 2010), entrepreneurs were asked to indicate the founding year of their venture so that company age at time of questioning could be calculated and controlled for. Team size might also affect intragroup dynamics (Jehn, 1995; Simons et al., 1999) and the probability of entrepreneurial exit (Boeker & Karichalil, 2002). Hence, a variable was included to control for team size, which was measured as the total number of entrepreneurs and angel investors. 7 In addition to being influenced by company– and team–level characteristics (Gimeno et al.; Ucbasaran, Lockett, et al., 2003), entrepreneurial exit is also influenced by individual–level features (DeTienne, 2010). An entrepreneur's human capital has been shown to influence exit type or success (Bates; Headd, 2003; Wennberg et al.), intended exit strategy (DeTienne & Cardon), and exit likelihood in general (Gimeno et al.; Headd). Thus, I controlled for the entrepreneur's age (number of years) and his/her entrepreneurial and consulting experience at time of questioning. Entrepreneurial experience was measured by asking entrepreneurs his/her number of years of working experience as a founder or entrepreneur. Additionally, I used the number of years of consulting experience because such experience enhances skills such as problem detection, knowledge generation, and dissemination as well as learning how to take advantage of opportunities (Dimov & Shepherd, 2005; Walske & Zacharakis, 2009). Similar to the traditionally studied human capital variables, such skills are valuable in business management and help with strategic business decisions thereby increasing the probability of achieving successful exits (Walske & Zacharakis; Zarutskie, 2010).

For the angel investors’ intention to exit model, controls for industry, portfolio company age, angel investor age, time since investment, and perceived venture performance were added. Since industry dummies and portfolio company age have been shown to impact investor exit, they were included and measured in the same way as in the entrepreneur's model (Chahine, Filatotchev, & Wright, 2007). Angel investor's age was also added as a control variable due to its effect on turnover likelihood (Bayazit & Mannix, 2003; Jehn, 1995). In addition, time since investment was included because it could be related to exit success and likelihood (Mason & Harrison, 2002). Finally, perceived firm performance (range 1–5) was also controlled for by asking respondents to rate the current performance of the venture relative to its competitors (Sapienza & Gupta, 1994). Given angel investors’ financial motives for investing (Mason, 2006; Sudek, 2004), perceived venture performance could positively influence the nature of their relationship with entrepreneurs and their intention to continue investing in the company as it does for venture capitalists (De Clercq & Sapienza, 2006). Given that this study aims to explain the effects of conflicts on angel investors’ intentions to exit their ventures over and above the influence of venture performance, it was deemed necessary to include this control variable. A quadratic effect of perceived performance was also added because investors may have a higher intention to exit low– and high–performing ventures than moderately performing ones (hence, a U–shaped relationship).

Data Quality: Common Method Bias

Most of the variables used in the analyses were gathered through the same questionnaire, giving potential cause for concerns around common method variance. To reduce the risk of this potential bias, several precautions were taken in designing the questionnaire, including reverse scoring of items, use of variation in wording of items, use of different scaling anchors for the key variables, and guaranteeing absolute anonymity to respondents (Lindell & Whitney, 2001; Podsakoff, Mackenzie, Lee, & Podsakoff, 2003). Further, all variables were measured using scales that had been previously validated and shown to have good psychometric properties (see above). In addition to the design of this study, the Harman's single factor test also suggests common method bias may be limited (Podsakoff & Organ, 1986). The exploratory factor analysis resulted in a 3–factor solution, with the first factor accounting for only 34% of the total variance (31% and 13% for the second and third factor, respectively).

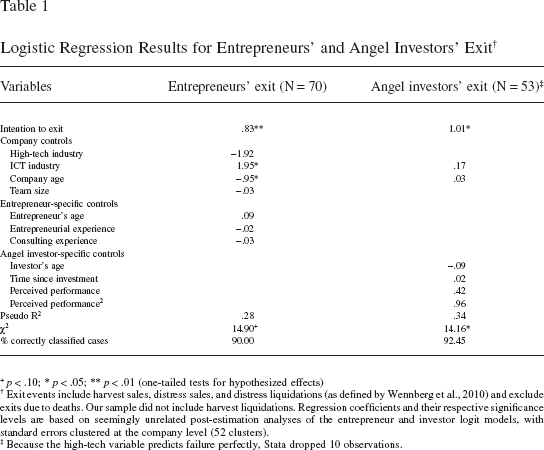

Further, intentions to exit should positively predict subsequent exit behavior (Brigham et al., 2007). To corroborate this, all entrepreneurs and angel investors from the original sample were contacted again after one year. Excluding exits due to deaths (two angel investors, two entrepreneurs), 16 individuals (seven angel investors and nine entrepreneurs) had left their ventures. Logistic regressions were run with the dependent variable taking the value of 1 in case of entrepreneur or angel investor exit and 0 for continuation.

Table 1 reveals that intentions to exit have a statistically significant, positive effect on both investor (p < .05) and entrepreneur exit (p < .01). In unreported results, analyses were rerun on specific exit types to account for exit multidimensionality (Wennberg et al., 2010). High–performing (low–performing) exits were defined as exits where the pre–exit performance perceived by the CEO was above (below) the sample mean. The results indicate that intentions to exit are also statistically significant predictors of sales exits, that is, distress and harvest sales, and of high–performing exits, that is, harvest sales (the sample did not include harvest liquidations). 8 Taken together, this suggests that the risk of common method bias is limited.

Logistic Regression Results for Entrepreneurs’ and Angel Investors’ Exit †

p < .10;

p < .05;

p < .01 (one–tailed tests for hypothesized effects)

Exit events include harvest sales, distress sales, and distress liquidations (as defined by Wennberg et al., 2010) and exclude exits due to deaths. Our sample did not include harvest liquidations. Regression coefficients and their respective significance levels are based on seemingly unrelated post–estimation analyses of the entrepreneur and investor logit models, with standard errors clustered at the company level (52 clusters).

Because the high–tech variable predicts failure perfectly, Stata dropped 10 observations.

Data Analysis

Angel investor and entrepreneurial exit might be driven by different factors. For this reason, separate OLS regressions were run for the entrepreneur subsample (N = 72) and the angel investor subsample (N = 65). Because I investigate the intentions to exit of investors and entrepreneurs belonging to the same set of ventures, I employ the seemingly unrelated estimation procedure (SuEst in STATA 10.0). Similar to seemingly unrelated regression, this technique allows for correlated errors across estimated equations or models by combining the estimation results into a single, simultaneous covariance matrix (StataCorp, 2007; Weesie, 1999). Additionally, this procedure allows for clustered standard errors per company (Weesie), a necessary correction due to observations of investors and entrepreneurs in our sample being non–independent. Finally, this estimation procedure has the advantage of being statistically more efficient than running two separate OLS regressions.

Results

Descriptive Statistics

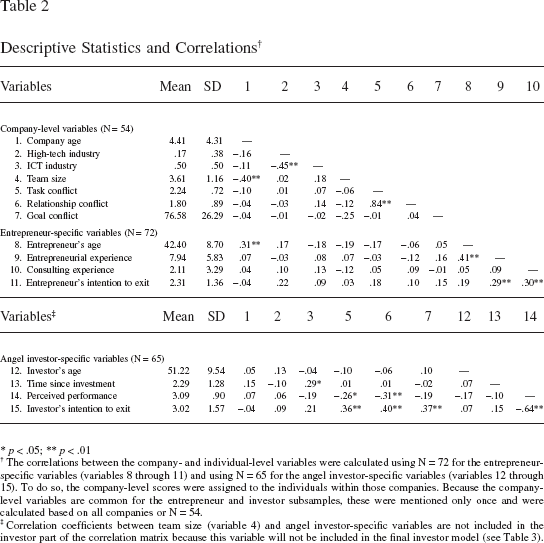

Table 2 provides an overview of the means, standard deviations, and correlations between company–, entrepreneur, and angel investor–specific variables. Variables with shared meaning and values for angel investors and entrepreneurs, such as company age, industry, and conflicts, were labeled company–level variables and were based on the company–level sample size (N = 54). All entrepreneur– and investor–specific variables were measured at the individual level (based on respective sample sizes of 72 and 65).

Descriptive Statistics and Correlations †

p < .05;

p < .01

The correlations between the company– and individual–level variables were calculated using N = 72 for the entrepreneur–specific variables (variables 8 through 11) and using N = 65 for the angel investor–specific variables (variables 12 through 15). To do so, the company–level scores were assigned to the individuals within those companies. Because the company–level variables are common for the entrepreneur and investor subsamples, these were mentioned only once and were calculated based on all companies or N = 54.

Correlation coefficients between team size (variable 4) and angel investor–specific variables are not included in the investor part of the correlation matrix because this variable will not be included in the final investor model (see Table 3).

Although no statistically significant correlations were found between entrepreneurs’ intentions to exit and conflict, I found statistically significant and positive correlations between angel investors’ intentions to exit and all conflict constructs. The correlation between task and goal conflict is trivial and its 95% confidence interval ranges from −.28 to .26, corroborating that these are distinct concepts (MacKenzie, Podsakoff, & Jarvis, 2005). Further, the correlation between task and relationship conflict was very high (.84) and statistically significant. For this reason, I conducted a confirmatory factor analysis using the entire sample (N = 137) because task and relationship conflicts are shared, team–level constructs. The two–factor model had a significantly better fit than the one–factor model (one–factor model: CFI = .85, GFI = .73, RMR = .07 compared with the two–factor model: CFI = .98, GFI = .94, RMR = .04) and the chi–square difference of 95.20 was significant at p < .001. Consistent with previous conflict studies (De Clercq et al., 2009; Forbes et al., 2010), this confirms the discriminant validity of task and relationship conflicts. Variance inflation factors further corroborate the limited threat of multicollinearity (maximum values of 4.41 and 4.19 in the entrepreneur's and angel investor's models, respectively).

Hypotheses Testing

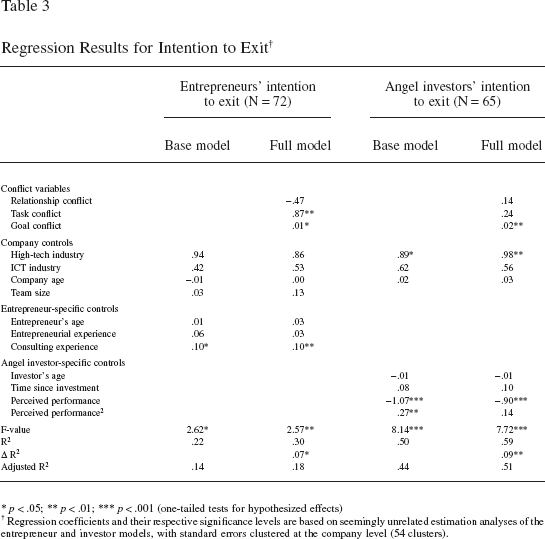

I report the results of the regression analyses with seemingly unrelated estimation for both entrepreneurs’ and angel investors’ intentions to exit in Table 3.

Regression Results for Intention to Exit †

p < .05;

p < .01;

p < .001 (one–tailed tests for hypothesized effects)

Regression coefficients and their respective significance levels are based on seemingly unrelated estimation analyses of the entrepreneur and investor models, with standard errors clustered at the company level (54 clusters).

In both models, I first entered the control variables (base model). For entrepreneurs’ intentions to exit, this reveals a statistically significant and positive effect of consulting experience. For angel investors’ intentions to exit, a strong, negative linear effect is revealed for perceived performance. Although the curvilinear term was also statistically significant, its significance was weaker and did not hold in the full model. Furthermore, the turning point for the curvilinear term was out of range (1.98 for the mean–centered perceived performance variable), which corroborates a linear effect. When ventures are better performing, angel investors have lower intentions to exit. The results also indicate that angel investors whose portfolio companies operate in high–tech manufacturing have a statistically significant higher intention to exit. Both base models were statistically significant (for the entrepreneurs: R2 = .22, p < .05; for the angel investors: R2 = .50, p < .001).

With regard to entrepreneurs’ intentions to exit, relationship conflicts (hypothesis 1a), task conflicts (hypothesis 2a), and goal conflicts (hypothesis 3a), were hypothesized to have a positive effect above and beyond the impact of the control variables. The full model presented in Table 3 reveals statistically significant and positive effects for task (p < .01) and goal conflicts (p < .05), but not for relationship conflicts. This provides support for hypotheses 2a and 3a, but not for hypothesis 1a. Adding these conflict predictors made a significant contribution to the base model (ΔR2 = .07, p < .05).

For angel investors, I hypothesized a positive effect on intentions to exit for relationship (hypothesis 1b) and goal conflicts (hypothesis 3b); I hypothesized that task conflicts would have no effect (hypothesis 2b). Similar to entrepreneurs’ intentions to exit, I found no statistically significant effect of relationship conflicts on angel investors’ intentions to exit. Hence, hypothesis 1b could not be supported. Further, the results revealed a statistically significant and positive effect of goal conflict (p < .01) and no statistically significant effect for task conflict, which supports hypotheses 2b and 3b. The addition of the predictor variables to the base model adds significant explanatory power to the angel investor's intention to exit model (ΔR2 = .09, p < .01).

Robustness Checks

I performed several additional analyses to check the robustness of these results. First, based on previous research (Gimeno et al., 1997), one could argue that perceived venture performance will also influence entrepreneurs’ intentions to exit. As such, I reran models with perceived performance added to the entrepreneurial model as a control variable (in both linear and linear plus quadratic form). In both cases, the previous results remained robust, perceived performance did not have a statistically significant effect on entrepreneurs’ intentions to exit, and model fit did not significantly improve. Second, I added controls to both the angel investor and entrepreneur models for the location of data collection (Belgium or California), investment stage, and industry–specific experience (measured as the number of years of working experience in the same industry as the current portfolio company/venture). Adding a country dummy would not only control for any potential cultural differences in conflict–intention to exit relationships but would also serve as a proxy for potential differences in the development of the respective risk capital markets and the availability of exit options. Similar to industry, investment stage may be related to different exit types (Mason & Harrison, 2002; Wiltbank, 2005). Finally, industry–specific experience has been shown to affect intended exit strategy (DeTienne & Cardon, 2010) and exit type (Wennberg et al., 2010; Wiltbank & Boeker, 2007). However, none of these additional control variables had a statistically significant effect and they also did not improve model fit. The results remained robust. Further, models were also run on a transformed, that is, squared, version of the intention to exit variable because this was highly skewed. Again, this did not alter the results. Finally, I have no information on exit agreements made between angel investors and entrepreneurs at the time of investment. As a result, I cannot completely rule out the possibility of having included conflicts about exit. To address this concern, I reran the main analyses excluding all ventures (11) that respondents had left 1 year later. The results were slightly stronger for both models, indicating that the risk of inflated findings as a consequence of having included such conflicts should be limited.

Discussion and Conclusions

In the present study, I set out to explain how conflicts between angel investors and entrepreneurs affect both parties’ intentions to exit. Building on conflict literature, I found that task conflicts between angel investors and entrepreneurs positively affect entrepreneurs’ intentions to exit their ventures and that goal conflicts positively affect both entrepreneurs’ and angel investors’ intentions to exit. In contrast, relationship conflicts do not affect intentions to exit. These findings are of interest for several reasons.

First, this paper is among the first to integrate relational dynamics among venture partners into the study of entrepreneurial and investor exits. Extant research on entrepreneurial exit has revealed the impact of individual–, team–, company–, and industry–level attributes on intended exit strategy, exit likelihood, and exit type. Research on the antecedents of angel investor exit is altogether lacking. What both streams of literature have in common is that they cannot provide an answer to the question of what processes lead to entrepreneurial and investor exit, nor how stakeholders affect entrepreneurs’ and investors’ desire to leave their ventures. By providing evidence of entrepreneur–investor conflicts positively affecting intentions to exit, I uncover the impact of the behavioral processes at play between entrepreneurs (or investors) and one of their key stakeholders, that is, their financiers (or investees). In so doing, I contribute to the literature that seeks to understand the driving forces of entrepreneurial and angel investor exit.

Second, this study addresses a call to open up the investor–investee dyad (Lockett et al., 2006). Thus far, research on the post–investment relationship between angel investors and entrepreneurs has focused on both parties’ expectations regarding their partnership and the roles angel investors assume in their portfolio companies (e.g., Brettel, 2003; Mason & Harrison, 1996). Little research, however, has studied the working relationship of active entrepreneur–angel investor “pairs.” Given that angel investors and entrepreneurs generally work together for a time period ranging between four and seven years, this lack of research attention is surprising. Although research on the investment decision–making processes of angel investors is certainly valuable and rewarding, it provides little insight into what happens once the investment decision has been made. My findings suggest that conflicts between angel investors and entrepreneurs can substantially increase the likelihood of either party exiting prematurely. This indicates that if scholars want to thoroughly understand the entire angel investment process, one cannot overlook the relational aspects of the angel investor–entrepreneur partnership.

In addition, entrepreneurial finance research has generally adopted an exclusive investor or entrepreneur perspective. By integrating both perspectives, I add to this literature in two ways. Although gathering data from one side of investor–investee dyads is often considered a limitation to studies (e.g., Parhankangas & Landström, 2006), my findings suggest that the distortion of doing so may be more limited than previously thought. Evidence regarding aggregation statistics indicates that angel investors and entrepreneurs strongly agree in terms of the degree of conflict present in their partnership. Thus, my findings suggest that the concern that data collected from only one side of the investor–investee dyad may be biased is unfounded. However, gathering both partners’ perceptions of their relational dynamics does allow for a more comprehensive view of their partnership. By providing specific evidence of how shared goal conflicts affect both angel investors’ and entrepreneurs’ intentions to exit, whereas task conflicts only affect entrepreneurs’ intentions to exit, this research provides more detailed insight into the specificity and unique nature of this phenomenon.

Third, my study also informs the conflict literature. Although task and relationship conflicts are commonly studied in intragroup conflict research (De Dreu & Weingart, 2003), including in entrepreneurial settings (e.g., Ensley et al., 2002; Higashide & Birley, 2002), goal conflicts are not. By examining these three types of conflicts, this study ties into a debate that has gained momentum in the intragroup conflict literature, namely that of how to define conflict (Tjosvold, 2007). My results support the view that both perceived and actual incompatibilities should be considered important because each has a unique, significant role to play in the conflict process. Theorizing conflict as consisting of both a perceptual and an actual component could provide an alternative lens to understand why conflict studies have produced so many mixed findings (De Dreu & Weingart; Jehn & Bendersky, 2003). Although early conflict theorists defined conflict as including both perceived and actual incompatibilities (Deutsch, 1973), conflict studies over the years have neglected this distinction and thus have potentially confounded their results. Incorporating both elements into future research should allow us to gain better insight into the complex relationship between conflict and team effectiveness and could resolve the debate as to whether conflict in teams and organizations should be stimulated or avoided altogether (Tjosvold).

Limitations, Future Research, and Implications

This study is not without limitations, which provide opportunities for future research. First, I collected data in two geographic locations (California and Belgium) and pooled it based on the results from the multigroup CFA. An argument could be made that differences in the degree of development of their respective risk capital markets could have an impact on angel investors’ and entrepreneurs’ degree of professionalization and their exit opportunities. As such, it could influence the relationship under study. Although the United States and western European countries are both known to have individualistic cultures, it would be interesting to see whether cross–cultural differences exist in the impact of angel investor–entrepreneur conflicts. This was beyond the scope of this paper, however. Furthermore, additional country controls were insignificant and did not change the results, indicating that this bias should not be large.

Second, one may argue that desiring to leave a venture does not necessarily equate with being able or willing to do so due to financial or legal restrictions. With regard to the former, angel investors may only exit if it is financially attractive to do so through, for instance, an IPO or by selling their shares to an interested party (Birley & Westhead, 1993; Mason & Harrison, 2002). However, a wide range of motivations and objectives, including nonfinancial ones, drive angel investors (Mason, 2006). Therefore, exit likelihood or desirability is not an exclusive function of the potential financial return achieved. Regarding the latter objection, research has indicated that angel investor contracts generally do not include exit provisions (Kelly & Hay, 2003). Taken together, even when exiting is potentially suboptimal from a financial point of view, angel investors should be able to exit if that is their wish. The statement that they generally will in the case of high intentions to exit is corroborated by the fact that these intentions are a form of psychological detachment from the venture, which increases the likelihood that individuals will actually leave (Bayazit & Mannix, 2003; Burris, Chiaburu, & Detert, 2008). To accurately reflect this on an empirical level, I altered the wording of the intention to exit measure to emphasize the voluntary aspect of the question and perceived venture performance was taken into account. In addition, intentions to exit were significantly and positively related to turnover for both entrepreneurs and angel investors, which indicate that the problem of being unable to exit was limited.

One could also argue that my intention to exit measure does not take into account the multidimensionality of entrepreneurial exit and angel investor exit (DeTienne, 2010; Wennberg et al., 2010). Given that I did not have data on intended exit strategy or on exit agreements made prior to investment, this is indeed a limitation of my study. I tried to reduce this bias by controlling for factors that have been to shown to influence type of investor or entrepreneurial exit or intended exit strategy. In addition, analyses indicated that angel investors’ and entrepreneurs’ intentions to exit were statistically significant predictors of actual exit for the overall sample of exits (distress liquidations, distress sales, and harvest sales) and for the samples of sales exits only and all high–performing exits only. Further, previous research has also indicated that angel investors often do not have a clear exit strategy preference (e.g., Brettel, 2003). Together, this should provide more confidence that my results will hold regardless of the type of exit strategy, whether planned or unplanned.

Similarly, by sampling active angel investors and entrepreneurs, I could be missing the worst–case scenarios where angel investors and/or entrepreneurs have already voluntarily left. Although I acknowledge this limitation, in my view based on my theoretical arguments, incorporating these companies into my sample would have only served to strengthen the negative results found in this study.

Finally, one could criticize the use of a conflict theory approach to investor exit because angel investors are assumed to invest with an intention to exit. From this standpoint, exit should be a desirable outcome, which implies that it is a choice (except in the case of bankruptcy). Nonetheless, the organizational behavior literature frames exit as an undesirable outcome, with conflict implying a push towards and hence an obligation to exit. Despite this fact, I argue that my approach is appropriate for two reasons. First, by focusing on young angel investments (maximum four years old), for which exit should not yet be an issue, the exits included in my sample should mainly be premature. Second, if exits were desirable, one would expect a positive correlation between conflict and angel investor satisfaction. Based on unreported results, this was not the case for any of the conflict constructs under examination. Taken together, in my view, this supports the choice to view conflicts leading to angel investor exit as a push relationship.

Based on the results and limitations of this study, there are several avenues for future research. First, the main explanation provided for the results concerning task and goal conflicts is linked to an entrepreneur's psychological ownership over a venture combined with expectations concerning the angel investor–entrepreneur partnership. Whereas the results are in line with the hypothesized relationships, more research is needed to confirm its underlying mechanisms. Future research is also needed to explain the lack of effect for relationship conflicts. Given the importance of fit in the angel investor–entrepreneur relationship, I expected this to play a major role in their intentions to exit, but the results did not confirm this. Does it matter to entrepreneurs and investors whether they get along? Is there only a minimum level of fit needed for this partnership to work? Second, this study should serve as a first step to further extend the investor and entrepreneurial exit frameworks to include the context in which they are situated. Although this study revealed the importance of conflict dynamics, important factors to be included in future studies could be other behavioral processes such as cohesion, potency, and efficacy as well as power distribution, communication processes, or the degree of fit or match between investors and entrepreneurs. Finally, although the focus of this research was on angel investors, it would be interesting to determine whether the findings apply to other stakeholders such as family members and venture capitalists. The latter are generally considered more rational (professional) than their angel investing counterparts. Therefore, one would implicitly assume that relational aspects would matter less in their exit decision–making process. However, several studies have already indicated that venture capitalists are not always the rational decision–making agents we make them out to be (e.g., Franke et al., 2006) and are also subject to human flaws such as biases and interpersonal dynamics.

Finally, this paper also has several practical implications. These findings suggest that both entrepreneurs and angel investors should pay careful attention to conflicts that may arise between them. The most important conflicts to be avoided are those resulting from the divergence of entrepreneurs’ and angel investors’ objectives. This can result in the exit of one or both parties, which, if it is premature, is less than desirable for both. Beginning the relationship with highly aligned goals, being clear about these goals, and upholding goal alignment throughout the entire relationship should substantially reduce the likelihood of goal conflicts arising subsequently. Further, it is important for both investors and entrepreneurs to recognize that, although their relationship represents a business partnership, they are dealing with human beings, not robots or money–dispensing machines. Angel investors who tend to rely heavily on their entrepreneurs to develop the venture (Fiet, 1995) should carefully craft their post–investment involvement to avoid intimidating entrepreneurs. Although advice may be well intentioned, entrepreneurs may perceive it as meddling and feel threatened. To avoid these potentially deleterious effects, entrepreneurs and angel investors may want to consider the importance of crafting a setting where debate is open–minded and welcome (Jehn & Bendersky, 2003).

Conclusion

Venture exit is a key event for both angel investors and entrepreneurs, one that represents the end of their partnership. Although they are generally treated separately, the findings of this research suggest that these literatures should be integrated to focus on the angel investor–investee dyad and its potentially dysfunctional dynamics, that is, conflict. I demonstrate that goal conflicts between angel investors and entrepreneurs positively affect both parties’ intentions to exit their ventures and that task conflicts increase entrepreneurs’ intentions to exit. Thus, this study extends the entrepreneurial and investor exit literature in three ways: (1) by integrating and corroborating the importance of the relationships entrepreneurs and angel investors develop with each other, that is, with their key partners or stakeholders; (2) by shedding more light on the behavioral processes that lead to entrepreneurial and investor exit; and (3) by examining the effect of shared group processes on entrepreneurial and angel investor intentions to exit separately, thereby providing a view of the unique character of each.

Footnotes

1.

In both cases I refer to exit from a particular deal, not from entrepreneurship or angel investing in general.

2.

This approach can be distinguished from the cooperative and competitive goal approach adopted by Tjosvold and his colleagues by the fact that they define cooperative and competitive goals as the perception thereof. In other words, when team members perceive their goals to be positively or cooperatively linked, conflicts can be constructive to team effectiveness through increased mutual trust, positive attitudes toward other team members, and open–minded debate (Deutsch, 1973; Tjosvold, 1998). Perceptions of competitively or negatively linked goals will lead to the opposite. Furthermore, this approach is also distinct from goal conflict as referred to by Higashide and Birley (2002) because they neither conceptualize nor measure this in terms of actual goal incompatibilities.

3.

During the data collection process for the Global Entrepreneurship Monitor in Belgium, an additional question was asked to respondents regarding whether they had made investments that were not family– or friend–related.

4.

This includes companies that I was not able to contact and hence whose angel–backed nature could not be verified.

5.

This correlation coefficient is based on Belgian data only because this question was not included in the U.S. questionnaire.

6.

Median Rwg(J) values were also calculated based on triangular and moderately skewed distributions instead of the generally used uniform null distribution (LeBreton & Senter, 2008). These values all exceed the .7 threshold, thus confirming adequate within–group agreement for aggregation. Because angel investors and entrepreneurs could be argued to form subgroups within their overarching teams, aggregation statistics were additionally calculated at the subgroup level. ICCs and Rwg(J) values all exceed threshold values.

7.

As defined in accordance with sample requirements.

8.

The number of low–performing, that is, distress, exits was too low to run the model. However, statistical results were stronger in the overall exit model than in the high–performing exit model (angel investor: p < .10; entrepreneur: p < .05), which would suggest that intentions to exit are also reliable predictors of low–performing exit.