Abstract

Although previous research shows that corporate spin–offs contribute to economic growth, few studies link growth to the type of corporate spin–off. We distinguish between three types of corporate spin–offs: incumbent–backed, opportunity, and necessity spin–offs. Using empirical data on 46 corporate spin–offs in Flanders, we find that opportunity spin–offs outperform the other two types. By identifying the type of corporate spin–offs, this study aims to add to our knowledge on the relationship between spin–off type and firm growth.

Introduction

Corporate spin–offs are an important way for industry incumbents to exploit opportunities in unfamiliar markets or technologies (Covin & Miles, 1999; Kuratko & Audretsch, 2009; Sharma & Chrisman, 1999). These opportunities arise from the firms’ technology and knowledge bases and are exploited for growth– and advantage–seeking purposes, thereby contributing to the incumbent's (the parent firm's) competitive advantage (Ireland, Covin, & Kuratko, 2009). Corporate spin–offs are supported by their parent firms through formal affiliations (Zahra, 1996). However, not all corporate spin–offs are the result of opportunities exploited by incumbents. Industry incumbents with abundant but underexploited knowledge provide opportunities for spin–off formation by employees (Agarwal, Echambadi, Franco, & Sarkar, 2004). In these types of ventures, employees pursue opportunities that originate in the incumbent but the resulting spin–off is not backed by the incumbent. This type of corporate spin–off is not the result of the incumbent's decision to exploit an opportunity; it is established by employees leaving the incumbent. This type of spin–off does not receive formal organizational sponsorship (Zahra, 1993). Adverse developments in the incumbent firm may also prompt an employee or employees to leave and start up their own company (Buenstorf, 2009). Events such as changes in management, takeovers, or bankruptcy of the incumbent firm have been shown to be potential drivers of corporate spin–offs. Thus, corporate spin–offs are a heterogeneous population of companies created by incumbents or by employees who leave the incumbent firm.

Different types of corporate spin–offs have different founding conditions. For example, ventures created by incumbents do not necessarily imply the involvement of entrepreneurs. The incumbent may install a professional management team to run the venture according to a corporate plan. In contrast to firms created by ex–employees, these spin–offs are backed by and receive support from the parent firm after founding (Evald, Clarke, & Jensen, 2009). The differences in the founding conditions of these types of corporate spin–offs may have a differential influence on how firms develop over time (Bamford, Dean, & McDougall, 2000; Boeker, 1989). Research suggests that the conditions of the firm at start–up influence its value creation, which is associated with either product– or capacity–building growth (Clarysse, Bruneel, & Wright, 2011). Surprisingly few studies consider the heterogeneity of corporate spin–offs in relation to growth. For instance, previous research has developed taxonomies of corporate spin–offs based on their knowledge relatedness with the incumbent firms, but do not consider the implications of this for growth (Parhankangas & Arenius, 2003). Other work examines the survival rate of spin–offs created by ex–employees and incumbent–backed entrants, but does not consider whether differences in these types of corporate spin–offs have an influence on growth (Agarwal et al., 2004). Some scholars have studied the influence of relatedness between the corporate spin–off and the incumbent, on sales growth in the corporate spin–off (e.g., Sapienza, Parhankangas, & Autio, 2004) or profitability (e.g., Davis, Robinson, Pearce, & Park, 1992). Arguably, a corporate spin–off that is supported by a parent firm will experience different growth compared with a spin–off that receives no support from an incumbent, and is created by an entrepreneurially motivated individual. Agarwal et al. (2004) suggest that it is important for future research to determine the effects of spin–off formation on performance consequences. The present study addresses the following research question: “What is the impact of corporate spin–off type on the firm's subsequent growth?”

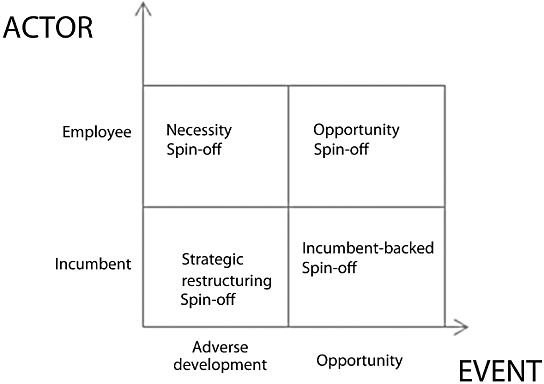

Building on recent developments in the literature on growth, we distinguish between employment growth and revenue growth, the most common indicators of firm growth (Wiklund & Shepherd, 2003). Our results suggest that, on both growth indicators, spin–offs resulting from the exploitation of an opportunity by employees outperform corporate spin–offs initiated by incumbent firms and spin–offs that are the result of unfavorable developments in the incumbent. This paper contributes to the literature on corporate entrepreneurship by examining the growth of different types of corporate spin–offs. We develop a typology of spin–offs based on two dimensions identified in the literature on corporate spin–offs. The first relates to the nature of the actor that starts the spin–off: incumbent firm or employee(s). The second dimension is the event that triggers the formation of the spin–off: an opportunity or adverse developments in the parent company. Thus, our study includes necessity spin–offs (i.e., the creation of a spin–off in response to an adverse development in the parent firm) which have received significantly less attention in the literature than incumbent–backed and opportunity spin–offs (Buenstorf, 2009).

We contribute also to the literature on growth that calls for a more diversified approach to the study of firm growth (Delmar, Davidsson, & Gartner, 2003). Previous research uses employment and revenue growth interchangeably, but these indicators represent different phenomena and processes (Gilbert, McDougall, & Audretsch, 2006). Since the founding conditions of the firm influence its development over time, we demonstrate that incumbent–backed, opportunity, and necessity spin–offs follow different growth paths. In the Background and Hypotheses section, we develop a categorization of spin–offs and develop hypotheses about how the different categories of corporate spin–offs are related to employment and revenue growth, respectively. The Data and Method section describes the data and method used to test our hypotheses and the results section follows. The final section provides a discussion of the implications of our findings for the corporate entrepreneurship and growth literature, and suggests some potential avenues for future research.

Background and Hypotheses

Categorization of Corporate Spin–Offs

We develop a categorization based on the event that triggers the formation of the spin–off (opportunity or adverse developments) and the actor that creates the company (incumbent or employee) (see Figure 1). 1 The entrepreneurship literature suggests that new businesses originate from the exploitation of opportunities (Shane & Venkataraman, 2000). The recognition of opportunities requires prior knowledge and information about markets, ways of serving these markets, and customer problems (Shane, 2000). The literature on corporate venturing reinforces this and defines a corporate spin–off as a new business based on ideas and discoveries developed in the incumbent organization (Narayanan, Yang, & Zahra, 2009). Within this perspective, the incumbent organization creates the new business to exploit opportunities in unfamiliar or unknown markets, based on their technology and knowledge developments, to achieve additional growth and/or advantage (Covin & Miles, 1999; Ireland et al., 2009; Kuratko & Audretsch, 2009). Corporate spin–offs enable incumbent organizations to exploit new opportunities and are considered to be an important driver of new business in ongoing enterprises (Hitt, Nixon, Hoskisson, & Kochhar, 1999). Spin–offs enable incumbents to experiment with new technologies and business practices that would not be possible within the parent firm due to internalization impediments (Keil, Autio, & George, 2008). These spin–offs are often carefully nurtured by the incumbent firms because they represent important sources of future growth for these firms.

We thank an anonymous reviewer for this suggestion.

Categorization of Corporate Spin–Offs 2

Firms created by incumbents as a result of an adverse development, that is, divesting an old business in mature or declining markets, have been described also as “strategic restructuring spin–offs” (e.g., Parhankangas & Arenius, 2003). We follow Narayanan et al. (2009) and do not consider restructuring spin–offs in this paper since they do not represent new business based on ideas or discoveries developed in the incumbent organization.

Incumbents maintain formal linkages with their spin–offs through equity or license agreements (Parhankangas & Arenius, 2003). The incumbent's ongoing participation in the spin–off allows it to identify future capability development needs. Related knowledge between the two organizations can enhance the corporate spin–off's ability effectively to evaluate the value of external knowledge, discard irrelevant knowledge, and assimilate new knowledge into their operations (Grant, 1996). Prior research shows that spin–offs start from a position of relative advantage compared with independent start–ups, because they inherit routines and procedures that have been developed in the incumbent (Phillips, 2002). Also, incumbent firms provide support to their spin–offs by allowing access to their resources and infrastructure (Zahra, 1996). Following Agarwal et al. (2004), we label this type of corporate spin–off an “Incumbent–backed spin–off.”

Not every technology or knowledge–based opportunity is exploited by the incumbent firm. Evidence on the automobile (Klepper, 2007), laser (Klepper & Thompson, 2006), semiconductor (Braun & MacDonald, 1978), and disk drive (Christensen, 1993) industries, for example, show that entrepreneurial ventures set up by former incumbent firm employees are widespread. Bhidé (2000) finds that the majority of the firm founders he studied exploited ideas identified while working for their previous employers. In contrast to Incumbent–backed spin–offs, these ventures were based on knowledge accumulated by their owners in the course of previous employment and were not supported by formal relationships with the incumbent firms (Agarwal et al., 2004).

Previous employment often facilitates the identification of entrepreneurial opportunities for new business set up (Schoonhoven & Romanelli, 2001). Former employees may have worked on the development of product and market ideas and built networks of contacts that subsequently lead to the identification of an opportunity and are the motivation for the establishment of a spin–off. Rather than sharing their ideas with the incumbent company, these employees exploit the opportunities independently of their employer (Anton & Yao, 1995; Klepper, 2001). Some employees may have ideas for launching a new activity but may receive no support from the incumbent company, leaving them frustrated (Hellmann, 2007). The incumbent company, for its part, may decide against trying to capitalize on a new idea for budgetary reasons, and may prioritize existing projects over new opportunities, or simply be unable to exploit every opportunity that arises (Moore & Davis, 2004). Employees may be unrealistically optimistic about their idea (Amador & Landier, 2003) and be frustrated by their employers’ unwillingness to provide them with resources and time to pursue what they see as a promising opportunity (Klepper, 2001; Porter, 1980). As a result, they may choose to leave their firms to independent companies (Wright, Hoskisson, & Busenitz, 2001). The importance of these spin–off ventures has been acknowledged increasingly (Agarwal et al., 2004; Chatterji, 2009). We label this type of corporate venture the “Opportunity spin–off” (Buenstorf, 2009).

Other triggers for spin–off activity by ex–employees include developments in the incumbent company that make continued employment there less attractive or even impossible for them. Internal disagreements over the commercial potential of projects or the firm's strategic direction are important drivers of spin–off formation (Klepper & Thompson, 2010). The decision of incumbent firms to discontinue research projects can be the trigger for disappointed researchers to leave the incumbent and start their own firms. Acquisition of an incumbent firm may take the form of an adverse “shock” and increase the chances of spin–off formation by employees (Klepper & Sleeper, 2005). Acquisitions commonly result in a reorganization within the firm, which may lead to less autonomy or divestiture of certain activities which are seen as redundant and no longer in line with the strategic direction of the acquiring firm. Finally, involuntary exit of the incumbent company through bankruptcy can be an important factor influencing the creation of spin–off companies. Eriksson and Kuhn (2006) show that a significant group of corporate spin–off creation is “pushed” by the bankruptcy of the incumbent, rather than “pulled” by the identification and exploitation of new opportunities by employees. We label this group “Necessity spin–offs” (Buenstorf, 2009).

The Link between Corporate Spin–Off Type and Growth

We develop hypotheses that link different types of corporate spin–offs to growth. We argue that the resources of Incumbent–backed spin–offs will grow more than the two other types in the first years after spin–off. Incumbent–backed spin–off firms are created by larger incumbent organizations which maintain an institutional relationship with the spin–off. This relationship can be used to mobilize the incumbent's resources. In addition to the direct effects on resource accumulation, Incumbent–backed spin–offs also may enjoy some indirect effects in the form of reputation spillovers from the incumbent. Previous research shows that firms with linkages to established organizations are endowed with higher status and greater legitimacy (Meyer & Rowan, 1977), which, in turn, facilitate the acquisition of external resources that are financed by risk capital and provide more opportunities to access resources that otherwise would be beyond the firm's reach (Pfeffer & Salancik, 1978). Large companies often collaborate closely with private venture capitalists to co–finance spin–offs as part of their corporate venturing programs (Hill, Maula, Birkinshaw, & Murray, 2009).

Opportunity and Necessity spin–offs are the result of an opportunity exploited by an employee or an adverse development in the incumbent firm and thus do not benefit from the direct and indirect effects of being formally affiliated with an established company (Larson, 1992). As independent companies, Opportunity and Necessity spin–offs have to build credibility in order to attract employees and investors. In sum, the formal relationship between Incumbent–backed spin–offs and their incumbent organizations gives them an advantage over Opportunity and Necessity spin–offs to attract and accumulate resources. We hypothesize therefore that:

Incumbent–backed spin–offs are created by incumbents to explore new product–market combinations. These corporate spin–offs develop and bring to market new technologies that are not part of the incumbent's core strategy. These technologies are often radical innovations that are new to the market, which means that their market opportunities are unclear (Parhankangas & Arenius, 2003). Their development time can be long, and it may be 10 to 15 years before the first product is launched (Agarwal & Bayus, 2002). Consequently, considerable investment of resources is required to translate these technologies into market–ready products. The economic benefits of corporate spin–offs requiring expensive and risky investments in new R&D or new product development may not be apparent in the short run and may require several years to come to fruition (Zahra & Covin, 1995). It is likely, therefore, that Incumbent–backed spin–offs will grow in terms only of capacity or resources after start–up, and it may be several years before sales are realized.

Adverse developments at incumbent firms triggering the establishment of Necessity spin–offs may have a direct negative influence on the firm's ability to increase revenue. One type of adverse development which may lead to the founding of a Necessity spin–off is a divestment by the incumbent, or bankruptcy. An important driver of the decision to divest a division is weak performance or limited growth prospects based on operation in unviable or unattractive markets (Hamilton & Chow, 1993; Porter, 1980; Whitney, 1996). Another trigger for the creation of a Necessity spin–off may be the acquisition of the incumbent by another company. On acquisition, the previous organization may have imposed changes to the organizational culture and be faced with a restructuring of its activities. Although the resulting spin–offs are new companies, they continue the former incumbent's activities. This means that the Necessity spin–off and the acquired firm may become direct competitors, targeting the same market. It is likely that the acquiring firm will use its stronger resource base and greater status to counter this competition, making it difficult for the Necessity spin–off to increase its revenue and capture market share.

In contrast, Opportunity spin–offs are created by employees keen to embrace a market opportunity. Unlike Incumbent–backed spin–offs, Opportunity spin–offs have no corporate involvement or heavy political or business corporate objectives. The involvement of the incumbent may cause Incumbent–backed spin–offs to suffer from organizational inertia, but Opportunity spin–offs are free to move quickly and decisively and to deploy new knowledge routines (Rosenbloom & Christensen, 1994). Opportunity spin–offs are likely to be created by entrepreneurial employees (Agarwal et al., 2004), which endow their firms with the traits needed to compete in high–tech environments (Moriarty & Kosnik, 1989). This type of spin–off will enjoy higher levels of market pioneering know–how (Agarwal et al., 2004) based on bringing the innovation to market, and the capabilities to commercialize innovations ahead of the competition. Building on this, we hypothesize that Opportunity spin–offs grow faster in terms of revenue than the other two types.

Data and Method

Sample

To test our hypotheses, we use a sample of corporate spin–offs in Flanders, Belgium. We define a corporate spin–off as “a separate legal entity that is concentrated around activities which were originally developed at an incumbent firm, and which is concentrated around a new business, with the purpose to develop and market new products or services based upon a proprietary technology or skill” (Van de Velde, Zahra, & Clarysse, 2006, p. 8). Flanders is a small, export–intensive economy, and an emerging high–tech region, located in the Northern part of Belgium (Cantwell & Iammarino, 2001). By focusing the research on a particular region, Flanders, we reduce unobserved heterogeneity between firms, resulting from variance in environmental conditions. In this study, we focus on high–tech sectors, since several researchers indicate that these sectors are fast moving; in other words, new technologies and new products are introduced at high speed (Bower & Christensen, 1995; Christensen, 1997). High–tech sectors, therefore, are characterized by corporate spin–offs started by incumbent firms (e.g., Parhankangas & Arenius, 2003) and by employees (e.g., Chatterji, 2009).

Since we are interested in corporate spin–offs set up by incumbent firms and former employees, we start with a large dataset of young, technology–based firms in Flanders. The original sample consists of almost all the companies founded in Flanders between 1991 and 2002 (205 firms) (Heirman, 2004). A young, technology–based firm is a new business start–up that develops and markets new products or services based on proprietary technology or skills. We exploited four databases to identify these firms: (1) a list of spin–offs from public research organizations in Flanders; (2) the portfolios of venture capitalists active in early–stage investment and located in Flanders; (3) the IWT database (IWT is a government agency that provides R&D subsidies to Flemish small and medium sized enterprises); and (4) a random sample drawn from the population of companies active in high–tech and medium high–tech sectors. From this sample, we identified 48 corporate spin–offs, representing 23.4% of the original sample of 205 young, technology–based firms.

Data Sources

We conducted initial face–to–face interviews with founders/CEOs and members of senior management teams in 2001–2003, and conducted follow–up interviews in 2005. In the first round of interviews, we targeted founders/CEOs, since they typically possess the most comprehensive knowledge of the organization's history, strategy, processes, and performance (Carter, Stearns, Reynolds, & Miller, 1994). In the second round of interviews, we talked to members of the top management team to gain richer insights. Two corporate spin–offs interviewed in the first round withdrew from the research project, leaving a final sample of 46 corporate spin–offs. The response rate is much higher than typical response rates reported in entrepreneurship research, mainly because we chose to conduct personal interviews with founders/CEOs and members of the management team at their firms’ premises rather than administering postal or telephone surveys. During the interviews, we focused on the circumstances surrounding the firm's creation and the relationship with the incumbent company. We collected information on spin–offs’ resources, market characteristics, and success and growth at time of founding and at the time of the interview. Additional information on the spin–off was collected using secondary data sources, such as web sites, brochures and press releases, both internal and external to the company. We extracted financial data from company balance sheets, available from the National Bank of Belgium.

Measures

Dependent Variable

The appropriate operationalization of growth in the context of new firms has been the subject of considerable debate (see Davidsson, Achtenhagen, & Naldi, 2007, for a review). Although revenue growth is the most widely used measure, firms can only realize sales if they have a product or service available. Therefore, the accumulation of resources and knowledge in order to develop products and bring them to the market might be more important for the initial stages of new ventures. The dependent variable in this study is growth of resources or revenues, because each represents different underlying phenomena and processes (Gilbert et al., 2006). In the resource–based and knowledge–based views of the firm (Barney, 1991; Kogut & Zander, 1992), employment growth is a proxy for resource and knowledge accumulation. Revenue growth is an indicator of successful market entry (Autio, Sapienza, & Almeida, 2000), that is, acceptance of the product in the market. We use annual absolute growth to measure employment growth. We define annual absolute growth in employment as the number of the firm's current employees (full–time equivalents [FTE]) minus the number of employees at firm founding (FTE), divided by company age. This provides an indication of linear employment growth (Heirman & Clarysse, 2005). We used a similar operationalization for the growth in revenues.

Independent Variable

We classify the spin–offs in the sample into “Incumbent–backed,”“Opportunity,” and “Necessity” spin–offs using a two–step process. We started by categorizing firms based on the actor that created the spin–off and the event that triggered the firm's formation. We asked an independent researcher to read the transcripts of the original interviews and make a categorization of the firms. We cross–checked our categories with those of the independent researcher before rechecking against the original interview and secondary data to ensure consistent categorization. First, we determined whether the opportunity to create the spin–off was identified and exploited by the incumbent firm, based on the existence of a formal relationship between the incumbent and the spin–off (i.e., equity participation in or a license agreement with the spin–off). A total of 15 corporate spin–offs met this criterion and thus are categorized as “Incumbent–backed spin–offs.” Second, we further refined the remaining 31 spin–offs, created by ex–employees without formal involvement of the incumbent, into “Opportunity” and “Necessity” spin–offs.

Building on Buenstorf (2009), we identified 12 “Necessity spin–offs” created in response to adverse developments in the incumbent firm. Of these, six spin–offs were created because a development project was discontinued by the incumbent, and four were triggered by the incumbent firm being acquired. The last two Necessity spin–offs were founded by employees in response to the incumbent firm's bankruptcy. Finally, we identified 19 cases of spin–off foundation based on an employee identifying and exploiting a new opportunity and leaving the incumbent firm to set up a new company; these are categorized as Opportunity spin–offs. In this coding scheme, the corporate spin–off categories are mutually exclusive (see Figure 1). To test hypothesis 1, we created a dummy variable that is coded 1 if the firm is an Incumbent–backed spin–off and 0 otherwise. To test hypothesis 2, we created a dummy variable that takes the value 1 if the firm is categorized as an Opportunity spin–off and 0 otherwise.

Control Variables

As controls, we include a number of variables that the literature suggests influence growth. At firm–level, we include measures for the business experience of the founding team and the age of the spin–off. In line with previous research (Cooper, Gimeno–Gascon, & Woo, 1994; Roberts, 1991), we control for the firm's human capital, represented by management know–how and the experience of the founder and/or founding team. We operationalize this measure as the total number of years of management experience across all the members of the founding team. We control also for the age of the corporate spin–off, calculated as the number of years since founding, to proxy for the firm's accumulated resources and knowledge stock. We include two variables—technological relatedness and market knowledge relatedness with the incumbent firm—to capture the extent to which the corporate spin–off shares knowledge with the incumbent firm. Corporate spin–offs that share more knowledge with the incumbent start from a larger knowledge base at founding and may capitalize on existing capabilities and routines (Hamel, 1991). Unrelated ventures, on the other hand, have to build their own knowledge base and identify and develop new capabilities, a process that requires considerable resources, management skill, and time. The operationalization of these variables is modeled on Parhankangas and Arenius (2003) and consists of three items per variable. The Cronbach's alpha is 0.79 for technological relatedness and 0.82 for market relatedness. Finally, we include a dummy variable to control for the influence of any industry effects, which is coded 1 if the firm operates in the information and communication technology sector and 0 otherwise.

Results

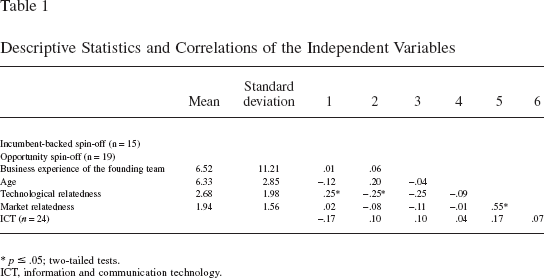

Table 1 provides an overview of the descriptive statistics of the independent variables and reveals some interesting differences between Incumbent–backed and Opportunity spin–offs. The former are associated with higher technology relatedness but not market relatedness, with the incumbent. This indicates that Incumbent–backed spin–offs use technology developed within the boundaries of the incumbent, but target markets that are unfamiliar to the incumbent. This finding is in line with our conceptualization of this type of spin–off. Opportunity spin–offs, on the other hand, commercialize technologies that generally are unrelated to the technology base of the incumbent firm, and confirm the characteristics described above. The correlation between technology and market relatedness is relatively high (.55). We examined the variation inflation factors (see Table 2) and found that a high correlation does not affect the interpretation of results (Neter, Wasserman, & Kuther, 1990).

Descriptive Statistics and Correlations of the Independent Variables

p ≤ .05; two–tailed tests.

ICT, information and communication technology.

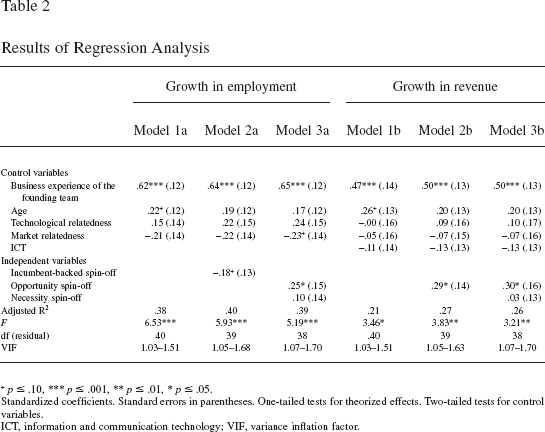

Results of Regression Analysis

p ≤ .10

p ≤ .001

p ≤ .01

p ≤ .05.

Standardized coefficients. Standard errors in parentheses. One–tailed tests for theorized effects. Two–tailed tests for control variables.

ICT, information and communication technology; VIF, variance inflation factor.

Table 2 reports the results of the multiple regression analysis. We hypothesized that Incumbent–backed spin–offs grow faster in terms of employment than the other two types of corporate spin–offs. The coefficient for Incumbent–backed spin–offs is negative and moderately significant (beta = −.18, p ≤ .10), so hypothesis 1 is rejected (Model 2a). Hypothesis 2 links the type of corporate spin–off to revenue growth. We argue that Opportunity spin–offs will show higher revenue growth rates compared with Incumbent–backed and Necessity spin–offs. Model 2b shows that this hypothesis is supported, indicated by the positive significant coefficient for Opportunity spin–offs (beta = .29, p ≤ .05). We examine also the economic effect sizes of our findings. Additional analysis shows that Incumbent–backed spin–offs grow by 2.06 FTE per year. This is much lower than employment growth in the other two types of corporate spin–offs (4.72 FTE). We find also that in Opportunity spin–offs, revenues increase by more than half a million Euros annually, twice the level of revenue growth in Incumbent–backed and Necessity spin–offs. 3 Models 3a and 3b include Opportunity and Necessity spin–offs (as employee driven); Incumbent–backed spin–offs are the control group. The results show that Opportunity spin–offs grow more than Incumbent–backed spin–offs in terms of both employment (beta = .25, p ≤ .05) and revenue (beta = .30, p ≤ .05), but that growth in employment and revenue by Necessity spin–offs is not significantly different from the control group. Apart from the business experience of the founding team, most of the control variables show weak influence on the dependent variables in our models. Older companies show stronger growth in employment and revenue. Finally, we find that market relatedness has a moderately significant negative influence on employment growth.

Additional analyses show that differences in employment growth between the types of spin–offs are not significant but the differences in revenue growth are moderately significant (p < .10).

Discussion

Traditionally, corporate spin–offs have been regarded as important mechanisms for industry incumbents to exploit opportunities that do not fit with their strategic direction. We described this type of spin–off as Incumbent backed since the firms maintain a formal relationship with the incumbent, from which they receive ongoing support. However, for strategic or budgetary reasons, incumbents may not be able to exploit all potential opportunities, or simply may fail to recognize them. These opportunities can be taken forward by employees who leave the incumbent firm to start their own ventures. These Opportunity spin–offs are the result of employees identifying and exploiting an opportunity. Some studies suggest that adverse developments in the incumbent, such as acquisition or bankruptcy, can motivate employees to create corporate spin–offs (Buenstorf, 2009). While the importance of Opportunity spin–offs has been increasingly acknowledged, Necessity spin–offs have received less attention. In this study, we link the type of corporate spin–off—Incumbent backed, Opportunity, and Necessity spin–off—to growth. By distinguishing between growth in employment and growth in revenues, we respond to recent calls in the literature not to use these indicators of growth interchangeably (Gilbert et al., 2006). Growth in employment is an indicator of resources and knowledge accumulation; revenue growth is an indicator of successful market entry. Previous research on firm growth generally ignores these differences and uses the indicators alternately (Delmar, 1997; Weinzimmer, Nystrom, & Freeman, 1998). We contribute to the literature by building arguments that the founding conditions, represented by the actor that creates the firm (incumbent or employee), and the event that triggers spin–off formation (opportunity or adverse development), will affect the nature of subsequent firm growth.

We hypothesized that in Incumbent–backed spin–offs, employment would grow faster than in Necessity spin–offs and Opportunity spin–offs; however, our results suggest the reverse is true and employment increases less in Incumbent–backed spin–offs than the other two types. On rechecking our interview data, we found that Incumbent–backed spin–offs are often already quite large at start–up. For example, one of the incumbents spun off a whole unit of 30 people, while another spun off an entire computer science department of 25 people. Incumbents tend to spin off the entire unit that has been developing the new technology. This implies that Incumbent–backed spin–offs enjoy a quite elaborate pool of resources and knowledge from the moment of their creation. Their large size at start–up reduces the need to search for additional resources and knowledge. Also, as Incumbent–backed spin–offs progress in their development of a new technology, some researchers may become redundant, leading to negative employment growth. This was the case for one of our Incumbent–backed spin–offs—a developer of ERP–tools—where the CEO decided to fire several researchers after the company completed its first product. We hypothesized also that Opportunity spin–offs would grow faster in terms of revenue than Incumbent–backed or Necessity spin–offs. In this case, our hypothesis is supported, and additional analysis indicates that Opportunity spin–offs are also positively associated with employment growth. Our finding suggests that Opportunity spin–offs are important agents of knowledge creation represented by employment growth, and economic growth represented by revenue growth.

The entrepreneurship literature suggests a strong positive relationship between motivational traits and firm performance (e.g., Baum, Locke, & Smith, 2000), and entrepreneurial motivation is considered to be an important predictor of growth (Baum & Locke, 2004). Entrepreneurially motivated individuals are more prone to focus on opportunities and also are willing to commit resources to pursue them. In our context, it is likely that Opportunity spin–offs are created by founders that are more highly motivated and driven than the founders of Incumbent–backed and Necessity spin–offs. Opportunity spin–offs are the result of an opportunity pursued by former employees, which indicates that they may have greater entrepreneurial capital and ability (Agarwal et al., 2004). Incumbent–backed spin–offs, on the other hand, are created by incumbent organizations and run by managers who are evaluated according to how closely they adhere to a corporate plan. To some extent, these managers are less dependent for their livelihoods on the success of the spin–off, as on operating under the umbrella of the incumbent. The commitment of individuals to the success of their firms has been suggested to be an important factor for achieving growth (Gundry & Welch, 2001). Entrepreneurs must be willing to make sacrifices and work toward the growth of the company. The commitment of Incumbent–backed spin–off managers may be low since they are evaluated based on compliance with the corporate plan rather than the success of the spin–off. Taken together, this paper suggests a two–dimensional categorization of corporate spin–offs which is based on the interplay between the exogenous opportunity and the endogenous individual features such as the motivation of employees. Future research could apply this categorization to a multi–level analysis that includes the individual level, focusing on motivation, and the firm level, which is the opportunity or adverse development that gives rise to the spin–off.

Limitations and Future Research Directions

Although our study provides some new insights, it has some limitations that point to directions for future research. First, our data set is comprised only of corporate spin–offs located in Flanders. Although the focus on a single region reduces unobserved heterogeneity that might result from variance in environmental conditions, it raises the question of whether our results would hold in other environmental settings. Furthermore, the limited sample size might be influencing the results of our analysis. Future studies using larger samples in different environments would contribute to the validity and generalizability of our findings. Second, this study is cross–sectional in nature, which does not allow us to examine whether the imprinting effect of the type of corporate spin–off on firm growth fades over time, or to investigate its potential effects on firm survival. For example, it might be that the founding team changes over time as professional management is brought in to take the firm to the next level.

The performance differences between Incumbent–backed, Necessity, and Opportunity spin–offs suggest that these companies might follow very different growth trajectories. In future research, it would be interesting to create a longitudinal database of corporate spin–offs to test these effects. In particular, it would be interesting to examine how the development of resources and capabilities evolves in each type of spin–off. Our data do not allow us to examine the influence on growth of ownership distribution in the spin–offs, between incumbent firms, founders, and the CEO. Research suggests that the incentive and compensation structure for founders and CEOs has an important influence on subsequent firm performance (e.g., Mehran, 1995; Sanders & Boivie, 2004). Analyses that include the ownership distribution of top management team members and founders might provide additional insights into the comparative performance between different types of corporate spin–offs. Finally, we can conclude from this study that further insights are needed regarding the diversity of corporate venturing processes and their outcomes. Collecting data from incumbent companies would allow more in–depth examination of the relationship between incumbent and corporate spin–off. For example, scholars could study how, why, and which resources and knowledge are transferred to the spin–off and what is their impact on spin–off performance. Another interesting area for future research would be an examination of how the characteristics of the incumbent firm influence the growth of corporate spin–offs.

Conclusion

In this study, we examined the relationship between different types of corporate spin–offs and growth. In the literature on corporate spin–offs, most scholars presume that in corporate spin–off creation, the incumbent firm takes the lead. However, some point to examples of employees leaving their firms to pursue opportunities or adverse developments at the incumbent triggering the creation of a spin–off. So–called Opportunity spin–offs, which are initiated by one or more employees in order to exploit an opportunity identified while working for the incumbent firm, demonstrate the highest growth in revenue and employees. This finding underscores the importance of entrepreneurial drive for realizing firm growth. Our results suggest that established companies should pay more attention to bottom–up opportunities spotted by employees. Since corporate spin–offs are agents of innovation, policy makers should develop specific schemes to stimulate and support venturing programs within established companies.