Abstract

This article investigates how prior corporate venture capital (CVC) relationships between two firms affect the likelihood of their subsequently entering a strategic alliance. Creating a portfolio of CVC investments provides the investing firm with a set of opportunities that can be pursued once the technological and market uncertainty have been reduced. If the technology appears to be promising, a follow–on investment, such as a strategic alliance, is made to ensure the transfer of the technological knowledge. This article shows that prior CVC investments can play a role in the formation of strategic alliances and investigates the conditions under which they are most likely to do so.

Introduction

New business development is a risky and uncertain process. Particularly in the earlier stages of new business development, technological and market uncertainty are generally high. However, in order to benefit from so–called first–mover advantages firms may invest in new technologies early on (Agarwal & Gort, 2001). To cope with high levels of uncertainty, firms can make small initial investments to learn how to reduce technological and market uncertainty about the business opportunity. These early investments can be regarded as learning investments (Janney & Dess, 2004) and are intended to mitigate the uncertainty through studies on the technological and market feasibility of particular new ideas. Prior studies have pointed to the benefits of “real options reasoning” as a tool for decision making under uncertainty in research and development (e.g., Dixit & Pindyck, 1994; McGrath, 1997; Trigeorgis, 1996). Real options can be described in terms of option creation and option exercise. The former is the initial investment decision, whereas the latter can be described as the exercise (or follow–on investment) of the option created in the first stage. This second investment is likely to be larger than the investment made for option creation (Rosenberger & Eisenhardt, 2003; Tong, Reuer, & Peng, 2008). Real options theory suggests that under high levels of uncertainty (such as new business development), firms should make small initial investments (option creation) that can be exercised later on through a follow–on investment. When uncertainty decreases, the investing firm can decide about a possible follow–on investment. New technological ideas can be generated internally, in which case initial investments in research and development (R&D) take the form of internal R&D investments. However, firms can also source ideas externally. In that case, firms invest in external sourcing of knowledge. Making small investments to acquire more information about different (or even competing) technologies that reside outside the firm can be an effective way to create multiple options on technology (March, 1991). Once the investing firm has acquired more information about the business opportunities related to a new technology, it can decide to terminate the investment or increase its commitment through a subsequent and more substantial investment. In other words, these small initial investments can serve as a way to create the right, but not the obligation, to execute this option in the future (Folta, 1998).

One possible way for firms to get acquainted with new technological opportunities is the use of corporate venture capital (CVC) investments. CVC investments are small equity investments made in young start–up firms, which is an interesting strategy for accessing emerging technologies that may reside outside a firm's boundaries (Dushnitsky & Lenox, 2005a, 2005b; Zahra, 1996; Zahra & Covin, 1995). Being oriented toward the earlier stages of technology development, CVC investments are an attractive way of creating a portfolio of different options on technology while the investing firm can initially learn about the technological and commercial opportunities. If the technology turns out to be promising, a more substantial follow–on investment might take the form of a strategic alliance between the venture and one of the business units of the investing firm, or it may lead to the acquisition of the start–up by the corporate investor. Benson and Ziedonis (2009) have examined how CVC investments in early–stage start–ups lead to improved firm performance when corporate investors subsequently acquire the start–ups. However, research examining how technology alliances as a follow–on investment between the corporate investor and the start–up can warrant the co–development or the transfer of technological knowledge is scarce and has only recently captured the attention of some scholars. For example, Ozmel, Jeffrey, and Gulati (2011) study the likelihood of alliance formation between an incumbent firm and a new venture, depending on the new venture's affiliation with VCs. In addition, Wadhwa and Phelps (2011) conceptualize CVC investments as a compound option and investigate the effect of uncertainty resolution on the exercise of this option. Hence, in line with previous research, we examine how established firms, by investing in CVC activities, gain information about the technology developed by VC–backed start–ups, which in turn is crucial to set up successful technology alliances with these start–ups (McNally, 1997; Sykes, 1990).

Following the reasoning presented earlier, it can be argued that strategic technology alliances are complementary to CVC investments, because they provide the opportunity for firms to further develop projects as they move through the innovation funnel. Different stages of development inherently involve different levels of uncertainty (e.g., future potential), but they also require different types of governance modes since the commercial value of technologies only gradually becomes clear as the venture moves through innovation stages (Chesbrough, 2003; Van de Vrande, Lemmens, & Vanhaverbeke, 2006). However, despite the increased attention to CVC investments as a way to spur innovation, the literature has been relatively silent on the dynamic nature of this type of investment and how a venture capital relationship may evolve into a strategic alliance when technologies become less risky. In order to shed light on the way firms try to cope with high levels of uncertainty in their new business development process, it is important to investigate the sequence firms follow in their technology sourcing strategy. Therefore, we address this gap in this study by focusing on the likelihood of firms entering a strategic alliance with prior CVC partners.

The contributions of this article are threefold. First, by shedding light on the dynamics of CVC, this article contributes to the growing body of literature on CVC and corporate venturing (e.g., Basu, Phelps, & Kotha, 2011; Hill, Maula, Birkinshaw, & Murray, 2009; Schildt, Maula, & Keil, 2005; Yang, Narayanan, & Zahra, 2009). Second, we contribute to the innovation management literature by emphasizing the importance for firms to engage in different types of external knowledge sourcing at different stages of the technology development. Although prior studies have stressed the importance of CVC investments for innovation (e.g., Dushnitsky & Lenox, 2005a; Keil, Maula, Schildt, & Zahra, 2008; Wadhwa & Kotha, 2006), and the role of CVC investments in the emergence of alliance networks (Dushnitsky & Lavie, 2010), they have not yet looked at the dynamic nature of these types of investments on a dyadic level. Finally, by studying the likelihood of CVC investments evolving into a more integrated mode of governance, this article contributes to real options theory (Bowman & Hurry, 1993; Folta, 1998; McGrath, 1997).

The remainder of this article is organized as follows. The next section provides a theoretical background concerning CVC investments and strategic alliances and the likelihood of firms entering a strategic alliance with a prior CVC partner. Next, we will examine the factors that affect the extent to which a follow–on investment through a strategic alliance is most likely to occur. Consistent with real options reasoning, we focus on different types of uncertainty, such as partner uncertainty, technological uncertainty, and market uncertainty (Tong & Li, 2011). Next, we develop hypotheses about the effects of partner uncertainty, technological uncertainty, and market uncertainty on the likelihood of a follow–on alliance being established. The hypotheses will be tested empirically using a sample of CVC investments and strategic alliances made by large firms in the pharmaceutical industry. The article concludes with a description and discussion of the main results, followed by some avenues for future research in this area.

Theory and Hypotheses

Real options theory suggests that firms are better off making small initial investments (option creation), thereby postponing the investment decision until initial learning investments have reduced the uncertainty to an acceptable level (Folta, 1998). These initial investments in new technology may take the form of CVC investments in a new venture (Benson & Ziedonis, 2009; Van de Vrande et al., 2006). Using CVC investments to invest in a number of emerging technologies has the advantage that it enables firms to create a set of strategic options for the future (Gompers & Lerner, 2000). CVC investments can be viewed as a way for established firms to identify and value emerging technologies developed by VC–backed start–ups (Benson & Ziedonis). These early–stage technologies are notoriously difficult to value because of technological and market uncertainty on the one hand, and relationship–specific uncertainty on the other. Once uncertainty has decreased to an acceptable level through the CVC investment, firms can decide to increase their level of commitment (option exercise). One way in which firms can do this is by establishing a strategic alliance with the venture to further facilitate the transfer of technological knowledge (Gulati, 1998). Real options theory thereby focuses on uncertainty as a determinant for the decision to further invest in a particular technology. Option creation through prior CVC investments is thus one way to cope with uncertainty related to a new business opportunity.

Uncertainty in real options reasoning manifests itself in many forms. With regard to technology sourcing and investment in R&D, the most common sources of uncertainty are partner uncertainty (Majd & Pindyck, 1987; Roberts & Weitzman, 1981), technological uncertainty (Kogut, 1988; Santoro & McGill, 2005; Williamson, 1985), and market uncertainty (Hoskisson & Busenitz, 2002; Roberts & Liu, 2001).

Partner uncertainty can be reduced by increasing the number of investment rounds that a corporate investor participates in. In this case, CVC investments are regarded as compound options—each new investment creates new options for the future (Trigeorgis, 1996). CVC investments are also instrumental in identifying and valuing the emerging business opportunities in VC–backed start–ups. Technological and market uncertainty in these early–stage ventures are very high and thus do not justify major financial investments at that point in time. CVC investments can be viewed as a first step (or series of steps) in acquiring more information to deal with the uncertainties related to the technology and market opportunities (Guler, 2007). However, established firms can mitigate these risks by investing in start–ups with more “common technological ground” and by avoiding early–stage investments. The concept of technological proximity explains the amount of overlap or common technological ground between the start–up and the investing company's technology portfolios. Technological uncertainty is easier to deal with when companies are familiar with each others’ technology (Nooteboom, Vanhaverbeke, Duysters, Gilsing, & Van den Oord, 2007; Puranam, Singh, & Chaudhuri, 2009). Stage of investment, on the other hand, refers to the maturity of the venture and hence to the amount of both technological and market uncertainty embedded in the investment (Dimov & Murray, 2008). Established firms can choose in which stage of investment they want to be active, thereby controlling the level of uncertainty they want to take.

In the sections that follow, we will explain the differences between CVC investment and strategic alliances, and how prior CVC investments in a firm may lead to strategic alliance formation between the two companies. Next, we will investigate more closely the different types of uncertainty and how they may affect the likelihood of a strategic technology alliance formation after an initial CVC investment.

CVC Investments and Strategic Alliances

Studies investigating the underlying reasons for firms to be involved in CVC investments have pointed to a range of different motives. These include getting a window on new technology, creating strategic value for the firm, identifying possible acquisition targets, and delivering financial return (Chesbrough, 2002; Dushnitsky & Lenox, 2005a, 2006; Keil, 2002; Siegel, Siegel, & MacMillan, 1988). For example, Siegel et al. found that the major objectives included “return on investment” and “exposure to new technologies and markets.”Chesbrough also distinguished among financial and strategic objectives to invest in promising start–up companies. Other studies (e.g., Chesbrough, 2000) argued that firms that engage in CVC, primarily for strategic reasons, are more successful than others (Dushnitsky & Lenox). Taken together, most of these studies point to getting access to new technologies in an early stage of development as an important driver behind corporate investments in start–up firms.

While new business development is a risky and uncertain process, investing early on in new knowledge and technologies can be necessary to get early access to new knowledge, which in turn can lead to first–mover advantages (Agarwal & Gort, 2001; Lieberman & Montgomery, 1988). 1 Maula, Keil, and Zahra (2003) demonstrated that CVC investors get early access to newly emerging technologies and can more effectively respond to technological threats than would otherwise be possible. However, due to the risky and uncertain nature of this process, companies are not inclined to make high–stake investments at the start. In line with real options reasoning (Bowman & Hurry, 1993; Folta, 1998; Hagedoorn & Sadowski, 1999; Haspeslagh & Jemison, 1991; Kogut, 1991; Vanhaverbeke, Duysters, & Noorderhaven, 2002), when uncertainty is high, firms are better off making small initial investments while learning about the investment opportunity and delaying major investments until the uncertainty has decreased to a level that justifies larger financial injections (Roberts & Berry, 1985; Van de Vrande et al., 2006). One way to manage these highly uncertain outcomes of the innovation process is by investing in CVC. CVC investments enable firms to make a number of small investments in entrepreneurial ventures that develop emerging or complementary technologies. In CVC investments, the established company obtains a minority equity stake in the privately held venture. As the uncertainty decreases over time thanks to the initial learning investments, the investing firm may choose to increase its involvement by making a follow–on investment. These follow–on investments can take the form of a strategic alliance, which provides the opportunity to build a relationship that allows for learning through intense collaboration (Allen & Hevert, 2007; Wadhwa & Kotha, 2006). This in turn, requires a certain level of commitment and involvement from the investing firm that goes beyond passive equity investments alone.

Intellectual property (IP) appears to protect first–mover advantages in some industries, such as pharmaceuticals. In other industries, later entrants can invent their own technology so quickly that the first mover's IP protection does not lead to a sustainable competitive advantage.

The notion of strategic alliances refers to “cooperative efforts in which two or more separate organizations, while maintaining their own corporate identities, join forces to share reciprocal inputs” (Bamford, Gomes–Casseres, & Robinson, 2003; Kale, Dyer, & Singh, 2002; Vanhaverbeke et al., 2002). Strategic alliances are particularly attractive in turbulent environments, because they enable firms to share costs and risks associated with new business development. Strategic alliances differ from CVC investments in a number of ways. First, the notion of CVC investments focuses specifically on venture capital investments. Venture capital investments are typically structured in a number of financing rounds, and with a number of co–investors. Strategic alliances on the other hand do not require an equity investment per se (many strategic alliances that are being formed do not involve equity [Duysters, Kok, & Vaandrager, 1999]) and do not involve multiple investment rounds. Second, managers consider CVC investments and alliances as distinct activities that have to be managed in different ways. In fact, many companies manage strategic alliances and CVC investments through separate dedicated corporate entities (Dushnitsky & Lavie, 2010). On the one hand, corporations set up a dedicated organizational entity with allocated funds to invest in interesting ventures (Chesbrough, 2002, 2003; Dushnitsky, 2004). On the other hand, several companies manage and organize strategic alliances through an alliance management department at the corporate level, but they are also managed in many cases at the divisional or business unit level (Dyer, Kale, & Singh, 2001; Heimeriks, Vanhaverbeke, & Duysters, 2007; Lavie, 2004). Third, strategic alliances imply that the otherwise independent partners become mutually dependent through their resource commitments in joint R&D. In a technology alliance, partners strive toward shared objectives and try to maximize the financial return from their collaboration. In contrast, in CVC investments, the investing company has different objectives than the management team of the portfolio firm; the investor invests unilaterally in the portfolio firm and claims in return several rights.

Hence, although CVC investments and strategic alliances can both be applied to explore new technologies, they differ substantially in their application and the way in which they are managed within firms (Dushnitsky & Lavie, 2010). Therefore, they can be considered as complementary instruments to source external (technological) knowledge. CVC investments focus on identifying and valuing early–stage technology in start–ups. CVC investments improve the firm's ability to identify promising portfolio firms as potential technology partners in the future and to value the business potential of technologies under development in the start–up. In other words, CVC–related activities improve the first two dimensions of their absorptive capacity (identification and valuation of external technology) (Benson & Ziedonis, 2009; Cohen & Levinthal, 1990). In contrast, strategic alliances are geared toward the joint development of a new technology or project. Strategic alliances thus focus on the deployment or integration of external technology—the third dimension of absorptive capacity. They focus on the co–development of technology or knowledge transfer between the partnering firms. In sum, CVC investments in combination with strategic alliances as follow–on investments provide an interesting gateway into technologies emerging from start–ups: following the trajectory, they may have superior capabilities to identify, assimilate, and deploy external technologies.

In the following section, we develop a set of hypotheses taking a real options approach as our underlying theoretical framework. Within this perspective, CVC investments are initial equity investments by established companies that can be considered as investments that create an option. We analyze how a CVC investment in a particular entrepreneurial venture raises the chance of an investor and the funded venture becoming strategic alliance partners in a later stage. In this way, strategic alliances are considered as follow–on investments (option exercising).

Prior CVC Investments

CVC investments can thus be beneficial to cope with high levels of technological uncertainty in the early stages of new business development. In addition, CVC ties with a partner firm help to reduce the level of partner uncertainty and thereby the threat of opportunistic behavior. Cooperation between firms is characterized by partner uncertainty, which occurs through information asymmetries (Balakrishnan & Koza, 1993). As a result of these information asymmetries, firms do not have all the necessary information to make an investment decision. Prior cooperation is one way in which information asymmetries can be reduced. Through prior cooperation, firms learn about their partners and their technologies.

Prior studies have indicated the use of less integrated governance modes as learning mechanisms to overcome information asymmetries (Reuer & Koza, 2000; Vanhaverbeke et al., 2002; Williamson, 1985). For example, Vanhaverbeke et al. show how, as a result of decreasing information asymmetries, alliances might lead to acquisitions. The same line of reasoning can be applied to the establishment of strategic alliances after prior CVC investments in an entrepreneurial venture. A recent study by MacMillan, Roberts, Livada, and Wang (2008) shows that most CVC investors take board seats in the venture they invest in, which empowers them to monitor the technological development within the portfolio company firsthand. Thereby, the information asymmetry that might exist between partners is reduced sharply and the investing firm is likely to get a more accurate picture of the actual knowledge that is being targeted. As a result, prior CVC investments can serve as a useful instrument to learn about new technologies and business opportunities. In this way, firms can defer commitment until technological and market uncertainty falls below an acceptable level through learning investments using different types of feasibility studies. Moreover, CVC investments enable the investing firm to get acquainted with the opportunity at hand and to overcome information asymmetries.

In other words, CVC decision making under high uncertainty serves to create various options to develop new businesses for a company through small option–like initial investments. These initial CVC ties with an entrepreneurial venture can help to minimize the technological and partner uncertainty surrounding the technology sourcing relationship. As a result, firms are more likely to ally with a partner with whom they have had prior CVC investments. Moreover, as soon as the technology under development appears to be promising, a more intense form of collaboration is desirable in order to ensure a transfer of the knowledge. The establishment of a strategic alliance that requires a stronger commitment from the investing company can be considered as exercising the option. Thus, we hypothesize:

Partner Uncertainty

As mentioned in the previous section, uncertainty between partners can occur when there are information asymmetries between them. Information asymmetry refers to the situation where the investing firm does not yet have access to all the relevant information that is needed to make an investment decision (Reuer & Koza, 2000; Vanhaverbeke et al., 2002). One way to overcome information asymmetry is through prior investments (Reuer & Koza). CVC investments are typically staged investments in which (corporate) investors invest in a number of financing rounds. After each round, there is the option to sell shares, back off, or participate in another round. As a result, participation in multiple investment rounds decreases information asymmetry. With each investment round, investors have the opportunity to acquire more knowledge about the technology under development (Guler, 2007) and in this way they can be considered in real option terms as small initial investments to gain more knowledge about the venture and defer the decision to partner with it. As a result, when an investor participates in more investment rounds, it builds familiarity with the venture and thereby reduces partner uncertainty. Consequently, the number of investment rounds a firm participates in will increase the chance of the corporate investor deciding to enter a strategic alliance with the venture.

Thus, we expect the number of investment rounds a firm participates in to be positively related to the likelihood of this CVC partnership evolving into a strategic alliance. We hypothesize:

Technological Uncertainty

Companies invest in portfolio firms to get access to novel knowledge they do not have in–house. The degree of technological novelty of externally developed knowledge depends on the technological proximity between the corporate investor and the portfolio firm. Technological proximity refers to the relative overlap between the technological knowledge bases of these two dyad partners. If this overlap is small, the two firms have little knowledge in common and the CVC investment can be considered as a highly explorative and thus highly risky investment in unrelated technologies (Nooteboom, 2000). CVC investments in portfolio firms with a larger technological overlap can be considered as less explorative investments or as investments in related technologies. CVC investment in start–ups with related technologies can thus be considered as less risky. Moreover, a stronger technological overlap or relatedness between the technology base of the corporate investor and that of the start–up indicates that the dyad partners can assimilate and integrate each others’ technology more easily once a follow–on technology alliance is established between the dyad partners (Nooteboom; Nooteboom et al., 2007). A large technological distance between the corporate investor and the start–up may preclude the sufficient mutual understanding needed to carry on. As a result, some overlap in the firms’ technological bases is necessary in order to recognize, assimilate, and integrate new knowledge from the technology partner (Cohen & Levinthal, 1990; Lane, Koka, & Pathak, 2006; Lane & Lubatkin, 1998).

When the technology of the start–up is familiar to the corporate investor, the relative absorptive capacity of the latter is likely to be stronger (Lane & Lubatkin, 1998). Thus, related knowledge will be more easily assimilated and integrated by the investing company. CVC investments in start–ups with related technologies will enable the investing company to understand the technology and its business potential more easily than in the case where the technology of the two firms is unrelated. As a consequence, CVC investments in start–ups with a related technology will reduce the technological uncertainty for the investor drastically, and identifying promising start–ups as alliance partners will be straightforward. In other words, CVC investments in ventures with related technology are more valuable as initial investments to learn about the technology of the entrepreneurial venture. This will be much more difficult when the established firm invests in a start–up with unrelated technology. Hence, CVC investments in start–ups with related technology will lead more easily to strategic alliances as the chance to assimilate externally developed knowledge is larger than in the case of unrelated knowledge. Furthermore, CVC investments in related technology may be made for different reasons than similar investments in unrelated technology. Reasons for firms to start CVC investments in unrelated technologies include getting a “window” on new technological areas, exploring emerging technologies, anticipating convergence between different technologies, etc. (Benson & Ziedonis, 2009). Unrelated investments are less or at least not directly motivated by new business development considerations and, hence, will be less likely to lead to follow–on investments. In the case of familiar technologies, firms may have the intention to establish an alliance with or to acquire the portfolio firms, but the technology is still too risky to do so. In that case firms start a CVC investment with the intention to transform it into an alliance or acquisition. In sum, we expect technological proximity to have a positive effect on the likelihood of firms establishing a strategic alliance with prior CVC partners. We therefore hypothesize:

Market Uncertainty

VCs and corporate investors rarely provide the capital that a venture needs up front but rather they invest in start–ups at distinct stages of their development (Gompers & Lerner, 2001; Sahlman, 1990). CVC investments are typically structured as venture capital deals, which are staged investments that occur in a number of rounds. The stage of the investment represents the development stage of the portfolio company and develops from “start–up/seed” to “early stage,” followed by “expansion” and “later stage” phases. Each stage typically costs more than the preceding one, resulting in increased commitments but also in reduced technological and market uncertainty. Later investment stages indicate that there are fewer unknowns about the technology a start–up is developing (Sorenson & Stuart, 2001). Uncertainty regarding the actual value of the technology that is being targeted is particularly high in the earliest stages of technology development. When the start–up goes through the different investment rounds, technological uncertainty decreases and the business potential of the venture materializes. As a result, the later the stage of the investment in the portfolio firm, the less uncertainty there is regarding the value of the underlying technology. Following real–options reasoning, when the uncertainty surrounding the investment decreases, the investing firm can decide upon a follow–on investment, for instance through a strategic alliance with the venture.

Start–ups receiving CVC funding during an early round may have little to offer to partners in terms of products or technologies compared with start–ups in the “expansion” or “later stage” phases (Kelley & Spinelli, 2001). They may be less interested in pursuing alliances since they do not need the complementary assets of the corporate investor until the technology under development reaches the validation stage (Grönlund, Rönnberg Sjödin, & Frishammar, 2010).

In other words, the chance of early–stage investments leading to a strategic alliance between the corporate investor and the venture is smaller than for later–stage investments where the business potential of the venture is already more developed. Consequently, we expect later–stage investments to be more likely to lead to a strategic alliance with the venture:

Methods

Data and Sample

A sample of pharmaceutical firms (observation years: 1990–2000) is used to test the hypotheses. The data set was constructed in the following way. The sample was selected using the Flemings Directory of Pharmaceutical Products Worldwide, which lists the largest pharmaceutical firms based on pharmaceutical revenues in 1989. The largest firms in the industry were selected to ensure the availability of the necessary data. Large firms are more likely to engage in external technology sourcing activities and are more likely to report them publicly (Keil et al., 2008). For that reason, prior research on alliances and acquisitions has also focused on the largest companies in the industry (Ahuja, 2000; Gulati, 1995; Gulati & Gargiulo, 1999; Keil et al.). Next, the sample was manually checked for parents and affiliates using Dun & Bradstreet's Who Owns Whom, which were then aggregated on parent company level. In addition, because some of these firms merged during the observation period, new firms were introduced after the merger event. After checking for duplicates, this led to 78 independent companies to be included in the sample.

For these firms, all CVC investments and strategic technology alliances were collected over the period 1985–2000, allowing the calculation of some of the independent variables using a 5–year time lag. Furthermore, patent data and financial information was collected for all focal firms. CVC data was derived from the Thomson VentureXpert database, data concerning alliances and joint ventures was obtained from the MERIT–CATI databank on Cooperative Agreements and Technology Indicators, and Thomson ONE Banker was used to collect information regarding the companies’ M&A activity. Because both the alliances and the CVC investments collected have a strong technology component, only technological M&As were included in our sample, following the method employed by Ahuja and Katila (2001).

In addition, patent information was collected for all firms included in our sample using data from the U.S. Patent and Trademark Office. Because the U.S. Patent and Trademark Office grants patents on both subsidiary and parent company level (Patel & Pavitt, 1997), and the organizational level on which patents are applied for differs between companies, the patents were consolidated on parent company level for each observation year, using Who Owns Whom by Dun & Bradstreet. Finally, financial data was drawn from Worldscope, including sales, research and development expenses, and the number of employees.

Measures

The dependent variable is a dichotomous variable indicating the establishment of a strategic alliance in observation year t between an incumbent firm and a start–up company that was backed by CVC. To obtain this information, each pair consisting of an incumbent firm and a start–up company was manually checked in the MERIT–CATI database to find out whether these two firms had at some point established a strategic alliance. The MERIT–CATI database collects data about strategic technology agreements, and has been used in many prior studies on alliance formation (e.g., Gulati, 1995; Hagedoorn, 2002; Narula & Santangelo, 2009; Vanhaverbeke, Gilsing, Beerkens, & Duysters, 2009). If a strategic alliance was found between a pair of firms in a particular observation year, this variable is set to 1; otherwise, it is set to 0. Included in our definition of alliances are contractual partnerships, such as joint R&D pacts and joint development agreement, and equity–based joint ventures (Hagedoorn). Because prior studies have indicated the possible occurrence of a CVC investment after a strategic alliance (Dushnitsky & Lavie, 2010), we also checked the database to ensure that no such relationship was present in the data.

Following our hypotheses, the independent variables in this study include prior CVC investments, technological proximity, technological capital, the investment stage of the portfolio firm, and the number of prior investments made by the dyad partner in the CVC–backed company. Prior CVC investment is a binary variable indicating whether or not a prior CVC investment between the two firms has taken place in the past. If a prior CVC investment had taken place, this variable was set to 1; otherwise, it was set to 0.

The number of prior investments is a count variable, indicating the number of previous CVC investments made by the incumbent firm in a specific CVC partner.

To assess the technological proximity between the investing firm and its partner, we use a categorical measure based on the companies’ Standard Industrial Classification (SIC) codes (Keil et al., 2008; Villalonga & McGahan, 2005; Wadhwa & Kotha, 2006). Although a measure based on patent portfolios may more accurately capture the differences in the underlying knowledge bases (e.g., Schildt et al., 2005), using patent data has some limitations in the context of CVC investments. Since the entrepreneurial ventures are small start–up firms, many of them do not yet have patents at the time of the investment, which would lead to the loss of many observations. Therefore, we have decided to follow Keil et al. and Wadhwa and Kotha and adopt a measure based on SIC codes, which is consistently available for all the firms in our sample. We classify the investments as Intra–industry when their SIC codes are identical, and as Related when the first three digits are the same. All the other investments were classified as Unrelated. This category is taken as the default category.

The investment stage of the portfolio firm indicates the development stage of the CVC–backed company in which it received its first investment. We develop two measures to assess the investment stage. First, we use a categorical variable, indicating whether an investment was made in a particular stage (Guler, 2007). We distinguish among “start–up/seed,”“early stage,”“expansion,”“later stage,” and “other,” where “other” is set as a control group and is therefore not included in the analyses. However, since the different stages are ordinal, we also include an ordinal variable, where higher numbers indicate a more developed stage. The stages that are distinguished in this data set are: (1) “start–up/seed”; (2) “early stage”; (3) “expansion”; and (4) “later stage.”

Because the decision to establish a strategic alliance might also be affected by other factors than the ones mentioned earlier, we included a number of control variables to capture firm– and dyad–specific characteristics. First of all, we controlled for the technological capital of the portfolio firm, as an indicator of technological progress (Guler, 2007). Technological capital partner firm is a count variable, indicating the number of patents held by the CVC–backed company. Next, we controlled for investor characteristics that may affect the decision to enter a strategic alliance, such as firm size and R&D intensity (Ahuja & Katila, 2001; Stuart, 1998). Firm size was measured as the natural logarithm of annual sales and R&D intensity was measured as the annual R&D expenditures divided by sales. Both variables are lagged by 1 year. Furthermore, we control for the geographical proximity of the two partners (Lindsey, 2008; Sorenson & Stuart, 2008), by including a dummy variable same region, which is set to 1 if the two partners are active in the same economic block (USA–USA or EUR–EUR 2 ). Finally, as the performance of firms may affect alliance formation (Gulati, 1995), we controlled for the success and maturity of the venture by including a dummy variable IPO. This variable indicates whether or not the CVC–backed company has gone through an IPO prior to the year of observation.

Please note that although other combinations are possible, the focal firms in the current data set are all European– or U.S.–based firms.

Method

A common method that can be found in the literature to estimate the likelihood of an event happening is the use of event history analysis with Cox proportional hazards. However, in the case of discrete–time data (i.e., when information about events is collected in discrete time settings, such as months or years), logit or complementary log–log models are to be preferred (Jenkins, 1995). Because our setting is discrete–time rather than continuous, we employ a complementary log–log model (Jenkins; Mitsuhashi & Greve, 2009) to estimate the likelihood of firms engaging in a technology alliance after a CVC investment. The data is set up as a dyad–year panel data set, where each dyad represents a combination of an incumbent firm and a CVC–backed company. The empirical analysis in this study is divided into two steps. First, we model the likelihood of forming a strategic alliance between all possible combinations of incumbent firms and CVC–backed companies in our data set to assess the effect of prior CVC investments between two firms on the likelihood of a strategic alliance at a later stage. Prior studies have used a variety of approaches when comparing actual relationships with possible alternatives. One approach is to use a matched sampling approach, where every realized tie is matched with one or more possible alternatives (Mitsuhashi & Greve; Sorenson & Stuart, 2001, 2008). According to these authors, using a data set consisting of all the possible dyads may lead to the creation of too many observations, making the standard errors difficult to interpret. However, this seems to be an issue particularly in cases with relationships involving more than two partners (e.g., Mitsuhashi & Greve) or in cases where considering all potential dyads would lead to a very large matrix, leading to computational issues (e.g., Sorenson & Stuart). In addition, random sampling of matched pairs also leads to a potential bias in estimating the likelihood of tie occurrence, as the proportion of realized ties in the matched sample is different from the proportion of realized ties in the population (Sorenson & Stuart). Another approach is to include all the possible matches in the analysis (e.g., Gulati, 1995; Gulati & Gargiulo, 1999; Stuart, 1998). Given that our data set only contains realized ties consisting of two firms, and that the number of potential dyads (5,320) does not lead to computational issues, we use the whole population and hence we include all the possible dyads in step one of our analysis.

Second, we model the hazard rate of forming a strategic alliance after a prior CVC investment, using only dyad–year observations where a CVC investment between the two firms has occurred. In this way, we are able to estimate the effects of a number of explanatory variables on the likelihood of forming a strategic alliance after a prior CVC investment. The second step is thus conditional on having a prior CVC investment between the two partners.

Results

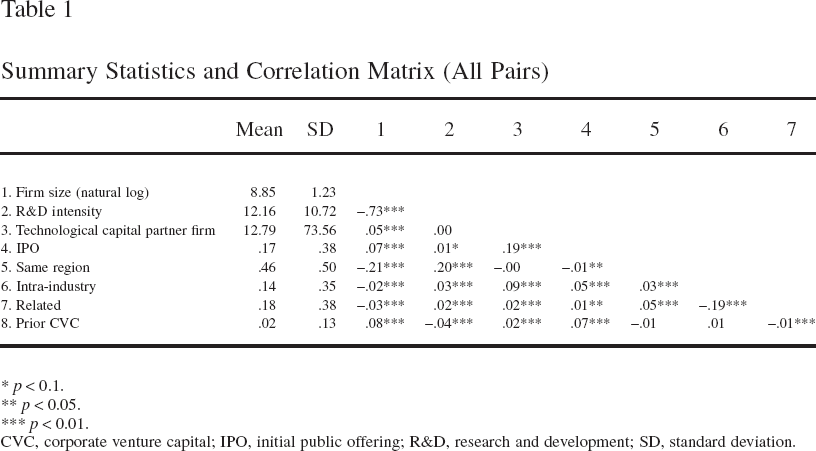

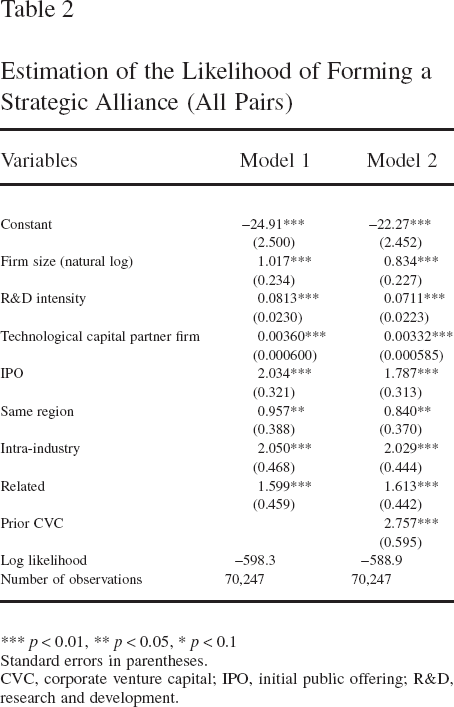

Tables 1 and 2 show the results of the first step of the analysis, in which the likelihood of establishing a strategic alliance was modeled for all possible pairs between an incumbent firm and a CVC–backed company. Table 1 shows the summary statistics, whereas Table 2 shows the results of the analysis. 3

As shown in Table 1, there is a high correlation between size and R&D intensity (ρ = −0.73; p < 0.01), which may indicate possible multicollinearity issues. Therefore, as a robustness check, we have performed additional analyses where the independent variables were included one by one. The results of these additional analyses are very similar to the results presented here, indicating that multicollinearity among the independent variables is not an issue in this article.

Summary Statistics and Correlation Matrix (All Pairs)

p < 0.1.

p < 0.05.

p < 0.01.

CVC, corporate venture capital; IPO, initial public offering; R&D, research and development; SD, standard deviation.

Estimation of the Likelihood of Forming a Strategic Alliance (All Pairs)

p < 0.01

p < 0.05

p < 0.1

Standard errors in parentheses.

CVC, corporate venture capital; IPO, initial public offering; R&D, research and development.

Model 1 in Table 2 shows the baseline model, with only the control variables included. Model 2 adds the variable of prior CVC investments, to estimate the effect of having prior CVC investments on the likelihood of alliance formation. Hypothesis 1 predicted that firms are more likely to engage in a strategic alliance with a partner firm in which they have made a CVC investment in the past. As shown in Model 2 in Table 2, the coefficient representing the effect of a prior CVC investment between a corporate investor and a portfolio firm is positive and significant (β = 2.757; p < 0.01). This indicates that having a prior CVC relationship increases the likelihood of forming an alliance between the two partners, thereby supporting hypothesis 1. Also note that the effects of the control variables are in line with those found in prior studies on alliance formation. For instance, Stuart (1998) found that publicly traded firms were more likely to engage in strategic alliances, whereas a negative effect was found for firms with no patents. In addition, prior studies have also indicated positive effects of firm size (e.g., Gulati, 1999; Stuart).

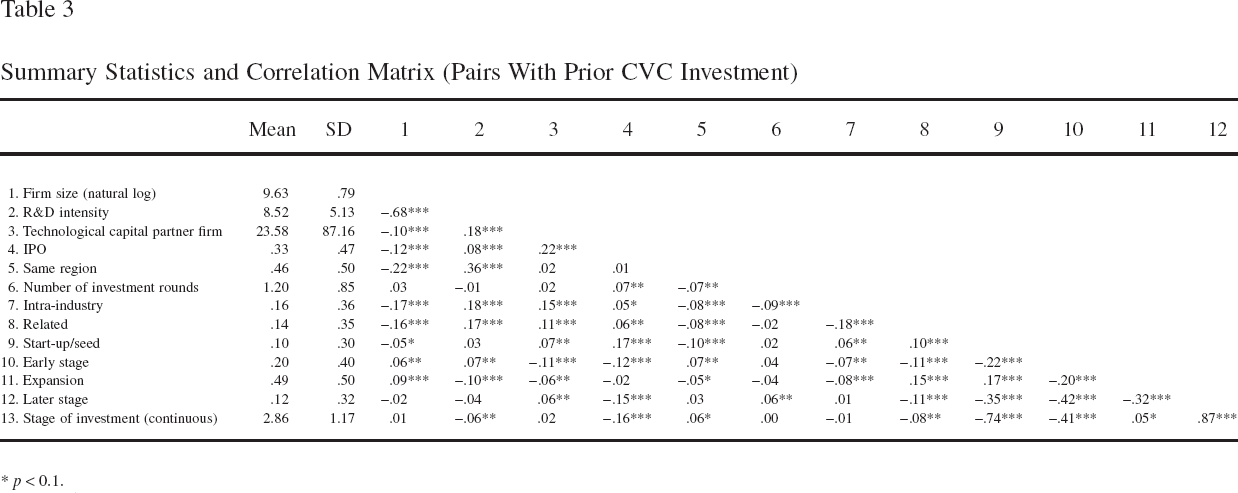

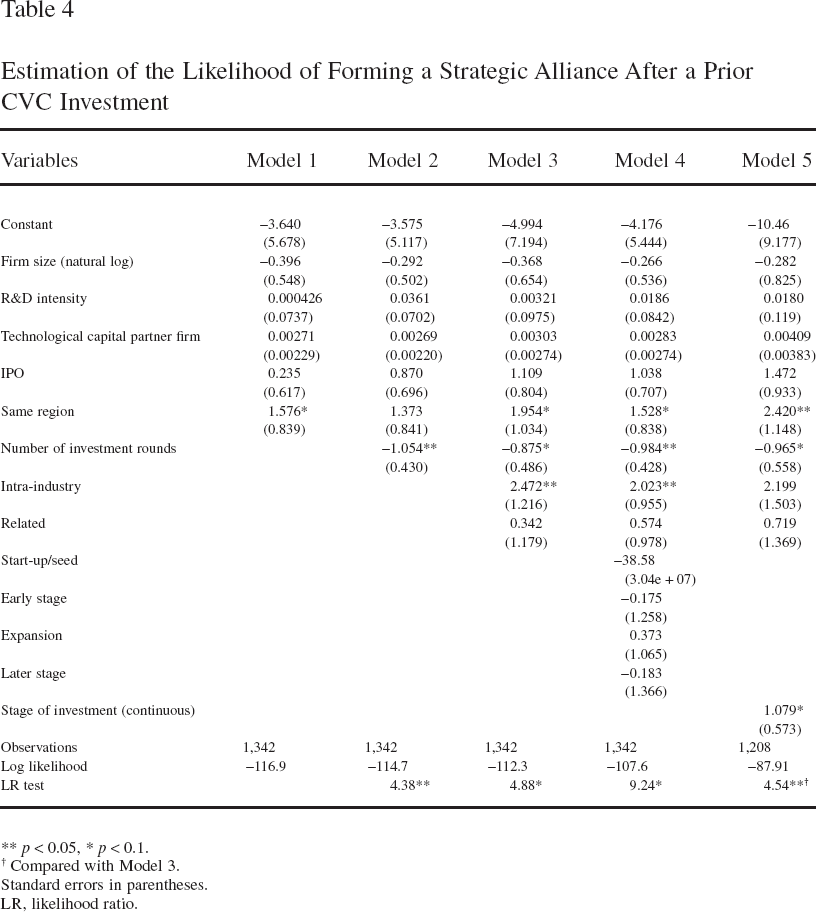

The second part of this study investigates the conditions under which a prior CVC investment leads to a subsequent strategic alliance. Tables 3 and 4 show the descriptive statistics and the results of the analysis.

Summary Statistics and Correlation Matrix (Pairs With Prior CVC Investment)

p < 0.1.

p < 0.05.

p < 0.01.

Estimation of the Likelihood of Forming a Strategic Alliance After a Prior CVC Investment

p < 0.05

p < 0.1.

Compared with Model 3.

Standard errors in parentheses.

LR, likelihood ratio.

Model 1 in Table 4 shows again the baseline model, with only the control variables included. In Model 2, the variable of number of investment rounds is added, while Model 3 also includes the two categorical variables representing technological proximity. Finally, the two different variables representing the stage of investment are added in Models 4 and 5.

Hypothesis 2 predicts a positive effect between the number of investment rounds an investor participates in and the likelihood of subsequent alliance formation. Contrary to our expectations, the coefficient in Model 2 of Table 4, representing the number of investment rounds, is negatively related to the likelihood of forming a strategic alliance (β = −1.054; p < 0.05). This implies that the more investment rounds a corporate investor participates in, the less likely it becomes that the corporate investor and the portfolio firm will engage in a strategic alliance. The suggestion that more investment rounds lead to more acquaintance with the venture and its technology and, therefore, to a higher chance of subsequently establishing an alliance is not supported by the results. Hence, we found no support for hypothesis 2.

In hypothesis 3, we predicted that technological proximity between two partners would have a positive impact on the likelihood of an investor establishing a strategic alliance with the portfolio firm. Model 3 in Table 4 shows a positive and significant coefficient for the variable representing that the two partners are active in the same industry (Intra–industry, β = 2.472; p < 0.05). The variable representing that the two firms operate in related industries was also positive, but not significant (β = 0.342 n.s.). Hence, these results indicate that firms are more likely to engage in a strategic alliance after an initial CVC investment, when they operate in the same industry, thereby supporting our hypothesis.

Finally, we expected the stage of investment to positively affect the likelihood of a CVC investment leading to a strategic alliance (hypothesis 4). To test this relationship, we have included both a categorical variable and an ordinal variable in our analysis. As shown in Model 4 in Table 4, none of the categorical variables was significant. However, when an ordinal variable was used rather than a categorical variable (Model 5), the results show a positive and significant coefficient for the stage of investment (β = 1.079; p < 0.1), indicating that CVC investments in later–stage companies increase the likelihood of this investment leading to a follow–on strategic alliance. We will come back to these findings in the discussion section of the article.

Conclusion and Discussion

CVC investments in start–ups may lead to follow–on investments in a later stage. Benson and Ziedonis (2009) examined how CVC–related activities allow established firms to better monitor the technology of start–ups and in this way identify the most interesting ones for possible acquisition. In this study, we have argued that CVC investments in young entrepreneurial firms might be a first step toward a more dedicated form of collaboration with the portfolio firm (McNally, 1997; Sykes, 1990) and that this sequencing of interorganizational collaboration can thus be analyzed in terms of real options: the initial CVC investment in a portfolio firm can be considered as an option creation process, and follow–on investments with a stronger commitment can be viewed as exercising options. Firms invest in a stepwise manner because under high levels of uncertainty (e.g., new business development and corporate venturing), they are inclined to make small initial investments to learn more about the technology and the market potential of the start–up. In this way, CVC investments deliver the necessary information to bring down uncertainty to acceptable levels, so that the investing company can start establishing stronger ties with the start–up in the following years. This article can be considered as one of the first studies exploring the dynamic nature of CVC investments and how a venture capital relationship may evolve into one with stronger (financial) commitment when technologies become more mature and uncertainty decreases. More specifically, we have addressed this research topic by explicitly focusing on the likelihood of firms entering a strategic alliance with a CVC partner, which is an interesting gateway for corporate investors to tap into external technologies emerging from start–ups.

We have found strong empirical support for the hypothesis that prior CVC investments in a portfolio firm increase the probability of the corporate investor establishing a strategic alliance with a start–up company. Consequently, CVC investments can be considered from a real option perspective (Tong & Li, 2011). They create options and allow corporate investors to get acquainted with a technology or business opportunity. As we have argued in this article, CVC investments enable established firms to better understand the technology under development in the start–up. Later on, they can exercise that option and establish technology alliances that represent a much stronger tie to ensure the assimilation and integration of the start–ups’ technology into their own technology base. Although this finding is in line with our expectations, there is an interesting contrast with prior studies. A study by Roijakkers, Hagedoorn, and Van Kranenburg (2005) on the likelihood of repeated alliance ties between large and small firms in the pharmaceutical industry found that prior ties have a negative effect on the likelihood of establishing a new tie. In addition, Hagedoorn and Sadowski (1999), who studied the transition from alliances to M&As, also found no support for this phenomenon. It can thus be concluded that CVC investments serve a different purpose than strategic alliances when it comes to the development of new business. Our results suggest that CVC investments are a first step in the process, aimed at identifying and evaluating external technology developed in start–ups. CVC investments represent in this way the first step toward a more integrated form of cooperation that can take the shape of acquisitions (Benson & Ziedonis, 2009; Tong & Li) or technology alliances (this study). Technology alliances are an interesting sourcing mode to assimilate and acquire the technology developed in these start–ups. Hence, CVCs and technology alliances have complementary functions in a firm's ability to absorb external technology (Cohen & Levinthal, 1990).

In addition, we have studied the conditions under which a prior CVC investment is most likely to lead to a technology alliance. First of all, the results of this study provide empirical support for the positive effect of technological proximity increasing the likelihood of the formation of an alliance after a CVC investment. Corporate investors are more likely to establish a strategic alliance as a follow–on investment if there is a considerable overlap between their technology base and that of the start–up in which they invested. This finding is in line with prior studies emphasizing the importance of technological similarity between partners in interfirm relationships (e.g., Lane & Lubatkin, 1998; Mowery, Oxley, & Silverman, 1998; Stuart, 1998). When a corporate investor participates in start–ups with related technologies, it can rely on its absorptive capacity to assimilate the technology of the venture and to understand the business potential. If the technology of the venture is unrelated, the investor cannot rely on its absorptive capacity to understand and learn about the technology: as a consequence, CVC investments in ventures with related technology are more valuable as option–creating investments to learn about the technology of the entrepreneurial venture.

Second, we also found some support for the hypothesis that the maturity of the venture (indicated by the stage of investment) has a positive effect on the likelihood of forming a strategic alliance. Late–stage investments in ventures minimize the technological and market uncertainty, which in turn makes it easier for the investing firm to judge the commercial potential of the technology under development. As a result, investing firms will be more inclined to enter a strategic alliance in order to transfer or further develop and commercialize the technology. However, we only find this positive relationship when we use an ordinal variable to rank the stages linearly. In contrast, we do not find an effect on the establishment of a subsequent alliance when we use categorical variables for the four stages. This implies that there is no specific stage that fosters the setup of a strategic alliance (compared with other stages), but ranking them as earlier or later stages shows that there is indeed a positive effect on the dependent variable. The results thus support hypothesis 4 indicating that a CVC investment in later stages increases the likelihood of a follow–on strategic alliance.

Third, we found no support for a possible positive relationship between the number of investment rounds a firm participates in and the chance of the corporate investor establishing an alliance afterwards. On the contrary, we find a negative relationship, indicating that the greater the number of investment rounds in which a firm participates in a venture, the lesser the likelihood of the investing company establishing a strategic alliance as a follow–on investment. One explanation might be that multiple investments indicate that the investing firm continues to believe in the venture but finds it too early or too risky to follow them up with a strategic alliance or spin–in. A CVC investment in a start–up with strong commercial potential will be readily invited to establish a technology alliance. When the business potential of the start–up is unclear the corporate investor will choose to exit or to participate in the next financing round but it will not establish a technology alliance as long as the risks are too high. An alternative explanation may be that as a result of multiple rounds of investments, the investing firm acquires sufficient knowledge about the new technology, and a subsequent alliance to transfer this knowledge is no longer necessary (the established company can for instance license the technology from the start–up). Another option is that the corporate investor might acquire the venture after several rounds instead of establishing a strategic alliance. In such cases, making a CVC investment in the venture may actually serve as a substitute rather than as a complement to establishing a strategic alliance. Although prior studies have indicated that the two governance modes are clearly distinct choices that are preferred under different circumstances (e.g., Dushnitsky & Lavie, 2010; Van de Vrande, Vanhaverbeke, & Duysters, 2009), further research in this area might provide a more fine–grained picture.

This study is a first step in the exploration of the role of CVC investments as an option–creating investment to get access to emerging technologies developed in entrepreneurial ventures. By doing so, this study contributes to the literature in three important ways. First, this article contributes to the growing research stream on CVC and corporate venturing (e.g., Basu et al., 2011; Hill et al., 2009; Schildt et al., 2005; Yang et al., 2009). For small firms looking for capital investors or corporate partners, these dynamics might affect their decision to engage in a relationship with a corporate partner. As such, the article contributes to earlier work on the choice entrepreneurs have between independent and CVC (e.g., Maula, Autio, & Murray, 2005), the likelihood of entrepreneurs forming an investment relationship with a corporation (e.g., Katila, Rosenberger, & Eisenhardt, 2008), and the chances of being acquired by the investing firm (e.g., Benson & Ziedonis, 2009).

Second, this article contributes to the broader stream of literature on innovation management. As mentioned earlier, prior studies have stressed the importance of CVC investments for innovation (e.g., Dushnitsky & Lenox, 2005a; Keil et al., 2008; Wadhwa & Kotha, 2006) and the role of CVC investments in the emergence of alliance networks (Dushnitsky & Lavie, 2010). However, research addressing the dynamics of these types of investments has only recently emerged (e.g., Ozmel et al., 2011; Wadhwa & Phelps, 2011). This article shows the relevance of investing in a portfolio of different R&D projects as a way to identify possible alliance partners. By doing so, we improve our understanding of the dynamic nature of new business development and external technology sourcing and how firms can cope with the varying levels of uncertainty that are present during the development of new technologies.

Finally, this article contributes to real options theory (Bowman & Hurry, 1993; Folta, 1998; McGrath, 1997). Real options theory suggests that under high levels of uncertainty firms are better off creating an option by making an initial investment decision. Such an initial investment decision can take the form of a CVC investment. These options can be exercised later on through a follow–on investment (such as a strategic alliance or acquisition). In particular, this study contributes to the existing body of literature on real options in interfirm relationships and sequential investments (e.g., Folta & Miller, 2002; Guler, 2007; Kogut, 1991; Kumar, 2005; Li & Mahoney, 2006; Van de Vrande et al., 2006), by showing how real options logic can be applied to the formation of a strategic alliance after an initial CVC investment. Moreover, we add to the understanding of the conditions under which a follow–on investment in interfirm relationships is most likely to occur by incorporating determinants that are specific for the context of CVC investments.

However, as an explorative study, there are also some limitations. First, we do not take into account whether and when investing firms choose an exit strategy. An exit strategy is a valid alternative, as many CVC investments turn out to have returns below the investor's initial expectations. Moreover, corporate investors also value CVC investments according to their strategic value for the company: business opportunities related to a portfolio firm might not generate a business that is large enough or the technology might be too distant from the existing technology base or business applications of the investing firm. Hence, future research could extend the scope of the current article by examining the development of start–ups after they have received a CVC investment. Taking together exits and follow–on decisions in a larger, integrated study could further improve our understanding of the role of CVC investments in the development of start–ups.

Second, although we do find support for the hypothesis that firms are more likely to engage in an alliance when their activities are largely related, it should be noted that the use of SIC codes is coarse grained and subject to some limitations. SIC codes capture the industry in which a company is active, while patent portfolios are an indicator of the underlying knowledge that is embedded in firms. As a consequence, they represent different values of relatedness (industry relatedness versus technological relatedness [Schildt et al., 2005]), both of which play an important, but possibly different, role in alliance formation after a prior CVC investment. Future research could take into account the combined perspectives of technological and industry relatedness, as well as other additional factors that may drive the decision to engage in a strategic alliance after an initial CVC investment, such as the uniqueness of the technology, the network of the start–up, or the technological capabilities of the investor.

Third, we have confined our attention in this article to the effect of prior CVC investments on the likelihood of subsequent technology alliance formation. This does not exclude the possibility of alliance formation activities increasing the incidence of CVC investments, as Dushnitsky and Lavie (2010) have demonstrated. However, their analysis is not intended to show that on the dyad level a strategic alliance can increase the likelihood of subsequent CVC investments—that is the opposite of our central claim. Rather, they investigate whether prior experience with alliances at the firm level might lead to more CVC investments up to a maximum (too many prior strategic alliances will lead again to fewer CVC investments). While we claim that a prior CVC investment between an established company and an entrepreneurial venture might lead to a strategic alliance, Dushnitsky and Lavie show that companies with a well–established portfolio of existing alliances (at the firm level) are also more inclined to get involved in CVC investments in the future. Since they work at the firm level, the factors that they identify as driving the link between alliances and CVC investments are quite different from our arguments on the dyad level. In sum, Dushnitsky and Lavie and our study both have their merits and complementary parts in analyzing CVC investments and strategic alliances. We are interested in the sequencing of actions between a sponsoring firm and a venture, but this does not preclude a company (at the firm level) from using the visibility gained by prior strategic alliances to become a more prominent CVC investor. An interesting avenue for future research emerges, as the interaction between CVC and alliances is prominent but the relationship may be very different. What is for example the effect of frequent alliance formation with portfolio companies by a corporate investor on its attractiveness as an investor?

Fourth, although a recent study by Benson and Ziedonis (2009) has investigated the financial performance of corporate investors when acquiring their portfolio firms, so far, we have no empirical evidence that firms that tap into external innovation sources through a sequencing strategy over time are also superior innovators. However, that is what open innovation scholars (Chesbrough, 2003, 2006) implicitly propose. Further research should provide empirical support for this proposition.

Fifth, we have only focused on sequential investments. However, companies also have to consider the right sourcing mode because taking a minority position in a VC–funded venture is only optimal under particular conditions compared with the establishment of a strategic alliance or the acquisition of the entrepreneurial venture (Tong & Li, 2011). We have not addressed this topic and have implicitly assumed in our study that the choice of a CVC was always a correct choice. Moreover, there are different ways to look at the relationship between venture capital and strategic alliances, as has been shown by Lindsey (2008).

Finally, we have focused only on technology alliances as follow–on investments in this article. This is of course a limited approach, since established firms also tend to acquire the start–ups in which they invested before (Benson & Ziedonis, 2009). Therefore, it would be interesting to enrich the analysis by integrating alliances and acquisitions as follow–on investments in a single study and examine under which conditions CVC investments will lead to alliances as follow–on investments and when they will lead to an acquisition of the start–up.