Abstract

Designing incentive contracts that constructively guide employee efforts is a particularly difficult challenge in novel innovation initiatives, where unforeseen events may occur. Empirical studies have observed a variety of incentive structures in innovation settings: “time and material contracts” (compensation for executing orders), “downside protection” (target‐driven incentives with protection from unexpected risks), and “upside rewards” (additional remuneration for pursuing opportunities). This paper develops a model of incentives in presence of unforeseen events and offers a theoretical prediction of which of the empirically observed incentive structures should be used under which circumstances. The combination of three key influences drives the shape of the best incentive contract. First, the presence of unforeseeable uncertainty, or the occurrence of events that cannot possibly be foreseen at the outset. These may force a change in the project's plan, making pure target setting insufficient. Second, fairness concerns dictate that the employee's expected compensation cannot be shifted downward by unforeseen events, because it would cause demotivation, hostility, and defection. Third, management may not be able to observe the detailed actions of the employee (moral hazard) nor whether a positive or negative unforeseen event has occurred (asymmetric information).

1. Introduction

British Telecom (BT) offers a famous service in the United Kingdom: its “1471 Call Return”. Customers can dial “1471” and obtain the number of the last person who called. The history of this service is quite circuitous: In the early 1990s, BT developed a digital display telephone, which would show caller ID and record the caller information in case of a missed call. BT tested the phone in a small Scottish town, but did not have sufficiently many prototypes for all households. BT offered households without it a “crutch”: they could call a service number to obtain the same information. It unexpectedly emerged that the households with the service number were as satisfied as those with a digital display phone. Thus, BT decided to change from a hardware product to a pure service, a paying number “1471”. After market introduction, BT, again unexpectedly, noticed that this service generated so much additional traffic (many who used 1471 called right back), that they decided to offer the service for free, introducing it with great fanfare at BT's 10th birthday in November 1994. By March 1996, 12 million BT customers used 1471 each week, making an average six million calls to the service every day. 1471 still exists in 2007, with additional features added (some paying).

Over the course of this innovation project, BT first redefined its product (from hardware to a service) and then changed its business model (from a revenue generating service to a free service generating an additional call volume). These repeated major changes are in contradiction to classic principles of stage gate processes and “design freeze” in product development (e.g., Cooper 1994, IPMA 1999). However, such major and unanticipated re‐definitions in the solution approach are typical in novel and long‐term innovation initiatives and have been repeatedly reported (e.g., Bank 1995, Chesbrough and Rosenbloom 2002, Loch et al. 2008). In such projects, no amount of planning, no matter how thorough, can foresee all major events (e.g., Morris and Hough 1987, Lynn et al. 1996, Williams 1999).

In general, managers of novel projects must deal with unforeseeable uncertainty, or the inability to recognize and articulate relevant variables and their functional relationships; Schrader et al. (1993) refer to this as “ambiguity”. Projects facing unforeseeable uncertainty must therefore be flexible and change their approach mid‐course as new information becomes available (Chew et al. 1991, Lynn et al. 1996, Thomke and Reinertsen 1998).

Emerging unforeseen events, which require new actions and result in redefinitions of target outcomes, pose major challenges for setting incentives for the project manager. How can a contract, which must be written at the outset, offer incentives for actions that can be specified only after unforeseen events emerge and that force or allow a new set of actions? In the BT example, incentives based on the sales of phones with digital display would have been irrelevant once the product was redefined, as would have been incentives based on revenues generated from the service. In fact, either of these incentives might have prevented or discouraged the recognition or pursuit of the new opportunity.

Not acknowledging looming emerging events in the incentive contract for the project team may have destructive results. Consider, for example, the project described in Loch and Terwiesch (2002) for building a first‐of‐a‐kind facility to convert iron ore into iron (a raw material for the steel industry). The client did not acknowledge the amount of uncertainty posed by using a radically new chemical process for the conversion (reduction of the ore in a 650 °C hydrogen atmosphere). The ramp‐up repeatedly presented unforeseeable problems, for which new solutions had to be developed. As a result, the project repeatedly missed deadlines, and ultimately, the project manager was demoted and then retired early. But the reason for the delays was not the project manager's ability; rather, it was the unrecognized level of uncertainty, requiring newly developed emerging solutions rather than plan execution. As a result, the facility took much longer than necessary to reach stable performance, and the careers of capable people were damaged.

In other cases that we know, the lacking acknowledgement of looming emerging events in project contracts leads to an unwillingness of the staff to take on the projects, and to information hiding (“low‐balling”) by project managers – both behaviors that compromise the organization's ability to undertake novel and innovative projects.

Our study examines how adjustable incentive contracts can respond to initially unforeseeable influences. Our model suggests that the contract choice depends on the principal's (firm's, or senior management's) ability to observe the employee's (project manager's) actions (moral hazard) and its ability to observe the emergence of previously unforeseeable influences (asymmetric information). If the firm can observe the project manager's actions (no moral hazard), the optimal contract uses process incentives: the manager is rewarded if he chooses the appropriate actions, independent of outcomes. If the firm cannot observe the actions but does recognize an emerging, initially unforeseeable, influence, it should offer incentives based on project outcomes, but retain the flexibility to modify the contract depending on whether the goal achievement became harder (“bad news”) or easier (“good news”). The contract also needs to include a minimal compensation to protect the manager from unforeseeable reductions in his wage. Finally, if the firm can neither observe the actions nor the new influences, the manager needs to be offered downside protection as well as upward incentives to motivate him to reveal and pursue unexpected opportunities: rewarding only target fulfillment reduces the manager's willingness to pursue additional opportunities.

While these contract types are intuitively appealing, no previous study has offered recommendations under which circumstances each contract type should be used. Our results offer one possible theoretical explanation for various contract forms observed in practice (these are described in the next section) and provide testable predictions under what circumstances which one should be used.

2. Literature Review

Our study is closely related to research in project management and in economics. In project management, contracts are typically classified into time and material (cost plus), fixed fee (lump sum), and incentive contracts (based on technical performance, delivery time, etc; in t'Veld and Peeters 1989, Ward and Chapman 1994). Various authors studied the effect of uncertainty and the contracting parties' prior relationship on contract choice, incentives, and negotiation costs (Bajari and Tadelis 2001, Corts and Singh 2004, Kalnins and Mayer 2004). The focus in this literature is on the management of “standard uncertainty” where the major influence variables are known (only their values are not).

A few articles make specific suggestions for innovative businesses or technologies. Several authors suggest that in presence of high uncertainty, the focus of incentives should be on input and process‐based measures rather than on output measures: people should be judged based on “the quality of their efforts” rather than on market outcomes (Davila et al. 2006, Hauser 1998, HBR 1995, Sutton 2001, Pich et al. 2002). Others propose to offer managers of innovative projects downside protection, that is, not to punish employees who take risks and fail, because such punishment would reduce the willingness to take on novel projects (Kohn 1993, Quinn 1985, Sutton 2001). Farson and Keyes (2002) and Davila et al. (2006) suggest that both failures and successes need to be evaluated subjectively to “discount the effect of uncontrollable events”: failures might be “excusable” and should not be punished, while successes due to “good fortune” should not be rewarded. Finally, “visible and significant” output‐based upward incentives, such as stock options, are suggested for innovative projects (HBR 1995, Loch and Tapper 2002, Quinn 1985). Kaplan and Strömberg (2003) observe that in venture capital contracts, both the outcome‐dependent part of remuneration and the board control rights of investors increase with the venture's uncertainty. In sum, management literature proposes, at various occasions, process incentives, upside incentives, and protection from failure. But which should be used when? No prescriptive theory is available, and indeed, some of the proposed arrangements contradict one another.

In economics, principal‐agency theory has developed a comprehensive body of knowledge about incentives under standard uncertainty (Mas‐Colell et al. 1995). However, when emerging unforeseen events require actions not even conceived at the outset, complete incentive contracts cannot be designed. Relative compensation schemes can address “common changes in the environment” (Green and Stokey 1983, Nalebuff and Stiglitz 1983, p. 21), but are not applicable when unforeseen events affect only one project or affect projects differently.

Unforeseen uncertainty has been used to explain incomplete contracts (e.g., Williamson 1975). Reallocating bargaining power (through property rights or authority) can avoid hold‐up problems (Grossman and Hart 1986). In a welfare neutral setting (but not a principal‐agent setting), optimal contracts are not affected by unforeseen events if possible payoff outcomes can be foreseen and the parties have access to a court (Maskin and Tirole 1999).

Some recent articles consider the effect of unforeseeable uncertainty on preferences (e.g., Dekel et al. 1998, 2001, Sagi 2006). This work develops axiomatic characterizations of preferences over the incomplete choice set “as if” the agent had his own representation of the complete state space. Applications include investment decisions (Kawamura 2005) and buyer–supplier settings (Anderlini et al. 2007). Our model differs from this and the incomplete contracts literature in that the agent takes further actions after an unforeseen event occurs. Thus, the uncertainty resolution influences the action choice.

A concept that is different from, but sometimes confused with, unforeseeable uncertainty is ambiguity. Ambiguity describes the situation of knowing the state space, but not the probabilities over it. Ambiguity aversion, the dislike of not knowing probabilities, prompts agents to behave conservatively (e.g., Camerer and Weber 1992, Klibanoff et al. 2005). Ambiguity models usually consider several probability distributions that are consistent with the agent's beliefs. Because the possible probability distributions are known, a complete contract can be drawn up, which is contingent on the realization of one of these distributions.

Unforeseeable uncertainty goes beyond ambiguity: Not only probabilities, but the state space and the available actions are partially unknown. If unforeseen events occur, they change the action choice set and enlarge the known state space. Because the events cannot be initially foreseen (by definition), a contract cannot be contingent on any pre‐specified event.

Two previous studies consider agents who act after unforeseen events have occurred. First, Simon (1951) allows a principal to choose from an a priori specified set of actions after the state of nature is known (authority relationship). This contract can accommodate unforeseen events as long as the pre‐specified choice set is still appropriate. Second, MacLeod (2000) considers a contract without time to renegotiate (e.g., fire fighters or surgeons), where the appropriate action is ensured ex post by “pattern matching” and a third party.

We will not assume any third party payments; in addition, we will also consider cases in which the principal cannot monitor the agent's actions and has less information about the project than the agent (who learns more details over time). We will show how an upfront contract can account for the unforeseeable uncertainty by requiring specific updates. In doing so, we make one critical assumption: It is socially unacceptable (or even illegal) to offer a contract with a certain “potential” (expected value) and then unexpectedly downward adjust that potential, because this would violate social justice and fairness.

This assumption is supported by the literature on “procedural justice” or “fair process” (for reviews, see Greenberg 1990 and Anderson and Schalk 1998). This literature suggests that psychological contracts between employees and the firm govern what is considered a fair process (Robinson and Rousseau 1994). Violations of these contracts result in a feeling of anger, betrayal, and resentment, causing employees to leave the company, neglect (waste time, call in sick, disobey instructions), or even sabotage (damage equipment; e.g., Skarlicki and Folger 1997, Turnley and Feldman 1999). Kim and Mauborgne (1997, 1998) have argued that the change in attitude is even more damaging when knowledge sharing is critical (e.g., in new product projects), because it cannot be monitored and enforced. Wu et al. (2008) analyzed with a principal‐agent model how such behavior can result from fairness sensitivity.

3. A Model of Unforeseeable Uncertainty

We consider a situation in which a principal (the firm, or senior management) employs an agent (project manager) to pursue a novel project. Both parties are aware that they have knowledge gaps and that, therefore, unforeseen events might emerge, requiring mid‐course adjustments to the initial project plan.

Similar to work in economics (e.g., Dekel et al. 2001, Sagi 2006), we model unforeseeable uncertainty by the incompleteness of the known state space (see also Sommer and Loch 2004). Let Ω denote the set of all possible states of the world ω. A state ω=(x 1, …, x n ) contains all variables x i that might possibly influence the project payoff Π. Π depends both on ω and on the actions a∈A: Π(a, ω). We denote the conditional probability density function (pdf) of Π over ω by f(Π|a), given action a has been taken. To simplify notation, we assume that f is continuous and Π is bounded, so that ∫Πf(Π|a)dΠ exists.

Unforeseeable uncertainty means that the project manager is not aware of all variables influencing performance. Let Ω K denote a d‐dimensional subspace of Ω, containing the known variables ω K =(x 1, …, x d ) the manager is aware of. Similarly, let Ω N denote the complement of Ω K containing the not‐known variables ω n =(x d+1, …, x n ) that the manager cannot foresee. In addition, the manager recognizes only a subset of the available actions A K ⊆A because he cannot identify actions associated with changing unknown variables.

While project managers may not know in a novel project what the unknown variables ω n are (by definition), empirical evidence suggests that they typically do know areas of knowledge gaps and can diagnose their existence at the outset, for example, from understanding that customer behavior is not predictable for a novel project category (Loch et al. 2008, McGrath and MacMillan 1995). In other words, it is reasonable to assume that firm and manager can diagnose whether they are vulnerable to unforeseeable, emerging events (although they cannot know what they are and how they will influence project performance).

The manager implicitly (not consciously) assumes that the unknown variables take on some fixed default value  . In the introductory “1471 Call Back” example, the project managers implicitly assumed that the right product design was hardware, and the business model was based on hardware driving sales revenues.

. In the introductory “1471 Call Back” example, the project managers implicitly assumed that the right product design was hardware, and the business model was based on hardware driving sales revenues.

The unknown variables thus enter the projected performance function as parameters:  , and the corresponding pdf is thus conditional on the implicit assumptions about them: f(Π|a,

, and the corresponding pdf is thus conditional on the implicit assumptions about them: f(Π|a,  . When the unforeseen variables emerge and are recognized, the manager learns the pdf f(Π|a) of the performance Π(ω, a) defined on the full state space Ω and the full action space A (now including actions that can influence or mitigate the effect of the previously unknown variables). Note that, in contrast to Bayesian learning (where an informative signal conditions the pdf), the recognition of unforeseen influence factors ω

n

enlarges the state space, making the pdf no longer conditional on

. When the unforeseen variables emerge and are recognized, the manager learns the pdf f(Π|a) of the performance Π(ω, a) defined on the full state space Ω and the full action space A (now including actions that can influence or mitigate the effect of the previously unknown variables). Note that, in contrast to Bayesian learning (where an informative signal conditions the pdf), the recognition of unforeseen influence factors ω

n

enlarges the state space, making the pdf no longer conditional on  .

.

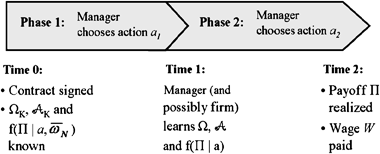

4. The Incentive Problem

In order to focus on the key question, we consider a simplified project time line with only two phases: one before and one after unforeseen events emerge (see Figure 1). When the contract is signed at the outset, only a subset Ω

K

⊂Ω of the state space and a subset A

K

⊆A of the available actions are known to both parties, and the pdf is conditional on the implicit assumptions about the unknown variables  . This reflects the typical case in novel projects or in start‐ups, where the firm or entrepreneur goes ahead based on an initial plan, knowing that the plan will change due to unforeseen events.

. This reflects the typical case in novel projects or in start‐ups, where the firm or entrepreneur goes ahead based on an initial plan, knowing that the plan will change due to unforeseen events.

After some initial actions a

1 (chosen based on the initial information  , as prescribed in standard principal‐agent theory), the unforeseen variables ω

n

are observed by the manager, who can now identify Ω, A and the corresponding pdf f(Π|a). In our “1471” example, the project managers realized that the most relevant design variables concerned a service design, and that revenues would be driven by call traffic, not sales. Once the unforeseen influences became visible, they drew the right conclusions. This is representative as the problem is usually not that managers cannot conceive of or understand the originally overlooked influence; it is simply infeasible to initially identify all implicit assumptions.

, as prescribed in standard principal‐agent theory), the unforeseen variables ω

n

are observed by the manager, who can now identify Ω, A and the corresponding pdf f(Π|a). In our “1471” example, the project managers realized that the most relevant design variables concerned a service design, and that revenues would be driven by call traffic, not sales. Once the unforeseen influences became visible, they drew the right conclusions. This is representative as the problem is usually not that managers cannot conceive of or understand the originally overlooked influence; it is simply infeasible to initially identify all implicit assumptions.

The (initially unforeseen) variables in ω n may or may not be observed by the firm, that is, upper management might be too far away from the project to zero in on these changes without indications from the project manager. If only the manager (but not the firm) sees the emerging new variables and the initially inconceivable actions, we have a situation of asymmetric information. Note that this situation is different from hidden information, where the set of possible events and actions are known to both parties at the outset and event‐action correspondences can be specified a priori, leading to truthful revelation of the information.

After observing the new variables ω n , the manager chooses his second action a 2. Thus, the complete action a consists of two parts a=(a 1, a 2), for which the manager incurs a cost c(a). The firm may or may not observe these actions. At the end of the project, the project performance Π is observed by both parties, and the wage W is paid to the manager.

We assume that the manager is averse to standard uncertainty (risk), a standard assumption in principal agency theory. Thus, his utility U[W−c(a)] is concave increasing in W. In addition, we assume he is averse to unforeseeable uncertainty: For the agent to accept the contract, it has to guarantee that he does not prefer to abandon the project for an outside opportunity both before and after new information is revealed. In contrast, the firm is risk neutral with respect to both standard and unforeseeable uncertainty and hence maximizes its expected payoff E(Π−W). Large firms are typically willing to undertake projects with unforeseeable uncertainty and to absorb its effects (Quinn 1985).

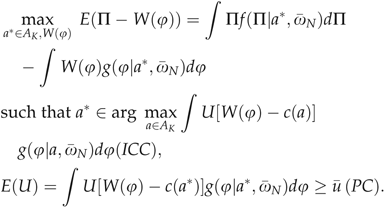

We follow classical principal agency theory by assuming that the firm offers the manager a wage contract with the goal to maximize its expected payoff, while ensuring that the manager accepts the contract (participation constraint, PC) and, given his more detailed knowledge and operational autonomy, that he chooses the “right” actions that maximize the firm's payoff (incentive compatibility constraint, ICC). The wage contract W must be based on factors observed by both parties. Thus, W is a function of the payoff Π or the action choice a (if observable for the firm). Let ϕ denote the factors W depends on, and g(ϕ) the pdf of ϕ, (i.e., if ϕ=Π then g=f, and if ϕ=a then g(a=a′|a′)=1 and g(a≠a′|a′)=0). The firm's initial maximization problem (based on the initially estimated probabilities and state space) is thus given by:

, for example, from accepting a different assignment or from leaving for a different employer. We make the implicit assumption that the payment is enforceable, that is, the firm has to honor the wage contract and cannot default on its promised payment. Our model can be extended to non‐enforceable contracts (where the firm could default on its payment without the manager having a legal recourse), in which repeated interactions (future projects) act as an enforcement device.

, for example, from accepting a different assignment or from leaving for a different employer. We make the implicit assumption that the payment is enforceable, that is, the firm has to honor the wage contract and cannot default on its promised payment. Our model can be extended to non‐enforceable contracts (where the firm could default on its payment without the manager having a legal recourse), in which repeated interactions (future projects) act as an enforcement device.

Now we can precisely describe the difficulty caused by unforeseeable uncertainty: When the manager learns Ω, A and thus the revised pdf f(Π|a), completely new actions might be needed or the actions specified for phase 2 might no longer satisfy the ICC, i.e., the agent might receive a higher payoff, choosing different actions than the required ones. Moreover, with the revised pdf the PC might no longer be met, for example,  : the expected wage after the emergence of new unforeseen events could decline. A manager might refuse to work on a project that is vulnerable to being affected by unforeseen events, or might abandon or sabotage the project, feeling betrayed by being held responsible for events outside his control.

: the expected wage after the emergence of new unforeseen events could decline. A manager might refuse to work on a project that is vulnerable to being affected by unforeseen events, or might abandon or sabotage the project, feeling betrayed by being held responsible for events outside his control.

In the next section, we will show that the initial contract should specify up front the adjustments to be made if and when unforeseen events occur. While the contract cannot be contingent on specific unforeseen events (by definition), the adjustment clause can call for and specify the type of changes to be made to the contract if new variables and actions emerge. These adjustments ensure that the manager accepts the contract at the outset and that the optimal actions are incentive compatible at the time when they are to be taken.

5. Structure of the Contract

In this section, we analyze how contracts need to be structured to maintain incentives in presence of unforeseeable uncertainty. Both the agent and the principal are aware at time 0 that they know only a subset Ω K ⊂Ω of the state space and only a subset A K ⊆A of the available actions. This knowledge allows the firm to specify adjustments up front in the contract. For example, if an unforeseen event occurs and this event makes the achievement of a certain project payoff more difficult, a bonus contract could specify that the bonus hurdle will be reduced (see Section 5.3). To obtain the contracts, we make the following assumptions:

A .

.

This assumption is fulfilled in either of two conditions: (a) It is socially unacceptable to offer a contract with a certain “potential” (e.g., with a certain expected value) and then unexpectedly downward adjust that potential mid‐course. Such downward adjustment due to unforeseen events is interpreted as arbitrary, excessively burdening the employee with risk and violating social justice and fairness (see the discussion in Section 2). (b) The manager can still revert to his outside option  (possibly with some penalty) after unforeseeable influences have emerged. If either (a) or (b) is fulfilled, Propositions 2 and 3 hold.

(possibly with some penalty) after unforeseeable influences have emerged. If either (a) or (b) is fulfilled, Propositions 2 and 3 hold.

A

If the action a is not observable, the contract must base W on the observed performance Π. In general, the shape of the wage function depends on how informative the observed outcomes are about the manager's actions; the theoretically optimal W depends only on the informativeness of the outcome about the chosen actions. Thus for some range of Π the optimal wage function may even decrease in Π (Salanié 1997). Because such contracts are not observed and would be hard to justify in practice, we restrict our attention to more realistic contracts with a monotonic wage function. Monotone wage functions are indeed optimal if the Mirrlees‐Rogerson conditions hold, (an assumption often made to guarantee the validity of the first‐order approach, Rogerson 1985). Furthermore, Holmström and Milgrom (1987) showed that monotonic (linear) functions are more robust than more complex contracts, remaining at least approximately optimal after small changes in the environment.

A

This assumption corresponds to the typical situation in practice: While upper management might be too far removed from the project to observe the previously unknown influence factors on its own initiative (it might be too expensive to monitor), the firm can verify the unforeseen events ex post after the agent has pointed them out. The firm might be able to verify the event directly in an audit, which is much cheaper than to search for unknown factors, not knowing where to look. In our “1471” example, BT could verify that the households who had the service “crutch” were as satisfied as those who had the actual phone (e.g., from interview recordings), and that the call volumes made the service charge unnecessary. More generally, the existence of an additional market opportunity is ex post verifiable, for example, in a targeted market test.

We distinguish four cases, which result from the combination of (a) whether or not the firm can observe the manager's actions a and (b) whether or not the firm can observe the emergence of unforeseen variables ω

n

(and thus Ω, A and f(Π|a)). In all cases, both parties know the initial distribution  and the cost function c(a) and both observe the final payoff Π. The assumptions required for each case are noted in the propositions.

and the cost function c(a) and both observe the final payoff Π. The assumptions required for each case are noted in the propositions.

5.1. Illustrative Example

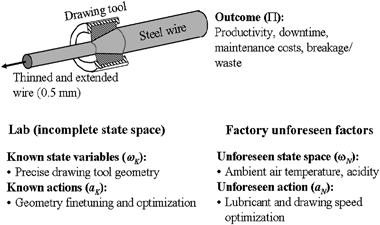

We accompany our formal results with a second example to illustrate the contract adjustment. This is a simplified representation of a real case with technical uncertainty (complementing the case of market uncertainty from the opening BT example) in tire thread process development: tire thread consists of very finely drawn steel wire which is then wound together into a mesh that reinforces steel tires. The metallurgy of cold drawing is poorly understood and complex, with many interacting factors influencing the wire strength.

The company developed and tested a new cold drawing tool in its R&D lab. The lab tests identified the precise geometry of the drawing tool as an important quality influence factor, which required tool optimization and fine‐tuning in the manufacturing ramp‐up (effort level of a

K

on the fine‐tuning action, see the left hand side of Figure 2). To keep the illustration simple, we provide a rough approximation of the situation we observed. We omit standard uncertainty and any actions before the unforeseen events emerge, and we reduce the multi‐dimensional performance problem to two critical performance dimensions (one known initially, and one known only after the unforeseen events emerge). In this approximation, the project manager perceives the concave process performance function  , and his effort cost for the fine‐tuning activity is c(a

K

)=a

K

+1. His utility is approximated by a linear function of his payoff (U=W−c), and his PC is normalized to zero

, and his effort cost for the fine‐tuning activity is c(a

K

)=a

K

+1. His utility is approximated by a linear function of his payoff (U=W−c), and his PC is normalized to zero  .

.

Standard optimization (ignoring incentives) tells us that the surplus‐maximizing action is a K *=4, the optimal performance Π(a K *)=12, the manager's effort cost c(a K *)=5, and the economic surplus 7. If the firm can observe the action, the contract will simply specify the optimal action and pay the manager 5 if he executes it. If the firm cannot monitor actions (moral hazard), principal‐agency theory tells us that a “hurdle contract”, which pays W=5 if the outcome Π≥12 and 0 otherwise, is optimal for a risk neutral agent (Levin 2003).

Cold drawing R&D is fraught with unforeseeable influence parameters. The team knows the transfer from a lab into a factory may produce surprises (there are too many possible influences to “fully analyze” the situation). In our example, the technicians were not aware that the drawing tool's performance also critically depended on the air temperature and air acidity, both of which were different in the factory than in the lab. Air temperature and acidity represent an additional parameter x

n

. Moreover, a second dimension of activity exists: a

n

consists of activities which change the lubricant and drawing speed, and combining these with a

K

increases the productivity. Thus, the full performance function emerges to be  . Initially, the team overlooked a

n

(implicitly setting it to a “default value” of 1) and missed the negative performance effect of the air acidity, tacitly assuming

. Initially, the team overlooked a

n

(implicitly setting it to a “default value” of 1) and missed the negative performance effect of the air acidity, tacitly assuming  . With both activities, the cost function becomes c(a

K

, a

n

)=a

K

+a

n

. We will use this example to illustrate the contract adjustments.

. With both activities, the cost function becomes c(a

K

, a

n

)=a

K

+a

n

. We will use this example to illustrate the contract adjustments.

5.2. Incentive Contracts when the Firm Can Monitor Actions

We first consider the case in which the firm can observe the manager's actions (whether or not it observes the emerging events). In this case, the optimal contract transfers the authority of choosing the actions to the firm, but requires appropriate payment of the agent's effort (whatever it may be) from choosing new actions after unforeseen events have occurred. Incentive contracts that use process monitoring and base payments on the observed actions are typically referred to as process incentives.

P

the firm has the authority to re‐determine a

2

*, if an unforeseen factor x

i

∉Ω

K

is observed, and the agent has the obligation to announce any factor x

i

∉Ω

K

unobserved by the firm.

where

where ,

,

The proof of Proposition 1 is an extension of Simon (1951). All proofs are shown in the Appendix A. If the firm can observe the actions, the payment adjustment isolates the risk averse manager from carrying any risk (up or down) resulting from either standard or unforeseeable uncertainty. In return, the firm has the right to choose the actions to be carried out. If unforeseen events are observed only by the manager, the manager is asked to reveal them, but is fully compensated for any change in the required actions.

In our illustrative example, the originally specified action is a K *=4. After the full performance function, including x n and a n , has emerged, the optimal actions are (a K *, a n *)=(6, 6), resulting in Π(a K *, a n *)=30−x n and c(a K *, a n *)=12. The firm tells the project manager to spend 6 units of effort each on geometry fine‐tuning and lubricant optimization and pays the agent a wage W=12, shielding him from any impact of the unforeseen variables and leaving his utility unchanged at U(W, c)=0. As the project manger is thus shielded, he is willing to announce unforeseen influences that are not observable to the firm.

5.3. Incentive Contracts if the Firm Cannot Monitor Actions

P

W(Π) is a non‐decreasing function of the project payoff Π, and if x

i

∉Ω

K

is observed revealing f(Π|a), the contract calls for an adjusted wage contract W

adj (implementing a new phase 2 action a

2adj

*) for which Equation (1) holds over f(Π|a). This “adjustment clause” guarantees the manager a downside protection against negative events

and adjusts the wage function to the difficulty of the situation: If ∀a

2∈A

K

the cdf

and adjusts the wage function to the difficulty of the situation: If ∀a

2∈A

K

the cdf  (1

st

order stochastic dominance)

(1

st

order stochastic dominance)  and vice versa.

and vice versa.

The adjustment clause modifies the wage function to account for the difficulty of the situation; it may make the required outcome for a given payment larger (if achieving profit became harder) or smaller (if a positive event made achieving profit easier), while guaranteeing the manager a downside protection against a lowering of the expected utility.

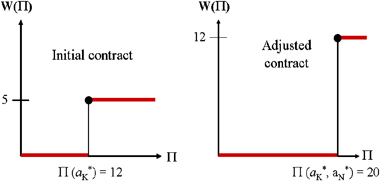

Let's demonstrate the contract adjustment in our illustrative example. We have already described the initial bonus hurdle incentive contract in Section 5.1. It is graphically shown in the left graph of Figure 3 with the performance bonus hurdle at Π=12.

After the manufacturing test, suppose it turns out that the unforeseeable quality problem from air acidity, x n , takes the value of 10. Then the optimal actions are (a K *, a n *)=(6, 6), the project manager's cost c(a K *, a n *)=12, and the achievable profit has improved to Π(a K *, a n *)=20. Given the improved potential, the firm should increase the performance hurdle at which the bonus is paid (right hand graph in Figure 3). However, with the increased hurdle comes also a higher payment (of 12 versus an originally foreseen 5). Thus, the modified contract also protects the manager from increased effort costs. The firm's remaining surplus has also improved to 8 (versus 7 originally foreseen).

P

W(Π) is a non‐decreasing function of the project payoff Π, and if x

i

∉Ω

K

is observed revealing f(Π|a) to the agent, the contract calls for an adjusted wage contract W

adj (implementing a new phase 2 action a

2adj

*) for which Equation (1) holds over f(Π|a) with the additional condition:

(revelation incentive). This “adjustment clause” guarantees the manager downside protection (

(revelation incentive). This “adjustment clause” guarantees the manager downside protection ( ) and provides incentives for the manager to reveal positive events.

) and provides incentives for the manager to reveal positive events.

Let us again illustrate this with our example: consider the same situation as in Section 5.3.1, only that the firm cannot observe the emergence of the new influences. The project manager reveals the changed situation spontaneously because he would need to invest a K =a n =3.5279, a total of 7.0548, to achieve the hurdle Π=12, but get paid only a wage of 5. Thus, the manager will reveal the new influences to get back to his reservation utility.

Now consider a slightly different situation. Suppose that the new action a

n

emerges as before, but there is no negative impact from air acidity (x

n

=0). Now, the maximum achievable performance is  . If the manager does not reveal this information, he can achieve the bonus level of 5 by choosing a

K

=a

n

=1.6754 and obtain a surplus of 1.6492 above his reservation utility. For the manager to be willing to reveal the positive news, the firm needs to reward him for identifying the new opportunity and compensate him for the surplus he could achieve. In other words, the firm needs to offer upward incentives.

. If the manager does not reveal this information, he can achieve the bonus level of 5 by choosing a

K

=a

n

=1.6754 and obtain a surplus of 1.6492 above his reservation utility. For the manager to be willing to reveal the positive news, the firm needs to reward him for identifying the new opportunity and compensate him for the surplus he could achieve. In other words, the firm needs to offer upward incentives.

When the project manager reveals a n , x n and the improved productivity, the firm sets the bonus hurdle to 30, and upward adjusts the bonus to 12+1.6492=13.6492, leaving the manager with the same surplus that he would achieve by not revealing the upside opportunity. The surplus represents an information rent that the project manager can demand because he has asymmetric information about emerging project‐relevant events. The firm is left with a surplus of 30−13.6492=16.3508. This is a substantial improvement compared with the surplus of 7 if the project manager had not revealed the newly emerged upside.

6. Discussion and Interpretation

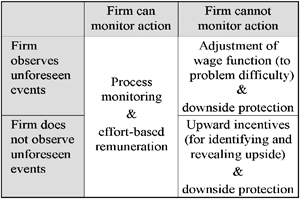

The described contracts have intuitive interpretations, and they suggest under which circumstances each of the various incentive contracts recommended in the management literature should be used. The results are summarized in managerial terms in Figure 4.

Whenever actions can be effectively monitored, our model supports the recommendation to provide process incentives (e.g., Davila et al. 2006, Hauser 1998, HBR 1995 Pich et al. 2002, Sutton 2001). Project management refers to these contracts as “material contracts,”Simon (1951) as “employment contracts.” The manager is remunerated for carrying out the requested actions, and the firm has the authority to re‐specify them in case of unanticipated events. If costlier actions become desirable (requiring more effort, or being less interesting), the manager will be fully compensated (e.g., through overtime pay, bonus, recognition, or a higher chance of promotion) and thus faces no payoff uncertainty.

Whenever action monitoring is not feasible (or too costly), outcome‐based incentives should be combined with a downside protection from unforeseen, unfavorable events. If the firm can observe the events, it should adjust the compensation to the difficulty of achieving a certain payoff, thereby isolating the manager from both the upside and the downside impacts of unforeseeable uncertainty. This scenario supports the recommendation not to punish failure (Kohn 1993, Quinn 1985, Sutton 2001), but not to reward managers for favorable events either (Davila et al. 2006, Farson and Keyes 2002). An example of “adjusting the compensation” is given by Jack Welch (then CEO of GE) in an interview (Loeb 1995):

“Our plastics business last year had an up year, something like 10% or 11%. But in my view, they had a relatively poor year. They should have been up 30% to 40%. They got caught in a squeeze with prices, and they didn't act fast enough. So, their bonuses were affected. Our aircraft engine business went down $50 million in earnings to $500 million. But we increased their bonus pool 17%. They had a drop, but they knocked the hell out of the competition around the world. They lost $2 billion in sales as the military market and the airline business came down. But they responded to their environment better and faster than their competitors did. Now, if we were operating under a budget system, plastics would be seen as having a nice year, and aircraft engines would have got a slap in the eye.”

When the manager alone observes the unforeseeable events (being closer to the details of execution), it is optimal to provide both downside protection and upside rewards for identifying unforeseen (and for the firm unobservable) opportunities. If, for example, the manager identifies and pursues an additional market or application for a product, he now benefits from the resulting payoff improvement (otherwise, he might not reveal the opportunity). These upside rewards can be interpreted as information rents paid to the agent. The model suggests that upside rewards should not be offered generally in novel projects, as is suggested in literature for novel projects (HBR 1995, Loch and Tapper 2002, Quinn 1985); they should be used only when the firm can observe neither the actions nor the unforeseen events. Otherwise upside incentives are not required and in fact inefficient.

7. Conclusion

We have addressed the question of how firms should set incentives for employees who execute highly uncertain, innovative projects. Such projects typically encounter events that cannot possibly be foreseen at the outset and require adjustments to the plan mid‐course as new information becomes available (e.g., Morris and Hough 1987 Pich et al. 2002). This prevents the applicability of standard incentive contracts, because initially specified actions and targets are usually no longer optimal after unanticipated events have occurred, and writing contracts contingent on the possible states is infeasible if the states cannot be foreseen at the outset.

We characterize incentive contracts in presence of unforeseeable uncertainty, where an uncertainty‐averse manager must take actions after unforeseen events have occurred. The optimal incentive contract defines a priori conditions for contract adjustment (contingent on effects of potential unforeseen events). The contracts have intuitive interpretations reflecting observed incentive schemes: process monitoring, downside protection, and upside rewards.

The contribution of this article is to offer a common decision framework for various incentives recommended in managerial literature: we provide a theory that offers a possible explanation of which of the empirically observed incentive schemes should be used under what circumstances. Such a decision framework for incentive contracts has not been offered before. The results are summarized in Figure 4.

An important follow‐up would be an empirical test of the theoretical propositions of this paper: the firm's ability to monitor unforeseen events and actions should influence the choice between process and outcome incentives and between protection and upward rewards. A better understanding of incentives under unforeseeable uncertainty is very valuable for firms that undertake long‐term or novel projects.

Footnotes

Appendices

Acknowledgments

The authors thank Tim Van Zandt for many insightful comments on this manuscript.