Abstract

We address the simultaneous determination of pricing, production, and capacity investment decisions by a monopolistic firm in a multi‐period setting under demand uncertainty. We analyze the optimal decision with particular emphasis on the relationship between price and capacity. We consider models that allow for either bi‐directional price changes or models with markdowns only, and in the latter case we prove that capacity and price are strategic substitutes.

1. Introduction

1.1. Background and Overview of Main Findings

Recent years have witnessed an increased interest in the use of pricing in operations management practices, with a particular focus on the integration of inventory control and dynamic (state‐dependent) pricing strategies. Concomitantly, studies focusing on the interface between capacity investment and replenishment strategies have led to further understanding of capacitated inventory systems and supply chains. A very useful qualitative insight in this context has been the understanding that capacity and inventory are in essence strategic substitutes. Roughly speaking, decision variables are said to be strategic substitutes if increasing the value of one variable decreases the return from increasing the other; a more precise definition will be advanced in section 4. One of the main motivations for the present paper is to develop similar insights that pertain to pricing and capacity decisions. As the literature review at the end of this section indicates, we are only aware of a few papers to date that focus on the problem of joint capacity planning and pricing strategies, and even less that go on to explore the three‐way relationship between capacity, inventory, and pricing decisions.

In this paper, we study a stylized problem in which a centralized monopolistic firm sells a product over a finite selling horizon; the number of periods constituting this time horizon measure the time elapsed from the first introduction of the product to the market, up until the point where the firm terminates its production and sale. The firm reviews the state of the system periodically and at the beginning of each period makes three decisions: (i) invest or disinvest in production capacity, (ii) replenish inventory (constrained by production capacity), and (iii) fix a price for the produced goods that will take effect in the following period. Subsequent to these decisions, demand is observed. We first allow the firm to carry inventory from one period to the next, and orders are allowed to be backlogged. Subsequently, we introduce a restriction that disallows carry‐over of inventory from period to period; the firm must then either satisfy inventory shortage using emergency replenishment or by paying penalty fees. In the next stage, we also restrict the firm's pricing flexibility by only allowing markdowns, i.e., the price of the product can only decrease over its life cycle.

The main contribution of this paper is in studying the relationship between pricing and capacity decisions in the context of a dynamic optimization problem that has capacity, inventory, and price as its variables. The analysis proceeds by first showing that the optimal capacity investment policy in the presence of pricing and inventory decisions is of a target interval form (see Theorem 1). Given a fixed capacity level, the optimal joint pricing–inventory decisions are seen to follow a modified base‐stock list‐price policy (see Theorem 2). These results serve as a basis for studying a model where no inventory carry‐over is allowed, and pricing is restricted to markdowns. In this important scenario we show that price and capacity are strategic substitutes both as decision variables and as state variables (see Theorem 3); an important implication is that these levers can be used in a complementary manner (see discussion in section 5.3). Several numerical examples illustrate some of these findings.

This section concludes with a review of related literature and known results. Section 2 describes the model and sets up the dynamic optimization problem. Section 3 provides the first set of results. Section 4 discusses the cases where no carry‐overs are allowed and when pricing is restricted to markdowns. Section 5 summarizes some qualitative insights that are gleaned from the main results and also provides a simple example that illustrates the key findings. All proofs are collected in the supporting information Appendix S1.

1.2. Literature Review and Positioning of the Present Paper

Given the voluminous literature on the topic of interest in this paper, we restrict our review to work that is closely related in terms of thrust and problem formulation. For a recent survey and further references on pricing, inventory, and capacity decisions the reader is referred to Chan et al. (2004, section 4.2).

A notable entry absent from the above list is work focusing on joint pricing and capacity decisions in an inventory setting, and the present paper indeed strives to fill that gap. In terms of the model and analysis tools, our work is most closely related to that by Angelus and Porteus (2002) and Federgruen and Heching (1999): the former studies the relationship between inventory and capacity, and the latter discusses inventory and prices. Our research is intended to complement theirs.

2. Problem Formulation

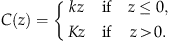

We consider a monopolistic firm that produces a single product whose capacity, inventory, and price are reviewed periodically. At the beginning of each period the firm makes three decisions: (i) capacity investment (or disinvestment), (ii) production level, and (iii) the price it will charge for the product. We assume that capacity investments and produced goods become available instantaneously. The life cycle of the product, and therefore the time horizon, is set to be T periods. The sequence of events in each period, t=1, …, T, is as follows:

Investment or disinvestment in capacity, setting it to a level equal to z

t

. Production (if needed) to set the inventory level to y

t

. A price p

t

is set and held fixed up until period t+1. Demand is realized and satisfied if it is less than available inventory, or backlogged otherwise. Backlog and holding costs are incurred.

Demand in period t, D

t

, depends on the prevailing price which is given by a general additive stochastic demand function

Feasible price levels are confined to the interval  , where

, where  and

and  are the highest and lowest prices, respectively. (In sections 4 and 5, we indicate how the main results extend to more general demand functions.)

are the highest and lowest prices, respectively. (In sections 4 and 5, we indicate how the main results extend to more general demand functions.)

Let x t be the inventory level at the beginning of period t before ordering and y t be the inventory level at the beginning of period t after ordering. The firm incurs two types of production and inventory costs: the end‐of‐period inventory carrying (and backlogging) costs, and a variable production cost. Specifically, h t (x) is the inventory (or backlogging) cost incurred in period t with terminal inventory level equals x and c t is the per unit purchasing or production cost in period t.

Let

h

t

(·) is convex for all t=1, …, T. d

t

(p

t

, ɛ

t

)=a

t

−b

t

p

t

+ɛ

t

where a

t

, b

t

>0,

, for all t=1, …, T,

, for all t=1, …, T, , for all t=1, …, T.

, for all t=1, …, T.

These assumptions ensure that the cost functions G t (y, p) are well defined, finite, and jointly convex in y and p for all t=1, …, T.

R is concave in d, where d

t

−1 is the inverse function of d

t

for fixed ɛ

t

. This assumption is rather benign and quite standard in the revenue management literature; Ferguson et al. (2006) provide examples of a linear function and an exponential demand function that satisfy these conditions; see also Chen and Simchi‐Levi (2002) for further discussion. In that case, one would need to impose directly that G(·,·) is jointly convex; see Federgruen and Heching (1999) for conditions ensuring that this holds.

is concave in d, where d

t

−1 is the inverse function of d

t

for fixed ɛ

t

. This assumption is rather benign and quite standard in the revenue management literature; Ferguson et al. (2006) provide examples of a linear function and an exponential demand function that satisfy these conditions; see also Chen and Simchi‐Levi (2002) for further discussion. In that case, one would need to impose directly that G(·,·) is jointly convex; see Federgruen and Heching (1999) for conditions ensuring that this holds.

Let γ

t

(y, p) denote the expected contribution in profits in period t, if the firm has y units at the beginning of the period (i.e., post‐production) and it charges p per produced unit that is sold on the market. That is, in period t

Hence h c amalgamates all costs that are associated with maintaining production, but are independent of the production volume. We assume that K≥k, which reflects the fact that capacity is usually sold for less than the purchase price. Revenues and costs are discounted with a discount factor α∈(0, 1]. We note that all capacity‐related costs are taken to be time‐homogeneous for simplicity, and the analysis that follows can easily be adjusted to account for such temporal dependency. We assume that a firm begins the life cycle of the product with capacity level z 0 and inventory level x 0 (allowing for the possibility of x 0=0, z 0=0). Note that our work pertains primarily to industries in which there is short lead time for capacity changes, as well as low fixed costs for capacity changes (apart from the friction of selling–buying). In industries, such as medical devices, in which soft‐tooling is being used, such quick capacity changes are possible.

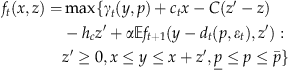

Let f

t

(z, x) be the maximum expected present value of the total net profits that can be earned in months t and on, given that the capacity level is z and inventory level is x at the beginning of period t. That is,

To recapitulate, at the beginning of each period t=1, …, T, the firm must determine a capacity investment level z′, an inventory level y, and a price p based on the initial inventory and capacity, x and z. These decisions are held fixed throughout period t. The objective of the firm is to maximize the sum of discounted profits over the time horizon T with respect to the above‐mentioned decision variables; the maximum value of this dynamic optimization problem is given by f 1(x, z).

For future purposes it will be convenient to rewrite f

t

(x, z) as follows (see Angelus and Porteus 2002):

3. The Optimal Policy and Key Relations

3.1. Main Results

In this section, we characterize the structure of a policy that maximizes the expected discounted profits. The results are very much in the spirit of those in Federgruen and Heching (1999) (albeit for a non‐capacitated system) and Angelus and Porteus (2002) (for a model with exogenously given prices).

Recall, the maximum value of this objective is given by f 1(·,·), where f t (·,·) is defined in (6). We will begin by analyzing the optimal capacity investment policy. Then, given the optimal capacity at the beginning of a period, we will derive the optimal joint inventory–pricing policy. It is important to note that the three decisions are made simultaneously; the optimal policy is described in a sequential manner to allow for a more transparent representation.

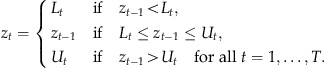

To characterize the optimal capacity investment policy, we first describe a family of ISD policies (invest/stay put/disinvest), often referred to as target interval policies.

D

L

t

≤U

t

; L

t

and U

t

are independent of z

t−1;

The upper and lower targets L t and U t can be functions of the state of the system (and past information observed up until time t), and the notation L t (·) and U t (·) will be used to indicate this dependence; in the following theorem, both are functions of the initial inventory x.

T .

.

Based on the optimal capacity investment, we will now show that the optimal joint production–pricing decision takes the form of a modified base‐stock list‐price policy (we use the term “modified” because of the capacity constraint on the production). This policy is characterized by a base‐stock level and a list‐price combination  which are given as a function of the initial inventory and capacity (x, z); the former and latter functions are the optimal inventory position and price levels, respectively, given that period t begins with capacity z and inventory level x, and are derived as follows:

which are given as a function of the initial inventory and capacity (x, z); the former and latter functions are the optimal inventory position and price levels, respectively, given that period t begins with capacity z and inventory level x, and are derived as follows:

and

and  for given initial capacity and inventory levels, x and z, are established in the proof of Theorem 2. Note that the “hat” notation is used to distinguish the optimal policy. For the purpose of the following theorem, we introduce the following definitions.

for given initial capacity and inventory levels, x and z, are established in the proof of Theorem 2. Note that the “hat” notation is used to distinguish the optimal policy. For the purpose of the following theorem, we introduce the following definitions.

D are said to be strategic substitutes with respect to a function

are said to be strategic substitutes with respect to a function  , if f(u, v) is submodular in u and v.

, if f(u, v) is submodular in u and v.

For a definition of submodularity, see, e.g., Topkis (1978), and for further discussion of economic implications and interpretation, see, e.g., Milgrom and Roberts (1990).

T

An optimal inventory–pricing policy is a base‐stock list price with base‐stock

For each period t∈{1, …, T}and fixed capacity and inventory state values

and list price

and list price

for t=1, …, T. At period t∈{1, …, T}and given a capacity level z: if

for t=1, …, T. At period t∈{1, …, T}and given a capacity level z: if

, it is optimal to order up to the base‐stock level

, it is optimal to order up to the base‐stock level

and to charge the list price

and to charge the list price

; if

; if

, it is optimal not to order and to charge

, it is optimal not to order and to charge

; and if

; and if

, it is optimal to order z units and charge

, it is optimal to order z units and charge

.

. , the price and inventory decision variables (y

t

, p

t

) are strategic substitutes with respect to the function a

t

(·,·,z) given in

(7)

.

, the price and inventory decision variables (y

t

, p

t

) are strategic substitutes with respect to the function a

t

(·,·,z) given in

(7)

.

R

R

4. Joint Capacity Planning and Pricing

In this section, we analyze a particular instance of the joint capacity planning and pricing problem when inventory cannot be carried over from period to period and prices can only be decreased throughout the time horizon. This situation arises when firms cannot use inventory produced in “off‐peak” periods to absorb “peak‐demand.” To this end, we assume that stockouts are satisfied at the end of the period in which they occur; Federgruen and Heching (1999) describe such a mechanism as emergency purchases or production runs.

4.1. Main Results

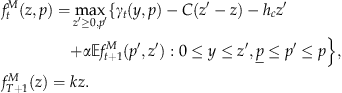

Let f

t

M

(z, p) denote the maximum expected present value of the total profits that can be earned in periods t up until T, given that period t starts with capacity z and price p. The optimality equations for t=1, …, T are given by

T

f

t

M

(z, p) is submodular and jointly concave in the state variables (p, z). The decision variables p′ and z′ are strategic substitutes with respect to f

t

M

(·,·). The optimal capacity policy is a target interval policy in each period. The capacity targets L

t

(p) and U

t

(p) satisfy L

t

(p)≤U

t

(p) for each t=1, …, T, and each initial price p. L

t

(p) and U

t

(p) are non‐increasing in p for each t=1, …, T.

Note that the upper and lower barriers L t (·), U t (·), t=1, …, T, are now functions of the price in the beginning of the period, unlike the case where inventory carry‐overs and bi‐directional price changes are allowed, in which case these barriers were functions of the inventory level in the beginning of the period.

R is concave in p and that G

t

(y, p) is jointly concave in (y, p) for all t=1, …, T. The first condition is easily satisfied for a broad family of demand functions. For a discussion of conditions that ensure the joint concavity of G

t

(·,·), see Federgruen and Heching (1999).

is concave in p and that G

t

(y, p) is jointly concave in (y, p) for all t=1, …, T. The first condition is easily satisfied for a broad family of demand functions. For a discussion of conditions that ensure the joint concavity of G

t

(·,·), see Federgruen and Heching (1999).

5. Discussion and Qualitative Insights

5.1. An Illustrative Example of the Joint Pricing–Inventory–Capacity Model

if if if

, order up to

, order up to  and set price to

and set price to  ;

; , order z units and set price to

, order z units and set price to  ;

; , order no more units and set price to

, order no more units and set price to  .

.

One can observe that, given the capacity level (after adjustment), z, the target inventory level at the beginning of the period is independent of the inventory level at the end of the previous period, x if x<a T /2−c T φ/2<x+z. Otherwise, keeping the capacity level fixed, the target inventory level is increasing linearly in x. Note that changing x may affect the optimal capacity level, and thus, indirectly affect the optimal inventory level. We next study the impact of the optimal capacity on the optimal ordering policy. It is easy to see that, unless a T /2−c T φ/2>x+z, the optimal target inventory level is independent of z.

In order to find the optimal capacity policy we need to compute the boundary functions L

T

(x) and U

T

(x). It is straightforward to show that

Thus, the width of the inactivity band can be computed in closed form and we observe that, as anticipated, the inactivity region increases with the difference between the cost of increasing capacity, and the price for sold capacity. Moreover, we observe that as the initial inventory level increases, both the upper level and the lower level of the inactivity region decrease, and thus as the inventory level increases, the optimal capacity level (weakly) decreases.

Note that if the initial capacity level z 0∈(L t (x), U t (x)), the capacity level is independent of the initial inventory. If this is indeed the case, the optimal inventory level depends on x only directly, as was discussed above. Thus, an increase in the initial inventory increases the target inventory level unless x<a T /2−c T φ/2<x+z 0. Note that in this region, the target inventory level does depend on the initial capacity level, and it increases with the initial capacity level. In all other regions, the target inventory level does not depend on the initial capacity level, but may depend on the target capacity level.

If, on the other hand, z

0>U

t

(x), then  . Note that, then, an increase in x, will decrease z, yet the sum of the two will remain constant. As the target inventory level depends only on the x+z, the target inventory level is independent of x, once x is above a level such that z

0>U

t

(x).

. Note that, then, an increase in x, will decrease z, yet the sum of the two will remain constant. As the target inventory level depends only on the x+z, the target inventory level is independent of x, once x is above a level such that z

0>U

t

(x).

We observe that for fixed b T , as the holding cost h decreases to zero, the inactivity region shrinks. Thus, capacity adjustments are always made if holding costs are negligible. At the same time, for any given value of h, if the price sensitivity b T decreases to zero the inactivity region will remain proportional to the holding cost. Thus, the higher the holding cost, the less likely that capacity adjustments will be made. To summarize: as the holding cost increases or price sensitivity decreases, the value of adjusting capacity decreases. As mentioned above, the inactivity region also depends on the difference between the cost of purchasing capacity and its selling value. In many firms, capacity changes are fairly costly. In these cases the difference between the costs will increase the size of the inactivity region, thus allowing the firms to only modify price and inventory levels, while keeping the capacity level unchanged.

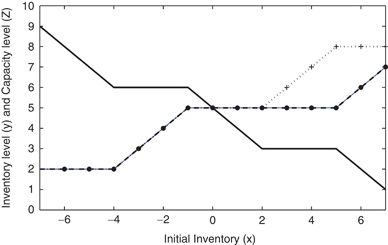

Figure 1 depicts the target inventory levels and optimal capacity levels for different levels of initial inventory. First, one can observe that in this case the optimal inventory level is a non‐decreasing function of the initial inventory level, and that capacity level is a non‐increasing function of the initial inventory. Note that the crossed line depicts the sum of the initial inventory and the optimal capacity level. This allows us to identify three production regions. As long as the initial inventory x is below 2, there is limited capacity and the firm sets the target inventory to x+z. When the inventory is the interval 2≤x≤5, the optimal inventory level is set to  , which is independent of x and z. When the initial inventory level is >5, the target inventory is identical to the initial inventory, i.e.,

, which is independent of x and z. When the initial inventory level is >5, the target inventory is identical to the initial inventory, i.e.,  . The capacity policy is as follows: as long as the initial inventory is below 6, the capacity is set to the upper limit, which decreases with the initial inventory. Once the initial inventory reaches −4, the capacity level reaches the inactivity region, and the capacity remains unchanged until the inventory level reaches −1. Note that due to the change in the production region, the slope of the capacity function changes again around inventory levels 2 and 5. One can also observe that when z is below the lower limit (e.g., when −7≤x≤−4), x+z is kept constant, and thus the optimal inventory is independent of either, as predicted by the analysis of the two‐period model.

. The capacity policy is as follows: as long as the initial inventory is below 6, the capacity is set to the upper limit, which decreases with the initial inventory. Once the initial inventory reaches −4, the capacity level reaches the inactivity region, and the capacity remains unchanged until the inventory level reaches −1. Note that due to the change in the production region, the slope of the capacity function changes again around inventory levels 2 and 5. One can also observe that when z is below the lower limit (e.g., when −7≤x≤−4), x+z is kept constant, and thus the optimal inventory is independent of either, as predicted by the analysis of the two‐period model.

5.2. Illustrative Examples of the Joint Capacity–Pricing Problem

In the region in which the initial price p>a T /2b T +c T /2, we have that if z is below a certain level, and K≫k, then both price and capacity are kept fixed. As capacity is below the level A T , the firm cannot further reduce price without incurring excessive shortage costs, and thus it will keep the price fixed. Capacity cannot change because related costs are too high. In this situation, inventory is essentially the only useful lever.

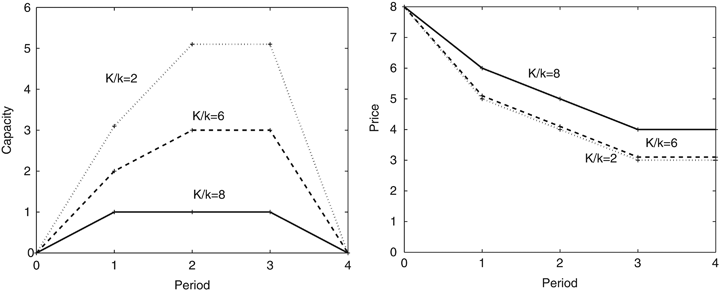

Figure 2 is concerned with three capacity investment irreversibility values: K/k=2, 6, 8 (dotted, dashed, and solid lines, respectively). For each of these ratios, we computed the optimal policy that maximizes the average profit over the finite horizon using standard dynamic programming. The figure depicts the optimal policy under a “typical” path that is obtained by setting the noise variable ɛ t to its mean value. We observe that as long as the ratio is lower than 6, the firm essentially uses the same pricing scheme, charging US$5, US$4, and US$3, and lowers the level of acquired capacity. However, once the ratio increases above 8, the firm utilizes a different pricing scheme, charging US$6, US$5, and US$4 while lowering the capacity level it purchases. As the firm can foresee that it will not be able to absorb demand using a high level of production (and capacity), and because it cannot increase its price in the middle of the product life cycle, it elects to charge a relatively high price in the first period even though the demand in this period is not greater than other periods.

The firm then decreases prices in each subsequent period. In terms of capacity planning: the firm always invests in capacity in the first period, may invest in the second period (to accommodate the peak‐demand anticipated in period 2), and “stays put” in the third period (even tough demand is expected to be lower than in the second period). The above may be viewed as an illustration of complementarity between price and capacity. To wit, the first period commences with a relatively high price, and a relatively low level of capacity, leading to a high utilization of this capacity. In the second period, the firm increases capacity level to its maximum, and lowers price to increase demand. In the third period, because the firm already has acquired a significant level of capacity, it will again lower its price to allow for full utilization of the capacity, even though the expected demand is lower than that in the middle period.

5.3. Additional Discussion

). The notion of complementarity that we are referring to is due to Edgeworth, according to which activities are considered complements if increasing the level of any one of them results in an increase in the return of engaging more in the other; see Milgrom and Roberts (1990, 1995) that summarize the principal results of the theory of supermodular optimization which underlies the notion of complementarity. They describe supermodularity as a way to formalize the intuitive idea of synergistic effects. In our example, a firm that coordinates sales planning and capacity investment has the potential to increase its profits on the basis of the observed complementarity.

). The notion of complementarity that we are referring to is due to Edgeworth, according to which activities are considered complements if increasing the level of any one of them results in an increase in the return of engaging more in the other; see Milgrom and Roberts (1990, 1995) that summarize the principal results of the theory of supermodular optimization which underlies the notion of complementarity. They describe supermodularity as a way to formalize the intuitive idea of synergistic effects. In our example, a firm that coordinates sales planning and capacity investment has the potential to increase its profits on the basis of the observed complementarity.

The first row depicts expected profits when capacity level is set at the beginning of the horizon. The second row depicts expected profits when capacity can be adjusted periodically. The third row depicts percentage improvement due to flexibility.

We observe in Table 1 that when the cost of adjusting capacity (i.e., the ratio K/k) is low, the value added from capacity flexibility is negligible. In particular, the firm can sell the capacity at the end of the life cycle without incurring any losses, and thus will probably invest in the maximum required capacity.