Abstract

The private finance initiative (PFI) is the coalition government's favoured method for funding capital projects. But,

In reality, PFI has bounced back with vigour. The bond markets remain out of action because the institutions that insured the bonds have been unable to regain their triple-A credit rating. But the banking sector is piling back in. Project finance is expensive compared to the credit boom years, but it is available — at least for short-term maturities. And, most importantly of all, the politicians are back on board.

Cabinet Office figures show that new PFI contracts involving £7 billion in capital expenditure will be signed over the next three years in England alone, mostly for new hospitals, roads and waste management facilities. A new schools PFI programme will provide an additional £2 billion of private investment under PFI. Over the same period, the Scottish government plans a further £2.5 billion in new privately financed investments for hospitals, schools and transport infrastructure. There remains a lot of opportunistic anti-PFI briefing from ministers, even as they sign off new PFI schemes, but it remains the only game in town for large public capital projects. For all the coalition's rhetoric about ‘doing PFI better’, its dependence on a credit-constrained banking sector means that the value for money of new deals will be far worse than almost all of those signed off by the last Labour government.

Cost of PFI

The PFI naysayers on the BMJ under-estimated PFI's economic and political charms — and the power of the industry (bankers, investors, contractors, advisers) that has been built up to deliver PFI projects.

British industry likes PFI. For the banks, projects offer stable, government-backed, low-risk investments, with returns higher than those available in higher-risk sectors such as commercial property. For the specialist investors and construction groups that sponsor new PFI projects, meanwhile, it offers returns of 15 to 70 per cent, along with negligible market risk and cash-flow that is unaffected by fluctuations in the wider economy. Most importantly, for government, it offers something that is probably irresistible — a chance to invest more than departmental capital budgets allow, and to do so without that investment showing up on the official borrowing figures. Given the anaemic rate of growth in the UK at present, and the priority afforded to deficit reduction by the coalition government, private finance offers a chance to get shovels in the ground, while at the same time maintaining the appearance of fiscal rectitude.

The PFI industry is increasingly bullish that good times are ahead. Ian Tyler, the chief executive of leading construction group Balfour Beatty, suggested in July that the government had ‘finally got its head around PFI’, adding that ministers had ‘faced up the hard reality’ that it was needed if investment is to take place while public capital budgets are scaled back to levels not seen since the early 1990s (i.e. the period when John Major introduced PFI in the first place). Mr Tyler's speech was followed by a number of government announcements that showed he was on the right track, including a new £2 billion PFI programme for schools and confirmation that a much-vaunted Treasury plan to seek savings on existing contracts would not come at the expense of corporate profit margins.

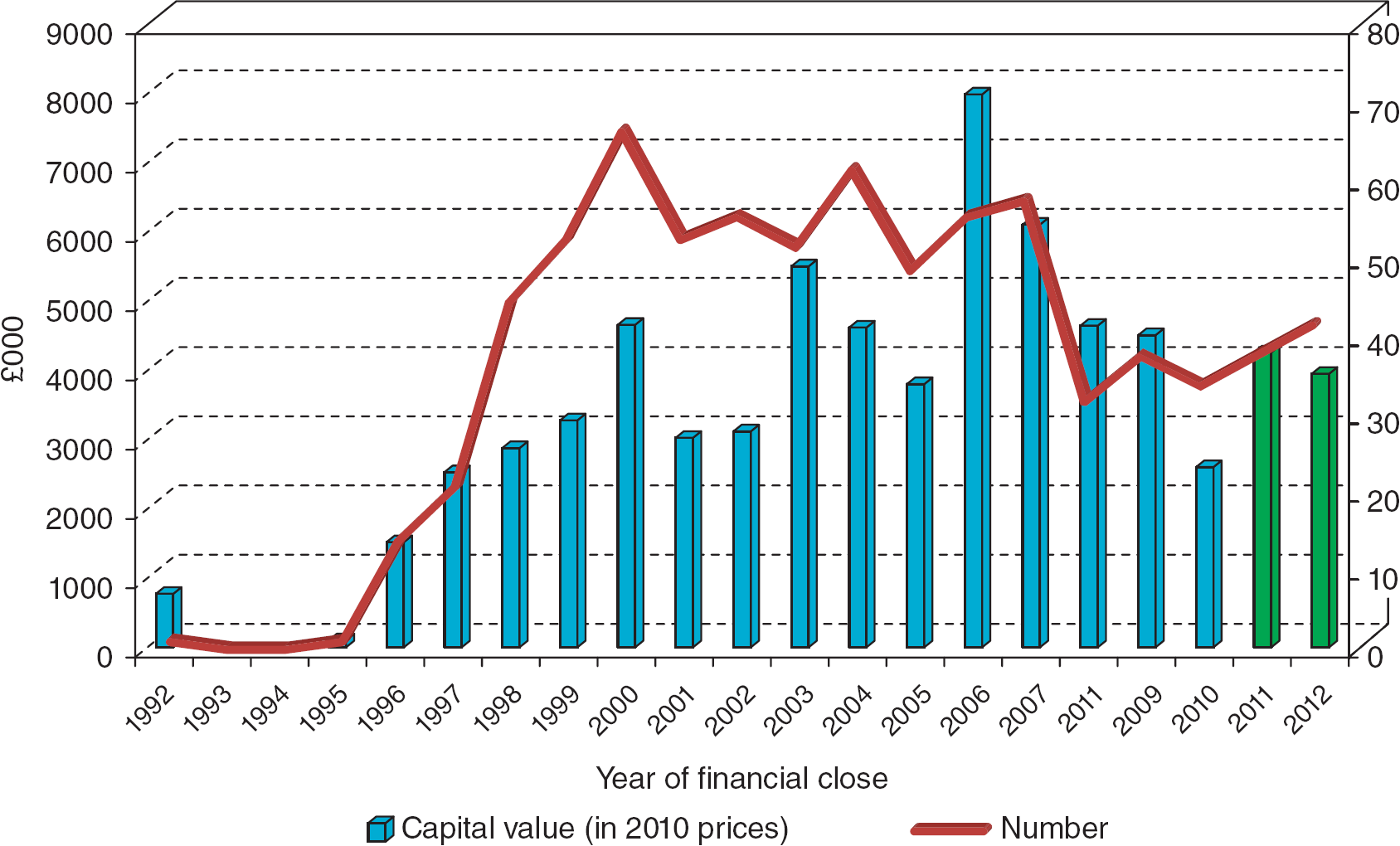

What this means is that the coalition government is pushing ahead with PFI projects that will represent much worse value for money than 99 per cent of the deals that were agreed under the Labour government, whose performance on PFI is so often decried by ministers. This is because, while private finance has always been more expensive than government borrowing, since the financial crisis the difference between the costs has widened significantly. The cost of capital for a typical PFI project is currently more than 8 per cent — double the long-term government gilt rate of about 4 per cent. The difference in financing costs means that PFI projects are significantly more expensive to fund over the life of a project, representing a significant long-term cost to taxpayers (see Figure 1).

Actual and projected number and capital value of PFI projects signed, per year (1992–2012)

No Evidence of Savings

I recently acted as the special adviser to the Treasury Select Committee in relation to its inquiry into PFI policy. The report, published in August, was described by the Financial Times as ‘the most searingly critical yet from any parliamentary committee‘. But, given the nature of the evidence we received, it could not have been otherwise. Despite reams of written evidence and many long and tiring oral evidence sessions, we saw no evidence of any savings or benefits in the operational tasks performed by PFI contractors (construction, maintenance and services). In other words, we found nothing to suggest that private sector involvement through PFI brought efficiencies of any great scale, and certainly not large enough to offset the significantly higher cost of finance identified above.

In one oral evidence session, the committee chairman Andrew Tyrie asked a selection of the great and the good from the PFI industry if anyone could cite a single piece of evidence to suggest that such efficiencies existed. He did not receive an answer. Evidence the committee studied suggests that the out-turn costs of construction and service provision are broadly similar between PFI and traditional procured projects, although in some areas PFI seems to perform more poorly. In particular, the level of design innovation is lower in PFI projects than on conventional projects, and the building quality is often worse. Perhaps most seriously, at least for sectors such as health care where the pace of change in technology and clinical practice is rapid, PFI creates a significant degree of inflexibility. This is in large part due to the irrevocable nature of contracts and the scale of the transaction costs involved in making even fairly minor changes to the specification of services.

How PFI Works — or Doesn't

The financial impact of PFI can be seen by looking at the cost projections relating to the Royal Liverpool and Broadgreen University Hospital NHS Trust's PFI project, one of the biggest PFIs to have been signed off by the coalition government so far. These projections are contained in the Trust's Outline Business Case, which was approved by the Secretary of State Andrew Lansley in June 2010.

According to this, the project is assumed to involve initial capital expenditure of £244 million and the contract is expected to run for 34 years, including a four-year construction period and a 30-year management phase in which the private partner will deliver maintenance services. During the management phase, the Trust will pay a periodic unitary charge to the private partner. This provides the private partner with a revenue stream from which to meet operational costs (primarily maintenance and lifecycle costs, along with the costs of running an office and paying insurance), and financial costs (primarily the costs of making principal and interest payments to ‘senior’ and ‘junior' debt providers, and a return to the owners of equity). The cash-flow to all these investors is called the project cash-flow, and this is the data source for this analysis.

This cash-flow takes the form of a series of expenditure cash-flows (relating to the four-year construction period) followed by a series of revenue cash-flows (in which income from the public sector significantly exceeds the private sector's operational costs, thereby providing revenue for distribution to investors). The additional financial cost of PFI can be derived by discounting the stream of cash-flows at the relevant discount rate — which is here taken to be the yield on government ‘gilts' of approximately the same maturity as the PFI loans (i.e. 30 year gilts). The current yield is about 4 per cent, but in recent months has occasionally moved up to 4.2 per cent, so this latter figure is the prudent comparator to use.

Discounting the project cash-flow stream at 4.2 per cent produces a net present value (NPV) of £175 million. This figure represents the additional financial cost of using private rather than public finance to deliver that amount of capital expenditure. If we assume that the outturn costs of construction, maintenance and services will be the same between the PFI and conventional procurement options — and there is no evidence that we should do otherwise-this means the government could have spent £175 million less, in NPV terms, by borrowing directly from the capital markets rather than through a PFI company.

A different way to analyse this is to discount the expenditure cash-flow and the revenue cash-flow separately at 4.2 per cent, and then compare the present values of each. On this basis, the present value of the revenue cash-flow is £421 million and the present value of the expenditure cash-flow is £246 million, a ratio of 1.7:1. Had the financing been provided at the gilt rate, rather than at the private finance rate, the ratio would be 1:1.

There are two different ways of interpreting the results of this analysis. The first, as noted, is that the public sector is paying £175 million more than it needs to in order to secure the amount of capital expenditure that it wants. This is the NPV of the higher cost of private finance. An alternative way to view this is in terms of foregone opportunities for additional capital investment. Assuming that PFI does not deliver efficiencies in construction, maintenance and/or services then, for the same present value of finance-related payments, the government could have secured 71 per cent more investment by borrowing on its own account.

The committee argued that the so-called ‘fiscal incentives' to use PFI should be removed. It advised the government to use PFI as sparingly as possible until the value for money and absolute cost problems associated with the policy have been addressed. The committee — which is dominated numerically and intellectually by coalition MPs who are not minded to expand public borrowing just now — said that consideration should be given to using more direct borrowing for investment. They argued that this will not directly affect the fiscal mandate as it is borrowing for investment, not for current spending.

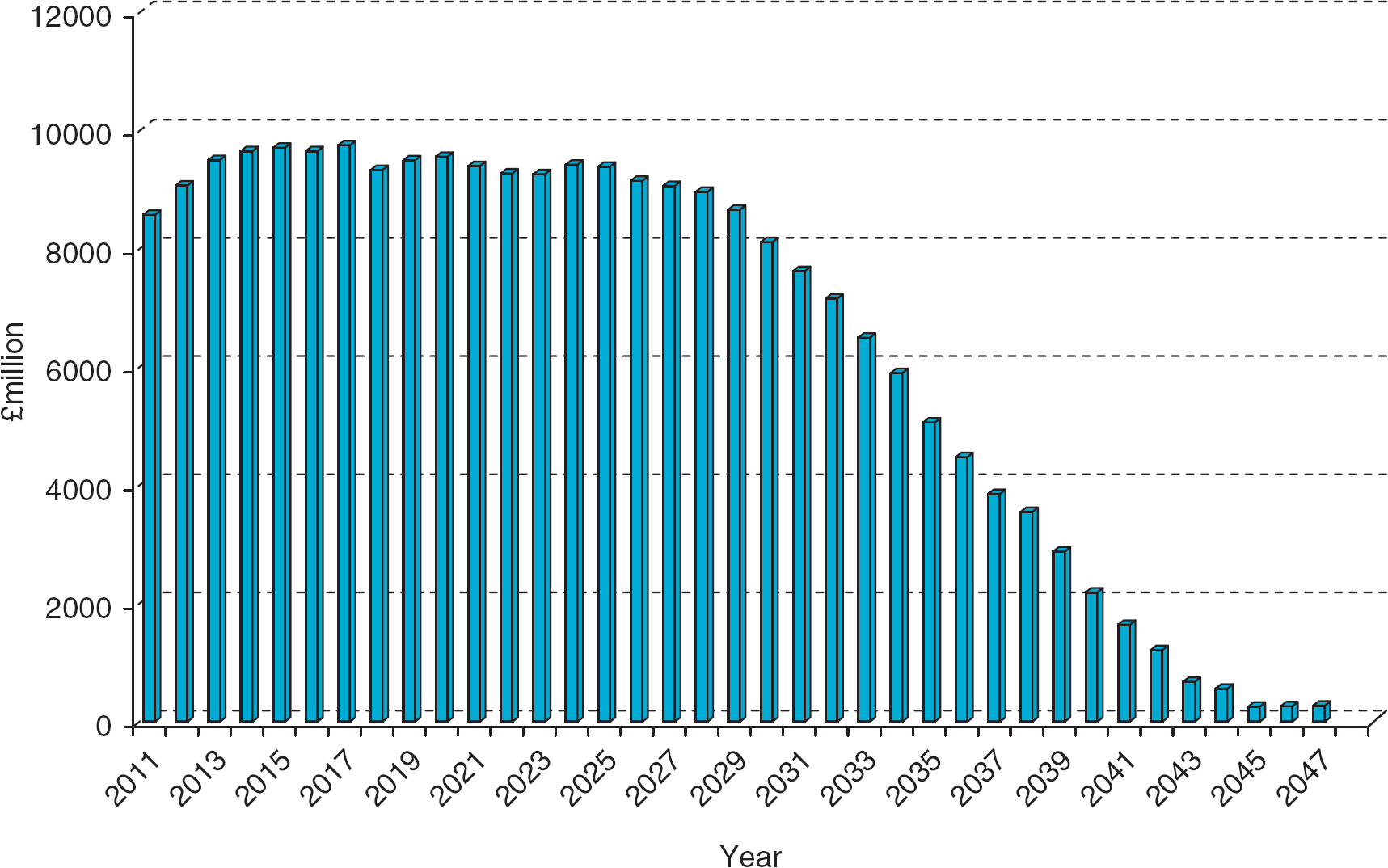

But there is little evidence that the government is listening. There are currently 61 projects in procurement, representing projected capital expenditure of £7 billion (see Figure 2).

Estimated payments under signed PFI contracts (2011–2048)

Reforming PFI

In this context, the priority for researchers is to suggest ways of minimising the ongoing revenue costs to the public sector of new PFI projects. My view is that costs can be reduced in two ways: (a) ensuring that the prices and profit margins charged by the private partner are at the market level (and that the market in this context is defined more broadly than PFI alone), and (b) that the likelihood of productivity gains throughout the contract period is recognised in contracts, so that there is a mechanism for sharing such gains. In respect of (a), it is important to consider both operational and financial costs. In terms of operational costs, it is clear that the costs of construction, maintenance and service provision must be benchmarked against best practice in the market more generally. As the National Audit Office has pointed out, this will require the compilation and active use of much better data than has been utilised by departments hitherto.

In terms of financial costs, Treasury officials have, since at least 2005, understood that project sponsors are demanding excessive rates of return. However, there is no evidence that returns have come down since then. The cost of equity for project sponsors — i.e. that which is quoted by major investors in terms of their discount rates for valuing their portfolios of PFI projects — is typically in the range of 7–9 per cent. In other words, we would expect returns to converge on this range given more or less competitive markets. They remain about double this. The returns targeted by primary investors are also around double those demanded by ‘secondary market’ investors — i.e. those who buy the equity from the primary investors — and the risks borne by primary investors during the construction and early operational stage of contracts do not appear to justify this. As the Treasury Select Committee argued, there is a case to be made for action to be taken to ensure that equity returns cluster around their efficient level, which should converge on the cost of equity range quoted by PFI investors, and much closer to secondary market discount rates.

In respect of (b), a private company in charge of services over a 30-year contract is likely to find opportunities to reduce costs over this period. Currently, of the services included within the PFI structure, only ‘soft' facilities management services, such as catering and cleaning, are benchmarked or market-tested during the contract period. As such, there is no mechanism under which the gains from such efficiencies in maintenance can be shared with the public sector — and thus the gains accrue to equity-holders in their entirety. Although maintenance services are subject to competitive tension in the tendering process, the standard PFI structure does not allow sharing from any efficiencies in building maintenance which contractors achieve over the contract's life.

Health Secretary Andrew Lansley has approved huge cost projections for new NHS Trust PFI projects. Corbis

These services are not value-tested and contractors do not share information on their maintenance spend with public authorities. This is likely to lead to opportunistic behaviour. Currently because ‘soft' facilities management services are benchmarked/market-tested, there is an incentive for a bidder to under-price this element of the services at the point of financial close, and over-price the hard facilities management services (i.e. build in a profit margin above the market level). When in subsequent years the price of the soft facilities management services are benchmarked, this will lead to the price going up. The public sector will in this event pay a market price for the soft services and an above-market price for the hard facilities management, and it will pay this above-market price for the entirety of the contract period.

One option would be to ensure that any free cash-flow (i.e. cash in excess of that required to pay operational or debt costs) in excess of that required to provide equity investors with the rate of return projected at financial close is shared with the public sector. This would ensure that the private sector retains an incentive to invest in productivity gains in maintenance (as under PFI now) but that the benefits from this are shared with the public sector (as is not currently the case).

Conclusion

At the time of writing, the government is drafting its second growth plan. An expansion of PFI now looks inevitable. It is telling that a former head of PFI policy at the Treasury, Geoffrey Spence, has been brought in to head up Infrastructure UK, a Treasury body that will play a leading role in designing the public investment elements of the growth plan.

As recent quarterly figures show, the UK needs more growth. Austerity in public spending reduces demand in the economy, and this is especially so for capital spending where the multipliers (i.e. the increase in demand provided by every additional pound spent) are highest. PFI enables the government to purchase capital goods and expand demand now, while paying for them later and in such a way that the main fiscal figures are unaffected. It is, as Nick Clegg might say, a ‘no brainer'. A key unanswered question is whether the government is interested in ways of making this policy work better for taxpayers and service users. Time will tell.