Abstract

Recent years have seen a drastic transformation in the organization of wholesale and retail markets. Where once clear distinctions between wholesale suppliers and retail competitors existed, now an era of blurring boundaries has emerged. This transformation has been marked by the introduction of online channels for suppliers to provide products directly to consumers while, at the same time, traditional retailers too persist. Thus, retailers are both wholesale customers and retail competitors of many manufacturers. The consequences of the rapid emergence of instances of such partial forward integration by suppliers are not yet fully known. To this end, we study how partial forward integration can affect competing firms' strategic investments. We find that integration shifts the environment from being one in which firms invest to undercut retail rivals to one in which firms invest more in boosting demand, even that of their competitors. A case in point is the tendency for a manufacturer to invest broadly in brand promotion (benefiting both itself and its retail competitor), rather than heavy promotion of its own sales channel. The shift in the nature of strategic investments arising from partial forward integration implies that such integration can benefit firms and consumers alike, even the firm which finds itself reliant on a competitor for supplies.

Introduction

Traditional views of distribution entail clear distinctions between vertical relationships among supply channel partners and horizontal relationships among retail competitors. Recent years, however, have seen a dramatic shift in the way products reach consumers which has, in turn, revolutionized the face of distribution channels. In particular, partial forward integration by suppliers into retail markets has led to a blurring in traditional boundaries. In such environments, a supplier can be both a (vertical) input provider to a traditional retailer while also competing in the (horizontal) market with the same retailer to reach end consumers.

In other words, partial forward integration is characterized by circumstances where a supplier to a firm also serves as the firm's competitor. Examples include soft‐drink producers, cereal manufacturers, and gasoline refiners who supply both to downstream affiliates and to retail competitors. Company‐owned franchises that compete for territory with independent franchises as well as factory outlets and catalog sales also fit the bill. Yet, the ubiquitous presence of partial forward integration did not take hold until the onset of the e‐commerce era, during which the joint presence of traditional retailers and online sales arms of manufacturers has become rampant (e.g., Tedeschi 2005).

In this article, we consider the ramifications of partial forward integration for the critical issue of firms' strategic investments. Research in economics, marketing, operations, and related fields has consistently stressed the crucial role of investments in altering product demand. This literature notes that a firm can engage in initiatives to promote its own demand (self‐investment) as well as undertake initiatives that can alter a rival's demand (cross‐investment). Although self‐investments are, of course, commonplace, cross‐investments too are prevalent. Cross‐investments can take positive forms, such as the promotion of product categories in lieu of specific brands or retail outlets, as well as negative forms, such as comparative advertising, establishing exclusive distribution arrangements, and lobbying for regulations that adversely affect rivals.

A typical case of positive cross‐investment is Sharp's aggressive promotion of Liquid Crystal Display (LCD) technology for flat panel televisions: Not only did this investment spur demand for Sharp's own products but it also boosted consumer interest in similar offerings of its main rivals, Sony and Samsung. Prominent examples of negative cross‐investment include Tylenol's ads alerting consumers that ibuprofen can cause stomach problems (Sorescu and Gelb 2000) and Apple's now iconic Mac vs. PC ad campaign that does less to promote its own product as it does to portray its competition as irrevocably “uncool.” These are not isolated incidents—negative advertising is estimated to be the source of one‐third of all advertisements (Grewal et al. 1997).

In terms of product promotion, the choice between positive self‐investments (constructive advertising) and negative cross‐investments (combative advertising) is well recognized as an important one (see, e.g., Chen et al. 2009). Even more broadly, as stressed in Iyer et al. (2005), a key consideration in promotion is whether to target consumers with already strong brand preferences (via positive self‐investment, for example) or to make strong distinctions to influence comparison shoppers (via a mix of positive self‐investment and negative cross‐investment, for example). It is choices such as these, and the impact of forward integration on them, which we detail in this article.

The first key implication of our analysis is in demonstrating how blurring vertical and horizontal boundaries created by partial forward integration can alter firms' investment choices. In particular, changes in the structure of distribution channels critically alters competitive posturing in the retail realm and pricing in the wholesale arena, which in turn alters investment decisions. We demonstrate that partial integration leads market participants to increase investments, both self‐ and cross‐investments, in product demand. Moreover, it leads the competitor who doubles as a supplier to take a much more cooperative posture in strategic investments, this despite the fact that its rival is harsh in its response.

To elaborate, under traditional distribution channels, wherein an independent supplier provides products to retail rivals, each rival has strong incentives to engage in predatory cross‐investments to undercut the competitive position of its respective rival. Under forward integration, the supplier, a vertically integrated provider (VIP), not only makes inputs but also competes in the final goods market. As might be expected, the VIP uses its pricing power to charge more than cost to its retail rival in wholesale trade. Thus, each unit of output sold by the VIP's rival in the retail market affords a wholesale markup for the VIP. Cognizant of its wholesale profits, the VIP seeks to provide a credible means through which it can convince its retail rival (i.e., wholesale customer) to procure more inputs. This desire translates into positive cross‐investments by the VIP, a stance that is not reciprocated by the rival. That is, the VIP has incentives to boost its retail rival's demand, whereas the retail rival seeks to undercut the VIP's retail demand. As such behavior helps balance the VIP's retail and wholesale profits, the VIP is a willing conscript in such asymmetric actions.

Our second key result is that the increase in investments due to partial forward integration, particularly the positive cross‐investments from the supplier, can translate into Pareto gains from such integration. That is, not only are the integrated firm and consumers better off due to integration, but so is the retailer who is beholden to its own competitor for inputs. This may provide some justification for the survival of the traditional retailer in the face of expanded e‐commerce efforts by manufacturers. True, such e‐commerce efforts stand to poach potential customers from bricks and ‐mortar retailers. However, at the same time, the e‐commerce efforts ensure the manufacturer has enough “skin in the game” to invest in brand and product line promotion. Provided the e‐commerce channel is not too much of a competitive threat (i.e., enough customers prefer a traditional shopping experience), all parties can gain from such expanded reach by the manufacturer.

Besides demonstrating how partial forward integration can change the nature of firm investments, our results also offer empirical predictions. First, firms and industries characterized by partial forward integration (i.e., hybrid distribution) should exhibit more positive investments and marketing/promotion efforts than other, traditional industries. The natural question that comes from this prediction is what industries have such arrangements. To that end, we note that hybrid distribution represents a mid‐point between the extremes of full vertical integration and complete reliance on independent distribution. Perhaps not surprisingly, firms that exhibit this mid‐point distribution form prominently are “middle market” firms, those residing in the vast space between small locally run businesses and large multinationals. Despite making up one‐third of private sector GDP and jobs, the middle market has been largely unstudied until recent years (National Center for the Middle Market 2011). Our results suggest that given its use of hybrid distribution, the middle market is likely to exhibit notably greater (and more constructive) investment than other types of firms.

A second prediction of our analysis is that among those industries with hybrid distribution at the forefront, producers focus investments and marketing on brand and product line promotion, while independent distributors hone investments on promoting their own distribution channel. As an example of such asymmetric cross‐investments manifest in practice, producers that sell through their own outlet stores as well as through independent retailers often undertake substantial brand‐specific advertising (i.e., positive self‐ and cross‐investments). In contrast, local retailers that sell such products often spend their advertising dollars promoting buying from their store and even demonizing the service provided by “impersonal” factory outlets (i.e., positive self‐investment but negative cross‐investment). Our results suggest that this phenomenon is far from unusual but instead may be exhibited empirically by a broad swath of firms, those in industries characterized by hybrid distribution.

As alluded to previously, the changing face of distribution channels has not gone unnoticed, including in academic research. Extant work has examined both causes and consequences of integration. In terms of causes, research has shown that partial forward integration can permit suppliers to better reach heterogeneous consumers, more effectively monitor independent distributors, and/or signal product profitability (Dutta et al. 1995, Gallini and Lutz 1992, Vinhas and Anderson 2005). In the case of Internet sales, Chen and Sudhir (2004) also demonstrate that the reduced search costs of a direct channel can reduce competitive pressure by permitting more precise consumer targeting among firms. In terms of negative consequences, the downside of partial integration lies in concerns of excessive supplier encroachment and the related inability to “direct traffic” in the channel (Kalnins 2004, Vinhas and Anderson 2005).

Concerns of excessive encroachment under partial forward integration also come with subtle benefits. For one, fear of its impending aggressive retail posture leads the supplier to take a more cooperative wholesale posture (Arya et al. 2007, Chiang et al. 2003). Such a cooperative wholesale posture by the supplier can also be reciprocated by marketing efforts undertaken by a retailer (Wang et al. 2009). Our result, that strategic investments are notably altered by partial forward integration, provides a similar theme. In contrast to Wang et al. (2009), however, we demonstrate that when a retailer can choose among self‐ and cross‐investments, the investment/marketing incentives are more nuanced. Though the supplier has incentives to promote the brand broadly, the retailer's incentives are more focused on promoting its own channel (and undercutting the supplier's channel). The net effect of this positive tack taken by the supplier that is not reciprocated by the retailer is that partial forward integration can not only benefit the manufacturer but can also benefit the traditional retailer.

The remainder of this article proceeds as follows. Section presents a baseline model of traditional distribution with a supplier and two independent retailers and identifies the ensuing equilibrium. Section presents the outcomes under partial forward integration, where the supplier is also one of the retail competitors. Section presents the key results of the economic consequences of partial integration: 4.1 examines the investment effects; 4.2 demonstrates the concomitant welfare effects; 4.3 considers different bargaining arrangements; 4.4 addresses the effects of confidentiality clauses; and 4.5 and 4.6 vary the nature of competition and investments, respectively. Finally, section concludes.

Traditional Distribution

Model

We consider a standard model of two retail firms, denoted firms 1 and 2, who engage in Cournot competition at the retail level. The (inverse) demand function in the retail market is p i = a − q i − γq j , i, j = 1, 2; i ≠ j, where p i denotes the price for firm i's good, and qi and q j denote the quantities supplied by firms i and j, respectively. The parameter γ ∊ (0, 1) represents the degree of substitution among the competing products with the limiting values of 0 and 1 corresponding to the cases of independent goods and perfect substitutes, respectively.

The firms rely on inputs supplied by an independent upstream monopolist. Each unit of the final product requires one unit of the input. The supplier charges a per‐unit wholesale price of w i to firm i. We normalize the supplier's production cost to 0 and let c denote each retail firm's cost of converting and selling each unit of the input, a > c. Following Singh and Vives (1984), it will be convenient to work with α, α = a − c, the demand intercept net of (downstream) cost.

Prior to purchasing inputs from the supplier, the downstream firms can each undertake strategic investments, either to affect their own profitability (self‐investments) or to affect their rival's profitability (cross‐investments). Specifically, firm i can alter its (net) demand intercept by s

i

through a self‐investment of

The timeline of events is summarized in Figure .

Timeline

Given this basic setting, we seek to identify equilibrium investment levels, profits of each firm, and implications for retail consumers. The ensuing analysis employs backward induction to identify the (subgame perfect) equilibria.

Subsequent to undertaking investments, firm i's net demand intercept is α + s

i

+ x

j

, indicating a boost (decline) in demand from positive (negative) self‐investment or positive (negative) cross‐investment by the rival. Thus, at the retail competition stage, given investment levels, wholesale price, and rival quantity, each firm chooses its product quantity to maximize its respective profit, as in Equation :

Jointly solving the first‐order condition of Equation for each firm reveals the chosen quantities as a function of investment levels and wholesale price:

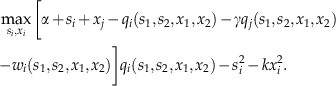

Intuitively, in q i (w 1,w 2,s 1,s 2,x 1,x 2), firm i's chosen retail quantity is increasing (decreasing) in its own (rival's) net demand and decreasing (increasing) in its own (rival's) wholesale price. Further, the degree of product substitutability governs the extent to which firm i's demand depends on its rival's particulars.

The equilibrium retail quantity decisions of the two firms determine the induced demand function for the supplier. Thus, the supplier sets its wholesale prices to solve Equation :

Solving the first‐order conditions of Equation reveals the supplier's chosen wholesale prices as a function of the firms' self‐ and cross‐investment levels:

In effect, the wholesale price chosen by the supplier is tailored to the demand of each retail firm, where the demand reflects the sum of the common underlying demand intercept (α), self‐investment (s

i

), and the rival's cross‐investment (x

j

). Given the induced wholesale prices and ensuing quantities stemming from the firms' self‐ and cross‐investment choices, the firms choose investments to solve Equation , where

Jointly solving the first‐order conditions of Equation reveals the equilibrium investment levels. Based on this, the equilibrium solution is summarized in Lemma (the “^” reflects the traditional distribution equilibrium).

Under traditional distribution, the equilibrium entails: Investments: Prices and quantities:

Part (i) of the lemma follows from jointly solving the first‐order conditions of Equation for firms 1 and 2; part (ii) follows from iteratively substituting these values into the optimal wholesale prices, w

i

(s

1,s

2,x

1,x

2), and retail quantities, q

i

(s

1,s

2,x

1,x

2). Using these prices, quantities, and investment levels in Equations and yields firm i's profit and supplier profit, denoted

A few observations stem immediately from Lemma . First, as might be expected, each firm undertakes positive self‐investment, that is,

Given the equilibrium investment levels and the ensuing effects on wholesale and retail activity under traditional distribution, we next derive the same consequences under integration.

Model

We now consider the variation of the traditional model in which the supplier undertakes partial forward integration in that it serves as one of the two competing retailers (say firm 1).

Equilibrium

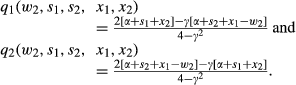

Again working backwards in the game, firm 2's quantity choice is as in Equation from before. Firm 1, the now integrated firm, seeks to maximize its profit as in Equation :

Note that Equation is analogous to (1) with i = 1, except that the integrated firm faces no wholesale price on the units it sells (since it makes them at cost) and also realizes wholesale profits of w

2

q

2 from units procured by firm 2 (since it is firm 2's supplier). Jointly solving the first‐order conditions of Equations and with i = 2, yields retail quantities presented below:

The retail quantities in the partial forward integration case are equivalent to those under traditional distribution, with w 1 replaced by zero. Intuitively, firm 1 now internalizes the actual production cost (normalized to zero). Further, under Cournot competition, the integrated firm takes the quantities of its retail rival (also its wholesale customer) as given when choosing its quantities. With wholesale price already set, the upshot is that the integrated firm ignores the wholesale market when competing in the retail market and, thus, retail outcomes as a function of investment levels are analogous to before (for more on this, see, e.g., Arya et al. 2008, Chen 2001).

Given the induced wholesale demand, q

2(w

2,s

1,s

2,x

1,x

2), firm 1 sets the wholesale price to solve:

The first‐order condition of Equation reveals the wholesale price set by the integrated firm:

The chosen wholesale price is equal to that under traditional distribution (the first term) adjusted due to the integrated firm's distinct advantage in retail competition as it acquires input at cost (the second term). Intuitively, since w 2(s 1,s 2,x 1,x 2) > 0, firm 1 enjoys wholesale profit for each unit firm 2 sells on the retail market. As such, firm 1 seeks an avenue through which it can ease its substantial retail advantage so as to balance wholesale and retail profits. The wholesale price adjustment serves this purpose. Consistent with this intuition, in the absence of retail competition (i.e., γ = 0), firm 1 need not worry about the effect of its retail power on wholesale profits, and thus, there is no pricing adjustment. Moreover, in the absence of investments, the adjustment is sure to be a discount, indicating that the integrated firm charges a lower wholesale price, so as to encourage the retail success of its rival. Finally, the extent of this adjustment depends on the relative profitability of its customer in the wholesale market (reflected in α + s 2 + x 1) and its customers in the retail market (reflected in α + s 1 + x 2), each of which the integrated firm can influence by its upfront choice of cross‐ and self‐investments, respectively.

Moving to the investment stage, consider next the choices made by the firms in the partial forward integration regime. Denoting q

i

(w

2(s

1,s

2,x

1,x

2),s

1,s

2,x

1,x

2) by q

i

(s

1,s

2,x

1,x

2), firms 1 and 2 choose investment levels to solve Equations and , respectively:

Notice that Equations and account for self‐and cross‐investment costs, retail competition between the two firms, and wholesale trade between the parties. The first‐order conditions of Equations and yield the investment levels presented in Lemma (i). Substituting these investment levels in w 2(s 1, s 2, x 1, x 2) and q i (s 1, s 2, x 1, x 2) reveals the equilibrium wholesale price and retail quantities presented in Lemma (ii).

Under partial forward integration, the equilibrium entails: Investments: Prices and quantities:

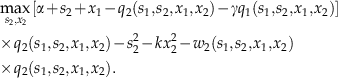

Using prices, quantities, and investment levels from Lemma in Equation and in Equation , for i = 2, yields firm 1 and firm 2 profits under partial forward integration, denoted

Investment Effects of Partial Forward Integration

Perhaps the most glaring consequence of partial forward integration is its effect on cross‐investments. From Lemma , both retail competitors undertake negative cross‐investments (e.g., negative advertising) under traditional distribution. However, from Lemma , asymmetric investment choices arise under integration. For firm 2, integration gives it an inferior status, giving it even more reason to be defensive. This translates into a negative cross‐investment for firm 2. However, firm 1, being both a supplier and competitor, seeks a means to assuage firm 2's fears to boost its own wholesale demand. Positive cross‐investment turns out to be an effective means of achieving this objective. This consequence of partial forward integration for cross‐investments is confirmed in the next proposition. (The proofs are detailed in the accompanying Online Appendix S1.)

Under traditional distribution, each firm undertakes negative cross‐investment, Under partial forward integration, firm 1 undertakes positive cross‐investment while firm 2 undertakes negative cross‐investment,

An upshot of Proposition is that integration can soften destructive cross‐investments, at least by one of the competing parties. As it turns out, this softened posture by one party does translate into greater net cross‐investments (Proposition (i)). In other words, partial forward integration has the societal upside of shifting the focus of aggregate cross‐investments to a more constructive posture. In addition, integration also boosts self‐investments (Proposition (ii)). That is, knowing that (in aggregate) firms will be less aggressive in undercutting each other's demands, firms also shift their stance vis‐a‐vis their own demand influencing activities. The bottom line is that not only are firms less destructive when it comes to their tack toward competitors, but they are also more constructive when it comes to how they approach their own customers.

Partial forward integration increases aggregate cross‐investment, Partial forward integration increases aggregate self‐investment,

Propositions and confirm that integration stands to vastly alter the firms' strategic investments. The question we address next is if and how such investment effects translate into welfare effects. After all, there are other (perhaps more direct) offsetting strategic consequences of integration to consider given the arrangement entails competition between firms with asymmetric costs, with one firm (firm 1) having a clear competitive advantage.

The effects of integration on overall welfare follow from an analysis of crisp forces. On the positive side, integration implies (i) at least one retail firm is acquiring inputs at cost and (ii) aggregate self‐investments and aggregate cross‐investments are each boosted. On the negative side, firm 2's wholesale price may be increased by its retail rival since the rival also controls supply terms. For example, in the limiting case of γ → 0, firm 1 is not concerned with retail encroachment and, thus, sets a higher wholesale price than an independent supplier to take advantage of the improved investment environment:

In short, integration can be potentially harmful for welfare, as it gives substantial power to manufacturers who have monopoly power in input provision and access to their own distribution channel, which permits exclusion. Nonetheless, when one accounts for the upsides of firm 1's efficient input provision and boosted aggregate self‐ and cross‐investments, formal analysis yields an unequivocal answer as noted in part (i) of the proposition: Welfare is surely improved, because there is increase in industry profits as well as consumer surplus. Part (ii) builds on this result to formally demonstrate that not only is welfare boosted but that Pareto gains too can arise. That is, due to the merged firm's cooperative cross‐investment posture, even the unintegrated firm can be made better off.

Under partial forward integration, Industry profit and consumer surplus are each increased and For γ < γ*(k), Pareto gains arise in that the unintegrated firm, the merged entity, and consumers are each made better off.

To hone in on the critical role of investments, and cross‐investments in particular, consider the impact of integration on firm 2, the party seemingly at most disadvantage. Suppose investments were not part of the equation, that is, s

i

= x

i

= 0. In this case, while the wholesale price for firm 2 is lowered by integration, it is nonetheless at a distinct disadvantage relative to firm 1. This is readily confirmed by substituting the wholesale prices and quantities into Equation for both the traditional and forward integration cases with investments set to zero each time. This exercise reveals that with no investments integration reduces firm 2's profit by

However, recall that partial integration leads firm 1 to be supportive of firm 2 by engaging in positive cross‐investment. As it turns out, this effect can be pronounced enough that even firm 2 prefers partial forward integration. That is, while the typical view is that a firm at the mercy of its retail rival for critical inputs will dislike such an arrangement, that thinking misses out on the changed investment incentives of the integrated firm. In particular, in its attempt to balance both wholesale and retail profits, the integrated entity engages in more constructive investments. Moreover, as the next result notes, circumstances under which the independent firm gains are driven entirely by cross‐investments, and the more pronounced these initiatives are, the more likely such win–win scenarios are to arise.

The spillover benefits of partial forward integration to the unintegrated firm are greater the more prominent cross‐investments are: γ*(k) is decreasing in k; and In the absence of cross‐investments, partial forward integration always reduces the profit of the unintegrated party:

Taken together, the results suggest that in the long run, as firms adjust investment choices, partial forward integration by suppliers may well be a societal boon. Moreover, the rapid popularity of integration is in line with the view that it possesses the potential to benefit not just the supplier who enters the retail realm but also traditional retailers who gain from the more positive stance of their competition. In other words, while the cost of foreclosure in the input market and encroachment in the output market due to partial integration is noted, this article stresses there are also positive repercussions for investments.

At this juncture, it seems appropriate to comment on the chosen timing of events wherein investments are undertaken upfront and wholesale terms are set subsequently. The rationale underlying this sequence is twofold. First, it conveys that investments tend to require advance long‐term planning. Second, relative to investments, wholesale prices are less sticky in that these prices may be reset by the input supplier after it observes the buyers' investments. Nonetheless, it is reasonable to ask to what degree such timing plays a critical role in deriving the primary results. Utilizing the same backward induction process as employed in sections and , it is tedious albeit straightforward to demonstrate that our main results on investment and Pareto gains continue to apply if investments were instead undertaken after wholesale prices are set. Continuing this theme of robustness, we next demonstrate that the key conclusions also apply (i) when the parties negotiate over the wholesale price, (ii) if wholesale price terms are subject to confidentiality agreements, (iii) when firms compete over prices in the retail realm, and (iv) under variation in the modeling of cross‐investments.

In the partial forward integration analysis thus far, we presumed that the wholesale price is dictated by firm 1. A natural follow‐up is to examine how firm investments would vary if instead the two firms negotiated over the wholesale price. In doing so, we utilize the standard Nash bargaining solution, generalized to allow asymmetric bargaining power (e.g., Myerson 1991). The parameters β and 1 − β, 0 ≤ β < 1, represent the bargaining powers of firm 2 and firm 1, respectively. Notice that this formulation encompasses the base model as a special case corresponding to the choice of β = 0.

Using q

i

(w

2,s

1,s

2,x

1,x

2) from section , firm i's profit is denoted π

i(w

2,s

1,s

2,x

1,x

2). Also, note that if the firms do not reach agreement, the status quo outcome entails firm 2 being foreclosed and firm 1 supplying products as a monopolist in the retail market it serves—the status quo payoffs for firm 2 and firm 1 are 0 and [1/4][α + s

1 + x

2]2, respectively. As a consequence, the negotiated wholesale price is the solution to the following (generalized) Nash bargaining problem:

Relegating details to the Online Appendix S1, the next proposition presents comparative statics of the key outcomes—wholesale price (

Under partial forward integration with (generalized) Nash bargaining, The wholesale price is decreasing in β, firm 1's quantity is decreasing in β, and firm 2's quantity is increasing in β; Firm 2 engages in positive self‐investment and negative cross‐investment for all β. Further, firm 2's self‐ (cross‐) investment is increasing (decreasing) in β; and Firm 1 engages in positive self‐investment and positive cross‐investment for all β. Further, firm 1's self‐ (cross‐) investment is convex (concave) with a minimum (maximum) at an intermediate β‐value.

The result in part (i) is as expected: A stronger bargaining position for firm 2 puts downward pressure on the wholesale price leading to increased procurement by firm 2 and, consequently, reduced retail sales by firm 1. Part (ii) notes that the stronger position for firm 2 also spurs it to engage in more positive self‐investment as well as provides it with increased incentives to sabotage its rival. As in the previous section, despite facing sabotage from firm 2, firm 1 responds in a cooperative fashion by undertaking positive self‐ and cross‐investments, as shown in (iii). The lack of monotonicity in investment levels for firm 1 can be traced to the impact of β on its sales. In particular, for β slightly greater than 0, the reduction in the double marginalization problem and the boost in sales in the wholesale market lead firm 1 to favor its wholesale client (i.e., firm 2) by increasing (decreasing) its cross‐ (self‐) investment. However, for sufficiently large β, the reduction in firm 1's sales in the retail market is the dominant factor, leading firm 1 to reduce aid to its strongly placed retail rival and to instead focus more on increasing its self‐investment. As a consequence, firm 1's self‐ and cross‐investments are convex and concave in β, respectively. However, despite this nonmonotonicity, the critical force that the firms adopt an asymmetric cross‐investment posture (firm 1 aids but firm 2 sabotages) is maintained for all β‐values.

The analysis thus far presumed that each firm was aware of the wholesale price terms set for its retail adversary. However, what if confidentiality clauses prevented the disclosure of vertical contracts? In such cases, retail competitors act based on their best guess of their rival's terms rather than actual terms. Clearly, such confidentiality clauses have no bite in the integration regime. After all, in this case, the integrated party is of course aware of its rival's terms, as it is the party establishing those terms. This is in stark contrast to the traditional regime, where wholesale terms are set by an independent supplier. In fact, the impact of unobservability of contract terms in such environments has been the subject of much analysis (e.g., McAfee and Schwartz 1994, O'Brien and Shaffer 1992, Rey and Verge 2004).

Intuitively, when contract terms are observed, the (common) supplier utilizes high wholesale prices to force retailers to increase their retail prices, thereby softening downstream competition. When the retailers are unable to observe each other's wholesale pricing terms, the supplier's ability to so tightly control downstream competition is undercut. As a consequence, it sets lower wholesale prices. The reduced cost of procuring products, in turn, boosts the retailers' incentives to invest. With confidentiality of terms providing increased investment incentives under traditional distribution, the question then is whether integration still provides additional gains. To answer this question, we first derive the confidentiality equilibrium under traditional distribution.

Formally, under traditional distribution and confidentiality of wholesale terms, denote firm i's conjecture of firm j's quantity by q'

j

. Anticipating that the rival will put this quantity on the market, firm i solves:

The first‐order condition of Equation yields the reaction function q

i

(w

i

, q'

j

) = [α + s

i

+ x

j

− w

i

− γq'

j

]/2. With wholesale prices unobservable, q

1(w

1, q'2) + q

2(w

2, q'1) serves as the induced demand function for the supplier. Notice the induced demand function reflects the standard deployment of passive beliefs in that the supplier's price quote to any retailer does not alter the recipient's conjectures about offers to its rival. The supplier thus chooses wholesale prices to solve:

Jointly solving the first‐order conditions of the above, the reaction functions q

i

(w

i

,q'

j

) = [α + s

i

+ x

j

− w

i

− γq'

j

]/2, and the equilibrium conditions q'

i

= q

i

reveals the wholesale prices and quantities as a function of the investment levels:

Using the above expressions, each firm chooses investments to solve:

Solving the first‐order conditions of the above yield the equilibrium investment levels under traditional distribution with confidentiality, denoted by Investments: Prices and quantities:

As noted earlier, the supplier's inability to coordinate retailers via observable wholesale prices results in a decrease in the price:

With confidentiality clauses, Aggregate self‐investment and aggregate cross‐investment are each increased by partial forward integration; Industry profit and consumer surplus are each increased by partial forward integration; and For γ < γ

φ

(k), Pareto gains arise due to partial forward integration in that the unintegrated firm, the merged entity, and consumers are each made better off.

The article's primary analysis considers the standard Cournot game in which quantities serve as strategic variables for the competing firms. There are numerous examples (e.g., disclosure choice, transfer pricing, incentive schemes) under which a change to a Bertrand game, wherein firms compete on retail prices, radically alters conclusions. The underlying rationale for the reversals invariably has to do with the fact that quantities are strategic substitutes in the Cournot setting, while the upward sloping reaction functions in the Bertrand setting imply prices are strategic complements.

In our setting, a shift from Cournot to Bertrand does, in fact, impact the equilibrium outcomes in both the traditional and integration regimes in significant ways. However, it does not change the article's key message in that the partial forward integration by suppliers continues to increase investments and, as a result, can be preferred by all parties. Formally, in conducting the analysis under price competition, we invert p

i

= a − q

i

− γq

j

and employ the ensuing consumer demand function

Under traditional distribution, we have the following: Investments: Prices and quantities: where Under partial forward integration, Investments: Prices and quantities:

The wholesale prices succinctly capture the close link between the nature of distribution and the nature of competition. In the traditional distribution case, as is well recognized, price competition is more fierce than quantity competition. Confronted with less profitable buyers in the Bertrand game, the supplier charges lower wholesale prices,

Despite the above changes, the critical theme that an integrated firm attempts to balance both wholesale and retail profits by its upfront investment actions continues unabated. Thus, irrespective of the nature of competition, forward integration creates an environment wherein firm 1 engages in positive cross‐investments to assist its wholesale customer (firm 2). As a consequence, partial forward integration continues to provide desirable upsides in the Bertrand setting as noted below.

When retail firms engage in price competition, Aggregate self‐investment and aggregate cross‐investment are each increased by partial forward integration; Industry profit and consumer surplus are each increased by partial forward integration; and For γ < γ

B

(k), Pareto gains arise due to partial forward integration in that the unintegrated firm, the merged entity, and consumers are each made better off.

The Relative Cost of Investments

In the primary analysis, we assumed cross‐investments were more costly to undertake than self‐investments, and modeled this possibility by restricting k ≥ 1. Though this is often descriptive in practice, the converse can also occur. That is, sometimes it is easier for a firm to influence the market's perception of its rival than credibly promote the merits of one's own product. To succinctly incorporate cases where cross‐investments are paramount, we consider a simple variant wherein self‐investments are prohibitively costly for firms to undertake and, thus, the focus is exclusively on cross‐investments. In this one‐sided investment setup, positive prices and quantities are assured for all 0 < γ < 1 if and only if k ≥ 9/25, and so we assume only this less restrictive k‐condition.

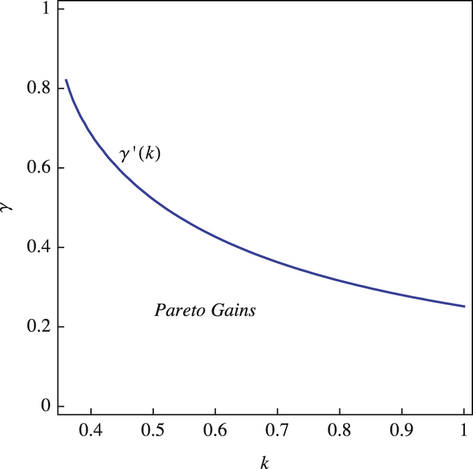

The following proposition shows our result on investment gains under integration continues to hold for all permissible k‐values. Further, while closed form expressions for the γ(k)‐cutoff below which Pareto gains arise is still unattainable, the ensuing figure (Figure ) gives an appreciation for the range of parameter values under which such gains arise.

(k,γ)‐Values under Which Pareto Gains Arise

When self‐investments are prohibitively costly, Each firms engages in negative cross‐investment under traditional distribution, while firm 1 (firm 2) engages in positive (negative) cross‐investment under partial forward integration. Moreover, aggregate cross‐investment is boosted by partial forward integration; and For γ < γ′(k), partial forward integration leads to Pareto gains in that the unintegrated firm, the merged entity, and consumers are each made better off.

Not only can cross‐investments sometimes be more critical than self‐investments, they also are often inherently intertwined. As one example, costly experimentation by a firm to determine ways to lower its own operational costs and/or improve product line visibility may provide rivals with an opportunity to free ride on such efforts. Formally, it is easy to adjust our model to account for spillovers by making two changes. First, we set x i = θs i —firm i's cross‐investment is contingent on its self‐investment with the degree of spillover measured by the parameter θ, 0 < θ ≤ 1. Second, set k = 0, so there is no explicit cross‐investment choice—self‐investments alone spill over to influence rivals. In effect, firm i's net demand intercept is now α + s i + θs j , indicating demand increases from either its own positive self‐investment or due to spillover from positive self‐investment by the rival.

The following proposition notes that the article's basic theme—that partial forward integration is associated with increased investments and opens the door to Pareto gains—is maintained in the spillover framework.

In the presence of spillovers, Aggregate self‐investment is higher under partial forward integration; and For γ < γ″(k), Pareto gains arise due to partial forward integration in that the unintegrated firm, the merged entity, and consumers are each made better off.

The blurring boundaries between distribution channel partners and retail competitors has had notable reverberations in the competitive landscape. In this article, we demonstrate that such reverberations are also manifest in the realm of strategic investments. We demonstrate that the new face of distribution channels characterized by partial forward integration leads to greater investments in boosting product demand, spurring consumer attraction both to overall product offerings and particular brands. This is in contrast to a more cutthroat desire to poach customers from rivals, even at the expense of harming demand for broad product classes, evidenced in traditional distribution networks. The net result of the more cooperative and productive strategic posture in new distribution channels is that even retail firms who are beholden to rivals for inputs can benefit from the blurred boundaries. We also demonstrate that the basic conclusions regarding the importance and net effects of strategic investments in determining the consequences of changing distribution networks are robust to several modeling variations.

The analysis here emphasized the most basic strategic choices of pricing (both at the wholesale and retail levels) and demand‐enhancing investments to succinctly make its point. That said, further research could expand upon the analysis to consider how new distribution networks affect longer term investment considerations such as product line design. After all, as stressed in Villas‐Boas (1998), a problem plaguing traditional distribution channels is that retailers are prone to target only particular customers and/or product lines at the expense of others. As a result, manufacturers take great pains to indirectly influence retailer behavior by judiciously designing product lines. A clear line of inquiry that emanates from this issue is if and how the manufacturer's concurrent presence in the retail market would alter investments that determine the design and make‐up of the product lines that ultimately reach consumers.

Footnotes

Acknowledgments

We thank Francesco Bova, John Christensen, Peter Christensen, John Fellingham, Hans Frimor, Jon Glover, Thomas Hemmer, Anil Makhija, Madhav Rajan, Doug Schroeder, Jiwoong Shin, Stefan Reichelstein, Dae‐Hee Yoon, the editor, the senior editor, and two referees for many helpful comments. Anil Arya and Brian Mittendorf are Fellows of the National Center for the Middle Market at the Fisher College of Business, OSU, and acknowledge the Center's support for this research. Anil Arya also gratefully acknowledges assistance from the John J. Gerlach Chair.

1

The prevalence of hybrid distribution among middle market firms is typified by Jeni's Splendid Ice Creams, a Columbus, Ohio, based firm that achieved its national reach (and middle market status) through both distribution agreements with independent distributors (e.g., Dean & Deluca, Dorothy Lane Market, etc.) and establishing global online offerings.

2

A necessary and sufficient condition for the first‐order approach to be valid and for the approach to yield positive prices and quantities is γ < 3/4, a condition assumed throughout.

3

The approach is commonly employed because it permits an axiomatic representation of the outcomes without necessitating an explicit description of the specific bargaining process.