Abstract

We analyze the dynamic price discrimination strategies of a monopolist who offers new services on a subscription basis. Access to customers' subscription histories permits the monopolist to design pricing policies that can be based on customers' past purchase behavior, and on the time period in which they made their purchases. Uncertainty regarding the value of new features, and heterogeneity in consumers' valuation for existing features, creates inter‐temporal incentives that influence both profits and the rate of adoption of new technology. We find that the comparison of pricing regimes critically depends on whether the monopolist finds it optimal to encourage all consumers to adopt the new technology early. The pricing regimes differ only when the prior heterogeneity in consumer valuation for the existing features is relatively large, in which case the monopolist finds it optimal to serve only the part of the population of consumers that has a relatively high valuation. The monopolist can improve his profits by committing to ignore consumer past behavior, and to vary prices based only on the time period. If a stronger commitment to never utilize any price discrimination is feasible, the profits of the monopolist are even higher. However, the “First Best” outcome cannot be achieved, because it requires the monopolist to discriminate in favor of returning customers, by offering them lower prices than it offers to new customers. We also investigate the effect of positive correlation between the consumer valuations for the existing and the new features of the technology. We find that, as the correlation increases, the gap in profits among the various regimes narrows, while the ranking of the regimes remains the same. In particular, with perfect correlation, time inconsistency issues that arise due to lack of commitment disappear completely for all regimes, and the “First Best” outcome is attainable.

Keywords

Introduction

The introduction of subscription services into the software industry is disrupting the traditional business model of selling software for a one‐time fixed payment. Microsoft and Adobe, for instance, offer their new versions of Office and Creative Suite software, respectively, on a subscription basis. A subscription model differs from the traditional model in two important ways. First, in a subscription environment, consumers are required to renew their subscription after every period, in order to continue using the software. Second, subscriptions allow a service provider to more successfully collect and maintain customer data. Such information can be used, for instance, to identify whether a customer is a first‐time customer or a returning customer. The service provider can use this information to design pricing strategies that are based on the time of purchase (he can vary the subscription price over time) and the customer's purchase history (he can offer different prices to new and to returning customers), thus giving rise to three possible price discrimination regimes: (i) Behavioral price discrimination, (B), under which the seller may offer different prices to new and to returning customers; (ii) Inter‐temporal price discrimination, (I), under which the seller may vary the price, charged to all customers, in different time periods; and (iii) Behavioral and Inter‐temporal price discrimination combined, (BI), where the seller may vary prices based upon both behavior and time.

There exists a wide variation in the way technology companies price their subscription prices for new software. Adobe, for instance, offers introductory discounts to academic users and to existing users of CS6 software on a subscription for Creative Cloud. Similarly, Intuit offers introductory discounts to new customers on subscriptions for QuickBooks Online and for QuickBooks Accountant. The introductory discounts are valid only for one subscription period. 1 Returning customers who want to renew their subscriptions are required to pay the then market price for the software, which tends to be higher than the introductory price. In contrast, some firms stay away from introductory offers that favor new customers over returning customers. For example, Microsoft does not offer any special discounts to new customers for a subscription to Office 365. However, both Adobe and Microsoft mention, in the offer terms, that the current price of the subscription is valid only for a limited period of time, and is subject to change, indicating that the firms wish to preserve their flexibility to vary prices in the future. Although the existing literature presents some insights on the relative profitability of such pricing strategies (see, for instance, Fudenberg and Villas‐Boas 2006, Jing 2011) there still exists an incomplete understanding of the inter‐temporal incentives of firms and of consumers in an environment where consumers gain information about a new technology from their experience with using it. In particular, the literature has not considered how the growth prospects of the market, and the extent of uncertainty facing the consumer, affect the comparison of the various pricing regimes. In this paper, our objective is to close that gap in the literature, by focusing on the pricing of a new service in a subscription environment, with forward looking consumers who are uncertain of their valuations for the new service.

New software, such as Adobe Creative Cloud, may be considered a bundle of new and of existing features. While consumers may be familiar with the existing features of the software, they face significant uncertainty with respect to the value of new features. Consumers who buy the service gain experience with the new features, and use the information gathered from that experience in making future purchasing decisions. Contingent upon the pricing strategy of the firm, consumers can strategically decide the timing of their first subscription to the new service. In particular, they can choose between subscribing to the service immediately and postponing their subscription to a later date, if they expect prices to decline over time. Postponing the subscription prevents them, however, from experimenting with the new features and assessing their added value. Whether such additional information influences their future behavior depends upon their valuation for the existing features. Consumers with very high valuations for the existing features may renew their subscription even if their valuations for the new features are relatively low. For instance, professional web designers, who tend to have relatively high valuations for Adobe's creative applications, may renew their subscription to Creative Cloud even if they find that the quality of the new applications is not impressive.

We explore how the different pricing regimes affect the profitability of a monopolistic firm, the extent of market coverage, and the pattern of prices over time, when the monopolist does not have the power to commit to future prices. Given that, in subscription markets, the firm can observe the past behavior of its customers, and can also change prices as time elapses, in order to implement a pricing regime that ignores past behavior, time, or both behavior and time, it is necessary for the firm to utilize a commitment device that prohibits it from using some or all of the observable variables at its disposal. In the absence of such commitment devices, the monopolist may utilize both behavior and time in designing its pricing policy. We also derive the equilibrium when the monopolist has full commitment power to credibly announce future prices to both new and returning customers. We use the full commitment case as a benchmark, to illustrate the characteristics of the “First Best” outcome that ensures the highest profits for the monopolist. In the “First Best” outcome, the monopolist rewards the loyalty of returning customers by charging them lower prices, and also commits to never reducing prices to new customers in future periods. We compare the various pricing regimes without commitment against the “First Best” benchmark, and demonstrate that the comparison depends critically upon the extent of coverage of the market and on the overall uncertainty facing consumers regarding their valuations for the new features.

We begin by analyzing the pricing regimes when the market is less than fully covered, that is, when there exists a segment of consumers who have not yet experienced the new service. Less than full coverage occurs in our model if the heterogeneity in consumer valuations for the existing features of the service is sufficiently large. We demonstrate that, in such growing markets, if the monopolist has the flexibility to choose among the three price discrimination regimes, his profits are highest if only time, and not past behavior, is utilized in pricing. A regime of inter‐temporal price discrimination is characterized by a declining schedule of prices over time, as the monopolist seeks to expand his market by making his service more affordable to low‐valuation consumers. In contrast to that declining schedule of prices, when only behavior is used as a basis for discrimination, the monopolist charges returning customers higher prices than new customers. Given their ability to choose whether to subscribe to the new service a second time, returning customers implicitly reveal that their valuation for the service is relatively high, thus providing an incentive for the monopolist to charge them a higher price. 2 Even though the regime of behavioral price discrimination is less profitable for the monopolist than is inter‐temporal price discrimination, behavioral price discrimination encourages a larger number of consumers to adopt the new technology early, because of the low introductory prices that the monopolist charges in such a case. We also find that utilizing both behavior and time as bases for discrimination has the most adverse effect on the profits of the monopolist. Anticipation of an increase in prices to experienced customers makes learning less attractive for consumers, and anticipation of a decrease in prices to new customers in the future encourages more consumers to postpone their purchases to a later period. The result that inter‐temporal price discrimination dominates all other price discrimination policies contradicts the result obtained in Jing (2011). In that paper, inter‐temporal price discrimination is shown to be sometimes dominated by behavioral price discrimination when the market is fully covered, that is, when the entire customer base adopts the new service early and the potential for further growth disappears. We further demonstrate that, if the monopolist has stronger commitment powers that permit him to commit to a constant price irrespective of the period of purchase and the purchase history of the consumer, his profits are even higher than with any price discrimination regime, including that of inter‐temporal price discrimination. We continue by analyzing the pricing regimes when the market is fully covered. Full coverage occurs, in our model, when the extent of heterogeneity in the consumer valuation for the existing features of the service is relatively small. Because all consumers adopt the new technology early, the monopolist does not have an incentive to reduce prices to new customers in later periods in order to expand his market. Moreover, customers in later periods are all returning customers, and the distinction between new and returning customers disappears. As a result, all pricing regimes yield identical profits and pricing patterns over time. Prices rise over time under either behavioral or inter‐temporal price discrimination, as repeat purchases by consumers signal to the monopolist that returning customers have high valuations for the product. Such a pricing trend is the opposite of the trend under the “First Best” outcome, where loyalty is rewarded in the form of lower prices. As a result, in the absence of commitment power, the monopolist still cannot achieve the “First Best” outcome even when the market is fully covered. The environment and results we obtain with full market coverage resemble those of Jing (2011).

Finally, we analyze the effect of correlation between the valuations for the new and the existing features on the comparison of the different pricing regimes. In the presence of correlation, the consumer's familiarity with her valuation for the existing features helps her resolve some of the uncertainty regarding her valuation for the new features, and the importance of consumer learning declines. We find that, as the degree of correlation increases, the difference in profitability between the best and worst performing pricing regimes diminishes, although the ranking of the various pricing schemes remains the same as it is in the case of no correlation. The difference disappears completely in the extreme case, in which the existing and the new valuations are perfectly correlated, and therefore, the consumer faces no uncertainty. Under perfect correlation, we find that all pricing regimes are equivalent and yield the “First Best” outcome, even when the monopolist does not have commitment power to set future prices. That result is similar to the one derived in the Durable Good Monopoly literature (Coase 1972 and Bulow 1982), where it has been demonstrated that by leasing instead of selling the product, the monopolist can overcome all time inconsistency issues that arise due to his lack of commitment powers. The Durable Good Monopoly literature focuses on an environment in which consumers face no uncertainty regarding their preferences, as is the case in our model when valuations are perfectly correlated.

Literature Review

Our work is primarily related to two streams of literature: dynamic pricing of experience goods and behavior‐based price discrimination. Nelson (1970) was the first to introduce the concept of an experience good. When buying such a good, consumers are initially uncertain of their valuations for the product, but gain information about their valuations after purchasing and using the product. Shapiro (1983) is an early study that derives the impact of such consumer learning on the path of pricing chosen by the firm. Subsequent studies focused on deriving the optimal pricing path when consumers are strategic and when heterogeneity exists in the population of consumers, in terms of their experience with the good (Cremer 1984) and with the rate of learning (Bergemann and Välimäki 2006). While those studies focus on a monopoly setting; Villas‐Boas (2004, 2006) considers learning in a competitive environment. He demonstrates that the pricing path and the profitability of each firm depend on the extent of negative or positive skewness of the distribution function of consumer valuations.

In subscription markets, buyers are not anonymous, so that service providers can distinguish between new and repeat customers. As a result, providers may price discriminate between new and existing customers. Behavior‐based price discrimination has been addressed in the literature in both monopolistic and competitive settings. Fudenberg and Villas‐Boas (2006) provide a comprehensive review of the literature in the area. Studies that investigate the role of behavior‐based price discrimination in competitive markets focus primarily on the ability of a firm to poach the existing customers of its competitors, by offering them better deals. In some studies, the driving force in enticing customers to switch relates to the existence of switching costs (see for instance, Chen 1997, Shaffer and Zhang 2000, Taylor 2003). In other studies, enticing customers relates to horizontal product differentiation among competitors (see, for instance, Chen and Pearcy 2010, Fudenberg and Tirole 2000, Pazgal and Soberman 2008, Shin and Sudhir 2010, Villas‐Boas 1999).

At the intersection of the above two streams, Caminal (2012), Cremer (1984), and Jing (2011) analyze behavior‐based price discrimination in a monopoly setting, when consumers are uncertain of their valuations for the new product, and where experience with the product reduces the degree of uncertainty. Caminal (2012) and Cremer (1984) analyze the optimality of coupons and loyalty programs that reward returning customers over new customers. They assume that the monopolist has the power to commit to future prices. In contrast, similar to the setting we consider, Jing (2011) evaluates time‐contingent pricing and behavior‐based price discrimination when the monopolist does not have the power to commit to future prices.

As in the experience good pricing literature, Jing (2011) assumes that consumers are completely uninformed of their valuations prior to gaining experience with the new product, and are, therefore, identical prior to purchasing the good for the first time. The price chosen by the monopolist leads to either none or all of the consumers buying the service in an early period. Because it is optimal for the monopolist to induce the entire population of consumers to begin experimenting with the product early, in later periods all consumers are returning customers. In a given period, therefore, the monopolist faces either all new or all returning customers, and the distinction between new or returning customers in a given period dis‐appears. In contrast, we assume that consumers are heterogeneous even before they learn their idiosyncratic valuations of the new features of the service. We find that when initial heterogeneity is relatively large, it is optimal for the monopolist to sell only to the segment of the population that has a sufficiently high valuation for the existing features. Because part of the market remains uncovered, in later periods, the monopolist is tempted to cut his price to new customers, in order to expand his market, thus giving rise to price discrimination based on time. Such incentives do not arise in Jing (2011), where his assumptions result in the entire population of consumers being attracted immediately. Our environment becomes identical to that modeled in Jing (2011) when the extent of prior heterogeneity among consumers is relatively small, so that the monopolist finds it optimal to cover the entire market right away. As a result, we obtain the same results as Jing in such a case. Any form of price discrimination (behavioral or inter‐temporal) yields identical profits for the monopolist. However, when the extent of prior heterogeneity is large and the market is less than fully covered, we derive results that contradict those derived in that previous study. Specifically, while inter‐temporal price discrimination unambiguously dominates any other form of price discrimination in our environment, in Jing (2011) this pricing policy may be dominated. Moreover, because in Jing (2011) consumers do not have access to any prior information regarding their valuations, it is impossible to assess, in this previous study, the role of correlation between the valuations for existing and new features on the different pricing policies of the monopolist.

Dynamic product design and pricing is another stream of literature that is related to our work. For instance, Dhebar (1994), Fudenberg and Tirole (1998), Kornish (2001), Krishnan and Ramachandran (2011), and Sankaranarayanan (2007)) study product design and pricing problem in the absence of commitment power. Those papers all assume that there exists a durable good monopolist who can offer technological improvements or upgrades to his product in the future. The monopolist cannot commit, however, to the extent of improvement, or to the future price of the product. The lack of commitment to future prices that we assume in our paper is extended, in this stream of literature, to include also the lack of commitment power regarding the quality of the product in the future. On the other hand, Bala and Carr (2009) investigate the optimality of upgrade pricing in the presence of user upgrade costs when the monopolist has the power to commit to the quality of the upgrade and the upgrade prices.

Model and Preliminaries

A monopolist is offering a new service, which consists of some new and existing features, on a subscription basis. Consumers have heterogeneous valuations for the existing features of the service. We designate the heterogeneity by the parameter θ, which is assumed to be uniformly distributed in the population over the interval [0, θ H ]. While each consumer knows her own valuation for the existing features, the monopolist is only familiar with the distribution of the valuations in the population. 3 We designate the value of new features by the parameter q. The valuation for the new features is unknown to both the monopolist and to the consumers. However, consumers can learn their valuation for the new features after using the new version for one subscription cycle. The realization of the value to the consumer for the new features varies across different consumers. For example, Adobe Creative Cloud includes a new web development tool called Muse. Customer reviews indicate that some users who tried the new tool value the new feature highly, due to its ease of use, but that some users were unhappy about the speed and performance aspects of the tool. 4 We assume that the distribution of valuations for the new features is uniform over the interval [0, q H ]. The reservation price of a consumer of type θ for the new service is θ + q. We assume that q and θ are independently distributed, and that the distributions of those variables in the population are common knowledge. We also assume that the marginal cost of providing the new version is negligible. That is a valid assumption for many software products, for which most of the costs are fixed, and relate to the cost of developing the product. 5 We consider a two‐period model, where, in each period, the monopolist has to make pricing decisions. The two‐period assumption is justified, given that the life cycle of software tends to be rather limited, as it is often replaced by totally new products, and because the hardware on which it is installed becomes obsolete.

We consider an environment in which the monopolist cannot credibly commit to future prices. As a result, under behavioral price discrimination, he cannot credibly commit to the price that returning customers will face in the future. Similarly, under inter‐temporal price discrimination, or under combined inter‐temporal and behavioral price discrimination, he cannot commit to the future prices any type of customer, old or new, will face. In the absence of commitment power, the monopolist chooses future prices when the future arrives. It is noteworthy that the regimes of exclusively behavioral or exclusively inter‐temporal price discrimination (regimes B or I) correspond to environments in which the monopolist does have some commitment power. With behavioral price discrimination, the monopolist can utilize a mechanism to credibly communicate to new customers that he will never charge lower prices to other new customers in the future. An example of such a mechanism is to offer new customers a refund if prices are ever lowered to other new customers in the future. Similarly, despite his ability to identify consumers' past behavior from their subscription histories, with inter‐temporal discrimination, the monopolist possesses a credible way of convincing customers that their level of experience with the new service does not affect the prices they will face in the future. Using contemporaneous Most Favored Customer clauses (Cooper 1986) that promise to reimburse customers if any other customer is offered a lower price in a given period may offer a vehicle to implement this type of partial price discrimination regime. The bi‐dimensional price discrimination regime, BI, does not require any commitment power on the part of the monopolist. Under BI, the monopolist does not preclude himself from incorporating, in his pricing, any available information about either the past subscription history of the customer or the period of time when the service is purchased. Regardless of the regime considered, we assume that the monopolist cannot commit, at present, to prices he will charge in the future. In the absence of such commitment power, we derive the equilibrium by backward induction.

In the first period, the monopolist sells the new version to consumers who have no experience with the new features. In the second period, the monopolist faces two groups of consumers: (i) New consumers, who have no experience with the new service, and (ii) Repeat consumers, who bought the new service in Period 1 and have, therefore, experience using the new features. Depending on the form of the price discrimination regime used by the monopolist, the price of the service in the second period may be different for new and for returning consumers. In the most general case, that is, the BI regime, the monopolist can choose three different prices: P 1N , the price charged to all consumers in the first period, P 2N , the price charged to new consumers in the second period, and P 2R , the price charged to returning consumers in the second period. In the B and I regimes, which are characterized by only one form of price discrimination, the monopolist chooses only two prices. Under the B regime, the price to new customers remains the same in the second period, that is, P 1N = P 2N = P N . Therefore, the monopolist chooses P N in the first period and P R in the second period. In the I regime, because new and returning customers are offered the same price in the second period, that is, P 2N = P 2R = P 2, the choice of the monopolist is reduced to only two prices P 1 and P 2. We describe our modeling approach by focusing on the case of price discrimination based on both time and behavior (BI). We use a similar approach to obtain the equilibrium with the unidimensional price discrimination regimes by imposing the additional constraints, P 2N = P 1N = P N for the B regime and P 2N = P 2R = P 2 for the I regime.

Assuming that the monopolist uses the BI regime we begin by considering the consumers' choice. When deciding on whether to buy the new version in the first period, consumers are forward‐looking, and try to assess their expected utility over both periods. Each consumer knows her valuation parameter θ with certainty. However, because her valuation for the new features is unknown in the first period, each consumer estimates it, using the prior distribution's mean

Note that a consumer who did not buy the new version in the first period may face a new price P 2N if she considers buying it in the second period. However, a consumer will find it optimal to postpone the purchase to the second period only if P 2N < P 1N . From Equations 1 and 2 it follows that if P 2N ≥ P 1N any consumer who chooses to buy the new version will do so in the first stage. As noted earlier, the two integral expressions in Equation 1 reflect the idea that when anticipating the expected utility derived in the second period, strategic consumers know that they will be able to incorporate information obtained as a result of their purchasing decision in the first period. Under the B regime, the monopolist does not vary prices over time, and charges new customers the same price that he charged in the first period (P 2N = P 1N ). Therefore, for a consumer who did not buy the new service in the first period, the net surplus in Period 2 is equal to zero.

Because we consider a growing market that is far from reaching saturation, we assume that, in both periods, there exists a group of consumers who have no experience of using the new version. Hence, the market is less than fully covered in each period, and, in the second period, the population of consumers may be divided into two segments: experienced and inexperienced consumers. To identify those two segments, we have to solve for the consumer of type θ* who is indifferent between buying and not buying in Period 1, that is, a consumer who satisfies the equation

Recall that we consider an environment in which the monopolist cannot credibly commit to the future price he will charge any type of customer. Instead, he optimally chooses the price new and returning customers pay when the future arrives. Consistent with that assumption, we solve the game by backward induction, beginning by characterizing the equilibrium of the second stage. Such an approach guarantees that the strategies chosen in the second stage are credible (such strategies have been referred to in the literature as closed‐loop strategies). Adobe and Intuit, for instance, offer trial agreements to new customers, without committing to future prices once the agreements expire. Our modeling approach is consistent with that reality.

In the second stage, the monopolist can observe the size of the segment of consumers who bought the new version in the first stage, θ

H

− θ*, and potentially may continue to do so in the second stage. At the beginning of the second stage, the monopolist takes the size of the θ

H

− θ* segment as given. His choice of P

2R

cannot change the size of the segment of experienced buyers who consider buying the service again. However, the price that the monopolist charges returning customers determines who in the region [θ*, θ

H

] will continue to buy the service, and under what circumstances. In particular, the second period price determines whether the repeat purchase decision of a returning customer is conditional on her experience with the new features. We use the term conditional buying to characterize circumstances under which a consumer utilizes her past experience with the new service in deciding whether to continue buying the service for a second time. Whether conditional buying occurs depends upon the price

θ* < P

2R

< θ

H

– Conditional buying by consumers in the lower tail. Only consumers having very low valuations for the existing version condition their continued purchase upon their realization of q. Consumers having high valuations continue to buy, irrespective of their realized value of q.

θ

H

< P

2R

< θ* + q

H

– Conditional buying by all consumers. All consumers condition their repeat purchase decision upon their realization for q, irrespective of their valuation for the existing version.

If the monopolist chooses to attract new customers in the second stage,

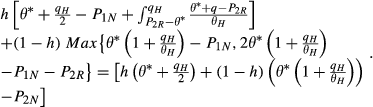

Assuming conditional buying by every customer type, we can write the payoff function of the monopolist in Period 2 as follows:

Note that each customer who purchased the new version in Period 1 buys it in Period 2 when q > P

2R

− θ, and chooses not to purchase in Period 2 when q < P

2R

− θ. Optimizing the objective function 3 with respect to P

2N

and P

2R

, yields the Period 2 equilibrium prices. For a given θ* and conditional buying by every customer type, the Period 2 equilibrium prices for the service and the Period 2 equilibrium profit are given by:

Given the optimal solution for Period 2, in Period 1 the monopolist chooses P

1N

, the price that is charged to all customers, so as to maximize his aggregate profits over the two periods (again, we ignore discounting in the aggregation). He knows, in particular, that the choice of price in Period 1 affects the number of consumers who choose to experiment with the new version, that is, the segment θ

H

− θ*. The consumer of type θ* is indifferent between buying and not buying the new service in Period 1, namely

Note that consumers have rational expectations, and can anticipate the future prices

Substituting the optimal Period 2 prices derived in Equations 4 into 6, we can solve for θ* in terms of P 1N , the Period 1 price charged by the monopolist. The solution for θ* in terms of P 1N determines the size of the segment of consumers who choose to experiment with the new version in Period 1, (θ H − θ*). The solution for θ* captures the traditional trade‐off between price and quantity. When the monopolist raises the Period 1 price P 1N , fewer consumers purchase the service and experiment with the new features, that is, the width of the interval (θ H − θ*) decreases. The functional relationship that ties θ* to P 1N is obtained from the utility optimization of the consumers. The monopolist knows that consumers are strategic, and can anticipate the expected benefit they will derive from buying the service not only in Period 1, but in Period 2 as well. Hence, the added benefit obtained by the consumer over both periods, as expressed in Equation 6, is used by the monopolist in deriving the Period 1 demand for the new version.

When choosing the Period 1 price, the monopolist maximizes his profits over both periods as follows:

When the market is less than fully covered in both Period 1 and Period 2: Under the BI and the I regimes, there does not exist an equilibrium with conditional buying by all returning consumers. Under the B regime, such an equilibrium exists when 1.482 <

According to part (i) of Proposition 1, under both the BI and the I regimes, when the market is less than fully covered, the Period 2 price that the monopolist chooses does not support conditional buying by all returning customers. Under those two regimes, the monopolist has an incentive to lower the price to new customers in Period 2 in order to expand his market. A lower price puts downward pressure on the price the monopolist can charge returning customers. As a result, the price to returning customers in Period 2 can never exceed θ

H

, and conditional buying by all cannot arise. In contrast, in the B regime, for larger values of the ratio

“First Best” Outcome

We now consider an environment in which the monopolist has the power to commit to future prices, in order to be able to derive a benchmark for “First Best” pricing by the monopolist. Lack of commitment power implies that the monopolist does not have the ability to credibly commit to prices he will charge in the future. In particular, he cannot credibly commit to the price returning customers will face in Period 2. In contrast, when the monopolist does have commitment power, he cannot renege on promises regarding Period 2 prices without incurring significant costs. The costs may be related to loss of reputation or damages incurred when breaking a written contract with customers. If such a commitment is feasible, it leads to the highest profits that can be obtained in our environment. We use this “First Best” outcome as a benchmark in evaluating the various price discrimination regimes without commitment. To derive the “First Best” outcome, we allow the monopolist full flexibility in choosing prices; so that prices may vary by period and by the purchase history of the customer. The monopolist chooses the prices in Period 1, and is fully committed to them. Because the monopolist can credibly communicate the future prices P 2N and P 2R , consumers no longer have to infer them from the Period 2 profit maximization of the monopolist. Rather, they are guaranteed that the monopolist will not renege on his promised prices.

Assuming less than full coverage of the market, and conditional buying by all returning customers, the payoff function for the two periods can be expressed as follows:

We characterize the “First Best” outcome and its related prices in Proposition 2.

When the monopolist has full commitment power to set future prices, and the market is less than fully covered, the equilibrium is characterized by conditional buying by only returning customers in the lower tail of the distribution. The monopolist sets the same price to new customers in both periods, implying that no new customers are attracted in Period 2. In the “First Best” outcome, the prices set by the monopolist are: The equilibrium with less than full coverage arises when

When the monopolist can commit to future prices at the beginning of Period 1, he never chooses to attract new customers in Period 2. As a result, price discrimination is based only upon the past behavior of the consumer. The result that the monopolist does not find it optimal to attract new customers in the future is similar to that derived in the Durable Good Monopoly literature (Coase 1972, Stokey 1979). In that literature, the profits of the monopolist are highest if he can credibly commit not to lower prices to new customers in the future. Hence, regardless of whether the monopolist sells a durable good (in the Durable Good Monopoly literature) or an experience‐based non‐durable good (in our case) such a commitment reduces the incentives of new customers to postpone their purchase. Similar to the non‐existence result of conditional buying by all that is reported in part (i) of Proposition 1, when the market is less than fully covered, conditional buying by all returning customers cannot arise under the “First Best” outcome as well. Instead, the price set by the monopolist for Period 2 is sufficiently low so that there is always a segment of returning customers who buy the service in Period 2 for all realizations of q.

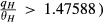

Part (iii) of Proposition 2 states that the monopolist finds it optimal to abandon part of the market only when there is sufficient prior heterogeneity in the consumer valuation for the existing features, which occurs when the ratio

Price Discrimination Regimes without Commitment Power to Future Prices

Given that conditional buying by all customers can never arise under the BI and the I regimes when the market is less than fully covered in both periods, next we explore the possible existence of conditional buying by only customers in the lower tail of the distribution. We begin by considering the BI regime that arises when the monopolist has no capacity to commit to ignoring some observables when setting prices. Subsequently, we consider the regimes when some partial commitment is feasible. In the B regime, the commitment is that the monopolist will ignore the period of purchase when offering a deal to a new customer. Hence, “early adopters” or “late adopters” are treated equally. In the I regime, the commitment is that the monopolist will not treat returning customers differently from new customers.

Behavioral and Inter‐temporal Price Discrimination (BI Regime)

Under the BI regime, the monopolist price discriminates based on the customer's past purchase history and the time of purchase. Assuming that the market is less than fully covered, the Period 2 payoff function of the monopolist when he uses both behavioral and inter‐temporal price discrimination can be expressed as follows:

The revenues of the monopolist in Period 2 accrue from three different segments of consumers: A segment of new consumers,

Using the relationship between the Period 1 and the Period 2 prices that is implied by the utility Equation 6, and the optimal Period 2 profit Equation (8b), the Period 1 optimization problem of the monopolist can be expressed as:

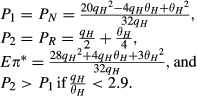

Under behavioral and inter‐temporal price discrimination (BI) with less than full coverage of the market: The optimal prices set by the monopolist are: The BI equilibrium with less than full coverage exists if The expected profits of the monopolist over both periods can be expressed as:

From Proposition 3(iv), the monopolist lowers his price to new customers in Period 2 in order to expand his market. In comparison to the prices they pay in Period 1, experienced customers face higher prices in Period 2. That implies that the pricing strategy of the monopolist does not reward loyalty. The monopolist charges a lower price to new consumers in Period 1 in order to encourage them to experiment with the new service. Once those consumers choose to continue the service a second time, the monopolist charges them a higher price. The monopolist takes advantage of the fact that returning customers tend to have higher valuations for the new service, as can be inferred from their decision to buy the service a second time. Because the monopolist does not cover the entire market in Period 1, he also has an incentive to lower prices further to new consumers in Period 2 in order to encourage consumers with relatively low valuations for the existing features to change their minds, and to experiment with the new features. Note that in the absence of commitment power, the monopolist violates two characteristics of the optimal pricing under the “First Best” outcome. First, instead of rewarding the loyalty of returning customers the monopolist actually penalizes loyalty. Second, instead of keeping prices constant over time to new customers in order to discourage them from postponing their purchase, the monopolist cuts prices to new customers in Period 2.

According to Proposition 3(ii), the equilibrium leads to less than full coverage in both periods only when the value of

Behavioral Price Discrimination (B Regime)

In this section, we derive the equilibrium for behavioral price discrimination where the monopolist price discriminates based only on the past purchase behavior of a consumer, by charging different prices to new and to returning customers. We designate the prices by P

N

and P

R

, for new and repeat customers, respectively. Consumers are forward‐looking, and incorporate the future expected benefit derived in Period 2 in their decision as to whether to buy the new version in Period 1. The overall expected utilities over both periods, when buying and not buying the new service, respectively, are as follows:

Note that a consumer who did not buy the new version in Period 1 remains a new customer in Period 2 as well thus still facing the price P

N

if she considers buying in Period 2. That observation explains the

With conditional buying by only returning customers in the lower tail of the distribution, the Period 2 expected profit of the monopolist can be written as follows:

Optimizing the objective equation (10a) with respect to P

R

yields the Period 2 equilibrium price. For a given θ*, the Period 2 equilibrium price for the service

In order to obtain the relationship between P

N

and θ*, the threshold consumer who is indifferent between buying and not buying the new version, we set

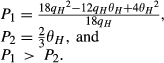

Under behavioral price discrimination (B), with less than full coverage of the market, and conditional buying only by customers in the lower tail of the distribution: The prices set by the monopolist are: The equilibrium, with less than full coverage, and conditional buying only by customers in the lower tail of the distribution, exists if The expected profits of the monopolist can be expressed as:

As in the bi‐dimensional regime BI, in the uni‐dimensional regime B, the price of the new service for returning customers is higher than it is for new customers. As in BI, the monopolist offers a low introductory price to new consumers, in order to encourage them to experiment with the new version. Once those consumers choose to renew their subscription in Period 2, the monopolist charges them a higher price. The monopolist takes advantage of the fact that returning customers tend to have higher valuations for the service, as can be implied by their decision to buy the service a second time. This is in contrast to the “First Best” case, where the monopolist charges returning customers a lower price than he charges new customers. In essence, under behavioral price discrimination, the monopolist rewards loyalty when he can commit to future prices, but punishes loyalty when he does not have such commitment power.

In contrast to the BI regime, however, the monopolist does not attract any new customers in Period 2, because he does not lower the price to new customers in Period 2, given that only past behavior and not time is utilized as a price discrimination device. Note that according to Proposition 1, when 1.6 >

Inter‐temporal Price Discrimination (I Regime)

Under inter‐temporal price discrimination, the monopolist price discriminates based on time only, by charging different prices in Periods 1 and 2. He does not discriminate in his pricing, however, between new and returning customers, despite the fact that he has access to the subscription histories of consumers. Let P

1 represent the price of the new version in Period 1, and P

2 its price in Period 2. Similar to the analysis of the previous cases, we derive the additional expected utility from buying the new version in Period 1 in order to determine the segment of consumers who buy in Period 1:

Unlike the B regime, but similar to the BI regime, with inter‐temporal price discrimination, a consumer who did not buy the new version in Period 1 may face a new price P

2 in Period 2. As a result, consumers may choose to buy the new version in Period 2, even though they did not do so in Period 1. However, only if P

2 < P

1, there may exist consumers who choose to postpone their purchase to Period 2. From Equations 18 and 19, if P

2 ≥ P

1

With conditional buying by only returning customers in the lower tail of the distribution, we can express the Period 2 expected profit of the monopolist as follows:

The monopolist chooses P

2 so as to maximize equation (15a). Differentiating

An expansion of the market will occur at the equilibrium only if the solution for

In Period 1, the monopolist chooses P

1 so as to maximize his profits over both periods. Assuming that an expansion of the market occurs implies the following optimization:

The value of θ* can be expressed in terms of the price P

1 by solving the equation

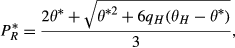

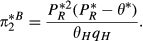

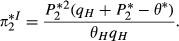

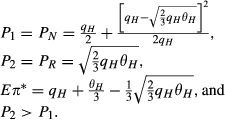

Under inter‐temporal price discrimination (I) with less than full coverage of the market: The prices set by the monopolist can be expressed as: The equilibrium with less than full coverage exists if The expected profit of the monopolist is:

Under inter‐temporal discrimination, as in the BI regime, the monopolist finds it optimal to lower the price to new customers in Period 2, in order to expand his market coverage. Because low valuation consumers choose not to purchase the service in Period 1, the monopolist is tempted to lower the price further in Period 2, in order to encourage some of the low valuation consumers to join the market. However, in contrast to the BI regime, under inter‐temporal discrimination the monopolist does not discriminate based upon past behavior of the consumers, and as a result, both new and returning customers benefit from the same lower price charged in Period 2. The pattern of prices to returning customers is similar, therefore, to that derived under the “First Best” outcome, where the monopolist rewards returning customers by offering them a lower price in Period 2. However, under inter‐temporal price discrimination, the same lower price is offered also to new customers, thus leading to some customers postponing their purchase to Period 2.

Comparison of the Three Price Discrimination Regimes

In Proposition 6, we compare the three price discrimination regimes in terms of profitability and market coverage.

According to Proposition 6, when the monopolist cannot commit to future prices, his profits are highest if he bases discrimination only on time, and lowest under the two‐dimensional price discrimination regime that incorporates both behavior and time in pricing. Behavioral price discrimination that bases discrimination only on the past subscription history of the consumer is ranked as intermediate between the other two regimes. Inter‐temporal price discrimination duplicates the pattern of prices in the “First Best” outcome by rewarding returning customers with a lower price in Period 2. However, in contrast to the “First Best” outcome, the same lower price is offered also to new customers in Period 2. Doing so introduces two counteracting effects on the incentives of consumers to purchase the new service early. On the one hand, low valuation consumers for the basic version can anticipate that the monopolist will lower prices in the future, in order to expand his market coverage, thus providing them an incentive to postpone their purchase, in order to benefit from the lower price. On the other hand, however, high valuation consumers for the basic service do not have to worry about being held hostage by the monopolist when they choose to renew their subscription. They have a stronger incentive, therefore, to experiment with the service in Period 1; thus providing themselves with the opportunity to assess their valuations for the new features early and allowing them also to benefit from an extra period of consumption. According to Proposition 6(i), the latter favorable effect is so significant that the regime of inter‐temporal price discrimination yields the highest profits to the monopolist. According to Proposition 6(ii), it is regime B, however, that encourages the largest number of customers to buy early, as there is no incentive for a new customer to postpone her purchase to Period 2. The BI regime yields the smallest number of customers buying the service early, because of the combined effect of encouraging low valuation consumers (for the basic version) to postpone the purchase in order to benefit from lower prices to be offered to new customers in Period 2, and high valuation consumers (for the basic version) to be less inclined to purchase early, because of their concern about facing higher prices as returning customers in Period 2.

From Proposition 6, it follows that the monopolist benefits most from the regime where only time is incorporated in pricing. Recall, however, that such a regime may not be easy to implement. The monopolist has to find a credible way of convincing consumers that he will never use their purchase histories to charge higher prices to experienced customers. Using anonymizing technologies that make it difficult to identify repeat customers may offer the monopolist a vehicle to implement such a regime. Alternatively, contemporaneous Most Favored Customer clauses, which offer to reimburse customers if any other customer is charged a lower price in a given period, may also facilitate implementing an I regime. In the absence of such commitment devices, the most likely regime to arise is regime BI, where both behavioral and inter‐temporal price discrimination are employed. Because the monopolist sells subscription services, he can observe customers past subscription histories, and can distinguish between new and returning customers. In addition, because he has limited ability to commit to future prices, he will have an incentive to vary the price to new consumers over time, in order to expand his market, and to attract additional relatively low valuation consumers. Hence, the bi‐dimensional price discrimination regime (regime BI) is the most sensible outcome that is likely to arise in the absence of commitment devices.

No Price Discrimination

In addition to the B and I regimes, where the monopolist possesses a mechanism to partially commit to different segments of the consumers, we now consider another possible regime, where the monopolist can commit to never utilize price discrimination; either based on time or based on purchase history. That is, he can commit to selling the service for the same price in both periods, and credibly communicate to consumers that the price he sets for the product early on will remain the same in the future, irrespective of whether they are new or returning customers. Note that such a commitment is actually stronger than the one utilized under the B or I regimes, given that the same price has to be credibly promised to two different types of consumers. However, it falls short of the full‐commitment case assumed under the “First Best” outcome, in which case the monopolist has full flexibility to vary prices across groups, and to credibly communicate to each group future prices in Period 1. In Proposition 7, we characterize the equilibrium that arises when it is feasible for the monopolist to practice a policy of no price discrimination.

When the monopolist is able to maintain a single price for all customers and for all periods, no new customers are attracted in Period 2. When the market is less than fully covered in both periods, there is conditional buying by only customers in the lower tail of the distribution. The price set by the monopolist, and his expected profits are, respectively:

The equilibrium with less than full coverage exists when

In Table 1, we display a numerical comparison of the three price discrimination regimes (BI, B, and I), and the no‐price‐discrimination regime. Optimal prices and profits are the values shown in the table, multiplied, respectively, by θ

H

and

Comparison of Price Discrimination Regimes

As shown in the numerical results reported in Table 1, a commitment to a policy of “no price discrimination” yields higher profits to the monopolist than do any of the three regimes of price discrimination BI, B, or I. “No price discrimination” dominates I, the regime we showed to be the most profitable of the three. The primary reason for that dominance is that a constant price over both periods eliminates any incentive for consumers to postpone a purchase. Note, however, that profits with a constant price are still lower than profits that accrue under the “First Best” outcome, when the monopolist has full commitment power, and chooses to reward the loyalty of returning customers by charging them a lower price.

We considered only two time periods in our analyses and in our calculations. We expect that the relative ranking of the three pricing regimes would remain the same if we considered a model with more than two periods of consumption, as long as the market remained less than fully covered in each of the periods. With less than full market coverage, the monopolist would still have incentives to reduce prices to new customers in later periods, in order to expand his market coverage. However, with more than two periods, that incentive would likely weaken over time, as market coverage increases. In addition, in the absence of commitment power, the monopolist would still have an incentive to increase the price to returning customers, even in a multi‐period model. The incentive to increase the price to returning customers would also likely weaken over time, as the expanded market coverage implies that an increased number of consumers with relatively low valuations for the existing features become part of the group of returning customers.

Pricing with Full Market Coverage

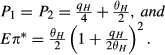

So far, we focused on analyzing pricing regimes when there is less than full coverage of the market in both periods. Less than full coverage implies that, in each period, there exist consumers who have not tried the new service as of yet. Hence, our focus has been on relatively new and growing markets that are far from reaching their saturation stage. In this section, we investigate how the pricing regimes compare when the market is fully covered, that is, when the market has reached a more mature stage, in which all consumers have tried the new service. Using the notation in the paper, this happens when

A consumer of type

When When 1.47588 < When 1.5 < When the market is fully covered and the monopolist has full commitment power to set future prices, the “First Best” outcome is characterized by conditional buying only by returning customers in the lower tail of the distribution,

According to Proposition 8, when the extent of prior heterogeneity in consumer valuations is relatively small (i.e.,

As with less than full market coverage, the “First Best” outcome with full coverage is characterized by rewarding the loyalty of consumers (in Proposition 8(iii)

Effect of Correlation between the Valuations for the Basic and New Features

Until now, we assumed that there is no correlation between the consumer's valuations for the new and the existing features. In the absence of correlation, the only way the consumer can learn about her valuation for the new features is by experimenting with the new service. The consumer's familiarity with her preference for the existing features does not provide her with any useful information regarding her valuation for the new features. However, if θ and q are not independently distributed, the value of θ does provide information about the value of q, and the importance of learning via experimentation declines. In the extreme case of perfect correlation between θ and q, the consumer can predict her valuation for the new features even before using the new service, and there is no additional learning derived by the consumer when using the new service. In order to assess the effect of such absence of learning, we consider the extreme case of perfect correlation, while continuing to assume that the marginal distributions of θ and q are uniform over [0, θ

H] and [0, qH], respectively. We assume that with perfect correlation, a value of θ uniquely determines a value of q, according to the equation

When there is perfect correlation between the consumer's valuations for the existing and the new features, and the market is less than fully covered, all three pricing regimes lead to the same prices and profits as the “First Best” outcome. Specifically,

When there is perfect correlation between θ and q, the monopolist charges the same price to new and to returning customers, and does not vary prices over time. Such a pricing strategy is optimal under the “First Best” outcome, when the monopolist has full commitment power. Hence, in the absence of any learning on the part of consumers, it is completely inconsequential whether the monopolist has the capacity to commit to future prices. The “First Best” outcome can be achieved even without any such capacity. Such a result is similar to one derived in the Durable Good Monopoly literature. In that literature, it has been established that, by reverting to leasing instead of outright selling of the durable good, the monopolist can restore the “First Best” outcome, even in the absence of the power to commit to future prices. The subscription environment we consider in our model is similar to the leasing strategy proposed in the Durable Good Monopoly literature. However, in the Durable Good Monopoly literature, it is assumed that the consumer faces no uncertainty, and is fully informed of her valuation for the product. The existence of full correlation in our setting eliminates the consumer's uncertainty about her valuation for the new features, because she can fully infer her realization of q from the knowledge of her value of θ. It is not surprising, therefore, that, in our setting of subscription services with perfect correlation, as in the leasing result obtained in the Durable Good Monopoly literature, the “First Best” outcome can be achieved even without commitment power. That result indicates that the uncertainty facing the consumer regarding her valuation of the new features, and the process of learning via experimentation, are the driving forces behind the differences among the three price discrimination strategies we consider.

Having considered the extreme cases of independence and perfect correlation between the valuations, we now develop a modeling approach that allows us to consider the intermediate case of partial correlation between the valuations. Doing so allows us to assess the effect of increased correlation on the different pricing regimes we consider. To consider intermediate values of correlation between θ and q, we introduce a parameter 1 ≥ h ≥ 0 that measures the probability that θ and q are independently distributed; (1 ‐ h) is the probability that there is perfect correlation between θ and q, as specified in Proposition 9. Both the monopolist and the consumer are aware of the value of h and incorporate it into their evaluations. For example, a consumer with valuation θ expects the value of new service to her to be

Note that, in case of perfect correlation (with probability 1 − h), a consumer who bought the new service in Period 1 may or may not buy it again. A consumer of type θ whose valuation of q is equal to

Assuming less than full market coverage in both periods, the equilibrium with no correlation leads to learning only by returning customers with valuations in the lower tail of the distribution. Assuming this fact remains true with partial correlation as well, the Period 2 payoff function of the monopolist under the BI regime can be expressed as follows in (18):

The first part of the payoff function represents the profit from new customers in Period 2. The cutoff value

Optimizing the Period 2 profits in Equation 25 with respect to P 2R and P 2N , and utilizing Equation 26 to express the Period 1 price as a function of θ*, leads to an optimization problem in the decision variable θ*. Using the same approach, we can derive also the equilibrium values for the B and I regimes. In Table 2, we perform a numerical analysis to compare the three regimes for varying levels of the parameter h that measures the degree of independence between the distributions of θ and q.

Comparison of Price Discrimination Regimes in the Presence of Correlation

In Table 2, we consider only values of the ratio

In addition to the three price discrimination regimes, we also include in Table 2 the strategy of “no price discrimination” discussed in subsection . The entries in Table 2 show that the ranking of the regimes that exists in Table 1 (no discrimination > I > B > BI) also holds in Table 2 for all values of h > 0; all four strategies are tied when h = 0, as established in Proposition 9. As the extent of correlation decreases (h increases), the difference in profits among the regimes increases. This indicates that, as the extent of correlation decreases, the importance of learning through experience is more significant, leading to greater divergence in profitability among the regimes.

Conclusion

Coase (1972) suggested that a monopolist who sells a durable good can overcome time inconsistency issues related to lack of commitment power by leasing the durable good. Although the current trend of selling software subscriptions corresponds to such a leasing strategy, we demonstrate, in this paper, that it does not necessarily resolve the time inconsistency problem when there is uncertainty regarding the value of the new technology. Uncertainty creates inter‐temporal incentives, for the consumers and for the monopolist, that are absent in the earlier literature. We investigate the effect of such uncertainty on price discrimination strategies when selling a new technology in a subscription environment. When the monopolist lacks the ability to commit to future prices, we find that the choice of the optimal pricing strategy depends upon whether the entire population of consumers chooses to adopt the new technology early. If there is a segment of the population that postpones the purchase of the technology, we find that the best price discrimination strategy is inter‐temporal price discrimination, in which only time, and not past behavior of the customer, serves as a basis for discrimination. Moreover, if the monopolist can credibly commit never to adopt any form of price discrimination, his profits are even higher. Even though it may be difficult to enforce commitment devices that promise not to differentiate between new and returning customers, or not to vary prices in the future, especially in the B2C market, firms can establish a reputation for following such policies by not offering introductory discounts that tend to favor new over returning customers, and by not varying prices over time. When the entire population of consumers chooses to adopt the technology early, we find that inter‐temporal and behavioral price discrimination strategies yield identical profits. Regardless of whether all consumers are “early adopters” though, the monopolist cannot achieve the “First Best” outcome that requires full commitment power to credibly communicate future prices. However, when a consumer's familiarity with the existing features of the technology provides her with a perfect signal of her valuation for the new features of the technology (because there is possibly perfect correlation between the valuations), the consumer no longer faces any uncertainly, and Coase's prediction is restored. That is, the “First Best” outcome is attainable even without any commitment device.

We make several simplifying assumptions to illustrate the effect of learning on the pricing strategies. Relaxing some of the assumptions is unlikely to change our qualitative results. For instance, the assumption that valuations are uniformly distributed in the population keeps the model analytically tractable, while allowing us to measure the extent of heterogeneity in the consumer population in terms of a single parameter; the spread of the distribution. Relaxing the assumption of uniform distributions is unlikely to change our qualitative results. For simplicity, we consider a two‐period model to illustrate the comparison of the pricing strategies. Extending the model to multiple periods is unlikely to provide any additional insights, as we illustrate our results in both growing and saturated markets. In addition, we do not allow the monopolist to alleviate some of the uncertainty facing the consumer regarding the value of the new technology. In practice, most service providers offer free trials for a limited time to encourage consumers to experiment with the new features in a risk‐free environment. However, the trials, being limited in nature, are unlikely to resolve completely the uncertainty facing the consumer.

Footnotes

Acknowledgments

We thank the editor, area editor, and two anonymous reviewers for their insightful feedback and comments that significantly improved the paper. We also benefitted from valuable suggestions made by Mustafa Akan, Tansev Geylani, and Jennifer Shang.

For personal software such as Creative Cloud and Office 365, the subscription period may be one month or one year. Service providers may sometimes offer longer contract periods for business users by entering into price agreements. Such price agreements are, however, more difficult to enforce in consumer markets as the service is less personalized and consumer needs change more rapidly.

On September 9 and 18, 2013 customer reviews of the Adobe Creative Cloud subscription on the Adobe website highlight concerns of customers regarding future subscription prices when signing up for introductory offers.

In the case of Adobe Creative Cloud and Microsoft Office 365, consumers have the option to continue using the installed version of the respective software. In such a setting, θ can be interpreted as the additional value that a consumer gains from shifting to the new subscription version.

Customer reviews of the Adobe Creative Cloud membership on the Amazon website vary tremendously. Of 43 reviews published on February 12, 2014, 19 gave it 5 stars and 11 gave it only 1 star. See all reviews at the link

Bulow (![]() ) has demonstrated that the existence of positive marginal costs can actually alleviate the time inconsistency problem facing the monopolist. In this paper, we do not consider the possibility that the monopolist can strategically choose a technology with high variable cost in order to alleviate this problem.

) has demonstrated that the existence of positive marginal costs can actually alleviate the time inconsistency problem facing the monopolist. In this paper, we do not consider the possibility that the monopolist can strategically choose a technology with high variable cost in order to alleviate this problem.

There are two additional cases that may arise at the equilibrium depending upon the choice of P 2R as follows:(i) P 2R < θ* – No conditional buying by any type of consumer. All returning customers continue to purchase, irrespective of their realized value of q.(ii) θ* + q H < P 2R < θ H + q H – Conditional buying by consumers in the upper tail. For such a large value of P 2R , consumers having low valuations never purchase the service again, and those having high valuations condition their purchase decision on their realized value of q.(i) It can be shown, however, that the two cases above are inconsistent with less than full coverage of the market. The authors can provide, upon request, a proof of that claim.