Abstract

What motivates the geographic footprint of the supply chains that multinational firms (MNFs) deploy? Traditional research in the operations and supply chain management literature tends to recommend locations primarily based on differentials in production costs and the ramifications of physical distance ignoring the role of taxation. MNFs that strategically position parts of their supply chains in low‐tax locations can allocate the profits across the divisions to improve post‐tax profits. For the profit allocation to be defensible to tax authorities, the divisional operations must possess real decision authority and bear meaningful risks. Generally speaking, the greater the transfer of risk and control, the larger the allowable allocation of profit. These transfers may also create inefficiencies due to misalignment of business goals and attitudes toward risk. We model these trade‐offs in the context of placing in a low‐tax region a subsidiary that oversees product distribution (as a limited risk distributor commissionnaire, limited risk distributor, or fully fledged distributor). Our analysis demonstrates that the MNF's preferences regarding the operating structures are not necessarily an obvious ordering based on the amount of risk and decision authority transferred to the division in the low‐tax jurisdiction. We derive and analyze threshold values of the performance parameters that describe the main trade‐offs involved in selecting an operating structure. We find some of the optimal decisions to exhibit interesting non‐monotone behavior. For instance, profits can increase when the tax rate in the low‐tax jurisdiction increases. Numerical analysis shows that the Limited‐Risk Distributor structure is rarely optimal and quantifies when each alternative dominates it.

Keywords

Introduction

Why are the supply chains of multinational firms (MNFs) structured the way they are? Traditional prescriptive research in the operations and supply chain management literature tends to recommend locations primarily based on differentials in operating costs (e.g., for labor, materials, and other resources) and the ramifications of physical distance (e.g., lead times, transportation costs, and other consequences of being close to or far from suppliers, customers, or other key actors in the supply chain). The role of taxes has received much less attention. That is, the prevailing paradigm is maximization of pre‐tax profit or minimization of pre‐tax cost.

In fact, tax is the largest single expense for many companies (Webber 2011a), and prudent geographic choices can often dramatically reduce tax liability (Helderman and Kraan 2011, Webber 2012). This opportunity exists because of the differences in tax legislation around the world. Tax‐friendly regions include Switzerland, Hong Kong, Singapore, Malaysia, Ireland, Serbia, Bulgaria, and Cyprus (Green 2011, Helderman and Kraan 2011, KPMG 2011, Wheatley 2011). Countries like these aspire to stimulate local economic activity, and in the optimistic scenario the tax base grows enough that the reduced tax rates more than pay for themselves (Webber 2011b). The effective tax rates themselves may even be directly negotiated between an MNF and a motivated government (Wheatley 2011). For instance, Bergin (2013) notes, “Tax deals are often agreed in advance with companies that are considering basing themselves in the Netherlands, so they know where they stand.” Cyprus and Luxembourg are other countries that have been known to allow companies to negotiate a tax rate (Needham 2013).

“International tax arbitrage” (sometimes called “cross‐border tax arbitrage”) refers to any tax strategy that exploits gaps between the tax systems of different nations. One way to perform this arbitrage is simply to move the entire firm or at least the corporate headquarters (“corporate inversion,” cf. Gelles (2013), Webber (2011b)) to a low‐tax region. But this might incur substantial overhead costs, cause problems for the organization's human resources, or have some other operational or strategic disadvantages.

Other alternatives are less extreme. Many entail organizationally separating the enterprise into pieces. Besides the “principal” company, which performs high value‐added functions and bears the most meaningful risks, individual pieces might correspond to a function such as manufacturing (e.g., by spinning off a division as a contract manufacturer or toller), procurement (e.g., by creating a central organization to handle all the firm's procurement), development of intellectual property (e.g., by creating a dedicated organization that licenses IP to the other divisions), or distribution (e.g., by creating various forms of local resellers). The MNF has some latitude to allocate the profits across the different pieces of the firm (“base shifting”), and then can improve post‐tax profits by positioning the most profit‐heavy pieces in low‐tax jurisdictions (Lemein 2005, Vroemen 2002).

For the profit allocation to be defensible to tax authorities, the operations in low‐tax regions must have meaningful decision authority and bear nontrivial risks such as, for example, taking financial responsibility for selling at a lower price. Broadly speaking, taking on more authority and risk will justify a larger allocation of the profit.

The crucial accounting concepts are the “arm's length principle” and the “substantial contribution” test. The “arm's length principle” entails making sure the roles and responsibilities retained by an internal division are associated with an economic return comparable to what an unrelated party with similar roles and responsibilities would earn. The calculation of the appropriate economic return must grapple with the difficulty of establishing “market” values of the goods at various handoffs in the supply chain. This is especially hard when the goods are work‐in‐process, and stand‐alone firms that can act as appropriate benchmarks for internal divisions simply do not exist. The “substantial contribution” test assesses whether the division truly plays a meaningful role in the overall business. For example, in March 2014, the US Congress accused Illinois‐based Caterpillar of creating a spare‐parts distribution subsidiary in Switzerland to dodge $2.4 billion of income taxes between 1999 and 2012. The charge claimed the transfers of profits “had no economic substance and were made solely to take advantage of the lower tax rate Caterpillar negotiated with Switzerland” (4–6%, vs. an effective rate of 29% in the US). The investigating Senate subcommittee concluded that while 85% of the profits on these spare parts were allocated to the Swiss division, few employees were actually located there. Certain critical business functions were performed in the US and Caterpillar had no comparable capabilities in Switzerland (Walsh 2014).

The OECD (Organisation for Economic Cooperation and Development) provides guidelines for assessing the responsibilities and risks of each involved party. This mechanism, called “functional analysis” (OECD 2010) and specified in the Discussion Draft for Public Comment on Transfer Pricing Guidelines for Business Restructuring (OECD 2008 and 2009), starts with the contractual arrangements between parties and subsequently examines correspondence and conduct to determine actual risk exposure and the parties' degree of control over the risks.

Entities can demonstrate their independence with special attention to lines of reporting (employees in local entities should not report to other entities, meaning that the employment, pay, and promotion decisions should be kept internal to the appropriate entity), data visibility (an internal division purported to be independent should not have access to data that a third party would not be able to see, such as raw materials costs or profit margins), and governance structure (each entity should retain its own board of directors or other governing body). Tax authorities go to some lengths to verify where the actual business is being done. For instance, they may request expense reports, email, and mobile phone records of employees. Red flags arise if employees have permanent office space in other countries, or if key meetings are frequently held outside of the division's official tax jurisdiction (Newman and Pinto 2012).

Some management consulting firms, especially those with a heritage in accounting, have built practices around helping MNFs design and implement such strategies. For example, Deloitte's notion of “Business Model Optimization” (BMO) has the theme of deeply integrating tax considerations into the design of the business model, including aspects such as the level of centralization and the geographic footprint (Driscoll et al. 2012, Newman and Pinto 2012). As Driscoll et al. (2012) notes, “Substantial tax benefit can be achieved by moving along the centralization continuum… provided the tax structure is calibrated with the operational change.” Specialized expertise in tax and corporate law may be necessary to prevent an MNF's tax avoidance strategy from turning into tax evasion.

As mentioned, MNFs have a number of ways to capitalize on opportunities for international tax arbitrage. One specifically related to the construction of the supply chain is based on creating a distributor division in a tax‐friendly region. This division performs sales and marketing functions and sells to end customers the product provided by the headquarters (HQ). HQ can then allocate a portion of profit to this division, and pay tax on this portion at the advantageous tax rate. Devonshire‐Ellis et al. (2011) and Deloitte (2014) elaborate on nuances of actual structures.

This is supply chain design in the sense of defining the locations where the key business decisions about distribution will be made. As Webber (2011a) notes, “One of the most important activities for both supply chain organizations and tax departments is recommending where to locate business processes.” These decisions alter the flows of information and funds, which can be just as meaningful to supply chain performance as are the flows of materials.

This study investigates three commonly observed options for the tax‐advantaged distribution division's operating structure: Commissionnaire, Limited‐Risk Distributor, and Fully‐Fledged Distributor. Precise definitions of these structures do not exist because in practice the implementations vary. They reside along a continuum of distribution models, which maps to a continuum of tax benefits.

This study uses the following understanding of the three structures, which closely resembles the descriptions in Bakker (2009) and is consistent with industry reports (see, e.g., Deloitte 2014). A Commissionnaire performs only sales and distribution and takes on very limited risk and authority, hence HQ is entitled to allocate only a very small percentage of profit to this division. A Fully‐Fledged Distributor has the most decision power and bears business risks, so HQ can declare a substantial portion of the profit in the distributor's jurisdiction. A Fully‐Fledged Distributor is typically a buy‐sell entity that makes purchasing decision and takes ownership of inventory. In our model, the Fully‐Fledged Distributor makes the purchasing decision. However, since we assume a market‐clearing mechanism, the inventory risk is not relevant. A Limited‐Risk Distributor is an intermediate form in terms of the duties performed and therefore the allowable profit allocation.

While use of these structures is common, 1 firms are not required to publicly declare or register these choices and tend to hold this information as confidential. 2 Some company examples have been revealed through lawsuits and government investigations. Zimmer Limited is known in tax law for setting precedent regarding the treatment of the Commissionaire structure (Sprague 2010). Dell AS in Norway, whose structure became public through a Norwegian Supreme Court case, is a Commissionaire, and Roche Vitaminas was converted from a Fully‐Fledged Distributor to Commissionnaire after 1999 (Lang et al. 2014). VPNA (a US subsidiary of Canada's Valent Pharmaceuticals) serves as a Limited‐Risk Distributor in purchasing finished product from other members of the Valeant group for distribution in the United States (Portman 2015).

Table 1 summarizes how risks and functions vary across these operating structures. It focuses on market (or product price) risk, that is, “the risk that a firm will not be able to sell products for prices it anticipated” as defined in Bakker (2009), as the main business risk borne by a Limited‐Risk Distributor or a Fully‐Fledged Distributor.

Differences among MNF Approaches to Distribution

We model these three operating structures. We also provide a benchmark, called “No Distributor,” in which the MNF does not establish a physical presence for distribution in the foreign jurisdiction and therefore cannot declare any profits there. Relative to No Distributor, the insertion of the distribution division into the supply chain adds overhead costs and inefficiencies due to decentralization of decision authority (to an extent necessary to justify the shifting of profit to the low‐tax region) and the possible need to relocate key staff. At the same time, a local distributor might have a comparative advantage in selling, due to focus and familiarity.

The supply chain designer must consider these factors along with the potential tax benefits. To illuminate the trade‐offs, we model the decisions related to supply chain structure, sales effort, and quantity, and explicitly distinguish between the incentives of HQ and the distributor.

We specifically address the following research questions: For each operating structure (No Distributor, Commissionnaire, Limited‐Risk Distributor, and Fully‐Fledged Distributor), what are the MNF's optimal decisions? What profit improvement can MNFs achieve by moving to a tax‐efficient structure? Which operating structure should the MNF use? How do the operational parameters of the MNF and the parameters of the tax jurisdiction affect the answers to all these questions?

We use the principal–agent framework to capture the interaction between the HQ and the manager governing the distributor division, and perform theoretical analysis supported by numerical examples. Our analysis demonstrates that the MNF's preferences regarding the operating structures are not necessarily an obvious ordering based on the amount of risk and decision authority transferred to the division in the low‐tax jurisdiction. We derive and analyze threshold values of the performance parameters that describe the main trade‐offs. We find some of the optimal decisions to exhibit non‐monotone or counterintuitive behavior that intrigues. For instance, prices are non‐monotone in cost, and profits can increase when the tax rate in the jurisdiction increases. Numerical analysis shows that the Limited‐Risk Distributor structure is rarely optimal and quantifies when each alternative dominates it.

Before proceeding, we emphasize that our intent is not to advocate for any particular one of these distribution structures. We also do not suggest prioritizing tax considerations over any others. Business strategy should come first, and tax strategy is just one element of this. We do encourage firms to systematically analyze the impact of taxes upon supply chain strategies and profitability, and this study proceeds in such a spirit.

The remainder of this study is organized as follows. Section 3 presents mathematical models of each operating structure. Section 4 derives optimal decisions for each structure and their sensitivities to the MNF parameters and tax rates. Section 5 numerically illustrates how much the MNF can gain from adopting tax‐efficient structures and when each structure is preferable. Section 6 summarizes the main insights and concludes.

Literature Review

Our study contributes to the small but growing body of literature concerning the impact of tax considerations on operational and supply chain decisions. Some earlier studies in this stream developed efficient procedures for optimizing large‐scale supply chains. For example, Cohen and Lee (1989) formulate a global firm's resource deployment problem as a mixed‐integer nonlinear program, Vidal and Goetschalckx (2001) optimize after‐tax profit of a global firm with a specific structure by computing optimal network flows and transfer prices. Interested readers should refer to Lu and Van Mieghem (2009) for an overview of the methods developed for solving complex global supply chain problems. Our study has broader scope in the sense of addressing the design of the firm's structure: how should the firm be structured/designed to best leverage a tax opportunity?

A recent study that also guides the design of a global supply chain's structure is Hsu and Zhu (2011). They analyze different import/export structures that vary in VAT (value‐added tax) implications, and recommend production and distribution decisions for an MNF that produces in China and sells within and outside the country. Our study focuses on supply chain restructuring, specifically the MNF's relocation of decision authority and risk exposure in order to reduce income tax liability.

Transfer pricing is one of the main mechanisms for allocating profit among different divisions of a firm. Multiple papers have investigated the interaction of transfer prices and operating decisions for a firm that operates across multiple tax jurisdictions. Shunko and Gavirneni (2007) study an MNF that sources from a foreign subsidiary. They analyze transfer price and sales price decisions in the presence of random price‐dependent demand, and show that tax optimization using proper transfer pricing has large benefits. Huh and Park (2013) examine different transfer pricing schemes in a newsvendor environment. Shunko et al. (2014) consider an MNF that faces a “make or buy” decision and study the interaction of transfer pricing and sourcing when costs at the MNF's foreign subsidiaries are uncertain. Here we do not explicitly model the transfer prices, instead focusing on the allocation of profits across the divisions and assuming the existence of transfer prices that achieve the desired allocation. Our study adds to this literature by carefully looking at the tax‐efficient business restructuring practices that justify the profit allocation by adequately shifting (decentralizing) the decision power and risk.

The literature on supply chain coordination has long sought to rectify the inefficiencies of decentralized decision making (see, e.g., Perakis and Roels (2007)), especially through the design of contracts between firms in the supply chain (cf. Tsay et al. (1999), Cachon (2003)). Recent work has cast decentralization in a more positive light. Belavina and Girotra (2012) show how decentralized decision‐making can strictly improve performance of the supply chain when the members of the supply chain engage in continuous trade. Shi et al. (2013) show that manufacturers selling to vertically heterogeneous customers offer higher product quality in a decentralized channel. Our paper demonstrates another motive for decentralization – as a legal prerequisite for capitalizing on a tax opportunity – and provides managerial insights into the form of decentralization (from among commonly practiced options) that will be most beneficial for an MNF.

Models

We now model all four operating structures described earlier, using the notation summarized in Table 2.

Summary of Notation

An MNF has headquarters (HQ) in a jurisdiction with tax rate t, produces (or sources) there a quantity q at per‐unit cost c (which represents all costs recorded by the MNF as cost of goods sold, including but not limited to sourcing, production, packaging, and logistics), and sells in the global market. It considers establishing a distributor organization in a different jurisdiction with tax rate τ < t (e.g., a US company taxed at 35% that serves the China market through a distributor in Hong Kong taxed at 16.5%). This creates an opportunity for tax arbitrage.

We adopt the inverse demand model used in Cachon and Lariviere (2005), in which demand depends on price and on sales effort of an amount e:

The marketing effort e (e.g., for sales and advertising) comes at a convexly increasing cost

With this the profit function will be jointly concave in e and q.

Our arithmetic for taxes

In all our models, as in reality, profit can be either positive (earnings) or negative (net operating loss or NOL). For example, if

We can also treat losses incurred in the foreign location symmetrically under the premise that the tax rate there is very low. Even if the local statutes governing carrybacks and carryforwards diverge from those of the United States, the impact on after‐tax profit will be negligible as any tax liability or credit would be small.

Finally, when consolidating after‐tax income from the United States and the foreign location, we assume that the foreign income is not repatriated back to the United States, hence is deferred from US taxation. Such income is referred to as “permanently reinvested earnings” and is prevalent among US MNFs. Graham et al. (2012) reports that permanent reinvested earnings for the 50 largest US companies totaled $610 billion in 2008.

The distributor division's risk‐averse manager

As mentioned earlier, regardless of the operating structure used for the distributor division, HQ hires a manager at the foreign location to manage the division. However, to justify a higher profit allocation to the distributor division in the Limited Risk and Fully‐Fledged Distributor structures, the MNF must actually transfer risk to the decision‐maker of the division: “...taxpayers are required to show that the principal company or risk taker has sufficient substance to actually manage and control the risks it has assumed” (Bakker 2009).

The manager's compensation contract can serve as a mechanism for transferring risk by including profit‐sharing. As the tax strategy relies on the manager not being a “dependent” agent, HQ must not directly force the manager's decisions even though the quantity decision is observable and verifiable. Hence, the manager makes the effort and quantity decisions according to her own objective function, which may be suboptimal from the HQ's perspective. In addition, recall that the OECD guidelines determine the real allocation of risk and control by close examination of contractual arrangements and actual conduct of the involved parties (OECD 2008 and 2009). Thus, in our models, HQ contracts on the uncertain outcome of the manager's actions. We follow the standard assumption of the Principal–Agent literature whereby HQ (the principal) is risk‐neutral as it is a large business entity with diversified investments, while the manager (the agent) is risk‐averse 3 (cf. Holmstrom and Milgrom (1991), Feltham and Xie (1994)).

The manager's compensation comprises a fixed payment and a bonus payment linked to the profit allocated to the distributor of type i, i ∈ {L, F}:

We express the manager's objective, using the certainty equivalent (CE) measure, which is a monotone transformation of the expectation of the utility function:

Since CE is a monotone transformation, it exhibits the same ordering of preferences as does the expected utility function. Hence, maximizing the manager's CE will determine his optimal behavior. Since r and

Note that the absence of legal restrictions on the profit transferred to the distributor division (i.e.,

The manager's reservation wage is w, so that the manager's individual rationality constraint is as follows:

No Distributor (Problem N)

In the benchmark case, the MNF has headquarters (HQ) and no foreign distributor, meaning that HQ undertakes all actions and decisions for the foreign jurisdiction, which comes at a fixed cost d and a variable cost

And the MNF's optimization problem is as follows:

The assumption of a favorable foreign tax rate (τ < t) in or near the sales region means the MNF can benefit from shifting profit to this jurisdiction. However, to do this the MNF must move away from Problem N by opening a distribution division in the foreign region. The MNF will then save cost d but incur the fixed cost of establishing a foreign distributor. Our model denotes this fixed cost as α, which captures the wages paid to the local personnel. By law the percentage of profit allocated to this distributor should be commensurate with the transferred amount of decision‐making power and risk. To establish “substantial contribution” or “business purpose,” the MNF hires a manager at that location who is compensated from the division revenue.

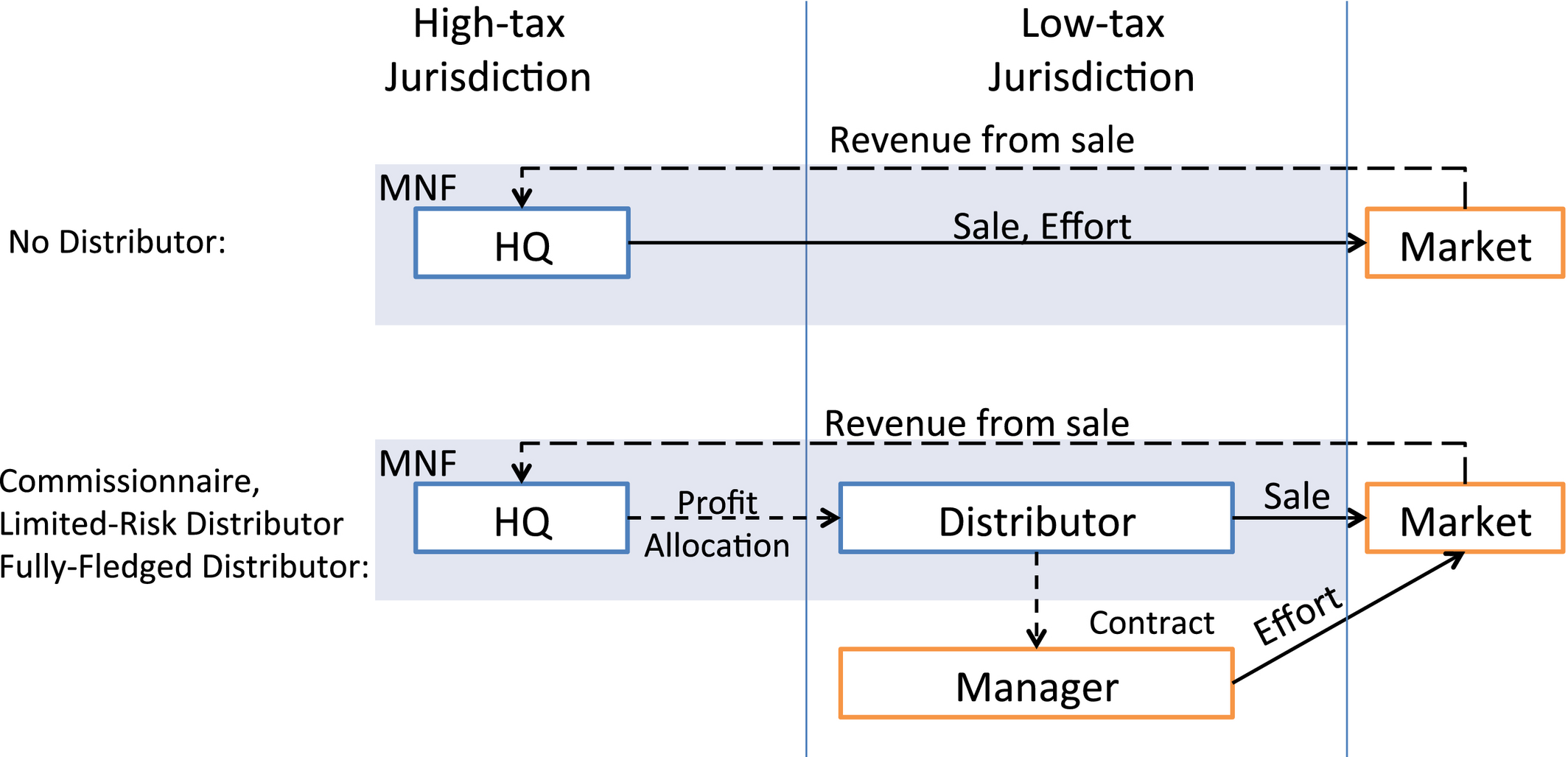

We consider three alternatives to the No Distributor operating structure, as described in this paper's opening section: Commissionnaire (C), Limited‐Risk Distributor (L), and Fully‐Fledged Distributor (F). Figure 1 depicts the differences among these structures. The dashed arrows indicate cash flows and solid arrows are decisions.

Options for MNF Structure

Product flows from HQ directly to the market (e.g., through drop‐shipping). So inserting a distributor division changes the organizational structure and cash flows, but does not create any new logistics costs. Tax law is generally more concerned about the financial liability for inventory than the physical possession, and liability does change hands in the Limited‐Risk Distributor and Fully‐Fledged Distributor structures with the distributor division taking title to the goods (and therefore bearing the market risk).

The order quantity is decided by the distributor division's manager in the Fully‐Fledged Distributor structure and by HQ in the other three. We next model the attributes of each structure to reflect the industry practices summarized earlier in Table 1.

Commissionnaire (Problem C)

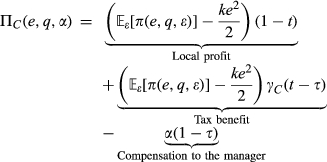

Under the Commissionnaire organizational structure, no risk is transferred to the division, the level of effort expected from the manager is forced by the employment contract, the effort expenses are covered by HQ, and the manager gets only a fixed payment: α > 0. Such structure legally entitles the MNF to allocate a small percentage of operating profit (

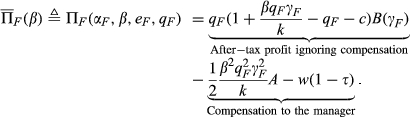

HQ's expected after‐tax profit is then:

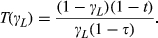

To provide intuition and facilitate the presentation of results, define

We can re‐write the objective function as:

Denoting the manager's pre‐tax reservation wage as w, the MNF's optimization problem when operating a Commissionnaire structure is:

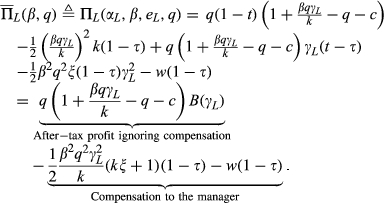

Limited‐Risk Distributor (Problem L)

Under the Limited‐Risk Distributor operating structure, the manager of the foreign distribution division bears some risk and controls the sales effort. HQ decides the quantity and sets parameters of the compensation contract between the division and the manager. This arrangement allows the division to own a fraction

A real MNF must demonstrate compliance of its

HQ then must solve the following problem:

Equation 11 is the incentive compatibility condition stating that the manager maximizes individual utility and Equation 12 is the individual rationality (or participation) constraint that determines whether the manager will sign the contract.

Fully‐Fledged Distributor (Problem F)

The MNF can transfer an even larger fraction of the profit to the tax‐advantaged region by using a Fully‐Fledged Distributor structure.

Like their counterparts in Problem L, Equation 14 imposes incentive compatibility and Equation 15 conveys individual rationality.

The next section presents solutions for all four problems, discusses their properties, and provides intuition for the findings.

Analysis

This section obtains optimal decisions for HQ and the distribution division manager for each operating structure (Propositions 1, 2, 3, and 6). For brevity we do not analytically compare each structure head‐to‐head against every other. Instead we follow a deliberate progression that isolates each advantage and disadvantage that occurs in the course of creating the distributor and then progressively giving it more control and risk. Problem C vs. Problem N (Proposition 3) sets the baseline to quantify the tax benefit attached to the creation of the distributor without any confounding influences. Problem L vs. Problem C (Proposition 5) highlights the impact of then passing risk to that distributor, whose decisions are colored by sensitivity to risk. Problem F vs. Problem L (Proposition 7) shows the consequences of delegating additional decision authority to the distributor who already bears risk. The figures in Section 5 will then compactly illustrate the complete set of head‐to‐head comparisons.

No Distributor (Problem N)

With the No Distributor structure, HQ sets effort level and quantity by optimizing the expected after‐tax profit as specified in Problem N. We subsequently denote the components of the optimal solution to Problem i as

Under the No Distributor structure (Problem N), the MNF's optimal decisions are:

Complete comparative statics of this and subsequent solutions appear in the Appendix along with all proofs of analytical results. Here we highlight only surprising findings:

Commissionnaire (Problem C)

Under the Commissionnaire structure, the MNF transfers a fraction of the profit to the distribution division and must compensate the division manager. All decisions, however, are still made centrally by HQ, so HQ needs only to pay the manager his reservation wage:

Under the Commissionnaire structure, the MNF's optimal decisions are:

The foreign tax rate τ comes into play in Problem C. In particular, profit

Juxtaposing the solutions to Problems N and C (Equations 16 and 17) illustrates a fundamental trade‐off in designing a tax‐efficient supply chain: adding an entity to act as a distribution company in the foreign jurisdiction can generate tax benefits (within the limits of tax law and captured by parameter

Let

The threshold indicates that in order for the Commissionnaire structure to be more profitable than the No Distributor structure, the fixed cost of the distributor division should be low, the difference in tax rates between the two jurisdictions should be high, and the costs of product and sales effort should be low. This combination of conditions indicates that a substantial profit margin is available for transfer to the foreign division.

Limited‐Risk Distributor (Problem L)

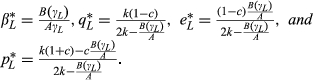

In the Limited‐Risk Distributor structure, the division manager dictates the sales effort (e) and HQ must offer an incentive‐compatible compensation contract that guarantees at least the manager's reservation wage. Since the individual rationality constraint (Equation 12) will bind at optimality we can follow the standard simplification in the Principal‐Agent literature and express α as:

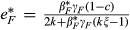

The manager's best‐response effort level is

Under the Limited‐Risk Distributor structure, the MNF's optimal decisions are as follows:

The resulting profit is:

In contrast to the previous two structures, all optimal decisions in Problem L depend on the tax rates in both jurisdictions and on the legally imposed limit on the transfer of profit. We can write

Second, if there is no tax difference between the two jurisdictions (t = τ),

Similar to the results for Problem C,

Comparison of profits in Problems C and L (Equations 17 and 19) illustrates another important trade‐off in tax‐efficient supply chain management: shifting more risk to a division may garner tax benefits, but also distorts incentives and burdens the MNF with the cost of compensating the risk‐bearing division for the allocated risk. The trade‐off is apparent from comparing Equations 17 and 19.

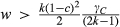

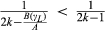

Let

Proposition 5 quantifies how high the allocation percentage

Most of the comparative statics are intuitive, but the impacts of the cost of effort (k) and risk exposure (ξ) on the threshold

Fully‐Fledged Distributor (Problem F)

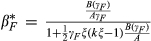

In the Fully‐Fledged Distributor structure, both decisions (sales effort (e) and quantity (q)) belong to the division manager and HQ must offer an incentive‐compatible compensation contract that guarantees at least the manager's reservation wage. Of the options considered in this study, this structure allows the MNF to transfer the greatest fraction of profit to the foreign division (

As with the Limited‐Risk Distributor structure, in the Fully‐Fledged Distributor structure the individual rationality constraint (Equation 15) binds at optimality. So the optimal α is

Under the Fully‐Fledged Distributor structure, the MNF's optimal decisions are:

The resulting optimal profit is:

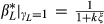

Since

Comparing the optimal bonus rate when

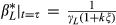

Again the price and profit exhibit some non‐monotone comparative statics (

This exhibits an interesting contrast to the solution of Problem L, where

Juxtaposing Equations 19 and 20 illuminates and quantifies the trade‐off (tax benefit vs. inefficiency due to decentralization) in moving from the Limited‐Risk Distributor structure to the Fully‐Fledged Distributor structure. We summarize the trade‐off using the following relationship.

Let

Proposition 7 quantifies how high the profit allocation must be for the Fully‐Fledged Distributor structure to be more profitable than the Limited‐Risk Distributor. Section 5.1 numerically characterizes the comparative statics of this threshold.

Summary of Results and Ordering of Decisions

Proposition 8 orders the solutions to Problems C, L, and F by size (the solutions are summarized in Table 3). This ordering can generate hypotheses for empirical accounting research. When δ = 1, the solutions to Problems N and C are identical.

Summary of Results (Optimal Profits Assume w = 0 and d = 0 for Clarity of Presentation)

The optimal decisions in Problems C, L, and F are ordered as follows.

Moving to either of the truly decentralized structures (Limited‐Risk Distributor and Fully‐Fledged Distributor) reduces the sales effort and the quantity. This is because in these structures, the MNF has to share the profit with the manager, which lowers the marginal benefit of increasing the effort level or quantity.

The ordering of the decisions between these two structures reflects the difference in the specific decisions delegated to the distributor's manager. The manager is risk‐averse and increasing the order will increase risk, so giving the manager control of the quantity (as Problem F does) will lead to an order smaller than what the risk‐neutral HQ would choose (in Problem L). The effort decision, however, belongs to the manager in both Problems L and F and depends on the compensation. The ordering of

Comparison of Different Structures

This section numerically illustrates the following: (a) the influence of the allowable profit allocation in determining which operating structure the MNF will prefer, (b) the profit improvement the MNF can achieve by adopting a tax‐efficient operating structure, and (c) the sets of conditions for which each operating structure is best.

How the Profit Allocation Percentage Determines the MNF's Preferred Structure

Propositions 3, 5 and 7 quantified the thresholds for the profit allocation percentage at which the MNF would switch operating structures. Here we numerically assess the thresholds using realistic values for the business and tax parameters. Figure 2 uses the actual current US corporate income tax rate as an anchor (t = 35%) and shows how the threshold for preferring No Distributor to Commissionnaire structure changes as the foreign tax rate grows from 0% to 35% (setting w = 0.001, δ = 1, d = 0, and c = 0.2; the other parameters are irrelevant).

How High must

How High must

Figure 3 shows that the threshold on

Figure 4 describes the threshold (

How High must

We numerically obtain the following comparative statics for

Profit Improvement from Tax Optimization

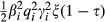

This section addresses a fundamental question of motivation for an MNF considering setting up a distributor division to leverage a region's tax rate: just how much profit improvement is on the table? We analytically obtain an upper bound for the special case of the foreign division having no special cost advantage in performing distribution. Then we numerically illustrate the actual profit improvement across various parameter combinations.

Suppose tax laws were to allow the MNF allocate some profit to the low‐tax region without actually changing the structure of the firm. No independent local manager would be needed, so all our models would have α = 0 and β = 0. This best‐case scenario provides upper bounds on the profit improvement that each tax‐motivated operating structure can achieve:

Figure 5 plots these bounds for a US‐based HQ (where the current corporate tax rate is 35%), using these profit allocation percentages:

Upper Bound on Profit Improvement Relative to the Fully Centralized Structure with No Decentralization Inefficiency

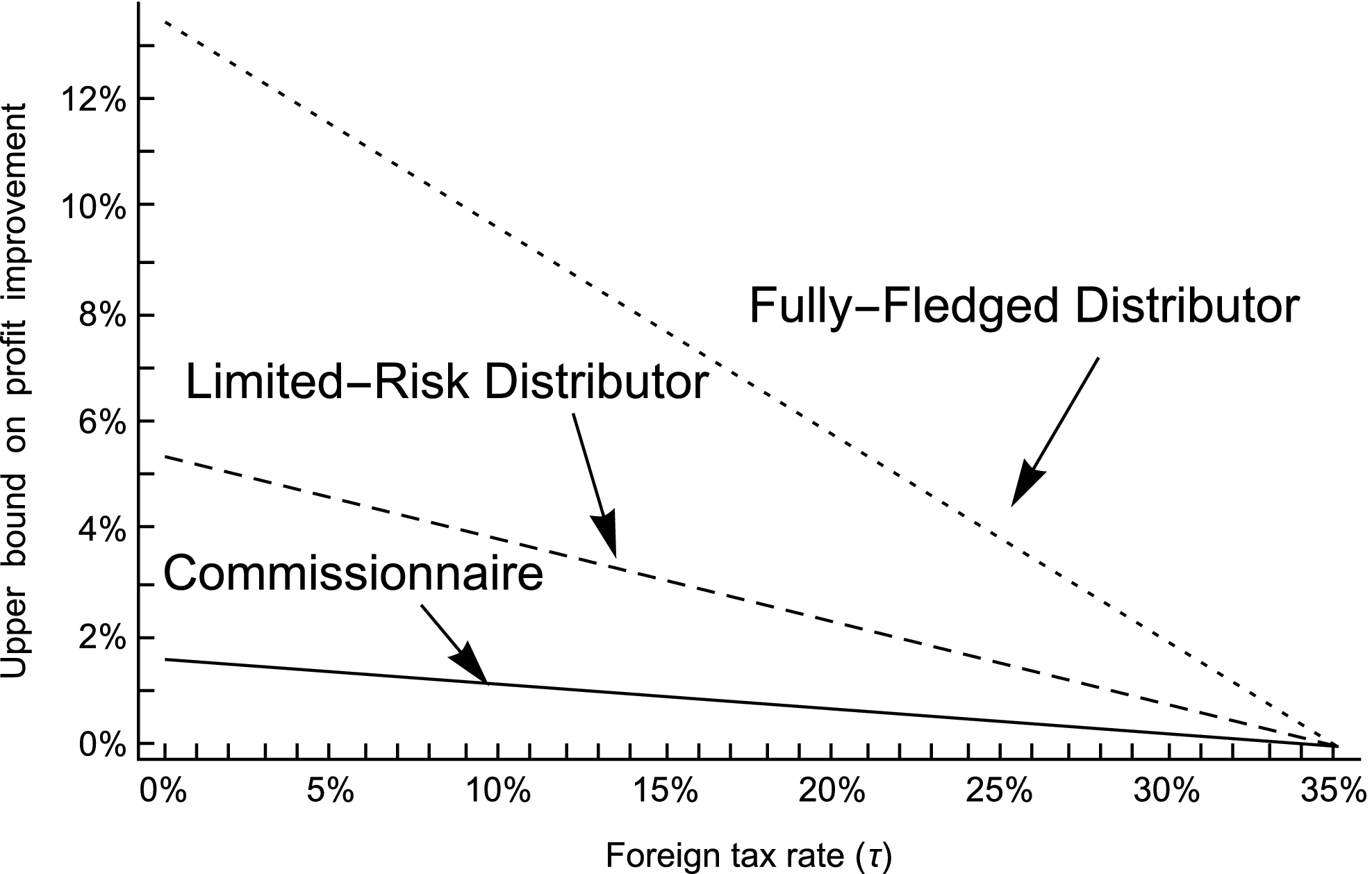

The legal requirement to shift some control and risk to an independent manager means the MNF's actual improvement in profitability will be strictly lower than these bounds, and will vary with k, ξ, w, and c. Figures 6 through 8 illustrate the influence of the cost of effort (k) for t = 35%, τ = 0%, w = 0.001, d = 0, δ = 1, and ξ = 10. These figures report the profit improvement as a percentage of the No Distributor benchmark profit, that is,

Profit Improvement from Choosing Commissionnaire Over No Distributor (

In all cases, the largest profit improvement occurs when the product cost c is low, meaning the margin is high. The main difference between implementing the Commissionnaire structure and choosing one of the risk‐transferring structures is the impact of the cost of effort: percentage profit improvement decreases in k when choosing the Commissionnaire (Figure 6) and increases in k when opting for the Limited‐Risk Distributor or the Fully‐Fledged Distributor (Figures 7 and 8). Increases in δ and/or d would reduce the profit in the No Distributor setting and thereby increase the profit improvement values (elevating those curves in Figures 6–8).

Profit Improvement from Choosing Limited‐Risk Distributor Over No Distributor (

Profit Improvement from Choosing Fully‐Fledged Distributor Over No Distributor (

Which Structure Should the MNF Use?

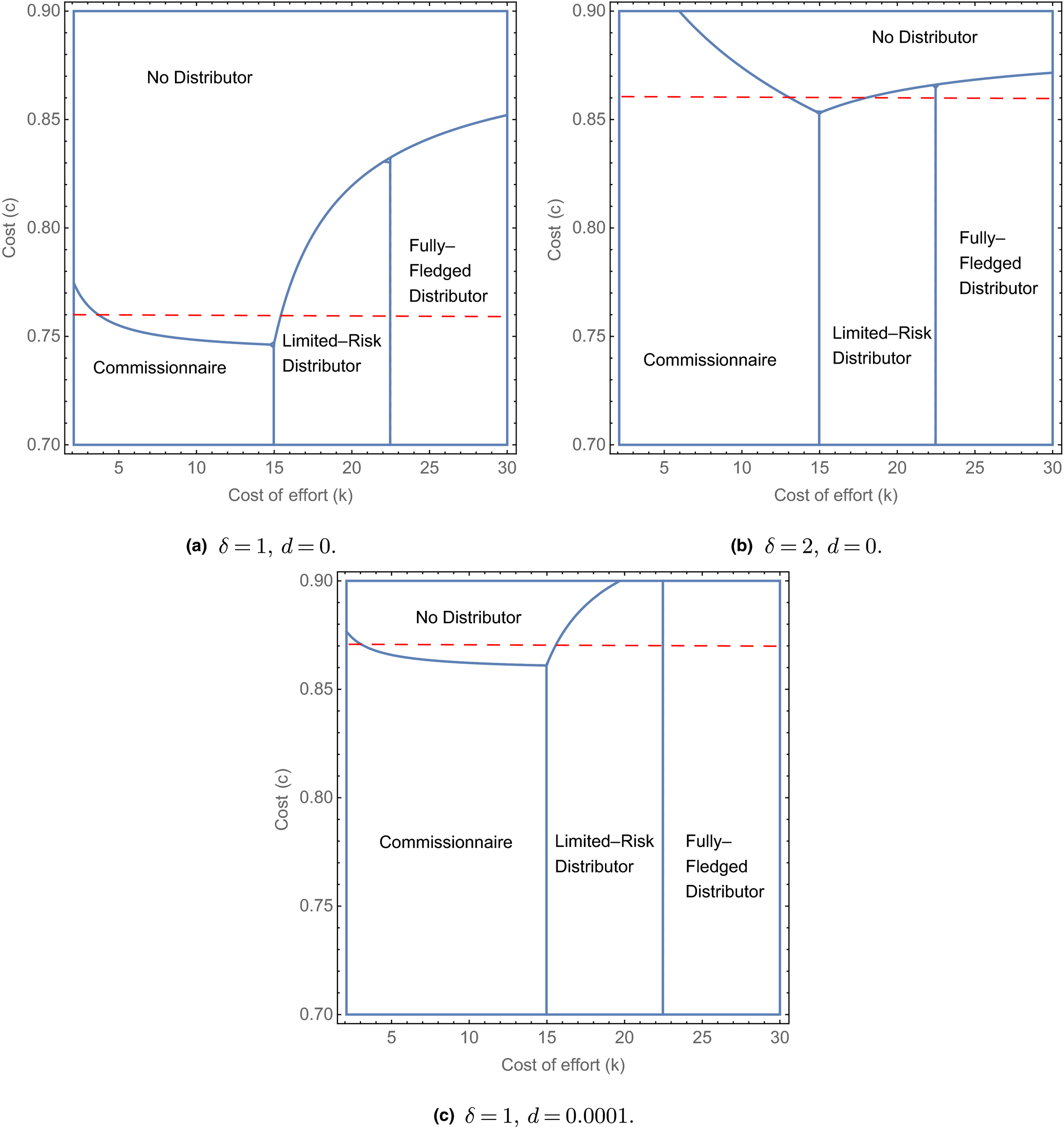

We now address the fundamental question of supply chain design by depicting when each structure dominates and how this conclusion will vary with the parameters of the MNF and the tax environment (two at a time). Figure 9 highlights the effect of the foreign tax rate (τ) and the cost of effort (k), when the other parameters are set at c = 0.6, t = 30%, ξ = 10, w = 0.0001, d = 0,

The Best Operating Structure for the MNF, for Combinations of the Foreign Tax Rate and the Cost of Effort

When the foreign tax rate is high, meaning that the opportunity for tax arbitrage is small, none of the tax‐efficient structures benefits the MNF. This reflects the fixed cost (w) of operating the foreign location.

Structures that transfer risk to the distributor division are attractive only when the cost of selling effort is high and the tax rate difference is large. We can understand this by concentrating on the choice between Commissionnaire and Limited‐Risk Distributor structures. Limited‐Risk Distributor enhances the tax benefit at the expense of distorting the incentives that determine the marketing effort as well as compensating the manager for bearing additional risk. If the tax opportunity is large, the distortion and compensation disadvantages would be the only reasons not to use the Limited‐Risk Distributor structure. When the cost of effort is small (which is tantamount to a strong influence over market demand), HQ wants the manager to exert great effort and achieves this only by offering a strong incentive, that is, a high bonus rate. But this makes the compensation cost outweigh the tax benefit, so the MNF will be better off with the Commissionnaire structure. Similar logic applies to the choice between the Limited‐Risk Distributor and Fully‐Fledged Distributor.

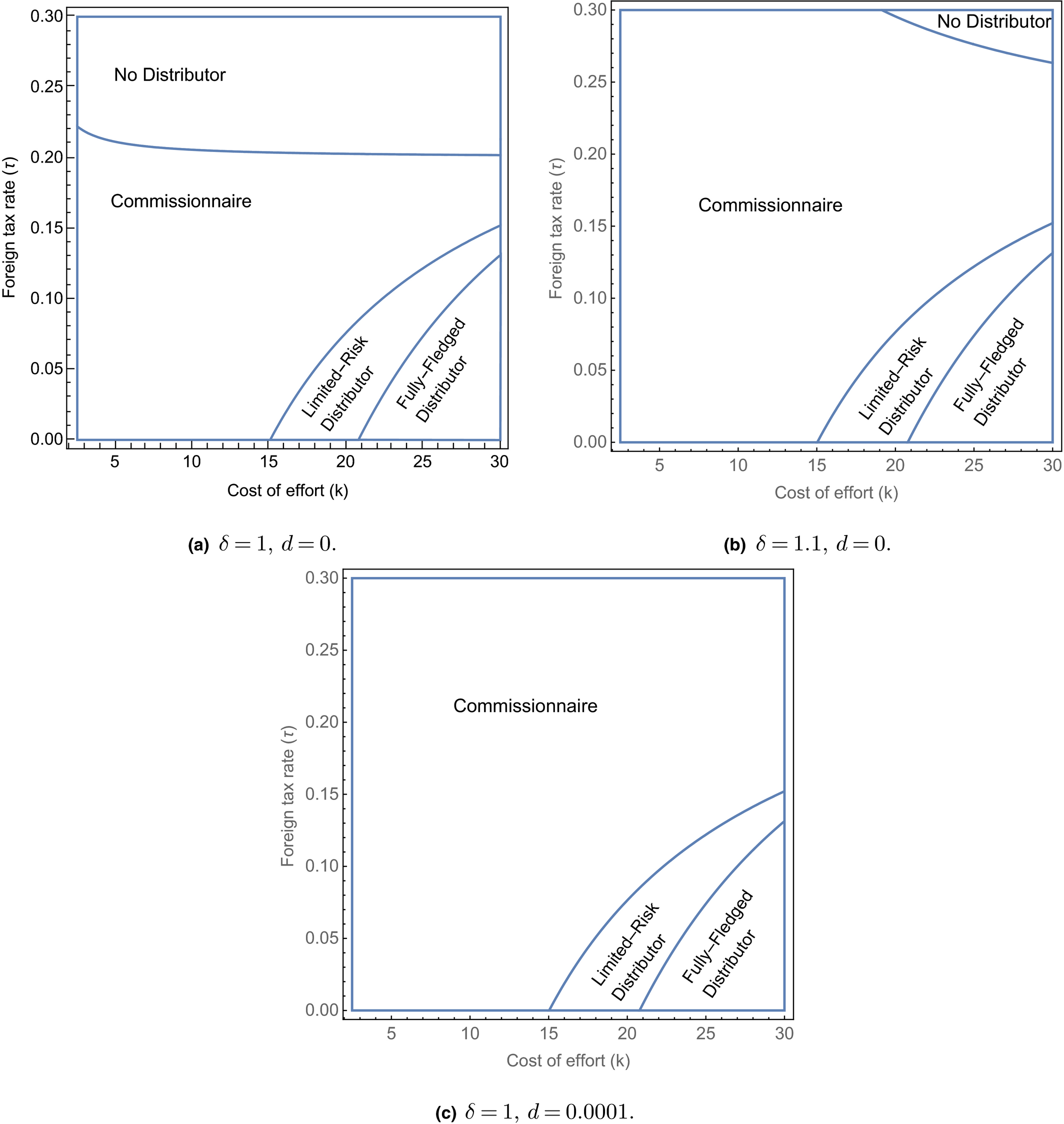

Figure 10 incorporates the issue of risk sensitivity by varying k and ξ. Recall that

The Best Operating Structure for the MNF, for Combinations of the Local Manager's Perceived Exposure to Risk and the Cost of Effort

We already know that the risk‐transferring structures are attractive when cost of effort (k) is large. Figure 10 illustrates that, of the two options, the Limited‐Risk Distributor is preferred when the risk exposure is not high and the cost of effort is not too high. The figure also shows a trade‐off between the two factors. The manager's risk exposure depends on the quantity ordered and in the Limited Risk structure HQ decides the quantity, hence dictating the risk to be inflicted upon the manager. Lacking control over the risk associated with the profit allocated to his division, the manager requires high compensation. The Fully Fledged structure gives the manager control over the quantity, thereby reducing the compensation requirement. So when the risk exposure parameter (ξ) and cost of effort (k) are high, the MNF prefers the Fully‐Fledged Distributor structure over the Limited‐Risk Distributor.

Lastly, Figure 11 looks at the trade‐off between procurement cost c and cost of effort k. To ensure that the stakes are sufficiently high, this analysis again uses the lowest possible foreign tax rate (τ = 0%; the other parameters are set at c = 0.6, t = 30%,

The Best Operating Structure for the MNF, for Combinations of the Production Cost and the Cost of Effort.

Conclusion and Future Research

As the saying goes, nothing is certain except for death and taxes. While businesses might not be able to do much about the former, they are increasingly savvy with respect to the latter, including in the design and management of their supply chains. A special opportunity arises for multinationals when governments offer low corporate tax rates to attract activity from foreign firms. A firm can exploit geographic differences in tax rates by placing in a low‐tax jurisdiction a subsidiary division, such as a distributor, that performs meaningful business functions. Commissionnaire, Limited‐Risk Distributor, and Fully‐Fledged Distributor are three ways to structure such an operation. These form a continuum in terms of the risk and control that go to the distributor division, which dictate the amount of profit the firm can legally recognize in the low‐tax region.

The legal requirement to give the division some autonomy distorts incentives and creates the burden of compensating the division for whatever risks are imposed upon it. Whereas decentralization is often considered detrimental for reasons like these, it can be seen as an enabler of tax savings when an opportunity for international tax arbitrage exists. We are not aware of any other research making this argument.

By weighing in on which, if any, of the three options a firm should implement, we help firms systematically choose the appropriate level of decentralization in light of this wrinkle. This required a model of multiple independent decision‐makers that includes market uncertainty, quantity and marketing effort decisions, divergence in risk attitudes, and fixed and contingent components of the compensation to the distributor division's manager.

The progression of our analysis has isolated each advantage and disadvantage occurring in the course of creating the distributor and then progressively giving it more control and risk. Comparing Commissionnaire (Problem C) and No Distributor (Problem N) set the baseline to quantify the tax benefit of creating the distribution division without any confounding influences. Comparing Limited‐Risk Distributor (Problem L) and Commissionnaire highlighted the impact of the then shifting risk to that distributor, whose decisions reflect sensitivity to risk. Comparing the Fully‐Fledged Distributor (Problem F) and Limited‐Risk Distributor showed the consequences of delegating additional decision authority to the distributor who already bears risk. We consolidated the individual findings by identifying conditions under which each of the operating structures would be best.

The large number of parameters and decisions renders absolute recommendations elusive. Nevertheless, we have established that the risk‐transferring structures (Limited‐Risk Distributor and Fully‐Fledged Distributor) are favorable when the tax rate difference is large and the cost of marketing effort is high. Though the impact of the large tax difference is intuitive, we have demonstrated that high cost of effort (or limited ability to influence market demand through effort) is another important factor since this reduces the costs of decentralization. And the Fully‐Fledged Distributor structure will tend to dominate the Limited‐Risk Distributor in many plausible scenarios. For instance, once risk is transferred to the distributor division, further delegation of decision power has only minor impact on costs since giving the division's manager additional levers to control his destiny will reduce his need for incentive compensation. We have provided full comparative statics for the decisions and financial outcomes induced by each of the operating structures.

The documented tax‐efficient supply chain practices reflect the conditions at a moment in time. Shifts in wage rates, currency exchange rates, and other environmental conditions might compel the relocation of certain business functions, which might cause the distributor division to drop beneath the threshold for “substantial contribution” (Driscoll et al. 2012, Newman and Pinto 2012). Tax rates can change, and so can the tax regulations and the way they are enforced. Indeed, the OECD's Base Erosion and Profit Shifting (BEPS) project (cf. Kadet 2016) issued guidelines in 2015 conveying a new push for transparency and a recommitment to taxing profits where the value is created, which makes alignment of tax and business strategies even more critical. Firms must monitor the tax landscape and be ready to adaptively refine their supply chain strategies. Our framework can contribute to these ongoing evaluations.

This study has not investigated alternatives to the profit‐sharing mechanism used to compensate the division manager. Our scope also excludes the explicit design of the transfer pricing system that accomplishes the proposed profit allocations. Like other analytical models, our framework does not touch on the organizational “change management” activities needed to transition away from the incumbent operating structure (Driscoll et al. 2012). We leave these issues for future research.

Footnotes

Acknowledgments

The authors are grateful to the following experts: Azedine Assassi (KPMG), David Cordova (Deloitte), Jeroen Djikman (KPMG), Michael Gilson (Deloitte), Ananth Iyer (Purdue University), Jeffrey Kadet (University of Washington, School of Law), Jerry Klopfer (KPMG), Tim Sarson (KPMG), Kris Timmermans (Accenture) and Glenn C. Walberg (University of Vermont). Their generosity with their time and expertise was crucial to keeping our research faithful to the actual implementations of the tax‐efficient supply chain strategies and to improving our manuscript.

1

T. Sarson (2016, KPMG UK, pers. comm.) describes some usage patterns by industry sector: (1) In the 1980s and 1990s a large number of US‐based sellers of fast‐moving consumer goods (FMCG) and technology products implemented Commissionaires in Europe (sometimes called the “European principal model”), together with toll manufacturing; (2) Limited‐Risk Distributors are the norm among auto manufacturers, makers of electronics, and pharmaceutical firms; and (3) Fully‐Fledged Distributors are common in industrial goods, the oil and gas industries, and solutions and engineering businesses.

2

KPMG and other consultancies have robust practices assisting clients fulfill legal requirements to maintain internal documentation that explains and justifies their choice of structure (A. Assassi, 2016, KPMG US, pers. comm.).

3

This study focuses specifically on differences in sensitivity to risk because transfer of risk and the compensation for this are under the microscope of the tax authorities when the time comes to justify the profit allocation.

4

5

This result is generalizable to any revenue function in which effort e and quantity q are complementary (technically,

6

An alternative way to define the profit base is to include wages paid to the distributor's personnel in the HQ's profit. All the optimal decisions would remain the same, but the optimal profit would become