Abstract

Sabotage activities often raise controversies and regulatory concerns due to the potential negative effects on competition and social welfare. These concerns are amplified when firms serving complementary markets integrate due to the integrated firm’s capability to engage in multi‐market sabotage. We note that the integrated firm’s incentive to engage in sabotage activities and the potential impact on social welfare has not been examined, and this drives the primary focus of our study. Interestingly, we find that the integrated firm may not have the incentive to engage in sabotage at all. We show that the integrated firm prefers to engage in sabotage (single‐market or multi‐market) only when it has cost advantages over its rivals in at least one of the markets. At the extreme, a certain level of sabotage actions could even force some product combinations out of the market and thus, there might be a need for regulatory intervention. A counter‐intuitive result is that under certain market conditions, the integrated firm’s sabotage activities correspond to those that would optimize social welfare.

Introduction

From an economics perspective, sabotage includes a set of firm‐specific, non‐price related actions negatively influencing competitor’s outcomes (see Beard et al. 2001, Mandy 2000). An example of such an action is Comcast providing its customers in Houston, Oregon, and Southwest Washington automatic increases in internet speeds...“if they subscribed to a package that includes cable television service and internet,..” through Comcast. 1 Obviously such a sabotage action would enhance customer’s perception of the ISP service provided by Comcast vis‐a‐vis the same service provide by competing firms (such as AT&T).

There are a large number of potential sabotage options available to integrated firms in direct competition with their non‐integrated rivals. For example,

When Google acquired YouTube in 2006, a keyword search for YouTube videos provided better results when using Google Chrome as compared to Microsoft Bing. In addition, within its own search process, Google favors YouTube video links over Vimeo links.

2

After the 2011 merger of Comcast and NBCUniversal resulted, certain exclusive content on NBC Universal was only offered to Comcast subscribers.

3

After Microsoft’s acquisition of LinkedIn in 2016, it was observed that LinkedIn’s app integrated directly with Windows 10 while this was not the case with other OS, and Microsoft’s mobile operating system did not support Facebook integration while that was not the case for LinkedIn.

4

Sabotage is even more likely to occur after an integration of firms providing complementary services. Although we focus primarily on actions undertaken by integrated firms, the analysis and resulting insights also hold for setting where firms across two complementary markets are exploring alliances to better serve their customers. Alliances stem from two or more companies agreeing to pool their resources to form a combined force in the marketplace. Thus, each participant in the alliance retains their individual entity but choose to compete against competitors as a unified business force. For example, consider Apple Pay and MasterCard who at first glance are competitors. 5 However, Apple collaborated with the second largest credit card provider in the world, MasterCard, to gain credibility in the merchant services and processing arena. While Apple Pay gets the benefit of MasterCard’s reputation, MasterCard gets the cache of being the first to be an Apple Pay authorized option. The experience of MasterCard helps Apple as it works out potential bugs and issues as Apple Pay gains acceptability. In such settings, it is also possible for the allied firms (in this case Apple Pay and MasterCard) to engage in sabotage actions against customers choosing either another Pay App (such as Square) or other credit card services (such as Visa and American Express).

Although sabotage could be viewed as anti‐competitive by regulators, standards and criteria used by such regulators have evolved over time. A market argument advocated by proponents of mergers and/or acquisitions is that fear of exclusion is not necessarily a reflector of anti‐competitive effects (see Krattenmaker and Salop 1986). Instead market arguments being made to regulators is that: As long as actions by integrated firms stem from efficient behavior and do not harm competitors more severely than habitual, unilateral independent decisions by the individual firms in the supply chain, such actions should not be construed as being anti‐competitive. The premise is that integration reflecting efficient behavior and, if successful in increasing market shares, is to be encouraged.

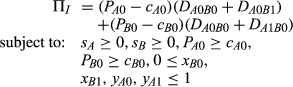

These aspects motivate the focus of this study. More specifically, we study an integrated firm’s incentive to engage in sabotage actions. Our general research question is: What is the optimal sabotage strategy for an integrated firm serving two complementary markets—no sabotage, single‐market sabotage, or multi‐market sabotage? Related questions we also address are: What are the key drivers of these sabotage choices? Which market(s) would be chosen for sabotage by the integrated firm? And finally, how would a social planner’s sabotage choices differ from those of the integrated firm?

Prior work in this domain focuses primarily on vertical integration. Since downstream buyers rely on upstream suppliers’ input, the upstream integrated firm’s sabotage activities impact downstream buyers in a single market. It is also worth noting that the majority of prior work has focused on cost‐side impacts of an integrated firm’s sabotage activities, that is, if the integrated upstream firm chooses to sabotage, it is reflected in increased costs for the competing downstream non‐integrated firm. Our focus differs on two important dimensions.

First, the setting we investigate is one in which the integrated firm could engage in either single‐market sabotage (i.e., sabotage its non‐integrated rivals in a single market) or multi‐market sabotage (i.e., sabotage its non‐integrated rivals in both markets). Returning to the earlier example of the 2016 Comcast‐NBCUniversal merger, the integrated firm competes with non‐integrated firms in two markets (e.g., AT&T as an ISP and CBS as a content provider). Thus, the integrated firm could undertake sabotage actions directed at either the ISP market, or the content provider market, or both markets.

Second, rather than focus on cost‐side effects of sabotage undertaken by the integrated firm, we instead consider demand‐reducing sabotage with product valuation effects. The two reasons driving this choice are: (a) a product valuation‐sabotage link in our setting captures user effects of sabotage; and (b) the insights using a valuation‐sabotage link also hold for the cost‐sabotage linkages except that the under the latter setting, the integrated firm is more likely to engage in sabotage.

The key contributions and insights we offer are as follows. We find that the integrated firm’s optimal sabotage strategy is strongly dependent on a firm’s relative cost advantage in both markets. This relative cost advantage increases as the integrated firm’s marginal cost is lower than that of its non‐integrated rivals and decreases in the degree of product differentiation in the two markets. The integrated firm will engage in multi‐market sabotage when the integrated firm’s overall relative cost advantage is high; it will engage in single‐market sabotage when the relative cost advantage is moderate; and will not pursue sabotage as an option when the relative cost advantage in both markets is small or non‐existent. We also find that if the integrated firm chooses to engage in sabotage, it will experience demand increases for its combined product offering but will also incur reduced demand for the mixed product combinations. Single‐market sabotage enables the integrated firm to increase prices in the sabotaged market, but it has to reduce prices in the other market. Thus, sabotage is a double‐edged sword and has countervailing effects on the integrated firm’s demands and profit margins.

Our findings also have some relevance for the net neutrality debate from the perspective of firm integration and sabotage. Net neutrality is a multi‐faceted worldwide debate that’s been going on for more than a decade. This study does not attempt to provide any definitive solution on whether to enforce net neutrality or not. Instead, this paper offers additional insights for this debate from the unique perspective of cross‐market integration and sabotage. For example, our findings suggest that cross‐market integration and the integrated firm’s potential sabotage activities could in extreme situations force certain product combinations out of the market. On the other hand, we also find that under certain other conditions, sabotage actions undertaken by the integrated firm could be socially optimal.

Finally, from a policy perspective, we provide some unique insights. In a Stackelberg leader‐follower setting with the integrated firm as the market leader, sabotage actions to optimize integrated firm profits tend to result in a loss of social welfare. Investigating optimal sabotage levels from the perspective of the regulator (i.e., those that optimize social welfare), we find that in certain “regions” (defined by the relative cost advantage for the integrated firm as compared to the non‐integrated firms) both the regulator and integrated firm will choose the same sabotage strategy. This (i.e., identical optimal sabotage decisions from the perspectives of the regulator and integrated firm) leads to the paradoxical result that sabotage as an option is not always detrimental to social welfare.

The remainder of this study is organized as follows. In the next section, we review the related literature. In section 3, we present the modeling framework of cross‐market integration and analyze the no‐integration case as a benchmark. Following that, in section 4, we analyze the equilibrium results of cross‐market integration with and without the sabotage option. Section 5 provides a social welfare analysis and discusses policy implications of our analysis. Section 6 analyzes two extensions of the main model—the simultaneous pricing game and game with incomplete information. Finally, conclusions and insights are discussed in section 7.

Literature Review

This study draws upon prior work in sabotage and integration, and bundling. In the area of sabotage and integration, prior research investigates whether a monopolist should sabotage the actions of downstream firms (i.e., a vertically integrated supply chain setting). Our focus is on a few key papers in this stream of work (for a recent overview, the reader is referred to Mandy et al. (2016)). Economides (1998) finds that an upstream monopolist always has an incentive to raise downstream rivals’ costs through sabotage activities while Sibley and Weisman (1998) shows that a regulated upstream monopolist may not always prefer to sabotage its downstream rivals and instead might prefer to lower rivals’ costs. Mandy (2000) finds that the upstream monopolist may refrain from sabotage when its downstream rivals are more cost efficient and its upstream profit margin is sizable. The setting investigated by Beard et al. (2001) is of a dominant firm and a competitive fringe in the upstream market and two downstream firms providing differentiated products engaging in price competition. The key finding is that the incentive for vertical integration always exists but the integrated firm will sabotage the downstream rival only when there is an input price regulation in the upstream market. Finally, Sappington and Weisman (2005) study a vertically integrated producer’s incentives to self‐sabotage and show that under certain market conditions, the vertically‐integrated producer has the incentive and the ability to disadvantage its downstream rivals differentially through symmetric cost increases or quality reductions for all rivals.

Product bundling strategies have been studied extensively in economics and marketing. Stremersch and Tellis (2002) and Venkatesh and Mahajan (2009) provide excellent overall reviews of the bundling literature. Most of the literature in this stream examines a monopoly firm’s bundling strategy in light of its own products offerings by comparing pure components, pure bundling, or mixed bundling pricing strategies to identify conditions when mixed bundling or pure bundling is optimal (Adams and Yellen 1976, Armstrong 1999, Bhargava 2013, Fang and Norman 2006, Whinston 1990). These results show that firms can use bundling discounts as a price‐discrimination tool. Research in bundling which has analyzed a similar setting to ours are those by Matutes and Regibeau (1992), Gans and King (2006), and Mialon (2014). Matutes and Regibeau (1992) studied duopoly competition in two product markets and show that mixed bundling is mutually unprofitable for the duopoly firms. Their focus was studying the bundling decisions of two integrated firms in each product market. Gans and King (2006), comparing bundling decisions of a co‐branded firms in two unrelated product markets with that of an integrated firm, find that bundling is profitable only when one pair of firms integrate competing with a non‐integrated pair, and if both pairs of firms integrate they will not offer bundled‐discount due to intense price competition. Mialon (2014) investigated whether firms will choose to integrate or form a strategic alliance and whether they will bundle their products. Their key result is that mixed bundling is not profitable and firms can do better with pure bundling.

If we consider an integrated firm in a two‐product complementary market, the key conceptual difference between bundling and sabotage actions is that in the former, the integrated firm discounts its own product combination offering while sabotage actions represent disincentives for consumers to purchase the non‐integrated firms product in combination with that of the integrated product. From an operational perspective, this leads to two distinct settings where under bundling, the discounting factor not only impacts sales of the integrated firm’s products but also its profit margin, while under sabotage, only sales of the integrated firm’s products are impacted. Hence, sabotage as the focal point of this research, is a completely different strategy choice from bundling.

Our study is related to these streams of work in the following ways. First, the sabotage literature investigates a vertically integrated setting and thus, sabotage actions are directed at a single market. Since there are also firm integrations across complementary product markets, we shift our focus to such a setting. In such a market setting, the integrated firm’s choices for sabotage encompass more than one market. Second, in the existing literature, the integrated firm’s sabotage activities are modeled in one of two ways—demand‐reducing sabotage (Crémer et al. 2000, Laffont and Tirole 2010, Mandy and Sappington 2007, Rubinfeld and Singer 2001, Sappington and Weisman 2005) and cost‐increasing sabotage (Beard et al. 2001, Economides 1998, Mandy 2000, Mandy and Sappington 2007, Mandy et al. 2016, Sappington and Weisman 2005, Sibley and Weisman 1998, Weisman and Kang 2001). When firms compete with each other through prices as modeled in our study, demand‐reducing sabotage has been shown to be often unprofitable while cost‐increasing sabotage has been shown to be profitable (Mandy and Sappington 2007). In our study, we adopt the more conservative approach of modeling the integrated firm’s sabotage activities as demand‐reducing sabotage. Specifically, the integrated firm may reduce the valuation of the product combination involving a rival’s product. This allows us to identify market conditions under which demand‐reducing sabotage is profitable for the integrated firm. Third, we follow the general approach adopted in prior research on bundling and sabotage (see e.g., Economides 1998, Gans and King 2006, Mandy and Sappington 2007, Mandy et al. 2016) by analyzing a Stackelber leader‐follower game setting reflecting cases where the integrated firm commands greater market power than it non‐integrated rivals. We also extend our analysis to a simultaneous game setting to analyze cases where market power differences between the integrated firm and its rivals are small or non‐existent.

In the next section, we present our modeling framework and analytically characterize our benchmark setting with no integration.

Modeling Framework

Preliminaries

We consider a stylized setting to analyze cross‐market integration and sabotage. There are two complementary products A and B (e.g., Internet access services and online content; and mobile devices and carrier services) and consumers need to consume both to derive any utility. In each product market, there are two competing firms, denoted by A0 and A1 (B0 and B1), both offering product A (product B). Since products A and B are complements, there are four product combination choices that consumers can choose from—A0B0, A0B1, A1B0, and A1B1. 6 In this setting, cross‐market integration refers to the case when one firm from market A and one firm from market B integrate.

Consumers are heterogeneous in terms of their preferences for the two individual products within a product combination. We capture this consumer heterogeneity using a two‐dimensional Hotelling model. In each market, the two competing firms’ products are located at the end points of a unit line, with A0 (B0) at point 0 and A1 (B1) at point 1; consumers are uniformly distributed along the unit line and incur a unit misfit cost t. 7 Hence, consumers’ overall preferences for product combinations can be specified as a uniform distribution on a unit square. These unit misfit cost t can also be interpreted as the degree of product differentiation, that is, a higher t implies greater differentiation with less intense competition.

Consumers are assumed to have a unit demand and share a common gross valuation v for a product combination. Following prior research using a Hotelling framework, we assume that consumers’ common gross valuation v is high enough such that the market is fully covered, that is, all consumers purchase a unit of product in each market. This results in complete market coverage and enables us to eliminate the impact of market expansion on firms’ pricing and sabotage decisions, and instead focus on the effect of firm competition.

When all four firms operate independently (i.e., no integration), each firm (indexed by ij for i = A, B and j = 0, 1) incurs a variable production cost of

Within the assumed market structure, the degree of product differentiation (t) and the integrated firm’s cost advantage (

Summary of Notation

Summary of Notation

To ensure that all firms capture a positive market share in equilibrium in the no‐integration case, we assume that

No Integration—Benchmark Setting

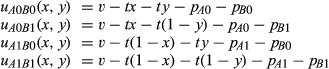

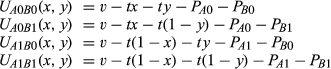

Given the market setting described above, a representative consumer located at (x, y) obtains the following net utilities for each product combination:

Pairwise comparisons of the net utilities for the four product combinations yield the following indifference points:

The market demands based on these indifference points are illustrated in Figure 1.

Market Demand for Each Product Combination in the No‐integration Case

Consumers who prefer A0’s product are located to the left of

When all four firms operate independently (i.e., no integration), the equilibrium prices are

Lemma 1 indicates that a firm’s price increases not only in its own marginal cost but also in its rival’s marginal cost. In each market, the efficient firm (with lower marginal cost) charges a lower price but earns a higher profit margin, gains a higher market share, and realizes a higher profit in equilibrium. When products offered in each market are more differentiated (i.e., higher t), consumers become more loyal to their preferred products. For the efficient firm, winning the rival’s customers through a lower price becomes less effective. Consequently, both firms in the market increase their prices and focus more on their own customers. Therefore, price competition is relaxed for a higher degree of product differentiation. In both markets, through offering a competitive price, the efficient firms can obtain some of their rivals’ less loyal customers who opt for price savings at the expense of incurring a higher misfit cost. As firms’ cost asymmetry increases (i.e., higher

With this characterization of the benchmark no‐integration setting, the focus now shifts to the analysis of integration with and without the sabotage option. To start, note that there are four possible integration scenarios: The Efficient‐Efficient integration: the integrated firm has a cost advantage in both markets, that is, The Efficient‐Inefficient integration: the integrated firm has a cost advantage in the market for product A and a cost disadvantage in the market for product B, that is, The Inefficient‐Efficient integration: the integrated firm has a cost disadvantage in the market for product A and a cost advantage in the market for product B, that is, The Inefficient‐Inefficient integration: the integrated firm has a cost disadvantage in both markets, that is,

In the next section, we conduct the equilibrium analysis for all of these integration scenarios.

Equilibrium Analysis of Integration

Merger and acquisition negotiations are usually confidential (even though one or both firms involved in such an activity might reveal the possibility within financial markets) and integration occurs provided both firms conclude negotiations successfully. In this study, we assume that this is the case and, without loss of generality, firms A0 and B0 have decided to integrate. For each of the four possible integration scenarios, we use similar notation as before except that all lowercase letters for key variables are now replaced by uppercase letters.

It is likely that given the confidentiality of the merger and acquisition process, firms that decide to integrate will also make strategic decisions including those on prices and sabotage activities, prior to publicly announcing the integration. This leads us to adopt a Stackelberg setting where the integrated firm (i.e., A0‐B0) is the first mover with the non‐integrated competing firms (i.e., A1 and B1) as followers. Although a Stackelberg setting might be construed as one where the integrated firm has a significant advantage over its independent competitors, this is not always the case. For example, Gal‐Or (1985), Tirole (1988), and Jiang and Katsamakas (2010) show that a firm in a Stackelberg pricing game often earns a higher profit when it acts as the second mover rather than as the first mover. Thus, our assumed Stackelberg setting is driven by the fact that it reflects practice rather than provides a competitive advantage to the integrated firm. For completeness, analysis for the simultaneous (rather than Stackelberg) pricing game is presented in section 6.

In the next two subsections, we analyze the integration game first without the sabotage option and then with the sabotage option.

Integration without the Sabotage Option

For a representative consumer (x, y), her net utilities for the four product combinations are the same as those for the benchmark no‐integration case:

Thus, the resulting demands for the four product combinations are

When A0 and B0 integrate, in the first stage, the integrated firm chooses its prices

When the integrated firm acts as the price leader in a Stackelberg pricing game without the sabotage option, there is always incentive for integration and the equilibrium prices are

Lemma 2 shows that as expected, the integrated firm (i.e., the leader) charges a higher price than in the no‐integration case. In response to the integrated firm’s higher prices, independent firms (i.e., the followers) in both markets also increase their prices. In other words, price competition is dampened. However, the relative price increase for the followers is less than that for the leader. Not only is the total profit of the integrated firm higher than the sum of the two firms’ profits before integration, the independent firms also realize a higher profit. Thus, if the integrated firm can act as the price leader and engage in a Stackelberg pricing game with other firms, there is always an incentive for integration. Consequently, consumers are subject to higher prices after integration.

In the next subsection, we study the case in which the integrated firm makes both pricing and sabotage decisions.

Integration with the Sabotage Option

If the integrated firm chooses to engage in sabotage, it is assumed that this will reduce consumers’ valuation for a mixed product combination which includes one of the integrated firm’s products and one of the competing non‐integrated firms’ products, that is, product combinations A1B0 or A0B1.

9

Integrated firm A0‐B0 has the option of either engaging in sabotage in the market for product A, or the market for product B, or both markets. Following prior studies in sabotage (Beard et al. 2001, Economides 1998, Mandy 2000, Sibley and Weisman 1998), we assume that sabotage does not accrue any direct costs.

10

For a representative consumer located at (x, y), her net utilities for the four product combinations are:

Pairwise comparisons of the net utilities for the four product combinations yield the following indifference points:

The resulting demand for each product combination is shown in Figure 2 and given by

Demands and Direct Effect of Sabotage on Demands

In the first stage, the integrated firm sets the sabotage levels (

Subsequently, independent firms A1 and B1 set their prices

To better understand the tradeoffs in making sabotage decisions by the integrated firm, we explore various effects of sabotage in the next three lemmas. Lemma 3 summarizes the direct effects of the integrated firm’s sabotage levels on demands.

When the integrated firm sabotages its rival in market A (B), the direct effect of sabotage on its demands is two folds: gaining new consumers in market A (B) but losing some existing consumers in market B (A), that is,

As shown in Figure 2, the change in the indifference point for each product combination indicates the direct impact of sabotage. When the integrated firm sabotages its rival in market A, that is, sabotaging A1 through

To summarize, the integrated firm’s sabotaging behavior has countervailing effects: sabotaging rivals’ products may help the integrated firm increase sale of its own product combination A0B0, but at the same time reduce sales of its own products A0 and B0 as sales of the mixed product combinations A0B1 and A1B0 decreases. Another interesting observation is that sabotaging in both markets through

In addition to the direct effect on demands, sabotage also affects firms’ prices indirectly in an intricate way, which is summarized in Lemma 4.

The indirect effect of sabotage on prices has the following properties: When the integrated firm’s sabotage level in market A (or B) increases, ‐ the price of the integrated firm’s A (or B) product increases, that is, ‐ the price of the integrated firm’s B (or A) product decreases, that is, ‐ the combined price of the integrated firm’s products A and B decreases, that is, When both Indirect Effect of Sabotage on Prices

As shown in Lemma 4, when the integrated firm sabotages its rival in market A, that is, sabotaging A1 through

When the integrated firm engages in multi‐market sabotage, that is, sabotage A1B0 through

While Lemma 3 characterizes the direct effect of sabotage on the individual product demands without considering the impact on prices, Lemma 5 details the full effect of sabotage on the integrated firm’s combined demand from both markets considering the impact on prices.

Factoring in the indirect effects of sabotage on prices, the full effect of sabotage on the integrated firm’s combined demand from products A and B can be either positive or negative depending on the integrated firm’s overall relative cost advantage Full Effect of Sabotage on the Combined Demand

Lemma 5 shows that for the integrated firm, sabotaging A1 through

Since the integrated firm competes in both A and B markets, it will maximize its total profit from both markets. This implies that there is a need to consider simultaneously the total sabotage level and the allocation of the total sabotage across the two markets. Thus, we can transform the integrated firm’s sabotage decisions on

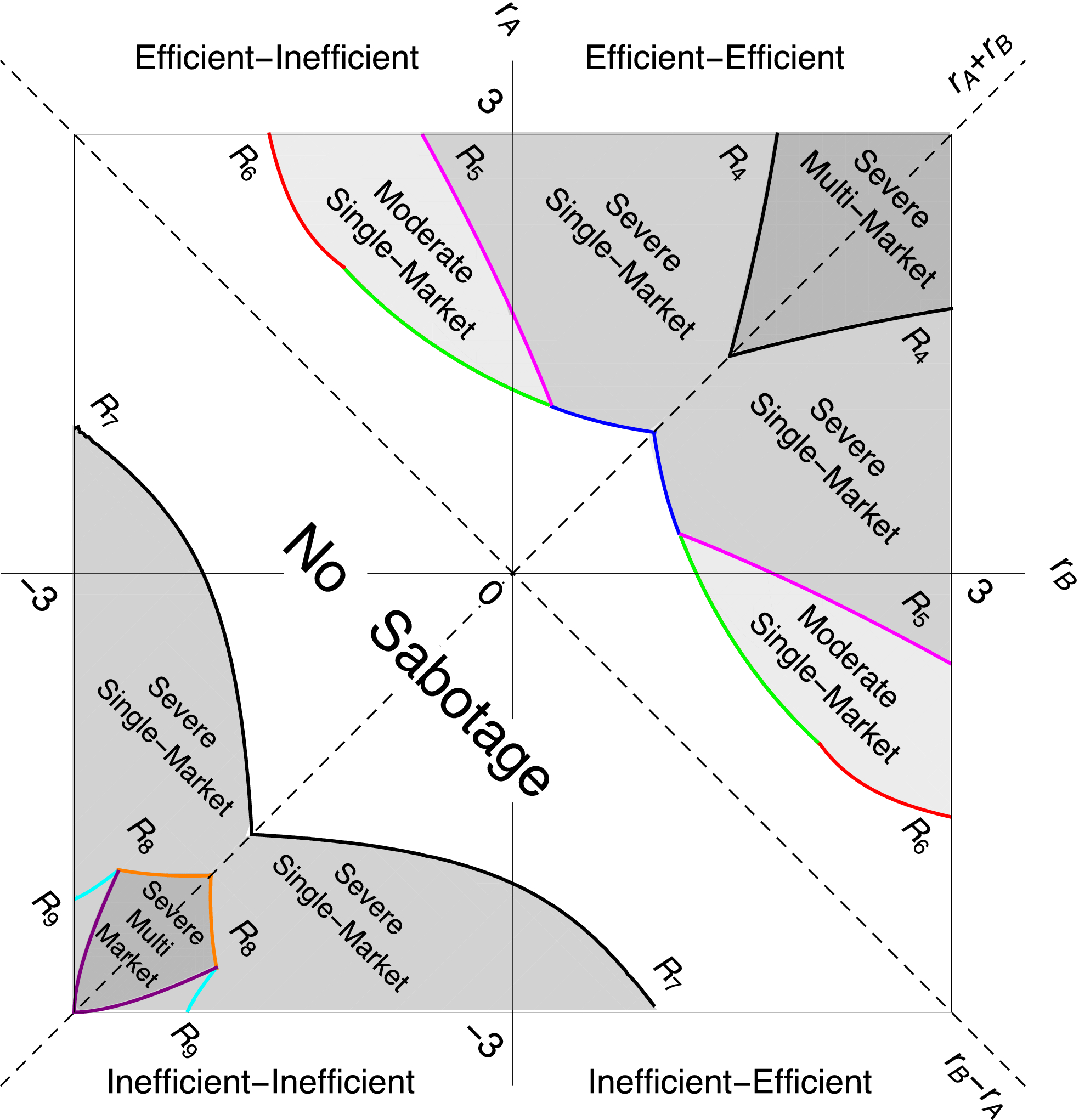

Under cross‐market integration, the integrated firm will Engage in severe multi‐market sabotage that drives product combinations A1B0 and A0B1 out of the market, that is, Engage in severe single‐market sabotage that drives either product combination A1B0 or A0B1 out of the market, that is, Engage in moderate single‐market sabotage, that is, Not engage in sabotage, that is, Equilibrium Sabotage

Analytic formulas for equilibrium sabotage, prices, profits, and thresholds

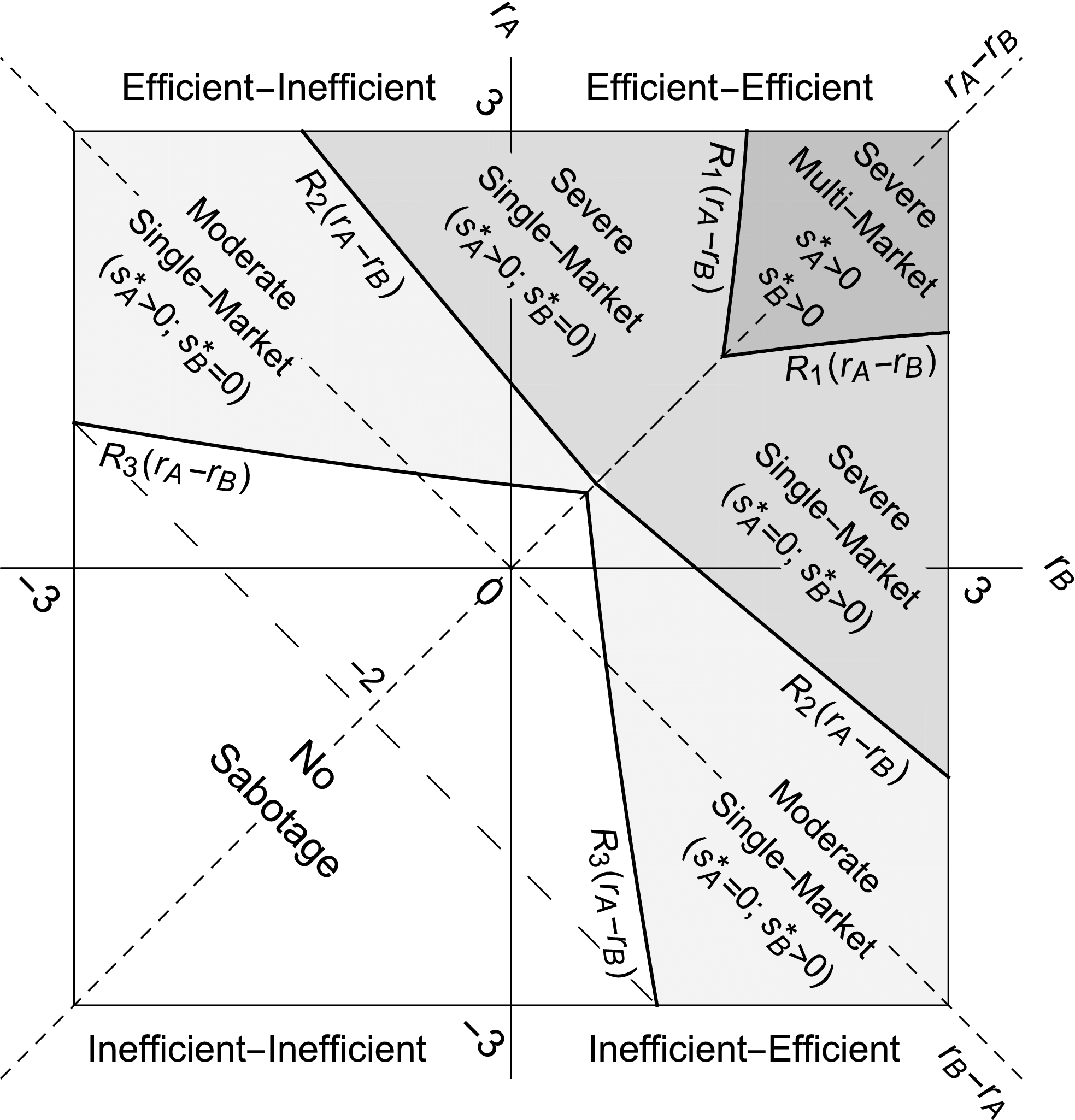

Proposition 1 shows that there are four possible equilibrium sabotage results and their separating criteria are defined by

Equilibrium Sabotage

As shown in the shaded regions in Figure 3, when the relative cost advantages of the two markets become more asymmetric (i.e.,

Equilibrium Demands with Integration and Sabotage

In the region above the curve

The region in between the curves

When the integrated firm’s relative cost advantage asymmetry in the two markets (

As

The intuition behind the results shown in Figure 4d for the no sabotage case is as follows. The region below the curve

In the next section, we analyze the integration game with the sabotage option from a social planner’s perspective.

Social Welfare Analysis

In this section, we first characterize the optimal sabotage decision from a social planner’s perspective. This is followed by a comparison between these decisions and those driven by the integrated firm with a view to provide policy implications.

Socially Optimal Sabotage

To analyze this scenario, we consider a three‐stage process. In the first stage, the social planner chooses sabotage levels (

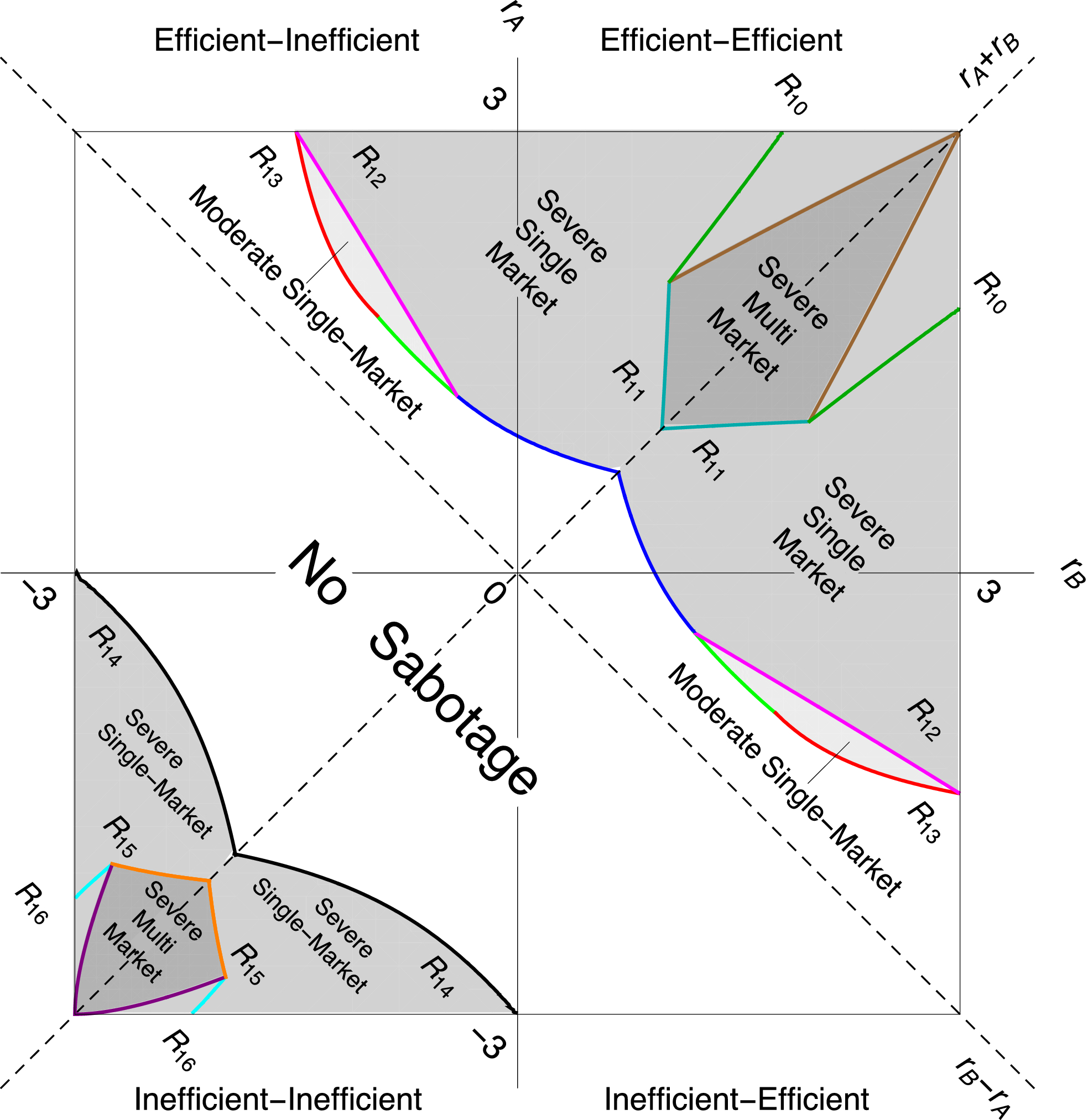

Using backward induction, we solve for the socially optimal sabotage decisions. The results are summarized in Proposition 2 and illustrated in Figure 5.

Socially Optimal Sabotage [Color figure can be viewed at

Under cross‐market integration, the social planner will prefer Severe multi‐market sabotage ( Severe single‐market sabotage ( Moderate single‐market sabotage ( No sabotage (

The social welfare levels and the definitions of thresholds

As shown in Figure 5, when the integrated firm’s overall relative cost advantage (

Policy Implications

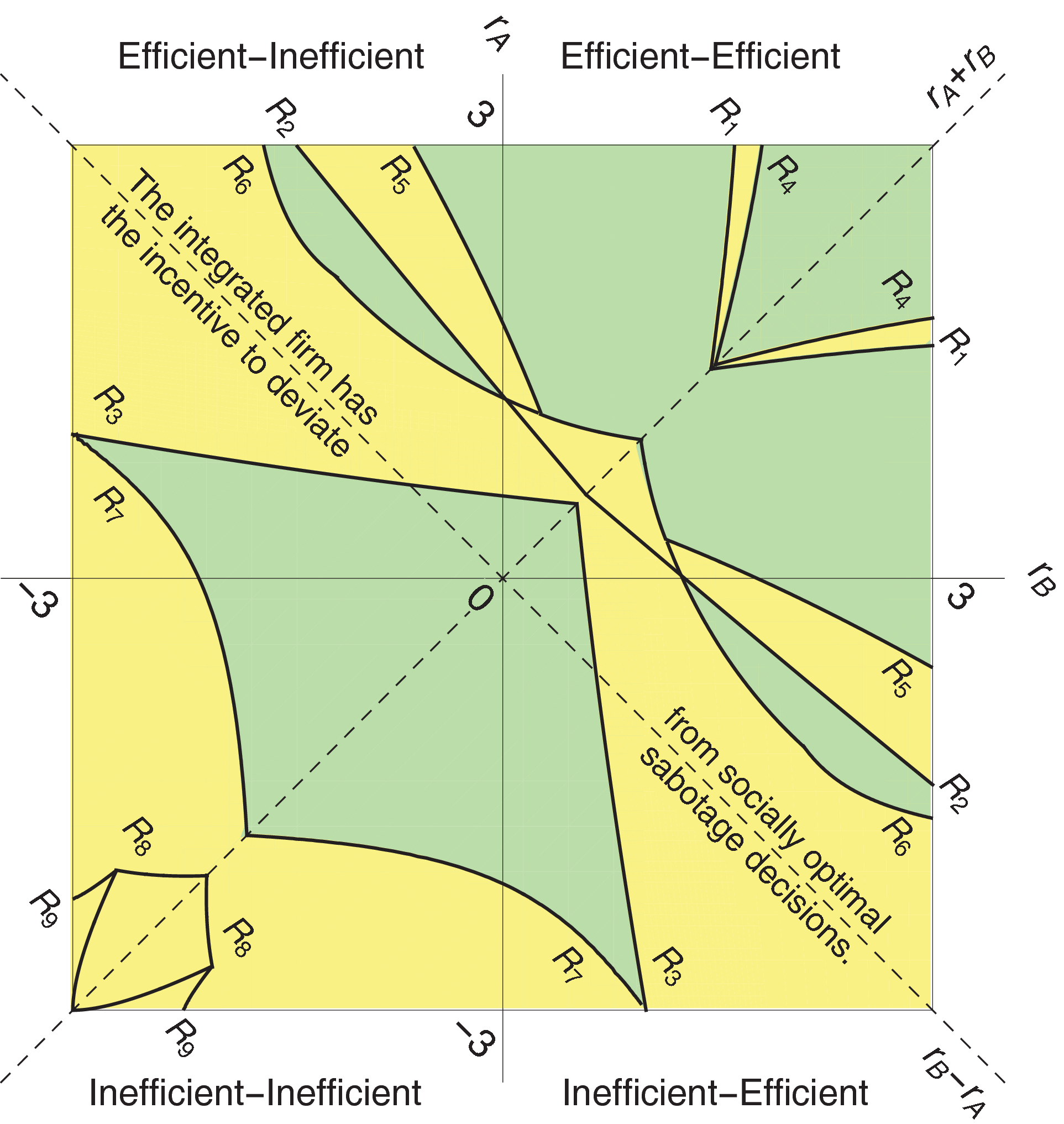

In order to provide policy implications, we start by comparing the equilibrium sabotage results from section 4.2 and the socially optimal sabotage results from section 5.1. The comparison results are summarized in Proposition 3 and illustrated in Figure 6.

Compare Equilibrium and Socially Optimal Sabotage [Color figure can be viewed at

The integrated firm’s sabotage decision coincides with the social planner’s in regions satisfying

Figure 6 illustrates regions of alignment and conflict between the equilibrium and the socially optimal sabotage decisions (green areas correspond to regions of alignment and yellow areas correspond to regions of conflict). The regions of conflict are of special interest because they represent the market conditions for potential regulatory intervention. The integrated firm may overuse or underuse sabotage to maximize its own profit at the cost of reducing social welfare. For example, the integrated firm prefers to undertake moderate single‐market sabotage under market conditions described by the curves

From a policy perspective, these results indicate that social planners need to closely monitor sabotage activities stemming from cross‐market integration. Instead of deploying uniform policy instruments for all integrations, it would be more appropriate to track changes in integrated firms’ operations vis‐a‐vis the non‐integrated competitors and then evaluate whether such changes lead to a reduction of social welfare. This is also reflected in practice when European regulators investigated potential abusive search manipulation practices by Google through market tests, leading to Google being fined a significant amount for such practices (Cendrowicz 2010, Fiveash 2016).

In the next section of the study, we discuss how these (and earlier) insights are moderated by examining two extensions.

Extensions

The focus of this section is to examine how the optimal sabotage decisions are moderated by the following: (a) analyzing a simultaneous game setting for cases where market power differences between the integrated firm and its rivals are small or non‐existent; and (b) consumer information on sabotage actions of the integrated firm. Each of these aspects is discussed in the next two sub‐sections.

Simultaneous Game Setting

The motivation for analyzing a simultaneous game setting stems from the fact that there might be situations where the differences in market power between the integrated firm and its rivals are not significant. The focus is to examining the extent of change in the prior insights derived for the Stackelberg leader‐follower game setting. The sequence of actions is: in stage 1, the integrated firm makes the sabotage decision; and in stage 2, all firms simultaneously set prices. Using backward induction, we start by solving the stage 2 problem for given levels of sabotage, and then using this characterization, we solve the stage 1 problem to determine optimal sabotage levels for the integrated firm. Proposition 4 summarizes the equilibrium results for the simultaneous pricing game.

When the integrated firm and the independent firms set their prices simultaneously, Even if the integrated firm has the option to sabotage its rivals in both markets, it does not have any incentive to do so in either market; The equilibrium prices under cross‐market integration are the same as those under no integration. Equilibrium Results of the Simultaneous Pricing Game

Proposition 4 shows that the integrated firm prefers not to sabotage its rivals in the simultaneous pricing game. The rationale behind this result lies in the effects sabotaging its rival in either market has on combined price and combined demand for the integrated firm. We find that sabotaging always leads to a lower combined price and sometimes leads to a higher combined demand. Furthermore, even in the presence of the combined‐demand‐increasing effect, the combined‐price‐decreasing effect dominates the combined‐demand‐increasing effect, leading to the no‐sabotage decision for the integrated firm. Note that under the simultaneous game setting, the integrated firm’s optimal pricing decisions are the same as those when they operate independently. This implies that if the integrated firm engages in a simultaneous pricing game with its competitors, there is no benefit or incentive to integrate.

How does the social planner’s perspective differ in this game setting? By analyzing the same setting as before except allowing for simultaneous pricing by all firms, the Proposition 5 details the social planner’s optimal choices to maximize social welfare.

Under cross‐market integration in the simultaneous pricing game, the social planner will prefer Severe multi‐market sabotage ( Severe single‐market sabotage ( Moderate single‐market sabotage ( No sabotage ( Socially Optimal Sabotage in the Simultaneous Pricing Game

The social welfare levels and the definitions of thresholds

Comparing the results of Propositions 4 and 5 (illustrated in Figure 7), we see that when firms engage in the simultaneous pricing game, the integrated firm tends to underuse sabotage to maximize its own profit at the cost of reduced social welfare. This misalignment happens when the integrated firm has either a high overall relative cost advantage or a high overall relative cost disadvantage. In such cases the social planner prefers to use sabotage as a tool to induce more consumption of cost‐efficient products.

Socially Optimal Sabotage in the Simultaneous Pricing Game [Color figure can be viewed at

Information Asymmetry

This extension explores how our current findings and insights are impacted if the integrated firm’s sabotage actions are not fully visible to consumers. The rationale underlying such an argument is that an integrated firm would not typically announce sabotage levels

Our approach to examining the impact of such information asymmetries is as follows.

11

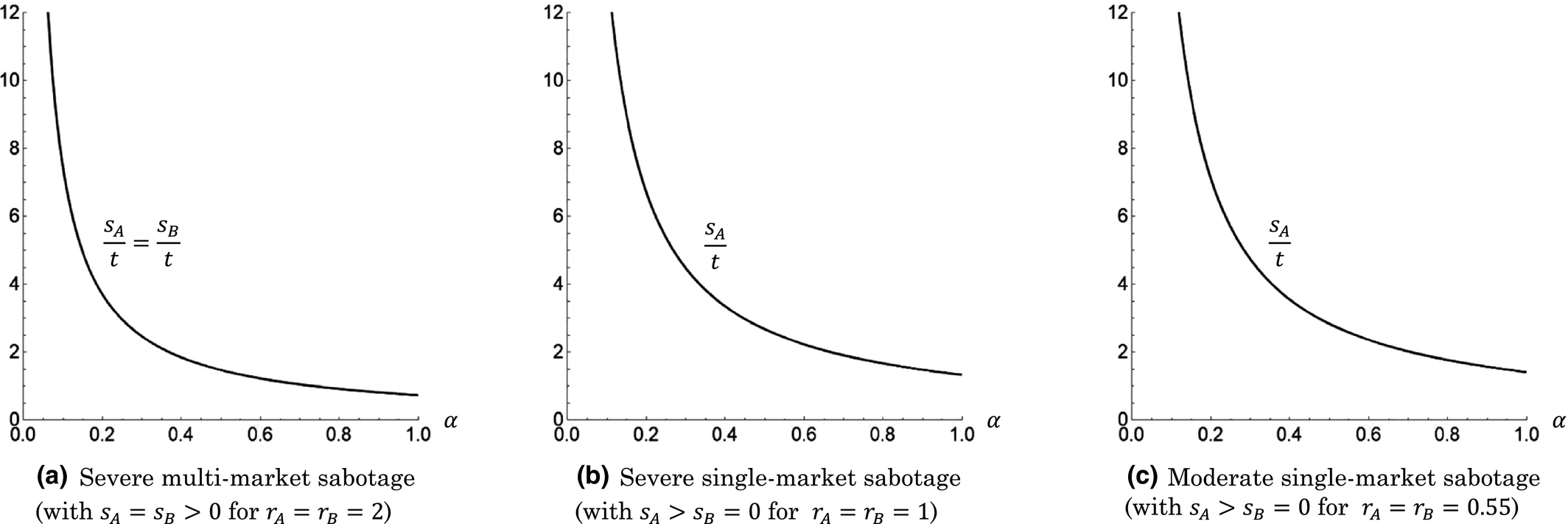

Define α ∈ (0, 1] as a parameter representing information asymmetry with higher levels reflecting less asymmetry and vice versa. Based on this, given the integrated firm’s sabotage decisions

Since information asymmetry in sabotage actions only leads to changes in consumer behavior without impacting the magnitude of integrated firm’s optimal profits, the revised optimal sabotage levels (

Impact of Information Asymmetry Parameter α on Sabotage Levels

Conclusions

Mergers and acquisitions of firms offering complementary products are well documented. Such cross‐market integration raises regulatory concerns of the possibility of multi‐market sabotage and its impacts on the competition in both markets and social welfare. This study examines the integrated firm’s incentive to engage in multi‐market sabotage and its impacts. It extends prior findings in the sabotage literature and provides policy implications in terms of competition and social welfare.

We find that although the integrated firm has the ability to sabotage its rivals in both markets, it should not always do so. When the integrated firm has a cost disadvantage in both markets, it does not have any incentive to sabotage. Sabotage (either single‐market or multi‐market) is preferable only when the integrated firm’s overall relative cost advantage is higher than a threshold. When its overall relative cost advantage is sufficiently high, the integrated firm may undertake sabotage activities that force some product combinations out of the market, leading to reduced product variety for consumers. We also show that even when the integrated firm has the incentive to sabotage, it does not always prefer multi‐market sabotage. Multi‐market sabotage is optimal only when the integrated firm has cost advantage in both markets and its overall relative cost advantage is very large. When its overall relative cost advantage is not as large, the integrated firm prefers single‐market sabotage. When the relative cost advantages of the two markets become more asymmetric, the integrated firm is more likely to engage in single‐market sabotage and less likely to engage in multi‐market sabotage. Under single‐market sabotage, sabotaging the market in which the integrated firm has a higher cost advantage is preferable. For example, when an integrated firm sells both hardware and software, our results suggest that the integrated firm is more likely to sabotage the hardware market because the cost advantage for hardware is usually higher than that for software. In the case of Microsoft selling both Xbox (game console) and Halo (the flagship game for Xbox), our results help explain why Halo is exclusively offered on Microsoft’s Xbox and not available on Sony’s PlayStation.

From the social planner’s perspective, we show that sabotage does not always hurt social welfare. In fact, the social planner may even encourage sabotage when two efficient firms integrate because more consumers will choose products offered by the more efficient firm (i.e., the integrated firm) due to sabotage. However, when comparing the preferences of the integrated firm and the social planner, we find market conditions under which the integrated firm may undertake excessive sabotage, which leads to a reduction in social welfare.

This suggests that when evaluating mergers and/or acquisitions, the regulator needs to carefully examine market conditions such as the integrated firm’s cost advantage and the intensity of competition in the two involved markets. Our findings suggest that when the integrated firm has a cost advantage in only one markets, regulatory intervention to restrict potential single‐market sabotage activities in that market would be required. When the integrated firm has a cost advantage in both markets and the markets are not sufficiently competitive, regulators should closely monitor the integrated firm to prevent over‐sabotage even though the firm’s sabotage decision often times coincides with regulators.

There are several avenues for extending our research. We assume that rivals of the integrated firm choose not to integrate (i.e., remain independent). However, these rivals in response to the integrated firm’s decision, might also choose to integrate. It would be of interest to examine whether sabotage would be an effective strategy in such a setting. From the firms’ perspective, we focus on analyzing the impact of various sabotage options (no sabotage, single‐market sabotage, multi‐market sabotage) on firms’ market shares and profitability. In certain cases, firms may consider other potential impacts related to sabotage. For example, not sabotaging may allow the integrated firm to test out their products so that a better integrated product can be offered later, e.g., delayed differentiation. Although we have explored the impact of information asymmetry in our analysis, it might be interesting to examine a two period setting where consumer decisions in the first period are made assuming no information on sabotage followed by a second period decision with full information on sabotage actions.

Another possibility is to extend our modeling framework to an oligopoly setting. Such an extension could provide different insights in the context of whether integration with sabotage is a preferred choice in the presence of more than two rival firms that do not pursue integration. Our analysis can also be extended to multiple complementary markets which will provide insights into the integrated firm’s incentive to engage in multilateral sabotage. It is worth noting that for markets that exhibit network externalities, the impact of sabotage activities for an integrated firm would still depend upon the complex trade‐off between the increase in demand and the corresponding decrease in margins. In essence, network externalities will exacerbate both the positive and negative effect of sabotage and while our key results would still hold, the precise equilibrium regions will of course, be different. A final issue of interest would be to explore how asymmetric consumer preferences in each market drive the sabotage decision. Although such and analysis is structurally intractable, it might be interesting to numerically explore how the sabotage strategy preference regions are moderated by the degree of asymmetry.

Acknowledgment

We thank the Department Editor, the Senior Editor and Reviewers at POM for their excellent guidance. Professor Vakharia’s research on this paper was supported through a Summer Research Grant awarded by the Warrngton College of Business at the University of Florida.

Footnotes

1

see

2

see

3

“..Xfinity TV will offer NBCUniversal’s Olympic content live and on‐demand, across multiple digital, mobile and tablet platforms, and for the first time ever, the Games will be available in 3D.” “We are excited to bring our Xfinity TV customers NBCUniversal’s coverage of every minute of every medal on every screen of the 2012 London Olympics,” said Matt Strauss, Senior Vice President, Digital and Emerging Platforms, Comcast Cable. “Through multiplatform Olympic‐themed search, tools and personalized features created to help our customers view and experience the events, we are providing a virtual passport to NBCUniversal’s comprehensive 2012 London Games programming.” (see

4

see

5

see

6

Consumer price for a product combination purchased is the sum of prices for the individual product offerings. This is distinct from the bundling literature where the firm offering the bundled product could enjoy a distinct price advantage over a firm offering the individual products.

7

Our assumption is that consumer preferences on both product offerings are symmetric and this is captured by this common unit misfit cost t on both dimensions. If however, we consider an asymmetric misfit cost

8

In this study, we capture firms’ efficiency asymmetry through their different marginal costs. Alternative model choices such as different consumer valuations of the competing firms generate similar results.

9

The reason for integrating the impact of sabotage as a value‐reduction action rather than a cost‐reduction action is twofold. First, cost‐increasing sabotage has no direct impact on market demand and instead forces rivals to increase prices and put them in an correspondingly disadvantaged position. In comparison, demand‐reducing sabotage has a more nuanced impact on all firms’ demands and prices, including the integrated firm, and may not even be a profitable strategy because of such complexities. Thus, as noted by Mandy and Sappington (![]() ), demand‐reducing sabotage has been shown to be often unprofitable while cost‐increasing sabotage has been shown to be profitable. Second, through an analysis of the integrated firm’s optimal sabotage strategy from a cost‐increasing perspective, we observe that cost‐increasing sabotage would lead to the extreme outcome in which the integrated firm captures the entire market. Hence, our approach is more conservative in comparison.

), demand‐reducing sabotage has been shown to be often unprofitable while cost‐increasing sabotage has been shown to be profitable. Second, through an analysis of the integrated firm’s optimal sabotage strategy from a cost‐increasing perspective, we observe that cost‐increasing sabotage would lead to the extreme outcome in which the integrated firm captures the entire market. Hence, our approach is more conservative in comparison.

10

In this study, we focus on examining the integrated firm’s incentive to engage in sabotage and do not consider its cost of undertaking such sabotage activities. Introducing sabotage cost in the form of fixed cost, or marginal cost, or both will simply reduce the parameter regions under which the integrated firm will sabotage and will not change our fundamental results.

11

An alternative approach is to focus on a two‐period model where in the first period, the integrated firm makes and executes sabotage decisions and consumers make their purchase decisions without knowing these decisions. In the second period, consumers become fully/partially aware of these sabotage decisions, and then make their second period purchase decisions.