Abstract

Motivated by Google’s technology specifications on Android devices, we consider firms’ decisions on production timing in a co‐opetitive supply chain comprising a manufacturer and an original equipment manufacturer (OEM), where the manufacturer acts as the OEM’s upstream contract manufacturer and downstream competitor. We consider the market acceptance uncertainty of key product designs. If a firm decides to implement ex post production strategy (PS), it can delay the production until the market acceptance uncertainty of its product is resolved. Otherwise, ex‐ante production strategy (AS) is implemented. We find that, due to the co‐opetition, PS does not always benefit either the manufacturer or the OEM, because the value of delayed production is diminished as the competitor may commit a production quantity earlier under AS. Further, firms’ decisions on production timing are dependent on the degree of market acceptance uncertainty of their products and competition intensity. We find that both firms choose PS when uncertainty is high, while only one of them chooses PS when uncertainty is moderate or low. Interestingly, when the competition is intense, the manufacturer tends to choose PS, which can benefit from both the resolved market acceptance uncertainty and OEM’s early commitment of production quantity.

Introduction

In recent years, many cell phone companies have outsourced their production to other manufacturers that also sell self‐branded phones. For example, Google outsourced the production of its phone, Pixel, to HTC (Wired 2016). Meanwhile, HTC produced its self‐branded phone and competed with Google in the consumer market. In this case, the manufacturer becomes both Google’s upstream partner and downstream competitor. This “co‐opetition” relationship (Brandenburger and Nalebuff 1996) has been observed among Google and Google’s other upstream manufacturers.

The competition and cooperation among original equipment manufacturers (OEMs) 1 and their competitive manufacturers have received attention in the operations management field. Previous studies have examined the supply chain parties’ strategic decisions and their incentives (e.g., selling or not selling self‐branded products) in different industries. For example, Lim and Tan (2010) and Wang et al. (2013) study electronics products. Chen et al. (2012) focus on the computer industry. Hsu et al. (2017) is motivated by the examples in retailing and logistics industries. In this study, we focus on the cell phone industry, particularly those phones with the Android operating system.

Since Android is open source, if firms customize their Android phones arbitrarily, it may expose Android to the risk of fragmented user experience. Therefore, Google tries to control hardware and software specifications to avoid such a risk by providing Android’s Compatibility Definition Document (CDD). 2 For example, the CDD requires the aspect ratio of a phone screen to be between 4:3 and 16:9. With these specifications, Google is able to ensure the “reliability and consistency” of the user experience on Android phones (Wired 2016). Furthermore, this CDD plays a significant role in the supply chain structure and manufacturers’ operational decisions.

Although Google provides the CDD, it is up to cell phone firms to decide whether they will follow the CDD. If a manufacturer decides not to follow the CDD, the firm may suffer from significant uncertainty in market acceptance because Android’s CDD is designed according to mainstream preference and is well known among enthusiastic Android fans. For example, in 2014 Amazon launched its Fire Phone running on a heavily customized Android operating system. This system is against many CDD specifications (e.g., it introduced a 3D display that is not part of the CDD). Two months after its release, Amazon was reported to have $83 million worth of unsold Fire Phones in its inventory (Time 2014). Having said that, not following the CDD is not necessarily a bad thing, because possible innovations could bring significant profits. For example, in 2016 Xiaomi launched Mix, an Android‐based phone with a bezel‐less and fillet‐cutting design as well as a screen aspect ratio of 17:9, which are all against the CDD specifications. This phone made “full screen” a hot trend in 2017 (Wired 2017). Therefore, it is a manufacturer’s strategic decision on whether or not to follow the CDD, especially in a co‐opetitive setting. In the example of HTC, Pixel was made exactly according to Google’s specifications (Wired 2016), whereas HTC saw non‐compliance in designing its self‐branded phone, e.g., HTC U11+ with a full screen (Gsmarena 2017).

Further, manufacturers’ decisions on whether to follow the CDD can also affect their production timing, which is closely related to market acceptance uncertainty. Companies can make their production quantity decisions either before or after they learn the market acceptance of a certain product design. Some companies choose to postpone the production decisions until they are fully aware of the uncertainty of market acceptance, which is referred to in this study as ex post production strategy (PS). For example, HTC released its “full screen” phone U11+ in late 2017 after “full screen” became a trend (Gsmarena 2017). Similar strategies were observed in Huawei’s launch of its first “full screen” phone, Maimang 6 (China Daily 2017), and in its development of the related technology in 2018 (LetsGoDigital 2018). By contrast, some companies, such as LG and Xiaomi, choose to produce early and face the market acceptance uncertainty (BBC 2017, Wired 2017), which is referred to in this study as ex‐ante production strategy (AS). Table 1 displays the main features from the motivating examples.

Main Features from Practice

Main Features from Practice

With a co‐opetitive supply chain comprising an OEM and a manufacturer, we investigate: (i) how the difference in market acceptance uncertainty affects co‐opetition between the OEM and manufacturer as well as their production timing decisions; and (ii) the manufacturer’s incentive to follow the OEM’s specifications in the co‐opetitive setting and the resulting effect.

We find that, both market acceptance uncertainty and competition intensity play critical roles in firms’ strategic choices between AS and PS. In the presence of competition, adopting PS does not always benefit a firm. This is because the firm that makes production decision first enjoys the first‐mover advantage (referred to as “commitment value” in the literature (Cvsa and Gilbert 2002, Roller and Tombak 1993, Spencer and Brander 1992, Wang et al. 2014a)). Intuitively, when a firm faces low market acceptance uncertainty, the commitment value may offset the value of information from PS (referred to as “information value”). However, with the co‐opetition between the OEM and manufacturer, we further find the following: When both firms face low uncertainty, one firm chooses AS and the other chooses PS in equilibrium (i.e., a sequential equilibrium). The underlying reason is that both firms’ early commitment values disappear if they choose AS simultaneously (i.e., a simultaneous equilibrium), and their differences in market acceptance uncertainty and source of profits result in a sequential equilibrium. In contrast, both firms choose PS when they face high uncertainty. This implies that market acceptance uncertainty determines the nature of competition and cooperation between the OEM and the manufacturer. In a simultaneous equilibrium, the manufacturer and the OEM choose the same strategy, and thus competition is intensified. Alternately, in a sequential equilibrium in which one firm chooses AS to seize early commitment value and the other firm chooses PS to obtain information value, the competition between two firms is softened. Overall, low uncertainty results in less competition in a sequential equilibrium. When uncertainty of the two firms is moderate, their preference over AS/PS is determined by competition intensity. Intuitively, the OEM is more likely to choose AS due to its lower uncertainty (i.e., lower information value under PS). Consistent with this intuition, we find that the OEM chooses AS when competition is sufficiently intense. Interestingly, although firms’ information values from PS is significantly reduced by intense competition, the manufacturer still chooses PS in this case. This is because, in the co‐opetitive relationship, the manufacturer benefits from the spillover value of the OEM’s early commitment. When competition is not very intense, however, the opposite holds true (i.e., the OEM chooses PS and the manufacturer chooses AS). This occurs also due to the co‐opetitive relationship. The OEM’s commitment value, from AS in this case, is significantly reduced by a high wholesale price paid to the manufacturer for contract manufacturing. Conversely, for the manufacturer, adopting AS leads to significant commitment value because high profit is achieved through both contract manufacturing and selling self‐branded products.

With regard to the manufacturer’s incentives to follow the OEM’s CDD, we obtain the following findings. First, the manufacturer has no incentives to follow the OEM’s CDD when they both have high market acceptance uncertainty and the competition is not very intense. The manufacturer’s market acceptance uncertainty is decreased by following the CDD, and this can result in a sequential equilibrium in which the manufacturer chooses AS and the OEM chooses PS. However, when the market acceptance uncertainty is high, the early commitment value from AS cannot offset the loss of information value from PS for the manufacturer. Second, the manufacturer may have incentives to follow the OEM’s CDD when the OEM’s uncertainty is moderate, the manufacturer’s uncertainty is high, and the competition is sufficiently intense. In this case, by following the CDD, the OEM chooses AS, and the manufacturer may benefit from high information value in a sequential equilibrium as well as the spillover value from the OEM’s early commitment.

The remainder of this study is organized as follows. We briefly review the related literature in section 2. In section 3, we describe the model setup. In section 4, we analyze firms’ strategic choices between AS and PS for the case in which the manufacturer does not follow the CDD, and in section 5, we analyze the case in which the manufacturer follows the CDD. The manufacturer’s decision on the CDD is investigated in section 6. Sections 7 and 8 provide extensions and conclusions.

Literature Review

Our work is related to the research that studies the value of waiting under demand uncertainty. Cachon (2004) investigates how order/production timing influences the allocation of inventory risk and hence supply chain efficiency. In his model, an early (a late) order is allowed before (after) demand is observed under a push (pull) contract, and inventory risk is born by the retailer (supplier). He also designs an advance‐purchase discount contract that better allocates the value of waiting under demand uncertainty, wherein the inventory risk is shared by the retailer and supplier. Similarly, Dong and Zhu (2007) study the impact of pull, push and advance‐purchase discount contracts on supply chain performance and identity Pareto improvement opportunities for the supply chain parties. Swinney et al. (2011) formulate the competition between an established firm and a start‐up by assuming the former is concerned with profit gains while the latter is concerned with the probability of survival. If firms produce late until demand uncertainty is resolved, they can benefit from the value of information. They identify equilibrium where the start‐up produces early while the established firm produces late. Chen and Xiao (2012) investigate the value of forecasting accuracy improvement in a three‐tier supply chain, and they find that the reseller’s improved accuracy is beneficial to both the manufacturer and the reseller under a wholesale price contract. Wang et al. (2014a) study two identical quantity competitors and their efficient‐responsive choices. An efficient firm produces early while a responsive firm produces late. Wang et al. (2014b) analyze firms’ decisions on timing of order (before or after demand is realized) in a three‐tier supply chain comprising an OEM, a contract manufacturer, and a supplier, by using two procurement outsourcing structures: control and delegation. Choi (2018) considers a fashion supply chain comprising an upstream make‐to‐order manufacturer and a downstream risk‐averse retailer. By comparing the slow‐response (early production) case with the quick‐response (late but responsive production) case, he investigates the impact of risk aversion on the quick‐response system and finds that the retailer benefits from later production due to a better demand forecast. Choi et al. (2018) and Choi (2017) further explore the value of quick‐response by considering a stochastically risk sensitive retailer (i.e., the retailer’s risk preference may vary from time to time) and a boundedly rational retailer, respectively. The forgoing works are mainly based on newsvendor‐typed models, which emphasize production quantity decisions under demand uncertainty, but lack the supply chain parties’ cross interactions when they make decisions. The only exception is Wang et al. (2014a), where symmetric competition models and the value of production timing are investigated. Our work is therefore mostly close to Wang et al. (2014a), but we consider a co‐opetition structure between the OEM and the manufacturer as well as their differences in market acceptance. We find that the firms’ AS/PS choices are fundamentally determined by their co‐opetitive relationships and market acceptance uncertainty.

Our work is also related to the literature on product design innovation. This stream of literature is comprehensively reviewed in Krishnan and Ulrich (2001). Most of the papers in this stream focus on cost‐reduction effect of production process innovation within a single firm. There has been recent growth in the literature considering the vertical interactions among supply chain parties. For example, by focusing on new product development, Bhattacharya et al. (1998) study firms’ product definition timing decisions (i.e., early definition to take advantage of low costs, or delayed definition to ensure a better fit to consumer preferences) in highly dynamic environments. Gilbert and Cvsa (2003) study product innovation interactions between a supplier and a buyer in a supply chain, where the supplier can strategically pre‐commit pricing decisions to stimulate downstream innovation, or postpone decisions until demand uncertainty is resolved. Ülkü et al. (2005) investigate firms’ optimal timing decisions on technological innovation adoption, which is dependent upon competition intensity, cost structure, and forecast improvement. Wang and Shin (2015) consider a downstream manufacturer and an upstream supplier that invests in innovation, which improves the product quality, thus, increasing the consumers’ assessment of the product value. They study the impact of contract types and upstream competition on the supplier’s investment in innovation. Wang et al. (2018) explore an upstream technology supplier’s licensing decision in two different supply chain structures: (i) the supplier separately licenses its technology to a design firm and a manufacturer firm in a network supply chain, and (ii) the supplier licenses to a firm with both design and manufacturing capacities in a traditional integrated supply chain. Different from these papers’ cost considerations, our work focuses on the effect of product innovations on the degree of market acceptance in a co‐opetitive setting, and study how it influences firms’ production timing decisions.

There is a growing amount of literature on co‐opetitive supply chains. Spiegel (1993) shows that outsourcing production to a potential rival can reduce its incentives to develop self‐branded business. Arya et al. (2007) study a single‐OEM, single‐supplier Cournot competition model, demonstrating that supplier encroachment can achieve better performance of both itself and the OEM by reducing wholesale price and increasing downstream competition. Lim and Tan (2010) investigate the interactions between an OEM and its upstream contract manufacturer (CM), finding that the OEM’s high degree of brand equity can prevent the CM from entering the market. Chen et al. (2012) examine the OEM’s sourcing decisions in the presence of a competing CM. Wang et al. (2013) consider a co‐opetitive supply chain comprising an OEM along with a competitive CM acting as the OEM’s upstream partner and downstream competitor, and they examine the impact of quantity competition on their preference over leadership and followership. Niu et al. (2015) conduct a similar study under price competition. Compared with the forgoing works, differences of our work exist on both practical and theoretical sides. We note that previous works study problems such as supplier encroachment, entry deterrence methods, and cooperation incentives issues. Our study is motivated by specific observations from the practice in Android phone industries. We characterize the manufacturers’ strategies regarding the specifications compliance. This links the study of market acceptance uncertainty and production timing in a natural way. We also note that, previous works on co‐opetition focus on the profit comparison with and without co‐opetition. Differently, we study the players’ incentives toward demand uncertainty, production timing, and operational decisions under an existing co‐opetition framework.

Model Settings

The Structures of the Supply Chain and Market

Consider a co‐opetitive supply chain comprising an OEM (denoted as o, e.g., Google in our motivating example) and a manufacturer (denoted as m), who acts as both the OEM’s upstream partner and downstream competitor. The OEM outsources its production to the manufacturer who also sells self‐branded products. The OEM’s products and the manufacturer’s products are partially substitutable as we explain below. Let w denote the wholesale price (for per unit of product) that the manufacturer charges the OEM.

The OEM and the manufacturer engage in quantity competition with market acceptance uncertainty. The inverse demand function for firm i is given by

Assumption 1 states that the OEM and the manufacturer conduct product design independently and have exclusive access to a market acceptance signal (relaxing this assumption will not change our main intuitions; see section 7.3 for the analysis). Assumption 2 captures the difference in market acceptance uncertainty faced by the OEM and the manufacturer. As explained in the Introduction, the OEM’s CDD is based on mainstream preference. Hence, the products designed according to the CDD have low market acceptance uncertainty. This assumption is consistent with industrial practice. For example, International Data Corporation (IDC) reports that, the top two Android‐based phone manufacturers in China, Xiaomi and Huawei, face significant variations in market share performance (IDC 2017a,b). In contrast, Google’s sales growth in Pixel family was steady (VentureBeat 2018).

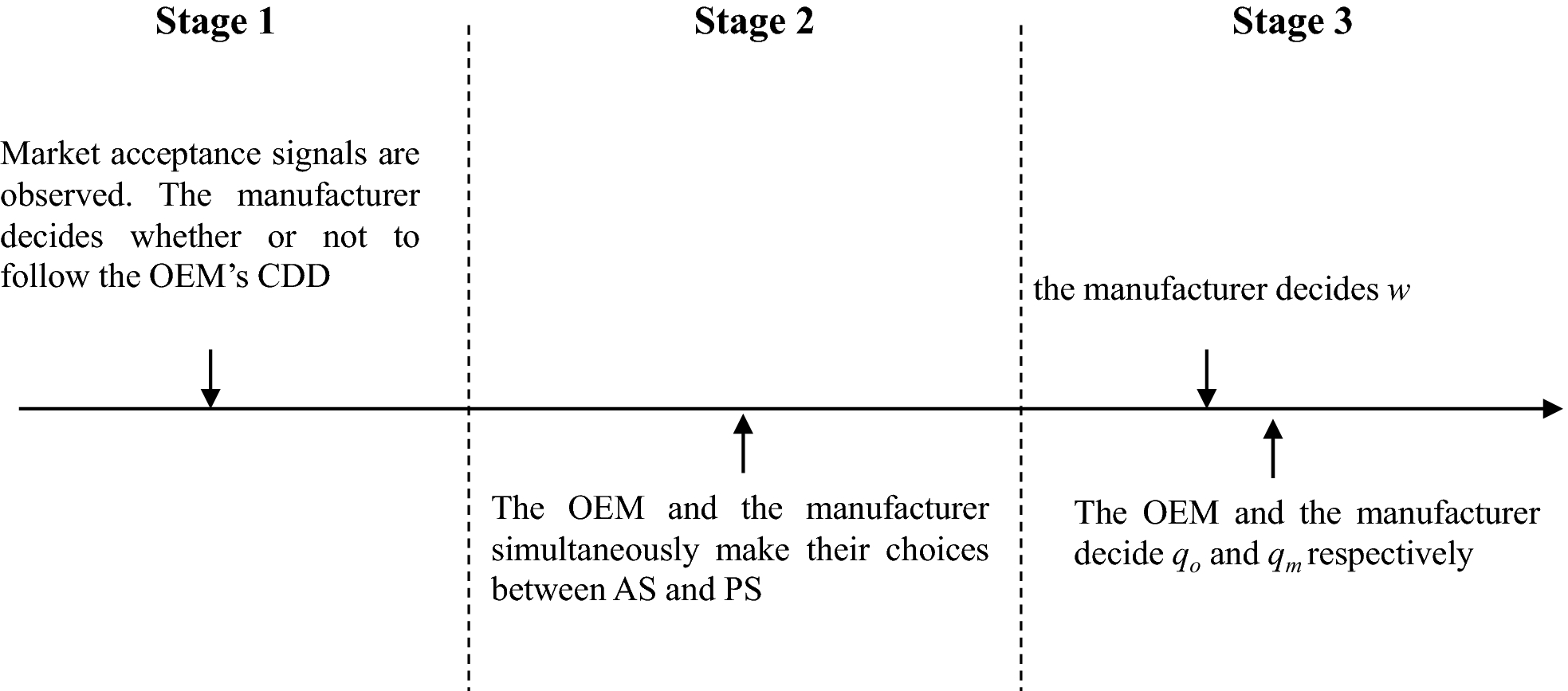

Three‐Stage Game

We consider that market acceptance uncertainty can be resolved after a certain time spot. Specifically, firms can make quantity decisions either at time 0 (i.e., adopting AS), or at time 1 (i.e., adopting PS). At time 0, the market condition noise The OEM and the manufacturer observe their valuation of market acceptance uncertainty. The manufacturer decides whether or not to follow the CDD. The OEM and the manufacturer simultaneously choose whether to implement AS (denoted as A) or PS (denoted as P);that is, they choose to make quantity decisions at time 0 or time 1. The manufacturer sets the wholesale price w. According to their choices on production timing, the OEM and the manufacturer set their quantity levels.

We formulate this problem as a three‐stage game. Figure 1 shows the sequence of events.

Sequence of Events

If the manufacturer does not follow the CDD, it designs the product and faces high uncertainty. The expected profit functions of the OEM and the manufacturer are, respectively,

We solve this game backwards. We first solve the third‐stage subgame (wholesale price and quantity decisions) for any given production timing choices in stage 2 and decision on the CDD of the manufacturer in stage 1. We then solve the timing decisions, and finally we solve the manufacturer’s decision on the CDD. To do so, in section 4, we solve the problems in stages 2 and 3 for the case in which the manufacturer does not follow the CDD, and in section 5, we analyze the case in which the manufacturer follows the CDD. In section 6, we compare the manufacturer’s profits in these two cases and obtain the manufacturer’s optimal decision on the CDD in equilibrium.

Since the OEM and the manufacturer engage in a simultaneous game if both of them implement AS or PS, and they engage in a sequential game otherwise, there are potentially four Cournot competition subgames in stage 3: a simultaneous game with uncertainty, a simultaneous game without uncertainty, a sequential game with the OEM as the Stackelberg leader, and a sequential game with the manufacturer as the Stackelberg leader. It is worth noting that, in a sequential game where one player enters early and the other waits, the early mover’s quantity is public information. For notational convenience, we let

Not Following the CDD (N)

In this section, we analyze our model in the case where the manufacturer does not follow the OEM’s CDD. By backward induction, we first focus on Stage 3 and derive firms’ operational decisions on the wholesale price and production quantities in the four possible subgames: (A, A), (P, P), (A, P), (P, A). We then investigate firms’ strategic decisions on production timing in stage 2.

Stage 3: Firms’ Decisions on

The equilibrium outcomes of the four subgames are summarized in Table 2. Lemma 1 shows the comparisons of equilibrium decisions among these four scenarios.

The Equilibrium Outcomes of Four Scenarios

By setting a proper wholesale price, the manufacturer is able to (i) increase its business opportunity (through

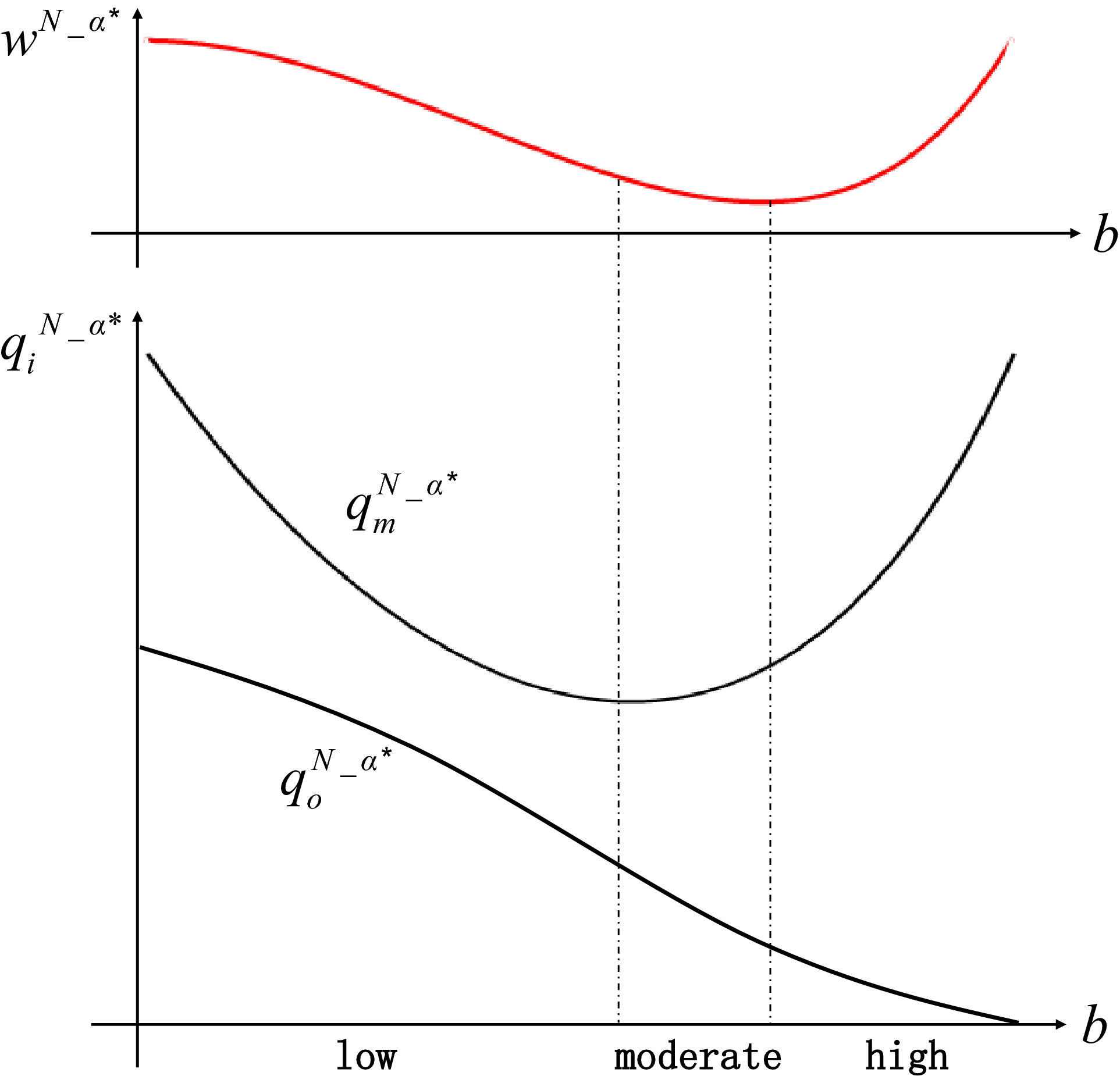

Impact of b on w, q, and Π

Lemma 2 shows that the manufacturer’s wholesale price is determined by competition intensity. More precisely, the manufacturer sets a high wholesale price when competition intensity is either high or low, whereas it sets a low wholesale price otherwise. We first highlight several essences: (i) as analyzed in Lemma 1, the manufacturer’s pricing power might suppress the OEM’s market share; and (ii) the interaction between the OEM and the manufacturer is closely related to the product substitutability (i.e., positively correlated). Keeping these in mind, we next elaborate the manufacturer’s wholesale price decisions (see Figure 2 for illustrations).

Effect of Wholesale Price on Firms’ Quantities [Color figure can be viewed at

When competition intensity is low, there is little interaction between the two firms’ actions because of low product substitutability. The OEM can still determine a high order size in spite of a high wholesale price. In spite of the OEM’s large quantity, the manufacturer can still choose a high quantity because it can still occupy a large market share due to the low competition intensity. This motivates the manufacturer to charge a high wholesale price to generate profits in both self‐branded business and manufacturing business.

In contrast, when competition is fierce, the interaction between the OEM and the manufacturer is strong, which enhances the manufacturer’s pricing power. The manufacturer thus charges a higher wholesale price to suppress the OEM’s market share. A high wholesale price and a high market share compensate for the reduced order size in the manufacturing business. In particular, however, when the manufacturer’s self‐branded products are improved to be perfectly substitutable to the OEM’s (i.e., b = 1), the OEM will withdraw the wholesale order and stop manufacturing business. This implies that, it is necessary for the manufacturer to take the OEM’s threat into account when developing self‐branded business.

When competition intensity is moderate, the manufacturer determines a low wholesale price. Because the OEM’s order decreases rapidly as competition intensity increases, a low wholesale price is used to incentivize the OEM to purchase more.

Stage 2: Firms’ Decisions on AS and PS

As Table 2 shows, profits are different in the four scenarios, but the profits have a similar structure in which they are comprised of two parts. The first part is independent of

Player i’s early commitment value (

Player i’s information value (

If a firm chooses AS to take advantage of early commitment, it faces operational risk, that is, over‐ or under‐production due to choosing production quantity before market acceptance is realized. Alternately, if it chooses PS, it can postpone the quantity decision until market acceptance uncertainty is resolved to take advantage of information. The choice depends on the trade‐off between the commitment value and the information value.

Based on Table 2, the OEM’s and manufacturer’s preferences over AS and PS can be deduced by comparing their profits. Table 3 shows the profit matrix of the OEM and the manufacturer.

Profit Matrix of the OEM and the Manufacturer

With the definitions in the profit matrix, we derive the following results.

For the OEM, there exists a threshold

Lemma 3 shows that, if the manufacturer chooses AS, it is better for the OEM to choose PS than AS, because there is no early commitment value when they both choose AS and play a simultaneous game; while there is information value when the OEM chooses PS.

However, if the manufacturer indeed chooses PS, the OEM’s preference over AS and PS depends on market acceptance uncertainty. When uncertainty is low, the OEM chooses AS because the early commitment value of AS dominates the information value of PS. In contrast, when uncertainty is high, the OEM chooses PS instead of AS. Although AS brings commitment value, it also puts the OEM in a position with high operational risk due to large uncertainty; that is, the information value from PS dominates the commitment value of AS. Lemma 3 indicates that, to make better production timing decisions, firms should evaluate the market acceptance of their products, and effects of early/delayed commitment. We find that the equilibrium outcomes of the manufacturer are similar to those of the OEM, which are captured in the following lemma.

For the manufacturer, there exists a threshold

Based on Lemmas 3 and 4, we derive a threshold

There exists a unique threshold

If If If If

If If If If

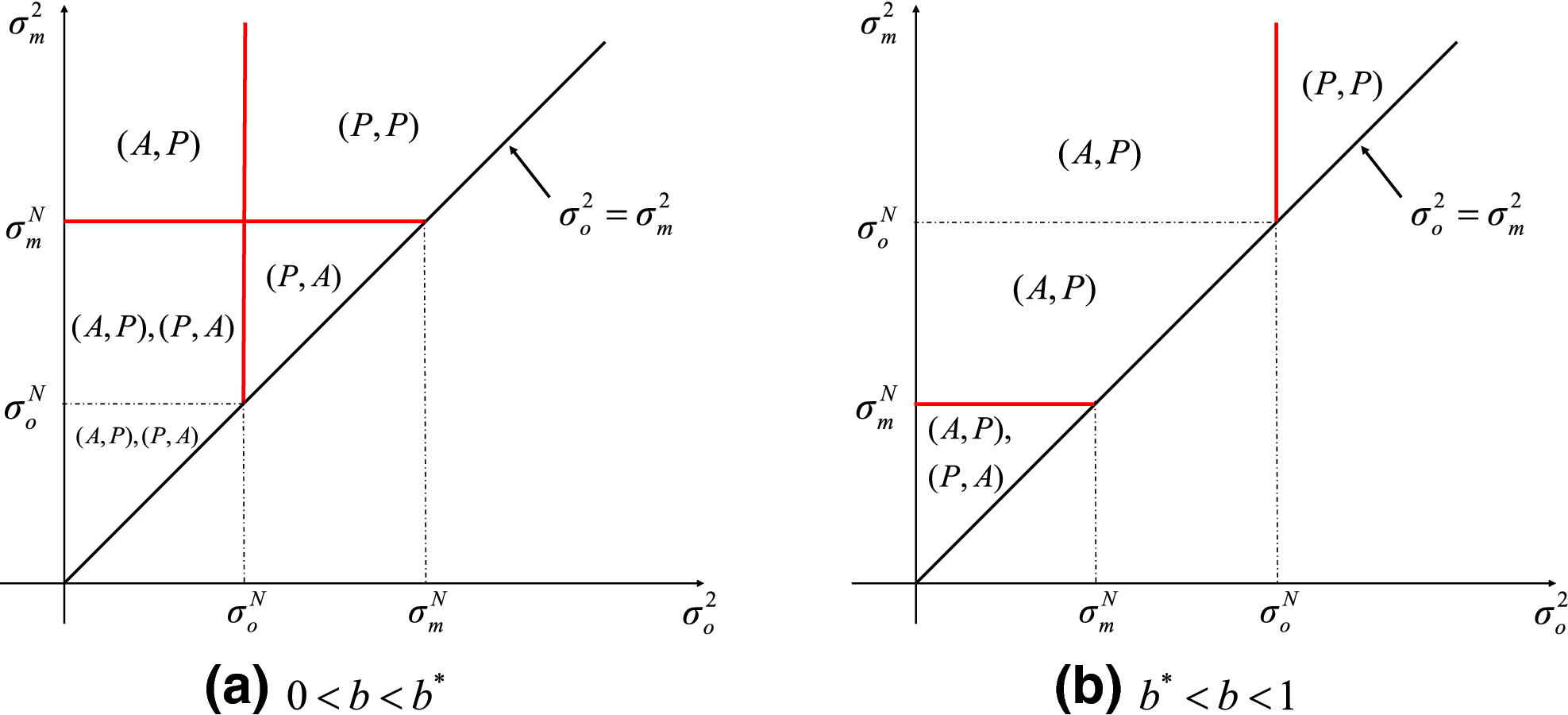

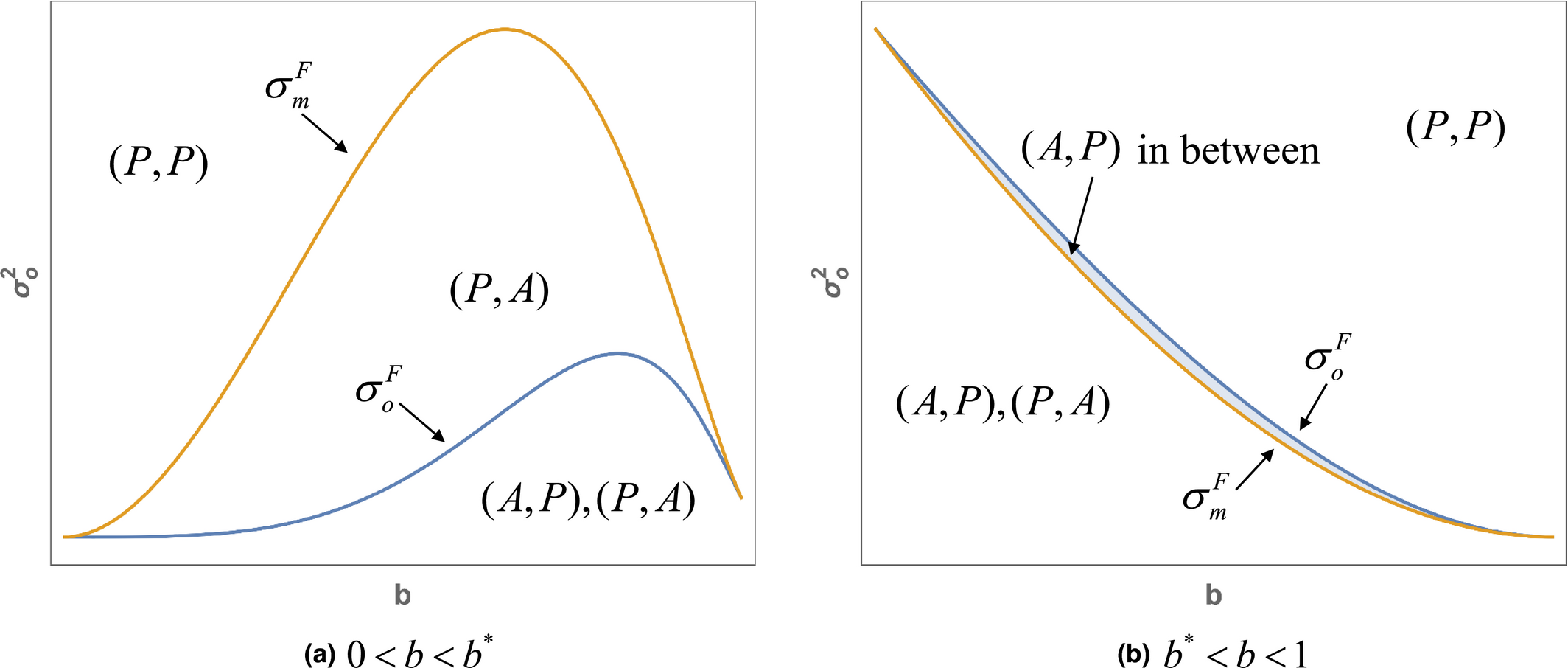

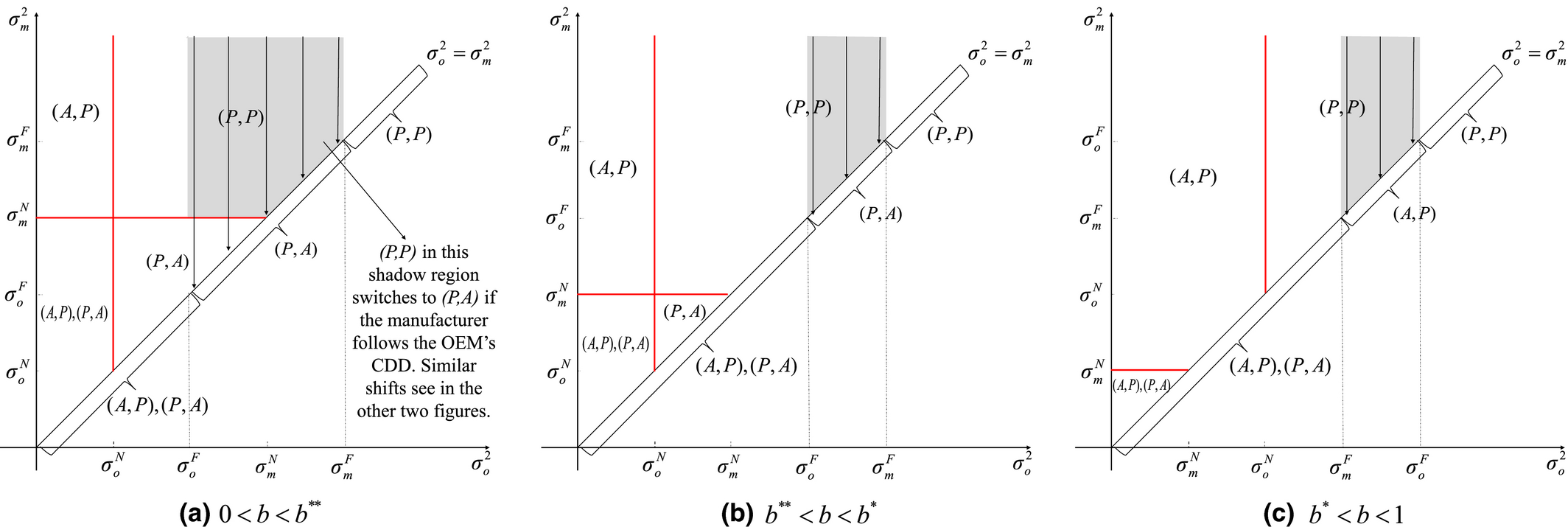

Figure 3 illustrates firms’ strategic choices in equilibrium on the two‐dimensional

Firms’ Production Timing in the Not‐Following Case [Color figure can be viewed at

When both firms face low uncertainty (with small

When both firms have high uncertainty (with large

When the manufacturer’s uncertainty is much larger than the OEM’s, the equilibrium is that the OEM chooses AS to take advantage of the commitment value, and the manufacturer chooses PS to benefit from the information value (the upper left region of Figure 3a and b).

When market acceptance uncertainty of both firms is moderate, we find that the preferences over AS and PS of the OEM and the manufacturer are determined by the competition intensity (the lower right region of Figure 3a and the middle region of Figure 3b). The OEM chooses AS while the manufacturer chooses PS when the competition is sufficiently intense (

Figure 4 illustrates how the information value changes in the competition intensity. One can see that, the information value decreases in b and decreases significantly when b is large;that is, the information value is significantly reduced when competition is sufficiently intense.

7

Thus, the OEM chooses AS to preempt the initiative and to obtain the early commitment value. However, the manufacturer chooses PS. Although the information value of the manufacturer is also reduced by intense competition, larger uncertainty

The Effect of b on Information Value (

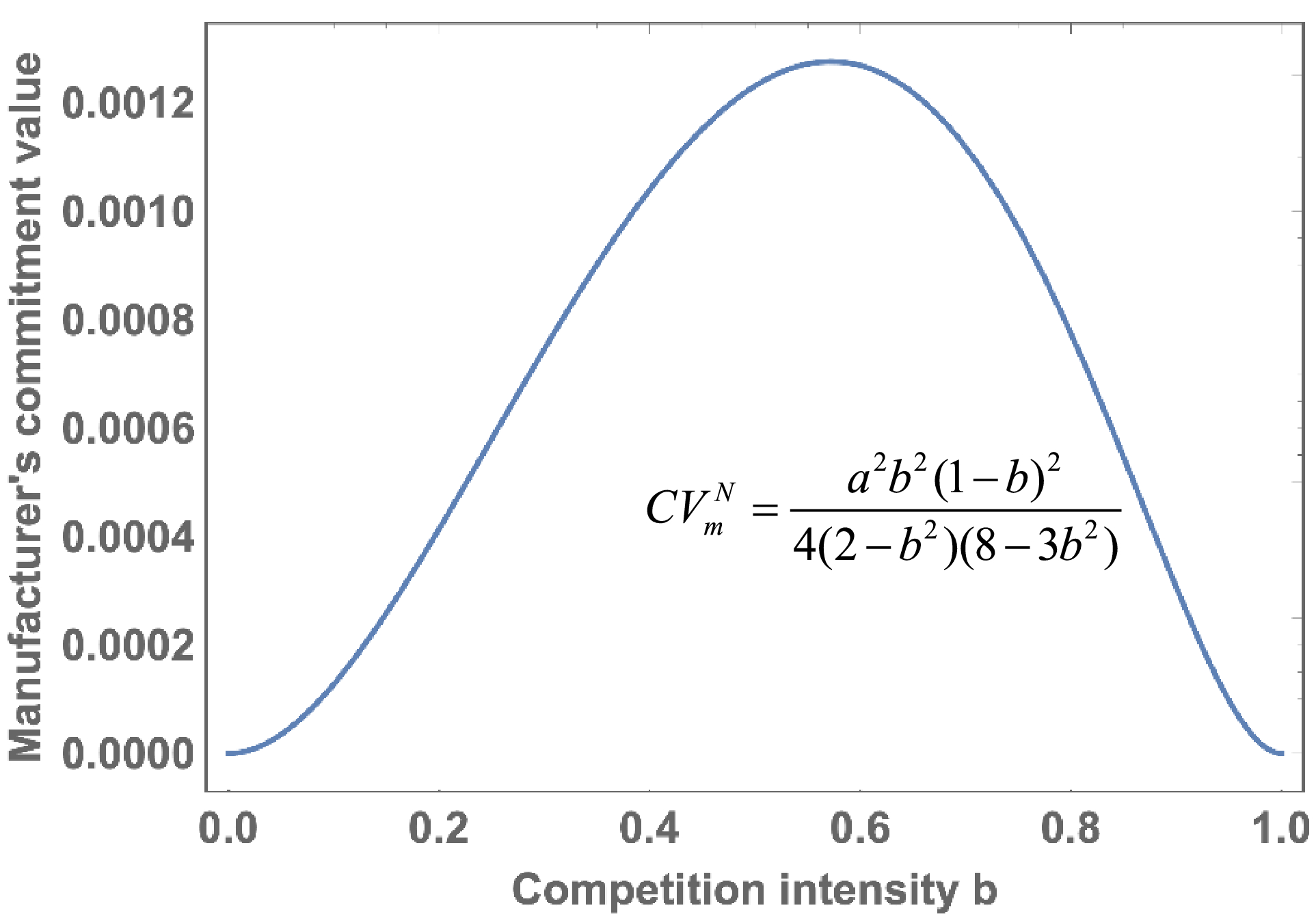

Interestingly, in the case with moderate uncertainty and less intense competition (i.e.,

The Effect of b on the Manufacturer’s Commitment Value (a = 1) [Color figure can be viewed at

Following the CDD (F)

Consider that the manufacturer follows the OEM’s CDD to conduct product design. In this case, there is no difference between the two firms’ market acceptance (i.e., they both have uncertainty

Similar to Lemma 3 and 4, we derive two thresholds

Firms’ Production Timing in the Following Case [Color figure can be viewed at

there exists a unique threshold

Proposition 2 is derived by comparing the thresholds in the cases where the manufacturer follows and does not follow the CDD. We show that

Incentives of Following the CDD (Stage 1)

In this section, we compare the manufacturer’s profits when following and not following the OEM’s CDD and derive its decision in Stage 1. To do so, we first derive two lemmas that investigate the information value and the commitment value in different scenarios.

Recall that firm i’s information value,

Firm i’s Information Values

We have the following observations. First, the coefficient of information value in a sequential game is always larger than that in a simultaneous game (i.e.,

Cooperation effect: given

Accuracy effect: the negative effect of following the CDD on information value by directly reducing uncertainty

Transparency effect: the negative effect of following the CDD on information value in a simultaneous game by reducing the coefficient of information value due to the change of information transparency.

We then present the lemma that characterizes the effect of competition intensity on the commitment value.

The commitment value of the manufacturer is larger than that of the OEM if and only if

Using these two lemmas, we can analyze how following the CDD affects the equilibrium. When the manufacturer follows the OEM’s CDD, both accuracy effect and transparency effect reduce the two firms’ information value (or the firms’ operational risk), resulting in an intermediate state, where both firms have the same information values and make their AS/PS choices based on the trade‐off between the commitment value and the information value. When

Equilibrium Changes if Following the CDD [Color figure can be viewed at

In the case where

Proposition 3 indicates that, in the case where there is less competition, the OEM benefits from the manufacturer’s following the CDD if the manufacturer faces high market acceptance uncertainty and the OEM’s uncertainty is moderate. This will change a simultaneous equilibrium with direct competition on postponement strategy (i.e., PS) into a sequential equilibrium with deviation from PS. The mitigation of competition results in two positive effects on the OEM’s profit. First, cooperation effect endows the OEM with a larger information value in a sequential game. Second, the OEM has a larger market share because it can determine a higher production quantity in the market with less competition.

However, it is interesting that more accurate information hurts rather than benefits the manufacturer. By following the OEM’s CDD, the manufacturer tries to reduce the operational risk of AS so that it can benefit from early commitment. However, this is not a wise decision. Note that the manufacturer has high market acceptance uncertainty if it does not follow the OEM’s CDD to design products. Although following the CDD can reduce the manufacturer’s uncertainty risk, it significantly reduces the information value from PS. Thus, the manufacturer suffers from following the CDD.

In the case where

This proposition indicates that, given tense competition, when both the OEM and the manufacturer face high demand uncertainty, the OEM will be hurt by the manufacturer’s following the CDD. Note that the OEM is more sensitive to the reduction of information value when

Note that, even if the manufacturer fails to change to AS by following the OEM’s CDD, there may be benefits. Overall, following the CDD has both negative and positive effects on the manufacturer; that is, accuracy effect reduces the information value while cooperation effect increases the benefits from information in a sequential game. Conversely, remaining on PS endows the manufacturer with spillover value from the OEM’s early commitment. It is worth noting that, when the manufacturer faces low uncertainty (i.e., with small

Extensions

In this section, we have four extensions: (i) revenue‐sharing contract, (ii) the manufacturer’s postponement of wholesale pricing, (iii) correlation of two firms’ market acceptance uncertainty, and (iv) non‐zero production cost. We use the following subscripts, r, w, d, and c, to represent the corresponding extensions, if necessary.

Revenue‐Sharing Contract

We have assumed the manufacturer signs a wholesale price contract with the OEM, following previous literature on contract manufacturing. In practice, the manufacturer and the OEM are possible to sign a revenue‐sharing contract with two parameters (w, ϕ) (Cachon 2003), where w is the wholesale price, and ϕ ∈ [0, 1] is the OEM’s share of revenue. The manufacturer’s share is 1 − ϕ. Following Cachon and Lariviere (2005), ϕ is exogenous. Firms’ expected profits are, respectively,

The following proposition shows how ϕ affects the equilibrium.

For any given ϕ ∈ [0, 1], there exists a threshold

When ϕ = 1, the revenue sharing model is the same as the base model. In this case,

Proposition 5 shows that under a revenue‐sharing contract, (A, P) cannot be an equilibrium in a less competitive market. This is because the manufacturer has an additional source of income from revenue‐sharing, which encourages the manufacturer to lower the wholesale price and to attract a larger order size from the OEM. This incentive of the manufacturer is strong, especially when competition is mild (b is small). In this case, a larger production quantity of the OEM does not have much of a negative impact on the manufacturer’s profit through competition, but has a positive impact on the manufacturer’s profit through revenue sharing. Recall that in the base model, the manufacturer adopts a low‐pricing strategy in the scenario (A, P) to spur the OEM to purchase more (see Lemma 1). Under the revenue‐sharing contract, the further adoption of a low‐pricing strategy in (A, P) with a small b is not necessary, because over‐stimulation of the OEM’s order (

Postponement of Wholesale Pricing

In our main body, we assumed that the wholesale price w is determined before uncertainty resolves, regardless of the OEM’s timing decisions (AS or PS). In this subsection, we investigate a case in which the manufacturer postpones the wholesale price decisions until the market uncertainty is resolved if the OEM adopts the PS strategy to take advantage of the information value. There are two possible scenarios in this case: (P, A) and (P, P). In (P, A), the sequence of events is as follows: (i) the manufacturer determines

Our main results qualitatively hold, except that two slight differences arise. First, in the case where the manufacturer does not follow the CDD, when firms’ uncertainty is moderate, (P, A) is an equilibrium ∀b ∈ (0, 1). Recall that in the base model, as b increases, the equilibrium changes from (P, A) to (A, P). As b becomes larger, the OEM suffers from a higher wholesale price. In addition, the information value also decreases with b. Therefore, the OEM shifts from PS to AS. In response to this change, the manufacturer shifts from AS to PS to take advantage of the spillover value from the OEM’s early commitment. However, in the case in which the wholesale price decisions are postponed, the OEM benefits from this postponement because it learns

Second, the impact of the manufacturer’s following the CDD is slightly different when the competition intensity b is small. Recall that in Proposition 3, if the manufacturer follows the CDD, the equilibrium might change from (P, P) to (P, A). This change makes the manufacturer worse off and the OEM better off. However, if the wholesale price is determined after uncertainty is resolved, we can show that this change of equilibrium makes the manufacturer worse off only if

Market Acceptance Uncertainty Correlation

In this subsection, we extend our base model by considering market acceptance uncertainty correlation: the manufacturer faces

Our main results qualitatively hold, except that the manufacturer’s following the CDD does not benefit itself any more. Recall that in Proposition 4, the manufacturer benefits from following the CDD if

Non‐Zero Production Cost

If the manufacturer incurs a marginal production cost c with c < a, firms’ expected profits are, respectively,

By comparing the above two expressions with the expressions in 2 and 3 of the main body, one can see that the expressions of

Conclusion

Technology specifications such as Android’s CDD are often viewed as Google’s important strategy to improve the user experience of Android devices, and they are closely linked with production timing decisions due to the market acceptance uncertainty. In this study, we develop a model to study the production timing decisions in a co‐opetitive supply chain, which comprises an OEM (e.g., Google in our motivating example) and a competitive manufacturer, which acts both as the OEM’s upstream partner and downstream competitor. The two firms sell partially substitutable products in a market with market acceptance uncertainty, which can be resolved after a certain time spot. As the CDD is based on mainstream preference, the OEM has lower uncertainty, resulting in more stable demand. They can choose either AS or PS, depending on the relative magnitude of the commitment value and the information value.

We find that, both market acceptance uncertainty and competition intensity have a significant impact on firms’ strategic choices between AS and PS. Both firms choose PS when they are at the risk of high uncertainty, while only one firm chooses PS when the uncertainty is low/moderate. This implies that, market acceptance uncertainty determines the nature of competition and cooperation between the OEM and the manufacturer. A simultaneous equilibrium occurs when both firms face high uncertainty and a sequential equilibrium occurs otherwise. When market acceptance uncertainty of the two firms varies in a moderate range, their strategic choices between AS and PS are affected by competition intensity in an interesting way. When competition is fierce, intuitively both firms have strong incentives to choose AS. However, we find that the OEM chooses AS but the manufacturer chooses PS in spite of his low information value. In this way, it can benefit from the OEM’s early commitment, which is named as spillover value because of the co‐opetition relationships between the two firms. When competition is not very intense, a completely different outcome occurs. By intuition, the OEM is likely to choose AS because of low uncertainty and, thus, low operational risk. However, the OEM chooses PS, because choosing AS incurs a significant cost increment for production outsourcing. The manufacturer chooses AS because of high wholesale price and self‐branded price, resulting in better performances in both manufacturing business and self‐branded business.

We further investigate the impact of following the CDD on firms’ choices between AS and PS. We show that information value is influenced by three effects including cooperation effect, accuracy effect and transparency effect, the scales of which are respectively modulated by strategic deviation from PS, signal accuracy and information transparency. These effects change the trade‐off between the commitment value and the information value, and correspondingly determine the profit performance of the two firms. They also influence the manufacturer’s incentives of following the OEM’s CDD. Based on the analysis, we identify the conditions under which following the CDD benefits the manufacturer.

These findings provide the following managerial implications to operation managers, especially those in Google, HTC, and LG. Note that they have co‐opetition relationships bilaterally but HTC (LG) chose PS (AS) strategy when “full screen” phone design was launched. Specifically, we suggest that the competitive manufacturer chooses PS when market uncertainty is large. Our suggestion can be consistent with practice because we observe that, in the Indian smartphone market with large variability, the followers gain prominent benefits from PS. the competitive manufacturer implements AS in a market with small variability and intense competition, because the information benefits from PS are limited. This result is consistent with the observation that these years LG has launched new Android smartphones ahead of MWC due to the “unabated competition”. in a market with moderate uncertainty and intense competition, the OEM is better to choose AS while the manufacturer chooses PS. This finding explains HTC’s late product launch in “full screen” phone design. However, we find that Google’s late launch practice might be a blunder. the OEM might either benefit from or be hurt by the manufacturer’s following the CDD, depending on competition intensity. In reality, as competition intensifies, Google has been witnessed to take an increasingly strict control over specifications on Android phone designs. Google might gain, if competition is not that intense, from such tightening which ensures the user experience on Android phones. However, Google has to be cautious if competition continues to intensify, because it might be exposed to the threat from its rivals.

Regarding the future research directions, we recommend to study newsvendor models under push (ordering before demand realization) and pull (ordering after demand realization) contracts, although the analysis can be challenging. In practice, it is also possible that firms only obtain an updated signal of the market rather than the full information. However, that requires new models based on Bayesian updating, and hence, is beyond the scope of our study.

Footnotes

Appendix A

Acknowledgments

The authors are grateful to the Department Editor, the Senior Editor, and the two anonymous reviewers for their helpful comments and suggestions. The authors contributed equally to this study and are ordered alphabetically according to their preferred first name. Kanglin Chen is the corresponding author. The authors’ work was supported in part by the NSFC Excellent Young Scientists Fund (No. 71822202), the NSFC (No. 71571194), Chang Jiang Scholars Program (Niu Baozhuang 2017), and the GDUPS (Niu Baozhuang 2017).

1

OEMs in this study are referred to as firms that specialize in their core competencies such as product design, development, and marketing, but outsource production to contract manufacturers. This definition is widely adopted in literature. See Plambeck and Taylor (2005), Ülkü et al. (2007), Chen et al. (2012), Kayiş et al. (2013), Wang et al. (2013), Hu and Qi (![]() ) for more references. In our study, e.g., Google is an OEM that relies on HTC for contract manufacturing.

) for more references. In our study, e.g., Google is an OEM that relies on HTC for contract manufacturing.

2

See

3

We assume a linear demand function here, which could be partially justified by empirical studies (Galetovic et al. 2018, Green and Newbery 1992). For example, Green and Newbery (1992) believe linear demand competition widely exists and works well in parameter estimations. Galetovic et al. (2018) assume a linear demand function and use data from the smartphone industry. We admit the limitations of linear demand functions and discuss alternative models as future research directions in section ![]() .

.

4

Because

7

This intuition can be practical. For example, Mobile World Congress (MWC) is the world’s largest exhibition, attracting many mobile device manufacturers to release their products. According to a most recent report by Gartner, however, these years Samsung and LG have launched new Android smartphones ahead of MWC (Gartner ![]() ). Anshul Gupta, Research Director at Gartner, attributes this phenomenon to the “unabated competition” (Gartner 2018), suggesting that waiting until the market becomes clear becomes less attractive as competition heats up.

). Anshul Gupta, Research Director at Gartner, attributes this phenomenon to the “unabated competition” (Gartner 2018), suggesting that waiting until the market becomes clear becomes less attractive as competition heats up.