Abstract

This study investigates manufacturer guarantor financing (MG) and third‐party logistics (3PL) guarantor financing (LG) in a four‐party supply chain game that features a manufacturer, a 3PL, a capital‐constrained retailer, and a bank. The manufacturer or 3PL can act as the guarantor for the retailer who borrows bank credit. Two different leadership structures are investigated, namely, Nash game and manufacturer leadership Stackelberg game, where the manufacturer and 3PL decide simultaneously and sequentially, respectively. The supply chain under both leadership structures prefers guarantor financing to traditional bank financing when the supply chain is sufficiently cost‐efficient. In the Nash game, however, firms encounter a free‐rider dilemma when choosing between MG and LG, wherein both potential guarantors prefer the other to be the guarantor. This free‐rider dilemma can be resolved in the Stackelberg game. We also observe the follower–guarantor advantage in the Stackelberg game, wherein all firms favor the follower to provide guarantor financing. Our analysis shows that the supply chain under guarantor financing with a longer decision hierarchy (i.e., the Stackelberg game) can be conditionally more effective than that with a shorter one (i.e., the Nash game). By further analyzing different cost structures, pricing mechanism, and retailer’s initial capital, we find that most of our qualitative results remain accurate under more sophisticated conditions. These findings enhance our understanding of the value of guarantor financing in a capital‐constrained supply chain and the impact of leadership structure on financing decisions.

Introduction

Financial constraints are prevalent worldwide, especially in developing countries. According to the World Bank Group Enterprise Surveys (The World Bank, 2018), which covers more than 131,000 firms across 139 countries, 26.5% of firms identify “access to finance” as a major constraint. In developing countries, such as those in Sub‐Saharan Africa, the ratio can reach 38.3%. Traditionally, bank financing is considered a solution for many capital‐constrained firms. However, according to the World Bank Group Enterprise Surveys, 79.2% of loans, on average, require collateral. The value of the collateral is 2.06 times the loan value, which is extremely demanding for many startups and fast‐growing firms, especially when they lack creditworthiness. Unfortunately, the lack of financial resources in one firm can jeopardize the performance of the entire supply chain.

To address the issue on creditworthiness, companies utilized guarantor financing as an alternative to traditional bank financing. In guarantor financing, one capital‐abundant supply chain member (e.g., the manufacturer) provides a guarantee for the capital‐constrained firm (e.g., the retailer) to borrow from a bank and repays the firm’s debt if the latter defaults on agreed repayments.

Two major guarantor financing schemes are widely used in developing countries where credit history and collateral are negligible for small firms. The first is referred to as manufacturer guarantor financing (MG), wherein the manufacturer serves as the guarantor. For example, the New Hope Group (NHG) is one of the largest feed producers in China. Thousands of farmers purchase feedstuff from NHG to cultivate dairy cows, chickens, and ducks. Most farmers are small in scale and they struggle to obtain financing because of their lack of collateral. To overcome this financing impediment, NHG started providing guarantor financing to farmers in 2007 when they attempt to obtain loans from banks. By the end of 2014, NHG secured loans of 18 billion yuan, which supported 90,000 farmers. Guarantor financing also rallied NHG’s own sales; for example, sales volume of feedstuff was improved by 1,350,000 tons in 2014 (Puhui, 2015).

The second major guarantor financing is called third‐party logistics (3PL) guarantor financing (LG), in which 3PL firms (e.g., UPS Capital, AIMS Logistics, and Schneider Logistics) step up their financing roles in supply chain procurement (Chen et al. 2018). In recent years, 3PL guarantor financing has swiftly gained popularity in developing countries, such as China. For example, Eternal Asia established a microcredit company in 2009 and further expanded investments to the company in 2013 to provide financial services for small businesses, especially supply chain members, by assuming their default risks (

Guarantor financing has been practiced for years, but it is relatively novel to supply chain finance literature, especially in a four‐party game that includes a manufacturer, a retailer, a 3PL, and a bank. To the best of our knowledge, no other study has theoretically investigated the effectiveness of MG and LG. In particular, no existing study has examined relative efficiency among different guarantor financing schemes that interact with the Stackelberg leadership structure. Moreover, no existing study has characterized the conditions to implement guarantor financing, even if traditional bank financing is viable. This study attempts to address these issues.

Primary Findings and Contributions

To study guarantor financing, we extend the classic selling‐to‐newsvendor model (i.e., a manufacturer selling through a retailer) to a four‐party (supply chain) game composed of a manufacturer, a 3PL firm, a capital‐constrained retailer, and a bank. We mainly consider two game settings, namely, Nash game and manufacturer leadership Stackelberg game. The supply chain game has two time periods. In the first time period, the manufacturer determines the wholesale price, the 3PL firm decides the logistic service rate, and their decision sequence depends on the leadership scenario (i.e., either Nash or Stackelberg game). The capital‐constrained retailer then decides its order quantity, secures a loan from the bank directly or under either MG or LG, and then pays the manufacturer and 3PL for the order and delivery, respectively. Demand is realized in the second time period and the retailer repays the bank. The guarantor will pay the rest of the loan to the bank if the retailer would default.

Four major findings are obtained. First, guarantor financing can outperform traditional bank financing (BF) for the whole supply chain, especially when upstream firm costs are sufficiently low and the financial risk satisfies certain conditions in both game settings. The rationale is that the retailer’s total purchasing cost (wholesale price plus logistic service rate) is higher in guarantor financing, but its loan interest rate is lower, which leads to a higher order quantity than BF. The interest‐rate benefit outweighs the purchasing‐cost drawback when costs of upstream firms are not substantially high.

Second, the willingness to act as guarantor varies under different game leadership structures. In the Nash game, the retailer and the supply chain are indifferent of either the manufacturer or the 3PL guarantor financing. However, the manufacturer and the 3PL prefer the other to be the guarantor (i.e., being a free‐rider in guarantor financing is better than being the guarantor).

The free‐rider dilemma can be resolved if the manufacturer emerges as the Stackelberg leader in the supply chain. In the manufacturer leadership Stackelberg game, all firms prefer the follower to be the guarantor. The supply chain can benefit from the follower–guarantor advantage because the follower–guarantor is constrained by the leader from charging an extremely high‐risk premium. In contrast, the manufacturer as the Stackelberg leader does not charge an extremely high wholesale price for not carrying the guarantor’s financial risk. This follower–guarantor advantage results in a high‐order quantity that benefits all firms in the supply chain.

Third, a Stackelberg leader always prefers to free‐ride the other upstream firm’s guarantor financing service. In contrast, the follower always prefers to be the guarantor due to the follower–guarantor advantage. However, from the guarantor’s perspective, being the follower is not always advantageous. The Stackelberg leadership advantage can outplay the follower–guarantor advantage when the financial risk level (i.e., the retailer’s default risk) is sufficiently low. This outcome can be attributed to the fact that the Stackelberg leader can more easily transfer the pricing pressure to the follower to demand a bigger profit margin for being the guarantor. Nevertheless, if the retailer is more likely to default, the guarantor can gain more benefits from being a follower than being the leader.

Fourth, under LG, all firms and the supply chain can perform better with a longer decision hierarchy (i.e., the Stackelberg game) than that with a shorter decision hierarchy (i.e., the Nash game). This finding contradicts the conventional wisdom that a flatter decision hierarchy is more efficient as confirmed under bank financing. This phenomenon occurs when financial risk is substantially high. In this situation, the manufacturer is more reluctant to increase its wholesale price in the Stackelberg game than in the Nash game, thereby resulting in a lower wholesale price and a higher order quantity in the Stackelberg game.

This study contributes to the extant literature in several aspects. First, this study is the first to analyze and compare different guarantor financing schemes in a four‐party supply chain game. Second, this study provides a theoretical guideline for capital‐constrained retailers on whom to request for the guarantor financing service. Third, this study demonstrates that the follower–guarantor advantage and the Stackelberg leadership advantage can outmatch each other, such that the guarantor does not always prefer to be the Stackelberg leader. Fourth, this study shows that the supply chain with a longer decision hierarchy might not be worse off. This result corroborates the practice of some focal firms, such as manufacturers, of stepping up as the Stackelberg leaders in supply chains.

Literature Review

This study is related to multiple research streams in the growing supply chain finance literature. The first research stream is related to the interface between financial and operational decisions in supply chains. Modigliani and Miller (1958) show that operational and financial decisions can be made separately in a perfect capital market. Brander and Lewis (1986) indicate that the choice of financial structure can affect the market in terms of a limited liability effect and strategic bankruptcy effect in an oligopoly market. A limited liability effect may leverage a firm to a more aggressive stance. Babich and Sobel (2004) explore how to coordinate operational decisions with financial decisions, which include production, sales, and loan size, to maximize the expected present value of the proceeds from an initial public offering. Buzacott and Zhang (2004) incorporate asset‐based financing into production decisions and present how asset‐based financing benefits the bank and the firm. Dada and Hu (2008) consider the inventory procurement problem of a capital‐constrained newsvendor by proposing a nonlinear loan schedule to coordinate the channel under traditional bank financing. Lai et al. (2009) and Chen et al. (2013) respectively employ a mathematical model and laboratory experiments to explore how order modes or inventory financing affects inventory decisions. Zhang (2010) extends the models of Lai et al. (2009) and Chen et al. (2013) to multiproduct settings. Li et al. (2013) consider a single‐product firm that makes the decisions related to production, borrowing, and dividends under demand uncertainty. Deng et al. (2018) study an assembly system with one assembler and multiple heterogeneous suppliers and reveal the conditions when buyer finance is better than bank finance for different parties. These models are not based on guarantor financing given their distinct focuses.

The second research stream is related to trade credit. Trade credit may be an effective alternative when traditional bank financing is limited (Burkart and Ellingsen 2004). Jing et al. (2012) show that when bank and trade credits are viable, the unique equilibrium is trade credit financing if and only if the production cost is relatively low. Kouvelis and Zhao (2012) argue that the retailer will always prefer manufacturer financing to bank financing, and the manufacturer will always finance the retailer. Chod (2016) identifies one of the advantages of trade credit over bank financing, wherein the former mitigates a limited liability effect. Peura et al. (2017) prove that trade credit can soften horizontal price competition in a Bertrand competition framework. Cai et al. (2014) discuss the usage of bank credit and trade credit when the capital‐constrained retailer has incentives to divert the credits to other investments in the presence of moral hazard. They compare four scenarios and analytically and empirically prove that trade credit and bank credit can be either substitutable or complementary. Hu and Yang (2018) discuss trade credit from the perspective of trade credit and explain the phenomenon of coexistence of trade credit and reverse factoring. We refer to Cai et al. (2014) and Lee and Rhee (2011) for more detailed discussions on trade credit.

Manufacturer guarantor financing is similar with trade credit because the manufacturer shoulders the retailer’s default risk in both financing schemes. However, multiple differences exist. First, in trade credit, the manufacturer delays payment from the retailer, whereas in manufacturer guarantor financing, the manufacturer receives the cash from the bank in advance. Second, the manufacturer increases the wholesale price in guarantor financing, whereas it charges interest or equivalent in trade credit financing. Third, compared with trade credit, guarantor financing provides a healthier cash flow for the manufacturer because banks provide the loans, especially when the manufacturer faces many capital‐constrained retailers.

The third research stream is related to the emerging practice of innovative supply chain financing. Wu et al. (2014) explore a buyer‐backed purchase order financing scheme, wherein the buyer supports the supplier in financing through a loan guarantee. Tunca and Zhu (2017) analyze the role and efficiency of buyer intermediation in supplier financing based on the practice of JD, a large Chinese online retailer. Yang et al. (2016) analyze the role of trade credit insurance as a risk management tool for suppliers to guarantee against payment default by buyers. This study supplements the practice database by discussing guarantor financing provided by upstream firms to a capital‐constrained downstream firm.

The fourth research stream is related to 3PL financing. In recent years, 3PL firms played an important role in supply chain procurement. However, only a few studies focused on this subject partly because of the complexity that stems from the long, three‐stage supply chains. One exception is Chen and Cai (2011) who formulate a Stackelberg model, wherein the 3PL firm provides 3PL credit financing services. Compared with the traditional manufacturer trade credit model, the 3PL credit model outperforms the manufacturer trade credit model when the 3PL firm’s marginal profit is greater than that of the manufacturer. Chen et al. (2018) also examine the financing role of a 3PL firm in supply chain procurement and show that delayed payment from the manufacturer to the 3PL firm can enhance firms and, thereby, the whole supply chain’s profit. Unlike 3PL credit financing and delayed payment, 3PL guarantor financing does not require the 3PL to pay cash in advance. Instead, it guarantees repayment to the bank if the retailer defaults.

The remainder of this study is organized as follows. The model is described in Section 2. We analyze three financing schemes in the Nash game and the manufacturer leadership Stackelberg game in Sections 3 and 4, respectively. We discuss three extensions in Section 5 and conclude in Section 6. All proofs are provided in the Appendix: Online Supplements.

Model

This model attempts to explore guarantor financing, wherein a capital‐constrained retailer borrows from the bank under an upstream firm’s financial guarantee to fund its purchase and logistics costs from upstream firms. We extend the classic selling‐to‐newsvendor model (i.e., a manufacturer selling through a retailer) to a four‐party game model by additionally including a 3PL firm and a bank. The manufacturer determines the wholesale price

We assume that the retailer has no capital and must obtain a loan amounting to

We assume that the manufacturer and the 3PL have constant positive marginal costs,

The classic newsvendor models in extant literature frequently assumed a fixed retail price for tractability. However, this assumption might have ignored the reality that retailers usually adjust their retail prices as purchasing costs change. To better describe pricing dynamics between retail price and purchasing cost, we assume that the products are sold at a markup retail price, that is,

Demand is uncertain and price sensitive. To be specific, the demand is assumed to be the product of expected demand and a positive random variable, which is

Notations

Notations

Financing Schemes

Three different financing schemes are studied in this article: manufacturer guarantor financing (MG), 3PL guarantor financing (LG), and traditional bank financing (BF).

Manufacturer Guarantor Financing (MG): The manufacturer serves as guarantor for the retailer to borrow from the bank. If the retailer would default, the manufacturer would cover the potential loss of the bank for lending to the retailer.

3PL Guarantor Financing (LG): The 3PL serves as the guarantor for the retailer to borrow from the bank. If the retailer would default, the 3PL would cover the potential loss of the bank for lending to the retailer.

Traditional Bank Financing (BF): The bank directly lends the money to the retailer and takes the default financial risk by itself.

Traditional bank financing serves as a benchmark in this study. In practice, the retailer, who is usually a small or startup company, cannot access a bank loan by itself due to lack of collateral or credit history. In our model, bank financing for supply chain members serves as a seemingly best scenario because firms can borrow from the bank without a third‐party’s guarantee and the bank market is risk‐free. In practice, the bank would charge extra risk premium, which incurs additional financing cost for the supply chain. Our analysis will show that guarantor financing is practical and could be better than the risk‐free case of bank financing. This finding means that guarantor financing can outperform bank financing for the supply chain, even if the bank is willing to offer loans directly to the retailer.

The main disparity between guarantor financing and traditional bank financing is that the retailer’s default risk is shifted from the bank to the guarantor. After demand realization, the retailer repays

We use subscript

Game Setting

The supply chain game consists of two time periods. In the first time period, the manufacturer determines the wholesale price

Nash Game: The manufacturer and the 3PL sign contracts with the retailer separately. These two upstream firms do not know the contract price of each other with the retailer. This means that both firms determine wholesale/service price only in anticipation of the other’s best response decision. This case is equivalent to that upstream firms simultaneously decide in a Nash game. This setting represents the basic situation, wherein the manufacturer and the 3PL are identical on decision sequence and information state.

2. Manufacturer Leadership Stackelberg Game: The manufacturer determines the wholesale price first and then the 3PL decides its logistic service rate. In practice, the 3PL can obtain information about the value of the product via insurance service, which makes manufacturer leadership Stackelberg game possible. Oftentimes, the wholesale price information can be also obtained on B2B websites, such as Alibaba (Alibaba.com) and Import Express Wholesale (import‐express.com).

In the second time period, the retailer decides on an optimal order quantity and then borrows a loan from the bank with an interest rate of r with or without guarantor financing. The retailer announces the retail price by adding a markup on purchasing cost. Price‐sensitive stochastic demand D is then realized and the retailer repays the bank. Under guarantor financing, if the retailer would default, the guarantor would cover the potential loss of the bank for lending to the retailer.

We use subscript

Profit Functions and Decisions of Firms

The profit functions of firms in the Nash game and Stackelberg game are the same. The difference lies in the decision sequence of the two upstream firms as stated in Section 2.2. We start solving for the bank's decision using backward induction. Under manufacturer and 3PL guarantor financing, the bank does not undertake any financial risk and sets the interest rate to the same value as the risk‐free interest rate, which is

Real interest rate

We then consider the decisions of upstream firms. In the Nash game, the manufacturer (3PL) optimizes its profit by deciding

For a meaningful discussion, any supply chain member that participates in the game must have a positive profit.

Financing under Nash Game

In the Nash game, the manufacturer and the 3PL sign contracts with the retailer separately without the knowledge of the pricing decision of the other. This section first analyzes decisions under bank financing and two kinds of guarantor financing in the Nash game and then compares these different financing schemes to underline the benefit of guarantor financing.

Equilibrium Analysis of Bank Financing

We start with the retailer’s best response function for any given wholesale price and logistic service rate by solving the game backwards. By combining the bank’s profit function in Equation (1) with the retailer’s profit function in Equation (2), we transfer the retailer’s problem in BF to the following:

which is equivalent to the risk‐free case without capital constraint. This finding is consistent with Xu and Birge (2004), Jing et al. (2012), and Kouvelis and Zhao (2012). The retailer’s optimal order quantity is solved as follows:

We define

By solving the game backwards, we can obtain the firms’ optimal decisions and profits, as summarized in Lemma 1:

Upstream firms can earn positive profit and are willing to participate in the Nash game with bank financing if

where

Condition

Through Lemma 1, we learn that the manufacturer and the 3PL earn the same marginal profits (

For the retailer,

Equilibrium Analysis of Guarantor Financing

The derivation procedure of equilibrium solution under guarantor financing is similar to that under bank financing. We summarize the optimal decisions and profits of all supply chain members in Lemma 2. We only list the manufacturer guarantor financing case because the optimal decisions and profits are symmetrical under 3PL guarantor financing.

Upstream firms can earn positive profit and are willing to participate in the Nash game with bank financing if

where

Similar to that under bank financing,

The term

The necessary condition for a positive expected demand stated in BF,

Comparison between Bank Financing and Guarantor Financing

This subsection compares firms’ performances between guarantor financing and bank financing in the Nash game. The comparison results are listed in Theorem 1.

In the Nash game,

The retailer prefers MG or LG to BF (i.e.,

The manufacturer (the 3PL) prefers MG (LG) to BF (i.e.,

The manufacturer (the 3PL) prefers LG (MG) to BF (i.e.,

Theorem 1 shows the significance of guarantor financing given that the supply chain members may still prefer guarantor financing even if the capital‐constrained retailer can borrow directly from the bank.

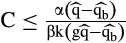

A trade‐off exists between guarantor financing and BF for the retailer. On the one hand, the retailer benefits from a lower interest rate in guarantor financing (interest‐rate effect) than in BF. On the other hand, the price of upstream firms depends on the operation cost and the financial risk cost (for serving as a guarantor). The guarantor increases the price for carrying the retailer’s default risk (i.e.,

The retailer prefers guarantor financing when

The potential guarantor also faces a trade‐off. On the one hand, the guarantor increases wholesale price or service price to enhance its profit margin (profit‐margin effect). On the other hand, the guarantor undertakes the retailer’s default risk and faces potential losses (financial‐risk effect). The guarantor‐cost effect is offset by interest‐rate effect when the supply chain cost is low; consequently, the retailer orders a large quantity. This outcome boosts the positive profit‐margin effect to overshadow the negative financial‐risk effect and, therefore, the guarantor benefits from providing guarantor financing.

The non‐guarantor in guarantor financing is forced to reduce price (profit margin loss), but it enjoys the benefit of guarantor financing (order quantity boost) without taking the guarantee risk. The sufficient condition for the non‐guarantor to enjoy guarantor financing is less constrained than the guarantor’s given that it does not shoulder the retailer’s default risk like the guarantor or the bank.

Comparison between Guarantor Financing Schemes

Given the importance of guarantor financing compared with bank financing, we are curious about which supply chain member is preferable as guarantor. A comparison of the two guarantor financing schemes achieves the following results:

In the Nash game, we obtain the following:

The retailer and the whole supply chain are indifferent to the manufacturer or the 3PL being the guarantor (i.e.,

The 3PL and the manufacturer prefer the other firm to be the guarantor (i.e.,

The upstream firm charges a higher price/rate when acting as guarantor (i.e.,

Combining the observations in Theorems 1 and 2, we can summarize the firms’ preference sequences of the three financing schemes in Corollary 1.

In the Nash game, the firms’ preference sequences of the three financing schemes are as follows:

For the retailer, 1) when

For the manufacturer, 1) when

For the 3PL, 1) when

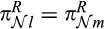

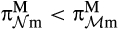

The explanation of trade‐offs for firms in Corollary 1 is similar to those for Theorems 1 and 2. We hereby employ Figure 1 to further illustrate the firms’ preference sequences between BF, MG, and LG. Notably, throughout this article,

Profits of Different Financing Schemes under Nash Game with Respect to the Manufacturer’s Cost

It is intuitive that the firms’ profits decrease with the manufacturer’s production cost

It is natural that firms’ profits will be affected by the retail price markup rate (

However, there exists a dilemma on which firm should provide guarantor financing. In particular, there is a trade‐off between the revenue margin and potential default loss. On the one hand, the guarantor can charge a higher price to earn a higher revenue margin. On the other hand, being the guarantor incurs a potential loss caused by the retailer’s default risk. Provided that the order quantity is the same under both guarantor financing types, in the trade‐off, the risk premium of the guarantor is edged out by the free‐rider benefit of allowing the other firm to serve as guarantor; therefore, both the manufacturer and the 3PL prefer the other firm to provide guarantor financing.

To illustrate this free‐riding dilemma in more details, we temporarily relax our original assumption here by assuming whether to be the guarantor is a decision of the manufacturer and the 3PL. In line with the practice, we also assume that only one firm, either the manufacturer or the 3PL, can be the guarantor. As a result, whoever not to be the guarantor will be a free‐rider in the guarantor financing game. The equilibrium outcome of the Nash game is summarized in the following table. To be consistent with the context, bank financing is available if no guarantee service is provided. Note that if bank financing is not available, the supply chain members will have more incentives to coordinate the supply chain.

According to Theorem 1, there exist conditions when guarantor financing outperforms bank financing for every supply chain member. Under the conditions, we can see that the game has two pure‐strategy Nash equilibria, which is a typical battle of the sexes game where each firm prefers the other to be the guarantor. Theoretically and practically, either equilibrium is possible considering that either firm might have been used to provide guarantee insurance to the retailer or is more likely to do so due to a stronger supply chain relationship with the retailer. If neither upstream firm would do so, they will lose the extra profits. Nevertheless, coordination can make one of the Nash equilibria be Pareto dominant.

One potential coordination solution is that the retailer can transfer an extra side payment to one of the upstream firms for the guarantee insurance. For example, the retailer can transfer the side payment to the 3PL. Compared to the case without guarantor, the retailer can earn additional

In reality, a focal firm, such as the manufacturer, may often emerge as the leader of the supply chain. Our next section proposes that such free‐riding dilemma will disappear in the manufacturer leadership Stackelberg game without extra coordination effort.

Financing under the Manufacturer Leadership Stackelberg Game

Due to the similarity of analysis between the Nash game and Stackelberg game, for a concise exposition, we skip the derivation details, but focus on the comparisons between different financing schemes and leadership structures to demonstrate how a change in leadership influences the game. We list the following equilibrium results for reference:

We obtain the following results under the manufacturer leadership Stackelberg game:

1. Given

2. Given

3. Provided

We have

Comparison between Bank Financing and Guarantor Financing

One may wonder whether the benefit of guarantor financing still holds for the retailer when the latter has access to bank financing in a Stackelberg game. The following comparison result confirms such benefit.

We compare LG and MG to BF in the manufacturer leadership Stackelberg game.

The retailer prefers LG to BF (i.e., The manufacturer prefers MG to BF (i.e., The 3PL prefers LG to BF (i.e.,

The threshold

Theorem 3 indicates that the advantage of guarantor financing relative to bank financing still conditionally holds. In other words, supply chain members may still favor guarantor financing even though bank financing is viable. We compare the thresholds and find that the condition for benefitting from a guarantor role in the Stackelberg game is less strict than that in a Nash game. In other words, guarantor financing becomes more attractive to upstream firms under the Stackelberg game. As the guarantor, the manufacturer can charge a higher risk premium and hence exploits its leadership position better than that in the Nash game. As the follower, the 3PL suffers for being forced by the leader to charge a lower service price, but the guarantor role enables the 3PL to earn extra revenue.

Follower–Guarantor Advantage

We also investigate which upstream firm is preferable to be the guarantor under the manufacturer leadership Stackelberg game.

We compare LG to MG in the manufacturer leadership Stackelberg game.

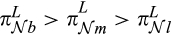

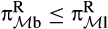

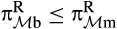

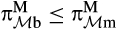

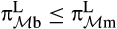

Every supply chain member prefers LG to MG (i.e.,

The preferences of all supply chain members are unexpectedly the same under the Stackelberg game, which means that all supply chain members earn more profit from LG than from MG. Hence, the manufacturer leadership Stackelberg game consolidates all firm preferences on the guarantor type and avoids the free‐rider dilemma in the Nash game.

In the Stackelberg game, the guarantor, which is the manufacturer or the 3PL, charges a higher price for the risk it takes (i.e.,

The preference of the manufacturer is also intuitive. Besides the free‐rider benefit discussed in Theorem 2 of Nash game that exempts the manufacturer from the guarantor financial risk, the manufacturer enjoys a higher order quantity when the 3PL is the guarantor. Therefore, the manufacturer also prefers LG to MG.

However, the preference of the 3PL is unexpected, which means that the 3PL favors the guarantor role over the free‐rider role. Three facets exist in the trade‐off. Under the manufacturer leadership Stackelberg game, order quantity is higher in LG than in MG (demand effect). Coupled with a higher revenue margin (revenue‐margin effect) for being the guarantor, the 3PL can overcome the potential default risk loss (financial‐risk effect) to achieve a better performance in LG than in MG.

This finding contradicts the conventional notion that a capital‐constrained retailer might want to seek guarantor financing from the dominant firm (i.e., the Stackelberg leader), given the classic Stackelberg leadership advantage. Theorem 4 cautions on the existence of the “follower–guarantor advantage” for the supply chain in guarantor financing. In this advantage, all members of the supply chain benefit from the follower acting as the guarantor. Thus, the capital‐constrained firm should instead request a dominated player to serve as the guarantor to prevent the Stackelberg leader from charging a higher risk premium for acting as the guarantor. The intertwining forces of these two advantages provide a new perspective on the role of supply chain leadership in guarantor financing. This aspect will be further discussed in the following subsection.

To provide a full picture of firms’ preference of the three financial schemes in the manufacturer Stackelberg game, we summarize the comparisons in Theorems 3 and 4 into the following corollary.

In the manufacturer leadership Stackelberg game, the firms’ preference sequences of the three financing schemes are as follows: For the retailer, 1) when For the manufacturer, 1) when For the 3PL, 1) when

The above threshold values can be further summarized in the following table

The explanation for Corollary 2 is similar to those for Corollary 1, Theorem 3, and Theorem 4 and, thus, skipped for a concise exposition.

Interaction between Guarantor and Leadership Roles

The previous section introduces the follower–guarantor advantage, wherein the supply chain benefits from letting the follower be the guarantor. However, is being the guarantor always beneficial to the follower? To address this concern, we hypothetically propose two new Stackelberg games only in this subsection for further discussion: MG and LG with 3PL Stackelberg leadership. The inclusion of these two games facilitates our discussion, but is not required (without these two games, the same qualitative conclusion can be achieved by equating firms’ operational costs for fair comparison). In practice, a 3PL firm may emerge as the leader of a supply chain, such as the orchestrator role of Eternal Asia in its one‐stop logistic system (Chen et al. 2018). Besides the original MG and LG with manufacturer leadership, we present a symmetric framework that allows the comparison of the firm’s profits among different leadership roles (leader vs. follower) and guarantor roles (guarantor vs. non‐guarantor/free‐rider). This analysis also enables the comparison between leadership advantage and the follower–guarantor advantage.

Comparison of different combinations of leadership roles and guarantor roles results in the following outcomes. Guarantor role preference: Leader: the free‐rider role is better than the guarantor role (i.e., Follower: the guarantor role is better than the free‐rider role (i.e., Leadership role preference: Free‐rider: the leadership role is better than the follower role; Guarantor: the leadership role is better if

Theorem 5 delivers several intriguing messages about firms’ preferences for different leadership roles and guarantor roles. First, if a firm starts as a leader/follower, its preference of a guarantor role is clear. The Stackelberg leader is known to have the leadership advantage, whereas the follower has the follower–guarantor advantage. In contrast, the guarantor is required to shoulder the retailer’s default risk. The leader will never choose to be a guarantor by forfeiting the benefit of the free‐rider role (Item 1.a), because the leader cannot benefit from the follower–guarantor advantage. In contrast, the follower constantly benefits from claiming the follower–guarantor advantage (Item 1.b). The follower may benefit from the free‐rider role, but such a benefit alone (without the leadership advantage) cannot exceed the follower–guarantor advantage. Conversely, a non‐guarantor free‐rider cannot claim the follower–guarantor advantage and, thus, strongly prefers to acquire the leadership advantage (Item 2.a). Consequently, as shown by the analysis, the dual role of leader and free‐rider is often the most attractive choice, whereas simultaneously being the follower and free‐rider is the worst.

The second major message indicates that the guarantor must choose between the leadership advantage and the follower–guarantor advantage (Item 2.b). This message is more intriguing than the first one. In particular, as the Stackelberg leader, the guarantor enjoys the dominant power, but is deprived of the follower–guarantor advantage. In contrast, a follower–guarantor misses the Stackelberg leadership advantage. We find that the guarantor’s preference of a leadership role depends on the financial risk level. The Stackelberg leader has a large room to increase its own profit margin when the guarantor’s financial risk level is sufficiently low (i.e.,

The guarantor’s choice of the leadership role also reflects the battle between the leadership advantage and the follower–guarantor advantage. Theorem 5 reveals that these two advantages vary over the financial risk level (i.e., the retailer’s default level). Overall, if the demand variance is high or the retailer is likely to default, the guarantor would benefit more as the follower than as the leader.

Comparison of Leadership Structures

This subsection conceptually supposes that the firm can choose between different leadership structures by comparing the Nash game with the Stackelberg game to explore whether a shorter decision hierarchy is better than a longer decision hierarchy. There is a perception that a shorter decision hierarchy is more efficient than a longer one. Similarly, in the context of this study, because of its shorter decision hierarchy, a Nash game might be considered more efficient than a Stackelberg game for the whole supply chain. We find this perception is true under bank financing, but the outcome could be reversed under guarantor financing.

Leadership Structure Analysis under Bank Financing

This subsection shows that the comparison result in bank financing without a guarantor’s influence fits the conventional wisdom where a supply chain with a shorter decision hierarchy is more efficient than that with a longer decision hierarchy. The comparison result is given as follows.

In bank financing, the retailer, 3PL, and supply chain prefer the Nash game (i.e.,

The underlying rationale for Theorem 6 lies in the triple marginalization in the manufacturer Stackelberg leadership game and the manufacturer leadership advantage. First, typically, a supply chain with a shorter supply chain decision hierarchy (in the Nash game) is more efficient than a longer one (in the Stackelberg game), because the triple marginalization of a longer supply chain decision hierarchy leads to a lower order quantity than that of a shorter decision hierarchy.

Second, being a Stackelberg leader in bank financing is the best choice for upstream firms (

Overall, the retailer, the 3PL, and the whole supply chain all suffer from the aforementioned worse triple marginalization, and the retailer and the 3PL further suffer from the follower disadvantages in the Stackelberg game. In other words, the whole supply chain benefits from a shorter decision hierarchy (i.e., the Nash game is preferred over the Stackelberg game). In contrast, for the manufacturer, the leadership advantage outpaces the triple marginalization harm, so the manufacturer leadership Stackelberg game is preferred.

Leadership Structure Analysis under Manufacturer Guarantor Financing

We obtain the following result by comparing the performance of MG between the Nash game and the manufacturer leadership Stackelberg game.

In MG, the retailer, 3PL, and supply chain prefer the Nash game (i.e.,

The conventional wisdom in Theorem 6 sustains under MG. In other words, the triple marginalization and follower disadvantages in the Stackelberg game continue to hurt the retailer, the 3PL, and the whole supply chain; as a result, they all prefer the Nash game. In fact, as the Stackelberg leader and guarantor, the manufacturer bears the retailer’s potential default risk and, thus, charges a higher risk premium than that under the Nash game and earn more profit, but at the expense of other firms. Correspondingly, the negative impact of triple marginalization is worsened, as the leadership advantage is widened, in the Stackelberg game, such that the state of the retailer, the 3PL, and the whole supply chain is aggravated as compared to that under BF, whereas the manufacturer is better off. As a result, the profit gaps between the Nash game and the Stackelberg game for all firms are indeed even wider under MG than under BF.

Leadership Structure Analysis under 3PL Guarantor Financing

We compare the performance of LG under different leadership structures and achieve the following result.

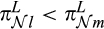

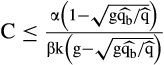

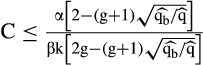

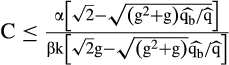

In LG, if

Unlike the findings in BF and MG, Theorem 8 reveals a different outcome that under LG the retailer, 3PL, and supply chain conditionally prefer a longer decision hierarchy (i.e., Stackelberg game) than a shorter one (i.e., Nash game). Note that the triple marginalization and follower disadvantages persist in the Stackelberg game. However, the trade‐off is subtler when the 3PL provides the guarantor financing. For the manufacturer, the leadership advantage continues to dominate the triple marginalization harm, so it still prefers the manufacturer leadership Stackelberg game. But, for the 3PL, the retailer, and the whole supply chain, the follower–guarantor advantage starts to play a critical role under certain conditions.

In particular, if the financial risk is sufficiently low (i.e.,

When financial risk is substantially high (i.e.,

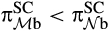

Figure 2 further illustrates the impact of the financial risk level on the supply chain’s preference of leadership structure. The parameter values are the same as those in Figure 1 except that we set

Supply Chain Profits under LG with Respect to Demand Variance Given

Extensions

We explore three extensions, namely, impact of cost structure, impact of retail pricing rules, and impact of initial capital.

Impact of Cost Structure with Economies of Scale

We generalize the cost structure of upstream firms to examine the impact of cost structure. We assume that the manufacturer’s and the 3PL’s total operational costs are in the form of

We further assume that

By comparing MG/LG and BF under both leadership structures, we find that guarantor financing is more attractive than bank financing when upstream firms are sufficiently cost‐efficient (i.e., upstream firms do not have severe diseconomies of scale). The result is consistent with our former finding that MG/LG can be better than BF when

Our analysis shows that the preference between MG and LG by different firms remains unchanged in the Nash game. In the Stackelberg game, the 3PL’s preference relies on the (dis)economy scale level, although the preferences of the manufacturer, the retailer, and the whole supply chain remain independent of the (dis)economy scale level. We state these findings in Theorem 9, which is an extension of Theorem 4.

Under the manufacturer leadership Stackelberg game:

The manufacturer, the retailer, and the whole supply chain prefer LG to MG (i.e., For the 3PL, given

Theorem 9 reveals that the 3PL does not always prefer LG to MG under manufacturer leadership. This result is different from the case of the linear cost structure without considering the (dis)economy scale level. The rationale behind this finding is as follows. As previously discussed, the 3PL faces a three‐facet trade‐off for serving as the guarantor in LG. The three facets include positive demand effect, positive revenue effect, and negative financial‐risk effect. When the manufacturer has substantial diseconomies of scale (i.e.,

We also find that the retailer and the 3PL’s preferences of different supply chain decision structures are affected by the (dis)economies of scales, although the manufacturer’s preference remains unchanged, as displayed below.

Consider LG. The retailer, the 3PL, and the supply chain prefer the Nash game (i.e., The manufacturer prefers the manufacturer leadership game (i.e., Extension of Theorem 8

The comparison between Theorem 10 and Theorem 8 shows that the impact of (dis)economies of scales on the retailer’s and 3PL’s preferences is not qualitative, but only quantitative. The difference is that, if the follower 3PL in the Stackelberg game has economies of scale (

We then conclude that extending the baseline model with a unit cost to a more general cost structure does not significantly alter our main findings. Our main qualitative findings (e.g., the observations on the follower–guarantor advantage and the higher performance in the supply chain with a longer decision hierarchy than in the supply chain with a shorter decision hierarchy) continue to hold as long as the upstream firms’ (dis)economies of scale are contained.

Impact of Retail Pricing Rules

Our baseline model assumes a markup retail price scheme to reflect the reality that the retailer will likely adjust its retail price as the wholesale price varies. Markup retail price can be considered an intermediate case between an exogenous retail price and an endogenous one. Nevertheless, numerically we observe that markup retail pricing can conditionally outperform the endogenous retail pricing; this occurs because a fixed markup prevents the upstream firms from increasing their prices, such that the triple marginalization problem is softened. This numerical finding might partially justify the use of markup retail pricing in practice. To study the influence of different pricing assumptions, we discuss guarantor financing practices under exogenous and endogenous pricing schemes. We start with the exogenous price as follows.

Impact of Exogenous Pricing

Given that reality is uncertain and evolves quickly, the assumption of an exogenous retail price is an extreme scenario. The condition where any retailer will never increase its retail price is hardly true even if the wholesale price skyrockets. Nevertheless, the exogenous retail price assumption has been used often in newsvendor models for tractability. Thus, we examine firm performance in guarantor financing with an exogenous retail price.

If the retail price is exogenous, the Stackelberg leader under manufacturer leadership in MG and LG sets the prices as high as possible and obtains all unreserved supply chain profit, whereas in the Nash game, the two upstream firms share the profit. In both game settings, the retailer only earns the reserved profit.

The result of Corollary 3 is expected because similar results have been reported in the extant literature on newsvendor Stackelberg games. Given that the retail price is fixed, the expected demand is constant. Under manufacturer leadership, the Stackelberg leader has the incentive to hike the price/rate and extracts all extra unreserved profit from the followers. If the other upstream firm is a guarantor, the firm will earn positive revenues, but its expected profit is zero due to the financial risk cost incurred by the retailer’s potential default. At the bottom of the supply chain, the retailer is powerless, especially when the retailer borrows from the bank under either guarantor financing scheme. Therefore, the retailer is indifferent between MG and LG. This result further confirms that not every retailer can benefit from guarantor financing, particularly if it is deprived of the power of retail pricing.

Impact of Endogenous Pricing

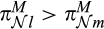

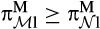

We then examine endogenous retail pricing. We firstly consider the assumption that price decision is made before demand realization. In this scenario, the retailer must simultaneously decide on the retail price and order quantity, which is analytically intractable. Employing the same numerical experiment setting as former ones, we can demonstrate that under the manufacturer leadership Stackelberg game, all supply chain members, except 3PL, prefer LG to MG (see Figure 3). The 3PL prefers to be the guarantor only if

Profits of Different Financing Schemes under Endogenous Pricing and Manufacturer Leadership Stackelberg Game with Respect to the Manufacturer’s Cost

Similar to that in our markup pricing setting, guarantor financing is more attractive than bank financing for the upstream firms and supply chain when the upstream firms are cost efficient. However, the retailer performs better in bank financing because the former gains more discretion under the assumption of endogenous pricing than under exogenous pricing.

We also explore a different endogenous pricing setting by allowing the retailer to decide the retail price after demand realization, an assumption like that in Kouvelis, et al. (2018). Although the firms’ preferences are very similar to those when the retailer decides the retail price before demand realization, either the manufacturer or the 3PL might prefer to be the guarantor, because they can earn a higher profit margin when the retailer can price after demand realization. Given the complexity of this extension, this topic on endogenous retail pricing—either before or after demand realization—remains a top research priority.

Impact of Initial Capital

For tractability, we assume zero initial capital for the retailer in our baseline model. For a model that includes a manufacturer, a 3PL, a retailer, and a bank, the analysis instantly becomes intractable when the retailer’s initial capital is positive. As Kouvelis and Zhao (2012) show, optimal decisions are mostly determined by implicit functions for a two‐party supply chain model with a positive initial capital. A similar analytical impasse occurs in the two‐firm supply chain models analyzed by Jing et al. (2012). To shed light on the impact of the initial capital on our main results, we only employ numerical experiments to examine the impact of the initial capital on the optimal solutions of different financing schemes.

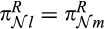

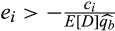

Figure 4 demonstrates how the firms’ profits change over the initial capital level in the manufacturer leadership Stackelberg game. First, the profits of the manufacturer under MG and the 3PL under LG initially increase and then decrease with initial capital within certain ranges. We explain the phenomenon from the trade‐off between the aforementioned financial‐risk effect, revenue margin, and demand effect. Notably, the retailer may become more risk‐seeking by ordering more when its initial capital is lower, because its loss is limited up to its entire initial capital. As shown in Figure 5a, the retailer tends to order less as the initial capital grows and, thus, the financial‐risk effect, revenue margin, and demand effect for the guarantor in either LG or MG diminish. Initially, the financial risk can be more substantially subdued when the initial capital is lower (vs. when the initial capital is higher). Thus, the benefit of financial risk reduction effectively outplays the reduced revenue‐margin effect [e.g., see the wholesale price (

Profits of Different Financing Schemes under Manufacturer Leadership Stackelberg Game with Respect to the Initial Capital Given

Firms’ Optimal Decisions under Different Financing Schemes under Manufacturer Leadership Stackelberg Game with Respect to the Initial Capital Given

We previously find that LG is always better than MG for every supply chain member when the retailer has no initial capital. The result still holds when the initial capital is not sufficiently high. On the other extreme, when the initial capital is abundant (no capital‐constrained), the retailer no longer requires external financing; therefore, no difference exists between these three different financing schemes. When the retailer’s initial capital is slightly insufficient (i.e., the retailer is only slightly capital constrained), the retailer does not borrow immediately because of the non‐zero risk‐free interest rate. In this situation, the retailer prefers to order a slightly decreased quantity under no financing to avoid any potential financing cost.

However, we observe that under the manufacturer leadership Stackelberg game, MG can outperform LG for every supply chain member when the initial capital is at the moderate level where the retailer still needs financing. Given that the manufacturer’s financial risk in MG is considerably diminished due to the substantial initial capital, the manufacturer is willing to reduce the wholesale price in exchange for an increased order quantity from the retailer [see Figures 5a and b]. Given that the manufacturer is the Stackelberg leader, its impact in MG is greater than that in LG. This observation indicates that the follower–guarantor advantage scales down as the initial capital builds up. In this situation, MG outperforms LG for all firms.

Conclusions

This study investigates two schemes of guarantor financing, namely, MG and LG, in a four‐party supply chain game that features a manufacturer, a 3PL, a capital‐constrained retailer, and a bank. We first analyze the MG, LG, and BF in a game where the two upstream firms decide simultaneously (Nash game). We find that the supply chain members may still choose MG or LG over BF, provided that the BF is viable for the retailer. However, a free‐rider dilemma exists in the Nash game, wherein both upstream firms prefer the other firm to be the guarantor. We then observe that such free‐rider dilemma can be resolved if the manufacturer emerges as the Stackelberg leader in a Stackelberg game between the two upstream firms, such that all firms prefer the follower assuming the guarantor role. This finding reveals the follower–guarantor advantage, which can thoroughly compensate for the Stackelberg follower disadvantage. This finding means that the follower may prefer to bear the financial risk as the guarantor. In fact, the follower–guarantor advantage can be so strong that a guarantor might decline the Stackelberg leadership despite being given such an opportunity. Our extended discussion shows that the follower–guarantor advantage decreases with the retailer’s initial capital level. Overall, the Stackelberg leadership raises the probability that guarantor financing outperforms bank financing. Moreover, by comparing the firms’ performances among the two game settings (i.e., Nash vs. Stackelberg), we observe that a supply chain with a longer decision hierarchy (i.e., Stackelberg) can conditionally outshine that with a shorter decision hierarchy (i.e., Nash). This outcome exhibits the benefit of having a focal firm as the Stackelberg leader in the supply chain.

Our results deliver several managerial implications. First, both guarantor financing and bank financing can outperform each other. Thus, a capital‐constrained firm should be further selective in financing scheme than retaining bank financing alone. Second, when multiple upstream firms, such as the manufacturer and the 3PL, are present, the capital‐constrained retailer should consider requesting for guarantor financing from the less dominant firm along the supply chain (i.e., the follower) instead of the most dominant firm (i.e., leader). Finally, under guarantor financing, a longer decision hierarchy can be better than a shorter one. Therefore, encouraging a focal firm to serve as the Stackelberg leader of the supply chain may benefit all firms.

This study is the first attempt to address manufacturer guarantor financing and 3PL guarantor financing in a four‐party game with two types of leadership structures. However, this study has some limitations due to the analytical complexity caused by the four‐party interaction. First, we assume common knowledge about demand uncertainty as applied in most related literature. Nevertheless, exploring these financing schemes is attractive from the perspective of the incentive theory. For example, demand uncertainty becomes incomplete information to upper stream firms. Second, we adopt markup retail pricing because of its popularity in practice and tractability, but our future research priority is to investigate the impact of other potential retail pricing strategies. Third, consistent with extant literature, we assume that the retailer will maximize its profit. In practice, the retailer may decide to maximize the probability of making a predetermined profit. If profit maximization is correlated with maximizing the probability of meeting a profit target, we suspect that our qualitative results will hold. Fourth, we realize that our outcomes can differ if the demand function is converted from a multiplicative form to an additive form. Although the analysis of an additive form becomes extremely challenging in our model setting, this direction remains a priority for our future research. Fifth, our main analysis assumes zero initial capital for tractability. However, we find that the initial capital level can influence the firms’ advantages in extensions. Therefore, this issue must be addressed in a tractable, but potentially simplified model in the future. Finally, examining the impact of salvage value, stock‐out penalty, and supply chain coordination is another priority topic for further investigation.

Footnotes

Acknowledgments

The authors are listed in reverse alphabetical order and contributed equally to this work. They are co‐first authors and co‐corresponding authors. We thank the department editor, Eric Johnson, the senior editor, and the two anonymous referees for their very insightful and constructive comments. Weihua Zhou acknowledges the support from the National Natural Science Foundation of China (Grants no. U1509221, 71571160) and National Key R&D Program of China (No. 2019YFB1404901). Gangshu Cai acknowledges the support from the National Natural Science Foundation of China through grant #71629001 and Santa Clara University research scholarship programs.