Abstract

Refurbishing of used products is increasingly being recognized as a value recovery strategy in sustainable operations. Hence, manufacturers, retailers, as well as third‐party firms, engage in refurbishing. Manufacturers, to some extent, can deter other players from refurbishing through various means such as product design, intellectual property, and restricting access to spare parts and diagnostic tools. While previous research has extensively examined the question of whether a manufacturer should allow an independent third‐party player to refurbish used products, the question of whether a manufacturer should allow his retailer to refurbish them, to our knowledge, remains unanswered. In this study, we examine whether a manufacturer should refurbish used products himself or allow his retailer to refurbish them. We compare two closed‐loop supply chain structures: Model‐M, where the manufacturer refurbishes used products; and Model‐R, where the retailer refurbishes. In a two‐period setting, new products are sold in both periods and some of the first‐period products are refurbishable in the second period. We show that when either (i) the refurbishability of used products is low and the attractiveness of refurbishing (value of the refurbished product as compared to the refurbishing cost) is either moderate or sufficiently high, or (ii) the refurbishability is high and the attractiveness of refurbishing is moderate, the manufacturer, despite forgoing profits and facing competition from refurbished products, is better off with letting the retailer refurbish used products (Model‐R) than with refurbishing them himself (Model‐M). Identifying a novel mechanism through which the manufacturer benefits in Model‐R is our key theoretical contribution to the closed‐loop supply chain literature. Moreover, we provide some useful and interesting insights to policymakers related to customer welfare and the environment. We also analyze the performances of these models (Model‐M and Model‐R) in terms of supply chain efficiency. In addition, we discuss how some of our key results change if a third‐party refurbisher coexists with the manufacturer and the retailer. Our results not only support some of the current policies and practices but also shed some light on their limitations and suggest some avenues for improvement.

Introduction

Refurbishing has widely been acknowledged by both practitioners and researchers as a profitable value recovery proposition and an environment‐friendly activity. As a result, firms are increasingly adopting this practice to gain a competitive advantage and enhance their brand image (Agrawal et al. 2019). In 2017, the market for refurbished smartphones grew by more than 13%, with 140 million units in sales, while the market for new smartphones had a modest growth of just 3% (Kang 2018). Persistence Market Research (PMR) predicts that sales of refurbished smartphones will grow 9.8% annually from 2018 to 2026, surpassing US$44 billion (PMR 2018). A similar trend is also observed in other categories such as PCs and laptops, driven by increasing demand for affordable products and growing environmental awareness. Refurbishing is not just restricted to manufacturers; retailers are also actively involved in refurbishing activities. For instance, GameStop, which operates a refurbishing factory, in 2013, earned about 25% revenue and roughly half of its profit from refurbishing used products and then reselling them to customers (Wang et al. 2017). Other retailers such as Best Buy and Newegg also have dedicated divisions to refurbish used products (e.g., Best Buy has Geek Squad division).

The growth of the refurbishing market is, however, accompanied by challenges for manufacturers. Manufacturers generally consider refurbishing of their used products by other players as a threat to their new products. Therefore, manufacturers often make it harder to refurbish their used products by employing various tactics such as designing less remanufacturable products, restricting access to spare parts and diagnostic tools, and not sharing repair manuals. For instance, Apple glues the battery of “Retina MacBook 2015” to the case, complicating the replacement of the battery. Manufacturers are also increasingly using software locks to prevent the refurbishing of their products by other players. For example, Apple disables the iPhone 7 and the iPhone 7 Plus when the owners of these phones get home buttons or screens replaced by other than Apple's authorized service centers (Koebler 2017), and disallows consumers from accessing battery health diagnostic tools if the phone batteries (even if genuine) are replaced by a third party (Campbell 2019). These practices have also been supported by the existing literature on refurbishing (Atasu et al. 2008, Debo et al. 2005, Ferguson and Toktay 2006), which mostly shows that a manufacturer is hurt when a third‐party player refurbishes used products. For instance, Apple has recently sued its recycling partner (GEEP) because the latter refurbished products that are meant to be only recycled (Carrique 2020).

Anecdotal evidence, however, suggests that manufacturers sometimes not only allow their retailers to refurbish used products but also enhance their retailers’ refurbishing capabilities by providing them with spare parts, diagnostic tools, and advanced repair equipment. For instance, Apple has installed proprietary screen‐repair machines at Best Buy, allowing Best Buy to fix broken iPhone screens and refurbish the phones more efficiently (Carnoy 2017). Thus, Apple facilitates the refurbishing of iPhones by Best Buy, which is also a retailer for Apple's new products.

The extant literature examines the implications of refurbishing by independent third‐party players. However, to the best of our knowledge, the implications of refurbishing by a retailer for supply chain profits have not been investigated thus far. The key difference between an independent third‐party refurbisher and a retailer is that the retailer sells the manufacturer's new products while the independent refurbisher does not. When the retailer refurbishes used products and sells them, she also makes decisions about the retail prices and the quantities of the manufacturer's new products. This strategic link between new products and refurbished products exists when the retailer refurbishes while it is absent when only a third party refurbishes. In this study, we examine the question of whether a manufacturer should refurbish used products himself or allow his retailer to refurbish, and aim to provide a theoretical rationale for manufacturers accommodating their retailers.

Contributions and Key Findings

This study's key focus is to investigate a manufacturer's optimal choice of closed‐loop supply chain structure. We specifically compare two closed‐loop supply chain structures: Model‐M and Model‐R. In Model‐M, the manufacturer (he) refurbishes used products and sells them through the retailer (she). In Model‐R, the retailer refurbishes used products and sells them directly to customers. We consider a two‐period setting to capture the intertemporal link between new products and their refurbished versions. In the first period, the manufacturer sells new products to the retailer, who, in turn, sells them to customers. In the second period, the manufacturer may again sell new products through the retailer. Besides, the products sold in the first period can be refurbished in the second period.

The key question we investigate is: Should a manufacturer allow his retailer to refurbish used products? If yes, under what conditions? As we mentioned earlier, the existing literature, while extensively studied refurbishing by third‐party players, has not examined this question. Intuitively, one would think that the manufacturer should deter the refurbishing by his retailer. This is so because the manufacturer has to forgo the profit from refurbishing and face competition from refurbished products if he allows the retailer to refurbish used products. On the contrary, our results suggest that, under certain conditions, the manufacturer, despite forgoing profits and facing competition from refurbished products, is better off with allowing the retailer to refurbish used products instead of refurbishing them himself.

The above result differs from the findings of past studies (e.g., Atasu et al. 2008, Debo et al. 2005, Ferguson and Toktay 2006) that mostly highlight adverse effects of the entry of third‐party refurbishers on a manufacturer and recommend strategies the manufacturer can adopt to restrict remanufacturing by third parties. Unlike the independent refurbisher, who sells only refurbished products, the retailer sells both the new and the refurbished products, linking both markets. Our findings suggest that this link results in a positive strategic effect on the manufacturer. Therefore, this study provides both theoretical and managerial contributions: our findings (i) suggest that refurbishing by the retailer is quite different from the refurbishing by a regular independent third‐party refurbisher, and thus the findings of the existing literature on refurbishing by a third party should not be extended to the supply chain context; and (ii) provide guidance to managers on when a manufacturer should authorize his retailer to refurbish used products.

Since our results differ from those of the existing literature that has examined a third‐party refurbisher, we extend our analysis to a setting where an independent third‐party refurbisher exists in the market along with the retailer. The previous literature highlighted the negative effect of a third‐party refurbisher on the manufacturer's profit. Intuitively, one would think that the presence of a third‐party refurbisher would change our results and might dissuade the manufacturer from also allowing his retailer to refurbish the used products. Therefore, we examine the following question: Should a manufacturer allow his retailer to refurbish used products in the presence of an independent third‐party refurbisher? Interestingly, our key findings remain qualitatively the same even in the presence of a third‐party refurbisher.

The new and refurbished products are linked since today's new products are the source of used products and thus of refurbished products sold in the future. Hence, it is essential to examine how the pricing and the sales quantity decisions of the new product sold in the first period are affected by the perceived quality of the refurbished product, ceteris paribus. Therefore, we examine the following research question: How does the quality of refurbished products affect the pricing and quantities of the new products in each model? As the quality of refurbished products increases, for a given refurbishing cost, refurbishing becomes more attractive in Model‐M and a stronger threat in Model‐R for the manufacturer. Intuitively, as the quality of refurbished products increases, the manufacturer in Model‐M should decrease his wholesale price of new products to sell more new products in the first period and thus refurbish more products in the second period. On the other hand, the manufacturer in Model‐R should intuitively increase his wholesale price of new products in the first period to restrict the supply of used products, and thereby limit refurbishing. Surprisingly, our findings in Model‐R, unlike in Model‐M, contradict our intuition. Specifically, when the perceived quality of refurbished products is moderate, the manufacturer in Model‐R decreases (rather than increases) his wholesale price as the quality of refurbished products increases. This result in Model‐R supports our earlier finding that refurbishing by the retailer is not necessarily a threat to the manufacturer.

Refurbishing may have an impact on not only the manufacturer but also the whole supply chain, the environment, and customers. Therefore, we examine the implications of the refurbishing structure on these stakeholders. Policymakers are increasingly demanding for environment‐friendly business practices (Xia et al. 2018). Refurbishing is also considered as an environment‐friendly and sustainable practice (Wang et al. 2017). For instance, end‐of‐use products can be refurbished and sold back to customers instead of being disposed of in landfills. In order to improve the sustainability of operations, policies have primarily focused on regulating manufacturers to manage their used products. For instance, Extended Producer Responsibility (EPR) policies require that manufacturers responsibly dispose of their post‐consumer products (OECD 2016, Rajapakshe et al. 2013, Subramanian et al. 2009). However, it is not clear what role a retailer can play in improving sustainability. Therefore, we investigate the role of a retailer in refurbishing of used products and examine the following question: Can allowing the retailer to refurbish used products be more environment‐friendly compared to the case when the manufacturer refurbishes himself? Interestingly, our findings show that when the retailer refurbishes used products, the environment has less negative impact than when the manufacturer does so. Therefore, our results suggest that policymakers should consider the possibility of making retailers more responsible for managing used products.

Regulators, such as the Federal Trade Commission, have always been concerned about the impact of business practices on customers’ welfare. Refurbishing has direct implications on customers’ welfare as it offers them an option to buy products of lower quality at lower prices. Having more options should increase the customer welfare (Liu and Cui 2010), but it is not clear as to which closed‐loop supply chain structure offers customers higher welfare. Bills such as the “right‐to‐repair” aim to force manufacturers to allow other parties to repair and refurbish their products. In our paper, we investigate whether passing such bills improves the customer welfare by allowing the retailer to refurbish. We specifically ask the following question: Can refurbishing of used products by the retailer (than by the manufacturer) give customers higher welfare? Our findings only partly support regulators’ claims. We show that only when the perceived quality of refurbished products is moderate, customer welfare in Model‐R (when the retailer refurbishes) is greater than in Model‐M (when the manufacturer refurbishes). However, when the perceived quality is either low or high, refurbishing by the manufacturer is better for the customers.

Supply chain efficiency has always been a concern for both managers and scholars (Cachon 2003, Jeuland and Shugan 2008, Li 2019, Shi et al. 2013b, Xia et al. 2018). We examine two closed‐loop supply chain structures, and compare the efficiencies of these two models. Specifically, we investigate: Can allowing the retailer to refurbish products make the supply chain better off than when the manufacturer refurbishes? We find that only when the perceived quality of refurbished products is moderate, under some conditions, the supply chain is better off in Model‐R than in Model‐M.

Finally, we investigate the conditions under which all stakeholders are better off with the same player refurbishing (manufacturer vs. retailer). We specifically ask the following question: Can the manufacturer's decision of who should refurbish used products also maximize the total supply chain profit, customer welfare, and environmental benefit? Our findings suggest that only when the retailer refurbishes used products (Model‐R), it is possible to simultaneously achieve a higher profit for the manufacturer, a more efficient supply chain, higher customer welfare, and lower negative environmental impact. This equilibrium exists for moderate values of perceived quality of refurbished products.

Overall, our analysis contributes to the refurbishing literature by examining different possible modes of refurbishing (by the manufacturer, the retailer, or the third party) and provides guidance to policymakers about the impact of refurbishing on different stakeholders. In the following subsection, we review the relevant literature.

Literature Review

In this study, we contribute to the closed‐loop supply chain literature. Our study is related to two different streams of research in the closed‐loop supply chain. The first stream investigates the impact of refurbishing (or remanufacturing) and the second stream examines the effect of the closed‐loop supply chain structure on various stakeholders. In the following subsections, we relate our work to each stream of literature and highlight our contributions.

Impact of Refurbishing

This stream of research examines the implications of refurbishing (or remanufacturing) used products in the market (Ferguson and Souza 2010, Guide and Wassenhove 2009). This literature has examined two key questions. The first question is whether and when a firm should refurbish used products. The cannibalization of new products by refurbished products has been an essential concern highlighted in the literature (e.g., Guide and Li 2010, Zhang and Zhang 2018). The complexity in managing used products lies in the fact that refurbished products are both substitutes for and complements to new products; the complementarity arises because the number of used products (cores) available for refurbishing is constrained by the number of new products sold previously (e.g., Atasu et al. 2008, Ferrer and Swaminathan 2006). When refurbishing is sufficiently attractive, the firm might deliberately underprice new products today in order to generate more used products in the future (Debo et al. 2005). Atasu et al. (2008) show that, under competition (either from another firm offering the new product or from a local refurbisher), refurbishing can be an effective marketing strategy for a firm in defending its market share through price discrimination. This stream of literature has examined the impact of refurbishing in the context where a firm directly sells products to customers. We contribute to this stream of literature by introducing a retailer in the supply chain. In the presence of a retailer, the manufacturer does not set the retail prices for customers, which might change his incentives in refurbishing.

The second question in the refurbishing literature is whether and when a firm should allow independent third‐party players to refurbish used products. If a manufacturer chooses not to refurbish used products, third‐party players may refurbish them, creating a competition for the manufacturer's new products. The literature examines the implications of potential competition from third‐party refurbishers on the manufacturer's profit (e.g., Ferguson and Toktay 2006, Majumder and Groenevelt 2001). This literature mostly highlights the adverse effects of the entry of third‐party refurbishers on a manufacturer and recommends strategies the manufacturer can adopt to restrict remanufacturing by third parties (Atasu et al. 2008, Debo et al. 2005, Ferguson and Toktay 2006). However, the literature also identifies a few benefits of refurbishing by a third‐party player to the manufacturer (Agrawal et al. 2015, Oraiopoulos et al. 2012). Agrawal et al. (2015), through a behavioral experiment, show that the perceived value of the new product sold by the manufacturer is higher in the presence of the remanufactured product offered by a third party than that by the manufacturer himself. Oraiopoulos et al. (2012), in a situation where the original equipment manufacturer (OEM) does not participate in remanufacturing and charges a relicensing fee to third‐party remanufacturers, find that the OEM's profit increases in the number of third‐party remanufacturers, stemming from both relicensing fee and resale value of new products.

In sum, the literature on refurbishing suggests that a manufacturer is worse off with other players refurbishing unless he can generate revenue from refurbished products (e.g., relicensing fee) or the increase in the customer's willingness to pay for new products (e.g., through a higher resale value or perceived value). In our paper, we control for these benefits by considering a setting where the manufacturer does not benefit directly from refurbishing and where customers’ willingness to pay does not change. We show that, even in the absence of the factors proposed in the literature, a manufacturer can benefit from refurbishing by another entity (the retailer in our context). Our results unveil a novel strategic factor stemming from the link between the new products and the refurbished products when the retailer refurbishes used products.

Closed‐Loop Supply Chain Management

Our paper contributes to the literature on the closed‐loop supply chain by examining the role of supply chain members in the reverse supply chain. Shulman et al. (2011) examine the question of who should collect used products that are remanufactured by the manufacturer. They show that both the retailer and the manufacturer are better off when the retailer collects used products. Shulman and Coughlan (2007) show that the manufacturer benefits by letting his retailer collect and sell used products. They show that used products increase the supply chain profit that can be captured by the manufacturer through a coordination mechanism such as a two‐part tariff. Shulman et al. (2010) examine the question of who should salvage the product returns in a supply chain and show that the manufacturer should accept and salvage the returns even if the retailer is more efficient in salvaging. However, this literature has not examined the question of who should refurbish in a supply chain context, which is the focus of our paper. To the best of our knowledge, implications of refurbishing in a supply chain context, where either the retailer or the manufacturer is refurbishing, has not been investigated. Retailers are different from third‐party refurbishers as they are partners of manufacturers for selling new products. Therefore, refurbishing of used products by the retailer can influence pricing and sales decisions for new products, and thereby profits of the manufacturer and the retailer.

The remainder of this study is organized as follows. In Section 2, we introduce the model setup and develop the modeling framework. Section 3 analyzes equilibria of the two‐period model. Section 4 discusses the manufacturer's choice of who should refurbish the used products and investigates the implications of both Model‐R and Model‐M on the supply chain, environment, and the customer welfare. Section 5 extends the analysis to a setting where an independent third‐party refurbisher also exists. Section 6 analyzes several other extensions. Section 7 concludes with a discussion of our results, the managerial implications, and limitations.

The Model

In practice, we can find examples where manufacturers, such as Apple and Samsung, refurbish their own products. In addition, we can also find examples where retailers, such as Best Buy, Newegg, and GameStop, refurbish the products. Therefore, we consider a supply chain consisting of a manufacturer and a retailer. The manufacturer produces and sells new products (e.g., smartphones) through the retailer (e.g., Apple sells through Best Buy). New products depreciate over time and these used products can be refurbished. The primary goal of this study is to investigate whether and when a manufacturer (e.g., Apple) should allow its retailer (e.g., Best Buy) for new products to refurbish used products. Therefore, we examine two closed‐loop supply chain structures: manufacturer refurbishing (Model‐M) and retailer refurbishing (Model‐R). In Model‐M, the manufacturer refurbishes used products and subsequently sells them through the retailer. In Model‐R, the retailer refurbishes used products and sells them to customers. Thus, the retailer sells both the new and the refurbished products to customers regardless of who refurbishes. Subsequently, in Section 5, we also analyze a setting where a third‐party refurbisher coexists along with the manufacturer and the retailer.

Model Setting

Following the previous literature that has examined the refurbishing problems in a finite horizon setting (e.g., Atasu et al. 2008, Ferguson and Toktay 2006, Ferrer and Swaminathan 2006, Majumder and Groenevelt 2001, Oraiopoulos et al. 2012), we consider a two‐period model whereby in the first period, only new products are available, and in the second period, used products are generated and can be refurbished and sold along with new products. In the first period, the manufacturer sells new products at wholesale price

Since refurbished products are derived from new products sold in the first period, the quantity of refurbished products that can potentially be sold in the second period is constrained by the number of new products sold in the first period. Thus, the decisions made in the first period could affect the decisions made in the second period.

Empirical research (Guide et al. 2006, Guide and Li 2010, Subramanian and Subramanyam 2012) shows that customers perceive refurbished products to be of lower quality than new products. Consistent with empirical research and in line with theoretical literature (Atasu et al. 2008, Ferguson and Toktay 2006, Oraiopoulos et al. 2012), we consider that customers have a lower willingness to pay for refurbished products compared to new products. The perceived quality of the refurbished products relative to the quality of the new products is captured by parameter δ ∈ (0,1). Thus, a customer of type θ's net utility from buying a refurbished product is U r = θδv − p r .

Customers make their purchase decisions to maximize their net utilities. Following the past literature (e.g., Ferguson and Toktay 2006, Oraiopoulos et al. 2012), we consider that each customer buys at the most one unit of the (new or refurbished) product in a period and the market size is normalized to one. In the second period, given the retail prices for the new and the refurbished products, a customer of type θ buys the new product if and only if U

2 ≥ max{U

r

, 0} and buys the refurbished product if U

r

≥ max{U

2, 0}. The customer of type θ

2 is indifferent between buying the new product and buying the refurbished product, while the customer of type θ

r

is indifferent between buying the refurbished product and not buying any of the products. Thus, the demands of the new (q

2) and the refurbished products (q

r

) in the second period are given by:

Closed‐Loop Supply Chain Models

In this section, we describe the sequence of decisions and the optimization problems of the manufacturer and the retailer in each model.

The Manufacturer Refurbishes Used Products: Model‐M

In this model, we follow a sequence of decisions commonly used in the supply chain literature (e.g., Bresnahan and Reiss 1985, Cachon 2003, Cachon and Kök 2010, Perakis and Roels 2007). At the beginning of the first period, the manufacturer sets the wholesale price

We solve the problem using backward induction, starting with the customers’ purchase decisions in the second period based on the demand functions. We denote the profit of player j for period k in Model i by

In the second period, the retailer, given the demand functions in (1), maximizes her second‐period profit by setting the retail prices p

2 and p

r

. The retailer solves the following optimization problem:

In the first period, given the wholesale price

The Retailer Refurbishes Used Products: Model‐R

In this model, since used products are refurbished and sold by the retailer, the wholesale price of the refurbished product is absent. The remaining decisions are the same as in Model‐M. Thus, in the second period, the manufacturer sets the wholesale price for the new product (

We solve Model‐R using backward induction. The customer's decisions are similar to those in Model‐M. In the second period, the retailer optimizes the retail prices p

2 and p

r

by solving:

The manufacturer's problem in the second period is to set the wholesale price

In the first period, given the wholesale price

Equilibria Analysis

In this section, we solve each model using backward induction. We first solve the retailer's optimization problem of setting the retail prices of the new and refurbished products in the second period. We then solve the manufacturer's wholesale price decisions in the second period (the wholesale price of the new product in Model‐R and wholesale prices of new and refurbished products in Model‐M). Subsequently, we solve the first‐period retail price decision of the retailer followed by the first‐period wholesale price decision of the manufacturer. In the following subsections, we present our results in the same order (backward induction): the second‐period Subgame equilibrium as a function of the first‐period decisions followed by the complete two‐period equilibrium results. The analysis is focused on the most interesting parameter space, where new products are sold in each period (i.e., q 2 > 0 and q 1 > 0). In this space, the refurbished products are not so attractive that they eliminate the sales of new products (i.e., δv−c r < v−c n ). 1 In order to identify the drivers of key results of the complete two‐period problem and get clear insights, we first analyze the results of the second‐period problem.

Second Period

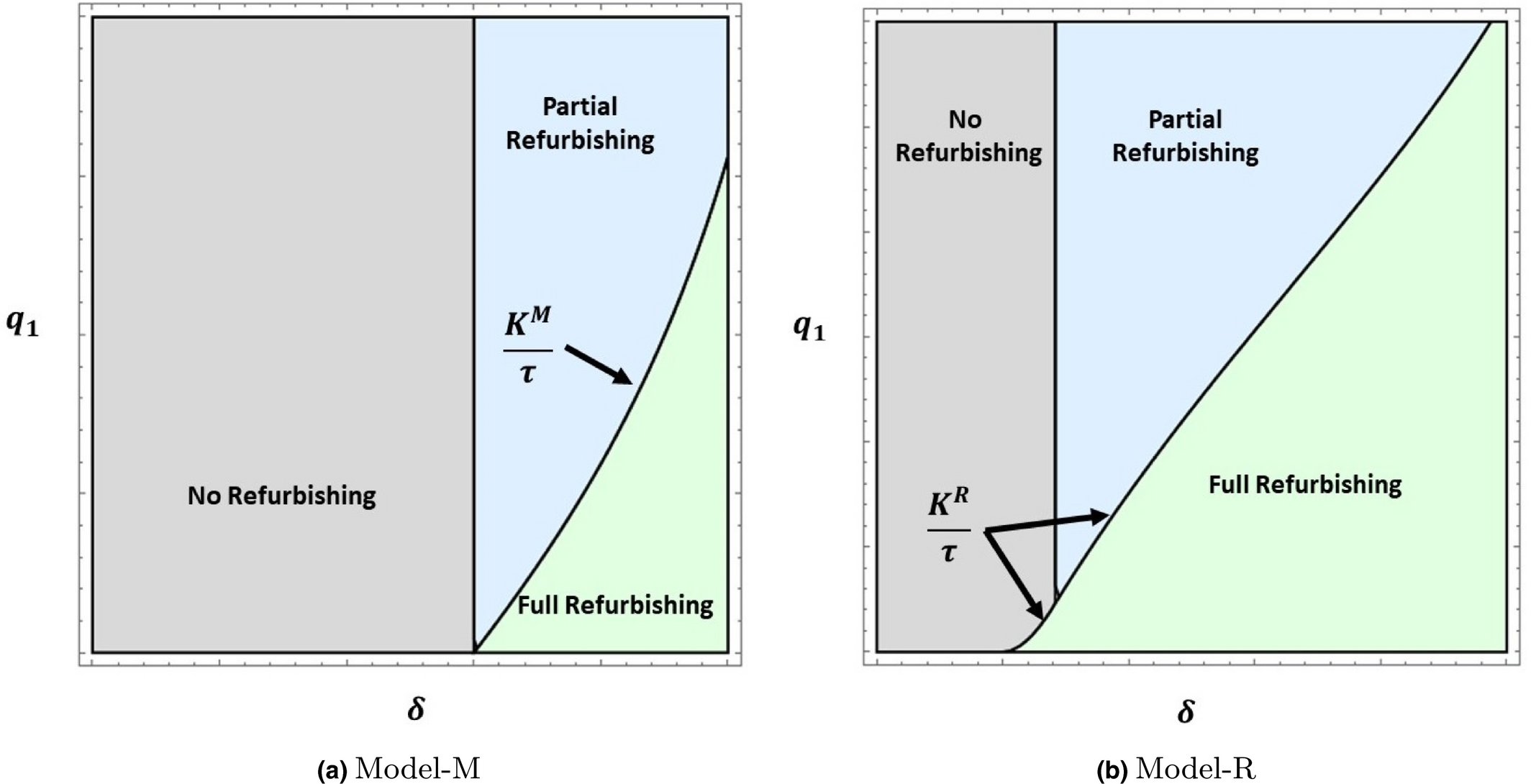

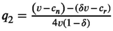

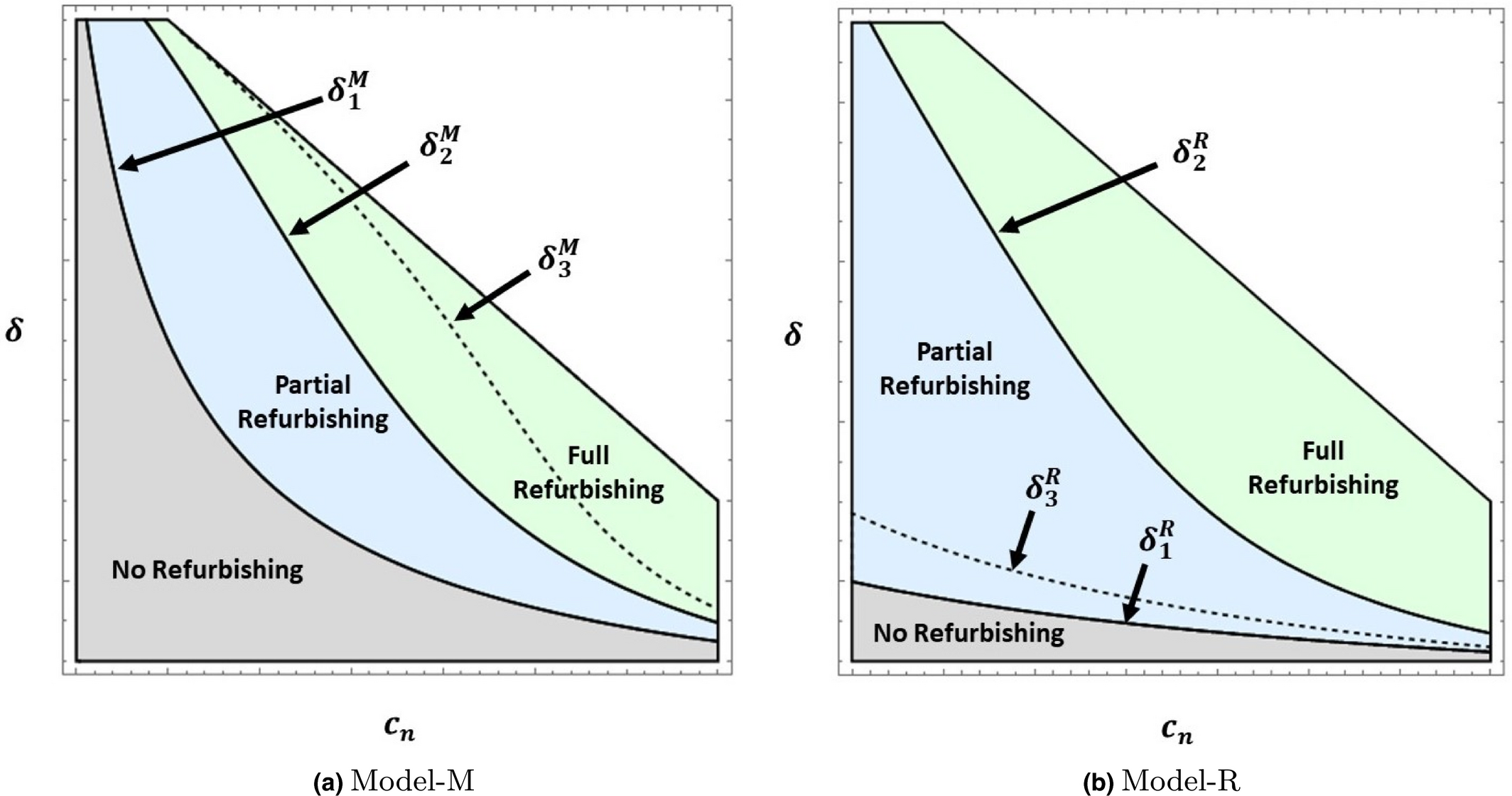

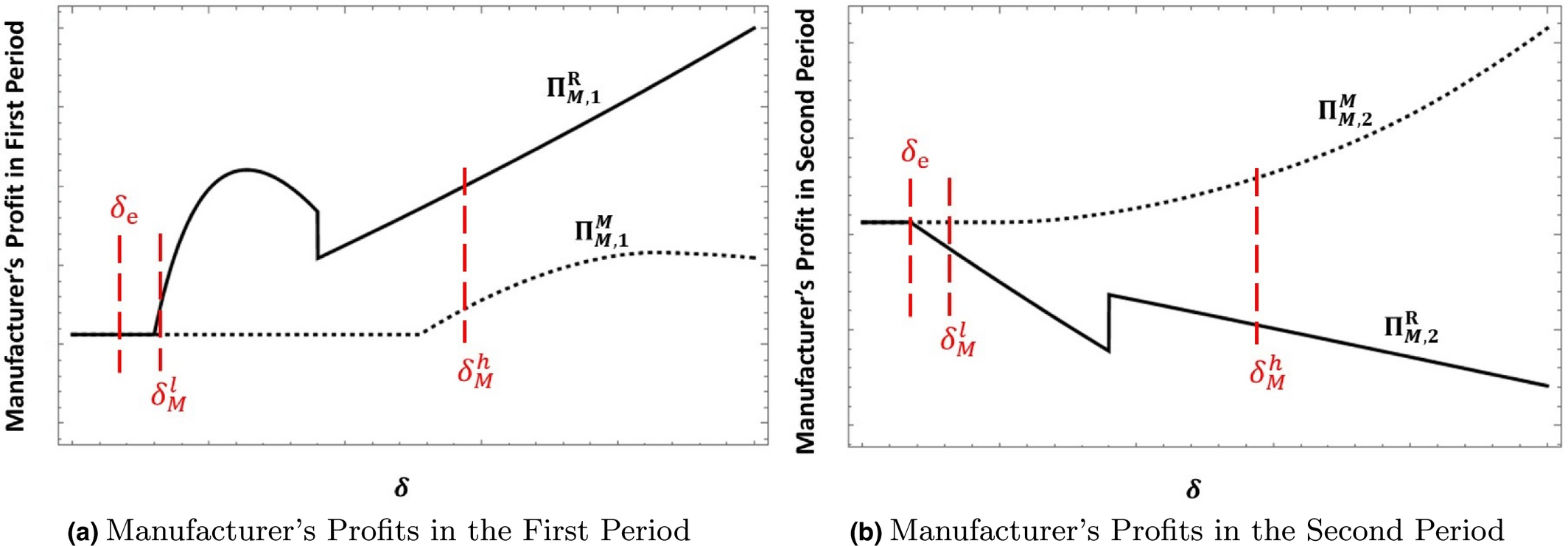

In the second period, the manufacturer sets the wholesale price(s) followed by the retailer setting the retail prices of the new and the refurbished products. Lemma 1 characterizes the resulting second‐period equilibria as functions of q 1. We also depict the refurbishing strategy in Figure 1 for Model‐M and Model‐R.

Refurbishing Strategy: Illustration of Lemma 1 [Color figure can be viewed at

Equilibrium decisions in the second period If If If

if δ≤δ

e

, then if if if δ > δ

e

and

All proofs are in the Online Appendix. Note that the quantity of new products sold in the first period (q 1) plays a critical role in determining the refurbishing strategy since the quantity of used products that can be refurbished in the second period is constrained by the refurbishable quantity of new products sold in the first period (q r ≤ τq 1). Under each model, three refurbishing strategies are possible: (I) no refurbishing (q r = 0), (II) partial refurbishing (0 < q r < τq 1), and (III) full refurbishing (0 < q r = τq 1). When the perceived quality of the refurbished product (δ) relative to the quality of the new product is sufficiently low, no used products are refurbished. However, when the perceived quality of the refurbished product (δ) is sufficiently high, refurbishing is the optimal strategy. Under this strategy, if the refurbishable quantity of new products sold in the first period (τq 1) is: (i) above threshold K M (K R ), the manufacturer (the retailer) in Model‐M (Model‐R) refurbishes only a fraction of the refurbishable products (partial refurbishing); (ii) lower than threshold K M (K R ), the manufacturer (the retailer) in Model‐M (Model‐R) refurbishes all the refurbishable products available (full refurbishing); and (iii) equal to threshold K M (K R ), the manufacturer (the retailer) in Model‐M (Model‐R) refurbishes all the refurbishable products (i.e., full refurbishing in Model‐M and partial refurbishing in Model‐R). We henceforth refer to thresholds K M and K R as the desired quantities of the refurbishable products in Model‐M and Model‐R, respectively.

In Model‐M, when the perceived quality of refurbished products is sufficiently high (

However, in Model‐R, the desired level of refurbishable products (K R ) allows the retailer to not only refurbish more products but also obtain higher margins on the new products. In fact, the manufacturer can influence the retailer's refurbishing strategy through the second‐period wholesale price. He can deter refurbishing (resulting in partial‐ or no‐refurbishing equilibrium) and thus induce the retailer to sell a high quantity of the new products (i.e., q 2) by setting a low wholesale price in the second period. Alternatively, the manufacturer can accommodate refurbishing (resulting in full‐refurbishing equilibrium) and induce the retailer to sell a low quantity of the new products by setting a high wholesale price. Note that the manufacturer faces the trade‐off between maximizing his margin and maximizing the sales quantity of the new products. When the quantity of refurbishable products is low (i.e., τq 1 < K R ), the manufacturer optimally sets a high wholesale price and thus accommodates refurbishing, resulting in a full refurbishing equilibrium (q r = τq 1). However, when the quantity of refurbishable products is sufficiently high (i.e., τq 1 ≥ K R ), the manufacturer sets a low wholesale price in order to deter refurbishing. This is so because when the quantity of refurbishable products is high (i.e., τq 1 ≥ K R ), setting a high wholesale price would induce the retailer to refurbish all the refurbishable products and decrease the sales of new products, resulting in a high loss to the manufacturer.

In order to understand the impact of the first‐period decisions on the second‐period equilibrium, we next examine how the quantity of new products sold in the first period (q 1) impacts the profits of the manufacturer and the retailer in the second period and compare this impact across both models.

As q

1 increases,

Interestingly, the quantity of new products sold in the first period (q

1) has opposite effects on the manufacturer's second‐period profit in Model‐M and Model‐R. Under Model‐M, the manufacturer's profit in the second period is monotonically increasing in the first‐period sales quantity (Lemma 2(a)) since the manufacturer benefits from refurbishing of used products, which are derived from new products sold in the first period. Specifically, the manufacturer's profit in the second period is strictly increasing in q

1 for

In contrast to the manufacturer's profit, the retailer's profit in the second period under both the models is monotonically increasing in the first‐period sales quantity (Lemma 2(b)) since the retailer sells refurbished products and, thereby, benefits from them. Moreover, the increase in the retailer's profit from an increase in the quantity of used products is (weakly) higher in Model‐R than in Model‐M. This is due to two distinct effects of the used products on the retailer's profit in the second period: a direct effect and a strategic effect. The direct effect is the increase in the retailer's profit in the second period attributed to the increase in the sales quantity of refurbished products (q r ) when the quantity of refurbishable products increases. This effect is present in both the models under full refurbishing (q r = τq 1). However, the direct effect is greater in Model‐R than in Model‐M because the retailer in Model‐R, unlike in Model‐M, gets the entire margin from selling the refurbished product (absence of double marginalization). Therefore, an increase in the quantity of used products increases the retailer's profit in the second period at a greater rate in Model‐R than in Model‐M.

The strategic effect is the increase in the retailer's profit in the second period solely attributed to the increase in the quantity of used products, but not to the increase in the sales quantity of refurbished products. The strategic effect is present only in Model‐R when the quantity of refurbishable products is higher than or equal to K R (i.e., τq 1 ≥ K R ). Recall that when the quantity of refurbishable products is low (i.e., τq 1 < K R ), the manufacturer accommodates refurbishing by setting a high wholesale price. However, when τq 1 ≥ K R , the manufacturer, in the second period, has to reduce the wholesale price of new products in order to dissuade the retailer from refurbishing all the refurbishable products, resulting in the retailer benefiting from the low wholesale price. Note that double marginalization effect exists in the new products market because the manufacturer and retailer put successive markups to maximize their own individual profits, reducing the supply chain profit. However, the strategic effect dampens the double marginalization effect and, thus, reduces the negative impact of the double marginalization on the supply chain. In order to benefit from the strategic effect, the retailer in Model‐R has the incentive to have more quantity of refurbishable products than she optimally refurbishes (i.e., q r < K R when τq 1 ≥ K R ). Therefore, when the quantity of refurbishable products is equal to the desirable quantity (τq 1 = K R ), the retailer keeps more quantity of refurbishable products than she optimally refurbishes (q r < τq 1).

The strategic effect is not present in Model‐M since the manufacturer in Model‐M directly, through the wholesale price w

r

, influences the sales quantity of refurbished products, whereas the manufacturer in Model‐R can only indirectly, through the wholesale price

We can show that K M < K R . The intuition is as follows: Since double marginalization is absent for the refurbished product in Model‐R, the retailer's unconstrained (i.e., in the absence of constraint q r ≤ τq 1) optimal sales quantity of the refurbished product in Model‐R is greater than that in Model‐M. In other words, the direct effect is stronger in Model‐R than in Model‐M. Furthermore, the retailer in Model‐R has the incentive to keep an additional quantity of refurbishable products in order to benefit by forcing the manufacturer to lower the wholesale price of the new product (the strategic effect).

In sum, an increase in the quantity of used products benefits the retailer more in Model‐R than in Model‐M because the retailer in Model‐R, unlike in Model‐M, benefits from both a stronger direct effect and the strategic effect. In the next section, we further discuss the impacts of these effects on the manufacturer's and retailer's decisions in the first period.

First Period

In this section, we analyze the results of the first‐period optimization problems of the manufacturer and the retailer. We analyze the retailer's best‐response retail price for a given wholesale price, followed by the manufacturer's wholesale price decision.

Retailer's Decision

In the first period, for a given wholesale price

For a given wholesale price in the first period, the retailer sells a (weakly) greater quantity of new products in Model‐R than in Model‐M

The intuition behind Lemma 3 is as follows. In Model‐M, the retailer benefits in the second period only from the direct effect of used products (more refurbished products), whereas in Model‐R, she benefits from both the direct and the strategic effects. Therefore, from the perspective of the second period, the retailer in the first period would like to sell a higher quantity of new products under Model‐R than under Model‐M. Since the retailer's first‐period profit, for a given wholesale price

Manufacturer's Decision

Anticipating the retailer's best‐response retail price in the first period, the manufacturer sets the wholesale price of the new product in the first period (

The equilibrium prices and quantities are as given in Tables 9 and 10 in Online Appendix.

2

In Table 9,

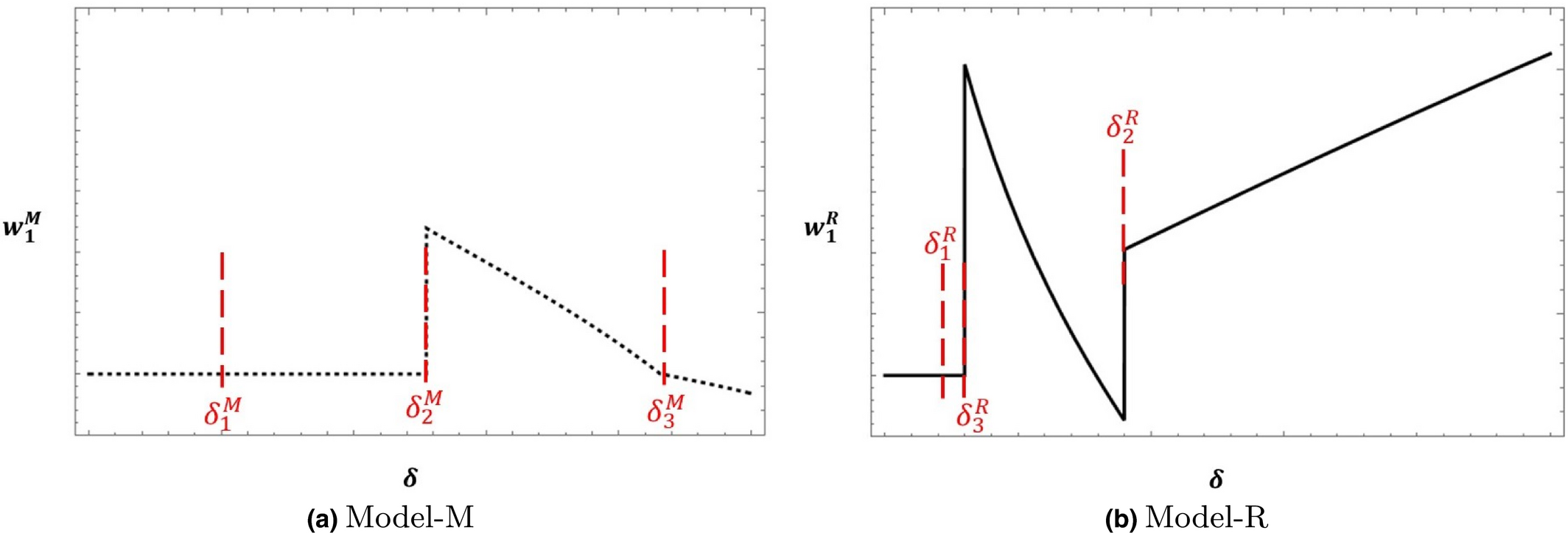

Equilibrium refurbishing strategy under each model is illustrated in Figure 2. When the perceived quality of the refurbished product is sufficiently high (

Equilibrium Refurbishing Strategy: Illustration of Lemma 4 [Color figure can be viewed at

The manufacturer can influence the refurbishing strategy in the second period by impacting the first‐period quantity (q

1) through the first‐period wholesale price (

As the perceived quality of refurbished products (δ) increases, the equilibrium wholesale price in the first period: (a) in Model‐R, remains constant when

In Model‐R, when the quality of refurbished products increases (δ), the manufacturer should intuitively increase the wholesale price of new products in the first period to restrict the supply of used products, and thereby limit the threat of refurbishing. In Model‐M, when the quality of refurbished products increases (δ), the manufacturer should intuitively decrease the wholesale price of new products in the first period to increase the supply of refurbishable products, and thereby benefit from refurbishing. Interestingly, this is not always the case in both models (see Figure 3).

Wholesale Price of the New Product in the First Period: Illustration of Lemma 5 [Color figure can be viewed at

In Model‐R, when refurbishing is very attractive to the retailer (i.e.,

However, when

When

Unlike in Model‐R, in Model‐M, the manufacturer would like to sell a high quantity of refurbished products in the second period when refurbishing is very attractive (i.e.,

Results and Insights

In the previous section, we derived equilibrium solution for both closed‐loop supply chain models with general parameters. We now analyze the impact of these models on all stakeholders—the manufacturer, the supply chain, customers, and the environment. In particular, we examine the manufacturer's choice of the optimal closed‐loop supply chain and its impact on the total supply chain profit, the customer welfare, and the environment. In Supplementary Appendix B.1, we also discuss implications of Model‐M and Model‐R on the retailer's profit.

When Should the Manufacturer Allow the Retailer to Refurbish?

With growing interest in refurbished products, many retailers such as Best Buy and GameStop are developing refurbishing capabilities. Therefore, manufacturers such as Apple and Sony need to make an important decision whether to allow their retailers to refurbish used products. In order to build the intuition about the different forces in play, we first examine the case (Scenario 1) where all used products are suitable for refurbishing (τ = 1). Next, we examine a more general case where only a fraction (τ ∈ [0,1]) of new products sold in the first period are refurbishable and the cost of refurbishing is an increasing function of δ (Scenario 2). In Scenario 1, we identify key forces in our model and discuss our results in‐depth. Since some of the forces hold in both scenarios, in Scenario 2, we focus on only the key differences. Note that the solution provided in Section 3 is general and allows us to analyze both scenarios by substituting the parameter values according to specifications in each scenario.

Scenario 1: Perfect Refurbishability (τ = 1)

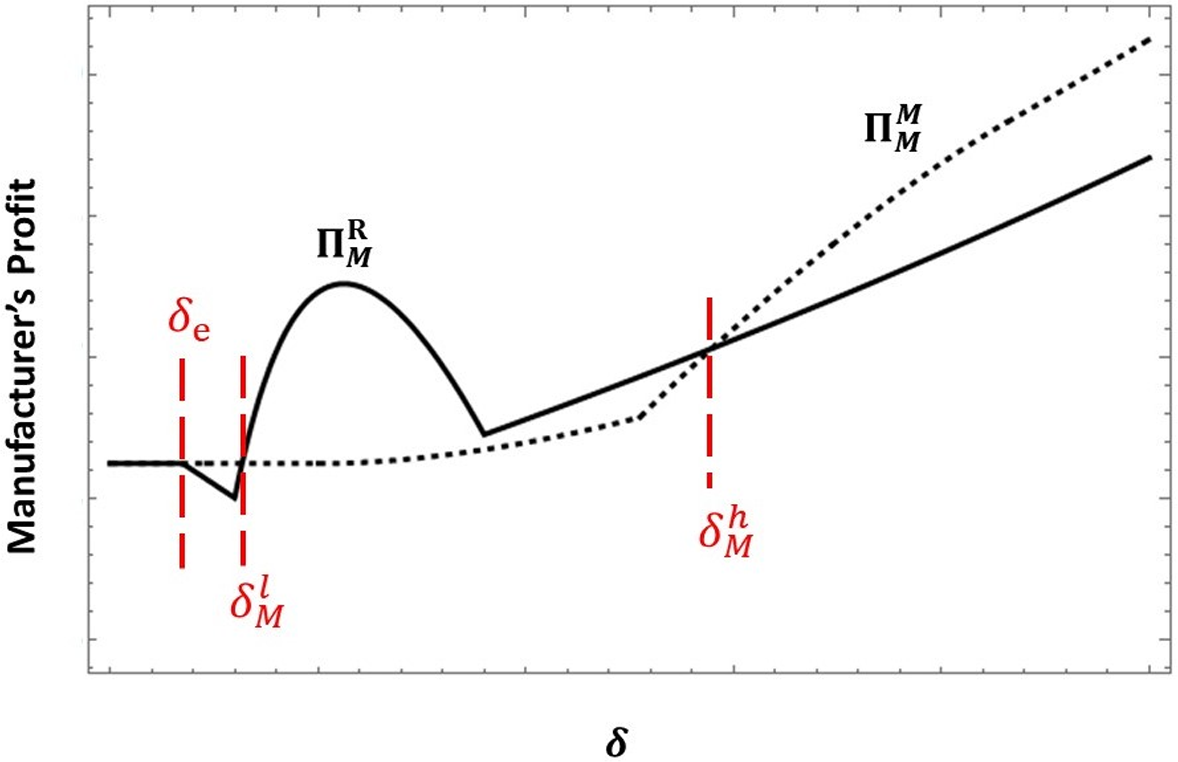

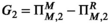

In this scenario, we analyze a setting where all the products sold in the first period can be refurbished (τ = 1). 3 We compare both the refurbishing models — Model‐M and Model‐R — to determine which of the models would be preferred by the manufacturer. The following proposition characterizes the conditions under which the manufacturer should refurbish used products himself (Model‐M) and the conditions under which he should let the retailer refurbish these products (Model‐R).

There exist thresholds

Intuitively, one would expect that the manufacturer should always prefer refurbishing used products himself (Model‐M) over letting the retailer refurbish them (Model‐R) because, unlike in Model‐M, in Model‐R, the manufacturer not only forgoes the profit from selling refurbished products but also has to compete with refurbished products sold by the retailer. However, Proposition 1 shows that under certain conditions, the manufacturer is better off with letting the retailer refurbish used products (Model‐R) than with refurbishing them himself (Model‐M). Specifically, we show that when the perceived quality of refurbished products is moderate (i.e.,

Manufacturer's Profit in Model‐M vs. Model‐R: Illustration of Proposition 1 [Color figure can be viewed at

Our findings are also supported by business practices we observe in the real world. For instance, Apple refurbishes the latest generation of the Macbook Pro 13 inch (2020 model) by itself. Moreover, according to Apple, “a refurbished MacBook Pro is virtually indistinguishable from a brand new model, so this represents a good opportunity for savings directly from Apple” (Hardwick 2020). Our results could provide a plausible explanation for Apple's decisions. We find that the manufacturer should indeed refurbish used products by itself when the perceived quality of the refurbished product is very high.

Another example relevant to our findings is that Apple also does not allow other parties (including its retailer) to refurbish the low quality refurbished products. For instance, Apple has sued its recycling partner (GEEP) because the partner refurbished and resold products that were meant to be recycled (Carrique 2020). According to Apple, these “products sent for recycling are no longer adequate to sell to consumers” and should not be refurbished and sold by any player. According to our findings, when

In order to understand the intuition behind the result in Proposition 1, we investigate the impact of closed‐loop supply chain structure on the profit of the manufacturer in each period separately. The following proposition summarizes this impact.

In the first period, the manufacturer obtains a higher profit in Model‐R than in Model‐M, but in the second period, he obtains a higher profit in Model‐M than in Model‐R.

The manufacturer in the second period is better off in Model‐M than in Model‐R (Figure 5(b)) because of the following two factors. First, in Model‐M, the manufacturer is able to sell two differentiated products at different prices, whereas, in Model‐R, he has to compete with the refurbished product offered by the retailer. Interestingly, in the first period, the manufacturer obtains a higher profit under Model‐R than under Model‐M (Figure 5(a)). The intuition behind the result is as follows. From Lemma 3, we know that the retailer, in the first period, sells a higher quantity of new products in Model‐R than in Model‐M for a given wholesale price (i.e.,

Manufacturer's Profit in Each Period in Model‐M vs. Model‐R: Illustration of Proposition 2 [Color figure can be viewed at

Our results show that in Model‐R the manufacturer is always worse off in the second period but better off in the first period. While the second‐period result is consistent with the literature (e.g., Atasu et al. 2008, Debo et al. 2005, Ferguson and Toktay 2006), the first‐period findings are not. Our results suggest that the manufacturer is always better off in the first period when the retailer is refurbishing even though he does not directly benefit from the refurbishing. 4 This new result stems from a new strategic link between used products and new products in the presence of a retailer, and this effect has not been investigated by the existing literature on refurbishing (e.g., Atasu et al. 2008, Debo et al. 2005, Ferguson and Toktay 2006).

Our results suggest that a manufacturer, expecting his retailer to refurbish used products, should strategically price his products during the product launch stage. Specifically, the manufacturer should optimally charge a high wholesale price during the initial period (when used products are not yet available for refurbishing). In this case, the manufacturer would increase his profit during the initial stage of the product's lifecycle while he should expect a loss after refurbished products start being offered by his retailer. Facing this dilemma, the manufacturer can decide whether he should allow his retailer to refurbish used products by following the prescription provided in Proposition 1.

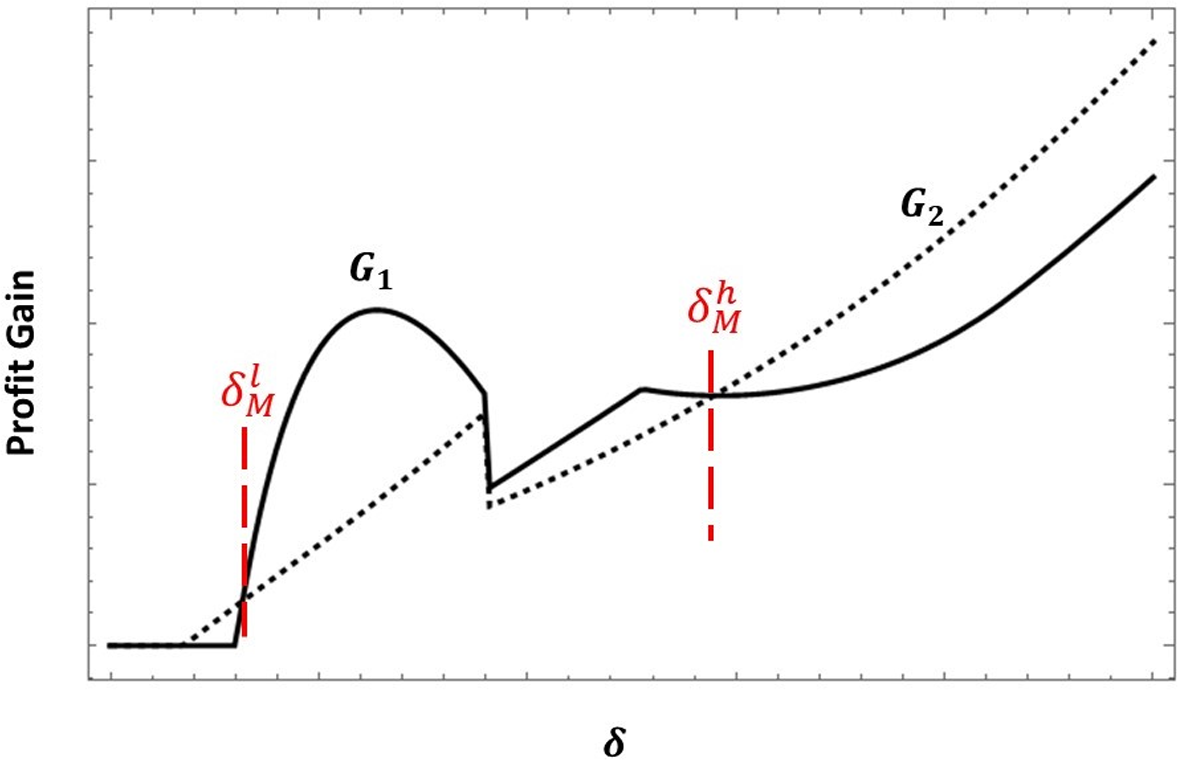

Let G

1 be the first‐period gain in Model‐R (

Corollary 1, depicted in Figure 6, shows that when the perceived quality of refurbished products is sufficiently high (i.e.,

1st Period Gain in Model‐R vs. 2nd Period Gain in Model‐M: Illustration of Corollary 1 [Color figure can be viewed at

However, when

Scenario 2: General τ and c r as a Function of δ

In Scenario 2, we examine the key question faced by the manufacturer whether he should allow his retailer to refurbish used products in a more general setting. Following the previous literature (e.g., Debo et al. 2005, Ferguson and Toktay 2006, Savaskan et al. 2004), we consider a setting where only a fraction of the products sold in the first period are refurbishable (τ ∈ [0,1]). Moreover, achieving a higher quality of the refurbished product often depends on some costly factors such as the quality of spare parts, the technology used, and the skilled labor employed. Hence, the cost of refurbishing could increase as a function of the quality of the resulting refurbished products. Therefore, in this section, we also consider the cost of refurbishing as an increasing function of the quality of the refurbished product.

Most of the literature on product quality models marginal cost as convex increasing in product quality (Atasu and Souza 2013, Desai 2001, Jerath et al. 2017, Moorthy 1988, and Shi et al. 2013a). This stream of literature commonly assumes marginal cost as a quadratic function of product quality (Atasu and Souza 2013, Desai 2001, Moorthy 1988, and Shi et al. 2013a). In the context of refurbishing, Ferguson et al. (2009) consider the cost of refurbishing a more general function that can be convex, linear or concave increasing in refurbished product quality. Similarly, we also consider the cost of refurbishing to have a general functional form that allows the cost of refurbishing to be convex, linear or concave increasing in the quality of the refurbished product. Specifically, we assume

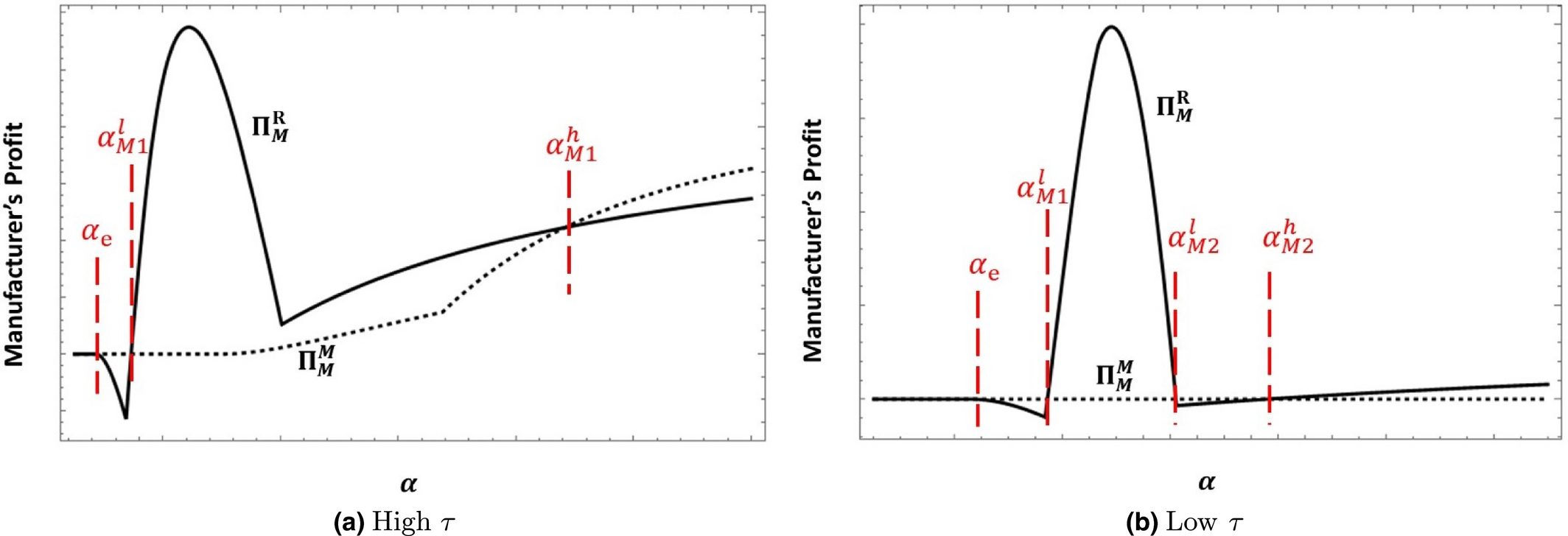

There exist When When

This proposition shows that the same forces that exist when τ = 1 (Scenario 1) continue to play a key role when τ < 1 in determining the optimal closed‐loop supply chain for the manufacturer (Figure 7). When the attractiveness of the refurbishing is very low (α ≤ α

e

), the manufacturer is indifferent between Model‐M and Model‐R because neither the manufacturer nor the retailer has the incentive to offer refurbish products. However, as the attractiveness of refurbishing increases (α > α

e

), the retailer in Model‐R has incentive to refurbish used products. In order to dissuade the retailer from offering refurbished products, the manufacturer lowers the wholesale price of the new product in the second period (

Manufacturer's Profit in Model‐M vs. Model‐R: Illustration of Proposition 3 [Color figure can be viewed at

Besides, product refurbishability also plays an important role in moderating the result. We find that when the refurbishability of the products sold in the first period (τ) is sufficiently high, the manufacturer, like in Scenario 1, allows the retailer to refurbish used products for moderate attractiveness of the refurbishing (δ in Scenario 1 and α in Scenario 2). The manufacturer faces the same trade‐off between the gain in the first period in Model‐R and the gain in the second period in Model‐M. This trade‐off also plays a key role when the refurbishability is low. Interestingly, when refurbishing is very attractive, the manufacturer is better off in Model‐M for high refurbishability and in Model‐R for low refurbishability. Also, when refurbishability is low, there is an additional region for moderate attractiveness (

When refurbishing is very attractive, the refurbishability of the products (τ) affects the optimal closed‐loop supply chain through its impact on the second‐period profit of the manufacturer in each model. The refurbishability of the products impacts the quantity of refurbished products in the second period. As we described in Section 3, this capacity constraint impacts the profit of the manufacturer in the first and second periods. When the refurbishing attractiveness (α) is sufficiently high, all the products available for refurbishing are refurbished (q

r

= τq

1) in both models. In this case, as the product's refurbishability (τ) increases, in the second period, the manufacturer benefits more in Model‐M (since he can refurbish more products) and is hurt more in Model‐R (since the retailer can produce more refurbished products which compete with the manufacturer's new products). Hence, as τ increases, the gain in the second period from Model‐M as compared to Model‐R (referred to as G

2 in Scenario 1) increases. Therefore, there is a threshold (

When refurbishing is moderately attractive, the manufacturer is better off in Model‐R under high refurbishability. However, when the refurbishability is low (

Proposition 3 extends the contribution of Proposition 1 to the refurbishing literature by uncovering the benefit that a manufacturer could extract when his retailer refurbishes used products. Our findings also unveil a novel effect of product refurbishability on the manufacturer's decision to allow another party to refurbish. The refurbishability plays a key role, mainly when the refurbishing attractiveness is very high. In this case, our model suggests that when the product refurbishability is high, the manufacturer should refurbish used products by himself, but when the refurbishability is low, the manufacturer should allow his retailer to refurbish. In practice, the product refurbishability could be thought of as a proxy for the real quality of new products. When the quality of the new product is very high, we expect a lower defect rate after usage, and hence a higher refurbishability. For instance, Apple has high‐quality products (such as the Macbook Pro 13 inch), and we expect these products to have a high refurbishability. Therefore, according to our results, Apple should refurbish used products as long as the refurbishing attractiveness/perceived quality of the refurbished products is sufficiently high (such as the Macbook Pro 13 inch (Hardwick 2020)).

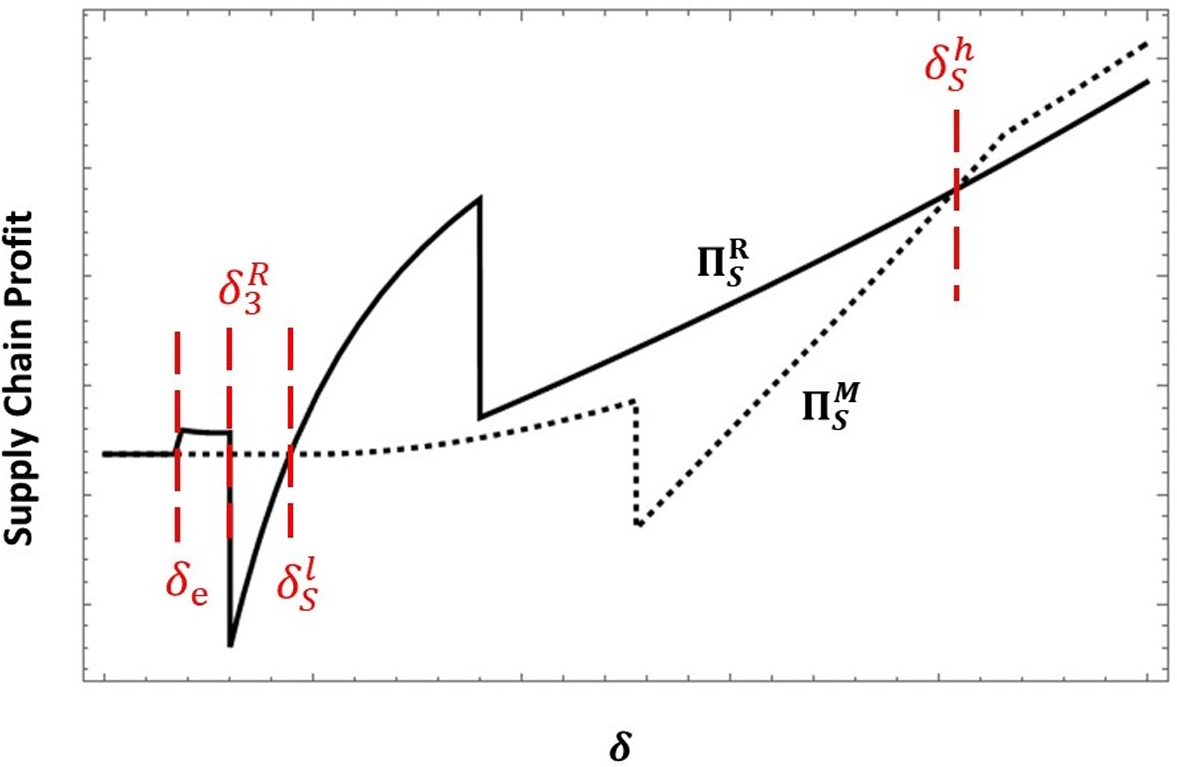

Implications on Supply Chain Profit

Supply chain efficiency has always been a concern for both managers and scholars (Cachon 2003, Jeuland and Shugan 2008, Li 2019, Shi et al. 2013b, Xia et al. 2018). In this section, we examine the effect of the supply chain structure on the total supply chain profit,

The supply chain earns higher profit in Model‐R compared to Model‐M if and only if

Even though the supply chain is not coordinated as each player maximizes his own profit, we, interestingly, find that Model‐R (as opposed to Model‐M) can improve not only the manufacturer's profit but also the total profit of the supply chain. The supply chain in Model‐R is better off than in Model‐M under conditions specified in Proposition 4 and illustrated in Figure 8 due to a combination of the following reasons: (a) in Model‐R, double marginalization is absent for refurbished products since used products are refurbished by the retailer; (b) the manufacturer sets a lower wholesale price of the new product in the second period (and thus resulting in lower retail price) under Model‐R than under Model‐M due to the competition from the retailer's refurbished products; and (c) the retail price of the new product in the first period is lower in Model‐R since the retailer has a greater incentive in Model‐R than in Model‐M to sell more new products in the first period and thus generate more used products.

Supply Chain Profit in Model‐M vs. Model‐R: Illustration of Proposition 4 [Color figure can be viewed at

Our results are related to the existing literature that examines the closed‐loop supply chain efficiency (e.g., Savaskan et al. 2004). For instance, Savaskan et al. (2004) show that when the retailer is the one who collects used products, the supply chain achieves a higher profit than when the manufacturer is the one who collects these used products. We contribute to this literature by examining the supply chain efficiency in a novel context: whether the manufacturer or the retailer should refurbish used products. Savaskan et al. (2004) show that the supply chain is always better off when the retailer plays an active role in the closed‐loop supply chain by collecting used products. When the perceived quality of the refurbished product is moderate, we also find that the supply chain is better off in Model‐R. A common factor in both papers that leads to this similar result is the dampening of the double marginalization effect when the retailer is the active player in the closed‐loop supply chain. It has been shown that double marginalization decreases the channel efficiency (e.g., Jeuland and Shugan 2008). However, under some conditions, our results are different than Savaskan et al. (2004) as the supply chain is better off when the manufacturer refurbishes used products. The key driver of this difference is that in our paper when the retailer refurbishes, she is hurt in the first period due to a very low retail price.

Our results suggest the need for more coordination between the manufacturer and the retailer not only in the forward supply chain (e.g., Jeuland and Shugan 2008) but also in the reverse supply chain. This collaboration could also be on the decision about who should refurbish used products to increase the total channel profitability.

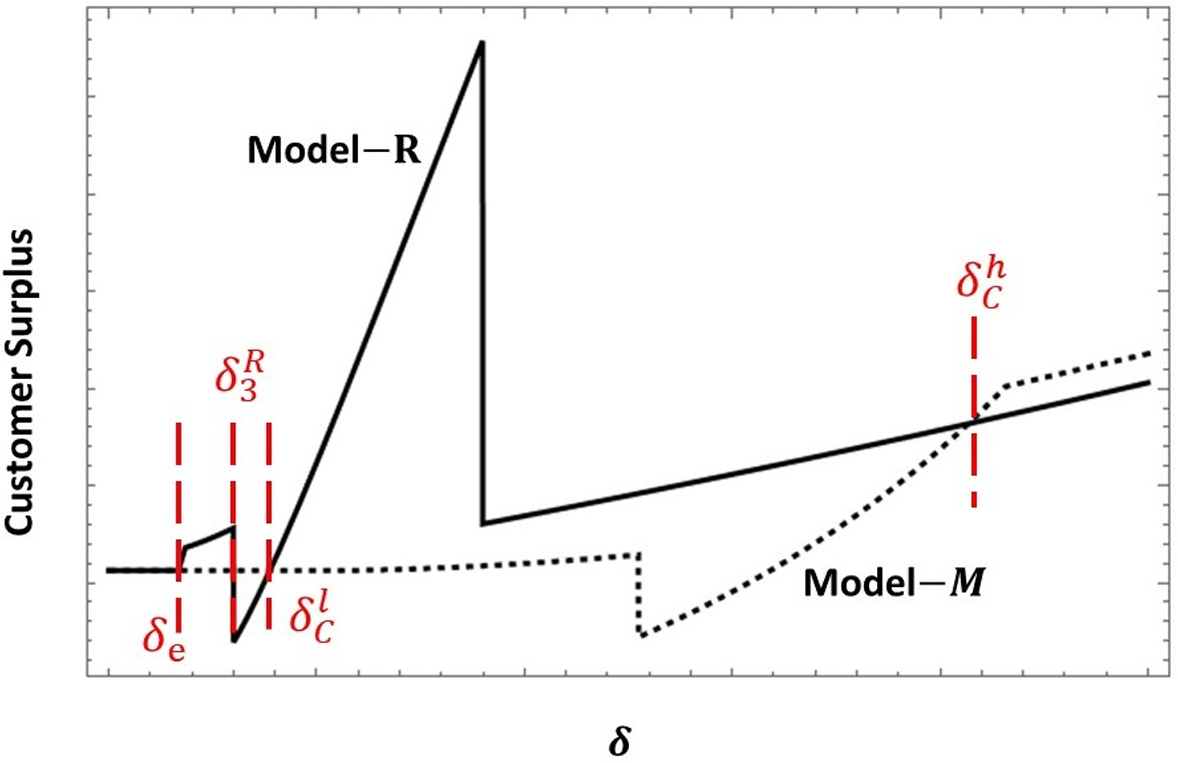

Implications on Customer Welfare

Regulators, such as the Federal Trade Commission, have always been concerned about the impact of business practices on customers’ welfare. Refurbishing has direct implications on customers’ welfare as it offers them an option to buy products of lower quality at lower prices. Having more options should increase the customer welfare (Liu and Cui 2010), but it is not clear as to which closed‐loop supply chain structure offers customers higher welfare. Policymakers have been concerned about how the refurbishing structure affects customer welfare. In this context, bills such as the “right‐to‐repair” have been proposed to force manufacturers to allow other parties to refurbish their products (Perzanowski 2021).

In this section, we investigate whether passing bills that allow a retailer to refurbish improves customer welfare. We specifically examine the effect of the closed‐loop supply chain structure on customer welfare, which is given by the following:

Customer welfare is higher in Model‐R than in Model‐M if and only if

Customer welfare in Model‐R is higher than in Model‐M under the conditions specified in Proposition 5 and illustrated in Figure 9 due to a combination of the following factors: (a) double marginalization for refurbished products in Model‐R is absent; (b) the manufacturer sets a lower wholesale price of the new product in the face of competition from the retailer's refurbished products in the second period; and (c) the retailer sets a lower price of the new product in order to sell more new products in the first period and thus generate more used products in Model‐R than in Model‐M.

Customer Welfare in Model‐M vs. Model‐R: Illustration of Proposition 5 [Color figure can be viewed at

These findings partly support the demand for the “right‐to‐repair” legislation and suggest that when a manufacturer allows his retailer to repair and refurbish used products, customers could be better off if the perceived quality of refurbished products is moderate. However, if the perceived quality of refurbished products is either low or high, customers would be better off when the manufacturer refurbishes used products by himself.

Implications on Environment

Policymakers, environmentalists, and customers are increasingly demanding for environment‐friendly business practices, including refurbishing. The landfill is widely acknowledged as one of the most hazardous activities that negatively impact the environment (e.g., Atasu and Subramanian 2012, Esenduran et al. 2019). One of the main benefits of refurbishing, among others, is the diversion of end‐of‐use products from being disposed of in landfills and thus the saving of the environment from the negative impact. We consider only the landfills to parsimoniously capture the difference between the two supply chain models in terms of the environmental impact. This is appropriate for product categories that cause damage to the environment predominantly from their disposal to landfills such as electronics (e.g., Atasu and Subramanian 2012). Accordingly, the environmental impact is

Negative environmental impact is never higher in Model‐R than in Model‐M.

Interestingly, as shown in Proposition 6, Model‐R is always better than (or as good as) Model‐M for the environment regardless of the quality of the refurbished product (δ). In Model‐R, we find that the retailer has an incentive to keep the difference between the quantities of the new product sold in the first period and the refurbished product lower than that in Model‐M

Propositions 4, 5, and 6 compare the impact of the two supply chain models on different stakeholders. We now examine the impact of the manufacturer's optimal closed‐loop supply chain structure on different stakeholders. Specifically, we look for regions where incentives of all stakeholders with regards to the choice of the supply chain structure are aligned.

The manufacturer, the supply chain, customers, and the environment are all better off only in Model‐R and only when the perceived quality of refurbished products is moderate (

The above corollary shows that Model‐R (not Model‐M) is the closed‐loop supply chain structure that can simultaneously align the incentives of the manufacturer, the supply chain, customers, and the environment. Specifically, when the perceived quality of the refurbished product is moderate, the retail prices of new product are low (improving the supply chain efficiency and the customer welfare), the quantity of the refurbished product is sufficiently high (lowering the environmental impact), and the margin of the manufacturer or the demand in the first period is higher (benefiting the manufacturer).

Closed‐Loop Supply Chains with a Third‐Party Refurbisher

We have investigated two closed‐loop supply chains (Model‐M and Model‐R) and examined the manufacturer's decision to allow the retailer to refurbish used products while controlling for the existence of another entity refurbishing these products. In reality, there are firms that specialize in refurbishing of used products and selling them to customers. For instance, Gazelle and Decluttr are well‐known third‐party players engaged in the refurbishing of used phones of OEMs such as Apple, Samsung, Motorola, and Google, and subsequently selling refurbished phones to customers (Callaham 2021). Firms such as AihuiShou and iFengPai also refurbish used phones of various OEMs (e.g., Apple, HTC, and Huawei) and sell them directly to customers. Unlike retailers, these firms usually operate independently of the manufacturer and do not sell new products. As we mentioned earlier, manufacturers face an important question of whether they should allow their retailers to refurbish used products. The previous literature has examined the impact of refurbishing by an independent refurbisher but not the impact of refurbishing by the retailer (e.g., Atasu et al. 2008, Debo et al. 2005, Ferguson and Toktay 2006). We therefore contribute to this literature by examining the impact of the refurbishing by the retailer in the presence of a third‐party refurbisher. We specifically investigate whether the manufacturer's incentive to allow his retailer to refurbish persists in the presence of a third‐party refurbisher.

In this section, we examine two new variants of closed‐loop supply chain models: Model‐3M and Model‐3R. In Model‐3M, the manufacturer and the third‐party refurbisher refurbish used products. The products refurbished by the manufacturer are sold by the retailer and those refurbished by the third‐party refurbisher are sold directly by him to customers. In Model‐3R, the retailer and the third‐party refurbisher refurbish used products and sell them to customers.

In order to ensure tractability, we normalize the quality of the new products v, and the refurbishability τ to 1.

6

The retailer (or the manufacturer) and the third‐party refurbisher have access to used products in certain proportions. We introduce a new parameter (β) that captures the proportion of used products that is available to the third‐party refurbisher.

7

Hence, the third party can refurbish

We solve these models using backward induction. In the second period, a customer can buy either a new or a refurbished product. A customer of type θ receives utility U 2N = θ−p 2 from buying a new product and utility U 2R = δθ−p r from buying a refurbished product from either the retailer or the third‐party refurbisher. Since the key variable of interest is the perceived quality of the refurbished product, we consider the same quality for the refurbished product offered by the third‐party refurbisher and that offered by the retailer (in Model‐3R) and the manufacturer (in Model‐3M). This also allows us to control for factors other than the perceived quality of the refurbished product. 8 The marginal customer located at θ = 1−q 2 is indifferent between buying a new and a refurbished product while the customer located at θ = 1−q 2−q rR −q r3 is indifferent between buying a refurbished product and not buying at all such that q 2 is the quantity of new products sold in the second period, q rR is the quantity of refurbished products sold by the retailer, and q r3 is the quantity of refurbished products sold by the third‐party refurbisher. Anticipating customers’ buying decisions, the retailer and the third‐party refurbisher simultaneously decide the quantities to be sold. Since these players cannot sell more refurbished products than their respective refurbishing capacities, they play the Cournot game. In the Cournot game, although each player might end up with different refurbishable quantities, the prices of undifferentiated refurbished products offered by the retailer and the third‐party refurbisher will be the same—the price that clears the total quantity of the refurbished products. We relegate the formulation of the manufacturer's and the retailer's optimization problems in Model‐3M and Model‐3R to Supplementary Appendix B.3.

The following proposition compares the manufacturer's profit in Model‐3M and Model‐3R:

There exist When When

Interestingly, Proposition 7 shows that the effect of refurbishing strategies on the manufacturer in the presence of the third‐party refurbisher is qualitatively similar to that in the setting where the third‐party refurbisher is absent (i.e., Scenario 2). We find that the proportion of the used products available for refurbishing (1−β) to the manufacturer in Model‐3M and to the retailer in Model‐3R plays the same role as refurbishability (τ) plays in Scenario 2. As β decreases, the quantity of refurbishable products available to the manufacturer in Model‐3M and the retailer in Model‐3R increases, similar to the effect of increasing τ in Scenario 2 (without a third‐party refurbisher).

Even in the presence of a third‐party refurbisher, we find that in the second period, the manufacturer is always better off in Model‐3M and in the first period, he is always better off in Model‐3R. The forces that drive the results in the setting without a third‐party refurbisher continue to drive the same results in this setting where there is a third‐party refurbisher. Since the retailer, unlike the third‐party refurbisher, also sells the manufacturer's new products, she continues to influence the quantity of used products to be available in the second period through the retail price of the new product in the first period when the third‐party refurbisher is present. The manufacturer always faces a trade‐off between increasing his second‐period profit in Model‐3M and increasing his first‐period profit in Model‐3R.

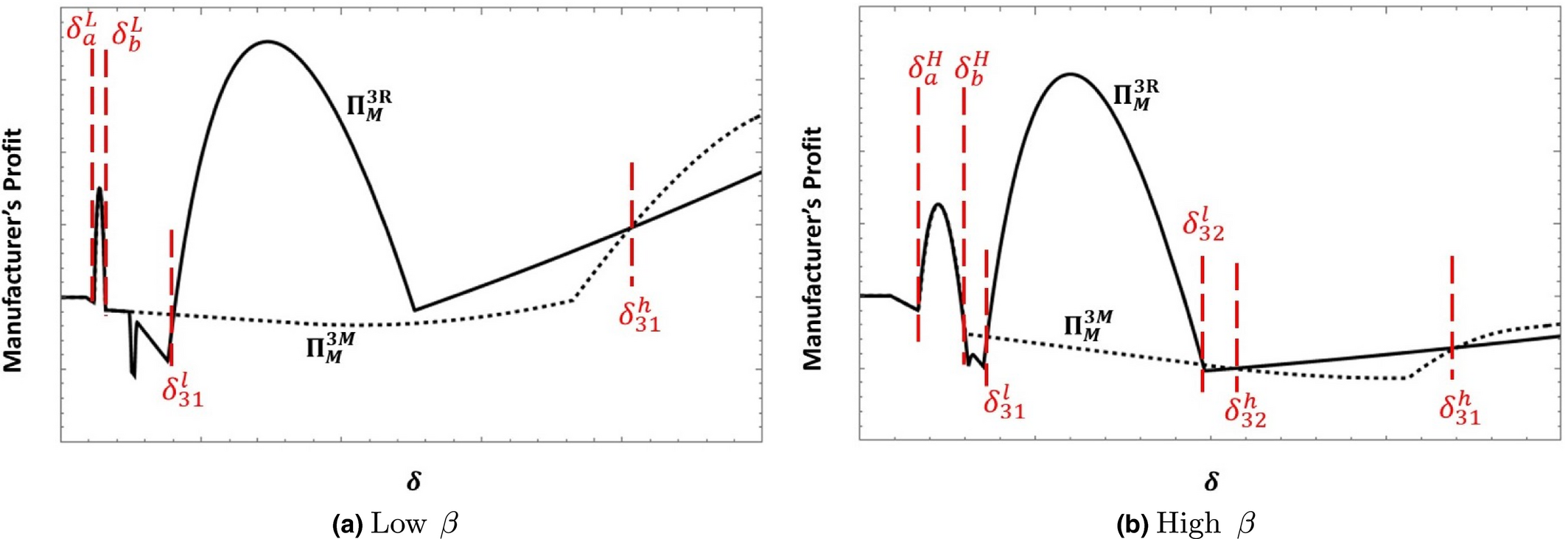

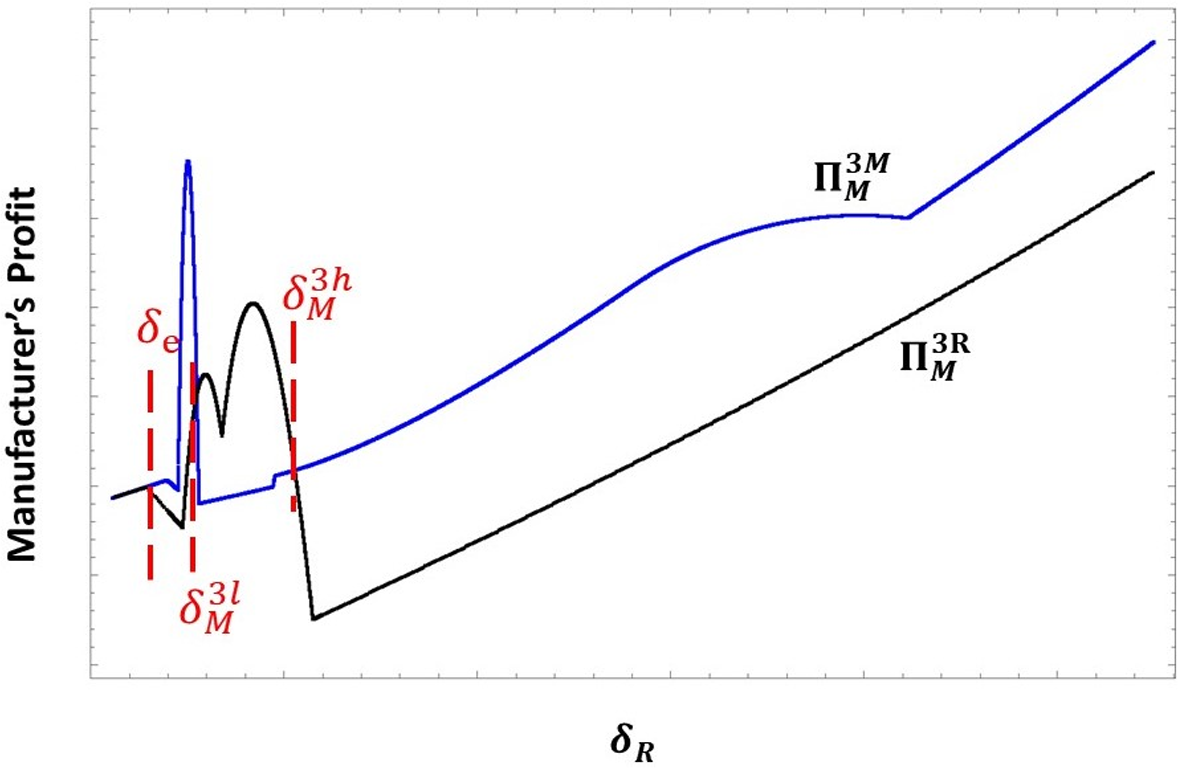

Although our results are qualitatively similar to the scenario without a third‐party refurbisher, it is important to note an interesting difference in the shape of the manufacturer's profit function (Figure 10) caused by the presence of the third‐party refurbisher. The third‐party refurbisher adds a competitive effect to our model. In our main setting, in the absence of a third‐party refurbisher, the retailer is the only player that sells refurbished products to customers in both models (Model‐M and Model‐R). However, in Model‐3M and Model‐3R, the third‐party refurbisher competes with the retailer in the second period by offering refurbished products. These refurbished products compete with the new products and the refurbished product sold by the retailer. We find that in both models, when the perceived quality of the refurbished product is low (

Manufacturer's Profit in Model‐3M vs. Model‐3R: Illustration of Proposition 7 [Color figure can be viewed at

The mechanism of this unique effect is as follows: When the perceived quality (δ) is low, the third‐party refurbisher has the incentive to refurbish used products while the retailer (in Model‐3R) and the manufacturer (in Model‐3M) do not have any incentive to refurbish used products. Since the refurbished product sold by the third‐party refurbisher competes with the new product, a high quantity of used products induces the manufacturer to lower the wholesale price of the new product in the second period. However, a lower wholesale price of the new product benefits the retailer in the second period. Therefore, the retailer has the incentive to choose a sufficiently high sales quantity in the first period (q 1). The manufacturer, accounting for the retailer's incentive, charges a high wholesale price in the first period and thus benefits in the first period. In a nutshell, the retailer leverages the presence of the third‐party refurbisher to increase her second‐period profit by inducing the manufacturer to lower the second‐period wholesale price, and the manufacturer, in turn, benefits in the first period by charging a high first‐period wholesale price.

Our results contribute to the refurbishing literature that examines the third‐party refurbishing (e.g., Atasu et al. 2008, Debo et al. 2005, Ferguson and Toktay 2006). To the best of our knowledge, this is the first paper to examine a setting where both a retailer and a third‐party refurbisher exist in the market. We find a novel effect that makes the manufacturer better off when the retailer refurbishes even in the presence of a third‐party refurbisher. This finding suggests that when an independent third‐party refurbisher exists in the market, a manufacturer should, under some conditions, encourage his retailer to also refurbish used products and compete with the independent third‐party refurbisher in the market of the refurbished product.

Extensions

Manufacturer Refurbishing and Selling Directly: Model‐MD

In this section, we analyze a modified Model‐M where the manufacturer sells refurbished products directly and compare it with Model‐R described in Section 2. We henceforth refer to this modified Model‐M as Model‐MD. In the first period, the sequence of the decisions and the optimization problems of the manufacturer and the retailer in Model‐MD remain the same as in Model‐M. In the second period, the manufacturer sets the wholesale price of the new product (

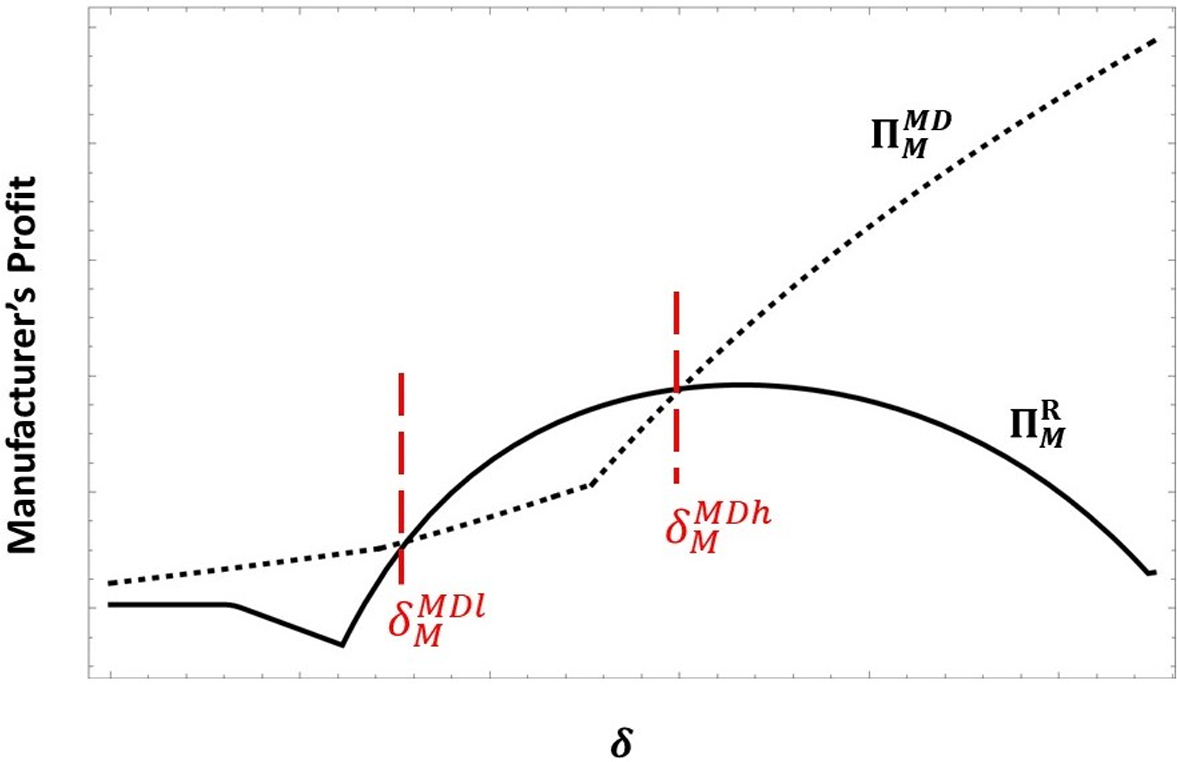

We find that our key result that the manufacturer is better off with allowing the retailer to refurbish used products (Model‐R) than with refurbishing them by himself (Model‐MD) for moderate values of the perceived quality of the refurbished product continues to hold (see Figure 11). In the second period, the manufacturer earns higher profit under Model‐MD, compared to Model‐R, because he gets entire profit generated from refurbishing under Model‐MD whereas he gets no profit from refurbishing under Model‐R. However, in the first period, the manufacturer earns higher profit under Model‐R, compared to Model‐MD, because he benefits from the retailer's incentive to sell a high quantity of the new products in the first period and to benefit from direct and strategic effects in the second period. When

Manufacturer's Profit in Model‐MD vs. Model‐R [Color figure can be viewed at

Two‐Period Product Life and Strategic Customers

In this section, we extend our analysis to a setting where new products sold in the first period only partially depreciate after the usage in the first period and that these used products still provide positive utilities to customers who continue to use them in the second period. We denote the quality of used products by δ u v. Thus, a customer θ who purchased a new product in the first period will derive utility θδ u v in the second period if he continues to use this product. Furthermore, if a customer holding a used product replaces it with a new product in the second period, the refurbisher can refurbish and increase the quality level from δ u v to δv, where δ u < δ. We provide more details about this setting in Supplementary Appendix B.5.

We solved this game numerically for various values of δ using backward induction since the problem is intractable with general parameters. Table 1 illustrates our results for different values of δ (low, moderate, and high values of δ). We find that for moderate values of δ the manufacturer is better off by allowing the retailer to refurbish used products whereas for higher values of δ he is better off by refurbishing used products himself.

Profit of the Manufacturer in Model‐M and Model‐R with Two‐Period Life of Products

Our key conclusion that the manufacturer can benefit by letting the retailer refurbish used products than by refurbishing them himself continues to hold even when we consider the two‐period life of the new product sold in the first period and the strategic customers. This is so because the retailer's incentive to sell a high quantity of the new product in the first period persists even when the life of the new product is two periods and customers are strategic. Strategic customers can postpone their purchases to buy the refurbished product, leading to an increase in the market for refurbished products. Hence, the presence of strategic customers gives the retailer a greater incentive to increase the supply of refurbished products by selling more products in the first period. As a result, the retailer's incentive to sell a high quantity of the new product in the first period continues to allow the manufacturer to charge a high wholesale price in the first period and, thus, earn higher profit in Model‐R, than in Model‐M for moderate values of δ.

Differentiated Refurbished Products by Third‐Party Refurbisher and Retailer

There are some instances where refurbished products sold by independent third‐party refurbishers are perceived to be of lower quality than those sold by retailers and manufacturers (Sheehy 2018). To incorporate such possibility, in this section, we analyze a setting where the perceived quality of the refurbished product sold by the third‐party refurbisher is lower than that sold by the retailer (both in Model‐3M and Model‐3R). We denote the perceived quality of the refurbished product sold by the retailer (both in Model‐3M and Model‐3R) and by the third‐party refurbisher by δ R and δ 3, respectively, such that δ R > δ 3 . A customer of type θ receives a utility U rR = δ R θ−p rR from buying the refurbished product sold at retail price p rR by the retailer and a utility U r3 = δ 3 θ−p r3 from buying the refurbished product sold at retail price p r3 by the third‐party refurbisher. Additional details of this setting have been provided in Supplementary Appendix B.6.

Our results show that even when the third‐party refurbisher and the retailer sell differentiated refurbished products, the manufacturer continues to be better off in Model‐3R than in Model‐3M for moderate qualities of refurbished products. Specifically, we find that the manufacturer earns higher profit by allowing the retailer to refurbish used products (Model‐3R) than by refurbishing them himself (Model‐3M) when perceived qualities of refurbished products are moderate (refer to Figure 12). In sum, our key results are robust to the retailer and the third‐party refurbisher offering differentiated refurbished products.

Manufacturer's Profit in Model‐3M vs. Model‐3R – Differentiated Refurbished Products [Color figure can be viewed at

Discussion, Limitations, and Future Research

Manufacturers are increasingly confronted with the key question of whether they should allow their retailers to refurbish used products. To our knowledge, the impact of refurbishing by a retailer on a manufacturer has not yet been studied. Furthermore, though the extant literature has examined the implications of refurbishing by third‐party players, the findings of this literature need not hold with regards to whether a manufacturer should deter his retailer from refurbishing. This is so because the retailer, unlike a third‐party player, is a supply chain partner of the manufacturer for selling new products. Therefore, in this study, we investigate whether a manufacturer should refurbish used products himself or allow his retailer to refurbish. The key insights obtained from our analysis are of relevance to both managers and policymakers.

One might think that the manufacturer would never be better off by letting the retailer to refurbish used products than by refurbishing them himself. This is so because the manufacturer has to forgo the profit from refurbishing and face competition from the refurbished products if he allows the retailer to refurbish used products. On the contrary, we show that when the perceived quality of refurbished products is moderate, the manufacturer, under certain conditions, is better off with the retailer refurbishing used products rather than refurbishing them himself. The reason behind this counter‐intuitive finding is as follows. The effect of an increase in the quantity of used products on the retailer's profit in the second period is higher when the retailer refurbishes used products (i.e., in Model‐R) than when the manufacturer refurbishes them (i.e., in Model‐M). Therefore, the retailer has the incentive to sell a higher quantity of new products in the first period under Model‐R than under Model‐M. In anticipation, the manufacturer in Model‐R strategically leverages this incentive of the retailer and earns a higher profit in the first period under Model‐R than under Model‐M. Our results show that though the manufacturer is worse off in the second period under Model‐R than under Model‐M, due to forgoing profits from refurbished products and facing competition from refurbished products, he is better off in the first period under Model‐R than under Model‐M, due to strategic benefits of allowing the retailer to refurbish used products. When the perceived quality of refurbished products is moderate, the manufacturer's first‐period gain in Model‐R more than offsets his second‐period loss, resulting in the manufacturer earning higher profit in Model‐R than in Model‐M.

Managerial Implications