Abstract

Online peer‐to‐peer (P2P) lending has emerged as an innovative financial technology (FinTech) platform that renders financial services that are potentially more inclusive and affordable than those offered by traditional financial institutions. A similar purpose is served by cryptocurrency markets, where transaction costs are reduced and financial accessibility is improved based on disruptive technologies such as blockchain and distributed ledgers. Despite these developments, however, in the operations management literature limited attention has been devoted to the contribution of online P2P lending to the promotion of financial inclusion (i.e., the availability and usage of financial services for all groups of people) and its dynamic interplay with cryptocurrency markets. The rise of cryptocurrency markets affects the composition and activity of borrowers and investors in P2P lending markets and hence the capacity of the latter to support financial inclusion, leading to an operations management challenge in online P2P lending. We examine how cryptocurrency markets influence P2P lending markets' democratization of access to financial services, particularly P2P borrowing. To investigate these effects in depth, we develop a simple theoretical model to derive testable propositions, which are then empirically validated on the basis of unique data sets. We find that the growth in cryptocurrency markets is associated with increased loan requests and larger loan amounts in P2P markets, especially from borrowers who maintain good credit ratings, possess technical knowledge about cryptocurrencies, and intend to borrow for investment purposes. Our results suggest that cryptocurrency markets bring economic gains to the P2P lending market, at least in the short term. Nonetheless, the transfer of funds from P2P lending to cryptocurrency markets, particularly by highly creditworthy and tech‐savvy investors, may provoke increased inequality in access to P2P lending markets. By scrutinizing the interdependence between two representative FinTech markets we uncover important operations management implications for theory and practice regarding the healthy growth and effective governance of crowdfunding platforms and the corresponding sustainability of their role in upholding financial inclusion.

INTRODUCTION

Financial services are essential for reducing poverty and enhancing economic well‐being, yet many people around the globe still lack access to formal financial services, such as banking (Honohan, 2008). According to the latest Findex data of the World Bank, approximately one third of adults in the world (i.e., 1.7 billion) are still unbanked and suffer inaccessibility of financial services. 1 Amid this inequality and struggle, emerging financial technologies, called FinTech, are believed to have the potential to reduce the financial disparity between those who have and those who have not. These innovations may augment resources dedicated to financial inclusion—a process that ensures access, availability, and usage of financial services for all groups of people including traditionally disadvantaged groups (Goldstein et al., 2019; Kendall, 2017; Philippon, 2019). 2 Customers' sense of well‐being closely intertwined with services such as financial inclusion is one of the unique operational characteristics of financial services (Hatzakis et al., 2010). Peer‐to‐peer (P2P) lending, for example, can stimulate financial inclusion by providing more accessible credit and ensuring more equality in actual credit usage (Alexander, 2017).

Nonetheless, the question of whether FinTech improves financial inclusion is not conclusively answered in the academic literature. Although some studies demonstrated that FinTech helps financial accessibility (e.g., Balyuk, 2022), other studies did not find any significant improvement in financial affordability as a result of FinTech adoption (Bartlett et al., 2022; Fuster et al., 2019; Tang, 2019). Moreover, limited attention has been paid to the dynamic interplay among various FinTech‐based financial services, such as P2P lending and cryptocurrencies, and its effects on financial inclusion.

Online P2P lending markets, such as Prosper and Lending Club, are among the early FinTech initiators that facilitate borrower/lender transactions without intervention from traditional lending channels, such as banks. In the United States, the volume of loans issued by the P2P lending industry in 2019 amounted to $67.9 billion, and this is estimated to reach $559 billion by 2027. 3 Despite this burgeoning trend, however, a heated debate continues over the potential of P2P lending to facilitate financial inclusion. Advocates maintain that P2P lending renders financial services that are more inclusive and accessible by ensuring convenience, speed, and efficiency in the processing of loan applications; these advantages are made possible by big data and machine learning technologies (Berg et al., 2020). 4 Critics, however, have shown the opposite or an insignificant effect of P2P lending, demonstrating that this industry has yet to live up to expectations (e.g., Buchak et al., 2018).

In the FinTech arena, the P2P lending industry has transformed the delivery of credit to consumers, but it does not hold a monopoly on this transformation. For example, blockchain technology‐driven cryptocurrency markets enable secure and anonymous transactions without using centralized banking systems or monetary authorities (Babich & Hilary, 2020; Hastig & Sodhi, 2020; Seth, 2020). At the outset, then, cryptocurrency markets can also advance the move toward financial inclusion (Lichtfous et al., 2018). Their presence and rise, however, can have unexpected ramifications on the role and effectiveness of P2P lending in serving the goal of financial inclusion. Given that money flows from one market to another, cryptocurrency markets are connected to P2P lending markets. 5 The emergence of cryptocurrencies can therefore be expected to bear on the composition of borrowers and investors and their activities in P2P lending markets. For instance, some investors may use P2P borrowing as a channel for securing resources in an attempt to seize an investment opportunity in a cryptocurrency market. Such transfers, however, may diminish the liquidity and capacity of P2P lending, which in turn, weakens services related to financial inclusion, changing the heterogeneity of customers from an operational perspective (Hatzakis et al., 2010).

In this light, this research investigates whether the recent developments in cryptocurrency markets influence borrowing activities in P2P lending markets and, if so, how such interdependencies and spillovers affect the financial inclusion in P2P lending. Specifically, we look into who is more likely to exploit P2P lending in seizing investment opportunities in the cryptocurrency industry. When traditionally disadvantaged groups are more likely to exploit P2P lending, we could say that financial inclusion is improved on a P2P lending market. Finally, we examine what actions should be taken to preserve the virtues (i.e., financial inclusion) served by FinTech markets and enhance operations in financial services. The motivation of this research is to address these issues.

Cryptocurrency markets can exert complex effects on P2P lending markets. If many P2P lenders switch to cryptocurrency markets to obtain significant arbitrage gains, 6 such shifts will reduce the pool of lenders in P2P markets, eventually lowering opportunities for borrowers to secure P2P funds and increasing borrowing rates. This may even deter some borrowers from using P2P lending. Amid the risks, however, the dominance of cryptocurrency markets continues, inducing more borrowers to secure loans in P2P lending markets in order to jump on the bandwagon driven by volatile cryptomarkets. Therefore, investigating how supply–demand matching in P2P lending changes in response to the cryptocurrency market, a disruptive technology, should be worthwhile from the perspective of operational risk management (Wang et al., 2021).

How borrowers in the lending market respond to cryptocurrency markets may depend on their characteristics, such as their credit levels and their familiarity with cryptocurrency and underlying blockchain technologies. For example, bullish cryptocurrency markets might mainly encourage creditworthy and tech‐savvy borrowers to leverage P2P lending as a venue for acquiring resources to be funneled into cryptocurrency investments. This practice then erodes financial inclusion because these traditionally advantaged borrowers take more credit on the P2P lending market while relatively disadvantaged borrowers face less available and affordable credit.

To shed light on the interdependence between P2P lending and cryptocurrency markets, we develop a simple analytical framework that incorporates lender/borrower demand from online P2P lending and cryptocurrency markets on the basis of expectations about market responses. Our framework predicts that, with all else equal, bullish cryptocurrency markets increase (decrease) the demand and participation from high (low) creditworthy borrowers in P2P lending markets. Empirically, we exploit several exogenous shocks to cryptocurrency markets to identify their effects on P2P borrowing and examine how these shocks differentially affect P2P borrowers.

A preview of our results indicates that buoyant cryptocurrency markets lead to increased P2P borrowing, suggesting that P2P lending is a funding source for cryptocurrency investment. Consistent with our theoretical prediction, this effect is more pronounced for borrowers who maintain good credit scores and have greater access to traditional credit and who are tech‐savvy. In addition, a hot cryptocurrency market is associated with a greater number of listings and unique borrowers, and the positive association is stronger for financially advantaged borrowers. All these patterns reflect that the emergence of cryptocurrency markets renders P2P borrowing less inclusive in terms of both accessibility and affordance because creditworthy and tech‐savvy borrowers can more effectively leverage the characteristics of cryptocurrency markets in their financial activities. Relatedly, the growth of cryptocurrency markets is associated with low default and interest rates because such markets that are currently in vogue attract creditworthy borrowers to P2P markets.

Our findings provide several theoretical and practical contributions. First, although the positive effects of technology‐driven markets have been under much scrutiny, OM scholars have paid limited attention to their adverse effects on wealth redistribution and financial accessibility (Gomber et al., 2018; Hastig & Sodhi, 2020; Pun et al., 2021). In particular, contrary to their original intent and purpose, technology‐enabled FinTech markets may penalize, rather than benefit, many people and firms who are at a disadvantage in accessing financial resources. This is an important issue for the operational risk management and thus deserves comprehensive scholarly attention. Specifically, understanding the interdependence of FinTech platforms is important to assess the implications of their expansion and sustainability. Reflecting the increasing importance of innovative online platforms such as crowdfunding and the debate on the sustainability of online P2P lending platforms, there has been a call for research on the value creation of these platforms (Chen et al., 2020). Second, to the best of our knowledge, our study is among the first to investigate the interdependence between P2P lending and cryptocurrency markets, with a particular focus on financial inclusion. 7 The P2P lending literature has focused mainly on within‐platform dynamics (e.g., Zhang & Liu, 2012). The present study extends extant scholarship by providing evidence of significant spillover and interdependence between the two FinTech platforms. Furthermore, we demonstrate that external investment options affect P2P borrowing decisions, thus causing changes to financial inclusion (e.g., Geva et al., 2019). Third, our study expands the nascent literature on cryptocurrencies and blockchain (Hastig & Sodhi, 2020; Pun et al., 2021). Although researchers have inquired into the determinants of cryptocurrency prices and important contractual and regulatory issues related to cryptocurrency markets, they have overlooked possible interactions with other FinTech markets. Finally, our study complements the emerging literature on the dynamics and interdependence of cross‐platforms. Recognizing that platforms affect various economic transactions, scholars have concentrated on cross‐platform spillover effects in several contexts (Bernstein et al., 2021; Burtch et al., 2018; Krijestorac et al., 2020). We broaden this line of inquiry by uncovering how cryptocurrency markets exert spillover effects on P2P lending.

The findings equally benefit managers and policy makers with respect to maintaining the stability and growth of FinTech‐driven markets, while accelerating financial inclusion for those who are in need of equal opportunities and accessibility to financial service provision. First, cryptocurrency markets can bring economic gains to P2P lending markets because an influx of good borrowers (highly creditworthy and tech‐savvy borrowers) increases loan requests and decreases default rates in the online P2P lending market. A problem, however, is that a bullish cryptocurrency market can also diminish the liquidity of P2P lending, thereby penalizing borrowers who have less than ideal credit ratings and who are technically less acquainted with cryptocurrencies. If the “right” balance and spillover can be found in the shift to cryptocurrencies, the interaction and exchange between these digital markets would herald a new wealth‐generating FinTech revolution. A wealth‐creating interactive spillover with other FinTech markets may not only accelerate the growth of P2P lending, but it may also preserve its stability and strengthen the ecosystems of online financial platforms. Second, although other benefits can also be achieved through FinTech platforms, we argue that financial inclusion should continue to be the primary goal of such technology‐enabled markets given that it is what separates them from their traditional counterparts (Lieber, 2011; Taylor, 2017). In this respect, our findings reinforce the importance of financial inclusion in P2P lending markets and provide managerial and policy‐related insights into the pathways through which to enhance the welfare of unbanked and financially excluded populations.

RELATED LITERATURE

Our paper is built broadly on four streams of research. First, this study is related to the nascent literature on FinTech and financial accessibility. Researchers have discussed various FinTech services and their potential to foster financial affordability (Ozili, 2018). On the one hand, FinTech can enhance financial inclusion by using digital innovations and creating technology‐enabled new products and services for consumers who would otherwise lack access to financial services. On the other hand, such a platform does not serve individuals without appropriate Internet connection and digital devices, albeit smartphone penetration is often higher than banking penetration in many developing countries (Salampasis & Mention, 2018). Moreover, people who are welcomed by traditional institutions might make better use of FinTech services, whereas many of those at the opposite end of the spectrum are structurally excluded to fully leverage these offerings.

Prior studies examined various FinTech innovations to identify their effects on financial accessibility, including research that delved into mobile services (Ghosh, 2016; Mbiti & Weil, 2015), crowdfunding (e.g., Kim & Hann, 2019), or blockchain (Chen & Bellavitis, 2020; Schuetz & Venkatesh, 2020). Our study is most closely related to research on the influence of P2P lending on financial inclusion (Arifin et al., 2018; Maskara et al., 2021). We extend this nascent literature by investigating how an emerging FinTech service (i.e., cryptocurrency market) affects the role of another FinTech service (i.e., P2P lending) that is more mature in terms of financial inclusion.

Second, we drew on the P2P lending literature in our exploration. Previous studies on P2P lending focused on lenders to identify herding behaviors (Zhang & Liu, 2012), home biases (Lin & Viswanathan, 2016), advantages for sophisticated lenders (Vallée & Zeng, 2019), and risk aversion (Paravisini et al., 2017). Some researchers have argued that hard and soft information and resources are important in evaluating loans; this information includes borrowers' friendship networks (e.g., Lin et al., 2013), social media information (Ge et al., 2017), peer lenders (Hildebrand et al., 2017; Iyer et al., 2016), loan descriptions (Caldieraro et al., 2018), borrowers' ethnicities (Pope & Sydnor, 2011), and borrowers' profile images (Duarte et al., 2020). Although those studies help explain the market mechanisms of online P2P lending, they provide limited insights into the forces that affect borrowing decisions in P2P lending markets. Other researchers attempted to shed light on P2P borrowing determinants, such as local access to finance (e.g., Tang, 2019), government affiliation (Jiang et al., 2019), and message reminders conveying lenders' positive expectations (Du et al., 2020). These studies underexplored the importance of dynamic interactions across diverse FinTech markets. We endeavor to fill this void and complement the literature by showing that external investment options can affect P2P borrowing.

Third, this study is associated with the emerging literature on cryptocurrency markets. Researchers evaluated the evolving and controversial digital currencies and suggested that intangible cryptocurrency, such as Bitcoin, may present technical value in solving the double‐spend problem as well as operational value in enabling frictionless commerce. Furthermore, new cryptocurrency brings surveillance value to the detection of fraud via public authentication and also public value that is reflected by people's acceptance (Alstyne, 2014). Related studies examined the effects of digital currencies on monetary systems (Iwamura et al., 2014), their extreme volatility and negative bubbles (Bianchetti et al., 2018; Fry & Cheah, 2016), surveillance applications (Foley et al., 2019), design of token contracts (Malinova & Park, 2018), blockchain adoption for solving counterfeiting (Pun et al., 2021), and the role of artificial intelligence‐based ratings (Basu et al., 2019) in an initial coin offering (ICO). Notably, Liu et al. (2021) showed the importance of the technological sophistication of ICO projects when it comes to valuing ICO success, implying that technological savviness is critical for cryptocurrency investments. Babich and Hilary (2020) provided key strengths and weakness of blockchain technology and suggested a future avenue of research for OM scholars. We respond to this call and provide the first empirical evidence that the blockchain‐enabled market interacts with another FinTech market.

Finally, this study is related to the literature on the dynamics of cross‐platforms and resource interdependency among different platforms. 8 Notably, Bernstein et al. (2021) examined competition between two ride‐sharing platforms (i.e., Uber and Lyft) and proposed an incentive mechanism to discourage multihoming. Burtch et al. (2018) found a negative relationship between the entry of gig economy platforms (i.e., Uber) and rates of crowdfunding project initiation on Kickstarter. Krijestorac et al. (2020) observed a positive cross‐platform spillover effect in the context of video consumption. We extend these initiatives by probing the interrelationship between P2P lending and another form of FinTech platform (i.e., cryptocurrency markets).

A MODEL OF TWO FINTECH MARKETS AND HYPOTHESIS DEVELOPMENT

Simple analytical framework

We develop a simple analytical framework to illustrate how the cryptocurrency market affects a self‐interested platform's decision‐making and payoff and consequently financial inequality of borrowers in the P2P lending market. With lax screening and 24/7 operations, in real time, the lenders are not the only ones who consider the cryptocurrency market, but the borrowers can also consider this market as an attractive investment source. To incorporate this potentiality, we consider two‐sided outside options. We first exploit key considerations in the posted price P2P lending model (Einav et al., 2018; Wei & Lin, 2017), and then include the cryptocurrency market as an outside option for both the lender and the borrower.

At stage 1 of the game sequence, the platform sets an interest amount, p, under the posted price mechanism to maximize its own payoff, as a self‐interested player, by attracting both sides to participate in the transaction (Einav et al., 2018; Wei & Lin, 2017). At stage 2, the borrower, given p, decides whether to accept the interest if it is less than or equal to the threshold interest amount,

For each loan, the borrower incurs a variable cost of c and obtains a random value of v. Without a new outside option, the borrower is willing to pay a maximum interest rate for a loan of

The borrower and the lender decide to participate in the loan transaction if they obtain a positive payoff. Let

To capture the impact of the outside shock on a lender's decision, we first consider the heterogeneous reservation utility of lenders for the loan. For mathematical tractability, we assume a uniform distribution of

(a)

For the sake of space, we describe the interpretation of Lemma 1 in Appendix B.2 in the Supporting Information. (a) If and only if

Proposition 1 summarizes under what conditions

With Propositions 1 (b) and 1 (c), we explain the case of

Regarding the moderation effect of γ on the relationship between τ and

Hypothesis development

On the basis of Proposition 1, we develop hypotheses related to the dynamics between cryptocurrency availability and financial inclusion. Prior studies on financial inclusion characterized financially advantaged groups as high‐creditworthy individuals who live in urban areas and/or have high‐skill occupations and finally disadvantaged populations as low‐creditworthy individuals residing in rural areas and/or employed in low‐skill occupations (e.g., Ozili, 2018; Salampasis & Mention, 2018). Financial inclusion is intended mainly to extend financial services to financially disadvantaged groups. Building on these previous works, we focus our analytical model on two factors that can help differentiate the financially disadvantaged from their advantaged counterparts: (1) the creditworthiness of borrowers (denoted as δ), and (2) the value of the outside option for borrowers (relative to lenders) (interpreted as technological savviness and denoted as γ).

We first associate δ with the creditworthiness of the borrowers, which has been the most salient factor for classifying individuals as finally advantaged (Buchak et al., 2018; Maskara et al., 2021). Prior studies showed that as creditworthiness improves, access to credit becomes easier. We thus incorporate this factor into our model. Another important, subtle factor is the relative value of the outside option for borrowers relative to lenders (denoted as γ). On the basis of this definition, borrowers with a high γ are likely to use the cryptocurrency market as a new investment option. We argue that borrowers should have enhanced technical knowledge about cryptocurrencies and blockchains in general to enable them to more effectively seize and capitalize on this opportunity. Because the cryptocurrency market is based on blockchain technology, technology sophistication should play an important role in the exploration of financial inclusion (Liu et al., 2021). Accordingly, to complement previous research, we conceptualize high γ borrowers as tech‐savvy individuals that represent a financially advantaged group. This clears the way for us to examine whether technological savviness (especially on the cryptocurrency market) can inhibit financial inclusion.

By reorganizing the condition underlying Proposition 1(a), we could observe that a bullish (bearish) cryptocurrency market may increase (decrease) the likelihood of participation by high creditworthy individuals (i.e.,

Contrastingly and interestingly, we can observe from Proposition 1(b) that a bullish (bearish) cryptocurrency market may decrease (increase) demand from low creditworthy or non‐tech‐savvy borrowers. First, a lender who targets low‐creditworthy borrowers may be attracted to the cryptocurrency market—a situation that may not be sufficiently offset by an increased interest rate, especially under a high default rate. Second, low‐creditworthy borrowers are discouraged from participating in the market by a high interest rate. Non‐tech‐savvy borrowers may not recognize opportunities in the cryptocurrency market, thus resulting in limited benefits from a bullish cryptocurrency economy. However, a platform will increase the interest rate to retain a lender seduced by the outside option, but such a rate is insufficient for the lender to stay because the increased interest comes mostly from lender demand and less from that by non‐tech‐savvy borrowers.

In sum, we theorize possible changes in financial inclusion in two FinTech markets by examining how P2P borrowing by financially advantaged (disadvantaged) groups is influenced by opportunities in the cryptocurrency market (see Appendix B.3 in the Supporting Information for graphical illustration). Specifically, we inquire into whether a bullish (bearish) cryptocurrency market provides more opportunities to either low‐creditworthy or non‐tech‐savvy borrowers who have been excluded from traditional financial services or whether the market reduces such exclusion. With Proposition 1, especially 1(c), as a basis, we submit the following: Positive (negative) shocks in the cryptocurrency market are associated with higher (lower) access and usage from high‐creditworthy borrowers than low‐creditworthy borrowers.

Positive (negative) shocks in the cryptocurrency market are associated with higher (lower) access and usage from tech‐savvy borrowers than non‐tech‐savvy borrowers.

Because we use the two attributes that distinguish financially advantaged groups from disadvantaged populations in the P2P lending market, another interesting yet unexplored question is which factor has a stronger impact on the link between cryptocurrency shocks and P2P borrowing. Thus, we compare the moderating effect of the technological savviness and creditworthiness of borrowers. The cross partial derivatives of borrower demand with respect to shock and creditworthiness and technological savviness are The moderating effect of creditworthiness on the relationship between cryptocurrency shocks and demand from P2P borrowers is greater than that of technological savviness.

EMPIRICAL ANALYSIS AND RESULTS

Data and variables

We downloaded data from Prosper.com on April 12, 2019. The data set includes all fund seekers on the company platform since its inception in 2006. For each listing, we obtained a comprehensive set of list characteristics, including the requested amount, borrower's interest rate, loan term, starting and ending time, and loan purpose. Furthermore, for successfully funded listings, we tracked the loan origination date and repayment status each month, which helps define whether a loan is defaulted. The data set also includes borrower‐specific characteristics such as Prosper rating (AA‐A‐B‐C‐D‐E‐HR) and debt‐to‐income ratio. 10 Because we are interested in differences in borrowers' reactions to cryptocurrency markets, we also collected their occupations and residential states.

We collected aggregate data from Coinmarketcap.com, which provide aggregate information on trading activities on key exchanges for Bitcoin, Ethereum, and other major cryptocurrencies. As of May 20, 2019, 2186 coins were trading in the market. Bitcoin and Ethereum account for 68% of the total cryptocurrency market capitalization. Thus, we focused on Bitcoin and Ethereum in our main analysis. In a robustness test, we included the top 10 cryptocurrencies in terms of market capitalization, which covers 83% of total market capitalization.

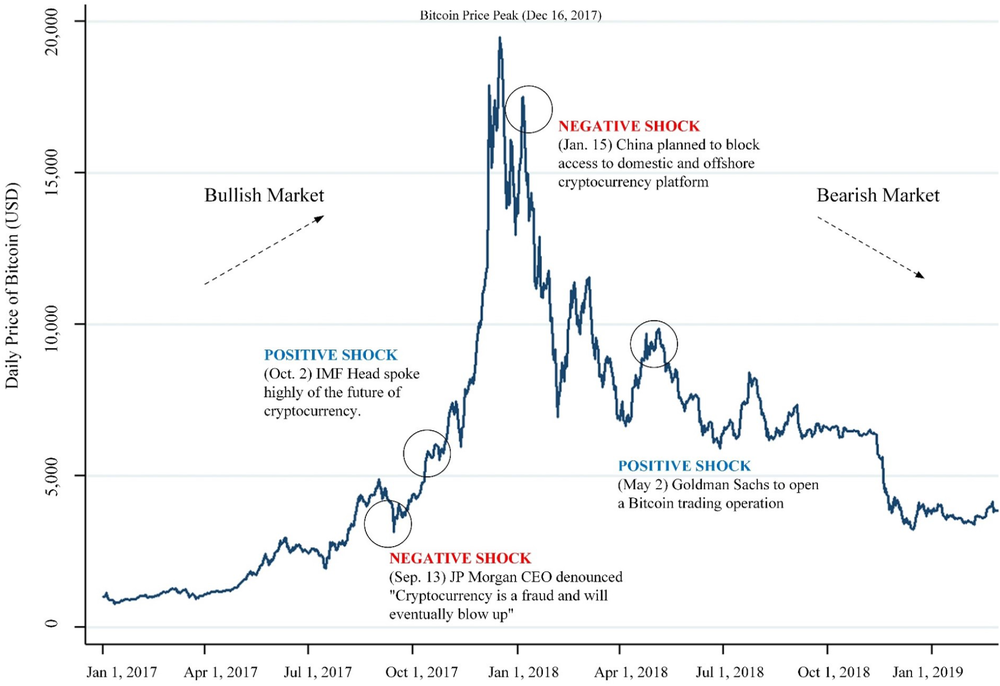

To examine cryptocurrency market effects on borrowing in the P2P lending market, we matched all listings from Prosper created from January 1, 2017 to February 28, 2019, with the cryptocurrency market data. We used the listing creation date because it should be closest to the actual borrower reaction in the cryptocurrency market. We then conducted analyses at two levels. To examine the effect on the overall volume of borrowing (i.e., the extensive margin), we aggregated and analyzed both data sets at the day level. To examine the effect on individual loans (i.e., the intensive margin) and resulting outcomes, we analyzed at the listing level. Using a period of more than 2 years allowed us to cover both boom‐and‐bust cryptocurrency periods. Figure 1 shows that the Bitcoin price rapidly increased in 2017 and then dropped in 2018. Thus, we can examine how cryptocurrency market shocks over the course of the cycle affect borrowers' incentives for using P2P lending markets.

The price of Bitcoin and exogenous shocks in the cryptocurrency markets

To capture the overall interest in P2P lending, we first computed the total amount of loan application at the day level. We also constructed the daily number of listings and the daily number of unique borrowers as dependent variables to test how the cryptocurrency market affects overall borrowing on the P2P lending market. Our results are robust to using different measures to capture the overall interest in P2P lending.

We also examined how the cryptocurrency market affects individual loans and outcomes. We used loan amount to see whether a hot cryptocurrency market induces individuals to borrow more from P2P lending. We also constructed two measures to capture loan outcomes. The default rate is measured 540 days after the loan initiation. If a loan has any missed interest payment at least once during the period, the loan is considered a default. The borrower rate is a yearly interest rate. Lower default rates and interest rates represent better loan performance.

Our key independent variables of interest are cryptocurrency market trends. For that, we constructed and used three measures in our main analysis. We first extracted three daily transaction outcomes (closing price, market capitalization, and trading volume) of Bitcoin and Ethereum. 11 We then took a weighted average of the metrics of each cryptocurrency (weighted by their loadings in the underlying principal components). 12 To quantify the average price of cryptocurrency over a given period, we further used a 10‐day exponential moving average 13 (e.g., Brock et al., 1992).

To mitigate the omitted variable bias, we include an extensive set of control variables that may be associated with online P2P lending. Using Prosper.com, we added relevant listing characteristics and borrower credit risk variables known to affect listing and loan outcomes (e.g., Caldieraro et al., 2018; Morse, 2015; Wei & Lin, 2017). Finally, we added several macroeconomic variables. Using the borrower location, we included monthly unemployment rates for each state from the Bureau of Labor Statistics. We also added the monthly Zillow home value index measured for each state from Zillow.com. Both are used to control for economic conditions that may affect borrowing from P2P lending markets (e.g., Wei & Lin, 2017). We also included daily Dow Jones Industrial Average numbers, monthly Federal fund rates, foreign exchange rate (USD/CNY), and daily gold price, because they are arguably natural investment channels. Table C.1 in the Supporting Information summarizes our sample and descriptive statistics.

Model‐free evidence

Figure C.1 in the Supporting Information shows how the P2P lending and the cryptocurrency markets evolved during our study period. In 2017, we observed an exponential increase in the cryptocurrency market in terms of trading volume and market capitalization and a subsequent steep decrease. Although the trend is less dramatic than in the cryptocurrency market, the P2P lending market showed a similar pattern. P2P lending increased in total listing amount until early 2018. It has since decreased slightly. Similar trends in both markets indicate that they may positively relate to each other.

Figure C.2 in the Supporting Information confirms that high‐creditworthy borrowers are the main causes of increased online P2P market demand. Specifically, during our study period, high‐creditworthy borrowers (Prosper ratings of AA, A, or B) increased (decreased) their demands at bullish (bearish) markets, whereas low‐creditworthy borrowers (Prosper ratings of D, E, or HR) changed slightly or insignificantly in response to cryptocurrency market trends (Figure C.3 in the Supporting Information for details), supporting our prediction.

Loan demand increased more for loans that seem potentially intended for cryptocurrency market investment. Based on the broad borrower‐reported loan purpose, we classified loans as having financing (i.e., debt consolidation and personal loan) or nonfinancing purposes (e.g., home improvement, medical, and vacation). Figure C.4 in the Supporting Information shows that financing‐related listings increased the most. Considering that loans with nonfinancing purposes were created for uses unrelated to cryptocurrency investing, the result supports that P2P lending is a potential source of capital for investing in cryptocurrency.

Furthermore, in Figure C.5 in the Supporting Information, the increase is stronger among borrowers with occupations that are generally highly skilled, tech‐savvy, and more likely to be interested in the cryptocurrency market (Ennis, 2016; Stray, 2017), such as computer programmers, executives, and professionals. In contrast, borrowers in low‐skilled jobs such as administrative assistants, car dealers, and laborers are expected to have minimal knowledge about the new cryptocurrency market.

Our model‐free evidences show that increased P2P borrowing comes mostly from borrowers with good credit ratings and high‐skilled occupations who are seeking loans related to cryptocurrency. This implies that when the cryptocurrency market increased rapidly, the increase might have made P2P lending less inclusive.

How cryptocurrency market shocks affect borrowers' incentives to use P2P lending

To examine how cryptocurrency markets affect the role and effectiveness of P2P lending in enhancing financial inclusion, we first focused on the usage of P2P borrowing. That is, we examined whether cryptocurrency markets affect borrowers' loan amounts on the P2P lending market, and how the effect varies between financially advantaged and disadvantaged groups. Our main empirical strategy was to exploit several natural shocks on the cryptocurrency markets, along with propensity score matching (PSM). We first identified two positive and two negative exogenous shocks (Figure 1). We wanted to include both positive and negative shocks in boom‐and‐bust periods to dampen concerns about picking up general trends during the periods if we examined only positive (negative) shocks in boom (bust) periods.

We then compared transaction outcomes on P2P lending before and after the natural shocks within a short‐term period. As the shocks essentially affect all the listings in the P2P lending market, we consider the listing in the 5‐day after‐shock period as the treatment and consider the listing in the 5‐day before‐shock period as the control group. 14 We used a PSM method to find a control group that most resembled the treatment group and then estimated the treatment effects associated with the cryptocurrency market changes (e.g., Wei & Lin, 2017). This allows a direct comparison of transaction outcomes between two matched listings with similar characteristics (propensity score).

We used a logit regression to calculate the propensity score for the probability of being in the treatment group,

We first observed two positive exogenous shocks on the cryptocurrency market. On May 2, 2018, Goldman Sachs became the first Wall Street bank to open a Bitcoin trading operation, in which they used Sachs money for various contracts linked to the price of Bitcoin (Popper, 2018). In addition, on October 2, 2017, Christine Lagarde, IMF CEO, announced that cryptocurrency could be the future (Hackett, 2017). Both shocks led to sudden and huge increases in the price of Bitcoin (Figure 1). We observed that unlike cryptocurrency markets, stock markets did not move much before and after the shocks, implying that the shocks are specific to the cryptocurrency rather than the general financial market (see Figure C.6 in the Supporting Information). Thus, we used natural shocks to help identify effects of the cryptocurrency market on the P2P lending market.

We then examined two negative exogenous shocks on the cryptocurrency market. On September 13, 2017, Jamie Dimon, JPMorgan CEO, warned that Bitcoin “is a fraud and will eventually blow up.” Bitcoin immediately slid by more than 10% in a single day (Kelly, 2016). On January 15, 2018, China clamped down on cryptocurrency and planned to block access to foreign cryptocurrency exchanges (Yang, 2018). Both shocks led to a huge decrease in the price of cryptocurrency (Figure 1 and Figure C.6 in the Supporting Information).

The matching estimates for the ATET of positive shocks in Panel A of Table 1 show that the two positive shocks overall led to an increase in loan amounts. Specifically, the shock related to Goldman Sach's crypto trading open (IMF head's positive mention) increased the loan by an average of 4.7% (3.3%). Negative shocks to the cryptocurrency markets were associated with smaller loan requests (Panel B of Table 1). China's cryptocurrency market regulation was associated with a 0.9% decrease in the listing amount within a short‐term 10‐day period. Dimon's statement had similarly negative effects. Together, the results show that positive cryptocurrency shocks led the same borrower to borrow more.

Matching estimates of the cryptocurrency shock effects on online P2P lending markets

Note: Robust t‐statistics are shown in parentheses. We follow Abadie and Imbens (2006) to calculate the standard errors of the matching estimates (AI Robust Standard Error). We used teffects psmatch2 syntax in STATA allowing for the estimate average treatment effect on the treated (i.e., ATET). We employed three‐nearest neighbors matching with replacement. Tech‐savvy occupations include investors, computer programmers, executives, professionals, and analysts who might be sensitive to the cryptocurrency market. Others occupations include administrative assistants, car dealers, and laborers who might not be sensitive to the cryptocurrency market, in general. Sensitivity analyses of treatment effects by Rosenbaum bounds indicate that our treatment effects are insensitive and less likely to be over/under‐estimated. *

We then examined whether credit rating and occupation affected borrower responses to positive cryptocurrency shocks (Table 1). We found that high‐creditworthy borrowers largely drove increases in loan amounts. For instance, borrowers with a Prosper rating of AA increased the requested amount of loans by about US $930 after the positive shock from Goldman Sachs, which corresponds to 7.01% of the average loan amount during the 10‐day window. In contrast, low‐creditworthy borrowers generally responded negatively to positive shocks, although some were not statistically significant. This implies that growth in the cryptocurrency market induced high‐creditworthy borrowers to use P2P borrowing more aggressively and exploit the full potential of the market better. In addition, the increase was more positive for borrowers in Type 1 occupations–investors, computer programmers, executives, professionals, and analysts–who are likely to have more familiarity with and have better access to the cryptocurrency market. That is, high‐creditworthy and tech‐savvy borrowers increased (decreased) their demands when the cryptocurrency market was in a good (bad) situation. In contrast, low‐creditworthy and low‐skilled borrowers showed the opposite behaviors, although statistically weaker. 16 These findings support our Hypotheses 1 and 2. Together, these results suggest that as the cryptocurrency market grows, P2P lending becomes less inclusive because advantaged borrowers that likely have less difficulty accessing traditional credit make more use of P2P borrowing for that opportunity.

Impact of cryptocurrency market on the P2P lending market

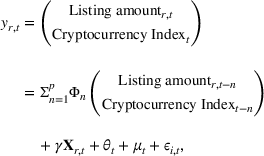

In this section, we turn to loan access and examine whether and how the cryptocurrency market affects borrowers' access to P2P loans. We could not test whether and how the chances of loan acquisition by different borrowers change in response to cryptocurrency market conditions, because once an application is approved for listing, the success of obtaining a loan is almost 100%. Few applications are unsuccessful. We instead explored whether the cryptocurrency market affects individuals who are willing to borrow and, if so, how much they are prepared to borrow. To investigate the effects of the cryptocurrency market on the incentive of borrowers to use P2P lending, we estimated the impact of the former on the latter at the market level by running ordinary least squares (OLS) regressions on daily aggregated data. Note that although OLS regressions provide initial base results, this estimation approach may be confronted with identification issues. For instance, we could not completely rule out whether some omitted variables (e.g., updated market news) may have affected both the cryptocurrency and P2P lending markets. To alleviate these concerns, we incorporated a large number of control variables into Table C.1 in the Supporting Information, including loan‐ and borrower‐related characteristics and macroeconomic variables. We also used instrumental variables to minimize the endogeneity issue driven by developments in the cryptocurrency market. Our OLS regression models for the overall borrowing of P2P lending are delineated as follows:

Daily‐aggregated associations between cryptocurrency markets (Bitcoin and Ethereum) and online P2P lending markets

Note: Robust t‐statistics are shown in parentheses. All models are based on daily‐aggregated borrowers' activities in the P2P lending market. In our main estimation, we use each of the three measures (i.e., market capitalization, trading volume, and exponential moving average) for the cryptocurrency index one by one due to the high correlation among them); this yielded similar results and we reported with market capitalization for brevity. To allow for the possibility of delayed impact of cryptocurrency markets on online P2P markets, we re‐estimated our model using 1‐day or 1‐week lagged values of our key independent variables—cryptocurrency market‐related variables. The results are similar to the results based on contemporaneous values. The current table allows a 1‐week lag between two markets. We estimate our modes in a hierarchical manner (i.e., estimating our model with control variables only then including independent variables on control variables); this yielded similar results. High‐credit group includes Prosper ratings AA, A, and B, and low‐credit group includes Prosper ratings E and HR. Tech‐savvy occupations include investors, computer programmers, executives, professionals, and analysts who might be sensitive to the cryptocurrency market. Non‐tech‐savvy occupations include administrative assistants, car dealers, and laborers who might not be sensitive to the cryptocurrency market, in general. *

In Table 2, the market growth of cryptocurrencies is significantly positively associated with the daily listing amount (Model 1 of Panel A) and daily number of listings (Model 1 of Panel B). This suggests that when the cryptocurrency market is hot, borrowing on the P2P lending market increases in the following week. Interestingly, we also observed an increase in the daily unique number of borrowers (Model 1 of Panel C), implying that hot cryptocurrency markets attract new borrowers to the P2P lending market. Economically, for a 1% increase in the market capitalization of the cryptocurrency market, a daily listing amount on the P2P lending market increases on average by 0.12%. We observed similar economic effects on the daily listing number and the daily unique number of borrowers.

To investigate how the cryptocurrency market affects the distribution of P2P borrowers, we broke down borrowers into two groups by credit rating or occupation. First, in Models 2 and 3, we broke down borrowers into high‐credit and low‐credit borrowers. Our results show that hot cryptocurrency markets are more positively associated with borrowing of high‐credit borrowers than that of low‐credit. Actually, we did not observe a significant association for low‐credit borrowers. This indicates that as the cryptocurrency market becomes hot, the P2P lending market has proportionally more borrowing from high‐credit borrowers. When we classified borrowers by their occupation, we further observed a positive association only in tech‐savvy borrowers. Together, the results show that borrowers responded differently to cryptocurrency market developments. High‐credit and tech‐savvy borrowers were more responsive to hot cryptocurrency markets. Given that they have been traditionally in a better condition in terms of access to credit, traditionally advantaged borrowers are more likely to issue P2P loans to seize new investment opportunities.

Importantly, our results show that a hot cryptocurrency market is more positively associated with the daily unique borrower number of high‐credit (

To dampen endogeneity concerns, we implemented the instrumental variable approach (IV approach, also known as a two‐stage least squares estimation). As instruments for the cryptocurrency market index, we used weather‐related variables employed in prior studies as instruments for trading assets (Hirshleifer & Shumway, 2003; Loughran & Schultz, 2004). Although weather affects stock market returns and trading volumes, it is arguably exogenous to investment behaviors. 17 We measured our instruments and conducted the analyses at the state–month level based on the smallest granularity of the weather data and the P2P lending data. Specifically, we used (1) average temperature by state and month and (2) precipitation by state and month as IVs for both the market index of cryptocurrencies (i.e., market capitalizations) and the stock market index (i.e., S&P500 Index; SNP500). We obtained monthly statewide average‐temperature and precipitation data from the National Oceanic and Atmospheric Administration (NOAA) National Centers for Environmental Information.

We then constructed a panel data set containing 1168 state–month observations with monthly aggregated data of two FinTech markets. Table 3 reports the results of the IV estimation. In the first stage, models show that average temperature (precipitation) is significantly positively (negatively) associated with both the market capitalizations of Bitcoin and Ethereum cryptocurrencies and the stock market (SNP500), corroborating that sunny and warm weather affects investor behavior (Hirshleifer & Shumway, 2003; Kaustia & Rantapuska, 2016; Loughran & Schultz, 2004). In the second stage, we regressed the overall borrowing of P2P lending (i.e., listing amount) on the fitted value of market capitalization of Bitcoin and Ethereum. Overall, the results of the IV estimation are qualitatively similar to the main results. In other words, a greater market capitalization of the cryptocurrency market is positively associated with the daily P2P borrowing. The association is observed mainly in high‐credit or tech‐savvy borrowers.

Two‐stage least squares results: Considering endogeneity of Cryptocurrency Market Index

Note: Robust t‐statistics are shown in parentheses. The table reports results from 2SLS using two instrument variables (IVs) about statewide weather. Specifically, we use (1) average temperature by state and month and (2) precipitation by state and month as IVs for both the market index of cryptocurrencies (i.e., market capitalizations, trading volume, and exponential moving averages) and the market index of stock (i.e., S&P500 Index; SNP500). Models are based on monthly statewide aggregated borrowers' activities in the P2P lending market and market capitalizations of cryptocurrencies (Bitcoin and Ethereum). We also estimate our models with other market indexes of cryptocurrency (e.g., trading volume and exponential moving averages) and stock market indexes (e.g., Dow Jones Industrial Average or Nasdaq); this yielded similar results but are not reported for brevity. High‐credit group includes Prosper ratings AA, A, and B, and low‐credit group includes Prosper ratings E and HR. Tech‐savvy occupations include investors, computer programmers, executives, professionals, and analysts who might be sensitive to the cryptocurrency market. Others occupations include administrative assistants, car dealers, and laborers who might not be sensitive to the cryptocurrency market, in general. *

Although we saw an increase in overall borrowing in response to hot cryptocurrency markets, we do not know whether loan outcomes would be better or worse. To address this, we conducted OLS or logistic regressions at the loan level:

In Models 6 and 7 of Table 3, we find that better cryptocurrency market conditions are associated with lower default rates and lower interest rates on the P2P lending market. In terms of economic significance, on average, a 1% increase in market capitalization of the cryptocurrency market is associated with a 0.003% decrease in borrower interest rates and a 3.03% decrease in default rates (in terms of marginal effects,

Overall, the findings from the two identification strategies suggest that hot cryptocurrency markets motivates creditworthy and tech‐savvy borrowers to borrow more actively and large amounts, thus skewing the market toward financially advantaged borrowers. This further implies that financially disadvantaged borrowers have difficulty accessing both FinTech markets, thereby diminishing financial inclusion, at least in the short run.

Robustness checks

We conducted a series of robustness checks to further ensure the validity of our results. First, we used measures to capture a broad scope of cryptocurrency markets. Our baseline measures of cryptocurrency markets based on Bitcoin and Ethereum account for about 60% of the total cryptocurrency market capitalization. To increase comprehensiveness, we observed the market capitalization of top 10 cryptocurrencies: Bitcoin, Ethereum, Ripple, Bitcoin Cash, EOS, Litecoin, Cardano, TRON, Dash, and Monero, which covered 83% of the total market capitalization as of June 27, 2018. We constructed three measures of cryptocurrency market trends and re‐estimated Equation (4) at the listing level. Table 4 indicates that the results based on the alternative measures of top 10 cryptocurrencies (Panel B) are qualitatively similar to the results with Bitcoin and Ethereum (Panel A).

Listing‐level associations between cryptocurrency markets and transaction outcomes of online P2P lending markets

Note: Robust t‐statistics are shown in parentheses. Top 10 cryptocurrencies are Bitcoin, Ethereum, Ripple, Bitcoin Cash, EOS, Litecoin, Cardano, TRON, Dash, and Monero, which covered 83% of the total market capitalization as of June 27, 2018. In our main estimation, we use each of the three measures for the cryptocurrency index one by one due to the high correlation among them. All models are based on either listing‐ or loan‐level analysis. For comparisons of default rate, we estimated logit models. To allow for the possibility of delayed impact of cryptocurrency markets on online P2P markets, we re‐estimated our model using 1‐day or 1‐week lagged values of our key independent variables—cryptocurrency market‐related variables. The results are similar to the results based on contemporaneous values. The current table allows a 1‐week lag between two markets. We estimate our modes in a hierarchical manner (i.e., estimating our model with control variables only then including independent variables on control variables); this yielded similar results. Tech‐savvy occupations include investors, computer programmers, executives, professionals, and analysts who might be sensitive to the cryptocurrency market. Others occupations include administrative assistants, car dealers, and laborers who might not be sensitive to the cryptocurrency market, in general. *

To further address potential endogeneity issues, we employed a vector autoregressive model with exogenous variables (VARX) used previously (e.g., Kök et al., 2020) to examine dynamic interactions between cryptocurrency markets and online P2P markets. To create time series data, we aggregated daily listings in P2P lending by Prosper credit ratings. The specific equation we estimate is given as follows:

The estimation results of our VARX model in Table C.3 in the Supporting Information indicate that the cryptocurrency market has a significant positive effect on the demand of high‐creditworthy borrowers ($776.298,

Finally, to address concerns that Prosper may fail to represent the online P2P lending market, we replicated our estimations using Lending Club data. Because this data set provides only monthly listing and loan data, we matched monthly aggregated data with the monthly cryptocurrency data set. Lending Club data yielded similar results (Table C.4 in the Supporting Information).

Additional analyses

We utilize data on individuals' investments in multiple assets, such as P2P loans, cryptocurrency, and others. These analyses are provided in Appendix D in the Supporting Information. Our archival data analysis shows that the cryptocurrency market affects P2P lending, but we surveyed P2P lending participants to gain a better understanding of the relationship between the two markets. A detailed description of the survey is provided in Appendix E in the Supporting Information. Finally, additional analyses on possible alternative explanations are provided in Appendix F in the Supporting Information.

DISCUSSION AND CONCLUSION

Key findings

Online P2P lending and cryptocurrency markets have emerged as two of the most active and popular FinTech platforms that capitalize on innovative technologies and efficient business processes to complement established finance. In particular, P2P lending has contributed to the growth of financial inclusion by which many individuals and firms, who are excluded by formal financial institutions, can gain access to an array of financial services (i.e., loans). As financial resources move from one market to another, the rapid growth of cryptocurrency markets may affect the operation of P2P lending and its capacity to exercise financial inclusion.

Controversies and polarized viewpoints continue in regard to the value proposition and future outlook of cryptocurrencies as viable FinTech initiatives. Before the advent of cryptocurrency markets, online P2P lending received considerable practical and academic attention as a new attractive platform for alternative financing, particularly for borrowers who are excluded by conventional financial institutions. Numerous empirical explorations abound in respect to the economics of P2P lending and cryptocurrency platforms, but most were conducted in isolation. The inter‐market relationships and cross‐platform dynamics of these markets should be scrutinized, as they affect the welfare of many investors, especially those who are financially disadvantaged.

Our results indicated that as an upsurge occurs in cryptocurrency markets, P2P lending markets acquire more borrowers and a greater volume of loan requests. Loans initiated in response to bullish cryptocurrency markets are associated with reduced default rates and interest rates, as shown by increases in the number of borrowing activities among high‐creditworthy borrowers and decreases in such transactions among low‐creditworthy borrowers. These effects are manifested primarily among borrowers with tech‐savvy occupations, suggesting that rising cryptocurrency markets drive high‐creditworthy and tech‐savvy borrowers toward P2P lending as an avenue for investment in cryptocurrency markets. Therefore, cryptocurrency markets may, in the long run, undermine the democratization of access that P2P lending platforms foster by serving superfluous consumers instead of imperative consumers.

Theoretical and managerial implications

Our study contributes to the literature in several ways. Empirical works on P2P lending examined the behaviors of participants and the market mechanism within P2P lending markets (e.g., Lin & Viswanathan, 2016; Liu et al., 2015; Wei & Lin, 2017). We extended these endeavors by demonstrating that a spillover effect occurs between the two dominant FinTech platforms and that such cross‐dynamics affect the welfare of many investors, including those who are constrained in accessing traditional financial services. A recent study found that the gig economy (i.e., Uber) and crowdfunding (i.e., Kickstarter) platforms have a negative relationship and might compete against each other (Burtch et al., 2018). In contrast, by focusing on cross‐platform‐related issues, our study provided evidence that a positive externality exists between P2P lending and cryptocurrency markets. Second, we broadened the scope of inquiry to cover financial inclusion via technology. A few studies have suggested that P2P lending and blockchain‐based applications potentially enhance financial inclusion (Arifin et al., 2018; Maskara et al., 2021; Schuetz & Venkatesh, 2020). We, however, showed that newer FinTech platforms (i.e., cryptocurrency) may bring significant change to the financial inclusion cultivated in an incumbent FinTech platform (i.e., P2P lending) by increasing inequality in access to these avenues.

In terms of practice, our study presents important implications through its revelation that creditworthy and tech‐savvy investors use P2P lending to invest in cryptocurrency and suggestions on how FinTech strategies should be formulated to protect the wealth of investors and sustain focus on financial inclusion. For instance, in addition to measuring their financial risk (Wang et al., 2015), in the short term, online P2P lending managers can extract the most value by tracking and managing high‐creditworthy and tech‐savvy borrowers. Nevertheless, despite the possible short‐term gains derived from the influx of additional loan requests from high‐quality borrowers, the increased inequality in access to FinTech platforms originating from service to certain groups may hurt the long‐term sustainability of P2P lending. This double‐edged sword of FinTech platforms should be considered with care with respect to people with low credit scores and technology literacy to ensure sustainable operations. For example, policy makers can provide appropriate technological education to individuals and firms with low credit ratings and technological knowledge to prevent the potential transition from technological illiteracy to financial exclusion. From an individual perspective, people should embrace fast‐changing financial technologies and actively look for possible opportunities from FinTech platforms under a proper understanding of these modern technologies.

Conclusion

This research is not without limitations. We identified several directions that can be pursued in future studies. Although our investigation focused on the effects of cryptocurrency on debt‐crowdfunding platforms, future work should also illuminate how cryptocurrency markets influence the transaction outcomes of other crowdfunding platforms, such as reward‐based (e.g., Burtch et al., 2021) and donation‐based crowdfunding (e.g., Ge et al., 2016; Weinmann & Mishra, 2019) or the stock market (e.g., Tafti et al., 2016). Further, given that there is heavy manipulation in the cryptocurrency market (e.g., Griffin & Shams, 2020), finding a way to isolate authentic transactions might be an interesting pursuit. Next, we obtained and analyzed P2P lending data from Prosper.com, which is considered the largest channel for crowdfunding in the United States. However, our sample company does not represent the entire population of P2P lending firms, and thus other researchers can extend the generalizability of our findings by including additional lending platforms in analyses. In addition, the effects of the interdependencies between the two FinTech platforms on financial inclusion may vary depending on the economic conditions of countries. Countries establish different regulations for governing P2P lending and cryptocurrencies in a manner that best suits their financial and economic conditions. Policy makers and government agencies may interpret and use our findings to conceive of the best way to protect investors and preserve their welfare, particularly those who do not have equal opportunities to gain financial access. Finally, while our study used weather variables as instrumental variables and exploits several exogenous shocks to the cryptomarket, teasing out alternative explanations is fundamentally difficult. Although we believe that the whole set of tests we conducted can rule out many possible alternatives, future studies should also investigate alternatives.

Notwithstanding these caveats, our study lays an important foundation for future research related to the role of emerging FinTech platforms in advancing efforts by a disadvantaged segment of society to obtain equal opportunities and access to financial services at affordable costs. Our work casts light on the inter‐dynamics of FinTech markets and implications revolving around social welfare, but it also raises a number of new issues. For instance, to what extent should regulatory frameworks be enforced to protect the interests of the disadvantaged? Likewise, how should government agencies discourage the use of P2P lending as a source channel for speculative investment in alternative markets? It may be necessary that the goals of FinTech and crowdfunding should evolve as competition intensifies and regulations strengthen, but its social value and responsibility over those in need of equal financial access and opportunities must also be sustained and expanded.

Footnotes

1

2

Table A.1 in the Supporting Information provides the literature review on the financial inclusions in terms of accessibility and usage of financial services.

3

4

P2P lending provides unique borrower benefits. Typical P2P lending markets leverage various big data and machine learning technologies and offer attractive interest rates, especially to borrowers who lack credit histories or have negative histories that would make it difficult for them to borrow at reasonable rates. P2P lending significantly hastens loan processing: Borrowers can acquire loans within a few minutes with a few clicks on a mobile app. We calculated that the average duration for loan success on Prosper in 2018 was only 3.8 h.

5

Examining the effects of cryptocurrency markets on P2P lending markets is relevant for at least two reasons. First, from the perspective of investors, cryptocurrencies and P2P loans are alternative assets that are driven by similar FinTech technologies, such as decentralized networks. Thus, the two markets may draw similar users. Second, cryptocurrency markets are significantly more volatile than traditional investment assets. They operate continuously while stock markets are closed on holidays. Thus, short‐term traders who want to invest in cryptocurrencies must react quickly. If they want to use financial leverage, they must borrow in a short period of time. Consequently, online P2P lending would be better than conventional lending channels as it allows borrowers to rapidly acquire loans anytime, anywhere, with a few clicks. Thus, we believe that the two markets are closely linked.

6

In the Lend Academy Forum (forum.lendacademy.com), an online community where P2P lending participants share their investment and borrowing experiences, many users consider investment in cryptocurrencies to be an alternative to P2P lending.

7

Of particular interest to this study is the interdependence between a financial market (e.g., the cryptocurrency market) and a credit market (e.g., the online P2P lending market). Therefore, we conducted a thorough literature review of this stream of literature and highlight the incremental contribution of this study. We thank the senior editor for providing this insight. Details are provided in Appendix A in the Supporting Information.

8

Table A.3 in the Supporting Information summarizes this stream of research.

9

Uniform distributions are assumed for traceability purposes. Ceteris paribus, relaxation of the distribution assumption, does not change our results.

10

Prosper does not provide lenders' transaction history, identity, investment amount, and actual returns for 2017–2019. To derive additional insights into lenders, we utilize individual‐level investment data on both P2P lending and cryptocurrency (Subsection 4.8 provides details).

11

We obtained daily trading information for the remaining top 10 cryptocurrencies (Ripple, Bitcoin Cash, EOS, Litecoin, Cardano, TRON, Dash, and Monero). Using this measure yields similar results (see Panel B in Table 4).

12

Using only Bitcoin yielded similar results but accounted for less than 50% of the total market capitalization of cryptocracies. Therefore, we focused on the two major cryptocurrencies accounting for 68% of the total market capitalization: Bitcoin and Ethereum.

13

Moving averages are called “moving” because, as the price moves, new data are added into the calculation, therefore changing the average. They help traders isolate the trend or lack of trend in a security or market, and can also signal when a trend is reversing. Two of the most common types are simple and exponential. A 10‐day simple moving average (SMA) adds the closing prices of the last 10 days divided by 10, whereas the exponential moving average (EMA) focuses more on recent prices than on a long series of data points, as the SMA required. This difference makes the EMA react more rapidly to price changes and the SMA react more slowly. Many short‐term traders prefer EMAs because they want to be alerted as soon as the price moves. We present our main results with EMAs, but using SMAs yielded similar results. We also employed the Relative Strength Index (RSI) as the volatility measure of cryptocurrency markets. Results in Table C.6 in the Supporting Information corroborate our main results. We thank an anonymous reviewer for providing this insight.

14

In addition, we tried 7‐day or 10‐day windows before and after shocks. The results from both periods were qualitatively similar to our 5‐day window results.

15

Using coarsened exact matching (CEM) yielded similar results. For all PSM estimates in ![]() , we conducted covariate imbalance testing and found no major differences between treated and control groups in terms of their means (e.g., Table C.5 and Figure C.8 in the Supporting Information). Details are available on request. We thank an anonymous reviewer for providing this insight.

, we conducted covariate imbalance testing and found no major differences between treated and control groups in terms of their means (e.g., Table C.5 and Figure C.8 in the Supporting Information). Details are available on request. We thank an anonymous reviewer for providing this insight.

16

To explore the possibility that high‐ versus low‐creditworthy borrowers show different sensitivities to cryptocurrency booms and busts (i.e., 2017 vs. 2018) but learn to leverage P2P lending when the bull market is over, we conducted univariate comparisons of the main key variables including macroenvironmental factors. Table C.2 in Appendix C of the Supporting Information shows results for difference‐of‐means tests showing that high‐creditworthy borrowers kept their demands constant with boom and bust markets, but low‐creditworthy borrowers increased their demands in bust markets. The number of unique borrowers was stable over boom and bust markets regardless of credit levels (Figure C.7 in the Supporting Information), and low‐creditworthy borrowers showed smaller demands than high‐creditworthy borrowers. Therefore, we conjecture that low‐creditworthy borrowers did not experience learning effects that would significantly affect our main results.

17

For instance, when it is sunny, people are in a good mood and tend to evaluate future prospects more optimistically. This then makes people consider positive information more salient and psychologically available, and boost stocks. However, P2P borrowing is very different from stock investing. When a borrower wants to issue a P2P loan, the interest rate is already determined by the P2P lending platform. Moreover, the lending platform does not change its interest rates frequently. Thus, the payoff for a borrower is rather expected. Thus, we doubt that any psychological mood has a significant role in P2P borrowing. In contrast, returns of stocks and cryptocurrencies change frequently even within a day. Thus, psychological mood can be important for investors in such assets. If people use P2P borrowing to invest in cryptocurrencies, weather can affect P2P borrowing, but only via cryptocurrency prices. As long as the weather effect is indirect, we believe that our instruments are valid. As long as the weather effect is indirect, we believe that our instruments are valid. In other words, we acknowledge that our weather instruments are only valid based on the assumption that they affect P2P borrowing only through investment in stock markets and cryptocurrencies. We thank anonymous reviewers for providing this insight.