Abstract

In this study, we examine the determinants and consequences of impression management (IM) support in communications between CEOs and journalists, whereby CEOs of other firms provide positive statements about a focal CEO’s leadership and strategy and/or external attributions for low performance at the focal CEO’s firm. Drawing from social exchange theory, our theoretical perspective suggests how IM support may result from norms of reciprocity among corporate leaders. We consider the potential for direct and generalized reciprocity in the provision of IM support, including generalized reciprocity in which CEOs who received IM support previously pay the support forward to another third-party CEO, and a second form of generalized reciprocity in which CEOs reciprocate IM support to fellow CEOs whom they believe have given similar support to other CEOs in the past. We also draw from the social psychological literature on persuasion to suggest why IM support for another CEO may have a more positive influence on the tenor of journalists’ coverage about the firm’s leadership than impression management by the CEO about his or her own leadership and strategy. We test our hypotheses with data from large and mid-sized public U.S. companies from 1999 to 2007, including original survey data from a large sample of CEOs and journalists. The results supported our hypotheses, and additional findings suggested that the apparent effects of impression management by leaders and staff about their own firms following a negative earnings surprise may be partially attributable to the effects of IM support.

Keywords

Impression management has long been recognized as an important aspect of corporate leadership (Selznick, 1957; Pfeffer, 1981). A large and growing literature in organization theory and strategy has examined how corporate leaders manage the impressions of organizational constituents in the wake of image-threatening events, such as the disclosure of low firm performance, accidents, or bankruptcy, or following the announcement of controversial policies such as generous CEO pay plans or corporate diversification (e.g., Sutton and Callahan, 1987; Marcus and Goodman, 1991; Elsbach, 1994, 2003; Bansal and Clelland, 2004). A number of studies have provided evidence that leaders often seek to reassure external constituents about the quality of a firm’s leadership following the disclosure of low corporate earnings by making “external performance attributions” in annual reports and press releases that attribute the disappointing results to uncontrollable factors in the industry and macroeconomic environment (e.g., Staw, McKechnie, and Puffer, 1983; Salancik and Meindl, 1984; for a review, see Elsbach, 2003). Other studies have shown how managers attempt to allay or avoid concerns about their leadership by framing controversial policies and strategies as necessary responses to external pressures in the competitive or institutional environment, or as serving the interests of shareholders or other key constituents (e.g., Elsbach, 1994; Westphal and Zajac, 1994; Wade, Porac, and Pollack, 1997; Arndt and Bigelow, 2000; Westphal and Bednar, 2008; Westphal and Graebner, 2010). Useem (1982, 1984: 87–91) also suggested that corporate leaders of large firms, in communicating with journalists and government officials, sometimes work to promote and defend the interests of “big business” and the capitalist “system” of which they are a part.

While this literature has yielded important insights about the tactics that executives and other spokespersons use to manage the impressions of external audiences about a firm’s leadership and performance prospects, it has not addressed a major limitation to the effectiveness of impression management that has been identified in the larger literature on social influence. In particular, as social psychologists and organizational behavior scholars have long acknowledged, the influence target often perceives impression management tactics as self-serving, which tends to limit their credibility and persuasiveness (Schlenker, 1980; Jones and Pittman, 1982; Schlenker and Weigold, 1992; Leary, 2004; Lam, Huang, and Snape, 2007). The social psychological literature on persuasion similarly suggests that, given some level of ex ante uncertainty about the accuracy of a persuasive message, people tend to consider the communicator’s apparent motive when evaluating the message. To the extent that the communicator stands to benefit from the act of persuasion, the audience will tend to give less credence to the message and will be less likely to act on it (Eagly, Wood, and Chaiken, 1978; Petty and Wegener, 1999; Crano and Prislin, 2006). These literatures would seem to suggest a limitation to the efficacy of corporate leaders’ impression management. Many of the impression management tactics that have been examined in the prior literature on corporate leadership, such as external attributions for low performance or justifications for controversial policies may be perceived by constituents as attempts by corporate leaders to protect the reputation of their firms and their own reputations as leaders. As a result, these communications may often lack credibility with a firm’s constituents, who may discount them to some degree in making judgments about a firm’s leadership.

There is, however, a form of impression management that is likely to be perceived by a firm’s constituents as less self-serving than forms of impression management that have been the focus of prior research on corporate leaders. Corporate leaders may manage impressions about the leadership of particular other firms. In speaking with journalists, analysts, and certain other external constituents, corporate leaders sometimes make positive statements about the leadership of other firms, or make attributions about the performance of those firms that reflect well on their leaders. During preliminary interviews we conducted with top managers in preparation for this study, one CEO noted,

it is not uncommon for CEOs to put in a good word about other CEOs in their conversations with journalists . . . saying that the CEO has a good strategy and has done a good job leading the company. Or saying the CEO has led the company well through some difficult industry conditions.

Another CEO added,

CEOs will sometimes have positive things to say about another CEO to reporters. The media is naturally prone to blaming [disappointing earnings] on the CEO. It helps to have [another CEO suggest] that tough industry conditions or the economy have something to do with it, or a lot to do with it.

Such communications, which typically include positive statements about a CEO’s leadership and strategy and/or external attributions for low performance at the CEO’s firm, constitute impression management support (hereafter “IM support”). The content of IM support parallels the content of impression management by corporate leaders on behalf of themselves and their firms, which likewise includes external attributions for relatively low firm performance (Staw, McKechnie, and Puffer, 1983; Salancik and Meindl, 1984) and positive claims about leadership and strategy (Westphal and Deephouse, 2011). Our interviews suggested that IM support is typically provided by CEOs of other firms in the same industry, broadly defined (e.g., competitors, buyers or suppliers), as such CEOs can speak credibly to journalists about a focal CEO’s leadership and the causes of firm performance. In the financial community, for example, industry-specific knowledge and expertise is presumed to be necessary to make informed attributions about firm performance (Reingold, 2006). As a result, attributions about a firm’s performance by CEOs in the same industry are far more credible to financial analysts and other members of the financial community than performance attributions by managers in other industries. Because the financial community is an important audience for journalists who cover earnings disclosures (Dyck and Zingales, 2002; Joe, Louis, and Robinson, 2009), such journalists tend to strongly prefer CEOs in the same industry as sources in writing these stories (Gans, 1979; Shoemaker and Reese, 1996). Thus, in reporting on an earnings disclosure, journalists tend not to solicit the opinions of CEOs in other industries, and such CEOs tend not to offer their assessments, knowing that they would not be viewed as a credible source.

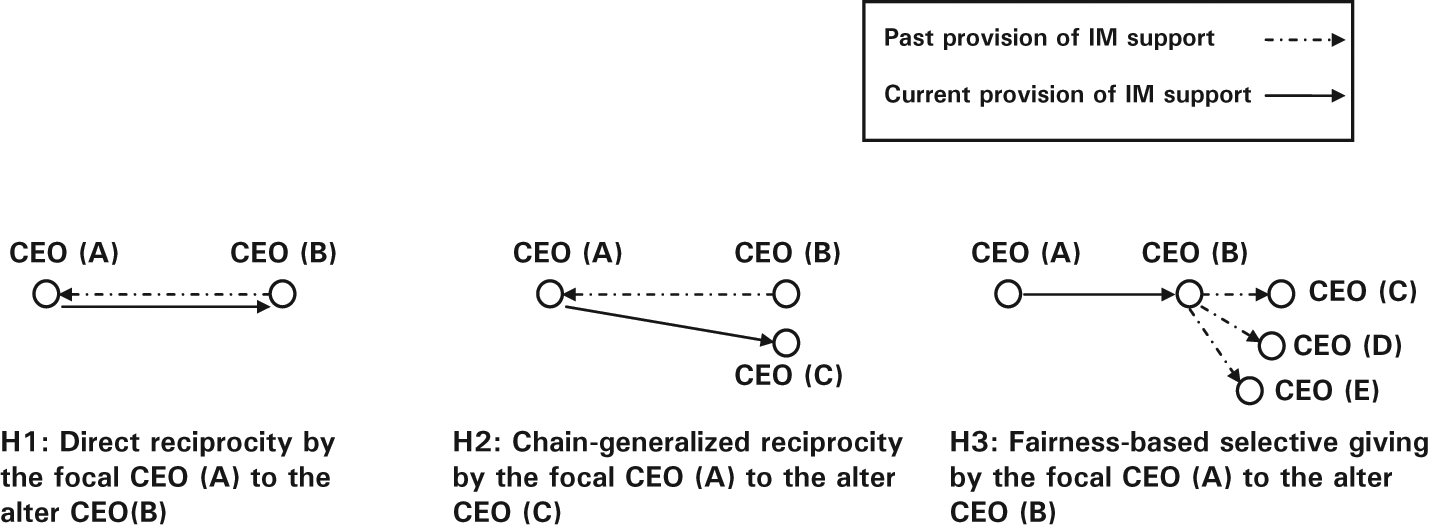

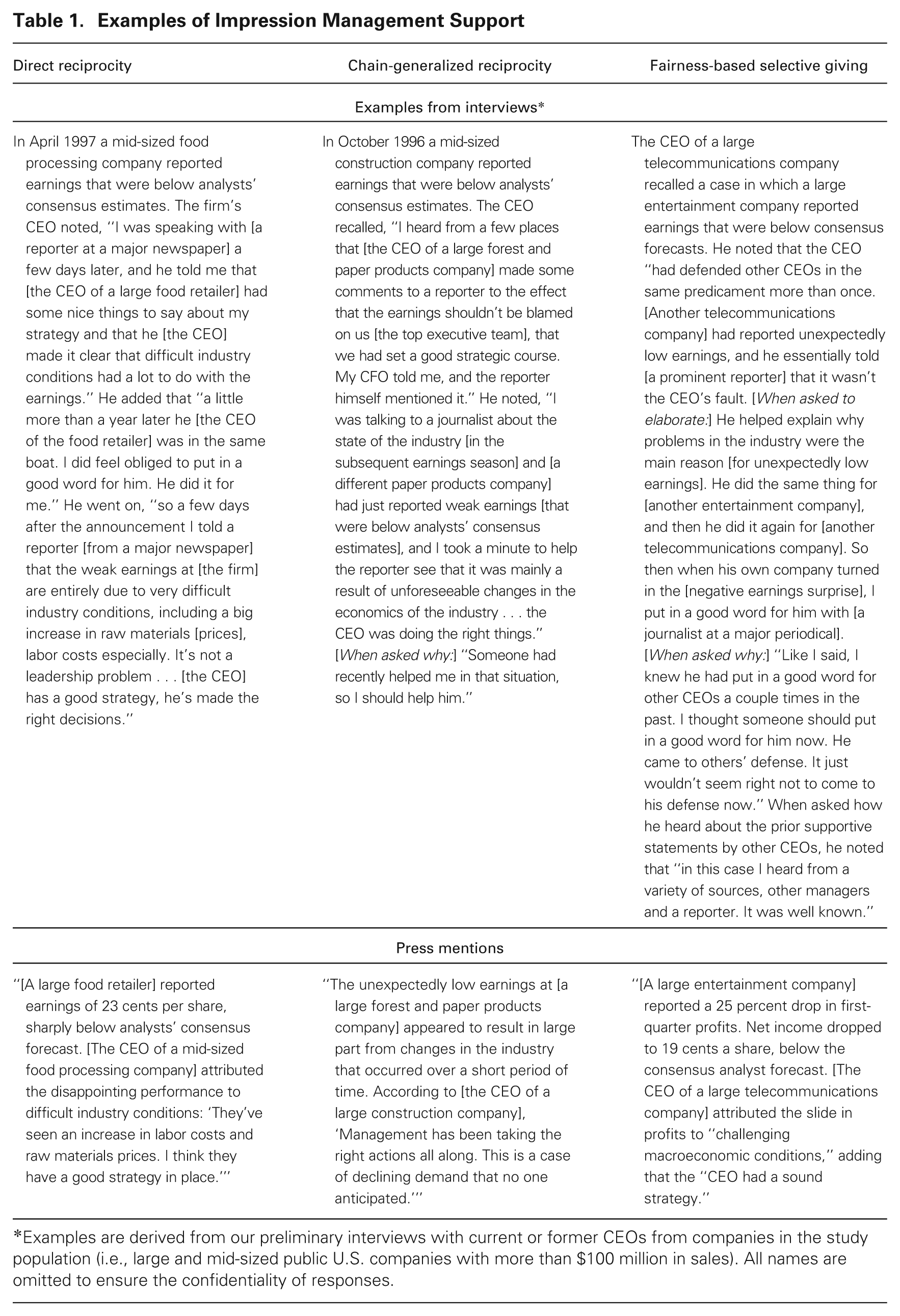

In this study, we investigate the determinants and consequences of IM support in communications between CEOs and journalists. The first part of our theoretical framework draws from social exchange theory to suggest how IM support may reflect norms of reciprocity among corporate leaders. In particular, we consider how IM support may result from (1) direct reciprocity in which CEOs who have received IM support from another CEO in the past tend to reciprocate the favor by providing their benefactor with similar such support when needed, (2) generalized reciprocity in which CEOs who received IM support in the past are more likely to provide similar support to another (third) CEO, and (3) a distinct form of generalized reciprocity known as fairness-based selective giving, wherein CEOs provide IM support for fellow CEOs whom they believe have given similar support to other corporate leaders in the past. Figure 1 depicts the three social exchange mechanisms in our framework, and table 1 includes specific examples of IM support from our interviews illustrating each form of reciprocity. Although in principle CEOs could engage in IM support in a strategic attempt to forge ties with other corporate leaders, in the present study, we focus on impression management that reflects normative obligations in social exchange relationships. Our theory suggests that when the three forms of social exchange are considered together, norms of reciprocity emerge as an important determinant of impression management behavior. The second portion of our framework addresses the consequences of IM support. We draw from the social psychological literature on persuasion to suggest why IM support for another CEO may have a more positive influence on the tenor of journalist coverage about the firm’s leadership than impression management by the CEO about his or her own leadership, strategy, and performance.

Different social exchange mechanisms in the provision of impression management support.

Examples of Impression Management Support

Examples are derived from our preliminary interviews with current or former CEOs from companies in the study population (i.e., large and mid-sized public U.S. companies with more than $100 million in sales). All names are omitted to ensure the confidentiality of responses.

On one level, this study identifies and examines a form of impression management by corporate leaders that has received little if any scholarly attention in the literature, namely, impression management by corporate leaders about the leadership of particular other firms. A primary contribution of our study to the literature on organizational impression management and the larger literature on social influence is to develop theory regarding why this particular form of impression management is likely to be more persuasive to constituents than forms of impression management that have been the focus of prior research and may therefore have an especially positive influence on constituents’ opinions about firms and their leaders. In particular, we theorize that IM support is likely to be relatively effective as a form of social influence because it should be perceived as less self-serving than impression management by corporate leaders about their own leadership, strategy, and performance and may therefore be relatively credible and persuasive to important firm constituents. In addition, our study identifies a novel category of determinants of impression management behavior. Prior research has focused primarily on organization-level factors (e.g., low firm performance) and individual-level factors (e.g., personality attributes) as determinants of impression management and has given little consideration to how such behavior may reflect social exchange processes within or between organizations. Accordingly, our theory also contributes to the social influence literature by revealing how different forms of social exchange can influence the propensity for corporate leaders to engage in impression management.

Social Exchange and Impression Management Support

The Role of Direct Reciprocity

Our social exchange perspective suggests that a focal CEO will be more likely to provide IM support for another CEO when the latter has provided such support to the focal CEO in the past. Direct reciprocation of this kind is compelled by the norm of reciprocity, which is a nearly universal code of moral conduct (Gouldner, 1960). An interdisciplinary literature on “inequity aversion” indicates that most people exhibit a psychological aversion to over-benefitting or under-benefitting from social relationships and will sacrifice material resources or non-material resources such as time to avoid such inequity (Fehr and Schmidt, 1999; Camerer and Fehr, 2004; Johansson and Svedsater, 2009). Studies have shown that when people receive specific forms of help from another person, such as verbal support in the face of criticism, they tend to exhibit psychological “distress” at the prospect of not providing similar help when their benefactor is in the same predicament (Vaananen et al., 2005). As a result, when an individual receives help from another person, he or she will be motivated to return the service when given the opportunity, to avoid the psychological distress that is created by over-benefitting from the relationship. In the present context, therefore, CEOs who have received IM support from another CEO should feel normatively and psychologically compelled to reciprocate the favor by providing their benefactor with similar support when given the opportunity to do so.

In some circumstances, the norm of reciprocity may be bolstered by instrumental motives to reciprocate, as individuals reciprocate favors to increase the probability of receiving more favors in the future (Blau, 1964; Deckop, Cirka, and Anderson, 2003). But there is growing evidence from the experimental literature that such instrumental motives tend to be weaker determinants of reciprocation than the perceived social obligation to reciprocate, especially when the favor in question involves helping another person cope with a significant problem (Fehr, Fischbacher, and Gächter, 2002; Gintis et al., 2003; Vaananen et al., 2005). In explaining these findings, psychologists have suggested that people tend to discount the present value of future helping behavior by another social actor, in part because systematic cognitive biases related to overconfidence and overoptimism lead individuals to underestimate the likelihood that they will need future help in dealing with a significant problem. At the same time, there is evidence that norms of reciprocity and the resulting psychological aversion to over-benefitting from social relationships have an especially strong effect on the propensity for individuals to reciprocate help in dealing with a significant personal or professional problem. A number of studies indicate that most people will reciprocate such helping behavior without any prospect of receiving further help in the future, as in one-shot exchanges between strangers, and at significant costs to themselves (Hoffman, McCabe, and Smith, 1998; Webster et al., 1999; Fehr, Fischbacher, and Gächter, 2002).

In the present context, norms of reciprocity and psychological aversion to inequity should induce CEOs to reciprocate the provision of IM support. Specifically, CEOs who have received IM support from another CEO following the disclosure of low corporate earnings should tend to reciprocate the favor by providing their benefactor with such support when given the opportunity (i.e., following the disclosure of low earnings at the benefactor’s firm). We expect reciprocation of IM support that occurs in response to unexpectedly low earnings or a “negative earnings surprise”—earnings below consensus forecasts of security analysts (Hirshleifer et al., 2008)—because prior research indicates that the risk of negative media coverage about firms, including negative statements about firms’ leadership or unfavorable performance attributions by journalists is especially high following a negative earnings surprise (Westphal and Deephouse, 2011). Negative earnings surprises prompt members of the financial community to assess the causes of the unexpectedly low performance (Barron, Byard, and Yu, 2008), and journalists seek to inform those assessments (Gans, 1979). As a result, journalists are more likely to report on firms’ leadership and strategy following these events. Moreover, there is inherent uncertainty about the degree to which negative earnings surprises are attributable to internal causes such as firms’ leadership and strategy versus external causes such as uncontrollable changes in the industry environment, creating the opportunity for social influence by corporate leaders. At the same time, social psychological perspectives on corporate leadership suggest that in the absence of social influence, journalists and other external constituents are predisposed to attribute firms’ performance (whether positive or negative) to corporate leaders, and to the CEO in particular as the most visible figurehead of the firm (Salancik and Meindl, 1984; Meindl, Ehrlich, and Dukerich, 1985; Hayward, Rindova, and Pollock, 2004). Accordingly, IM support following a negative earnings surprise is likely to be especially helpful to CEOs and thus especially likely to be viewed as a favor that should be reciprocated when the opportunity arises. This leads to the following hypothesis:

The Role of Generalized Reciprocity

Social exchange theory suggests that generalized reciprocity can extend beyond dyadic exchange. Contemporary typologies of social exchange include three main forms of generalized reciprocity, two of which could help explain IM support among corporate leaders. The first, potentially relevant form of generalized exchange is so-called “chain-generalized reciprocity,” in which a social actor A helps another actor B, who in turn “pays it forward” by helping a third actor C (Lévi-Strauss, 1969; Ekeh, 1974: 53; Takahashi, 2000; Molm, Collett, and Schaefer, 2007; Baker and Levine, 2010). Such reciprocity has been implicated in a wide range of helping behaviors, from mentoring (e.g., a senior colleague mentoring a junior colleague as he or she was mentored) to donating blood, to journal reviewing. Social exchange theory suggests that the diffusion of helping behaviors can result from generalized norms of reciprocity in which individuals who have received a particular kind of help feel obligated to help others as they were helped when the opportunity to provide aid presents itself (Ekeh, 1974; Uehara, 1990; Westphal and Zajac, 1997; Takahashi, 2000). As noted above, research on inequity aversion has shown that most people are psychologically predisposed to avoid over-benefitting or under-benefitting from their social relationships (Fehr and Schmidt, 1999; Camerer and Fehr, 2004; Johansson and Svedsater, 2009). One kind of social inequity is to receive a particular form of help from one’s peers and then fail to provide such help to others when given the opportunity (Vaananen et al., 2005). Most people feel psychological distress or guilt from such inequity and are motivated to avoid it (Huseman, Hatfield, and Miles, 1987; Vaananen et al., 2005). Thus inequity aversion is a social psychological mechanism by which generalized norms of reciprocity promote the spread of helping behavior in a population. The potential for inequity aversion to motivate helping is illustrated by the following quote from our preliminary interviews:

I felt compelled to put in a good word for him with [a journalist]. Someone did that for me a couple years ago in the same situation, so I felt like I should do it for him. [When asked why he felt compelled:] Again, someone helped me in the same situation. It wouldn’t feel right not to take the opportunity to help this guy. I’d feel guilty in a way.

A growing, interdisciplinary literature on generalized reciprocity has provided fairly robust evidence that people who receive a favor from another social actor are more likely to perform that favor for a third actor when given the opportunity, even when helping requires the sacrifice of material or other resources (e.g., time) without any prospect of receiving further benefits (as in one-shot, unilateral exchanges between strangers, or when givers and receivers are anonymous) (e.g., Gintis et al., 2003; Greiner and Levati, 2005; Stanca, 2009; Baker and Levine, 2010). Social exchange theory suggests that the frequency of such reciprocity is likely to be especially high when there is a common basis for social identification among actors, as when they occupy a similar social role or are members of the same community (Ekeh, 1974; Buchan, Croson, and Dawes, 2002; Flynn, 2005; Lawler, Thye, and Yoon, 2008). Research on corporate elites has provided extensive qualitative evidence, as well as recent large-sample survey evidence, that CEOs of large companies tend to socially identify with each other, at least to some degree, as fellow corporate leaders (Useem and Karabel, 1986; O’Reilly, Main, and Crystal, 1988; McDonald and Westphal, 2010). Accordingly, generalized reciprocity may occur on a relatively frequent basis among CEOs of large companies.

Thus theory and research on social exchange suggests that CEOs who have received a particular form of help from a fellow CEO should be more inclined to provide such help to another (third) CEO when given the opportunity. In particular, CEOs who have received IM support from a fellow CEO following the disclosure of negative earnings will be more likely to provide such support to another CEO following the disclosure of negative earnings at the other CEO’s firm. As discussed above, IM support should occur most frequently among CEOs in the same industry. This leads to the following hypothesis:

Contemporary typologies of social exchange include a second form of generalized reciprocity in which the provision of help by one social actor A to another actor B is reciprocated by a third actor C. In this scenario, C feels obligated to help A to the extent that A has provided similar help to others in the past. This form of reciprocity has been characterized as “fairness-based selective giving,” or social indirect reciprocity (Takahashi, 2000, 2005; Penner et al., 2005; Stanca, 2009; Baker and Levine, 2010: 5). 1 The literature on inequity aversion indicates that most people are psychologically predisposed to avoid or reduce social inequity, not only in their own relationships but also in relationships among their peers (Camerer and Fehr, 2004; Johansson and Svedsater, 2009). One such inequity is when a peer who has helped others in the past does not receive similar help from his or her peers when needed. Research indicates that most people feel cognitive dissonance when exposed to social inequities of this kind, and they feel psychological distress or guilt when they do not take opportunities to redress or avoid such inequities (Walster, Berscheid, and Walster, 1973; Johansson and Svedsater, 2009). Such inequity aversion provides the foundation for fairness-based selective giving. There is growing evidence that people are more likely to help a peer in need when they believe that the peer has provided similar help to others in the past, even when helping requires the sacrifice of material or other resources without any expectation of receiving further benefits (as in anonymous, unilateral exchanges) (Gintis et al., 2003; Seinen and Schram, 2006; Stanca, 2009; Baker and Levine, 2010).

This literature would also suggest that people are especially likely to engage in fairness-based helping toward peers or comparison others with whom they can socially identify (e.g., individuals who occupy the same or similar social roles) (Walster, Berscheid, and Walster, 1973; Johansson and Svedsater, 2009). As discussed above, there is considerable evidence that CEOs of large companies tend to view each other as peers and are prone to socially identify with each other as fellow corporate leaders. Thus we expect that fairness-based helping could occur among members of the corporate elite and may be manifested in the provision of IM support among corporate CEOs. Specifically, CEOs should be more likely to provide IM support for fellow CEOs whom they believe have provided similar support for other corporate leaders in the past. The potential for inequity aversion to motivate IM support in this way is illustrated by the following quote from our interviews: “I knew he had put in a good word for other CEOs a couple times in the past. I thought someone should put in a good word for him now. He came to others’ defense. It just wouldn’t seem right not to come to his defense now.” Overall, our theory leads to the following hypothesis:

IM Support and Journalists’ Reporting

As noted above, social influence theorists have acknowledged that impression management is less likely to be effective to the extent that it appears self-serving to the influence target. According to the elaboration likelihood model of persuasion, given some level of ex ante uncertainty about the accuracy of a persuasive message, the perceived self-interest of the communicator is a primary heuristic cue in assessing the veridicality or trustworthiness of the message (Crano and Prislin, 2006; Durantini et al., 2006; Petty and Brinol, 2008). The greater the extent to which a stated opinion appears to be motivated by self-interest, the more people are likely to reflect on counterarguments and seek out other points of view (Crano and Prislin, 2006; Reinhard and Messner, 2009). In fact, this literature indicates that people tend to over-utilize perceived self-interest as an indicator of a message’s validity. To economize on cognitive effort and attention, most people reflexively devote less cognitive scrutiny to persuasive messages to the extent that the communicator is not obviously motivated by self-interest, or there is not a relatively strong and salient ulterior motive for the communication, even when the message is one-sided and they (members of the audience) have a material incentive to form an accurate judgment (Petty and Wegener, 1999; Durantini et al., 2006).

Moreover, people are especially likely to rely on the level of perceived self-interest of the communicator as a heuristic cue when they face knowledge asymmetries about the subject (Petty and Wegener, 1999). In the present context, journalists face knowledge asymmetries vis-à-vis CEOs in assessing the quality of firms’ leadership and in making attributions about firms’ performance, and they normally have significant constraints on the time and attention that they can devote to any one story (Tuchman, 1972; Gans, 1979; Cose, 1989; Shoemaker and Reese, 1996; Wiesenfeld, Wurthmann, and Hambrick, 2008). Thus CEOs’ communications are especially useful to journalists in assessing the quality of firms’ leadership and making attributions about firms’ performance, rather than relying on their own, less expert opinion or incurring the costs of gathering additional information. At the same time, knowledge asymmetries make journalists vulnerable to misleading statements by CEOs. The persuasion literature would suggest that, under such conditions, journalists are especially likely to use the level of apparent self-interest of the CEO as a heuristic cue of the reliability of the CEO’s assessment. The less the CEO has an obvious self-interest in persuading the journalist about the quality of a firm’s leadership or the causes of a firm’s performance, the more inherently credible the CEO will be to the journalist, the less critical scrutiny the journalist will tend to devote to the persuasive message or to seeking out opposing points of view, and consequently the more weight the journalist will ultimately give to the CEO’s account in reporting on the firm’s leadership and performance. Ethnographic studies of journalistic practice in the sociology and communication literatures also indicate that journalists evaluate the quality of a source based largely on its apparent objectivity (Tuchman, 1972; Shoemaker and Reese, 1996; Croteau and Hoynes, 2003). Thus journalists are less likely to rely on the assessment of a CEO to the extent that the CEO’s judgment would appear obviously self-serving to important audiences (e.g., editors and readers).

Whereas CEOs have a relatively strong self-interest in persuading journalists about the quality of their own leadership and strategy, and in making external attributions for the low performance of their firms, they have a relatively less obvious self-interest in persuading journalists about the quality of other CEOs’ leadership and strategies, or in making external attributions for other firms’ low performance. There is evidence from the social psychological literature on helping that people tend to systematically underestimate the extent to which various forms of social support provided to other social actors are motivated by self-interest (Davis and Maitner, 2010). In making attributions about the extent to which supportive behaviors reflect self-serving motives, people tend to focus primarily on direct or immediate benefits to a focal actor from giving support to another social actor, while giving less consideration to indirect or longer-term benefits of providing support (Penner et al., 2005; Fiske and Taylor, 2008; Davis and Maitner, 2010). Given that the potential benefits to a CEO of making positive statements about the leadership and strategy of another firm are likely to be more indirect and less immediate than the potential benefits of managing impressions about the CEO’s own leadership and strategy, social psychological perspectives on social support would suggest that positive statements by CEOs about the leadership and strategy of another firm may appear less self-serving and thus have greater credibility in the eyes of journalists than positive statements or external performance attributions by CEOs about their own firms. As a result, our theoretical argument would suggest that IM support as conceptualized above will have a more positive influence on the tenor of journalists’ reporting than CEOs’ impression management about their own firms. Specifically, such support will be especially effective in reducing the propensity for journalists to make negative statements about a CEO’s leadership and strategy or external attributions for low performance of the CEO’s firm. Moreover, IM support should be especially likely to reduce the negativity of journalists’ coverage following the disclosure of negative earnings surprises, because, as noted above, the risk of negative coverage about a firm’s leadership is especially high after a negative earnings surprise. This leads to a final hypothesis about the relationship between IM support and the negativity of journalists’ reporting about the firm’s leadership following a negative earnings surprise, wherein less negative reporting is indicated by fewer negative statements made by the journalist about the firm’s leadership and more external attributions for low firm performance.

Method

Sample and Data Collection

The population for this study included CEOs at large- and mid-sized public U.S. companies with more than $100 million in sales, as listed in the Reference USA index. The initial sample frame included 800 CEOs who responded to a 1998 survey on corporate governance. K-S tests indicated that these CEOs were representative of CEOs in the larger population on each of the archival variables in our study, discussed below. Three hundred and sixty-seven of these CEOs (46 percent) agreed to participate in the study, which involved responding to questionnaires about their communications with journalists, other executives, and constituents from 1999 to 2007. We measured IM support with survey responses from both potential support providers and receivers. As noted above, our preliminary interviews suggested that IM support may be provided by CEOs of competitors, CEOs of firms in buyer industries (i.e., current or potential buyers), or CEOs of firms in supplier industries (see Appendix for further details). Thus we also sent questionnaires to CEOs of firms in the population that are competitors, buyers, or suppliers of firms with a participating CEO. Industry was defined by the two-digit SIC code, and potential buyer and supplier firms were identified using input-output accounts data generated by the Bureau of Economic Analysis. To measure IM support, we sent surveys to these CEOs at regular intervals surrounding each earnings disclosure by firms with a participating CEO (i.e., just prior to an earnings disclosure, two weeks after the disclosure, and four weeks after the disclosure) during the study period. The average response rate to these surveys was 41 percent and did not change significantly during the study period.

We also surveyed journalists at the same regular intervals surrounding each earnings disclosure by firms in the sample: just prior to the disclosure, two weeks after the disclosure, and four weeks after the disclosure. For each earnings disclosure, we identified journalists from major news and business publications in the U.S., as listed in Factiva and LexisNexis (Pollock and Rindova, 2003), who had reported on the firm making the disclosure during the 12 months prior to disclosure. We also identified journalists from daily newspapers in a city in which the focal firm was headquartered or had significant operations who had reported on the firm during the 12 months prior to disclosure. From this set of journalists, we surveyed up to three individuals for each earnings disclosure; if more than three journalists covered a particular firm, three were randomly selected to receive surveys (see Appendix for further detail). The average response rate to these surveys was 42 percent and did not change significantly during the study period.

We used Heckman models to test for sample selection bias (Heckman and Borjas, 1980). The selection equation estimates the likelihood of responding to the survey, and the inverse Mills ratio is included in a second-stage equation that estimates the hypothesized relationships. The selection equation included independent and control variables measured with archival data, as well as variables that explain variation in the survey process. The selection parameter was consistently non-significant, and the hypothesized results were not substantively different from those presented below, providing evidence that nonresponse bias does not threaten the validity of our results. We used standard sources for our archival measures, and these are summarized in the Appendix.

Measures

Low earnings relative to consensus forecasts (negative earnings surprise)

In the primary analyses, we measured negative earnings surprises by calculating the difference between a focal firm’s most recently reported quarterly earnings and the median forecasted earnings for the same period among all analysts who covered the firm (Kasznik and Lev, 1995; Barron, Byard, and Yu, 2008; Hirshleifer et al., 2008). This value was adjusted by the firm’s stock price at the end of the most recent quarter (Kasznik and Lev, 1995; Barron, Byard, and Yu, 2008). The variable was inverted so that higher values indicate more negative earnings relative to consensus forecasts and was set to zero when earnings were above forecasts. In separate analyses, we (1) used a dichotomous variable coded “1” if earnings were below consensus forecasts, (2) used the raw values, unadjusted for stock price, (3) controlled for earnings above forecasts, and (4) controlled for the average reported earnings of competitors. The hypothesized results were substantively unchanged in each of these models.

Journalists’ reporting about the company

To measure the negativity of journalists’ reporting in tests of H4, we identified all articles written by journalists in the sample during the four-month period following the period in which IM support was measured that mentioned a firm or CEO in the sample. We also coded such articles in the prior two-year period in developing controls for prior journalists’ reporting. Three coders independently assessed each article. The coders had substantially different backgrounds, permitting a stronger test of interrater reliability (Weber, 1985). In the primary analysis, the recording unit was the sentence. In line with recent content analyses of journalists’ reports, each sentence referring to a company or CEO in the sample was coded as positive, negative, or neutral (Deephouse, 2000; Pollock and Rindova, 2003). Coders then determined whether each negative statement referred to the leadership or strategy of the firm. We summed the number of such statements in articles by the focal journalist over the specified time period and compared the resulting measures across the three coders. The intraclass correlation coefficient (ICC) was .92, indicating high interrater reliability. Coders also judged whether each statement represented an external attribution for low firm performance, using coding instructions based on Staw, McKechnie, and Puffer’s (1983) procedure for identifying external attributions in annual reports (also Westphal and Deephouse, 2011). Again we summed the number of external attributions in articles by the focal journalist over the specified time period and compared the resulting measures across the three coders. There was a similarly high level of interrater reliability (ICC = .93).

We tried many variations of this coding procedure to assess the robustness of our results. For example, the results were robust to (1) alternative recording units, including the paragraph, the “point,” or the entire article; (2) measuring the negativity of each journalist’s statement using either a 4-point Likert-type scale or the Janis-Fadner coefficient of imbalance; and (3) measuring the negativity of journalists’ reporting over various time windows. While in the primary analyses, we used a two-month window (i.e., two months following the period in which IM support was measured), the results were substantively unchanged using shorter or longer windows (e.g., two weeks, one month, three months, or four months).

IM support

We developed multi-item scales to assess the extent to which CEOs provided IM support over specific time periods (see Appendix for scale items). The scales were designed to capture key dimensions of IM support identified in our preliminary interviews and discussed in our theoretical argument. Specific items prompted CEOs to indicate the number of instances in which they made positive statements about another CEO’s leadership to journalists, for example, “In communicating with a journalist [over specified time period], did you make positive remarks about [alter’s] leadership? . . . How many times? [Specify journalist(s) and date(s)]”, and external attributions for low performance of another CEO’s firm, for instance, “In communicating with a journalist [over specified time period], did you suggest that low firm performance at [alter’s firm] can be attributed to uncontrollable factors in the industry or macroeconomic environment? . . . How many times? [Specify journalist(s) and date(s)]”. The scales also included items that assess whether CEOs intended to manage the impressions of constituents about another CEO in making external performance attributions and positive statements about the CEO’s leadership to journalists, for example, “In communicating with a journalist [over specified time period], did you make the case that low firm performance at [alter’s firm] cannot be attributed to firm strategy, mainly to help bolster [alter’s] image with firm constituents? . . . How many times? [Specify journalist(s) and date(s)]”. Respondents answered these questions separately for each CEO in their industry with whom they were familiar (including CEOs of potential buyer and supplier firms). Confirmatory factor analysis (CFA) indicated that the IM support items loaded on the same factor as expected, without loading on other factors in the measurement model, and the standardized validity coefficients were highly significant for all scale items. The alpha for the scale was also acceptably high (.89).

Participating (“focal”) CEOs answered these questions on a quarterly basis during the study period. As noted above, we also surveyed CEOs of competitors, buyers, or suppliers of a focal CEO’s firm at regular intervals surrounding earnings disclosures by the focal firm (i.e., just prior to an earnings disclosure, two weeks after the disclosure, and four weeks after the disclosure). Thus CEOs responded to the questions about IM support for each of these time intervals.

As discussed further below, the unit of analysis in models of IM support is the CEO dyad (i.e., dyadic combinations of a focal CEO and other CEOs in the same industry). The dependent variable in these models is the number of instances of IM support provided by a focal CEO for another CEO (“alter”)—as reported by the focal CEO—following the disclosure of quarterly earnings at alter’s firm. In the primary analysis, we measured IM support for the two-week period following earnings disclosures, while controlling for support in the prior period. Separate analyses indicated that the results were robust to alternative time windows, including one week and four weeks following an earnings disclosure. For H1, which predicted direct reciprocity of IM support, the independent variable represents the number of instances of IM support provided by alter to the focal CEO—as reported by alter—following a negative earnings surprise at the focal CEO’s firm during the prior two-year period (t-2 to t0). We also separately measured IM support provided by alter during the previous three-year period (t-5 to t-2). 2 For H2, which predicted generalized reciprocity of IM support, the independent variable represents the number of instances of IM support provided by all other CEOs except the alter to the focal CEO following a negative earnings surprise at the focal CEO’s firm during the prior two-year period (see Appendix for further detail).

We developed a separate survey scale to test H3, which predicted that a focal CEO would be more likely to provide IM support for another CEO (alter) to the extent that he or she was aware of prior instances of IM support by alter for other CEOs. The scale items are provided in the Appendix. They directly parallel items in the IM support scale described above, for example, “Are you aware of instances [over specified time period] in which [alter] made positive remarks about another CEO’s leadership to a journalist? [Specify CEO(s)]. How many times that you are aware of [i.e., for each CEO]?”. CFA indicated that the items loaded on a single factor as expected. Validity coefficients were highly significant for all items, and reliability was acceptably high (α = .91). The independent variable for tests of H3 represents the number of instances of IM support provided by alter for other CEOs during the prior two-year period of which the focal CEO is aware. This measure was based on survey responses from the focal CEO just prior to the earnings disclosure at alter’s firm. Again we also separately measured the CEO’s awareness of IM support by alter during the previous three-year period. There was a high correlation between the focal CEO’s perception of IM support by alter and self-reported IM support by alter (ICC = .88), suggesting that CEOs tended to be become aware of IM support by other CEOs in the same industry.

As discussed further below, the unit of analysis in models of journalists’ reporting is the firm-journalist dyad (i.e., a focal CEO and a journalist who reports on the CEO’s firm). In the primary models, we used journalists’ responses to measure the independent variable for H4, which addresses the effect of IM support on journalists’ reporting about firm leadership. Journalists responded to questions that directly parallel the IM support items described above and listed in the Appendix, for example, “Since [date of the earnings disclosure], did [another CEO] suggest that low firm performance at [the focal CEO’s firm] can be attributed to uncontrollable factors in the industry or macroeconomic environment? . . . [Specify the CEO(s) who made the suggestion(s)] How many times [did the CEO make such a suggestion]? [Specify date(s) on which suggestion(s) were made]”. The independent variable for H4 represents the number of instances in which other CEOs made positive statements about the focal CEO’s leadership or external attributions for low performance at the focal CEO’s firm in conversations with the focal journalist during the two-week period subsequent to an earnings disclosure. In separate tests of H4, we measured IM support using CEOs' responses and over shorter and longer time periods, including one week and four weeks following earnings disclosures, and the hypothesized results presented below were unchanged.

We also developed alternative indicators of IM support by examining whether CEOs in the sample frame were quoted by journalists as making positive statements about another firm’s leadership or external attributions for another firm’s low performance. Specific examples of such quotations are included in table 1 above. We searched multiple archival sources, including Factiva and LexisNexis, for articles during the relevant time periods that quoted CEOs in the sample. The three coders mentioned above then assessed whether each quotation represented a positive statement about another firm’s leadership or an external attribution for another firm’s low performance. There was an adequately high level of interrater agreement among the three coders in making these assessments: weighted kappas (K) ranged from .88 to .90. We then developed the following independent variables to provide alternative tests of H1–H3: the number of times alter was quoted in the press as making positive statements about the focal firm’s leadership or external attributions for the focal firm’s low performance during the prior two-year period (H1); the number of times other CEOs (except alter) were quoted in the press as making positive statements about the focal firm’s leadership or external attributions for the focal firm’s low performance during that period (H2); and the number of times alter was quoted in the press as making positive statements about other firms’ leadership (aside from the focal firm) or external attributions for other firms’ low performance (H3).

Other forms of impression management

We used survey scales and archival data to develop six measures of impression management by top executives and other staff about their own firms. These measures were validated by Westphal and Deephouse (2011) and are described in detail in the Appendix. They gauge impression management in conference calls, letters to shareholders, and press releases, and they also measure impression management by CEOs, CFOs, and public relations staff in communications with journalists outside conference calls.

Other controls

Details about the other controls are provided in the Appendix. Models of IM support included the following controls: friendship ties, demographic similarity, and common board ties between CEOs; multi-item survey scales that indicate the level of communication between the focal CEO and journalists and the number of occasions on which journalists invited the CEO to comment on the performance of alter’s firm over the period for which IM support was measured; the number of board appointments held by each CEO; the tenure of each CEO; the log of total sales at each CEO’s firm; the most recently disclosed corporate earnings (relative to consensus forecasts) at the focal CEO’s firm; dummy variables that indicate whether the focal CEO’s firm was a current or potential supplier of alter’s firm, a current or potential buyer, a competitor, or an alliance partner; the mean-deviated four-firm concentration ratio of the focal firm’s industry; Mizruchi’s (1992) measure of market constraint; industry dummy variables (not reported); and prior levels of the dependent variable (i.e., prior instances of support by the focal CEO and other CEOs for alter over the previous two-year period). In models of journalists’ reports, we controlled for the following: friendship ties between CEOs and journalists; survey measures developed by Westphal and Deephouse (2011) that indicate CEO ingratiation toward journalists and journalists’ awareness of instances in which other reporters were unable to communicate with the focal CEO; CEO tenure; the number of board appointments held by the CEO; the CEO’s attendance at an elite undergraduate or business school; the level of CEO compensation; the most recently reported return on assets and total sales (logged) of the CEO’s firm; other major firm announcements during the prior six-month period that could be expected to influence journalists’ reports; the average number of negative statements about the firm’s leadership and the average number of external performance attributions made by other journalists over the period for which IM support was measured; dummy variables indicating (1) whether the focal journalist was employed by a general news outlet or an outlet that focuses on business news and (2) whether the journalist was employed by the particular media outlet as a commentator; prior levels of the dependent variable (i.e., negative statements about the firm’s leadership and external attributions for low performance issued by the focal journalist during the prior two-year period); prior positive statements about (a) the focal firm’s leadership and (b) the focal firm’s industry (i.e., statements by the journalist about trends or opportunities in the industry that suggest relatively good performance prospects for firms in the industry); prior negative statements about the focal firm’s industry (statements about trends, problems, or threats in the industry that suggest relatively poor prospects).

Analysis

We measured IM support and journalists’ reports on a quarterly basis (surrounding each quarterly earnings disclosure) over a nine-year period. The independent variables for H1–H3 measured IM support over the previous five-year time period (i.e., the five years prior to an earnings disclosure). Thus we tested these hypotheses by estimating IM support for the remaining four-year panel (2004–2007), which includes 16 quarterly spells of data. The dependent measure is a count variable with overdispersion. Thus we estimated IM support using negative binomial regression. To correct for serial correlation, we used the random effects model. The Hausman (1978) test confirmed that a random effects model is adequate for estimating the model coefficients (p > .20). The unit of analysis in these models is the CEO dyad (i.e., dyadic combinations of potential support providers and other CEOs in the industry who are potential support receivers). Because this sample includes multiple dyads that involve the same CEO, we adjusted for non-independence of observations using a robust variance estimator for clustered data (Wooldridge, 2003). Our measures of journalists’ reports are counts that do not exhibit overdispersion (a likelihood-ratio test indicated that the overdispersion parameter is not significantly different from zero). Thus we estimated these variables using random effects Poisson regression. The Hausman test again confirmed that a random effects specification is appropriate. The unit of analysis is the firm-journalist dyad, and multiple dyads involve the same journalist. Thus we again used a robust variance estimator to correct for bias in the standard errors from non-independence of observations. We ran further analyses to assess robustness to alternative estimators, and these are summarized in the Appendix.

We estimated the effects of IM support on journalists’ reports in two ways. In one set of models, we used interaction terms to examine whether IM support and other forms of impression management dampen the effect of negative earnings surprises on negative journalists’ reports about firm leadership in the full sample. As an alternative approach, we developed Heckman selection models in which the selection equation estimates the likelihood of a negative earnings surprise using probit regression, and parameter estimates from that equation are included in second-stage Poisson models to estimate negative statements by journalists about firm leadership and external attributions for low performance (for the subsample of firms that disclosed a negative earnings surprise). These models control for unmeasured differences between firms that disclosed a negative earnings surprise and other firms in the population.

Results

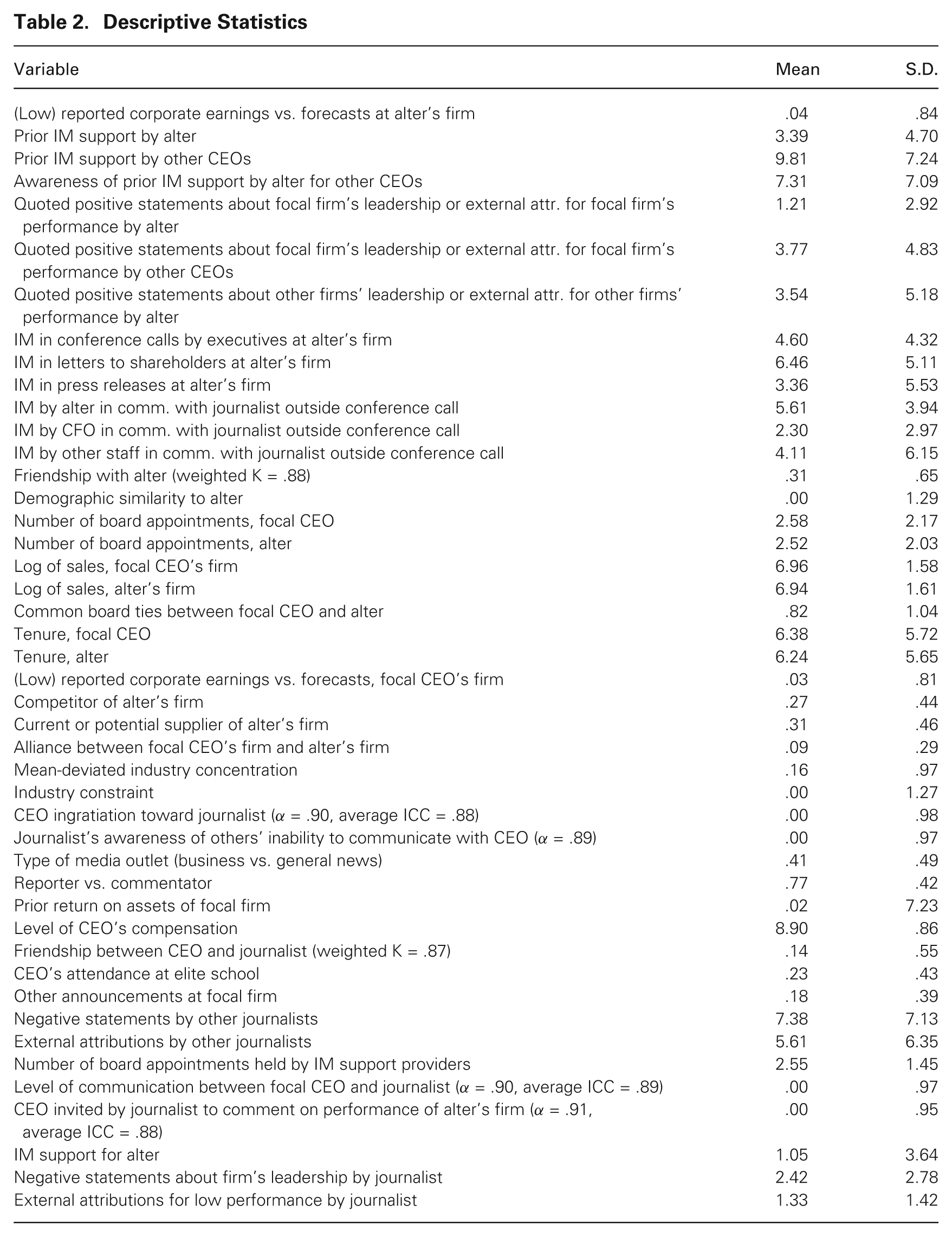

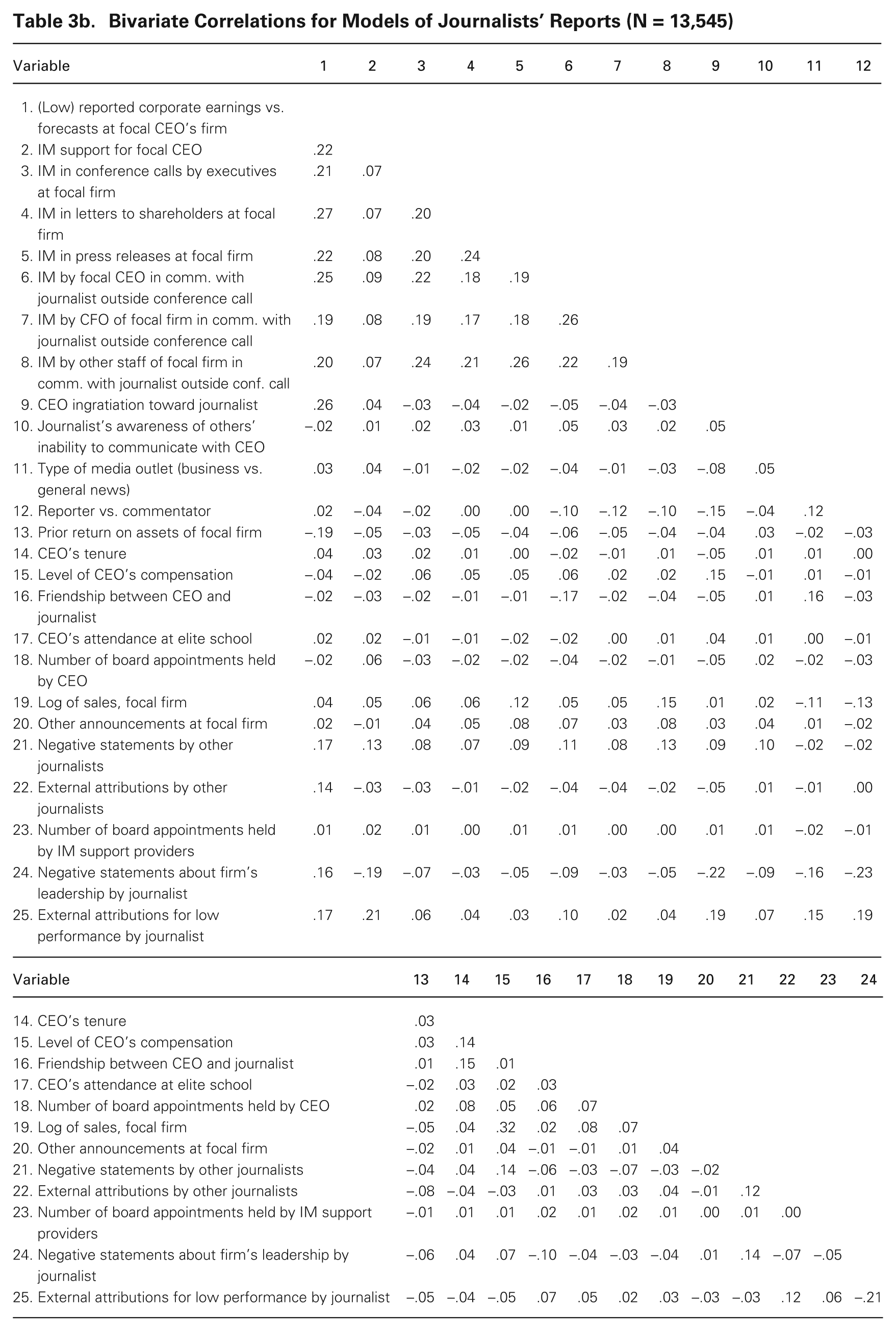

Descriptive statistics are provided in table 2, and tables 3a and 3b show bivariate correlations. The descriptive statistics indicate that IM support is not a rare event among CEOs in the sample frame: on average, CEOs made positive statements about another firm’s leadership or external attributions for low performance of another firm approximately three times over a two-year period. Table 4 shows negative binomial regression models of IM support. Models 1 and 2 include survey measures of prior IM support to test H1–H3. The results of model 2 support H1: there is a positive interaction between low earnings vs. consensus forecasts (negative earnings surprise) at another CEO’s firm (alter’s firm) and the prior receipt of IM support from alter following a negative earnings surprise on the extent to which the focal CEO subsequently provides IM support to alter. The results of model 2 also support H2: there is a positive interaction between a negative earnings surprise at alter’s firm and the focal CEO’s prior receipt of IM support from other CEOs following a negative earnings surprise on the extent to which the focal CEO subsequently provides IM support to alter. Moreover, the results in model 2 support H3 as well: there is a positive interaction between a negative earnings surprise at alter’s firm and the focal CEO’s awareness of prior IM support by alter for other CEOs on the extent to which the focal CEO subsequently provides IM support to alter. The magnitude of these effects is notable. For example, an increase in the prior receipt of IM support from alter of one standard deviation (from the mean level) increases the likelihood by 163 percent that the focal CEO will provide IM support for alter during the two-week period following a negative earnings surprise at alter’s firm. An increase of one standard deviation in the prior receipt of IM support from other CEOs than alter increases the likelihood by 102 percent that the focal CEO will provide IM support for alter following a negative earnings surprise at alter’s firm. And an increase of one standard deviation in the prior provision of IM support by alter for other CEOs increases the chances by 87 percent that the focal CEO will provide IM support for alter after a negative earnings surprise at alter’s firm.

Descriptive Statistics

Bivariate Correlations for Models of Impression Management Support (N = 36,406)

Bivariate Correlations for Models of Journalists’ Reports (N = 13,545)

Random Effect Negative Binomial Regression of Impression Management Support (N = 36,406)*

p < .05; •• p < .01; ••• p < .001; t-tests are one-tailed for hypothesized effects, two-tailed for control variables.

Standard errors are in parentheses.

We developed alternative indicators of IM support that gauge whether CEOs had previously been quoted by journalists as making positive statements about another firm’s leadership or external attributions for another firm’s low performance. These variables are included in models 3 and 4, and they corroborate the results in model 2. The interaction effects in model 4 show that a focal CEO is more likely to provide IM support to another CEO (alter) following low reported earnings at alter’s firm to the extent that (1) alter was previously quoted in the press as making positive statements about the focal CEO’s leadership or external attributions for the focal firm’s low performance (consistent with H1), (2) other CEOs than alter were previously quoted as making positive statements about the focal CEO’s leadership or external attributions for the focal firm’s low performance (consistent with H2), and (3) alter was previously quoted as making positive statements about other firms’ leadership or external attributions for other firms’ low performance (consistent with H3). In separate analyses, we estimated effects of the independent variables on the provision of IM support for the reduced sample of dyads in which alter’s firm experienced a negative earnings surprise, using Heckman selection models (i.e., the selection equation estimates the likelihood of a negative earnings surprise at alter’s firm using probit regression, and parameter estimates from that equation are included in second-stage negative binomial models estimating IM support by the focal CEO). As shown in models 5 and 6, the hypotheses are strongly supported in these models as well.

The results of Poisson regression models are provided in table 5, and they support H4. As shown in model 2, there is a significant interaction between negative earnings surprises and IM support on subsequent journalist reports, such that the effect of negative earnings surprises on subsequent negative statements about a focal firm’s leadership by a journalist is significantly reduced to the extent that CEOs provide IM support for the focal firm’s CEO that involves making positive statements about the leadership of the CEO’s firm and external attributions for the firm’s low performance in communicating with the journalist. Heckman models provide similar results: as shown in model 4, among firms that announce a negative earnings surprise, IM support directed at a journalist by other firms’ CEOs reduces the journalist’s subsequent propensity to make negative statements about the focal firm’s leadership, controlling for unmeasured differences between firms that issue a negative earnings surprise and other firms in the sample frame. Models 5–6 estimate journalists’ external attributions for low performance of a focal firm. The results in model 6 indicate that among firms that announce a negative earnings surprise, IM support directed at a journalist by other firms’ CEOs increases the journalist’s propensity to make external attributions for low firm performance, again controlling for differences between firms that issue a negative earnings surprise and others in the sample frame. Moreover, the effects of impression management by top executives and staff about their own firms are consistently weaker than the effects of IM support in the complete models. Among the six variables that indicate various forms of IM by leaders and staff about their own firms, only IM by the focal CEO in communication with a journalist outside conference calls has a significant effect on journalists’ reports when IM support is included in the models. Wald tests also indicated that the effect of IM by the focal CEO was significantly weaker than the effect of IM support in each of the models (p < .001). The magnitude of the effects of IM support is also relatively strong. For example, among firms that announce a negative earnings surprise, an increase in IM support from the mean level that involves two more positive statements about the focal firm’s leadership and two more external attributions for the focal firm’s low performance by other firms’ CEOs reduces the number of negative statements by a journalist about the focal firm’s leadership by approximately 74 percent. An equivalent increase in IM by the focal firm’s CEO reduces the number of negative statements made by a journalist about the focal firm’s leadership by approximately 23 percent.

Poisson Regression of Journalists’ Reports (N = 13,545)*

p < .05; ••p < .01; •••p < .001.

Standard errors are in parentheses.

A comparison of models 3 and 5 with models that include IM support indicates that the effects of IM by the focal CEO on journalists’ coverage are significantly stronger when IM support is excluded from the model. Moreover, of the other five variables that indicate IM by personnel of the focal firm, three are significant when IM support is excluded from the model, and all become non-significant when IM support is added to the model. To further compare the effect of IM support with the effects of IM by top executives and staff of the focal firm, we conducted a second-order factor analysis of the IM measures. This analysis showed that the six first-order factors that represent different forms of IM by executives and staff of the focal firm load onto a single, second-order or “meta” factor that represents IM about the focal firm. In other models, this second-order factor was significantly related to the negativity of subsequent journalists’ coverage when IM support was excluded from the models and became non-significant when IM support was included. Taken together, these results indicate that the effects of IM by leaders and staff about their own firms on journalists’ reports are partially confounded by the effect of IM support provided by other CEOs.

A premise of our theory is that CEOs can become aware of IM support that they have received from other CEOs. This premise was supported by qualitative evidence from our interviews and large-sample evidence from our surveys. For example, 94 percent of top managers who responded to our initial survey agreed or strongly agreed that “when a CEO makes positive statements to a journalist about another CEO in the same industry, other CEOs in the industry will tend to find out.” Responses to other survey items revealed that CEOs were typically aware of particular instances of IM support that had been reported in prior surveys. In the interviews, we asked top managers to indicate how they and other leaders normally learn about positive statements made by CEOs about other corporate leaders. Based on their responses, we developed a series of survey questions that asked CEOs to indicate how they became aware of a specific instance of support by another leader (the most recent instance reported). Responses indicated four channels through which CEOs most often learn about IM support: 43 percent heard about the particular instance of support from the journalist with whom the source CEO communicated, 26 percent learned about it from reading an article in which the source CEO was quoted or referenced, 19 percent heard about the support directly from the CEO who provided it, 28 percent heard about the support from another manager or director, and 8 percent heard about the support from another source (the total exceeds 100 percent because CEOs may learn about IM support from multiple sources). As one CEO whom we interviewed remarked, “If another CEO has said nice things about you, you’ll usually find out about it, either from the CEO, the journalist, or another manager. Given the amount of gossip that goes on, other managers find out about it as well.” Another CEO noted, “Naturally CEOs want to know what other CEOs are saying about them to the press and others. Journalists know this, other managers know it obviously. So they often tell them. And sometimes [the CEO] is quoted in the article, so you find out that way too” (see the Appendix for further details).

As discussed in the Appendix, we examined whether CEOs’ external attributions for low performance of another CEO’s (alter’s) firm in conversations with journalists reflect their actual beliefs about the extent to which low firm performance is attributable to alter’s leadership or strategy. The surveys included multiple items that gauged the extent to which a potential support provider attributes low performance of alter’s firm to external vs. internal causes and evaluates alter’s strategy and leadership positively (see Appendix). Separate analyses indicated that each of these survey measures (whether measured for a focal CEO who is a potential support provider or averaged across all potential support providers) did not significantly predict the extent to which the focal CEO provided IM support to alter and did not interact with low reported earnings at alter’s firm to predict IM support. The hypothesized results also remained unchanged when these measures were included as controls in any of the models (i.e., models estimating IM support and the various models of journalists’ reports). These results suggest that IM support that involves external attributions for low performance at alter’s firm and positive statements about alter’s leadership and strategy does not merely reflect a focal CEO’s beliefs about alter’s actual responsibility for performance outcomes. Moreover, the hypothesized relationship between IM support for alter and journalists’ reports is not confounded by a prevailing belief or recognition among CEOs (potential support providers) that alter’s leadership or strategy is not actually to blame for low performance at alter’s firm. Our survey data also indicate that when CEOs make positive statements about another CEO’s leadership to a journalist or make external attributions for another firm’s low performance in communicating with a journalist, they typically intend to influence constituents’ impressions about the CEO. Our survey measures of IM support include multiple items that gauge the extent to which CEOs intended to manage impressions of constituents about another CEO in making external performance attributions and positive statements about the CEO’s leadership to journalists. These items loaded on the same factor as items that did not gauge intent, suggesting that the behaviors that we examine typically represent deliberate acts of impression management.

Our social exchange perspective suggests that the prior receipt of IM support should increase a CEO’s perceived social obligation to provide similar help to another CEO when given the opportunity. In the Appendix, we report the results of supplemental analyses indicating that a reliable measure of CEOs’ perceived obligation to provide IM support to another CEO mediated the effects of our independent variables on CEOs’ subsequent provision of support. As discussed further in the Appendix, our control variables and supplemental analyses also help rule out the possibility that social cohesion in the corporate elite provides an alternative explanation for our findings. Further analyses indicated that the hypothesized effects of IM support on journalists’ coverage were not contingent on whether (1) support was provided in one-on-one conversations with journalists rather than conference calls or other group conversations that included other managers, staff, or journalists, or (2) the topic of other firms’ leadership and performance was raised by the CEO or journalist. We also included controls and estimated separate models to address the possibility that the apparent effects of our independent variables on IM support are influenced by variation in the extent to which CEOs are given the opportunity by journalists to comment on other firms’ performance. As discussed in the measures section, the results were also robust to using survey data from different respondents to measure IM support (potential support providers, potential support receivers, or journalists) and to using different time windows to measure IM support and the negativity of journalists’ reports.

It might be suggested that IM support by CEOs can be self-serving. In making external attributions for the low performance of a competitor, for example, CEOs might indirectly influence attributions about the performance of their own firms. On one level, our theoretical argument does not presume that IM support is entirely selfless behavior. Our theory presumes only that norms of direct and generalized reciprocity can influence CEOs’ propensity to provide IM support and that IM support will appear less obviously self-serving to journalists than impression management by CEOs about their own firms. The first premise is supported by the hypothesized effects of received IM support on the propensity for CEOs to provide support for other leaders, as well as supplemental survey evidence that these effects are mediated by CEOs’ perceived obligation to make positive statements about another CEO’s leadership. In addition, there is survey evidence that journalists generally view IM support as less self-serving than impression management by CEOs about their own firms. In the final year of the study, after responding to questions that gauge IM support, journalists were asked to what extent they viewed such behavior as self-serving. Ninety-two percent of respondents indicated that they viewed such behavior as “only slightly self-serving” or “not at all self-serving.” By contrast, after responding to questions that gauge impression management by CEOs or staff about their own firms, 83 percent indicated that they viewed such behavior as “somewhat self-serving” or “extremely self-serving.” In the Appendix, we also provide survey evidence that journalists tend to perceive external performance attributions and positive statements about the leadership and strategy of other firms as more credible than comparable statements by CEOs or staff about their own firms and that they tend to perceive less need to gather additional information from other sources to corroborate positive statements about other firms than positive statements about CEOs’ own firms. Further analyses indicated that the provision of IM support by a focal CEO was not significantly associated with the negativity of subsequent journalists’ reports about the CEO’s firm or various indicators of subsequent performance at the focal firm or alter’s firm.

Discussion

Overall the results provided strong support for our theoretical framework. The first set of results suggested that IM support can reflect three distinct forms of reciprocity among corporate leaders, and a second set of results showed that IM support by CEOs in their communications with journalists strongly affected the favorability of journalists’ coverage following a negative earnings surprise. In particular, such support reduced journalists’ propensity to make negative statements about a firm’s leadership and increased their propensity to make external attributions for low firm performance, and the effects of IM support were significantly stronger than the effects of impression management by CEOs about their own firms.

These findings contribute to the literatures on organizational impression management and social influence. While a growing body of research has yielded important insights into how corporate leaders manage the impressions of a firm’s constituents in the wake of image-threatening events such as low firm performance, this literature has not addressed a significant limitation to the efficacy of impression management that is suggested by the larger literatures on social influence and persuasion. Specifically, social psychologists have acknowledged that the influence target often perceives impression management tactics to be relatively self-serving, which limits their credibility and persuasiveness. In the present study, we contribute to the literature on organizational impression management and the larger organizational literature on social influence by identifying and examining a form of impression management that is likely to be perceived as less self-serving than impression management by CEOs about the leadership, strategy, and performance of their own firms, and which may therefore be especially credible and persuasive to a firm’s constituents, including journalists. Although studies on organizational impression management have typically examined efforts by leaders or their spokespersons to manage impressions about their own firms’ leadership, strategy or performance, a few studies have examined efforts by leaders to manage impressions about their industry or a larger collective of firms of which they are a member (Useem, 1979; Elsbach, 1994; Domhoff, 2002). Although these studies have made important contributions to our understanding of impression management, they still examined forms of impression management that constituents are likely to perceive as relatively self-serving. For example, impression management by leaders about controversial practices in their industry is likely to be perceived as self-serving to the extent that the focal leader’s firm is a member of the industry and engaged in those practices. Similarly, comments that promote and defend the practices of “big business” at large (Useem, 1982, 1984: 87–91) are likely to be perceived as lacking in credibility when they are made by CEOs of big companies engaged in those practices. In this study, we examined impression management by corporate leaders about the leadership of particular other firms, rather than the industry at large, which includes the focal firm, or the corporate elite, which includes the focal leader. Though leaders could benefit indirectly in some cases from engaging in such behavior, our theory suggests why journalists are likely to perceive IM support as relatively less self-serving than impression management that directly implicates the spokesperson’s firm.

The findings supported our theoretical expectation that IM support is likely to be more persuasive to journalists than impression management by CEOs about their own firms, and further results indicated that IM support may also be more effective in influencing journalists’ coverage than impression management by other managers and staff in conference calls, annual reports, and press releases. Thus aside from examining a form of impression management that has received little if any systematic research attention in the literature, a primary contribution of our study is to develop theory regarding why this form of impression management is likely to be more persuasive to constituents than forms of impression management that have been the focus of prior studies and may therefore have a more positive influence on constituents’ opinions about firms and their leaders.

Moreover, results indicated that the apparent effects of impression management by leaders and staff about their own firms following a negative earnings surprise may be partially attributable to the effects of IM support. When IM support was added to models of journalists’ coverage, the effects of other forms of impression management became significantly weaker. Future research should examine whether the effects of impression management on the perceptions and behavior of other firm constituents, such as security analysts and institutional investors, may also be partly attributable to IM support rather than impression management by top managers and staff about their own firms.

In addition, our theoretical framework and supportive findings contribute to the social influence literature by identifying a novel category of determinants of impression management behavior. The extant literature has focused primarily on organization-level factors such as low firm performance and individual-level factors such as personality as determinants of impression management. Little theory or research has considered how social exchange processes, whether dyadic or generalized, could influence impression management behavior by corporate leaders or other organizational actors. Moreover, in suggesting how norms of reciprocity can motivate CEOs to manage impressions about other corporate leaders, our study advances a broader conception of impression management as a kind of social support or helping behavior.

In revealing how IM support can reflect multiple forms of generalized reciprocity, our theory can help explain the prevalence of IM support in the corporate elite. Our theoretical framework specified two social mechanisms by which IM support can diffuse more broadly in the population—chain-generalized reciprocity and fairness-based selective giving—and our analysis provided empirical evidence indicating that both mechanisms of exchange contribute to IM support by CEOs. With both forms of reciprocity occurring, a single instance of IM support can prompt multiple instances of support in subsequent time periods. For example, if CEO A provides support for CEO B, CEO B is subsequently more likely to provide support for another CEO C who needs help (i.e., chain-generalized reciprocity), and another CEO D is subsequently more likely to provide support for CEO A, when A needs help (i.e., fairness-based selective giving). As a result, through the combined effects of these social mechanisms, IM support is unlikely to remain rare in the population of corporate leaders.

In demonstrating that IM support can have a relatively strong effect on the tenor of journalists’ reporting about firms’ leadership, our study reveals an important social influence on firms’ and leaders’ reputations. There is growing evidence that journalists’ reports have a significant impact on organizational reputation and legitimacy among a broad array of stakeholders, including various members of the financial community, customers, public policy makers, and the general public (Deephouse, 2000; Pollock and Rindova, 2003; Fiss and Hirsch, 2005; Johnson et al., 2005; Wiesenfeld, Wuthmann, and Hambrick, 2008). Media reports are also an important input to the social process by which leaders’ images are constructed. Positive coverage can enhance CEOs’ celebrity status, increasing their earning power and expanding their career opportunities, whereas negative coverage can diminish their earning power, damage their career prospects, and limit their internal power and authority (Hayward, Rindova, and Pollock, 2004; Wade et al., 2006; Graffin et al., 2008; Wiesenfeld, Wuthmann, and Hambrick, 2008). There is also growing recognition that media coverage can serve an important role in corporate control. Recent studies suggest that negative press coverage can exert pressure on firms to adopt corporate governance reforms or dismiss CEOs in response to low firm performance (Dyck and Zingales, 2002; Miller, 2006; Joe, Louis, and Robinson, 2009; Bednar, 2012). Thus, in showing that IM support can have a relatively strong effect on the negativity of journalists’ coverage in the face of negative information about a firm’s performance, this study reveals an important mechanism of social influence on firms’ and leaders’ reputation, with potentially important consequences for firms, leaders, and corporate stakeholders.