Abstract

In examining how framing influences an audience’s appreciation of products, practices, and people, including the framer, we take the perspective of the audience that evaluates the framing. We examine the effects of framing on evaluations when audiences are exposed to a multiplicity of frames, both by the same actor as the result of recurrent communications over time and by multiple actors who vie for attention. Using 36,012 research reports by securities analysts, covering the biotechnology and pharmaceutical industry between 1989 and 2012, we tested the relationships between analysts’ framing repertoires and professional investors’ evaluations of analysts as measured in the publication of Institutional Investor’s short list of the best analysts of the year. We found that investors appreciate analysts with framing repertoires that resonate with their needs, that are internally coherent over time, and that offer a moderate amount of novelty in comparison to others’ framings. We also found that framing is particularly important for analysts without existing high status, that is, who have never before been recognized as stars or who cannot benefit from association with a prestigious employer.

Framing, defined as a “mental bracket” that delimits attention to a portion of reality (Zerubavel, 1991), is an essential tool that actors use to garner the appreciation of others for a variety of products, practices, and people (Hoffman and Jennings, 2011), including their own selves (Goffman, 1959). For example, by framing grass-fed beef as natural, sustainable, and authentic, activists recast this previously disparaged product as superior and led consumers to see it as a distinct market category worth a price premium (Weber, Heinze, and DeSoucey, 2008). Similarly, by casting hostile takeovers in “more accepting and benign terms” (Hirsch, 1986: 814), the media granted legitimacy to this traditionally deviant practice. And by presenting themselves as “gospel women,” Catholic nuns in the U.S. shaped the Vatican’s understanding of their centrality within the church (Giorgi, Guider, and Bartunek, 2014). Taken together, these studies demonstrate that framing can positively shape audiences’ evaluations.

Despite offering extensive evidence of the consequentiality of framing, current research has given limited attention to the context in which an audience “consumes” and evaluates framing. Rather than being exposed to and appraising one frame at a time, audiences are often immersed in rich discursive contexts characterized by a multiplicity of frames. More specifically, an audience can be exposed to multiple framing efforts by the same actor, as the result of recurrent communication episodes over time (Weber, 2005; Loewenstein, Ocasio, and Jones, 2012), and to framings of multiple other actors who also vie for the audience’s attention and appreciation (Van de Rijt et al., 2013). This is the case, for instance, for professional investors who read hundreds of analysts’ reports over the course of a year, public relations professionals who scan multiple media outlets to evaluate a corporate image, or political analysts who routinely access multiple news commentaries to inform their opinions. In these common situations, audiences evaluate framing not in a vacuum but as part of a broader discursive context in which the framing is embedded (e.g., Fine and White, 2002).

In such circumstances, audiences can evaluate framing in two ways: cumulatively, basing their evaluations on a “repertoire” or portfolio of frames that an actor deploys over time (Swidler, 1986, 2001; Janssen, 1997; Allen and Parsons, 2006; Tilly, 2010), rather than on an individual frame (Lawrence, Winn, and Jennings, 2001), and comparatively, evaluating the framing relative to other actors’ framings (Lamont, 1987, 2012). Examining the effectiveness of framing in such contexts is important because mounting evidence shows that audiences’ evaluations change, or even reverse, when an object is evaluated in relation to other objects rather than in isolation (Bowers, 2014). The question is how framing influences audience appreciation in contexts in which audiences are exposed to multiple framings. By the term “appreciation” we refer to the conferral of value to an object or person (Lamont, 2012) that translates into prestige or esteem (Allen and Parsons, 2006). Such appreciation can result, for example, in top placement in rankings, induction into a hall of fame, or bestowal of honors, awards, and prizes that serve to consecrate individuals and objects (English, 2005; Espeland and Sauder, 2007) and symbolically set them apart as “exemplars of excellence” in a given field (Allen and Parsons, 2006: 808).

Work on social valuation processes (see Lamont, 2012; Zuckerman, 2012, for recent reviews), which examines how audiences confer value to people or objects, brings attention to the context in which an audience consumes and appreciates people, such as presidents, writers, scientists, or athletes (English, 2005), or objects, such as movies (Baumann, 2007), novels (Griswold, 1987), or music (Santoro, 2010). For example, the consecration of Jacques Derrida as a dominant intellectual in France hinged on the availability of other scholars “with whom he shared a market” (Lamont, 1987: 584) and in relation to whom Derrida’s work was evaluated as a novel way to make sense of 1960s politics. This example suggests that audiences do not evaluate an object or person per se but, rather, in reference to the many other objects or people that they are exposed to.

Research on social evaluation, along with research on framing, provides grounding for a theory about how audiences come to appreciate framings in rich discursive contexts. First, framing repertoires should be effective at garnering positive evaluations when they display resonance with the needs, expectations, or interests of the target audience. Second, consistency in an actor’s framing repertoire—a degree of predictability in framings over time (intra-individual)—makes it easier for the audience to identify a particular framer, leading to greater appreciation (Rao, Monin, and Durand, 2003; Zuckerman, 2012). Third, using some novelty in framing repertoires—presenting content in a new but still familiar way compared with others’ framings—can attract and retain audiences’ attention, making an actor positively stand out in relation to others (Barthes, 1983; Schudson, 1989; Martens, Jennings, and Jennings, 2007). Fourth, status is likely to be a moderator of the impact of framing on audience appreciation. Differences in social status among framers—differences in esteem that each actor can claim because of his or her position (Graffin et al., 2013)—influence evaluations of an object or person, providing an advantage to higher-status objects or individuals independently of other factors (Washington and Zajac, 2005; Lamont, 2012). Combined, these arguments suggest that in rich discursive contexts, audiences will evaluate framing with reference to their own needs (resonance), the frames deployed by the same actor in previous communications (consistency), the frames used by other actors (moderate novelty), and information about the framer’s standing compared with others (status).

We chose to study the empirical context of securities analysts, whose job consists of researching a particular industry and periodically communicating their analyses and recommendations in written reports to an audience of professional investors, such as managers of mutual or pension funds. In this context, investors are bombarded with information and scan multiple analysts’ reports to inform their opinions and make investment decisions. At the end of every year, the most prestigious industry magazine, Institutional Investor, invites investors to pick the best analysts per industry: first, second, and third place, and runner-up. Inclusion in this short list turns analysts into “stars” (Beunza and Stark, 2004; Groysberg, Lee, and Nanda, 2008), providing them not only with substantial financial rewards but also with visibility and prestige.

Framing and Audience Appreciation

Given people’s inability to access reality in its completeness (Husserl, 1931; Schutz, 1967; Eco, 1979), frames act as mental brackets, lenses, or picture frames (Goffman, 1974) that create order out of chaos (Zerubavel, 1991). Framing often focuses on a few dimensions that structure communication with an audience and simplify sensemaking efforts and evaluations of an object or person. For example, social movements that aim at persuading their target audience of the urgency and appropriateness of change do so through choices of frames that identify a problem, a solution to such problem, and a motivation for taking action (Benford and Snow, 2000). Similarly, entrepreneurs who need to raise funds for their new ventures make their plea by identifying a subject, an object or goal that the subject is in search of, and a set of forces that enable or impede the subject from attaining the desired object or goal (Fiol, 1989; Czarniawska, 2004). And by framing a dish through the choice of ingredients, method of preparation, and modality of display, chefs communicate their taste and orientation to critics and consumers (Rao, Monin, and Durand, 2003).

As the examples above suggest, framing not only facilitates communication but also colors audiences’ interpretations, hence shaping their appreciation of products, practices, and people (Cerulo, 2001; Hoffman and Jennings, 2011). Research shows that framing can persuade others of the appropriateness of a strategic direction or worldview (Hallett and Ventresca, 2006; Powell and Colyvas, 2008), elicit desired reactions to an event by casting it as an opportunity or a threat (Staw, Sandelands, and Dutton, 1981), foster participation in a project (Small, 2002), or influence evaluations of the legitimacy of a market (Anteby, 2010). Frames not only define what is in and out of the frame, hence limiting our perception of the world, but they also provide a particular object or person with a positive or negative valence, hence shaping our preferences and appreciation (Hallahan, 1999).

Given the consequentiality of framing for audiences’ appreciation, a critical question in this line of work is why some frames succeed at influencing audiences’ evaluations and others do not (Babb, 1996). Research has concluded that framing is effective when it resonates with the beliefs, values, and ideas of its target audience (Goffman, 1951; McAdam, 1986; Benford and Snow, 2000). For example, the leader of the Bill of Rights movement successfully brought together a broad coalition of over one million individuals by appealing to their shared value of privacy protection (Vasi and Strang, 2009). Only by showing alignment with one’s audience can framing elicit the desired reactions and behaviors (King, 2008). Still, while empirically compelling, this research overlooks the more complex context in which audiences “consume” framing and develop an appreciation for a particular person or object.

In the literature on framing, the term “context” is used to refer to the stories, myths, and folktales that characterize a particular historical situation (Benford and Snow, 2000); the key argument is that frames grounded in these stories, myths, and folktales exhibit greater potency at molding others’ evaluations (Gamson et al., 1992). For example, Zilber (2006) showed how the use of existing cultural myths to explain and justify the high-tech industry’s economic bubbles in Israel strongly resonated with the local audience. Yet this literature glosses over the more immediate situational conditions under which audiences interpret and evaluate framing.

In many social situations, audience members evaluate framings while immersed in a discursive context characterized by a multiplicity of frames: multiple framings by the same actor over time—for example, a journalist’s series of articles or a financial analyst’s set of reports—and by multiple other actors—other journalists or financial analysts who also vie for the audience’s attention and appreciation. This is a common situation in professional settings in which experts periodically offer commentary, news, or advice to their target audience of investors, consumers, or suppliers. In these recurrent situations, actors still engage in framing to project a positive image of their own selves or of their work (Goffman, 1955, 1959, 1963; Elsbach, 2003), while competing with others for audience attention.

In such rich discursive contexts, audiences evaluate frames not in isolation but in reference to other frames that are available in that context. For example, political analysts consume news articles and commentaries in light of what the author has written before and also in light of what other journalists are writing about (Fine and White, 2002). In contexts characterized by a multiplicity of framings, audience members are likely to evaluate framing in two ways: cumulatively, basing their evaluations on a repertoire or portfolio of framings that an actor has accumulated over time (intra-individual), and comparatively, relative to other actors’ framings (inter-individual).

Research suggests that in recurrent communications, audiences’ evaluations are based on a repertoire or portfolio of contributions (Swidler, 1986, 2001; Tilly, 2010). In their study of professional baseball players’ induction into the Hall of Fame, Allen and Parsons (2006) found that the conferral of such prestige hinges on cumulative recognition of players’ achievements. Similarly, reviewers’ assessments of the writings of fiction authors are often constrained by evaluations of their previous works (Janssen, 1997). And research shows that art objects, literary works, or scientific theories cumulatively gain traction to the point at which they are consecrated and integrated into the canon (Lamont, 1987, 2012). Applied to the evaluation of framings, this suggests that when an actor deploys multiple frames over time, audiences evaluate said actor on the basis of an accumulation of frames, rather than a single frame.

Further, when a context is characterized by multiple offerings, audiences assess the value of an object or a person “in a relational (or indexical) process involving distinguishing and comparing entities” (Lamont, 2012: 205). Research on fashion in given names (Lieberson, 2000) provides evidence for this mechanism of comparative evaluation: parents evaluate a name in relation to its available alternatives and to its popularity, choosing a highly or less popular name depending on their need to conform or distinguish themselves from others. Examples of comparative evaluations abound in other settings as well: an intellectual’s novelty is assessed in relation to other theorists’ work (Lamont, 1987), the gravity of a politician’s scandal is evaluated in light of others’ scandals (Graffin et al., 2013), and the quality of law schools is gauged in comparison to available others (Espeland and Sauder, 2007). Work in social psychology confirms that audiences make sense of and give value to an object or person through comparison (Ashmore, Deaux, and McLaughlin-Volpe, 2004). One context in which comparative evaluations are especially salient is the market for investment advice.

The Market for Investment Advice

The market for investment advice represents a unique setting for examining how framings can shape an audience’s appreciation in contexts characterized by a multiplicity of frames. This is the case for four reasons. First, in this professional setting there is a clear-cut distinction between the actors who engage in framing (securities analysts) and their target audience (institutional investors). Second, analysts periodically communicate the results of their work to institutional investors through written reports, which allows us to systematically analyze the frames used in communicating with the audience over time and across analysts. Analysts often use highly visible parts of the report, such as an executive summary or boxes or different fonts, to frame the content by highlighting certain aspects while glossing over others. Third, the audience’s appreciation is formally measured. Every year the audience of institutional investors expresses its appreciation for the top analysts by sector through a comprehensive survey, and such appreciation results in the Institutional Investor (II)’s “best analysts of the year” ranking (also referred to as “All-America” analyst ranking). The designation does not rank all analysts but identifies only the first, second, third, and runner-up analysts in a given industry, hence ranking between four and six analysts per year (depending on potential tied rankings among analysts) as above the rest. Finally, another advantage of this empirical context is that the Wall Street Journal (WSJ) mathematically computes analysts’ best technical performance—their ability to give profitable investment advice in terms of buy, sell, or hold stock recommendations to investors—and publishes the results in an alternative ranking, allowing us to distinguish overall audience appreciation (as measured in the II ranking of All-America analysts that results from a survey) from technical performance.

Our further characterization of the industry context is based on primary and secondary qualitative data collected in a pre-study of the empirical setting. We initially conducted 26 in-depth, semi-structured interviews with 14 analysts and 12 investors between 2004 and 2013. Thirteen analysts worked for major investment banks, and one for a smaller research firm; ten investors worked for mutual funds, one for a hedge fund, and one was the founder of a wealth management company. We complemented the interviews with over 200 newspaper and trade press articles, six business school cases, 50 securities analysts’ reports, and several academic articles about the industry. These data span nearly 30 years, from the early 1980s through mid-2013. Archival data gave us the ability to access real-time accounts of analysts and investors over a longer time period to cross-validate the recent, and often retrospective, accounts provided in the interviews.

Investment banks or independent research firms employ securities analysts to gather, interpret, and disseminate knowledge about a particular industry. Analysts communicate the results of their work through the recurrent publication of reports, which offer investment advice (in terms of buy, sell, or hold recommendations) and analyses of firm and industry prospects. The main audience for analysts’ advice consists of institutional investors, such as chief investment officers and portfolio managers of money management firms, mutual funds, hedge funds, and pension funds (Groysberg, Lee, and Nanda, 2008), who make the buy or sell decisions. Although analysts also make phone calls and organize small conferences, they mainly use reports to communicate with investors given that it is not unusual for an analyst to serve more than 800 institutional clients on an ongoing basis (Groysberg, Lee, and Nanda, 2008).

Investors, for their part, may receive up to a thousand emails per day (investor interview). Because they routinely use reports produced by different analysts to inform their investment decisions (Brenner, 1991), investors do not have the time to read carefully. Rather, they quickly scan reports “like you would do with a newspaper” (senior investor interview) by looking at a few highly visible elements, such as the executive summary on the first page, text highlighted in bold, headings, bulleted lists, or boxes. The information contained in these elements “frames” a report’s often-heterogeneous content, which even in short reports includes discussions of other aspects of the company, its products and markets, as well as tables, financials, and figures. The information conveyed in these easily accessible elements frames investors’ reading of subsequent content by selectively priming their attention and by offering cues to what the report is about, its motivation, and main takeaways.

Investors’ evaluation of analysts is highly formalized. Every October since 1972, the industry’s premier magazine, Institutional Investor, conducts a survey and invites institutional investors to pick the “best analysts of the year” (first, second, and third place, and runner-up) by industry, without specifying any particular criterion of selection; it then creates an aggregate ranking using the average of the numeric scores each analyst receives, weighted by the asset size of the responding institution (Phillips and Zuckerman, 2001). For example, in 2001, 3,200 individuals representing over 400 institutions voted in this process (Dini, 2001).

Only the top four to six analysts per industry are designated members of the “All-America Research Team” each year, with no mention of any other analysts. The analysts ranked All-America enjoy rewards in terms of visibility (He, Mian, and Sankaraguruswamy, 2005), pay (Groysberg and Lee, 2009), and career opportunities (Hayward and Boeker, 1998). As one industry expert observed (Kover, 1997), “Even in the list-mad magazine world, there’s nothing else quite like it. Regulars who make the list invariably earn a lot more than those who don’t—$1 million is said to be the typical pay differential.”

The potential role for subjectivity and diverse criteria in investors’ evaluations is highlighted by the role of an alternative ranking conducted by the WSJ. Unlike the II list, this ranking, published annually in June, is based solely on the quality of an analyst’s stock-picking advice (Light and Tilsner, 1993). It calculates the hypothetical performance of a portfolio of stocks if an investor were to buy and sell stocks according to the analyst’s recommendations. The WSJ ranking, however, is often dismissed by industry insiders as a “math exercise that has little to do with equity research” (analyst interview). This lack of appreciation for the WSJ ranking might be attributed to two main reasons: first, analysts’ and investors’ conceptualization of the role of analysts as providers of advice rather than stock recommendations; and second, a generalized distrust in the analysts’ recommendations that the WSJ assesses because banks—analysts’ employers—aim at maintaining their relationships with companies as clients, making negative recommendations less acceptable and hence rare.

Many significant changes affected the context of investment advice during the time covered in this study. The regulatory reforms in 2000, with the Regulation Fair Disclosure, and in 2003, with the Global Research Analyst Settlement, aimed at increasing market transparency by separating research and investment banking (Cowen, Groysberg, and Healy, 2006). At the technological level, the advent of the Internet in the late 1990s was seen as the most significant threat to the financial analysis profession because it democratized access to firms’ information, such as earnings releases, product development, and acquisitions, and accelerated the speed of information dissemination. While scholars have shown that these changes had a negative impact, for example, on the number of sell-side analysts employed in the United States (Groysberg and Healy, 2013: 85), analysts’ fundamental activities and the role of their reports in investors’ work have remained substantially unchanged (Knorr-Cetina, 2011). A qualitative analysis of Institutional Investor’s collection of articles on investors’ tastes since the 1980s confirms the stability of evaluators’ tastes and needs. For example, investors’ preferences in the late 1980s for analysts who could “zero in on the important points” (Institutional Investor, 1989: 124) and “present science in a very simple language” (Institutional Investor, 1989: 110) recurred in every subsequent year (Institutional Investor, 1999: 116). An analysis of investors’ preferences across different types of investors in 2005 revealed that, independently of their size, investors rated industry knowledge as the single most important attribute of analysts’ reports, with clarity of communication consistently in the “top ten” attributes (Institutional Investor, 2005). This consistency in investors’ preferences—and the unchanged nature of analysts’ fundamental activities (Groysberg and Healy, 2013)—suggests a certain degree of resilience in the evaluative criteria of reports, despite significant changes in the broader setting that affected the speed and modality of production and consumption of investment advice.

The importance of clear and informative communication in investors’ criteria for evaluation indicates that framing will influence the audience’s appreciation of the framer. Two primary mechanisms are likely to influence an audience’s appreciation of the framer: resonance and distinctiveness. In the framing literature, resonance is a well-documented mechanism for frame effectiveness, and it broadly emphasizes the need to keep the audience’s understandings in mind when crafting a message (e.g., McAdam, 1996). The second mechanism is distinctiveness (Bourdieu, 1984; Rao, Monin, and Durand, 2003), which captures the competition among framers to gain the audience’s attention and be recognized as relatively unique. Building on insights that the social standing of the evaluatee influences evaluation processes (Allen and Parsons, 2006; Sauder, 2006; Lamont, 2012), we expect status to moderate the impact of framing resonance and distinctiveness on audience appreciation.

Resonance

An extensive literature on framing consistently shows that frames that resonate with their intended audiences—showing alignment with the target’s values, beliefs, and ideas (Vasi and Strang, 2009)—are effective in influencing others (Benford and Snow, 2000; Hardy, Palmer, and Phillips, 2000; Steyaert and Hjorth, 2008). The impression management literature, however, points out that despite the potentially considerable effort that goes into fulfilling an audience’s expectations in one’s self-presentation, such resonance may not be sufficient to gain the audience’s appreciation. For example, it can be perceived as a “façade of conformity” (Hewlin, 2003), a false representation that aims at ingratiation and self-promotion (Jones and Pittman, 1982). This is the case, for example, of the perfectly packaged political candidate whose resonance with a particular section of the electorate is seen as hypocritical, failing to inspire passion and support (Bolino, 1999).

While resonance at the ideological level can be rejected on the basis of a perceived lack of authenticity, in this setting resonance should garner positive evaluations because it pragmatically suggests the fulfillment of needs, expectations, and interests that arise from audience members’ tasks and goals. For example, in a similar setting characterized by a lack of ideological conflict, entrepreneurs’ stories can successfully gain investors’ support if they can pragmatically cue audiences to the viability and profitability of their new ventures (Lounsbury and Glynn, 2001). Similarly, Rao and Giorgi (2006) showed that by framing private prisons as a variable cost for the state, the proponents of privatization resonated with government officials’ pragmatic need to manage a burgeoning inmate population on limited state funds. Hence we hypothesize that investors will value framing repertoires that hint at the fulfillment of needs that result from their own task of making investment decisions:

Distinctiveness

The seemingly simple path to garnering positive audience evaluations is complicated by the multiplicity of frames that characterize the context in which audiences conduct their evaluations. Under conditions of competition with multiple others, even by hinting at investors’ needs, an analyst might fail to grab their attention and stand out (Elsbach and Sutton, 1992; Elsbach and Bhattacharya, 2001). To garner attention when there is competition, analysts need to develop distinctiveness (Porac, Thomas, and Baden Fuller, 1989; Deephouse, 1999)—a sense of differentiation from others (Vignoles, Chryssochoou, and Breakwell, 2000)—as an alternative path to audience appreciation. Two strategies for gaining distinctiveness include consistency, which is about maintaining focus in one’s framing choices over time (intra-individual), and moderate novelty, which is about framing choices that stand out in relation to other framers (inter-individual).

Consistency

One way to garner audience attention and appreciation is through a framing repertoire that consistently uses a small subset of framings, rather than a repertoire that evokes a wide variety of framing choices over different reports. For example, an analyst can consistently cater to investors’ needs for industry knowledge by choosing to frame his or her reports as industry comparisons and offering updates on scientific discoveries in the biotech sector, thereby creating a signature style of writing reports. It is important to note that framing choices—what the analyst chooses to emphasize as important about the report—do not necessarily reflect the whole content of a report, which can include, for example, data on a competitor. Such framing choices constitute cues and primes that attract investors’ attention and guide further reading.

A repertoire of framing choices that is consistent over time presents at least two potential advantages associated with distinctiveness. First, in this context investors rely on analysts’ reports mostly to gather diverse perspectives before making a decision, so they want analysts to make a case “for the bull and the bear” (Beunza and Garud, 2007: 18). They therefore may prefer to turn to several “specialists” who can reliably provide distinct perspectives, recognizing, for example, one analyst for his or her industry insights and another for his or her financial orientation. Second, research on social evaluation processes suggests that easy-to-identify actors enjoy greater audience appeal (Pontikes, 2012), for example, in the form of better stock market valuations (Zuckerman, 1999), increased sales (Hsu, Hannan, and Koçak, 2009), or higher rankings (Hsu, 2006). This is nothwithstanding alternative work showing that audiences positively evaluate a certain degree of novelty, or “optimal distinctiveness,” that is a reconciliation of opposing needs for assimilation and differentiation from others (Brewer, 1991), where “incessant experimentation and self-renewal” can also lead to audience appreciation over time (Alvarez et al., 2005: 864). We expect such countervailing processes for assimilation to be less important in the context of routine market exchange between finance professionals in which assimilation occurs by virtue of participating in a standard and institutionalized discourse and exchange. Therefore we hypothesize:

Moderate novelty

The importance of distinctiveness in contexts characterized by a multiplicity of frames builds on the insight that an audience’s capacity to engage with different frame producers is limited, so behaviors that enhance visibility are rewarded (Phillips and Zuckerman, 2001; Rindova, Pollock, and Hayward, 2006). Because evaluations are inherently comparative, an individual analyst’s framing repertoire is assessed in relation to others, so in the hypothetical scenario of all analysts employing framing repertoires of equal resonance with investors’ needs, no distinctions can emerge as long as investors pay attention to every analyst. But investors are continuously exposed to hundreds of reports, and one way for an analyst to gain distinctiveness is through novelty. The novelty of an individual analyst’s framing of a report refers to how different the evoked frames are from those predominant in recently published reports. Reports framed in more novel ways are more intriguing (Martens, Jennings, and Jennings, 2007), more easily remembered by investors, and thus more likely to be positively evaluated (Bourdieu, 1984; DiMaggio, 1997; Gartman, 2002).

We hence propose that novelty helps analysts garner audiences’ appreciation, but with a caveat. Consumer behavior research indicates that audiences positively evaluate reports that present some novel elements but are still easy to make sense of (moderate novelty) (Chernev, 2004; Simonson, 2008). Although the optimum amount of novelty is difficult to derive theoretically, and what is moderate can only be established empirically, we expect the relation between novelty and audience evaluations to be non-monotonic, with an optimum level at moderate degrees of novelty:

Status

Scholars of social evaluations observe that audiences take into account the status of the evaluated actor in how they process other information about the actor (Merton, 1968). Status is thus an important contextual factor in why some actors receive more recognition for their work than others (Allen and Parsons, 2006). Following recent research, we define status as “a socially constructed ranking of social actors based on the esteem that each actor claims by virtue of his or her position in a group characterized by distinction or worth” (Graffin et al., 2013: 315). Such status differences can be the result of processes of evaluations that occurred in the past—for example, the bestowal of an honor or an individual’s top placement in a ranking (individual status)—or from affiliation with high-status others, such as a prestigious employer or university (organizational status).

Our interest in status stems from the observation that actors do not deploy their framing efforts on an equal playing field: some actors are better positioned than others because of their higher status and enjoy benefits in terms of existing appreciation that make audience members predisposed to positively evaluate their current performances (Washington and Zajac, 2005; Graffin et al., 2013). Given the common belief that people of high status are also more competent and deserving of esteem (Merton, 1968), audiences may expect high-status actors to offer more desirable framings. This expectation may color investors’ perception of analysts’ actual framing efforts as more consistent and novel than they are and in addition offer a priori advantages of distinctiveness. Status then can be expected to moderate the role of framing practices in garnering audience appreciation if audiences pay closer attention to the framing practices of lower- than high-status actors.

Individual status

The “social magic” (Bourdieu, 1991: 117) that results from the recognition of excellence in one’s field tends to create a lasting difference between those who have been identified as the “best” at some point and those who never have. For example, Allen and Lincoln (2004) found that prior recognition of films contributed to their likelihood of further social appreciation. In the present setting, research shows that “star” analysts—those who have been included in the II All-America list in the past—enjoy lasting benefits of esteem and visibility, even if they do not necessarily produce the same performance or contribute to a firm’s competitive advantage (Clarke et al., 2007; Groysberg, Lee, and Nanda, 2008). We expect contemporary framing practices to play a less significant role in gaining audience appreciation for star analysts, who can rely on their status to impress investors:

Organizational status

Association with high-status others can affect audiences’ evaluations of one’s quality or competence (Stuart, Hoang, and Hybels, 1999). For example, research has shown that scientists associated with more prestigious universities are likely to enjoy greater esteem and recognition than other scientists with comparable achievements (Cole and Cole, 1973). Similarly, Allen and Parsons (2006) found that baseball players who are members of successful teams, especially those that appear in the World Series, can be expected to receive more recognition for their achievements than players who are members of less successful teams. Because analysts who work for prestigious banks similarly benefit from the endorsement of their high-status employers, they should be less dependent on particular framing practices to attract positive audience evaluations. Framing should be a more important pathway to recognition for analysts who cannot benefit from positive reputational spillovers of their prestigious employers:

Our hypothesis that skillful framing is less significant for garnering audience appreciation when analysts enjoy the benefits of high status is based on the literature on social evaluation. It should be noted, however, that impression management research suggests that this prediction is not universal and thus is in need of testing. The greater visibility and scrutiny associated with higher standing can also make framing more important for high-status actors, who face greater expectations to exemplify desired behavior and risk a “fall from grace” when they deviate from such expectations (Bansal and Clelland, 2004: 95; Graffin et al., 2013). This effect seems to be particularly pertinent in settings in which framing preferences are ideological (Graffin et al., 2013) or when status is not stable (Bothner, Kim, and Smith, 2012).

Methods

We tested our hypotheses using longitudinal data on 94 U.S. analysts covering the biotechnology and pharmaceutical industry between 1989 and 2012, for a total of 520 analyst-years. We obtained analyst reports from Investext Plus (part of Thompson), a widely used database of historical full-text investment analysis reports. We designed the panel to include sets of ranked and non-ranked analysts for each year. Every year, II designates between four and six analysts per industry as members of the All-America Research Team (first, second, and third place, and runner-up).

Some banks and individuals do not make historic reports available through Investext. As a result, our sample includes 32 of 62 unique analysts who were designated All-America in at least one year (many were included for several years). Because we sampled analysts (vs. analyst-years), we also included annual observations for the same analysts in years when they did not achieve the designation. We then constructed a comparison group of analysts who were never ranked All-America. To do so, we first established which companies all ranked analysts covered in a given year, separately for biotechnology and pharmaceuticals. This set of companies can be seen as the minimal “core” coverage for an analyst to be considered a biotechnology or pharmaceutical analyst. We then constructed a sampling frame that included all analysts who covered all of these core companies, and we selected 62 analysts at random from this pool. We used replacement when an analyst’s reports were missing in Investext and the number of non-ranked analysts for that year was less than the potential number of ranked analysts. We again used all years for which data were available for an analyst thus included. With the inclusion of the additional 62 analysts who were never ranked, the total sample amounts to 94 analysts and 520 analyst-year observations. The number of observations varies between 11 and 19 analysts per year and between 2 and 13 years per analyst. The included analysts produced a total of 36,012 reports.

This design produced an unbalanced panel data set that met two objectives: to maximize use of the small number of ranked analysts and to ensure a comparison group of non-ranked analysts for each year. Because part of this comparison group includes analysts who were never ranked, and others who were ranked before or after the present year, our analyses estimate average within- and between-analyst effects.

Realistically, however, investors are unlikely to consider the full set of analysts covering a core set of companies in their evaluations and can be influenced only by the framing practices of analysts whose reports they are exposed to. Exposure to investors’ evaluations in the survey can be conceptualized as akin to exposure to a treatment in counterfactual-based models of causal inference (Hirano and Imbens, 2001; Morgan and Harding, 2006), regardless of whether one is interested in formal causality or simply improved correlational estimates (Morgan and Winship, 2007: 87). The comparability of the control group of non-ranked analysts can be enhanced either by stratifying the sample and selecting only analysts from strata that are very similar to ranked analysts on observable characteristics or via a number of statistical corrections based on observables, namely regression adjustments, matching, and reweighting. We employed a statistical correction, a propensity score reweighting approach in which we rebalanced the control sample to give greater weight to comparison cases that bear closer resemblance to the group of ranked analysts on a set of observable characteristics and lesser weight to those that are more distant on those characteristics (Morgan and Harding, 2006). Weighting is a preferable approach to matching in modest-size samples with sparse data in some strata, making it more applicable to our data set. The reweighting procedure is described in detail below.

Measuring framings

Existing research shows that frames are often articulated along a few stylized dimensions (Martens, Jennings, and Jennings, 2007), such as subject, goal, and helpers (Fiol, 1989; Czarniawska, 2004), or problem, solution, and motivation (Benford and Snow, 2000), to make content intelligible and predictable for an audience. Because research has not yet established a standard set of framing dimensions for analyst reports, we identified such dimensions inductively and developed a coding scheme. Investors assess their interest in a particular report by scanning highly visible elements, such as an executive summary or heading structure, so we focused on the framing of such elements, rather than the whole content of the report, which includes diverse pieces of information, from figures to tables and commentaries.

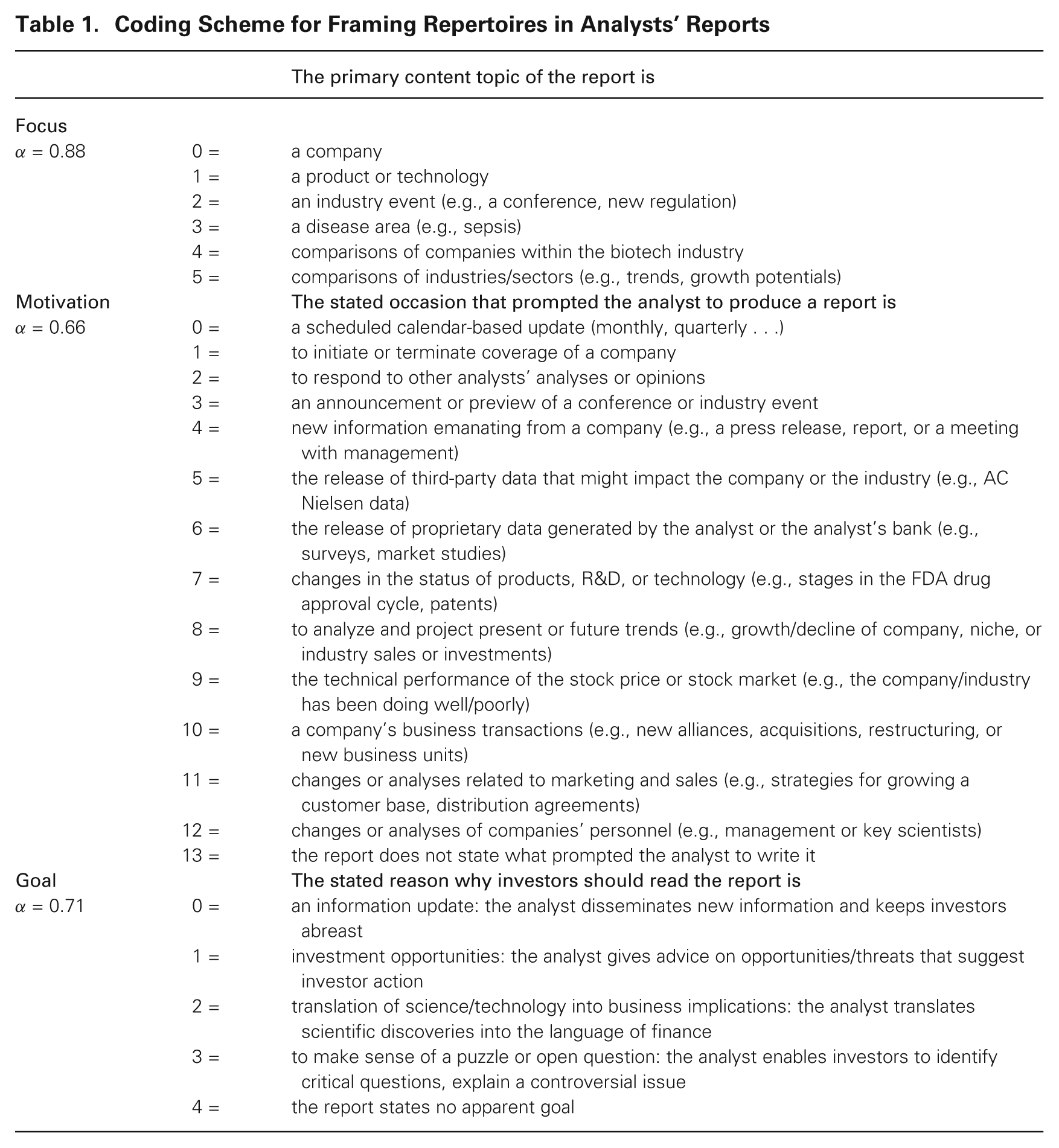

We found that three dimensions characterize framing in analysts’ reports: the focus or stated content of the report, the motivation for writing the report and reaching out to investors, and the goal or takeaway expected for investors from reading the report. We followed a three-step procedure to identify these dimensions and their associated categories. First, each author independently read 50 analysts’ reports and identified recurring dimensions, which we then compared and adjusted through discussion. We then asked 18 experienced analysts and investors who had no knowledge of these preliminary dimensions to describe what they use to initially characterize reports. This stage yielded no additional dimensions, but it simplified the existing category scheme. Finally, we tested the revised dimensions on a sample of reports, with each author coding 20 reports. At this stage, the dimensions allowed us to code each report exhaustively and consensually. Table 1 shows the dimensions and their corresponding categories.

Coding Scheme for Framing Repertoires in Analysts’ Reports

We used the dimensions of focus, motivation, and goal for coding the corpus of analysts’ reports. An attempt at computer-automation of coding of these frames proved difficult. Neither dictionary-based content analysis (Krippendorff, 2012) nor machine-learning approaches (Manning, Raghavan, and Schütze, 2008) reached acceptable levels of reliability. This is not surprising, because computational techniques process only information manifest in unformatted text, while framing in this context is accomplished through more subtle textual, visual, and structural means, such as sentences highlighted in boxes or in bold.

We then resorted to manual coding. We recruited coders familiar with the language of financial economics, pharmaceuticals, and biotechnology and provided them with identical written and oral instructions for how to recognize and code the dimensions and their categories. We coded a random subsample of 25 percent of the reports produced by each analyst in a given year, with a minimum of 15 reports. We used Krippendorff’s alpha (Krippendorff, 2012) to evaluate the intercoder reliability for the unique categories within each dimension. We calculated reliability statistics for each framing dimension from a random sample of 100 reports that were coded by two coders. If codes were assigned at random, alpha would take the value of 0; if agreement were complete, alpha would take the value of 1. The alpha coefficient was 0.88 for the categories describing a report’s focus, 0.71 for those describing its goal, and 0.66 for those describing its motivation. No consensual cut-off points exist for acceptable values of alpha, but values between 0.65 and 0.80 are considered acceptable for novel coding schemes, and values above 0.80 are seen as high (Chappell, Havrilesky, and McGregor, 1997). We also tested whether our categories could be collapsed into higher-order constructs (Mohr, 1998). We used hierarchical cluster analysis, but we did not find any clear clusters, and factor analysis, which did not yield a clear drop-off point in eigenvalues or unambiguous factor loadings. This confirms that the categories within each presentational dimension are mutually exclusive and that the choice of categories in one dimension is independent of the categories used in the others.

Dependent variable

The dependent variable is the inclusion of an analyst in II’s All-America Research Team (first, second, and third place, plus runner-up), coded as zero or one. We used a binary variable rather than the order of the ranking to reflect the views of interviewed analysts and investors, who simply distinguish “ranked” from “unranked” analysts and pay far less attention to ranking within the All-America Research Team. Robustness checks with the alternative ordinal variable are reported below.

Independent variables

All independent variables are time lagged. We constructed framing variables from reports published in the 12 months prior to the publication of II rankings. We measured resonance as how much framings correspond to audiences’ needs. To avoid potential tautological inferences, we empirically identified investors’ stated needs rather than inferring them from observable signs of appreciation. We triangulated several data sources to identify investors’ needs. First, we coded the needs that experienced investors articulated in our own interviews. Second, we used the lists published annually by II of what investors expect from analysts’ services. These relatively stable lists are generated from a second annual survey of investors. They are available since 1998, so both sources cover only part of our sample period. We therefore also categorized 279 quotes from investors that II has published with the annual All-America Teams since 1987. In the comments, investors express what they appreciated about All-America analysts, such as “straight-shooting style,”“clear pitches,” or “translations of the science.”

Across the three sources, we found convergence on three main needs that were enduring and widely shared: clarity of presentation, technological industry knowledge, and financial orientation. Clarity of presentation refers to the main point of a report being explicit, simple, and quick to grasp for investors. This expectation is directly linked to investors’ practice of quickly skimming reports and looking for a coherent perspective or story. Technological industry knowledge refers to an expectation that analysts show that they can assess the scientific basis of the industry and navigate the complexity of biotechnology and pharmaceutical R&D. This expectation reflects a common belief that competition and long-term performance in this industry are fundamentally driven by science-based innovation and that timely information about these processes is especially valuable. Financial orientation refers to analysts presenting information in ways that can be easily translated into investment decisions, by clearly stating investment implications and opportunities for returns and by structuring information in a way that corresponds to investment portfolio management approaches such as comparative attractiveness of stocks or sectors in the industry. This expectation reflects investors’ action-oriented reading of reports and their need to act quickly on information.

To measure resonance with investors’ needs, we matched framing categories with the three sets of needs and verified the validity of our coding by corresponding with industry practitioners. We operationalized clarity of presentation by using the categories “no clearly stated motivation” and “no clearly stated goal” (both reverse coded). All reports need to have a topical focus, but analysts have greater discretion in stating the motivation and goal of a document explicitly. To compute the variable, we averaged the percentage of an analyst’s reports that had a stated motivation or goal issued by the analyst over the prior 12-month period. We operationalized technological industry knowledge as the stated goal of a report being to translate scientific discoveries into investment implications and the topic as being about products or technologies. The corresponding variable is the percentage of reports with these categories in the prior 12 months. The third dimension of resonance is the financial orientation of the analyst’s offerings. We assigned three framings to this category: discussing the attractiveness of a company’s stock in comparison with other firms’ stocks, or of an industry in comparison with other industries, and including an explicit goal of identifying investment opportunities. The variable was calculated as the percentage of reports that use any of these three categories over the previous 12 months.

We then examined whether the three dimensions could be combined into a single variable of resonance with general investors’ needs. We first regressed the three variables and the control variables described below on our dependent variable. The coefficients of all three preferences described above were statistically significant at p < .05 and similar in size and direction (0.42, 0.35, and 0.41). A Wald test suggested that the three coefficients did not differ significantly from each other (p = .68), so combining the variables did not result in a loss of information. We computed an omnibus variable by adding the categories identified as resonating with either of the specific investors’ needs, so a report that resonates with all three receives a higher score than one that resonates with only one. We then aggregated reports to analyst-years in a procedure analogous to that for the separate variables.

Repertoire consistency

We used a continuous metric of concentration, the Herfindahl-Hirschman index, to capture the consistency of an analyst’s framing repertoire in the corpus of his or her reports during the 12 months prior to the II ranking. The index is bounded between 0 and 1, with 0 reflecting an even distribution across categories (variability) and 1 indicating the use of a sole category in all reports (consistency). We first created separate consistency variables for each framing dimension—focus, motivation, and goal—and then computed a measure of overall consistency as a linear combination of the distributions across the categories on all three dimensions.

Repertoire novelty

We created a novelty score for each report and then aggregated this measure to the analyst-year. The score for a report was computed as follows: we calculated the aggregate percentage of all reports that used a category in the 90 days prior to the publication of the focal report and then calculated novelty as 1 − aggregate percentage. We used a 90-day moving-average window with linearly decreasing weights because of the importance of quarterly reporting cycles and the fast-moving industry environment. 1 We created a variable of overall novelty by averaging the novelty scores on the three dimensions and then calculated an analyst-level novelty score as the average novelty of all reports by the analyst in the 12 months prior to the II survey.

Status as a moderator

We included an analyst’s previous II ranking as a proxy of visibility and individual status. We coded the variable as 1 if an analyst had been included in the All-America Team in any of the previous years, and 0 otherwise. We included the analyst’s employer organization status to control for organizational sources of esteem unrelated to the analyst’s framing practices. Employer status not only captures individual status by affiliation but also serves as a proxy for access to other highly qualified analysts and for the resources available to the analyst to promote his or her work. The variable was calculated as the inverse of II’s (continuous) ranking of banks for that year, ranging from −1 (top ranked) to −25 (not ranked).

Control variables

We included the analyst’s previous year ranking. We also included a number of variables that may affect evaluations but are unrelated to framing practices. We included investment advice performance, productivity, and expert credentials. We used the annual ranking produced by WSJ as described above to capture investment advice performance. This ranking is based on the hypothetical performance of a portfolio of stocks if an investor were to buy and sell stock according to the analyst’s recommendations. Analysts are then ranked by the investment gain over the year and are listed as either ranked or non-ranked, so that the resulting variable is binary. 2 We included two measures of productivity: extent of coverage (number of companies covered) and writing productivity (total number of pages published in the year). We measured expert credentials through a dummy variable for doctorate degrees in medicine or biosciences.

Analysis

We used a propensity-score-based reweighting procedure to give greater weight to observations of non-ranked analysts who are more similar to ranked analysts on dimensions other than framing. Although this approach complicates inferences about population-level effects, it allows us to better isolate the effect of framing from potentially conflating factors. We used the standardized mortality ratio (SMR) procedure described by Nichols (2007, 2008) and Sato and Matsuyama (2003). The method is an extension of inverse probability treatment weights (IPTW; see, for example, Hirano, Imbens, and Ridder, 2003), whereby the odds ratios of the estimated propensity score are used as weights for the control-group observations (non-ranked) and the weights of observations in the treatment group (ranked) are set to 1. 3

In estimating the propensity score, we included variables for two factors that are not part of our hypotheses: analyst visibility and the information content of reports. Analysts whose reports are not accessible to a large enough subset of investors logically cannot rely on framing as a means to garner audience appreciation. We included three variables related to visibility: the II rank of an analyst’s employer, whether the analyst had been previously ranked at least once in the WSJ ranking, and the number of companies covered.

Further, to distinguish framing effects from the information that is framed, the most informative comparison is between analysts who communicate similar information. We constructed two variables to reflect the similarity of information provided by an analyst compared with ranked analysts in a given year. The first variable uses company coverage. We recorded which companies each analyst covers in a given year and, from this information, which companies the analysts that were designated All-America in that year covered collectively. We then computed an annual Jaccard similarity metric between the set of companies covered by each analyst and the set of companies collectively covered by the ranked analysts.

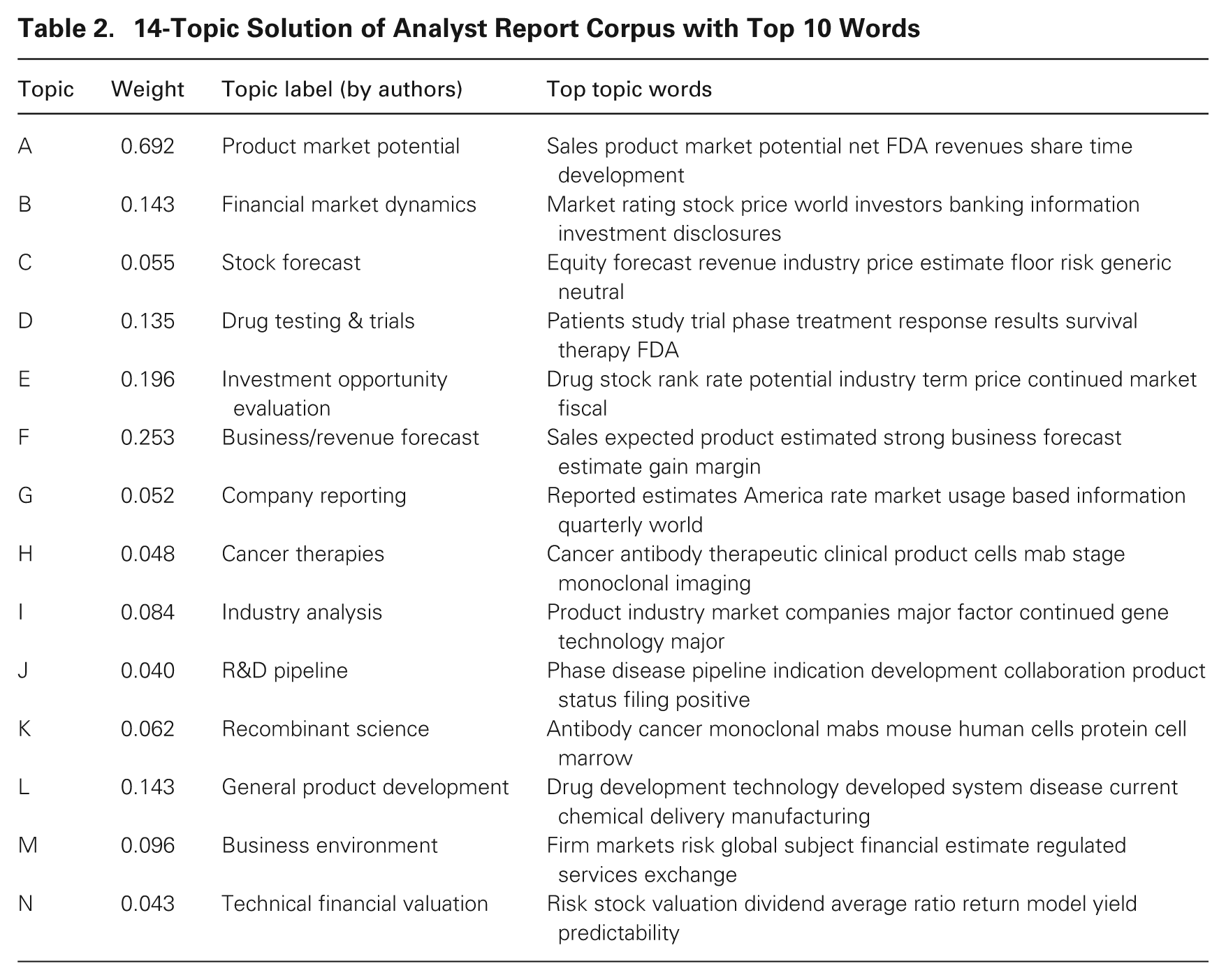

The second variable uses the aggregate information content of the reports produced by analysts. We used a text-mining technique—unsupervised topic models using the Latent Dirichlet Allocation (LDA) algorithm (Blei et al., 2003; Blei, 2012; Mohr and Bogdanov, 2013)—to inductively identify 14 broad themes (topics) in the same corpus of documents that we used in the coding of framing choices. 4 Each document is assigned a score for each topic (between 0 and 1, with the total across topics adding up to 1), resulting in a 14-dimensional vector. The identified topics, sample words, and possible labels are shown in table 2. We aggregated document-level topic scores to the analyst-year and calculated Mahalanobis similarity metrics between the annual average topic profile of the ranked analysts and that of individual analysts.

14-Topic Solution of Analyst Report Corpus with Top 10 Words

We then estimated panel probit models for an analyst being designated All-America in a given year on the reweighted observations, using the semi-parametric General Estimation Equation (GEE). This technique offers two advantages: first, it is relatively robust to assumptions about the covariance structure, and second, it is well suited to panel models with limited dependent variables. The Wooldridge test of autocorrelation suggested the presence of autocorrelation (p < .01), and the Arellano–Bond test for autocorrelation in first-differenced errors was significant for first-order but not for second-order autocorrelation in all shown models (p < .01 and p = .41 in the full model). We therefore specified a first-order AR(1) autoregressive disturbance term for all estimations. 5 In addition, we specified all reported models with robust standard errors (Gujarati, 1995; Bijleveld and van der Kamp, 1998). Finally, Breusch–Pagan LM tests for incorporating random effects were non-significant.

Results

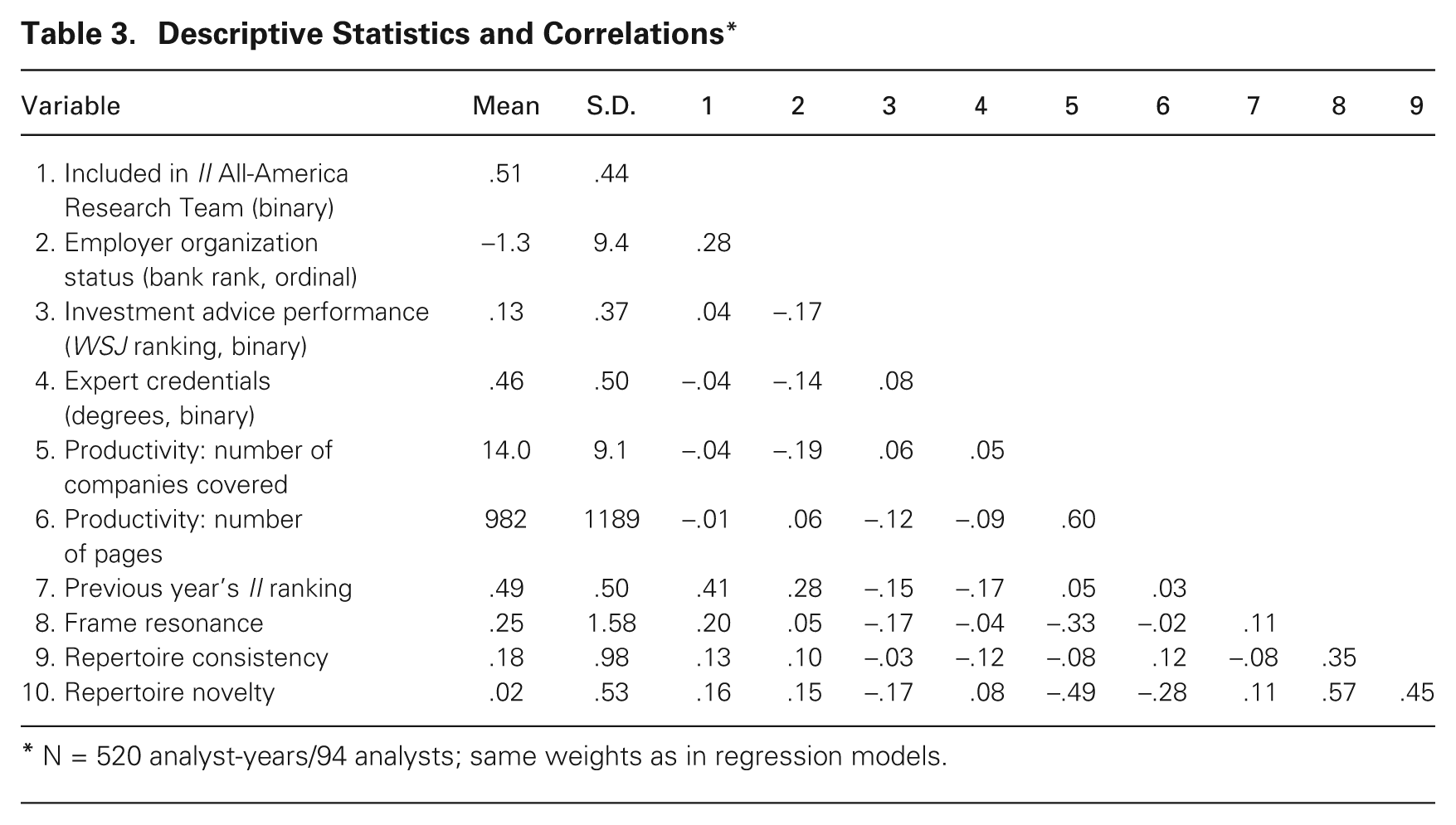

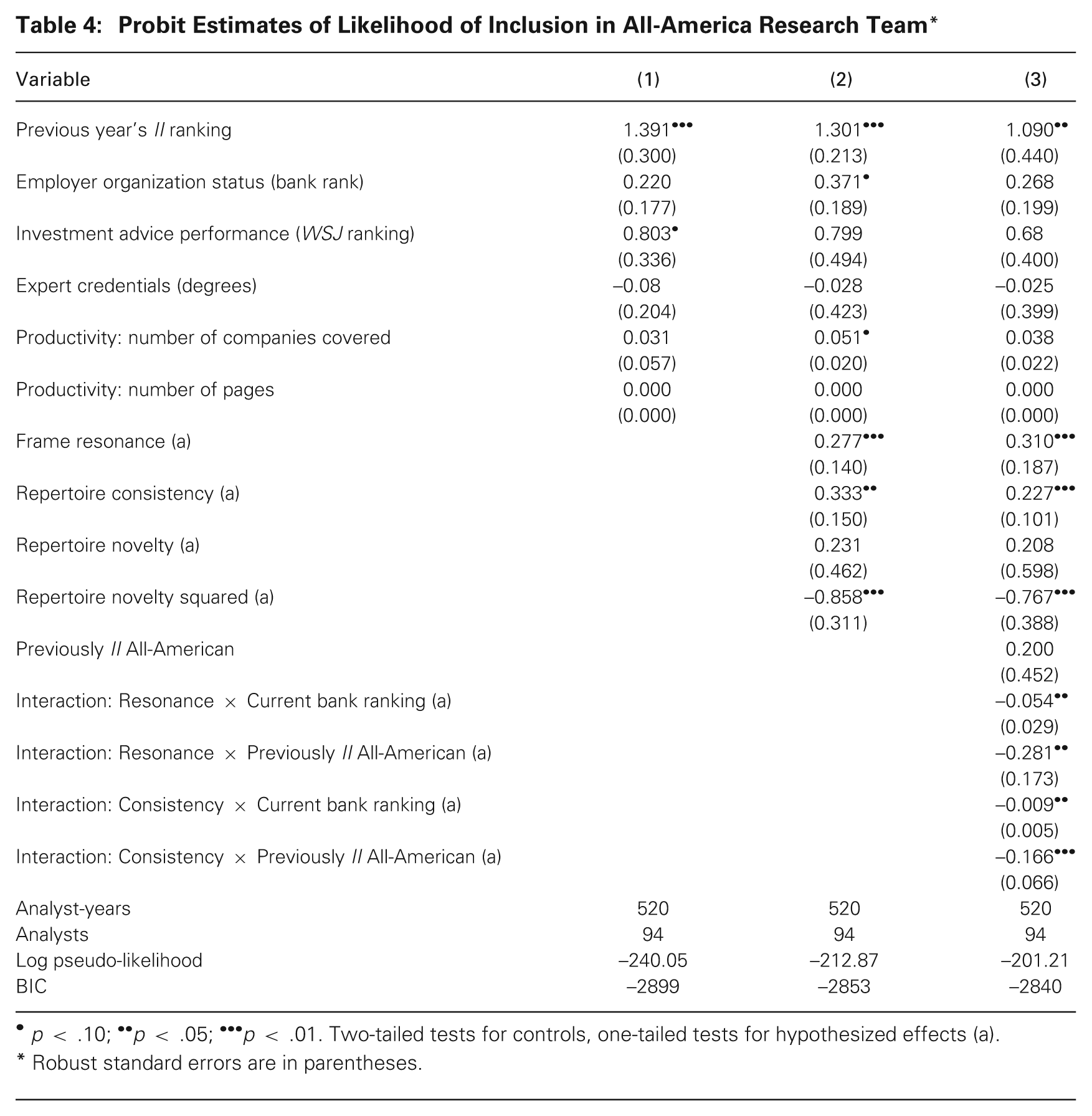

Table 3 shows descriptive statistics, and table 4 displays coefficient estimates. Model 1 in table 4 shows the effects of control variables only. Model 2 includes in addition the frame resonance, repertoire consistency, and novelty variables corresponding to hypotheses 1–3. Model 3 includes interaction terms between the framing dimensions of resonance and consistency and, respectively, bank ranking and prior II ranking, corresponding to hypotheses 4 and 5. 6 We found strong support for hypothesis 1 (frame resonance) across all models. Hypothesis 2, that more consistent repertoires lead to greater audience appreciation, was also supported. With other covariates held at their mean and binary variables at zero, moving from the 25th to the 75th percentile on resonance is estimated to increase the predicted probability of being ranked by about 8 percentage points, and doing the same on consistency by about 5. Hypothesis 3 predicted that framing repertoires employing moderate novelty are associated with better evaluations. This was also confirmed, as the quadratic term in models 2 and 3 was significant. We tested whether including the quadratic term increased model fit and found that the BIC was 4.32 points lower over a nested model without the quadratic term. According to Raftery (1995), this indicates positive evidence for improved fit. We also plotted the variable against predicted probabilities, holding other covariates at their mean and binary covariates at 0, to establish whether the quadratic term represented a symmetrical inverted-U shape or a decrease without a crest. We found that it did represent an inverted-U shape, though with greater negative effects for too much novelty than for too little.

Descriptive Statistics and Correlations*

N = 520 analyst-years/94 analysts; same weights as in regression models.

Probit Estimates of Likelihood of Inclusion in All-America Research Team*

p < .10;

Robust standard errors are in parentheses.

We found partial support for hypotheses 4 and 5. The interaction terms of individual and organizational status with resonance are significant and negative, as are those with consistency. We were unable to estimate a full model that also included the equivalent interaction term with novelty—aside from being rather complex to interpret, the interaction between binary moderators and the quadratic specification of novelty likely exceeded the statistical power of our sample. We did estimate the interactions with novelty in a separate model but found no significant effect either with the linear or the quadratic specification. We interpret this result as not supportive of hypothesis 5 for repertoire novelty.

The Online Appendix discusses the results of a number of analyses we performed to elaborate and check the robustness of our findings. We replicated the reported analyses as ordered probit models, included and excluded lagged dependent variables, split the sample by time period, included year dummies, and estimated analyst fixed-effects models. These analyses corroborate the findings reported above.

Taken together, the results of our analyses suggest that when exposed to a stream of framings over time and by many framers, audiences appreciate framings that appeal to their own needs for performing their job (resonance) and that are distinctive in terms of consistency and offering moderate novelty compared with others. Both individual and organizational status moderate the impact of framing resonance and consistency on audience appreciation, suggesting that the effect of framing is less prominent for high-status actors. These findings are robust over a range of model specifications. We were unable to find a parallel effect for novelty. Aside from the statistical limitations described above, one may speculate that in a fast-paced context, even high-status actors need to hold audiences’ attention by providing novel insights, whereas they are already seen as distinctive and resonant regardless of their framing practices because of their status.

Discussion and Conclusions

We set out to explore how framing can garner audiences’ appreciation in contexts in which audiences are exposed to multiple framings. Extensive evidence suggests that framing shapes audiences’ evaluations (e.g., Lounsbury and Glynn, 2001; Elsbach and Kramer, 2003; Fiss and Zajac, 2006; Martens, Jennings, and Jennings, 2007), but most current research overlooks the context in which audience members receive, interpret, and evaluate framing, limiting understanding of the effectiveness of framing. In many cases, audiences are bombarded with a multiplicity of framings (Weick, 1995; Levinthal and Rerup, 2006; Anteby, 2008), both by the same actor who engages in multiple communications over time and by multiple actors who also want to be heard. This multiplicity influences how framings are assessed, hence shaping their impact (Bowers, 2014).

Drawing on work on social evaluation, we proposed that audiences evaluate framing in two ways: cumulatively, in regard to a repertoire of frames deployed over time by an actor, and comparatively, in relation to other actors’ framings. Because of these more complex evaluation dynamics, the traditional recipe offered by the framing literature for success—resonance with one’s audience (Benford and Snow, 2000; Lounsbury and Glynn, 2001; Cornelissen and Werner, 2014)—is not the only way to garner appreciation. Actors also benefit from distinctiveness (e.g., Deephouse, 1999), which can be achieved either by crafting an easy-to-recognize identity through consistent framing choices over time (Rao, Monin, and Durand, 2003; Pontikes, 2012) or by offering moderate novelty in comparison with others (Chernev, 2004; Martens, Jennings, and Jennings, 2007). In addition, the prestige and visibility of actors affect how the audience processes and evaluates framing patterns. High-status analysts, who enjoy either personal or organizational status, are appreciated almost regardless of their framing practices. Our study holds implications for research on framing and impression management, as well as for research on financial markets.

Contributions to Framing Research

Resonance and distinctiveness

While framing research has generally emphasized resonance as a foundational mechanism for effectiveness (Benford and Snow, 2000; Cornelissen and Werner, 2014), impression management scholars have pointed out that resonant frames can also raise suspicions of ingratiation or self-promotion in the eyes of the framing targets (Jones and Pittman, 1982). In the context of our study, we did find support for the resonance mechanism: when analysts package their reports in ways that are consistent with the expectations and preferences of investors, appreciation ensues, especially for those without existing sources of status. We suggest that resonance in this context is effective because the nature of the interaction is pragmatic and professional, rather than ideological and political. Lesser-known analysts garner audience appreciation by delivering what investors want and are not evaluated on whether they espouse an ideology whose authentic enactment can be called into question (Hewlin, 2003). While resonant framing may thus not be universally effective, we expect the positive effect we found to extend to other similarly pragmatic audiences.

Based on the same principle of pragmatic audience evaluations, we extend our understanding of frame effectiveness beyond resonance to include distinctiveness as a path to audience appreciation. When audiences are bombarded with multiple framings, distinctiveness—in the form of consistency and moderate novelty—can be as effective as resonance. The old framing literature adage of “know thy audience” can thus be extended to include not only the audience’s interests but also the context in which frames are processed. Under conditions of competition with multiple others, standing out and differentiating oneself becomes an independent path to audience appreciation (Porac, Thomas, and Baden Fuller, 1989; Deephouse, 1999). The more nuanced interplay between resonance and differentiation is fertile terrain for further research.

Status and framing

By shifting attention to the context in which evaluations unfold, this study also contributes to research on framing by addressing the role of status as a moderator of the influence of framings on audience appreciation. The role of status results from the basic observation that high-status actors enjoy greater audience appreciation independently of their performance (in this study, framings) (Washington and Zajac, 2005). Status may also color the audience’s perception of framings and lead to a complementary relationship between the use of symbolic resources, such as framing, and existing status in gaining appreciation. Actors deprived of status resources must rely on framing to garner positive audience evaluations, while framing is less important for high-status actors who benefit from the Matthew effect, by which the rich get richer and the poor get poorer (Merton, 1968; Stewart, 2005). It should be noted, however, that this relationship may not be universal. Proper framing could be especially important for high-status or central actors under conditions in which audiences pay close attention to the framings of high-status actors. For example, the character of high-status actors could be under scrutiny because audiences’ evaluations are more ideologically based, the relationship with frame producers is conflictual, or high-status actors are the object of intense identification (Rhee and Haunschild, 2006; Rindova, Pollock, and Hayward, 2006). In the setting of investment advice, we found partial support for the Matthew effect and no support for an increased vulnerability of high-status analysts. We believe this finding again reflects the context of a professional exchange between analysts and investors. Our finding is consistent with other research in similar contexts, such as studies of cultural entrepreneurship that show that storytelling has a more significant effect for entrepreneurs who cannot rely on other resources (Lounsbury and Glynn, 2001; Martens, Jennings, and Jennings, 2007).

It would also be informative to assess if the framing-based path to status mobility suggested by our study—distinctiveness—applies to the entire population across a status hierarchy or if it is localized. Research on middle-status conformity (Phillips and Zuckerman, 2001), for example, implies that distinctiveness would be a pathway from middle to high status, but not from low to middle status. We were unable to answer this question empirically because the observable status dimensions in our sample are binary rather than continuous and capture only the top end of the status hierarchy. Our prediction would be that the pattern found for analysts generalizes to other settings in which audiences value diversity and novelty independently of status, in particular, settings in which status distinctions are categorical rather than continuous.

Framing and self-presentation

This study contributes to framing research by providing an empirical test of the self-presentational implications of framing (Goffman, 1959). Extant work has stressed how framing can persuade an audience of the quality, desirability, or worth of a new wine, organizational form, or film-making technique, for example (Rao and Giorgi, 2006); but we lacked empirical evidence of how such evaluations of an object—in this case, investment analysis and advice—translate into an evaluation of a subject—in this case, the analysts. We show that products or services that satisfy an audience’s needs and expectations develop a positive halo that extends to their producers (e.g., Brown and Perry, 1994). The fact that reports are strictly about financial matters, with no space for analysts to explicitly talk about themselves, does not preclude the formation of such a halo and its potential for analysts’ self-presentation. Goffman (1959) noted that assessment of others’ qualities is often done indirectly, by looking at their framing choices of clothing, stories, or home décor. The way we frame our decisions (Elsbach and Elofson, 2000), office space (Elsbach, 2003), or talk (Bourdieu, 1984) reveals much to an audience about our trustworthiness, competence, or social membership. We suggest a set of aggregation mechanisms, in the form of comparative properties of framing repertoires, that link framing practices to individual outcomes.

A related contribution of the self-presentational implications of framing pertains to the literature on celebrity in organization theory that shows how prestige and fame are exogenously constructed and bestowed upon an actor by the media (Malmendier and Tate, 2005; Rindova, Pollock, and Hayward, 2006; Graffin et al., 2008); our study complements this line of research by showing how outcomes such as prestige and fame can be endogenously achieved in the interaction with one’s audience through a mix of resonance and distinctiveness (Boltanski and Thevenot, 2006).

Implications for the Study of Financial Markets

Symbols and substance

A consideration of what audiences appreciate and value leads us to think more deeply about the relationship between symbolic and substantive bases of evaluation. This seems to be particularly cogent for a setting such as financial advice, considering that analysts’ audience of institutional investors collectively managed significant equity assets, estimated for 2013 around $10.5 trillion (Institutional Investor, 2013). Further, because in the context of this study the communication of frame producers can be observed over long periods, our findings suggest that investors could potentially identify which analysts “get it right” with their predictions vs. are “interesting” with novel or resonant framings.

An interesting puzzle is why these expert institutional investors would value anything more than stock-picking ability (represented by the Wall Street Journal’s ranking). While our results show that analysts’ stock-picking ability, as measured in the WSJ’s ranking, is taken into account in shaping investors’ appreciation, much variance remains unaccounted for. This fact speaks to how reports are actually used, interpreted, and evaluated by investors. What emerged from our qualitative analysis is that in the course of over 20 years, how analysts’ reports are used in practice did not substantially change (Knorr-Cetina, 2011; Groysberg and Healy, 2013); investors use reports to look for “a case for the bull and the bear,” not for stock-picking advice.

Analysts are then better conceptualized as conversation makers or producers of discourse (Espeland and Stevens, 1998; Fourcade, 2007) who can develop interesting perspectives and opinions about a firm or an industry. In this role, analysts do more than evaluate or classify stocks (Callon and Muniesa, 2005; Beunza and Garud, 2007). They facilitate financial markets as discourse makers who keep conversations going among participants by framing information in engaging ways (Fourcade, 2007). Moreover, the effect of framing does not wane over time in favor of more substantive factors (e.g., Zuckerman, 2012), possibly because of the inherent degree of uncertainty and guessing required in financial markets. Our study extends the perspective of analysts as conversation makers by examining how the use of frames in basic communication tasks not only facilitates coordination by creating shared understandings but also gives rise to distinctions among the producers of frames. Using skillful framing to keep information understandable, varied, and novel is, in fact, rewarded, as would be expected if the work of analysts were also cultural. Despite great changes in technology and regulation, the role of analysts as Wall Street conversation makers has proven to be resilient (Groysberg and Healy, 2013).

Repertoires as resource and constraint

A discussion of the use of symbolic resources such as framing connects our research with the literature on culture as a toolkit (Swidler, 1986, 2001). By bringing attention to the interdependence of framings among actors that vie for an audience’s attention, we further show the relevance of the embeddedness of particular communications in a larger field of cultural production (Bourdieu, 1977, 1984). The notion of repertoire conceptually allows for bridging micro-performances and the construction of a person-level character, which is key to evaluation processes and to bestowing prestige. In this sense, our study also contributes to a central debate in cultural analysis. Several prominent theorists of the repertoire perspective of culture (Gamson and Modigliani, 1989; Lamont and Thévenot, 2000; Swidler, 2001; Weber and Dacin, 2011) have emphasized the resource-like character of culture and actors’ ability to freely select from toolkits in public culture. But this perspective has been criticized for not bridging, at least empirically, conceptions of culture as resource and as constraint (Vaisey, 2009). Our work suggests that while many tools may be used to perform an analyst’s job, only some confer distinction and star status. The constraining influence of culture thus works in part indirectly, via the outcomes of audience evaluation that socially promote the users of some repertoires over others.

The (potentially) dark side of framing

Does a conceptualization of analysts as conversation makers give rise to a pessimistic view of financial markets? Markets may feed on hype, and such hype can be manufactured through the use of framing. This is the case portrayed in Martin Scorsese’s movie The Wolf of Wall Street, in which the “wolf” is purely concerned with framing junk stocks as valuable to acquire great personal wealth, while in the process bringing families into financial ruin. The fact that framing can shape evaluations of experts who mobilize trillions of dollars can be even more unsettling. Our take, however, is more optimistic, with investors as competent sensemakers who can put analysts’ advice into perspective: investors pay attention to good stock-picking recommendations but appreciate framings that help them solve pragmatic aspects of their job, such as processing much fast-moving information for taking action. Hence investors appreciate resonance, which allows them to process information faster and understand an action’s implications; consistency, which speaks to the need for building a portfolio of perspectives; novelty, which suggests no tolerance for redundant information but also a need to apprehend information quickly; and finally, status, which indicates the difficulty of screening the entire population of analysts and giving more weight to information from certified important sources. Our findings show that investors appreciate and confer marks of distinction on those analysts who can frame the content they need in the context in which they work.

Footnotes

Acknowledgements

We thank Dev Jennings and three anonymous reviewers, as well as Callen Anthony, Daniel Beunza, Tina Dacin, Rich DeJordy, Wendy Espeland, Jeremy Freese, Mary Ann Glynn, Boris Groysberg, Paul Hirsch, Paul Ingram, Candace Jones, Stefan Jonsson, Najung Kim, Brayden King, Christi Lockwood, Jeff Manza, Mike Pratt, Huggy Rao, Lauren Rivera, Giovanni Valentini, and participants at Northwestern University’s Culture and Society and Kellogg’s Management and Organizations workshops for helpful comments on earlier versions.

The results are robust to changing the period to four or two months prior to publication of the report. They are equally robust to additional weighting for more proximate comparison-peer analysts. For this, we computed an annual Jaccard similarity coefficient between each pair of analysts using their company coverage. We standardized the similarity metric by year and used it as a second weight for the reports used in the computation of the novelty variable.

The WSJ ranking is available only after 1991. To maintain our sample size, we used a statistical imputation approach for the earlier years (see Little, 1992, for a description of the detailed procedure). We used the predicted likelihood of being ranked in the WSJ, which we estimated from a best-fit logistic regression using all available covariates. We then added a random error term to each point prediction. This approach preserves the mean, variance, and distribution of the variable without biasing the estimation (Roth, 1994).

We also replicated our analyses using IPTW and found consistent results for the hypothesized relationships in terms of direction and significance of coefficient estimates.

How to determine the appropriate number of topics for a corpus is an area of ongoing research and debate (see, e.g., Chang et al., 2009). We used the commonly used criteria of minimizing word intrusion and topic interpretability to arrive at a 14-topic specification.