Abstract

We explore the relationship between status and reputation, examining how its dynamics change over time as these two intangible assets coevolve and how reputation and status are influenced by participation in highly visible events. Using a sample of more than 400 newly founded venture capital (VC) firms, we find that reputation and status positively influence each other but that reputation has a greater effect on status, particularly when firms are older. We also find that the effect of past status on current status weakens as VC firms age, but the relationship between past and current reputation remains consistent with age. Furthermore, our findings show that participating in big hits—blockbuster initial public offerings—has a positive relationship with status when firms are young and a positive relationship with reputation when firms are older, and it helps low-status and low-reputation firms more than it helps high-status and high-reputation firms. This study helps differentiate status and reputation, shows how they coevolve, and provides insight into how new firms build these important intangible assets.

Keywords

Coevolutionary processes—defined as mutually beneficial and sustainable ways of coexisting—are ubiquitous in nature. Biologists have used them to describe interdependencies in the development of species, such as the influence of predatory wolves on the evolution of caribou (Mech et al., 1998) and how plants compete for pollinators (Ehrlich and Raven, 1964); astronomers have used them to explain the relationship between black holes and galaxies (Peterson, Somerville, and Storchi-Bergmann, 2010); and social scientists have used them to describe how community networks and technology (Rosenkopf and Tushman, 1998), motivations and conceptual structures (Delton and Sell, 2014), and industries and their environments (Geels, 2014) influence each other. In this study, we focus on the coevolution of two valuable intangible assets, organizational reputation and status (Washington and Zajac, 2005; Barron and Rolfe, 2012).

The interdependence of reputation and status is reflected in the literature. For example, Podolny (1993) used “reputation” and “status” interchangeably in his status-based model of market competition; Shrum and Wuthnow (1988) combined them, referring to “reputational status”; and some scholars (e.g., Rindova et al., 2005; Lange, Lee, and Dai, 2011) have conceptualized status as a component of reputation. Further, the two constructs have many similarities: both are path dependent and accrue value over time; both provide signals that influence public evaluations of firms; and both affect organizational outcomes, including the ability to charge premium prices, acquire resources, and influence partnering decisions (Barron and Rolfe, 2012).

Recent research has begun to parse out the differences between these two constructs and explore their roles in the social construction of markets (e.g., Washington and Zajac, 2005; Jensen and Roy, 2008; Lee, Pollock, and Jin, 2011; Ertug and Castellucci, 2013). Washington and Zajac (2005: 283) summarized the key theoretical differences between reputation and status when they stated, “status is fundamentally a sociological concept that captures differences in social rank that generate privilege or discrimination (not performance-based awards), while reputation is fundamentally an economic concept that captures differences in perceived or actual quality or merit that generate earned, performance-based rewards.”

Despite the progress made in distinguishing status and reputation by focusing on the different ways they affect common outcomes, the question of how they influence each other has gone largely unaddressed. Researchers have speculated about which construct drives the other (e.g., Podolny, 2005; Sorensen, 2007) and have considered how the reputation of a firm’s initial partners influences its future status (Milanov and Shepherd, 2013), but no research we are aware of has systematically considered how status and reputation coevolve. Understanding the nature and nuances of the relationship between reputation and status and how it evolves over time is important because reputation and status are built in different ways and create different kinds of value (Washington and Zajac, 2005; Barron and Rolfe, 2012). Building each intangible asset requires understanding how reputation and status change over time and how significant events can influence the trajectory of their development. For young firms, understanding this relationship can provide crucial guidance for investing their scarce resources and attention to effectively build their status and reputation (Rindova, Petkova, and Kotha, 2007; Fund et al., 2008). A deeper understanding of how status and reputation coevolve can also shed light on how these two intangible assets influence organizational outcomes and success (e.g., Dimov, Shepherd, and Sutcliffe, 2007; Ertug and Castellucci, 2013).

We synthesize and build on prior work by collecting data from newly founded venture capital (VC) firms so that we can explore how reputation and status coevolve over time and the factors that influence their coevolution. We develop theory to explain how reputation and status influence each other, the relationship between past and current reputation and status, how these relationships change over time, and how they are shaped by visible, positive events. The VC industry is an ideal setting for examining these issues for several reasons. First, reputation has both symbolic and substantive benefits for the firms that VCs fund (Lee, Pollock, and Jin, 2011). Second, the extensive webs of interorganizational relations constructed through investment syndicates exert significant influence on VC firms’ functioning and behavior (Hochberg, Ljungqvist, and Lu, 2007; Milanov and Shepherd, 2013) and make studying how the relationships evolve over time possible (Fund et al., 2008). Finally, the VC industry is bound together by an implicit coevolutionary network: start-ups depend on VCs for capital and other resources, VCs require access to promising start-ups that can provide investment returns that allow them to raise more and larger funds, and investors depend on VCs to identify and develop start-ups to help them grow their investment portfolios. VCs’ status and reputation help facilitate all these interactions in the face of substantial uncertainties.

The Coevolution of Reputation and Status

Both organizational reputation and status are intangible, “social approval” assets that provide benefits via their ability to create favorable collective perceptions (Pfarrer, Pollock, and Rindova, 2010: 1131). As such, the two concepts overlap and are often confused. Reputation has been defined in many ways by different scholars and research traditions. We adopt the definition put forth by Rindova and colleagues (2005) that a firm’s reputation is best understood as broad public recognition of the quality of a firm’s activities and outputs. This definition captures two critical elements of reputation that allow it to create value: (1) the perceived predictability of a firm based on past performance and behaviors (i.e., being known for reliability or quality) and (2) the extent to which these perceptions are widely known and shared. With respect to status, in a recent review of the status literature Sauder, Lynn, and Podolny (2012: 268) stated, “Status, for organizations as well as individuals, is broadly understood as the position in a social hierarchy that results from accumulated acts of deference” and further noted, “A central thesis of organizational research is that a firm’s status (and implicitly the deference to that firm) is influenced by the status of the entities with whom the firm affiliates.” Status is a socially constructed asset that can “generate privilege or discrimination” (Washington and Zajac, 2005: 283) and is used to signal quality when uncertainty is high (Lynn, Podolny, and Tao, 2009). Its cachet is ascribed by observers based on their perception that the organization is favored by other high-status actors, which is deduced from observable patterns of affiliation.

Although these definitions are conceptually similar, they differ in four fundamental ways. First, status primarily reflects perceptions of an organization’s position in a social hierarchy based on observable patterns of connections (Sauder, Lynn, and Podolny, 2012), such as affiliations with prestigious partners and centrality in market networks (Podolny, 1993, 2001; Washington and Zajac, 2005). As Sauder and colleagues (2012: 269) noted, “Although status is often used as a signal of the degree to which an individual or firm possesses a desirable quality, quality is often more difficult to observe than connections.” Status is more distantly related to the organization’s ability to meet its stakeholders’ expectations than reputation, and the benefits of status arise from the “privilege” conferred by the actor’s social standing (Washington and Zajac, 2005: 283).

In contrast, reputation is derived from stakeholders’ estimations of organizational attributes that shape expectations of the firm’s future behaviors (Milgrom and Roberts, 1986; Weigelt and Camerer, 1988). These estimations and expectations are driven by stakeholders’ observations of or direct prior experience with the organization. Although reputation is often assessed relative to a peer group of actors, and actors can be ranked based on their reputations (Espeland and Sauder, 2007; Deephouse and Suchman, 2008), these relative rankings result from assessing and ordering actors based on specific performance dimensions. Thus, though the ordinal listings of different actors’ reputations are used to make relative comparisons, they are not relational reflections of their social standing based on patterns of deference. Here, perceived quality largely depends on a firm’s “merit” (Washington and Zajac, 2005: 283) or observable track record of delivering quality products or services (Pfarrer, Pollock, and Rindova, 2010).

Further, in developing theory to reconcile different perspectives on the emergence and reinforcement of status orders, Gould (2002) argued that even though status orders are partly based on actors’ attributes, the rewards and benefits conferred by a given status level will not be commensurate with the differences in individual quality. Because the underlying differences are socially influenced, high-status actors get more credit and low-status actors get less credit than they deserve based on objective assessments of their quality alone. Thus, whereas reputation is closely tied to perceptions of merit, quality, and high performance, Gould suggested that status may be only loosely coupled with quality because social enactment processes that establish and maintain status orders and the privilege status generates systematically distort the relationship between status and quality. Bothner, Kim, and Bishop (2012) provided additional empirical evidence that very high levels of status are associated with declines in performance, which could be due to the complacency or distractions associated with high status.

A second difference is that no assumption of full intersubjective agreement among observers is required to establish an organization’s reputation. A firm can have different reputations with different stakeholder groups for different things (Lange, Lee, and Dai, 2011; Jensen, Kim, and Kim, 2012), and its relative standing in different reputation rankings can vary accordingly. But intersubjective agreement is needed when determining an organization’s status because differences in status reflect fundamental social characteristics or structures that can be unrelated to—and exist independently of—real or perceived quality differences (Washington and Zajac, 2005). Washington and Zajac’s (2005) Jaguar example vividly illustrated the differences between reputation and status. Although the automobile manufacturer long suffered from a reputation for poor quality, it nonetheless was able to charge premium prices because of the privilege that accompanied its high social status as a luxury automobile manufacturer and the associated social status of those who drove its vehicles. Further, though recent increases in perceived and actual product quality have improved Jaguar’s reputation, its status remained unchanged or perhaps even decreased after it was acquired by Ford, a company that is not as highly associated with luxury, social status, and privilege.

Third, reputation and status differ in their influence on firms’ strategic decisions. For example, Dimov and colleagues (2007) found that a VC’s reputation weakens the negative relationship between finance capacity and the decision to invest in early-stage ventures, while a VC’s status strengthens the same relationship. Ertug and Castellucci (2013) found that National Basketball Association (NBA) teams were more likely to focus on high-reputation players when they were concerned about product quality (i.e., winning games), while high-status players were used to increase revenues. And Jensen and Roy (2008) found that following the demise of Arthur Andersen, companies searching for new auditing firms used status to screen potential firms and then used reputation to choose a specific firm within the chosen status bracket.

Fourth, reputation and status may also differentially affect stakeholders’ decisions (Deephouse and Suchman, 2008). Lee and colleagues (2011) found that although both VCs’ reputation and status enhance initial market responses to the IPO firms they invest in, only reputation, which is based in part on VCs’ abilities to successfully develop start-up firms’ capabilities, is also related to post-IPO operating performance. Status is also strongly associated with partner quality in director networks, while reputation affords firms diverse networks and opportunities to span structural holes (Chandler et al., 2013), and congruence between reputation and status enhances alliance formation (Stern, Dukerich, and Zajac, 2014). Taken together, this research establishes clear theoretical differences between status and reputation and shows the different ways they can influence strategic decision making and firm performance.

The Venture Capital Firm Context

Today’s VC industry took shape in the early 1980s after a 1979 amendment to the U.S. Employee Retirement Income Security Act (ERISA) modified the “prudent man” rule governing pension fund investments. Until then, pension funds were prohibited from investing significant sums in high-risk assets, including venture capital funds. According to Gompers and Lerner (2006), who reviewed the industry’s history, VCs raised $495 million (in 2002 dollars) in new investments in 1978, and during the 1980s raised between $1.5 billion and $5.6 billion a year. Following the recession of the early 1990s these amounts increased from $2.3 billion in 1992 to $12.7 billion in 1997, reached $62 billion in 1999, and hit a high of $108 billion in 2000. Hundreds of new VC firms were also founded during this period, making it useful for studying the coevolutionary dynamics of status and reputation in firms’ early years.

Several additional aspects of the VC industry make it useful for studying the coevolution of reputation and status. As Fund and colleagues (2008: 567–568) noted, a strong status hierarchy exists within the industry, and investment syndicates are commonly used to spread risks and share rewards. The resulting embedded ties among the VC industry’s elite participants complement its well-developed legal structure, creating socially reinforced boundaries that limit access to core deal networks. These well-defined and easily observed VC syndicate networks have made this context attractive to organizational (e.g., Podolny, 2001; Guler, 2007; Hallen, 2008; Ma, Rhee, and Yang, 2013) and finance (e.g., Hochberg, Ljungqvist, and Lu, 2007; Sorensen, 2007) scholars studying status.

The VC industry has also been attractive to scholars studying reputation. VC firms have to build reputations with investors in their funds for identifying and developing high-potential companies that can provide the investors with significant returns (Gompers, 1996; Lee and Wahal, 2004). They also need to identify and negotiate agreements with promising start-ups. As the most attractive start-ups often have multiple VCs vying to invest in them, a VC firm’s reputation for working with and developing firms is important (Sapienza, Manigart, and Vermeir, 1996; Fund et al., 2008; Lee, Pollock, and Jin, 2011). Because their two primary stakeholder groups have similar interests, generalized perceptions of VC firms are likely to hold across both groups, thereby minimizing questions about whether firms have different reputations with different stakeholder groups (Jensen, Kim, and Kim, 2012).

The Coevolution of Reputation and Status

Despite the widespread interest in organizational reputation and status, there has been limited research on how they coevolve. Research has established that status and reputation are positively correlated. High reputation based on strong performance can increase access to elite social circles (Hallen, 2008; Milanov and Shepherd, 2013) while high status can provide greater access to the information, opportunities, and resources that can enhance reputation (Benjamin and Podolny, 1999; Sorensen, 2007). Consistent with prior research, we treat this coevolutionary process as roughly contemporaneous. 1 Because both reputation and status provide benefits that aid in developing the other construct, we expect them to have a positive relationship as they coevolve. As this expectation is unsurprising, we do not present a formal hypothesis, but it does form our baseline assumption.

The effects of firm age

Though we expect reputation and status to positively influence each other, we do not expect the nature of this relationship to remain constant over time. During its early years a firm has little standing in its industry’s social hierarchy, and what status it has is largely the result of the founder’s personal status (Fund et al., 2008; Hallen, 2008; Ewens and Rhodes-Kropf, 2013). To enhance its status, the new firm needs to build relationships with high-status actors. This is particularly critical in the VC industry, in which VCs routinely participate in syndicates that provide investment opportunities and information about other VCs (Podolny, 2001). Access to these syndicates shapes a VC firm’s opportunities and performance (Hochberg, Ljungqvist, and Lu, 2007; Sorensen, 2007), and gaining access to these networks requires building a track record of performance (Rindova, Petkova, and Kotha, 2007; Fund et al., 2008).

Although high-status actors prefer to affiliate with other high-status actors (Sauder, Lynn, and Podolny, 2012), high-status firms form relationships with low-status firms because they expect they will work harder than other high-status firms on their behalf (Castellucci and Ertug, 2010). To the extent that new VCs demonstrate energy and effort by bringing promising deals to high-status VCs, thereby building their reputations, the new VCs will be able to develop relationships that begin to enhance their own status (Fund et al., 2008; Milanov and Shepherd, 2013). These affiliations provide young firms with endorsement benefits (Petkova, 2012) and access to higher-quality deals (Sorensen, 2007), further enhancing their performance and reputation.

Prior research suggests that status tends to be “stickier” than reputation (Washington and Zajac, 2005). Once established, status orders are relatively stable and self-reinforcing because high- and low-status actors behave in ways that reinforce the current status order: low-status actors defer to high-status actors, and high-status actors prefer to interact with others of similar status (Podolny, 1993; Gould, 2002). Further, high-status actors attract more attention and are given more credit for outcomes than low-status actors, a phenomenon known as the “Matthew effect” (Merton, 1968). In contrast, reputations must be constantly reinforced (Lange, Lee, and Dai, 2011) and therefore change more easily. Consistent behavior is a key aspect of establishing and maintaining a reputation (Pfarrer, Pollock, and Rindova, 2010). If a firm behaves inconsistently or its performance declines, its reputation follows suit (Basdeo et al., 2006; Love and Kraatz, 2009). These effects may be delayed or gradual, particularly if the declines are small and occur over time (Rhee and Valdez, 2009), but large drops in performance or crises can lead to significant reputational declines in very short order (Coombs, 1998).

Taken together, this suggests that while new firms typically occupy lower-status positions, they can change existing patterns of interaction—and thus their own status—by developing a positive reputation. Although status provides benefits that enhance reputation, reputation needs to be developed before status can be changed and these benefits are accessed. Thus we expect that reputation will have a greater influence on status than status has on reputation during the early years of a VC firm’s life, when both are more malleable. But as a VC firm ages and its status increases as a function of its reputation, VC firms should be able to access the status benefits that make it easier to continue being successful, thereby enhancing their reputation (Benjamin and Podolny, 1999; Sorensen, 2007; Fund et al., 2008). To the extent that a new status equilibrium is established (Gould, 2002), over time a VC firm’s status should stabilize and be less susceptible to changes in reputation (Gould, 2002; Sauder, Lynn, and Podolny, 2012). As such, we expect that as firms mature, status will have a greater influence on reputation than reputation will have on status. We therefore hypothesize:

The effects of past status and reputation over time

Just as a firm’s age affects the relationship between reputation and status, we expect that it also influences the relationship between a firm’s prior and current reputation and status. Research has shown that initial conditions influence subsequent status when firms are young and their position in the status order is being established (Fund et al., 2008; Bendersky and Hays, 2012), that status becomes more stable and tends toward equilibrium over time (Gould, 2002; Washington and Zajac, 2005), and that reputation is dynamic and needs to be continually reinforced (Love and Kraatz, 2009; Pfarrer, Pollock, and Rindova, 2010). This suggests that though prior status and reputation are positively related to current status and reputation, the strength of that relationship may change as new firms age and their status becomes stabilized.

We expect that when firms are young, status in one period will have a strong influence on status in the next period, for several reasons. First, young firms’ positions in the industry’s status hierarchy are still being negotiated and are unlikely to have reached an equilibrium (Gould, 2002; Bendersky and Hays, 2012). Status can take considerable time to build (Gould, 2002), which can lead to more instability and thus a greater influence of prior status on current status in the early years. Second, as we argued above, when firms are young their abilities and track records are not well known (Bunderson, 2003), which is in part why we expect reputation to have a stronger effect on status than status has on reputation in young firms. As such, other firms’ uncertainties about young firms’ abilities are higher, and prior status may be relied on more as a signal of quality (Lynn, Podolny, and Tao, 2009), thereby playing a stronger role in partner selection and the social construction of the firm’s status (Castellucci and Ertug, 2010). Third, most young VCs have lower status, so the marginal benefits of a change in status may be greater for them than for older firms, which may tend to have higher status (Gould, 2002; Sauder, Lynn, and Podolny, 2012).

As VC firms age, their capabilities and history of relationships will be better known (Bunderson, 2003), and their relative standing in the status order will achieve equilibrium and stabilize (Gould, 2002). While changes in status can still occur, older firms will more quickly reestablish a new equilibrium (Gould, 2002); thus status changes during the prior period will have a weaker effect on status in the current period when firms are older. In contrast, because reputation needs to be continually reinforced, it is always susceptible to changes in prior reputation (Love and Kraatz, 2009); thus the effect of changes in prior reputation on current reputation will not weaken as the VC firm ages. We therefore hypothesize:

Big hits

Research on path dependence (David, 2005; Sydow, Schreyogg, and Koch, 2009) shows that significant events can change organizations’ life trajectories. Further, reputation research suggests the positive attention from associating with “big hits” can enhance reputation (Pollock, Rindova, and Maggitti, 2008; Denrell and Fang, 2010). Visible performance outcomes can increase an actor’s “cognitive” centrality (Bunderson, 2003)—the extent to which other actors within a group have an accurate understanding of an actor’s expertise and abilities—which in turn enhances the actor’s “structural” centrality, or status, and ability to gain resources and opportunities that enhance subsequent performance and reputation (Fund et al., 2008).

Although association is not indicative of causation, individuals often make causal attributions based on observable associations, particularly in situations in which establishing causation can be difficult (e.g., Levitt and March, 1988). This is why observable status connections are used as proxies for quality (Sauder, Lynn, and Podolny, 2012). Further, actors are often rewarded for their “visionary” insights when they accurately predict extreme outcomes, or big hits, such as new disruptive technologies or the next big pop music star (Denrell and Fang, 2010). Association with such highly visible, positive events can have a “halo” effect, enhancing the perceived importance and competence of the affiliates (Rindova, Petkova, and Kotha, 2007; Petkova, 2012). In the VC firm context, one such event is participation in “blockbuster deals”—initial public offerings (IPOs) that experience high levels of “underpricing” (Pollock and Gulati, 2007), which is the percentage change in the value of the stock on the first day it trades on the public market. Taking portfolio companies public is the best outcome possible for a VC investment because IPOs generate approximately four times greater returns on average (Guler, 2007) than private sales to other companies—the other form of successful VC “exit” from an investment.

Blockbuster deals are viewed positively because VCs do not liquidate their entire investment as part of the IPO. Although VCs may sell some portion of their stock as part of the IPO, too much “insider” selling at IPO is interpreted negatively by the markets (Gompers, 1996). Further, the value of the VC’s investment grows substantially to the extent there is a big jump in price once the stock begins public trading. For example, Fund and colleagues (2008) noted that VC firm Benchmark Capital’s investment in eBay experienced a 163-percent price jump at IPO in 1998, making its $2.6 million investment worth $414.4 million. By early 1999 its investment was worth $2.5 billion.

Blockbuster deals also attract significant attention, creating a “buzz” about the start-up that leads to increased web traffic (Demers and Lewellen, 2003), media coverage (Pollock, Rindova, and Maggitti, 2008), analyst coverage (Cliff and Denis, 2004), and alliance formations (Pollock and Gulati, 2007), among other positive outcomes. Blockbuster deals provide the VC firms funding these start-ups with an opportunity to “grandstand,” which can increase investors’ desires to put money in the VC’s future funds (Gompers, 1996; Lee and Wahal, 2004). Similarly, start-ups will want to take investments from these VCs in the hopes they will have similar success. In this way, participation in blockbuster deals influences the coevolution of reputation and status and the interdependencies among VCs, their investors, and the firms that they invest in.

Though blockbuster deals have a positive effect on both a VC firm’s reputation and status, we expect the effect will vary with the firm’s age. A high level of general visibility is an important component of reputation. Rindova and colleagues (2005) argued that a firm’s visibility determines the value it receives from its quality and performance because the value of a firm’s reputation is a function of the extent to which its merit is widely recognized. Because reputation must be continually reinforced (Pfarrer, Pollock, and Rindova, 2010), we expect that participation in blockbuster deals will continue enhancing a VC firm’s reputation as it ages.

In contrast, general visibility has not been treated as a central component of status. Though increased visibility can enhance a VC firm’s cognitive centrality within the industry when it is young (Bunderson, 2003; Fund et al., 2008), increased visibility and buzz are less likely to help increase an actor’s status once its position in the status order is established. Bothner and colleagues (2012) also suggested that high visibility can even lead to distractions that erode a high-status actor’s performance. Thus when firms are young and unknown, we expect blockbuster deals will enhance their status because they bring the firms to the attention of high-status VCs (Fund et al., 2008). But as a VC firm ages and its position in the status order stabilizes, the visibility and attention are less likely to affect its status (Gould, 2002). We therefore hypothesize:

Not all VC firms will benefit equally from investing in blockbuster deals, however, because stakeholders’ expectations will affect the extent of their influence. Blockbuster deals provide valuable signals only if they provide new information (Pollock et al., 2010), and information disconfirming prior beliefs is more salient and likely to be noticed than information confirming expectations (Anderson, 1981). Thus the lower the expectation that a VC will be involved in a blockbuster deal, the bigger the surprise and the greater the effect on reputation and status participating in a blockbuster deal is likely to have (Pfarrer, Pollock, and Rindova, 2010). Participation in blockbuster deals suggests that a VC firm has access to high-quality deal flow and/or is able to develop start-ups effectively (Sorensen, 2007; Lee, Pollock, and Jin, 2011)—characteristics typically associated with high-reputation and high-status firms. Low-reputation and low-status VC firms are not expected to participate in blockbuster deals because they are not expected to have the same skills and access (Sorensen, 2007; Milanov and Shepherd, 2013). If participating in blockbuster deals merely meets expectations for high-reputation/high-status VCs, it should have a smaller effect on the VC’s subsequent reputation and status than for low-status/low-reputation VCs. Further, firms with high status and reputations already have access to the resources these intangible assets provide, so the incremental benefits from any reputation and status increases will be smaller. We therefore hypothesize:

Methods

Our data came from the Thomson Banker One (TBO) Private Equity database and included all U.S. VC firms founded between 1990 and 2000. Like prior VC studies (e.g., Podolny, 2001; Hochberg, Ljungqvist, and Lu, 2007), our analysis focused on the VC firm level. The TBO dataset includes investment information (funding round date, disclosed funding round amount, and participating VCs), VC information (founding date, fund size, geographic location, affiliation), and portfolio firm information (developmental stage at each funding round date, industry, and IPO status). The TBO dataset classifies both traditional private equity firms (PEFs) and VCs as PEFs. Traditional PEFs engage primarily in buyouts, and their syndication rationales and networking behaviors differ substantially from those of VCs (Campbell, 2003). We included only firms that invested in rounds considered Seed, Startup, Startup Financing, Early Stage, First Stage Financing, Expansion, Later, Balanced, or Research and Development. Manual web searches confirmed that this effectively differentiated VCs from traditional PEFs.

We identified 545 VC firms founded between 1990 and 2000. VC firm foundings were on a clear, increasing trend over the sampling period, with the peak coinciding with the height of the dot-com bubble. We constructed panel data for each VC firm from its founding through 2010 to track the coevolutionary process between status and reputation. Due to missing network data and the need for at least two successive-year observations to estimate Arellano–Bond models, our final sample consisted of 433 VCs for the status evolution models and 444 VCs for the reputation evolution models. 2 To enhance comparability between the status and reputation evolution models, our final sample included only VCs for which we had both reputation and status scores. Thus our final sample consisted of 433 VCs and 3,093 and 3,242 VC-year observations for the status and reputation evolution models, respectively.

We conducted t-tests based on the earliest observation of each firm to assess whether the sample attrition created selection bias. Because our data were panel data, the earliest observation best captures initial conditions of the firm for assessing sample selection bias. Observations after the earliest point may well contain not just the initial conditions but also the effects of the evolutionary process that we theorize. The t-tests revealed no significant differences across VC firms included and excluded from our sample with respect to founding year, reputation, age, industry diversification, and early-stage preference.

Jointly Determined Variables

Status

Research has established that a good proxy for VC status is centrality in syndication networks (Podolny, 2001; Guler, 2007; Hallen, 2008). We used available data on all the VCs in the TBO database, not just our sample, to calculate this measure. For each VC firm we constructed one-year adjacency matrices. To smooth patterns of affiliation (Baum et al., 2005), each annual adjacency matrix included coinvestment networks based on five-year moving periods beginning with the VC firm’s founding year (i.e., 1990–1994, 1991–1995, etc.). For VC firms less than five years old we used all available data.

We operationalized status using Bonacich’s (1987) beta centrality, a measure of global centrality that considers the focal actor’s centrality, its connected actors’ centralities, their connected actors’ centralities, and so on (Bonacich, 1987). When beta is set to zero, network centrality is akin to degree centrality, focusing only on the local structure. The larger the value of beta, the more the centrality measure reflects the global structure. In our analysis, we set beta to 75 percent of the reciprocal of the largest eigenvalue. We also standardized our status measure so that its effect size could be compared with the effects of reputation. We used UCINET version 6.399 (Borgatti, Everett, and Freeman, 2002) to calculate our status measure. 3

Reputation

Our VC reputation measure is a modified version of the Lee, Pollock, and Jin (2011) LPJ reputation index, which is available at www.timothypollock.com/vc_reputation. 4 The LPJ reputation index is a multi-item, time-varying index that reflects a VC firm’s ability to raise investment capital and develop start-ups, the two performance dimensions important to other VCs, investors, and start-ups seeking VC funding (Lee, Pollock, and Jin, 2011). It is an objective as opposed to perceptual measure of reputation in that it is composed of objective measures expected to influence stakeholders’ perceptions. Objective reputation measures are often employed when perceptual measures are unavailable, and they can be constructed retrospectively for use in longitudinal analyses.

Like the LPJ index, our index included five formative indicators of VC firm reputation: (1) average of the total dollar amount of funds under management over the prior five years, (2) average of the number of investment funds under management in the prior five years, (3) number of start-ups invested in over the prior five years, (4) total dollar amount of funds invested in start-ups over the prior five years, and (5) number of companies taken public in the prior five years. 5 The original LPJ index also included firm age, which we excluded from our index because we used it as a moderator in our theory and analyses. The two versions of the index are correlated at .98, and our results were the same regardless of the version used. These indicators were also standardized and aggregated using a five-year moving average.

Like Lee and colleagues (2011), we needed to make the values comparable across time. Market dynamics can make cross-year comparisons difficult; for example, what was considered a large amount of capital under management or number of IPOs was very different in 1991 and 1999. Thus we rescaled the index so that within-year differences are maintained while cross-year variance in values due to market conditions is eliminated, and we converted our measure to a 100-point scale that is comparable across years. As the standardized index can take on negative values, for each year we added a constant equal to .01 plus the positive value of the lowest reputation score that year to all scores (making all values positive) and divided each score by the largest value that year. We then multiplied the resulting value by 100. This rescaling allows for cross-year comparisons while maintaining the relative ratings among VCs within each year. Like status, this final measure was standardized so that the relative effects of reputation and status could be compared when testing H2. The results were unchanged when unstandardized measures of reputation and status were used in the analysis.

Independent Variables

Firm age

Consistent with prior research (Lee, Pollock, and Jin, 2011; Milanov and Shepherd, 2013), VC firm age was calculated as the focal year minus the year a VC firm raised its first fund.

Blockbuster deals

This measure equaled the number of blockbuster IPOs a VC invested in as of the year before the current year. We used an IPO’s underpricing (percentage change in stock price on the first day of trading) to operationalize blockbuster deals because it is an easily observable and widely viewed indicator of the IPO’s success (Pollock and Gulati, 2007; Pollock, Rindova, and Maggitti, 2008). We weighted each IPO’s underpricing by its IPO value to allow for any potential size effects, as smaller offerings have a greater ability to generate higher levels of underpricing. Blockbuster deals were defined as those whose weighted underpricing was above the 75th percentile of IPO underpricing for all IPOs that year. 6 This measure is a count that increases only when a VC participates in a blockbuster deal. So if a VC firm was founded in 1992, had its first blockbuster deal in 1995, and had its second blockbuster deal in 1997, this measure would take a value of zero until 1996, would have a value of one in 1996 and 1997, and would take a value of 2 in 1998. Eighty-nine VC firms in our sample participated in at least one blockbuster deal. Of the firms with blockbuster deals, their average age at first blockbuster deal was 5.42 years. The total number of blockbuster deals VCs in our sample participated in ranged from zero to six.

Control Variables

Structural holes

Prior research has suggested that the number of structural holes in a network can influence status and reputation (Burt, 2005). Following the prior literature, we operationalized structural holes as 1 minus network constraint. Network constraint for an actor i is defined using the following formula (Burt, 1992: 54):

where

IPO success ratio

Although our reputation measure captures the number of companies taken public and the number of companies funded over the prior five years, it does not directly capture the rate at which investments are converted into IPOs (Chang, 2004). The IPO success ratio was operationalized as the accumulated number of companies taken public divided by the accumulated number of companies invested in by a VC in the current year (Chang, 2004).

Industry diversification

Most VCs tend to specialize in one or a few industries (Lee, Pollock, and Jin, 2011), and a VC’s status and reputation may be influenced by the number of industries it invests in. VCs that invest in more industries can develop a greater range of ties to other VCs but may also have somewhat less industry-specific expertise and resources than more-focused VCs (Lee, Pollock, and Jin, 2011). We identified industry segments based on the Venture Economics Industry Classification (VEIC) codes of the start-ups funded, and we operationalized industry diversification using the entropy measure (Jacquemin and Berry, 1979) 7 :

where i indicates an industry segment and p is the portion of investment amount in industry segment i. This measure is bounded at zero, at which point a focal VC invests in only one industry, and increases with increasing industry diversification.

Early-stage preference

This variable captures the extent to which a VC invests in early-stage ventures. Whether a firm invests earlier or later in a start-up’s development could have consequences for its status and reputation. Early-stage investments tend to be smaller and riskier, so firms preferring to invest in early stages may develop fewer network ties than firms that invest in later rounds and join larger syndicates. Investment-stage preference can also affect a VC firm’s reputation. For example, early-stage investors may invest in more firms and raise smaller funds more frequently than firms that specialize in late-stage investments.

To determine investment-stage preference we collected information from the TBO database on a VC’s first investment (“company stage level 1”) in each company it funded. Company stage level 1 consists of Startup/Seed, Early Stage, Expansion, and Later Stage. We then constructed a continuous measure of early-stage specialization by dividing the number of first investments in Startup/Seed and Early Stage by the number of total investments. The greater the ratio, the more the VC prefers to invest in early stages.

Year dummies

Because a variety of factors that can influence status and reputation vary from year to year, we included a set of dummy variables coded 1 for each observation year in our sample (1990 is the omitted year) and zero otherwise. Because of the large number of variables, we do not report their effects in the tables, although they were included in all models.

We did not include time-constant control variables in our models because the statistical approach we employed automatically controls for these fixed effects by first differencing (Arellano, 2003), as we discuss next.

Model Specification and Estimation Strategy

We modeled the coevolutionary processes of status and reputation as a system of two interdependent structural equations:

where

This model incorporates three essential features. First, it conceptualizes the evolutionary processes of status and reputation accumulation as dynamic and path dependent (Podolny and Phillips, 1996; David, 2005), causing serial correlation of the error terms unless controlled for. Using the lagged dependent variable as an explanatory variable takes path dependence into consideration and addresses serial correlation stemming from persistence. The degrees of path dependence or persistence of status and reputation are reflected in

Although this model specification incorporating path dependence, simultaneity, and unobserved heterogeneity allowed us to test our theoretical arguments, each of these features introduced different kinds of endogeneity to the models. The lagged dependent variable is correlated with the error term (Greene, 2008), the simultaneity implicit in our model specification in which both causal effects are positive is likely to overestimate the simultaneously determined parameters (Greene, 2008), and unobserved heterogeneity is a source of endogeneity. While there are well-established econometric treatments for each source of endogeneity, it is difficult to address all three sources of endogeneity simultaneously.

We addressed this issue by employing the Arellano–Bond (AB) estimator (Arellano and Bond, 1991) using the xtabond2 command (Roodman, 2009) in STATA 11. The AB estimator addresses various kinds of endogeneity by instrumenting endogenous variables with predetermined as well as exogenous variables. The lagged terms of covariates can serve as valid instruments, given that they are predetermined and hence cannot be associated with the current error term, as long as error terms are not serially correlated (Arellano and Bond, 1991). The resulting estimates are robust against the kinds of endogeneity we faced. This estimator also addresses unobserved heterogeneity by first-differencing (Roodman, 2009), which is similar to the fixed-effects estimator; thus time-constant control variables are not required. 8 Taken together, the AB estimator addresses all three sources of endogeneity.

The AB estimator relies on the generalized method of moments (GMM) (Hansen, 1982). Although the system GMM estimator generates more efficient estimates (Blundell and Bond, 1998), we employed the AB difference GMM estimator because system GMM requires stationarity, or a steady state, for consistent estimation (Arellano, 2003). Given that our sample consists of relatively young firms, it is unlikely that the evolutionary processes of their status and reputation are close to a steady state, particularly in the early years. To control for heteroscedasticity, we report robust standard errors.

We followed the procedures recommended by Roodman (2009) to select the instruments for our models. Any predictor-variable value can theoretically be used as an instrument, but to correctly specify the lag structure it is important to consider whether a focal variable is strictly exogenous, predetermined, or endogenous (Arellano, 2003). If the variable is strictly exogenous, then all its lagging, current, and leading values can be valid instruments; if the variable is predetermined, its one-period or earlier lags can be valid instruments; and if the variable is endogenous, its two-period or earlier lags can be valid instruments. Because all our predictor variables except for the year dummies are potentially endogenous, we began selecting instruments using at least two-year lags. Then we determined whether each instrument (i.e., a two-year or earlier lag) met the orthogonality condition using Hansen’s J statistic and the difference-in-Sargan statistic, and whether it induced second-order autocorrelation using the AB statistic. We fine-tuned each variable’s lag structure using this procedure. Valid lag structures are empirically determined based on the sample (Roodman, 2009). Because we used a variety of samples—ten split samples for testing H1a, H1b, H3a, and H3b and the total sample for testing H2 and H4—we fine-tuned the lag structure for each sample used.

This process identified two generic lag structures: one for the older-firm (i.e., > 5 years, > 7 years, etc.) and total samples, and the other for the younger-firm (i.e., ≤ 5 years, ≤ 7 years, etc.) samples. All in all, for the older-firm and total samples we used five- and six-year lags of the lagged dependent variables and six- and seven-year lags of the jointly determined variables, three- and four-year lags for the rest of the endogenous variables, and all values of the year dummies. For the younger-firm samples we used one- and two-year lags of the lagged dependent variables (i.e., two- and three-year lags of the dependent variables) and two- and three-year lags of the jointly determined variables, two- and three-year lags for the rest of the endogenous variables, and all values of the year dummies. 9 We reconfirmed that the instruments as a group satisfied all the conditions required for statistical consistency. 10 The older-firm and total samples required longer lags because their later year values likely contain more of the firm’s past history; shorter lags are more likely to be correlated with the current error term (Roodman, 2009: 107).

To test H1a and H1b we compared the status and reputation coefficients across two models—one in which reputation predicted status and one in which status predicted reputation—and assessed whether the effects of reputation on status were different than the effects of status on reputation across different time periods. We employed the Wald χ2-test; the null hypothesis assumed the non-nested models’ parameter estimates are the same. The test statistic is:

This statistic follows a χ2 distribution with one degree of freedom (Greene, 2008) and requires not only each parameter estimate’s variance but also the covariance between them. Given that these two models are non-nested and thus estimated separately, this covariance is not automatically generated from the estimation of individual models.

To obtain this covariance, we followed the procedure recommended by Weesie (1999) and used the stack command in STATA to combine the two non-nested datasets into a single “stacked” dataset in which each set of the two non-nested but jointly determined observations (i.e., one from the status model and the other from the reputation model) was given the same identifier. This allowed us to cluster the two non-nested models and generate covariances using the xtabond2 command with the vce(cluster) option specified. The resulting variance–covariance matrix gave us the covariance of all the parameter estimates from the two non-nested models (Weesie, 1999). The parameter estimates generated by the stacked model were exactly the same as those generated by the individual models. For the Wald tests, we used the test command in STATA.

Results

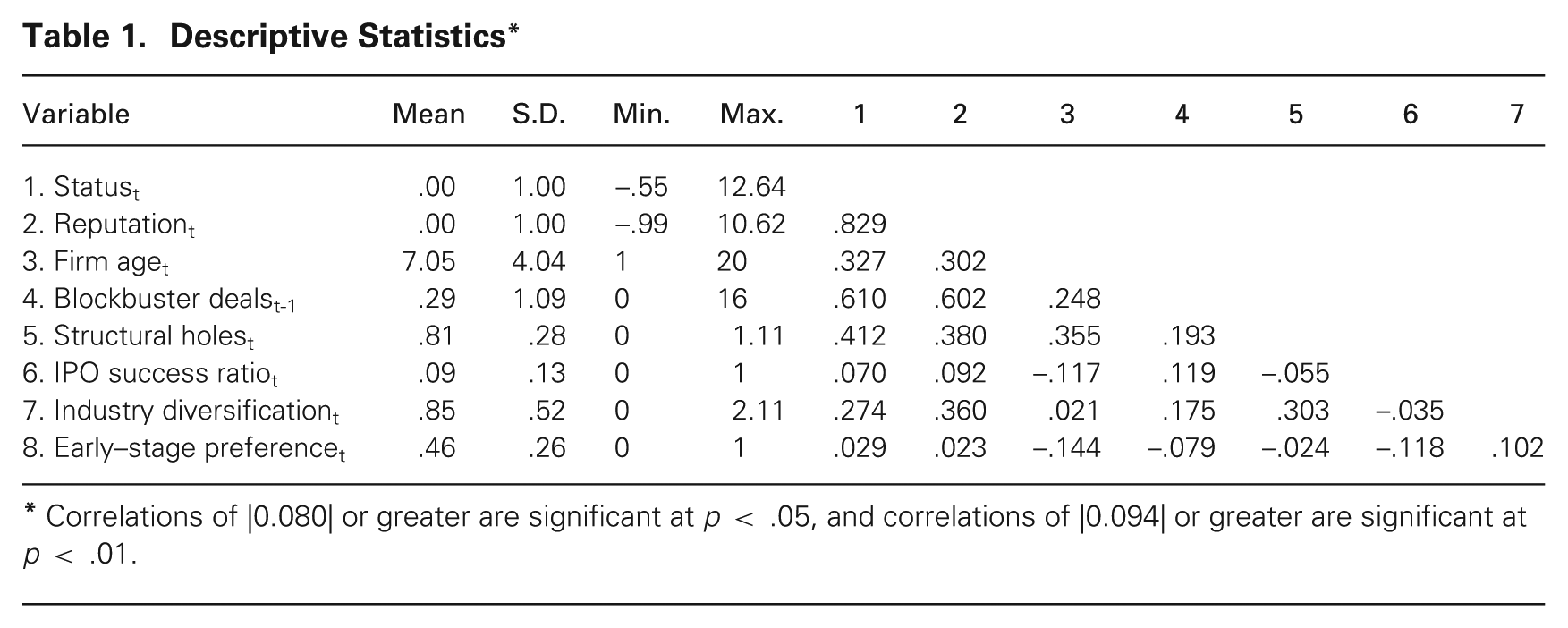

Table 1 presents the descriptive statistics and correlations for all the variables in our sample. Although the correlations between some variables are moderately high, VIF tests (mean VIF = 2.40, maximum VIF = 5.2) and the condition number (approximately 20 for all models) suggest collinearity is not an issue. In addition, the second-order autocorrelation test, AR(2), demonstrated no second-order autocorrelation of residuals in any model. Hansen’s J statistic for over-identifying restrictions also is not significant in any model. This indicates that the instruments our models used were all valid as a group, and the difference-in-Hansen statistic confirmed that each instrument group was valid.

Descriptive Statistics*

Correlations of |0.080| or greater are significant at p < .05, and correlations of |0.094| or greater are significant at p < .01.

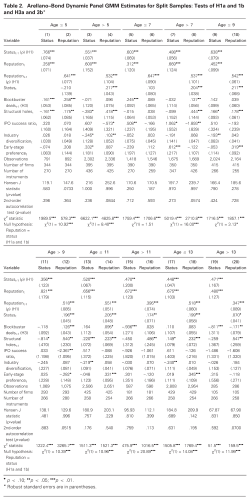

Table 2 presents the results of our analyses testing H1a, H1b, H3a, and H3b, and table 3 presents the analyses testing H2 and H4. The results in table 3 support our baseline expectation that reputation and status will coevolve. Reputation and status are positively and significantly related to each other in all models in table 3. Using the results in models 1 and 2 to assess their respective effect sizes, a 5-percent increase in reputation and status leads to 3.2-percent and 0.95-percent increases in status and reputation, respectively, holding all else fixed. Thus the effect of reputation on status appears to be greater than that of status on reputation. A Wald χ2-test (p < .01) confirmed that the effect of reputation on status is significantly larger than that of status on reputation in our models.

Arellano–Bond Dynamic Panel GMM Estimates for Split Samples: Tests of H1a and 1b and H3a and 3b*

p < .10;

Robust standard errors are in parentheses.

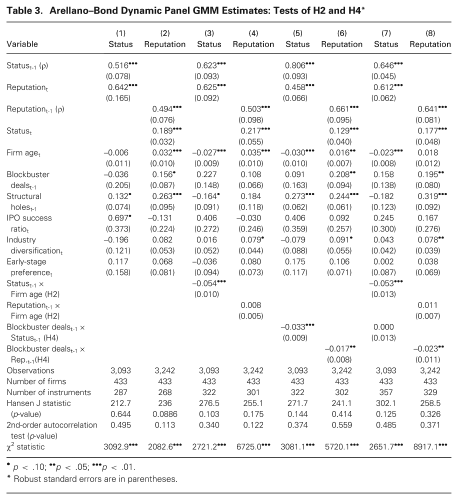

Arellano–Bond Dynamic Panel GMM Estimates: Tests of H2 and H4*

p < .10;

Robust standard errors are in parentheses.

H1a, H1b, and H2 explored how the relationships between status and reputation, as well as the relationships between past status (or reputation) and current status (or reputation) changed as a firm aged. H1a argued that reputation would have a greater effect on status than status would have on reputation when firms are young, while H1b argued that status would have a greater effect on reputation than reputation would have on status when firms are older. To test these hypotheses we ran a series of regressions splitting the sample into subsamples based on different age increments, presented in table 2. To have enough observations to conduct meaningful tests we began with firms less than or equal to, and firms greater than, five years of age, and we increased the lower age break by two years in each regression. Our analysis shows that reputation has a positive and significant relationship with status in all models, but status does not have a significant relationship with reputation until VC firms are nine years old. The bottom row of the table shows the results of tests comparing the coefficients. Although reputation has a larger coefficient in all models and status is not statistically significant in some models predicting reputation, the difference in coefficient size is statistically significant only for firms 11 or more years old. Thus H1a is partially supported and H1b is not supported.

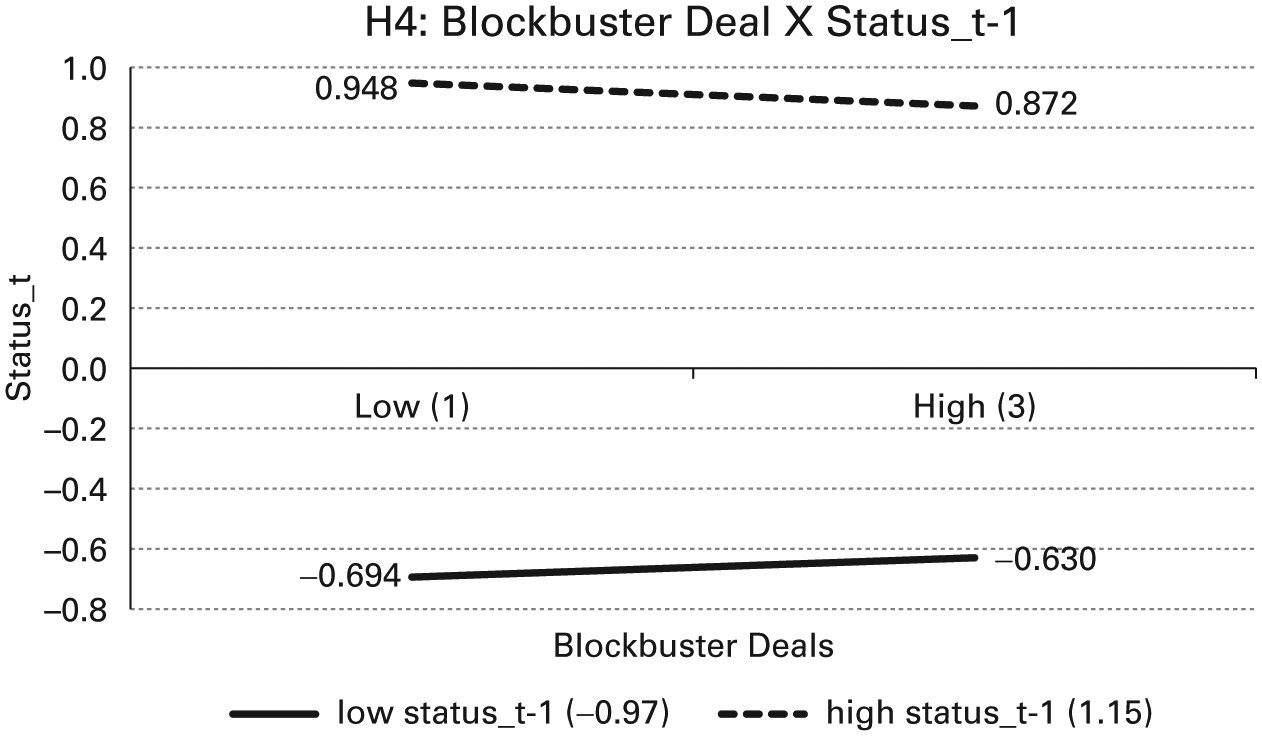

H2 argued that firm age would weaken the relationship between changes in prior and current status but would not affect the relationship between changes in prior and current reputation. The results in models 3 and 4 of table 3 support this hypothesis. The interaction between age and prior status is negative and significant (p < .001), but the interaction between prior reputation and age is not significant. As discussed above, the lagged dependent variable’s coefficient reflects the degree of persistence or path dependence of the evolutionary process (Arellano, 2003). Thus the results in models 3 and 4 indicate that 62.3 percent of status and 50.3 percent of reputation in year t–1 persist in year t, holding other factors fixed, suggesting the evolutionary process of status exhibits a greater persistence (or path dependence) than that of reputation. The coefficient for the interaction between age and prior status suggests that the effect of prior status decreases by 5.4 percent each year as the VC firm ages.

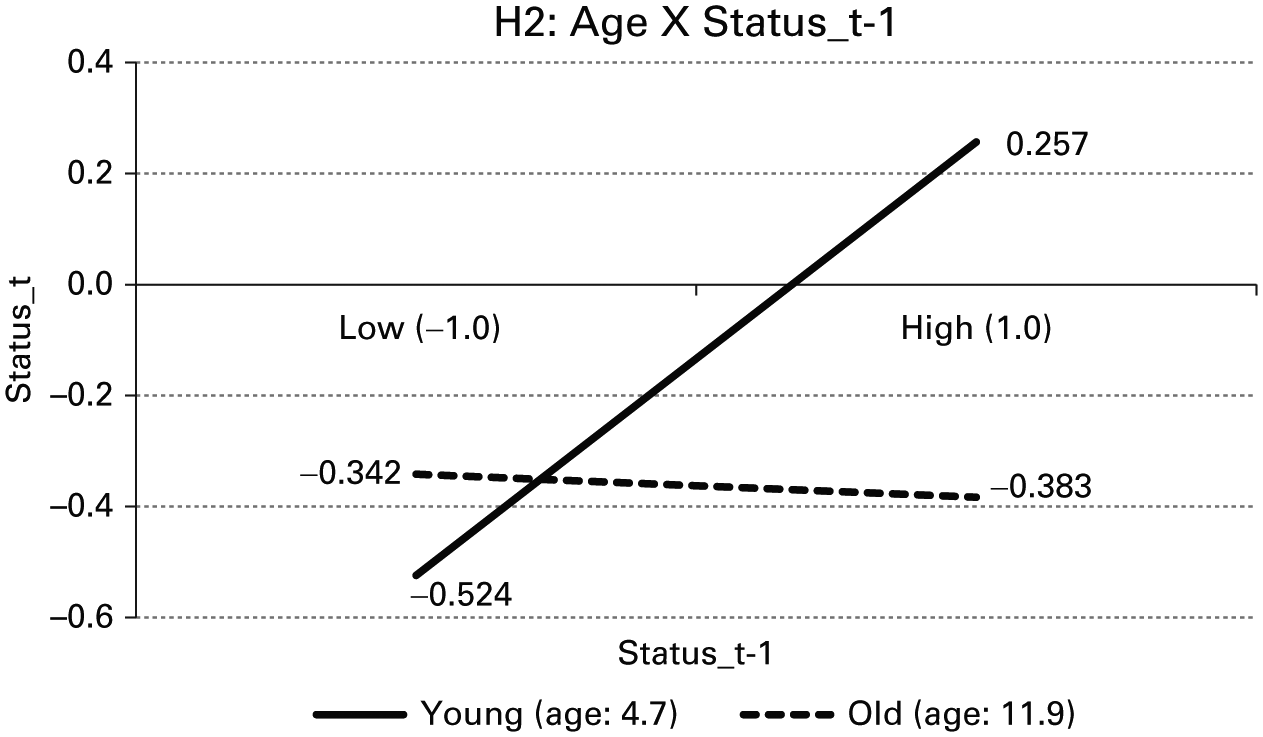

To gain a better understanding of this relationship we graphed the interaction in figure 1 using values one standard deviation above and below the mean for each variable. The effect of prior status on current status (i.e., path dependence) is 0.392 for young firms (about five years old) and is reduced to −0.020 for the older firms (about 12 years old). Thus the effect of changes in prior status on changes in current status (i.e., path dependence) becomes weaker as firms age.

Interaction of age and the past status on the current status.

We conducted a set of power analyses to ensure that the non-significant interaction between age and prior reputation was not due to low statistical power. As our models use the GMM estimation technique, we could not tap the well-established power-analysis procedure employed with ordinary least squares (OLS) regressions (Cohen, 1988). Instead, we conducted multiple Monte Carlo simulations to estimate the statistical power of our model (Feiveson, 2002), using a significance level of .05 and 1,000 iterations. According to the simulation results, our models’ average power was .91, suggesting they have sufficient power to detect even small effect sizes. 11 Thus we can safely conclude that the non-significant finding from our model estimates does not come from a type II error but from a negligible interaction effect.

H3a and H3b argued that participating in blockbuster deals positively affects both reputation and status when VC firms are young but will affect only reputation when VC firms are older. Because there is no theoretical reason to determine a specific break point, we tested this hypothesis using the results in table 2, which presents the relationships over a range of years. The results show that (1) the number of blockbuster deals has a positive and significant relationship with status for VC firms 7 years old and younger, (2) this relationship becomes non-significant when VC firms 8 to 10 years old are included, and (3) this relationship is negative and significant for VC firms more than 11 years old. The results for reputation show that the number of blockbuster deals has a positive and significant relationship with reputation when VC firms 10 to 13 years old are included, and the relationship becomes non-significant for VC firms more than 13 years old.

These results support H3a for status but not reputation and partially support H3b for reputation but not status. The negative, significant relationship between blockbuster deals and status for VC firms 13 years or older is surprising and suggests that participation in blockbuster deals could have negative consequences for older VCs. But the findings for firms 11 and 13 years old and older, as well as for firms less than or equal to 5 years old, must be interpreted with some caution. The sample sizes for these models are much smaller than for the other time periods. AB models provide less consistent estimates when samples sizes are small. If the small N models are disregarded, the results in the models with the largest Ns (VCs greater than 5, 7, and 9 years old) suggest there is a positive and significant relationship between blockbuster deals and reputation and a non-significant relationship between blockbuster deals and status, consistent with H3b.

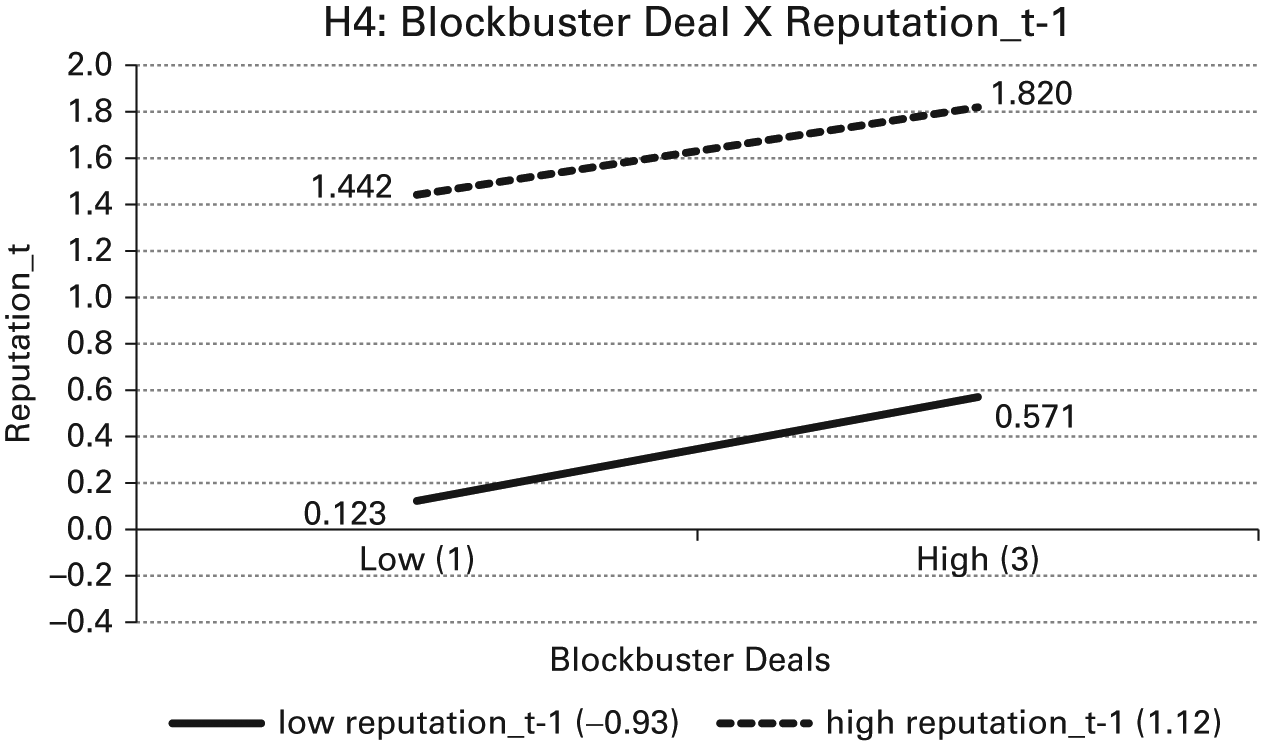

H4 argued that the relationship between blockbuster deals, status, and reputation would be stronger for lower-reputation and lower-status VC firms than for higher-reputation and higher-status firms. Models 5–8 in table 3 test this hypothesis. The interaction between blockbuster deals and prior reputation is negative and significant in both models 6 (p < .05) and 8 (p < .05), providing support for H4 for reputation. The interaction between prior status and blockbuster deals is negative and significant (p < .001) in model 5 but is not statistically significant in the fully specified model. Thus H4 is partially supported for status.

Figures 2 and 3 graph the significant interactions from models 5 and 6 for values one standard deviation above and below the mean for past status and reputation and for one and three blockbuster deals. We used different values for blockbuster deals because one standard deviation below the mean becomes a negative value, which has no practical meaning. Figure 2 shows that the effect of blockbuster deals on current status is 0.032 for each blockbuster when prior status is low, while it is −0.038 for VC firms whose prior status is high. Similarly, figure 3 shows that the effect of blockbuster deals on current reputation is 0.224 for each blockbuster when prior reputation is low, while it is 0.189 for VC firms whose prior reputation is high. The figures show that participation in blockbuster deals appears to have a stronger effect on reputation than on status, as the slopes of the lines in the reputation graph are steeper than in the status graph. Further, participation in blockbuster deals appears to have a slightly negative relationship with subsequent status for high-status VCs.

Interaction of blockbuster deals and the past status on the current status.

Interaction of blockbuster deals and the past reputation on the current reputation.

Robustness Tests

Three-stage least squares

Three-stage least squares (3SLS) extends 2SLS to a system of equations by incorporating the estimation feature of seemingly unrelated regression models. One possible benefit of using 3SLS instead of the AB estimator is a potential efficiency gain. This comes at a substantial cost, however, because 3SLS cannot address the bias stemming from the lagged dependent variables. Given that consistency generally takes priority over efficiency, the AB estimator is more appropriate for our analysis. Nonetheless, we re-ran our models using 3SLS and included firm dummies to deal with unobserved heterogeneity. Given the paucity of available instruments, we assumed that one-year lags of all covariates except for the simultaneously determined variables (reputation/status) are exogenous. The pattern of results was the same as reported here, but the coefficients of the lagged dependent variables were quite inflated when compared with our AB results, and the model R2s were excessively high (approximately .97). Given that 3SLS does not control for the bias caused by lagged dependent variables, this was not surprising. Further analysis using single-equation 2SLS found the results were almost the same as those from 3SLS, indicating there was little efficiency gain from using 3SLS and further supporting our use of the AB estimator.

Non-linear effects of blockbuster deals

We also conducted additional analyses to assess whether blockbuster deals might have non-linear relationships with status and reputation. First, we added a squared blockbuster deals term to our full sample model. For status, the relationship was indeed curvilinear, but the inflection point was about six blockbuster deals, which is the top of our data range. Including the squared term in our age models yielded a similar pattern of results. Thus the relationship is most conservatively interpreted as positive but diminishing. In contrast, the squared term was not significant when predicting reputation. The results were similar in our age models with the exception of the ≤ and > 9 year models, in which the term was negative and significant. So the conservative interpretation is that the relationship between blockbuster deals and VC reputation is linear.

As an alternative approach, we created a spline capturing the first, second, and third blockbuster deals. Each variable took on a value of zero until that blockbuster number had been reached and then had the value 1, 2, or 3, respectively, every year thereafter. For status, the terms for one and two blockbusters were significant, and the term for the second blockbuster was significantly larger than for the first blockbuster deal, which is consistent with our other findings. For reputation, only the second blockbuster deal was significant.

Discussion

In this study we explored how status and reputation coevolve, and we examined the nuances of this relationship by considering how it changes over time and the effects of participating in significant, highly visible events. We examined these issues using data on newly founded VC firms and discovered that although status and reputation positively influence each other as they coevolve, their influence is not equivalent and changes over time. We also found that status and reputation are influenced in different ways by their prior levels as they age and by participation in big hits. These findings provide both theoretical and practical insights.

Age and Asymmetric Influence

Though reputation and status coevolve in a mutually beneficial way, reputation precedes status in their abilities to enhance each other and appears to have a greater influence on status than status has on reputation in more mature firms. These findings are theoretically important because they offer a basis for assessing which intangible asset has more value, particularly in the early stages of an organization’s life. Given that untangling reputation and status has been a central theoretical and empirical challenge (Barron and Rolfe, 2012), this finding is important because it suggests when in a firm’s life these two constructs are likely to be different from one another, increasing scholars’ abilities to determine which asset may be influencing other outcomes of interest.

Our findings also provide insights into how young firms should allocate their scarce resources and attention to build reputation and status. Overall success could suffer if they focus on building the wrong intangible asset at the wrong stage of development. While it is important to form relationships with high-status others (Benjamin and Podolny, 1999), it is even more critical to develop a record of performance that builds a solid reputation early in the firm’s life (Rindova, Petkova, and Kotha, 2007; Hallen, 2008). A good, early reputation enhances status, and the two continue to evolve in a dynamic, mutually beneficial way that allows the firm to later reap the rewards of both status and reputation. New VC firms that spend more time courting high-status VCs than they do developing their portfolio firms may not perform as well and are more likely to develop a poorer reputation among start-ups.

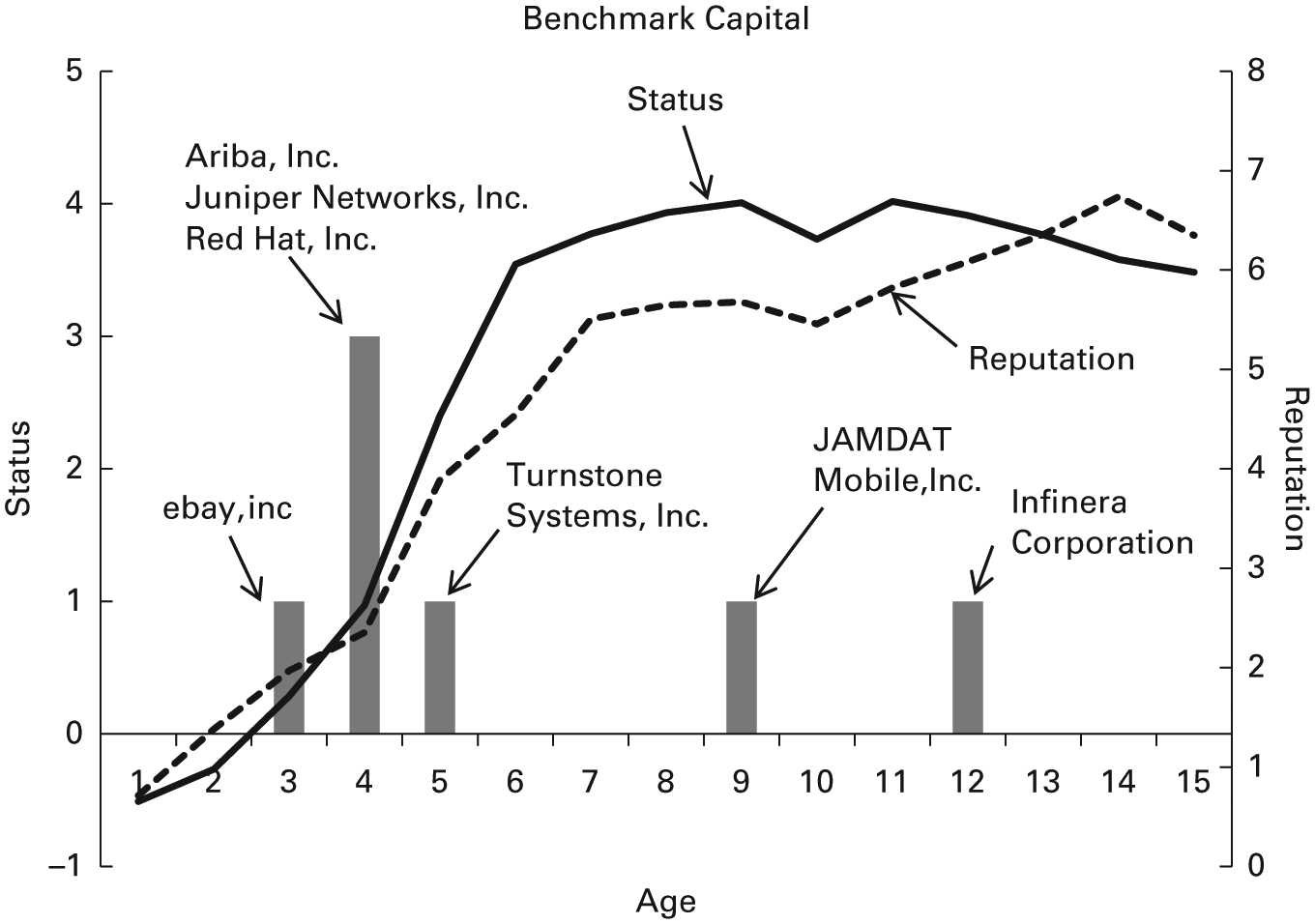

Benchmark Capital’s early days (Fund et al., 2008) provide a useful illustration of the relationships we identified. Benchmark was founded in 1995 by three well-regarded—but not star—VCs and a software entrepreneur with no VC experience. A fifth partner, an experienced executive recruiter with no VC experience, was brought on shortly after founding. After raising its first fund, Benchmark rapidly invested in a number of companies, including a couple of second-round investments in companies funded by their former firms (which had disbanded) and other new, seed-stage deals. Although they lost out to more-established VCs on many early deals, they worked hard to provide unparalleled levels of support to their start-ups and aggressively built ties with more prominent VCs. The reputation it developed led eBay to choose Benchmark as its primary VC investor, and Benchmark is largely credited with helping eBay recruit Meg Whitman to become its CEO (Stross, 2000). When eBay’s IPO exploded, Benchmark used the event to enhance both its status and reputation with institutional investors, start-ups, and other VCs, and it is now considered among the top VC firms in Silicon Valley.

Our results also suggest that though the relationship between changes in prior and current status weakens as a firm matures, the relationship between changes in prior and current reputation is unaffected by firm age. Thus our results are consistent with prior research arguing that status is “stickier” than reputation (Gould, 2002; Washington and Zajac, 2005), but they offer a more complex understanding of how this stickiness occurs, at least for young firms. Prior research has suggested that status homophily and stable deference patterns lead to stability in status orders (Merton, 1968; Gould, 2002). But our findings suggest that for young firms, a strong reputation also enhances the stickiness of status. Even as the relationship between prior and current status weakens, the relationship between reputation and status remains largely stable. Thus investing in a firm’s reputation indirectly helps reinforce its standing in the status order. Future research should continue to explore this relationship and assess whether investments in reputation can ultimately yield greater benefits than direct investments in maintaining status.

The Effects of Big Hits

We also provide insights into how involvement in big hits (Denrell and Fang, 2010) can affect the developmental courses of status and reputation. Our findings suggest these events are more beneficial for enhancing status than reputation when VC firms are young but are more beneficial for enhancing reputation than status when VC firms are older. Figure 4, which maps Benchmark Capital’s blockbuster deals onto the trajectory of its status and reputation over time, is illustrative of our findings. Benchmark experienced its most significant gains in status and reputation following its blockbuster deals of 1998 (eBay), 1999 (Ariba, Juniper Networks, and Red Hat), and 2000 (Turnstone Networks). It saw smaller increases after its 2004 (JAMDAT Mobile) and 2007 (Infinera) blockbuster deals. Further, the slope of the status line appears to be a bit steeper in the early years, while reputation appears to have a slightly steeper slope in the later years and continues to increase even as status declines slightly.

Benchmark’s blockbuster deals and the trajectory of its status and reputation.

One possible interpretation of our findings is that blockbuster deals have a greater effect on status because the associated attention and visibility they provide speed up the enhancement of a firm’s cognitive centrality (Bunderson, 2003; Fund et al., 2008) among VCs, and thus its status. In contrast, because it takes time to establish a track record of performance, blockbuster deals’ visibility and attention have less influence on reputation until the necessary performance record is established. Our finding that the effect of blockbuster deals becomes significant around 11 years of age—when the performance of the VC’s first venture fund is known—supports this interpretation.

Our results also show that participating in blockbuster deals yields greater benefits for low-status and low-reputation VCs. Blockbuster deals that create substantial buzz (Pollock and Gulati, 2007) can help low-reputation firms enhance their reputations more quickly because they are more surprising and have greater signaling value than for high-reputation firms. Our results also suggest that low-status firms can derive some benefit from participating in blockbuster deals, allowing them to build their status more rapidly. Prior research has found that status can take a long time to build (Podolny, 2005; Washington and Zajac, 2005). Thus we contribute to the conversation on building status by demonstrating that big hits can reduce the amount of time it takes for a firm to enhance its status.

We also add to theorizing about the Matthew effect (Merton, 1968). Merton argued that high-status scientists will get more credit for a new idea or finding than a low-status scientist who discovers the same thing. He did not argue, however, that the high-status scientist’s status would be increased. Indeed, as Merton was focusing on the highest-status scientists, it was not possible for their status to become greater. One thing Merton did not consider is whether the lower-status scientists still benefited from the discovery. They may not get as much credit, but unless they get no credit their status is likely to improve somewhat, and the relative increase could be greater than any relative increase higher-status actors may experience. For example, although top-tier VC firms like Accel Partners and Greylock Partners may have received more acclaim for their investments in Facebook, VC firm Elevation Partners, founded in 2004, may have gained the most. The website WhoownsFacebook.com (2012) noted, “Once pilloried with the moniker ‘world’s dumbest VC investor,’ Elevation Partners may shut up some of its critics” as its 1.5 percent stake was valued at nearly $1.3 billion.

Our results also provide some evidence that participation in blockbuster deals can have a negative effect on status for older firms and high-status VCs. The moderating effect of prior status was small, so any inferences should be treated as speculative, but one interpretation of this finding is that when high-status VCs participate in more blockbuster deals they may feel less need to syndicate future deals with other high-status actors, who will demand greater equity participation and also want to have a larger say in how the start-ups are managed. Rather, they may handle deals by themselves or include more low-status VCs that will defer to the higher-status VC (Gould, 2002; Castellucci and Ertug, 2010), be less likely to challenge its leadership (Ma, Rhee, and Yang, 2013), and be more likely to accept lower levels of equity participation (Hsu, 2004). This interpretation is consistent with Fund and colleagues’ (2008) observation that new VC firms Benchmark Capital and August Capital participated in syndicates with the most central VCs less frequently as they became more central in industry deal networks.

Our post-hoc analysis, however, indicated that what we might instead be observing is a non-linear relationship between blockbuster deals and VC status. The results of this analysis showed that the benefits of blockbuster deals taper off as a firm has more of them. It may be that once a firm has had more than two blockbuster deals, thereby verifying that the first blockbuster deal was not a fluke, additional blockbuster deals are less surprising (Anderson, 1981), provide little new information, and do not add to a firm’s cognitive centrality (Bunderson, 2003). Future research should continue to explore these non-linear effects.

In general, we believe that our study makes several contributions to our understanding of status and reputation. We have long known that status and reputation are related constructs, and our findings enhance our understanding of the nature of this relationship. For instance, there is evidence that status is often used to make inferences about reputation (Bowles and Gintis, 1976; Camic, 1992) and that status can motivate firms to behave in ways that build their reputation to reflect their status (Benjamin and Podolny, 1999). These studies either look at status and reputation at the individual level or focus on more mature firms. We extend this work by demonstrating that for young firms, reputation generally precedes status. But if a firm is involved in a big hit, that firm’s status can receive a boost.

Limitations and Future Research

As with all studies, our study has several limitations that provide opportunities for future research. One opportunity arises from our decision to consider only venture capital firms that were formed during a period of significant industry expansion. Though VC firms have a number of useful characteristics, our findings may not generalize to firms in other industries or to other eras. Future research should continue to investigate how the relationships between reputation and status coevolve in other industries and contexts, such as those in which status hierarchies are more difficult to ascertain; those like sports or entertainment, in which reputation and status can play an outsized role on outcomes; and those such as pharmaceuticals and high technology that also rely heavily on big hits.

A second limitation is that although we were able to obtain unique measures of reputation and status for VC firms, we were limited in the other types of data we could obtain. This creates two potential issues. First, whereas our reputation measure is composed of five items, status is composed of a single item, Bonacich beta centrality. Thus it is possible that status may be subject to more measurement error. But theoretical conceptions of status do not have the same dimensionality issues as reputation, and the status measure we used has been employed in status research for over 20 years (e.g., Podolny, 1993, 2001; Benjamin and Podolny, 1999; Hallen, 2008; Ma, Rhee, and Yang, 2013). Though it would be ideal to create a multi-item measure of VC status, we are unaware of any data that could be used and cover the same 20-year time period. Future research in other contexts that allow for the creation of multi-item status measures should continue to explore these relationships and assess whether measurement error is an issue.

Second, although we theoretically and empirically treat the effects of reputation and status on each other as contemporaneous, it may be possible that some components of our measure may experience greater lagged effects than others, though analyses not reported here supported treating reputation and status as contemporaneous, and as noted earlier, any such effects would likely serve to make our measure a more conservative test of our arguments.

A third limitation is that we were unable to consider other factors that could affect status and reputation. We considered how firm age moderated the basic relationships between status and reputation and prior and current status/reputation. We also considered how prior status and reputation moderated the relationship between participation in blockbuster deals and current status and reputation. But factors such as the availability of other resources, levels of innovativeness, or management team characteristics could all moderate the relationships that we were interested in. Future research in other contexts in which data on such factors are available can continue to explore these issues and identify more boundary conditions that shape these relationships.

A related limitation is that though our reputation measure has many positive characteristics, it is not a direct measure of stakeholders’ perceptions. Rather, it is composed of multiple objective indicators expected to influence stakeholders’ perceptions. Many prior studies of VC reputation have used various components of our index as indicators of VC reputation (e.g., Gompers, 1996; Lee and Wahal, 2004), and Lee and colleagues (2011) took steps to assess the face validity of their reputation index. And although no long-term perceptual measure of VC reputation exists, a recent study (Hallen and Pahnke, 2015) using a perceptual VC reputation measure collected over a shorter time period corroborates the efficacy of our objective measure.

Further, a number of the index’s components can be related to size. Size is a theoretically problematic construct, however, because it lacks discriminant validity and is correlated with a variety of other constructs (Kimberly, 1976), making it useful as an omnibus control variable—and a crude proxy for reputation (Lee and Wahal, 2004)—but difficult to use as the basis for an alternative theoretical argument. Lee and colleagues (2011) also conducted extensive robustness tests of the index’s individual components and found not only that no one component of the measure was driving their findings but also that the component of their index most indicative of size, the total assets under management, was the only variable that had a significant relationship with just one of their two dependent variables. Future research should continue to explore, or attempt to develop, other measures of VC reputation, perhaps based on direct stakeholder surveys (e.g., Dowling and Gardberg, 2012).