Abstract

In nascent industries―whose new technologies are often poorly understood by regulators―contending with regulatory uncertainty can be crucial to organizational survival and growth. Prior research on nonmarket strategy has largely focused on established firms in mature industries, but such strategies are apt to differ for new ventures, which generally have limited resources and market power and operate in novel domains in which the rules of the game are underdeveloped. How do new ventures navigate regulatory uncertainty? To explore this question, we conduct an inductive, multi-case research study of five ventures that pioneered the nascent personal-genomics industry. Drawing on extensive qualitative data, we develop an emergent theoretical framework that elucidates how ventures navigate evolving regulatory uncertainty. Grounded in a power versus industry-evolution logic, this framework illuminates how ventures’ strategies for doing so vary and theorizes why certain strategies appear more effective than others. In doing so, we also introduce a novel logic of interaction—regulatory co-creation—that ventures can employ to shape emerging regulations. Taken together, our theory and findings challenge existing perspectives on strategy in nascent industries, shed light on the dynamic interplay between market and nonmarket strategy, and recast the relationship between ventures and regulators during the emergence of new technology industries.

Keywords

In 2015, a Washington, DC-area resident lost control of his store-bought drone and crash-landed it on the White House lawn. The incident triggered an immediate lockdown at the presidential mansion and aimed an unwelcome spotlight at a fledgling industry: enthusiasts had welcomed the advent of consumer drone technology, but critics were now voicing growing alarm about a variety of issues, including safety and privacy. The Federal Aviation Authority (FAA) faced difficult questions about how to regulate such devices. Should drones be treated as toys or as aircraft? Should they require a pilot’s license? In turn, this highly uncertain regulatory environment, lacking pertinent precedents, tested the resolve of innovators eager to exploit a new business opportunity. The case of consumer drones is not unique. A steady stream of emerging innovations—from autonomous vehicles to gene editing to lab-grown meat substitutes—suggests that similar challenges will keep arising for the foreseeable future. Understanding how new ventures cope effectively with the regulatory uncertainty that so often accompanies industry emergence is important for both scholars and executives.

A growing body of research has examined nascent industries. A key theme is the extreme uncertainty that prevails in such industries and the difficulties it creates for managers (Benner and Tripsas, 2012). Nascent industries are plagued by imperfect information in the forms of fuzzy product and category definitions (Hargadon and Douglas, 2001; Hsu and Grodal, 2021), unclear market structures (Adner and Kapoor, 2010), shifting technologies (Tushman and Anderson, 1986), ill-defined customers (Santos and Eisenhardt, 2009), and misleading or missing information about business opportunities and risks (Gavetti and Rivkin, 2007; Moeen and Agarwal, 2017). In the context of these uncertainties, variations in product class or technologies compete for dominance via a complex interplay between economic and sociopolitical dynamics (Tushman and Rosenkopf, 1992).

To document this interplay, scholars have examined how ventures seek to overcome market uncertainty (particularly unknowns about customers and the offerings they will value) as well as resource uncertainty. This work has pinpointed several organizational strategies for experimentation and learning—probing (Brown and Eisenhardt, 1997), testing (Murray and Tripsas, 2004), continuous morphing (Rindova and Kotha, 2001), improvising (Davis, Eisenhardt, and Bingham, 2009), and pivoting (McDonald and Gao, 2019)―that enable ventures to adapt flexibly to uncertain, changing environments. It has also specified the influence processes by which entrepreneurs gain resource providers’ support despite skepticism about a new industry’s viability (Lounsbury and Glynn, 2001, 2019; Zott and Huy, 2007). Curiously, this work has devoted less attention to strategies for managing regulatory uncertainty, despite the enduring salience of regulators in these contexts (Tushman and Rosenkopf, 1992; Funk and Hirschman, 2014; Pollman and Barry, 2017). As Aldrich and Fiol (1994: 661) pointed out over 25 years ago, “government regulatory agencies have shown considerable resistance to new industries whose activities challenge an older industry but which use unfamiliar or novel technologies.”

Research on nonmarket strategy does explore the antecedents and consequences of corporate political activities like lobbying, campaign contributions, and political connections (Hillman and Hitt, 1999; Siegel, 2007; Ahuja and Yayavaram, 2011; Dorobantu, Kaul, and Zelner, 2017) and thus broadly considers how firms influence regulatory entities to gain advantage (Baron, 1995). Larger and more diversified firms engage in more political activity (Hillman, Keim, and Schuler, 2004), and efficacy hinges on co-opting, managing, or reducing dependence on powerful government actors (Pfeffer and Salancik, 1978; Hillman, 2005; Shi, Gao, and Aguilera, 2021). Yet these insights may have limited pertinence to new ventures: nonmarket strategy studies have focused primarily on established firms operating in mature industries, such as electric utilities (Bonardi, Holburn, and Vanden Bergh, 2006), defense (Kim, 2019), financial services (Yue, Luo, and Ingram, 2013), and telecommunications (de Figueiredo and Tiller, 2001)―industries subject to well-established laws and guidelines that are clear to market participants (Edelman and Suchman, 1997) and in which the rules of the game are already fixed and known (Hillman and Hitt, 1999). Regulations in nascent industries, by contrast, are typically underdeveloped, malleable, and in flux (Lee, Hiatt, and Lounsbury, 2017; Grandy and Hiatt, 2020). And unlike large, established firms, new ventures typically have limited resources and market power (Fisher, Kotha, and Lahiri, 2016; Katila et al., 2022) and may be unable to wield traditional tools of nonmarket influence. “Bigger companies have the capital and the clout to build lobbying muscle and develop relationships with government officials,” noted an experienced venture capitalist (Tunguz, 2022). In short, conventional nonmarket-strategy theories may tell us little about regulatory strategies for new ventures in nascent industries.

An emerging stream of research at the intersection of entrepreneurship and nonmarket strategy has hinted that regulatory agencies are susceptible to influence. This work has begun to examine how resource-constrained new ventures can engage regulators, focusing on methods aimed at influencing regulators indirectly through their key stakeholders, such as peer agencies (Hiatt and Park, 2013) and consumers (Ozcan and Gurses, 2018). Such strategic actions primarily focus on soft-power communication tactics (such as claims-making and framing) for indirectly influencing regulators (Gurses and Ozcan, 2015). Meanwhile, from a practitioner angle, entrepreneurs and the popular media have deployed swaggering catchphrases like “move fast and break things” and “it is better to beg forgiveness than to ask for permission” (Pollman and Barry, 2017: 446, 398), as well as narratives glorifying startups that ignore regulators (Tusk, 2018). Such possibilities and provocations notwithstanding, we lack systematic understanding of how entrepreneurs strategize in the face of regulatory uncertainty, particularly regarding direct engagement with regulators. Also, a process perspective on strategies for engaging with regulators over time could advance our understanding of the dynamics of new-venture strategy for navigating nascent industries.

This article aims to develop new theory on ventures’ regulatory strategies by asking: how do new ventures vary in their strategies for navigating regulatory uncertainty, and which strategies appear more effective in a nascent-industry context? Given limited theory on this topic, we conduct an inductive, multi-case study of the five ventures that launched the direct-to-consumer (DTC) genetic-testing industry popularly known as “personal genomics.” Using archival data, field observations, and 91 interviews with firm executives, stakeholders, and regulators, we develop a novel theoretical framework that traces the evolution of regulatory uncertainty in a nascent industry and the processes that ventures adopt to navigate and shape it. Taken together, our theory sheds new light on the complex sociopolitical dynamics of nascent industries as ventures and regulatory agencies interact to create the future.

Theoretical Background: Managing Uncertainty in Nascent Industries

Nascent industries are business environments at “an early stage of formation” (Santos and Eisenhardt, 2009: 644), when a handful of firms typically begin developing “category-defying products and services based on new technologies, regulatory environments, or ideas about consumer demands” (Zuzul and Edmondson, 2017: 303–304). As incubators for entrepreneurship and innovation (Moeen, Agarwal, and Shah, 2020), such industries, and the products and services that spur their creation, can dispel market gaps, reimagine existing capabilities, and create new opportunity spaces for economic growth (McDonald and Eisenhardt, 2020).

But nascent industries can be challenging environments to compete in, due to the uncertainty associated with them (Sine, Haveman, and Tolbert, 2005; Navis and Glynn, 2010). Technological uncertainty prevails, in particular, during the “fuzzy front end” of an industry’s evolution (Abernathy and Utterback, 1978; Benner, 2010; Eggers, 2012; Suarez, Grodal, and Gotsopoulos, 2015: 438; Schilling, 2017), when technologies and product-class variants vie for dominance, as “manufacturers, suppliers, customers, and regulatory agencies compete to decrease the uncertainty associated with variation during the era of ferment” (Anderson and Tushman, 1990: 614). Amid the fog, executives have limited information with which to assess business opportunities and risks; during strategy formulation, their ventures are often restricted to haphazard or path-dependent search mechanisms (Gavetti and Levinthal, 2000; Beckman and Burton, 2008; Zuzul and Tripsas, 2020). Market uncertainty also prevails, characterized by shifting industry boundaries (Grodal, 2018), unclear products and categories (Hargadon and Douglas, 2001), ambiguous customer preferences (Raffaelli, 2019), divergent stakeholder expectations (Benner and Ranganathan, 2013), and scant information about opportunities and demand (Anthony, Nelson, and Tripsas, 2016).

In light of these challenges, a growing body of research investigates how ventures overcome uncertainty to compete in nascent industries. One strand, which examines how entrepreneurs employ experimentation and learning to adapt and compete, has identified several flexible organizational processes. For example, low-cost probes of the future via experimental products (Brown and Eisenhardt, 1997), strategic switchbacks (Marx and Hsu, 2015), and pivoting (Hampel, Tracey, and Weber, 2020) enable ventures to keep up with rapidly evolving new technology domains (DeSantola and Gulati, 2017; Snihur and Zott, 2020). A key insight is that the timing and sequence of actions may be just as important as their content. Another strand of research looks at how entrepreneurs address resource uncertainty by convincing stakeholders to provide what they need to compete (Clough et al., 2019). Symbolic actions, such as crafting resonant stories (Lounsbury and Glynn, 2001, 2019), projecting and managing frames (McDonald and Gao, 2019), and leveraging cultural toolkits (Weber, Heinze, and DeSoucey, 2008; Kellogg, 2011; Granqvist, Grodal, and Woolley, 2013), and persuasive activities like affiliating with known product domains (Wry, Lounsbury, and Jennings, 2014) and signaling around tangible “proof-points” (Hallen and Eisenhardt, 2012) can help ventures gain legitimacy and amass financial capital, advice, and positive external perceptions (Rindova and Petkova, 2007; Pahnke, Katila, and Eisenhardt, 2015; Gehman and Soublière, 2017). Symbolic actions can yield material economic benefits as constrained entrepreneurs leverage such economizing strategies to attain desired resources and support (Zott and Huy, 2007).

Research on nascent industries thus emphasizes efficient, flexible organizational processes for addressing market or resource uncertainty, but it does not address strategies explicitly aimed at managing regulatory uncertainty, even though technological discontinuities often render rules and regulations outdated (Kaplan and Tripsas, 2008; Funk and Hirschman, 2014; Khanna, 2018). As Aldrich and Fiol (1994: 661) pointed out, “new industries whose activities and long-term consequences are not well understood may have trouble in winning approval from cautious government agencies.” Regulators differ from market actors in that they are driven not by profit or efficiency logics but by preoccupations unique to their public-oriented mission, such as risk aversion and a mandate to protect public safety (Hiatt and Park, 2013).

Nonmarket-strategy research, though not specific to nascent industries, examines efforts to influence political and regulatory actors (Baron, 1995; Hillman, Keim, and Schuler, 2004; Zhu and Chung, 2014; Dorobantu, Kaul, and Zelner, 2017). It shows that larger firms, primarily in mature industries, are more politically active and sophisticated. For instance, Macher and Mayo’s (2015: 2034) empirical analysis of over 10,000 firms globally found that “large firms possess superior scale, resources, and relationships vis-à-vis small firms in policymaking influence that provide advantages in different industry and political institution environments.” Nonmarket strategies, such as lobbying, campaign contributions, and political connections, are associated with more-favorable policy outcomes―lower taxes (Richter, Samphantharak, and Timmons, 2009), more earmarks (de Figueiredo and Silverman, 2006), and competition-restricting policies (Schuler, 1996)―and can be deployed by individual firms (Jia, 2018) or in strategic coordination with other key stakeholders (Westphal et al., 2012; Yue, 2015; Henisz, 2017). Corporations tend to prioritize (Cheng and Groysberg, 2018) and engage in ongoing levels of nonmarket activity to monitor the regulatory environment (Drutman, 2015). Nonmarket strategy can also be reactive: corporations often ramp up nonmarket activities when regulatory issues come to a head (Short and Toffel, 2010), or strategically arbitrage into more-favorable regulatory venues (Rao, Yue, and Ingram, 2011; Sytch and Kim, 2021). Scholars have also found that the rules governing an industry can be malleable, allowing firms to shape the meaning or interpretation of regulations in their broader legal environment (Edelman and Suchman, 1997). For instance, Edelman, Uggen, and Erlanger (1999) highlighted the “endogeneity” of legal regulation in their study of equal-employment-opportunity (EEO) grievance procedures; they showed that corporations and their lobbyists mediate the impact of law by actively constructing the meaning of compliance.

Existing paradigms, though broadly informative, provide an incomplete understanding of how ventures navigate regulatory uncertainty in nascent industries. For instance, entrepreneurs may adopt political-influence tactics, like those highlighted in nonmarket-strategy research. But resource- and legitimacy-constrained new ventures may be unable to afford or use the traditional tools of influence employed by large corporations in mature industries with fixed and known regulations—corporations that often have Washington-based government affairs offices that make a practice of cultivating key political stakeholders over time. As Georgallis, Dowell, and Durand (2019: 528) noted in their study of new-industry emergence, such conventional nonmarket strategies as lobbying and regulatory capture are “unlikely to be primary drivers of such support when the focal industry is nascent and has relatively little leverage over government actors.” Ventures might also turn to flexible organizational processes, which research suggests is crucial for adapting to nascent-market uncertainty. However, regulators have a public-oriented mission to serve multiple stakeholders, and strategies suited to profit-seeking firms governed by efficiency objectives may not work or may work differently when aimed at such nonmarket entities.

An emerging stream of research at the intersection of entrepreneurship and nonmarket strategy has begun to generate insights that could inform how ventures navigate regulatory uncertainty. Hiatt and Park (2013), in a call to action for scholars to study regulators (not just policymakers) given their key role in the interpretation and execution of laws, examined the regulatory decisions on genetically modified organisms. They argued that regulators face legitimacy pressures and that biotech firms could thus indirectly influence them by appealing to prominent third-party actors on whom regulators’ legitimacy depends, such as peer regulatory agencies and powerful stakeholders. Ozcan and Gurses’s (2018) study of regulatory categorization decisions for dietary supplements found that firms could indirectly influence regulators via pressure from consumers; they highlighted soft-power tactics for winning over consumers—such as invoking culturally resonant meta-narratives that “hook” and “activate” consumers to engage in regulatory advocacy. Lee, Hiatt, and Lounsbury’s (2017) study of the organic-food product category demonstrated that by delineating categorical boundaries and establishing and enforcing standards, an industry association can serve as an invaluable market intermediary for resource-constrained firms striving to legitimate a nascent category. 1

This work suggests that resource-constrained ventures can influence regulatory decisions indirectly via regulators’ key stakeholders (i.e., customers, peer agencies, and prominent associations) and can employ resource-efficient soft-power strategies like framing and claims-making to influence such stakeholders. Though insightful, this work leaves several questions unresolved. First, though mass-media accounts have publicized seemingly effective direct interactions between startups and regulators, little academic research has analyzed direct-engagement strategies vis-à-vis regulators, particularly in terms of their content and dynamics. Second, though research has examined specific regulatory event junctures (such as initial categorization and approvals of new products), less research has used a process perspective to examine how and when new ventures can engage regulators, particularly with regard to interdependencies across time among actions, sequences, and regulations. Third, some strategies, such as forming industry associations, may be difficult to coordinate and might not always work, particularly across dissimilar contexts (Yue, Wang, and Rao, 2022). Finally, research on interdependencies between market and nonmarket strategies is limited. Some work has theorized that market actions could affect nonmarket outcomes (and vice versa) (Funk and Hirschman, 2017; Baron, 2018), but little empirical work has delineated how this effect plays out in practice, particularly in nascent industries (Garud et al., 2022).

Thus we still have an underdeveloped understanding of how entrepreneurs strategize under regulatory uncertainty―particularly in terms of the content, sequence, and typology of actions for engaging regulators as a nascent industry evolves. Yet effectively navigating (and perhaps shaping) regulatory uncertainty is crucial for ventures’ survival. The consumer drone industry again offers a case in point. Initially the FAA required drone users to hold a pilot’s license, a demand-dampening move “that could cripple commercial drone flight” (Harwell, 2014), before abandoning the license requirement in 2015. By examining how ventures vary in their regulatory strategies and why certain strategies appear more effective, we aim to elucidate how ventures in a nascent industry can navigate and shape regulatory uncertainty.

Methods

Because little theory exists on how ventures in nascent industries navigate regulatory uncertainty, we undertake inductive theory building (Edmondson and McManus, 2007; Charmaz, 2010) using multiple cases (Eisenhardt, 1989; Yin, 2013). Multiple cases allow for a replication logic that treats each case as an experiment (Eisenhardt and Graebner, 2007); inferences drawn from one case can be compared to others to confirm or refute an insight (Yin, 2013). This approach fosters more robust and generalizable theory development than do single-case approaches (Eisenhardt, Graebner, and Sonenshein, 2016) and is well suited to answering how questions (Langley, 1999; Gehman et al., 2018).

Research Setting: The Personal-Genomics Industry

Our research setting is the direct-to-consumer (DTC) genetic-testing industry (“personal genomics”), which launched in 2007. Personal-genomics companies analyze a consumer’s DNA, using a saliva sample, and then report on the consumer’s ancestry, inherited traits, and genetic risks for developing various diseases. Genetic risk assessments draw on scientific research that specifies how variations in the genetic code correlate with the probability of developing various health conditions. Proponents of personal genomics argue that awareness of genetic risk factors enables consumers to manage their health more proactively, which promotes prevention and reduces the need for medical treatment.

The personal-genomics industry was made possible by a technological discontinuity: in 2003 the human genome was fully sequenced after a 13-year, $2.7-billion effort known as The Human Genome Project. For the first time, scientists had mapped “the genetic blueprint of life” by specifying the sequence of the 30 billion nucleotide base pairs that make up human DNA. This effort has been hailed as one of the great feats of exploration in human history (National Institutes of Health, 2019) and a watershed moment for biomedical science (Pisano et al., 2020).

DNA is a foundational component of human biology: found in every cell in the body, it carries genetic instructions that tell cells what to do, such as constructing proteins and other cell components. Since 2003, the cost of genetic sequencing has plummeted, prompting a wave of research, known as genome-wide association studies, that correlates genetic variation with disease risks (Pisano et al., 2020). Cost-efficient gene-scanning technologies have also emerged; SNP genotyping—a method that scans only the areas of DNA known to be correlated with disease risk—is much cheaper than sequencing an entire genome. The use of SNP genotyping technology enabled personal-genomics ventures to launch at a relatively low product price point.

We study the industry from its inception in 2007 through 2017. Personal genomics is an ideal setting in which to study innovation strategy amid regulatory uncertainty. Consistent with our definition of a nascent industry, the industry was catalyzed by a technological discontinuity (DNA sequencing) that led to an era of ferment characterized by uncertainty (Tushman and Anderson, 1986). A handful of ventures competed in a context of fluctuating industry structure, rudimentary business models, ill-defined customers, and regulatory uncertainty (Navis and Glynn, 2010; Zuzul and Tripsas, 2020). Initially, regulators struggled with whether and how to regulate such products. Should the tests be considered medical devices or novelty items? Should they require a doctor’s prescription? Uncertainty flourished against a backdrop of traditional genetic tests that could be obtained only via a physician’s order and only in highly specified circumstances, such as a family history of a specific disease. Traditional tests were also costly and limited to specific conditions, and they often took months. No clear means existed to pursue genetic tests for a broad array of conditions that consumers could use to proactively manage their health.

The nascent personal-genomics industry was characterized by rich variation not only in ventures’ strategies and actions but also in regulators’ activities; the Food and Drug Administration’s (FDA) approach to regulating the industry changed substantially over time. Because regulation had not yet solidified when we began this study, nor had a clear winner emerged, we were able to study the industry both retrospectively and in real time.

Sample

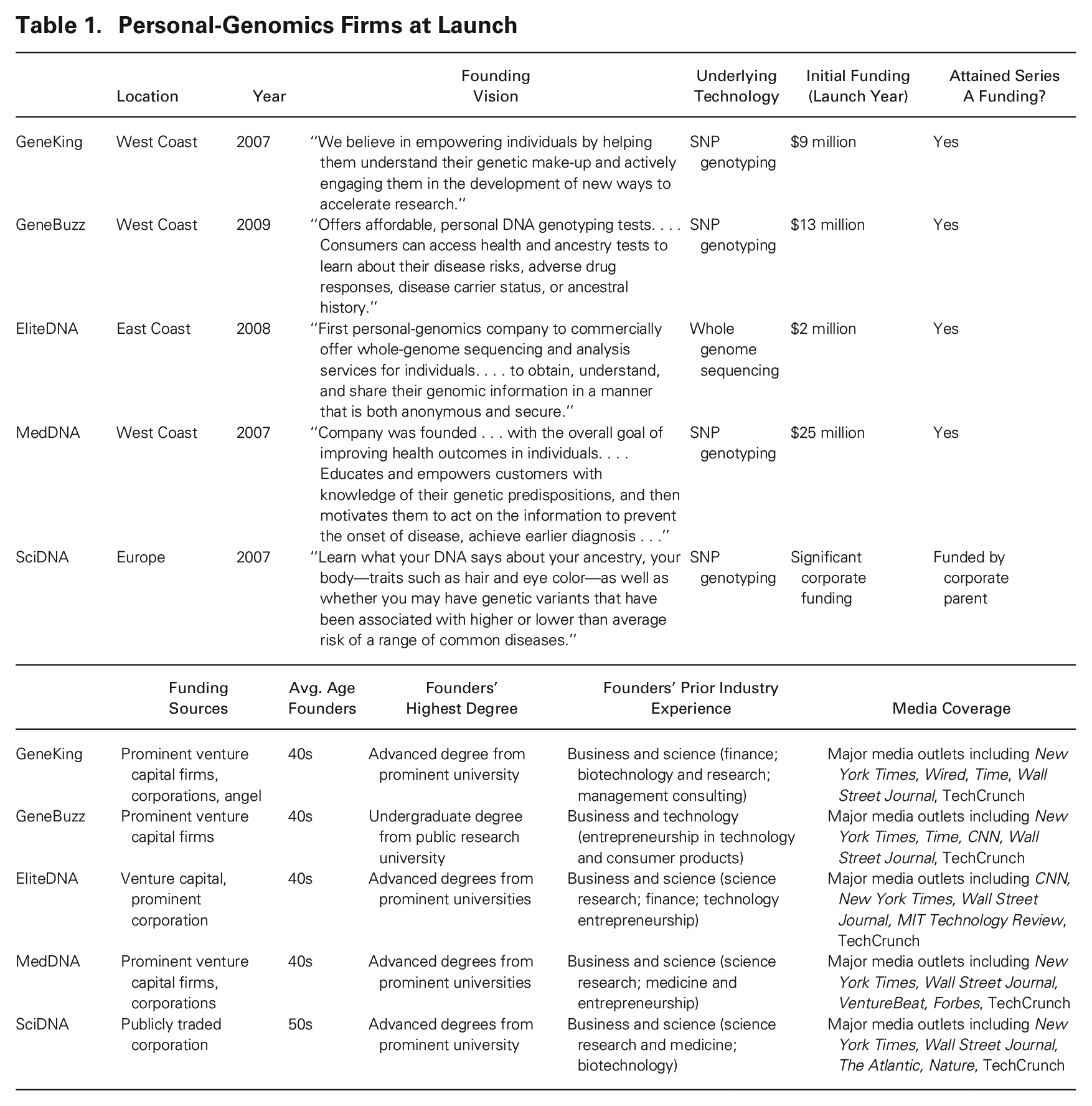

Our sample consists of the five ventures that launched the personal-genomics industry: GeneKing, GeneBuzz, EliteDNA, MedDNA, and SciDNA (we use pseudonyms to facilitate candid data collection). Our sampling logic is grounded in theoretical sampling: we selected the firms for their theoretical similarity (as new ventures navigating regulatory uncertainty in a nascent industry) and for their potential to illuminate the mechanisms, constructs, and interrelationships that characterize such ventures’ nonmarket activities. This approach aligns with a rich tradition of theory elaboration in qualitative research (see Eisenhardt and Graebner, 2007, and Eisenhardt, Graebner, and Sonenshein, 2016, on theoretical sampling). Table 1 describes the five firms when they launched.

Personal-Genomics Firms at Launch

Several external indicators confirm the appropriateness of our sampling strategy. 2 In 2010 the FDA sent letters to several DTC personal-genomics firms asserting its jurisdiction and requiring them to apply for pre-market approval before marketing and selling their products. The FDA’s choice of recipients for its letter helps corroborate our choice of firms to study, as scholars have noted that regulatory oversight helps demarcate the boundaries of a field (Grodal, 2018). That same year the Government Accountability Office released a report on the industry that also helps corroborate the choice of firms. Interviews with informants and journalists, as well as archival media articles, further corroborate that these five firms pioneered the industry.

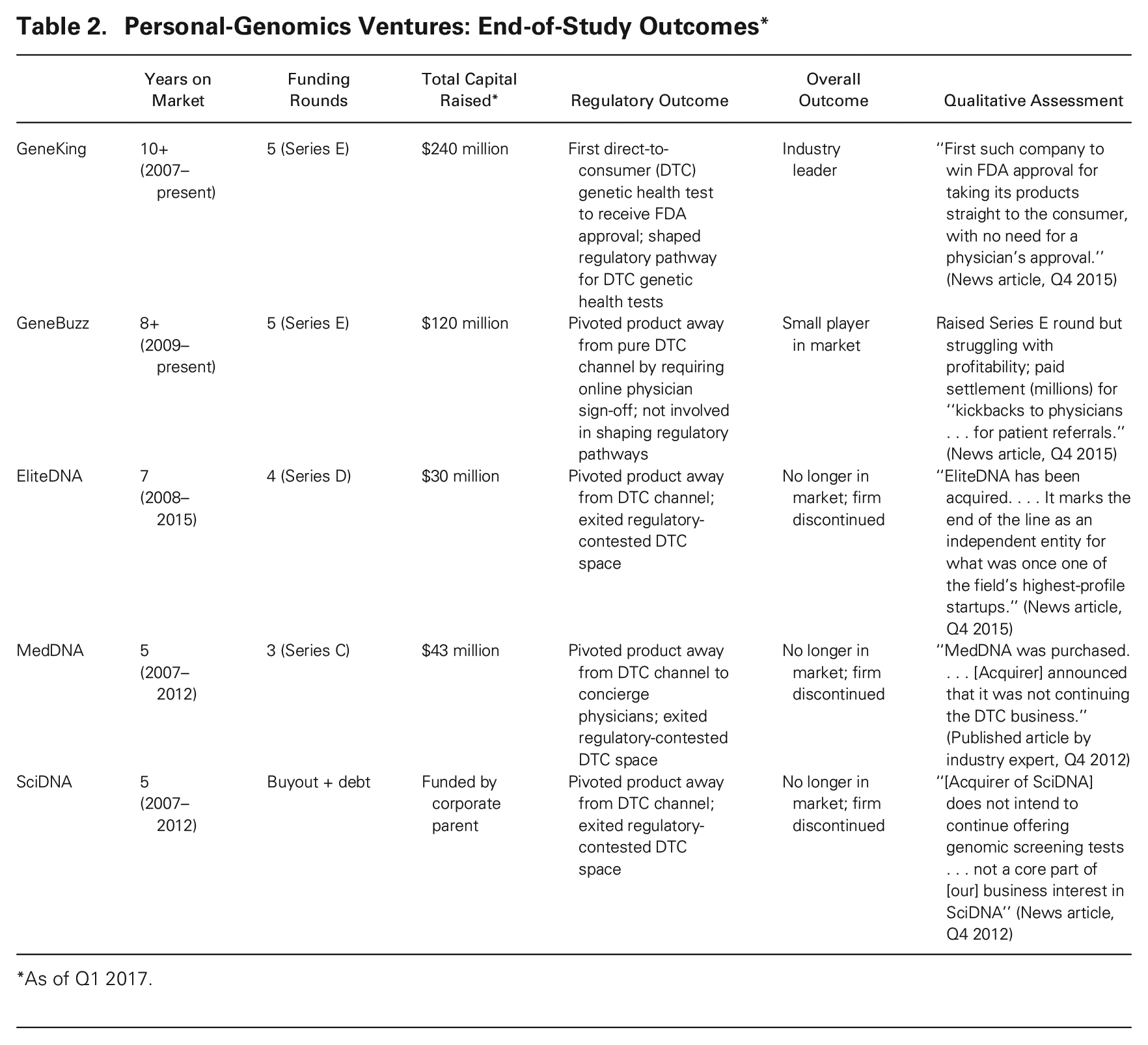

Internal indicators also support the appropriateness of our sample. All five firms began with the same objective: to provide a genetic-testing product directly to consumers. All five were launched around the same time (within roughly a year-and-a-half window) and received media coverage from leading newspapers and magazines. Their founders were all highly credentialed; four of the firms had at least one founder with an advanced degree from an elite university (such as a Ph.D., MD, or MBA) and prior industry experience that spanned both business and science. The founders’ ages were similar, too, primarily averaging in the early 40s. All five firms attracted funding from prominent resource providers, including prestigious venture-capital firms and corporations, and the four firms that relied on external funding attained Series A funding early on. All five were new ventures: four pure startups and one (SciDNA) incubated within a corporation. They also used similar sequencing technology: four used SNP genotyping, and one (EliteDNA) used whole-genome-sequencing technology. The firms differed, however, in their strategies for managing regulatory uncertainty. The presence of polar types (high- versus low-performing firms) among the five firms facilitates comparison of contrasting patterns (Eisenhardt and Graebner, 2007). By tracking variations in the firms’ strategies and outcomes over time (as demonstrated in Table 2), we use a “racing” design (Eisenhardt, 2021: 150)—the cases (i.e., firms) begin at roughly the same time, under similar initial conditions, and race to regulatory resolution—to facilitate development of robust and generalizable theory.

Personal-Genomics Ventures: End-of-Study Outcomes*

As of Q1 2017.

Data Collection

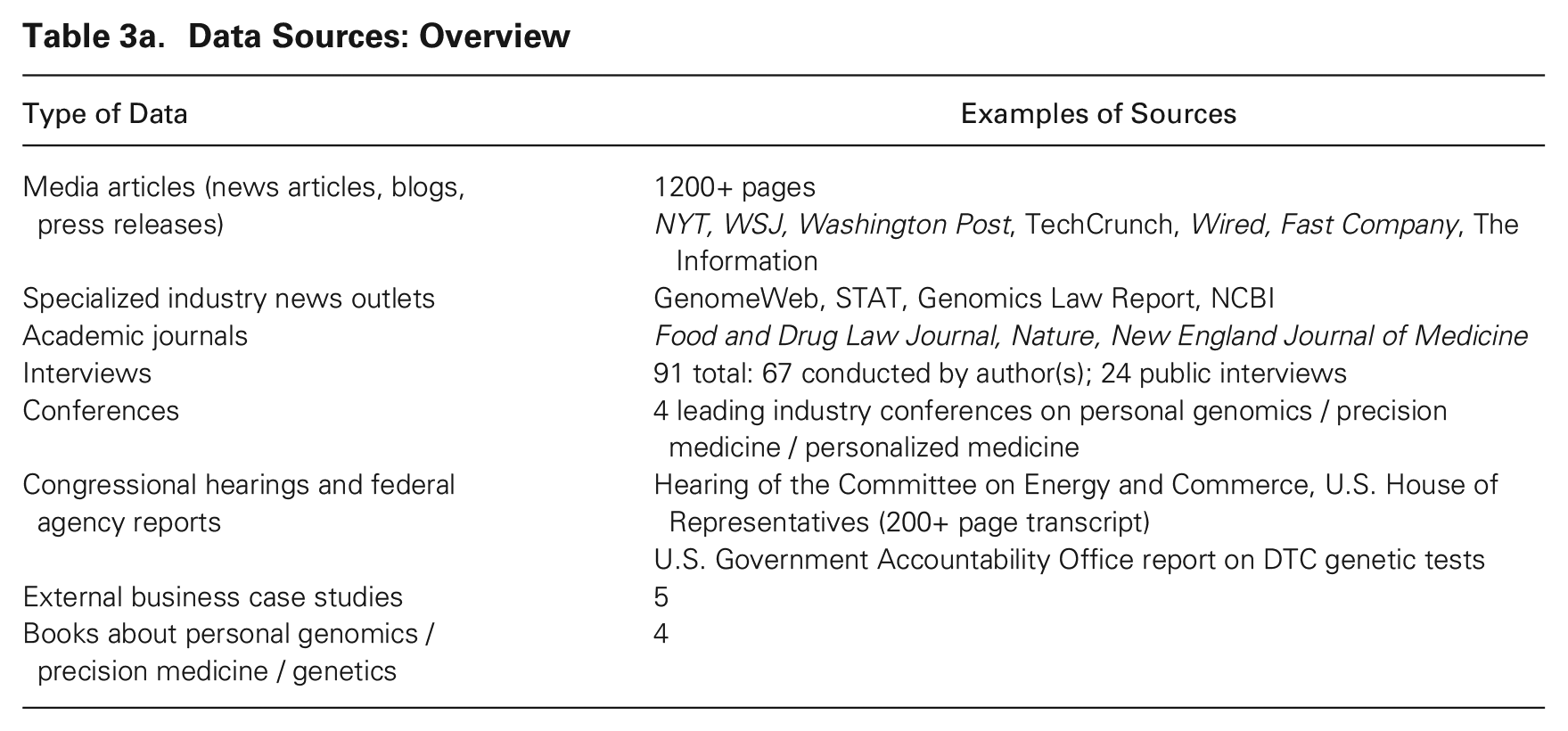

Our data, collected over a span of four years, consist of extensive archival data and 91 interviews conducted in waves. To establish the study’s feasibility, we first reviewed the archival material and conducted ten pilot interviews with industry insiders; both sources suggested that personal genomics was an appropriate research setting, characterized by rich content and striking variation in ventures’ actions. We then scaled up the data-collection process. What follows is a description of the types of data we collected (summarized in Tables 3a and 3b) and the process of synthesizing and analyzing it.

Data Sources: Overview

Data Sources: Interviews

We collected archival data from both internal and external sources. Internal sources include pitch decks for investors, memos, press releases, blog posts, and public filings; external sources consist of media coverage, analyst reports, books, press releases, transcripts from Congressional hearings, and other public materials. To ensure systematic and comprehensive collection of archival data, we consulted a research librarian familiar with such online databases as Factiva, LexisNexis, and Bloomberg. We also hired research assistants to pursue independent archival data collection and compared our data with theirs.

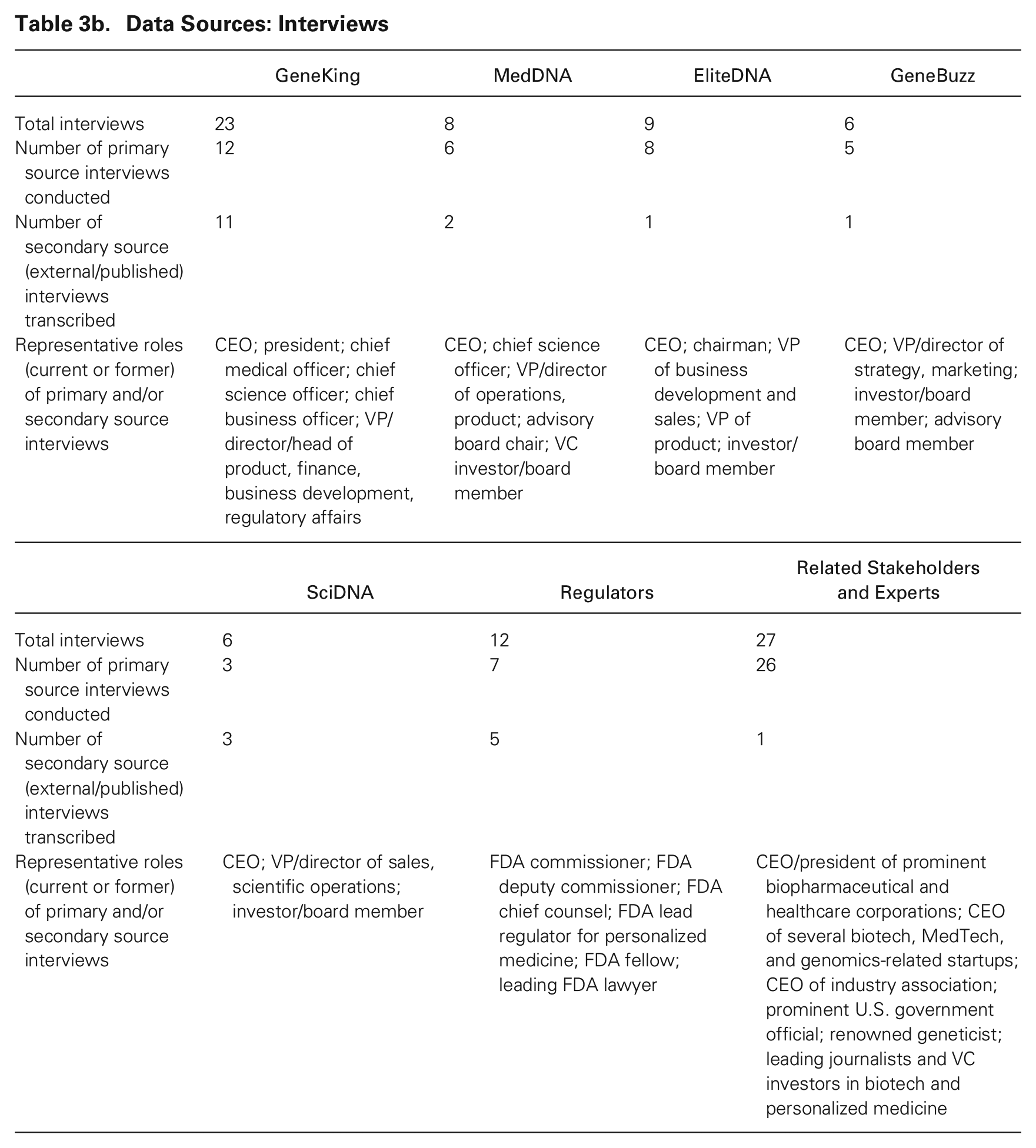

Our interview data consist of 91 interviews with internal and external informants: we conducted 67 semi-structured interviews and collected 24 publicly available interviews. We continued interviewing until a point of theoretical saturation when interviews yielded few new insights and concepts and linkages had become well developed. Interviews ranged from 30 minutes to 2.5 hours; most lasted around an hour. Most informants agreed to be audio-recorded; those interviews were professionally transcribed.

We interviewed current and former executives of the firms in our sample, with titles such as CEO, co-founder, chairman, chief medical officer, chief science officer, and EVP/vice president/director/head of product, finance, business development, marketing, and regulatory affairs, as well as company affiliates such as investors, board members, and advisors. We interviewed industry experts and stakeholders, including leading analysts, journalists, scientists, lobbyists, lawyers, and executives from related fields, including two former CEOs of Fortune 500 corporations that had invested in firms in our sample and the CEO and senior executives of industry associations and related firms in the broader precision-medicine sector. Finally, we collected unique qualitative data on regulators. We interviewed several current and former regulators, including an FDA commissioner and chief counsel, as well as former senior government officials. At FDA headquarters, the first author interviewed a lead regulator with oversight over personal genomics. To the best of our knowledge, qualitative data that shed light on the reasoning, processes, and actions that characterize firm–regulator interactions are rare in nonmarket-strategy and organizations research. These data thus present a unique opportunity to examine the usually opaque processes that underlie nonmarket strategy in nascent industries.

We took several steps to ensure data validity. First, informants’ names are anonymized, and we use pseudonyms for each venture, following conventional practice in qualitative research to facilitate candid conversations (Perlow, Okhuysen, and Repenning, 2002; Santos and Eisenhardt, 2009; Neeley, 2013). Second, we interviewed informants at different hierarchical levels and in different functions, from the C-suite down to various managerial levels in the business, product, science, and regulatory functions (Jick, 1979). Third, we asked open-ended questions and avoided leading questions, so that constructs would emerge from the informants themselves (Edmondson, Bohmer, and Pisano, 2001). We also drew on archival data that captured real-time views and sentiments—press releases, blog posts, news articles, and the like—to triangulate the interview data with archival data. Finally, data collection began well before a clear winner had emerged in the industry; none of the firms had won regulatory approval to offer genetic health reports of any kind to consumers, no regulatory pathway existed, and in fact the viability of the entire industry was up in the air. In Q4 2015, over a year after the study began, the tide began to turn when one of the ventures received FDA approval to report on a specific health condition; several more health conditions were subsequently approved.

The interview guide we compiled had three main sections. The first consisted of open-ended questions about the firm’s history, from its founding to the present. We probed the market and nonmarket actions that informants reported, inquiring about how and why particular actions occurred and about actions contemplated but not carried out. The second section focused on themes pertinent to the research question, including the nature of regulatory uncertainty and how the firm interpreted it, as well as actions and processes pursued to navigate uncertainty and their consequences. We also asked how market phenomena, such as strategy formulation and competitive dynamics, related to or were affected by nonmarket regulatory dynamics. Finally, we inquired about informants’ views on the industry’s evolution, and we touched on any ambiguities that had arisen in the interview. With external informants, we used a similar interview guide but focused on the industry as a whole. Though the interview guide is linear and open-ended, its sections could overlap depending on the informant and the flow of the interview.

Additionally, the first author attended four prominent conferences on personal genomics, precision medicine, and “health-tech.” These conferences were opportunities to gain cutting-edge insights on personal genomics, stress-test emergent ideas, observe practitioner interactions, and make contacts that led to several research interviews.

Finally, to familiarize ourselves with personal-genomics products and to gain a user’s perspective on the product experience, both authors purchased and used genetic-testing products from two of the firms in our sample.

Data Analysis

In keeping with standard practice in multi-case inductive research (Eisenhardt and Graebner, 2007), we created a 100- to 150-page chronological case narrative for each of the five firms, using archival data. Separately, we coded the interview data. We then iterated between theory and data and composed memos to document tentative observations, insights, theoretical connections, and questions that arose from the interviews. For a second perspective, we hired a research assistant to independently code the interviews and then compared codes to ensure that we were not systematically overlooking potentially important constructs. We then blended interview data into case narratives. The resulting narratives, which combine archival and interview data from internal and external sources, provide rich and triangulated material for inductive theory building (Davis and Eisenhardt, 2011). We then analyzed each case through the lens of our research questions: how do new ventures vary in their strategies for navigating regulatory uncertainty, and which strategies appear more effective in a nascent-industry context? To facilitate analysis, we wrote analytical memos and constructed tables about each case.

We then engaged in cross-case analysis to pinpoint consistent patterns and themes and to identify emerging constructs (Hannah and Eisenhardt, 2018). Rich variation emerged in terms of firms’ strategy formulation and of their actions amid regulatory uncertainty and responses to regulatory pressure. Through a process of active and iterative categorization (Grodal, Anteby, and Holm, 2021), we compiled tables of emerging theoretical constructs, compared constructs across cases, refined them, and ultimately compared them to the literature. This emergent and iterative process is typical of grounded, inductive research (Eisenhardt, 1989).

We focused on both market and nonmarket outcomes. 3 To assess outcomes in a multidimensional way, we examined key audiences—regulators, the media, resource providers, customers, and analysts—and several indicators. For nonmarket outcomes, we examined regulators’ reactions to the firms, embodied in such negative quantitative indicators as the number of regulatory actions taken (e.g., letters sent, denials of market access) and such positive quantitative indicators as the type and number of conditions approved. We also assessed qualitative indicators, such as regulators’ evaluations of firms’ outcomes as expressed in public sources and in private interviews. In our data tables, we also categorized outcomes where useful, using labels such as receiving demerits, escaping regulation, and influencing regulations. For market outcomes, we collected quantitative measures of VC funding and VC partners’ qualitative assessments of the firms. We also collected indicators of product traction and media reactions to the firms, both quantitative (media hits) and qualitative (the tone of opinions expressed), and qualitative evaluations of the firms’ outcomes by industry experts.

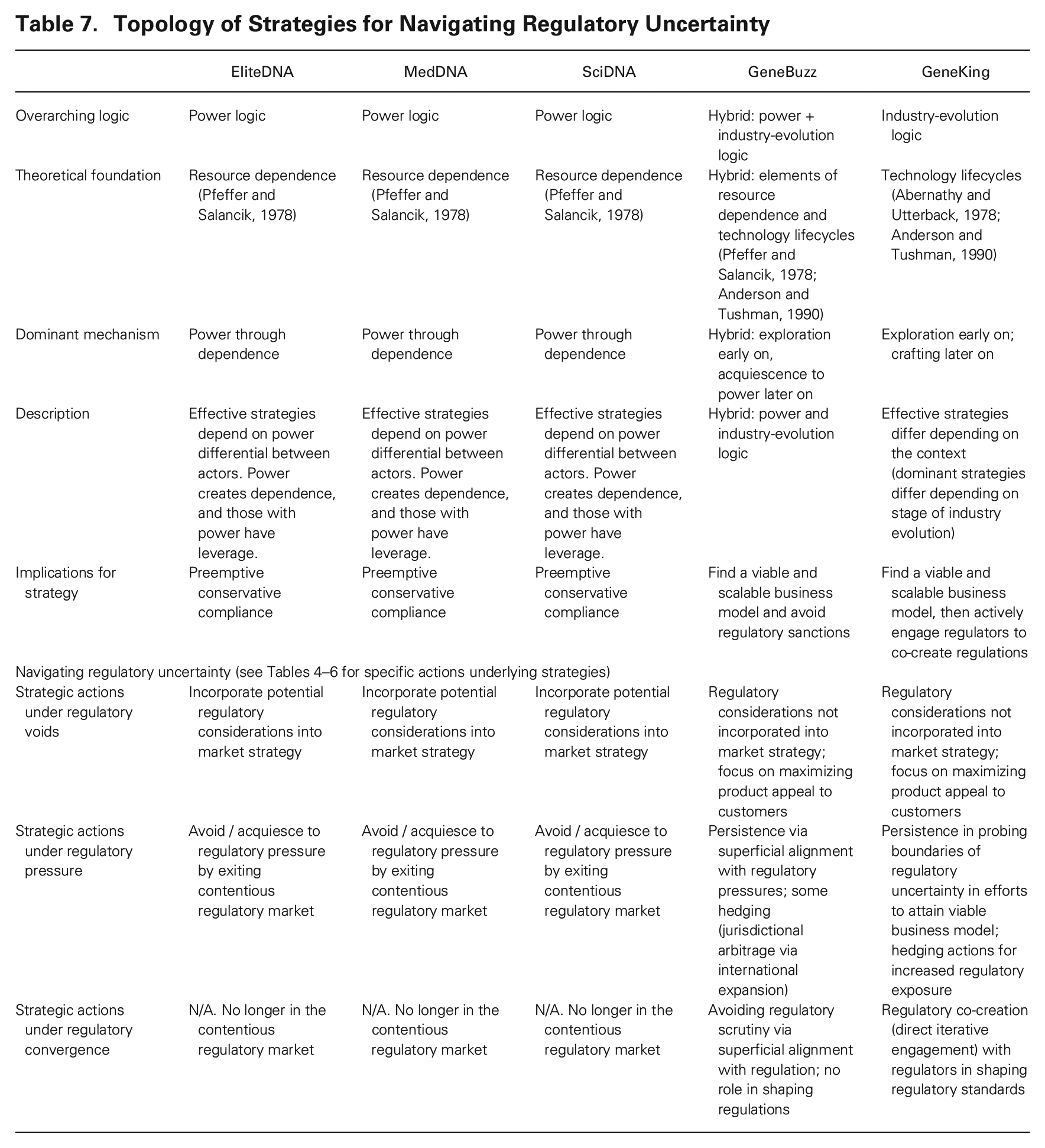

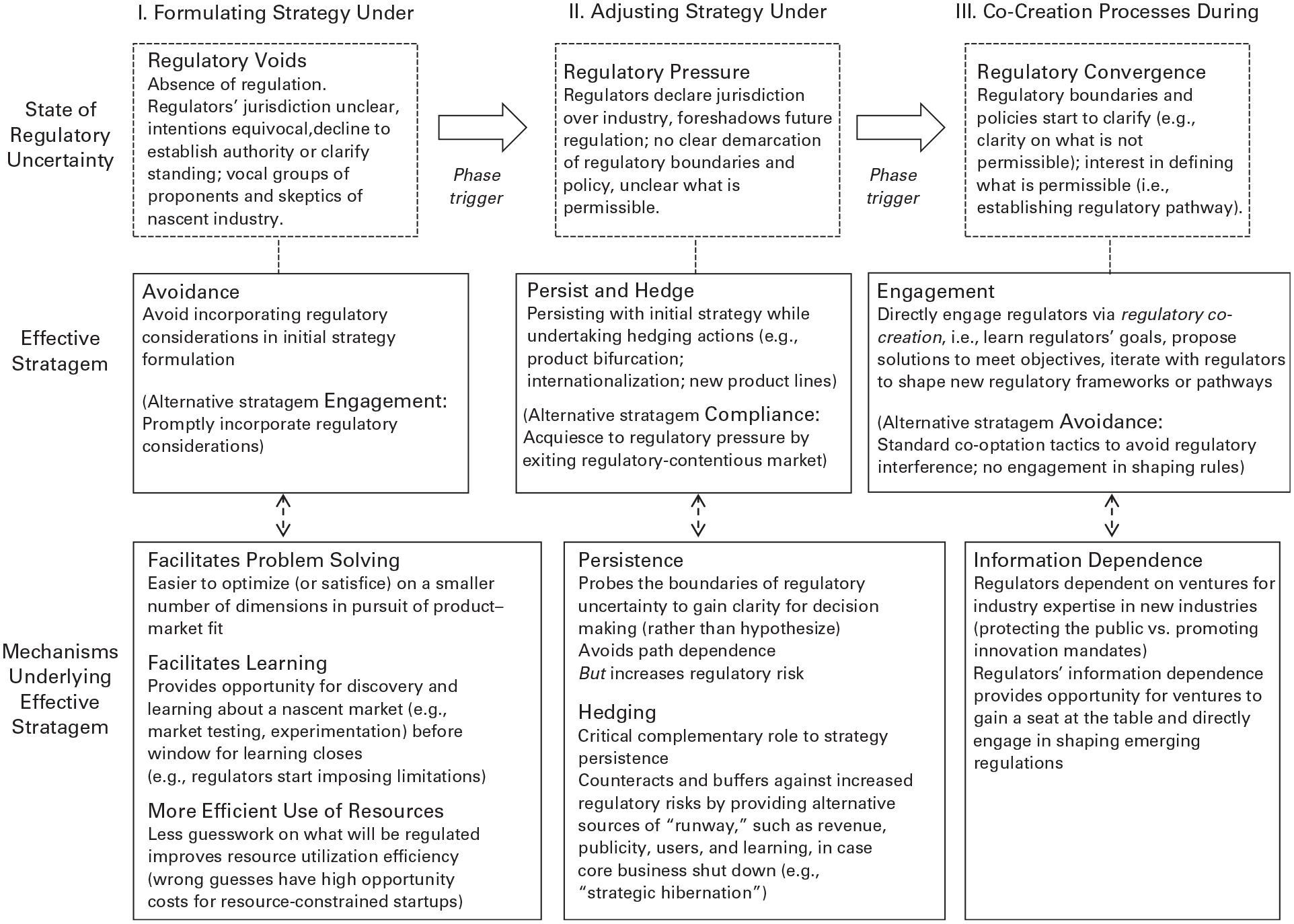

Navigating Regulatory Uncertainty: An Emergent Framework

Power Logic vs. Industry-Evolution Logic

We develop a theoretical framework for how new ventures navigate regulatory uncertainty. Our framework unpacks how ventures’ strategies varied as the nascent personal-genomics industry evolved and theorizes about why certain strategies seem more effective than others. We organized our analysis around three evolving phases of regulatory uncertainty that we observed: regulatory voids, regulatory pressures, and regulatory convergence. We define these phases as intervals of time during which the level of regulatory uncertainty was qualitatively similar for the ventures. The theoretical framework, which specifies the range, content, and sequence of actions that ventures take to manage such uncertainty, emerged inductively from our data. In short, we tracked and compared the strategic approaches and actions of the five firms throughout different stages of regulatory uncertainty, and we linked those actions to audience assessments, regulatory reactions, and the firms’ trajectories.

The ventures differed in their approaches to managing regulatory uncertainty. One set of ventures employed what we term a power logic, as might be expected from a resource-dependence perspective. These ventures (EliteDNA, MedDNA, and SciDNA) preemptively acquiesced to the power of authority in the face of regulatory uncertainty. For example, when formulating their initial strategies in the absence of regulations and amid jurisdictional uncertainty, they speculated on and took into account potential regulations. When regulators eventually claimed jurisdiction over the industry with general guidelines, these ventures immediately conformed by adjusting their strategies to align with regulators’ emergent (and potential) objections or by pivoting their products into categories with more-clearly defined regulations.

The ventures that employed (to varying degrees) what we term an industry-evolution logic focused first on exploration (early in the industry’s evolution) and then on crafting (as the industry later coalesced), thus pushing the boundaries of regulatory uncertainty. One firm (GeneKing) fully embraced this logic, doing very little to incorporate regulatory considerations into its initial strategy. The firm then reacted to emerging regulatory guidelines with persistence, instead of pivoting to safer product categories; as the industry coalesced, it then used its market learnings to directly engage with powerful regulatory actors to shape emerging regulations. Another firm (GeneBuzz) took a hybrid approach, progressing from an industry-evolution logic to a power logic as the industry coalesced. The following sections contrast these two logics, linking each approach to its outcome and theorizing why certain strategies appear more effective. The resulting theoretical framework elucidates the type, content, and sequence of strategies that ventures employ in the face of regulatory uncertainty, as well as the ways these strategies may empower or constrain firms’ trajectories in a nascent industry.

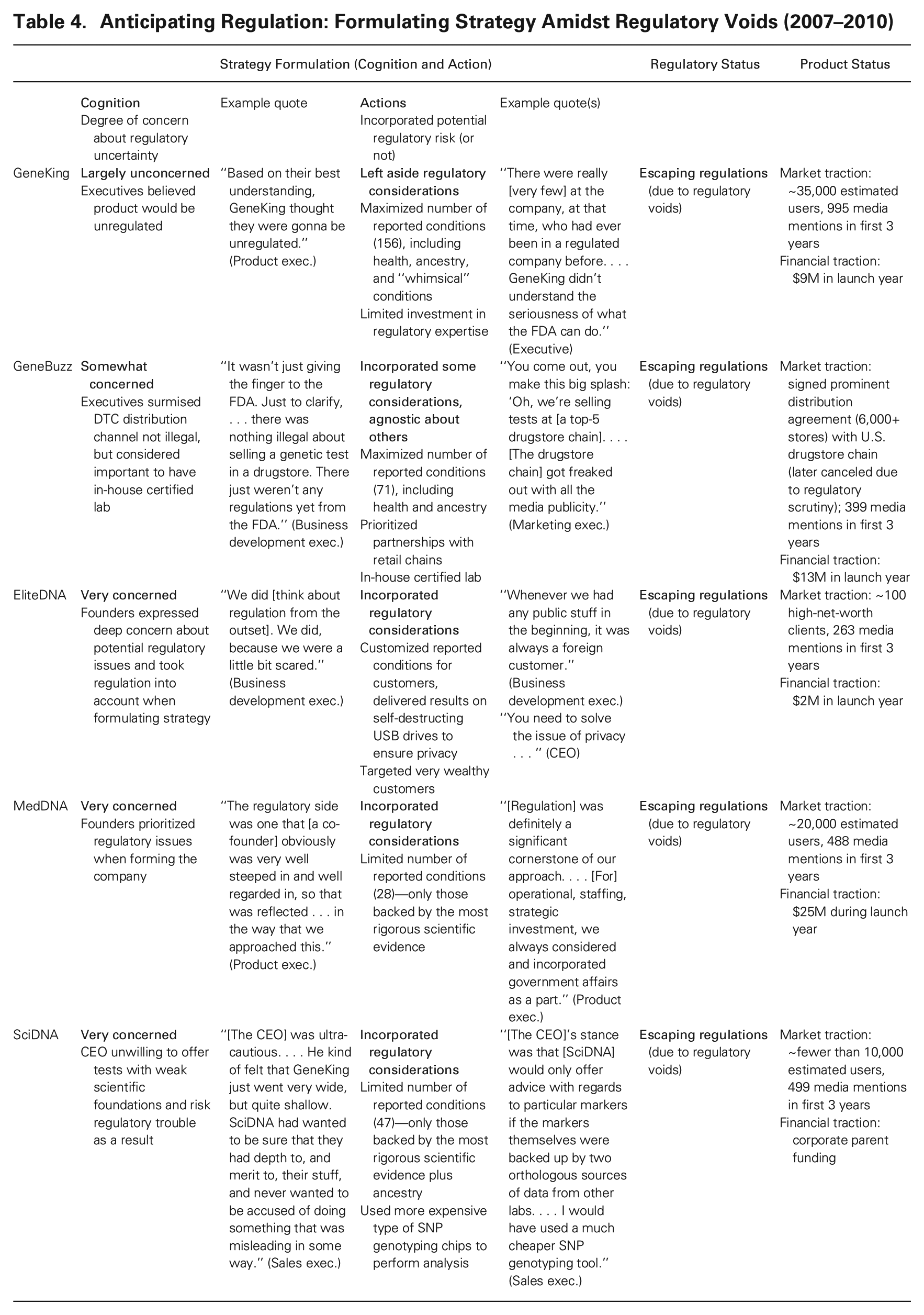

Anticipating Regulation: Formulating Strategy amid Regulatory Voids

The personal-genomics industry faced significant regulatory uncertainty between 2007 and 2017. Ambiguity about regulators’ intentions and jurisdiction allowed for opposing interest groups to invoke entirely different considerations when debating how personal-genomics services ought to be regulated. Vocal skeptics argued for imposing certain requirements on the industry. Some worried about the accuracy and utility of genomic tests; research correlating genetic variations with disease risk was still in its infancy. Others worried that consumers would experience extreme duress or make rash decisions in response to results from an unproven technology; they argued that an intermediary—ideally, a doctor—should be required to help consumers interpret their genetic information and make appropriate decisions. Still others spotlighted the privacy issues raised by private companies’ possession of sensitive genetic data. 4

Proponents of the industry pushed back, stressing that personal-genomics services merely provide risk assessments, not diagnoses; consumers have a right to their own genetic information, they argued, without involving an intermediary. They pointed out that no existing laws specifically governed direct-to-consumer genetic tests and that most genetic tests prescribed by doctors to identify specific heritable diseases were unregulated. 5 Meanwhile the FDA did little to establish its authority or to clarify where the agency stood on critical issues. A 2008 news article reported that the FDA “declined to discuss” what might be in store for the nascent industry, as a senior FDA official declared that “of course we are watching this field with great interest.” 6 Such equivocal signals from a federal regulatory agency, in conjunction with competing interpretations of personal-genomics technology, created significant uncertainty. MedDNA’s CEO spoke for many in the industry by lamenting that “nobody really understands the way the FDA works. . . . It all looks kind of scary.”

The five ventures took different approaches amid these regulatory voids. We tracked the degree to which they treated regulatory uncertainty as a matter of concern at the time of founding and how (if at all) they incorporated regulatory considerations when formulating their initial strategies. Following Ott, Eisenhardt, and Bingham (2017), we conceptualized strategy formulation in entrepreneurial settings as grounded in both managerial cognition (pursuing a holistic understanding of the market and its opportunities) and action (making moves and learning from them). We then assessed how executives incorporated regulatory considerations.

Pre-empting regulation in initial strategy formulation

From the outset, EliteDNA, MedDNA, and SciDNA seemed to approach regulatory uncertainty with deliberate consideration. Uneasy about the possibility of future FDA interventions, these ventures surmised and factored regulators’ potential objections into their initial strategies. “We did think [about potential regulation] from the beginning . . . because we were a little bit scared,” recalled a founding executive at EliteDNA. Such worries shaped their strategies’ scope, intended advantage, and key activities.

This group of ventures proactively pre-empted potential regulatory objections to their business. EliteDNA illustrates. It purposefully targeted customers outside the United States, where the FDA lacks jurisdiction. “We tried as much as possible to keep to international customers,” said one executive. It also built its value proposition on health and exclusivity, targeting ultra-wealthy customers by offering whole-genome sequencing, the most expensive and advanced sequencing technology. At an initial price of several hundred thousand dollars, EliteDNA’s product bypassed the mass market—the customer segment whose vulnerability skeptics and regulators expressed the greatest reservations about. A news article on EliteDNA quipped that the genome has overtaken Bentley as the latest status symbol. To mitigate alarm about consumers’ limited ability to decipher their genetic test results, EliteDNA sent a trained intermediary—a physician—to meet twice with each client, first to collect DNA samples and then to present results and genetic data on self-destructing USB sticks, to steer clear of thorny privacy issues. “If someone tried to hack [clients’ genetic data], it would go away,” explained an EliteDNA executive.

Regulators’ possible objections also loomed large for MedDNA. “The regulatory side was one that [our co-founder] was very well steeped in,” a product executive recalled. “So that was reflected in the way that we approached [our product-market strategy].” Anticipating skepticism about its tests’ validity, MedDNA designed its initial product to report on a select few health conditions whose association with genetic variations was backed by the most stringent research, thus deliberately limiting its potential value to consumers. (Other ventures reported on far more conditions and included information on ancestry and other non-health-related characteristics.) Early on, the company amassed regulatory expertise by hiring senior employees with extensive backgrounds in business–government relations, especially law and compliance. “Within the operational, staffing, [and] strategic investment [plans], we always considered and incorporated government affairs,” a MedDNA executive recalled. To head off the charge that consumers would not adequately comprehend their genetic test results (and could experience psychological stress), MedDNA integrated genetic counseling into its core product: without an additional charge, customers could request help from a genetic counselor. This feature drove up the cost of the product (and its price), but executives considered it worthwhile and apt to distinguish MedDNA’s offering in the eyes of both customers and regulators. “None of the other [competitors] had integrated genetic counseling, and we purposefully integrated [it],” said a product executive. MedDNA hoped that this conservative approach would lower the company’s regulatory risk and help attract funding. Negative regulatory actions “cause a lot of uncertainty in your investor base,” the CEO asserted.

Like EliteDNA and MedDNA, SciDNA’s expressed concern over potential regulatory pushback led it to incorporate distinctive elements into its strategy. The CEO “wanted to be sure that [we] had depth to, and merit to, [our] stuff, and never wanted to be accused of doing something that was misleading in some way,” recalled a sales executive. To head off charges of inaccuracy, it withheld information from customers (deliberately narrowing its overall value proposition) by revealing test results only about conditions whose association with genetic variation was substantiated by multiple scientific sources; SciDNA did not report results for a broader set of conditions with weak scientific underpinnings. Executives publicly disparaged competing ventures that “just went very wide but quite shallow” by reporting on a broader range of conditions, and they reproached those willing to compromise rigor for consumer appeal. SciDNA also used a more-expensive type of SNP genotyping chip to scan DNA samples, overshooting on technology to forestall a potential regulatory crackdown. According to a sales executive, the chip “offered perhaps 999 times more information than was useful or meant anything to the customer.” SciDNA thus had to raise the product’s price—a decision unpopular with its sales executives.

Attentiveness to regulation in their initial strategies facilitated fundraising and favorable media coverage of the three ventures. The media lauded MedDNA’s apparent seriousness and rigor: one publication observed in 2009 that the venture “paint[ed] itself as the more serious and respectable member of the personal-genomics industry.” MedDNA also attracted interest from prominent Silicon Valley venture-capital firms, raising more money than any of its competitors in its launch year. SciDNA and EliteDNA also did well at fundraising: SciDNA was generously funded by its corporate parent, and EliteDNA intentionally eschewed early venture funding but received several lucrative offers and later accepted a multimillion-dollar investment round.

But factoring regulation into their initial strategies (i.e., pre-empting regulation) seemed to hobble the ventures’ progress in the market in unforeseen ways. Executives bemoaned their lack of “market traction” in the forms of publicity (free marketing, generated through media attention, which creates brand awareness and legitimacy) and users (who provide revenue and signal credibility to investors). By 2009, roughly a year into launch, EliteDNA, MedDNA, and SciDNA lagged their competitors in terms of publicity and users. A SciDNA executive expressed surprise at the firm’s unexpectedly low uptake: “Initially, perhaps we got ten people a day using the service [on] a good day. . . . I thought this was a brilliant area that was just going to take off.” A MedDNA executive attributed similar disappointing progress to elements of its regulation-anticipating approach: “[The product] was a very serious, kind of scary, hard-to-approach type of service that might have been too daunting, with a price point that may have served as a barrier.”

Leaving aside regulation in initial strategy formulation

GeneKing and GeneBuzz took a different tack at the outset, approaching regulatory uncertainty with equanimity. As an analyst wrote in 2009, “Although [GeneBuzz] is headquartered in [a U.S. state], where regulators and legislators have been more publicly attentive to direct-to-consumer genomics companies than perhaps anywhere else in the world, GeneBuzz’s CEO does not sound overly concerned.” Apparently indifferent about possible future regulatory interventions, neither venture incorporated regulatory considerations in formulating their initial strategy.

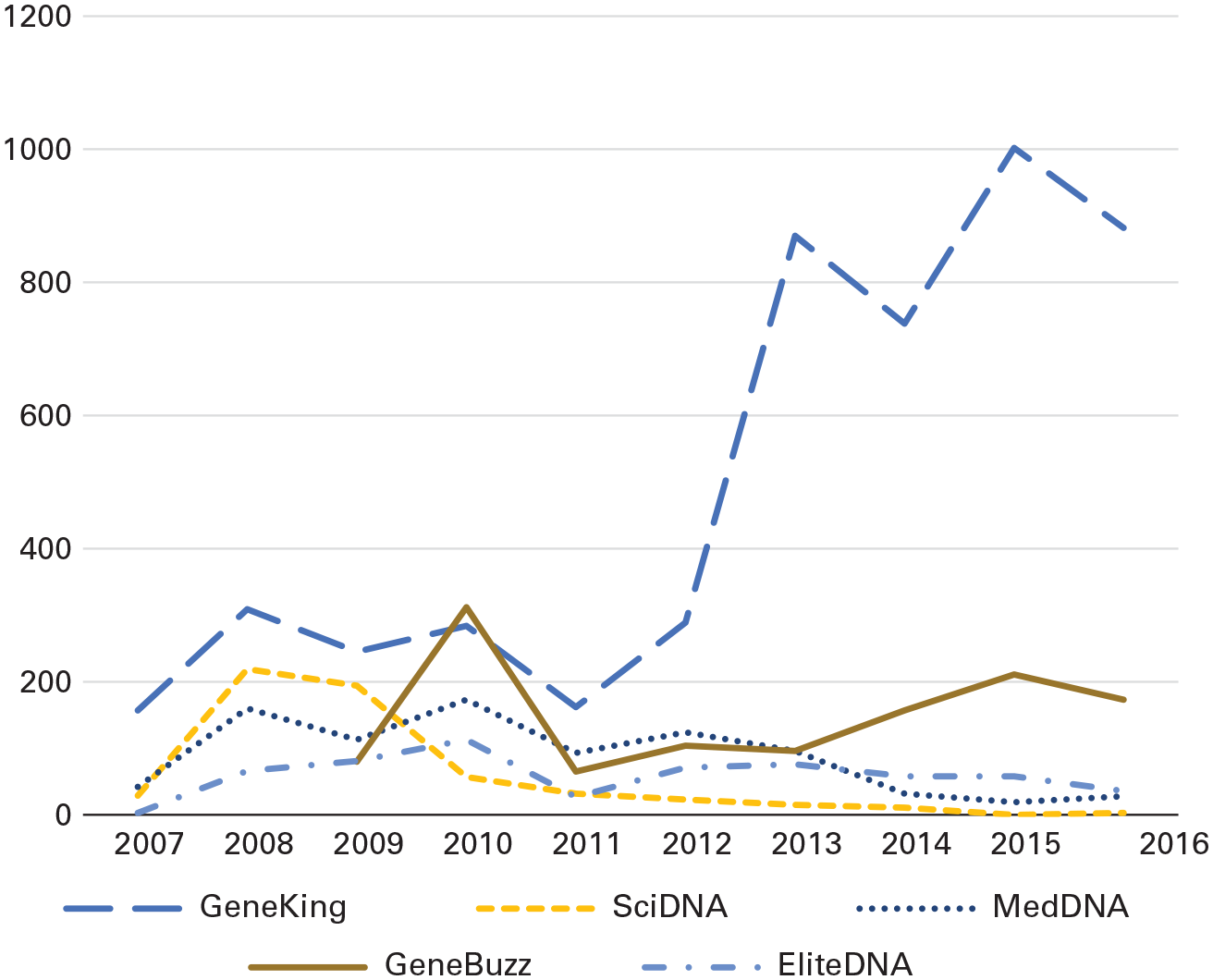

GeneKing illustrates. To amplify consumer appeal, GeneKing maximized the number of health conditions it reported on and offered additional information about ancestry and other non-health (“whimsical”) conditions, noted a product executive. GeneKing’s product reported on 128 health conditions, in contrast to MedDNA’s 28 and SciDNA’s 47. (Though capable of reporting on the same number of conditions, the others chose not to do so to project medical seriousness and avoid regulatory crackdowns due to inaccuracy.) GeneKing also pursued mass-market consumers, despite many industry observers’ belief that the typical consumer was unqualified to interpret genetic information. 7 Nor did GeneKing position intermediaries (doctors or genetic counselors) between its product and the consumer. Instead, the company developed new mass-market-friendly features, such as social networking between users who shared certain genetic traits—an option that MedDNA had considered but rejected, in keeping with its medically rigorous image. An executive at a competing venture complimented GeneKing’s strategy of catering to consumers: “[They] very smartly would seed single questions that were just a single click from a multiple choice [and] did a very good job of making people feel engaged.”

GeneKing’s product and engineering teams were hesitant to compromise the core product by adopting constraints to potentially placate regulators. “The engineering team was like, ‘Look, we can’t do this. It will kill our ability to build the product. . . . Any restriction on my ability to do whatever I want is a bad thing inherently,’” recalled a finance executive. Although a few employees had regulatory expertise, the policy team was understaffed and given low priority by senior management. An executive explained,

There was really [very few people at the company] who had ever been in a regulated company before. . . . The CEO would go to a meeting about the [big-box retailer] project rather than a meeting about making decisions about what should be submitted in the [regulatory] 510(k) . . . that would be postponed out three weeks.

Like GeneKing, GeneBuzz did little to incorporate regulatory considerations into its initial strategy. Over the objections of industry observers, it targeted the mass retail market—potentially the largest and most lucrative customer segment. And because GeneBuzz had launched a little later than the four other firms, it prioritized attention-getting actions and rapid market penetration. At its launch, for instance, GeneBuzz announced a distribution deal with a large U.S. pharmacy chain, the first such partnership in the personal-genomics industry. A marketing executive explained that GeneBuzz was solely focused on publicity: “You come out, you make this big splash—‘Oh, we’re selling tests at [drugstore chain].’ I mean, that’s a pretty shock-and-awe marketing strategy.” It also tailored its value proposition by offering a lower price than its competitors and designed its product around ease of use. A leading magazine exclaimed, “Direct-to-consumer (DTC) genetic testing has been offered for some time now, though not at this low of a price. Its affordability aside, GeneBuzz’s DNA test is also fabulously easy.”

Compared to competitors perceived as lower-regulatory-risk bets, GeneKing and GeneBuzz raised less money in their initial year of launch than did MedDNA ($9 million and $13 million, respectively, versus MedDNA’s $25 million). A prominent venture-capital firm even divested from GeneKing to invest in MedDNA—an unusual move in venture capital and a seemingly strong public endorsement of MedDNA’s strategy and prospects. However, GeneKing and GeneBuzz generated more market traction than their three competitors; GeneKing attracted the most media mentions in its initial year, and GeneBuzz was close behind. EliteDNA, MedDNA, and SciDNA also trailed in user uptake: in the industry’s first three years of existence, MedDNA counted 20,000 users and SciDNA fewer than 10,000; EliteDNA had 100 high-net-worth clients. Meanwhile, GeneKing accumulated 35,000 users, and GeneBuzz’s widely publicized pharmacy-chain deal would make its product readily available to the mass market. Table 4 summarizes these strategy formulation considerations.

Anticipating Regulation: Formulating Strategy Amidst Regulatory Voids (2007–2010)

Mechanisms and interpretation

Prior research on nonmarket strategy, grounded in resource dependence theory, has emphasized direct regulatory engagement via co-optation tactics like lobbying and political connections to manage regulatory uncertainty and dependence (Pfeffer and Salancik, 1978; Hillman, 2005; Shi, Gao, and Aguilera, 2021). Our comparative case analysis suggests, however, that different mechanisms may be at play in nascent industries. We posit that, in the context of regulatory voids in the early stage of a nascent industry, a delay in incorporating potential regulatory considerations into strategy formulation could actually help a venture achieve greater market traction. How could this be?

First, such delay may facilitate problem solving. Not taking into account regulatory considerations during strategy formulation allows ventures to optimize (or satisfice) on a smaller number of value dimensions, which facilitates broader search and reduces the complexity of a fundamental nascent-industry problem: attaining product–market fit. Conversely, incorporating regulatory considerations early on makes an already hard problem even harder. (It may also be unclear which initiatives regulators will ultimately take issue with.) MedDNA, for example, guarded against hypothetical regulatory risk by integrating counseling (contributing to its high cost and price point) and by reporting only on disease conditions whose association with genetic variation had the most stringent scientific support (lowering the value and novelty of its offering). As an industry observer pointed out, “It’s hard to justify the extra expense on the grounds of clinical value: in essence, MedDNA provides you with less information than its competitors (because it doesn’t offer ancestry or non-disease gene testing).”

Delay also potentially allows for extended discovery and learning about a nascent industry. During an unregulated interval, ventures can experiment, learn from customer reactions, and improve their products; prematurely incorporating attentiveness to potential regulation may foreclose this option and constrain search (Rivkin and Siggelkow, 2006). Finally, delay could guide efficient use of resources: when ventures preemptively adjust their strategies to forestall hypothetical regulator objections, they may guess incorrectly which issues—privacy, accuracy, accessibility, etc.—regulators will act on. This approach can lead to inefficient use of scarce resources that could have been used more productively to refine the core product. The opportunity cost of resources is particularly acute for new ventures whose executives have limited time and money (Eisenmann, 2006), are boundedly rational (Gavetti and Rivkin, 2007; Greve and Seidel, 2015; Cohen, Bingham, and Hallen, 2019), and thus cannot do everything at once (DeSantola, Gulati, and Zhelyazkov, 2022). Prioritizing becomes especially important. Insights from our comparative case data suggest that ventures that constrain their initial strategy in anticipation of hypothetical regulatory action may face greater subsequent market-traction challenges, compared to competitors that do not do so.

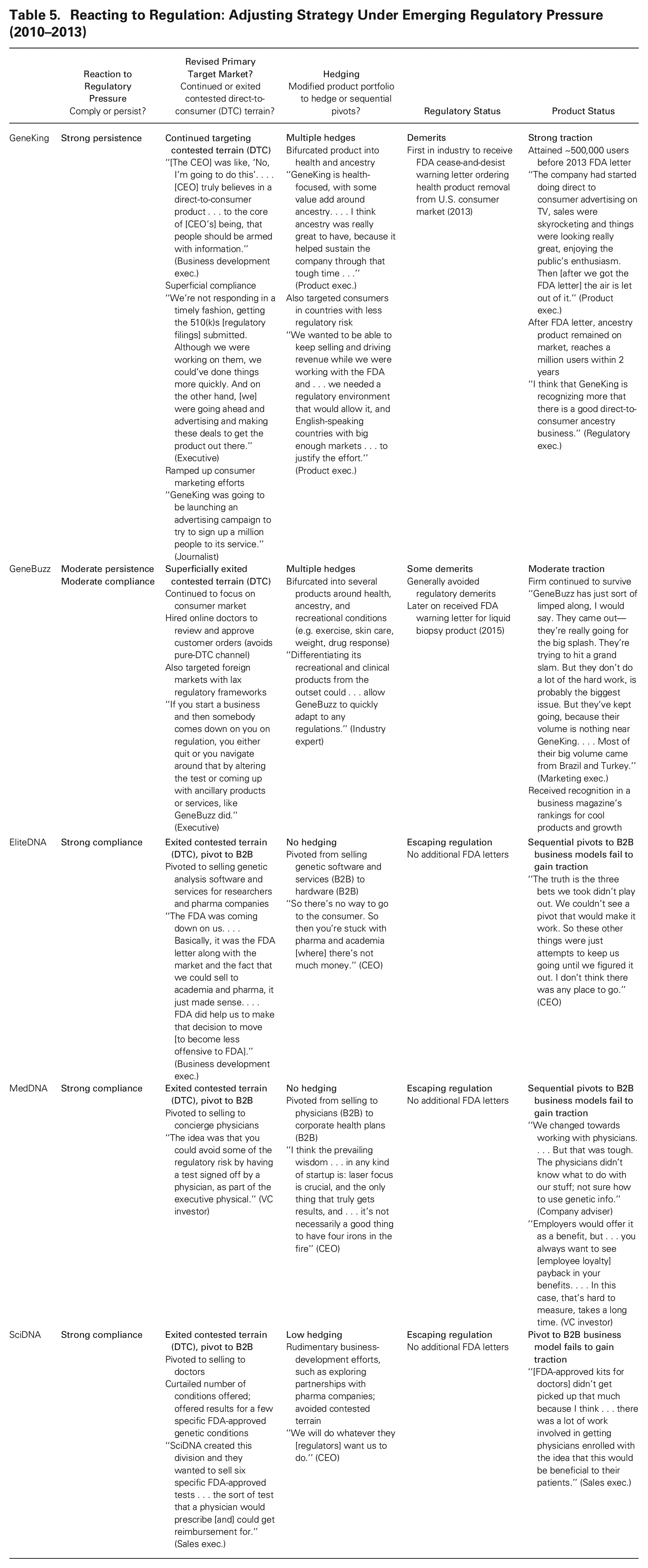

Reacting to Regulation: Adjusting Strategy under Emerging Regulatory Pressure

Within three years of the industry’s founding, regulators at both the state and federal levels began to take a more active posture. State regulators acted first. In early 2008, New York State’s Department of Health sent cease-and-desist letters to genetic-testing firms, citing physicians’ lack of involvement in the direct-to-consumer process; California followed suit in mid-2008. But the most significant regulatory event occurred in 2010, following GeneBuzz’s announcement of its distribution partnership with a leading U.S. pharmacy chain, which a newspaper termed “the boldest move yet to bring personalized genomic science to the mass market.”

GeneBuzz’s action triggered federal regulators, the FDA, to abruptly declare regulatory jurisdiction over the industry. The agency sent a letter to all five firms warning that it considered DTC genetic tests to be medical devices and that each firm needed pre-market FDA approval before selling to consumers. Mass-market consumers elicited particular attention: citing its duty to “protect the public,” the agency asserted that inaccurate tests could lead consumers to take drastic actions. “It is not unknown for women to take out their ovaries if they are at high risk of ovarian cancer,” a lead regulator declared to the media. The letter represented a strong signal from the FDA, which had previously been noncommittal about whether and how the industry would be regulated. Yet the warning left room for interpretation. First, the ventures were not explicitly ordered to take their products off the market until they received approval. The rationale, according to a public statement from the lead regulator, was that “it would be unfair to remove the tests from the market because the [FDA] had not clearly told the companies that the devices needed approval.” Second, the FDA was apparently open to discussion with executives who doubted that their firms’ products required FDA review.

Despite regulators’ intervention at both the state and federal levels, regulatory uncertainty thus persisted in the personal-genomics industry. “No one has a clear understanding of where the FDA is drawing the line at this point,” observed an industry analyst. Perhaps, he mused, the FDA itself did not know what it wanted and was “trying to keep up with a commercial space that is moving way faster than they are capable of.”

Reacting via compliance

The five ventures reacted differently to regulatory actions. A key point of divergence was whether ventures complied with emerging regulatory pressure by changing their strategy to better align with regulators’ concerns or persisted in elaborating their strategy despite the FDA’s objections. MedDNA, SciDNA, and EliteDNA took the compliance route. To them, the letters signified an increasingly risky and more closely scrutinized regulatory environment; they yielded to regulatory pressure by fully shifting away from the consumer segment flagged by the FDA, changing their strategy’s scope from the consumer segment (B2C) to target businesses instead (B2B). This lowered their perceived regulatory risk, since FDA scrutiny focused on potential harm to mass-market consumers.

Of the five ventures, MedDNA complied most thoroughly. The FDA had asserted that personal-genomics products must be “analytically and clinically accurate so that individuals are not misled by incorrect test results.” The company reacted by voluntarily halting sales to individual consumers altogether. Moving to a B2B model, it shifted its focus to concierge doctors: physicians who provide personalized care to wealthy patients on an annual-retainer basis. As one of its investors observed, MedDNA reduced its perceived regulatory risk by selling to “informed doctors” instead of “uninformed consumers.” Given FDA concerns about accuracy, MedDNA acquired its own government-certified (CLIA) lab. (Most of its competitors outsourced samples to a certified lab.) Rather than complying only when the law compelled it, MedDNA sought, in the words of an industry analyst, “to comply with the most stringent requirements currently in place.”

Even as MedDNA struggled to gain traction in the market, this approach yielded several regulatory wins. As the first venture to overcome initial state-level regulatory challenges, it became the “only personal-genomics company with approval to operate in all 50 states,” according to one analyst. Company executives expressed satisfaction at having met their goal of receiving no more FDA letters, thus avoiding additional scrutiny and negative publicity. But scaling up in the physician market required a large and expensive sales force to educate doctors, few of whom were familiar with personal-genomics technology. Expanding beyond the small concierge-doctor segment proved difficult. “One of the challenges was [that], as soon as you got out of that concierge-type world, physicians just literally did not have the time to learn about it or to integrate it,” explained a product executive. Thus MedDNA pivoted to a different B2B segment: persuading large corporations to include personal-genomics services in employees’ benefit plans.

EliteDNA and SciDNA also acquiesced to regulatory pressure. Following the FDA letters, for example, SciDNA’s CEO promised in a media interview that “we will do whatever [regulators] want us to do.” Both ventures responded by changing their strategies’ scope―that is, by abandoning the large, lucrative consumer segment. Both opted for a B2B model. Rather than wealthy individual clients, EliteDNA targeted academic research institutions, marketing genomic analysis software and services to research labs. Such institutions, executives reasoned, posed minimal regulatory problems. EliteDNA’s CEO reflected on the move:

We all got the [FDA] letters at the same time. . . . We said, “Who else can pay? There’s obviously big pharma and academic centers [where] we don’t have to worry about regulations.” And so we pivoted. And we suspended our consumer marketing at that point. And that was a big change for the firm.

SciDNA also shifted to a B2B model, marketing FDA-approved genetic tests for specific conditions to physician groups (as an additional service that doctors could offer their patients).

EliteDNA and SciDNA also posted some regulatory wins, though slightly more modest than MedDNA’s. Because both ventures still outsourced samples to government-approved labs, they were granted market access in every state but New York and avoided further FDA intervention. But they had trouble gaining market traction for their new class of products. When EliteDNA’s genome-analysis services attracted little interest from academic researchers, the company reoriented again to sell hardware (for interpreting genetic information) to clinicians. Meanwhile SciDNA’s marketing of FDA-approved individual genetic tests to doctors faced challenges: building up a sales force to sell to doctors at scale was time-consuming and expensive (as MedDNA had already learned).

Reacting via persistence and hedging

In contrast to three of its competitors, GeneKing persisted in elaborating its original strategy. Despite regulatory pressure, it continued to focus on the lucrative consumer segment. In the face of the FDA’s expressed aim to assure that “individuals are not misled,” GeneKing doubled down on consumers, making several improvements to enhance its value proposition. In Q4 2009, for example, the company launched a relative-finder feature, allowing users to trace ancestors in any branch of their family tree, a vast improvement over the more-limited DNA genealogy tests then in common use. Over the next two years, this feature identified over 60,000 pairs of relatives and helped grow GeneKing’s user base to over 100,000. The feature was used in a prominent TV documentary series on celebrities’ ancestry; its host noted that “there is no doubt that receiving ancestry information through [this] feature is the high point for each of our guests on the show.” GeneKing’s head of product confirmed that optimizing for consumer appeal was a strategic priority:

[The CEO] had a really critical insight: just make it fun and whimsical and consumer-friendly . . . like [whether one can smell] asparagus metabolite in urine, and stuff like that. . . . People would talk about that, relate to it, and it would help demystify the abstractness [of] our DNA. . . . [The CEO] really wanted to invest in those things.

GeneKing’s reaction to regulatory pressures also embodied persistence: it complied only with directives that did not compromise its consumer focus. For example, when New York State insisted that GeneKing involve a physician in the ordering process to sell to in-state consumers, the company exited the New York market. After the 2010 FDA letters, when MedDNA, EliteDNA, and SciDNA opted to comply, GeneKing publicly questioned the FDA’s stance, asserting that “people have the right to know as much about their genes and their bodies as they choose.” GeneKing continued to sell (and advertise) directly to consumers without involving a physician intermediary. And in 2013, in a bid to massively scale up its presence in the U.S. consumer market, GeneKing launched a multi-million-dollar TV advertising blitz.

Meanwhile, persistence went hand in hand with several hedging actions designed to establish GeneKing’s presence in market segments featuring lower regulatory scrutiny. One such action was to expand the company’s scope to international markets with less-stringent regulatory requirements, such as Canada’s, in Q1 2008. Another was to bifurcate its product into separate product lines—consumer ancestry (low potential regulatory scrutiny) and consumer health (high potential regulatory scrutiny)—in Q4 2009. The consumer-health product played directly into the FDA’s expressed reservations about extreme consumer reactions to unwelcome information or inaccurate tests. The ancestry product, by contrast, had few actionable implications. Bifurcation also proved resource efficient: a similar amount of work (through economies of scope) on GeneKing’s part would produce two products instead of one.

Unsurprisingly, maintaining its consumer orientation made GeneKing vulnerable to increased scrutiny and risk of intervention, and it suffered more regulatory setbacks (and thus more negative media attention) than its competitors MedDNA, EliteDNA, and SciDNA. In Q4 2013 GeneKing received a cease-and-desist warning letter from the FDA, shortly after launching a nationwide TV advertising campaign. The letter, which was made public, ordered GeneKing to immediately cease marketing and selling its health product and asserted that it had ignored the FDA’s entreaties and failed to validate its product to the agency’s satisfaction. Given no choice, GeneKing suspended health-related genetic tests; it continued to sell ancestry-related tests.

From a market-traction standpoint, GeneKing’s product continued to grow in popularity. Before the FDA banned its health products in 2013, the company’s focus on consumer appeal seemed to be paying off: it had already acquired around 500,000 users, far more than any of its competitors. Even after its health product was banned, GeneKing continued to grow via its presence in international markets and its ancestry product. A product executive explained the benefits of the latter as the company navigated regulatory challenges: “GeneKing is health-focused, with some value-add around ancestry. . . . Ancestry was really great to have, because it helped sustain the company through that tough time.” According to this executive, revenue from the ancestry product bought the venture time to sort out its regulatory issues.

GeneBuzz also persisted in its consumer-focused strategy, though in a less overt manner. In essence, GeneBuzz complied with the specific points of the FDA’s regulatory objection but not with its overall spirit. For example, physician signoff was required for consumers to order its product, but company-affiliated doctors could simply sign off via its website. “The doctor would just rubber-stamp it online,” a business-development executive explained. Like GeneKing, GeneBuzz also pursued hedging actions. First, having observed GeneKing, it offered bifurcated ancestry, wellness, and health products. And GeneBuzz also expanded to countries with less-stringent regulation, particularly developing countries. “We could go sell this outside the U.S. and not have all the problems,” an executive explained.

As with GeneKing, GeneBuzz’s persistence led to some unfortunate regulatory outcomes. After announcing its pharmacy-chain distribution deal in 2010, GeneBuzz received a FDA letter; the resulting negative media coverage prompted the pharmacy chain to pull out of the deal. A GeneBuzz executive explained that the media and consumers had “freaked out that you could walk into a drugstore, get your deodorant, your toothpaste, shampoo, and ‘Oh yeah, I’ll also pick up a genetic test.’ It seemed so outrageous to people.” But GeneBuzz’s market traction and related outcomes were more promising. The company had been on the verge of mass-market retail access until the pharmacy chain delayed the deal. But its hedging decision to sell internationally seemed to pay off: much of its initial sales volume after the FDA warning letter came from abroad. A marketing executive noted that “Most of [GeneBuzz]’s big volume came from Brazil and Turkey,” where profit margins were acceptable and regulations less stringent. Table 5 summarizes the ventures’ reactions to regulatory pressure.

Reacting to Regulation: Adjusting Strategy Under Emerging Regulatory Pressure (2010–2013)

Mechanisms and interpretation

Via persistence and hedging, GeneKing and GeneBuzz seemed to avoid the product-traction challenges experienced by the three firms that had acquiesced to regulatory pressure by shifting away from the consumer segment to a less risky model. Why would an approach based in persistence and hedging be more effective than avoidance as a way to make progress in a nascent industry?

Our data suggest that two underlying processes may make persistence beneficial. First, a persistent venture can probe the limits of regulatory uncertainty, rather than merely speculating about whether something is allowed and basing actions on conjecture. For example, when GeneBuzz hired doctors to rubber-stamp consumers’ orders online, it was unclear how the FDA would react. The FDA did not object, and this workaround became the basis of GeneBuzz’s U.S. consumer strategy. Second, when a venture persists with its strategy, it may be able to avoid path dependence in subsequent reorientations. A venture that prematurely changes strategy due to regulatory pressure may lock onto a particular path that constrains its future reorientation options. After MedDNA reoriented from a B2C to a B2B strategy, targeting concierge doctors, its activity system shifted to that of a regulated company. When it had to reorient again after the concierge market proved unviable, it could reorient only to strategies with similar activity systems, such as regulation-safe corporate employee-benefit plans. Because its routines and activities had coalesced around regulation, reorientation to a consumer-oriented activity system would have required radical changes. When a venture shifts strategy to better align with regulators’ objections, it may also be more likely to encounter unexpected problems; such reorientations tend to occur on the fly, precluding full scrutiny of the contingencies of the new strategy.

But persistence may also invite regulatory scrutiny. In other words, probing the limits of regulatory uncertainty may generate valuable information, but discovering the boundaries can also be harmful. For example, GeneKing’s multimillion-dollar advertising campaign pushed regulators to clarify the exact parameters of their tolerance, resulting in the cease-and-desist letter. This sequence of events created some clarity in a murky regulatory environment but also put GeneKing on a difficult path. “Deliberately trying to force a battle with the FDA . . . would potentially win points for the movement [GeneKing] represents, but kill the company itself,” an industry expert observed.

This is why hedging may be a critical complement to persistence. Hedging actions counteract the downsides of persistence by providing an alternative source of revenue, publicity, and users (or an opportunity for learning) in case the core business gets shut down. GeneKing offers an example: after the cease-and-desist letter, its ancestry product kept the company afloat while it engaged with regulators to get its health products approved. Ventures with limited resources may find it costly to hedge (Eggers, 2012), since new product lines and entering new geographic markets can entail high fixed costs. The cases of GeneKing and GeneBuzz reveal a novel resource-efficient way to hedge for accomplishing dual objectives: product bifurcation.

In short, a venture could potentially respond to regulatory pressure by persisting rather than acquiescing. We posit that this approach may increase the likelihood of attaining product–market fit. But persistence may also carry enhanced regulatory risk, which ventures may be able to manage via complementary hedging activities. Thus we posit that persistence, in tandem with hedging, may be an effective way for ventures to react to emerging regulatory pressures.

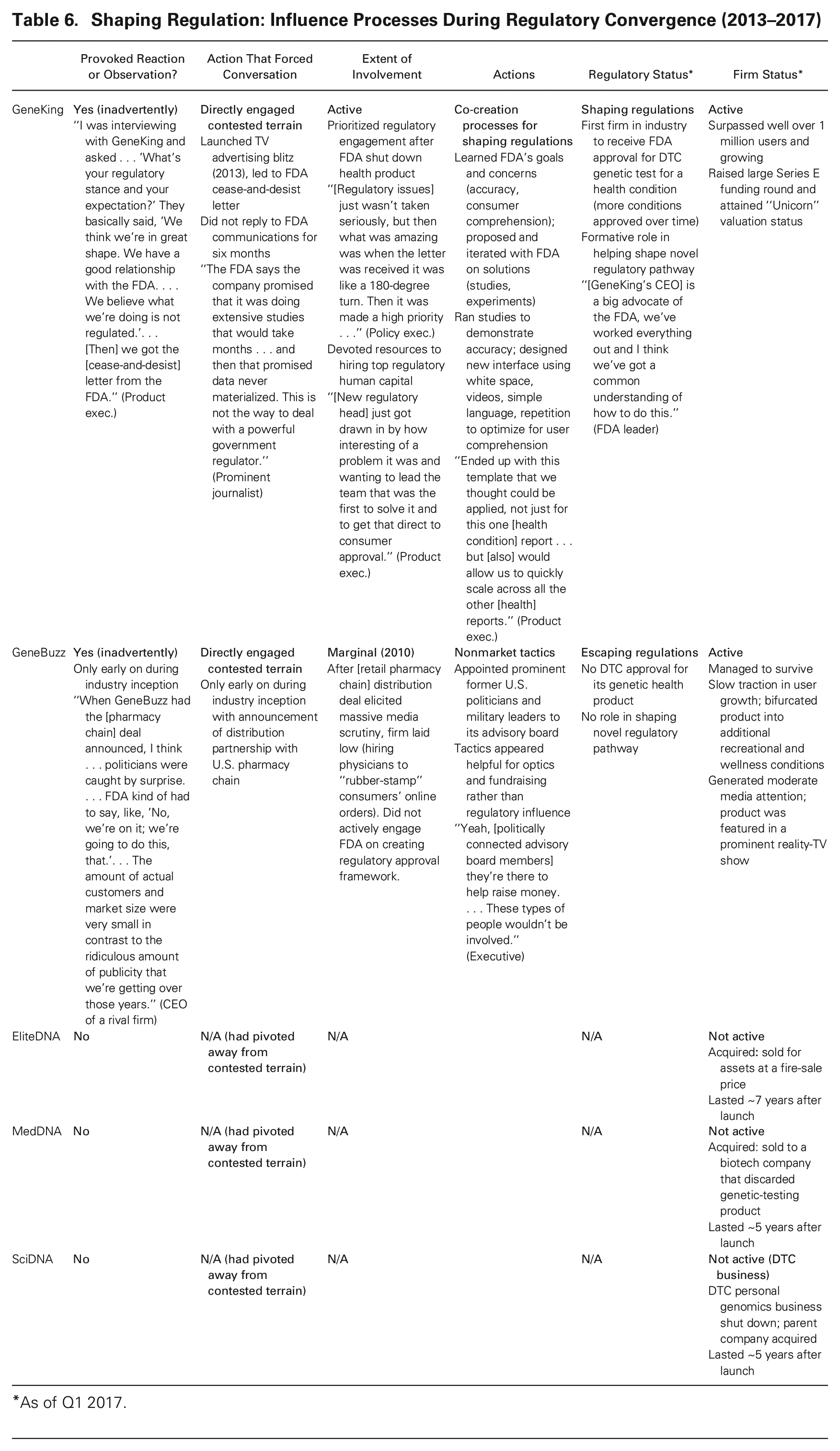

Shaping Regulation: Co-Creation Processes during Regulatory Convergence

The FDA’s sharp cease-and-desist letter to GeneKing in Q4 2013 marked a new phase in the evolution of the personal-genomics industry. By that point, the industry—more than five years after its inception—had begun to experience attrition. MedDNA had been acquired in 2012 by a biotechnology company attracted by its expertise and technology; its personal-genomics product was discontinued. SciDNA was also acquired in 2012, by a corporation eager to leverage its scientific database to develop drugs; its personal-genomics product, too, was discontinued. EliteDNA, having abandoned the (affluent) consumer market several years earlier, remained in the B2B market, but its reorientation to selling clinical hardware for genetic analysis had failed to gain traction; ultimately the company was sold for assets in 2015.

Only two significant players remained by late 2013: GeneKing and GeneBuzz. GeneKing was still selling ancestry products directly to consumers; its health products had been banned. GeneBuzz derived most of its sales from abroad; it had changed its U.S. product to focus on wellness and genetics-based fitness assessments, and it sold to consumers indirectly by authorizing affiliated doctors to rubber-stamp online orders.

By this time, the scope and direction of regulation were converging into focus. The FDA had asserted jurisdiction over the industry via the 2010 letters, and in subsequent years it had made clear what it objected to: any ramp-up in the consumer market without a physician intermediary, including direct distribution via retail chains (GeneBuzz) and mass-market advertising campaigns (GeneKing). It remained unclear, however, about what was permissible; the FDA had not created a clear pathway to regulatory approval. Meanwhile the two remaining firms differed in their approaches to shaping regulation, and they experienced different outcomes. GeneBuzz employed conventional nonmarket tactics to avoid and buffer against further regulatory scrutiny, such as challenges to its workaround of having company-affiliated online doctors rubber-stamping consumer orders. A GeneBuzz executive explained,

With the uncertainty about regulation and all, at the end of the day people want to make money; [GeneBuzz] wants to have a business. If [we] can just stay in the gray area on regulation, then [we’ll] do that.

The nonmarket tactics that GeneBuzz employed to “have a business” included campaign contributions—its CEO made large personal contributions to politicians of both parties—and political connections: the venture added several former generals, Congressional leaders, and U.S. cabinet secretaries to its advisory board and announced each appointment via press release.