Abstract

The Child Tax Credit (CTC) expansion was an extraordinary experiment not just in policy design but also in policy implementation. As such, it cast light on the possibilities and blind spots of using the tax system to deliver safety-net benefits. The rapid and widespread take-up of the benefit reflected the use of a specific implementation tool that reduced administrative burden for the public: auto-enrollment via the tax system. But use of this tool also excluded families who could benefit from the program but were disconnected from the tax system. These tended to be families with the lowest incomes. Thus, while the CTC expansion offered a classic example of “targeting within universalism” by broadening a policy’s beneficiaries while making it more redistributive, its implementation revealed that a different sort of targeting is needed to reach those with the lowest incomes and to achieve the hoped-for redistributive impact.

The expansion of the Child Tax Credit (CTC) represents an extraordinary experiment in American policy, and it is one beset by paradoxes. It succeeded in its core goal of reducing child poverty, which fell to record lows while it was in effect (Bitler, this volume; Creamer et al. 2022), but this success was not rewarded by permanent adoption of the credit. The policy’s success reflected aspects of its implementation: the federal government’s decision to auto-enroll those it could verify as eligible reduced burdens in a way that enabled a rapid and widespread take-up beyond what is typically seen with income transfer programs. But the take-up rate was lower for the poorest individuals who would benefit most from the program.

To understand the impacts of the expanded CTC, including its potential moving forward, we need to understand and resolve these paradoxes, which we argue are rooted in the policy’s implementation. The shift toward delivering social welfare benefits through the tax system, as highlighted by the CTC expansion, has important implications for peoples’ ability to access those benefits.

We apply an administrative burden perspective to unpack what went right and what went wrong with the expanded CTC’s implementation. Administrative processes matter to the quality and effectiveness of implementation. In particular, the use of the tax system, which facilitated auto-enrollment, allowed the expansion to rapidly reach most individuals with minimal frictions. But using the tax system also meant that those disconnected from it, largely the Americans with the lowest incomes, faced a different and more onerous application process. In particular, the poorest eligible beneficiaries were significantly less likely to receive the CTC compared to well-off eligible beneficiaries, despite an overall high take-up rate. While the policy design of the expanded CTC reflects the practices of “targeting within universalism” (i.e., folding low-income populations into a more universal policy), the temporary expansion came up short because implementation processes saw many of the neediest of the targeted population fail to access the program (Skocpol 1991).

Given the expansion of CTCs at the state level and the long-term potential of a federal expansion, understanding implementation successes and failures can inform future efforts. The first lesson is to address the disadvantages of delivering social welfare benefits through the tax system, including challenges with delivering benefits to people whose incomes are low enough that they don’t need to file tax returns. Moreover, the agency’s broader mission, and related organizational culture and capacity, are focused on collecting taxes rather than delivering benefits. The second lesson is to build on the advantages of delivering social welfare benefits through the tax system, such as by broadening automated payments, thereby widening the “easy lane” for those seeking benefits. To ensure better targeting, the benefit needs to be as easy to access for those with lower incomes as it is for those who are well-off—analogous to how Social Security functions. The final lesson is that the policy design needs to maximize the potential to reduce burdens, such as by limiting additional conditionality requirements beyond earnings, including work requirements.

The Goals and Design of the CTC Expansion

The central goal of the expanded CTC was poverty reduction. In particular, it sought to reach the most economically vulnerable Americans who had not been previously eligible for the credit. The most prominent advocates of the expansion, including both policymakers and academics, repeatedly noted this as the key goal. For example, Senator Michael Bennet (D-CO), a leading political advocate for the program, notes, “[as] the Superintendent of Denver Public Schools, [I] saw every day how growing up in poverty shapes a child’s future in ways that are deeply unfair. That’s why [I have] been a tireless advocate for expanding the Child Tax Credit” (Bennet 2023). Moreover, the 2019 National Academies (NASEM) report, titled A Roadmap to Reducing Child Poverty, is cited as the intellectual trigger for the 2021 expansion. It specifically argued that the CTC expansion was the most viable approach to dramatically reduce child poverty (NASEM 2019).

Why were poverty reduction advocates so supportive of this initiative? The “old” CTC, which returned at the end of the 2021 expansion, provided a $2,000 annual credit for each eligible child. The credit is not universal and is, arguably, regressive. A family earning less than $2,500 receives no credit. Further, families who do qualify, but have low incomes, receive a smaller benefit. For example, a single-parent family, including two children and earning between $2,500 and $30,000, receives only a partial credit. A key design feature driving this difference is that only a portion of the credit is refundable, meaning that beneficiaries don’t receive the full credit if it exceeds what they paid in taxes (Center on Budget and Policy Priorities 2022). The overall consequence is that the CTC is more beneficial for high-income than for lower-income families. Indeed, under current law, roughly one in four children under the age of 17 will either get no CTC benefit or a reduced benefit because their family’s income is too low, while families with incomes up to $400,000 will get the full credit (Cox et al. 2023).

A program that excludes so many families with lower incomes has limited capacity to reduce poverty. The explicit poverty reduction goal of the 2021 expansion, relative to prior iterations, was reflected not only in terms of providing more generous benefits but also in terms of expanding the populations it reached, making it a more universal program by incorporating the lowest-income households. Universalizing the credit folded in the poorest Americans, while still benefiting the middle class and even some high-income Americans. The expansion to universalism was limited by income, but now at the upper end of the spectrum rather than for both upper- and lower-income earners. The benefit phased out for single filers earning more than $112,000 and married filers earning more than $150,000. The expanded CTC was vastly more progressive. Roughly 19 million families who had either received a reduced credit or no credit became eligible (Marr et al. 2022).

Who Did and Did Not Benefit from the CTC

By December 31, 2021, almost 62 million children had received the new child tax credit (Internal Revenue Service [IRS] 2023b). Nearly all of these recipients had done little to access this new benefit, valued at up to $3,600 per child under the age of six and $3,000 per child ages six to 17. The money simply appeared, by direct deposit, in their checking accounts. In large part due to the simplicity, current estimates are that around 90 percent of those eligible received it (Curran 2022; Greenstein 2022). 1 However, as we will detail below, some groups, including low-income populations, had a bit more difficulty accessing the benefit (Curran 2022).

The CTC expansion led to dramatic declines in poverty (Parolin, Collyer, and Curran 2022; Pilkauskas et al. 2023), as well as food and housing insecurity (Adams et al. 2022; Karpman et al. 2022; Moellman, Vaughn, and Ziliak, this volume; Parolin et al. 2023; Pilkauskas et al. 2022; Shafer et al. 2022). There is some evidence that the extra payments improved adult mental health (Gennetian and Gassman-Pines, this volume) and child health as measured in terms of either healthy foods consumed or birth weights (Ruffini 2022). Studies of such effects are consistent with studies of how the money was spent—for example, on food and nutrition, routine household expenses, essential items for children, savings for emergencies, and debt payments (Hamilton et al. 2022; Michelmore and Pilkauskas 2023).

The rapidity and scale of the take-up, and the subsequent positive effects, speak to a clear policy success. But the promise of the expanded CTC to benefit the poorest Americans was not fully realized, in terms of who actually received the credit. Of the roughly 4 million children at risk of not receiving benefits for which they were eligible, most were in the lowest-income categories (Cox et al. 2021).

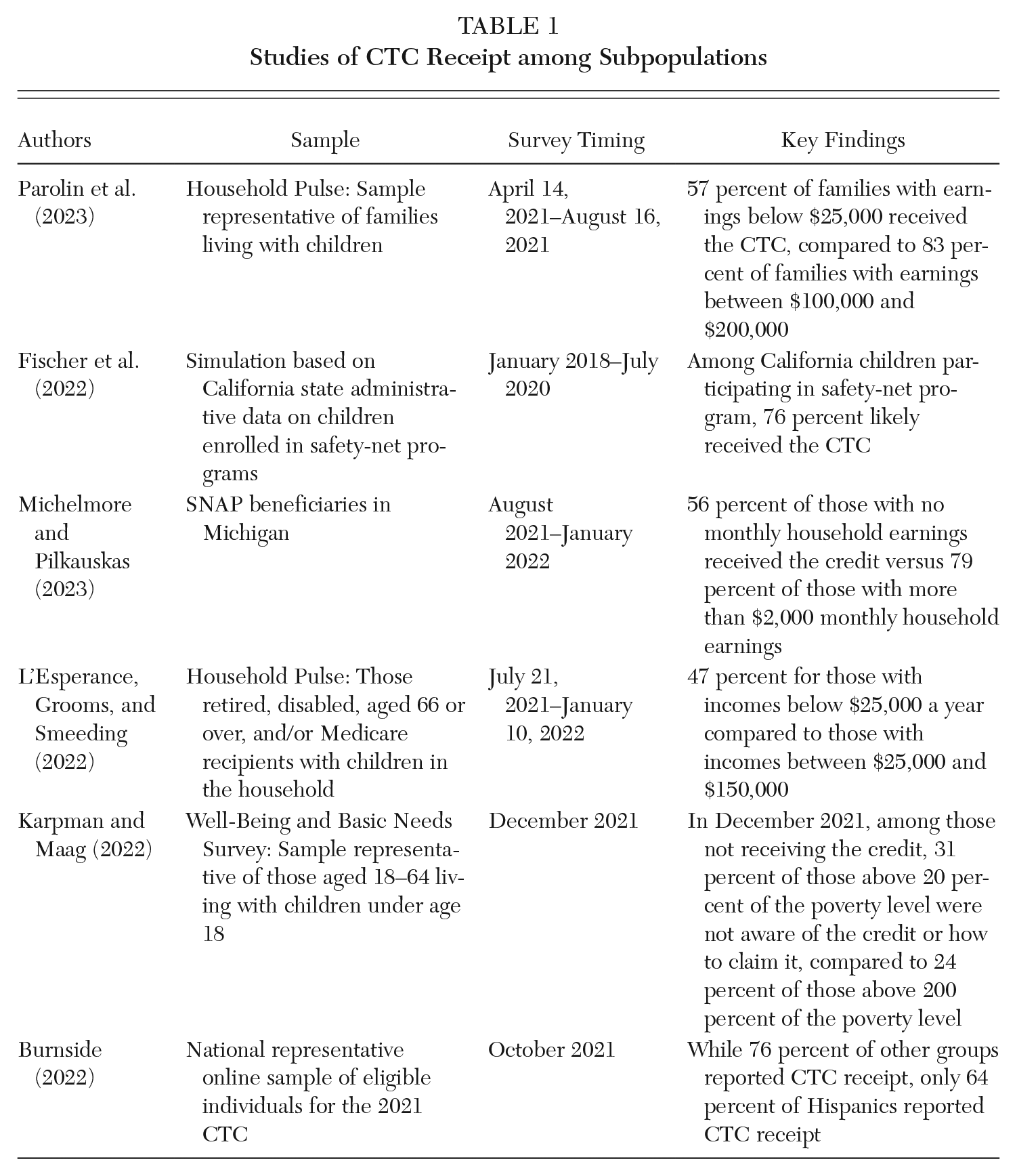

While we still don’t have precise data on the eligible nonrecipients of the expanded CTC, preliminary evidence indicates that they were likely in low-income populations. Table 1 summarizes the existing studies on the topic, which we discuss here. Analyses of California administrative data show that roughly a third of newly eligible Californian children receiving other safety-net benefits were at substantial risk of not benefiting from the expanded CTC (Fischer et al. 2022). Specifically, people with no earnings received only 58 percent of their eligible CTC dollars compared to 89 percent of those earning between $5,000 and $10,000 and 93 percent of those earning more than $10,000. While those data were simulated, data from the Census Household Pulse Survey found 57 percent of children in families earning less than $25,000 received the monthly CTC payment compared to 69 percent of families earning between $100,000 and $200,000 (Parolin 2023; Parolin et al. 2023).

Studies of CTC Receipt among Subpopulations

Further, an analysis of Supplemental Nutrition Assistance Program (SNAP) users with children in Michigan found that CTC receipt was strongly correlated with income, with the 55 to 60 percent of those with little to no income reporting not receiving the credit in a specific month, compared to 80 percent of those with income of at least $2,000. Prior tax filing was the strongest predictor of receipt. Even controlling for income, education, size of benefit, and other demographics, receipt of the CTC was strongly connected to being tied to the tax system: those who had filed taxes were 24 percentage points more likely to receive the CTC compared to those who did not (Michelmore and Pilkauskas 2023). 2 Another study found that low-income individuals were less likely to know about the credit or how to apply (Karpman and Maag 2022). More generally, additional analyses found that eligible families with lower educational levels and Hispanic families were less likely to receive the benefit (Burnside 2022; Michelmore and Pilkauskas 2023).

In sum, the implementation of the CTC dramatically increased income for many poor Americans, with almost no administrative burden impeding access. However, the initial evidence suggests that those who were least likely to receive it were disproportionately those experiencing significant poverty, thereby blunting the antipoverty effect of the program. While the precise numbers vary, the pattern across data sources consistently shows lower take-up among groups in the highest level of poverty. Both the success of the CTC and its limits reflect aspects of its policy implementation, the subject we turn to next.

The Policy Implementation of the CTC: Building an Easy Lane with Auto-Enrollment

An examination of implementation, or administrative choices, can help clarify why the promised benefits for very poor Americans were not fully realized. Both the aggregate high take-up levels and the failure to reach those who needed extra help or support are explained by a closer look at the implementation process.

To understand the CTC implementation process, we use an administrative burden framework. This framework centers on people’s experiences of state programs and, in particular, the frictions they encounter in policy implementation (Herd et al. 2023). When it comes to applying for social safety-net benefits, these frictions can come in the form of learning costs (knowing about a program, one’s eligibility, and the application processes), compliance costs (completing forms, providing documentation, and satisfying other bureaucratic requirements), and psychological costs (emotional responses to these experiences, such as stigma, stress, fear, or frustration) (Herd and Moynihan 2018). Even relatively minor burdens might discourage take-up, and as such costs mount, take-up is likely to decline.

The administrative burden framework also suggests that burdens will be experienced more by some groups than by others. This disparity might be a reflection of individual differences; for example, those with poorer physical and mental health are more likely to struggle with burdens (Bell et al. 2023). Moreover, structural factors might see some groups more targeted with burdens than others. For example, individuals receiving Medicaid face much higher burdens accessing those benefits than do individuals accessing tax-subsidized employer-based coverage. White and higher-income Americans are more likely to benefit from low-burden employer-based coverage (Ray, Herd, and Moynihan 2023). As a result, burdens might reinforce existing patterns of inequality.

Policymakers can minimize burdens in a variety of ways, including informational nudges, outreach, simplified administrative processes, and the provision of help to clients. The Biden administration has encouraged such actions through a series of executive orders and agency guidance that combine a mixture of advice for agencies to offer and reporting requirements for them to follow (Herd et al. 2023).

Perhaps the most powerful implementation tool for reducing burdens is auto-enrollment. While what auto-enrollment means varies in practice, here, we refer to it as the principle that state actors use administrative data to proactively enroll and maintain individuals in a program or other administrative category. For clients, auto-enrollment changes the default choice: rather than requiring them to seek out and apply for a program, the state does this for them, while still providing them with the option to opt out.

There is substantial evidence of the power of auto-enrollment in generating greater participation in programs. Indeed, the use of auto-enrollment for pensions is one of the foundational examples from behavioral science on the power of choice architecture (Thaler and Sunstein 2009). Individuals are much more likely to save for their pensions if the default does not require them to opt in to a savings program, an insight that has changed how many governments structure pension options (Government Accountability Office [GAO] 2022). The use of auto-enrollment can have positive distributive effects. For example, Arulsamy and Delaney (2022) found that automating pension savings was especially helpful for those with poorer mental health.

Auto-enrollment matters not just for initial application for a program but also for programs that require ongoing renewals. Changes to the Medicaid enrollment process under the pandemic-related Public Health Emergency offer an example. During this time, states were not allowed to drop participants from Medicaid and thus effectively adopted an auto-renewal program that eliminated the traditional problem of clients’ churning off the program during renewal periods. To give a sense of the enormity of this problem—and by extension, the potential benefits of auto-enrollment—Dague and Ukert (2023) estimated the effects of suspending Medicaid renewals during the pandemic. They found that this unplanned auto-renewal led to a greater increase in health care coverage than the Affordable Care Act. A simple but powerful change in administrative processes mattered more to coverage than the biggest health policy expansion of recent decades.

The expanded CTC minimized burdens for the vast majority of those eligible by employing auto-enrollment. To do so, it relied on the tax system to deliver the benefit. This choice reflected a broader shift to turning to the tax system as a means of delivering social services in recent decades. The growth of the CTC, even before its expansion, and the Earned Income Tax Credit (EITC) coincided with a decline in cash welfare programs like Temporary Assistance to Needy Families (TANF). The turn to the tax system has facilitated the rise of what has variously been described as the “hidden” welfare state (Howard 1997) or the “submerged” state (Mettler 2011) and has raised concerns that reliance on the tax system inhibits awareness about crucial programs and forestalls democratic debate about them. But it has also minimized the types of burdens that claimants could expect to encounter in their dealings with the state, while also reducing the financial costs of administering programs (Herd and Moynihan 2023).

The reliance on the tax system minimized burdens in a number of ways even before the CTC expansion. First, because clients were likely to already be dealing with the IRS through their annual tax payments, claiming a benefit was tied to a familiar and routine administrative process. They did not need to deal with a separate set of bureaucracies with idiosyncratic rules that might vary by state or locality or to satisfy a separate set of administrative processes (Herd et al. 2023). Second, the connection with the tax system minimized learning costs in other ways. Even if clients were unfamiliar with the specifics of the CTC or EITC, tax preparers offered a broadly available pool of helpers to navigate this process (although this brings its own compliance costs in terms of additional fees). The connection to the tax system, and by extension to one’s work, also minimized the types of psychological costs associated with perceptions of undeservingness (Howard 1997). The cultural norms of the IRS, as well as the practicalities of the tax system, have led it to rely on ex post audits rather than ex ante burdens to identify and reduce potential fraud (Herd and Moynihan 2018).

Auto-enrollment provided additional advantages with the expansion of the CTC. Policymakers leveraged tax data to identify who was eligible and to provide them the benefits automatically. Those who had filed a tax return in either 2019 or 2020 received an automated payment in their bank accounts. For those who were newly eligible, no additional steps were needed. Such an approach reflected the urgency of pandemic policymaking. Stimulus payments were also provided via automatic enrollment, with the IRS using administrative data on income and dependents to process the payments. The use of monthly payments helped to distinguish the CTC from other pandemic-era programs, making it more closely resemble a child allowance payment provided in other countries.

It was this use of tax data and automatic enrollment that allowed such enormous and rapid take-up. For the newly eligible for whom the IRS had data, there was no need to learn about their eligibility or the program, no additional forms to complete, and no psychological costs.

Such distributions via the tax system, however, can come with substantial burdens. The largest problem is that many low-income Americans are disconnected from the IRS. Around 10 percent of Americans don’t file a tax return (Cilke 2014; Zucker and Wagner 2021). This group is mostly low-income Americans who don’t earn enough to pay taxes. Only those with income above a minimum threshold ($18,800 for head of household filers and $25,100 for married filers) are required to file. The reach of auto-enrollment, however, is a function of the comprehensiveness of the administrative data that fuels it. IRS tax data don’t include those who don’t file (Gale and Marron 2012; Robertson, Zucker, and Olson 2020).

As the poorest families are less likely to participate in the tax system, so too are they less likely to gain benefits distributed through that system. Indeed, this is an issue in the other large tax benefit program for low-income Americans, the EITC. Nonfilers, who constitute about two-thirds of the 20 percent eligible for the EITC, don’t receive it (Robertson, Zucker, and Olson 2020). Because the expanded CTC was not taxable income, this removed one source of complication for claimants. In short, the CTC did not affect their eligibility for other social welfare programs.

Those who had not recently submitted tax returns could apply for both Economic Impact Payments (EIP) and the CTC via the IRS online portal. If they succeeded in applying for the EIP, they would be automatically enrolled in the CTC. An estimated 720,000 children received the CTC via this channel (U.S. Department of the Treasury 2021). But again, burdens mattered. Learning costs loom especially large for new programs or programs that have substantially changed. One-third of seemingly eligible claimants who said they did not apply for the benefit did not believe their family was eligible, while one in four said they were unaware of the credit or did not know how to claim it (Hamilton et al. 2022; Karpman and Maag 2022). They also had to negotiate an unfamiliar administrative process and overcome whatever psychological concerns they might have had about the program, including potential fears of the IRS. For example, parents who were undocumented immigrants and needed to file with their Individual Taxpayer Identification Number were reluctant to participate, reflecting the fear and uncertainty such populations feel about engaging with formal government systems, even if their children are eligible for benefits (Code for America 2022). Because this population was disproportionately lower-income, they were more likely to be experiencing scarcity, which is associated with greater difficulty in overcoming administrative burdens (Christensen et al. 2020). And because all of this occurred at a time when the IRS customer service capacities were struggling from a lack of resources, claimants had little hope of gaining direct help from IRS employees.

The design of the online portal for nonfilers to claim the expanded CTC was initially poor, garnering headlines like “Democrats Have a Plan to Slash Child Poverty, but It Goes through a Shoddy Website” (Golshan 2021) and “The IRS’s Child Tax Credit Portal ‘Looks Like Crap and It’s Not Really Usable’ for Low-Income Americans Trying to Get $300 Monthly Federal Payments” (Zeballos-Roig 2021). There was no Spanish-language version or mobile-friendly option, even though those with low incomes are more likely to own a smartphone than a desktop computer. The language in the application process reflected the formality of the tax system. To design this portal, the White House initially had worked with Intuit, the maker of TurboTax, and a partner in a much-criticized “free file alliance” that had offered a shoddy version of free electronic filing and lobbied strongly against the IRS producing its own free electronic filing system.

By October, the much-criticized IRS nonfiler tool stopped accepting applications. By this point, the White House had partnered with Code for America, a civic tech nonprofit, to offer GetCTC, a website though which people could submit their applications. Code for America had experience designing user-friendly safety-net digital interfaces. GetCTC was mobile-friendly and available in Spanish, and its interface was designed in simplified language rather than the formal jargon of a tax return form. About three-quarters of filers using the tool used their smartphone and completed the application within 30 minutes. This implies that simplified reporting structures help reach much of the hard-to-reach population. Code for America estimated that one in four of those who used GetCTC had never filed taxes in their lives, and more than half were people of color. Code for America emphasizes the efforts needed to engage nonfilers: “The eligible non-filers we sought were the proverbial needles in a haystack, and as such, most outreach efforts required huge volumes of outreach to generate a meaningful number of returns” (Code for America 2022, 3).

The U.S. Department of the Treasury and the White House had sought to reach this population through outreach campaigns, outreach tool kits, and navigator training. The White House even declared a Child Tax Credit Awareness Day in 2021. We lack rigorous evidence about the effectiveness of these efforts. Informational nudges, if well-targeted and well-communicated, can have positive effects on enrollment in cases where learning costs are an issue. Providing direct help to users to deal with compliance costs can be even more consequential (Herd et al. 2023). But the effect of such efforts pales relative to the impact of auto-enrollment.

Overall, the design of the expanded CTC created two dramatically different paths for participants. Auto-enrollment created an easy lane, one with almost no administrative barriers. But those not already engaged in the tax system faced a hard challenge. In aggregate, lower-income Americans were made significantly better off by the use of auto-enrollment, but those with the lowest incomes were more likely to struggle to access the CTC.

Lessons for the Future

Targeting within universalism depends upon implementation

The implementation of the CTC also poses a challenge to how we think about “targeting within universalism,” which Skocpol (1991, 414) defines as leveraging “universal policy frameworks for extra benefits and services that disproportionately help less privileged people without stigmatizing them.” The logic of targeting within universalism is that redistribution becomes more politically feasible within the guise of universalism. Programs like Social Security and Medicare, which reflect this approach, effectively redistribute resources while maintaining political resilience.

The policy redesign of the expanded CTC followed the targeting-within-universalism playbook. The base of beneficiaries was expanded, and the distribution of resources became more progressive by incorporating families with lower incomes. In this respect, it reflected both the shift toward using the tax system as a means of building the safety net and the limits of an approach that directs increases in safety-net spending for children to families with earnings and income above the poverty line (Hoynes and Schanzenbach 2018). Making the payments refundable and removing the income requirement would ensure that the CTC would become a more progressive tax credit.

But what the CTC expansion shows is that it’s not enough to design a universal policy; rather, the program needs to be implemented in a way that ensures the targeting actually happens. The administrative burden framework speaks to the limits of targeting within universalism. The use of the tax system, with its limited connection to low-income Americans, meant that, although every category of client benefited from auto-enrollment, implementation was vastly different for different populations. Where higher-income individuals experienced almost no burden with an automated payment, many low-income individuals experienced significantly greater burdens, often to the point that some did not receive benefits to which they were entitled. This stands in stark contrast to Social Security, a classic example of successful targeting within universalism, where low- and high-income beneficiaries face the same burdens.

The accidental welfare agency must invest in safety-net implementation

Through a series of discrete policy choices that expanded the use of the tax system to deliver benefits, while reducing most other types of welfare, the IRS has become the organization with the greatest responsibility for making the safety net more accessible (Herd and Moynihan 2023). In many ways, the IRS is an accidental welfare agency. Like most public organizations that generally resist taking on tasks they see as beyond their core function, the IRS and its state counterparts did not seek this status (Wilson 1989).

Close observers of the IRS have noted its resistance to shifting the organizational culture and practices to focusing on expanding access to safety-net resources (Olson 2017; Wielk, Carothers, and Snyderman 2022), especially as the U.S. experiments with programs that look like universal income guarantees. The mission statement of the largest federal agency distributing safety-net benefits—“provide America’s taxpayers top quality service by helping them understand and meet their tax responsibilities and enforce the law with integrity and fairness to all”—does not mention engagement in the welfare system.

This reluctance stems partly from the larger failure to invest in sufficient resources to meet the new demands placed upon the agency. This situation may, belatedly, be changing. Under the Inflation Reduction Act, the IRS has gained new resources that allow it to improve customer service, including creating a Customer Experience Office. Moreover, it has experimented with outreach to likely eligible clients, encouraging them to apply for benefits like the CTC and EITC. Simplifying the tax-reporting system would reduce the number of nonfilers, in turn allowing auto-enrollment to reach a broader audience. The plan to pilot IRS-provided free electronic filing, with the possibility of prefilled tax data, brings this closer to reality (IRS 2023a).

Lessons from the implementation of the expanded CTC point both to what the IRS should keep doing and to areas for improvement. For those who do not complete returns, Congress could still increase take-up via a combination of outreach and simplified portals (Robertson, Zucker, and Olson 2020). The IRS has contact information for the vast number of nonfilers to pursue this approach. Moreover, the IRS and the Social Security Administration already have the longest-standing, and perhaps the closest, data-sharing arrangements across nearly all federal agencies. Closer coordination, including additional data sharing, could facilitate these kinds of outreach efforts, as well as possibly facilitate more auto-enrollment.

Widen the easy lane, target the hard-to-reach

The rapid and high take-up rates of the CTC point to the benefit of an implementation process designed to minimize administrative burdens. In particular, auto-enrollment effectively allowed the IRS to shift burdens away from individuals. Because the expanded CTC did not include more of the lowest-income groups—although it could have—it failed to fully reach its redistributive goals. The solution is not to abandon tools such as auto-enrollment but, rather, to broaden those who are participating in the tax system and engage better with those who are not. When the expanded CTC expired, so too did auto-enrollment. But the centrality of auto-enrollment to the success of the CTC suggests it should be a more broadly used tool—and not just for the CTC; for example, the one-third of eligible EITC nonrecipients who are filers could be automatically enrolled (at least for childless households [Robertson, Zucker, and Olson 2020]).

Auto-enrollment depends upon (1) the existence of sufficient administrative data, (2) legal permission, (3) political willingness, and (4) administrative and technological capacity to use the data for enrollment purposes. Such conditions are not always present. In some cases, the data do not exist or do not provide the necessary information to satisfy eligibility requirements. One particular challenge with the CTC is dealing with families with complex living arrangements—for example, cases where multiple individuals might be eligible for claiming the benefit. Legal constraints on the sharing or use of data can be significant. It may take years to design cross-agency or state–federal data-sharing agreements. Much of the legal permission framework at the federal level has evolved little since the 1970s, even as the potential for administrative data has dramatically increased. While the IRS is constrained by statute, in terms of how it shares data, it has much broader latitude within the tax system. Political opposition, directed to particular programs or the client base they aim to serve, may also discourage the use of auto-enrollment to make those programs more accessible, and this opposition may also work toward limiting administrative resources that reduce burdens. That said, government agencies also need to overcome other barriers, such as resistant organizational cultures.

In addition, administrative data can be used to reduce burdens in ways other than auto-enrollment—that is, by identifying and communicating with likely eligible beneficiaries and even prefilling their applications. For example, SNAP and Medicaid data could be crossmatched with IRS data to identify likely eligible nonparticipants (Greenstein 2022), and administrative data could be used to share prefilled forms with users (Code for America 2022).

Minimize predictable burdens in policy design

Beyond the administrative strategies discussed above, policy design also matters for administrative burden. This point is relevant both for any attempt to reintroduce the expanded CTC at the federal level and for states in the process of expanding state CTCs now.

The easy lane of program access calls not only for introducing specific implementation tools like auto-enrollment but also for designing policies that make the use of those tools feasible. The more criteria that policymakers wish to see satisfied, the less likely it becomes that state actors can verify those criteria without input from clients, in turn triggering more administrative burdens and limiting the reach of the programs.

This is not a hypothetical concern. For example, Senator Joe Manchin (D-WV), who critically opposed a longer-term CTC expansion, pointed to a desire for work requirements: “Let’s make sure we’re getting it to the right people. There [are] no work requirements whatsoever. . . . Don’t you think if you want to help the children, the people should make some effort?” (Herd and Moynihan 2021). Similarly, Republican senators open to expanding the CTC saw work requirements as a core feature of such an expansion. But work requirements generate significant administrative burdens that reduce program take-up (Gray et al. 2023). While the IRS or state tax agencies might be able to verify work for many, they cannot capture more nuanced work patterns (such as the number of hours per week). Documenting exceptions for work requirements (such as for retirees, the disabled, or those in education) would also generate new hassles for applicants to overcome. Thus, while policy design choices that add eligibility criteria might make it more politically feasible to broaden the generosity and reach of the CTC, they come with a high risk of excluding many because of resulting implementation difficulties.

In addition to the risks associated with work requirements, other policy design choices can add administrative complexity and increase burden at the state level. For example, making credits only available for very young children—a common requirement—introduces learning costs. Likewise, a benefit available only for a short period reduces the probability that people will learn about it and actually access it. States sometimes require either a Social Security number or an individual taxpayer identification number (ITIN). Common among immigrants without a Social Security number, the ITIN is especially difficult to obtain. Legislation should provide statutory flexibility regarding how residence is actually documented. More broadly, ways to enhance access (such as providing tax agencies with more flexibility and budgetary support for outreach efforts) are also critical components to policy design.

Conclusion

The expanded CTC was one of the most significant experiments of social welfare policy in recent decades. The policy design, which was to effectively target resources to the poorest Americans in the context of a more universal policy, reflected a long-standing, and often successful, political strategy of targeting within universalism. What we demonstrate, however, is that even as implementation choices largely improved access, the lowest-income populations faced the most significant administrative burdens.

Poverty reduction advocates were elated about the passage of the temporary expansion of the CTC. Many hoped that it would prove to be effective and popular enough that policymakers would feel compelled to continue it. In The Atlantic, Annie Lowrey (2022) wrote, “[H]ow the policy failed to create its own constituency is the $100 billion question, of interest to the Democratic politicians hoping to reinstate it as well as to experts designing new social programs in the future.” But once the temporary CTC expansion expired, it expired. The most straightforward mechanical explanation is that temporary programs like the CTC expansion need affirmative decisions merely to continue to exist. 3 A wave of popular support to continue the expansion never emerged, and the incorporation of the CTC into the tax system may have played a role (Mettler 2011). People struggled to see the program as distinct from a flurry of other pandemic-era programs, including stimulus-check payments that were also tied to the number of dependents. Nor did Democrats, by and large, make the CTC a campaign issue. And, finally, the short-term nature of the CTC expansion limited the ability of the government and advocates to fully implement outreach.

Proponents of an expanded CTC remain hopeful. Just a few years ago, a policy considered marginal is now a widely embraced goal among Democratic policymakers. In some ways, this reflects a pattern of policy change fueled by ideas and evidence among insiders rather than mobilizing mass publics. Increases to the CTC relied on political horse-trading with conservatives willing to expand the safety net via tax credits in return for maintaining tax cuts—a bargain that has made the tax system the most politically feasible vehicle for CTC expansion (Greenstein, this volume). The aftermath of the expansion gives advocates not just an idea but mounds of evidence to persuade policymakers to continue the fight for this policy. This evidence matters beyond the federal level. States have been actively expanding their own CTCs. New Mexico, New Jersey, Minnesota, Oregon, and Utah created new CTCs in 2022–2023. California, Colorado, Maine, Maryland, New Jersey, New Mexico, New York, and Vermont expanded their CTCs in 2022–2023 (Davis and Butkus 2022). With the exception of Utah, all of those states now have refundable tax credits, the most innovative aspect of the federal expansion to reaching those with the lowest incomes (Davis and Butkus 2022). As the expansion of the CTC evolves, whether at the federal level or via state supplements, it is critical that implementation tools to improve access to the benefits are not overlooked.

Footnotes

Notes

Pamela Herd is a professor of public policy at Georgetown University. Her research focuses on the consequences of inequality and ways to reduce it. Her book, Administrative Burden, coauthored with Donald Moynihan, is the winner of multiple best-book awards and has helped inform recent executive actions to reduce burden in federal benefit programs.

Donald Moynihan is a professor of public policy at Georgetown University in the McCourt School of Public Policy. His research seeks to improve how the government works. His book, Administrative Burden, coauthored with Pamela Herd, is the winner of multiple best-book awards and has helped inform recent executive actions to reduce burden in federal benefit programs.