Abstract

National health care costs have doubled over the past 10 years to 3 trillion dollars accounting for 18% of the gross domestic product in 2018.

1

In general surgery, laparoscopic cholecystectomy (LC) is the most commonly performed operation in the US and remains a popular focus for cost reduction interventions. These studies mainly focus on cost outcomes; however, the success of these projects is directly related to the organizational changes made by the hospital and surgeons.

2

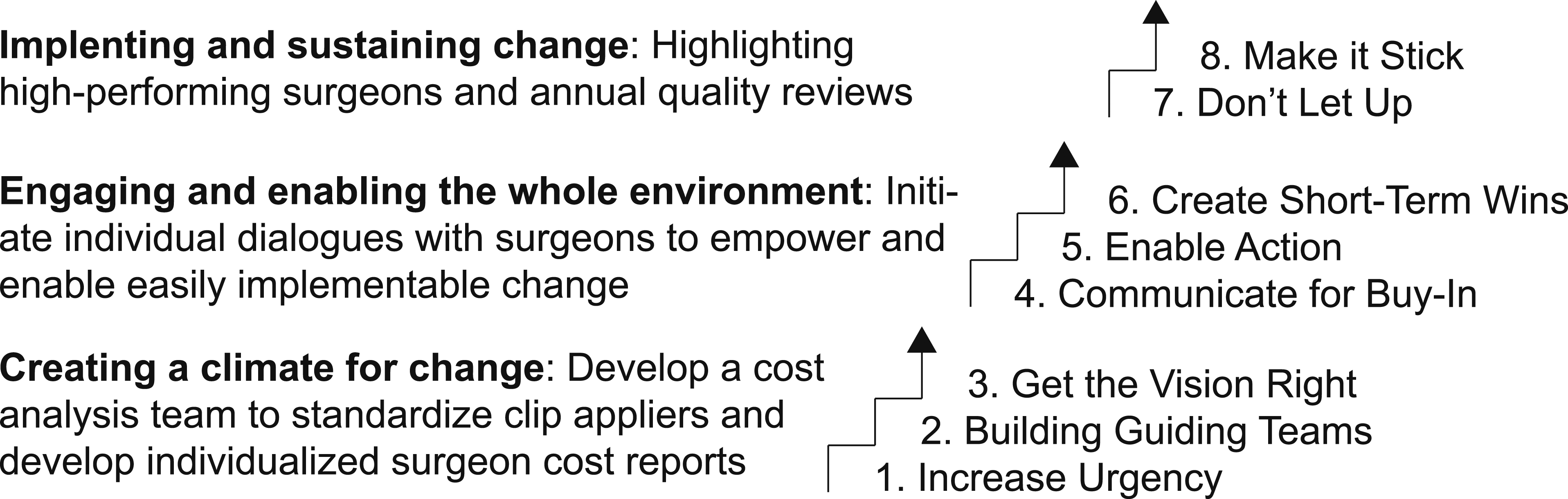

The field of change management aims to ease these struggles in order to create effective and sustainable change. Kotter’s theory of change management uses a nonlinear 8-step model focusing on creating a climate of change, engaging and enabling the whole organization, and implementing and sustaining change (Figure 1).3,4 The aim of our study was to better understand the cost variation of LCs and develop an intervention substantiated by Kotter’s theory of change management that could easily be adopted and implemented by surgeons. Kotter’s theory of change managment.

Starting with creating a climate of change, a cost analysis team, also described as the guiding team by Kotter, was developed to analyze cost reports and implement a strategy to decrease the cost variations associated with LCs. Cost analysis of the pre-intervention data identified the laparoscopic clip applier device as the highest driver in cost variation. The cost analysis team developed a clear vision of decreasing cost variation in LCs by universalizing the clip applier for all surgeons. Aimed at creating a sense of urgency for change, individual surgeon report cards were sent via email and presented at a faculty meeting, displaying their average associated costs of LC compared to all other surgeons in the department. To engage and enable the whole environment, each surgeon was then individually approached by the cost analysis team to engage in dialog and communicate the vision for change. If the surgeon agreed to universalize their clip applier, all the necessary changes were made by the cost analysis team, making the change more seamless and effortless for surgeon. The intervention was not forced upon any surgeon. If they did not initially agree, they were reapproached to assess their willingness to participate. The guiding team wanted to ensure the surgeon was empowered to change through evidence-based decisions and not forced to make another practice change due to administrative cost savings.

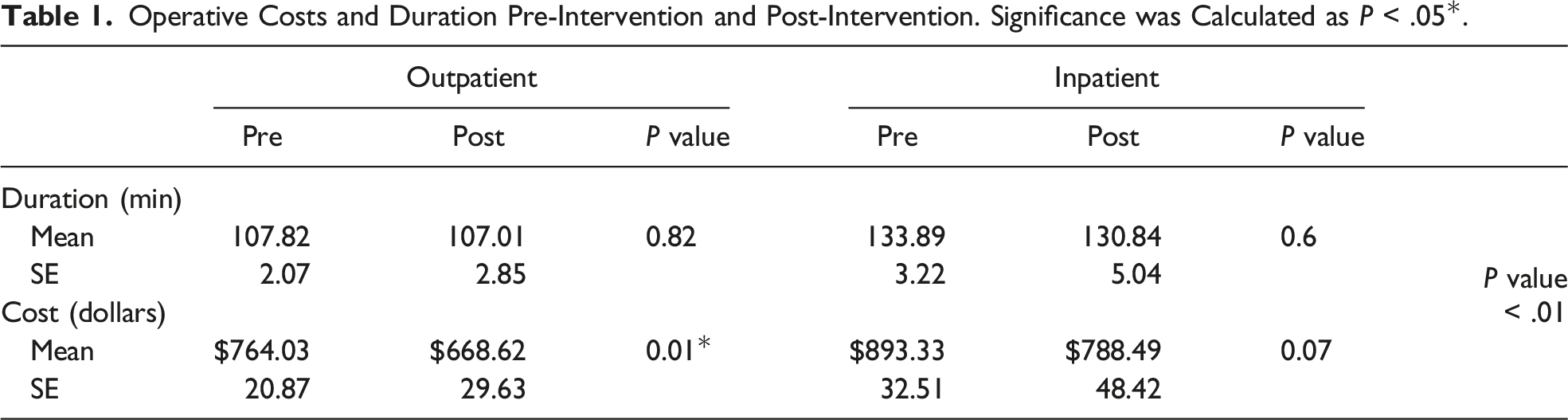

Retrospective cost analysis was performed between July 2017 and July 2018 on all LCs at a large academic hospital. Cases were queried from the hospital electronic medical record by Current Procedural Terminology codes for LC (47562, 47563). In total, for pre-intervention, there were 154 inpatient and 285 outpatient LCs included for analysis. The following variables were analyzed: operation date, patient status (inpatient vs. outpatient), case duration, and cost. The operation cost was calculated as the sum of each item’s cost multiplied by the number used. The same process, criteria, and variables were collected for the post-intervention data between October 18, 2020, and March 19, 2020. In total, for post-intervention, there were 73 inpatient and 129 outpatient LCs included for analysis. Two-sided student’s T-tests were used to compare means between continuous variables and Pearson’s chi-squared tests were used to compare categorical variables with a significance value of P < .05.

Operative Costs and Duration Pre-Intervention and Post-Intervention. Significance was Calculated as P < .05*.

We present an interventional study to decrease operative supply costs for LCs using Kotter’s change management theory. Implementation of Kotter’s change management theory effectively created a climate of urgency and change within the Department of Surgery. Importantly, these changes were not forced adaptations; all changes were voluntarily adopted and evolved under surgeon guidance. Surgeons were empowered to make lasting change through a clear vision and easily implementable policy. As a result, both outpatient and inpatient operative supply costs decreased from pre-intervention to post-intervention.

Our study uses a well-established change management theory to allow for easily adoptable standardization of supplies and surgeon report cards to reduce the operative supply costs for LCs. We show that Kotter’s change management framework is implementable within an academic surgery department and effective at reducing costs. For outpatient procedures, supply costs and standard deviation decreased between the pre-intervention and post-intervention groups. Inpatient procedural costs decreased between pre-intervention and post-intervention groups; however, there was an increase in standard deviation. This discrepancy is likely due to an unrepresentative inpatient post-intervention group limited by sample size. This is a retrospective single institution study with a limited sample size and the results should be interrupted with caution. The sample size of the post-intervention groups is limited compared to the pre-intervention groups.

Future studies will focus on the third aspect of Kotter’s theory of change management, implementing and sustaining change. High-performing surgeons will be highlighted at morbidity and mortality (M&M) conferences during dedicated quality improvement time. In addition, surgeons will receive monthly report cards to remind them of the changes they are enabling for their patients and the hospital system. Monthly results will also be presented in aggregate at M&M conference to the entire Department of Surgery. In conclusion, provision of surgeon specific cost data can lead to surgeon-initiated preference changes which can lead to system level decreases in supply cost for a common surgical procedure.

Footnotes

Author Contributions

Shawn M. Purnell: statistical analysis, manuscript preparation, critical revision

Kevin Y. Pei: manuscript preparation and critical revision

Alexi Bloom: conception and design

Julie Tilton: conception and design

Karen Dickinson: conception and design

Feibi Zheng: conception and design, manuscript preparation, and critical revision

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.