Abstract

Among the numerous legislative initiatives implemented around the globe on digital platforms, some of these provisions are explicitly directed toward app stores. As they have all the distinctive features of multi-sided markets, app store owners represent the prototype of digital gatekeepers, controlling access to mobile ecosystems and competing with business users operating on the platforms. In light of the rule-setting and dual role of these gateway players, regulatory interventions are required in order to ensure that large app stores are treated like common carriers or public utilities, thereby imposing upon them a neutrality regime vis-à-vis new entrants. For the very same reasons, dominant app store providers have been subject to an increasing number of antitrust investigations attempting to ensure equal treatment and to avoid self-preferencing at the expense of rivals’ services. Against this background, the article investigates whether antitrust provisions are flexible enough to curb anticompetitive practices carried out by app stores and the extent to which regulatory interventions could, on the other hand, be necessary in order to address the seemingly unique features of the app economy.

I. Introduction

App stores are at the forefront of the debate on the regulation of the digital markets. Indeed, they represent the prototype of multi-sided platforms, having all their distinctive features: the presence of significant indirect network effects and economies of scale and scope leading to highly concentrated and not easily contestable markets; the growth in ecosystems providing a variety of products and services that serve as vital gateways for business users to reach potential end customers; the control and intermediation power exerted by gatekeepers, which act as private regulators, determining the terms and conditions under which users can join the network, playing a dual role as both intermediaries and trading operators on the platform.

With regard to app stores, the gatekeeping position of Apple and Google, and the related concerns about their rule-setting and dual role have been the subject of market studies launched by the Australian Competition and Consumer Commission (ACCC), 1 the Netherlands Authority for Consumers & Markets (ACM), 2 the U.K. Competition and Markets Authority (CMA), 3 the Japan Federal Trade Commission (JFTC), 4 and the U.S. House of Representatives. 5 Furthermore, the terms and conditions for accessing app stores, such as in-app purchasing rules and restrictions on the freedom of choice regarding payment apps on smartphones, are being scrutinized by courts and antitrust authorities all around the world. Moreover, numerous legislative initiatives have been implemented to safeguard market contestability and establish a level playing field by promoting regulatory approaches that essentially aim to characterize large digital platforms as common carriers or public utilities in order to impose upon them a neutrality regime. Notably, a new ex ante regulatory regime has been advanced in the European Commission’s Digital Markets Act (DMA) proposal and in the CMA’s code of conduct aimed at governing online platforms with “gatekeeping” position or “strategic market status,” respectively. 6 In pursuing the same goal, Germany has strengthened its national Competition Act (GWB), introducing a new Section 19a which sets specific standards of conduct for undertakings of “paramount significance for competition across markets.” 7 In a similar vein, in June 2021, the U.S. House of Representatives unveiled a five-bill antitrust package designed to curb the market power of large online platforms representing “critical trading partners.” 8

This approach was endorsed by the European General Court in the recent Google Shopping 9 case. The Court relied on a principle of equal treatment, considering it to be a general principle of the European Union (EU) law inferred from case law applied to public undertakings. 10

Despite their differences, the legislative initiatives cited above do share the same aims and concerns. By and large, the call for action stems from the hurdles experienced by antitrust enforcers, aiming to remedy an enforcement failure. 11 With regard to the digital markets, antitrust is considered to be falling short mainly because competition rules apply ex post and require an extensive investigation on a case-by-case basis. Therefore, corrective tools are required to speed up the enforcement process and to achieve the result of prohibiting certain practices.

Against this background, some of the obligations envisaged are clearly addressed to app stores in an attempt to introduce a platform and device neutrality regime. Notably, the European DMA, the German Section 19a, and some of the U.S. bills (in particular, the American Choice and Innovation Online Act, and the Augmenting Compatibility and Competition by Enabling Service Switching Act, and the Ending Platform Monopolies Act) prohibit, for instance, the designated platforms from: discriminating between users by engaging in self-preferencing and applying unfair access conditions; preventing users from sideloading (i.e., installing apps without going through an app store) and un-installing pre-installed apps; impeding data portability and interoperability; and imposing anti-steering provisions. Moreover, in August 2021, an ad hoc app store bill (“Open App Markets Act”) was introduced in the U.S. Senate to reduce “gatekeeper power” in the app economy. 12 Finally, although the U.K. regime follows a principle-based rather than a rule-based approach that relies on firm-specific codes of conduct, the CMA has also suggested a range of procompetitive interventions (including third-party access to data, interoperability and common standards, interventions to overcome consumer inertia and default bias, obligations to provide access on fair and reasonable terms, and separation remedies) that cannot be achieved via codes of conduct and would have a major impact on app stores. 13 In its Interim Report on mobile ecosystems, the CMA has considered possible interventions aimed at addressing Apple and Google’s market power, which include allowing sideloading and removing anti-steering provisions and restrictions to alternative payment options for in-app purchases. 14 The findings of the CMA’s market study on mobile ecosystems will provide information on how the regime is designed and implemented by the newly appointed Digital Markets Unit, supporting the development of codes of conduct in relation to app stores and the potential use of the aforementioned procompetitive interventions.

However, the very first country to approve legislation on app stores was South Korea. Its Legislation and Judiciary Committee, indeed, supported the amendment to the Telecommunications Business Act which, among other things, will prohibit app store operators in dominant market positions from forcing payment systems upon content providers and inappropriately delaying the review of, or deleting, mobile contents from app markets. 15

Against this background, this article aims to investigate whether antitrust provisions are flexible enough to keep up with the dynamics of digital app stores and whether regulatory interventions are, on the other hand, required in order to address their unique features.

The work is structured as follows. Section II describes the role and economic features of app stores. Section III analyses antitrust investigations and private litigation initiated against Google and Apple stores by focusing on the different practices at stake. Section IV illustrates the regulatory initiatives recently implemented to address the seemingly distinctive features of the digital markets and the strategic role played by large online platforms. Section V explores how the main anticompetitive practices within app stores can be tackled by current antitrust rules and the potential role played by regulation in bridging the enforcement gaps. Section VI concludes.

II. App Store Ecosystems

The economic features of the digital economy are epitomized by the structure of mobile ecosystems in which consumers can access a variety of products, contents, and services through an app store, embedded in a specific operating system, which is, in turn, installed on a smart device. Indeed, app stores represent an essential component of mobile ecosystems which, built on the combination of an operating system and mobile phone, have emerged as digital infrastructures on which a huge number of retail and social interactions now take place. Notably, working as distribution channels, app stores act as a catalyst, governing interactions between app providers and mobile users. They are essentially a gateway giving app developers access to such new digital markets by offering their apps to users of a specific mobile operating system. Similarly, consumers use them to search, update, install, and remove a wide array of applications from their devices.

The two most predominant mobile operating systems, namely, Apple’s iOS and Google’s Android, come with their own closely integrated app stores (App Store and Play Store) and web browsers (Safari and Chrome). 16 Apple allows users and developers to use only the App Store while Google strongly encourages the use of its own Play Store, which is pre-installed on devices that comply with Android’s compatibility requirements. Although consumers perhaps only notice minimal divergences between the two, for developers, the experience can be quite different. Indeed, iOS-based and Android-based platforms embrace two different business models. While the former is a walled garden, being vertically and exclusively integrated throughout the whole mobile value chain (running from app stores to devices), the latter is an open ecosystem with competitive and independent manufacturers producing the devices and Google managing the Play Store.

Although Google is said to have gradually followed a walled garden approach aimed at keeping users increasingly within its ecosystem, 17 the business model adopted still differs from Apple’s, and this differentiation is crucial for the antitrust analysis. 18 Indeed, while the latter generates revenue primarily through device sales (device-funded ecosystem), the former’s main source of revenue is through digital advertising (ad-funded ecosystem). 19

From an economic perspective, app stores magnify the features of multi-sided markets and the multi-layered architecture of ecosystems. According to the literature on multi-sided markets, an app store enables interactions between two or multiple groups of users that would not be able to capture the value generated by their interaction if it were not for the platform. Furthermore, it influences the volume of transactions by applying asymmetric prices to groups working on different sides. 20 The value of the service offered by the platform to one group increases with the number of such users as well as the number of participants in the other group (direct and indirect network effects). 21 Due to the interdependence between the groups that interact through the platform, an app store needs to bring (and keep) both sides on board, thus gathering and ensuring a sufficient number of agents on every side in order to reach a critical mass to trigger indirect network effects. Finally, access to data might influence the ability to compete, granting to app store controllers informative advantages as a result of their role as intermediaries.

The combination of these economic distinctive traits gains prominence in terms of competition dynamics. Indeed, platforms may benefit from self-reinforcing effects, which favor the emergence of highly concentrated markets. The more users are attracted to the platform, the more the platform is considered valuable, the more data are collected, the more the service provided can be improved, and the more the user is encouraged to stay within the digital ecosystem and is discouraged from switching to competing services.

One consequence of these characteristics is also the presence of economies of scope and the development of conglomerate structures, which assist us in understanding why, in digital markets, the competition is increasingly between the ecosystems. 22 Once a digital ecosystem has been established, it attracts hardware, devices, software, apps, websites, and a varied range of complementary services. This centripetal force facilitates the creation of an ecosystem based on technical standards, which can pose serious protocol interoperability problems and increase switching costs and lock-in scenarios. Indeed, the need to ensure that everything is compatible with each other favors the development of the ecosystem around a dominant design, whose controller may be considered an orchestrator. 23 As platform providers strive to become the default gateway to online content and services, competition is essentially for the market, rather than on the market.

However, in accordance with the natural dualism of multi-sided markets, the very same economic factors that allow mobile ecosystems to grow also represent the main threats to their success, requiring a difficult balance to be struck in order to ensure the ecosystem continues to thrive and so as not to dissuade a specific user group from engaging with the platform. Indeed, it has been noted that a platform ecosystem resembles a meta-organization, combining a set of product or service providers, users, and advertisers. 24 As a consequence, the value created is not fully under the control of the platform owner but depends upon the participation and actions of content and service providers (complementors). Therefore, platform ecosystems are extremely sensitive to bad behavior. 25 Such bad conduct by users generates negative externalities, which in turn reduce economic efficiency, make the platform less attractive, and could ultimately disrupt the entire ecosystem. For these reasons, governance is crucial to the success of digital ecosystems, and multi-sided platform owners must take action to preserve the value and integrity of their ecosystems. They must address potential market failures by adopting a variety of legal, technological, and informational measures, regulating access to and interactions around their ecosystems. 26

In general terms, the main justifications offered by platforms for their governance policies apparently reflect vital needs, namely, to ensure the financial sustainability of the platform, the quality of the content or services provided, and the quantity and quality (including security) of interactions between users. Notably, with regard to app stores, some payment restrictions have been introduced to address concerns related to the financial viability of the platform: Apple and Google seek to justify the use of their in-app payment systems through which they collect fees for certain purchases based upon the argument that this is how they are able to prevent developers from free-riding on app store investments.

Governance of platform access also plays a significant role in influencing interactions between app developers by incentivizing their value creation activities (such as development of innovative complements and knowledge sharing), which are critical to the attractiveness of the ecosystem. 27 For instance, bringing large numbers of software application producers on board may generate crowding-out effects, undermining complementors’ incentives for developing apps. 28 In essence, if app stores are becoming so overwhelmed by the offer of apps that providers are struggling to stand out and attract users to their app, the lower profitability for app developers may lead to a decline in product innovation and a consequent loss of value for the ecosystem. For the same reason, app stores are attentive to the ranking and featuring of apps in order to reduce consumers’ search costs and increase the discoverability of apps.

Similarly, due to indirect network effects, the quality of apps may affect the profitability of the entire ecosystem. 29 Therefore, in line with the aim of increasing the overall value of their ecosystem, app stores have an incentive to review and monitor apps, gathering as many qualitatively good apps as possible. 30 From this perspective, the need to minimize negative externalities represents the main justification put forward by Google for imposing anti-fragmentation agreements upon device manufacturers, preventing them from using any alternative version of Android not approved by Google. Indeed, fragmentation is a significant threat and a recurrent problem in open-source platforms 31 : if device makers are free to “fork” Android to create bespoke versions, incompatible versions may emerge, undermining the integrity of the operating system and making it vulnerable to negative externalities.

Finally, app stores have an incentive to exert control over apps in order to protect users, guaranteeing security, privacy, and safety by mitigating threats from vulnerable apps and keeping malicious and privacy-invasive apps out of the app store. 32

However, by establishing rules to mold the behavior of users, platforms act as private regulators self-entitled to incentivize, penalize, and even exclude some figures, which inevitably generates disputes and investigations. 33 There is systemic disagreement, in the case of app stores, as to whether the refusal or removal of an app meets a legitimate justification or if, by contrast, it is just a pretext for stifling competition, especially when, as a result of the dual role of the app store owner, a competitive app is involved. Furthermore, due to architectural and governance control, platforms may have leverage and incentives to manage their ecosystems in order to strengthen their bargaining power vis-à-vis business users and to influence consumer choices.

In short, by and large, the challenges brought about by the economic features of multi-sided digital platforms affect all stages of the antitrust analysis.

Based upon the relevant market definition, competition authorities need to assess not only whether different mobile ecosystems are separate markets but also whether the multi-sidedness of the market should be considered as a whole, rather than looking at only one side in isolation. By facilitating a direct transaction between two groups of users, app stores belong to the category of transaction platforms, which should require an integrated market approach, at least according to a strand of economic literature 34 endorsed by the U.S. Supreme Court in Amex. 35

The role played by app stores within mobile ecosystems and the importance of ecosystem competition also support the need for a bespoke approach to the digital markets by replacing the market definition concept with the ecosystem concept. 36 In this respect, the recent market study carried out by the CMA on Apple’s and Google’s mobile ecosystems precisely seeks to assess the interconnections between the different markets. 37 In a similar vein, relying on new powers assigned by Section 19a GWB, the German Competition Authority has opened an investigation to determine whether Apple holds a position of paramount significance across the markets thanks to the creation of a digital ecosystem 38 : the main focus of the investigation will be on the operation of the App Store as it enables Apple to influence the business activities of third parties. Finally, in its Android decision, the European Commission referred several times to the concept of ecosystem and considered mobile ecosystems to be different markets on their own while app stores were considered to be mere aftermarkets within which the platform owner is a near-monopolist. 39

Furthermore, when it comes to determining the level of market power enjoyed by an undertaking, the competition authorities would need to carry out a preliminary assessment covering the platform’s degree of diversification and the relevance of its network effects as well as the possibilities enjoyed by users on each side of transacting over alternative platforms (multi-homing). Accordingly, in 2017, the German legislator updated the national antitrust law introducing new criteria which, particularly in the case of multi-sided markets and networks, must be considered in addition to the existing criteria for the assessment of market power. Pursuant to Section 18(3) GWB, the new criteria include direct and indirect network effects, the parallel use of several services and the switching costs for users, economies of scale arising in connection with network effects, access to data relevant for competition, and competitive pressure driven by innovation.

Moreover, the aforementioned dualism of multi-sided markets should necessarily influence the antitrust evaluation of the behaviors and strategies implemented in app marketplaces. Due to network externalities, the circumstances in which a practice may determine a restriction of the market are exactly the same as those in which it may generate procompetitive effects. Therefore, the features of platform economics and the dualistic competitive interpretation of behaviors require, in principle, the antitrust authorities to assess the effects of a specific practice (rather than considering it, by its very nature, to be harmful to competition) and to make a judgment on counterfactual hypotheses in order to measure the actual impact on competition. This would allow the authorities to evaluate whether the behaviors in question are justified economically by testing the realistic scenario that would occur if the investigated conduct were absent and giving appropriate consideration to the business model applied by the platform. Indeed, as acknowledged in the special advisers’ report for the European Commission, the efficiencies of certain practices in the platform economy are “not yet well understood and our knowledge and understanding still needs to evolve step by step.” 40

III. Platform-Related Behaviours Targeted in Antitrust Disputes and Investigations

The vast array of ongoing antitrust disputes and investigations concerning app stores provides a fascinating insight into the more contentious issues involving the conduct of app store providers worldwide. At their heart, in relation to the app economy, these legal actions are based upon a threefold competitive concern. First, Google and Apple enjoy a gatekeeping position by which they control access to their mobile ecosystems autonomously. Second, they have the ability to act as private regulators by establishing rules that apply to all players using the app store. Third, as the two companies perform the dual role of competing within their own platform alongside other businesses and policing the same marketplace, conflicts of interest threaten to hamper competition. Such factors, coupled with scale and speed in the use of data online, are leading the antitrust authorities to believe that several business practices that, until now, have been considered perfectly legitimate could be seen as exclusionary abuses of market power when it comes to the online platform economy. However, it is worth considering that such practices and policies take place against the broader background of interplatform competition in which Apple and Google are competing with each other to attract and retain customers on their mobile ecosystems. Therefore, it is crucial to ensure that any measures proposed to increase competition within mobile ecosystems do not jeopardize competitive pressure between mobile ecosystems.

Self-preferencing represents the most egregious example of the difficulty in assessing the behaviors of app stores from a competition policy perspective. This term usually refers to the ability of a gatekeeper to favor its own services over those of third-party providers hosted on the same platform. 41 However, various business practices can fall within this vague concept. 42

As Google and Apple are in charge of the technical architecture underpinning their respective mobile ecosystems, on a purely technical level, self-preferencing may initially arise from restricted forms of interoperability between the mobile ecosystem and independent apps. 43 For instance, the application programming interfaces (APIs) necessary for making full use of the hardware and software components of a device may not be freely and thoroughly accessible from third-party apps, limiting their ability to offer certain services or to provide adequate levels of product quality and customer experience to compete on a level playing field with Apple and Google.

Furthermore, by controlling the user interface, app stores enjoy additional leeway for undermining third-party apps. First and foremost, they have substantial discretion over the functioning of ranking and auction algorithms displaying apps to consumers, which allow platforms to place the apps they prefer at the top of search results or in a prominent position in dedicated sections. 44 Moreover, default options allow app stores constantly to offer consumers proprietary apps rather than alternatives provided by autonomous developers. Default options, together with pre-installation, are likely to limit consumer choice, entrench market power, and reduce the potential for innovation in downstream markets. 45 Indeed, independent developers face an uphill battle when competing against proprietary apps pre-installed on devices.

Self-preferencing can also take place through terms and conditions imposed by the app store on third-party developers. The terms and conditions implemented by app stores envisage a vast amount of requirements regarding content, app functionality, collection, and distribution of revenues between the app and the app store. Therefore, the power held by Apple and Google in establishing the terms and conditions for operating within their mobile ecosystem is a major concern for antitrust authorities and policymakers. 46

While there are multiple grounds to justify objectively and consider the beneficial impacts of such rules and, more generally, the app-reviewing process (e.g., privacy protection, customer experience, cybersecurity), 47 it cannot be overlooked that they may also translate into an indirect form of self-favoring. In particular, it is often the case that app stores’ terms and conditions are broadly defined, thereby making it tricky to gauge in advance what is allowed and what is forbidden, raising the risk of inconsistent application, and ultimately offering a way to exclude competitors arbitrarily due to non-compliance. 48 For instance, some developers reported that the App Store managed to shield Apple Pay from the competition by denying access to rival payment apps in light of alleged inconsistencies with its guidelines. 49 In the same vein, others complained that Apple hampered the viability of rival apps when introducing its own competing applications by selectively disabling key features for a seamless customer experience. 50

Given the difficulty in tackling self-preferencing as a stand-alone practice and due to the significant amount of conduct under scrutiny, in the following paragraphs we will focus on the most relevant behaviors, providing an overview of the recent investigations and antitrust cases on both sides of the Atlantic.

A. Terms Related to App Payments: Fees and Anti-Steering Provisions

The practice of charging commission fees on third-party apps coupled with the imposition of anti-steering provisions has surfaced as one the main competitive concerns involving app stores. 51 When users install an app and purchase within an app (in-app purchase system—IAP system) Apple and Google charge a fee ranging between 30 and 15 percent. 52 In addition, the app stores’ rules explicitly prevent app developers from using payment channels other than Google Play Billing and In-App Purchase, respectively, provided by Google and Apple. Moreover, in the case of Apple, due to an anti-steering provision, app developers are prevented from informing users of alternative options for purchasing paid content: indeed, while the App Store allows users to consume content purchased elsewhere (e.g., on the app developer’s website) in the app, its rules prevent developers from informing users about these purchasing possibilities.

The level of the commission is difficult to assess from an antitrust perspective. On the one hand, it puts rivals at a competitive disadvantage, raising their costs or squeezing their margins, leading overall to higher prices for consumers. On the other hand, the commission perhaps, at least partly, reflects the cost of services incurred in maintaining the app store and the benefits provided by the app marketplace as a privileged channel for the distribution of developers’ apps, thereby allowing particularly small and new developers to reach a large audience with a relatively small investment. 53 Moreover, it is troublesome to establish if and how much the amount of the commission charged for in-app payments is inflated by Apple and Google’s market power. 54

Admittedly, the concerns are not only represented by the 30 percent commission in itself but mainly by the fact that it comes with the obligation to use only the payment mechanism provided by Google and Apple, as anti-steering provisions limit the flow of information to consumers on the payment structure related to in-app purchases. 55 Indeed, this policy has led to a number of complaints regarding the fact that Apple and Google are unlawfully foreclosing app distributors, deterring entry into the app market, and depriving end users of potential new apps.

In Cameron v. Apple, two California-based app developers filed a class action complaint, arguing that Apple’s ability to charge supra-competitive fees over time demonstrates its market power and the lack of alternatives for developers. 56 The level of the commission also features in the litigation brought by a group of users in Apple v. Pepper, arguing that Apple has monopolized the retail market for the sale of apps and has unlawfully used its monopolistic power to charge consumers higher-than-competitive prices. 57 Furthermore, the combination of high commission fees and anti-steering provisions is at the heart of the litigation brought by Epic Games against Google and Apple. The dispute was triggered by the removal of the popular Fortnite game from the App Store and the Play Store as a reaction to the offer of a new direct (and cheaper) payment option alternative to Apple and Google’s payment processor. 58

Epic Games alleges that Apple and Google engaged in anticompetitive behaviors in order to maintain monopoly power unlawfully both in their own ecosystems’ app distribution and in-app payment processing markets. Notably, according to Epic Games, Apple and Google implemented a twofold antitrust violation. First, they imposed an anticompetitive restriction by coercing all app developers wishing to use the app store to use exclusively their own payment processing mechanisms for all in-app purchases, thereby unlawfully extending their monopoly power from the app distribution market. Second, as the sole payment processor, Apple and Google can then leverage their monopolist intermediary position to extract supra-competitive rents through a 30 percent fee on all in-app purchases. In accordance with Epic’s narrative, this translates into a foreclosure of other payment processors, having exclusionary effects on app developers and causing harm to consumers in terms of reduced innovation and higher prices. Furthermore, Epic argues that Apple’s App Store anti-steering rule unlawfully prohibits developers from directly or indirectly targeting iOS users to use a purchasing method other than the in-app purchase.

On similar grounds, a group of U.S. State attorneys general launched an antitrust lawsuit accusing Google of unlawfully restricting trade and maintaining monopolies in the markets for Android software application distribution and for payment processing of digital content purchased within Android apps. 59 Mimicking Epic Games’ complaint, according to the allegations, Google has closed off its purportedly open Android operating system from competition in app distribution by imposing an “extravagant” 30 percent commission fee on sales made through the app and implementing an anticompetitive restriction requiring Android app customers to use Google Play Billing for in-app purchases of digital content.

In September 2021, Judge Rogers handed down the decision in the Epic Games case, concluding that Apple’s anti-steering provisions are anticompetitive as they hide critical information from consumers and illegally stifle consumer choice. 60 Therefore, pursuant to the injunction issued by the Californian District Court, Apple is no longer allowed to prohibit developers from informing users about alternative payment options to Apple’s IAP system. Notably, Apple is restrained from prohibiting developers to include in their apps and their metadata buttons, external links, or other calls to action that direct customers toward purchasing mechanisms, in addition to the IAP system, and communicating with customers through points of contact obtained voluntarily from the latter by way of account registration within the app. Having said that, Apple remains free to prohibit third-party IAP systems within the App Store, thus maintaining the convenience of its own IAP. Indeed, the Court only challenged the prohibition on communicating external alternatives and allowing links to those external sites.

Furthermore, the decision did not challenge the amount of Apple’s fee, 61 or impose sideloading apps on to iOS devices, or allow third-party competing app stores on iOS. Moreover, the Court held that Epic Games had failed to prove that users are locked-in, as the low switching rate between operating systems instead appears to stem from the level of overall satisfaction with the existing devices. 62 Finally, the Court did not conclude that Apple is a monopolist. Indeed, the injunction was granted under California state unfair competition law, rather than under antitrust law. Notably, rejecting the arguments of both Apple and Epic with regard to the relevant market, Judge Rogers stated that the effective area of competition is the market for digital mobile gaming transactions (rather than digital games generally or just Apple’s own ecosystem) and, although Apple enjoys a considerable market share of more than 55 percent and extraordinarily high profit margins, “these factors alone do not show antitrust conduct. Success is not illegal.” 63

Moving to the other side of the Atlantic, the European Commission, the ACM, and the CMA are investigating the in-app purchasing rules put into place by Apple. 64 Following a complaint lodged by Spotify, the European Commission recently sent a statement of objections, informing Apple of its preliminary view that it had abused its dominant position held in the distribution of music streaming apps through its App Store due to the imposition of proprietary IAP for the distribution of paid digital content and the systemic use of anti-steering provisions. 65 In the European Commission’s view, these behaviors allow Apple to increase the costs of its rivals and to distort the competitive process for music streaming services, ultimately harming consumers who end up bearing the 30 percent commission fee.

More recently, Netherlands ACM has ordered Apple to adjust the conditions applied to dating-app providers allowing them to use their own in-app payment system. 66 The ACM has considered Apple’ conditions not proportional to the additional payment service and unnecessary for running the App Store, hence unreasonable and in violation of competition rules. The District Court of Rotterdam upheld the injunction against Apple dismissing, among other things, the arguments that IAP is needed for security and privacy. 67

Finally, the Competition Commission of India has joined in by ordering an investigation against Alphabet (the parent company of Google India) and Apple for abusing their dominant position by mandating, among other things, third-party apps to use their IAP systems for charging their users. 68

On the contrary, the ACCC did not recommend that Apple or Google should be precluded from imposing the use of their IAP systems. 69 According to the Australian Authority, it is unclear how effective the unbundling would be at addressing the issues raised by Apple and Google’s control over their respective marketplaces and payment systems, and the detriment that may be caused to app developers by any resulting changes to Apple and Google’s revenue-raising model. With regard to the latter, the ACCC mentioned, in particular, the risk that changes in Apple and Google’s fee or commission structure may limit app marketplaces to less efficient forms of charges (e.g., the imposition of higher flat fees on apps providing digital goods and services), encouraging smaller innovative apps to explore alternative avenues to app marketplaces in order to avoid paying the fee, in turn reducing the apps available through the app store, and reducing its value to consumers.

More recently, the Russian antitrust enforcer has also targeted Apple’s anti-steering provisions, warning the company to remove them in order to avoid a full-scale investigation. 70 Furthermore, closing its investigation, the Japan Fair Trade Commission accepted Apple’s measures to allow developers to include an in-app link within “reader” apps, which provide previously purchased content or content subscriptions for digital magazines, newspapers, books, audio, music, and video (e.g., Spotify, Netflix, Amazon Prime, and Kindle). 71 While the agreement was made with the JFTC, Apple undertook to implement this change globally to all reader apps on the store, thus allowing all developers of reader apps around the world to link up to an external website in order to set up or manage an account, thereby avoiding the App Store’s fee. Although the remedy will not apply to games, 72 the JFTC acknowledged that it will eliminate concerns about the prohibition on providing sales channels other than IAP.

B. Access to Near-Field Communication

Near-field communication (NFC) is a short-range wireless connectivity standard enabling data exchange between devices in close proximity (ten centimeters or less). Within the app economy and the Internet of Things (IoT) ecosystem, NFC chips retain great commercial value as they allow a vast array of applications to read or write data out of electronic tags attached to real-world objects and other devices. 73 For instance, by means of this form of communication, mobile applications can perform “card emulation” functions, acting as payment, transport, or access cards. Notably, this technology could be quite disruptive to the payment system as it facilitates tap-and-go contactless payments between smartphones and payment terminals without the need for consumers to carry a physical card.

Both Google and Apple have developed their own payment services, namely, Google Pay and Apple Pay, allowing users to upload their payment card details onto their device and pay by tapping a terminal. However, in line with their respective business models, they adopted different strategies to harness the potential of NFC. Since 2013, Android has offered third-party developers access to NFC chips, thereby allowing rival apps (such as Samsung Pay and PayPal) to provide “tap and go” payment services on a level playing field with Google Pay. Conversely, Apple has been more cautious in sharing NFC functionalities with third-party apps by reserving, for instance, “tap and go” payments on iPhones and Apple Watches for its in-house app. 74 The firm has always motivated this restriction by invoking the need to ensure high standards of security for iPhone users, together with the overall integrity of its mobile ecosystem. 75 While it has not yet been definitively ascertained whether or not these limitations are justifiable, it is worth noting that similar security-related issues were never raised within the Android ecosystem. Similarly, critics pointed out that Apple’s line of defense is not entirely consistent as access to NFC chips is denied only to rival payment apps, but not to hotel companies, gym equipment makers, and car manufacturers seeking access to non-payment functions.

Unsurprisingly, NFC limitations by Apple have attracted antitrust scrutiny from several competition agencies concerned about their potential anticompetitive impact. In 2020, both the European Commission and the ACM launched an investigation into the terms, conditions, and other measures limiting access to NFC functionality for rivals. 76 These assessments are based upon the competitive concern that Apple is undermining competition by reserving the potential of NFC technology exclusively to its own proprietary payment app. The fear is that, with consumers increasingly relying upon contactless payments due to the Covid-19 pandemic, Apple could leverage its dominance within the mobile ecosystem to monopolize the lucrative market of value-added financial services within its own ecosystem.

At the same time, Google has not escaped attracting antitrust attention with reference to its own mobile payment services. The investigation launched by the Competition Commission of India in November 2020 targeted what appears to be a surreptitious attempt to foreclose competing payment apps. 77 With the only mobile payment method accepted on the Play Store being Google Pay, there is a concern that users, due to the status quo bias, would not switch to competing apps when making other physical and digital transactions different from in-app purchases. 78 Consequently, according to the Indian antitrust authority, alternative applications facilitating mobile payments are at a competitive disadvantage as they face higher barriers to entry compared to Google Pay.

C. Refusal to Deal

As app stores act as gateways for app developers to reach potential end customers, a significant amount of cases involve refusals to deal with rivals. The overall category includes different types of practices, which are difficult to evaluate under a common standard. Therefore, it is worth applying an overall distinction according to the market level involved. First, there are refusals to deal which occur in the primary market of Apple’s and Google’s ecosystem (access request to the operating system in order in order to deliver a rival app store). Second, there are refusals involving a secondary market that poses economic threats to their core business or into which Apple and Google are vertically integrated (access request to their app stores in order to supply a rival app). 79

With regard to the former, one of the main allegations against Apple in Epic Games relates to its denial of access to the essential facility represented by the iOS mobile operating system. By refusing to allow rival app stores on iOS devices, Apple is accused of preventing app distributors from competing in the iOS app distribution market, ultimately entrenching its monopoly power in that market. 80 From this perspective, access to the operating system is essential for effective competition in the iOS app distribution market and app distributors are practically unable to duplicate iOS. However, as it is technically feasible for Apple to provide app distributors with access to iOS, this would not interfere with or significantly inhibit Apple’s ability to conduct its business. Hence, Epic argues, Apple’s denial of access to iOS has no legitimate business purpose and serves only to assist Apple in maintaining its unlawful monopoly position in the iOS app distribution market.

In relation to the latter, the Unlockd case, which involves the removal of an app from the app store, is interesting. 81 The start-up Unlockd used to offer an app enabling mobile phone users to obtain rewards in exchange for opting in to advertisements. In April 2018, Google announced its intention to remove the app from the Play Store in light of an alleged infringement of its terms and conditions which prohibit apps from paying users to view ads. Unlockd complained that Google’s policy was disadvantageous to app developers wishing to develop innovative business models in competition with Google’s own online advertising business, and managed to receive judgments from the Federal Court of Australia and the U.K. High Court of Justice granting interim injunctions that stopped Google removing the app from the platform. However, thereafter, the start-up suffered from a lack of funding due to a failed IPO, eventually going into administration and withdrawing its claims. 82

The very same analysis of the conduct in question can also be applied to the rejection of an app at the end of the app store review process. Indeed, before being admitted into the app store, third-party mobile apps must undergo a review process to check whether they comply with the guidelines in terms of functionality, performance, safety, and security. For instance, Apple has recently disclosed a number of statistics about its app rejection process in 2020, revealing that: nearly 1 million new apps, and an additional nearly 1 million app updates, were rejected or removed because they were unfinished or not functioning properly, or they lacked a sufficient mechanism for moderating user-generated content; 48,000 apps were removed for using hidden or undocumented features; 150,000 apps were removed as they were found to be spam, copycats, or misleading to users; 95,000 apps were removed due to fraudulent violations (often because they changed functionality after Apple’s review to become a different kind of app, including gambling apps or pornography hubs); and 215,000 apps were removed due to privacy violations. 83

App review processes and associated terms and conditions are under the scrutiny of antitrust authorities due to concerns expressed by some app developers about their opaqueness and their inconsistency of enforcement. 84 These concerns are heightened by the dual role played by Apple and Google as downstream app developers in competition with third-party apps, and as app store providers and regulators: this conflict of interest may lead Apple and Google to establish and enforce rules for accessing their app marketplaces to guarantee preferential treatment for their own apps and to undermine the competitive pressure originating from third-party apps. For instance, although Unlockd is not in direct competition with Google, it does affect Google’s ability to gain profits from its core advertising business.

An interesting case, particularly due to the remedies imposed, is the recent Italian Competition Authority’s (AGCM) decision against Google for refusing to integrate Enel’s X Recharge app (JuicePass) into Android Auto, an infotainment system that integrates on a car dashboard some features of Android devices, such as navigation, calls, maps, music, and text messages. 85 By enabling a wide range of services for recharging electric cars (in particular, allowing drivers to locate a charging station, manage the charging session, and reserve a slot at the station), JuicePass is apparently a rival of Google Maps app, which enables similar functionalities but does not include reservation and payment services. Therefore, according to the AGCM, by refusing to integrate JuicePass into the Android Auto ecosystem, Google was attempting to favor its own app, ultimately reserving the full spectrum of recharging services to Google Maps.

The AGCM’s reasoning is based upon the fact that Android Auto forms a “competitive space” within which service apps compete against the additional functionalities effectively or potentially offered by Google’s proprietary navigation app. 86 However, the Italian authority considered that Android Auto is indispensable for the purposes of applying the essential facility doctrine. 87 This is despite the fact that drivers with a smartphone can easily access JuicePass through both the Play Store and the App Store.

Due to Google’s gatekeeping position and the conflict of interests generated by its dual role, the AGCM mandated the company to ensure an effective level playing field for all service apps offering recharge services to avoid Google continuing to favor its own navigation app within the Android Auto ecosystem. This means that Google is required to develop and update a proper template to accommodate the needs of third-party recharge applications, thereby allowing their interoperability with Android Auto. 88

IV. Regulating Digital Platforms

Alongside numerous antitrust disputes and investigations on the practices of digital platforms, sometimes specifically involving app stores, a wave of regulatory initiatives is emerging to address the distinctive features of digital markets and the strategic role played by large online platforms.

As a result of the combination of economic factors (strong economies of scale, extreme indirect network effects, remarkable economies of scope due the role of data as a critical input, conglomerate effects, consumers’ behavioral biases, and single-homing tendency), the digital markets are highly concentrated, prone to tipping and not easily contestable. 89 Furthermore, competition in the digital economy increasingly consists of a competition between ecosystems attracting and leveraging a wide range of complementary services around technical standards, which, in turn, can pose interoperability problems, increasing switching costs and lock-in scenarios. In addition, while competition law enforcement occurs ex post and requires an extensive investigation of very complex facts on a case-by-case basis, 90 digital markets move too fast to be supervised ex post; therefore, antitrust enforcers often find themselves intervening after the tipping point has already been reached. Finally, large online platforms enjoy a brand-new type of market power combining a gatekeeping or bottleneck position in the digital ecosystem with a parallel role as rule-setter within the established digital environment.

Accordingly, due to their regulatory role and intermediation power, large digital platforms should take on special responsibility for ensuring a level playing field and undistorted competition both on the platform and on neighboring markets. This is seen as particularly necessary whenever they perform a dual role, acting as both referee and player on their own ecosystems, thereby competing with their business customers operational on the platform and increasing concerns about the incentive to discriminate by self-favoring their own products and services as opposed to those of their rivals.

These arguments essentially question the capability of current antitrust rules to scrutinize the practices and business models of platforms, supporting the idea that existing antitrust is unfit to address effectively the challenges posed by the economic features of digital markets and the emergence of large technology platforms, which instead require ex ante interventions and regulatory approaches.

Against this backdrop, three main models have emerged thus far.

In the United Kingdom, the CMA has supported the adoption of a legally binding firm-specific code of conduct, which will shape the behavior of firms with “strategic market status” governing elements of how they do business with other companies and treat their users, and the appointment of a Digital Markets Unit tasked with overseeing this framework and enforcing the new set of rules. 91 The Digital Markets Unit will also be allowed to impose procompetitive interventions on firms with the strategic market status, which may include third-party access to data, data mobility, interoperability and common standards, interventions to overcome consumer inertia and default bias, obligations to provide access on fair and reasonable terms, and separation remedies.

In the DMA proposal, the European Commission has opted for a sector-specific approach to digital services, suggesting an ex ante regulatory regime aimed at governing online platforms with “gatekeeping” positions through a set of eighteen detailed obligations (ranging from a prohibition on parity clauses, anti-steering clauses, self-preferencing and certain bundling strategies to duties to deal, data portability, and interoperability). 92 The obligations amount to per se violations since they are enforced irrespective of the business model employed by the platform and without allowing any efficiency defense.

Finally, the German legislature has decided to strengthen its national antitrust enforcement tools by introducing a new Section 19a to the GWB containing a list of seven types of abusive practices for undertakings of “paramount significance for competition across markets.” 93 Although the list is similar and functionally equivalent to the European DMA proposal, the German provision does not consider the practices at stake per se prohibited, but introduces a reversal of the burden of proof, allowing firms to provide objective justifications for their conduct. In a similar vein, other European Member States, such as Austria, Greece, and Italy, are looking at the German approach to update their domestic antitrust provisions. 94

On the other side of the Atlantic, the U.S. President Joe Biden has signed an Executive Order aimed at promoting competition in the American economy and enforcing antitrust laws to “meet the challenges posed by new industries and technologies, including the rise of the dominant Internet platforms.” 95 In particular, the Executive Order identified, as practices that should be investigated and pursued, “serial mergers, the acquisition of nascent competitors, the aggregation of data, unfair competition in attention markets, the surveillance of users, and the presence of network effects.” Moreover, the U.S. House of Representatives has unveiled a five-bill antitrust package designed to curb the market power of large online platforms representing “critical trading partners” by curtailing their ability to buy competitors, imposing line of business restrictions and a non-discrimination regime, mandating data portability and interoperability. 96 Just as in the European DMA, the relevant requirement in the designation process relates to the size of the platform (e.g., market capitalization and number of users), thus dispensing the authorities from proving the market power aspect. However, unlike the DMA, the U.S. bills allow for an affirmative defense, enabling the designated platform to demonstrate that its conduct under scrutiny is objectively justified and does not cause damage to the competitive process.

In the international scenario, it is also worth noting that in February 2021 China’s State Administration for Market Regulation issued the “Antitrust Guidelines for the Platform Economy,” which represent China’s first specific antitrust rules on platforms and identify several practices which are considered unlawful, such as refusing access to the platform, adopting parity clauses and “choosing one from two” exclusivity obligations, using big data to discriminate and manipulate the market. 97

Despite the differences between the aforementioned models and approaches, these initiatives share the common goal of bridging the apparent enforcement gaps in current antitrust rules by expanding the toolkit and dispensing enforcers from the need to deal with the constraints of the antitrust law regime (such as proof of dominance and the effects of a certain behavior on the market) to address anticompetitive behaviors that standard antitrust analysis would struggle to combat. 98 Notably, these interventions are leaning toward making the assessment of some practices faster and simpler by introducing a blend of corrective tools, such as ex ante prohibitions, market investigations, legal presumptions, and inversions of the burden of proof. Indeed, for instance, the obligations envisaged in the DMA apparently capture practices subject to past and ongoing antitrust cases.

Moreover, these interventions are based upon the very same premise of considering digital platforms to be common carriers, thus subject to a public utilities-style regulation. 99 Accordingly, reforms based upon structural separation, line of business restrictions, and duties to deal should be considered in order to reduce the intermediation power exerted by dominant platforms and any conflicts of interest 100 . Notably, the common carriage regime and the essential facility doctrine should be revived in order to remedy the harm caused by self-preferencing 101 and to guarantee access to digital bottleneck facilities, 102 respectively. In a similar vein, the European General Court in Google Shopping extended to a dominant platform the principle of equal treatment applied to public undertakings. 103

A. Platform and Device Neutrality Provisions: App Stores as Public Utilities?

Against this background, some provisions are relevant to app stores, while others explicitly target them.

Considering first the European DMA proposal, as online intermediation services, app stores are considered core platform services and are thus included in the list of digital services that are within the scope of application of the new regulation. 104 As a consequence, providers designated as gatekeepers must comply with the obligations laid down in Articles 5 and 6. The first relevant obligation for app stores relates to the anti-steering provision which is at the center of the European Apple App Store case and Epic Games’ complaint against Apple 105 : in accordance with the provision at issue, business users should be free to promote and choose the distribution channel they consider most appropriate to interact with any end-users.

The ban on parity clauses may also play a role in interplatform competition by prohibiting, for example, a gatekeeper from requiring—as a condition for accessing an app store—that its pricing terms or conditions of sale must be equal to or more favorable on its app store than the terms or conditions on another app store. 106

Other provisions tackle specific forms of self-preferencing aimed at preventing a gatekeeper from unfairly benefiting from its dual role. This applies to the ban on sherlocking (the use of data of business users to compete against them), 107 on preventing end-users from un-installing any pre-installed software applications on its core platform service, 108 on giving more favorable treatment by ranking its own services and products higher, 109 and on providing preferential access to technical functionality (operating system, hardware or software features) to its own ancillary services, such as identification or payment services and technical services which support the provision of payment services. 110 In the latter case, the DMA includes a clear reference to the Apple Pay investigation. The proposal mentions, as an example of the conduct in question, the case of a gatekeeper that manufactures devices and restricts access to some of the functionalities of its devices (such as NFC technology and the software used to operate that technology) which may be necessary for the effective provision of downstream services. 111 Therefore, the goal of the provision is to address leveraging by gatekeepers into ancillary services: as gatekeepers frequently provide the portfolio of their services as part of an integrated ecosystem, they are likely to have increased ability and incentive to leverage their power from their core platform services to adjacent markets. 112

Concerns about potential leveraging strategies are also addressed by the prohibition on bundling and tying. Notably, a gatekeeper must refrain from exploiting the “dependency” position of business users to require the inclusion of identification services provided by a gatekeeper together with one or more core platform services. 113 Therefore, an app store operator must not unilaterally require app developers to integrate the app store’s own user ID functionality into their apps and to display this ID functionality to their app customers. In a similar vein, a gatekeeper must not require business or end-users to subscribe to any core platform services as a condition for accessing another core platform service. 114

Furthermore, some provisions are essentially intended to apply to app stores. First, app store providers must allow sideloading and even open the door to third-party app stores (so-called “store-within-a-store”). Indeed, pursuant to the proposed DMA, app store providers must allow the installation and effective use of third-party apps or app stores using, or interoperating with, their operating systems and allow these apps or app stores to be accessed by means other than their core platform services. 115 The goal of the obligation is to increase the contestability of app stores, and this could have a severe impact on Apple’s and Google’s governance of their app stores, namely, the terms and conditions, review process, and IAP system. 116 Second, app store gatekeepers shall apply fair, reasonable, and non-discriminatory (FRAND) access conditions for business users. 117 The obligation does not establish an access right to app stores but aims to address the imbalance in commercial relationships that could lead to unfair and unjustifiably differentiated conditions to the detriment of business users, for instance, by challenging Apple’s and Google’s practice of charging commission fees on third-party apps. 118 Moreover, gatekeepers should refrain from technically restricting the ability of end-users to switch between different apps and services. 119 However, pre-installation should not be construed as constituting a prohibited barrier to switching. 120

Finally, as a general rule facilitating switching or multi-homing, gatekeepers must provide effective portability of data generated through the activity of a business user or an individual and provide tools for end-users to facilitate the exercise of data portability, including by providing continuous and real-time access, such as through high-quality APIs 121 . Furthermore, gatekeepers must provide business users, free of charge, with effective, high-quality, continuous, and real-time access and use of aggregated or non-aggregated data. 122

Alongside the obligations envisaged in the European DMA proposal, the new Section 19a of the German Competition Law also contains an exhaustive list of seven (broadly defined) types of practice that may be prohibited by the Bundeskartellamt once an undertaking is designated as being of paramount significance for competition across markets. 123

The possibility for the German Competition Authority to prohibit the following activities is particularly relevant to app stores: self-preferencing (especially in the presentation of offers, for instance, through the ranking and advertisement of apps in app stores, or via exclusive pre-installations); measures that hinder supply or sales activities of other (even non-competitor) firms; measures that impede other undertakings by processing data relevant to competition that have been collected by the platform, or that demand terms and conditions permitting the processing of relevant data received from other undertakings for purposes other than those that are required to provide its own services to such undertakings; practices (such as predatory pricing, exclusivity agreements, tying, and bundling) hindering rivals on a market on which the designated undertaking can rapidly expand its position; restrictions on the interoperability or the portability of data; and the request for disproportionate remuneration from business users.

Moreover, Germany has paved the way for new rules allowing e-money issuers and mobile payment service providers to access platform-based technical infrastructures. Notably, Section 58a of the German Payment Services Supervisory Act (PSSA) provides them with the right to access the functionalities of the operating systems of online devices and the respective NFC interface technical infrastructure integrated in mobile phones and other devices. 124 At its heart, such an ex ante regulatory intervention imposes on digital platforms a duty to share their market ecosystem with potential competitors in the field of payment services. The provision aims to unbundle the market for stationary hardware from software applications running on them, counterbalancing the gatekeeper position and the network effects enjoyed by digital enterprises operating large platforms which could have facilitated their rapid monopolization of the payment services market, also by means of self-preferencing. In fact, the right in question applies only when the hardware-based infrastructure is used to execute e-money transactions or to provide payment services. This regulatory mechanism is designed to prevent operators enjoying close proximity to users from leveraging on their position and gaining full control of front-end customer interaction to the detriment of potential competitors.

The rule has been labeled “Lex Apple Pay” as it is likely to have a particular impact upon Apple’s proprietary business model; the German Savings Banks Association has reportedly lobbied for a legislative measure to improve the position of payment service providers in relation to Apple. 125 Indeed, since Apple’s NFC interface can only be accessed via Apple Pay, payment service providers cannot integrate their own payment solutions into the iPhone’s NFC system without paying onboarding and transaction fees for using the Apple Pay App. Interestingly, shortly before the entry into force of Section 58a in January 2020, 371 of 379 Germans savings banks agreed to use Apple Pay, foregoing the option of direct access to the NFC interface through their own apps.

Turning to the U.S. scenario, several provisions envisaged in recently released bills resemble those implemented in Europe. In June 2021, the House of Representatives unveiled a five-bill package targeting large online platforms by introducing dramatic statutory changes to antitrust law. Three bills are particularly relevant to app stores.

Notably, the Ending Platform Monopolies Act aims to tackle the dual role of platforms, thereby eliminating their potential conflicts of interest and related risks of preferential treatment for their own products and services, by imposing line of business restrictions. 126 Designated platforms would be prohibited from owning, controlling, or having a beneficial interest in a line of business other than the covered platform that: utilizes the covered platform for the sale or provision of products or services; offers a product or service that the covered platform requires a business user to purchase or utilize as a condition for accessing the covered platform, or as a condition for preferred status or placement of a business user’s product or services on the covered platform; or gives rise to a conflict of interest. As a result, the Act may potentially prevent Apple and Google from offering their proprietary apps in their own app stores. 127

In addition, the Augmenting Compatibility and Competition by Enabling Service Switching (ACCESS) Act would mandate data portability and interoperability. 128 In particular, in order to reduce switching costs for users, a designated platform must maintain a set of transparent, third-party accessible interfaces (including APIs) to: enable the secure transfer of data to a user, or with the affirmative consent of a user, to a business user if instructed by a user, in a structured, commonly used, and machine-readable format; and facilitate and maintain interoperability with a competing business or a potential competing business.

Furthermore, the American Choice and Innovation Online Act is intended to outlaw certain discriminatory behaviors by designated platforms. 129 In particular, the bill prohibits any conduct that: gives an advantage to the covered platform operator’s own products, services, or lines of business over those of another business user; excludes or disadvantages the products, services, or lines of business of another business user compared with the covered platform operator’s own products, services, or lines of business; or discriminates between similarly situated business users. 130 Moreover, the bill prevents a designated platform from: restricting or impeding the capacity of a business user to access or interoperate with the platform’s technical functionality 131 ; conditioning access to the platform or preferred status or placement on the purchase or use of other products or services offered by the platform operator 132 ; sherlocking 133 ; restricting or impeding a business user from accessing data generated on the platform by the activities of the business user or its customers, and preventing the portability of such data to other systems or applications 134 ; restricting or impeding users from un-installing pre-installed apps or changing default settings that direct or steer users toward products or services offered by the covered platform operator 135 ; introducing anti-steering provisions that restrict or impede businesses users from communicating information or providing hyperlinks on the platform to end users to facilitate business transactions 136 ; treating the platform operator’s own products, services, or lines of business more favorably than those of another business user in connection with any user interfaces, including search or ranking functionality offered by the platform 137 ; interfering with or restricting a business user’s pricing of its goods or services (e.g., by imposing parity clauses) 138 ; and restricting or impeding a business user, its customers, or users from interoperating or connecting to any product or service (e.g., by impeding sideloading). 139

In short, in addition to the European DMA proposal, the provisions of this non-discrimination bill would significantly affect the governance of app stores by preventing Apple and Google from enforcing their current policies.

In August 2021, a bipartisan trio of senators (Blumenthal, Blackburn, and Klobuchar) also put forward an ad hoc app store bill in the U.S. Senate. 140 By explicitly referring to gatekeeper power in the app economy, the Open App Markets Act would introduce similar obligations to those included in the European DMA. Notably, it would ban app stores from forcing developers to use the IAP system, imposing parity clauses, or punishing developers that offer lower prices on a separate app store or through their own payment systems 141 ; introducing anti-steering provisions 142 ; sherlocking 143 ; impeding or restricting sideloading, app un-installing, and the possibility of choosing third-party apps and app stores as defaults 144 ; self-preferencing in ranking 145 ; and impeding or restricting access to technical functionality. 146

Finally, in the United Kingdom, the findings of the ongoing CMA’s market study on mobile ecosystems will inform the scope of the new regulatory regime, providing the basis for the development of codes of conduct and the potential use of procompetitive interventions by the Digital Market Unit. 147 Two of the issues tackled by the study involve app stores directly and, in particular, relate to competition in the distribution of mobile apps and the dual role of Apple and Google in competition between app developers. In light of this, the CMA aims to investigate a wide range of phenomena, namely, the extent to which consumer behavior is influenced by the way platforms shape the choices available to users, including the pre-installation of mobile apps, default settings and other aspects of choice architecture; the potential justifications for interoperability restrictions; the prominent placement of Apple and Google’s proprietary apps in the rankings of their app stores or prominent positioning in dedicated sections of their app store; the relevance of sideloading and in-app payment systems; potential benefits (e.g., increased security) and costs (e.g., reduced innovation, choice and competition) of more closed ecosystems as opposed to more open ones; the collection and use of commercial information on rivals that would facilitate Apple or Google’s expansion into different app categories; the restrictions on the ability of third-party developers to access software and hardware functionalities that are used by Apple and Google’s proprietary apps; the impact that app review processes may have on competition between third-party developers.

In its Interim Report, the CMA has considered a range of possible interventions aimed at addressing Apple and Google’s market power by targeting specific forms of conduct, such as a requirement to allow sideloading under certain conditions, remove anti-steering provisions, and allow alternative in-app payment options to be displayed alongside their own payment services within apps 148 .

Notably, the first app store proposal to be converted into law occurred in South Korea. 149 The recently revised Telecommunications Business Act will prohibit dominant platforms from compelling app developers to use a specific payment system, charging them commissions on in-app purchases, and unjustifiably deleting apps from the store or delaying their review process.

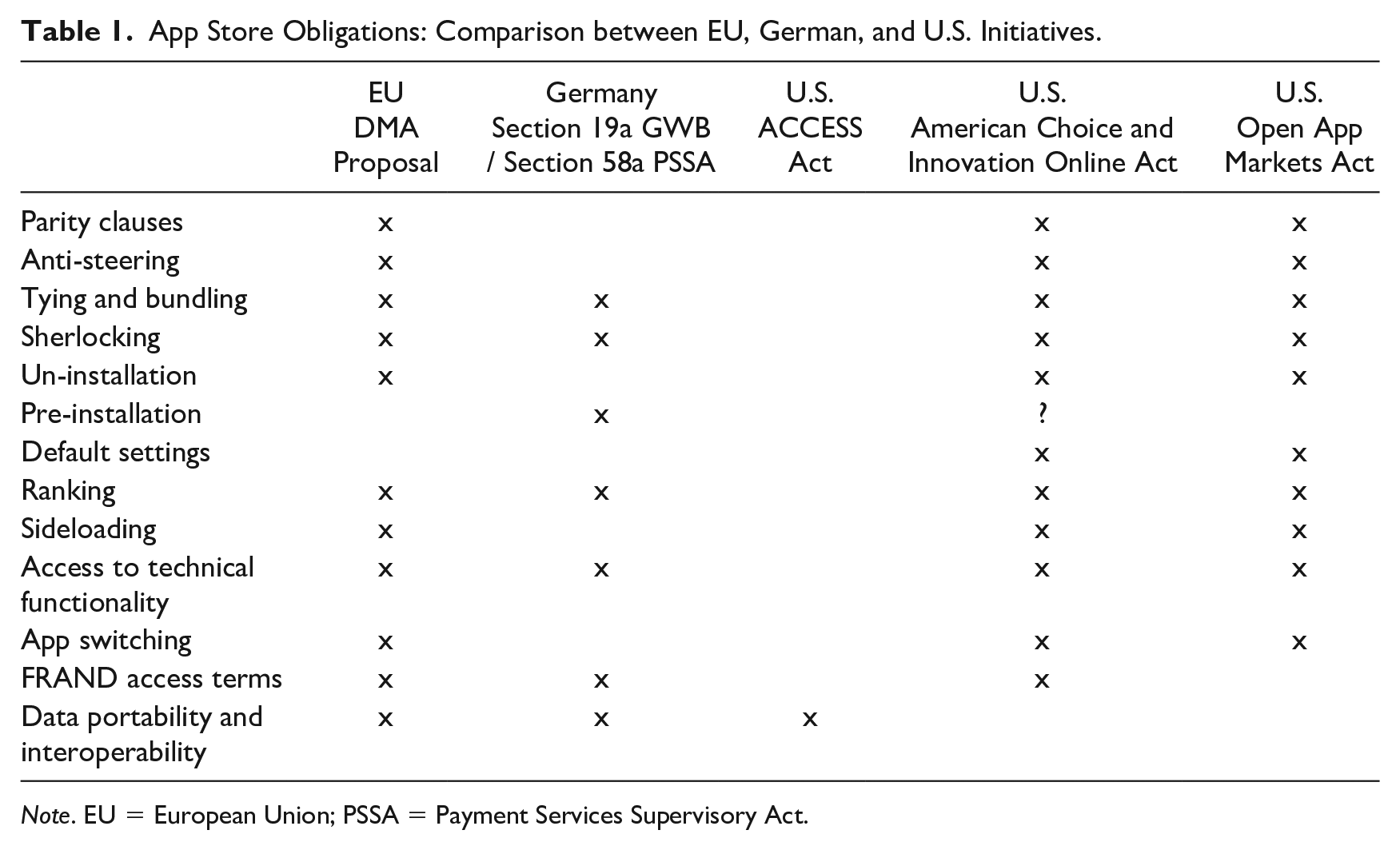

By and large, focusing on the content of the international initiatives undertaken so far from the perspective of app stores, they are attempting to introduce a neutrality regime with the aim of increasing contestability, facilitating the possibility of switching by users, tackling conflicts of interests, and addressing imbalances in the commercial relationship. This goal is pursued by introducing obligations in terms of both device and platform neutrality. While the former includes provisions on app un-installing, sideloading, app switching, access to technical functionality, and the possibility of changing default settings, the latter entails data portability and interoperability obligations, and the ban on self-preferencing, sherlocking, and unfair access conditions (see Table 1).

App Store Obligations: Comparison between EU, German, and U.S. Initiatives.

Note. EU = European Union; PSSA = Payment Services Supervisory Act.

This line of reasoning was confirmed by the European Google Shopping decision. In evaluating the conduct of a dominant player accused of favoring its own service at the expense of those of its rivals, the Court referred to the Regulation on net neutrality

150

and the CJEU decision in Telenor

151

regarding zero-rating practices, arguing that the legal obligation of non-discrimination that ensues from this legislation for internet access providers on the upstream market cannot be disregarded when analysing the practices of an operator like Google on the downstream market, given the undisputed ultra-dominant position of Google on the market for general search services and its special responsibility not to allow its behaviour to impair genuine, undistorted competition in the internal market.

152

In a similar vein, in the United States, the Federal Communications Commission’s 2015 “Open Internet Order” justified the net neutrality regulation pointing to the significant bargaining power exerted by broadband providers which act as “gatekeepers” standing between edge providers and consumers. 153

Against this background, the U.S. Ending Platform Monopolies Act pushes the regulatory intervention even further by imposing a line of business restrictions to eliminate any risk of conflict of interests by platforms. 154 As noted, this may require Apple and Google not to offer their apps in their own stores. Furthermore, the provisions, such as those approved in South Korea, banning app store operators from forcing app developers to use their payment systems may jeopardize the current monetization model of Google and Apple. Indeed, Google is attempting to comply with the new South Korean legislation without changing its underlying monetization model. Notably, Google announced that developers will be able to add an alternative in-app billing system, alongside Google Play’s billing system, for their mobile and tablet users in South Korea. 155 However, service fees for distributing apps via Android and Google Play will continue to be based on digital sales on the platform: since developers will incur costs to support their billing system, when a user selects alternative billing, Google will reduce the developer’s service fee by 4 percent.

Furthermore, an interesting question concerns app pre-installation, namely, whether a designated platform can pre-install apps and mainly decide which apps will benefit from this preferential treatment. Indeed, to enable end-user choice and address this form of self-preferencing, some initiatives encompass an explicit obligation to ensure the un-installing of any pre-installed apps. However, different approaches emerge as regards the possibility for an app store operator to select pre-installed apps. Notably, while the DMA allows pre-installation, not considering it a barrier to switching, 156 the German Section 19a presumes as unlawful the exclusive pre-installation of the gatekeeper’s own offers, considering it a measure that could favor the latter over the offers of its rivals when mediating access to supply and sales markets, or that could impede other undertakings in carrying out their business activities on supply or sales markets. 157

The situation is also unclear in the United States. Indeed, as noted by Randal Picker, there is an argument that, by pre-installing some apps, the designated platform is giving advantages to its own offers over those of another business user, excluding or penalizing the offers of another business user or discriminating between similarly situated business users. 158 These practices may all be outlawed by the American Choice and Innovation Online Act. 159 Therefore, the provision in question may require an app store operator to pre-install every app in a category if installing a corresponding proprietary app; otherwise, it would be engaging in unlawful discrimination. In other words, the safety net for a designated platform to avoid liability would be an all-or-none pre-installation strategy. According to Picker, for instance, if Apple pre-installs Apple Music, it must also pre-install Spotify. 160 Alternatively, the platform owner could provide a “choice screen” allowing users to turn the proprietary app off and choose a third-party developer service.

V. Tackling App Store Practices: Antitrust or Regulation?