Abstract

In this study, I examine the role racial minorities in the boardroom can play in reducing social injustice by promoting more equal access to mortgage credit to minority households. I develop a simple theoretical model that posits directors who are racial minorities provide the credit unions they govern with a perspective that shapes lenders’ trust of minority applicants. This trust is shaped by homophily and the tendency of individuals to prefer interactions with similar individuals. Using mortgage loan data from a cross-section of credit unions in the United States from 185,446 applications, I find that credit unions where the majority of board members are minorities are less likely to reject a similarly qualified minority applicant than their counterparts. Governance by minority directors significantly reduces the effects of discrimination faced by minority applicants. The board’s effect is strongest in minority neighborhoods and where the homophily is stronger between directors and applicants.

Equality of economic opportunities for all individuals within American society is an important ideal of social justice. Owning a home, for most Americans, plays an important role in one’s future economic opportunity by building wealth, and has also been shown to affect education and other social outcomes. It has, therefore, been a long-standing policy goal in the United States to increase homeownership, particularly among minority families, to reduce the large differences in homeownership rates across racial and ethnic groups, where 76% of White households are homeowners as compared with 51% of Hispanic and 47% of Black households (U.S. Census Bureau, 2020). Increasing homeownership among under-represented minorities though requires greater access to mortgage loans. Historically, minority applicants (Black and Hispanic) for mortgages have been subject to discrimination by lenders. For example, Munnell and colleagues (1996) observed that Black and Hispanic applicants were 8.2 percentage points more likely to have their mortgage loan rejected by banks in Boston than comparably qualified White applicants. Minorities, knowing they are more likely to be rejected, are less likely to apply for loans (Neville et al., 2018), which further contributes to inequality. Lenders, therefore, have an important role in reducing economic inequality (Bapuji et al., 2020) and promoting social justice (Logsdon & Van Buren, 2008) by using fair methods to allocate credit (i.e., procedural justice) and ensuring an equitable allocation (i.e., distributive justice).

Recent calls for greater social justice have sought to remedy this type of firm behavior by redistributing power to increase the governance role of under-represented groups on firms’ boards of directors. 1 The belief is that by adding racially diverse directors to firms’ boards, there will be a greater consideration in strategic decisions based on the unique perspectives of minorities. Perspectives of minority directors are shaped, in part, by a history of discrimination and emphasize treating others in an inclusive and ethical manner (Buse et al., 2016; Smith et al., 2001). A more inclusive perspective of minority directors is thought (Hafsi & Turgut, 2013; Harjoto et al., 2015; Smith et al., 2001) to increase firms’ consideration of their social responsibilities. The empirical evidence of a relation between the race of board members and firm performance is divided (Johnson et al., 2013). For example, Hafsi and Turgut (2013) and Harjoto et al. (2015) find no relation between racial minority directors on the board and firms’ performance with respect to corporate social responsibility (CSR), whereas Buse et al. (2016) find non-profit organizations exhibit more inclusive practices the more racially diverse their boards.

According to Hillman et al. (2001), one is more likely to identify a relationship between board composition and firms’ decision making the more proximal the relation is between the board and decisions “set at the highest level of the organization” (p. 296). I theorize minority directors have a stronger interest in decisions that directly influence the well-being of minority stakeholders, more so than multi-dimensional measures of CSR performance. This interest is influenced by the homophily principle (McPherson et al., 2001), as individuals who are minorities share ties along a number of dimensions and a strong affinity with each other (Ibarra, 1995) that forms trust. Homophily based on race and ethnicity has been previously shown to influence investment decisions among venture capitalists (Gompers et al., 2016; Hegde & Tumlinson, 2014) and has been theorized (Black et al., 1997, 2001; Bostic, 2003; Fisman et al., 2017; Patel et al., in press) to influence lending decisions. Patel and colleagues (in press), for example, in their analysis of microfinance decisions call on future research to incorporate homophily between lenders and applicants into the theoretical framework of lending decisions. There is also some empirical evidence that suggests homophily influences lending decisions. Fisman et al. (2017) find that homophilous pairings between loan officers and applicants based on their caste increase lending in India, while other studies (Black et al., 1997, 2001; Bostic, 2003) have found no relation between the mortgage lending decisions of minority-owned (i.e., the majority of owners are minorities) commercial banks and minority applicants in the United States. This article compliments these previous studies and answers the call by Patel and colleagues (in press) by examining the effects homophily between directors and loan applicants has on lending decisions.

Using individual loan application data from the Home Mortgage Disclosure Act (HMDA), I find minority applicants for mortgages are 8.5 percentage points (77%) more likely, than comparably qualified White applicants, to have their mortgage loan rejected by credit unions. My contribution is that I am able to identify a mechanism in which this disparity in lending decisions between minorities and Whites is reduced based on homophily between minority directors and applicants. Credit unions governed by a board where the majority of directors are racial minorities (i.e., a majority-minority board) are 3 percentage points less likely to reject a similar mortgage application from an under-represented minority applicant than a credit union with a majority-White board. Homophily between majority-minority boards and minority applicants thus reduces the effects of discrimination on lending to minorities by more than one third. This effect is even stronger among more racially homophilous pairings, as credit unions governed by Hispanic boards reduce the effects of discrimination on lending to Hispanic applicants by nearly two thirds. Credit unions with boards where the majority of directors are minorities are found to provide more equitable access to mortgage credit to minority households than majority-White boards. I therefore demonstrate a context in which firms are more likely to promote social justice and reduce economic inequality. These findings suggest increasing representation of minorities in lending decisions may reduce the effects of discrimination observed in other lending settings, such as mortgage lending in Italy (Secchi & Seri, 2017) and microfinance (Patel et al., in press).

Theoretical Development and Hypotheses

Boards of Directors, Homophily, and Credit Unions

Directors on boards have different perspectives based on an array of individual characteristics, which vary by their relation to management (insider vs. outsider), demographics (gender, race/ethnicity), human capital (expertise), and stakeholder role (owner, customer, community member). This difference in perspective is said to shape the knowledge, and thus resources, a director brings to the firm (Hillman et al., 2000; Pfeffer & Salancik, 1978) and also the interests they work to promote (Hillman et al., 2001) and monitor (Hillman & Dalziel, 2003) on behalf of stakeholders. For a thorough review of the literature that empirically examines the relationship between board characteristics and firm performance, see Dalton and colleagues (1998), Endrikat and colleagues (2021), and Johnson and colleagues (2013). The conclusion drawn from these studies is it is difficult to discern how and when board members’ traits matter to firm decision making, as the findings often vary by context. The context I examine is the lending decisions made by credit unions in the United States in relation to the racial composition of the board of directors.

The United States is a natural setting for this analysis as demographic projections based on estimates from the 2020 Census indicate that the majority of the population will be non-White in the next few decades. Research has shown (Endrikat et al., 2021; Post & Byron, 2015) increasing a country’s gender parity amplifies the effects the presence of female directors have on the board, thus it stands to reason the racial composition of the board will continue to grow over time in importance to corporate governance. In addition, the murder of George Floyd has resulted in corporate America placing greater attention to social justice and reducing racial inequality in their public commitments (Jan et al., 2021) to support initiatives advancing homeownership, education, and entrepreneurship among minorities. Companies driven by profit, though, must balance a number of interests, which reduces their ability to act as a catalyst for promoting social justice and creates an important role for non-profits.

Credit unions are non-profit, member-owned, financial cooperatives that serve the needs of more than 120 million Americans (National Credit Union Administration [NCUA], 2019) as a financial intermediary by using their members’ savings deposits to fund loans to other members. They are governed by a board of directors, who are unpaid volunteers elected from their membership. 2 Membership in a particular credit union is restricted to individuals who each share a common bond, which is either based on occupation, association, and/or geography. Each member, regardless of the amount of their deposits, has an equal vote in electing directors to the board. This unique structure is such that directors of credit unions are more likely to be representative of their community, more so than either insiders or experts on the board. Community directors offer the board a non-business and more broad perspective to meeting stakeholder interests (Evans et al., 2022; Hillman et al., 2000, 2001), which may increase a firm’s emphasis on social performance. The governance structure of credit unions also differs significantly from commercial banks, as the interests of key stakeholder groups are more closely aligned (Macey & O’Hara, 2003) given credit unions’ members are also owners, customers, and members of the community. In addition, the chair of the board is distinct from a credit union’s CEO/manager, thus their governance is not potentially influenced by CEO-Chair duality, which can increase asymmetric information between the board and the firm’s management (Endrikat et al., 2021). Directors of credit unions thus tend to be more homogeneous along a number of individual characteristics (e.g., outsider, expertise, stakeholder group, CEO duality) than those of the typical firm, but are more likely to be representative of their diverse communities and include racial and ethnic minorities.

One of the roles of a board of directors is to monitor management’s actions and, if necessary, assert control to align the firm’s strategic actions with stakeholders’ interests. Typically, the board is not directly involved in the firm’s “tactical programs,” but instead makes sure the firm “is aware of stakeholder needs and takes them into account in board decisions and corporate strategy . . . ” (Ayuso et al., 2014, p. 420). In the case of mutually owned credit unions, the board of directors’ interest is in the provision of financial services to their members (Fried et al., 1993; Forker et al., 2014), which primarily includes the ability of members to earn interest on their savings deposits and obtain access to credit via loans. According to federal statute (12 U.S.C. § 1761b), a credit union’s board of directors is legally required to establish a credit union’s lending policies. This includes setting interest rates on loans, collateral requirements, and maximum loan limits, in addition to appointing loan officers to make decisions on whether to approve loan applications. Board members also review loan applications denied by loan officers at the request of applicants, which creates a strong and proximal relationship between the board and a credit union’s lending decisions.

Directors from under-represented groups (i.e., minorities and women) are believed (Buse et al., 2016; Hafsi & Turgut, 2013; Harjoto et al., 2015; Smith et al., 2001) to have a greater sensitivity, based on past discrimination, toward firms meeting the needs of diverse stakeholders. Among non-profit organizations, Buse and colleagues (2016) observe that racially and ethnically diverse boards exhibit more inclusive behaviors, which includes greater participation by diverse directors in developing the board’s most important policies. Buse and colleagues (2016) find that this more inclusive behavior among organizations results in improved governance practices by the board in terms of monitoring the organization and providing legal, ethical, and financial oversight. Hafsi and Turgut (2013) and Harjoto and colleagues (2015), though, find no evidence that firms with racially diverse directors perform better in terms of CSR. If directors from under-represented groups are in the minority on the board, they may find communication on the board difficult (Forbes & Milliken, 1999) and their expertise marginalized (Carter et al., 2003; Evans et al., 2022), which would explain why in certain contexts, the unique perspective of minority directors may not influence a firm’s performance. It is therefore possible that a critical mass (Post et al., 2011) of under-represented directors is necessary to influence board decisions. To avoid the potential for their marginalization, I exploit the high degree of diversity among credit union boards to examine decision making when directors who are racial and ethnic minorities are in the majority on the board (i.e., a majority-minority board).

It is also possible that the broad decisions regarding social performance examined in previous studies (Hafsi & Turgut, 2013; Harjoto et al., 2015) are not proximal enough to racially diverse board members’ interests, if they lie outside the scope of the firm’s main economic activities (Evans et al., 2022). Lending decisions (i.e., whether to deny a loan application) are among a lender’s core activities and have been shown (Palvia et al., 2014; Ward & Forker, 2017) to be associated with the presence of under-represented female directors on the board. The theory is the more influence women have on the board, there is likely a greater consideration of risk, based on women’s perspectives toward more risk-aversion (Croson & Gneezy, 2009). Palvia and colleagues (2014) find evidence of this relation, as the risk of failure among small banks in the United States during the financial crisis (2007–2010) was lower if the board of directors was chaired by a woman. Ward and Forker (2017) find further evidence that the gender composition of the board, more generally, influences risk-taking, as increasing the percentage of women on the board of directors improves loan quality among credit unions in Northern Ireland.

Previous findings suggest a more direct measure of minority directors’ perspectives and interests (Hillman et al., 2001) may be required to identify a relationship between the racial and ethnic composition of the board and lending decisions. In the case of mortgage lending, it is well established that under-represented racial minorities (i.e., Black and Hispanic individuals) in the United States are subject to discrimination and receive less access to mortgage credit (Blackburn & Vermilyea, 2006; Korver-Glenn, 2018; Munnell et al., 1996; Wheeler & Olson, 2015), whereas women do not appear to be affected (Goenner, 2010; Munnell et al., 1996). Based on this history, directors who are racial minorities are more likely to be sensitive to reducing discrimination and increasing the equitable provision of mortgage credit to minorities. This relation is further strengthened by their shared interests and ties shaped by homophily.

Homophily is a force of nature where individuals with similar characteristics are drawn together. The strongest attraction is shown (McPherson et al., 2001) to be along the dimensions of race and ethnicity. A strong correlation between individual attributes, though, implies homophily along one dimension is associated with homophily along others (Blau, 1977). For example, correlation between socio-economic status, neighborhood of residence, race, and a history of discrimination suggests minority individuals share an understanding beyond their race or ethnicity. A shared understanding (knowledge and experience) between individuals is said to facilitate their communication and the coordination of activities.

McPherson and colleagues (2001) note this tendency of individuals to prefer interactions with those who are similar affects human behavior more generally, as it “limits people’s social worlds in a way that has powerful implications for the information they receive, the attitudes they form, and the interactions they experience” (p. 415). The result, they note, is that information flows tend to be localized due to homophily, which then influences the formation of social networks, voluntary associations, and social capital. Ibarra (1995), for example, observes that minority individuals in mid-level management positions form the strongest network ties, or social capital, in business relationships with other minorities. The implication is minority directors, based on their shared understanding and network ties (e.g., social capital) with other minorities, are better suited toward understanding and meeting the unique needs of a firm’s minority customers. In the context of lending, this might imply minority directors have a better ability to communicate (e.g., marketing, loan counseling) with minority applicants and are better able to evaluate minority neighborhoods, which improves the ability of the credit unions they govern to provide credit to minority applicants.

Homophily, though, also promotes confiding between individuals (Marsden, 1988) that forms honesty and greater trust within groups of similar individuals, relative to relations with members from outside the group (Ruef et al., 2003). Homophily, therefore, results in a strong affinity (i.e., attraction) between individuals who are more likely to trust each other when faced with uncertainty. Evidence of this behavior has been observed in the investment decisions of venture capitalists. Faced with projects with similar observable measures of risk, venture capitalists are more likely to invest in start-ups with executives of their same ethnicity (Hegde & Tumlinson, 2014) and are more likely to syndicate (i.e., jointly finance) a project with other venture capitalists of the same ethnicity (Gompers et al., 2016). Homophilous pairings are said to engender greater trust and thus lessen a venture capitalist’s uncertainty in their investment decisions. Lenders face similar uncertainty in their decisions whether to provide funds (i.e., invest) to loan applicants.

A Signaling Model of Lending: Theory and Hypotheses

Previous studies (Black et al., 1997, 2001; Bostic, 2003; Fisman et al., 2017) have also considered the effects of homophilous relations on lending decisions. Fisman and colleagues (2017) find the share of credit extended by a bank in India is 6.5 percentage points higher among homophilous relations between loan officers and borrowers of the same religion/caste. Other studies (Black et al., 1997, 2001; Bostic, 2003), though, have failed to find a similar relation between the mortgage lending decisions of minority-owned commercial banks and minority applicants in the United States. Minority-directors of credit unions are more proximate to lending decisions, relative to minority-owners of banks, given they are explicitly required to set lending policies and directly oversee their implementation. In addition, minority directors of credit unions may be more willing, based on their non-profit structure, to consider social outcomes, such as the equal provision of credit to minority applicants, relative to bank owners, who may simply care about maximizing the returns on their investment. I therefore posit the racial composition of the majority of the board members is likely to influence a credit union’s lending decisions with their stakeholders who are minorities.

Below, I sketch a simple signaling model to theoretically motivate how homophilous pairings between the board and loan applicants influence lending decisions and identify factors that influence the context of this relation. 3 The model is an adaptation of a model used by Aigner and Cain (1977) to explain discrimination in employment decisions. The key feature of the model is lenders do not know an applicant’s true level of risk (q) due to asymmetric information and instead observe only a noisy signal (y) of an applicant’s risk based on the loan application data y = q + u. The signal’s error, u, is assumed to be normally distributed with mean equal to zero and constant variance. The lender’s assessment of an applicant’s risk can then be shown to equal a weighted average of the mean level of risk from the underlying population and the applicant’s observed risk measure (signal), where the weights are determined by the reliability (variance) of the signal. As the signal’s strength increases (i.e., as the level of uncertainty decreases), lenders place greater weight (i.e., trust) on observed risk measures in their lending decisions and less weight on the underlying risk in the population.

Let us assume there are two types of applicants {a, b} and that lenders have learned from past experience type b is on average higher risk. If lenders are equally well able to assess an applicant’s risk (i.e., their signals have similar variance), then for a similar observed risk score,

Now let us also assume there are two types of lenders {a, b} and that homophily between type b lenders and applicants is such that type b lenders perceive the reliability of the signal from an observed risk score from type b applicants to be stronger than type a lenders. This implies mathematically the variance in the signal’s error is smaller between type b lenders and type b applicants, than between type a lenders and type b applicants (i.e.,

The theoretical model also indicates the level of asymmetric information between lenders and applicants, captured by the difference in

The first mechanism relates to the strength of the homophily that forms trust between the lender and applicant. While minority individuals tend to share more similarities to other minorities, relative to Whites, individuals of a particular racial group tend to have the closest ties with their own race (McPherson et al., 2001; Wimmer & Lewis, 2010). Directors are, therefore, more likely to have a better understanding of the needs of their own racial group and promote these interests on the board (Hillman et al., 2001). Hispanic individuals, for example, share a common language (Spanish), thus one might expect credit unions with Hispanic board members to be more effective in their communication (Noriega & Blair, 2008) and transfer of information with Hispanic applicants, more so than with applicants who are Black or Asian. This implies the trust lenders with majority-minority boards place in a minority applicant increases with their racial similarity, relative to a majority-White board. The second hypothesis is then as follows:

The second mechanism that influences the information asymmetry between lenders and applicants for mortgage loans is the neighborhood where the property is located. Quillian and Pager (2001) show while perceptions of neighborhood disorder are influenced by observed differences (e.g., crime statistics, graffiti, boarded up buildings), they are also influenced by a neighborhood’s racial diversity. Neighborhoods with a higher percentage of minorities (i.e., minority neighborhoods) are perceived to have greater disorder than those of White neighborhoods with other similar observables. This suggests comparable minority neighborhoods are also perceived to be higher risk than comparable White neighborhoods, and homes in these neighborhoods are not perceived to be equal in value and collateral (Korver-Glenn, 2018). Quillian and Pager (2001) find this bias against the perception of minority neighborhoods is significantly less among minority residents of the same race and ethnicity (i.e., increasing a neighborhood’s share of Hispanics) and has less effect on the perception of disorder among Hispanics than Whites, with a similar reduction of bias observed among Blacks. Credit unions governed by majority-minority boards, I theorize, are subject to less bias with respect to their assessment of properties in minority neighborhoods, relative to their counterparts with majority-White boards. The third hypothesis is then as follows:

Method

Empirical Model Specification

The empirical model specification of the mortgage lending decision is adapted from the theoretical model. The dependent variable is the binary outcome of the lender’s decision whether to deny a mortgage application. Let the decision of credit union l to deny a mortgage loan from applicant i, in metro area m, be given by Equation 1:

Influencing the lenders’ decisions are a vector of applicant risk characteristics observed by the lender from the loan application, denoted by

The model specification also controls for credit union and metropolitan statistical area (MSA) fixed effects. Fixed effects control for the fact that lending decisions not only depend on applicant characteristics but also on a credit union’s underwriting guidelines and differences in market conditions. A credit union’s underwriting guidelines are influenced by both observable factors (e.g., past loan performance, liquidity, net worth) and unobservable factors (e.g., management’s risk-aversion, firm strategy). For example, a credit union with a poorly performing loan portfolio may increase their requirements to approve a loan, which would affect their lending decisions, relative to a credit union with strong financial performance. If these observed or unobserved effects were left uncontrolled for in the specification, then the estimates would be biased. Including a separate fixed effect,

To test the first hypothesis, I use the interaction term in the specification,

The third hypothesis considers the effects a majority-minority board has on lending to minority applicants in minority neighborhoods. I test this hypothesis by expanding the model specification in Equation 2 with additional interaction terms between minority applicants and minority neighborhoods, minority neighborhoods and majority-minority boards, and minority applicants, minority neighborhoods, and majority-minority boards.

A minority applicant with characteristics,

Data and Sample

The loan data used in this article are drawn from the publicly available 2015 HMDA Loan Application Registrar. 4 A number of studies have used HMDA data to examine the effects of race on the distribution of mortgage credit (Holmes & Horvitz, 1994; Wheeler & Olson, 2015) and mortgage lending decisions (Black et al., 1997, 2001; Bostic, 2003) by commercial banks. The database contains basic information collected by depository institutions from loan applicants and includes risk characteristics of the applicant, the census tract of the property location, and details of the loan that include the lender’s decision. The analysis is limited to conventional loan applications at credit unions for the purchase of single family (1–4 family), owner-occupied, properties. The sample consists of 185,466 loan applications from 1,690 credit unions. Credit unions are only required to report their loan information if their total assets are more than US$44 million, they have an office or branch within an MSA, and they originate at least one mortgage loan, which explains why a large number (4,452) of small credit unions are not represented in the data.

Measures

The dependent variable in the model specification is the outcome of the lender’s decision whether to deny a mortgage application. For the lending decision, loans are classified as denied if either a preapproval request is denied or the application is denied and are classified as approved if they are either originated or approved and not accepted by the applicant. The specification controls for several standard (Wheeler & Olson, 2015) measures of applicant risk, which include the applicant’s income (natural logarithm), the loan amount (natural logarithm), and the ratio of the loan amount to income. 5 Including the loan amount serves as a proxy for an applicant’s accumulated wealth (Black et al., 2001), while the ratio of the loan amount to income proxies for an applicant’s debt to income ratio (Wheeler & Olson, 2015). Demographic variables are also included to control for applicants’ gender (Avery et al., 2007; Wheeler & Olson, 2015) and race.

Loan applicants are asked to report their race (White, Black or African American, Asian, American Indian or Alaska Native, Native Hawaiian or other Pacific Islander) and ethnicity (Hispanic or non-Hispanic). The complication is individuals are allowed to choose multiple racial categories, which results in several different possible groupings when combined with ethnicity. I use Avery and colleagues’ (2007) hierarchical approach, which classifies individuals into a single category in the order of Black, Hispanic, American Indian, Pacific Islander, Asian, and White. That is to say, an applicant who identifies as Black for any of the races they report is uniquely classified as Black. Individuals who are not already classified (non-Black) are then classified Hispanic, if their ethnicity is Hispanic. The process continues in order with American Indians, until each of the applicants are in one of six racial categories. The analysis is restricted to Black, Hispanic, Asian, and White applicants, given a lack of observations among the other racial categories. I define minority applicants as Black or Hispanic (i.e., under-represented minorities) and non-minorities as White or Asian and also examine each racial and ethnic group separately.

Added to the specification are two variables that indicate potentially distinct loan products (Avery et al., 2007). Applicants can initiate their loan request for a preapproval, which differs from prequalification in that it represents a commitment by the lender and requires a full review of the applicant and verification of information. Avery and colleagues (2007) suggest it is possible loans subject to a preapproval process may have different underwriting standards than other loans, which I control for by including an indicator variable. The other loan product identifiable in the dataset is a piggyback loan, where mortgage applicants take out two loans simultaneously to avoid the payment of private mortgage insurance (PMI). The loan with first-lien status would have a loan to value (LTV) ratio of 80% to avoid PMI, whereas the second-lien loan would have junior-lien status and typically a LTV ratio of 10%. Second-lien piggyback loans are excluded from the sample to avoid having non-independent observations, and an indicator is included to account for piggybacked first-lien loans possibly having different underwriting standards.

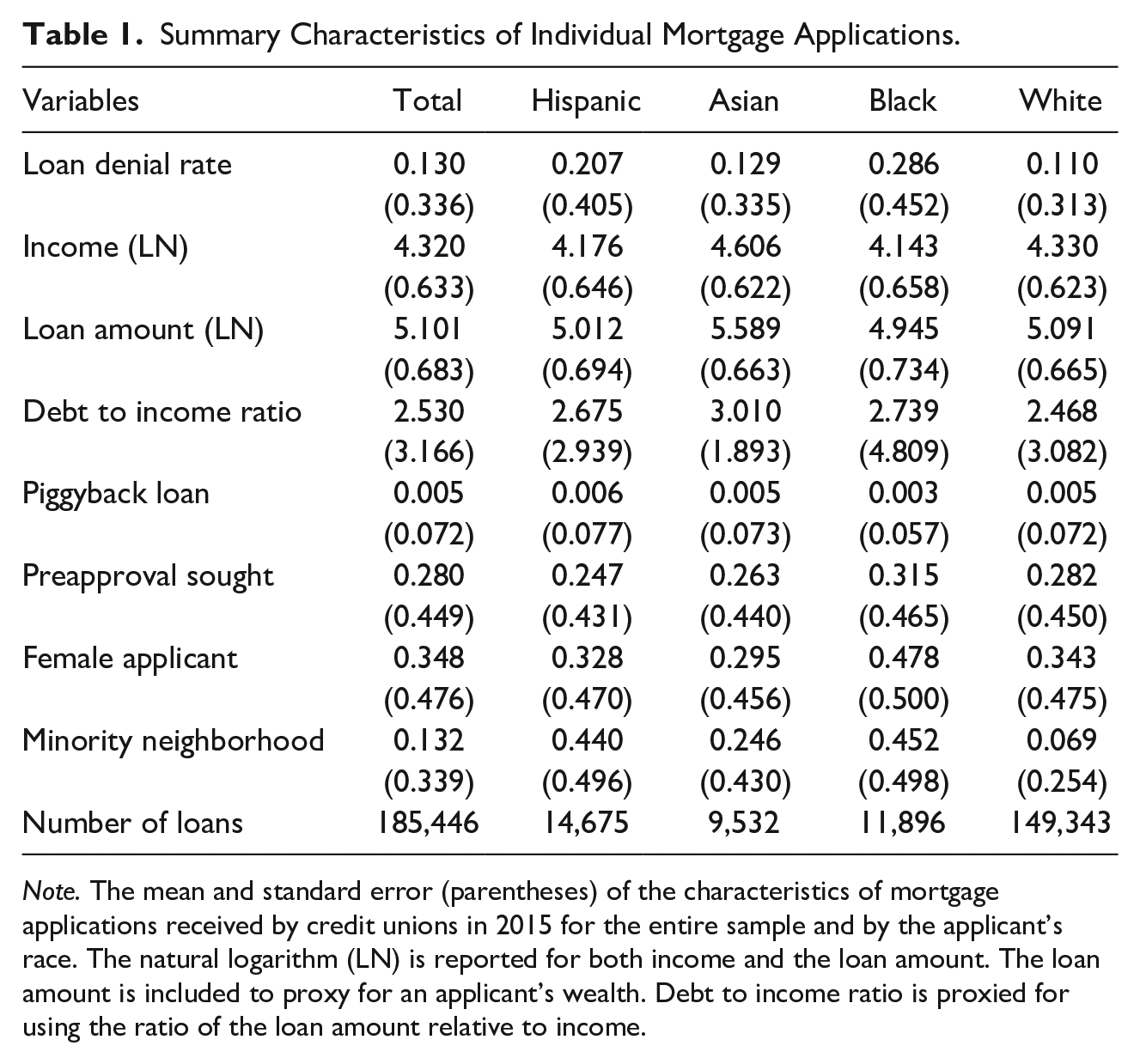

Summary statistics for the individual loan-level data broken down by the applicants’ race and ethnicity appear in Table 1. 6 Eighty-one percent of mortgage applications by credit unions are from White applicants, with Hispanics making up 8% of the sample, Blacks making up 6%, and Asians 5%. Minority applicants, on average, are more likely to have their loan applications denied than White applicants, as Hispanics and Blacks are denied 21% and 29% of the time when compared with 13% for Asians and 11% for Whites. Without conditioning on other factors, Black applicants are 2.6 times more likely to be rejected than a White applicant. Not surprisingly, the data also show that under-represented minority applicants (Hispanic and Black) are more likely to apply for loans on properties in minority neighborhoods. Asian applicants, on average, have the highest income and seek the largest loans. The other measures tend to be similar across different racial groups.

Summary Characteristics of Individual Mortgage Applications.

Note. The mean and standard error (parentheses) of the characteristics of mortgage applications received by credit unions in 2015 for the entire sample and by the applicant’s race. The natural logarithm (LN) is reported for both income and the loan amount. The loan amount is included to proxy for an applicant’s wealth. Debt to income ratio is proxied for using the ratio of the loan amount relative to income.

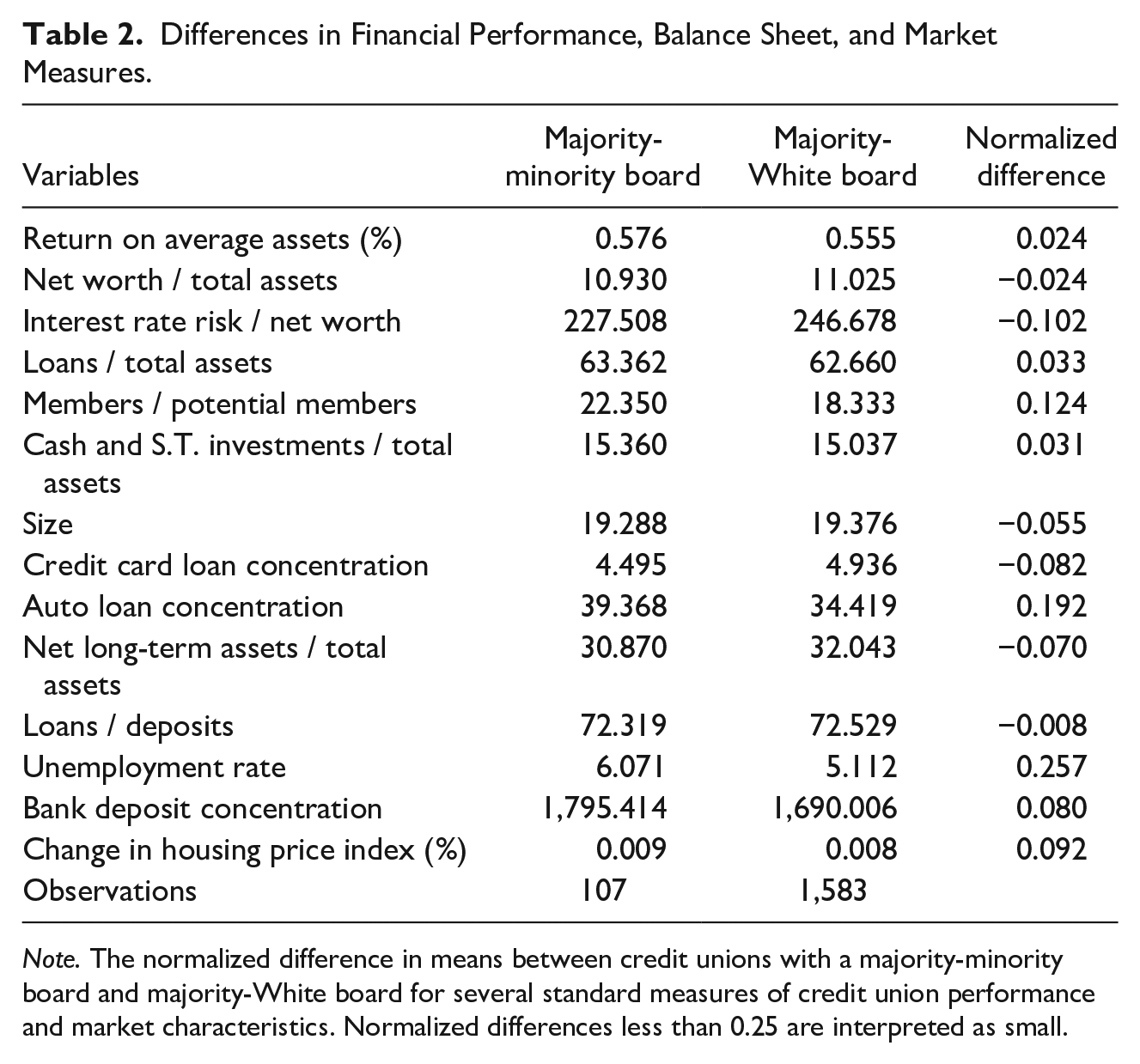

Call report data publicly released by the NCUA since 2012 contain information indicating whether the majority of a credit union’s board members are minorities (e.g., Black, Hispanic, American Indian, Pacific Islander, Asian). 7 The data reveal that there is very little transition over time between credit unions run with one type of board being run by another, as less than 1% of credit unions’ racial composition changes in a given year. Of the 1,690 credit unions in the HMDA data, I observe 107 with majority-minority boards in 2015. Credit unions with majority-minority boards are very similar to those with a majority-White board across a number of financial performance, balance sheet (asset and liability), and market measures. None of the measures examined have a normalized difference greater than 0.26, which is small and indicates the two groups are statistically similar (Imbens, 2015). Normalized differences between the types of boards appear in Table 2. 8

Differences in Financial Performance, Balance Sheet, and Market Measures.

Note. The normalized difference in means between credit unions with a majority-minority board and majority-White board for several standard measures of credit union performance and market characteristics. Normalized differences less than 0.25 are interpreted as small.

The return on average assets is similar across the two types of boards—majority-minority boards have a return on assets of 0.576% and majority-White have a return of 0.555%. Furthermore, I find the two types of credit unions are similarly capitalized (net worth / total assets), and have similar exposure to interest rate risk. Liquidity as measured by the ratios of loans to total assets and cash to total assets are similar across the two groups. Loan shares in credit cards (unsecured credit) and auto loans are also similar, as is the share of long-term assets among total assets. There is also no significant difference in size—credit unions with a majority-minority board average US$420 million in total assets, relative to US$656 million for majority-White boards. Market conditions are also similar across the credit union’s home markets for the two groups. I find there to be no difference in the level of banking competition (Ely, 2014) and home price appreciation (Bogin et al., 2016) in the MSA, or county when applicable, where the credit union is headquartered, and find only a small difference in unemployment. This similarity between credit unions that vary in the racial composition of their boards differs from the significant difference in size and operating environments observed by Black et al. (2001) among banks. The similarity here of the observables of the two lender types is important, as it reduces the potential for differences in unobservable factors introducing bias into the estimates and eliminates the need for matching.

Statistical Analysis

To test the hypotheses, I need to find the marginal effect of having a majority-minority board on lending to minority applicants, which in the model specification is determined by an interaction term between an applicants’ race and an indicator of a majority-minority board. Typically, when faced with a binary dependent variable, one would use a logit or probit specification to estimate the model. Matters are complicated here because of the need to control for individual lender fixed effects in the model specification, which are correlated with the regressors. A probit model with fixed effects is not an option, as estimates of the model’s coefficients are known to be inconsistent (Wooldridge, 2010). One is able to use fixed effects logit to find consistent estimates of the regressors (α, β), but the issue is that one cannot determine the corresponding marginal effects. The marginal effects of a variable in the logit model are a non-linear function of all the coefficient estimates (α, β, δ i ) and the covariates evaluated at values selected by the researcher. Unfortunately, the fixed effects logit model does not produce consistent estimates of the lender fixed effects (δ i ), therefore one is unable to evaluate the marginal effect without assuming arbitrary values of the lender effects.

The estimation approach used here is a linear fixed effects model, which is also referred to as the within estimator. The one drawback of the model is that the predicted response is not necessarily constrained between 0 and 1, but this is not crucial here, as my interest is only on the marginal effects for testing the hypotheses. The linear prediction model provides consistent and unbiased estimates of the regressors (α, β) and allows reasonable predictions of their marginal effects, even in the presence of a binary dependent variable (Wooldridge, 2010). The marginal effects of the linear specification are also easy to interpret, as they do not depend on the lender-level fixed effects, which are unable to be consistently estimated. The errors of the linear model with a binary dependent variable are known to exhibit heteroscedasticity if left uncorrected, but this is remedied by the use of cluster robust standard errors that correct for heteroscedasticity and correlation of errors within lenders.

Results

Board Composition and Individual Mortgage Lending Decisions

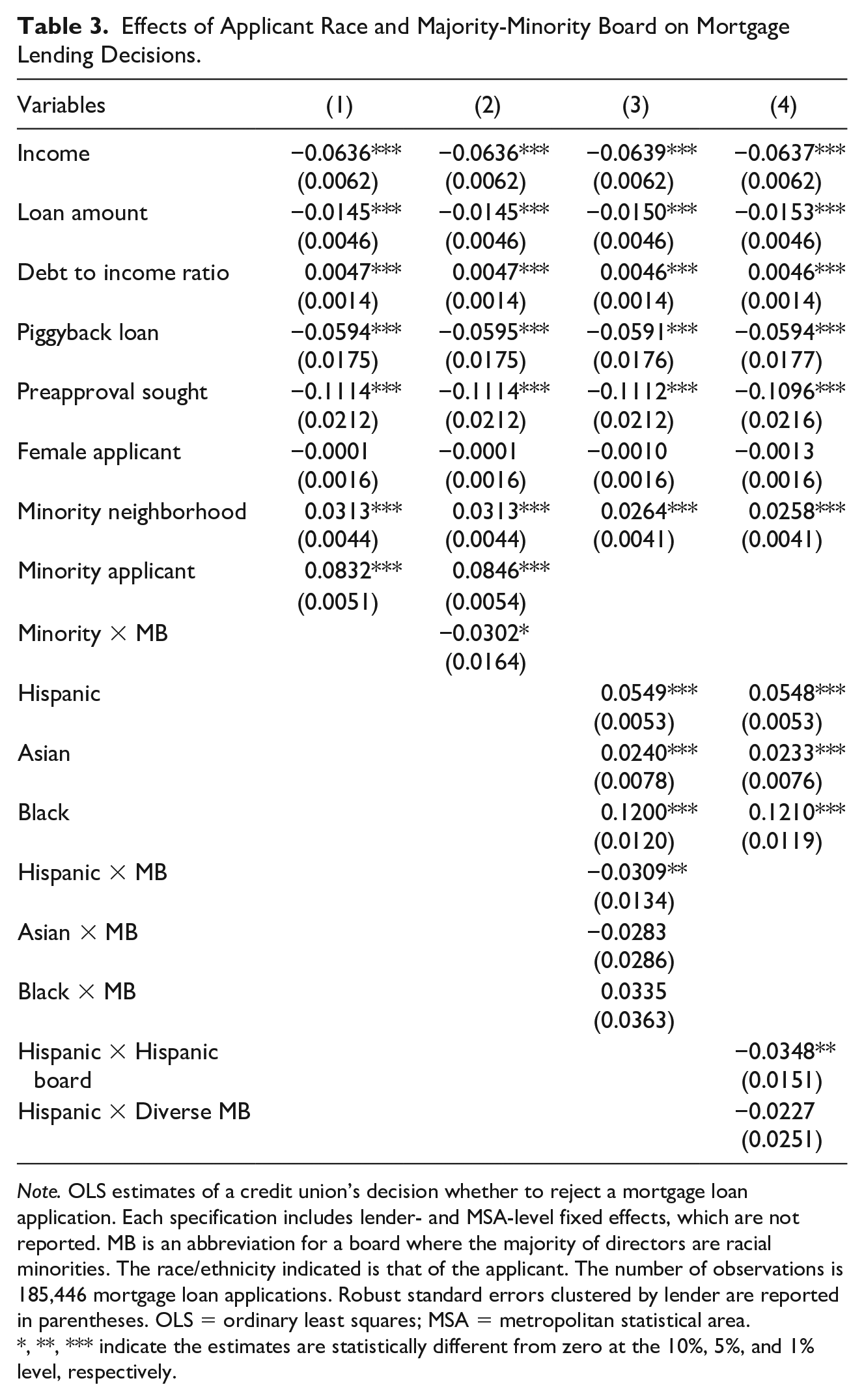

The first set of results from Model 1 (Table 3, column 1) establishes a baseline on the lending decision when the credit union’s lending policies do not depend on the majority of the board’s homophily with the applicant. Under-represented minority (Black and Hispanic) applicants are on average 8.3 percentage points more likely to have their mortgage loan applications rejected than comparable White and Asian applicants. This estimate is similar in magnitude to the 8.2 percentage point difference found in Munnell and colleagues’ (1996) analysis of commercial bank loans in Boston in 1990. The coefficients for the control variables are what one would expect. Increasing an applicant’s income by 1% reduces their likelihood of being rejected by 6.4 percentage points (p value .000). Higher wealth, which is proxied for by the logarithm of the loan amount, reduces the likelihood of rejection by 1.5 percentage points (p value .002) for a 1% increase in the loan amount. The final applicant measure of risk, the debt to income proxy, indicates a one standard deviation in its value increases the likelihood of denial by 1.5 percentage points (p value .001). I find that loans that either go through a preapproval process or involve a piggyback loan are less likely to be denied, which indicates each are unique in terms of their underwriting standards. Gender did not have a statistically significant effect (p value .974) on the lending decision—a result also found by Munnell and colleagues (1996). Loan applicants with properties in minority neighborhoods were 3.1 percentage points more likely to have their loans rejected, all else equal.

Effects of Applicant Race and Majority-Minority Board on Mortgage Lending Decisions.

Note. OLS estimates of a credit union’s decision whether to reject a mortgage loan application. Each specification includes lender- and MSA-level fixed effects, which are not reported. MB is an abbreviation for a board where the majority of directors are racial minorities. The race/ethnicity indicated is that of the applicant. The number of observations is 185,446 mortgage loan applications. Robust standard errors clustered by lender are reported in parentheses. OLS = ordinary least squares; MSA = metropolitan statistical area.

, **, *** indicate the estimates are statistically different from zero at the 10%, 5%, and 1% level, respectively.

Next, I add to the model specification in Model 2 an interaction between whether an individual is a minority applicant (Black or Hispanic) and whether the credit union has a majority-minority board to test if they have lending policies that favor minority applicants (Hypothesis 1, that is, they are less likely to reject a similarly qualified minority applicant). The estimate of the interaction term in Model 2 (Table 3, column 2) indicates credit unions with majority-minority boards are 3.0 percentage points less likely to reject an under-represented minority applicant than are credit unions run by majority-White boards. The estimate is statistically different than zero (two-tailed test) at the 10% level with a p value equal to .066. Homophily between majority-minority boards and minority applicants reduces the probability a minority is rejected by 15.5% and reduces the effects of discrimination in lending to minorities by more than one third (36%). 9 This finding supports the first hypothesis that credit unions with majority-minority boards are less likely to reject minority applicants, relative to boards where the majority of directors are White.

I next examine in Model 3 whether the observed difference in lending policies is homogeneous across different racial groups of applicants. The specification of Model 3 (Table 3, column 3) includes indicator variables for each applicant’s race and ethnicity (Hispanic, Asian, and Black), where White is the omitted reference group. Each groups’ indicator variable is interacted with an indicator of a majority-minority board, such that the marginal effect of an applicant’s race is conditional on whether their credit union has a majority-minority board. The results indicate the probability an applicant is rejected differs by their race and ethnicity. Among credit unions governed by majority-White boards, Hispanic individuals are 5.5 percentage points more likely to be rejected than White applicants, while Asian and Black applicants are 2.4 and 12 percentage points, respectively, more likely rejected than White applicants. Finding Asian applicants are discriminated against less than the other two minority groups is consistent with others (Avery et al., 2007) who find lending patterns to Asian applicants are more similar to Whites than other minorities. I find that Hispanic applicants, though, are 3.1 percentage points less likely to be denied by a credit union with a majority-minority board than by a majority-White board—a result statistically different than zero at the 5% level with a p value of .021. Credit unions governed by majority-minority boards thus reduce the probability a Hispanic applicant is denied by 18.7% and reduce the effects of discrimination on lending to Hispanic applicants by more than one half (56.3%). However, I did not find the presence of a majority-minority board had an effect on whether an Asian or Black applicant was denied, relative to a majority-White board.

Contained in the call report profile information of credit unions with majority-minority boards are indicators for whether a minority racial or ethnic group is represented within a board. The data do not allow one to identify the specific percentage of each group within each majority-minority board, but one is able to identify variation in the racial and ethnic composition of members on majority-minority boards (i.e., one is able to distinguish a majority-minority board made up of Hispanic board members, a Hispanic board) versus a majority-minority board consisting of Hispanic, Asian, and Black board members, along with several other pairings. I use this information to test (Hypothesis 2) whether the racial composition of directors on majority-minority boards effects credit union lending policies toward applicants of the same race and ethnicity, relative to those of majority-White boards. I find, in results not reported here, that the only statistically significant relation is between majority-minority boards made up of Hispanic directors and Hispanic applicants. 10 The specification of Model 4 reported in Table 3, column 4, uses a restricted sample of loans from majority-White boards and Hispanic boards. The estimates indicate that Hispanic boards are 3.2 percentage points less likely to reject Hispanic applicants than are majority-White boards (p value .023). Credit unions governed by Hispanic boards thus reduce the probability a Hispanic applicant is denied by 21.1% and reduce the effects of discrimination on lending to Hispanic applicants by nearly two thirds (63.5%). This supports the second hypothesis that directors of a majority-minority board implement more lenient lending policies toward applicants of similar ethnicity and race.

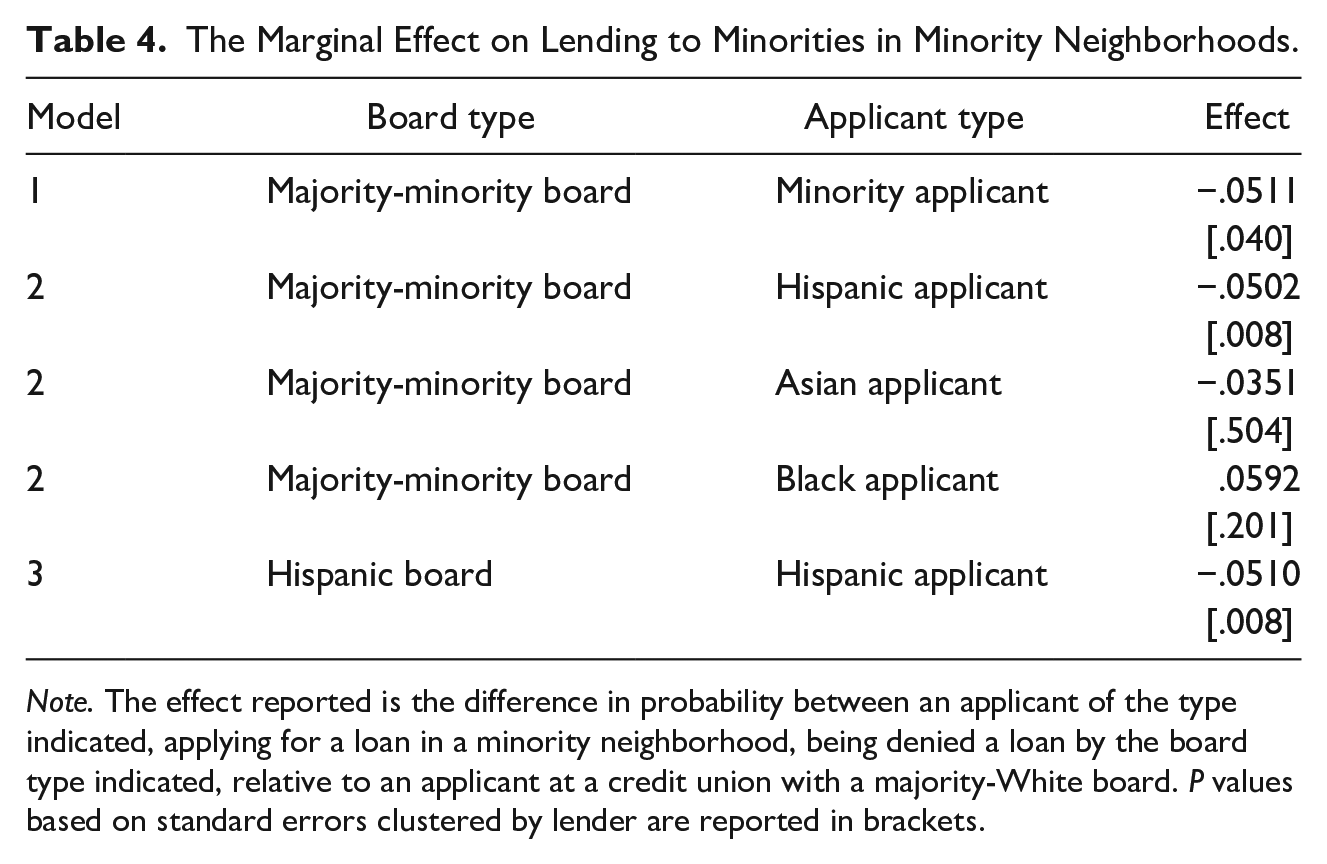

Next, I examine whether a property in a minority census tract has an effect on credit unions’ lending policies toward minority applicants (Hypothesis 3). My interest is in testing the relative difference in policies between majority-minority and majority-White boards, which is the sum of the three coefficients on the interaction terms between minority applicants and a majority-minority board; a majority-minority board and minority tract; and minority applicants, a majority-minority board, and minority tract. To conserve space, I report for each specification only the sum of the three coefficients and the associated p value needed to test the third hypothesis. The results for Model 1 (Table 4, row 1) indicate a strong relation between a majority-minority board’s lending policies and lending to minority applicants in minority neighborhoods. Under-represented minority applicants in a minority census tract are 5.1 percentage points less likely (p value .040) to have their application rejected from a credit union with a majority-minority board, relative to a majority-White board. This effect is stronger in terms of magnitude and statistical significance than the 3.0 percentage point difference (p value .066) I found more generally. I thus find evidence to support my third hypothesis that majority-minority boards have a stronger effect on decision making when uncertainty with the firm’s environment is larger.

The Marginal Effect on Lending to Minorities in Minority Neighborhoods.

Note. The effect reported is the difference in probability between an applicant of the type indicated, applying for a loan in a minority neighborhood, being denied a loan by the board type indicated, relative to an applicant at a credit union with a majority-White board. P values based on standard errors clustered by lender are reported in brackets.

Examining the heterogeneous effects of race across minority neighborhoods, I find that the results in Model 2 (Table 4, rows 2–4) are again being driven by Hispanics and corroborate my previous findings. Hispanic applicants in minority tracts are 5.0 percentage points less likely (p value .008) to have their application rejected from a credit union with a majority-minority board, relative to a majority-White board. I again find no evidence of an impact on the lending policies by credit unions with majority-minority boards to Asian or Black applicants in minority neighborhoods—the p value for Asian applicants is .504 and is .201 for Black applicants. The final specification of Model 3 (Table 4, row 5) restricts the sample again to credit unions with majority-White boards and Hispanic boards. I interact minority tract, an applicant’s race, and whether a majority-minority board is Hispanic. The estimates indicate that Hispanic applicants in minority neighborhoods are 5.6 percentage points less likely to be rejected by a Hispanic board than a majority-White board—an estimate statistically different than zero with a p value of .008.

Mortgage Lending in the Aggregate

In this next analysis, I examine the relative importance credit unions and their boards place on providing mortgage credit to minority applicants at the aggregate level. That is, I consider whether credit unions with majority-minority boards and Hispanic boards originate a larger share of their loans to minority applicants than their counterparts with a majority-White board. This accounts not only for possible differences in lending decisions but also differences in outreach (e.g., marketing, counseling) prior to an application being completed. The model’s specification is given by Equation 3, where I estimate lender l’s share of mortgage loans (by dollar value) originated in metro area m that are to minority applicants

The individual loan data are aggregated by lender and metro area, which implies there are multiple observations for lenders that operate in more than one metro.

11

Controlling for a lender’s share of loan applications and originations are several differences in lenders’ financial conditions that are included in

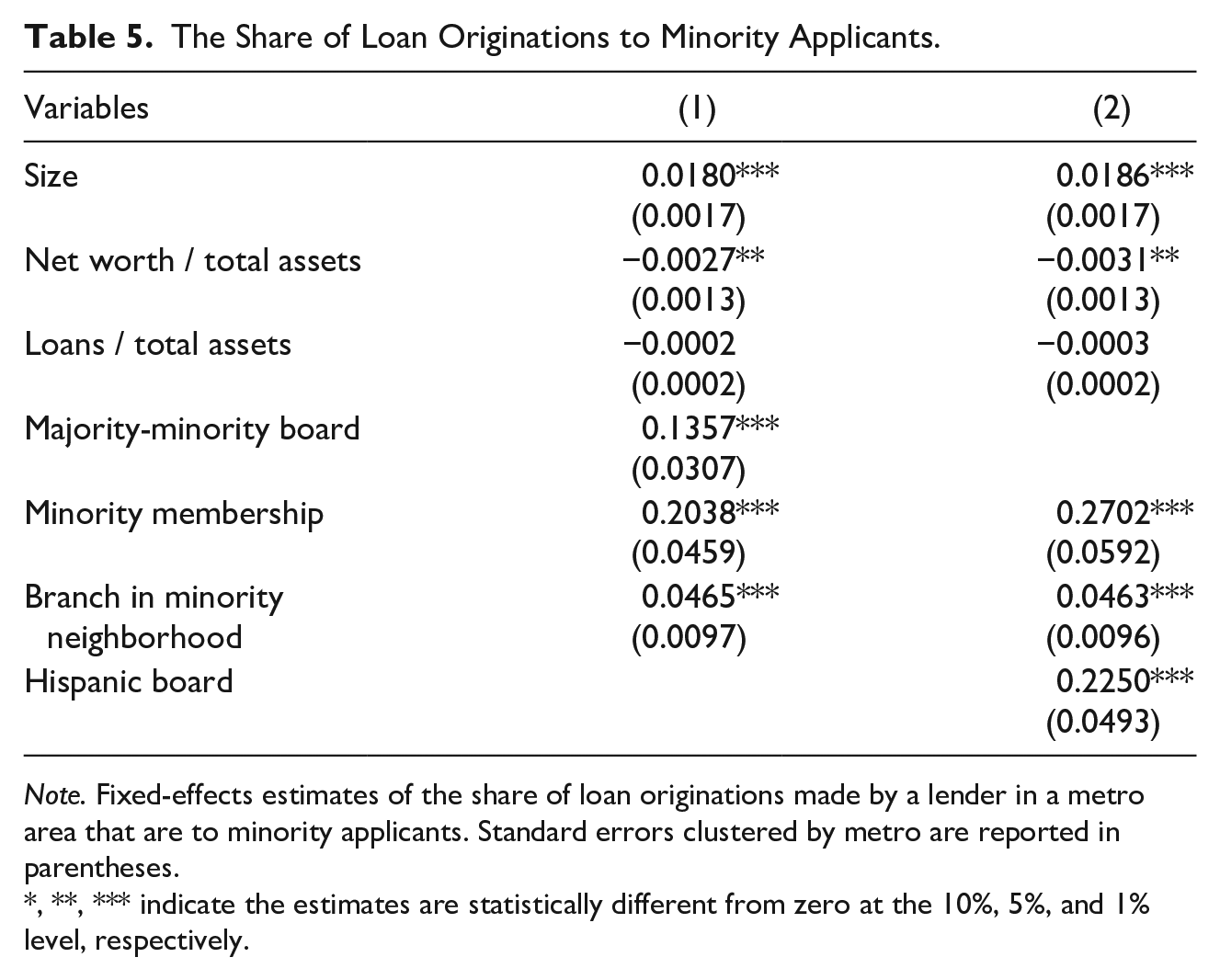

I find in Model 1 (Table 5, column 1) credit unions that have a majority-minority board originate a higher share of their loan applications to minority applicants within an MSA than do majority-White boards. The difference I observe is 13.6 percentage points and is statistically different than zero with a p value of less than .001. For comparison, Fisman and colleagues (2017) observe a shared caste/religion between loan officers and applicants increases a group’s share of credit by 6.5 percentage points. The racial demographics of the credit union’s members have a large effect on the share of credit. Not surprisingly, I find credit unions where a majority of members are racial minorities have a higher share of loan originations than when they are in the minority. A credit union having a branch location within a minority tract of the MSA also increased the share of loans to minorities by 4.7 percentage points. A credit union’s size was found to increase the emphasis on minority lending. Increasing size by 1% increases the share of origination to minorities by 1.8 percentage points. Credit unions that were more solvent (i.e., had a larger net worth relative to total assets) were observed to have lower shares of their loan originations to minority applicants, and specialization in lending had no effect. In Model 2’s specification (Table 5, column 2), I limit the sample to majority-White and Hispanic boards to consider the effect a minority board of Hispanic directors has on the share of loans to minorities. The share of loans originated to minorities from boards of Hispanic directors is 22.5 percentage points higher than those where White directors are the majority of the board.

The Share of Loan Originations to Minority Applicants.

Note. Fixed-effects estimates of the share of loan originations made by a lender in a metro area that are to minority applicants. Standard errors clustered by metro are reported in parentheses.

, **, *** indicate the estimates are statistically different from zero at the 10%, 5%, and 1% level, respectively.

Discussion

This article examines whether homophily between minority individuals influences lending to minority applicants by credit unions governed by a majority of directors who are racial minorities. I find the effects of discrimination observed by minority applicants is reduced by 3 percentage points, or more than one third, when they apply at a credit union governed by a majority-minority board. I also find majority-minority boards place a greater emphasis on lending to minorities than majority-White boards in the aggregate, as their share of mortgage loans made to minorities is 13.6 percentage points higher. The impact of the board on individual lending decisions is moderated by the neighborhood where the property is located. Credit unions governed by a majority-minority board are 5.1 percentage points less likely to reject a minority applicant in a minority neighborhood relative to a majority-White board. Homophily and the benefits of greater trust are thus shown to increase among minority individuals with added uncertainty in their economic environment.

The strength of homophily on lending decisions is also shown to vary by racial group and has been found to vary in other investment decisions (Hegde & Tumlinson, 2014). I find Hispanic boards and applicants share strong ties, while there is no evidence to suggest a similar racial homophily among Asian or Black individuals. This may, in part, be explained by the small number of homophilous relations observed in the dataset between boards and applicants who are Asian (91 observations) or Black (158), relative to those between Hispanics (2,578).

A heterogeneous effect might also be explained by variation in the strength of homophily across ethnicities within a racial group. Hispanic individuals share a common language (Spanish) and religion (Catholicism), which creates a higher degree of cultural similarity across different ethnicities among Hispanics. Wimmer and Lewis (2010) find this results in a high degree of homophily among the friendships of Hispanic young adults across both race (i.e., Hispanic) and ethnicity (e.g., Cuban, Mexican, Dominican). This differs significantly from Asians, where they find homophily only exists between exclusive pairs of Chinese, Vietnamese, South Asian, and East Asian young adults. It is thus possible the homophily between Asian boards and Asian applicants is weak if directors and applicants are of different ethnicities, which is a distinction I am unable to identify in the data. Homophily, though, is observed by Wimmer and Lewis (2010) to be strong among Blacks across both race and ethnicity; thus, it is less clear why I may not observe an effect between Black minority boards and Black applicants. It might be possible that Black directors hold a racial bias against their own race’s financial decision making that is consistent with the perspective of the majority. Korver-Glenn (2018) observed evidence of this perception from a Black lender she interviewed, who explained the observed disparity in lending decisions by race is because Black and Hispanic applicants “screw up their credit” (p. 645). Black and colleagues (1997) observe more widespread evidence of this in-group bias among Blacks, as they find Black applicants are more likely to be rejected by Black-owned than White-owned banks. Differences in individuals’ taste preferences (Becker, 1957) may then shape the effect homophily has on lending decisions.

Homophily is said to form trust and is shown here in various contexts to influence lending decisions. An unresolved question is whether this trust is “blind” in the sense that it is solely motivated in these contexts by a taste preference for in-group interactions. If homophilous relations are based on taste and do not involve the transfer of valuable information and a reduction in asymmetric information, then investment decisions based on homophily are expected (Fisman et al., 2017; Gompers et al., 2016; Hegde & Tumlinson, 2014) to perform more poorly in comparison. For example, if Hispanics prefer homophilous pairings based on race, then they may be willing to accept higher observed risks from loans originated to Hispanics based on a taste preference alone. In this case, credit unions governed by Hispanic boards would systematically make riskier loans to Hispanic applicants and their mortgage loan portfolio would be expected to perform worse than their counterparts without this preference.

An alternative is trust in homophilous pairings is informative if it increases the transfer of information and reduces the effects of asymmetric information. In this case, loans originated by Hispanic credit unions to Hispanic applicants might appear higher risk based on observables, but are of similar risk when accounting for the unobservable transfer of information that reduces uncertainty in lending. Information transfer would imply loan portfolios across different board types might perform similarly, despite a difference in lending decisions. I find no evidence to suggest credit unions with majority-minority boards perform any differently than those with majority-White boards, as a comparison of the average return on assets and delinquency rate of mortgage loan portfolios are not statistically different across the two groups. Similarly, I find no statistically significant difference in the performance of credit unions with Hispanic boards and those with majority-White boards. This suggests homophily in certain contexts allows for the transfer of information between lenders and applicants that is unobserved by the researcher in the data and reduces risk in the lender’s judgment.

For example, it is well documented (Scott, 2015) among low-income Hispanic households in the United States that it is common to have extended family members contribute income toward the cost of housing. This additional income is difficult to verify and is not included in an applicant’s reported income under the HMDA and is less likely to be used in underwriting decisions. 13 If credit unions with Hispanic boards better understand this relationship among Hispanics and implement policies to verify and use familial income in their lending decisions, then it would appear based on observable income and other risk measures that they are willing to accept higher risks from Hispanic applicants than a majority-White board. These applicants may, therefore, be of similar risk after accounting for differences in unobserved familial income, which would explain the seemingly difference in the leniency of lending policies and the similarity in loan performance.

Limitations and Future Research Directions

The theoretical model I developed is adapted from the employment model of Aigner and Cain (1977). Therefore, my model’s implications may also be generalizable to employment decisions, where firms with racially diverse boards are more likely to employ diverse employees or employees similar to their own race. Damaraju and Makhija (2018) find evidence of this behavior based on caste and CEO selection in India. Further research should explore the effects diverse boards have on promoting diversity in employment decisions, as it relates to decision makers throughout all levels of the firm. Racially diverse employees also help firms understand their diverse customer base (Richard, 2000) and may act as an additional mediator in the relation between board diversity and firm decision making. This is a limitation of my study, as I lack data on the racial composition of the credit unions’ managers and employees. The inclusion of a fixed effect for each credit union allows for differences in the racial composition of employees to affect the mean, but it does not allow for employee diversity to have a heterogeneous effect on lending to minority applicants (Fisman et al., 2017).

Another limitation of my study is a lack of data on the number of minority directors of each race that compose these boards. Instead, I am only able to identify in Call Report data indicators of whether the board has a majority of directors who are racial minorities and whether a given racial group is present. This prevents me from examining whether homophily affects lending decisions in cases where there is a critical mass of minority directors less than the majority (Post et al., 2011). In settings where diversity is less prevalent, or is less homophilous, it may be insufficient to shape decisions affecting minority stakeholders by simply increasing representation of minorities on boards along the margin. In addition, while board members of credit unions are more homogeneous along a number of individual characteristics than in the typical firm setting, I only considered the effects of race, given the well-established disparity in lending outcomes across racial groups. Future researchers might wish to similarly consider whether the gender composition of the board influences individual lending decisions. Given I find no evidence to suggest female applicants are subject to different lending policies than male applicants, I believe this line of inquiry may be less fruitful.

Conclusion

Discrimination in lending outcomes among under-represented racial minorities (Black and Hispanic) is well established. I find here that directors of credit unions, where the majority of directors are racial minorities, provide the credit unions they govern with a perspective and trust based on homophily that shapes the firm’s interactions with minority applicants, the result of which is credit unions with majority-minority boards are less likely to reject minority applicants with similar loan applications and place a greater emphasis on lending to minorities, relative to lenders with majority-White boards. I identify a strong business case for increasing the representation of minority directors among lenders, as it promotes social justice by providing greater access to mortgage credit to minority households without negatively affecting performance. Lending by credit unions is limited by their members’ deposits, thus another means of increasing economic opportunity is influenced by an individual’s choice of financial institution. Choosing to save with a credit union governed by minorities will increase access to credit by minorities, which is important to their financial wellness and that of their communities, as it provides a “passport to the broader economy” (Summers, 2000). My findings also call for the need to further identify and reduce the sources of bias that continue to perpetuate lenders’ (Korver-Glenn, 2018) perceptions of minorities, with a particular emphasis on those of Black applicants.

Supplemental Material

sj-docx-1-bas-10.1177_00076503211062182 – Supplemental material for Majority-Minority Boards of Directors and Decision Making: The Effects of Homophily on Lending Decisions

Supplemental material, sj-docx-1-bas-10.1177_00076503211062182 for Majority-Minority Boards of Directors and Decision Making: The Effects of Homophily on Lending Decisions by Cullen F. Goenner in Business & Society

Footnotes

Acknowledgements

I would like to thank the editor Punit Arora and three anonymous reviewers of the journal for their insightful comments, which helped to improve this article. I also extend thanks to Margie Tieslau, Corinne Post, and conference participants at the Missouri Valley Economic Association annual meeting for their feedback. I also acknowledge research support from the Nistler College of Business and Public Administration at the University of North Dakota.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biography

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.