Abstract

Existing research suggests people with stronger moral character traits are more inclined to ethical investing. We take a moral foundations framing approach that synthesizes framing theory and moral foundations theory to investigate whether a moral state of mind created by moral foundations frames can also increase retail investors’ ethical investment intention. We also hypothesize how this moral foundations framing effect is moderated by the perceived return performance of the ethical fund. We test our hypotheses through two online experiments with retail investors in the United States. Study 1 demonstrates that the moral foundations framing effect varies by moral foundation. Focusing on the Fairness foundation, Study 2 shows that the framing effect is stronger under the win-win dual objective condition, relative to a conflict of interest condition. This stronger effect indicates that the moral foundations framing effect appears to be more effective when the investor perceives that ethical investments are financially lucrative. Our study provides preliminary evidence for the potential of the moral foundations framing approach and contributes to scholarship in both business ethics and ethical investing.

Ethical investing refers to “the exercise of ethical and social criteria in the selection and management of investment portfolios, generally consisting of company shares (stocks)” (Cowton, 1994). Business ethics scholars have demonstrated that ethical investing is pursued, in part, because it is the “right thing to do,” which defines a moral motivation (Beauchamp & Bowie, 2004). Why some investors engage in ethical investing while others do not has generated interest among ethics scholars, yet most research has focused on individuals’ moral traits, suggesting that people with moral character traits are more inclined to ethical investments (McLachlan & Gardner, 2004; Nilsson, 2008; Peifer, 2014).

We posit that, in addition to moral traits, states of mind such as moral frames that investors use to interpret information and form judgment also play a critical role in shaping individuals’ ethical investment intention, which refers to the intention to invest in an ethical investment option. To examine this possibility, we synthesize framing theory (Chong & Druckman, 2007) and moral foundations theory (MFT) (J. Graham et al., 2013) to develop a moral foundations framing approach that explores the effect of moral foundations frames on ethical investment intention. While the role of frames has been recognized in business ethics scholarship (Amatulli et al., 2019; Døskeland & Pedersen, 2021; Glac, 2009; K. A. Graham et al., 2015; Grimm, 2020), our study is among the first to investigate frames that are anchored in specific moral foundations. This moral foundations framing approach is useful because it acknowledges moral pluralism (i.e., there are multiple moral foundations; J. Graham et al., 2013). More specifically, MFT posits there are at least five salient moral foundations that animate moral activity across time and space: Care/Harm, Fairness/Cheating, Loyalty/Betrayal, Authority/Subversion, and Sanctity/Degradation (Haidt, 2012). This moral pluralism offers a flexible research agenda for many ethical topics, which may differentially resonate with various moral foundations. The moral foundations framing approach also provides practitioners with insights into how a moral state of mind, beyond moral traits, could foster ethical decisions and actions by effectively conveying a moral message with resonant moral foundations language. Indeed, how to motivate people to do the right thing is an important practical question at the core of business ethics (Heath, 2008).

We are particularly interested in retail investors (i.e., nonprofessionals making their own personal financial investment decisions) because they have shown a growing demand in ethical investment options and represent a substantial capital market that ethical investing has just begun to engage (Madsbjerg, 2019; Morgan Stanley Report, 2017). Moreover, retail investors seem to have motivations that are distinct from those of the traditional ethical investor groups such as institutional investors (Barber et al., 2019; Døskeland & Pedersen, 2021; Lewis, 2001).

In this article, we employ a moral foundations framing approach to explore two research questions. The first question is: does framing ethical investment opportunities with specific moral foundations language enhance retail investors’ ethical investment intention? We incorporate the four-component model of ethical decision-making and behavior (Jones, 1991; Rest, 1986) to motivate our first hypothesis. The four-component model posits that an ethical decision process consists of four sequential stages (i.e., recognizing the moral issue, making a moral judgment, establishing a moral intention, and engaging in moral behavior). We expect that moral foundations frames, by shaping investors’ moral awareness and judgment, will increase their ethical investment intentions.

Inherent to ethical investing is its dual-objective nature (i.e., the simultaneous pursuit of both ethical and financial objectives). Ethical investing researchers have long debated the question of whether there is a trade-off between ethical and financial returns (see Revelli & Viviani, 2015, for a review). Although the literature does not provide a conclusive answer (Barber et al., 2019; Renneboog et al., 2008; Revelli & Viviani, 2015), there is a widely accepted perception among many investors that investing ethically requires a financial sacrifice (Lewis & Mackenzie, 2000; Morgan Stanley Report, 2017; Peifer, 2014). This prevalent perception forms a conflict of interest dual-objective scenario, where ethical and financial objectives are in tension and doing the moral thing is individually costly. Furthermore, existing scholarship that has theorized ethical decision-making, in general, under dual-objective conditions tends to focus on a conflict of interest scenario (Etzioni, 2003; Kish-Gephart et al., 2014; Moore & Loewenstein, 2004).

However, we observe increased messaging that explicitly emphasizes the positive financial rewards of ethical investing. For example, Cahill (2010) describes the financial component of impact investing, a recent instantiation of ethical investing, with phrases like “at least a nominal return to the investor,” “generating financial profit,” and “market-beating financial returns” (p. 267). Furthermore, some investors report a belief that their ethical investments are financially lucrative (Mudaliar et al., 2019). This elaborates a win-win dual-objective scenario where investors “do the right thing” and make a handsome profit.

It would seem the win-win scenario is likely to attract more ethical investments relative to a conflict of interest scenario. But this is not the other research question we pursue. Instead, our second research question focuses on how different perceptions of ethical fund return performance (i.e., a conflict of interest vs. a win-win dual-objective scenario) moderate our moral foundations framing effect. As there are compelling mechanisms leading to opposite predictions, we present two competing moderation hypotheses. We first draw on the four-component model (Jones, 1991; Rest, 1986) to predict that the framing effect will be stronger under the win-win condition because the removal of perceived financial sacrifice lifts the barriers that stall advancement in the ethical decision-making progression. We then borrow crowding theory (Frey, 2012) to generate a competing hypothesis that our moral foundations framing effect will be stronger in the conflict of interest condition because the perception of superior financial rewards under the win-win condition may crowd out ethical considerations induced by our framing.

We conduct two online experiments with retail investors in the United States recruited through Amazon Mechanical Turk (MTurk). In Study 1, participants are randomly assigned to read about an ethical fund that is described with Care, Fair, Loyalty, Authority, or Sanctity moral foundations dictionary words. We also include a control condition that describes the same fund without any moral foundations dictionary words. We only find support for the moral foundations framing effect when framing with Fairness language and not the other four moral foundations. In Study 2, we only focus on Fairness framing and add a second experimental dimension where we manipulate the dual-objective function by telling respondents that ethical funds tend to outperform/underperform conventional investments. We find that the Fairness framing effect is stronger in the win-win scenario (i.e., a perception that ethical funds outperform conventional funds) than the conflict of interest scenario (i.e., a perception that ethical funds underperform). We conclude that the moral foundations framing effect tends to be hindered by perceived financial sacrifice, but is significantly bolstered when a financial reward is anticipated. We end with a discussion of our contributions to business ethics in general, and ethical investing in particular.

Literature Review

From Moral Traits to Moral States

Existing empirical studies in ethical investing demonstrate that moral people, measured in various ways, tend to be more favorably inclined to ethical investments. Nilsson (2008) finds investors who have prosocial attitudes on specific issues that their ethical mutual fund attends to tend to invest a larger share of their investment portfolio in those ethical mutual funds. McLachlan and Gardner (2004) find ethical investors tend to report a greater perception of moral intensity than conventional investors. Peifer (2014) finds ethical investors in a religiously affiliated mutual fund who care more about screening out unethical firms are more loyal investors to the fund. Nilsson (2009) finds a substantial portion of ethical investors are motivated by the social attribute. In sum, these correlational studies indicate that people with higher levels of a moral attribute tend to be more interested in ethical investing. Although these studies offer insights into investors’ moral motivations, they offer relatively limited practical implications because it may not be easy to change a person’s moral trait disposition (Hitlin & Civettini, 2017).

Psychologists have long distinguished between the concepts of traits and states, the former being personal characteristics that are stable and consistent across time and situations, whereas the latter is a temporary way of being that is unstable and inconsistent (Allport & Odbert, 1936; Norman, 1967). Researchers have shown that states influence human judgment and decision-making, much like personality traits do (Bernard & Smith, 2006; Van Gelder & De Vries, 2012). Inspired by this research, we suspect that a moral state of mind should influence investors’ moral motivation toward ethical investing. To test this possibility, we develop a moral foundations framing approach and examine whether a moral state of mind created by frames suffused with moral foundations language increases investors’ ethical investment intention.

Framing Theory

Over the past few decades, an influential body of literature on framing theory has emerged in sociology and blossomed in a variety of disciplines (Benford & Snow, 2000; Entman, 1993; Tversky & Kahneman, 1981). According to Goffman (1974) who was among the first scholars pioneering this field, frames refer to the “schemata of interpretation” (p. 21) or frameworks that help to make sense of issues and events. In their review of framing theory, Chong and Druckman (2007) define framing as the “process by which people develop a particular conceptualization of an issue or reorient their thinking about an issue” (p. 104). A fundamental tenet of framing theory is that an issue can be viewed from a variety of perspectives or frames. When a frame is made salient, it will shape individuals’ attitudes about an issue and guide information interpretation in the decision process (Chong & Druckman, 2007; Druckman, 2004). Frames achieve this by influencing the availability, accessibility, and applicability of the considerations used in one’s judgment and evaluation. A good illustration is that a free speech frame and a public safety frame can substantially alter people’s attitudes toward a hate group rally (Chong & Druckman, 2007).

Framing studies are mostly employed in the fields of political science, communications, and public opinion. Recently, framing theory has also been applied in the field of business ethics (Bateman et al., 2001; Derry & Waikar, 2008; Glac, 2009; Lee & Riffe, 2019; Liu et al., 2015). To list a few of the studies, K. A. Graham et al. (2015) investigated the role of loss versus gain framing in unethical pro-organizational behavior. Grimm (2020) examined the influences of different frames of poverty on corporate actors’ handling of tension between profitability and poverty reduction. Døskeland and Pedersen (2016, 2021) explored the impact of financial framing and moral framing on responsible investment behaviors. However, while the business ethics scholarship has started to explore the role of frames in shaping ethical decisions and actions, only limited research (Døskeland & Pedersen, 2016, 2021) has studied frames that are directly linked to morality in general. We are not aware of studies that have explored various dimensions of morality. To address this limitation, we blend framing theory with MFT to develop a moral foundations framing approach.

Moral Foundations Theory

Grounded in cultural psychology, MFT maintains that there are various fundamental categories of human morality across cultures (J. Graham et al., 2013). In general, MFT emphasizes four basic assumptions. First, the categories of moral concern are universal and innate, which means they are organized in human minds in advance of experience. Second, the universal and innate moral mind is revised through learning experiences. Third, moral judgment is generally intuitive, occurring in a rapid, automatic, and effortless processing. Fourth, morality is plural (i.e., there are multiple moral categories).

In this article, we focus on MFT’s claims about moral pluralism. Moral pluralists maintain that multiple elements are needed to adequately represent and explain the full breadth of morality. They also believe that there can be more than one moral element at play in a situation or issue (J. Graham et al., 2013). Taking a moral pluralist approach, MFT scholars have identified five foundations (or intuitions) of morality. The Care/Harm foundation refers to concern for the suffering of others. Fairness/Cheating is concerned about unfair treatment. Loyalty/Betrayal refers to obligations of group membership, which might be one’s family, local organization, or one’s country. Authority/Subversion relates to social order and the obligations of hierarchical relationships. Sanctity/Degradation concerns physical and spiritual contagion or contamination. Feelings of disgust is also an important part of this moral foundation. To be clear, while moral pluralism asserts multiple moral foundations can be used to frame an issue, in the article, we frame an issue with one moral foundation at a time to isolate and test each moral foundations framing effect (i.e., a Care framing effect, a Fairness framing effect, etc.).

Moral Foundations Framing

MFT is a useful theoretical perspective for our framing approach for several reasons. Framing theory suggests that an issue can be viewed from different perspectives, and MFT maintains that a situation can be approached from different moral foundations. This commonality makes a moral foundations framing approach possible by framing issues according to MFT’s moral foundations. Moreover, MFT enables more nuanced moral framing because it provides more precise ways to operationalize different dimensions of morality. Each moral foundation might help frame an issue or event from a specific moral dimension. More specifically, there is a list of moral foundations dictionary words useful for researchers to clearly operationalize when something is being framed by a moral foundation and when it is not. To apply the moral foundations framing approach to the field of business ethics, we conceptualize the issue, or event that is differentially framed, as a potential economic transaction with moral attributes. An employee might consider working for an ethical firm. An investor might choose an ethical investment. A consumer may consider purchasing an environmentally friendly product or service.

It is important to emphasize that each of these economic transactions already contains a moral dimension. In other words, we are theorizing a potentially subtle moral foundations framing effect. The condition that is not framed by a moral foundation is still clearly an ethical option (e.g., the coffee beans are grown by farmers who earn above poverty-level compensation). The moral foundations framed version describes the same consumer good (i.e., coffee) with language rooted in a specific moral foundation (e.g., the fair-trade coffee offers a more just and equitable deal for coffee growers). Our moral foundations framing approach questions whether highlighting the fairness moral foundation with the words “fair” and “just” and “equitable,” in this example, will have an impact on ethical decision-making.

In this study, we employ the moral foundations framing approach to study moral motivations in the context of ethical investing. The moral foundations framing approach is applicable to ethical investing because various moral foundations undergird different ethical investments. Borrowing the screening and advocacy categories from the Forum for Sustainable and Responsible Investment (2020), the Human Rights and Community Development categories can be framed by the Care moral foundation (Haidt & Graham, 2009). The fairness foundation could frame the Diversity & EEO (equal employment opportunity) and Executive Pay categories. The Loyalty and Authority foundations might help frame the Board Issues category, which pertain to corporate governance methods to reign in executive insubordination. The sanctity foundation could frame the Pollutions/Toxics and Tobacco categories.

Hypotheses

Ethical Decision-Making

In this article, we examine whether framing ethical funds with moral foundations language will enhance investment intention. We focus on investment intention in our study because of the critical role of intention in engendering actual behavior. While intentions are distinct from actual behaviors, they are considered the most important and immediate predictor of behaviors by major attitude-behavior models such as the theory of reasoned action (Fishbein & Ajzen, 1975) and the theory of planned behavior (Ajzen, 1985, 1991; Ajzen & Madden, 1986). According to a meta-analysis of 47 studies exploring causality between intention and behavior, Webb and Sheeran (2008) find that a medium-to-large change in intention causes a medium-to-large change in behavior when behavior is measured objectively. The importance of intention is also emphasized in morality research. The establishment of moral intentions has been included as a critical step in various ethical decision-making and behavioral models (Hunt & Vitell, 1986; Jones, 1991; Rest, 1986; Trevino et al., 2006) and found to mediate moral attributes and moral behaviors (Eisenberg, 1986).

To hypothesize the effects of moral foundations frames on ethical investment intention, we borrow the classic four-component model of ethical decision-making and behavior (Jones, 1991; Rest, 1986). This model suggests that ethical decision-making is developed through four stages: recognizing a moral issue, making a moral judgment, establishing a moral intent, and engaging in moral behavior. An important tenet of this model is that success in one stage does not necessarily translate to the success in the next stage. For instance, an individual who correctly makes a moral judgment does not necessarily advance to establishing a moral intent. There are many factors that could obstruct this advancement across the four stages. But before we scrutinize a potential obstacle (see below), we focus on the “fuel,” so to speak, that propels individuals further along the ethical decision-making stages. Namely, we posit that the use of moral foundations frames increases the likelihood of successful advancement through the stages of ethical decision-making by amplifying the moral considerations. More specifically, our moral foundations framing amplifies a single moral foundation. This amplification should enhance the likelihood of successful advancement through each phase of ethical decision-making because the framing will likely create a moral state of mind in the individual by making a particular moral foundation salient. This moral state of mind will make the individual more likely to recognize a moral issue, make a moral judgment, establish a moral intent, and engage in moral behavior. As moral pluralism suggests each moral foundation is distinct, we create one hypothesis for each foundation.

Dual-Objective Function: Conflict of Interest or Win-Win

Ethical decisions can be couched as a dual-objective function: the ethical objective and the self-interested objective. Accordingly, ethical investing faces a dual-objective function where individuals are faced with an ethical choice while still being concerned about their financial objective. We label the scenario where both objectives are easily and simultaneously achieved as a win-win condition; the individual can do the right thing and earn above average returns on their investment. The conflict of interest condition refers to a trade-off, where doing the right thing is associated with lower return performance.

Researchers have long debated the question of whether there is a trade-off between ethics (operationalized by corporate social responsibility [CSR]) and financial returns. Revelli and Viviani (2015) conduct a meta-analysis of 85 studies and conclude that “the consideration of corporate social responsibility in stock market portfolios is neither a weakness nor a strength compared with conventional investments” (p. 158). Despite this empirical evidence that there is no difference, on average, investors still perceive more stark differences.

For instance, there is the widely held perception among many investors that ethical investing requires a degree of financial sacrifice. For example, Lewis and Mackenzie (2000) find 42.4% of their U.K. ethical investors sampled expect lower financial return from their ethical investment, relative to “ordinary investments.” Only 13.7% expect higher returns. Peifer (2014) finds only 7% of ethical investors sampled believe their fund tends to earn higher returns than most conventional funds, whereas 36% believe the ethical fund underperforms. In a recent survey conducted by Morgan Stanley Report (2017), 53% of investors believe that ethical investing requires a financial trade-off, and this belief is held to a greater degree among Millennials (59%). In sum, we think it is reasonable to expect many investors perceive ethical investing to be a conflict of interest scenario.

However, ethical investing can be perceived as a win-win scenario. Recent instantiations of ethical investing (e.g., Environmental, Social, and Governance (ESG) investing, impact investing) tout its win-win appeal with supporting evidence. In the GIIN’s 2019 Annual Impact Investor Survey, an overwhelming proportion of the respondents reported that portfolio performance met or exceeded investor expectations for both impact return (98% of respondents) and financial return (91% of respondents) (Mudaliar et al., 2019).

More theoretically, existing scholarship that conceptualizes ethical decision-making as a dual-objective function tends to focus on conflicts of interest (Kish-Gephart et al., 2014; Moore & Loewenstein, 2004). Etzioni (2003) theorizes morality among economic actors and expects the economic context to be ripe with conflicts of interest. “My thesis is not that values drive behaviour, but that there is a continual conflict and tension between self-interest and the pleasure principle on one hand, and powerful moral commitments on the other” (Etzioni, 2003, p. 113). Indeed, Rest (1984) suggests that when the personal cost of morality is high, people tend to defensively reevaluate the situation. Similarly, Trevino (1986) proposes that the link between cognitive moral development and ethical decision outcomes is contingent on situational factors including personal costs. In sum, when scholars acknowledge the dual-objective nature of ethical decision-making, they tend to assume the moral option conflicts with the self-interested option (i.e., the conflict of interest scenario). Under this condition, we expect that decision makers will “carry an additional burden” at each ethical decision-making stage. Applying this logic to our moral foundations framing approach, the perception of costly action will counterbalance the added moral “fuel” that moral foundations framing provides and stall the decision makers’ advancement along the stages of ethical decision-making.

Although existing scholarship has explored ethical decision amid a conflict of interest scenario, we are unaware of parallel theoretical work on ethical decision under an alternative “win-win” scenario. A win-win scenario refers to cases where making the moral decision is individually rewarding, not costly. Specifically, would the removal of perceived cost, and replacement with perceived benefit, enhance moral foundations framing effects? As we have discussed, ethical decisions that are also costly stall advancement in the ethical decision-making progression. By contrast, in a win-win scenario, decision makers are no longer burdened by the conflict scenario’s sacrifice for “being good” and are therefore liberated to freely heed their moral state of mind aroused by moral foundations frames. We therefore predict the following moderation hypothesis:

There is also a compelling competing hypothesis that should be entertained. Namely, the win-win scenario’s perception of above-average financial return could crowd out one’s intrinsic motivation (e.g., moral, motivation for ethical investing). Crowding Theory suggests there may be hidden costs of a reward and that monetary incentives can crowd out one’s intrinsic motivation for action and in some cases reduce the desired behavior (Frey, 2012). “One is said to be intrinsically motivated to perform an activity when he receives no apparent reward except the activity itself” (Deci, 1971, p. 105). Moral motivations are one kind of intrinsic motivation and “external intervention affects the internally held values of individuals” and “may induce a shift from other-regarding or group-regarding to more selfish preferences and behavior” (Frey, 2012, p. 79). In their review of empirical evidence of crowding theory in environmental conservation policy, Rode et al. (2015) identify “release from moral responsibility” as one psychological mechanism underlying crowding theory. Bowles (2008) provides evidence that policies designed for self-interested citizens may undermine their moral sentiments. Applying crowding theory to our case, we can consider the perception of lucrative financial rewards as an extrinsic monetary motivation for investing in an ethical fund, which may crowd out the decision maker’s considerations of the scenario’s moral attributes, such as the moral state induced by moral foundations framing.

Study 1

The purpose of Study 1 was to examine Hypotheses 1a-1e. To reiterate, we expected that the use of each moral foundation frame, relative to no moral foundation framing, would increase ethical investment intentions.

Experimental Design

We implemented a 6 × 1 between-subjects experimental design. As one of the six conditions is the control condition, we presented five distinct moral framing tests, one for each moral foundation. Participants were randomly assigned into one of the six conditions to eliminate any potential difference other than the treatment (or lack thereof in the control condition) between the conditions. Each participant was asked to imagine a scenario where an employer has just added a well-respected mutual fund family (i.e., SageInvest—a made-up name) to his or her retirement plan. The fund family offers two mutual funds, across which respondents must allocate their hypothetical retirement savings. One is named the “Index Fund” and the other the “Social Fund.” The Index fund was identically represented in all six conditions alongside the Social Fund. The Social fund was manipulated by differently framing (or no framing, in the control condition) its description across conditions.

To provide respondents with relevant details of the investment scenario, we judged it was important to mention the funds’ return performance history. Considering the fact that there is a widely held perception among investors that ethical investing is more financially costly compared with conventional investments (Juengling, 2015; Lewis & Mackenzie, 2000; Peifer, 2014), we presented the social fund to respondents as underperforming the Index Fund. Respondents viewed yearly return performance percentages for each fund in bar graph form. For each time period, the Index Fund earns about 1 to 2 percentage points higher than the Social Fund. The same bar graphs were presented in all conditions.

Ethical fund content

Our moral foundations framing approach is general and intended to apply to various ethical issues. To incorporate the full span of moral pluralism offered by MFT, we carefully selected an issue for which we can argue that all five moral foundations are relevant—corporate tax noncompliance. While corporate tax noncompliance is not currently an issue that ethical investment funds frequently address, it is an important contemporary public issue (Matthews, 2016) and has become a noteworthy research topic in business ethics (Greenwood & Freeman, 2018; West, 2018). Large corporations have been criticized for finding and exploiting loopholes that allow them to pay relatively little in federal corporate taxes (e.g., relocating their legal domicile to a tax-haven country through subsidiary creation). Research has shown that such tax noncompliant behaviors are punished by deteriorated corporate reputation as well as consumers’ decreased purchase intention and willingness to pay (Hardeck & Hertl, 2014).

Moral foundations framing

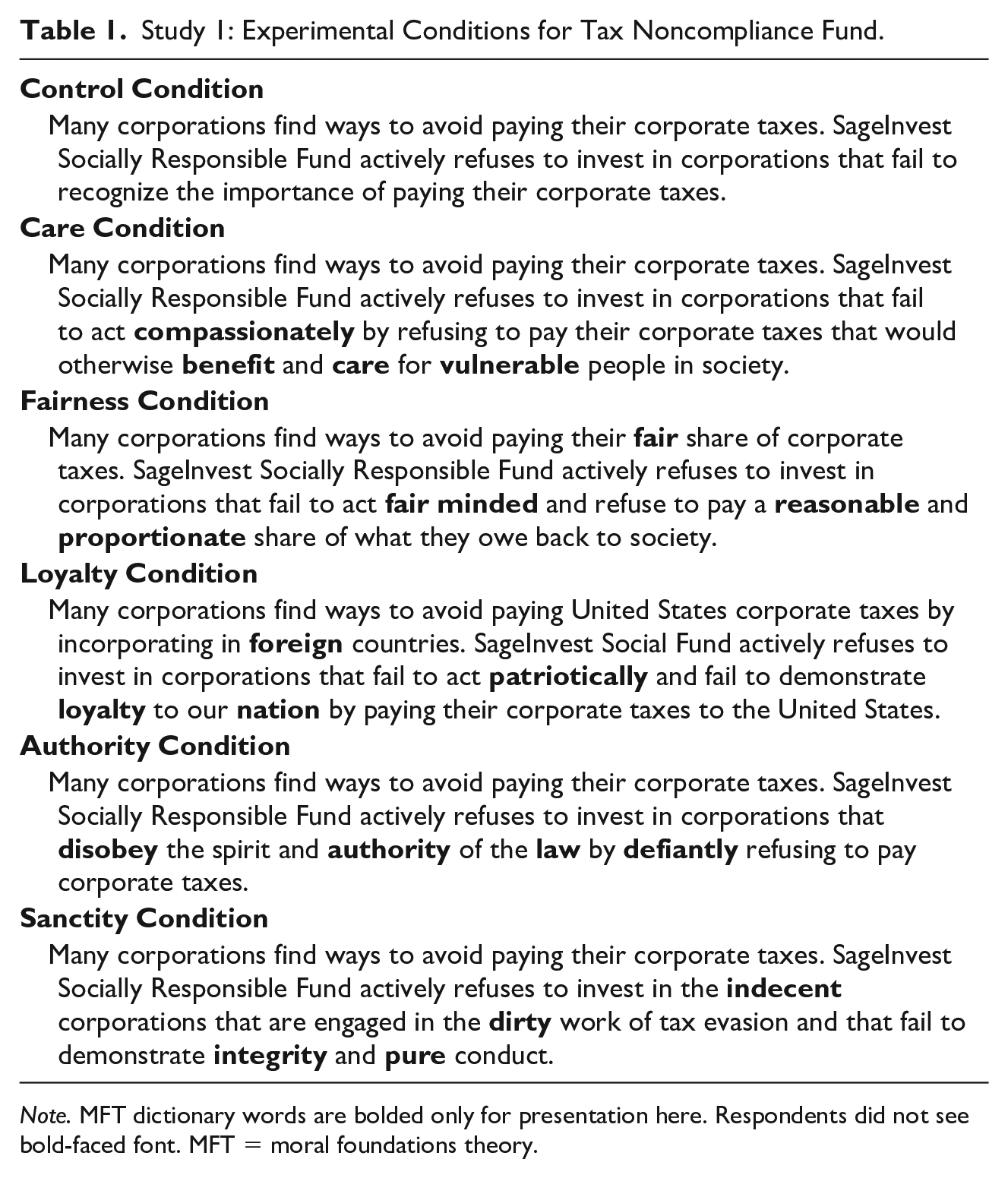

This study’s experimental manipulation occurs in how the Social Fund is described. Five treatment conditions morally frame the Social Fund with one moral foundation by borrowing words from the moral foundations dictionary (J. Graham et al., 2009). No moral foundations language is used in the control condition (see Table 1).

Study 1: Experimental Conditions for Tax Noncompliance Fund.

Note. MFT dictionary words are bolded only for presentation here. Respondents did not see bold-faced font. MFT = moral foundations theory.

Tax noncompliance can be framed by all five moral foundations. Research has shown that concerns about fairness and justice affect attitudes toward tax compliance (Brizi et al., 2015; Falkinger, 1995; Kim, 2002; Verboon & Dijke, 2007). For instance, honest taxpayers care about others’ tax cheating behavior, and the more importance they place on the tax rules that have been violated, the higher the degree of sanction on the dishonest actor(s) they demand (Wenzel, 2002). The Fairness moral foundation proposed by MFT makes people sensitive to issues of justice and proportionality and arouses anger toward those who violate such principles (Koleva et al., 2012). Thus, we believe the Fairness foundation is underlying the beliefs that everyone should pay their fair share of taxes.

The Loyalty moral foundation is also relevant. Research has shown that patriotism is important (Konrad & Qari, 2012) and is often appealed to as a “civic virtue” to encourage tax compliance (Slemrod, 2007). Tax dodgers are punished not only by legal sanctions but also by guilt and shame induced by social norms that emphasize this civic virtue to the country (Slemrod, 2007). MFT’s Loyalty foundation emphasizes the interest of one’s group (e.g., country) and appreciates virtues such as loyalty, patriotism, and self-sacrifice (J. Graham et al., 2013; Koleva et al., 2012). Thus, the Loyalty foundation should endorse tax compliance as a civic virtue and cause anger toward in-group members (e.g., companies) who avoid paying taxes.

In addition to Fairness and Loyalty foundations, we also judge Care, Authority, and Sanctity moral foundations to be relevant to the tax noncompliance issue. The advocacy of tax compliance could be motivated by compassion and care for financially vulnerable, marginalized groups in society. Meanwhile, research has shown that obedience to authority and laws substantially promotes tax compliance behavior (Cadsby et al., 2006; Orviska & Hudson, 2002). Finally, the concern for moral purity and integrity is likely to lead to disapproval of tax noncompliant behavior and perhaps emotions of disgust.

Study Participants

We used MTurk to recruit a sample of actual investors for the experiment. We consider the MTurk platform suitable for our study for several reasons. First, the focus of our research is a particular investor group, retail investors. MTurk is an efficient way for us to reach this population. A traditional undergraduate sample, for example, would be unlikely to yield as many investors as an MTurk sample. Second, social scientists have shown evidence supporting the legitimacy of MTurk recruitment for online surveys and experiments. Although MTurk samples are not exactly nationally representative, they do not differ fundamentally and tend to produce similar or better results than population-based samples and undergraduate students (Berinsky et al., 2012; Paolacci et al., 2010). For example, Weinberg et al. (2014) conduct the same vignette-based experiment on a nationally representative sample and an MTurk sample and find that “while demographic differences exist, most notably in age, the actual results of our experiments are very similar, especially once these demographic differences have been taken into account. Indicators of data quality were actually slightly better among the crowdsource subjects” (p. 292). For these considerations, we felt it reasonable to recruit retail investors from MTurk for our study. Meanwhile, we recognized possible data quality concerns typically associated with crowdsource samples. To mitigate such concerns, we included attention checks and open-ended questions to identify low-quality responses and made sure there were no suspicious response patterns in our data set.

Recruited in December 2016, our initial data set included 442 investors who answered yes to the following survey question: “Does your household have any investments in stocks, mutual funds, or other securities?” Thirty-four percent reported the approximate value of those investments to be less than US$10,000, 35% reported US$10,000 to US$50,000, and 31% reported more than US$50,000. Investors were then asked to indicate their agreement with the following statement: “I am actively engaged in making the investment decisions regarding these stocks, mutual funds and other securities.” Forty percent reported to “strongly agree” with that statement, and another 39% reported to “somewhat agree.” We believe these descriptive statistics demonstrate our ability to successfully recruit retail investors. Participants were paid US$0.75, and the median time to complete the survey was about 10 min.

As mentioned above, we acknowledge there are data quality concerns with online samples, like those collected via MTurk. We therefore took the following measures to validate our analysis sample’s data quality. We included two attention checks in our questionnaire, borrowed from the Moral Foundations Questionnaire (J. Graham et al., 2008). The first attention check asking “Whether or not someone was good at math” is relevant to the participant’s judgment of right or wrong. The second attention check asks whether the participant agrees that “It is better to do good than to do bad.” Thirteen respondents (3%) were dropped due to missing both attention checks. This sample size will be further trimmed by 15 due to listwise deletion, leaving a sum of 414 respondents across our condition samples. It is also worth noting that as our experimental vignette features employer-sponsored investments common in the United States, we limited MTurk’s recruitment filter to U.S. residents. Forty-four percent of the analysis sample is female. The mean age is 38.70 years (SD =11.88).

Measures

Dependent variable

We asked each respondent to “indicate the percentage of your investment savings you would invest in each mutual fund. You may allocate 0% to a mutual fund, as long as your allocations add up to 100%.” Ethical investment intention was measured by the percentage of the respondents’ hypothetical retirement portfolio allocated to the Social fund. Two observations have missing values for this outcome variable and are therefore dropped from the analysis sample via listwise deletion.

Independent variables

The Moral foundations framing indicator variable indicates exposure to a treatment condition. In this and in the next study, we include two covariates in each model that tests our moral framing hypotheses.

As existing literature suggests that moral people tend to be more favorably inclined to ethical investments (McLachlan & Gardner, 2004; Nilsson, 2008, 2009), we control for the potential effect of individual difference in moral foundations endorsement. Moral foundations endorsement measures the strength of the participant’s relevant moral foundations intuition via the Moral Foundations Questionnaire (MFQ) (J. Graham et al., 2008). Each moral foundation was measured by six items. The six items were averaged together to measure each level of moral foundations endorsement. The resulting Care endorsement Cronbach’s alpha is .77, Fairness is .74, Loyalty is .78, Authority is .77, and Sanctity is .87. These figures are greater than the widely used acceptable level of .70 (Cortina, 1993), indicating adequate reliability of each moral foundation endorsement scale shown in our data.

Political orientation tends to influence individuals’ attitudes toward initiatives involving social and environmental considerations. Giuli and Kostovetsky (2014) find that U.S. firms with Democratic founders, chief executive officers (CEOs), directors, and headquartered in Democratic-leaning states score higher on CSR than firms with Republican counterparts. Paul et al. (1997) reveal that Democratic consumers care more about corporate social performance than Republicans in the United States. Specific to ethical investing, Lewis and Mackenzie (2000) find that ethical investors in the United Kingdom tend to be more left leaning. Furthermore, researchers find that political liberals in the United States tend to place more weight on the Care and Fairness moral foundations (which are inherent in many social and environmental issues) than the remaining foundations, whereas conservatives tend to equally endorse all moral foundations (J. Graham et al., 2009, 2011; Haidt & Graham, 2007). We therefore include a measure of Political Conservative determined by the following question: “We hear a lot of talk these days about liberals and conservatives. I’m going to show you a 7-point scale on which the political views that people might hold are arranged from extremely liberal to extremely conservative. Where would you place yourself on this scale?” The answers categories range from 1 = “extremely liberal” to 7 = “extremely conservative,” and the mean value is 3.72. Fifteen observations with missing Political Conservative data were dropped via listwise deletion.

Results and Discussion

As a manipulation check, after reporting their Social Fund allocation, respondents provided an open-ended answer to explain why investing in the Social Fund is ethical. Responses were then coded for the presence of MFT dictionary words (J. Graham et al., 2009). The rationale is that if our framing successfully manipulated the participant to adopt a particular moral foundations frame, his or her moral awareness and judgment of the Social Fund would be anchored by the frame. Consequently, in explaining why they thought the Social Fund was ethical, their reasoning would likely be based on the relevant moral foundation and conveyed through the language from that particular foundation. We use a separate logistic regression analysis (i.e., one for each moral foundation) to predict the presence of any germane MFT dictionary words, relative to all the other conditions. We find that care condition respondents are more likely (than those in all other conditions) to use care MFT words (odds ratio = 2.18, p = .04). The fairness manipulation is weak (odds ratio = 1.62, p = .20). The loyalty manipulation is strongly significant (odds ratio = 8.85, p = .00). Our manipulation checks clearly failed for both the authority and sanctity condition. These manipulation check results might have been affected by two factors. First, the framing manipulation might not have been strong enough. Second, there could also be unconscious manipulation effects that were in play but not captured by our manipulation checks. Indeed, as a theory highlighting the intuitive nature of morality, MFT contends that moral judgments are often rapid and unconscious. In other words, people’s reactions to moral stimuli can occur without conscious awareness of the process, nor can the process be articulated in words or reasoning (J. Graham et al., 2013). Considering this possibility, we report our findings notwithstanding the weak manipulation check results.

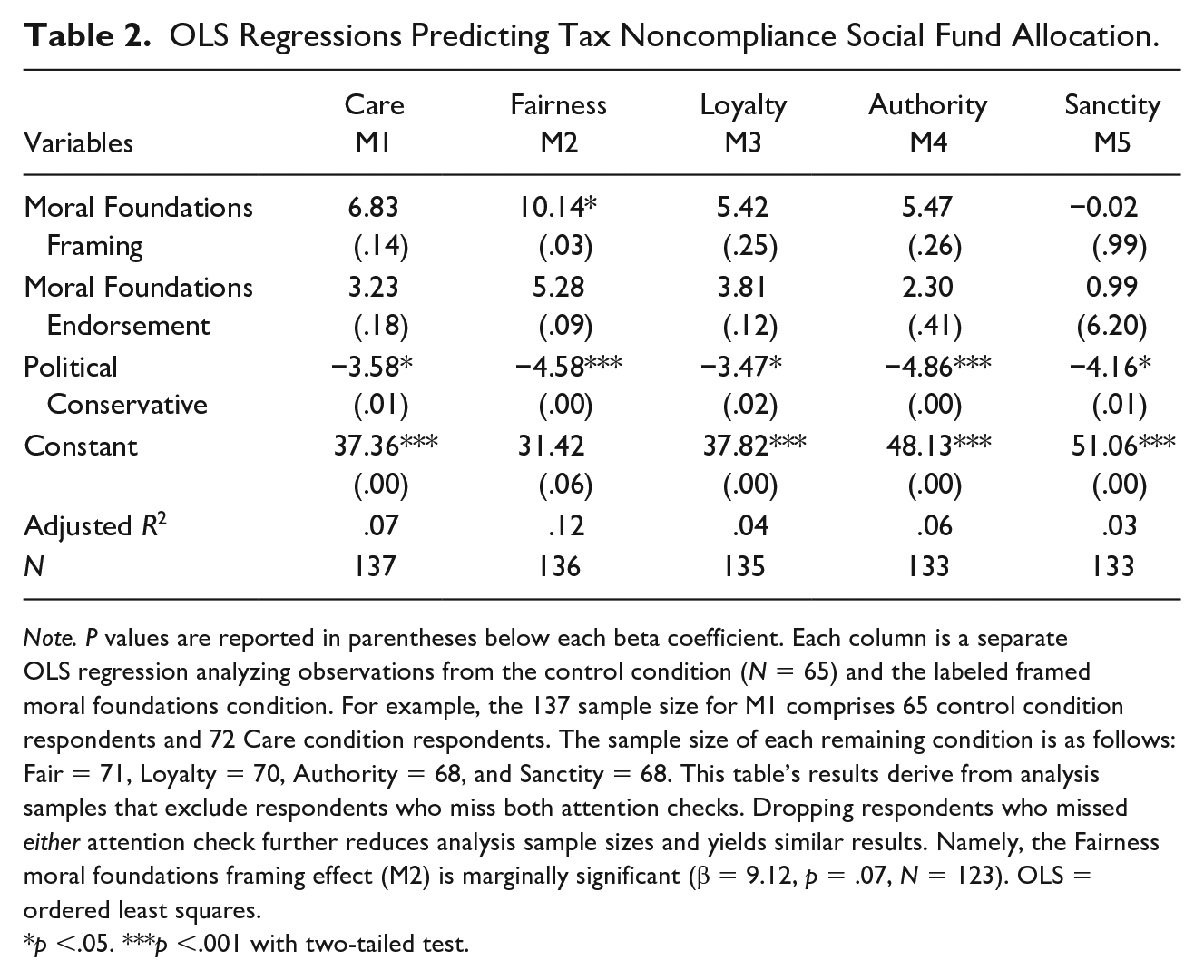

To test Hypotheses 1a–1e, we employed five ordered least squares (OLS) regression models, with each model regressing the intended allocation to the Social Fund (Table 2). Each model analyzes observations from the control condition and the relevant treatment condition. For example, Model 1’s analysis sample comprises observations from the control condition and the Care condition, and Moral foundations framing equals 1 for respondents randomly assigned to the Care condition and 0 for respondents in the control condition. We do not find a statistically significant effect in the Care treatment condition (β = 6.83, p = .14), which fails to support Hypothesis 1a. However, we find that the Fairness treatment condition yields a significantly higher level of investment intention relative to the control condition (β = 10.14, p = .03). Hypothesis 1b is thus supported. The treatment conditions of Loyalty, Authority, and Sanctity do not vary significantly from the control condition, although the difference is largely in the expected direction (see M3–M5 in Table 2). Hypotheses 1c–1e are therefore unsupported.

OLS Regressions Predicting Tax Noncompliance Social Fund Allocation.

Note. P values are reported in parentheses below each beta coefficient. Each column is a separate OLS regression analyzing observations from the control condition (N = 65) and the labeled framed moral foundations condition. For example, the 137 sample size for M1 comprises 65 control condition respondents and 72 Care condition respondents. The sample size of each remaining condition is as follows: Fair = 71, Loyalty = 70, Authority = 68, and Sanctity = 68. This table’s results derive from analysis samples that exclude respondents who miss both attention checks. Dropping respondents who missed either attention check further reduces analysis sample sizes and yields similar results. Namely, the Fairness moral foundations framing effect (M2) is marginally significant (β = 9.12, p = .07, N = 123). OLS = ordered least squares.

p <.05. ***p <.001 with two-tailed test.

We find that political conservatives allocate less to the Social Fund than liberals. Namely, each Political conservative coefficient in Models 1–5 in Table 2 is negative and statistically significant, ranging from −4.86 to −3.47. This finding is consistent with existing research that political conservatives, relative to their liberal counterparts, are less inclined toward socially responsible initiatives (Giuli & Kostovetsky, 2014; Lewis & Mackenzie, 2000; Paul et al., 1997). The fact that our data generate political conservative findings that are consistent with prior research that used different samples provides support for the external validity of our data and results.

In summary, we tested Hypotheses 1a–1e that predict the moral foundations framing effects on ethical investment intention. We only found support for our hypothesis in the Fairness condition, which leads us to conclude that moral foundations framing effects vary by moral foundation. Several factors may have contributed to this variance. First, prior research has shown that the Fairness foundation is the most robust among all foundations against monetary influence. In a survey asking respondents what immoral things they would do for different amounts of money ranging from US$0 to a million dollars, the Fairness foundation is the most difficult to compromise for monetary gains (J. Graham et al., 2009). Second, the relevance of moral foundations to the content of the ethical fund may also matter. While we are able to frame the ethical fund using all five moral foundations languages, our literature review suggests that the tax noncompliance issue is most commonly approached from the angle of fairness/justice (Brizi et al., 2015; Falkinger, 1995; Kim, 2002; Verboon & Dijke, 2007).

Study 2

The purpose of Study 2 is to examine Hypotheses 2 and 3, which predict that the effect of a moral foundations frame on ethical investment intention is moderated by the perception of return performance or the dual-objective scenario. While much of Study 2’s experimental design mirrors Study 1, there are some differences. Most importantly, we added the dual-objective scenario element to the experimental design. We also decided to focus on the one moral foundation that appeared the most resonant among investors in Study 1—Fairness. We therefore focused on fund content that is more prevalent in ethical investing and relevant for Fairness framing—CEO compensation. Finally, we describe the fund as investing in firms with fairer CEO compensation.

Experimental Design

We employed a 2 (no moral foundations framing vs. framing) × 2 (conflict of interest vs. win-win scenario) between-subjects research design. Participants were randomly assigned to one of the four conditions. Similar to Study 1, an Index fund and a Social fund were presented to participants in each condition. The description of the Index fund was identical across all conditions. The description of the Social fund was manipulated and participants were asked to imagine what proportion of their retirement investments they would allocate to the Index and Social funds.

Ethical fund content

In Study 1, we focused on corporate tax noncompliance because it could be framed by each moral foundation. As the focus of this article is not to determine which moral foundation is most resonant in the field of ethical investing, for Study 2 we decided to only focus on the moral foundation that obtained the strongest significant framing effect in Study 1 (i.e., Fairness). For fund content, we chose executive compensation which is readily relevant to the Fairness moral foundation. Moreover, mutual funds that address executive compensation are common in U.S. ethical investment landscape (Forum for Sustainable and Responsible Investment, 2020). Recent research has shown that excessive executive compensation has come under increasing public scrutiny. Mohan et al. (2018) find that consumers tend to avoid buying products from companies with high CEO pay.

Moral foundations framing

The following fund description shows in brackets the Fairness moral foundations dictionary words that were included in the moral framing treatment conditions and omitted from the other two conditions. To avoid any potential issue with framing manipulation in Study 2, we decided to amplify the framing effect by including the word “Fairness” in the fund name and boldfacing all additional Fairness dictionary words:

The SageInvest Social [

Win-win versus conflict of interest scenario

We manipulated the perceived social fund return performance with the following description:

You will notice the return performance information below indicates that our Social [Fairness] fund has out[under]performed the Index fund. While, past performance is not a guarantee of future return performance, financial experts agree that socially responsible investments, like the SageInvest Social [Fairness] Fund, tend to out[under]perform mutual funds that are not socially responsible.

The win-win scenario is operationalized by a condition where the social fund return performance is high or outperforms the Index fund. The conflict of interest scenario is operationalized by the condition where the social fund underperforms.

Study Participants

In January 2020, we recruited investors through MTurk to participate in our experiment and used MTurk premium service to reach a higher proportion of mutual fund investors. We confirmed their investor status with a survey question. Using a web application, we ensured none of these participants were also in Study 1. Participants were paid US$1.00, and the median time to complete the survey was about 8 min. Based on information collected via a survey question, we maintained for analysis participants who currently invest in a mutual fund or had done so in the past. Four participants (1%) were dropped for missing both attention checks. The attention checks are the following: “Select not very relevant to indicate you are paying attention” and “Select slightly agree to indicate you are paying attention.” Dropping those who missed attention checks resulted in a sample size of 383 for analysis. Forty-seven percent of the analysis sample is female. The mean age is 43.88 years (SD = 12.22).

Measures

Dependent variable

As in Study 1, we used the percent allocated to the Social fund as our continuous dependent variable that ranges from 0 to 100.

Independent variables

The Moral foundations framing indicator variable equals 1 for participants exposed to a fairness framing condition, and 0 if not. The Win-win indicator variable equals 1 for the condition where the social fund has higher returns than the Index Fund, and 0 when the social fund underperforms, which operationalizes the conflict of interest scenario. Six Fairness MFQ (J. Graham et al., 2008) items were averaged together to measure Fairness foundation endorsement (Cronbach’s alpha = .70). Political conservative has a mean value of 3.65, where 1 = “extremely liberal” and 7 = “extremely conservative.” One participant had missing data for political orientation and was dropped via listwise deletion.

Results and Discussion

As a Fairness framing manipulation check, all participants were invited to write an open-ended response to describe moral concerns associated with CEO compensation. This occurred after participants made the allocation that we use as an outcome variable. Responses were manually coded for the presence of moral foundations dictionary Fairness words. The rationale, again, is that if the manipulation was successful, participants’ responses would be anchored by the Fairness frame and contain more Fairness foundation language. Using logistic regression, we found that those in the Fairness framing conditions were more likely to include any Fairness foundation language in their response than those in the non-framed conditions (odds ratio = 5.98, p < .001). This result confirms our moral framing manipulation was successful.

To test our win-win manipulation, respondents were asked (after reporting their fund allocation) which mutual fund was likely to receive higher return performance based on the information they just read. Among respondents exposed to the condition where social funds overperform, 89% correctly answered social fund (4% answered index and 7% indicated both would receive equal performance). Among respondents exposed to the condition where social funds underperform, 90% correctly answered index fund (6% answered social and 4% indicated both would receive equal performance). These results confirm our win-win manipulation was successful (χ2 = 292.35, p < .001).

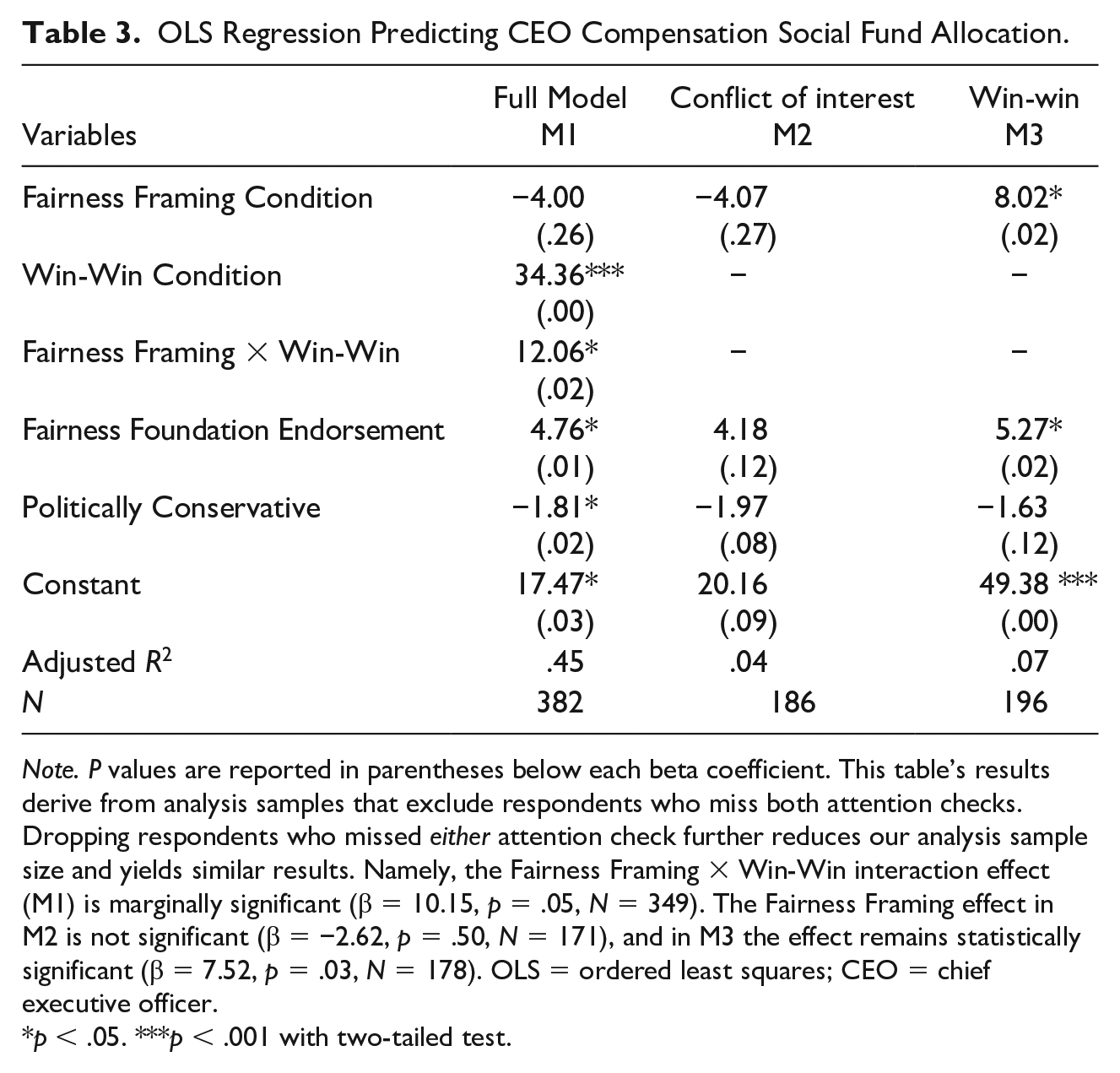

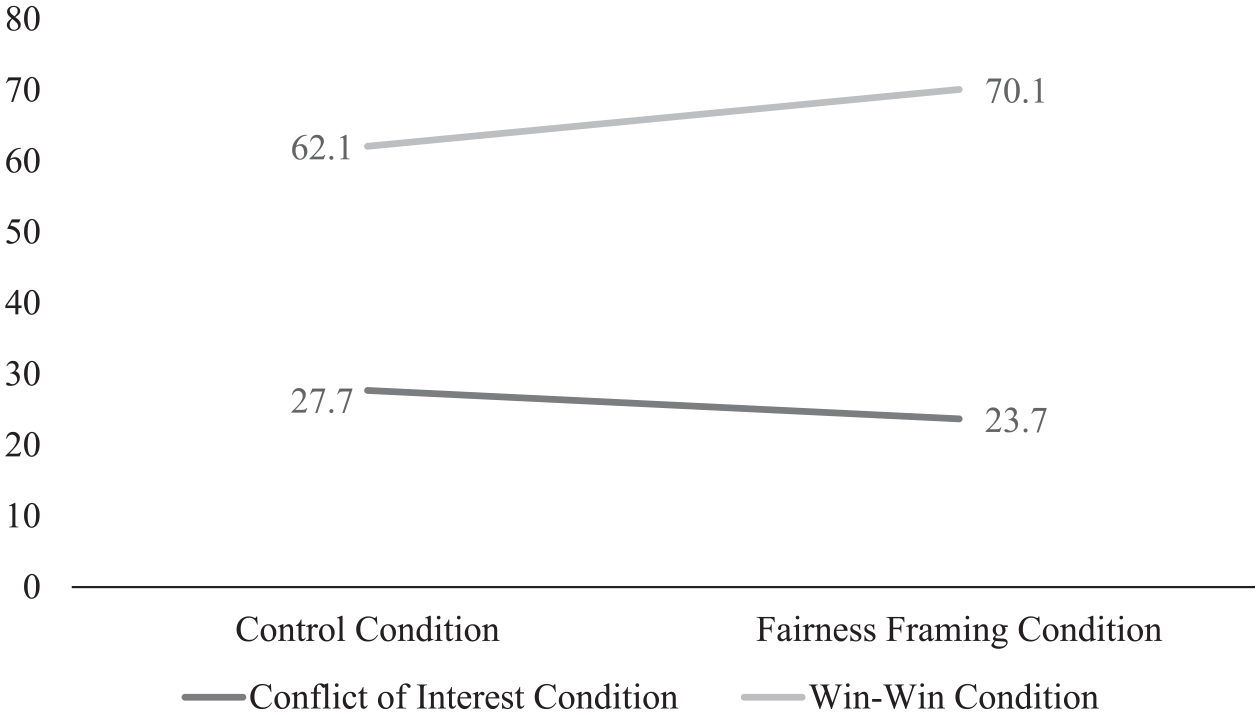

We employed OLS for hypothesis testing. Model 1 in Table 3 shows that the interaction term of fairness framing and win-win is positive and significant (β = 12.06, p =.02), supporting Hypothesis 2 that the effect of a moral foundations frame on ethical investment intention is stronger in the win-win scenario compared with the conflict of interest scenario. Hypothesis 3 which presents a competing prediction that the framing effect will be weaker in the win-win scenario is thus rejected. This moderating effect is illustrated in Figure 1 which presents the predicted social fund allocation at each relevant condition combination. Namely, the predicted social fund allocation, assuming mean levels for each covariate in the model, is 62% for participants in the control condition/high return performance and 70% for the Fairness framing condition/high return performance—an increase of 8 percentage points. The same comparison at low return performance is relatively flat.

OLS Regression Predicting CEO Compensation Social Fund Allocation.

Note. P values are reported in parentheses below each beta coefficient. This table’s results derive from analysis samples that exclude respondents who miss both attention checks. Dropping respondents who missed either attention check further reduces our analysis sample size and yields similar results. Namely, the Fairness Framing × Win-Win interaction effect (M1) is marginally significant (β = 10.15, p = .05, N = 349). The Fairness Framing effect in M2 is not significant (β = −2.62, p = .50, N = 171), and in M3 the effect remains statistically significant (β = 7.52, p = .03, N = 178). OLS = ordered least squares; CEO = chief executive officer.

p < .05. ***p < .001 with two-tailed test.

Predicted social fund allocation by experimental conditions (N = 382).

To gain more insight into the impact of different dual-objective conditions, we conducted post hoc analyses to observe the moral foundations framing effect on investment intention in each dual-objective scenario. Model 2 in Table 3 shows the results for the conflict of interest condition. We find the Fairness framing effect is not statistically significant. This result suggests that in a conflict of interest scenario, the potential effect of a moral foundations framing in establishing the intention toward an ethical investment opportunity is hindered by concerns for self-interest. As for covariates, Fairness endorsement is not significant and political conservative is negative and marginally significant (β = −1.97, p = .08).

Model 3 in Table 3 presents results for the win-win condition. We find a positive and significant effect of Fairness framing on investment intention (β = 8.02, p = .02). In a win-win investment scenario, participants who were exposed to the Fairness framing condition report the intention to invest more to their Social fund by 8.02 percentage points than those in the control condition. We also find correlational evidence that Fairness endorsement is positive and significant (β = 5.27, p = .02), while political conservative is not statistically significant.

In summary, we found support for Hypothesis 2 and not Hypothesis 3. We further found that while the moral foundations frame significantly increased investment intention in the win-win condition, it failed to do so in the conflict of interest condition. This finding suggests that financial rewards do not crowd out investors’ moral considerations or make the fund’s moral attributes irrelevant in the decision process. Instead, the results support our interpretation of the ethical decision-making four-component model (Jones, 1991) and show that the win-win condition liberates investors from financial concerns to freely engage with moral considerations. As a result, investors with a more salient moral state of mind aroused by Fairness framing show significantly stronger investment intention toward the ethical fund.

A plausible reason why Fairness framing was significant in Study 1 but not significant in Study 2’s conflict of interest condition is that we much more explicitly communicated return performance information in Study 2. The Fairness frame was able to enhance the “fuel” of moral awareness and intention in Study 1 where return performance was not a central factor, but failed to do so in Study 2 when the financial sacrifice was made salient. Thus, we feel comfortable interpreting that the effect of moral foundations frames on ethical investment intention is contingent on the nature of the dual objectives. Although the framing effect tends to be hindered by financial sacrifice in the conflict of interest scenario, it is effective in the win-win scenario because the hindrance that stalls ethical decision-making is lifted.

It is interesting to observe that the results of covariates also vary in different dual-objective scenarios. Investor’s moral trait, as measured by Fairness endorsement, is not significant in the conflict scenario but becomes significant in the win-win scenario. This difference suggests that “more moral” investors are more inclined toward ethical investment opportunities than “less moral” investors when there is an anticipated financial reward. Investors’ political orientation is negative and marginally significant in the conflict scenario but is not significant in the win-win scenario. This result indicates that political conservatives have lower ethical investment intentions than liberals when there is a perceived financial sacrifice. However, conservatives are similarly willing as liberals to invest ethically when there is the prospect of a financial reward.

General Discussion

In this article, we investigate the effect of moral foundations frames on retail investors’ ethical investment intention. Through two online experiments with U.S. retail investors, we observe evidence of a moral foundations framing effect that is independent of investors’ moral traits. In Study 1, we learn the moral foundations framing effect varies by moral foundation, with a significant effect found with the Fairness foundation, but nonsignificant effects found in the other four moral foundations. In study 2, we find this Fairness framing effect is stronger in the win-win scenario than the conflict of interest scenario. In addition to the moral foundations framing effect, we find that moral foundations endorsement and political orientation function differently under different dual-objective conditions.

In answering the question of why some investors engage in ethical investments while others do not, existing studies have largely focused on investors’ moral traits and show that individuals who are more “moral” tend to be more interested in ethical investing (McLachlan & Gardner, 2004; Nilsson, 2008; Peifer, 2014). We contend that, in addition to moral traits, a moral state of mind can drive intentions toward ethical investment. Our findings of the Fairness foundation framing provide preliminary evidence that frames in relevant moral foundations, independent of one’s (un)virtuous characteristics, can create a moral state that fosters ethical investment intention. This result lends support to the role of states of mind in decision-making (Bernard & Smith, 2006; Van Gelder & De Vries, 2012) and shows that frames can be effective tools to shape states of mind. The results also confirm the impact of frames on ethical decision-making (Amatulli et al., 2019; Glac, 2009; K. A. Graham et al., 2015) and further highlight moral foundations frames as a potential source of moral motivation. In this way, our work advances research on morality and offers practical implications. While it is difficult to change a person’ moral character, practitioners may effectively engage potential investors, as demonstrated in our Fairness findings, by creating a moral state of mind through moral foundations framing. This implication is meaningful because an essential question in business ethics is how to motivate people to do the right thing (Heath, 2008).

Our moral foundations framing approach also makes a valuable contribution to business ethics because it takes a plural view of morality and enables ethics researchers to examine the moral root cause of a phenomenon from different angles. While this article focuses on ethical investing, we see great potential for our moral foundations framing approach to be used in various areas of business ethics. In this article, Fairness is the only moral foundation that generates support for our core moral foundations framing hypothesis. We expect, however, that ethical funds that focus on content other than tax compliance and CEO compensation could be “successfully” framed by other moral foundations. Our study initiates inquiry on moral foundations framing and provides preliminary evidence for the potential of this approach. We encourage future research to consider how different moral foundations resonate with different ethical content and further explore how different moral foundations frames operate in ethical decision-making in business. In sum, not all moral foundations are equal, and future research might study those differences.

In Study 2, we also advance scholarly understanding of the dual-objective function that involves morality and self-interest. Existing ethics literature has primarily focused on a conflict of interest scenario that features a trade-off between moral pursuit and self-interest (Etzioni, 2003). Limited theorization and research have investigated how ethical decision-making operates in a win-win scenario. This omission is consequential for research on ethical investing due to increased usage of win-win language in practice. For instance, the Morgan Stanley Report (2017) report claims the conflict of interest perception is a “myth” (p. 2). “Perceptions of a trade-off between sustainable investing and financial gain have proven stubborn, despite mounting evidence to the contrary” (p. 1). If these trends continue, our Study 2 results suggest enhanced moral engagement from investors. This prediction is particularly intriguing due to the plausible competing hypothesis (i.e., H3) we theoretically generate, but find no support for. Namely, Crowding Theory (Frey, 2012) leads us to expect financial incentives for ethical investing to crowd out moral considerations. We find support for the opposite. The promise of finance benefits appears to release investors from the costly burden of acting ethically and causes them to be more sensitive to moral foundations framing. Furthermore, in Study 2, the moral foundations endorsement covariate is positively and significantly associated with ethical investment intention in the win-win condition but not in the conflict of interest conditions. We therefore find correlational evidence that moral traits (operationalized by Fairness moral foundations endorsement) propel ethical decision-making only in the win-win condition. In sum, these findings suggest that the moral case for ethical investing can flourish even while the financial case is trumpeted.

Methodologically, the moral foundations framing approach we propose allows scholars to move beyond correlational studies and conduct experiments to explore causality between various moral phenomena and outcomes. For instance, researchers can single out and make salient a particular moral aspect through framing manipulation and observe its causal effect. Being able to test causation is critical for strengthening research on morality in business ethics because it helps to rule out confounding factors and alternative explanations often associated with correlational studies.

Finally, our study advances understanding of retail investors in ethical investing. As ethical investing continues to become more mainstream, it has shifted away from institutional investors and high net-worth individuals to retail investors (Madsbjerg, 2019). Despite this “democratizing” process, limited ethical investing research has investigated the motivations of retail investors. This investor group is worth scholarly attention because retail investors represent a substantial capital market that ethical investing has just begun to engage. Madsbjerg (2019) shows that U.S. retail investors alone hold investing power over US$17 trillion and the global retail investment market is projected to reach US$100 trillion by 2020. Our study sheds light on the ethical investing motivation of retail investors by showing that retail investors’ anticipated fulfillment of financial objectives is critical for them to more freely pursue their ethical objectives.

Limitations and Future Research

Despite the above-mentioned contributions, our research has some limitations. First, the content of the ethical funds in our studies appears to resonate more with the Fairness foundation than the other moral foundations. This fact in combination with the unsatisfactory results of manipulation check in Study 1 hindered us from drawing a definitive conclusion on the framing effects for other moral foundations. Future research can improve manipulation design and test the moral foundations framing effects with other environmental and social issues. We suspect that the effectiveness of moral foundations framing depends partially on the relevance of the foundation to the ethical content.

Second, we readily acknowledge there is a third, middle of the road, dual-objective scenario where investors perceive that ethical funds tend to produce about the same return performance as conventional funds. Would moral foundations frames effectively enhance ethical investment intentions in this condition? Because such a condition would likely relieve the tension and conflict of the decision-making process, we suspect the answer is yes, like we demonstrated in our win-win condition, but with a smaller effect size. As this equal return scenario presents a situation free of the influence of return performance, it is an ideal condition to investigate other factors (e.g., gender, wealth) that may shape the effectiveness of moral foundations frames. It is also worth noting that while we operationalized dual objectives using categories to simplify experimental design, the magnitude of return difference could affect decision-making. To gain more nuanced insights, future research can refine the condition of dual objectives as a continuum from high financial sacrifices through zero loss to high financial rewards.

A third limitation is that, due to the exploratory nature of this study, we only focused on investors’ intentions and not actual investment behaviors. We acknowledge that intentions are distinct from actual behaviors. There is also a difference between what people say they intend to do in an experimental setting and what they actually do in real life. We thus encourage further research to investigate whether and how investors’ actual investment behaviors may be influenced by moral foundations framing. Researchers can design field experiments to capture investors’ real investment decisions. Indeed, conducting future research on non-online recruited samples can also enhance the external validity of our findings.

Conclusion

In this article, we employ a moral foundations framing approach to explore whether a moral state of mind created by moral foundations frames can increase retail investors’ ethical investment intention. Through two online experiments with U.S. retail investors, we observe that the moral foundations framing effect varies by moral foundation and that there is a stronger moral foundations framing effect in the win-win scenario. Our study provides preliminary evidence for the potential of moral foundations approach and opens up meaningful research opportunities for future inquiry.

Footnotes

Acknowledgements

The authors would like to thank the editor and three anonymous reviewers for their helpful comments and suggestions on the previous drafts of this article. We appreciate the helpful feedback provided by the International Association for Business and Society (IABS) Corporate Governance Workshop.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the Lake Institute Network of Emerging Scholars from the Indiana University Lilly Family School of Philanthropy and by PSC CUNY Research Grants (#67786-0045, #68409-0046)