Abstract

Although a tainted outside director’s social status may serve as a buffer against devaluation owing to an affiliate firm’s corporate financial misconduct, the extent of this buffer effect is unclear. We propose a threshold approach by introducing the expectancy violation perspective, which generates a theoretical tension from the network-embeddedness perspective, to clarify the following question: From which perspective does the buffer effect of social status become more salient? Specifically, we propose an inverted U–shaped relationship between the directors’ social status and the departure of tainted outside directors from host firms. We theorize that when directors’ social status exceeds a certain threshold, the network-embeddedness perspective is more dominant than the expectancy violation perspective. Moreover, a host firm’s external stakeholder attention and board social status moderate the inverted-U effect such that its turning point shifts to the right because such contingencies increase the threshold for the buffer. Using a sample of tainted outside directors penalized for associated firms’ financial misconduct, we find evidence that supports our predictions. Our study helps clarify the boundary between the competing theoretical perspectives of expectancy violation and network embeddedness to explain the phenomenon of tainted director departure.

Keywords

It has been widely assumed that the careers of tainted outside directors of affiliated firms that have disclosed corporate financial misconduct may suffer owing to the potential penalties that may be levied on their host firms (Cowen & Marcel, 2011; Janney & Gove, 2019). However, it is unclear whether this assumption is correct. Existing studies have sought to answer this by drawing on different theoretical perspectives. They have investigated the validity of the following dilemma: Is the social status of tainted outside directors a liability for their careers in host firms, or is it a buffer? Social status refers to “a socially constructed, intersubjectively agreed-upon, and accepted ordering or ranking of individuals, groups, organizations, or activities in a social system” (Washington & Zajac, 2005, p. 1147). The network-embeddedness perspective suggests that high status in a social network can serve as a buffer from stigmatization and devaluation for directors (Jiang et al., 2018). According to this perspective, the social status of a tainted outside director within an embedded network serves as a safeguard, protecting the director from devaluation in the host firm (Balkundi et al., 2011; Schepker & Barker, 2018; Wiesenfeld et al., 2008).

However, the expectancy violation perspective provides a contrary view, suggesting that the violation of an expectation to fulfill an individual’s duties will lead to disappointment and penalties (Burgoon, 2015; Hayibor, 2012; Wayne et al., 2023). The high social status of outside directors also elevates the firm’s expectations that their service as directors will bolster the firm’s reputation (Muller et al., 2024). Consequently, tainted outsider directors’ social status can be a liability, resulting in greater disappointment within host firms when the tainted directors fail to prevent misconduct in affiliated firms. The aforementioned competing perspectives present an unanswered dilemma: Does the social status of tainted outside directors act as a liability, prompting the likelihood of their departure from non-fraudulent host firms, or as a buffer, reducing this likelihood?

To address this question, we introduce a threshold approach to identify which perspective is more dominant when the social status of tainted outsider directors increases. According to the expectancy violation perspective, the failure to meet firm expectations results in increased disappointment and penalties (Burgoon, 2015). As the social status of outside directors increases, the high expectations placed on them confer a heavier burden; furthermore, high expectations are more likely to cause conflicts regarding firm expectations in the future. Conversely, the network-embeddedness perspective suggests that extremely low-level social status does not create an advantage stemming from the individual’s position in a social network (Burt, 2000; El-Khatib et al., 2021). This perspective posits that only high-level social status can act as a buffer, shielding tainted outside directors from penalties due to expectancy violations (Schepker & Barker, 2018). That is, regarding tainted directors’ departures from host firms, expectancy violations will be dominant when their social status increases from low to moderate (liability). By contrast, network embeddedness will dominate when their social status continuously increases to a sufficiently high level (buffer). Thus, we propose an inverted U–shaped relationship between tainted outside directors’ social status and their departure from a non-fraudulent host firm after their affiliated firm faces accusations of misconduct.

From the expectancy violation perspective, not only do their own host firms have expectations for outside directors, but stakeholders from both “Main Street” (i.e., the media) and “Wall Street” (i.e., institutional investors and security analysts; Lamin & Zaheer, 2012) also anticipate that these directors will uphold their firms’ reputations (Capriotti, 2009; Gond & Piani, 2013; Ryan & Schneider, 2003). Accordingly, we argue that the attention that both stakeholder groups pay to outside directors can elevate the buffer threshold, as firms are under pressure to maintain elevated normative standards due to this amplified scrutiny. Moreover, from the network-embeddedness perspective, a board’s collective high social status can elevate the buffer threshold as it can substitute for the function of a tainted individual director’s social status to maintain firm legitimacy (Westphal, 1999). Under these circumstances, tainted outside directors must possess higher levels of individual social status to meet the heightened thresholds and shield themselves from devaluation in their host firms. Combining these arguments, we propose two sets of contingent effects: (a) attention from external stakeholders (both Main Street and Wall Street) and (b) the social status of the host firm’s board, which amplifies the threshold for the buffer effect of tainted outside directors’ social status.

This study explores the aforementioned theoretical dilemma to clarify the relationship between social status and tainted directors’ careers. First, our study addresses the theoretical dilemma by applying the divergent theoretical perspectives of network embeddedness and expectancy violation to elucidate the effect of social status on tainted director departures from host firms (Burgoon, 2015; Schepker & Barker, 2018). We argue that a single perspective may not sufficiently explain this theoretical dilemma and that we need to integrate arguments from both the network-embeddedness perspective and the expectancy violation perspective to fully explicate this phenomenon. Second, this study combines insights from different streams of research on the turnover of top elites (Burgoon, 2015; Tian et al., 2022). Thus, we provide a new framework for understanding the tensions between distinct perspectives. Finally, our study contributes to the corporate governance (CG) literature by revealing host firms’ external and internal CG mechanisms as contingency conditions of the liability–buffer duality of the elite social status (Al-Bassam et al., 2018; Endrikat et al., 2021; Post et al., 2011; Puncheva, 2008). We show that the relationship between social status and tainted director departure from the host firm can be influenced by conditions such as stakeholder attention and the host firm’s board social status.

Theoretical Background and Hypotheses

Expectancy Violation and Network Embeddedness: A Dilemma

Network-Embeddedness Perspective

Recently, network embeddedness has become the dominant theoretical perspective on social status as a buffer. According to Wiesenfeld et al. (2008, p. 240), the buffer effect may occur for at least four reasons: (a) firms tend to harbor goodwill toward directors high in social status and are reluctant to denigrate them, as such goodwill often leads to a positive affective response; (b) directors with high social status tend to be perceived as trustworthy, given that the norms of reciprocity and trustworthiness arise from embedded individuals in a network; (c) directors with high social status have more opportunities to justify their innocence through personal connections and communication—as such, these directors are more likely to be excused; and (d) directors with high social status may sit on multiple influential boards or have close elite friends. Such network ties may buffer them from stigmatization or devaluation by disseminating specific and personal information that contradicts publicly available stereotypical depictions.

As a result, outside directors with high social status often have strong relationships with other influential directors and can rely on their networks to buffer them from devaluation when faced with allegations of corporate misconduct (El-Khatib et al., 2021). In turn, their upper-class origins can mitigate tainted directors’ likelihood of losing out on other board appointments (Wurthmann, 2014). Evidence has also shown that some stigmatized directors may survive with the help of their high social status, despite the apparent damage to their reputations associated with that stigma (Schepker & Barker, 2018; Tian et al., 2022; Tracey & Phillips, 2016; Wiesenfeld et al., 2008). However, this stream of research has paid little attention to the potentially negative consequences of social status.

Expectancy Violation Perspective

An expectancy violation is an instance in which individuals face negative repercussions due to their violation of widely accepted norms or behaviors. Services on a corporate board confer prestige, status, financial rewards, and other perquisites to outside directors; as such, they are expected to maintain their reputation and legitimacy of the boards on which they serve (Hambrick & D’Aveni, 1992; Mizruchi, 1983). Because directors are often a firm’s public representatives, when their performance falls short of expectations, the situation can cause disappointment among the firm’s managers and stakeholders. Specifically, expectancy violations may raise concerns about a corporate leader’s trustworthiness (Schepker & Barker, 2018), integrity, competence, or capability (Kim et al., 2004) because such violations are often perceived as a permanent indication of a flawed individual (Farber, 2005; Stevenson & Radin, 2009). Once corporate misconduct occurs, outside directors are likely to suffer violation penalties because they fail to meet firm expectations for monitoring and surveillance, thereby increasing the risk of devaluation in the job market (Cowen & Marcel, 2011; Wiesenfeld et al., 2008; Wurthmann, 2014).

Our study extends the expectancy violation perspective by focusing on situations in which an individual performs below expectations (i.e., a director’s failure to fulfill their duties) and the consequent negative valence (e.g., the magnitude of disappointment and devaluation in host firms in terms of director social status). Violation valence refers to the extent to which an individual’s violations are perceived, evaluated, or justified (D. I. Johnson, 2012; White, 2015). A negative valence of violations is often related to two factors. First, the interpretation of the nature of violations is primarily influenced by how corporate misconduct runs counter to social norms. Devaluations are also harmful because of the broadcast effect through which negative evaluations spread widely and publicly regarding the association between the accused firm and its directors (Pontikes et al., 2010). Second, violation valence relies on various factors associated with tainted individuals, including their attractiveness, status, reputation, position, visibility, and resources (Burgoon & Walther, 1990). Certain directors may bear higher levels of personal responsibility and accountability for violation penalties because they are subject to higher expectations associated with their elevated social status. For instance, directors serving as audit and governance committee chairs are viewed as more responsible (or culpable) than others if they fail to detect alleged financial-reporting fraud (Kang, 2008). From this viewpoint, outside directors’ social status can be viewed as a liability in the event of corporate misconduct because a high-status individual is often subject to higher expectations, and their violations cause greater disappointment and negative consequences (Jackson et al., 1993).

Although these two competing perspectives present a dilemma in terms of understanding the effect of social status on the departure of tainted outside directors, we argue that a plausible way to understand this dilemma is to investigate the threshold that determines when social status acts as a buffer against the devaluation of a director.

A Threshold Approach for Two Competing Perspectives

We propose an inverted U–shaped relationship between tainted outside directors’ social status and their departure from non-fraudulent host firms following corporate misconduct. From an expectancy violation perspective, a tainted director’s social status may increase the chance of that director’s departure for two reasons. First, a higher social status elevates a firm’s expectations; firms expect outside directors to have a high social status to enhance the board’s reputation and legitimacy (Certo, 2003; Mizruchi, 1996). Directors who fail to prevent misconduct also fail to meet these expectations, and their presence may even damage the reputation of their host firms (Arthaud-Day et al., 2006). When an outside director’s social status increases, the liability effect of that social status may become stronger because the host firm’s perceived violation valence also increases.

Second, outside directors with high social status often receive greater attention, recognition, and visibility because of their accomplishments in elite networks (Merton, 1968). Thus, they can be perceived as “falling stars” due to their failure to carry out their duties appropriately (Pollock et al., 2016; Wade et al., 2008) and are put under the spotlight to a greater extent than others after corporate misconduct becomes known. In this scenario, outside directors who possess higher social status yet violate a firm’s expectations will face more severe penalties (Dai et al., 2018; Hillman & Dalziel, 2003). Because the visibility associated with their high status allows news of corporate misconduct to be widely broadcast, outsider directors with high social status are often held more accountable than others (Graffin et al., 2013). Given that high expectations lead to greater disappointment in the face of corporate misconduct, host firms may depose outside directors with high social status from accused firms to protect and repair their legitimacy.

We further argue that the network-embeddedness perspective becomes more salient when outside directors’ social status exceeds a threshold (especially at an extremely high level) and that the buffer effect of high social status against devaluation outweighs the liability effect for three reasons. First, when directors’ social status is extremely high, such status is more likely to trigger conciliatory responses from host firms and create insurance for the directors against devaluation following negative events (Jones et al., 2000). In addition, outside directors with sufficiently high social status are more likely to defend themselves, justify their innocence, and divert blame because of their perceived trustworthiness within their host firms (Davis et al., 2003). Consequently, these directors may escape blame, negative evaluations, devaluation, or violation penalties (Mizruchi, 1996; Wiesenfeld et al., 2008). In contrast, outside directors whose social status falls below the threshold may not be afforded the same leniency (El-Khatib et al., 2021; Jiang et al., 2017). Thus, they are more likely to be blamed for failed fiduciary duties and expectancy violations.

In this context, social status is regarded as a combination of fungible personal resources that signal the positive aspects of individual capabilities, a reduction in harmful information dissemination, and avoidance of devaluation (Schepker & Barker, 2018). When directors’ careers are at risk, they are likely to activate their network ties and receive support from their social network (Jiang et al., 2014).

In addition, when the social status of outside directors exceeds a threshold, it may provide a resource buffer that enables directors to escape personal stigma and devaluation (Jiang et al., 2017) through access to external resources such as “money, people, machines, information, technology, products, and services” (Miner et al., 1990, p. 690). Very high levels of social status reflect the ability of an outside director to extract resources from relationships and, therefore, guard their position against violation penalties in organizations (Schepker & Barker, 2018). In this situation, the buffer effect is more salient, as host firms can benefit more from directors’ connections to external resources that the firm may not have otherwise had access to (Cai & Sevilir, 2012; Hillman & Dalziel, 2003). In many cases, the costs of losing an outside director with extremely high social status can be very high, subsequently translating into lower firm performance. If the benefits of retaining an outside director outweigh the costs, the host firm will likely retain the director because of the need for external resources.

Combining these arguments, we posit that tainted outside directors’ social status has an inverted U–shaped impact on their departure from host firms. When the social status threshold is moderate, tainted directors are subject to the most stringent penalties (Phillips & Zuckerman, 2001). In other words, from the expectancy violation perspective, outside directors with moderate levels of social status are more likely to suffer violation penalties than directors with low social status (White, 2015). At the same time, from the network-embeddedness perspective, such directors are less likely to benefit from the buffering mechanism than directors with sufficiently high social status. Only when social status exceeds a threshold will it generate a sufficiently favorable impression to neutralize “guilt by association” (Sun et al., 2015) and encourage host firms to harbor goodwill toward the tainted directors. This leads to the following hypothesis:

Shifting in Threshold of Buffer

We further theorize that the buffer threshold may shift depending on two contingencies: external stakeholder attention and the host firm’s board social status. We propose that the turning point of the inverted U–shaped effect of director social status shifts rightward when external stakeholder attention and the host firm’s board social status are high.

External Stakeholder Attention as a Moderator

Expectancy violations begin with a discrepancy between expected and actual outcomes (Fediuk et al., 2010). However, not all discrepancies are noticed, and not all noticed discrepancies are perceived as violations. From the expectancy violation perspective, whether a discrepancy is noticeable and violates expectations depends on stakeholders’ willingness to maintain a watchful eye—a relationship best described as follows: “Interpretations of violations are in the eye of the beholder” (Fediuk et al., 2010, p. 640). When stakeholders pay greater attention to an organization, they may sense that its behavior is contrary to their expectations (Fediuk et al., 2010). External stakeholders, often categorized as Main Street versus Wall Street stakeholders (Lamin & Zaheer, 2012), are inclined to monitor a firm’s adherence to social norms, codes, and standards. Main Street, represented by the mass media, has a professional responsibility to scrutinize a firm’s actions, whereas Wall Street, represented by investment communities, places significant emphasis on a firm’s legitimacy, which can impact investors. Collectively, stakeholder attention imposes pressure on firms to set higher standards to retain the appropriate directors to meet stakeholder expectations. When external stakeholders closely follow host firms, the threshold for firms to retain tainted outside directors is higher. Accordingly, the turning point shifts rightward for the inverted U–shaped influence of the directors’ social status on their departure.

In this study, we focus on three types of key external stakeholders—the media, institutional investors, and security analysts—because they emphasize firms’ conformity to social norms and are less tolerant of violations (Capriotti, 2009; Gond & Piani, 2013; Ryan & Schneider, 2003). Mass media (Main Street stakeholders) rely on media reports to identify firms’ events, actions, and directorial information, which consequently shape their perceptions of a firm’s legitimacy (Lamin & Zaheer, 2012). The media may raise the threshold for the buffer effect of outside directors’ social status because the press often serves as a “watchdog” that emphasizes social norms and monitors firms’ behavior, propagates reports of legitimacy (or lack of it), and acts as a social arbiter by evaluating organizations (Bednar, 2012). When host firm media coverage is high, the buffer threshold for an outside director’s social status increases as the host firm is under greater pressure to maintain its board’s reputation (Wade et al., 2008) and improve normative standards. Specifically, given that the media investigate corporate events and efficiently deliver messages to the public (Dyck et al., 2008), a firm more extensively covered by the press often attracts greater attention to its reputation (Deephouse, 2000). Therefore, to maintain directorships in host firms, tainted outside directors must have a much higher social status to exceed the elevated buffer threshold.

By comparison, institutional investors, as a significant stakeholder group within the investment community, need to exert considerable influence on firms’ objectives, strategies, capital structures, and decision-making, to protect their own interests (Cowen & Marcel, 2011; Kobeissi & Damanpour, 2009). Terminating poor-performing directors is an example of institutional investors protecting their interests (Gond & Piani, 2013). In contrast to smaller investors, who hold minority positions and lack the time and information needed to monitor a firm’s behavior, institutional investors hold large quantities of capital and significant ownership positions in host firms. Thus, institutional investors have financial commitments that warrant employing professionals to analyze host firms’ CG to protect their interests. They are also likely to actively voice their concerns and may even divest from firms based on potential negative impacts on share value and social problems that emerge within the environmental, social, and governance (ESG) framework (McNulty & Nordberg, 2016). Their proactive involvement in ESG matters aims to guide firms toward sustainable and ethical practices to protect their potential interests. Institutional investors may also protect their interests by engaging in activism to change directors when they fail to fulfill their duty of detecting misconduct.

In addition, studies suggest that institutional investors frequently adopt long-term investment horizons because of their index portfolio strategies, enabling them to evaluate a firm’s legitimacy within an extended timeframe (R. A. Johnson & Greening, 1999). Consequently, they manifest a “caretaking” role wherein they attentively monitor, are responsible for, and actively influence the activities and decisions of the firms they invest in (Shropshire et al., 2023). They often “express an evaluation of the corporate governance mechanisms of the firm” (Sauerwald et al., 2016, p. 542). Thus, institutional investor attention is likely to raise the buffer threshold for the outside directors’ social status to justify a firm’s decisions. In firms with substantial shareholdings, institutional investors are more inclined to scrutinize company decisions and exert influence by removing tainted outside directors through activist measures (Gillan & Starks, 2003). Alternatively, they may walk away by selling their shares if the director is not terminated without reasonable justification. Thus, when institutional investor attention increases the buffer threshold, tainted directors must have more social status to exceed this threshold and activate a buffering mechanism to maintain their directorship.

Finally, security analysts tend to raise firms’ normative standards to protect their reputations and shareholder interests because potential corporate misconduct by covered firms may damage their reputation and shareholder interests. In general, security analysts make influential judgments about host firms and provide regular forecasts of host firms’ earnings and long-term growth for shareholders. They issue stock recommendations and target price forecasts that significantly affect the share prices of covered firms (Cowen et al., 2006). In addition, security analysts function as critical intermediaries between firms and investors by continually gathering, processing, and disseminating stock-related information to various investors (Chung & Jo, 1996).

Security analysts play a multifaceted role and have marketing and monitoring functions. Regarding the marketing function, security analysts employed by brokerage houses play a crucial role in generating transactions with potential shareholders, and so they have a vested interest in following stocks of high-quality firms that are more marketable. Consequently, firms that receive more attention from analysts tend to have higher expectations from potential shareholders. In turn, analysts’ extensive attention can elevate the standards that tainted corporate leaders are measured against while demanding that host firms meet amplified stakeholder expectations. In terms of their monitoring function, security analysts’ role in communicating shareholder dissatisfaction with firms has grown significantly, fostering sound CG practices in response to investor demands (Chung & Jo, 1996). Thus, security analysts influence firms’ decisions by shaping investor perceptions. In turn, a wide variety of investors often align their decisions with analysts’ evaluations (Busenbark et al., 2017; Hong & Kacperczyk, 2009). Consequently, in scenarios involving extensive analyst attention, tainted outside directors must possess sufficient social status to satisfy the heightened threshold required by host firms to justify their retention decisions.

In summary, when external stakeholders, such as the media, institutional investors, and security analysts, pay closer attention to host firms, the buffer threshold increases for tainted outside directors. Consequently, directors with sufficient social status to meet the elevated threshold may activate the buffering mechanism, as indicated by the turning point of the inverted U–shaped relationship between director social status and departure, which shifts rightward once corporate misconduct occurs. Hence, we propose the following hypotheses:

Board Social Status as a Moderator

From the network-embeddedness perspective, “an individual or a social unit” can possess social capital and gain social status (Tian et al., 2011). Board social status captures all other board members’ collective relationships in the interlocking network beyond that of a particular member (Hillman & Dalziel, 2003). In other words, board social status refers to the degree to which board members, excluding tainted outside directors, have external contacts through their personal ties in the same interlocking network (Cowen & Marcel, 2011; Hillman & Dalziel, 2003). Given that board social status can substitute for director social status (Westphal, 1999), we argue that board social status may alter the inverted U–shaped relationship by raising the buffer threshold for director social status and shifting the turning point to the right.

Specifically, a host firm may raise its buffer threshold when its board social status is high. In such a case, the host firm is better able to access and secure external resources and support through its members’ social networks to stabilize operations, regardless of any individual director’s departure from the board, because the firm is not constrained by a particular director’s social status (Borgatti & Cross, 2003; Westphal, 1999). Moreover, the board can attract more capable director candidates who satisfy particular firm needs or can better compensate for a tainted director’s social status. Therefore, a high board social status provides a firm with a resource that can buffer it from external uncertainties by allowing it to access high-quality resources to secure superior organizational outcomes.

Accordingly, tainted outside directors must have greater social status to exceed the elevated buffer threshold by overcoming the substitute effect of a high board social status. Alternatively, firms may discount the failures of certain tainted outside directors with very high social status (Rao et al., 2005; Wiesenfeld et al., 2008) because the structural complexity of these directors’ personal ties creates a barrier to imitation or substitution (Evans et al., 2022). Their departure causes the organization to suffer, regardless of whether the director is deemed reputationally tainted (Wiesenfeld et al., 2008). By contrast, when the host firm’s board social status is deficient, the social status of a tainted outside director is difficult to replace. Such boards may face pressure to ensure continued firm operations by accessing external information and resources or facilitating inter-firm commitment (Bazerman & Schoorman, 1983). Low board social status is more likely to increase a host firm’s reliance on the social status of tainted outside directors to deal with this pressure. Thus, the buffer threshold for director social status is lower when board social status is low than when it is high. Taken together, we propose the following hypothesis:

Method

Data

To test our hypotheses, we collected data from the WIND Information Corporation (WIND) and China Stock Market and Accounting Research (CSMAR), the two most widely used databases for public firms listed on the Shanghai Stock Exchange and the Shenzhen Stock Exchange (Jiang et al., 2017; Tian et al., 2021; Yiu et al., 2014). We identified tainted outside directors as those who were in host firms and were associated with other firms that were penalized for financial misconduct by the China Securities Regulatory Commission (CSRC). The CSRC, similar to the U.S. Securities and Exchange Commission (SEC), was established in 1998 to monitor and regulate public firms in China by developing regulations, monitoring conformity, and enforcing sanctions. In January 2001, the CSRC issued its Code of Corporate Governance. 1 Thus, the window for our observations was 2001–2017.

Our sample construction followed the procedure described in prior research (e.g., Srinivasan, 2005), especially in the context of China (e.g., Yiu et al., 2014, 2019). We tracked each director in a host firm for 3 years after an accused firm connected through the director was penalized by the CSRC. Thus, our sample included all host firms with tainted outside directors associated with penalized firms from 2001 to 2014. We also note that the outside directors of host firms penalized by the CSRC were not included in our sample because they were directly involved in misconduct, and not simply tainted. 2 Our sampling procedure identified 6,176 tainted outside directors in 1,899 host firms and 1,003 penalized firms. Because some tainted outside directors departed within 3 years and held board positions in multiple firms, our final sample was an unbalanced panel of 21,700 director-host firm-year observations.

Measurements

Departure of a Tainted Outside Director From the Host Firm

As we will subsequently discuss, we used the Cox regression to model the time of a director’s departure from the host firm. More specifically, we examined whether a tainted director departed within a 4-year timeframe from year t, when the CSRC penalized the director’s firm, until year t + 3 (Srinivasan, 2005). According to Chinese Corporate Law, 3 director elections are held every 3 years, same as the United States (Cowen & Marcel, 2011). Thus, our time window allows us to capture the scenarios, even though firms’ election schedules might vary. We coded the variable as 1 if the director’s departure occurred from the host firm in a given year, or 0 otherwise. All time-variant predictor variables (described next) were lagged by 1 year.

Director Social Status

We measured the social status of a tainted outside director using eigenvector centrality in the interlocking network of all listed firms in China, in line with existing studies (Jiang et al., 2017; Markóczy et al., 2013). Eigenvector centrality considers not only the number of connections an individual has but also the quality or importance of those connections (Bonacich, 1987). On social networks, connections to influential or high-status individuals can enhance one’s status. By considering the centrality scores of neighboring nodes, eigenvector centrality captures the idea that being connected to other individuals with high social status contributes to one’s own status. Thus, we employed eigenvector centrality to measure social status in our setting (Carpenter et al., 2012).

Specifically,

where

This equation means that the eigenvector centrality is the eigenvector of the adjacency matrix

Host-Firm Media Coverage

This variable was measured by the logged number of unique newspapers that reported information on a host firm each year (J. Chen et al., 2016).

Host-Firm Institutional Ownership

A host firm’s institutional ownership was measured by the proportion of the firm’s shares owned by institutional investors (e.g., banks, insurance companies, and mutual funds; Wu et al., 2016).

Host-Firm Analyst Coverage

We measured a host firm’s analyst coverage as the logged number of unique brokerage houses that issued reports about the host firm (J. Chen et al., 2016). Like investment banks in the United States, brokerage houses in China often publish analyst reports on different aspects of selected listed firms. We measured this variable using the logged value to correct its highly skewed nature.

Host-Firm Board Social Status

We first excluded tainted outside directors from the host board and then calculated the eigenvector centrality of each host director in the interlocking network (Jiang et al., 2017). We then averaged the centrality scores of all the directors on the host board to measure the board’s social status.

Control Variables

We controlled for several variables identified in prior literature that may also affect director departure. Regarding host-firm characteristics, we controlled for firm size, measured by the logged firm’s total assets; firm performance, measured by return on assets (ROA); and firm leverage, measured by the debt-to-assets ratio. Small firms, poorly performing firms, and firms with high debt levels are more likely to retain outside directors due to a lack of resources (Thornhill & Amit, 2003). We also controlled for host-firm state ownership, measured as the proportion of the firm’s shares owned by the government, given the government’s power to influence a firm’s decisions.

Moreover, we controlled for host-firm board independence, measured as the number of independent board members divided by board size (Yiu et al., 2019), because directors are expected to protect shareholders’ interests against misconduct (G. Chen et al., 2006). We controlled for host-firm use of a foreign auditor, which was coded as 1 if the host firm hired one of the Big Four auditing firms (i.e., Ernst & Young, Deloitte & Touche, KPMG, and PricewaterhouseCoopers), or 0 otherwise. We also controlled for CEO tenure in the host firm, measured by the number of years the CEO worked there.

Given that director tenure may influence departure, we controlled for director tenure in the host firm, measured by the number of years that a tainted outside director served on the host firm’s board (Graffin et al., 2013; Zhang & Rajagopalan, 2003). We controlled for director gender, which was coded as 1 for females and 0 for males, because female leaders may experience gender stereotypes and biased judgments (Heilman, 2012). Moreover, we controlled for director age because older directors are more likely to retire. In addition, given the information advantages in identifying director candidates, and thereby potential director departures, we controlled for director structural holes, calculated as 1 minus the value of the social network constraint (Burt, 2004). We also controlled for director as audit member in host firm, which was coded as 1 if the director served on the audit committee in the host firm, or 0 otherwise (Srinivasan, 2005). We controlled for director power in the host firm, which was coded as 1 if the director served as board chair in host firm or 0 otherwise (Banerjee et al., 2020).

Regarding penalized firms’ characteristics, we controlled for their size, state ownership, and performance, measured in the same manner as previously described for host firms. An accused firm with a large size and high performance and was owned by the state may provide valuable external resources to host firms, thereby affecting the departure of tainted outside directors. We controlled for the penalty on the penalized firm using the total fines (logged) imposed by the CSRC on the penalized firm. We also controlled for the director as an executive in the penalized firm (coded as 1 if the director was an executive or 0 otherwise), given that a director’s duty in the penalized firm may affect the host firm’s decision. We controlled for director departure from the penalized firm (coded as 1 for departure or 0 otherwise), given that a tainted director leaving a penalized firm may indicate the director’s liability for corporate misconduct. We also controlled for director as audit member and director power in penalized firm.

Finally, we fixed the year effect and host firms’ industry effect, which allowed us to exclude the influence of time and industrial variance on director departures. For example, since 2012, the Chinese government has implemented an anti-corruption campaign that may have affected the public perception of tainted directors.

Regression Analysis

We used the Cox proportional hazards regression (Cox, 1972) to calculate the hazard of director departure from host firms. The Cox regression can solve the right censoring issue that ordinary least squares (OLS) or logit regressions cannot handle. This also allowed us to use time-varying covariates because of independent assumptions regarding the baseline hazard. The Cox model assumes that the hazard of any observation is a constant proportion of the hazard of any dependent observation in the sample. This model has been widely used in survival analyses (Jiang et al., 2017; Staw & Hoang, 1995; Xia, 2011; Yu & Cannella, 2007). As we tracked each director over multiple years, we used robust estimations by clustering director IDs to correct for potential correlations in our sample. As an alternative approach, we clustered the IDs of the host firms, which produced consistent results. This method adjusts the estimated variances of the Cox regression hazard ratios obtained for a fitted model to account for the misspecification of the assumed correlation structure.

Since we excluded directors punished by the CSRC, it was necessary to address the potential sample-selection bias (i.e., the likelihood of a director committing financial misconduct), given that our major predictors might also explain why certain directors are more likely to become involved in financial misconduct. We adopted a two-stage Heckman model, which requires valid instrumental variables to address self-selection bias (Heckman, 1979). We included the size of interlock network community as an instrumental variable in the first stage and estimated our model specification by including the control variables from the first stage in the second stage. We took two steps to construct the instrumental variable: (a) We structured the interlock network communities within a network by applying the multilevel modularity optimization algorithm (Clauset et al., 2004); and (b) we measured the size of interlock network community by counting the total number of directors in each community. Conceptually, this instrumental variable affects the likelihood of a director committing misconduct in an accused firm but may not necessarily affect the host firm’s decision. We calculated the inverse Mills ratio from the first stage using probit regression and controlled for it in the second stage using a Cox regression model.

Results

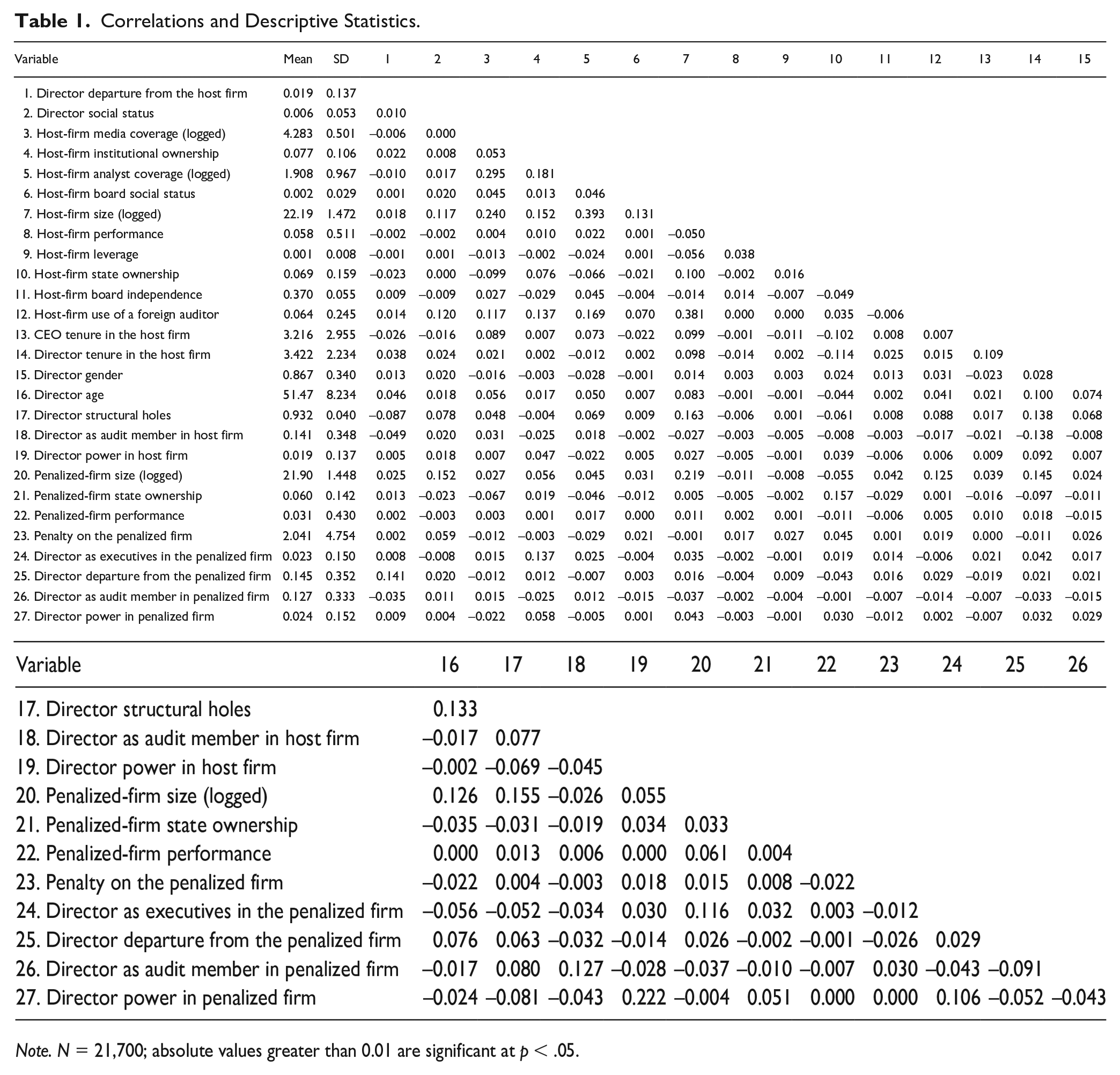

Table 1 provides the means, standard deviations, and correlations for all the variables included in the analyses. The strongest correlation was found between host-firm size and host-firm analyst coverage (r = .393). We computed the variance inflation factors (VIFs) for all variables in all models. The maximum VIF was 1.54, and the mean VIF was 1.07, indicating that multicollinearity was not a concern in our regression analyses. We mean-centered the relevant variables to test the hypothesized interaction effects, which helped avoid possible multicollinearity problems. To facilitate the interpretation of our results, the variables presented in Table 1 are not mean-centered.

Correlations and Descriptive Statistics.

Note. N = 21,700; absolute values greater than 0.01 are significant at p < .05.

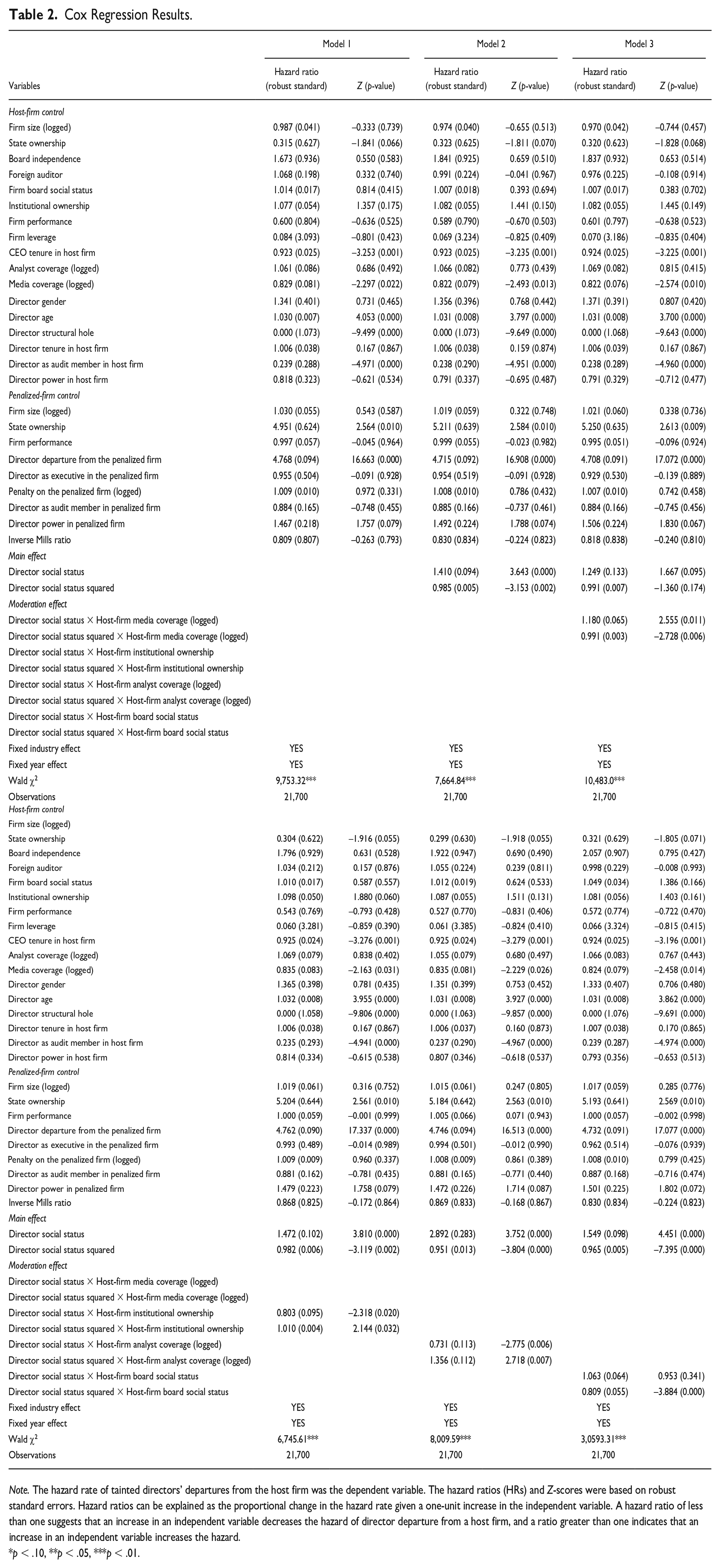

Table 2 presents the results of the Cox regression analysis with hazard ratios, robust standard errors, Z-scores, and p-values. Hazard ratios are interpreted as proportional changes in hazard ratios with a one-unit increase in the independent variables. Ratios less than 1 suggest that an increase in an independent variable decreases the hazard of direct departure from a host firm, and ratios greater than 1 indicate that an increase in an independent variable enhances the hazard. Model 1 includes only the control variables. Model 2 tests the main effect of directors’ social status and its squared term. Models 3–5 test the moderating effects of media coverage, institutional investors, and security analysts. Model 6 tests the moderating effect of the host firm’s board social status.

Cox Regression Results.

Note. The hazard rate of tainted directors’ departures from the host firm was the dependent variable. The hazard ratios (HRs) and Z-scores were based on robust standard errors. Hazard ratios can be explained as the proportional change in the hazard rate given a one-unit increase in the independent variable. A hazard ratio of less than one suggests that an increase in an independent variable decreases the hazard of director departure from a host firm, and a ratio greater than one indicates that an increase in an independent variable increases the hazard.

p < .10, **p < .05, ***p < .01.

The results in Table 2 show that the hazard ratio of the host firm state ownership was 0.315 (z = −1.841, p = .066), while that of the penalized firm state ownership was 4.951 (z = 2.564, p = .010). Thus, when the state ownership of penalized firms increased, the likelihood of tainted directors departing from the host firms also increased. In contrast, when host firms’ state ownership increased, the likelihood of tainted directors departing from those host firms decreased. A possible reason for this is that the state ownership of penalized firms increases the expectation violation perceived by stakeholders regarding tainted directors, as host firms may expect directors in state-owned firms to exhibit high levels of professionalism and normative standards. In contrast, the state ownership of host firms may buffer outside negative judgments and expectations related to tainted directors. Given that state-owned host firms are high in both informal power and legitimacy, they can bear negative judgments and expectations from outside and continue on their planned course of action.

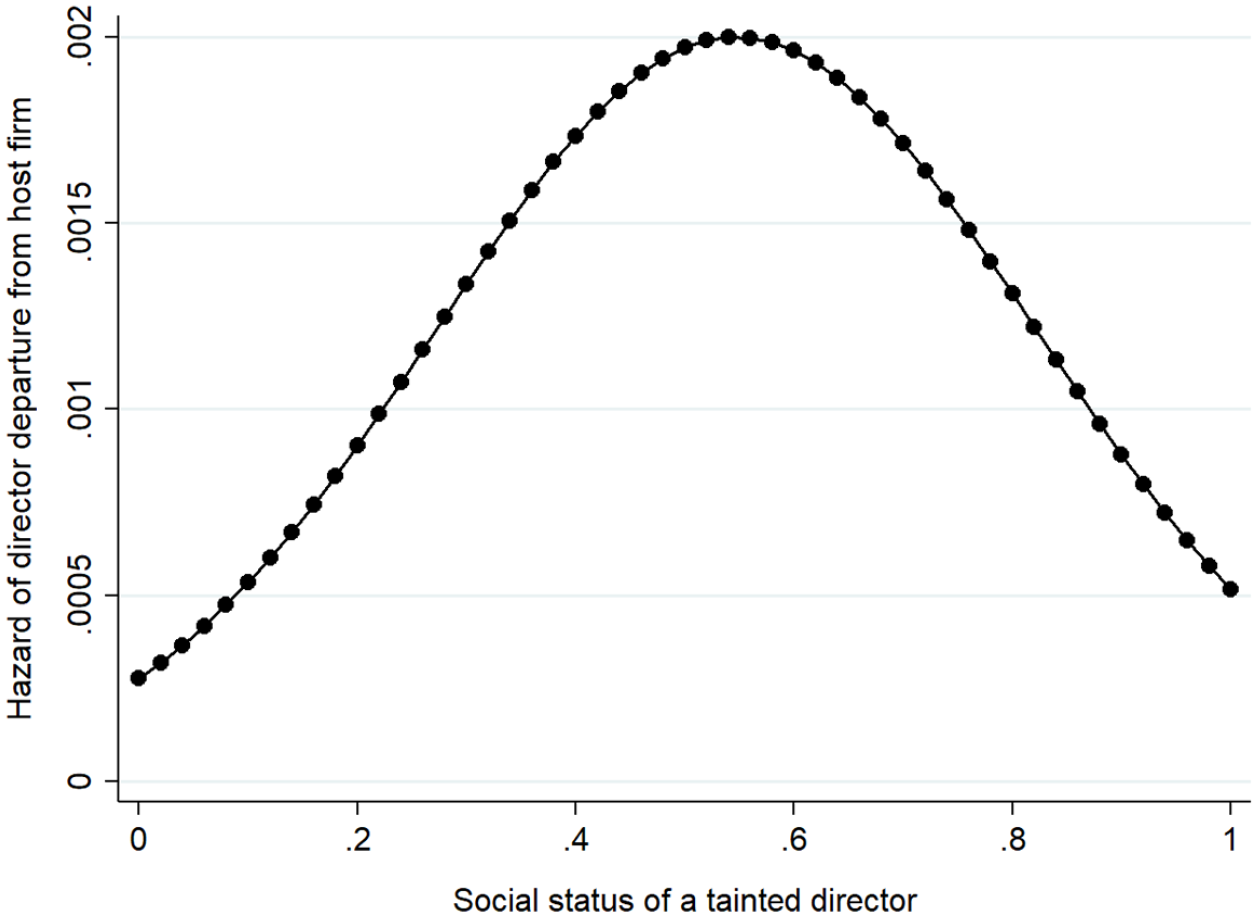

Hypothesis 1 posits that the social status of tainted outside directors has an inverted U–shaped effect on directors’ departure from non-fraudulent host firms. Based on the results of the Cox regressions, we ran delta tests following the three steps suggested by Haans et al. (2016). First, Model 2 in Table 2 shows that the hazard ratio of director social status is 1.410 (z = 3.643, p = .000), indicating that

Inverted U–Shaped Effect of Tainted Director’s Social Status.

To examine the economic significance of our findings, we used a subsample to test the inverted U–shaped relationship (Haans et al., 2016). Theoretically, when a director’s social status is relatively low (i.e., lower than the mean minus 10% of the standard deviation), the relationship between the director’s social status and departure from the host firm is positive. However, when the director’s social status is relatively high (i.e., higher than the mean plus 10% of the standard deviation), the relationship is negative. The results reveal that when a tainted outside director’s social status is at a relatively low level, the hazard ratio of director social status is 1.116 (z = 2.376, p = .018); that is, when social status increases by one unit, the probability of director departure from the host firm increases by 11.6%. In contrast, when a tainted director’s social status is at a relatively high level, the hazard ratio of the director’s social status is 0.311 (z = −2.717, p = .007); that is, when the social status increases by one unit, the odds of the director’s departure from the host firm decreases by 68.9%.

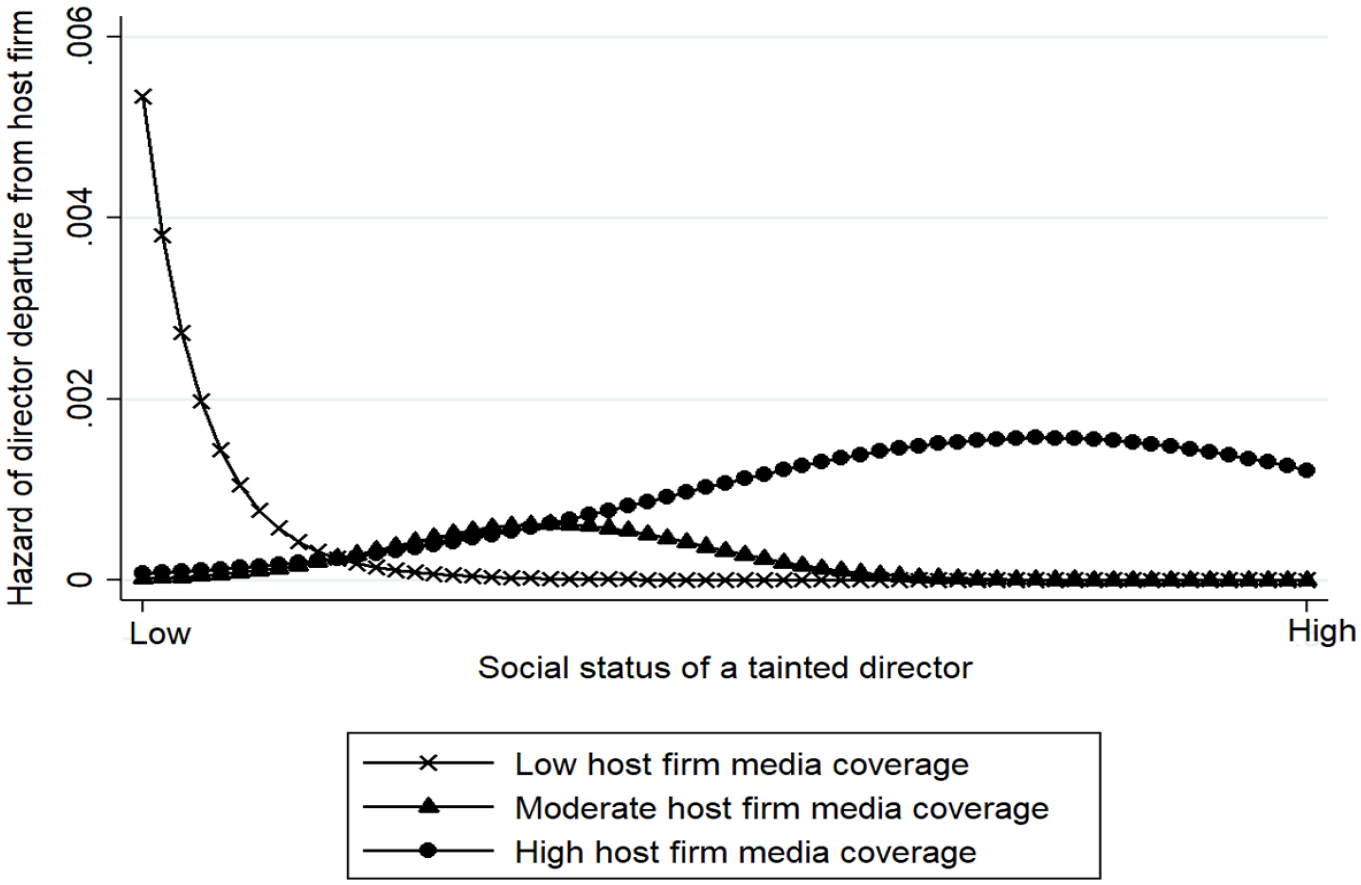

Hypothesis 2a predicts that the turning point of the inverted U–shaped effect of tainted outside directors’ social status on departure shifts right when the host firm attracts more media coverage. As indicated by Model 3 in Table 2, the hazard ratio for the interaction between director social status and media coverage is 1.180 (z = 1.935, p = .065), and the hazard ratio for the interaction between the squared term of director social status and media coverage is 0.991 (z = −2.728, p = .006). To demonstrate this interaction, we have plotted it in Figure 2. Figure 2 shows that the lowest threshold occurs with a low level of media coverage of the host firm, which is beyond the observed data, whereas the highest threshold corresponds to a high level of media coverage of the host firm, indicating that the turning point shifts rightward when the host firm has more media coverage. Specifically, the threshold at which the buffer became effective was lower for the host firm with less media coverage (i.e., the mean minus 10% of the standard deviation) and higher for the host firm with more media coverage (i.e., the mean plus 10% of the standard deviation). Therefore, Hypothesis 2a is supported.

Moderating Effect of Host-Firm Media Coverage.

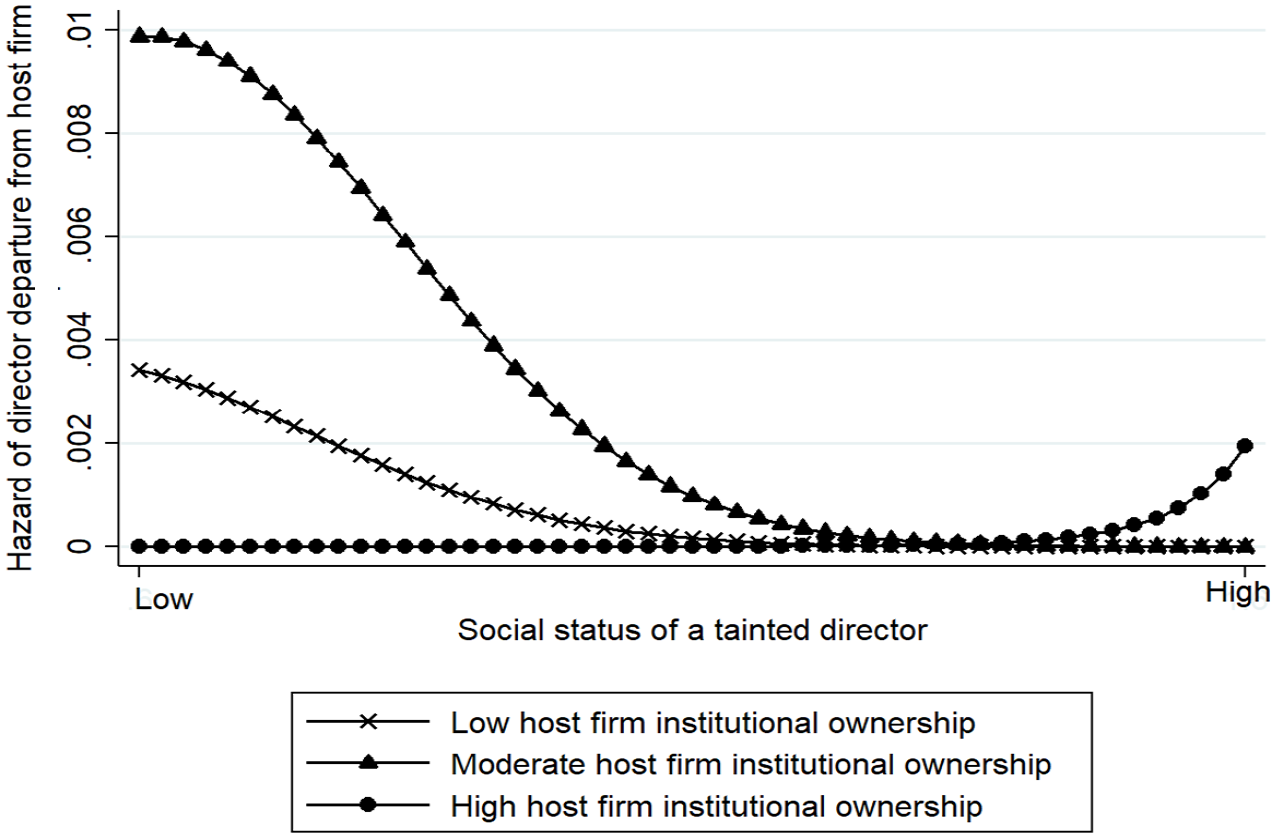

Hypothesis 2b proposes that the turning point of the inverted U–shaped effect shifts to the right when the host firm has higher institutional ownership. As shown in Model 4, the hazard ratio of the interaction between director social status and institutional ownership was 0.803 (z = −2.318, p = .020), and the hazard ratio of the interaction between the squared term of director social status and institutional ownership is 1.010 (z = 2.144, p = .032). Figure 3 shows that the turning point shifts to the right when the host firm has a higher level of institutional ownership. Thus, Hypothesis 2b is supported.

Moderating Effect of Host-Firm Institutional Ownership.

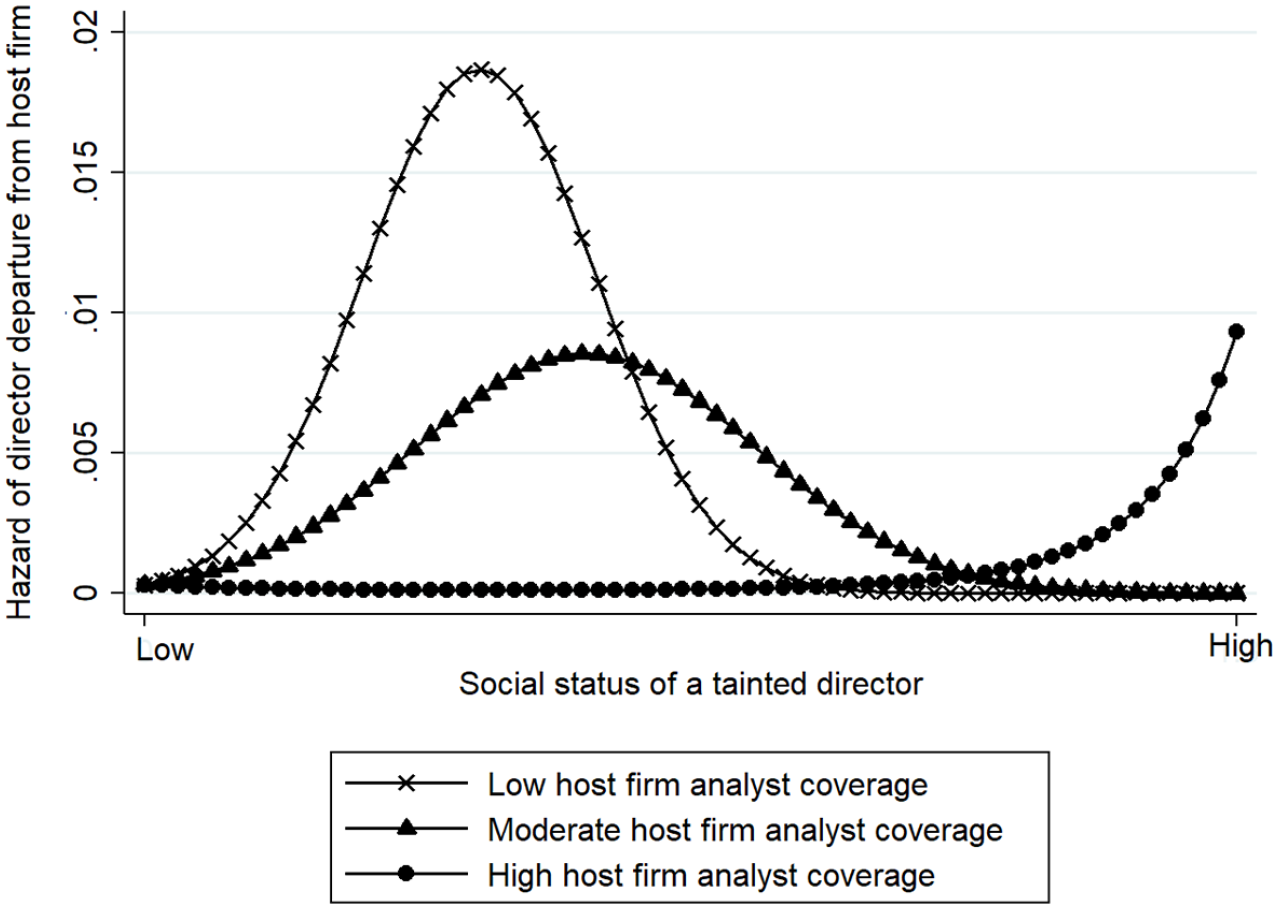

Hypothesis 2c suggests that the turning point of the inverted U–shaped effect of tainted outside directors’ social status on departure shifts right when the host firm has a higher level of analyst coverage. As shown in Model 5, the hazard ratio of the interaction between director social status and analyst coverage is 0.731 (z = −2.775, p = .006), and the hazard ratio of the interaction between the squared term of director social status and analyst coverage is 1.356 (z = 2.718, p = .007). Figure 4 illustrates that the turning point shifts to the right when the host firm has greater analyst coverage. Thus, Hypothesis 2c is supported.

Moderating Effect of Host-Firm Analyst Coverage.

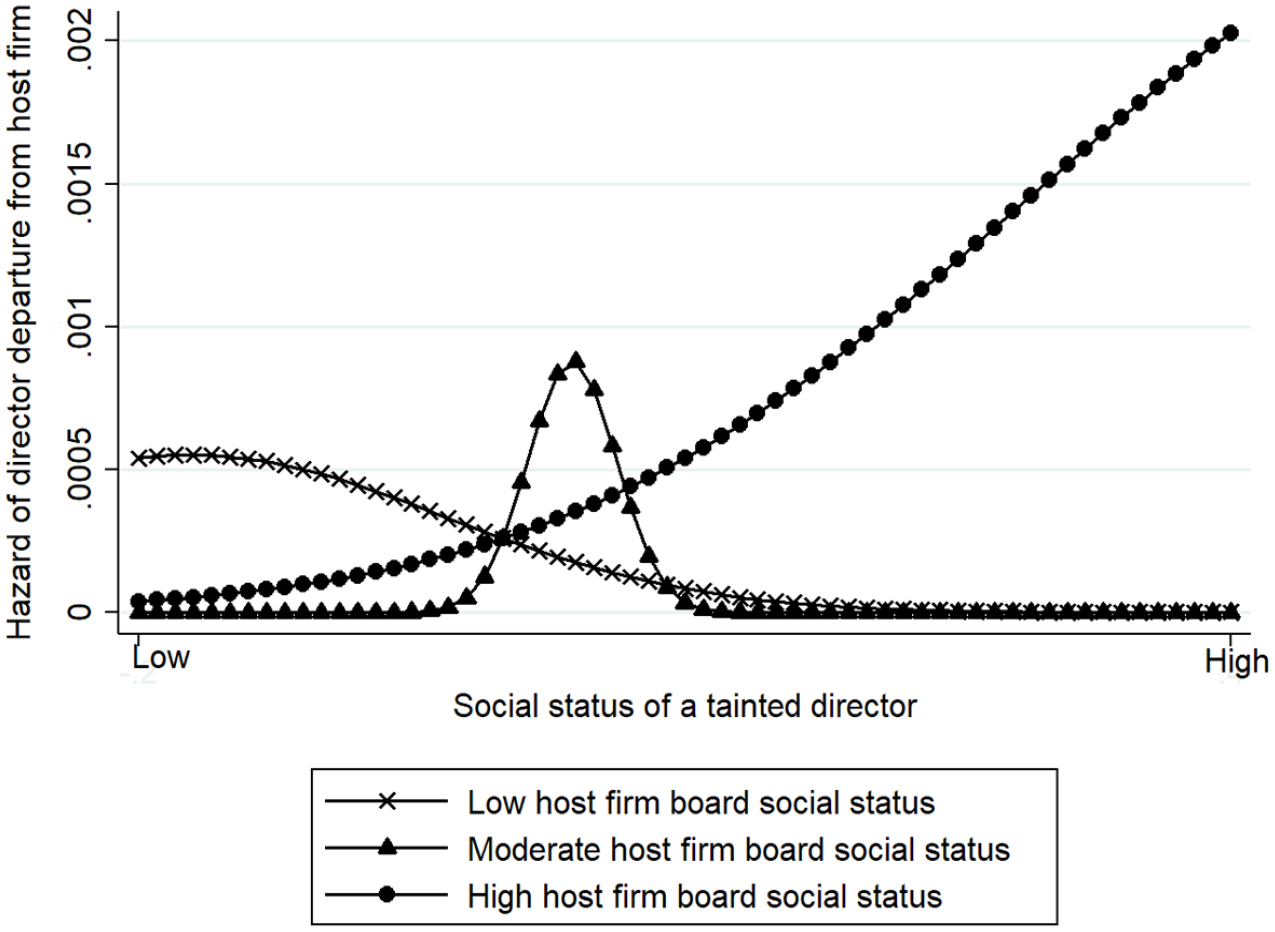

Hypothesis 3 proposes that the turning point of the inverted U–shaped effect shifts to the right when the board social status of a host firm is higher. The results in Model 6 show that the hazard ratio of the interaction between director social status and host firm board social status is 1.063 (z = 0.953, p = .341), and the hazard ratio of the interaction between the director’s social status squared term and host firm board social status is 0.809 (z = −3.884, p = .000). Figure 5 illustrates that the turning point of the inverted U shifts to the right when the board social status of a host firm is high. Thus, Hypothesis 3 is supported.

Moderating Effect of Host-Firm Board Social Status.

Robustness Tests

Alternative Measurements

To check the robustness of the findings relevant to Hypotheses 2a and 2c, we employed the number of media and analyst reports (J. Chen et al., 2016) as alternative measurements. These tests yielded stable results, confirming the robustness of the evidence for Hypotheses 2a and 2c. To test the robustness of Hypothesis 3, we adopted degree centrality, defined as the number of unique ties that an individual director had with other directors in the database by virtue of sitting on the same board together, as an alternative measure. We averaged the centrality scores of all directors on a host board to measure the board’s social status. We found robust evidence for Hypothesis 3.

Adding Directors Punished for Being Involved in Misconduct

During our observation window, 113 directors were penalized by the CSRC. Adding punished directors to the sample did not change the consistency of our results. All results are available upon reasonable request.

Discussion

Theoretical Contributions

This study contributes to the literature on business and society by providing a more nuanced understanding of the theoretical dilemma regarding the liability versus the buffer effect of social status on tainted director departures. Such a dilemma, which in this case focuses on expectancy violation and social embeddedness perspectives, may indicate gaps or contradictions in our understanding of a particular phenomenon (e.g., the role played by social status). By addressing this dilemma, we advance our knowledge in the field by providing a resolution or synthesis that helps reconcile conflicting perspectives (Cunha & Putnam, 2019; Smith & Lewis, 2011). As Smith and Lewis (2011, p. 395) stated, “[U]nderlying tensions are not only normal but, if harnessed, can be beneficial and powerful.” To this end, we enrich the organizational theory literature on this paradox by providing additional insights into this theoretical dilemma.

Recent studies have investigated expectancy violations in relation to message cueing in corporate social responsibility practices (Rim et al., 2020) and impression management (Rui & Stefanone, 2018). However, previous studies have mainly focused on the linear effect of expectancy violations on penalties following negative corporate events (Zavyalova et al., 2012). Limited research has linked the expectancy violation perspective to social status on director dismissal and reveal the curved linear effect. Although social status may magnify violation penalties for the directors of accused firms (Kang, 2008), this perspective falls short of explaining the buffer effect of tainted directors’ social status. Indeed, a key insight from the expectancy violation perspective is that social status can be a burden because the violation of high expectations leads to penalties. However, this assumption is limited, as the liability–buffer dilemma illustrates. By addressing this dilemma, we not only facilitate conversations between studies separately drawing on expectancy violations or the network-embeddedness perspective by highlighting the threshold of the expectancy violation penalty but also challenge the two perspectives’ limits and seek more fluid, reflexive, and sustainable sense-making approaches.

Our study also contributes to social network literature by integrating individuals’ network structures and career outcomes into the proposed model. Researchers have widely recognized the importance of identifying individuals and the unique behavioral features they possess in explaining their decisions and outcomes. Previous studies have investigated various individual characteristics including cognitive perception (Carnabuci & Quintane, 2023), psychological trauma (Tian et al., 2023), and gender (Brands et al., 2022). Unfortunately, this research stream has paid little attention to what occurs when individuals in a social network become tainted. In our study, we integrated social network centrality and research on tainted individuals as complementary approaches. Specifically, we explore how tainted individuals’ network centrality affects their career devaluation in host firms. Our findings suggest that a tainted director with a “go-to guy” status in the social network can maintain a high level of trust that offsets a trust violation (Stevenson & Radin, 2009). In this way, directors’ “investment in social relations” (Stevenson & Radin, 2009, p. 19) may serve as a relational asset (Ibarra & Andrews, 1993), buffering tainted directors from devaluation. Thus, we find that social network centrality leads to an inverted U–shaped effect on a tainted director’s departure, thereby enriching the current research on social network theory that integrates social network structure and individual outcomes.

Our study also enriches CG literature by revealing the boundary conditions of the threshold approach. Prior research has focused on how CG leads to responsible actions such as good CG practices, environmental corporate social responsibility, and stakeholder performance (Al-Bassam et al., 2018; Endrikat et al., 2021; Naciti et al., 2022; Post et al., 2011; Puncheva, 2008). However, CG may fail, resulting in financial misconduct. According to our findings, a host firm’s board social status and external stakeholder attention moderate the inverted-U effect such that its turning point shifts to the right because such contingencies increase the threshold of the buffer. In other words, when stakeholder attention is high, firms raise their expectations for tainted outside directors. Moreover, after a negative firm event, a tainted director’s social status is more likely to be devalued when the board’s social status of the host firm is high rather than low.

Notably, our research sheds light on the influence of two types of stakeholders—namely, those from Wall Street and Main Street—on CG practices. Prior research suggests that these two types of stakeholders typically have different preferences regarding how a firm should defend its legitimacy (Lamin & Zaheer, 2012). In contrast, our key finding is that despite the expected divergence in preferences, the moderating effect of these stakeholders’ attention consistently leads to a rightward shift in the turning point of the inverted U–shaped relationship, enhancing the optimal level of the tainted directors’ social status and preventing the directors from being dismissed from host firms. The findings imply that the attention of Wall Street and Main Street stakeholders plays an important role in shaping CG practices, suggesting that firms and directors should maintain good relationships with various stakeholder groups.

Our findings have important implications for strategic research on network-based social status. Firms must pay attention to board interlocks that may damage their reputations if they decide to retain tainted directors. Although the literature has shown how financial misconduct leads to the turnover of corporate executives (e.g., CEOs, CFOs, and COOs) and directors with bad reputations (Collins et al., 2008; Kester et al., 2013; Srinivasan, 2005), the role of elite social status remains unclear. Indeed, “the consequences of misconduct on both internal and external labor markets may be even stronger for directors than for executives, as the board is ultimately responsible, by legal definition, for organizational misconduct” (Greve et al., 2010, p. 90). It is not a forgone conclusion that the findings related to executive turnover are equally applicable to tainted outside directors. Thus, it is vital to theorize and test the extent to which host firms dismiss tainted outside directors following corporate misconduct, along with its scope conditions.

Practical Implications

The findings of this study have several practical implications. Although the board delegates most management functions to the top management, it retains the ultimate control to make decisions. Directors with high social status are expected to monitor management, ratify important decisions, establish an appropriate control system, and avoid colluding with top managers to expropriate stockholders. Research has widely acknowledged that directors’ social status is associated with career goals, including director selection (Cowen & Marcel, 2011), retention (Srinivasan, 2005), ship jumping (Jiang et al., 2017), and career success (Seibert et al., 2001). Corporate elites should understand the nature of social status once corporate misconduct occurs, as interlocking directors link accused firms to interlocked firms. Consequently, non-fraudulent host firms concerned about potential damage may have to distance themselves from tainted outside directors (Cowen & Marcel, 2011).

Corporate elites should also recognize that the assumptions inherent in the expectancy violation perspective question the premise of a buffer derived from the network-embeddedness perspective, leading to competing explanations and a dilemma in seeking to understand the effects of outside directors’ social status as a liability versus a buffer for tainted directors’ departures after misconduct. The dismissal of tainted outside directors is viewed as a negative sanction for poor performance. For example, a firm’s misconduct signals that a weak board has failed to prevent the management from committing fraud. In such a case, directors may be subject to penalties. Moreover, individual directors must consider the board’s social status. Generally, sitting on a board with a high social status can help individual directors build social connections. However, when a director is deemed tainted, the director’s social status can be compensated for, making it difficult to avoid devaluation. Finally, stakeholder expectations of good governance can make avoiding devaluation difficult.

In regard to Chinese CG practices, China’s CG mechanisms are generally considered relatively weak and incomplete; in turn, some firms may try to take advantage of these limitations and engage in financial misconduct (Tian et al., 2022). Although outside directors are supposed to warn society and shareholders about this kind of misconduct, not all directors do their duty well, and such behavior is especially likely when directors think they can leave the accused firm but continue to retain their job opportunities in other firms. However, our findings indicate that their careers can be jeopardized more broadly by affiliations with penalized firms. Thus, our findings stress the additional dangers and risks to outside directors who do not perform their jobs professionally.

Limitations and Future Research Directions

The limitations of this study provide opportunities for future research. First, our findings are based on data from one country (i.e., China), a context where informal institutions and cultural norms play a significant role in CG. In particular, guanxi (Yang & Wang, 2011; Yiu et al., 2019), mianzi (Ji et al., 2021), and beliefs in fengshui (Tsang, 2004) are integral to business operations. Guanxi, or networks of personal connections in China, often hinge on emotional bonds and are crucial facilitators of cooperative activities (Yang & Wang, 2011). Mianzi, which represents social prestige and self-worth, is a pivotal aspect of CG that influences business interactions and consumer behavior (Christian & Wang, 2022). In addition, fengshui, the practice of arranging physical spaces to achieve harmony with the environment, is believed to have positive outcomes for businesses (Tsang, 2004). However, it remains uncertain whether these findings can be generalized beyond China. Variations in the levels of the directors’ social status and stakeholder perceptions of adverse events across different national contexts could lead to dynamics distinct from those identified in our study.

Second, although we theorized how financial misconduct affects the departure of tainted outside directors, we did not include other types of violations in our model. Although financial misconduct is the most widely and frequently occurring type of corporate wrongdoing (e.g., Arthaud-Day et al., 2006; Yiu et al., 2014, 2019), we encourage future research to include other types of corporate misconduct and examine the robustness of our findings across various types of negative events.

Third, we focused only on the director’s departure from the host firm and did not specify why the director left the host firm. Future research could use surveys to collect firsthand data from directors to verify the main findings.

In conclusion, this study addresses the dilemma of whether social status benefits or jeopardizes tainted directors’ careers. By integrating the network embeddedness and expectancy violation perspectives to clarify directors’ relative dominance in terms of social status, we identified an inverted U–shaped relationship between social status and the departure of tainted outside directors from host firms by using a threshold approach. Moreover, the host firm’s board social status and external stakeholder attention moderate the inverted-U effect such that its turning point shifts to the right because such contingencies increase the threshold of the buffer. Our threshold approach provides fresh insights compared to prior monatomic studies that were not sufficient to understand the aforementioned dilemma. We hope that our theoretical framework and findings will inspire future research to seek a better understanding of directors’ social status.

Footnotes

Acknowledgements

The authors express their sincere gratitude to the editor Dr. Johanne Grosvold and the two anonymous reviewers for their invaluable feedback and insightful comments, which have greatly contributed to improving this manuscript.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors disclose and acknowledge the receipt of funding from the Fundamental Research Funds for the Central Universities (22120230357) and the National Science Foundation of China (grant numbers 72372102 and 72342026).