Abstract

Capturing carbon is increasingly critical to keeping the Paris Agreement within reach. However, developing and scaling solutions that permanently remove CO2 from the atmosphere represents a major technological and societal challenge. In this context, the role of incumbents in shaping the trajectory of emerging technologies remains unclear and often ambiguous. Adopting a competence-based perspective centered on technological coherence, this article examines the role of fossil fuel companies in the evolving carbon sequestration industry, contrasting carbon capture and storage—a technology that captures CO2 from emission sources—with direct air capture (DAC), a novel approach that directly removes carbon from ambient air. Using International Energy Agency data on carbon capture projects combined with corporate, financial, and patent records, we reconstruct and analyze the global network of organizations active in the sector. Results show that fossil fuel companies are central players in the global carbon capture landscape, leveraging established assets and expertise, but are largely disconnected from emerging DAC projects. This supports the view that DAC is a competence-destroying innovation for the fossil fuel industry, involving substantial process and product discontinuities, as further confirmed by patent analysis, which reports a substantial distance between incumbents’ and DAC-related technical knowledge. In contexts characterized by high entry barriers, technological coherence—beyond complementary assets and societal value—appears crucial for assessing how incumbents engage with technologies addressing grand challenges. Jointly monitoring collaboration networks and innovation activities within incumbent industries is therefore essential for understanding how new technologies may (or may not) contribute to sustainability transitions.

Keywords

Introduction

Climate change is one of the most pressing societal issues of the century. The need to phase out fossil fuels and decarbonize our economies presents significant technological and organizational challenges for both firms and society as a whole (Nyberg, Ferns, et al., 2022). In its latest report, the Intergovernmental Panel on Climate Change (IPCC) emphasized that carbon dioxide removal (CDR) will be necessary for our decarbonization strategy toward net-zero emissions (IPCC, 2022). In other words, meeting the Paris Agreement target (i.e., keeping the increase in global temperature well below 2°C) requires both a fast commitment to reducing emissions and removing a non-negligible amount of the CO2 already present in the atmosphere through the development and upscaling of negative emissions technologies (K. Anderson & Peters, 2016).

The development of these technologies, however, does not occur in a vacuum, but is shaped by the strategic choices and institutional power of different organizations operating within various sectors and simultaneously pursuing multiple goals. On the one hand, firms can leverage new technologies to address grand challenges, such as climate change, thereby contributing to sustainable growth (den Hond & Moser, 2023; George et al., 2021). On the other hand, they often possess vested interests that position them as gatekeepers of change, pushing for their business models without altering production practices or strategically delaying the diffusion of disruptive technology (Panwar, 2023). Indeed, carbon removal technologies are not merely technical fixes but illustrative cases of how new technologies can simultaneously advance the social good while generating tensions with organizations’ long-term sustainability commitments and profit imperatives, with significant implications for policy, societal well-being, and climate outcomes (Smith & Levis, 2011).

The fossil fuel industry, in particular, has responded to growing criticism from global climate movements with a series of strategies ranging from denial and delay to lobbying (e.g., for initiatives related to carbon capture and storage [CCS] and “green coal”) and controlled engagement (Boon, 2019; Markusson et al., 2012; Schifeling & Hoffman, 2019; Ferns et al., 2019). This suggests that climate technologies are not neutral tools, but innovations whose trajectories are driven by specific organizational interests, raising concerns about whether these paths enhance or undermine societal well-being in the face of grand challenges. Consequently, understanding how incumbents and new entrants affect the emergence, development, and deployment of essential CDR technologies is pivotal to informing policy and shaping public perception.

Carbon removal may work through a variety of channels, ranging from nature-based solutions such as afforestation and reforestation to technology-based methods that filter and isolate CO2 molecules. Although nature-based solutions currently account for the majority of total removals, their potential for rapid and permanent carbon sequestration is limited. While capturing CO2 from the atmosphere is not entirely a novel idea, and solutions for carbon sequestration at the emissions site have been already adopted by fossil fuel companies (see Carton et al., 2020), removing CO2 from the ambient air, where the concentration is much lower, represents a fundamentally different challenge (SCDR, 2024) that introduces both technical hurdles and new market opportunities for existing industries (Beck, 2020). Although both approaches can be considered as “green” technologies—as they have the potential to reduce emissions and mitigate climate change—in what follows, we will distinguish between “conventional” or “point-source” CCS and direct air capture (DAC), which consists of the actual removal of CO2 from ambient air (Beck, 2020; Shayegh et al., 2021). Such a distinction is critical because, whereas CCS technologies build upon the competencies, skills, and capabilities already embedded within the fossil fuel industry’s knowledge base, DAC constitutes a disruptive and potentially competence-destroying technological breakthrough. Importantly, this technological distinction also maps onto different societal and environmental implications: CCS is closely aligned with incumbent-led “managed decarbonization”, whereas DAC has the potential to enable more independent and verifiable negative emissions.

As of today, negative emissions solutions are in the early stages of development, thus characterized by high costs and limited scalability. While both necessary and promising, a full-scale commitment to and reliance on carbon removal technologies might further delay emissions-reduction efforts, paradoxically shifting the purpose of such technologies from a potential insurance against mitigation failures to a source of further resistance to urgent climate actions (Fuss et al. 2014). Indeed, interest in carbon removal methods has grown significantly in recent years, not only among policymakers, the scientific community, and philanthropic foundations, but also across several industries, particularly within high-emitting sectors (Mac Dowell et al., 2022). Yet a fundamental question remains: which types of organizations—established incumbents or new entrants—will develop such technologies, at what scale and pace, and toward which economic and societal goals? Equally important is a related question: under what conditions do new technologies for climate mitigation genuinely advance social well-being, rather than primarily protect incumbent interests?

Against this backdrop, this study examines the evolving landscape of carbon removal technologies and identifies the leading players shaping the development and deployment of CCS and DAC technologies (Nyberg, Ferns, et al., 2022). Understanding the fossil fuel industry’s response to the technological discontinuities introduced by CCS and DAC is crucial, given its central role in the green transition. High-emitting firms may seek to obscure emissions through superficial CO₂ removal projects while continuing fossil fuel use, whereas corporations genuinely committed to carbon management must advocate regulatory reforms that enable ambitious emission-reduction and CO₂ removal strategies. Such efforts reduce the risk of being outcompeted by firms with lower environmental standards (Panwar, 2023) and allow firms to capitalize on emerging technological opportunities. Yet, transitioning organizations face a stability–change paradox (Hahn et al., 2014, 2015; Rosales et al., 2022), balancing existing competencies with transformative change (Farjoun, 2010). Sustainability-oriented partnerships appear critical to resolving this paradox and supporting successful transitions (Dzhengiz et al., 2023).

First, we map the global development of CCS and DAC technologies using network science techniques to disentangle the relationships between firms, universities, research centers, and public agencies involved in carbon capture, utilization and storage projects (Grandori & Soda, 1995; Jacobsen et al., 2022). Then, we examine how incumbent firms in the fossil fuel industry have faced the emergence of CCS and DAC, building on a competence-based view of sectoral dynamics induced by technological discontinuities (Abernathy & Clark, 1985; P. Anderson & Tushman, 1990; Bergek et al., 2013; Utterback & Suárez, 1993). In principle, technological discontinuities can intensify technological competition or even lead to the complete breakdown of competitive patterns, resulting in the demise of established firms. The ability of incumbent firms to react to the emergence of new technologies and different competitive conditions depends both on industry characteristics (e.g., entry barriers, scale intensity, appropriability conditions; see Malerba, 2002; Pavitt, 1984) and on the nature of the technological discontinuity itself (P. Anderson & Tushman, 1990). When discontinuity builds upon rather than threatens incumbents’ competencies and routines, firms tend to engage with the new technology and contribute to its development—especially in highly concentrated and scale-intensive Schumpeter Mark II (Schumpeter, 1942) industries. Conversely, when new technologies radically transform the knowledge and skills required to produce and operate, incumbents often avoid direct entry. This does not preclude them from capturing technological opportunities, often through acquisitions of technology-based firms in contexts of high entry costs or technological complementarities (Andersson & Xiao, 2016). As socio-technical transitions research highlights, incumbents can respond to emerging technologies by reconfiguring existing systems, resisting disruption, or blocking technological change (Geels & Schot, 2007; Cunningham et al., 2021; Sovacool et al., 2023).

To detect the role of key actors in the carbon capture sector, we compile a global dataset on 916 large-scale carbon capture, utilization and storage projects by leveraging and extending the most recent data assembled by the International Energy Agency (IEA). We then construct a collaboration network comprising 679 stakeholders involved in multi-partner projects and retrieve additional firm-level financial and patent information from Bureau van Dijk (BvD) Orbis, Orbis Intellectual Property, and EPO Patstat. By integrating these different data sources, we identify fossil fuel companies (i.e., oil and gas firms) and investigate their involvement in CCS and DAC projects, as well as the technological proximity between their patent portfolios and DAC technologies. To the best of our knowledge, this is the first study that combines an analysis of the organizations involved in the carbon capture project network with patent data, assessing the role of fossil fuel firms in the development of the carbon removal industry.

The article provides three key contributions. First, it offers a conceptual distinction between CCS and DAC based on their compatibility with incumbents’ (i.e., fossil fuel companies) capabilities, framing CCS as a competence-enhancing innovation and DAC as a competence-destroying innovation. Second, it provides empirical evidence that fossil fuel firms are structurally embedded in the carbon capture collaboration network but largely disconnected from DAC projects. Indeed, we highlight the relatively limited participation of fossil fuel companies in competence-destroying projects, suggesting that the DAC technological trajectory may develop independently of the fossil fuel industry’s influence. Third, it presents quantitative evidence of a significant technological distance between fossil fuel firms and DAC-related actors, showing that incumbents are not currently involved in collaborations that would facilitate skill acquisition or organizational learning in DAC. Taken together, these findings advance a competence-based perspective on incumbents’ responses to technological discontinuities. Building on research on competence-enhancing and competence-destroying change (Henderson & Clark, 1990; Tushman & Anderson, 1986) and on heterogeneous incumbent adaptation (Bergek et al., 2013; Eggers & Park, 2018; Tripsas, 1997a, 1997b), we argue that incumbents’ engagement with sustainability-oriented and societally-demanded technological shifts still depends on the coherence between emerging technological paradigms and their existing knowledge base. Rather than uniformly resisting paradigm shifts, incumbent firms selectively adapt independently of complementary assets and resources (Eggers & Park, 2018). Indeed, they tend to engage early and with increasing weight when discontinuities build on established competences, but remain reluctant to enter when new technologies feature different capabilities from the incumbents’ core even if complementary assets and resources are present (i.e., those related to the transport and long-term storage of CO2).

More broadly, the case of carbon removal highlights how emerging climate technologies are simultaneously technical, organizational, and political phenomena. Their development does not depend solely on scientific and technological feasibility, but also on how different types of organizations mobilize resources, navigate tensions, and reconcile competing economic and societal objectives (Battilana et al., 2015). As such, understanding carbon removal technologies requires a multidisciplinary perspective to investigate how technological change interacts with firms’ strategies, industry structures, and broader societal goals (Fernandes et al., 2021). By examining CCS and DAC through this lens, this study sheds light on how novel technologies intended to address grand environmental challenges can generate new forms of coordination, conflict, and transformation across different organizations (Brammer et al., 2022; den Hond & Moser, 2023).

The remainder of the article is organized as follows. Section “The Carbon Removal Industry: Diverging Technologies and Emerging Pathways” introduces the context of our analysis from a multidisciplinary perspective. Section “Theoretical Background” presents the theoretical background and our main hypotheses. Section “Data and Methods” describes the data and methods. Section “Results” presents the results. Finally, section “Discussion and Conclusions” offers a critical discussion and concludes the article.

The Carbon Removal Industry: Diverging Technologies and Emerging Pathways

The increasing urgency of climate change mitigation has brought renewed attention to carbon removal technologies. Among these, CCS and DAC have emerged as two leading technical pathways for reducing atmospheric CO2 concentrations. While both aim to reduce net greenhouse gas emissions, they fundamentally differ in technological requirements, maturity, industrial structure, and key actors involved.

CCS and DAC: Similarities and Differences

CCS—also often referred to as point-source capture or Carbon Capture, Utilization and Storage (CCUS) when utilization is included—captures CO2 at the point of emission from industrial facilities or fossil fuel power plants. These technologies are commercially viable and already in use, particularly in natural gas processing, where many incumbent energy firms consider them technologically “adjacent” to their core operations. As such, the CCS industry has developed around existing infrastructures, including pipelines, geological storage reservoirs, and chemical separation technologies, with extensive involvement from fossil fuel firms (Beck, 2020; IEA, 2024). These features make CCS an exemplary case of competence-enhancing innovation, enabling oil and gas companies to extend their technological and infrastructural capabilities into carbon mitigation.

DAC, by contrast, is a more radical technological approach that involves extracting CO2 directly from the ambient atmosphere. It belongs to the set of strategies that could lead to net-negative emissions, that is, allowing us to remove more carbon dioxide than is emitted. As of today, however, DAC is typically more energy-intensive and costly, as its technological development requires further innovation in materials science (e.g., sorbents), modular plant design, and integration with renewable energy systems (McQueen et al., 2021; Sanz-Pérez et al., 2016). All this makes DAC less compatible with the technical routines and infrastructure typical of the fossil fuel industry. Indeed, its development has largely been led by new entrants, often university spin-offs or venture-backed firms with strong ties to public research and philanthropy. This technological and organizational separation positions DAC as a competence-destroying innovation, with the potential to challenge the incumbents’ interests if scaled independently.

While both CCS and DAC are currently operating far below the levels needed for meaningful climate impact, their deployment trajectories and organizational configurations differ substantially. On the one hand, CCS has historically advanced—though with limited success (see Martin-Roberts et al., 2021)—through large-scale industrial projects driven by incumbents and often supported by policy incentives aimed at industrial decarbonization (Oh & Al-Juaied, 2024). DAC, on the other hand, is still in the early stages of commercialization, with only a handful of operational plants active globally and a heavy reliance on non-market funding, including corporate advanced purchase agreements (e.g., Frontier), state innovation programs, and carbon removal credit buyers.

The Different Fate of DAC First Movers: Carbon Engineering Versus Climeworks

The industrial and strategic divergence between CCS and DAC is echoed within the DAC sector itself. A comparison between two leading players—Carbon Engineering and Climeworks—illustrates the distinct developmental pathways emerging in the industry. Both companies were founded in 2009 with strong academic roots, but they have pursued fundamentally different technological goals, funding models, and partnership strategies (see also Figure B.7 in the Supplemental Appendix).

Carbon Engineering (CE), a Canadian company founded by academic physicist David Keith (formerly at Harvard, now a professor at the University of Chicago), has focused on developing DAC technologies to convert captured CO2 into synthetic fuels (so-called “Air-to-Fuel”). This approach naturally aligns with the business models and infrastructure of the fossil fuel sector. CE’s early partnerships with Occidental Petroleum and 1PointFive, and its eventual acquisition by Occidental in 2023, suggest a path for DAC’s strategic integration into oil and gas companies’ core operations—potentially enabling these firms to extend their value chains into carbon management while preserving their core competencies and asset bases. To some extent, CE’s trajectory represents a fossil-aligned pathway for DAC, where the technology is absorbed into incumbents’ structures through investment and acquisition, making it a form of “green diversification” rather than technological disruption.

Climeworks, a Swiss company spun out of ETH Zurich, has instead pursued a model focused on permanent CO2 removal and mineralization, in partnership with non-fossil actors such as Carbfix, and more detached from the core interests of the oil and gas industry. For instance, its projects in Iceland, including the Orca and Mammoth plants, reflect a commitment to direct, verifiable removals integrated into renewable energy systems. Additionally, Climeworks’ funding strategy has emphasized institutional capital, public-private research collaborations, and the voluntary carbon market, culminating in the largest-ever DAC funding round in 2022. This model represents a clean-slate pathway in which DAC evolves as a standalone industry aligned with long-term environmental integrity, potentially competing with or displacing fossil interests.

These two models capture the strategic ambiguity currently present in DAC’s evolution. Will the industry be shaped and dominated by the legacy of fossil fuel players leveraging their infrastructure and capital to internalize DAC into their existing business models? Or will DAC emerge as a genuinely disruptive technology, developed independently and governed by new market norms, policy instruments, and actors?

Sectoral Dynamics, Strategic Ambiguity, and the Role of Fossil Fuel Firms

The diverging trajectories of Carbon Engineering and Climeworks also reflect deeper tensions in the broader decarbonization landscape, particularly the contested role of fossil fuel incumbents.

Historically, fossil fuel companies have demonstrated the capacity to shape the climate policy agenda in ways that maintain the legitimacy of the oil and gas industry. Boon (2019) documents how firms have sought to position themselves as necessary actors in any pragmatic transition, emphasizing “realistic” solutions that accommodate the continued use of fossil fuels. Within this framework, CCS has emerged as the industry’s preferred mitigation strategy, enabling the continued use of fossil fuels while ostensibly reducing emissions. Unlike renewables or electrification, CCS does not threaten the underlying asset base of fossil fuel firms, nor does it require major shifts in energy infrastructure or demand.

Building on this logic, Ferns & Amaeshi (2021) argue that fossil fuel firms engage in organizational hypocrisy—symbolically aligning with climate action while materially obstructing transformative change. They highlight how oil and gas companies may simultaneously endorse the Paris Agreement and invest in decarbonization while continuing to lobby against binding regulations and promoting incremental or “technically neutral” policies. In this context, support for CCS is often just a delaying tactic: a means to claim climate leadership without challenging the economic and political power of fossil capital.

This strategic ambiguity appears evident in how firms promote CCS as a “low regret” option, pushing for public subsidies and regulatory support for its deployment (Ferns & Amaeshi, 2021; Markusson et al., 2012). Yet, this often happens without a credible commitment to phasing down fossil fuel production (Gunderson et al., 2020), and instead with an emphasis on using captured CO2 for enhanced oil recovery (EOR; as the Carbon Engineering case has proven)—reinforcing fossil dependence rather than undermining it. As Boon (2019) further notes, the fossil fuel industry has historically adapted to new regulatory landscapes not by changing its core product, but by reframing its relevance to societal goals, including energy security, economic development, and now, decarbonization. A key example of such an approach is rooted in the industry-promoted solution to emission mitigation through forms of “clean carbon,” eventually achieved through CCS (Nyberg, Wright, & Bowden, 2022).

In the emerging carbon removal sector, this legacy creates tension: CCS can be seen as a tool of climate stabilization or as a mechanism for industrial entrenchment. The involvement of fossil fuel companies in DAC technologies—especially when tied to utilization pathways such as synthetic fuels—raises similar concerns that the technology could legitimize continued fossil emissions rather than drive structural change.

This tension underscores the importance of disaggregating CCS and DAC not only technologically but politically and institutionally. While both can play a role in the net-zero transition, their deployment pathways, actor coalitions, and governance implications differ sharply. CCS, as currently promoted by fossil fuel incumbents, is often linked to a “managed decarbonization” model in which hydrocarbon production is maintained under the guise of climate responsibility. DAC, especially when led by independent firms pursuing permanent removals, has the potential to challenge this model—but only if it is supported by governance structures that reward negative emissions outcomes and prevent co-optation.

The future of carbon removal technologies—and the broader decarbonization agenda—depends not just on technical innovation, but also on who governs them, how they are financed, and what role they are expected to play in the energy transition. The cases of Carbon Engineering and Climeworks illustrate divergent approaches: one integrates with existing energy infrastructure, the other pursues a model centered on dedicated carbon removal systems.

Theoretical Background

Industry Structure, Discontinuities, and Entry

As technological innovation increasingly creates markets for new products and services, keeping up with a changing technological landscape is critical for a company’s long-term survival. As emphasized by Schumpeter (1942), a process of “creative destruction” may unfold, eventually leading to the demise of established firms in favor of new entrants, if incumbents fail to react promptly. To survive, firms must respond to the newly created markets or niches. The ability to respond to a new market is part of a class of organizational abilities called “dynamic capabilities.” Eisenhardt and Martin (2000, p. 1107) define dynamic capabilities as “organizational and strategic routines by which firms achieve new resource configurations as markets emerge.” However, according to Teece et al. (1997), these capabilities both constrain and enable a firm’s ability to change, and they must be built through experience rather than acquired through market transactions.

Several studies suggest that incumbent firms often fail to respond to discontinuous technological changes because their experience leads to routinization and organizational inertia. Nelson and Winter (1982) provided the foundational argument according to which firms develop routines as repositories of experience, but these same routines can create rigidity and limit an organization’s ability to react to a changing environment. In line with this view, experience fosters habitual routines that reinforce existing practices, increasing rigidity (Hannan & Freeman, 1984; Leonard-Barton, 1992; Tripsas & Gavetti, 2000) and impeding adaptation (Gersick, 1989; Gersick & Hackman, 1990; Henderson & Clark, 1990; Tushman & Anderson, 1986). Further, Teece et al. (1997, p. 520) and Teece (2007) suggest that incumbents frequently fail to enter new market niches due to a “mismatch [. . .] between the set of organizational processes needed to support the conventional product/service and the requirements of the new market.” However, not all innovations, technological discontinuities, and new markets are alike (Dosi, 1988; Dosi & Nelson, 2010; Breschi et al., 2000).

Some innovations destroy existing technological competencies and capabilities, while others refine and improve them (Abernathy & Clark, 1985). Tushman and Anderson (1986) label these types of innovation as “competence-destroying” and “competence-enhancing,” respectively. Such dichotomy has proved effective in formalizing how organizations face and react to technological discontinuities across a variety of industries and episodes, ranging from new drug discoveries to digitalization and AI-centered products (McKinley, 2022; Paschen et al., 2020; Pemer & Werr, 2023). Competence-enhancing discontinuities involve consistent price and/or performance improvements that build on existing knowledge and skills (Tushman & Anderson, 1986). They refine and extend an established product design, typically by improving individual components (Henderson & Clark, 1990). These discontinuities are generally introduced by incumbent firms (Gilbert, 2012) and tend to reinforce their competitive positions by allowing them to exploit their existing competencies and increase barriers to entry (Abernathy & Clark, 1985; Henderson & Clark, 1990). It is rare for new firms to enter an industry following a competence-enhancing discontinuous innovation (Maine & Garnsey, 2006). Such discontinuities characterize the typical patterns of innovations in Schumpeter Mark II regimes (Breschi et al., 2000; Malerba & Orsenigo, 1996), which feature high concentration, dominance of incumbents, persistent ranking of innovators, and high entry barriers.

In contrast, competence-destroying discontinuities fundamentally change the knowledge and skills required to develop and produce a product, making existing knowledge obsolete (Tushman & Anderson, 1986). These innovations are often introduced by new entrants and tend to lower the industry barriers to entry. Generally, new knowledge comes from outside the industry and the sectoral system of innovation (Malerba, 2002). During these discontinuities, previous competence-based competitive advantages are eliminated as existing competencies become obsolete and new technological paradigms emerge (Dosi, 1982). In such cases, industry incumbents are often locked into their previous successes within the old technological paradigm (Tushman & Anderson, 1986); their existing skills, abilities, and operational methods constrain their actions and make it difficult to respond effectively (Abernathy & Clark, 1985; Leonard-Barton, 1992; Macher & Richman, 2004).

More recently, Paschen et al. (2020) developed a framework to analyze innovation typologies and guide managers in addressing technological discontinuities. Their model combines two dimensions: (a) the innovation’s boundary—product or process—and (b) its impact on organizational competencies—either competence-enhancing or competence-destroying. This taxonomy clarifies which capabilities and skills are most affected by technological change.

However, it is worth stressing that competence-enhancing and competence-destroying innovations should not be seen as fully separate. Pemer and Werr (2023) studied a high-skills industry (the professional service industry), showing that both innovations could complement each other through a process of “competence expansion” consisting of three overlapping sub-processes—namely skill acquisition, skill dissemination, and skill integration. In particular, expanding the knowledge base—especially through hiring and internal training—is considered a prerequisite for the overall process.

The Fossil Fuel Industry in the Development and Deployment of CCS and DAC

Our article focuses on the fossil fuel industry, an established sector characterized by considerable stability and concentration, significant market power, and high entry barriers. According to Pavitt’s classification, the extractive industry falls into the scale-intensive category. In these industries, economies of scale are relevant, and production processes are characterized by a certain rigidity, leading to incremental technological change driven by large incumbents, often through their suppliers. Consistently, the fossil fuel industry typically follows a Schumpeterian Mark II pattern of innovation (Maleki et al., 2016), where high cumulativeness and appropriability conditions create significant technological barriers to entry for new firms. Productivity growth in this type of market stems mainly from the continuous accumulation of knowledge by well-established, oligopolistic innovators (Breschi et al., 2000; Castellacci & Zheng, 2010; Dosi & Nelson, 2010). In this context, two main sources of knowledge drive innovation and technological discontinuities (Pavitt, 1984). The first source lies within production engineering departments, which help identify and address technical imbalances and bottlenecks typical of large-scale, interdependent systems, thereby improving productivity. Over time, these departments also acquire the capability to specify or design new equipment that enhances performance. The second major source of innovation in production-intensive firms is represented by the relatively small and specialized suppliers that provide equipment and instrumentation, with whom incumbents typically have a close and complementary relationship (Pavitt, 1984; Sánchez & Hartlieb, 2020). This setting motivates our choice to focus on the network of project partners with whom fossil fuel firms engage when operating carbon capture, storage, or utilization.

As mentioned in section “The Carbon Removal Industry: Diverging Technologies and Emerging Pathways,” point-source CCS—capturing CO2 from industrial and power plants—is commercially viable and deployment-ready (Beck, 2020). These technologies are integrated systems that have gained momentum over the last decade, opening up new opportunities and markets. First, they capture the CO2 generated by the processing of chemicals and gases (Beck, 2020), then either reuse it or store it permanently. Utilization involves various processes and chemical reactions that convert CO2 into a range of products, including chemicals, fuels, mineral carbonation, durable materials, and EOR (Chauvy & De Weireld, 2020; Turakulov et al., 2024). In contrast, storage technologies allow for the permanent sequestration of CO2 in underground geological reservoirs. Given these features, the emergence of CCS technologies can be seen as competence-enhancing discontinuities within the fossil fuel and extraction industry. They adapt, refine, and extend well-established industry processes. In fact, the majority of large-scale CCS facilities in operation in 2020 were applied to natural gas processing. Thus, we hypothesize that industry incumbents are systematically involved in projects leading to the operationalization of CCS technologies.

As outlined in the theoretical discussion above, competence-enhancing discontinuities tend to reinforce incumbents’ competitive position by strengthening their existing capabilities and infrastructures (Gilbert, 2012). In this light, developments of “point” CCS technologies could be seen as competence-enhancing process innovations (Paschen et al., 2020), as they improve internal processes leading to substantially greater efficiency—potentially reaching zero emissions while operating the same facility and using the same fuel. Consequently, such innovations are highly sought after by incumbents.

While early-stage carbon sequestration projects targeted (relatively) easier-to-capture emission sources, projects further along the energy transition need to focus on hard-to-abate sectors, where capture is both more expensive and challenging to manage. Removing CO2 from the atmosphere (or from the ocean) is technologically challenging due to the difficulty of filtering molecules from low-concentration environments and the significant use of costly inputs, such as electricity and water. For this reason, DAC remains technologically immature (SCDR, 2024; Tripodi et al., 2024) and is currently being developed primarily by a few university spin-offs, such as Carbon Engineering and Climeworks. The emergence of DAC technologies, therefore, represents a competence-destroying discontinuity that requires distinct knowledge and skills. Further, while simultaneously creating a new market for permanent removals, where fossil fuel firms have traditionally not operated, it is offering new business opportunities. Indeed, as mentioned above, while traditional models of carbon capture, such as pre-combustion and post-combustion CO2 capture from large point sources, can slow the rise in atmospheric CO2 concentration, DAC presents a remarkably different challenge (Sanz-Pérez et al., 2016). In more detail, the last 15 years have witnessed a significant increase in the use of chemical sorbents cycled through sorption and desorption processes for CO2 removal from ultra-dilute gases, such as air. However, “it is concluded that there are many new materials that could play a role in emerging DAC technologies. These materials need to be further investigated and developed with a practical sorbent–air contacting process in mind if society is to make rapid progress in deploying DAC as a means of mitigating climate change” (Sanz-Pérez et al., 2016).

These kinds of competence-destroying innovations are typically introduced by new entrants, while industry incumbents tend to be less prepared to seize new opportunities due to consolidated routines, the burden of previous successes with the older technological paradigm, and more constraining investor expectations (Leonard-Barton, 1992; Macher & Richman, 2004). Building on these arguments, we formulate our second hypothesis.

However, the recent surge in media coverage and policy support for DAC methods (and carbon capture initiatives more in general; see Beck 2020; SCDR, 2024; Tripodi et al., 2024), as well as a clear complementary expertise for the eventual transport and storage of liquified or gasified CO2, inevitably made the market for removals very appealing to fossil fuel companies. As a stark example, Occidental Petroleum–one of the largest US oil companies–acquired Carbon Engineering for 1.1 billion USD in 2023. Such acquisitions are anything but unusual, especially in scale-intensive and Schumpeter Mark II industries. The acquisition of a small innovative firm is a classic means of entering a new and unrelated market. Yip (1982) suggests that an “acquisition entry” occurs when an existing competitor is acquired by a firm not previously competing in that market. The acquirer typically intends to use the acquired business as a base for expansion, rather than merely holding it as a portfolio investment. High barriers of entry have been consistently reported as a primary factor facilitating this strategy (Harzing, 2002; Lee & Lieberman, 2010; Yip, 1982). Furthermore, new technology-based firms are more likely to be acquired in market contexts where entry costs are high, access to finance is constrained, and incumbents possess valuable complementary capabilities and resources (Andersson & Xiao, 2016). Taken together, these observations lead to our third hypothesis.

The competence-destroying nature of DAC makes entry by acquisition a more feasible strategy for fossil fuel firms. Though the role that DAC and “point-source” CCS technologies share in the positioning of oil and gas firms as necessary actors in any pragmatic decarbonization process could call for both their direct and indirect entry into the DAC market (see Boon, 2019; Nyberg, Wright, & Bowden, 2022; Wright & Nyberg, 2024).

Data and Methods

Data

To quantitatively test our hypotheses, we assemble the first systematic dataset encompassing carbon capture projects, the organizations involved, and firm-level financial and patent information. To this end, we combine four different data sources: information on industrial carbon capture projects from the IEA, firm-level data from the BvD Orbis database, and patent data from both Orbis Intellectual Property and EPO PATSTAT. First, we inspect the landscape of collaborations in the development and deployment of large-scale carbon removal facilities by leveraging the IEA’s CCUS Projects Database (IEA, 2024), which encompasses 916 CO2 capture, transport, storage, and utilization projects that have been commissioned or are in the planning stages globally.

This comprehensive database includes projects commissioned from the 1990s to February 2024. To be included, projects must have an announced capacity exceeding 100,000 tons per year (or 1,000 tons per year for DAC facilities). The database prioritizes projects with a clear emissions reduction scope, excluding those related to CO2 capture for utilization pathways with low climate benefits (e.g., food and beverages), conventional industrial processes (e.g., internal use for urea production), and the use of naturally occurring CO2 for EOR.

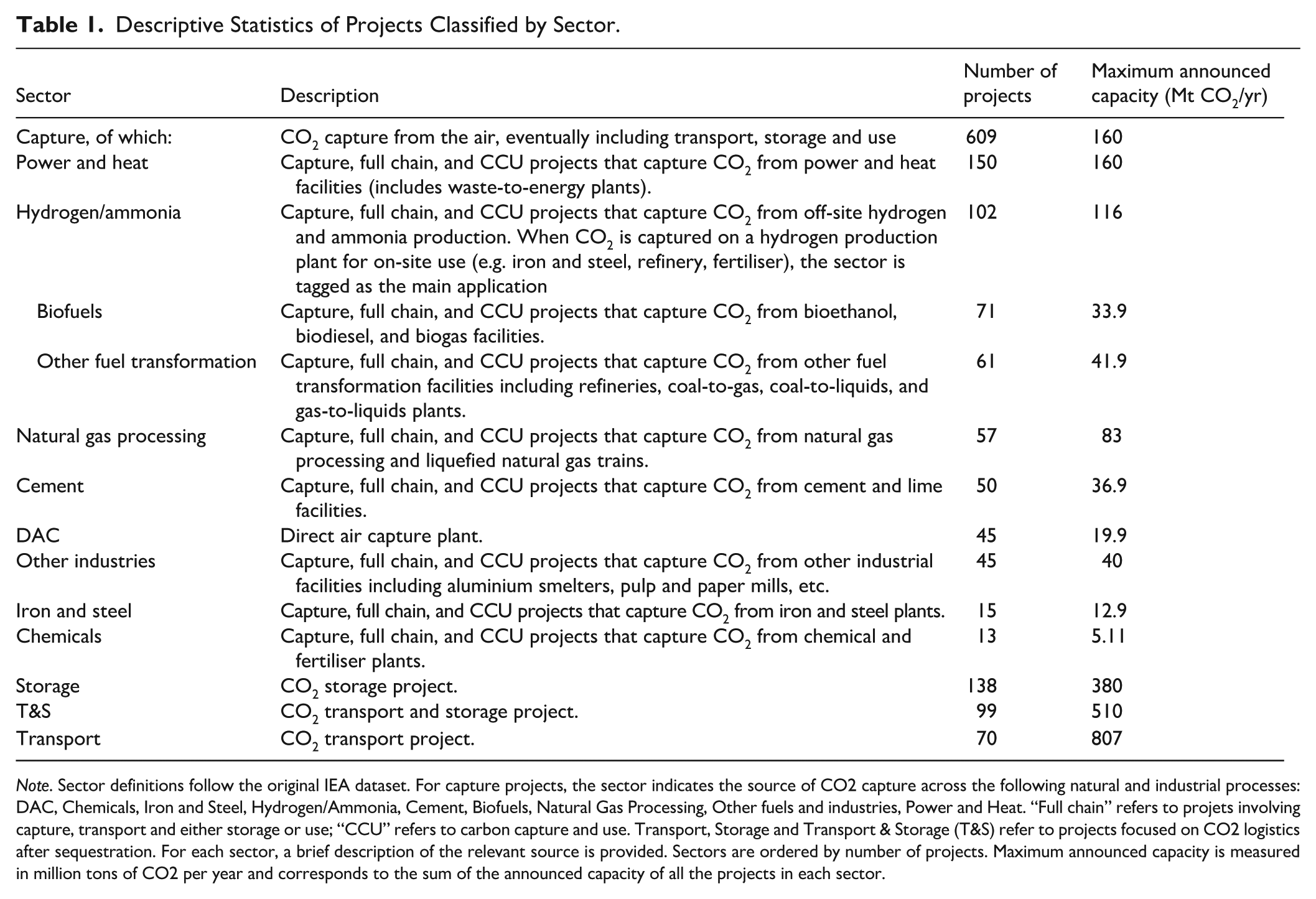

The database categorizes projects by sector, defined as the source of CO2 capture. In Table 1, we report the number of projects belonging to each sector, the maximum quantity of carbon dioxide sequestered (per year), and a brief description of the respective source of capture. Since the large majority of projects begin after 2010 (see Figure 1), our analysis covers the 2010 to 2024 time window. As projects on DAC appear for the first time in 2019, for DAC-specific analysis, we focus on the period from 2019 to 2024.

Descriptive Statistics of Projects Classified by Sector.

Note. Sector definitions follow the original IEA dataset. For capture projects, the sector indicates the source of CO2 capture across the following natural and industrial processes: DAC, Chemicals, Iron and Steel, Hydrogen/Ammonia, Cement, Biofuels, Natural Gas Processing, Other fuels and industries, Power and Heat. “Full chain” refers to projets involving capture, transport and either storage or use; “CCU” refers to carbon capture and use. Transport, Storage and Transport & Storage (T&S) refer to projects focused on CO2 logistics after sequestration. For each sector, a brief description of the relevant source is provided. Sectors are ordered by number of projects. Maximum announced capacity is measured in million tons of CO2 per year and corresponds to the sum of the announced capacity of all the projects in each sector.

Geographic and Temporal Distribution of Carbon Capture Projects.

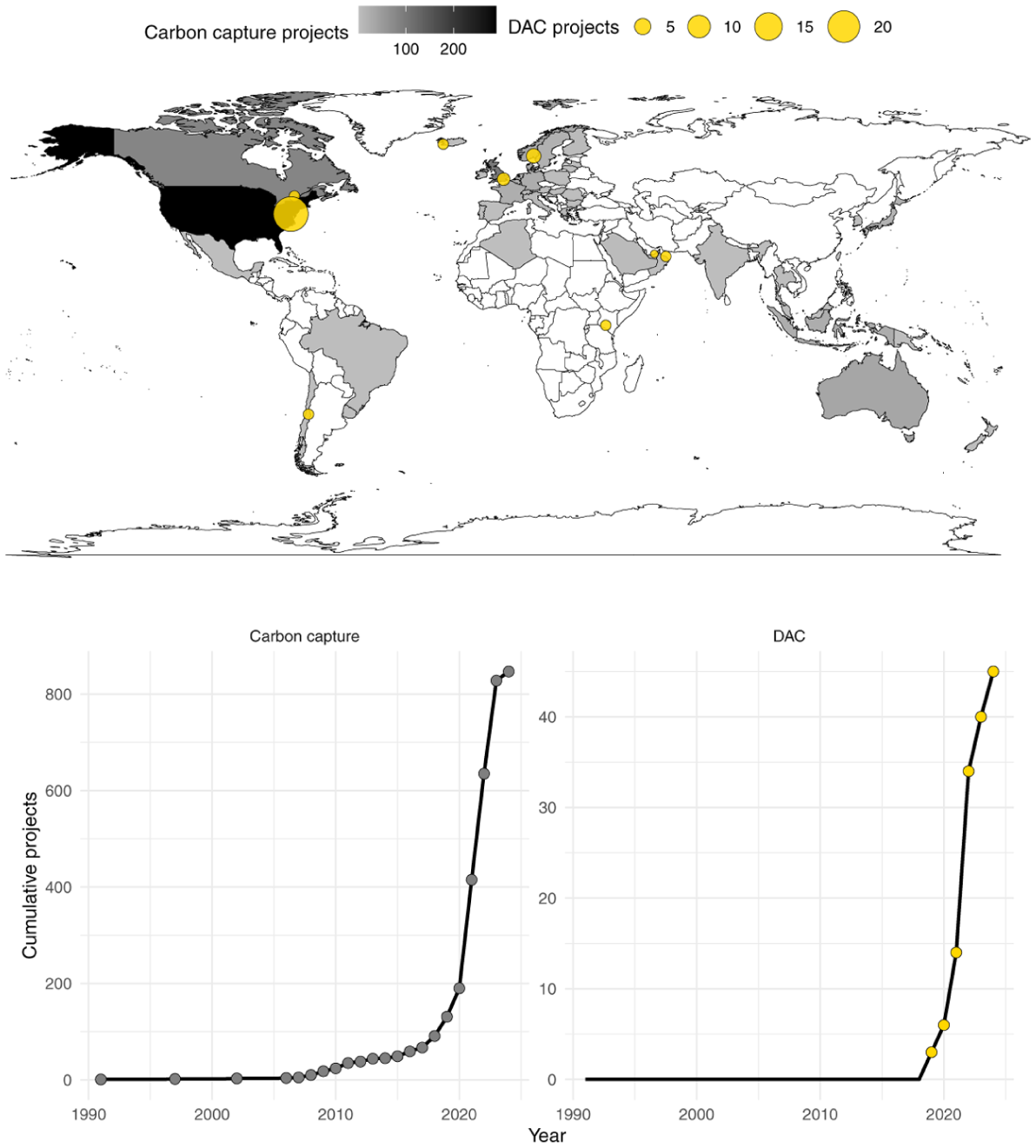

Figure 1 reports the geographical and temporal distribution of projects in our dataset, emphasizing a notable surge in the last few years and high concentration in countries rich in petroleum resources, suggesting a potential alignment with the interests of fossil fuel companies.

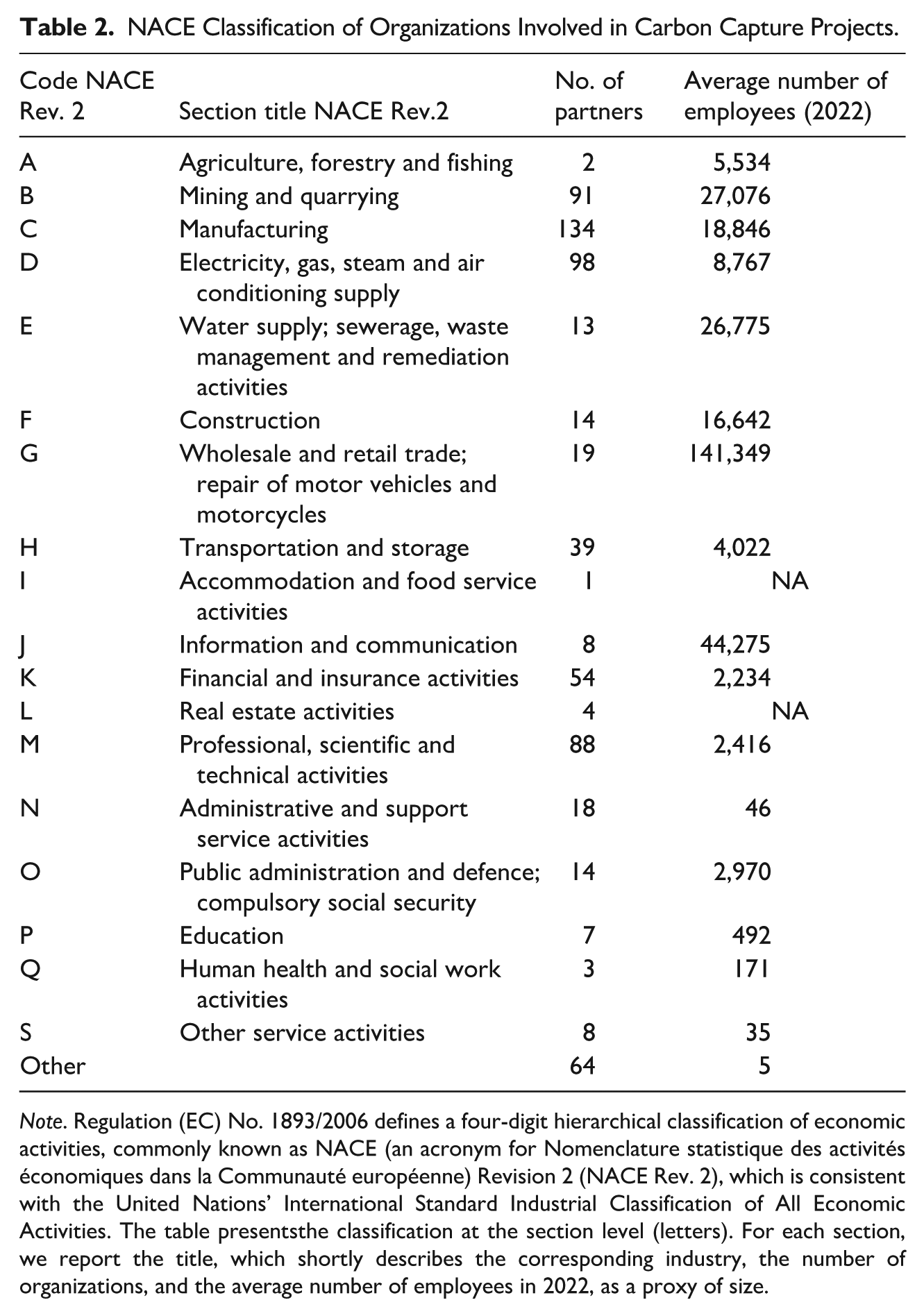

More relevant to our purpose is the information concerning the partners involved in each project. The original IEA dataset encompassed 802 partners, with no specific indication of their roles in the project. Consistent with the goal of this work, in what follows, we focus on projects involving multiple partners to analyze interorganizational relationships and construct a collaboration network. We then match partner organizations by name and country (when available) and, after controlling for sector of activity, integrate the IEA CCUS database with firm-level information from the BvD Orbis dataset. From Orbis, we retrieve each firm’s industry classification (NACE Rev. 2, 4-digit level), number of employees, total sales, total assets, return on assets (ROA), all in 2022, and the Global Ultimate Owner (GUO). This classification and firm-level data allow us to better characterize the types of organizations participating in carbon capture projects.

The final sample comprises 679 organizations participating in 508 projects, of which 614 (over 90%) are successfully matched to the Orbis database. Table 2 reports the NACE classification and average size (measured by the number of employees) for those companies. Table A.1 in the Supplemental Appendix provides a more granular NACE classification (i.e., divisions). Partners not matched with the Orbis database (reported as “Other” in Table 2) include universities, government departments, business consortia, and Indian reservations.

NACE Classification of Organizations Involved in Carbon Capture Projects.

Note. Regulation (EC) No. 1893/2006 defines a four-digit hierarchical classification of economic activities, commonly known as NACE (an acronym for Nomenclature statistique des activités économiques dans la Communauté européenne) Revision 2 (NACE Rev. 2), which is consistent with the United Nations’ International Standard Industrial Classification of All Economic Activities. The table presentsthe classification at the section level (letters). For each section, we report the title, which shortly describes the corresponding industry, the number of organizations, and the average number of employees in 2022, as a proxy of size.

The 4-digit NACE classification allows us to capture and discuss the diversity of partners across all projects. Additionally, for DAC-related projects, we provide a more detailed breakdown of the heterogeneous roles covered by partners. This further zoom-in aims to distinguish the contributions of the various partners, and particularly the role of fossil fuel firms, within DAC projects’ development.

Finally, we extend our dataset to include patent information. We first retrieve the BvD identifiers for all firms in our sample from Orbis and then collect their patents using Orbis Intellectual Property. Then, we match such data with EPO PATSTAT 2023 (Autumn edition) by publication number and DOCDB patent family number to retrieve additional patent information. As patents are filed in different legislations, we considered DOCDB patent families to identify unique inventions across legislations.

Classifying Organizations in DAC Projects

As discussed in the previous section, DAC projects are of particular interest due to their innovative potential compared to standard CCS technologies and their notable progress over the last few years. Indeed, Figure 1 depicts a sharp increase in DAC projects, with a growth rate even higher than that of other carbon removal technologies. The spatial and temporal patterns observed reveal a dynamic evolution of carbon capture technologies tied to resource distribution. Accordingly, this study investigates the role of fossil fuel companies in DAC projects, asking whether DAC constitutes a competence-destroying innovation or an incremental, competence-enhancing extension of existing capabilities.

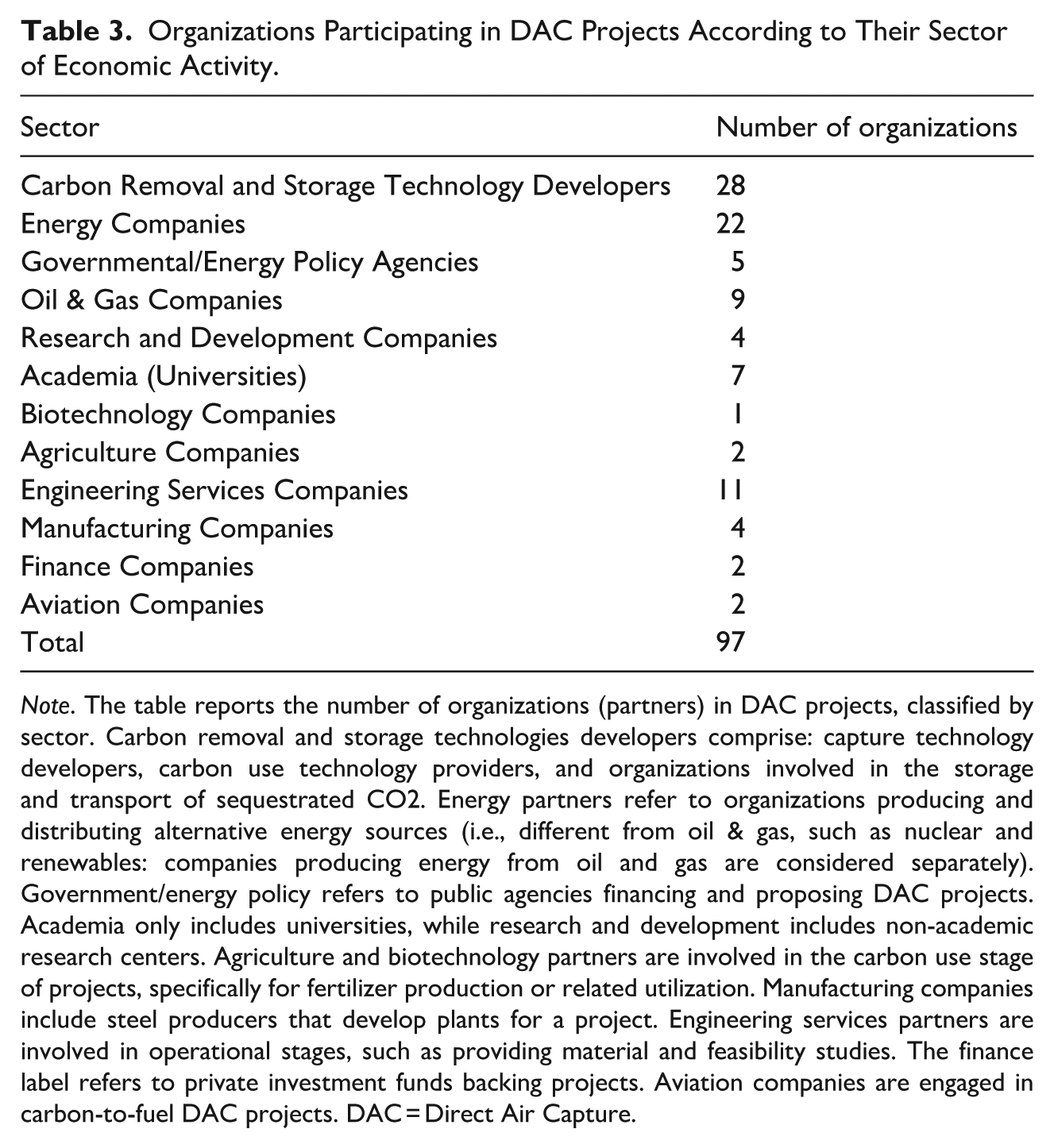

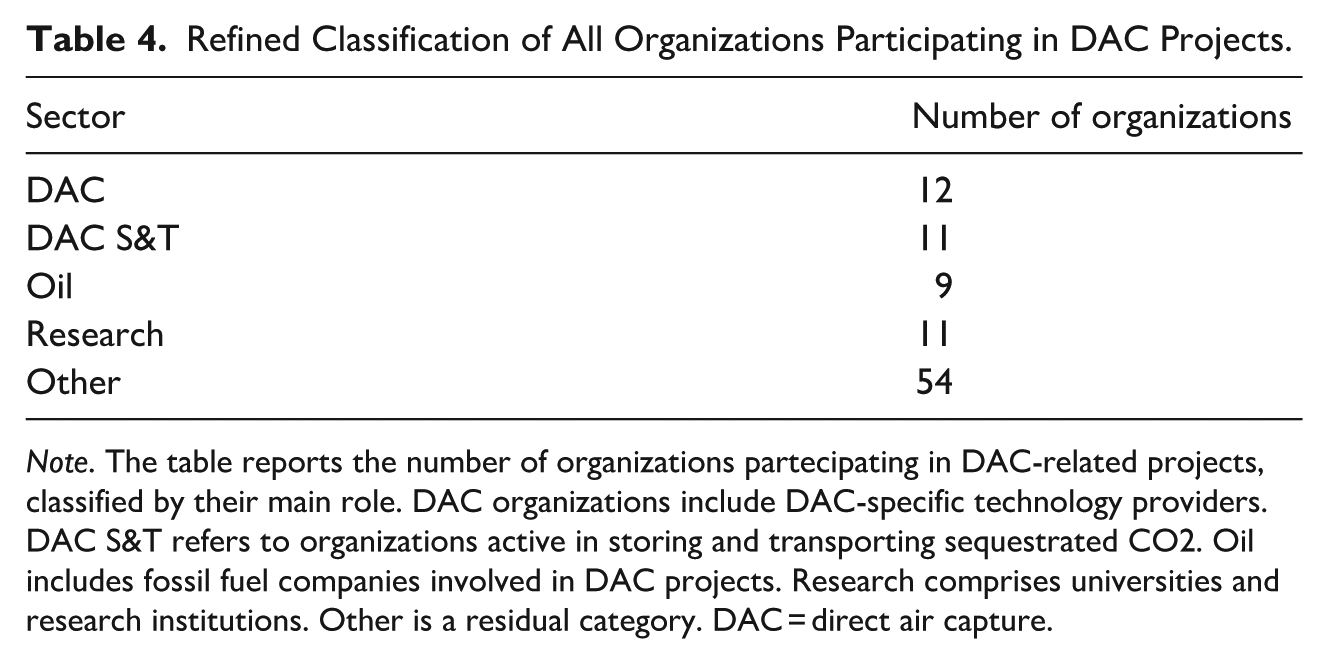

DAC projects involve multiple organizations with different roles. 1 As reported in Table 3, firms constitute the most represented category, with a clear majority of them developing carbon capture and storage methods (28) or non-fossil fuel-based energy technologies (22). Knowledge-intensive business services firms are also well represented in these projects (11 engineering services firms), signaling that DAC constitutes a novel knowledge-intensive market segment (Muller & Zenker, 2001). This is further confirmed by the presence of seven academic institutions and four research centers. As of today, nine oil and gas companies have participated in DAC projects. To facilitate visualization, we further categorize these organizations into five groups, summarized in Table 4. DAC indicates technology providers involved in developing direct carbon capture methods. DAC S&T refers to organizations involved in carbon storage and/or transport. Oil is a label for fossil fuel companies. Research comprises both academic and non-academic research and development institutions. “Other” is a residual category.

Organizations Participating in DAC Projects According to Their Sector of Economic Activity.

Note. The table reports the number of organizations (partners) in DAC projects, classified by sector. Carbon removal and storage technologies developers comprise: capture technology developers, carbon use technology providers, and organizations involved in the storage and transport of sequestrated CO2. Energy partners refer to organizations producing and distributing alternative energy sources (i.e., different from oil & gas, such as nuclear and renewables: companies producing energy from oil and gas are considered separately). Government/energy policy refers to public agencies financing and proposing DAC projects. Academia only includes universities, while research and development includes non-academic research centers. Agriculture and biotechnology partners are involved in the carbon use stage of projects, specifically for fertilizer production or related utilization. Manufacturing companies include steel producers that develop plants for a project. Engineering services partners are involved in operational stages, such as providing material and feasibility studies. The finance label refers to private investment funds backing projects. Aviation companies are engaged in carbon-to-fuel DAC projects. DAC = Direct Air Capture.

Refined Classification of All Organizations Participating in DAC Projects.

Note. The table reports the number of organizations partecipating in DAC-related projects, classified by their main role. DAC organizations include DAC-specific technology providers. DAC S&T refers to organizations active in storing and transporting sequestrated CO2. Oil includes fossil fuel companies involved in DAC projects. Research comprises universities and research institutions. Other is a residual category. DAC = direct air capture.

Methods

Our analysis integrates different empirical methods. First, we examine the network of collaborations across the full dataset of carbon capture projects (section “Descriptive analysis of the collaboration network”). Next, we employ linear regressions and null statistical models to inspect whether fossil fuel firms cover relatively more central positions in the network of CCS and DAC projects (section “Regressions and Null Models Testing for the Centrality and Connections of Fossil Fuel Firms”). Finally, we rely on patent data to examine the technological distance between the patent portfolios of fossil fuel firms already involved in the development and deployment of CCS and the emerging DAC technologies (section “Examining the Technological Distance Between CCS and DAC”).

Descriptive Analysis of the Collaboration Network

The assessment of the carbon removal industry’s development is facilitated by a bipartite network connecting projects to organizations. This network, a graph with nodes divided into two distinct layers, is a powerful tool for understanding the relationships between carbon capture projects and the organizations involved in them. By leveraging the information on all partners listed in our sample, we can gain a comprehensive view of the industry’s development (Tripodi et al., 2020; Tumminello et al., 2011). In our bipartite network, the first layer encompasses all projects, while the second layer represents the partners (i.e., organizations) involved in these projects. Notably, no link is established between nodes within the same layer. Instead, the links that connect nodes across the two layers (i.e., projects and organizations) are based on project participation. Such links form a binary bi-adjacency matrix where rows represent projects and columns represent organizations. Since our focus is on collaboration, we derive a weighted monopartite projection on the partners’ layer by counting co-occurrences in the original bipartite network. This resulting projection takes the form of a square matrix representing the collaboration network among organizations involved in the carbon capture landscape. In other words, it describes how organizations are connected through collaborative carbon capture projects.

By analyzing this collaboration network and examining the role of fossil fuel firms within it, we test our first hypothesis (HP1) concerning the centrality of fossil fuel firms in developing and deploying carbon capture technologies.

We begin by focusing on a set of measures describing the general structure of the carbon capture collaboration network. The size of the connected components indicates the overall cohesion of the network. A connected component is the maximal set of nodes reachable from any other node in the same set by a path. Many real-world undirected networks exhibit a giant connected component (i.e., a component that includes most of the nodes), indicating high overall cohesion. Next, we measure the relative importance of each node in the network by calculating various centrality measures: degree centrality, node strength, betweenness, and eigenvector centrality. 2 These measures allow us to detect which actors are central and more influential in the network of carbon capture projects. As such, we will accept or reject HP1 by evaluating the relative centrality and node strength of fossil fuel firms.

Regressions and Null Models Testing for the Centrality and Connections of Fossil Fuel Firms

To corroborate the previous descriptive evidence, we also conduct an econometric analysis to determine whether being a fossil fuel firm is associated with greater centrality in the carbon capture collaboration network, while controlling for firm-specific characteristics. We estimate four fixed-effects models with the dependent variables being alternative measures of network centrality: degree, strength, eigenvector centrality, and betweenness. The core explanatory variable is a dummy variable (Class) indicating whether a firm is a fossil fuel company. In our baseline specification, we control for the number of DOCDB patent families (as a proxy for firm technological capabilities) and the number of employees in 2022 (as a proxy for firm size). Hence, we estimate using OLS the following equation(s):

where Yᵢ is a centrality measure (i.e., Degree, Strength, Eigenvector, or Betweenness); Classᵢ is a dummy equal to 1 if firm i is a fossil fuel company; Patentsᵢ is the number of patent families; Employeesᵢ is the number of employees in 2022; γ c are country fixed effects; and εᵢ is the error term. A set of robustness checks for these regressions includes alternative specifications with sectoral fixed effects, additional measures of firm size (i.e., sales and assets, in 2022), and profitability ratios (i.e., ROA using net income in 2022). Results remain robust to these different specifications and are summarized in the Supplemental Appendix (see Tables B.3–B.7).

The second part of our investigation concerns DAC technologies and the role of fossil fuel firms in this emerging area. To test our second and third hypotheses (HP2 and HP3), we analyze the relationship between oil companies and DAC technology providers in the collaboration network. Since the number of DAC technology providers is limited, we go beyond the simple edge count between these two types of entities and propose a configuration null model exercise. Configuration null models (Bollobás, 2001; Maslov & Sneppen, 2002) are commonly used in network science to build random networks with the same structural properties as the original graph and to detect the importance of node categories (sectors in our case) or their connections, independently of their frequency of occurrence in the network. This approach enables us to accurately compare heterogeneous sectors within the network (i.e., with varying occurrence and average degree), such as oil and DAC companies, as illustrated in the following section. Specifically, we simulate 1,000 random project networks by preserving the degree of each node (i.e., its number of edges) while randomly connecting them. We then count the number of edges between different types of nodes in both the random and observed project networks. By comparing the random and the observed number of edges between DAC technology providers and oil companies, we can test whether the observed number of connections is driven by the structural properties of the network (e.g., frequency of node sectors and node degrees). In other words, we can test whether such connections occur more or less frequently than would be expected under random conditions. By observing whether fossil fuel firms are relatively connected to (or disconnected from) DAC technology providers, we assess the validity of HP2. The assessment is based on the distribution of the number of edges across all networks, computing the ratio between the observed number of links and the average number of expected links derived from 1,000 randomly generated networks connecting DAC technology providers and oil companies. More formally:

If the above ratio is equal to 1, the observed connections are simply explained by the network’s structural properties. If it is lower than 1, observed edges are underrepresented, meaning that the connections between oil and DAC companies appear less frequently than expected (under the null model). That is, oil companies are not significantly entering the DAC niche, which would confirm our HP2. Conversely, if the ratio is greater than 1, observed oil-DAC edges are overrepresented. In this case, we would interpret such an overrepresentation as evidence that oil companies appear more interested in DAC technologies than expected, given their typical behavior in forming project partnerships, and we would reject HP2.

We repeat this exercise also considering the classification of companies’ GUO to explicitly check whether oil companies have been indirectly trying to enter the DAC sector through acquisitions or mergers. Indeed, by leveraging our null model while simultaneously accounting for the ultimate owner of DAC companies, our findings can support or reject HP3.

Examining the Technological Distance Between CCS and DAC

Finally, we extend our analysis to characterize the patenting activities of fossil fuel firms in the carbon removal industry and to evaluate the technological distance between innovations in DAC and their patent portfolios.

To start with, we define DAC innovations as patent families assigned to DAC technology providers within the macro domain Y02C (“Capture, storage, sequestration or disposal of greenhouse gases,” according to the Cooperative Patent Classification [CPC]), identifying 38 patent families. To assess DAC technological distance relative to the patent portfolios of fossil fuel firms, we leverage the technology codes assigned to each patent according to the CPC system. 3 This enables us to construct a technology space based on the normalized co-occurrence of cited CPC codes (Breschi et al., 2003), where technologies that co-occur more frequently are considered closer. The technology space is derived from all patents filed at the United States Patent and Trademark Office (USPTO), with co-occurrence values normalized using cosine similarity. Hence, we measure the distance between two patent families (p and p′) as the average distance between cited CPC codes:

where c and c′ are CPC codes cited by p and p′, respectively. fc and fc′ are their frequency in patent citations, and scc′ is their similarity (ranging between 0 and 1) as defined in the technology space. This distance ranges between 0 and 1. Following this procedure, we calculate the technological distance between DAC innovations and the patent portfolios of fossil fuel firms. Comparing the internal coherence (proximity) of DAC patents with their distance from fossil fuel portfolios allows us to test whether DAC represents a competence-destroying rather than a competence-enhancing trajectory, consistent with HP1 and HP2.

Results

The Structure of Collaborations in Carbon Capture

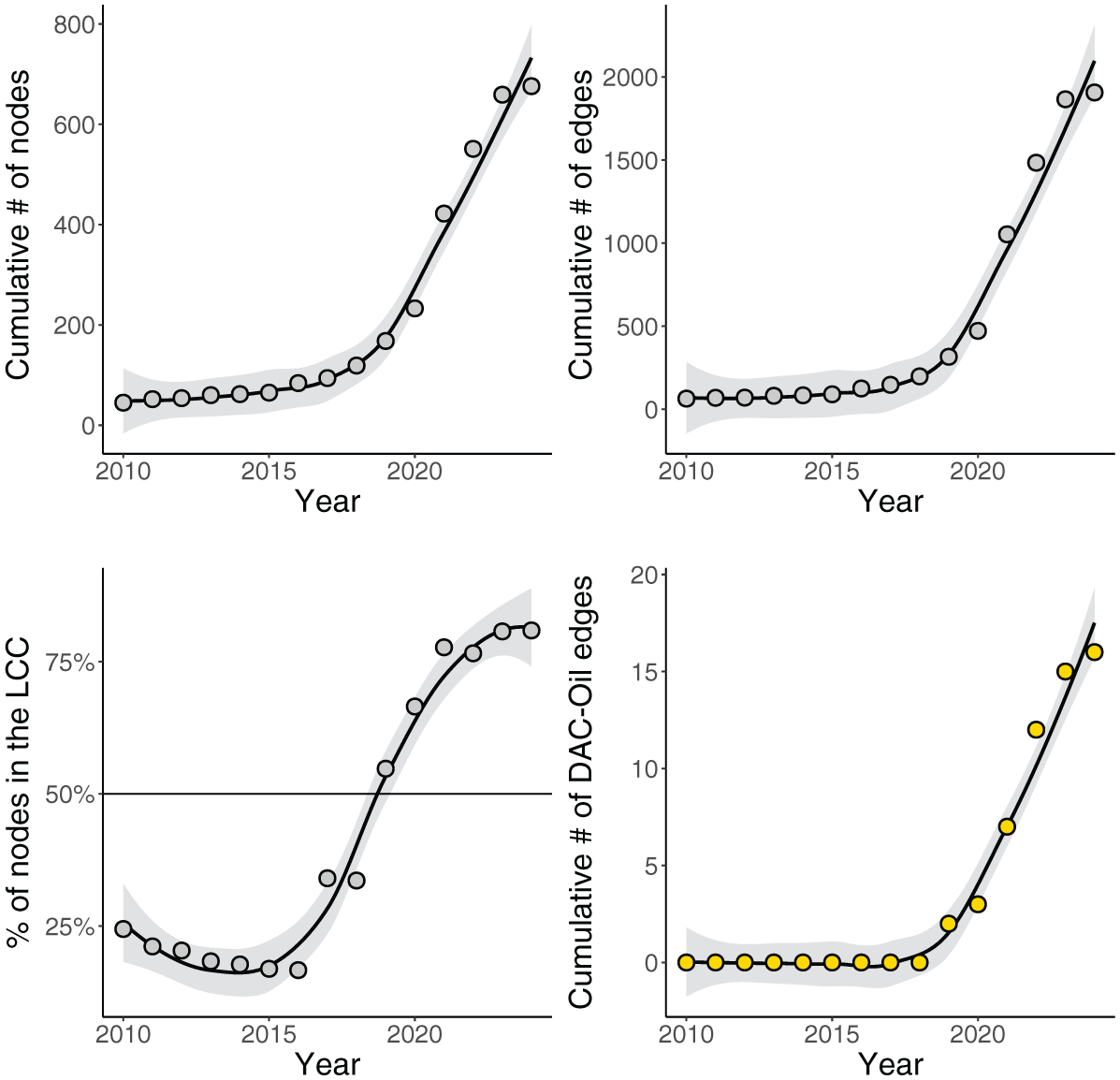

The carbon capture collaboration network (in 2024) includes 679 nodes and 1,886 links based on 508 projects that share at least two partners. The network structure reveals the emergence of high cohesion, as illustrated by a giant connected component including over 80% of organizations operating in different carbon capture, utilization, and storage sectors. These nodes comprise the core of the carbon capture landscape and interact with one another, directly or indirectly, through shared projects. The network appears sparse, with an edge density of around 1% and a global clustering coefficient of around 0.3.

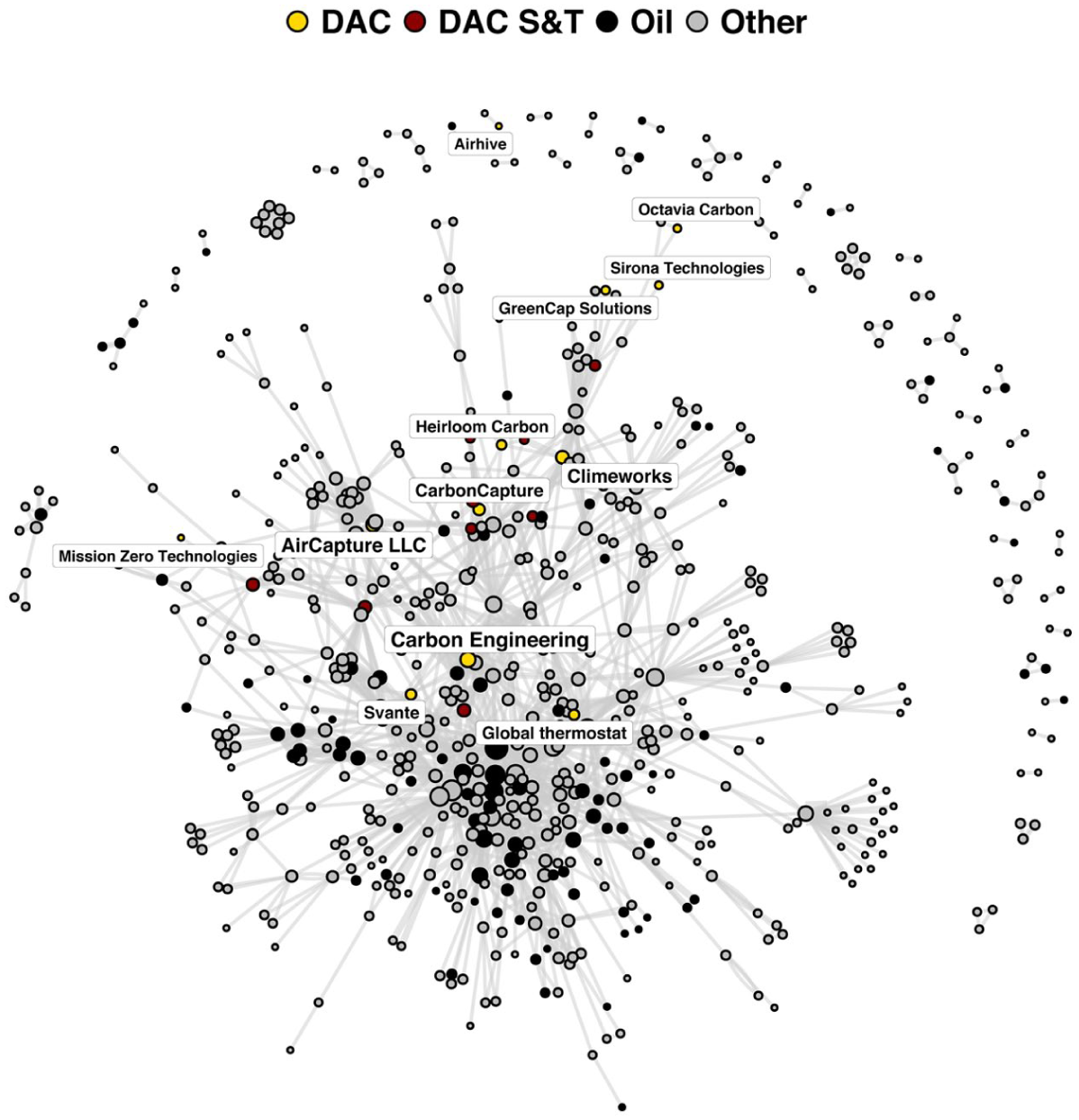

Based on the classification developed above (see Table 1), we can further highlight the roles of different organizations among the 679 nodes in the network. More specifically, in Figure 2, we focus on DAC technology providers (in yellow), carbon storage and transport involved in DAC projects (DAC S&T, in red), and oil companies (in black). Interestingly, even from a simple visual inspection, fossil fuel companies (black nodes) appear relatively central in the 2024 collaboration network.

Carbon Capture Collaboration Network.

Observing the network evolution from 2010 to 2024 provides further insights. Figure 3 highlights that 2019 marks a turning point for the carbon capture industry, with the network starting to grow exponentially and the emergence of a giant connected component (i.e., a large share of nodes belonging to a single component of the network). In addition, the number of links connecting DAC technology providers and oil companies also tends to increase over time and takes off approximately in 2019. These trends suggest both (a) a steadily growing interest and investment in carbon removal technologies, and (b) the emergence of ties between fossil fuel firms and DAC actors.

Evolution of the Carbon Capture Collaboration Network Over the Last Two Decades (2010–2024).

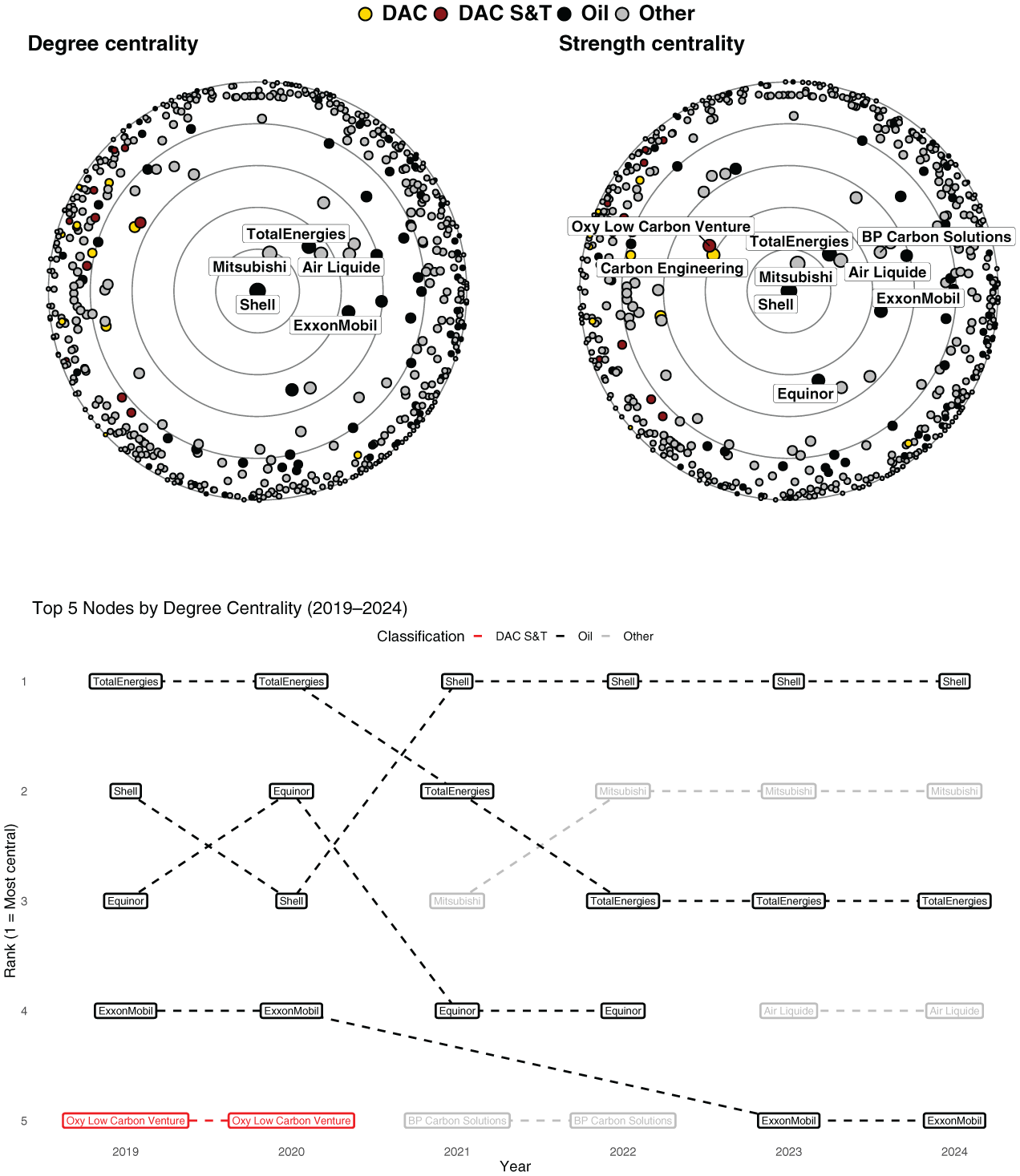

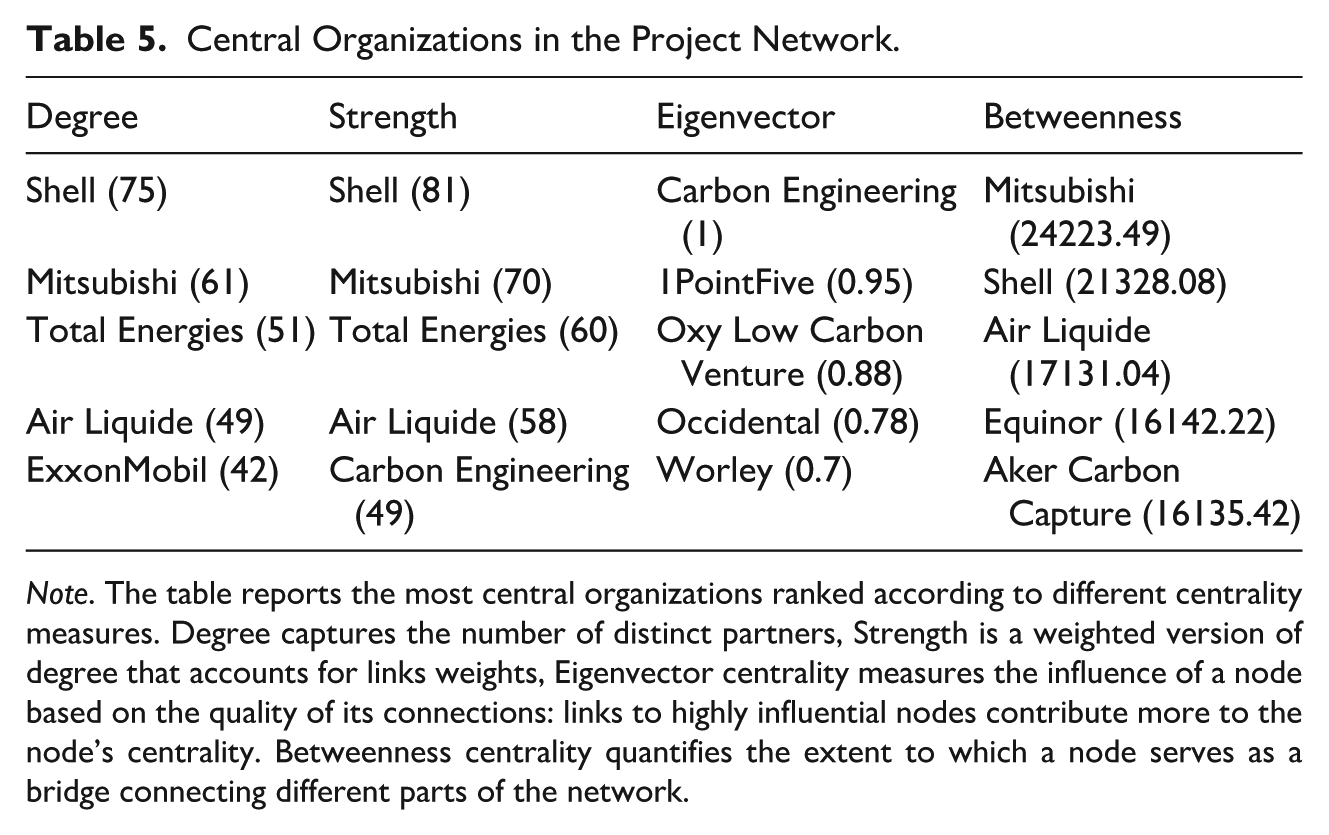

To better investigate the relative importance of the different organizations in our network and to test the role of fossil fuel companies quantitatively, we rank nodes by centrality scores. Figure 4 shows the nodes in the giant connected component arranged by degree and eigenvector centrality. Our analysis indicates that the business ecosystem of industrial carbon capture is currently dominated by a small fraction of companies, mainly in the highest-emitting, hard-to-abate sectors. Specifically, the three most central nodes, that is, the most essential nodes for interactions in the network, are Shell, Mitsubishi, and Total Energies. Surprisingly, though, when looking at eigenvector centrality, Carbon Engineering, a leading DAC company, stands out due to its connections with Shell, Occidental, and other central nodes in the network. These results support our first hypothesis (HP1) and provide relevant insights. First, large incumbent companies, many of which operate in the oil and gas sector, play a significant role in the carbon capture projects network: they are connected to more partners than others (high degree centrality) and maintain more frequent collaborations (high strength). This reinforces concerns about their propensity to take further action in phasing out fossil fuels and their vested interests in substantive mitigation processes (see also Ferns & Amaeshi, 2021; Gunderson et al., 2020; Nyberg, Wright, & Bowden, 2022). Second, DAC technology providers populate the network’s periphery, with some remarkable exceptions, such as Carbon Engineering (see Table 5 for additional details).

Graphical Representation of Central Nodes in the Network of Carbon Capture Collaborations.

Central Organizations in the Project Network.

Note. The table reports the most central organizations ranked according to different centrality measures. Degree captures the number of distinct partners, Strength is a weighted version of degree that accounts for links weights, Eigenvector centrality measures the influence of a node based on the quality of its connections: links to highly influential nodes contribute more to the node’s centrality. Betweenness centrality quantifies the extent to which a node serves as a bridge connecting different parts of the network.

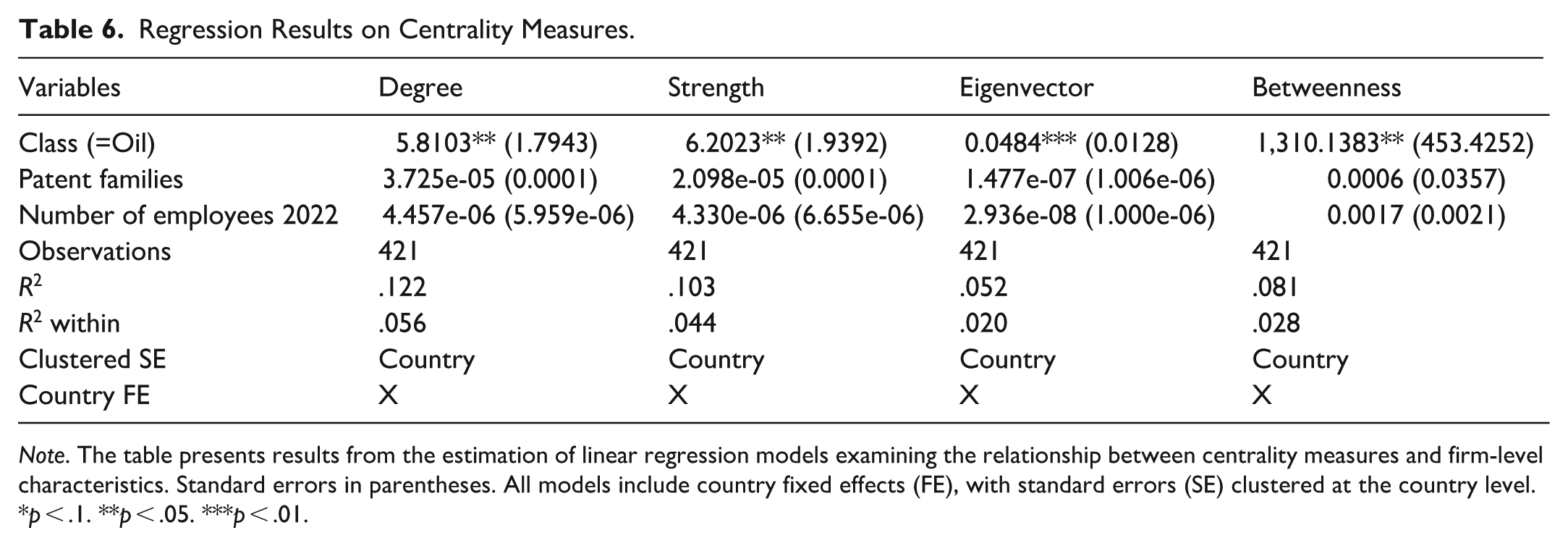

Regression analysis robustly confirms these results. Table 6 shows that fossil fuel companies are consistently more central in the network, even after accounting for technological capabilities—as proxied by the stock of knowledge embedded in the patent stock—firm size, country, and industry heterogeneity (see also Figure B.6 and Tables B.3–B.7 in the Supplemental Appendix). These results hold across degree, eigenvector, strength, and betweenness centrality, lending additional support to HP1 and suggesting that the carbon capture collaboration network is significantly shaped by the influence of fossil fuel firms, which tend to engage with more partners, specifically with the most influential, and more intensively, while keeping the role of brokers in defining collaborations.

Regression Results on Centrality Measures.

Note. The table presents results from the estimation of linear regression models examining the relationship between centrality measures and firm-level characteristics. Standard errors in parentheses. All models include country fixed effects (FE), with standard errors (SE) clustered at the country level.

p < .1. **p < .05. ***p < .01.

The centrality of fossil fuel firms in the landscape of carbon removal projects is not a recent phenomenon. As insisted by Boon (2019) and Carton et al. (2020), it rather stems from the historical involvement of the oil and gas industry in the promotion of carbon capture, utilization, and storage as a key element in the overall decarbonization process, which provided legitimacy to the industry’s commitment in the fight against the climate crisis (Fitzgerald, 2012). Despite the limited length of our sample, looking at the evolution of the network across the year exhibits notable stability over time and confirms that fossil fuel firms consistently rank amongst the most central actors (see Figure 4, bottom panel and Figures B.1–B.5 in the Supplemental Appendix). This persistent centrality suggests that, despite structural change and the growing prominence of other sectors, such organizations continue to play a coordinating and bridging role in the landscape of carbon removal projects.

The Evolution of DAC Projects and the Actors Involved

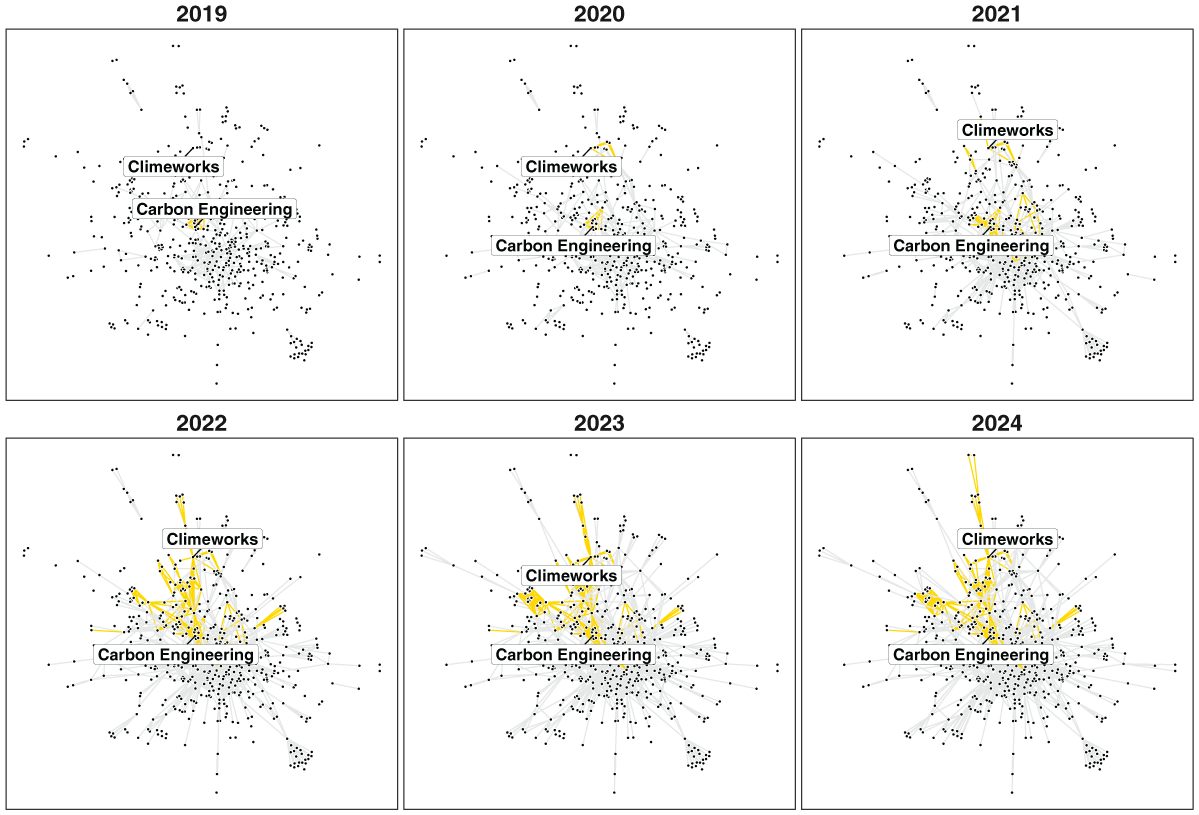

To better describe the evolution of the DAC landscape, we focus on the dynamics of the giant connected component, starting in 2019, which—as noted above—is a critical point in time for the industry and marks the first appearance of a DAC project. We also keep track of the position of the two main technology developers in the early stage of the industry: Carbon Engineering and Climeworks. Figure 5 displays the evolution of DAC projects (yellow links) from 2019 to 2024. As expected, the network becomes increasingly dense, with a rising number of DAC projects emerging each year. However, Carbon Engineering and Climeworks follow a different trajectory: while the former occupies a more central position, granted by its collaborations with fossil fuel companies, the latter appears more peripheral. Over time, both companies expand their partners’ network, and starting in 2022, the overall DAC subgraph (which separates the nodes and links associated with DAC projects) becomes increasingly connected, highlighting how carbon removal projects gained momentum.

Collaboration Network in DAC Projects and Key Players Over Time.

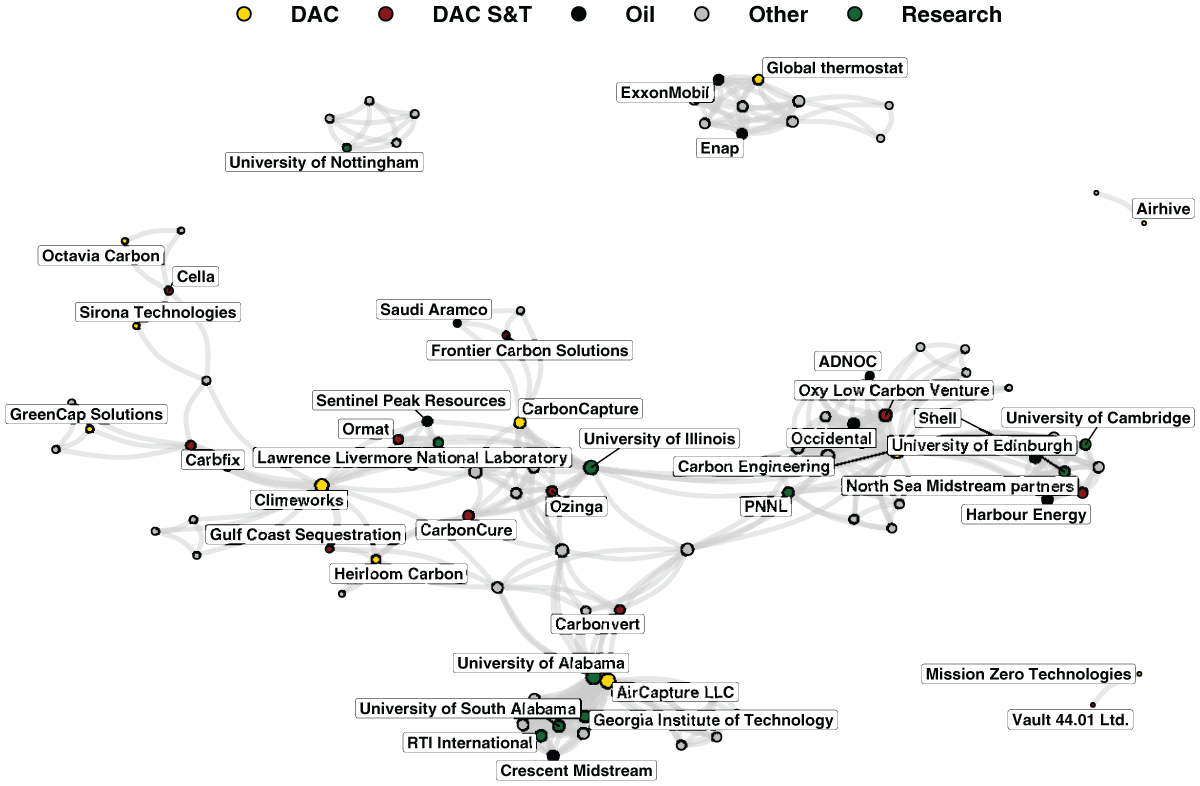

In 2024, the DAC subgraph comprises 96 nodes and 327 links, with most nodes (approximately 80%) forming a large, connected component. Carbon Engineering emerges as the most central actor. In contrast to the overall carbon capture network, universities and research institutions play a crucial role in DAC projects (green nodes). To visualize this, Figure 6 presents all DAC players and their positions within the network. Partners fall into five different categories: technology providers, carbon storage and transport involved in DAC projects, oil companies, research centers, and a broad “Other” category. This segmentation provides a deeper understanding of the roles and interactions among different types of organizations within the DAC landscape. The three most important DAC players (Carbon Engineering, Climeworks, and AirCapture) almost constitute separate sub-networks, but they are indeed connected by some bridging partners, such as the University of Illinois, suggesting that research institutions may have a brokering role in the development of DAC. Differently, while oil companies hold a central position in the full project network (see section “The Structure of Collaborations in Carbon Capture: A Multi-Actor Process” and Figures 2 and 3), their role in the DAC subgraph appears more marginal.

Graphical Representation of the Network of DAC Projects.

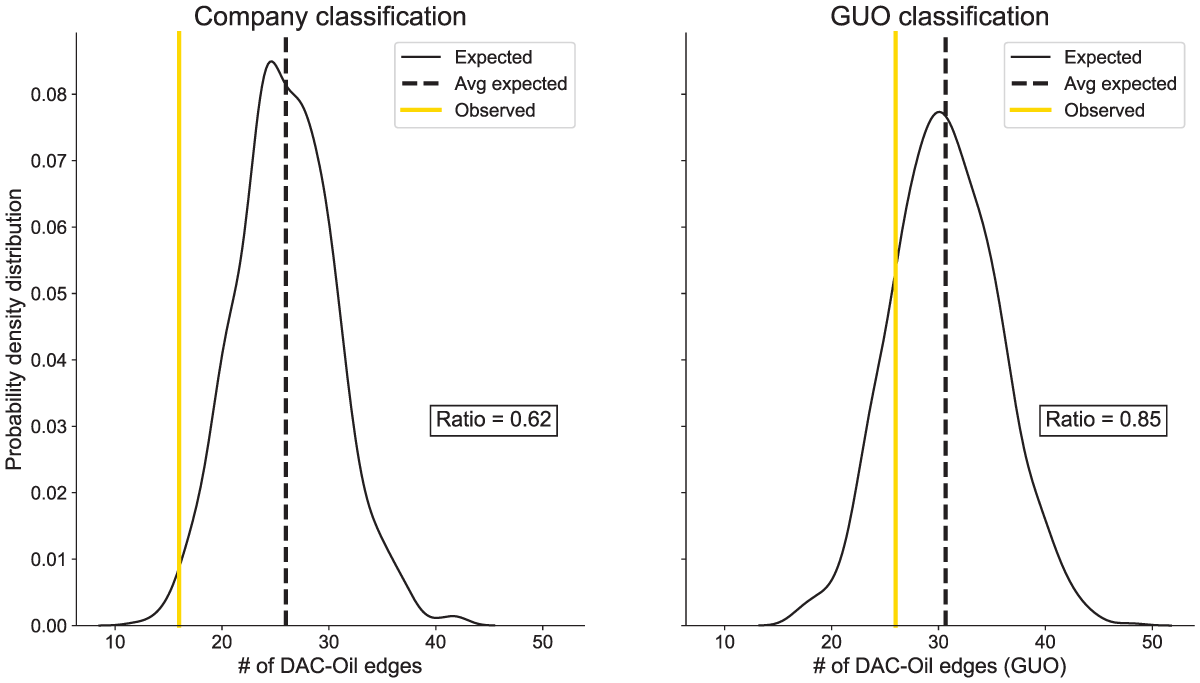

To test our second hypothesis (HP2), we analyze the connections (network edges) between fossil fuel companies and DAC technology providers to assess whether the oil sector has been directly involved in the development of DAC projects. We identify only 16 direct edges between these two categories of nodes, corresponding to 0.4% of the total edges in the network. Such a relatively small value, however, may be explained by the limited number of DAC technology providers. To address this, we build a network configuration model (i.e., null model) that accounts for the frequency of node categories and their average number of connections, as described in section “Regressions and Null Models Testing for the Centrality and Connections of Fossil Fuel Firms.” This model randomizes edges between nodes, preserving their degree (i.e., the number of links they have with other nodes). In the resulting networks, the centrality of each node and the frequency of sectors remain unchanged, allowing us to determine the expected number of edges between different types of nodes. Figure 7 (left-hand side panel) reports the number of edges between DAC technology providers and oil companies in 1,000 random networks derived from our null model. The distribution of the expected number of edges, given the sectors’ frequency and relevance in the network (in black), confirms the marginal role of oil companies in the development of DAC technologies. The observed number of edges between DAC and oil firms (in yellow) is, indeed, lower than in the randomly generated networks. While we observe 16 direct links between DAC technology providers and oil companies, the average number of edges in the random networks is 25.7, meaning that only 62% of the expected connections between businesses in these two sectors are realized in the empirically observed project network. 4 The configuration model also suggests that DAC technology providers are closely linked to DAC S&T companies, as their connection is 4.7 times higher than expected. At the same time, fossil fuel firms tend to connect with other oil companies, displaying almost double the number of oil-to-oil edges in the real network than what the null model would predict (for more details, see Table B.1 in the Supplemental Appendix).

Observed and Expected Edges Between DAC Developers and Oil Companies.

Our analysis so far has considered node classification across different sectors based on the firm’s production activities. However, oil companies may attempt to enter the “race” to develop DAC technologies indirectly, by acquiring other companies or creating subsidiaries (HP3). For example, Occidental Petroleum Corporation established Oxy Low Carbon Venture to manage its carbon capture and storage projects. Oxy plays an active role in several carbon capture, utilization, and storage projects, including a few in DAC. To account for such indirect participation and test HP3, we reclassify each node by the sector of its GUO. In this way, if a company is ultimately owned by a fossil fuel firm, we classify it as “Oil” regardless of its production activity. When accounting for GUO classification, the number of edges between DAC technology providers and oil companies increases to 26. Yet, as shown in Figure 7 (right panel), this remains below the null model’s prediction: the expected number of edges is 30.8, implying that only 85% of expected connections occur (see Table B.2 in the Supplemental Appendix for details). This test confirms HP2 and rejects HP3. Despite the growing interest of fossil fuel firms in DAC technologies, they do not play a prominent role in the sector.

Patent Portfolios, Technological Distance, and the Competence-Destroying Nature of DAC

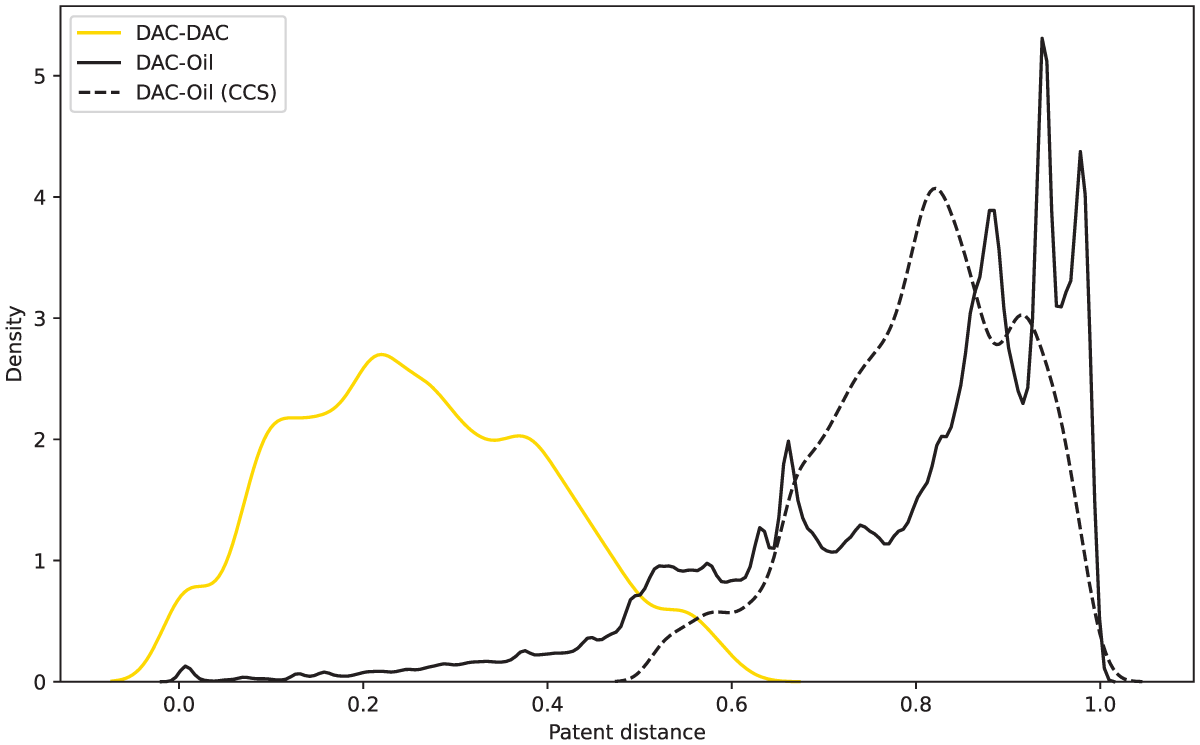

Following the procedure described in section “Classifying Organizations in Direct Air Capture Projects,” we identify 1,241 carbon capture-related inventions among the 370,041 DOCDB patent families assigned to firms in our sample between 1980 and 2023. Of these, 256 are attributed to fossil fuel companies, including IFP Energies Nouvelles, Saudi Aramco, ExxonMobil, Chevron, TotalEnergies, ENI, and Equinor, implying that more than 20% of all carbon capture innovations are attributable to oil firms. Such descriptive evidence further supports HP1, confirming the central role of fossil fuel firms in the development of carbon capture technologies. In contrast, 38 patent families are assigned to DAC technology providers and classified as DAC patents. We then follow Breschi et al. (2003) to compute the technological distance between innovations, comparing DAC patents with those of fossil fuel firms—both across their entire patent portfolios and specifically within their CCS-related inventions.

Figure 8 illustrates the distribution of the technological distances between all DAC-fossil fuel patent pairs (black, solid line) and, for comparison, the distribution of distances between pairs of DAC-DAC patents (gold, dashed line). Our analysis reveals a substantial difference: while DAC patents exhibit high internal similarity (average distance: 0.26), DAC and fossil fuel technologies are clearly distinct (average distance: 0.78). A t-test confirms that the two distributions are significantly different (p < .001), indicating a statistically significant technological distance between DAC and fossil fuel technologies. Remarkably, these results hold even when exclusively considering fossil fuel firms’ stock of CCS patents (black, dashed line). These results not only provide strong support for HP2 but also reinforce the interpretation of our results through the lens of competence-enhancing and competence-destroying technological discontinuities. Whereas “point-source” CCS remains closely aligned with the core operational and engineering capabilities of the oil and gas industry (see section “The Carbon Removal Industry: Diverging Technologies and Emerging Pathways”), DAC appears technologically distant from both CCS and the wider patent base of fossil fuel firms. The pronounced technological gap—visible not only in mean values but across the entire distribution of patent pairs—suggests that the fossil fuel sector has not yet engaged in the kind of creative accumulation via competence expansion necessary to navigate discontinuities (Bergek et al., 2011, 2013; Geels, 2006; Pemer & Werr, 2023).

Technological Distance Between DAC and Fossil Fuel Firms’ Patents.

Discussion and Conclusions

The development of technologies to operationalize negative emissions can play a crucial role in tackling climate change, with the nature of such a development potentially transformative for the fossil fuel sector. In this work, we specifically investigated the role of fossil fuel companies in the landscape of large-scale carbon capture projects, adopting a competence-based view of the sector’s dynamics. Our empirical investigation, based on network science tools and patent analysis, suggests that large incumbents play a central role in the development of the carbon capture industry, but appear relatively distant from potentially more disruptive technologies, such as DAC. This dual strategic evolution is consistent with the co-existence of competence-enhancing and competence-destroying innovation currently characterizing the carbon capture business ecosystem.

This article contributes to the literature of technological change and sustainability transitions by empirically demonstrating how the structural evolution of carbon capture projects—specifically in CCS and DAC—is shaped by their relationship to incumbent capabilities. Drawing on the foundational distinction between competence-enhancing and competence-destroying technological discontinuities (Dosi, 1982; Tushman & Anderson, 1986), the findings show that CCS has emerged as a domain closely aligned with the fossil fuel industry’s existing technical and infrastructural competencies. This alignment has facilitated the entry and consolidation of firms that leverage CCS to preserve asset value and reinforce their role in a low-carbon economy without fundamentally altering core operations. DAC, in contrast, has thus far remained largely competence-destroying for incumbents—characterized by novel engineering challenges, modular deployment models, and a lack of synergies with fossil-based infrastructures (except in relation to transport and storage)—thereby attracting new entrants and remaining peripheral to fossil fuel corporate strategies. This pattern supports prior work suggesting that incumbents are more likely to engage with innovations that reinforce existing capabilities and business models (Geels, 2014) and avoid or delay those that would require substantive organizational transformation or threaten profitability (Boon, 2019; Ferns & Amaeshi, 2021). Further, DAC can be perceived as a competence-destroying innovation (both as a process and a product) for the fossil fuel sector (Paschen et al., 2020). Indeed, it requires different technologies to operate and creates substantially novel products (i.e., certificates of carbon removal) for markets different from those the industry traditionally uses. Such a “double nature” of DAC makes the involvement of the fossil fuel industry even more difficult and uncertain. Crucially, both DAC and CCS rely on complementary assets and resources that are critical to their commercialization and large-scale deployment. Specifically, beyond capture technologies themselves, both pathways require access to downstream infrastructure and capabilities for the transport and permanent storage of CO2, including pipeline networks, compression facilities, geological storage sites, monitoring systems, and regulatory and liability management capabilities. These end-of-chain assets are well known to constitute key bottlenecks for scaling carbon removal and carbon capture solutions and are often controlled by incumbent actors in the energy and industrial sectors. From a commercialization perspective, this would suggest that incumbents possess many of the complementary assets needed to support both DAC and CCS deployment (Eggers & Park, 2018), potentially positioning them as central actors in both technological trajectories. Yet, despite similarities in downstream asset requirements, incumbents’ engagement differs markedly across the two pathways, indicating that the mere availability of complementary assets is insufficient to explain patterns of entry and strategic involvement.