Abstract

We study why family businesses consider different investments to fulfil their internal and external corporate social responsibility (CSR) and how these impact their firm performance. We analysed data from 8,469 family businesses from the Chinese Private Enterprise Surveys using the feasible generalised least squares estimation method, and found that family (ownership and management) involvement inhibits investment in internal CSR, while having an insignificant impact on investment in external CSR. Formalised governance practices significantly weaken the adverse effects of family involvement on internal CSR and enhance the motivation of family businesses to undertake external CSR. Finally, internal and external CSR function both independently and synergistically to enhance the performance of family businesses. By incorporating formal family governance into a research framework, this study provides a theoretical basis for explaining the differences in the fulfilment of internal and external CSR by family businesses. In doing so, it expands the literature on formal family governance and on the relationship between CSR and firm performance. The findings also have practical implications for how family businesses balance the interests and responsibilities of internal and external stakeholders to achieve a competitive advantage in the long term.

Introduction

Family firms are those managed, governed, and controlled by members of a core family, which manages the succession between generations (Åberg et al., 2024). As a combination of family and corporate systems, family firms inherently possess characteristics of both and must balance family versus business goals, non-economic versus economic objectives, and family versus corporate governance (Åberg et al., 2024; Chrisman et al., 2012). Thus, family firms often devote varying levels of effort to corporate social responsibility (CSR) when addressing the interests of internal and external stakeholders (Cruz et al., 2014).

There has been a noticeable increase in research on CSR in family firms in recent years. Existing studies on family firms tend to focus on the impact of family equity ownership (Fehre & Weber, 2019; Labelle et al., 2018; Lamb et al., 2017; Madden et al., 2020), family owners’ participation in firm management (Ahmad et al., 2020; Nekhili et al., 2017), family members’ positions within the firm (Cui et al., 2018; Lamb & Butler, 2018), founder control (Dick et al., 2021), sustainability activities and strategic marketing (Battisti et al., 2023), family-foundation giving (Cruz et al., 2014), and firm age (Madden et al., 2020) on CSR fulfilment. These studies have primarily employed socioemotional wealth (SEW) and agency theory to account for why family firms select or refuse to proactively fulfil CSR.

Research based on the SEW theory has posited that family firms prioritise non-economic family goals more than non-family firms, making them more proactive in fulfilling CSR (Berrone et al., 2010; Dyer & Whetten, 2006; Gómez-Mejía et al., 2007; Temouri et al., 2022). However, research based on agency theory has suggested that since agents with informational advantages prioritise their interests over those of other stakeholders (Jensen & Meckling, 1976), family firms are likely to reduce their intention to proactively engage in CSR (Le Breton-Miller & Miller, 2009).

Based on this, researchers have further compared the differences between family and non-family firms in terms of their implementation of internal and external CSR. Since the benefits of external CSR to the firm’s reputation are more evident, family firms tend to see CSR as a matter of charitable donations, environmental management, and other public welfare activities (Farooq et al., 2017). By contrast, internal CSR emphasises employee welfare and career development. Family firms view this as a burden and may, therefore, neglect employees’ legal rights, for example, by letting wages fall into arrears and not providing adequate safety conditions (Neckebrouck et al., 2018). Family firms thus emphasise external CSR more than non-family firms while investing less in internal CSR. Different types of Chief Executive Officer (CEOs) (Meier & Schier, 2021) and family-firm characteristics (Rivera-Franco et al., 2025) also have heterogeneous impacts on how family firms implement internal and external CSR. Despite this broad research, a significant controversy remains regarding the roles of different levels of family involvement and governance practices in these firms’ fulfilment of internal and external CSR.

We address this gap by taking stakeholder theory as an integrative perspective and incorporating SEW theory and agency theory to explore why family firms devote differing levels of effort to internal and external CSR and the consequent impact on firm performance. We focus on the role of formal family governance as a key moderator that weakens the motivation of families to sacrifice the interests of internal stakeholders and strengthens their intention to engage in external CSR.

This study uses the Chinese Private Enterprise Survey (CPES) databases for the years 2010, 2016, and 2020 to empirically test our hypotheses. We mitigated the problem of heteroskedasticity using the feasible generalised least squares (FGLS) estimation method. Chinese private enterprises provide a suitable context for studying CSR behaviour. Since the reform and opening up, private enterprises have become the dominant equity structure in contemporary China and play an extremely important role in CSR. For instance, they far exceed state-owned enterprises (SOEs) in charitable donations, accounting for the vast majority of such contributions (S. Li et al., 2017; W. Li & Zhang, 2010). CSR is also attracting increasing attention from investors, but research in the Chinese context remains insufficient (Z. Ma & Bu, 2021). Although most private enterprises in China are family firms (J. Chen et al., 2021; Y. Wang et al., 2024), and although existing research has analysed CSR in private enterprises in developed economies (Jamali & Karam, 2018; S. Li et al., 2017; W. Li & Zhang, 2010), these findings cannot be directly applied to developing countries. Focusing on family firms in China contributes to expanding research on CSR fulfilment in private enterprises within developing economies.

This study makes three main contributions to the research on CSR in family firms. First, our research deepens the understanding of bifurcation bias in the fulfilment of CSR in family firms by integrating SEW theory and agency theory into stakeholder theory. SEW theory and agency theory often yield contradictory predictions about the CSR engagement of family firms, largely because prior research has not effectively distinguished between internal and external CSR. Following Cruz et al. (2014) and Farooq et al. (2017), we disaggregate CSR into its internal and external dimensions to clarify why and how family firms behave differently toward inside and outside stakeholders.

Second, our research advances the literature on formal family governance by testing its key moderating role in the relationship between family involvement and internal/external CSR fulfilment in family firms. Existing research has distinguished between internal and external CSR in family firms and found that family firms have different impacts on internal and external CSR (Cruz et al., 2014). Further studies have found that, depending on the CEO type (Meier & Schier, 2021) and family-firm identity (Rivera-Franco et al., 2025), family firms have different preferences with regard to fulfilling internal and external CSR. There remains a significant unaddressed controversy regarding how different levels of family involvement and governance practices impact the fulfilment of internal and external CSR. This article, by incorporating formal family governance into its research framework, provides a theoretical foundation for explaining the differences in internal and external CSR among family firms. Third, our research reveals the independent and synergistic effects of internal and external CSR on family firm performance, advancing the literature on the relationship between CSR and firm performance while suggesting useful practices for family firms to improve firm performance.

The remainder of the article is organised as follows. Section ‘Family Firms, Governance and CSR Reforms in China’ considers family firms, governance, and CSR reforms in China. Section ‘Theory’ sets out the theory, and section ‘Empirical Literature Review and Hypotheses Development’ contains the literature review and hypotheses development. Section ‘Research Design’ describes the research design and empirical results, and this is followed by a discussion. Section ‘Summary and Conclusion’ contains the summary and conclusion.

Family Firms, Governance, and CSR Reforms in China

International calls for environmental protection and sustainable development have resulted in CSR becoming a key strategy for family firms (Carroll & Shabana, 2010), and those in China are no exception (Cumming et al., 2024; B. Liu et al., 2023; L. Ma, 2023). Unlike businesses in most other countries, Chinese family firms only began to flourish after the reform and opening-up policy of the 1970s. Family firms have long been at a disadvantage compared to SOEs in terms of status and legitimacy (J. Li et al., 2019; B. Liu et al., 2023; Y. Wang et al., 2024).

Chinese family firms are characterised by a prevalent command culture, seeking to reduce production costs through long work hours, low wages, and poor working conditions (Yuan et al., 2008). This absolute authority and power lead to unethical behaviour and a lack of CSR (Du, 2015). In this national context, early family firms prioritised growth and competitiveness, often neglecting CSR obligations such as employee rights and environmental protection.

Since the 1980s, China has successively promulgated laws such as the 1989 Environmental Protection Law, the 1994 Labour Law, and the Consumer Rights and Interests Protection Law of 1993, enforcing CSR in areas such as environmental protection, workers’ rights, and consumer rights. However, due to insufficient enforcement efforts, compared with businesses in developed countries, Chinese family firms still have significant room for improvement in fulfilling their CSR and are still in the exploratory stage.

Beyond these legal obligations, the characteristics of family firms also motivate them to fulfil CSR. Based on SEW theory, family firms have a stronger incentive to build and maintain a positive image and reputation (Berrone et al., 2010). CSR is often viewed as a form of good governance practice closely linked to reputation (L. Ma, 2023). In this context, Chinese family firms’ desire to maintain a positive reputation, as well as to legitimise their actions and address negative stakeholder perceptions, drives vigorous CSR efforts (B. Li et al., 2020; L. Ma, 2023; Y. Wang et al., 2024).

The above reforms motivated our research. We focus on how family involvement and formal governance practices of Chinese family firms affect the fulfilment of internal and external CSR, and, in turn, firm performance.

Theory

CSR: A Stakeholder Perspective

The concept of CSR suggests that corporations do not exist solely for the benefit of their shareholders. They also need to consider the interests of other stakeholders, for example, employees, consumers, suppliers, communities, and governments (Ali Gull et al., 2023). With the rise of economic globalisation and the expansion of multinational corporations, CSR has attracted extensive attention from scholars. Research often addresses the following question: ‘To whom should enterprises be responsible?’ The introduction of stakeholder theory has greatly expanded CSR research and has gradually become the mainstream theoretical framework in the field (Dmytriyev et al., 2021).

Stakeholders are persons, groups, or organisations that can affect a firm’s vision and mission, are affected by the company’s strategic outputs, and have a claim on firm performance (Parmar et al., 2010). They can be categorised into two groups: internal stakeholders, including managers, non-management employees, shareholders, and major funders, 1 and external stakeholders, including customers, suppliers, communities, labour unions, and governments (Parmar et al., 2010). In this study, CSR for internal stakeholders is referred to as internal CSR, while the CSR for external stakeholders is referred to as external CSR. These two types of CSR differ in their operational logic. Internal CSR is typically driven by instrumental rationality, such as whether it can minimise transaction costs and improve economic efficiency within firms (T. M. Jones, 1995). External CSR, by contrast, is based on the socially constructed value systems of external stakeholders (Suchman, 1995), emphasising that fulfilling CSR is a social norm that can improve the company’s reputation and legitimacy.

The study’s hypotheses are developed by incorporating SEW theory and agency theory into stakeholder theory. Regarding internal CSR, family firms may exhibit a stronger tendency towards agency behaviour, especially in China (Luo & Chung, 2013). This tendency increases internal agency costs and reduces their willingness to engage in internal CSR. In this context, family firms may prioritise their own interests at the expense of other internal stakeholders, such as their employees. Asymmetric altruism and nepotism often lead family firms to focus more on the interests of family members and utilise the firm’s resources to satisfy the family’s own needs, neglecting their responsibilities towards other internal stakeholders (Déniz & Suárez, 2005).

External CSR is more socially visible than internal CSR and more likely to be observed and monitored by external stakeholders, resulting in social pressure for family firms to take on external CSR (Cruz et al., 2014). Furthermore, external CSR fulfilment can generate positive moral capital among stakeholders and communities, which makes them form more favourable value judgements about firms that actively fulfil their CSR (Cruz et al., 2014).

CSR in Family Firms: Basic Theoretical Assumptions

According to the general responsibility principle, responsibility is linked to a specific social role, implying that the assumption of responsibility by a particular subject is commensurate with the rights associated with that role (Ali Gull et al., 2023; Crane et al., 2019). Similarly, firms need to assume responsibilities that correspond to their societal roles and rights. For family firms, which encompass both family and firm targets, family managers function as agents of the family. They are endowed by the family with specific rights and powers and are responsible for protecting its interests and those of its members (Chrisman et al., 2004). Family managers are also endowed with rights and powers by various stakeholders and are responsible for protecting the interests of the firm (Madison et al., 2016). However, the behavioural logic guiding family managers when fulfilling authority and assuming their responsibilities depends on the particular entity.

Regarding internal CSR, family managers adopt an instrumental rationality, assessing whether such practices bring economic benefits to the firm. Regarding external CSR, they are driven by social expectations and the need for legitimacy, prioritising SEW enhancement. However, this emphasis on SEW may lead family firms to adopt selective and instrumental CSR strategies (Zientara, 2017). From the instrumental rationality perspective, family firms might not take up CSR to lower corporate costs and operational risks (Neckebrouck et al., 2018). Family firms may simultaneously try to enhance their reputation and legitimacy by engaging in external CSR (Berrone et al., 2010; Cruz et al., 2014). Overall, with higher levels of family involvement, the family firm’s goals, strategic behaviour, and development trajectory are more closely aligned with the family’s will (Chrisman et al., 2012). The willingness and ability of family managers to control internal risks and acquire a positive external reputation and legitimacy can increase as family involvement deepens. Therefore, family involvement is a crucial factor in the approach of family firms to internal and external CSR.

As family involvement increases, family firms are more influenced by family nepotism (e.g., family lineage), exposing them to informal power, culture, and interests beyond the goals, structures, and institutions of formal organisations (Eddleston & Kellermanns, 2007). Informal governance is prevalent in family firms and is strongly relational in character due to the family’s involvement (J. Ma, 2021). Governance depends on the distribution of power and the checks and balances within the family, which is bound by blood ties and kinship, and ultimately influences corporate governance and decision-making (M. Bertrand et al., 2008).

Family firms are also legal entities consisting of complex contracts with formal features of contractual governance. As firms grow, they tend to establish formal governance structures and policies to constrain and mitigate the adverse effects of informal altruism and nepotism that may result from family involvement (Chrisman et al., 2004). Thus, the constraints imposed by formal governance mechanisms on relational governance will further influence the relationship between family involvement and CSR.

Finally, CSR significantly affects internal and external stakeholders’ recognition, commitment, and support for family firms, which, in turn, influences their performance (H. Wang & Qian, 2011). Based on the above analysis, the basic assumption of this study is that family involvement affects internal and external CSR through different behavioural logics, thereby impacting firm performance. In this process, formal family governance is a key boundary condition.

Empirical Literature Review and Hypotheses Development

Family Involvement and CSR Fulfilment

Chinese society is structured according to a differential mode of association (cha-xu pattern), a framework for social relations and a primary method for resource allocation within families driven by kinship and altruistic behaviour (Fei et al., 1992; Y. Liu et al., 2015). Owners of family firms classify members based on their closeness to the family, with the varying levels of trust and responsibility in those relationships influencing organisational behaviour (C. C. Chen et al., 2013). As a result, when the family firm is confronted with different stakeholders, the motivation and performance of its behaviour can vary.

This article focuses on small and medium-sized enterprises (SMEs) that are characterised by substantial family involvement in their ownership and management. Such enterprises differ significantly from large, publicly listed companies in terms of organisational characteristics, guiding principles, and financial and human resources. First, compared with large enterprises, moral motivation is usually more influential in small, owner-managed enterprises (Burton & Goldsby, 2009; Lepoutre & Heene, 2006). Therefore, SMEs are more likely to undertake CSR for moral reasons. Second, in SMEs, employee responsibility is rarely formalised through codes of ethics and social reporting (Russo & Tencati, 2009), thereby limiting internal CSR implementation. Third, compared with large, listed companies, SMEs lack high-quality internal resources and have a smaller market share (Park & Ghauri, 2015). These will affect enterprises’ resource allocation and lead to significant differences in investment across different types of CSR.

Due to China’s unique political structure, social norms, and legal environment (Baron & Tang, 2009; J. Tang et al., 2008), its SMEs also implement CSR in unique ways. First, the obstacles faced by Chinese SMEs may lead them to prioritise CSR activities for economic reasons rather than for social value (H. Liu & Fong, 2010). Compared to developed countries, China’s financial system remains underdeveloped, making financing SMEs difficult, which largely determines whether enterprises fulfil CSR (B. Liu et al., 2020). Second, in China’s unique institutional environment, the power relationship between SMEs and various stakeholders impacts firms’ CSR participation (Z. Tang & Tang, 2015). Consequently, the incentives and driving forces for SMEs to implement CSR are also significantly different from those of publicly listed companies. In terms of quantity, SMEs in China account for more than 90% of all businesses, and studying CSR within this vast group has significant theoretical and practical importance. This study argues that in the context of China, family involvement may have distinct impacts on CSR fulfilment depending on whether the stakeholders are internal or external.

Family Involvement and Internal CSR

Agency theory holds that agents with managerial power and informational advantages maximise their own interests at the expense of other internal stakeholders (Jensen & Meckling, 1976). Family firm owners and managers establish a generalised principal–agent relationship with other internal stakeholders. Non-family managers as agents prioritise short-term survival and maximise economic benefits, viewing the fulfilment of internal CSR as a way to increase short-term economic gains (Déniz & Suárez, 2005). Due to family-specific trust, family firms may be especially likely to exhibit agentic behaviour (Luo & Chung, 2013), a tendency that intensifies with deeper family involvement. Yet, excessive family involvement may increase internal principal–agent costs, reducing the likelihood of fulfilling internal CSR. For example, in China, family owners and managers often hollow out their companies by holding large cash reserves for private gain (Q. Liu et al., 2015). In this context, family firms may be inclined to satisfy their own interests at the expense of those of other internal stakeholders, such as their employees. Although SMEs may also develop CSR strategies concerning employees, these are often not formalised as ethical guidelines and social reports (Russo & Tencati, 2009).

Moreover, in China, interpersonal trust exists mainly within the family network. It is based on blood ties or kinship and excludes external members (Fukuyama, 1996). A typical example is the prevalence of nepotism and the lack of trust given to external managers in Chinese family firms (Zhang & Ma, 2009). The internal CSR of family firms thus follows a ‘differential mode of association’, where the focus extends from family members to those outside the family. In this context, and as stated above, family firms tend to be asymmetrically altruistic (Schulze et al., 2003). As such, it is difficult for non-family members to be genuinely trusted, while family members benefit from quicker paths to promotion, more flexible pay scales, and higher organisational status and career stability. Asymmetric altruism and nepotism result in family firms focusing more on the interests of family members and utilising the firm’s resources to satisfy the family’s needs, neglecting their responsibilities towards other internal stakeholders (Déniz & Suárez, 2005). Based on the above arguments, we propose the following hypothesis:

However, increased family involvement may also encourage family firms to make more internal CSR investments. First, compared to non-family firms, family firms typically have more employees who are related to the family, encouraging the firm to invest in broader CSR, including investments in human resources and human rights (Berrone et al. 2012). This is especially true for SMEs. Second, family firms are more likely to prioritise the interests of internal stakeholders (Marques et al., 2014), achieve SEW goals by ‘sincerely focusing on employee well-being’ (Stavrou et al., 2007), and expect to extend family identity to internal stakeholders who are not family members (Wielsma & Brunninge, 2019).

Third, maintaining family harmony is especially important (Le Breton-Miller & Miller, 2013). In the interests of avoiding internal conflicts within the firm, family firms have a stronger moral responsibility (Meier & Schier, 2021) and a strong desire to protect family members and employees through long-term relationships (Meier & Schier, 2016). Fourth, to retain talent, family firms encourage employees to strive for their sustainable development by actively engaging in CSR (Rivera-Franco et al., 2025). Moreover, establishing long-term relationships with internal stakeholders enhances the family’s social capital and enterprise resilience (Carney, 2005). The above factors motivate family firms to meet their responsibilities towards internal stakeholders. Based on the above arguments, we propose the following hypothesis:

Family Involvement and External CSR

In addition to short-term financial performance, SEW is the primary goal pursued by family firms (Gómez-Mejía et al., 2007). The fulfilment of external CSR can effectively enhance the firm’s reputation (Berrone et al., 2010) and help maintain the family’s control and influence (Berrone et al., 2012), which are valuable socioemotional assets. As such, family firms are primarily driven by social norms to prioritise the family’s SEW, at the expense of short-term growth (Berrone et al., 2010).

Unlike firms with dispersed shareholdings, family firms have concentrated shareholdings held by family members. When a family firm exhibits a lack of CSR, the family can be blamed, and, in serious cases, the family’s reputation and business may be ruined (Deephouse & Jaskiewicz, 2013). Therefore, family firms attach great importance and are motivated to pursue external CSR because it is more socially visible and more easily observed by external stakeholders, creating social pressure (Cruz et al., 2014).

In China, particularly, the rapid rate of growth and wealth accumulation by family firms is often associated with a lack of CSR in initiatives to improve environmental, food safety, and labour conditions (Berrone et al., 2023; Marquis & Qian, 2014). Regarding this point, actively undertaking external CSR can effectively weaken the negative effects noted above. This explains why family firms tend to release more CSR reports to the public (Campopiano & De Massis, 2015).

For SMEs, the motivation to engage in external CSR activities is especially obvious. Compared to large, publicly listed enterprises, SMEs lack high-quality internal resources, face greater financial constraints, and have a lower market share (Park & Ghauri, 2015). This leads enterprises to invest limited resources in external CSR activities, which offer greater social visibility.

External CSR fulfilment can generate positive moral capital among stakeholders and communities, leading them to make more positive judgements of the firm that actively fulfils CSR (Cruz et al., 2014). In particular, when family firms are exposed to the risk of losing both relational and financial capital, CSR can serve as a buffer and insurance mechanism (Shiu & Yang, 2017), protecting their relational assets and income streams from the double loss of economic value (Dyer & Whetten, 2006) and SEW (Dou et al., 2014). Research also indicates that SMEs’ reputations are mainly built through behaviours such as charitable donations (Spence et al., 2003). Consequently, family involvement encourages family firms to obtain this protective mechanism through external CSR.

Family involvement gives managers the power and legitimacy to shape the firm’s goals, strategies, and behaviours (Chrisman et al., 2012). As family involvement increases, the degree to which family managers take ownership and manage the firm increases. Compared with listed companies, owners of SMEs have greater control over their enterprise, and corporate values are largely determined and implemented by the business owners themselves (Hanke & Stark, 2009). External CSR initiatives can sometimes reduce a firm’s cash flow and increase operating costs (Brammer & Millington, 2008), while the economic interests of non-family members may make them more resistant to CSR efforts. In this way, greater family involvement can guarantee the power and legitimacy of family managers to overcome internal resistance and actively fulfil their external CSR (Deephouse & Jaskiewicz, 2013). Based on the above arguments, we propose the following hypothesis:

Even so, increased family involvement may reduce the firm’s external CSR. First, to maintain a high degree of control over the organisation, family firms, especially SMEs, prefer unified ownership and control (Chrisman & Patel, 2012). This leads family firms to rely on their personal wealth or family assets to fund the enterprise (S. Young, 1995), thereby reducing their dependence on external financing. Consequently, the enterprise has a reduced need for external legitimacy and lacks the incentive to invest in external CSR.

Second, families often regard governance structures as tools to pursue family goals. Enterprises with high levels of family involvement are more likely to prioritise family goals (Berrone et al. 2012; Nason et al. 2019) and to use governance mechanisms to strengthen family control. External stakeholders, however, can easily undermine that control (Dick et al., 2021). Consequently, family firms may place less emphasis on external CSR implementation or even adopt mechanisms that violate good corporate governance practices (Cruz et al., 2014; C. D. Jones et al., 2008).

Third, family firms attract less attention from regulators and external stakeholders, reducing their motivation to engage in external CSR. Unlike listed companies, which have decentralised ownership, family firms are concentrated in the hands of a few family owners and managers. This provides owners with the economic incentive to closely supervise managers (Morck et al., 1988), thus attracting less attention from external stakeholders. Existing research suggests that as family involvement increases, the pressure from external stakeholders may decrease (Morck & Yeung, 2004). Furthermore, private (family) firms are predominantly SMEs with a lower market share (Park & Ghauri, 2015), making them less likely to attract close scrutiny from regulators and external stakeholders (Miller et al., 2013), reducing their motivation to actively engage in external CSR. Based on the above arguments, we propose the following hypothesis:

Moderating Role of Formal Governance Mechanisms: Formal Institutions and Formal Decision-Making Procedures

Governance mechanisms consist of formal and informal rules, procedures, and practices that originate from inside and outside the firm to direct and control its behaviour (Chrisman et al., 2018). Governance mechanisms can originate from inside (internal) or outside (external) the firm. Simultaneously, governance mechanisms can be formal or informal. Formal governance mechanisms are codified by regulations, rules, policies, and procedures, whereas informal governance mechanisms are represented by norms and values of society and/or the interests of salient stakeholders.

In corporate governance and strategic decision-making, family firms, particularly those that are privately held, often have informal governance structures and decision-making procedures (Cruz et al., 2014). Informal family governance can align the goals of principals and agents, reduce agency costs, and lower transaction costs within a certain period (Chrisman et al., 2004). However, excessive family involvement can blur the lines between hierarchical authority and personal relationships, making it impossible to separate private goals and behaviours rooted in favour, blood ties, and collateral relationships from the public sphere, and ultimately undermining the efficiency of family governance (Karra et al., 2006). In this regard, the importance of formal family governance is emphasised since the implementation of more binding formal institutions and formal decision-making procedures can mitigate the adverse effects of informal governance (J. Ma, 2021).

We focus on two internal formal governance mechanisms: formal institutions and decision-making procedures. Both are formal governance mechanisms, and they are parallel categories. Formal institutions in this study are the presence of independent directors (Chung & Kim, 2018; Witt et al., 2022). Formal decision-making procedures, which involve decentralising authority and delegating decision-making power (Dekker et al., 2015), are considered a key aspect of professionalising a business (Stewart & Hitt, 2012). In this study, we primarily refer to the level of formalisation in the implementation of management practices and who manages the day-to-day operations. Thus, formal institutions and formal decision-making procedures are two distinct yet parallel components of formal governance mechanisms.

For example, the Lee Kum Kee Group (a Chinese family firm; https://sg.lkk.com/) emphasises family governance by defining organisational norms and mission, and by establishing formal governance structures and policies. These governance structures are recognised within the family and constitute a crucial component of its formal organisation, operating in parallel with the firm’s operational organisation and governance as a market entity. Similarly, in the realm of CSR, we argue that more formalised governance and decision-making procedures in family firms can play a positive role. This is reflected in the fact that it may both weaken (strengthen) the negative (positive) effects of family involvement on internal CSR fulfilment and strengthen (weaken) the incentive (negative) for family involvement in external CSR.

Formal governance mechanisms help weaken the negative effects of informal governance. Internal CSR, such as employee training and insurance, is visible to internal stakeholders, but there is little adequate oversight and pressure to fulfil these obligations (Cruz et al., 2014). As family involvement increases, family managers face less scrutiny. Thus, formal governance institutions and decision-making procedures can help balance family authority and provide effective oversight and checks on family members (J. Ma, 2021), thereby optimising operational and governance efficiency. In informal governance, the presence of non-altruistic motives and nepotism causes family firms to prioritise family members over general employees, particularly non-family members (Cruz et al., 2014). Formal family governance can constrain nepotistic behaviours and balance the interests of family and non-family members, ensuring the fulfilment of internal CSR.

Excessive family involvement allows family managers unrestricted discretionary power (Anderson & Reeb, 2003), reinforcing their behaviours as agents. When internal CSR are perceived as short-term costs (Ciocirlan, 2008), family agents with informational advantages may sacrifice the interests of internal stakeholders to pursue personal gains (Jensen & Meckling, 1976), thereby reducing the firm’s fulfilment of internal CSR. In this situation, developing formal institutions and decision-making processes within the firm can limit over-reliance on informal relational governance, mitigating the negative impacts of family involvement on internal CSR fulfilment.

Based on the above arguments, we propose the following hypothesis:

Establishing formal governance mechanisms may boost the positive impact of family involvement on internal CSR. With increased family involvement and to avoid internal conflicts, family firms exhibit a strong sense of moral responsibility and protectiveness towards employees with whom they have a long-term relationship (Meier & Schier, 2016, 2021). Family firms also expect that providing CSR benefits to employees will help them retain talent and enhance their social capital and corporate resilience (Carney, 2005). In this context, formal governance mechanisms can create a favourable governance environment and improve governance efficiency (Peng, 2004), thereby ensuring that enterprises fulfil their CSR obligations to internal stakeholders. This is especially true for SMEs, where formal governance mechanisms help regulate enterprise behaviour and strengthen the implementation of internal CSR.

Based on the above arguments, we propose the following hypothesis:

As for external CSR, formal governance mechanisms could strengthen the positive impact of family involvement on external CSR. Family firms face legitimacy discounts, which are seen by outside stakeholders as parochialism, nepotism, and rights based on birth rather than professional competency (Claessens et al., 2002; Luo & Chung, 2005). The development of formal governance structures and decision-making procedures can serve as signals of the governance quality, making them more easily recognised and acknowledged by external stakeholders, boosting legitimacy and the availability of resources (Chung & Luo, 2008). This gives family firms greater motivation and ability to enhance their family reputation through the fulfilment of external CSR.

Second, external CSR such as donations and environmental protection often require formalised procedures that demand considerable time, effort, and financial resources to fulfil (Heugens & Dentchev, 2007). However, in family firms, informal governance typically conflicts with formalised procedural standards, thereby increasing the costs of fulfilling external CSR (Ciocirlan, 2008). If the governance of family firms aligns more closely with formal institutions and formal decision-making procedures, these conflicts and costs can be minimised. Research indicates that internal stakeholder pressure correlates with family firms’ increased reliance on substantive CSR strategies, for example, reducing carbon emissions (Block et al., 2023). This suggests that optimising informal family governance structures enables family firms to respond more effectively to internal stakeholder pressures, thereby improving their external CSR performance.

Moreover, short-term external CSR initiatives may reduce cash flow and increase operating costs (Brammer & Millington, 2008), lowering firm value. In this situation, the ‘double-strength’ governance model, which integrates strong relational and contractual governance through informal relationship governance and formal family governance, can significantly enhance the performance of family firms (Mustakallio et al., 2002) by providing resources to fulfil their external CSR. Therefore, as family involvement deepens, rational family firms will seek to establish formal governance structures and policy rules and actively fulfil their external CSR. Based on the above arguments, we propose the following hypothesis:

On the other hand, formal governance mechanisms may weaken the negative effects of family involvement on external CSR. Family firms tend to maintain a unified ownership structure, and SMEs may attract even less attention from external stakeholders, leading to a decreased willingness among family firms to fulfil external CSR. However, lower external CSR investment would damage family SEW, such as family reputation and external stakeholder trust, thereby weakening the long-term value of family firms. From a long-term perspective, this encourages family firms to transform and strengthen their motivation to engage in external CSR. Introducing formal institutions and decision-making procedures could help family firms regulate their behaviour institutionally and be more easily recognised and trusted by external stakeholders, thereby weakening the negative effects of family involvement on external CSR. Based on the above arguments, we propose the following hypothesis:

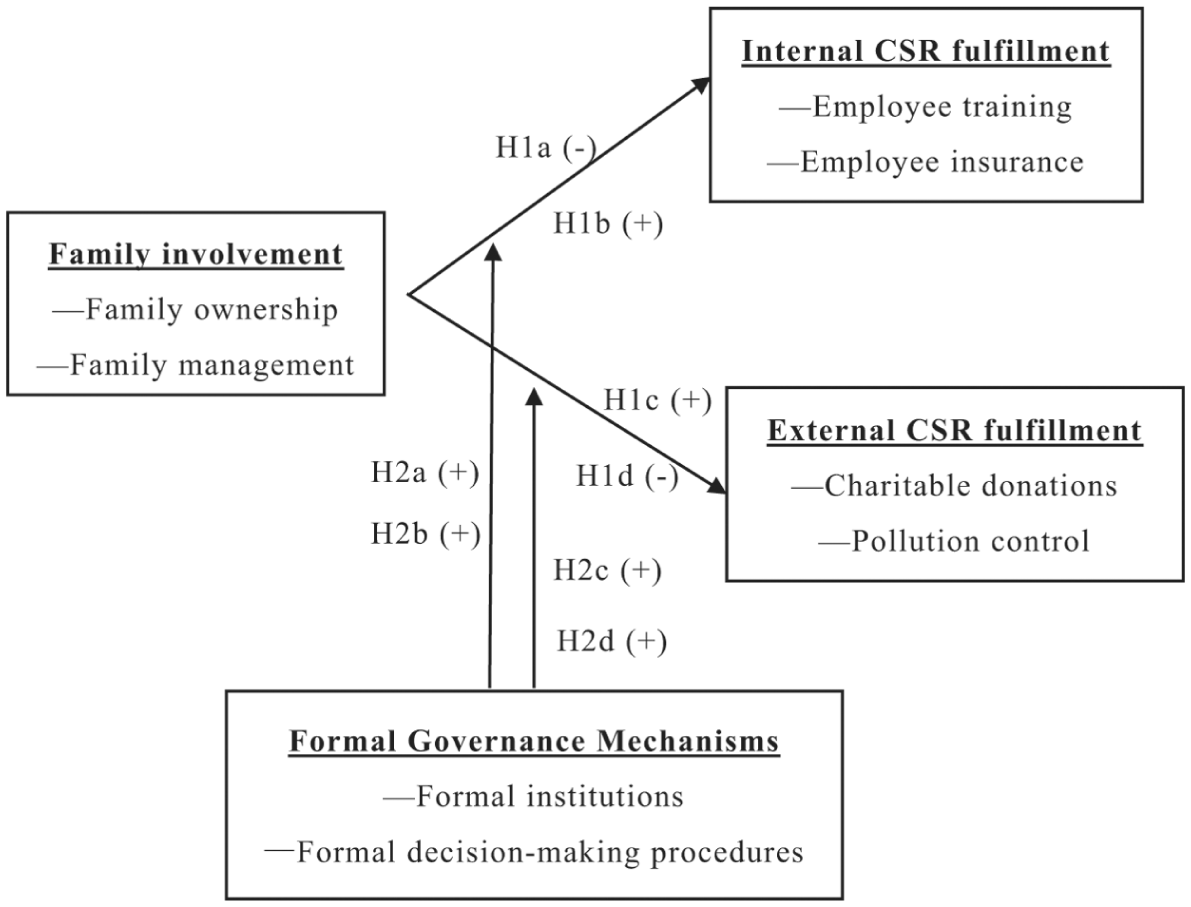

Figure 1 depicts the study’s research model.

The Research Model.

Research Design

Sample and Data Sources

The data in this study come from the CPES for the following years: 1995, 1997, 2000, 2002, 2004, 2006, 2008, 2010, 2012, 2014, 2016, 2018, and 2020. The CPES is currently conducted by the Private Enterprise Research Task Force, which comprises the United Front Work Department of the CPC Central Committee, the All-China Federation of Industry and Commerce, the State Administration for Market Regulation, the Chinese Academy of Social Sciences, and the China Society for Private Economy Research. The survey is implemented by four organisations: the Research Office of the All-China Federation of Industry and Commerce, the Department of Individual and Private Economy Supervision of the former State Administration for Industry and Commerce, the Secretariat of the China Society for Private Economy Research, and the Institute of Sociology of the Chinese Academy of Social Sciences. The United Front Work Department of the CPC Central Committee and the All-China Federation of Industry and Commerce include the survey in their annual work plans and provide funding for the research. The surveys are part of an ongoing national project that collects information from representatives of the Chinese private sector to support the central government’s policymaking processes and to examine various aspects of the corporate governance and business operations of privately owned enterprises (Jia, 2014).

For each survey, a nationwide random sample of privately owned enterprises is generated using multistage stratified sampling across all the Chinese provinces and industries, and direct interviews were conducted with the firm owners. The database provides useful information on a representative sample of Chinese privately owned enterprises. Because the original aim was to collect information on several aspects of business operations, but not on corporate governance, interviewer-induced biases related to firm governance are less likely. The database findings have been used in previous studies on the corporate governance and strategy of private firms in China, and over half the surveyed firms are family businesses (Jia, 2014; Marquis & Qiao, 2020).

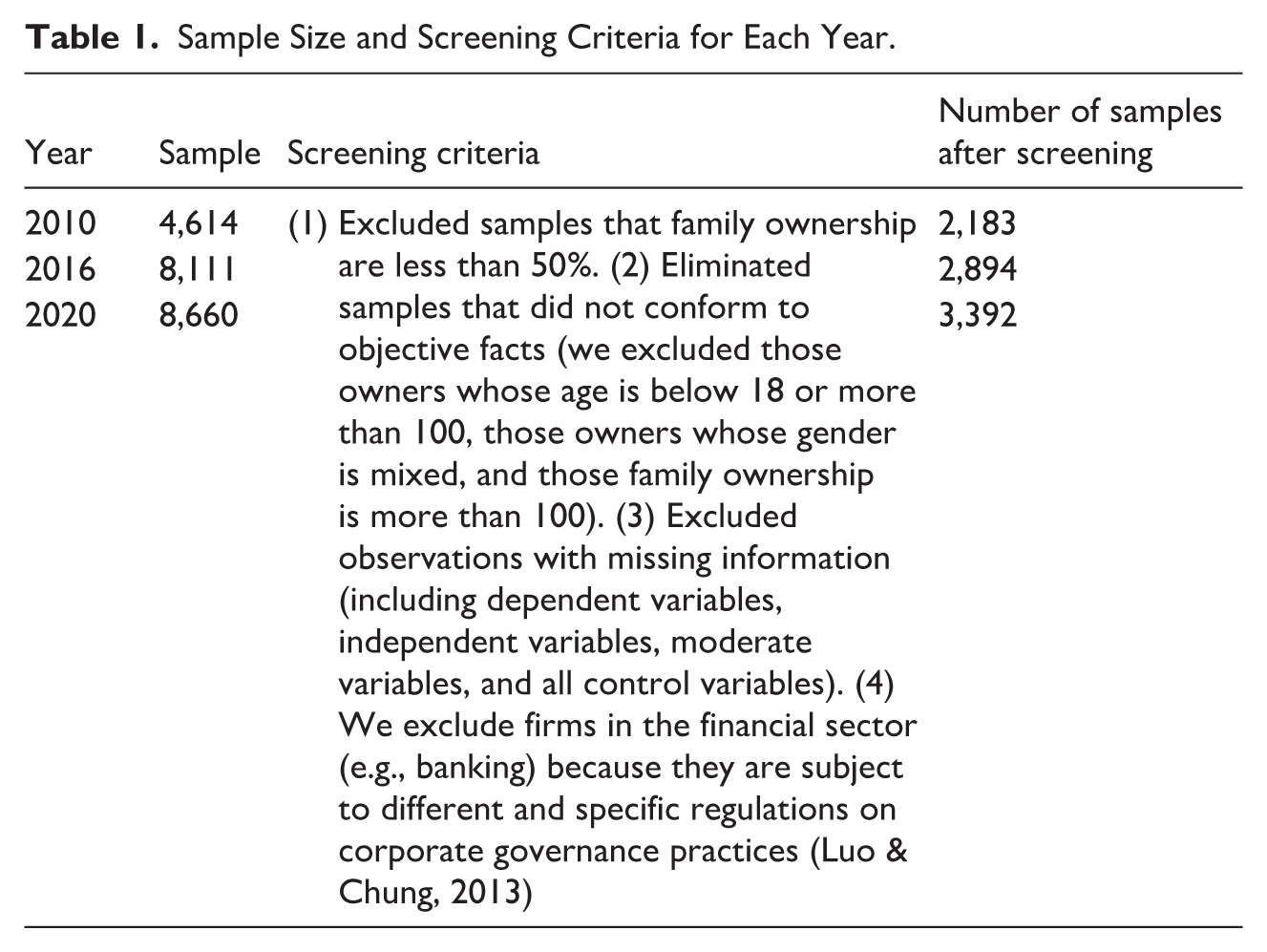

Each year’s survey included the same set of basic questions, though the themes varied. We use data from 2010, 2016, and 2020 for our empirical analysis. Since the data from other years do not include our core variable (i.e., family involvement, CSR), we did not include them in the analysis. Furthermore, the last CPES survey was in 2020, meaning we could only update the sample data to that point. We will update the sample data if the survey is conducted in future years. For 2010, 2016, and 2020, the sample sizes are 4,614, 8,111, and 8,660 enterprises, respectively.

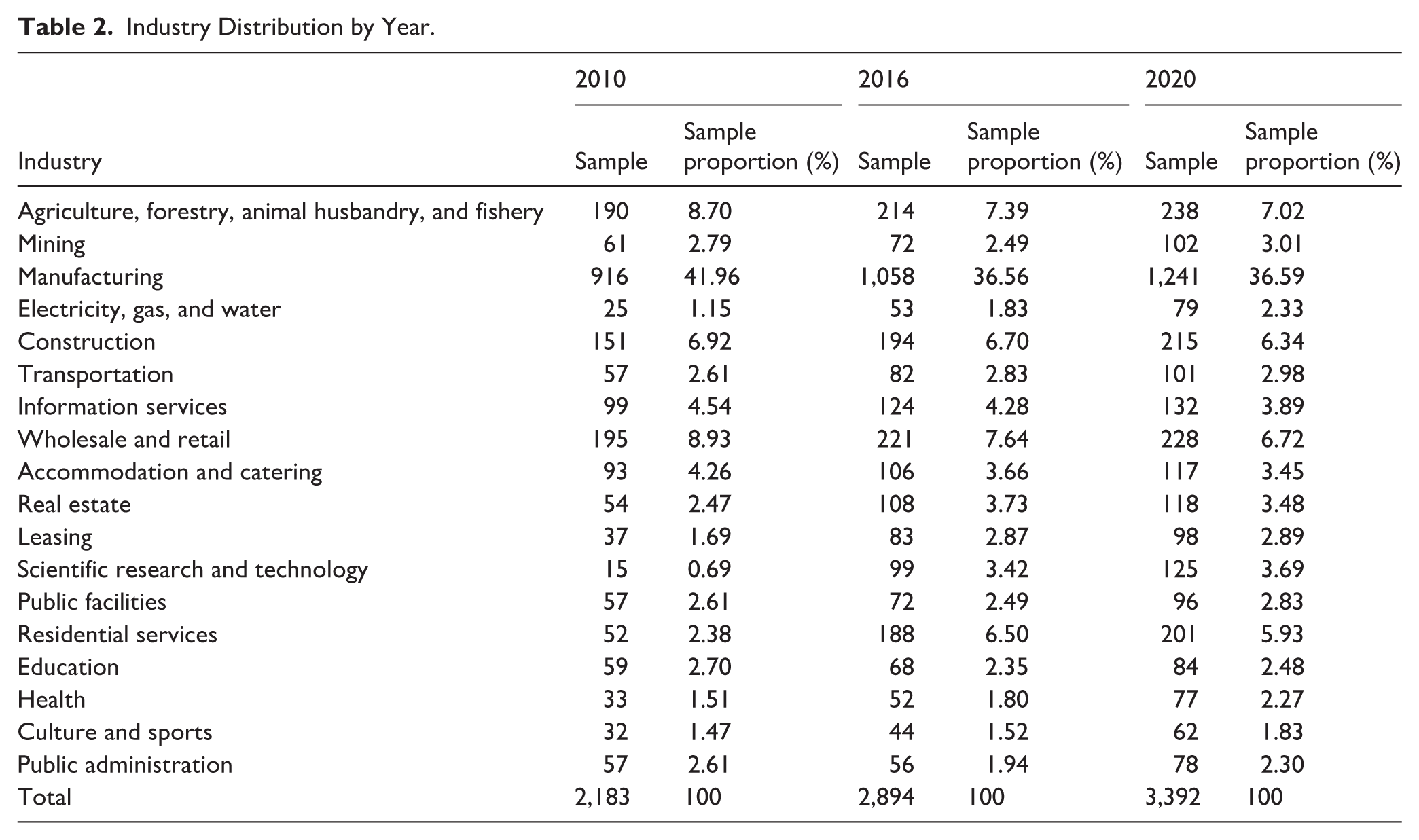

We then implemented the following measures to ensure high-quality data. First, following previous studies (Anderson & Reeb, 2004; Chrisman & Patel, 2012), the inclusion criteria were that the firm is a private enterprise with more than 50% family ownership 2 and with at least one founding family member on the board of directors or the top management team (TMT). Second, to ensure the accuracy and consistency of the data, we eliminated observations that did not conform to objective facts 3 and excluded observations with missing information (including dependent, independent, moderator, and all control variables). Third, we excluded firms in the financial sector (e.g., banking) because they are subject to different and specific regulations on corporate governance practices (Luo & Chung, 2013). Finally, drawing on previous research (Jia, 2014), we constructed a pooled cross-sectional dataset of 8,469 family businesses. Of these, 2,183 observations are from 2010, 2,894 from 2016, and 3,392 from 2020. Tables 1 and 2 show the sample size, screening criteria, and industry distribution for each survey year. Overall, across all three surveys, manufacturing enterprises account for the largest proportion, comprising 41.96%, 36.56%, and 36.59% of the sample in 2010, 2016, and 2020, respectively.

Sample Size and Screening Criteria for Each Year.

Industry Distribution by Year.

Regression Model Settings

Based on the research hypotheses, the following models are constructed for testing:

In Model (1), which is used to test Hypotheses 1a and 1b, Socres denotes CSR (including internal and external dimensions), Faminvol indicates family involvement (as owners and managers), and Con represents the control variables. In Model (2), which is used to test Hypotheses 2a and 2b, FormInsti denotes the formal governance mechanisms (including formal institutions and formal decision-making procedures). In Model (3), which is used to test Hypotheses 3a and 3b, while Model (4) is used to test Hypothesis 3c. Performance denotes firm performance, while Socresin and Socresout denote internal and external CSR, respectively.

Variable Measurements

Family Involvement

We measure the extent of family involvement in family firms across two dimensions: family ownership and family management (Chrisman et al., 2012; Dou et al., 2014). Family owners’ involvement is measured as the ratio of family-member ownership to total ownership. Family involvement in management is measured as the ratio of family members in management positions to total managers.

Internal CSR and External CSR

We categorise CSR into internal and external dimensions, according to different stakeholder types (Farooq et al., 2017; Hawn & Ioannou, 2016; Yin et al., 2024). We define internal CSR as an internally focused action aimed at achieving structural change (Hawn & Ioannou, 2016). Internal CSR focuses on employee welfare and business ethics, for example, through internal education and vocational training (Kim et al., 2010). We measure family firms’ commitment to CSR concerning employees by the amount spent on employee training and employee social insurance.

External CSR refers to outwardly focused actions, mainly directed at external stakeholders, such as actions designed to gain recognition from external members and organisations (McDonnell & King, 2013; Sine et al., 2007). Typical external CSR initiatives involve poverty alleviation (Jenkins, 2005), responses to climate change (Le Menestrel et al., 2002), and environmental sustainability (Basu & Palazzo, 2008). Based on this, we used expenditure on charitable donations and pollution control to measure external CSR.

For data processing, we use the natural logarithms of expenditure on employee training, social insurance, charitable donations, and pollution control. Then, following Yin et al. (2024), we conduct a principal component analysis to extract a common factor for employee training and employee social insurance expenditure as a measure of internal CSR. The common factor for charitable donations and pollution control expenditure represents external CSR.

Formal Governance Mechanisms

Formal governance mechanisms mainly include formal institutions and formal decision-making processes. We measure formal institutions as the proportion of independent directors (percentage of independent directors on the board; Chung & Kim, 2018; Witt et al., 2022). Formal decision-making procedures are measured by determining ‘who is responsible for the daily management of the enterprise’ (Dekker et al., 2015; Mustakallio et al., 2002). This variable is assigned a value of 1 if professional managers are responsible for the enterprise’s daily management, and 0 otherwise.

Control Variables

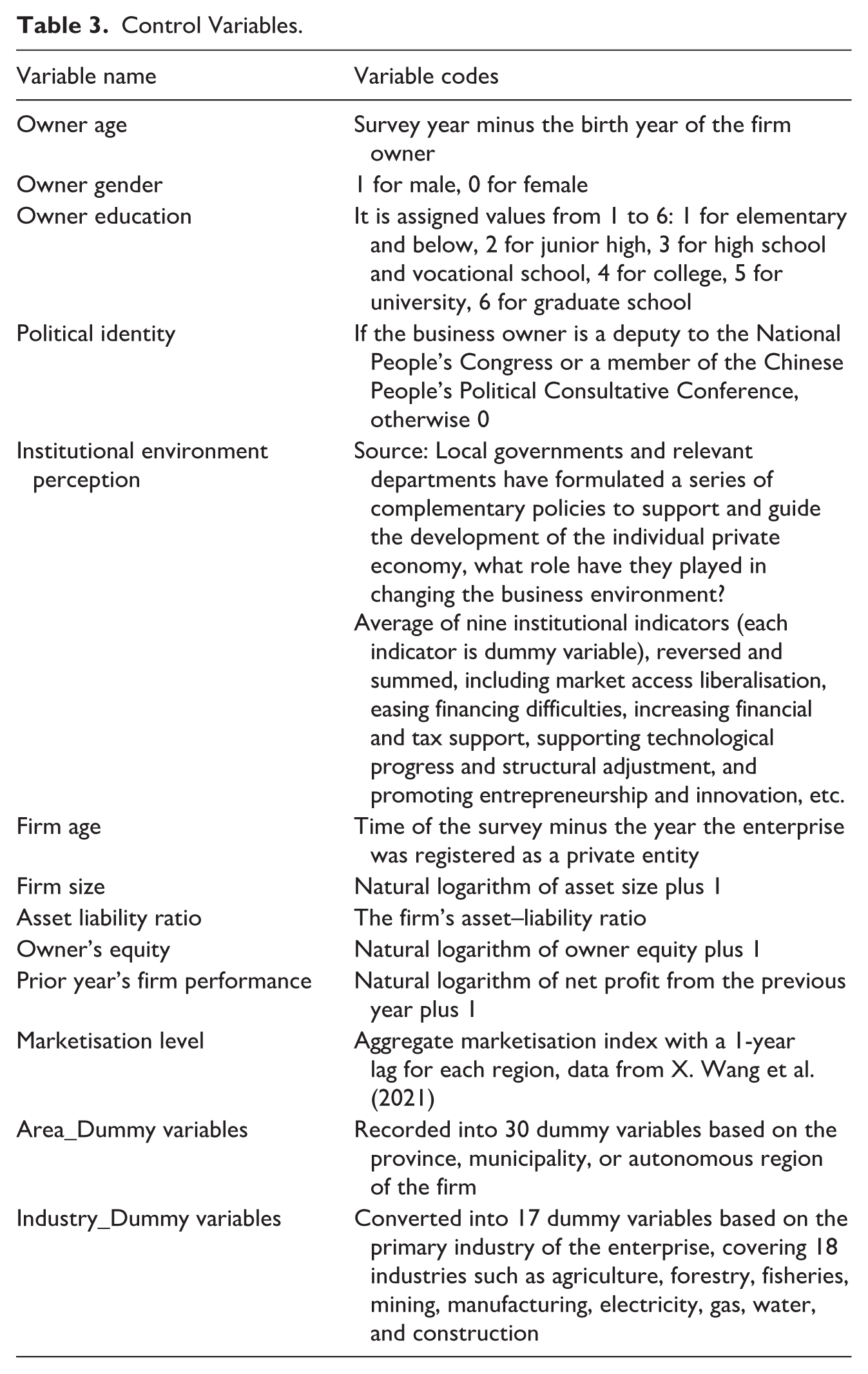

The personal characteristics and firm-level traits of top managers significantly influence CSR (O. Bertrand et al., 2021; Gupta et al., 2021; Ji et al., 2021). Therefore, we include owner and firm-level control variables. At the ownership level, we control for the family owner’s gender, age, education, political identity, and perceived institutional environment. At the firm level, we control for firm age, asset size, asset–liability ratio, owner’s equity, prior year’s performance, and industry type. We also control for area-level variables, including the region where the firm is located and the level of marketisation. Control variable measurements are shown in Table 3.

Control Variables.

Empirical Results and Discussion

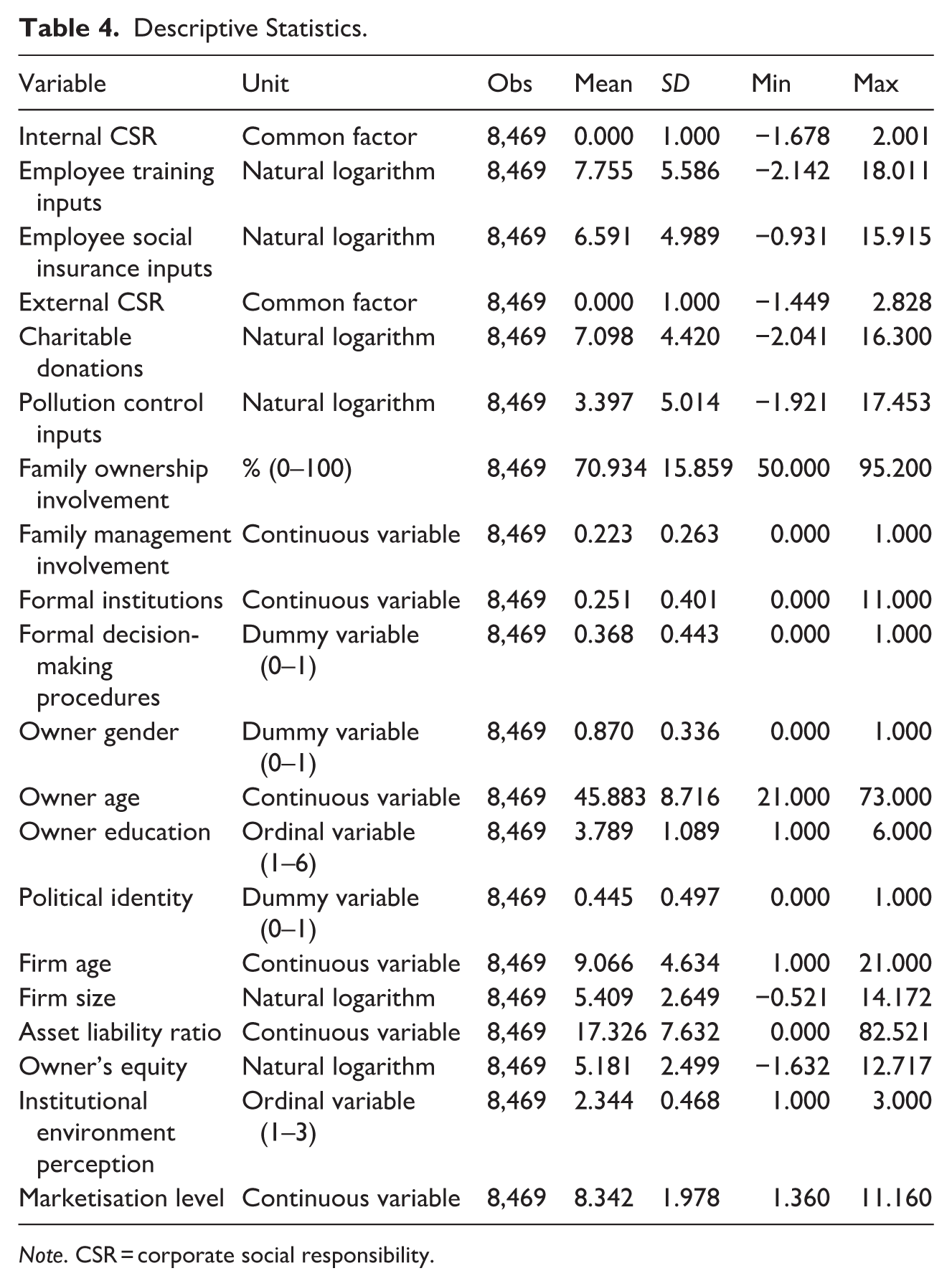

Descriptive Statistics

Tables 4 and 5 present the descriptive statistics and correlation coefficients of this study. Table 4 shows that all variables are within a reasonable range. The minimum and maximum values of family owners’ involvement are 50% and 95.2%, respectively, with an average value of 70.9%. The average level of management involvement is 22.3%. There are large differences in internal CSR, external CSR, net profit, and sales revenue among the family firms surveyed.

Descriptive Statistics.

Note. CSR = corporate social responsibility.

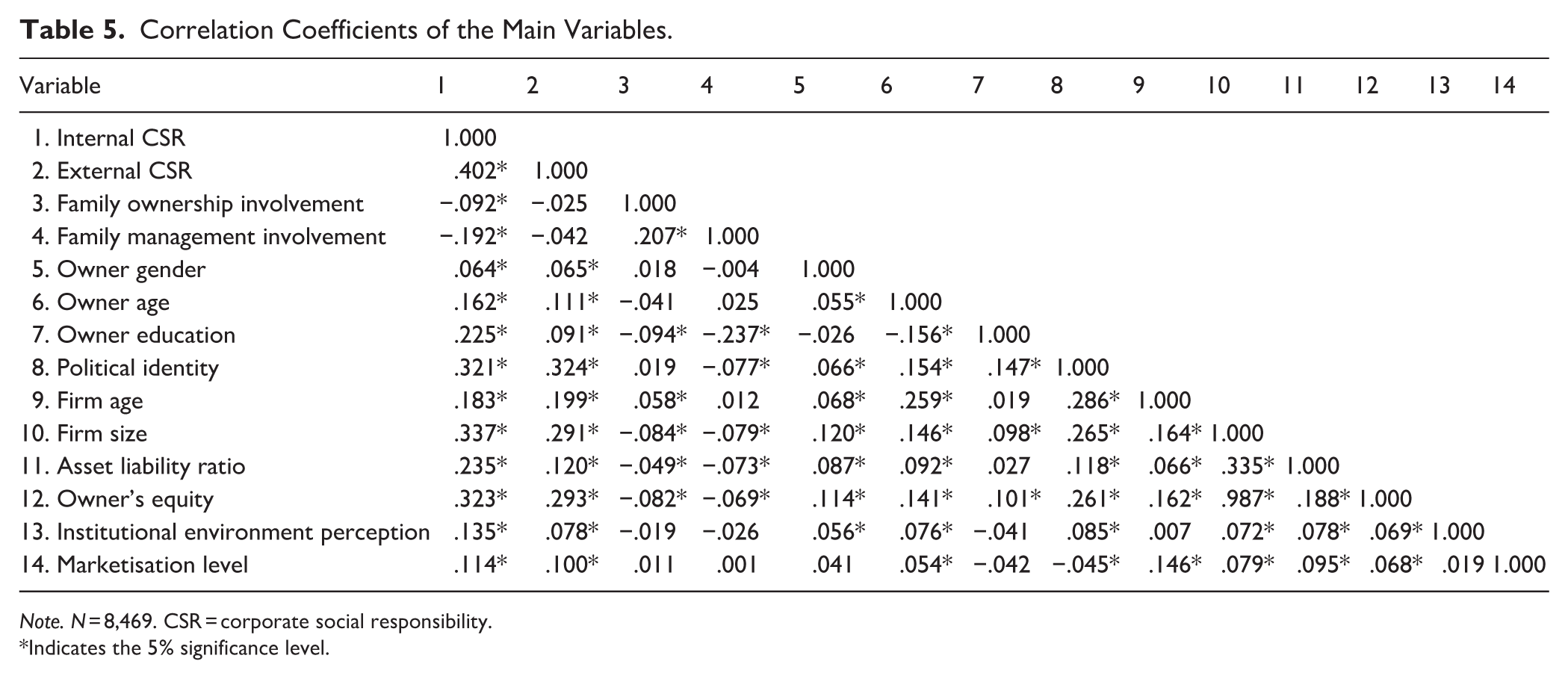

Correlation Coefficients of the Main Variables.

Note. N = 8,469. CSR = corporate social responsibility.

Indicates the 5% significance level.

Comparing the descriptive results with the existing CPES survey results (Ge & Micelotta, 2019; Jia, 2014; W. Li et al., 2015; Marquis & Qiao, 2020), we find that the personal characteristics of owners, such as age, gender ratio, education, and political identity, remained consistent across survey years. As regards enterprise characteristics, firm age, average sales, and family ownership fluctuated in different survey years. After 2008 and 2009, charitable donations showed a decreasing trend over the following 10 years, and fluctuations across enterprises increased.

Table 5 shows that family involvement in ownership and management is significantly negatively correlated with internal CSR, providing preliminary support for Hypothesis 1a, whereas its impact on external CSR is not supported. A regression analysis is conducted to further examine the causal relationships.

Hypothesis Testing

Our data analysis is performed using STATA 12.0 software (StataCorp, Texas, USA). The FGLS method is employed to mitigate problems of heteroscedasticity and outliers. Continuous variables are winsorised at the 1% level. Continuous moderating variables are mean-centred. All regression models passed the multicollinearity test.

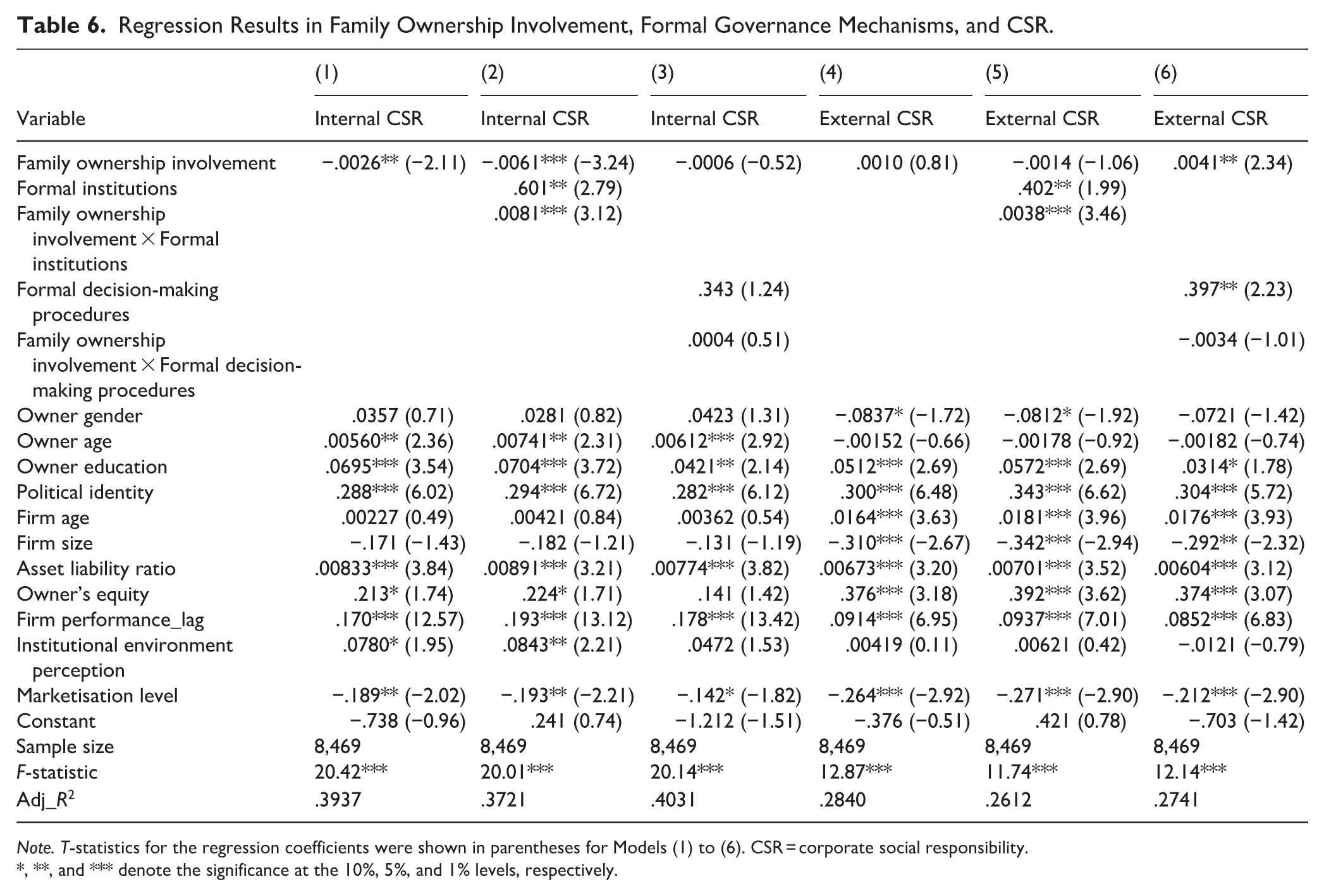

Table 6 presents the regression results for family involvement in ownership on CSR and the moderating effects of formal institutions and formal decision-making procedures. Models (1) to (3) report the impact of family ownership involvement on internal CSR. Model (1) shows that family ownership involvement is significantly negatively related to internal CSR (β = −.0026, p < .05). Model (2) shows that the interaction between family ownership involvement and formal institutions is significant and positive (β = .0081, p < .01). Thus, family ownership involvement reduces internal CSR fulfilment, and the establishment of formal institutions weakens this negative effect. Model (3) shows that the interaction between family ownership involvement and formal decision-making procedures is positive but not significant (β = .0004, p > .1), indicating that formal decision-making procedures cannot weaken the adverse effects of family involvement on internal CSR. Thus, Hypothesis 1a is supported, and Hypothesis 2a is partially supported.

Regression Results in Family Ownership Involvement, Formal Governance Mechanisms, and CSR.

Note. T-statistics for the regression coefficients were shown in parentheses for Models (1) to (6). CSR = corporate social responsibility.

, **, and *** denote the significance at the 10%, 5%, and 1% levels, respectively.

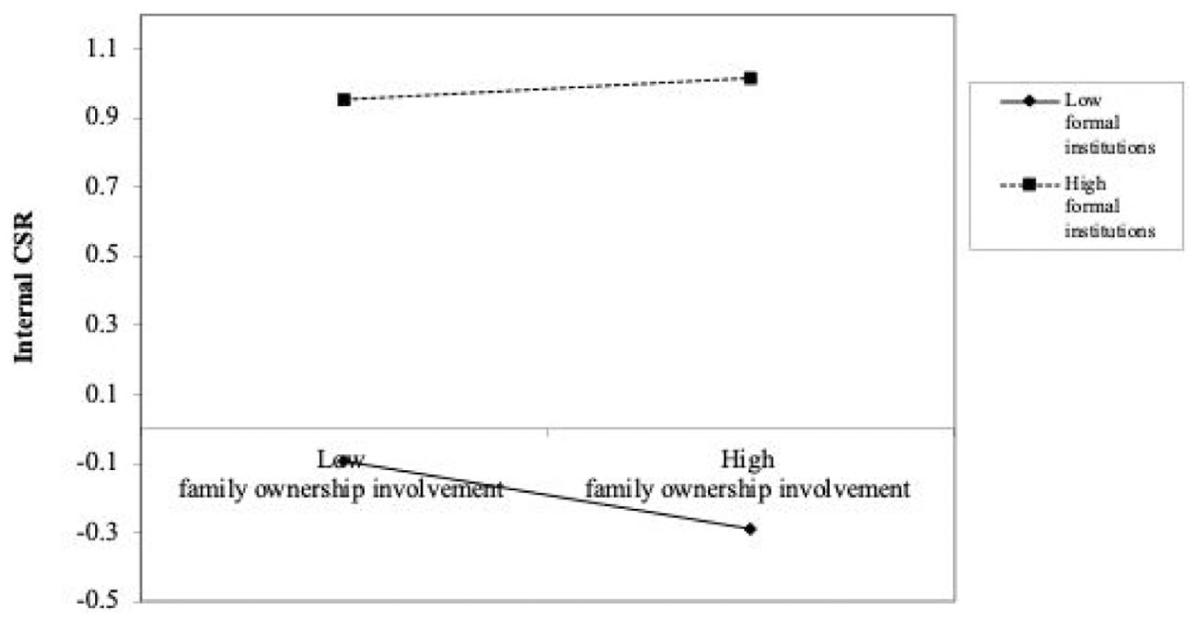

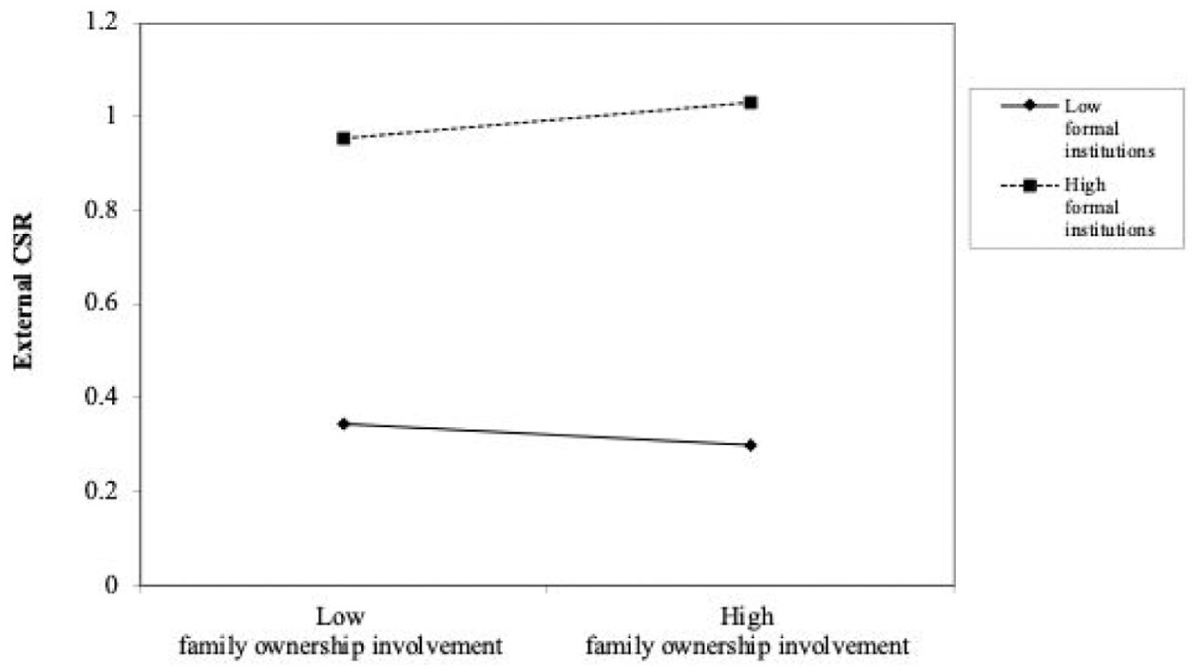

Models (4) to (6) show the effects of family ownership involvement on external CSR. Model (4) shows that family ownership involvement is positively but insignificantly related to external CSR (β = .0010, p > .1). Model (5) shows that the interaction between family ownership involvement and formal institutions is significant and positive (β = .0038, p < .01). These results suggest that family ownership involvement can, to some extent, promote firms’ external CSR and that the establishment of formal institutions reinforces this positive effect. Model (6) shows that the interaction between family ownership involvement and formal decision-making procedures is not significant. Therefore, Hypotheses 1c and 1d are not supported, and Hypothesis 2c is partially supported. The moderating effects reported in Models (3) and (5) are shown in Figures 2 and 3, respectively.

Moderating Effect of Formal Institutions on the Impact of Family Ownership Involvement on Internal CSR.

Moderating Effect of Formal Institutions on the Impact of Family Ownership Involvement on External CSR.

Table 7 presents the regression results on the impact of family management involvement on CSR and the moderating effects of formal institutions and formal decision-making procedures on this relationship. Models (1) to (3) report the impact of family management involvement on internal CSR. Model (1) shows that family management involvement is significantly negatively related to internal CSR (β = −.313, p < .01). Models (2) and (3) show that the interaction between family management involvement and formal institutions (β = −.0701, p > .1), as well as the interaction between family management involvement and formal decision-making procedures (β = .0247, p > .1), are not significant. Thus, family management involvement reduces firms’ fulfilment of internal CSR. However, the establishment of formal institutions and formal decision-making procedures does not weaken this negative effect. Thus, Hypothesis 1a is supported, but Hypotheses 2a and 2b are not supported.

Regression Results in Family Management Involvement, Formal Governance Mechanisms, and CSR.

Note. T-statistics for the regression coefficients were shown in parentheses for Models (1) to (6). CSR = corporate social responsibility.

, **, and *** denote the significance at the 10%, 5%, and 1% levels, respectively.

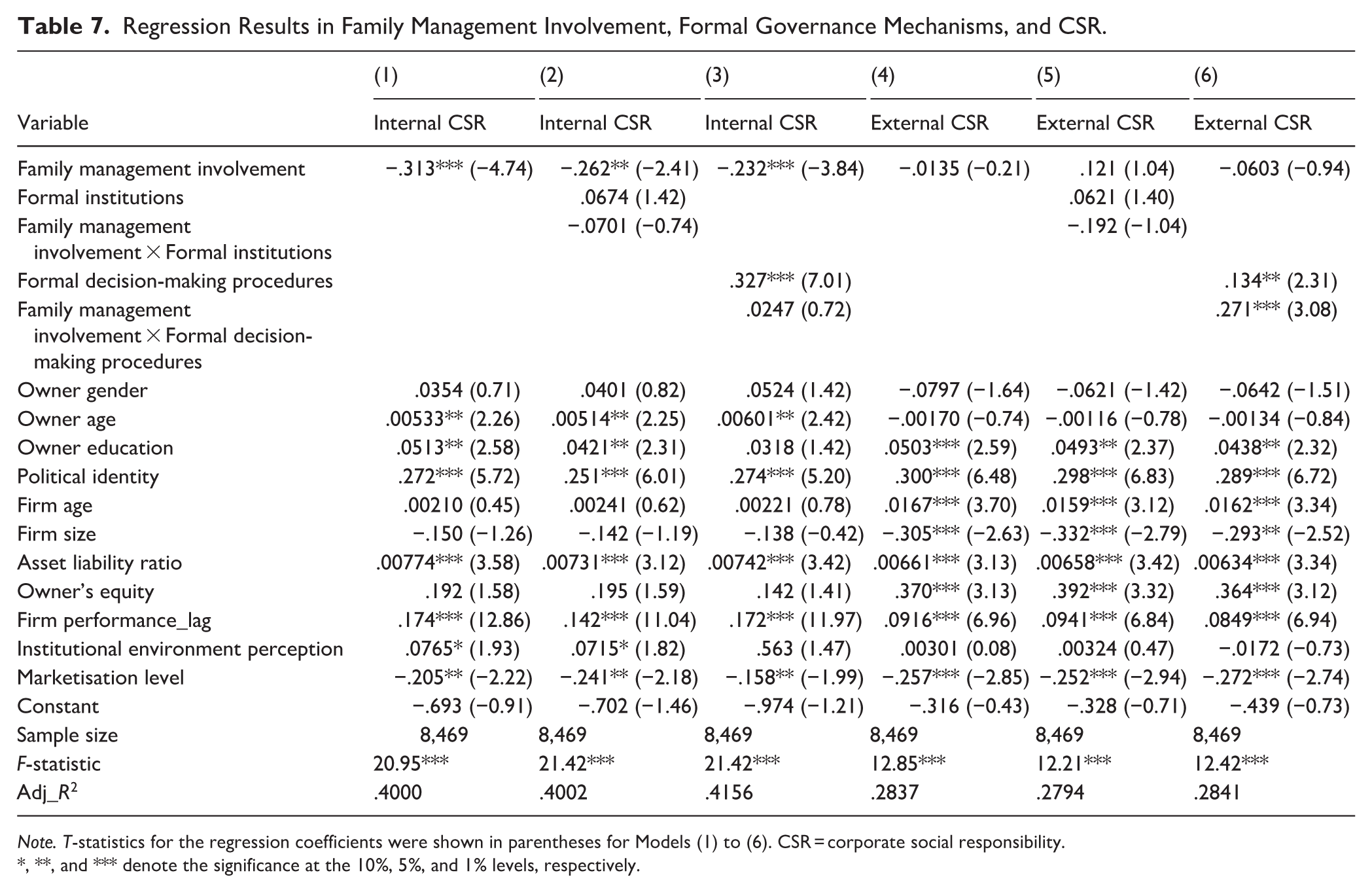

Models (4) to (6) report the impact of family management involvement on external CSR. Model (4) shows that family management involvement is negatively and insignificantly related to external CSR (β = −.0135, p > .1). Models (5) and (6) show that the interaction term between family management involvement and formal institutions (β = −.192, p > .1) is insignificant, whereas the interaction term between family management involvement and formal decision-making procedures is significantly positive (β = .271, p < .01). Therefore, family management involvement does not have a significant positive effect on the fulfilment of external CSR, but its interaction with formal decision-making procedures significantly drives firms to actively fulfil their external CSR. Thus, Hypotheses 1c and 1d are not supported, and Hypothesis 2c is partially supported. The moderating effects in Model (6) are shown in Figure 4.

Moderating Effect of Formal Decision-Making Procedures on the Impact of Family Management Involvement on External CSR.

In summary, the regression results indicate that the impact of different measures on formal governance mechanisms varies for family ownership involvement and family management involvement. Formal institutions have a greater impact on family ownership involvement, while formal decision-making procedures have a greater impact on family management involvement.

This result may be related to the different functions of professional managers and independent directors. Independent directors play a primarily supervisory role on the board of directors of the enterprise. They are not influenced by affiliations with the enterprise, shareholders, or management (Crespí-Cladera & Pascual-Fuster, 2014), and do not directly participate in enterprise management. They typically serve shorter terms and have less contact with the management team or the family (Samara & Berbegal-Mirabent, 2018). They primarily fulfil their duties through independent judgement, which helps improve the quality of board oversight and reduces the likelihood of conflicts of interest. Therefore, independent directors primarily play a supervisory role within the enterprise rather than directly participating in management, thus having a greater impact on family ownership involvement.

Introducing professional management is one way to professionalise the management of family firms. By taking charge of the day-to-day management of a family firm, they can significantly influence the decisions and management decisions of the family firm’s management team. The essence of a professional manager is to introduce a new management model into family firms through professional (non-family) management (Dyer, 1986) to help the enterprise achieve growth and expansion (Hall & Nordqvist, 2008), thereby increasing family management involvement.

Robustness Tests

Alternative Variable

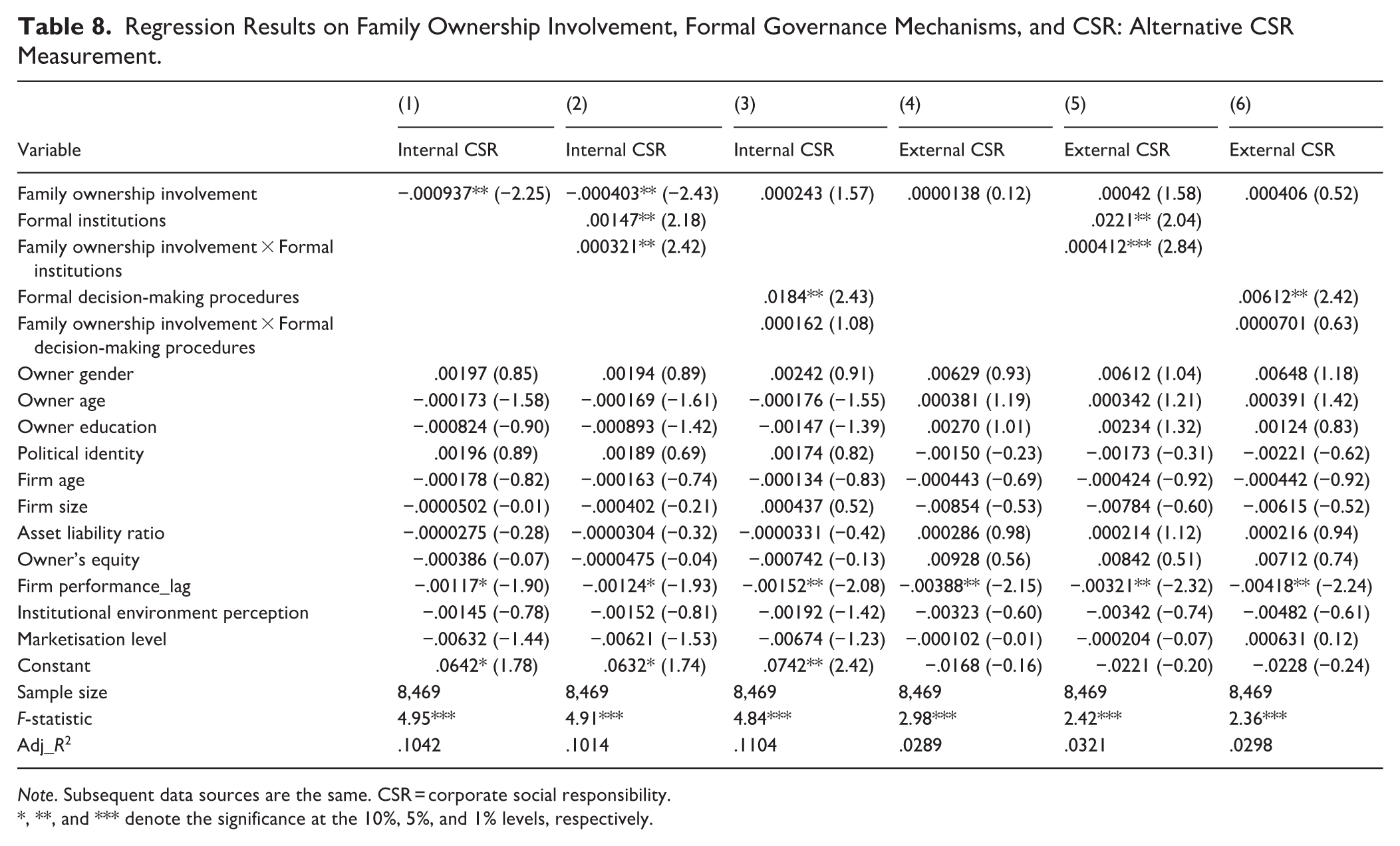

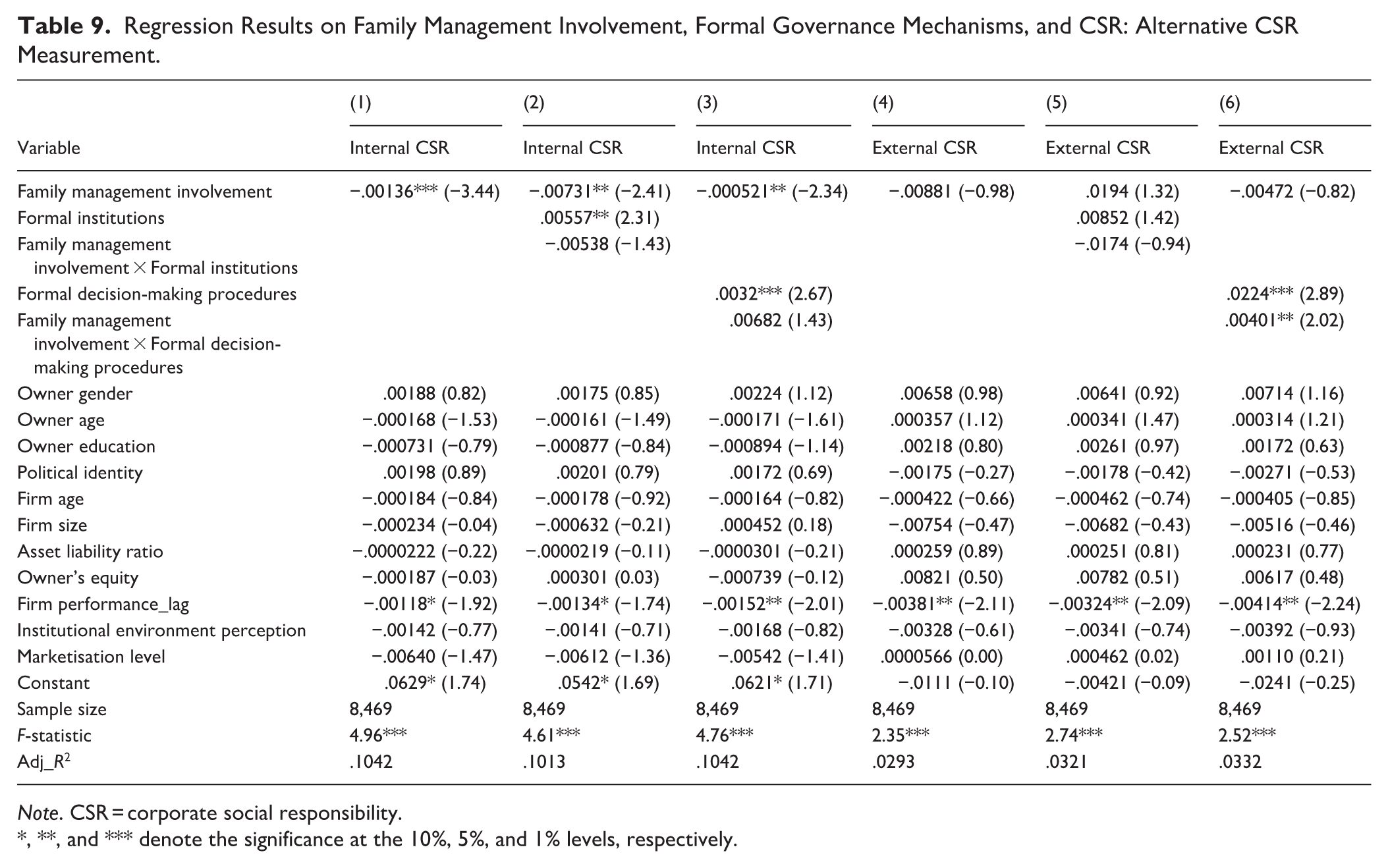

Further regression analysis is conducted, substituting alternative measures of CSR. Internal CSR is measured using the mean value of employee-training-investment intensity (employee-training investment/sales revenue) and employee-social-insurance-investment intensity (employee social insurance investment/sales revenue). For external CSR, we use the mean intensity of charitable donations (charitable donations/sales revenue) and of investment in pollution control (investment in pollution control/sales revenue). Tables 8 and 9 show the regression results for family ownership involvement and family management involvement, respectively. The results are consistent with previous findings.

Regression Results on Family Ownership Involvement, Formal Governance Mechanisms, and CSR: Alternative CSR Measurement.

Note. Subsequent data sources are the same. CSR = corporate social responsibility.

, **, and *** denote the significance at the 10%, 5%, and 1% levels, respectively.

Regression Results on Family Management Involvement, Formal Governance Mechanisms, and CSR: Alternative CSR Measurement.

Note. CSR = corporate social responsibility.

, **, and *** denote the significance at the 10%, 5%, and 1% levels, respectively.

Excluding Alternative Explanations

We also conduct analyses to exclude alternative explanations. Due to space constraints, not all results are reported here, but interested readers may request a copy from the authors. First, we exclude the alternative explanation of industry differences in industry type. Firms in the high-tech sector rely heavily on the knowledge and human capital of their personnel, which may lead them to place greater emphasis on internal CSR, while lowering their willingness to engage in external CSR. We test this by dividing the sample into high-tech firms (information services, research, and technology) and non-high-tech firms and conducting separate regressions. The results indicate no significant difference between these groups in the direction or significance of the main variables, thereby ruling out alternative explanations based on industry characteristics. Second, we exclude differences in family-firm types. Family firms exhibit significant heterogeneity. Founder-controlled firms (with no family members on the TMT or board; Luo & Chung, 2013) differ considerably from traditional family firms in terms of their goals and behavioural logic (Miller et al., 2011). We exclude founder-controlled firms and find that none of the regression results change fundamentally.

Further Tests

CSR and Firm Performance

The fulfilment of internal CSR within family firms can enhance internal cohesion (Marques et al., 2014), while the fulfilment of external CSR can boost the company’s reputation and garner support and recognition from external stakeholders (Berrone et al., 2010). Another interesting research question in this study concerns the possible effects of internal and external CSR on the performance of family firms.

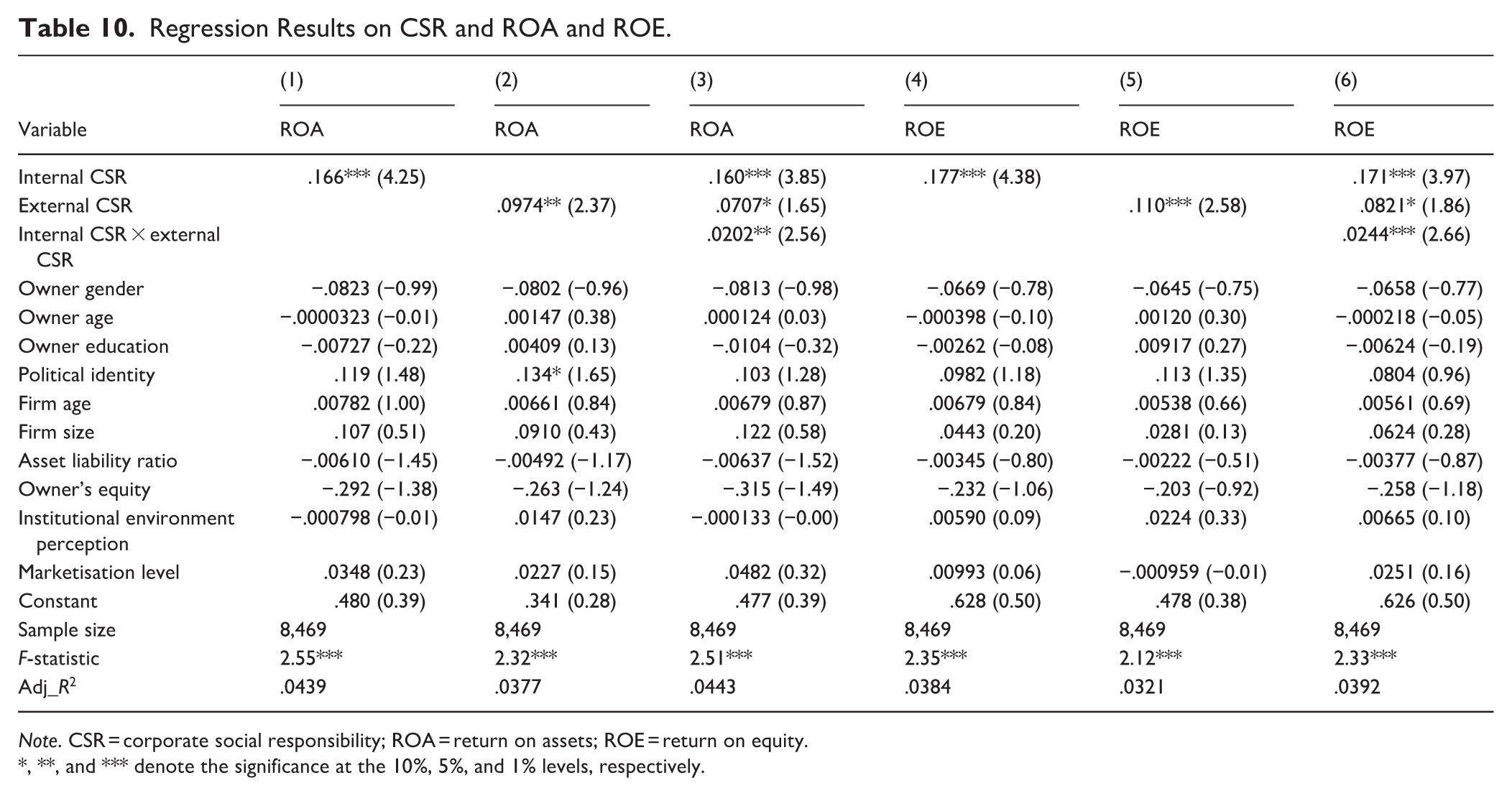

Referring to existing studies (Dekker et al., 2015), we use return on assets (ROA) and return on equity (ROE) to measure firm performance. The calculation formulas are: ROA = net profit/total assets; ROE = net profit/shareholders’ equity.

Table 10 shows the regression results of the impact of CSR on ROA and ROE. The results of Model (1) to (3) show that both internal CSR (β = .166, p < .01) and external CSR (β = .0974, p < .05) are significantly and positively correlated with ROA, and their interaction term is also significant and positively correlated with ROA (β = .0202, p < .05). The results for Models (4) to (6) are similar. Our results indicate that both internal and external CSR in family firms can significantly improve firm performance. Moreover, their effect is complementary and mutually reinforcing, and they exert a synergistic effect on firm performance.

Regression Results on CSR and ROA and ROE.

Note. CSR = corporate social responsibility; ROA = return on assets; ROE = return on equity.

, **, and *** denote the significance at the 10%, 5%, and 1% levels, respectively.

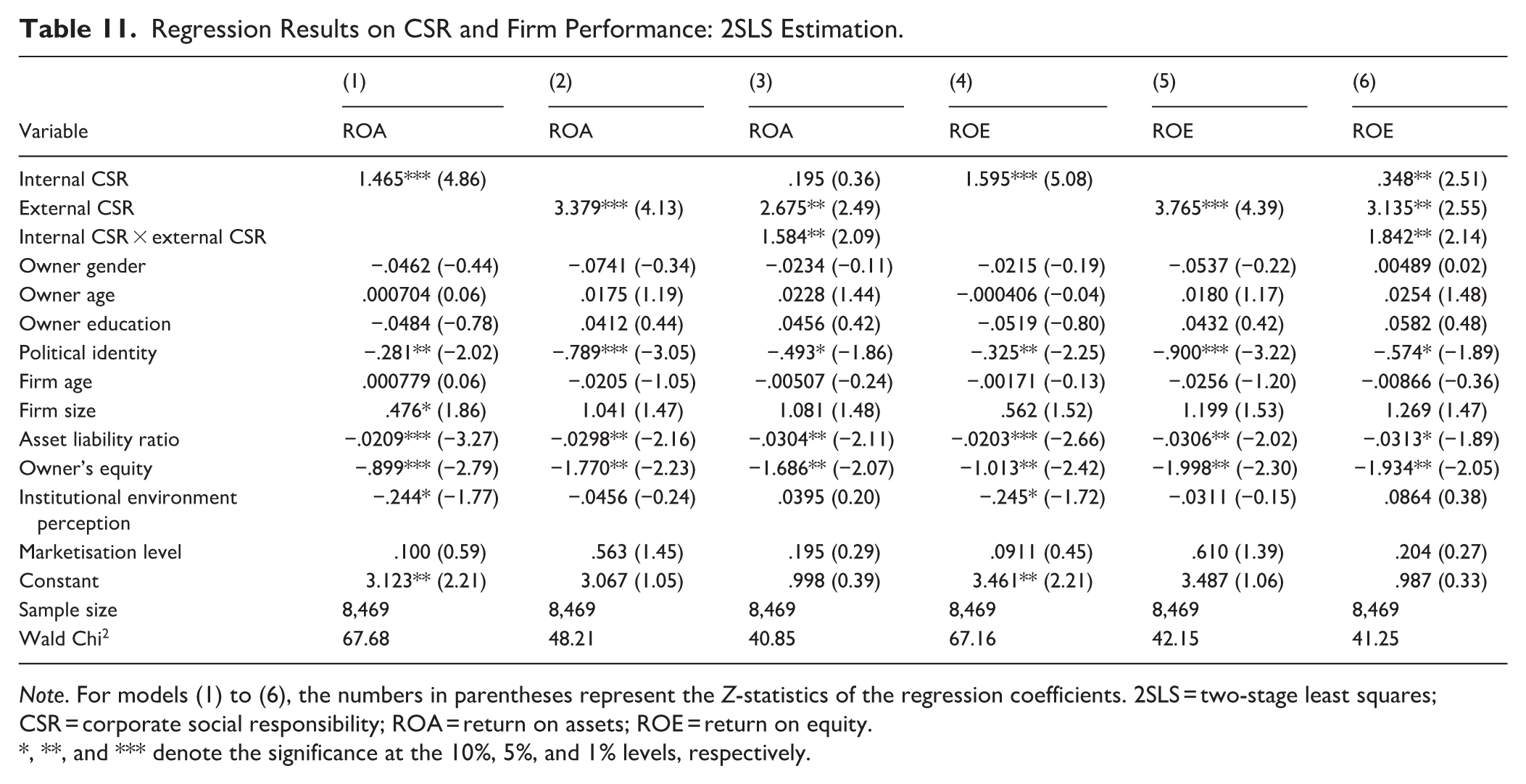

We address potential endogeneity by analysing the above relationships using two-stage least squares (2SLS), the Heckman two-stage method, and propensity score matching (PSM). First, we use an instrumental variable (IV) for 2SLS estimation. Following Fisman and Svensson’s (2007) approach of using regional means as IVs, this article uses the regional means of internal and external CSR inputs as IVs. Table 11 reports the 2SLS regression results.

Regression Results on CSR and Firm Performance: 2SLS Estimation.

Note. For models (1) to (6), the numbers in parentheses represent the Z-statistics of the regression coefficients. 2SLS = two-stage least squares; CSR = corporate social responsibility; ROA = return on assets; ROE = return on equity.

, **, and *** denote the significance at the 10%, 5%, and 1% levels, respectively.

Before using IVs, their validity needs to be examined. The overidentification test shows that p = .3631, supporting the null hypothesis that all IVs are exogenous (Stock et al., 2002). Based on the weak-IV test results, the partial F-statistic = 13.421, which exceeds the critical value of 11.59 (Stock et al., 2002); therefore, the null Hypothesis of weak IV can be rejected. This indicates that the chosen IVs are valid. The results in Table 11 show that both internal and external CSR are significantly and positively related to firm performance, and their interaction terms are also significant and positive, suggesting that the findings are robust.

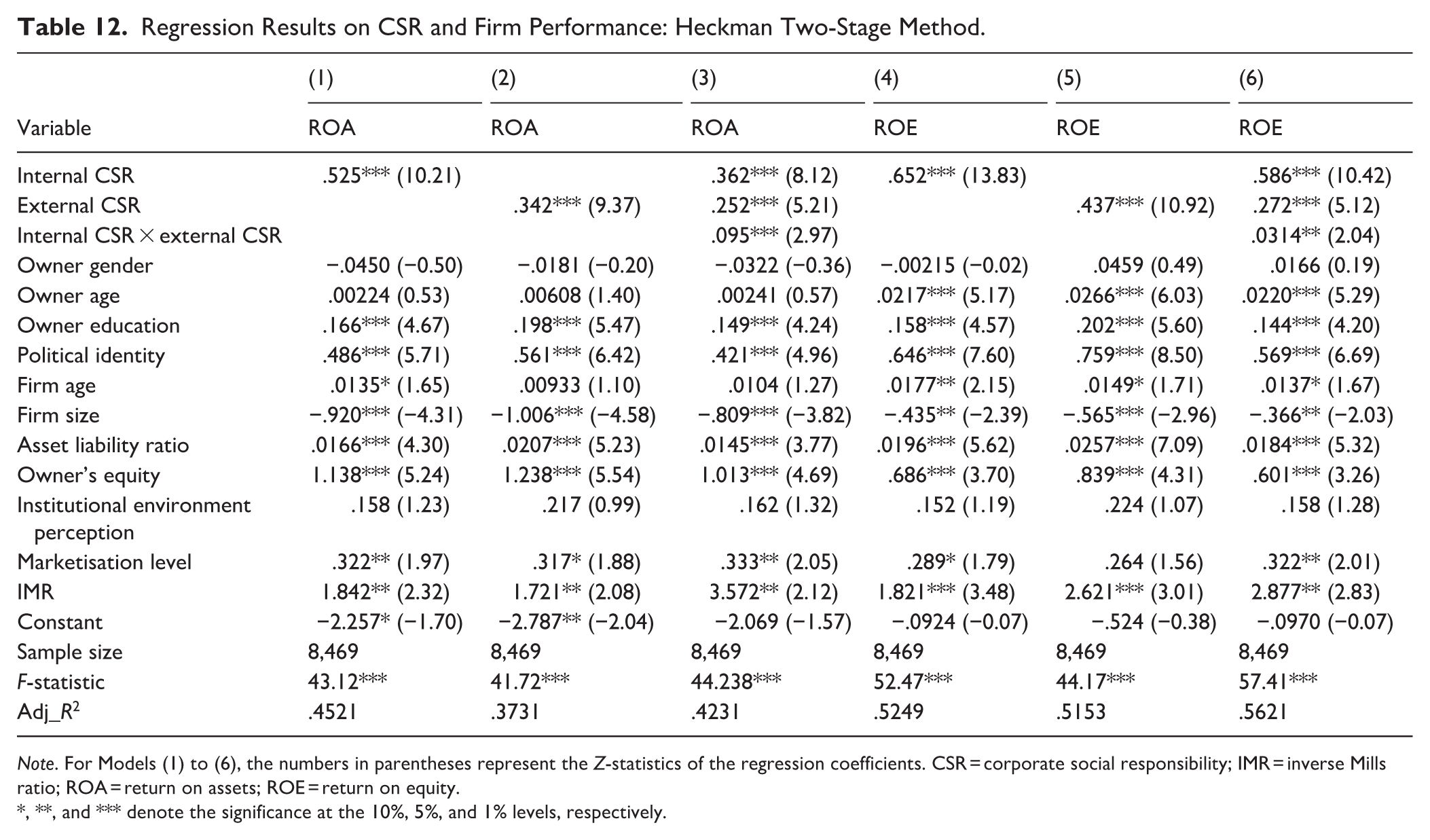

Second, we use the Heckman two-stage method (Heckman, 1979) to address the problem of self-selection bias and add the inverse Mills ratio (IMR) as an IV. Specifically, in the first stage, we use the following as dependent variables: whether the enterprise conducted internal CSR investment (0–1 dummy variable) and whether it conducted external CSR investment (0–1 dummy variable). The average values of ‘industry – region’ for internal CSR (Internal CSR_M) and external CSR (External CSR_M) are taken as IVs to construct the probit model, calculate the IMR, and include it in the second stage of the regression analysis.

Table 12 presents the results of the Heckman two-stage regression analysis. These show that family firms can significantly improve their performance by fulfilling both internal CSR and external CSR, and that the two have a complementary effect. After addressing the self-selection problem, the results of the Heckman two-stage regression are consistent with the article’s conclusions, indicating that the results are robust.

Regression Results on CSR and Firm Performance: Heckman Two-Stage Method.

Note. For Models (1) to (6), the numbers in parentheses represent the Z-statistics of the regression coefficients. CSR = corporate social responsibility; IMR = inverse Mills ratio; ROA = return on assets; ROE = return on equity.

, **, and *** denote the significance at the 10%, 5%, and 1% levels, respectively.

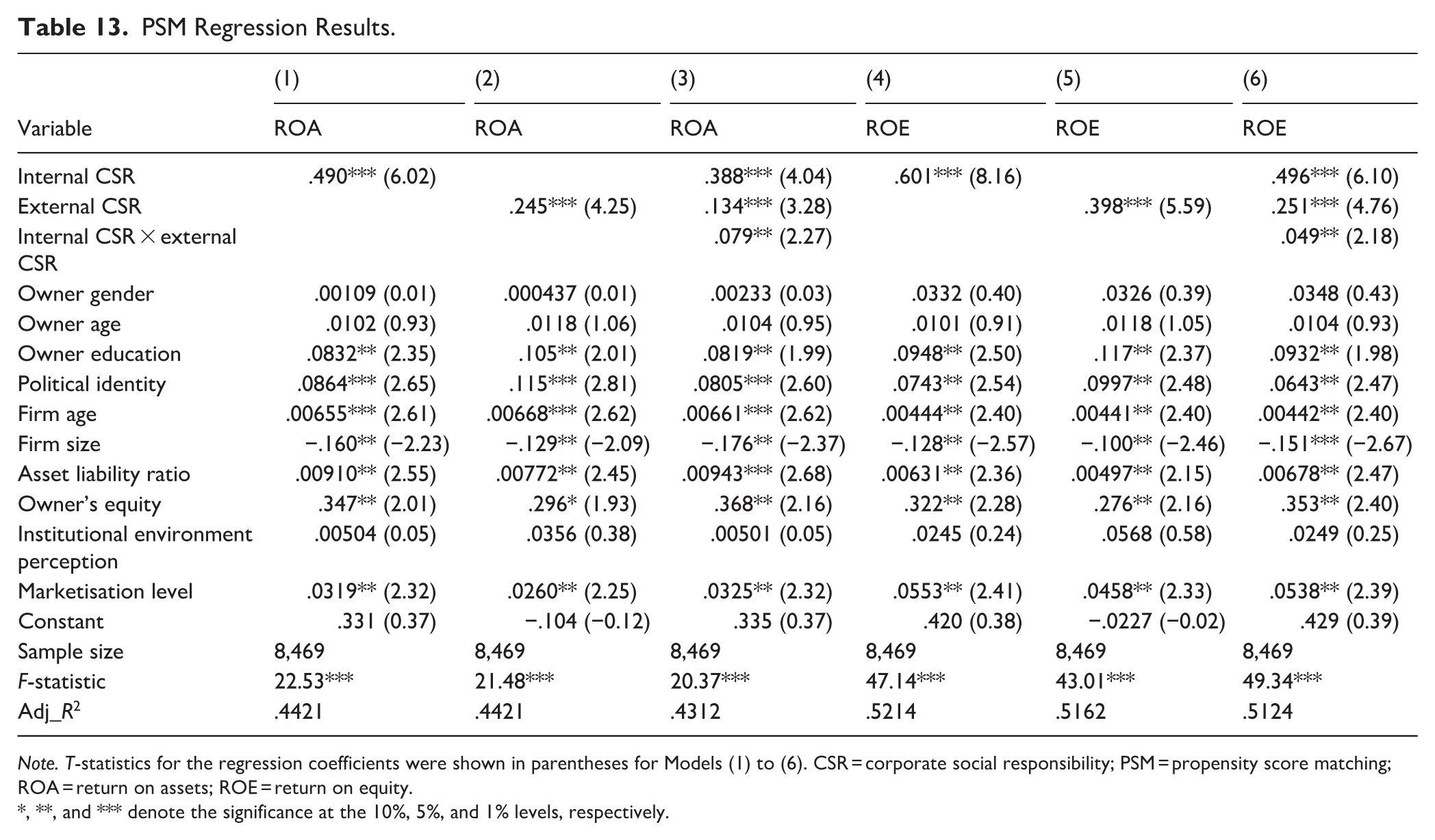

Third, we use PSM to address the potential of self-selection bias (Heckman et al., 1998). We group internal and external CSR separately, and when either is greater than the same industry mean in the same year, they are treated as 1 (i.e., the treatment group). When they are less than the mean, they are taken as 0, that is, the control group. Then, all continuous control variables are selected as covariates for 1:4 nearest-neighbour matching. 4 Finally, the matched samples are regressed.

Table 13 presents the regression results of the PSM analysis. The results show that both internal and external CSR are significantly and positively related to firm performance, and their interaction term is also significant and positive, exhibiting a complementary effect. After applying PSM, the conclusions remain unchanged, confirming the robustness of the findings.

PSM Regression Results.

Note. T-statistics for the regression coefficients were shown in parentheses for Models (1) to (6). CSR = corporate social responsibility; PSM = propensity score matching; ROA = return on assets; ROE = return on equity.

, **, and *** denote the significance at the 10%, 5%, and 1% levels, respectively.

CSR Disaggregating

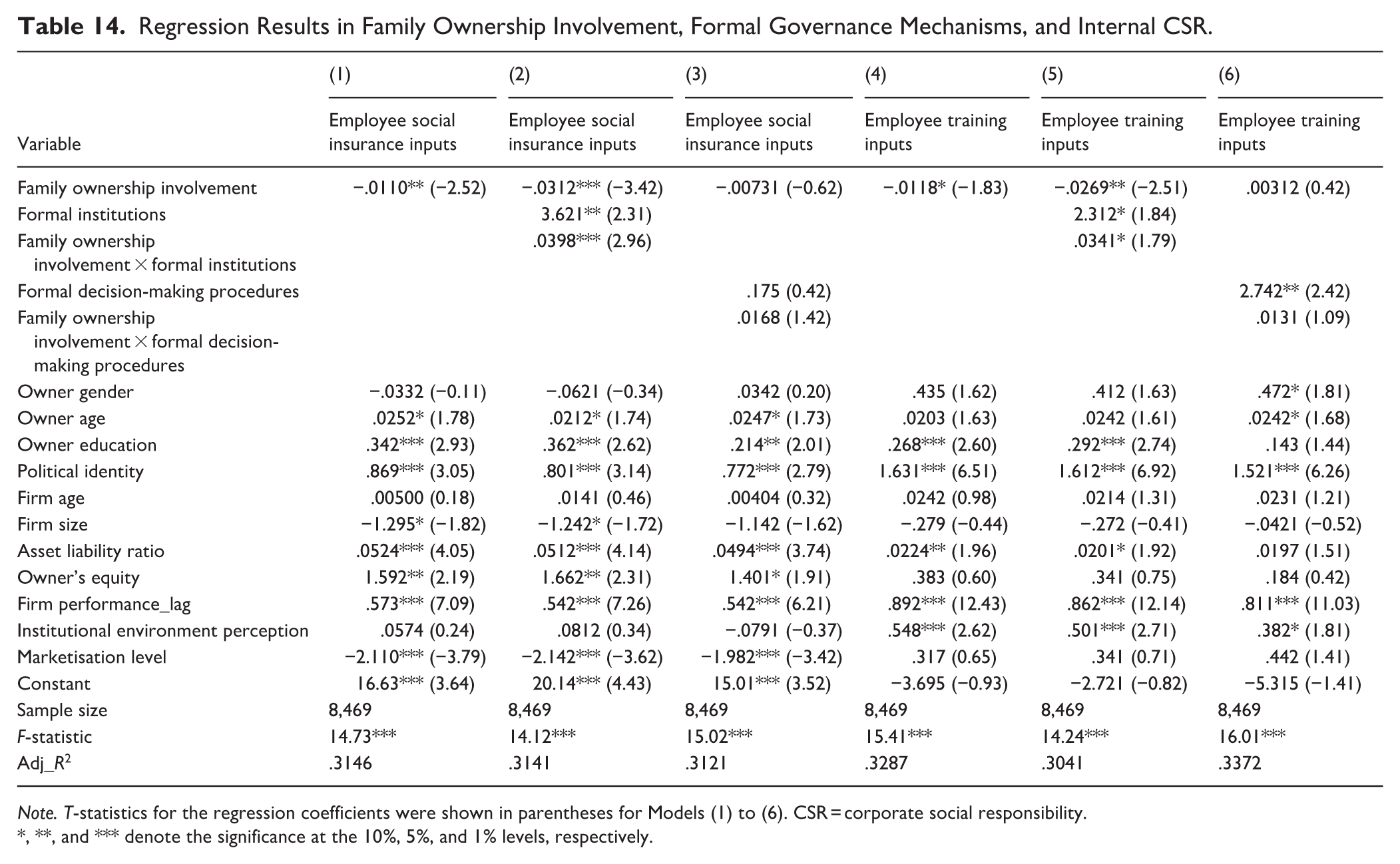

In the main-effects regression analysis, we use principal component analysis to measure internal and external CSR. We disaggregate the internal and external CSR indicators and run separate regressions. Internal CSR is divided into employee-social-insurance and employee-training inputs, and external CSR is divided into charitable-donations and pollution-control inputs. All these variables are logarithmic. Regression results are shown in Tables 14 to 17.

Regression Results in Family Ownership Involvement, Formal Governance Mechanisms, and Internal CSR.

Note. T-statistics for the regression coefficients were shown in parentheses for Models (1) to (6). CSR = corporate social responsibility.

, **, and *** denote the significance at the 10%, 5%, and 1% levels, respectively.

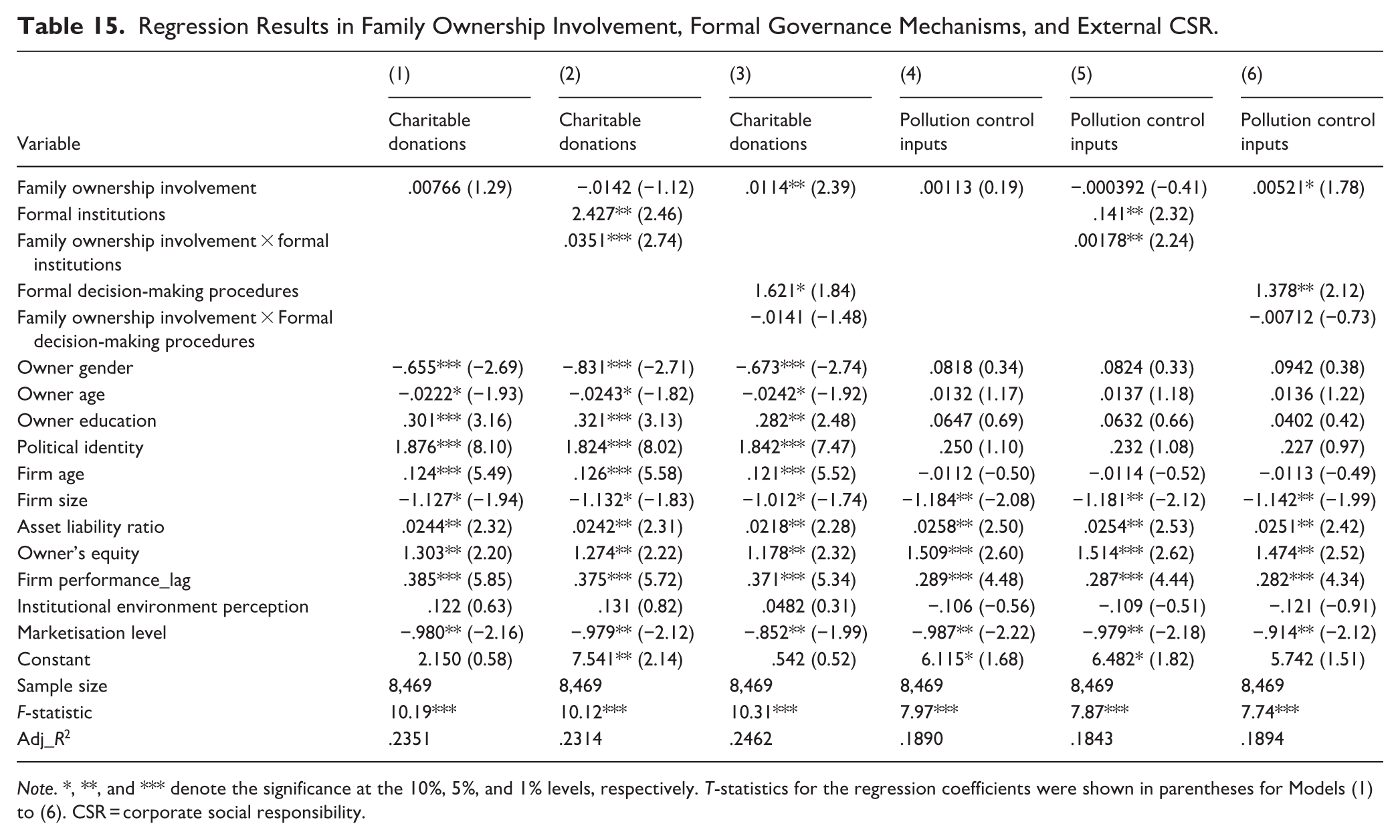

Regression Results in Family Ownership Involvement, Formal Governance Mechanisms, and External CSR.

Note. *, **, and *** denote the significance at the 10%, 5%, and 1% levels, respectively. T-statistics for the regression coefficients were shown in parentheses for Models (1) to (6). CSR = corporate social responsibility.

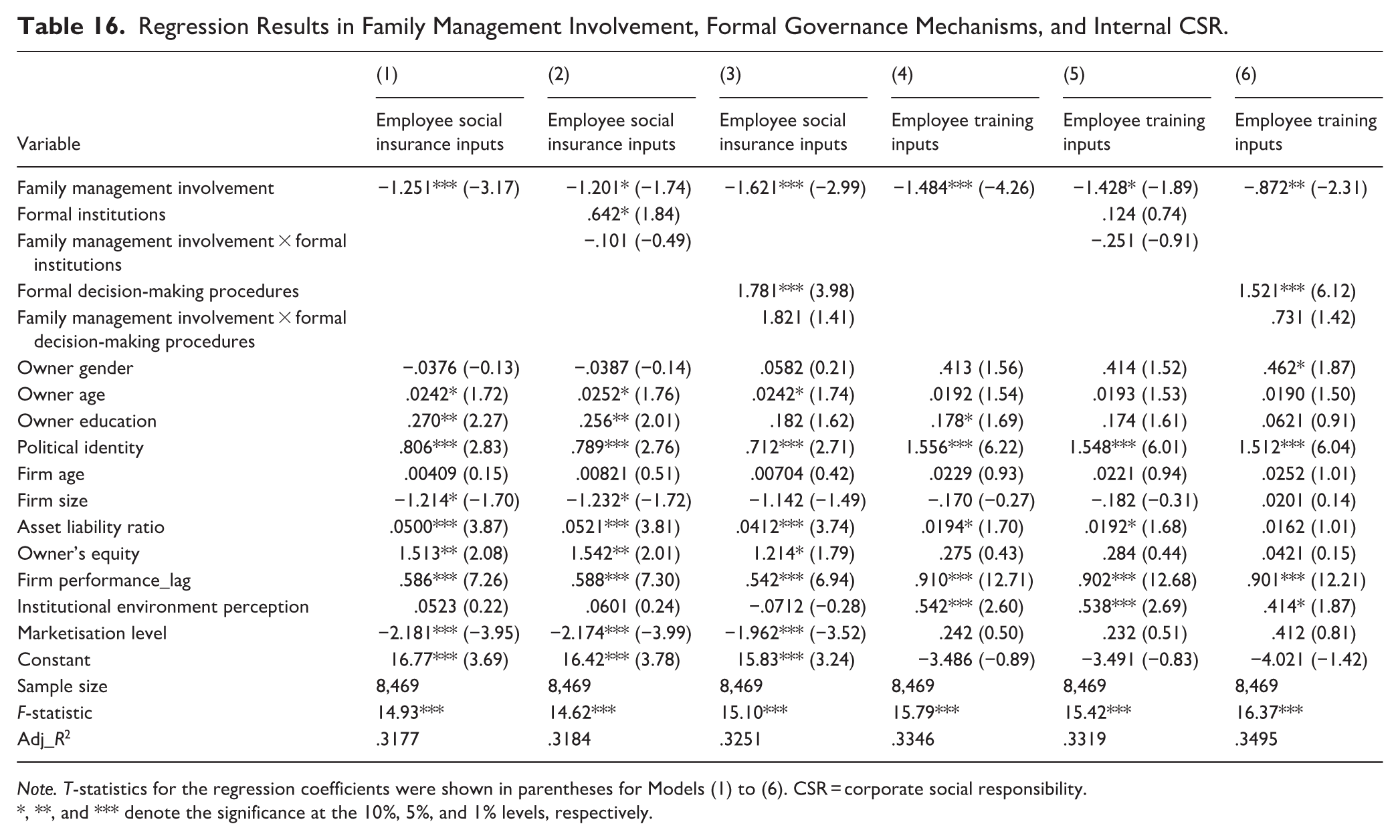

Regression Results in Family Management Involvement, Formal Governance Mechanisms, and Internal CSR.

Note. T-statistics for the regression coefficients were shown in parentheses for Models (1) to (6). CSR = corporate social responsibility.

, **, and *** denote the significance at the 10%, 5%, and 1% levels, respectively.

Regression Results in Family Management Involvement, Formal Governance Mechanisms, and External CSR.

Note. T-statistics for the regression coefficients were shown in parentheses for Models (1) to (6). CSR = corporate social responsibility.

, **, and *** denote the significance at the 10%, 5%, and 1% levels, respectively.

Table 14 presents regression results for family ownership involvement, formal governance mechanisms, and internal CSR. Model (1) shows that family ownership involvement is significantly and negatively related to employee-social-insurance inputs (β = −.0110, p < .05). Model (2) shows that the interaction term between family ownership involvement and formal institutions is significant and positive (β = .0398, p < .01). Thus, while family ownership involvement reduces employee social insurance, the establishment of formal institutions weakens this negative effect. Model (3) shows that the interaction term between family ownership involvement and formal decision-making procedures is positive but not significant (β = .0168, p > .1), indicating that formal decision-making procedures do not weaken the adverse effects of family involvement on employee social insurance.

Models (4) to (6) examine the effect of family ownership involvement on employee training inputs. Model (4) shows that family ownership involvement is significantly and negatively related to employee training inputs (β = −.0118, p < .1). Model (5) shows that the interaction term between family ownership involvement and formal institutions is significant and positive (β = .0341, p < .1). These results suggest that family ownership involvement reduces employee training, to some extent, and with the establishment of formal institutions, the negative effect is weakened. Model (6) shows that the interaction term between family ownership involvement and formal decision-making procedures is not significant. Therefore, Hypothesis 1a is supported, and Hypothesis 2a is partially supported.

Table 15 presents the regression results for family ownership involvement, formal governance mechanisms, and external CSR. Models (1) to (3) examine the impact of family ownership involvement on charitable donations. Model (1) shows that family ownership involvement is positively but insignificantly related to charitable donations (β = .00766, p > .1). Model (2) shows that the interaction term between family ownership involvement and formal institutions is significant and positive (β = .0351, p < .01). These results suggest that family ownership involvement can, to some extent, contribute to firms’ making charitable donations, and with the establishment of formal institutions, the positive effect is reinforced. Model (3) shows that the interaction term between family ownership involvement and formal decision-making procedures is not significant (β = −.0141, p > .1).

Models (4) to (6) show the impact of family ownership involvement on pollution control efforts. Model (4) shows that family ownership involvement is positively but insignificantly related to pollution-control inputs (β = .00113, p > .1). Model (5) shows that the interaction term between family ownership involvement and formal institutions is significant and positive (β = .00178, p < .05). These results suggest that family ownership involvement can, to some extent, contribute to fulfilling firms’ pollution-control inputs, and with the establishment of formal institutions, the positive effect is reinforced. Model (6) shows that the interaction term between family ownership involvement and formal decision-making procedures is not significant. The above results show that Hypotheses 1c and 1d are not supported, and Hypothesis 2c is partially supported.

Table 16 shows the regression results for family management involvement, formal governance mechanisms, and internal CSR. Models (1) to (3) report the impact of family management involvement on employee-social-insurance inputs. Model (1) showed that family management involvement is significantly negatively related to employee-social-insurance inputs (β = −1.251, p < .01). Models (2) and (3) show that the interaction terms between family management involvement and formal institutions (β = −.101, p > .1), as well as the interaction term between family management involvement and formal decision-making procedures (β = 1.821, p > .1), are not significant. As a result, family management involvement reduces the fulfilment of employee-social-insurance inputs; the establishment of formal institutions and formal decision-making procedures does not weaken this negative effect. Thus, Hypothesis 1a is supported, and Hypotheses 2a and 2b are not supported.

Models (4) to (6) show the impact of family management involvement on employee training inputs. Model (4) shows that family management involvement is negatively related to employee training inputs (β = −1.484, p < .01). Models (5) and (6) show that the interaction term between family management involvement and formal institutions (β = −.251, p > .1) is insignificant, and the interaction term between family management involvement and formal decision-making procedures (β = .731, p > .1) is not significant.

Therefore, family management involvement has a significant negative effect on the fulfilment of employee training inputs, but formal institutions and formal decision-making procedures do not weaken the adverse effects of family involvement on employee training inputs. As such, Hypothesis 1a is supported, and Hypotheses 2a and 2b are not supported.

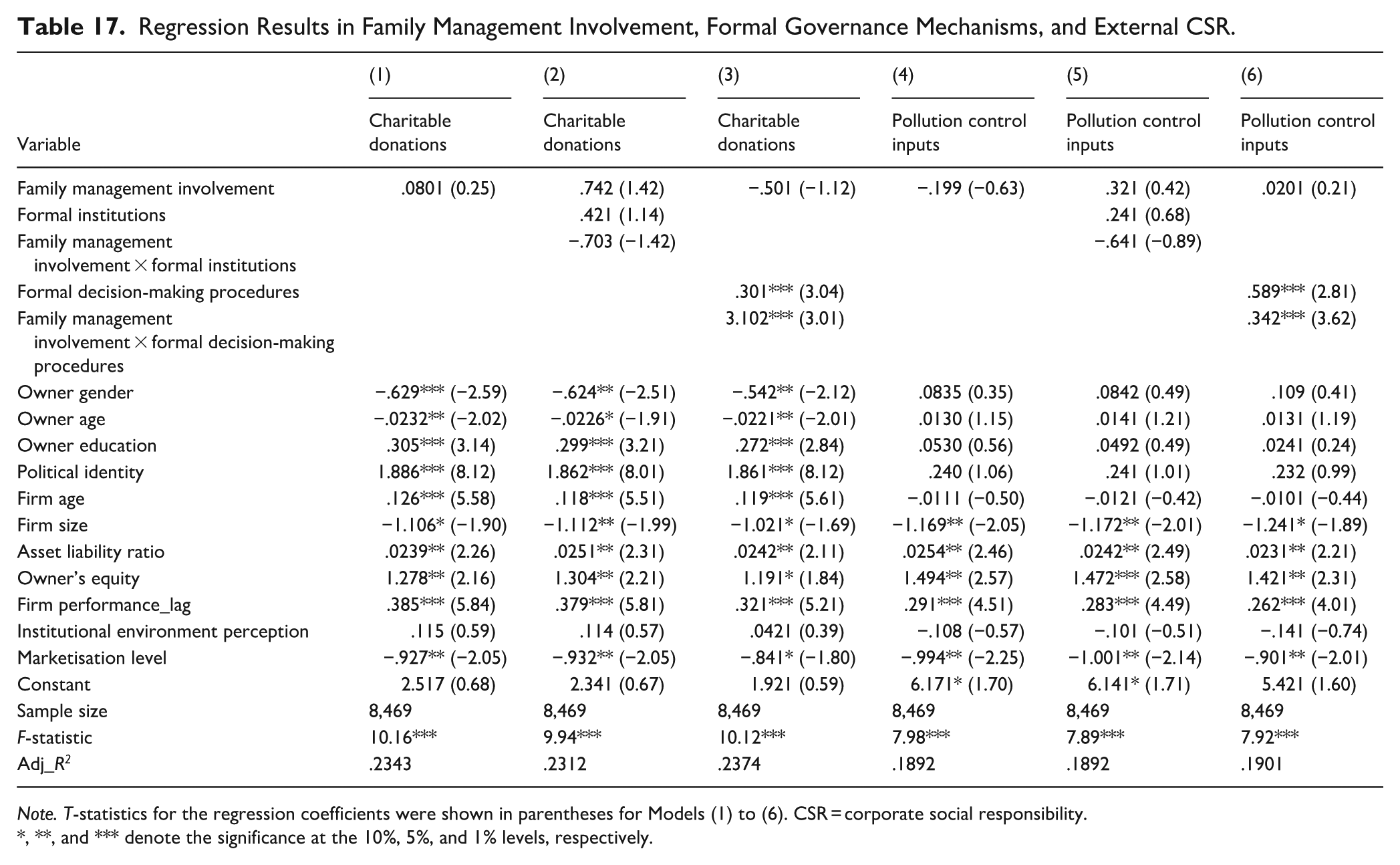

Table 17 shows the regression results for family management involvement, formal governance mechanisms, and external CSR. Models (1) to (3) report the impact of family management involvement on charitable donations. Model (1) shows that family management involvement is positively but insignificantly related to charitable donations (β = .0801, p > .1). Model (2) shows that the interaction term between family management involvement and formal institutions is negative but not significant (β = −.703, p > .1). Model (3) shows that the interaction term between family management involvement and formal decision-making procedures is significantly positive (β = 3.102, p < .01). These results suggest that family management involvement can contribute to fulfilling firms’ charitable donations to some extent, and with the formal decision-making procedures, the positive effect is reinforced.

Models (4) to (6) show the impact of family management involvement on pollution-control inputs. Model (4) shows that family management involvement is negatively but insignificantly related to pollution-control inputs (β = −.199, p > .1). Model (5) shows that the interaction term between family management involvement and formal institutions is negative but not significant (β = −.641, p > .1). Model (6) shows that the interaction term between family management involvement and formal decision-making procedures is significantly positive (β = .342, p < .01). These results suggest that family management involvement does not have a significant positive effect on the fulfilment of pollution-control inputs, while the interaction between family management involvement and formal decision-making procedures significantly drives firms to actively increase their pollution-control inputs.

After disaggregating the indicators of internal CSR and external CSR, the regression results are consistent with the original test. That is, family ownership involvement reduces internal CSR fulfilment, and with the establishment of formal institutions, this negative effect is weakened. Therefore, Hypothesis 1a is supported, and Hypothesis 2a is partially supported. Family ownership involvement can contribute to fulfilling firms’ external CSR to some extent, and with the establishment of formal institutions, the positive effect is reinforced. Hypotheses 1c and 1d are not supported, and Hypothesis 2c is partially supported. Family management involvement reduces the fulfilment of internal CSR. However, the establishment of formal institutions and formal decision-making procedures does not weaken this negative effect. Thus, Hypothesis 1a is supported, and Hypothesis 2a is not supported. Family management involvement has no significant effect on external CSR, while the interaction between family management involvement and formal decision-making procedures significantly drives firms to actively increase external CSR. Hypotheses 1c and 1d are not supported, and Hypothesis 2c is partially supported.

Summary and Conclusion

Main Findings

Based on the data sourced from the CPES datasets from 2010, 2016, and 2020, this study explored the relationships between family involvement and CSR fulfilment. The key findings are as follows.

First, family involvement (both in ownership and management) significantly inhibited the fulfilment of internal CSR in family firms, which is consistent with Cruz et al. (2014). However, family involvement does not significantly facilitate the fulfilment of external CSR.

Second, formal family governance (formal family institutions and family decision-making procedures) played a crucial moderating role in the relationship between family involvement and CSR fulfilment. Regarding family ownership involvement, formal institutions can weaken its negative impact on internal CSR. While family ownership involvement did not increase external CSR, formal institutions can enhance the commitment of family firms to external CSR. Regarding family management involvement, its impact on external CSR fulfilment is not significant, but its incentive effect on external CSR is enhanced when family decision-making procedures are more formalised.

Furthermore, comparing the impact of formal governance mechanisms reveals that formal institutions have a greater impact on family ownership involvement, while formal decision-making procedures have a greater impact on family management involvement. This indicates that professional managers and independent directors play different roles. Independent directors play a mostly supervisory role, typically serving shorter terms and not becoming directly involved in enterprise management, thus having a greater impact on family ownership involvement. By contrast, professional management primarily introduces professional management models into family firms, thereby having a greater impact on family management involvement.

Third, the findings suggest that internal and external CSR function independently to enhance firm performance. Furthermore, fulfilling internal and external CSR can play a complementary role. Therefore, effectively balancing the interests and responsibilities of internal and external stakeholders is also a crucial source of long-term competitive advantage for family firms.

Theoretical Implications

This study makes three main contributions to the research on CSR in family firms. First, our findings advance understanding of bifurcation bias in the fulfilment of CSR in family firms using stakeholder theory supplemented by SEW theory and agency theory, which offer conflicting predictions about CSR engagement by family firms. SEW theory holds that family firms fulfil CSR to preserve their SEW (Berrone et al., 2010; Dyer & Whetten, 2006; Gómez-Mejía et al., 2007; Temouri et al., 2022). Agency theory posits that family firms are unwilling to fulfil CSR because the family is pursuing its own interests (Le Breton-Miller & Miller, 2009). In our view, this controversy arises because prior research has not effectively distinguished between internal and external CSR. To this end, we distinguish the various roles of family firm involvement in fulfilling internal and external CSR. In doing so, this study integrates agency theory and the SEW theory into a unified research model, clarifying their explanatory role in the internal and external fulfilment of CSR in family firms.