Abstract

This study explores the relationship between early-stage imprints and late-stage succession strategies in the transfer of branded organizational values and social missions through the sale and exit process of a single founder hybrid social enterprise (HSE) to a First Nations community-owned business. Employing a novel process tracing methodology, we inferentially and causally examine the journey from start up to entrepreneurial exit to determine why and how a specific outcome happened. Our findings demonstrate how early imprints shape organizational values and the tensions inherent in dual founder agency, which in turn influences succession planning strategies aimed at transferring social brands. The findings also indicate a need for theoretically decoupling sale from exit outcomes as an important but understudied window for imprinting theory. This research contributes to the business and society literature by offering new insights into the causal mechanisms underpinning HSE founder exit, the significance of post-sale founder imprints and the nuanced processes of transferring social brands to value-aligned buyers.

Keywords

Introduction

“Who we are didn’t happen by chance . . .” Founder

Many entrepreneurs establish ventures that develop high quality, innovative products, and services that meet consumer needs while also cultivating social brands that contribute further distinctive value (Besharov, 2022; Cohen & Muñoz, 2017). These ventures, broadly categorized as hybrid social enterprises (HSE), encompass a diverse array of legal structures, missions, mandates, and movements that are either directed internally, externally, or both and that may be loosely or tightly coupled with how they produce and or capture value (Battilana & Lee, 2014; Crane et al., 2014). Given their broad implications for business and society, HSEs have been the subject of extensive scholarly inquiry, particularly concerning their legitimacy (S. Lee & Lee, 2015), mission integration (Gamble et al., 2020), mission drift (Ebrahim et al., 2014), sustainability (Battilana & Dorado, 2010) categorization (Rawhouser et al., 2015), and influence on entrepreneurial and management practices (Doherty et al., 2014). However, one aspect that remains insufficiently explored is the exit of entrepreneurs from HSEs and the implications that such exits may have on the mission alignment, organizational sustainability, and the continuity of their social missions and brands (Lortie & Castogiovanni, 2015).

The urgency in addressing and supporting the entrepreneurial exit, succession, and transfer process is underscored by the following shocking numbers. Across developed economies, over 51% of privately held businesses are owned by baby boomers who are expected to transition ownership over the next decade (Marks, 2024). To underscore this further, a report conducted by the Canadian Federation of Independent Business estimates that over the next 10 years, 76% of small business owners will seek to exit (Bomal et al., 2023). Disturbingly, only 9% of these owners have developed succession plans, with 54% citing finding a suitable buyer/successor as the top obstacle, leaving many owners at elevated risk of unsuccessful or abandoned transitions (Bomal et al., 2023). This silver tsunami carries significant implications for HSEs that are faced with a much shallower pool of values-based buyers, and where owners are further challenged to transfer not only a business, but also the deeply held social missions that are often contingent upon various community and stakeholder relationships that are critically tied to a founder’s identity (Manelli et al., 2023).

To date, empirical studies on HSEs have paid scant attention to founder exits involving social brands, focusing instead on individual narratives (Sarason, 2018), exit due to failure (Muñoz et al., 2020), and corporate acquisition of social brands (Austin & Leonard, 2008). Yet there is limited research exploring how and why the legitimacy and vitality of organizational values and missions are sustained beyond a founder’s departure (Singaram et al., 2023). Given the unique nature of HSEs, understanding the potential differences in the dynamics of founder departures is crucial to exploring this phenomenon (Bacq et al., 2019). As such, founder exits and how the business is transferred can have profound implications for many aspects of the going concern that include organizational identity, stakeholder relationships, and operational continuity (Singaram et al., 2024), particularly when a social brand is highly coupled with a long-term founder (Hertel et al., 2022).

Despite the practical significance of founder exits in HSEs, theoretical frameworks for analyzing the phenomenon of social brand transfer remain underdeveloped (Singaram et al., 2023). Existing tools such as threshold theories do not sufficiently account for the cost/benefit decision-making processes and contexts of mission-involved founders (DeTienne, 2010), while stewardship theories face challenges in effectively measuring social impact performance (Muñoz et al., 2022). Similarly, the resource-based view offers limited explanatory power for founder exits in HSEs, as these transitions often involve the transfer of intangible organizational resources, capabilities, and distinct value capture mechanisms to future owners that are sometimes difficult to quantify (Lortie & Castogiovanni, 2015; Wennberg & DeTienne, 2014). These limitations stem from the failure of conventional frameworks to adroitly incorporate organizational culture, social missions, embedded community perspectives, and brand legitimacy which are deeply intertwined with the consideration of socioemotional value relevant to both founders and buyers (DeTienne & Chirico, 2013).

A process theory approach to conceptualizing founder exits in HSEs may provide some insight into why social brand transfers may continue in the transferred business. Scholars of entrepreneurial process have shown that founders leave significant, enduring, and indelible imprints upon the ventures they create (D. H. Hsu & Lim, 2014; Jaskiewicz et al., 2015; M. Lee & Battilana, 2020). These founders seek to preserve and extract value from their ventures, necessitating exploration of strategies for best accomplishing a transfer when considering these path dependencies (Ip & Jacobs, 2006). However, few studies have sought to explore the interaction of the contrasting and tensioned perspectives of imprinting and strategic choice factors that shape the founder exit process in HSEs (Albert & DeTienne, 2016; Mathias et al., 2015). A deeper investigation into this intersection could yield valuable insights into how HSE exits unfold, particularly when social branding and nonfinancial motives play a central role in the sale of these enterprises (De Cuyper et al., 2020; Zellweger, 2017).

We analyze the case of a CEO-founder who facilitated an entrepreneurial exit through an equity sale and partnership model, transferring both the enterprise and its associated social brand to HSEs owned by two local First Nations communities. In Canada, First Nation business development corporations are community-owned enterprises established by First Nations governments to generate revenue, employment, and social benefits for their members. They typically operate at arm’s length from elected councils but are accountable to the community, pursuing a dual mandate of wealth creation and social development (Anderson, 1997; Colbourne, 2017). This dual mission reflects the hybrid logics that characterize HSEs more broadly, making such organizations particularly relevant partners in values-aligned ownership transitions. While this context provides an important empirical backdrop for the present case, the study does not attempt to generalize about the complex nature of Indigenous entrepreneurship or economic development beyond the point of their classified status as HSEs that are evidenced to encompass various missions and values beyond profit (Colbourne, 2017).

We pose the following research questions: (a) What is the relationship between founder imprints and succession strategies in the context of long-term HSE leadership transitions? (b) What are the causal factors and theoretical underpinnings that contribute to the successful transfer of a socially branded HSE to new ownership? And (c) what are the nuances in process, if any, in the context of HSE transfer to other value aligned HSEs?

To address these questions, we employ a novel autobiographical process-tracing methodology that captures data ranging from the founder’s childhood, pre-start up, start up, and sale process combined with current data collection on the sale, exit, and aftermath (Cassell et al., 2020; Dickel et al., 2021; Mahoney, 2012). Process tracing is a powerful tool for establishing causal relationships in qualitative case study research (Collier, 2011). Paired with imprinting theory, which complements process tracing theory by examining the enduring impact of past critical events on entrepreneurial outcomes in the present and in the future (McMullen & Dimov, 2013), this approach allows researchers to systematically examine sequences of events, test hypotheses against confirmatory and disconfirmatory evidence, and generate insights into complex social phenomena (Bennett & Checkel, 2012). Employing this methodology, we identify the antecedents and overall causal mechanisms (CMs) that help explain a specific observed outcome, offering insights into how and why it happened.

The findings provide several contributions to theory and practice. First, we examine the scope of the succession challenge facing HSEs specifically by illuminating the tensions and causal relationships surrounding imprinting/strategic choice in the context of founder exits in general, and socially branded HSEs in particular. The imprinting perspective sheds new insight into the role of early founder imprints on social brand legitimacy, and how this may impact how strategies emerge toward distinct exit pathways compared with typical business exits. Second, we explain why traditional succession frameworks may be inadequate for values-driven enterprises. Our findings develop agency theory beyond typical principal agent constellations of sellers and advisors/buyers by focusing specifically on the duality of the founder’s agency. The findings show how and why the tensioned shifting of founder roles between agent and principal may lead to sedimentary founder capabilities significant to HSE sale and exit processes. Third, we highlight the importance of late-stage imprints on social brand transfer and provide actionable insight for founders, advisors, and potential buyers that point to a more pronounced need to decouple sale and exit outcomes in order to unify values when navigating HSE transition and exit strategies, especially when deeply imprinted founder values and social missions are a key part of the transfer process.

Literature Review

HSEs and Entrepreneurial Exit

HSEs represent a relatively new mode of organizing that integrates economic and social value creation (Battilana & Lee, 2014). This approach allows HSEs to address complex community needs, innovate blended product constellations, and signal distinct organizational identities that align with customer values. To ensure financial sustainability, HSEs employ a diverse range of business practices (Doherty et al., 2014). The innovation and evolution of these ventures has led to a proliferation of organizational structures, business models and varying degrees and types of hybridity, challenging traditional public and private sector boundaries and definitions (Alter, 2007).

The emergence of HSEs has sparked scholarly inquiry into the tensions and paradoxes that arise within these models, as well as the theoretical frameworks that attempt to reconcile this specific intersection of business and society (Besharov, 2022; Smith et al., 2013). HSEs exhibit a wide spectrum of revenue and mission coupling (Santos et al., 2015), incorporate multiple mission categories such as governance, customer relations, environmental impact, community engagement, and worker welfare (Moroz et al., 2018), and display varying degrees of balance and commitment to these priorities (Gamble et al., 2020). As a result, HSEs present an intriguing yet complex research phenomenon (Battilana & Lee, 2014).

Despite the growing prevalence of HSEs, there is a notable gap in research regarding the transfer of organizational values, social missions, and brand identity during founder-led sales, transfer or exits to new ownership (Lortie & Castogiovanni, 2015). Several high profile cases of HSE exits, such as Ben and Jerry’s, Stonyfield Farm Yogurt, and The Body Shop, illustrate the goal of multinational corporations acquiring social brands to gain competitive advantage in markets with mission-minded customers (Austin & Leonard, 2008). These cases raise questions about the extent to which such acquisitions preserve or dilute the original social mission, and especially in the recent Ben and Jerry’s case, the ongoing challenges that may persist well after acquisition 1 . Given the increasing significance of HSEs and social brands within the global economy, understanding the motivations, factors, and strategies behind these transfers is critical for assessing their transferability and long-term impact considering the impending exit of a huge percentage of owners and founders over the next decade (Mirvis, 2008).

The localized and firm-specific processes, however, by which long-tenured founders exit their HSEs remain largely underexplored, particularly in privately or collectively held ventures (Singaram et al., 2024). Research suggests that transferred businesses demonstrate higher survival and performance rates than startups (Van Teeffelen, 2012), underscoring the importance of understanding how and why social brands endure beyond founder succession and exit (Spence, 2016; Viljamaa et al., 2024). Although the business succession literature includes frameworks such as threshold theory, agency theory, and stewardship theory, most studies approach succession from a family firm/management perspective (Nordqvist et al., 2013). This approach may neglect the important role of founder identities, social imprints, and path dependencies in shaping exit processes (Simsek et al., 2015; Singaram et al., 2023).

Theory on Strategy and Exit

Strategic choice theories in business typically focus on explicit, deliberate, and goal-oriented decision-making, which guides the formation of long-term plans (Ip & Jacobs, 2006). While intended strategies reflect premeditated objectives, realized strategies often emerge incrementally in response to shifting environmental conditions and past decisions (Mintzberg, 1978). Strategic adaptation is thus an ongoing process of implementation, requiring businesses to adjust their models to external changes to sustain growth and profitability (Saebi et al., 2017).

The emphasis on planning has led to the conceptualization of business succession as a long-term strategic process involving owner exit (Wolfe, 1996). Succession strategies are particularly relevant to family businesses, where intergenerational transfers influence firm continuity (Sharma et al., 2003). Business succession planning, as defined by Martin et al. (2002), refers to “the transfer of a business that results from the owner’s wish to retire or leave the business for some other reason” (p. 6), with potential successors including family members, employees, or external buyers (e.g., partnerships, mergers, takeovers, or buyouts). Despite the extensive focus on when and whether succession strategies are formulated (Ip & Jacobs, 2006), researchers have paid insufficient attention to the role of founder values, mission alignment, and path dependencies in shaping exit strategies (Simsek et al., 2015; Singaram et al., 2023; Sydow et al., 2009). This gap highlights the need for a more integrated understanding of how imprinting interacts with strategic planning to influence HSE exits and brand continuity (Faifman et al., 2024).

Theory on Imprinting and Exit

Imprinting theory posits that organizational qualities established during sensitive windows in a venture’s early stages significantly shape its future trajectory (Marquis & Tilcsik, 2013). By analyzing these formative moments, scholars can trace the lasting effects of internal and external influences on individuals, teams, and organizations (Boeker, 1989; Dobrev & Gotsopoulos, 2010; Marquis & Huang, 2010). Sensitive windows may emerge due to internal factors (e.g., founder identity, values, capabilities, resource allocation) or external stimuli (e.g., market conditions, policy changes, regional influences) (Kimberly, 1979; Simsek et al., 2015). These imprints have a profound impact on how founders exit their enterprises and how social values are transferred to new owners (Albert & DeTienne, 2016; Aldrich, 2015; De Cuyper et al., 2020; Singaram et al., 2023).

Sensitive windows may also function as attentional apertures, allowing entrepreneurs to recognize constraints or contradictions in their business models. This reflexive process enables founders to either reinforce, recast, or resist organizational traits in response to changing conditions (Marquis & Tilcsik, 2013; Moroz et al., 2018). Current entrepreneurial exit research remains largely focused on early-stage imprinting (Coleman et al., 2013), motivational drivers (Cardon et al., 2005), business models (Wennberg & DeTienne, 2014), and exit pathways (DeTienne, 2010), leaving gaps in the study of late-stage imprinting effects. Understanding how imprints evolve, especially in later-stage decision-making and exit strategies, provides a crucial yet under-examined perspective on HSE founder exits.

A fundamental tension in entrepreneurial exit research emerges between imprinting theory and strategic choice theory. The former suggests that early-stage conditions shape long-term outcomes, while the latter asserts that deliberate decision-making can override inertia and path dependency (Judge et al., 2015). Recent work in Business and Society similarly demonstrates that historical imprints can persist across major institutional transitions while also being attenuated by firm-level strategic choices, reinforcing the need to examine imprinting and strategy as interacting rather than competing explanations of organizational outcomes (Popli et al., 2025). This dichotomy complicates efforts to systematically identify and analyze the CMs influencing HSE founder exits. Consequently, further research is needed to clarify how imprinting and strategy interact, particularly regarding the transfer of organizational values and social brands to new ownership (S. Lee & Lee, 2015; Simsek et al., 2015; Viljamaa et al., 2024).

Theory on Agency and Exit

Agency theory has been used in conjunction with strategy perspectives to link agency concerns with individual- and firm-level decision-making (Eisenhardt, 1990). The misalignment of incentives between principals and agents have been widely observed in succession and transfer research where founder, management, buyer, and adviser overlaps may introduce a wide range of idiosyncratic agency hazards (Michel & Kammerlander, 2015). Nevertheless, Ip and Jacobs (2006) note a lack of strong theoretical grounding in succession literature where agency lenses are routinely paired with or contrasted against stewardship to model governance, succession planning, transfer, and sale decisions. From this lens, agency problems typically inform who succeeds, how authority is transferred, when ownership exits occur, and how to categorize, explain, or distinguish among founders’ intended and realized exit routes (DeTienne, 2010). Cumulatively, these strands establish agency theory as a central explanatory frame for succession, transfer, and exit outcomes in owner-managed firms (Chua et al., 2003).

One area where agency theory has to date been underutilized is to explore the tensions faced by founders of HSEs who behave as principals of the going concern and as agents of the values embedded in social missions and stakeholder relationships. The accountability of founders to these multiple and contradictory goals foregrounds several risks marked by tenuous lines between mission purpose and drift that might reveal boundary conditions where standard principal-agent assumptions may not apply (Ebrahim et al., 2014). Recent work by Singaram et al. (2023) on HSEs provides an open space for examining the oscillation among principal and agent perspectives within founders through how roles tied to identity, well-being, and nonfinancial preservation point to how they engage or disengage to build dynamic capabilities that lead to different transfer and exit strategies, as well as posttransfer conditions associated with social brand endurance (Mathias et al., 2017).

A Process Perspective on Entrepreneurial Transfer and Exit

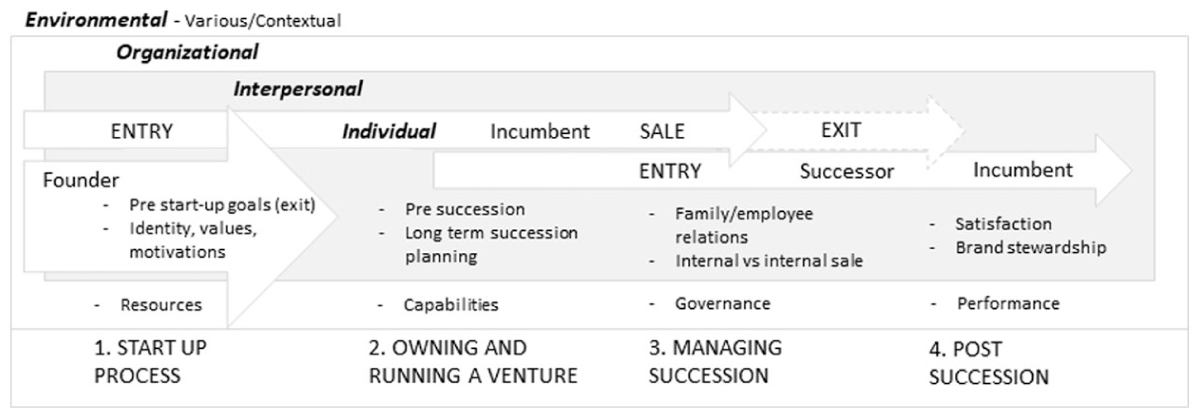

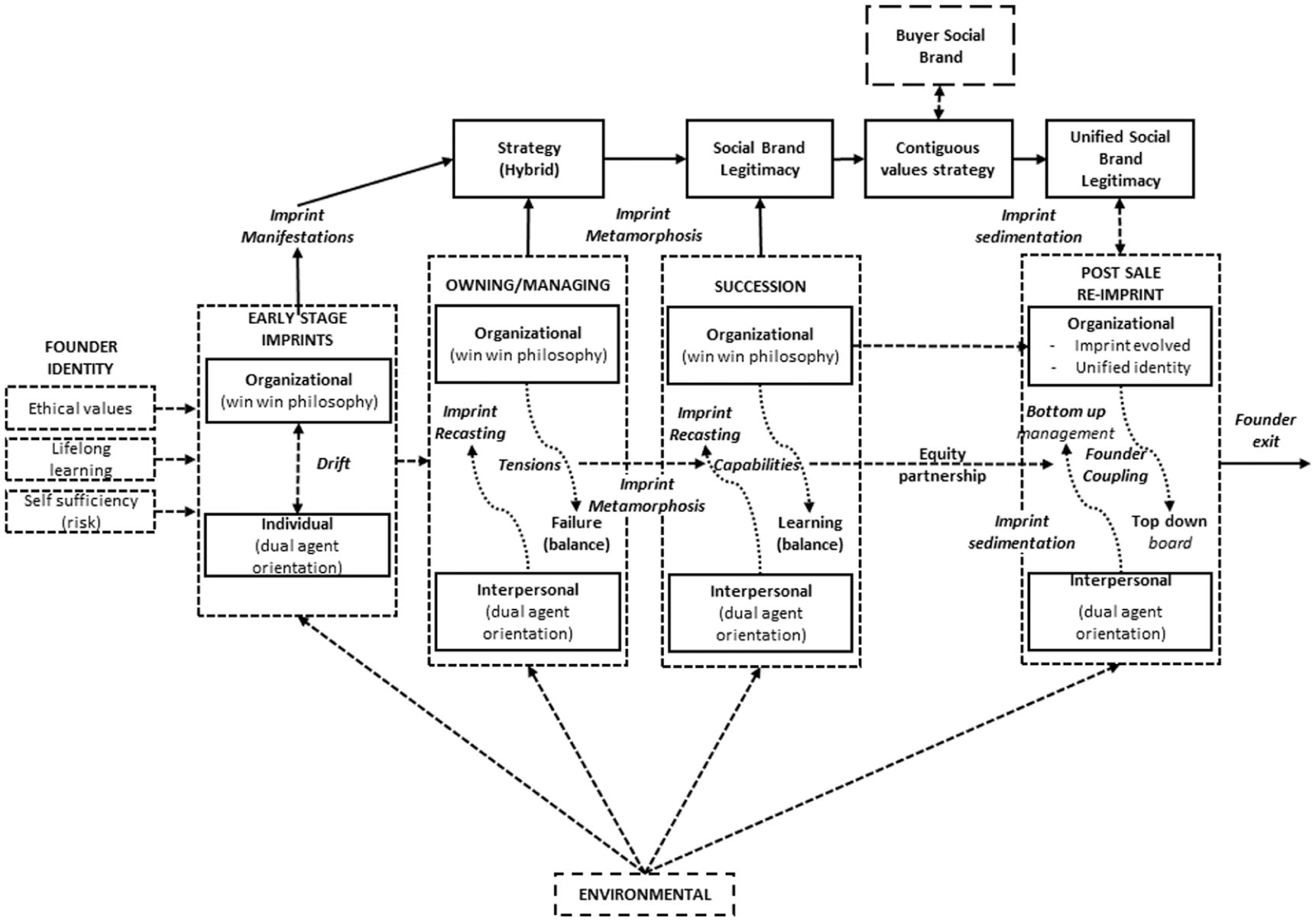

A process-oriented framework provides a structured approach to integrating imprinting, strategy, and agency theories within transfer and exit research. Entrepreneurial process models often use business life cycle frameworks to examine succession and exit (DeTienne et al., 2015; Handler, 1994). This study adopts Nordqvist et al.’s (2013) multilevel framework, which categorizes entrepreneurial exit into four analytical levels: (a) environmental, (b) organizational, (c) interpersonal, and (d) individual and four key stages: (1) startup, (2) owning and operating a firm, (3) managing succession, and (4) postsuccession (Figure 1).

A Process Perspective of Entrepreneurial Exit (Adapted from Nordqvist et al., 2013).

By updating and refining this framework, we aim to clarify the interplay between imprinting and strategic choice in HSE founder exits. Our analysis highlights how early-stage imprints shape later-stage decision-making and identifies the need to distinguish between intentional (deliberate) and emergent (unintended) processes in founder succession (Mintzberg, 1978; Simsek et al., 2015). This approach extends and advances theoretical and empirical understanding of how and why organizational values, social brands, and impact missions persist beyond founder transitions by holistically focusing on how and why they emerge (Dickel et al., 2021; Kuratko et al., 2017; Muñoz et al., 2018).

Methods

Overview of Methodology

This study uses a longitudinal, single case method that captures a rich stream of empirical evidence (Eisenhardt & Graebner, 2007; Yin, 2003). The case falls within the context of a single founder equity sale, exit, and social brand transfer of an HSE with mission priority categories that involve worker welfare (racial diversity, worker safety/certification, wage innovations, and employee development), community (volunteerism, employee contribution/recognition programs, and cause based donations), customers (integrity guarantee), and governance (top management stock ownership plan and best managed awards). This case takes into consideration key facts such as (a) the HSE has achieved several certifications, (b) is ranked as a national top 50 Best Managed, and (c) falls within manufacturing and service industries. It is also unique in that it involves sale to community owned First Nation HSEs, endowing it with both generic and distinct characteristics for exploration (Eisenhardt & Graebner, 2007). A methodological cluster of autobiographical memory, participant reflexivity, observational, and triangulated key informant interview techniques are used for data collection (Bryant, 2014; Cassell et al., 2020; Mathias & Smith, 2016; M. B. Miles & Huberman, 1994).

Process tracing is the analytical engine of our probative inquiry. In the simplest of terms, it may be used to answer questions using posthoc empirical data that take the form of “was X a cause of Y in the case of Z?,” much like how an evidence-based case is built around prosecuting a specific crime in a court of law (Befani & Mayne, 2014). The objective of process tracing is to logically and evidentially remove all doubt about the X, Y, Z relationship through a careful and rigorous process of elimination and confirmation of competing theories until only one remains possible, no matter how improbable (Mahoney, 2012). Scholars have used process tracing previously to identify, test, and confirm various hypotheses related to issues such as nuclear taboo (Tannenwald, 1999), the causal linking of political change to instances of rapid modernization (Lerner, 1958), voting behaviors (Brady & Collier, 2010), and organizational behavior (Ford et al., 1989). Recent contributions to management illustrate its effectiveness as a methodology such as in Derbyshire (2022), where it was employed to develop contingency strategies through the study of business history, while Muñoz et al. (2018) have used it to better understand certification behaviors in HSEs. The method stands as a rigorous data analysis tool for capturing the richness and nuance of the entrepreneurial process that is not observed in other studies (Collier, 2011; Langley, 1999; Martinez et al., 2011).

Process tracing involves the unpacking of a CM. While Shaffer (2015) points out that there is no clear consensus on what a CM may be, Beach and Pederson (2019) suggest that it can be broken down into causal process observations (CPOs) composed of inferences from data on processes (activities, actions, events in time, etc.) and entities (individuals, organizations, etc.). In conjunction with generalizations from case context, CPOs may be used to link together a set of sequential steps necessary for an event to occur using a systems approach (Machamer, 2004; Rohlfing, 2012). Thus, CPOs may be used as empirical evidence to explain why something occurs, where each smaller inference in part forms the sequential building blocks of the how something occurs – the CM that is necessary to give rise to a specific outcome. As there may be no a priori expectations, theories, or hypothesis to test, CPOs can be used to inductively provide insight on the dependent (Y), independent (X1, X2, X3 . . .), and intervening 2 (M1, M2, M3 . . .) variables relevant to the case within a qualitative methodology setting. CPOs may also be used deductively to generate within-case hypothesis sequences for testing probable chains of causal relationships (Brady & Collier, 2010). In both inductive and deductive applications, CPOs (inferences about the CM) are used in conjunction with generalizations based on prior knowledge. Prior knowledge may range from established patterns (but not theory), theories pertaining to interconnected behaviors or phenomenon, theories that offer explanation, or universally accepted rules or laws (Waltz, 1997, p. 5).

Application of the process tracing methodology to a single case obviously requires a great degree of “open-mindedness to accommodate new perspectives on the knowledge discovery process” (Hindle, 2004, p. 1), especially when considering how process theory may be used and developed to produce new discoveries. Therefore, the selection of a qualitative methodology that is novel to an established field of research is a matter of strategy that challenges the state of the art of knowledge production (Habermas, 2015). The specific attraction of process tracing as a methodology to investigate entrepreneurial exit in HSEs is that it attempts to go beyond understanding the reasons behind certain outcomes by formulating and testing richly detailed, event-based variables (imprints/strategy) to establish causal links that are explicitly traceable (Langley, 1999).

Context of Data Collection

Data collection started approximately 16 months after the founding owner of a large fabrication company with over 135 employees announced their intention to enter into a deal to sell 60% of the company to two First Nation businesses in 2016 that would also be classified as HSEs 3 . The period explored spans over 60 years (1960–2023), covering the complete entrepreneurial arc of the founder CEO: from early life, education, and career, to start up, through managing and growing, to transfer, posttransfer, and finally exit. Interviews were guided by Pillemer’s (1998) rubric of personal event memories and participant reflexivity methodologies (Cassell et al., 2020). This method of critical autobiographical memory aligns well with entrepreneurial process and imprinting theories (see Bryant, 2014). Approximately 32 hrs of time with the founder across 10 meetings was captured using audio transcripts, notes, and correspondence. 4 The data were collected over a 5-year period as researchers sought to (a) pinpoint specific events that took place at particular times, (b) elicit detailed accounts of personal and organizational circumstances to determine whether or not the event was a sensitive window during specific stages of the company’s life cycle, (c) evoke reflexive sensations of re-experiencing events to gain clarity about them, (d) link details to images or moments relevant to phenomenal experiences (Cassell et al., 2020), and (e) re-visit events so as to cross examine salience, weightings of importance and congruity of events experienced.

After the first round of interviews with the CEO founder, the autobiographic memory methodology was complemented using multiple interview sessions with 12 key informants that were internal (key management figures) and external (CEOs and officers of both buyer companies, legal agents, etc.) to the firm which produced about 24 hr of audio transcripts and meeting discussion notes. The data drawn from these key informants helped to triangulate and weight specific events, decisions, and outcomes. The data from CEO/founder and key informants was then collated and presented again to the CEO/founder to confirm the veracity of the data collected (Lincoln & Guba, 2004). This approach to data collection emulates and reflects other qualitative studies that employ key informant interviews, archival analysis, 5 single cases, and longitudinal content analysis using the lens of imprinting theory to better understand entrepreneurial process (Suddaby et al., 2015).

Data Analysis and Results

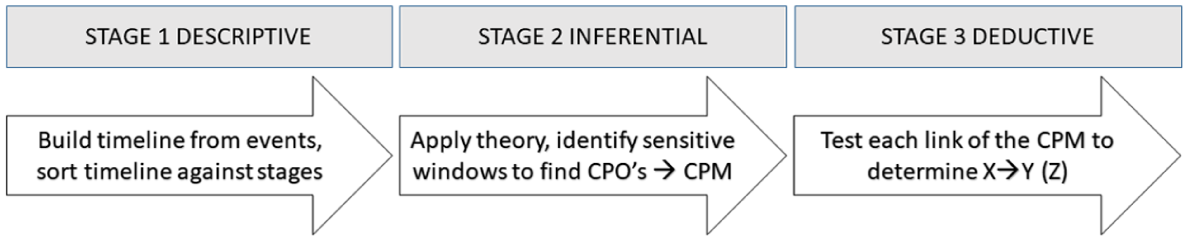

A three-stage analytical strategy was conducted that involved descriptive, inferential, and deductive stages (Collier, 2011; Mahoney, 2012). The first stage (descriptive) was focused on the conceptualization of a timeline of all relevant events. In the second stage (inferential), key events were drawn out of the timelines that could be identified as sensitive windows. These sensitive windows formed the basis of the CPOs and were set out as sequential and interlocked components (n1, n2. . ., nx) of the causal process mechanism (CPM) informing the two observed outcomes:

Three Stage Research Analytical Strategy.

Stage 1: Descriptive Inferences

As stated in Befani and Mayne (2014) and Milanov and Fernhaber (2009), a process in the form of a succession of key events in time was conceptualized using Figure 1 as a guide. The rationale behind this descriptive process was to highlight and sequence the events that were reported/observed as precipitated by actors, decision-making activities, or context/environment to assist in pattern finding in stage 2 (Simsek et al., 2015). The outcome of this work is a chain of events relevant to sale (Zi) and eventual exit (Zii). 8

Stage 2 Causal Inferences: Sensitive Windows and Imprints

Two analytical activities were accomplished in stage 2. The first includes analyzing the evidence to identify sensitive windows as well as plausible and relevant CPOs within them linked to Zi (equity purchase) and Zii (entrepreneurial exit). The second consists of theory-aided pattern finding where a set of interlocking CPO assumptions are used to fully frame the CPM, where each CPO is a hypothesized “part” (sensitive window). In each instance, imprinting theory is used to identify the path dependencies involved to move from description to inferential causality. One of the most difficult tasks involved in process tracing is the need to piece together observable or known facts (or evidence) into a chain of interlocking events that may be theorized as causally leading to the outcome being analyzed (Collier, 2011). Therefore, process-based theorizing relies on insights from existing theory, contextual knowledge, prior understanding of the phenomenon and sensitivity to timing in order to distinguish ordinary observations from those that constitute critical evidence for the outcome in question (Befani & Mayne, 2014). Accordingly, this process was strongly informed by the process framework developed (Figure 1).

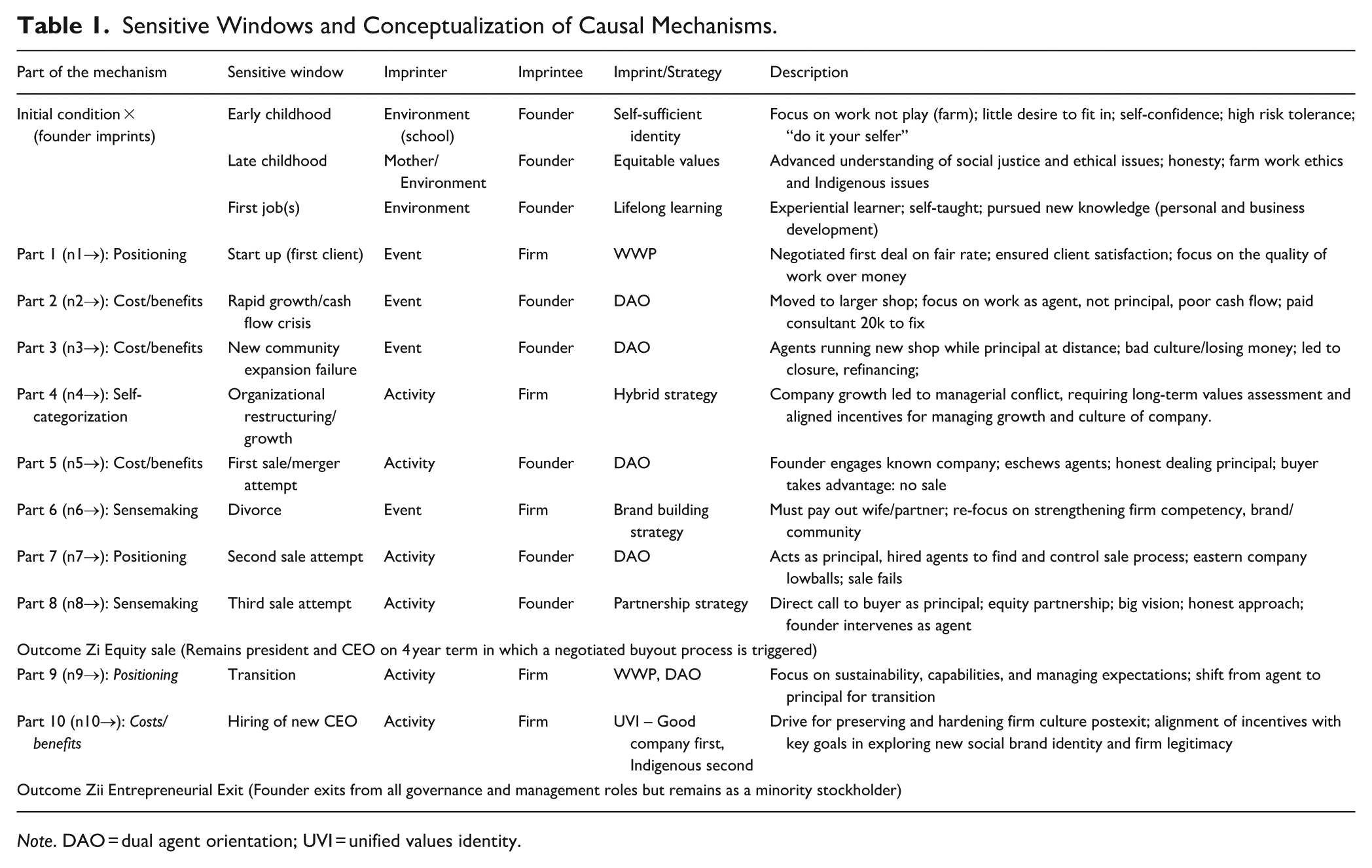

Imprinting theory suggests that one start with the identification of the most obvious sensitive windows and then work forward and backward to assign causal assumptions (Mathias et al., 2015). We used the stratification work cycle to identify how entrepreneurs plausibly apprehend constraints or contradictions, thereby enabling an evaluation of whether a critical sensitive window is present (Moroz et al., 2018). To determine whether a critical sensitive window for imprinting, resisting, recasting, or reinforcing/inertia took place, each key event was probed as to whether (a) a re-appraisal of costs and benefits (b) ambidextrous sense making of contexts, practices, and temporalities, (c) self-categorization, or (d) firm/market (re) positioning (legitimacy) was engaged (Simsek et al., 2015). This resulted in the identification of 10 sensitive windows, each serving as a CPO anchor within the CM. We then re-engaged in reflexive interviews with the entrepreneur/ founder to confirm the relevance of the sensitive windows identified, the genesis of these events, and the historical substance of the imprints (Charmaz, 2014). This led to the conceptualization of three initial condition imprints (self-sufficient identity, equitable values, and lifelong learning [LL]) upon the founder (Boeker, 1987; Westhead et al., 2005) and three imprints stamped during or in operation after start up (win-win philosophy [WWP], dual agent orientation [DAO], and unified vision identity) across the 10 sensitive windows identified (Stinchcombe, 1965). Table 1 presents the overarching critical period mechanism by illustrating the identification of sensitive windows, the pattern of effects among the imprinter, imprintee, and imprint, and a general description of each resulting imprint (highlighted in bold). The plotted evidence (n1 → n10) represents an interlocked chain of events (CPOs) that denote several important patterns of regularity (George & Bennett, 2005).

Sensitive Windows and Conceptualization of Causal Mechanisms.

Note. DAO = dual agent orientation; UVI = unified values identity.

Stage 3: Iterative Logic Tests

One of the most glaring deficiencies in the development of process theories in the field of entrepreneurship is the lack of attention placed upon what is necessary and sufficient to explain why an outcome occurs (Moroz & Hindle, 2012; Van de Ven & Engleman, 2004). Therefore, the last stage of analysis involves moving from induction to deduction by devising hypotheses from the CPOs to specifically test the logical consistency and strength of the causal chain of events that explain the causal relationships leading to outcomes Zi and Zii (George & Bennett, 2005).

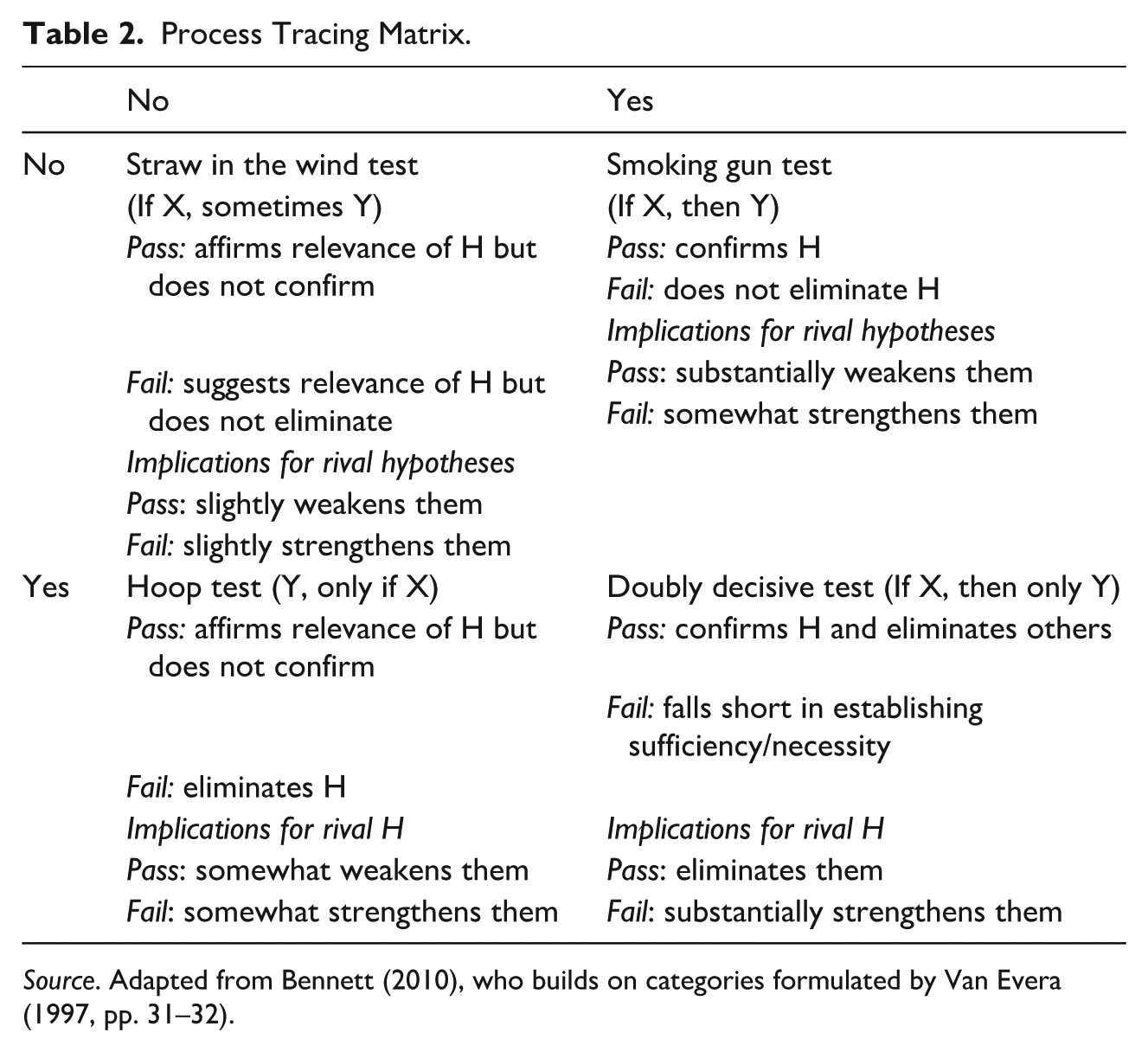

The linked sets of hypotheses to be tested are defined as data set observation matrices (Collier, 2011). These matrices may be populated by up to four types of empirical tests (see Table 2) ranging from weakest to strongest: (a) straw in the wind 9 (gives plausibility or raise doubts about H), (b) hoop (cannot provide direct support for H, but can eliminate H), (c) smoking gun (strongly supports H but failure does not reject H), and (d) doubly decisive 10 (confirm one hypothesis and eliminates all others). Each CPO is scored using a binary yes or no criteria that involve the examination of (1) whether passing a test is a necessary condition for establishing a causal connection and (2) whether it is sufficient for establishing a causal connection, relevant to an outcome (Collier, 2011; Moroz & Hindle, 2012). Trivial necessity and tautological tests were also conducted to ensure logical causal relationships (Mahoney, 2012).

Process Tracing Matrix.

Source. Adapted from Bennett (2010), who builds on categories formulated by Van Evera (1997, pp. 31–32).

Two interrelated and recursive activities were engaged to formulate hypotheses upon the posthoc data collected that could then be tested in a methodologically sound and relevant manner. A sequenced set of X → Y relationships were established to illustrate the deductive reasoning/evidence for establishing hypotheses on a linked set of causal relationships against the two selected outcomes. To be precise, imprinting theory is used to formulate hypotheses on sensitive windows, while past studies on small and medium enterprise (SME) transfer/succession/exit are used to discover a CM (or set of alternate CMs) loosely based on observable routines, values, capabilities, strategies, and resources. Straw in the wind tests (if X, sometimes Y) were used upon each of the hypotheses to ensure that they were relevant to the context, theoretical lens, and overall chain of events being explored. They are not represented in the data set observation, as all X → Y states passed the straw in the wind test as a first step.

Through a recursive exercise conducted by the authors, 11 the strength of each part of the mechanism is subjected to scrutiny to confirm/deny the logical consistency of events for explaining the outcomes observed, while also increasing the confidence that there was an interlocked causal chain (George & Bennett, 2005). Furthermore, through our deeper understanding of the genesis (the conditions of the imprint), metamorphosis (any changes in the conditions relevant to the imprint, such as resistance, recasting, reinforcement/inertia), and manifestation processes (path dependencies, trajectories, or strategies emerging from the original imprint), the CM could be further elaborated upon by linking imprints (or their manifestations) to outcomes with greater confidence (Bennett & Checkel, 2012; Simsek et al., 2015).

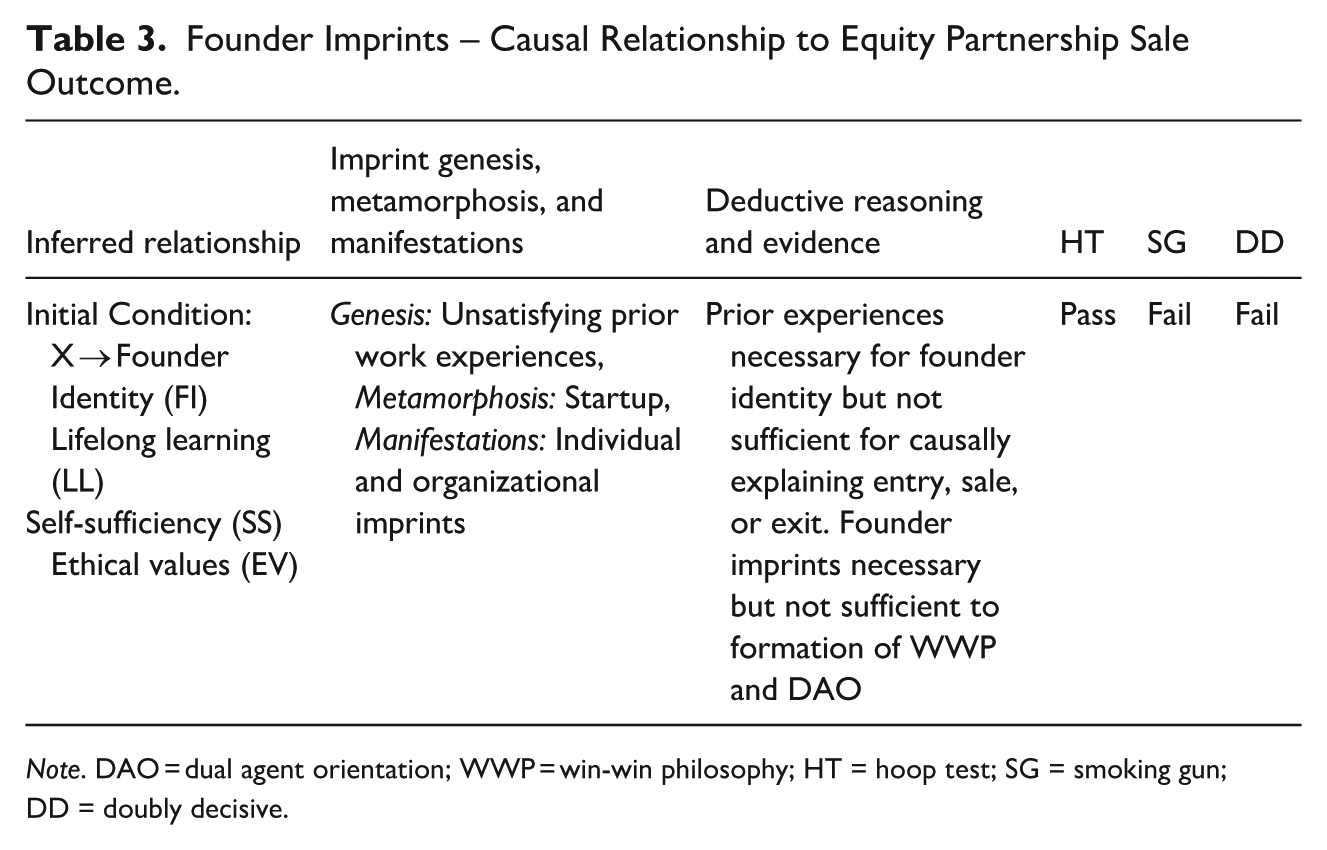

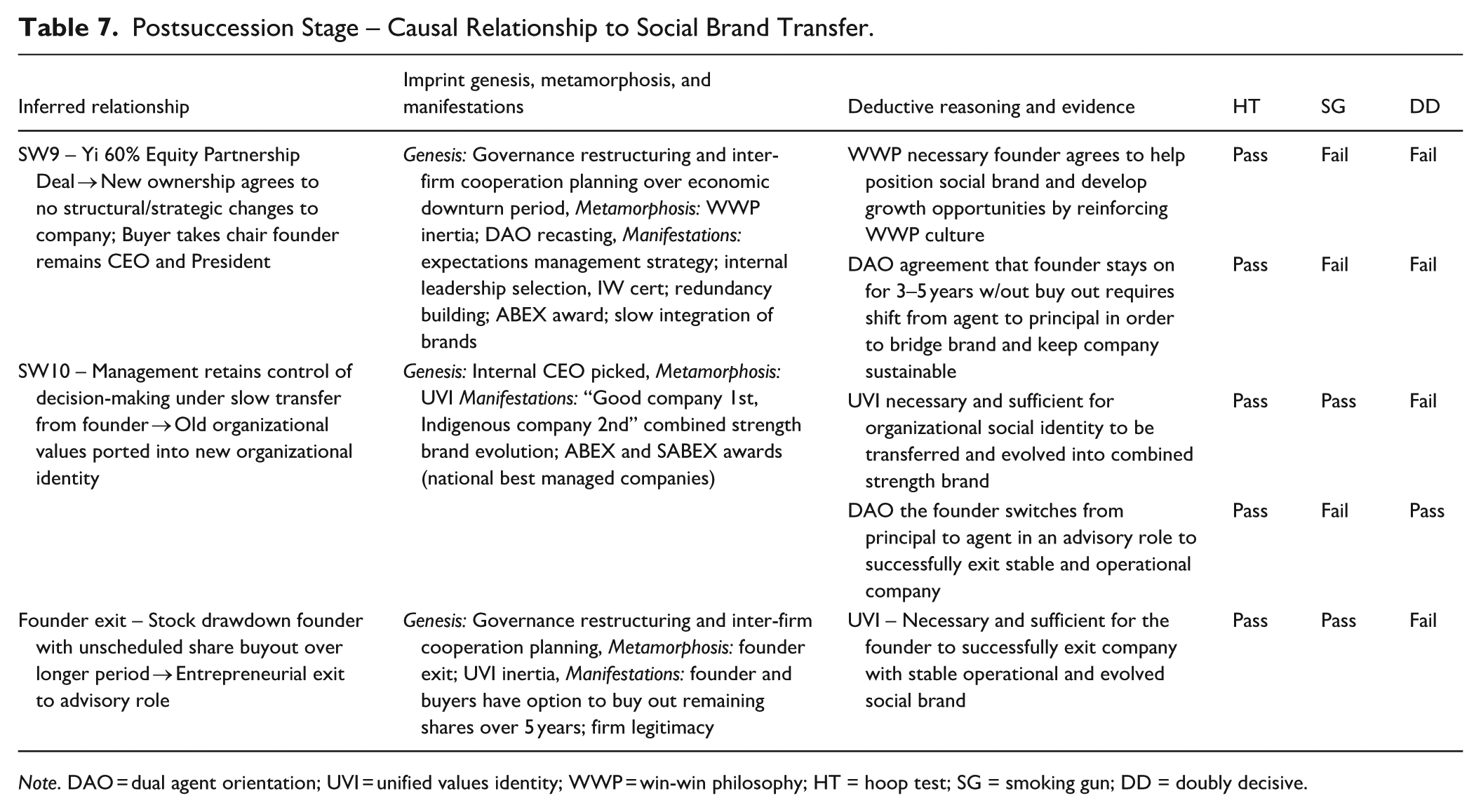

The inferred relationships to be tested, imprint scaffolds, deductive reasoning/evidence, and the logic tests are housed in Tables 3 to 7. Each logic table corresponds with each stage of the exit process and its narrative explanation in order to help the reader navigate the matrices as CMs by which imprints are linked to outcomes through a pass of both the hoop and smoking gun test, stating a positive relationship. Of note, DAO is found to be necessary and sufficient for the sale, while unified values identity (UVI) in Table 7 is found to be necessary and sufficient for social brand transfer and founder exit.

Founder Imprints – Causal Relationship to Equity Partnership Sale Outcome.

Note. DAO = dual agent orientation; WWP = win-win philosophy; HT = hoop test; SG = smoking gun; DD = doubly decisive.

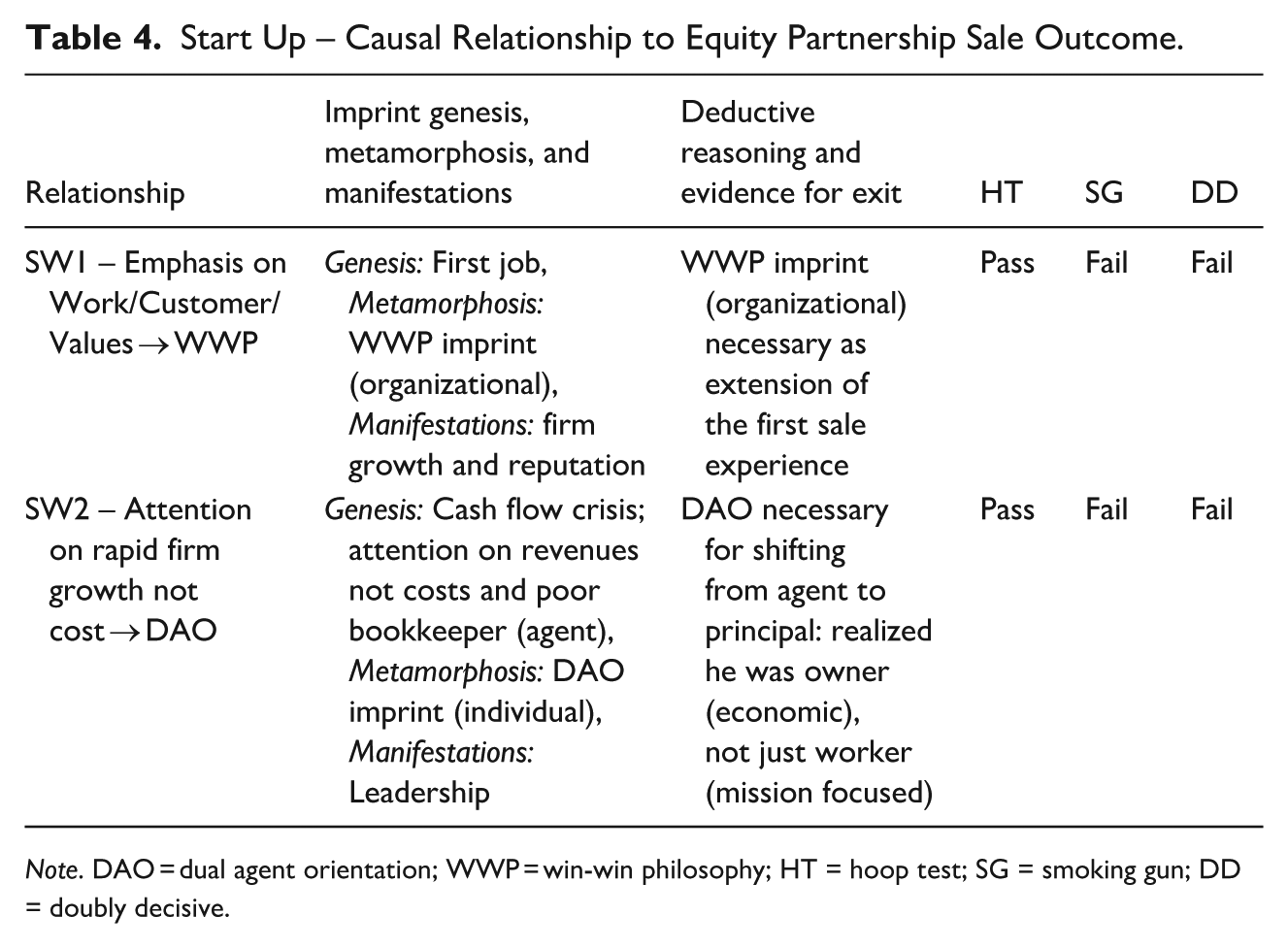

Start Up – Causal Relationship to Equity Partnership Sale Outcome.

Note. DAO = dual agent orientation; WWP = win-win philosophy; HT = hoop test; SG = smoking gun; DD = doubly decisive.

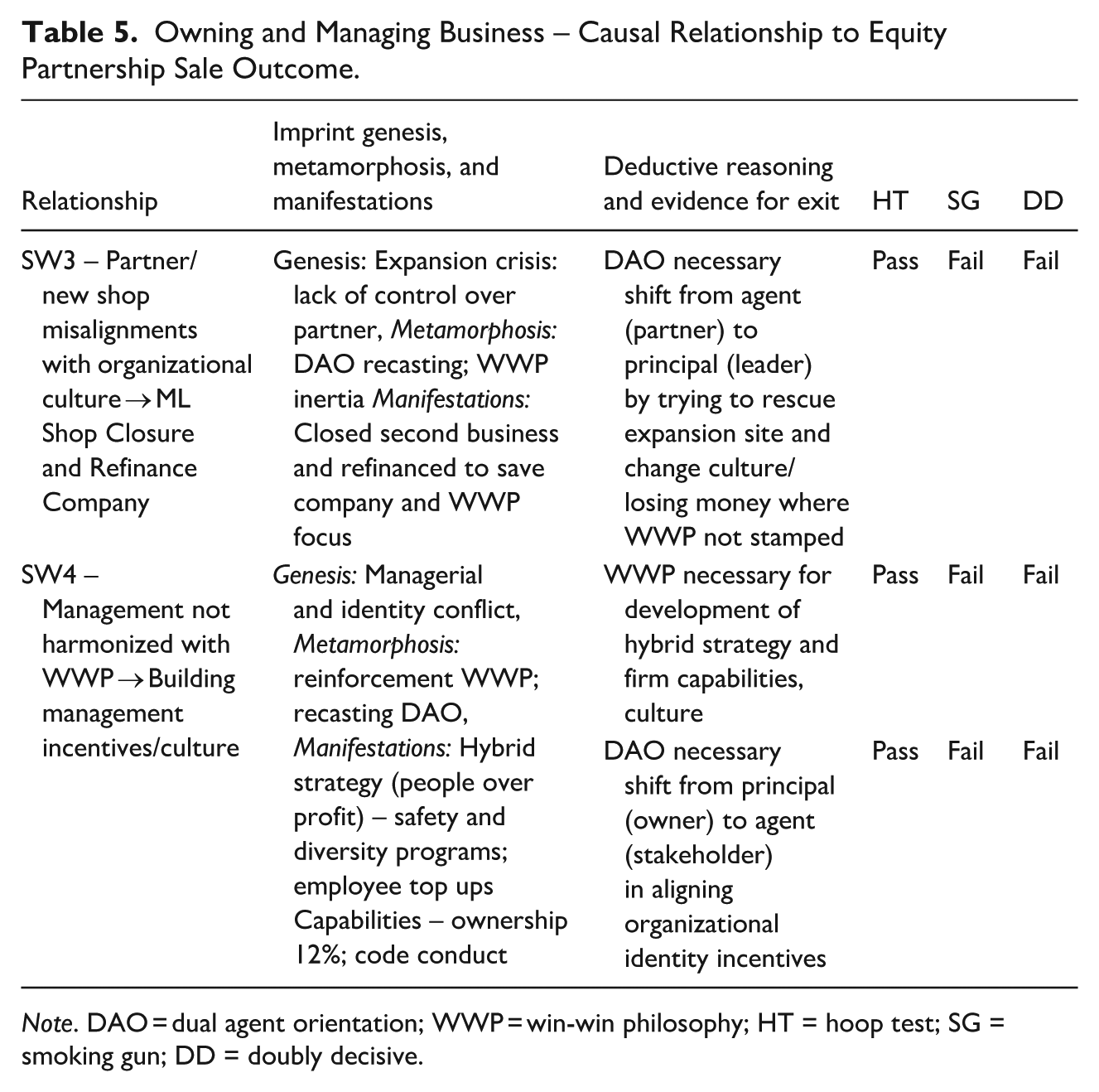

Owning and Managing Business – Causal Relationship to Equity Partnership Sale Outcome.

Note. DAO = dual agent orientation; WWP = win-win philosophy; HT = hoop test; SG = smoking gun; DD = doubly decisive.

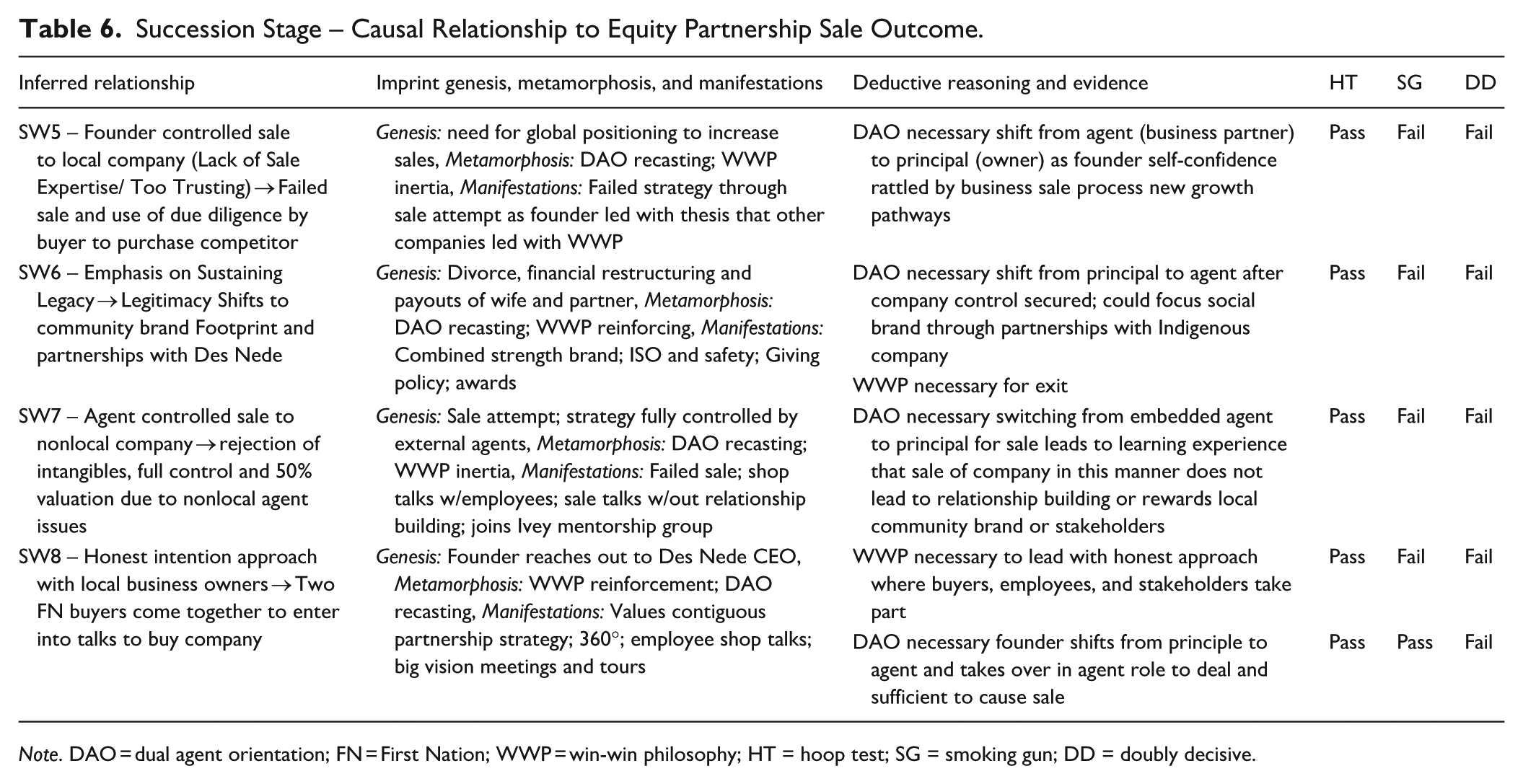

Succession Stage – Causal Relationship to Equity Partnership Sale Outcome.

Note. DAO = dual agent orientation; FN = First Nation; WWP = win-win philosophy; HT = hoop test; SG = smoking gun; DD = doubly decisive.

Postsuccession Stage – Causal Relationship to Social Brand Transfer.

Note. DAO = dual agent orientation; UVI = unified values identity; WWP = win-win philosophy; HT = hoop test; SG = smoking gun; DD = doubly decisive.

Research Findings

There is a range of findings that provide both confirmatory, paradoxical, and novel contributions to the HSE sale (Zi) and exit (Zii) significant to the social brand transfer process (see Figure 3). The first is that process tracing allowed for the testing of a highly path-dependent sequence of interlocked events that provide evidence to the significance of founder identity on two environmental imprints. The first imprint (organizational) is the WWP which manifests the hybrid strategy and is a necessary (but not sufficient) causal condition for the equity sale and social brand transfer of the company to First Nation controlled buyers. The second imprint (interpersonal) is DAO and reflects the tensions involved with the founder continuously shifting between principal and embedded agent roles conceptualized as imprint sedimentation across the HSE life cycle. DAO is found to be necessary and sufficient for the equity partnership sale of the company and manifests across several strategies in tandem with the founder’s need to shift roles between multiple missions.

Model of Imprinting and HSE Brand Transfer and Founder Exit.

The second is that process tracing was useful for discovering relationships between imprints and strategy. In particular, the causal process model points to strategies most relevant to sale and brand transfer were sequentially linked to manifestations derived from the WWP and DAO imprints. For instance, the WWP orientation imprint was causally linked to manifestations in the form of the hybrid strategy as well as the partnership strategy that led to the equity sale. The DAO imprint was linked to manifestations in the form of strategies involving the founder’s ability to navigate tensions among missions to “remain true to his principles and identity.” Moreover, the DAO imprint was found to be necessary and sufficient for the sale of the company in SW8 through the founder shifting from principal to embedded agent to intervene in the sale negotiations to save the equity sale deal and preserve the transfer of the social brand.

Third was the identification of an overlooked sensitive window and existence of a late-stage imprint post sale categorized as UVI. This imprint was formed under the pressure of navigating between two very distinct social brands in the face of economic downturn and the inability of the new organization to leverage their new First Nation controlled status into a winning growth strategy. The eventual manifestation of a strategic approach that was viewed as legitimate by stakeholders emerged from buyer and seller building upon the consistency of the old brand. This evolved “combined strength” brand signaled the new organizational identity as being unified as “a good company first and First Nation company second.”

Last, while the social brand derived from early founder imprints was necessary for establishing authenticity and sincerity toward community goals and values that resonated with First Nation HSEs, allowing the founder to synergize the organizational values of the company with those of the buyers, it was not sufficient for the sale. The financial bottom line and the DAO of the founder to facilitate the deal as agent (taking a stakeholder perspective) and not principal was the key causal factor in securing the equity deal, despite the significance of the social brand.

Founder Identity

First, the founder’s identity is characterized by the individual imprints of a deep commitment to ethical values (EV), LL, and a strong sense of self-sufficiency (SS). These imprints embrace doing things for the right reasons, fairness, and perceptions of work and play, making mistakes quickly to learn from them and reflects a confidence in oneself that accepts risks for adhering to values when building relationships:

Ethical Values (EV): “Work was fun and play a waste of time . . . Mother taught me treaties at age eight [and] I wanted to be an advocate . . . I wanted to build something . . . that didn’t exist.” – Founder

The founder’s identity was filtered through his early experiences and interest with First Nations:

EV: “I ended up going to elementary school with, with a lot of the kids from Sweetgrass and Redfast and some of them became my friend. It was very interesting because at that time I tried to understand why their lives were so much different than mine. And it sort of always resonated with me and made me wonder why there was such segregation, like how come they were treated differently?” – Founder Lifelong Learning (LL): “I used to make mistakes quickly so that I can learn, and I was never afraid of making mistakes . . . My thirst for knowledge, thirst to learn and to grow.” – Founder Self-Sufficiency (SS): “Risk never bothered me. I always want to understand that I could survive what I was risking. . . [the] path less travelled you’ll find me on. – Founder” SS: “Jim has been that sales face, that relationship builder.” – Manager

The founder’s identity provided the foundation for future organizational and individual imprints (Boeker, 1989; Marquis & Tilcsik, 2013). The CPOs across each stage and sensitive window are explicated below.

Start Up Stage

The causal path toward the HSE’s eventual sale to a First Nation controlled HSE was evidenced by two imprints that originated at start-up: one resistant to change – WWP – and one prone to recasting – DAO.

The genesis of the WWP imprint is traced back to the founder’s first transaction while starting up as a mobile welding service (SW1). He negotiated a deal that he characterized as a win-win. This philosophy is an organizational level imprint that is central to the founder’s values and mission focused approach to business. The WWP extends from the founder’s identity where the ethics and values imprinted at an earlier age extends to fairness in social interactions and relationships, even if it put the founder’s business at risk, laying the groundwork for a hybrid strategy, partnership sale and eventual social brand transfer to a First Nation HSE: (I am . . .) Very much a diplomat . . . The farmer was happy because it was a fair price, and he knew exactly what he’s going to pay. I still have a receipt that I gave him for the payment of like $707. – Founder The one thing Jim has always emphasized is the desire for making relationships matter. Every business transaction should be done with the desired outcome of a win-win. – Manager So that’s I think where my philosophy’s really grounded. That was sort of the foundation when I realized this was truly a good thing. I really believe in something, I believe in myself, I’ve always had a lot of self confidence, and I thought that if something worthwhile doing, I wouldn’t let that thought, “what am I risking if I lose it” enter into the equation. – Founder

The DAO imprint came about through a critical window (SW2) where the founder was growing the business rapidly and faced cash flow challenges without paying attention to the costs of expansion. The imprint is interpersonal and reflects the founder’s need to switch from embedded agent (enjoying the work and creating win-wins) to principal to deal with financial management and the pitfalls of external agent incentives (the bookkeeper). Due to this drift, the founder had to pay a consultant $20,000 to resolve the issue, leading to the imprint that caused him to be more attentive to both principal and embedded agent roles: I found quite a bit of fun . . . I did trailer hitches and before long I had two, three, then four then five, eventually still in that same shop, several welding rigs now and probably eight employees. And we were too tight. . . I didn’t realize that when we moved (to the 6000 sq. ft shop), that our overhead had increased. – Founder Such a simple thing! But at that time, I was more focused on the jobs . . . I wasn’t thinking about the business, I thought that the business was taking care of itself I guess as long as long as I handle what was going on in the short run. It challenged our cash flow on new overhead . . . I had to let go of my accountant and hired a consultant for 20k to fix the mess and show me how to never let it happen again. – Founder

The DAO imprint sheds light on how the founder would engage in entrepreneurial agency to achieve values-based missions and in so doing, act as an embedded agent (Seo & Creed, 2002). Through an agency lens, entrepreneurs may act as agents (like employees or someone contracted to stakeholders), and in other circumstances, may behave more like a principal (leader/owner). Sensitive windows may heighten the tensions associated with acting more like an agent than a principal or vice versa when a founder is dealing with two or more missions (Zahra et al., 2009). An imprinted DAO in HSE contexts may catalyze the emergence of sensitive windows under certain environmental conditions. DAO imprints may also provide founders with the ability to understand and be alert to the many complex issues emerging from hybridity, such as social mission drift and the role conflict that may emerge from it (Fisher, 2001).

Owning and Running Stage

The two imprints can be causally linked to several organizational and individual manifestations in the owning and running stage that are bred from tensions between founder principal and agent roles. For instance, the eventual failure of a new business in another city is traced to the DAO imprint (SW3). This second venture was started through a partnership with the founder’s estimator (employee). In doing so, the founder’s role shifted to an embedded agent (partner) looking for win-wins (treated as inertia in this SW) for his partner and employees. The expansion failure was a significant learning experience for the founder. Acting as an embedded agent, the founder created several tensions that included salvaging the business while dealing with the loss of the partner’s stake in the expansion by giving them a 15% share in the first business: Although the 2 businesses were not connected, I had taken 51%. And my estimator, he wanted to be involved, and I said okay, if you want to be involved, more like my suicidal partner, you going to continue working and put some money in it. So, he mortgaged his home and put a big chunk of money on it and a year later he had decided we have got to shut it down and we’ve lost our investment. – Founder I had about 6 employees there and I was very challenged to get the right supervision, and I found that every time I went down there rather than doing business development, I was fighting fires. I was trying to deal with issues that my guys up there had created for me. – Founder Then I said I’m not letting my partner down. I lost everything I put into it, but I didn’t put money into it, I put equipment, I put my time and the loss of towards. So, I said okay I am giving you 15%. His initial $50000 today is worth probably $3million. I didn’t have to give that to him; I did because I thought it was the right thing to do and if I could do it all over again I would still do it. – Founder

The expansion failure can be directly traced to a lack of WWP orientation in the new business as the founder was not present early on as it was in another city. He realized during this failure that bad employee culture was the problem, and this problem could also be extended to external agents such as bankers that were not aligned with the WWP.

Cultural misalignment emerged again in SW4, manifesting as managerial infighting at the first shop. The realization that WWP values were essential to the core of the founder’s business and vision led directly to the manifestation of a hybrid strategy. Shifting roles again from principal to embedded agent, the founder highlighted the need for training on conflict resolution and a commitment to social responsibility. He brought employees together as equals (including the founder) to hammer out a code of conduct that would serve as the basis for the hybrid strategy: They weren’t even in tune with our culture back then and so, I pulled together about 25 people from across the company for a day got a facilitator . . . what we ended up with.”– Founder We don’t have any training on conflict and conflict resolution. We never had to do that. I think a lot of people they buy into our code of conduct . . . I see our company being socially responsible and it’s very important to the ownership. – Founder

To align key management with his vision and develop the capabilities needed, the founder offered them a 12% ownership stake: It wasn’t because I don’t want you to leave the company, it’s that I want you to, in the founder’s mind, I want you to participate in what you’re building. – Manager

The company also developed strong internal capabilities by hiring individuals whose values aligned with those of the organization.

It’s not just specifically around a financial picture. It’s around the culture. It’s around a set of values. We have to hire people where their core values need to be in line with our core values. – Founder I started thinking a little about succession and continuing growth of the company . . . The company had incredibly solid people within and that was important to me . . . their core values need to be in line with our core values . . . So now when the supervisors leave us through retirement or otherwise, we have replacements now, and the replacements are more along the model we are trying to create. – Founder

The outcome of the WWP imprint resulted in a growing social brand: safety policies, employee development, certifications and community focused investments diversity, and inclusion efforts. This social brand was signaled to and noticed by many First Nation communities: I was called up by a group from a community in northern Saskatchewan. Would you consider coming up and spending three days with us. . . share your business acumen and your philosophy?

Succession Stage

After attending regular meetings with a group of business owners, and realizing the differences he had with them, the founder began to once again think about succession and community: The whole Aboriginal piece is so critically important . . . he really started to move in those circles and now involved in those circles and get more involved and then the lights were coming on about the demographics of this province. – Manager

The company’s social brand legitimacy within the community was growing. The founder was soon engaged by a First Nation owned company they had worked with: It was a consultant who came to the table, we’re really interested in your business, brought the managing, the individual that was managing the First Nation into the door, started to talk about okay, let’s walk together on this. – Manager

Shifting from principal to agent again, the founder proceeded to work with the company to explore merger opportunities with a mission-minded approach. But a deal never came to fruition (SW5): Yes. we’re absolutely going to do a deal here . . . touched all the right trust levers for (founder) in gaining that, let’s get a bunch of documents into a data room, let’s do the due diligence on this, this is all good . . . then all of a sudden it went radio silence. I guess they were negotiating with another company at the same time, a competitor in our field. That was a very, that broke trust with (founder) and probably the first time I saw it really break trust with him because he does go out there. He is very trusting of people, and he does put himself out there. – Manager

This failed merger led to further metamorphosis of the dual agency orientation imprint through the learning it prompted in the founder. A shift in the founder’s role to principal was set out for the next strategy with the use of external agents to advance the succession and sale process, while the founder adopted a more principal role: What is the formalized process, not just a handshake, but really what is the formalized process if we’re going to enter into something like this again, what’s the framework we need to be operating by? So that took us into that (next) stage. – Manager

A new sensitive window (SW6) emerged when the founder entered into divorce proceedings. The founder was forced to buy out the shares of the embittered early business partner – the estimator (15%) and settle the divorce (22%). Financial restructuring of the company brought about the freedom to fully reinforce the WWP toward community investments, strategic alliances, and employee-focused development and diversity efforts: I have grown up in the company with a strong sense of stewardship, driving the culture of our company and community . . . We have a map with pins from all different countries where we have employees from. – Founder

The company was named one of the nation’s top 50 managed companies and stood as a testament to its high standards and consistent social brand performance such as diversity hiring and employee assistance and development programs, avoiding churn and reinforcing firm culture. The company also doubled down on business integrity and transparency to achieve ISO and CSR certification requirements: We avoid the cone of silence and ensure transparency of motivation. – Founder We might not make money on [a] job, but that doesn’t matter. We maintain incredible integrity in our estimates . . . “As the culture evolved, we attracted more people who recognized what we had here.” – Founder

The legitimacy of the social brand and consistent revenue growth provided an excellent window (SW7) to sell the company. But the founder’s role in this process had shifted to owner, not agent. The company engaged experienced business sale agents to handle succession: There was a (equity) company out of Ontario, who said wow we’re really interested in you guys, we’d like some information . . . talked about a lot of numbers and at the end of the day, they wanted the lowest number they possibly could, and they wanted thirty percent returns on a year over year basis. – Founder It was never about I want to cash out because he’s always looked behind the doors and I said I have a responsibility to these families; I have a responsibility to this product and it’s important to me, to this community, to this sector. – Founder

However, the sale route did not fit with the founder’s vision as there was little valuation placed on the social brand, especially from nonlocal buyers: This isn’t about private equity coming in and doing the wave, if we don’t do what they want in five years, they shut us down. This is about and it isn’t a legacy to have my name on [on it], this is legacy in terms of what is good for the province, what’s good for this community. I created jobs, they’re sustained jobs. They’re going to stay here when I leave these people still have a job. – Founder

The founder recalled reflecting on the company he had built and who he felt would be the best partners (SW8). After discussion with management, they laid out a plan for a succession strategy that would involve partnerships with First Nation HSEs in the sector that shared similar values: The resource companies were putting some value on Indigenous inclusion. Having some experience working with an Indigenous group back in the 90s, I decided it was time to re-engage with them . . . and start talking about doing some work together and we did execute on a few things. – Founder

The founder emphasized the importance of community involvement and genuine relationships in succession planning and recognized the significance of engaging with First Nation communities for future growth and partnerships

12

: In order to even be considered for ownership, one thing that was important is someone who’s involved in the community. – Founder

The contiguous values approach emerged from relationships that the founder had with the firm’s past business dealings and joint ventures with other companies. This was very much akin to dating, learning about your potential partner, and understanding where there were similarities in values and where there was contrast. The founder eventually called a counterpart CEO of a First Nation (FN) company that they had worked with several times and directly asked if they would be interested in discussing an equity partnership sale: If I’m the First Nations development company, I want to deal with somebody that is absolutely sincere and in it for the right reasons. – Founder

This progressed into the discussion of synergies and opportunities, and the eventual ask by the buyer to have another First Nation company come into the discussions, as it would be tough for just the one company to manage an equity sale. Discussions soon began in earnest. The lessons learned from past succession failures and the shifting principal/ agent roles (DAO recasting) led to a mixed-method approach whereby agents were brought in to move the negotiations forward with a great deal of oversight and communication with the founder. After 6 months, when negotiations suddenly went cold, the founder ignored agent advice that it would harm their negotiation position and personally took over: demonstrating capabilities that required shifting back to the embedded agent role. The founder soon realized that the buyers needed to get to a lower capitalization on the deal. The founder identified a way to do this: to pay out capital reserves to lower firm valuation to a level acceptable by the buyers and of course, the founder saw this as a win-win situation: There were some interesting challenges . . . part of those challenges was the consultants and the lawyers, and the accountants provide a layer of insulation in between us and our new pursued partners, the partners that we were pursuing. – Founder This isn’t ringing true, and we said okay, we need you to step aside momentarily. We need face to face now. We need to sit at the table with them and understand their position on a couple of things and we think they need to understand our position of. That was a turning point in the deal. It could have fallen apart. The wheels could have fallen off the bus. That was the turning point. We really needed to do that, get that face to face and go here’s who we are, here’s our culture. This is what we need in this transaction. What do you need in this transaction and what’s important to you and it was different language at this point. Then we could get together and close the deal. – Manager

While the founder and buyers were drawn together by the social brand, it was not sufficient for sale, the equity sale deal (Zi) was reached wholly on financial terms, where the sufficient conditions for brokering the deal required the capabilities of the founder to engage in a tensioned role shift from principal to embedded agent to save the deal and ensure that the transfer of the social brand was still viable.

Postsuccession Stage

The next sensitive window involved a downturn in the economy and the departure of the CEO of one of the buyers following the sale of the company (SW9). This served to reinforce the WWP imprint. The founder committed to staying on as president and CEO and retained a significant share in the company. More important, it required current management to retain all decision-making. This helped maintain continuity for stakeholders during the transition and gave the company time to sort out its new governance, and the state of its new sister companies: I had committed to staying at a minimum of three years as president and CEO and with the possibility of staying on for another couple of years, one to two years for sure. . . . From a financial perspective, there is no obligation within the period of time that I’m here for them to buy the rest of my share itself because I still have 27.5% of the operating company. – Founder I really do believe that unless the people that are on the board understand the business very, very well, if they become an operational board, that’s the beginning of the end. – Founder So, they’ve had transition. They’ve had change at the top. The individual that Jim specifically went after is no longer even connected to the organization. That makes us nervous. That’s not a good feeling. – Manager

Transitioning from an HSE to a First Nation controlled HSE was viewed as an opportunity to grow due to supply management inclusion policies. But this did not happen automatically, and new jobs did not just appear: One of the reasons why we went this way, was because we really believed that there would be more opportunities, not fewer but more, and maybe a little more emphasis put on that. – Buyer

Stakeholders and partners alike had no clear expectation as to what being a First Nation owned HSE meant. There were issues as to how partner companies would operate jointly.

All we’re doing is messing around or playing at sister company levels, we’re not getting answers. We’re not getting direction. We’re not clear on expectations. – Manager . . . [the] culture [of the sister companies] is really . . . it was bizarre to us. – Manager

Thus a business as usual approach to managing expectations based on the current identity was advanced (not immediately pursuing new opportunities), slowing down processes (exploring and synthesizing partner capabilities), and codifying founder, management and partner ownership commitments to the new venture through a hands off approach by the new owner majority as to how the company was managed (establishing stable governance): We went through strategic planning session with them and I said we’re not going to have an outside facilitator in this, not that any of us are experts, but I want to really be honest around the table without expectations now and I want us to be able to share openly what our expectations were. . . around connections, around influence, around reputation. We need to be able to talk to this. – Founder One of the largest risks associated with this investment was the fact that JNE, although a big company, was born an entrepreneurial effort. It was difficult, like talking to a father to let his child go. . . . “How do you transfer someone from a business?” – Buyer

The UVI imprint (SW10) emerged from pivotal negotiations among the founder and new board that involved open and honest negotiations centering on the need for both the founder and partners to intentionally manage the transfer of the firm’s managerial capabilities and its community-rooted social brand (Eisenhardt & Schoonhoven, 1990; Geroski et al., 2010). This trust allowed the founder to transfer the social brand with an evolved identity that could serve to insulate the company from politics that sometimes emerged from working with the First Nation HSE: You know, there’re two kinds. There’s one guy who sits around and destroys the company just because he’s afraid to leave and let go. And there’s the guy that wants the next group to come and succeed, and (the founder) is in that category. – Founder Those people own 60% of our operating company, they’re equity partners. At very least we need to be seen occasionally in their communities. Not to break down the insulating value over a wall between us that protects them and protects us. But we need to be able to go around, but once in a while to say, hey, you know, I hope that we’re doing a good job for you. I want you to see that we care. – Founder

In so doing, they sought to build redundancies in capabilities both internally and externally in anticipation of the entrepreneur’s eventual exit, as the founder slowly continued to extend and evolve the culture and identity of the firm into an evolved brand with stakeholder support: It couldn’t have happened as long as the founder and CFO and the five people that stood behind them were involved. Everything revolves around the founder . . . we took great comfort in the fact that there wasn’t a drop-dead date. – Buyer One of the things that I think is the role that I’ve played in the past and will continue to play, is to help developing and protect the culture here. – Manager

The sedimentation of the new re-imprint upon exit was dependent upon the coupling and transfer of the combined strength brand to the new management and governance structure, enveloping it in new meaning that was extended beyond the First Nation ownership to focus on the brand itself: I think what business owners don’t want is they don’t want the politics. – Founder It’s really about the win-win because if a resource company says it’s important for them to support FN companies and you have a 38-year-old company that’s proven to be successful; and now we are an FN company. . . . We are gaining some recognition . . . and they know who we are. . . . I think it gives us an additional new purpose. – Manager They just want to say we’re a great company. So, ultimately that’s what we’re shooting for, is we want to do all the right things for inclusion, but essentially if we’re really successful, we’re not going to be considered an Indigenous or an aboriginal or First Nations company. We’re going to be considered a great company. That’s a big part of the goal – Buyer

Stakeholders who trusted the founder, also trusted the evolved “combined strength” social brand, as the company and new ownership had demonstrated that it was committed to do what it had been doing for 38 years beyond founder exit (Zii): but as a First Nation owned HSE.

Discussion

Consistent with past research, the findings of this study confirm the significance of early founder and organizational imprints on start-ups (Geroski et al., 2010; Mathias et al., 2015; Stinchcombe, 1965). Our findings, however, extend imprinting theory to HSEs in several ways. First, we show how early founder imprints can manifest as social brands (Dickel et al., 2021). The CPMs laid out in this article suggest imprints may be more causally significant than strategy in explaining successful social brands (DeTienne et al., 2015). Furthermore, not all companies start off locked into social goals (Santos et al., 2015), but they may achieve brand legitimacy nonetheless when founders reinforce early organizational and individual imprints through deliberate, emergent or unrealized strategy manifestations (Mintzberg, 1978; Muñoz et al., 2018). Although Mintzberg and others believe that strategies (intentions) influence organizational structure and future decision-making, we show the opposite is also true. Organizational structure and past decision-making (behaviors) forged within windows of critical tensions were of similar, if not greater importance (M. B. Miles & Huberman, 1994 R. E. Miles et al., 1978; Quinn, 1989).

Complementary to some of the limited studies in this space, we argue that viewing imprints solely as constraints may be limiting, particularly in cases where a founder’s early identity aligns with opportunities such as the legitimization and transfer of a social brand (Muñoz et al., 2018) and serves as a significant factor when considering exit and brand continuance (Singaram et al., 2024). In this respect, our findings complement recent work by Popli et al. (2025), who show how legacy institutional imprints shape misconduct and how strategic choices may weaken these effects. We extend this imprinting-strategy logic to founder and organizational imprints in a values-based transfer context, showing how strategic choice may not only attenuate imprints but also preserve, recast, and re-imprint them during HSE sale and exit.

Second, the process tracing methodology was instrumental in capturing an individual imprint related to the founder that instead of resisting change, was susceptible to change, generating failures, tensions, and eventual capabilities reflecting a dual agency orientation (Peake et al., 2015). Imprinting theory has previously been linked to decision-making processes by explaining different orientations that emerge within both typical and hybrid ventures (M. Lee & Battilana, 2020; Marquis & Tilcsik, 2013; Mathias et al., 2015). However, limited research explicitly examines the intersection of imprinting theory and agency theory, particularly within the context of HSEs.

DAO within HSEs may be conceptualized as learning processes associated with the latent and deliberate behaviors of founders as they navigate their dual roles as principals of a going concern and as embedded agents of their identity-based values or missions (Ethier & Deaux, 1994; Jensen & Meckling, 2019). The tensions not only introduce a general level of risk (drift, failure) but also confuse the founder as to whether risk taking behaviors are aligned with principal or embedded agent roles (Seo & Creed, 2002). Only through sedimentary learning 13 (often through experiences from the tensions of drift, failure, and opportunity) may the founder realize dual agency orientation as a capability (avoiding tensions through balancing roles). While past studies have applied agency perspectives to entrepreneurial exit to gauge risk related to early investor conditions (Hohen & Schweizer, 2021), team member exits (Gregori & Parastuty, 2021) financial perspectives (Wright et al., 2001) advisors (Michel & Kammerlander, 2015), intermediaries (Battisti & Williamson, 2015) and management power relationships (Chua et al., 2003), there has been little study of dual agency conflicts related to founders (Jensen & Meckling, 2019), making this a novel contribution to the study of HSE exits.

To further our understanding of dual agency orientation and how it emerges, we provide the following theoretical scaffolding of our findings. When used in conjunction with imprinting theory, Mahoney (2012) notes that a sequence of events may have deterministic properties while Garud and Karnoe (2013) argue that path dependence from weak imprints over a long period of sedimentation may be explained as a steady accumulation of differences. While this perspective of path dependence is sometimes contrasted against imprinting effects, it is often difficult or near impossible to decouple the two in conditions of weak imprints and their metamorphosis over time into the manifestation of distinct capabilities – the ability to shift between principal and embedded agent (Simsek et al., 2015).

Imprinting theory suggests that DAO manifests as a capability for navigating between these roles. Considering the findings above, the core of the DAO imprint being a necessary component of the CPM was based on the founder’s tendency to shift between roles over time due to a growing awareness of principal/embedded agent tensions. The persistence of the DAO imprint across the observed chain of events, even though it was weak and continually recast, provides evidence for exactly that: the ability to shift from the principal to agent role causally led to an event that was both necessary (hoop test) and sufficient (smoking gun test) to the eventual sale outcome (Zi). In this case, the founder’s DAO had developed to the point where the founder could effectively balance principal/agent roles with his identity and goals. While previous studies viewed this from an organizational perspective, our study provides new insights into how HSE founders develop capabilities that are critical for navigating between tensioned principal/agent roles and missions without drifting too far one way or another (Bretos et al., 2024; Ramus & Vaccaro, 2017).

Third, one distinct contribution of this study that did not emerge as fully as expected was the involvement and transfer of an HSEs social brand to the control of buyers who also manage similar social brands. To date, there are few studies in this emergent space, making it a notable gap. Our findings inject a missing nuance into the phenomenon that point to the importance of early imprints that allow for legitimately blending social brand transfer and stewardship (Bacq & Eddleston, 2018; Singaram et al., 2024). In the case of this partnership, the blend was hierarchical: good business first, and social objectives second (Muñoz et al., 2020). As the social brand was found to be necessary, but not sufficient for the equity sale to happen, our findings support the importance of seller/buyer values matching and increased attention on the alignment of social values and stewardship/legacy motivations in HSE brand transfers (Van Teeffelen, 2012).

Having tried and failed several times before to mobilize the right succession strategy (casting DAO as a balancing capability), the founder deliberately committed to search, identify, and manufacture (through the two different community ventures) a potential buyer that aligned with the hybrid missions of the company. This partnership was based on the concept of contiguous values in that while the HSEs’ brands and missions differed (two of the partners being First Nation controlled), the core values of the partner companies were similar as expressed through their leadership (Colbourne, 2017). The concept of contiguous values partnerships is important to HSEs but differs from typical First Nations partnerships where resources under the control of First Nations peoples may be recombined with complementary capabilities that benefit both (Anderson, 1997), to instead focus on social brand positioning and views on what constitutes business success or well-being (Mrabure, 2019).

Fourth, the founder’s commitment to social brand transfer postsale contributed to a new sedimented organizational imprint: unified values identity. The literature on how imprints form beyond the founding phase often disregards the influence of the initial founders and the context involved to focus on the persistence of early founder stamps (Johnson, 2007). This is mainly due to power asymmetries that emerge as new buyers take control and dictate vision and strategy (Boeker & Karichalil, 2002). Scholars are silent on how founders may still imprint beyond sale, even though theory is clear on the possibility of multiple sensitive windows, including sale and exit (Marquis & Tilcsik, 2013). The period of negotiations with the new board and management of the company postsale was viewed by the founder as a mechanism for generating trust, figuring out the identities, goals and capabilities of the new and old ownership. It served as a shaking out period where the initial WWP imprint led to a sedimentary process undertaken by old and new management that resulted in re-imprinting (De Cuyper et al., 2020).