Abstract

This special issue explores the impacts of behavioral strategy on management practice. Behavioral strategy can best contribute to management practice by shifting its focus from individual decision biases to the design of behaviorally informed decision processes at the level of the firm. This introduction identifies three types of organizational decision processes, shows how they interact with individual and group biases, and proposes a model showing how managers can design and deploy these processes to shape the strategy of the firm. It then introduces the articles in this special issue and discusses their contributions to the future of behavioral strategy.

Behavioral strategy has made significant inroads in academic research. A search for keywords related to behavioral strategy in the abstracts of Strategic Management Journal articles—terms like “cognition,” “psychology,” “behavior,” and “emotion”—found an increase of 145% in six years: the terms appeared in 9.0% of abstracts in 2010 and 2012, 12.8% of abstracts in 2014, and 22.1% in 2016. 2 The percentage of SMJ articles in which the term “behavioral strategy” appeared in the full text was zero in 2010, 1.2% in 2012, 1.8% in 2014, and 4.6% in 2016. A search of articles in Academy of Management Review and Academy of Management Journal found that the term “behavioral strategy” appeared in the text of 1.4% of articles in 2010, 3.4% in 2012, 5.2% in 2014, and 5.5% in 2016. Overall, the search term “behavioral strategy” appeared in 0.8% of articles published in SMJ, AMJ, and AMR in 2010, compared with 5.2% in 2016—an increase of 550%. 3

Is behavioral strategy making similar impacts on management practice? Yes and no. In public policy, governments are relying on “nudge units” to improve outcomes in areas such as tax compliance, energy conservation, and healthcare. 4 Popular books on cognitive biases and psychological pathologies are read by managers, and strategy consulting firms such as McKinsey & Company use behavioral decision theory to help clients make better investment decisions. 5 In three prominent journals read by practitioners—California Management Review, Harvard Business Review, and MIT Sloan Management Review—terms like “cognition,” “psychology,” “behavior,” and “emotion” have increased, but not as dramatically as in academic journals, appearing in 10.5% of practitioner articles in 2010, 10.4% in 2012, 10.6% in 2014, and 14.0% in 2016. Overall, there is progress, but behavioral strategy is far from realizing its full potential in management practice.

The main obstacle to progress is behavioral strategy’s emphasis on individual cognitive biases. Experience has shown that people cannot easily address any of the known cognitive biases—status quo bias, confirmation bias, the planning fallacy, and such—no matter how much they learn about them. What managers really need is not a longer list of “Thou shalt nots” but a positive set of tools for designing a behaviorally informed decision architecture of the firm. These tools should leverage what we know about cognitive and social psychology by linking the design of decision processes to desired outcomes at the level of the enterprise. A few scholars have offered suggestions of this kind, 6 but behavioral strategy as a field has not completed the essential turn that would allow it to make significant contributions to practice; that is, pivoting away from individual cognitive biases and toward the design of decision processes that capture what we know about cognitive and social psychology.

The articles in this Special Issue reflect this shift away from a “reductionist” view of behavioral strategy, in which individuals are the main level of analysis, 7 to a more holistic understanding of strategy and human behavior in the context of the firm. Before introducing these articles, we examine why this shift is essential for bringing behavioral strategy to real-world practice, and we introduce a typology of the strategic decision processes that constitute the strategic architecture of the firm. We then show how managers can modify these processes, using behaviorally informed decision processes as a powerful lever to direct the strategy of the firm. We conclude by introducing the articles in the Special Issue and showing their potential contributions to the future of behavioral strategy.

The Problem with Reductionism

Research in behavioral strategy has been classified into three schools of thought: Reductionist, Pluralist, and Contextualist. The Reductionist school is grounded in behavioral decision theory and behavioral economics, using experimental methods to study individual judgment and decision making. 8 The Pluralist school uses a variety of statistical and qualitative methods to study the wider decision environment of the firm, taking account of individual cognition (e.g., bounded rationality), social psychology (e.g., group identification, group conflict), and organizational phenomena such as learning and political bargaining. The Contextualist school favors qualitative or ethnographic methods, emphasizing the worldviews and perceptual frames of actors participating in particular organizational and strategic contexts.

With its emphasis on individual decision biases and heuristics, the Reductionist school has produced important insights, with real consequences for practicing managers. For example, researchers have linked excessive risk taking in acquisitions to CEO overconfidence and hubris 9 ; they have shown how excess entrepreneurial market entry derives from myopic self-focus and the neglect of competition 10 ; how attending to sunk costs and anchoring on the status quo can distort resource allocations 11 ; and how executives justify their preferred strategies by constructing false analogies, or by making false inferences on limited or unrepresentative data. 12

Reductionist experimental research is rigorous and cumulative, and the approach lends itself to classroom teaching and executive seminars. Through business schools, strategy consultancies, and authors of popular books, research on cognitive biases has reached a wide audience. 13 In practice, this has allowed academics and consultants (including ourselves) 14 to convey behavioral strategy research and practical advice with a consistent tone and message.

The problem with Reductionism is that it cannot solve the main strategy problems executives actually face in complex organizations. There are several reasons for this. First, most decision biases arise from unconscious or evolutionary neurobiological processes that lie beyond the awareness or control of decision makers. Biases are behaviorally and neurally hardwired to such an extent that decision makers cannot (or will not) abandon them in response to research findings or advice from consultants. Conscious or unconsciously, people do not want to lose their cognitive biases, but derive psychological comfort or practical value from them. 15 Not all debiasing techniques are fruitless, but research findings suggest that interventions designed to remove individual decision biases are less effective than those designed to modify the environments in which decisions are made. 16

Another problem is that cognitive biases studied in the lab are statistical phenomena, not universal truths. Some executive decisions may be relatively bias-free, but the unobservability of biases makes it hard to distinguish biased from unbiased decisions. We know, for example, that CEOs tend to overestimate the potential revenue synergies of acquisition targets; but we cannot know in advance, or in any particular case, that a CEO is guilty of this bias. The best we can say is “You probably have biases, so beware,” which is of limited value to executives. 17

The most serious problem, however, is that the Reductionist school does not address the core behavioral issues facing decision makers in organizations. Organizational decisions are not the sum of the biases of individuals, nor do they mimic the biases of one individual, but they effectuate a range of socio-cultural and behavioral forces, including the psychological dynamics of small group behavior (e.g., top management teams), intergroup politics (e.g., divisional or departmental), systems and processes (e.g., structures and incentives that facilitate or impede strategy execution), and interactions with external boards and stakeholders. 18 Individual biases play a role in organizational decisions, but not as a simple one-to-one mapping onto the strategy of the firm. 19

Behavioral strategy can make significant contributions to management practice, but only by fully engaging the Reductionist, Pluralist, and Contextualist perspectives. The Reductionist school cannot carry the load, and this is not its purpose. Organizational decisions entail large behavioral forces with significant consequences for strategic management practice.

Strategic Decision Processes

Strategic decision processes take many forms, including long-range strategic planning, short-range executive problem solving, bargaining within a top management team, interdepartmental and board politics, and many other routines and processes. We accept the view of Mintzberg and colleagues that these processes qualify as “strategic” when they become “important in terms of the actions taken, the resources committed, or the precedents set.” 20 This means that we are not concerned with one person or activity, but with the wider “decision architecture of the firm”—that is, with the full range of actors and processes that shape decisions about the overall direction of the enterprise.

We know that individuals are susceptible to decision biases but also that strategic decision processes can distort these biases or create new biases. Some decision processes counteract or neutralize individual decision biases; for example, a capital expenditure process that requires green lights at several levels of approval tends to dampen familiarity bias and favoritism. Other processes amplify individual biases; for example, a corporate executive allocating resources to business units may use past allocations as a key reference point, amplifying status quo bias. Some organizational processes create their own biases; for example, adding many layers of decision approval may create a collective degree of risk aversion that is not shared by any individual decision maker.

The crucial point for strategy executives is that, although people have limited conscious power over their own biases, they can design strategic decision processes to deal with individual and small-group biases before they become institutionalized as organizational decisions. This requires executives to understand how individual and group biases are influenced by organizational decision processes, and to design “decision architectures” that align strategic decisions with organizational goals.

Strategic decision processes tend to become routinized around a small number of repeated decision problems. 21 For example, decision processes in pharmaceutical companies become routinized around the research and development pipeline, and (in many cases) mergers and acquisitions; decision processes in materials companies become routinized around resource exploration and capital investment decisions; and decision processes in fast-moving branded consumer companies become routinized around product and marketing decisions. This means that decision processes tend to follow patterns that allow us to identify a relatively small number of types.

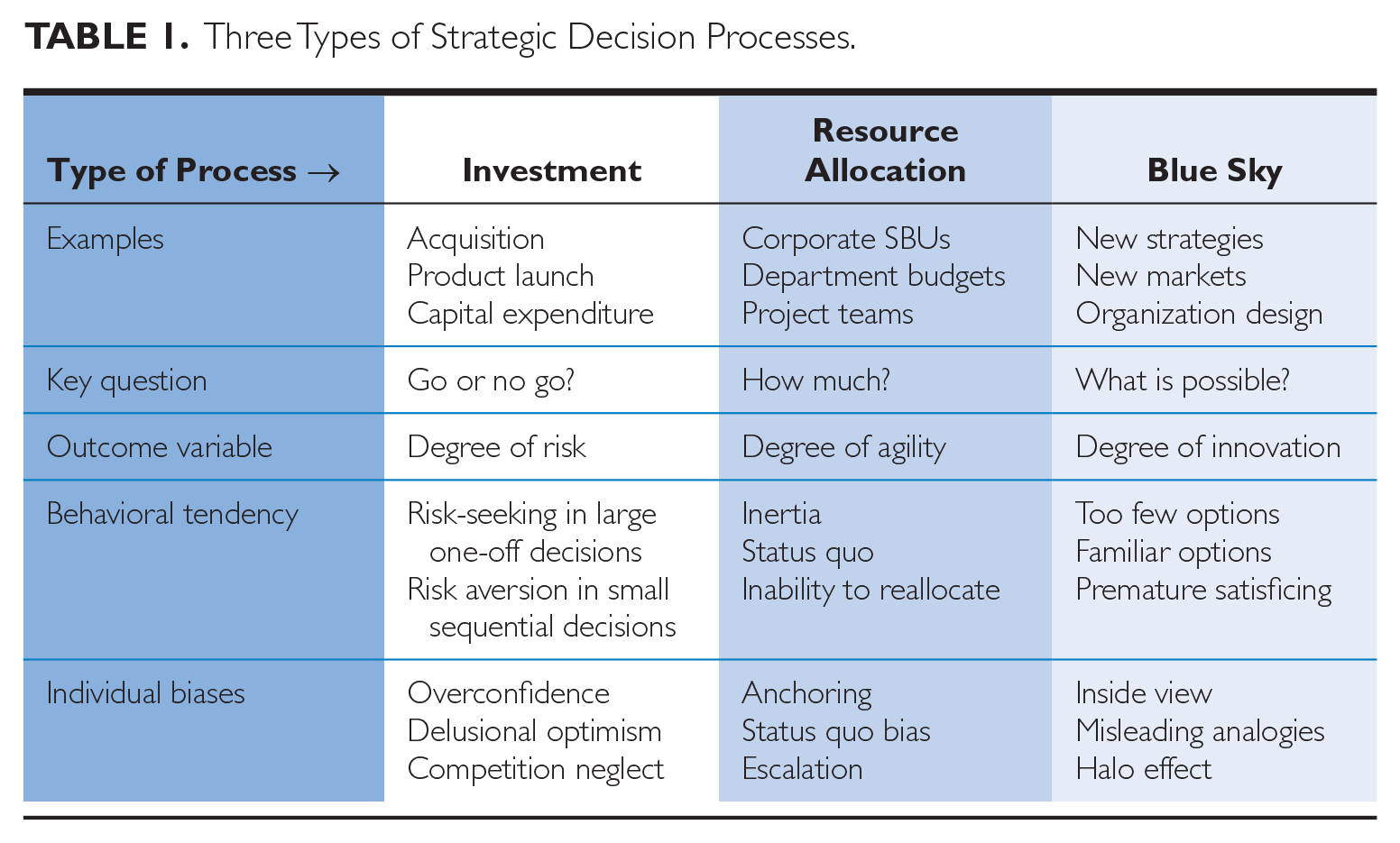

In the following discussion, we classify strategic decision processes into three types: investment processes, resource allocation processes, and blue sky processes. Investment processes involve major decisions with a “go” or “no-go” quality that require significant commitments to a particular course of action; resource allocation processes involve decisions with a “how much?” quality requiring the distribution of scarce resources; and blue sky processes involve open-ended decisions with a “what is possible?” quality calling for creative reevaluation of product lines, markets, or the general direction of the enterprise.

Investment Processes

Investment processes involve large commitments or strategic “bets” that start with a closed-ended question, often with a yes or no answer: Shall we launch this product? Hire this senior executive? Enter this market? Build this plant? Acquire this company? Sometimes they involve choices taken from a small number of options: Shall we enter market A or B? Develop product X or Y? Executives do not always refer to these as investment processes, but they have the essential qualities of investment decisions, namely, the forecasting of costs and benefits and the evaluation of risk.

The essential outcome variable in investment decisions is the degree of risk; that is, managers need to design organizational processes to achieve the desired level of risk. 22 In particular, these processes need to counteract individual biases in forecasting and risk estimation, which can lead to excess risk aversion or risk taking. Research shows that individuals facing large, one-off investment decisions tend to make overoptimistic forecasts and overconfident self-attributions that ignore the capabilities and responses of competitors. 23 Executives become obsessed with their own ideas and follow them against all evidence to the contrary—a phenomenon Peter Drucker called “investment in managerial ego.” 24 Because these biases are unconscious, people take on more risk than they intend, and more than they realize at the time of decision. If such biases passed unchecked into collective decision making, a company might invest too aggressively in new market entry, 25 or overpay for acquisitions due to overestimation of synergies. 26 Executives need tools for designing investment processes that recognize these tendencies and produce the desired levels of risk.

On the contrary, executives often become attached to existing strategies or asset classes, displaying a degree of timidity or loss-aversion that produces insufficient risk taking and investment. For example, decision makers often fail to consider the pooled risk of an entire portfolio of investments, causing risk aversion in individual investment decisions, or in a series of investments staged over time. 27 Equipped with a more nuanced behavioral view, executives can design processes that generate a degree of risk suited to their conscious risk preferences.

Resource Allocation Processes

Resource allocation processes involve questions about “how much?” Every strategy process requires resource allocation decisions, whether resources are being allocated across divisions, departments, geographic territories, product groups, or project teams. The archetypal example is the multibusiness corporation allocating budgets and investment capital to strategic business units.

The essential outcome variable in resource allocation decisions is agility; that is, managers need to design organizational processes to achieve the desired degree of change and reallocation. In practice, these processes need to counteract individual biases toward inertia. Empirical research shows that individual decision makers are reluctant to change existing resource allocations—that is, they adhere too closely to the status quo and show too little agility in responding to external events. Executives unconsciously anchor resource allocations on static reference points—such as the previous year’s budget—and thus unwittingly perpetuate past failures, or escalate commitment to failing courses of action. 28 Incumbent firms change too little and too slowly in response to disruptive market entry, and multibusiness corporations consistently fail to reallocate capital among business units as aggressively as capital markets. 29

Biases toward inertia and the status quo pervade organizations at every level; for example, prospect theory shows that people are loss-averse, which means that managers of underperforming units will fight harder to defend existing resource allocations than managers of high-performing units will fight to appropriate their resources. Because these anti-agility biases are pervasive, they are not easily dampened by training or exhortation. A more effective approach is to design strategic decision processes that neutralize these biases and produce the desired levels of strategic agility.

Blue Sky Processes

Blue sky processes begin with open-ended strategy questions, usually involving high uncertainty, ill-defined problems, and the absence of clearly articulated strategic options. They raise questions such as the following: How can we respond to an emerging technology? How can we accelerate company growth? What should our new organization look like? How should we compete?

The essential outcome variable in blue sky processes is innovation; that is, managers need to design organizational processes that produce the desired degree of novelty or creativity. In behavioral terms, these processes need to counteract individual biases toward considering strategic options that are too few in number and too familiar to decision makers. Shareholders and managers alike often complain about lack of innovation, but these problems are deeply ingrained in the cognitive biases of decision makers. The first order of business in blue sky decisions is to think expansively about new ideas, alternatives, and courses of action. However, people tend to focus instead on repeating their own past successes (availability bias), avoiding their own past failures (the “hot stove effect”), making analogies to organizations they deem similar (often wrongly), and following the well-worn paths of successful companies (the “halo effect”). 30 When one or two plausible-sounding ideas emerge, people quickly anchor on them or “satisfice,” develop hopeful scenarios, and become psychologically attached to them. 31 Idea generation stops and the blue sky process reduces to an investment process, choosing between two or three familiar options.

Experience suggests that blue sky processes produce too little innovation, failing to generate truly novel insights or action plans. They produce too few strategic options, and the options emerge too quickly from the narrow “inside view” of decision makers. Only through a behaviorally informed strategic architecture can executives expect to overcome these biases and develop truly novel strategic actions.

Table 1 summarizes the three types of strategic decision processes, their key features, and outcome variables.

Three Types of Strategic Decision Processes.

Strategic Decision Architecture

Behavioral strategy can contribute to management practice by helping managers design decision processes that achieve desired levels of risk, agility, and innovation. This requires an understanding of how individual and group biases operate on the three types of decision processes (summarized in Table 1), and of how organizational design can amplify, neutralize, or dampen these biases.

We do not argue that firms should always strive to reduce risk, or to become more agile and innovative. Rather, we argue that the levels of risk, agility, and innovation should be conscious strategic choices by executives, not unintended consequences of individual and group biases that operate behind the scenes to distort organizational decisions. Executives should strategize with a purpose, setting the desired outcomes of their decision processes and selecting the decision architectures best suited to achieving those outcomes.

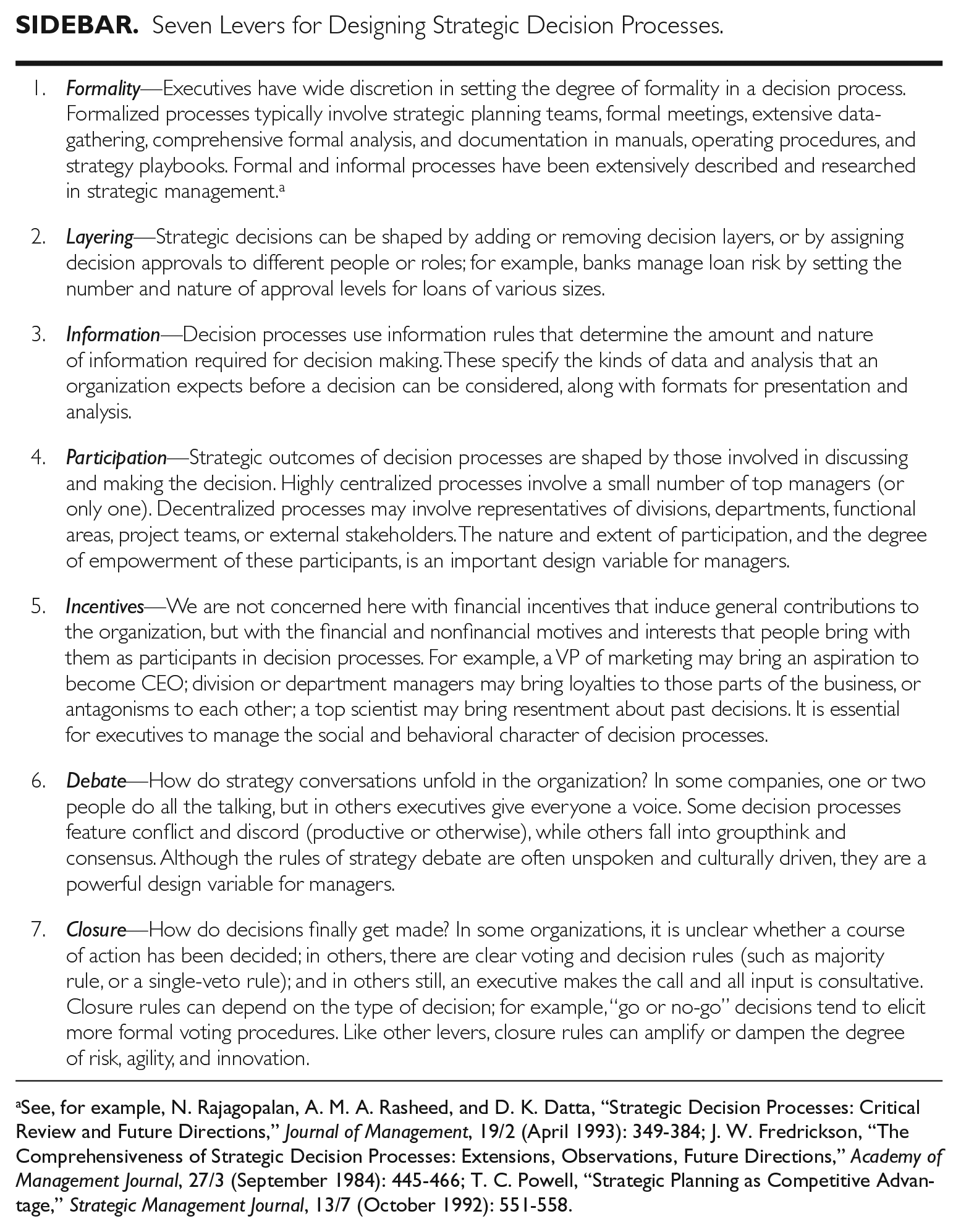

In designing decision processes, executives have a number of tools at their disposal. In the Sidebar, we identify the seven most powerful levers for shaping the architecture of strategic decision processes. These are Formality, Layering, Information, Participation, Incentives, Debate, and Closure. The Sidebar gives a brief description and example of each.

Seven Levers for Designing Strategic Decision Processes.

See, for example, N. Rajagopalan, A. M. A. Rasheed, and D. K. Datta, “Strategic Decision Processes: Critical Review and Future Directions,” Journal of Management, 19/2 (April 1993): 349-384; J. W. Fredrickson, “The Comprehensiveness of Strategic Decision Processes: Extensions, Observations, Future Directions,” Academy of Management Journal, 27/3 (September 1984): 445-466; T. C. Powell, “Strategic Planning as Competitive Advantage,” Strategic Management Journal, 13/7 (October 1992): 551-558.

Designing Investment Processes to Calibrate Risk

The key challenge facing executives in investment processes is to produce outcomes that carry an acceptable degree of risk. We do not suggest that one degree of risk is best, but that executives should use the levers of decision architecture to calibrate outcomes to the levels of risk most appropriate to their circumstances and risk preferences.

The most powerful levers for calibrating risk in investment processes are formality, layering, and closure. In large, one-off investment decisions, higher levels of these variables—more formalization, more decision layers, more stringent closure rules for decision approval—act as a brake on excess optimism and unintentional risk-seeking. For example, many companies lack established processes for evaluating mergers and acquisitions, and when an opportunity arises, executives and boards fall into overconfidence and wishful thinking. The best way to dampen the effects of “irrational exuberance” is to establish clear decision processes that calibrate organizational risk to the actual risk preferences of decision makers.

Conversely, if managers use highly formalized processes to make a sequence of small investment decisions, they may neglect the effects of risk-pooling, and thus stifle the organization by excess risk aversion. For these decisions, organizations achieve the desired level of risk by dialing back the key variables—that is, using less formality, fewer decision layers, and less stringent closure rules.

Although executives use these levers intuitively, decision processes can produce counter-intuitive results, making it essential that executives grasp the behavioral nature of strategic decision architecture. For example, a private equity firm conducted an analysis showing that past investment decisions carried an unacceptable degree of risk. This happened despite a conservative closure rule in the investment committee: if two members (out of 12) objected to a proposal, it was rejected. The firm responded with a more stringent closure rule, with proposals being rejected if only one member objected. However, this turned out to be less stringent than the previous rule. Requiring only one veto to stop a proposal put the lone objector in the spotlight, isolated from colleagues and exposed to censure. The “rule of one” made things worse, with team members avoiding confrontation and accepting risky investments. Consequently, the firm changed the closure rule so that it took four objectors to reject a proposal. This encouraged people to form coalitions and engage in livelier debates that ultimately produced a more satisfactory risk profile.

Executives can also calibrate the degree of investment risk by using other levers in the Sidebar. For example, they can dampen excess risk taking by setting more stringent information requirements for investment proposals, or by requiring wider participation in the decision process. To deal with excess risk aversion in sequential decisions, firms can “batch” information for these decisions, improving the transparency of the overall risk profile. Using the levers in combination gives executives a flexible set of tools for managing risk, and better results than attempting to eliminate individual decision biases.

Designing Resource Allocation Processes to Calibrate Agility

The key challenge facing executives in resource allocation processes is to produce outcomes that carry an acceptable degree of agility. Although agility is widely praised as an unambiguous good, the truth is more complex. Organizational change is costly and destabilizing, and every strategic decision requires executives to balance the relative costs and benefits of enacting change or staying the course. 32 We do not prescribe a particular balance of agility and continuity, but urge executives to use decision architecture to calibrate outcomes to desired levels of agility in their organizations.

The most powerful levers for calibrating agility in resource allocation are participation, information, and incentives. In large organizations, resource allocation processes often become routine and formalized, being linked with budgeting, planning, capital investment, and other periodic processes. Resource allocation becomes automatic, much like accounting, risk management, and other standard operating procedures. When this happens, executives unconsciously adhere to the status quo and underestimate the need for change; or in some cases, lose sight of the strategic importance of resource allocation. When executives anchor resource allocations on formal routines in which past budgets serve as defaults, they achieve too little agility in resource reallocation.

Executives can address this tendency by altering patterns of participation in resource allocation decisions. For example, they can select participants with experience across several departments or lines of business, participants in close proximity to customers and suppliers, or participants not directly involved in the budgeting process.

Managers can also design new information requirements to encourage a more proactive approach to resource allocation. For example, companies can design new measurement and reporting systems focused on proportions of reallocation among divisions or departments. One consumer goods company created such a system by adding a tool for “rebased” budgeting, including a computer model showing allocations based purely on past performance data (revenues, growth, and profitability). Managers were not required to adopt the computer’s allocations, but the data shifted their attention to more objective, “rebased” reference points.

Organizations can also induce agility by using incentives. These include standard economic incentives—such as tying compensation to firm-level outcomes rather than to divisional or departmental growth—as well as more creative solutions. For example, executives can create new resource categories, setting aside funds unattached to any business unit and requiring unit managers to apply separately for these funds.

As with other processes, any of the levers in the Sidebar can be used to calibrate agility in resource allocation. For example, allowing more time for debate, or adopting more stringent closure rules, can impact the balance between agility and continuity. The crucial point is that the levers give strategists more control than is possible by focusing on individual decision biases.

Designing Blue Sky Processes to Calibrate Innovation

The key challenge facing executives in blue sky processes is to produce outcomes that carry an acceptable degree of innovation. Like agility, innovation is often portrayed as an unambiguous good, and noninnovation as evil. But innovation incurs economic and social costs that strategists need to balance against the need to exploit existing strengths and to imitate the best practices of other firms—the classic balance between “exploration” and “exploitation.” 33 We do not argue for heedless innovation, but urge executives to use the seven levers to calibrate outcomes to achieve appropriate levels of innovation.

The most powerful levers for calibrating innovation in blue sky processes are debate, participation, and incentives. Many individual biases militate against strategic innovation, so organizations that neglect the design of blue sky processes tend to repeat old strategies, anchor quickly on familiar options, neglect new options, and take an “inside view” that ignores new technologies, market opportunities, changing customer preferences, and the actions of actual or potential competitors.

Organizations can enhance innovation by broadening both the rules of debate—that is, their implicit or explicit patterns of strategy conversation—and the bases of participation. For example, blue sky processes often require managers to provide reasons that fit the worldviews of their superiors, implicitly discouraging causal arguments supported by evidence. Unfortunately, reason-based arguments tied to existing worldviews amplify the tendency to stagnation. For example, research shows that investment managers tend to prefer glamor stocks that are “rhetorically safe”—that is, supported by reasons their superiors accept—over less familiar choices that yield higher returns at lower risk. The researchers concluded: “If groups engage in dynamic processes that lead them to focus on alternatives described by good reasons . . . the process we document may yield alternatives that have notable disadvantages but that happen to come attached to a good reason.” 34

Executives can break these dysfunctional patterns by designing strategic debates that encourage people to advocate innovations supported by causal arguments and evidence, irrespective of existing worldviews. Such processes nearly always require organizations to broaden participation in strategic debates, often going outside the organization. For example, gaming company Valve Corporation makes extensive use of crowdsourcing, incentivizing gamers to propose new products and using an internal system of “social proofs,” in which people form coalitions around new ideas and marshal evidence to demonstrate their market potential. 35 Crucially, these decision processes encourage innovation through an increased tolerance for dissent. For example, Google insists on “discord plus deadline,” Amazon expects people to “have backbone, disagree and commit,” and McKinsey & Company urges every consultant and employee to “uphold the obligation to dissent.”

The key to calibrating innovation in blue sky processes is to measure past innovation, make an honest assessment of innovation performance, and design decision environments calibrated to organizational goals. Whether the problem lies in too little innovation or heedless innovation, any or all of the seven levers can help strategists manage innovation without having to remediate the individual biases of decision makers.

Conclusion

To contribute to management practice, behavioral strategy needs to show managers how to make better decisions in organizational settings. Behavioral decision research shows that individual cognitive biases can distort decision making, but does not show how managers can predict or manage their impacts in organizations. Individual biases are unconscious and persistent mental events, and unpromising targets for control or intervention. We believe that organizational strategists should focus instead on decision processes at the level of the organization, neutralizing the impacts of individual biases by using the levers of decision architecture to calibrate decision outcomes to organizational goals. The descriptive summaries in Table 1, the Sidebar, and the text compose a basic toolkit for managing these processes.

At the same time, organizations are complex systems and strategic decision architecture is far from simple. Decision processes sit within organizational histories and cultures that produce surprising feedback loops and unintended effects. In putting these ideas into practice, strategists should be aware of complications and pitfalls, as well as opportunities.

For example, the three decision processes overlap to some degree, giving rise to hybrid processes. Investment decisions inevitably involve resource allocations, or can be construed as blue sky processes. Executives need to exercise judgment in defining the decision process and choosing the right levers for intervention. This is a potential pitfall but also an opportunity, since framing the decision process provides executives with another design lever for strategy processes: classifying the decision as an investment process puts the spotlight on risk and invites scrutiny of one or two options; framing it as resource allocation emphasizes agility (or inertia) and the broader context of resource distribution; and framing it as a blue sky process draws attention to innovation (or stagnation) and the “open-ended” nature of the decision. Depending on organizational goals, executives may prefer to draw attention to risk propensity, resource agility, or innovation.

As noted, individual decision biases are statistical phenomena, not universal truths. Because we cannot directly observe mental events, we find out about biases after the fact, by observing their effects. So, a manager might reasonably ask: If our top executives are relatively unbiased, will using the seven levers overcompensate for biases that are not, in fact, present? Will we end up with too much risk aversion in large investment decisions? Costly agility in resource allocation decisions? Heedless innovation in blue sky processes?

These questions shed light on an important consequence of taking a behavioral approach to strategy; namely, the need for organizations to improve measurement systems for key strategic outcomes such as investment risk, resource agility, and strategic innovation. If properly designed, these measurement systems will tell managers what they need to know about the impacts of individual and group biases. If they show that an organization is consistently hitting its targets for all outcomes, then either executives are relatively unbiased or the organization’s decision processes are already neutralizing executive biases. Either way, the best policy for managers is to know the tendencies of executive decision biases; to develop systems for measuring investment risk, resource agility, and strategic innovation; and to use the tools of decision architecture to manage outcomes.

California Management Review Special Issue: Behavioral Strategy and Management Practice

In issuing the original Call for Papers more than two years ago, we defined the scope of the Special Issue as follows:

The purpose of this Special Issue of California Management Review is to examine what happens when Behavioral Strategy meets management practice. If decision makers are not rational in a strict economic sense, what are the consequences for competition, organization, and strategy? In a psychologically informed world, how should executives think about decision processes, market entry, resource allocation, new strategic initiatives, innovation, and strategy execution? If decision environments are filled with cognitive biases, emotions, ideologies, social processes, and political conflicts, how can managers best allocate resources and position the firm for competitive advantage?

The Call for Papers invited people to submit 1,500-word proposals from which we, as co-editors, chose a subset for development into full papers for the Special Issue. We were fortunate to receive a very large number of proposals, from which we chose 15 for development into full papers. When review processes were complete for all papers, the six papers that appear in this issue were chosen for publication.

We want to thank everyone who submitted a proposal to the Special Issue, as well as those who kindly reviewed submissions. We received more good proposals than we could develop or publish, and had to make very difficult calls on papers we would like to have published. In the end, we extend our gratitude to all authors and reviewers for their patience with the review process, and we hope that the Special Issue has achieved its purpose of bringing behavioral strategy theory and research to the practice of strategic management.

We believe that each of the six published papers contains at least one big idea that contributes uniquely to this purpose. The article by Wiersema and Weber combines a range of behavioral perspectives—including expectancy theory, attribution theory, and motivation theory—to explain how and why some CEOs manage to survive unfavorable events while others are dismissed. The article sheds light not only on CEO dismissal, but on crucial problems such as corporate reputation management and the responsibilities of corporate boards.

The article by Smit and Kil focuses on decision biases in acquisition decisions, particularly the neglect of uncertainty due to executive hubris and overconfidence. Although acquirers could reduce investment risk by acquiring minority stakes, or “toeholds,” in target companies, these arrangements account for only five percent of all acquisitions. The authors provide a real-options decision process to help managers make better acquisition decisions.

Mazutis and Eckardt examine an issue out of the latest headlines, namely, inertia in corporate decisions in relation to global climate change. The authors argue that the causes of corporate inertia go beyond economic disincentives and the “tragedy of the commons,” involving cognitive biases such as gain/loss framing, over-optimism, hyperbolic discounting, and external locus of control. Interpreting the problem through a psychological lens allows the authors to propose corporate-level behavioral solutions to climate change inertia.

The article by Healey and Hodgkinson explores the role of emotions in strategic decision making, particularly in companies facing the need for rapid innovation in dynamic environments. Drawing on research in experimental psychology and cognitive neuroscience, the authors provide managerial checklists for managing the emotional dynamics of sensing, seizing, and transforming market opportunities.

Liu and colleagues draw on behavioral research to show how managers can learn from the “nudges” and “behavioral insights” that have proven so successful in government and public policy decision making. Recognizing the persistence of individual cognitive biases, the authors offer an applied framework and two case studies showing how managers can engage good biases to overcome bad biases, and engineer decision environments for better results.

The article by Powell takes a different approach, arguing that strategists systematically overstate the intellectual difficulties of strategy making while underestimating the challenges of putting strategies into practice. This “chess syndrome” gives rise to market opportunities for companies that diligently execute a small number of fundamental activities critical to industry success. Powell offers a managerial framework for identifying, measuring, and executing the fundamentals of business success.

We hope you enjoy reading the Special Issue. In addition to those who submitted and reviewed papers, we give special thanks to Kora Cypress and her team at CMR, and to Editor-in-Chief David Vogel, all of whom worked patiently to bring the Special Issue to fruition.

Footnotes

Notes

Author Biographies

Olivier Sibony is a writer, educator, and consultant specializing in strategy, strategic decision making, and the organization of decision processes. He is an Associate Fellow of Saïd Business School, Affiliate Professor at HEC Paris, and guest lecturer at London Business School (email:

Dan Lovallo is a professor of business strategy at the University of Sydney Business School and a senior research fellow at the Institute for Business Innovation at the University of California, Berkeley (email:

Thomas C. Powell is a professor of strategy at the Saïd Business School, University of Oxford (email: